An Act relating to Duties of Excise

1 Short title

This Act may be cited as the Excise Tariff Act 1921.

1A General administration of Act

The CEO has the general administration of this Act.

2 Certain Acts to be read as one with this Act

The Excise Act 1901, the Petroleum Revenue Act 1985 and the Petroleum Excise (Prices) Act 1987 shall be read as one with this Act.

3 Definitions

(1) In this Act, unless the contrary intention appears:

area includes:

(a) a part of the surface of the earth and the subsoil beneath that part; and

(b) a part of the surface of the earth and a part of the subsoil beneath that part.

biodiesel means mono‑alkyl esters of fatty acids of a kind used as a fuel, derived from animal or vegetable fats or oils whether or not used.

blended tobacco goods has the meaning given by subsection 6AAC(1).

CEO means the Commissioner of Taxation.

delayed‑entry oil means stabilised crude petroleum oil or condensate (other than oil or condensate in respect of which subitem 20.1 or 21.1 of the Schedule applies) produced from a prescribed source, but not entered for home consumption, before the operative day for that source.

delayed‑entry oil rate, in relation to delayed‑entry oil, has the meaning given by section 6E.

diesel does not include biodiesel.

exempt offshore area means a production area, within the meaning of section 5B:

(a) that is outside the outer limits of the territorial sea of Australia; and

(b) that is not, and has not been, a prescribed source.

exempt offshore condensate means condensate that is included in exempt offshore oil and condensate.

exempt offshore field means a field:

(a) that is prescribed by By‑law; and

(b) that consists of, or encompasses, an exempt offshore area or 2 or more exempt offshore areas.

exempt offshore oil means stabilised crude petroleum oil that is included in exempt offshore oil and condensate.

exempt offshore oil and condensate means the first 4767.3 megalitres of:

(a) if a particular exempt offshore field produces stabilised crude petroleum oil and condensate—the stabilised crude petroleum oil and condensate that is produced from the field; or

(b) if a particular exempt offshore field produces either stabilised crude petroleum oil or condensate (but not both)—the stabilised crude petroleum oil or condensate (as the case requires) that is produced from the field;

being a field from which neither petroleum oil nor condensate was produced before 1 July 1987.

exempt oils and hydraulic fluids means goods described in subsection (6).

fuel oil means a petroleum product, whether obtained through a process of blending or otherwise, that has the physical characteristics described in subsection (4).

installation means a subsea installation, for the production of petroleum oil or condensate, that is connected to a fixed platform, a floating production system or any other petroleum collection system.

intermediate area means an area declared by the Resources Minister, by notice in writing published in the Gazette, to be an intermediate area for the purposes of this Act, being an area that contains at least one old accumulation but that does not contain a relevant accumulation which was developed before 23 October 1984.

intermediate oil means stabilized crude petroleum oil (other than new oil, delayed‑entry oil or oil in respect of which subitem 20.1 of the Schedule applies) produced from an intermediate area.

liquefied petroleum gas means:

(a) liquid propane; or

(b) a liquid mixture of propane and butane; or

(c) a liquid mixture of propane and other hydrocarbons that consists mainly of propane; or

(d) a liquid mixture of propane, butane and other hydrocarbons that consists mainly of propane and butane.

new oil means stabilized crude petroleum oil (other than delayed‑entry oil or oil in respect of which subitem 20.1 of the Schedule applies) produced from:

(a) a relevant accumulation that was discovered on or after 18 September 1975 and before 1 July 1983 by drilling a well that was classified by the Minister, for the purposes of Excise By‑law No. 78, as:

(i) a new field discovery; or

(ii) a new pool (pay) discovery; or

(iii) a deeper‑pool discovery; or

(iv) a shallower‑pool discovery;

subsequent to a determination of the well type by the relevant Energy Minister after drilling and before 1 July 1983; or

(b) a relevant accumulation that was discovered on or after 18 September 1975 and before 1 July 1983 by drilling a well that was not determined by the relevant Energy Minister before 1 July 1983 to be a well of any particular type; or

(c) a relevant accumulation that was discovered on or after 1 July 1983.

oil producing region:

(a) has the same meaning as in the Petroleum Excise (Prices) Act 1987; and

(b) includes:

(i) a production area within the meaning of section 5B, being an area from which condensate is obtained and that is prescribed by the regulations as an oil producing region; or

(ii) 2 or more production areas within the meaning of that section from which condensate is obtained, being areas that are together so prescribed.

Note: Part IA of the Petroleum Excise (Prices) Act 1987 gives that Act operation in relation to condensate in addition to its operation in relation to stabilised crude petroleum oil. Paragraph (b) of this definition ensures that the definition covers production areas from which condensate is obtained.

old accumulation means a relevant accumulation that was discovered before 18 September 1975.

onshore field means a field:

(a) that is prescribed by By‑law; and

(b) that consists of, or encompasses, a production area (within the meaning of section 5B), or 2 or more production areas, that:

(i) is in a State or Territory or inside the outer limits of the territorial sea of Australia; and

(ii) is not, and has not been, a prescribed source.

operative day, in relation to a prescribed source, means the 1 July that is the day prescribed petroleum produced from that source on or after which is exempt from Excise duty because of the Petroleum Revenue Act 1985.

platform means a platform for the production of petroleum oil or condensate.

pre‑operative year, in relation to a prescribed source, means the financial year immediately preceding the operative day for that source.

prescribed source means:

(a) a prescribed production area within the meaning of section 6B; or

(b) a prescribed new production area within the meaning of section 6C; or

(ba) a prescribed condensate production area within the meaning of section 6CA; or

(c) a prescribed intermediate production area within the meaning of section 6D;

prescribed petroleum produced from which after 1 July in a particular year is exempt from Excise duty because of the Petroleum Revenue Act 1985.

pre‑threshold onshore condensate means condensate that is included in pre‑threshold onshore oil and condensate.

pre‑threshold onshore oil means stabilised crude petroleum oil that is included in pre‑threshold onshore oil and condensate.

pre‑threshold onshore oil and condensate means:

(a) if a particular onshore field produces stabilised crude petroleum oil and condensate—stabilised crude petroleum oil and condensate produced from the field after 30 June 1987 that is included in the first 4767.3 megalitres of stabilised crude petroleum oil and condensate produced from the field; or

(b) if a particular onshore field produces stabilised crude petroleum oil but not condensate—stabilised crude petroleum oil produced from the field after 30 June 1987 that is included in the first 4767.3 megalitres of stabilised crude petroleum oil produced from the field; or

(c) if a particular onshore field produces condensate but not stabilised crude petroleum oil—condensate produced from the field after 30 June 1987 that is included in the first 4767.3 megalitres of condensate produced from the field.

relevant accumulation means a naturally occurring discrete accumulation of oil, of gas, or of both.

relevant Energy Minister means:

(a) on and after 18 September 1975 and before 5 October 1976—the Minister for Minerals and Energy; and

(b) on and after 5 October 1976 and before 20 December 1977—the Minister for National Resources; and

(c) on and after 20 December 1977 and before 8 December 1979—the Minister for National Development; and

(d) on and after 8 December 1979 and before 11 March 1983—the Minister for National Development and Energy; and

(e) on and after 11 March 1983 and before 1 July 1983—the Minister for Resources and Energy.

Resource Rent Tax area means an area that, for the purposes of the Petroleum Resource Rent Tax Assessment Act 1987:

(a) is the:

(i) exploration permit area of an exploration permit other than one of the North West Shelf exploration permits; or

(ii) retention lease area of a retention lease that is related to an exploration permit other than one of the North West Shelf exploration permits; or

(iii) production licence area of a production licence that is related to an exploration permit other than one of the North West Shelf exploration permits; and

(b) is not an onshore area within the meaning of that Act.

Statistician means the Australian Statistician.

(1A) For the avoidance of doubt, it is declared to be the intention of the Parliament that if:

(a) a particular area was, for the purposes of this Act as in force immediately before the date fixed by Proclamation for the commencement of this Act, an exempt onshore field; and

(b) with effect from that date that area became an onshore field for the purposes of that Act as in force at that date;

then, in calculating the first 4767.3 megalitres of stabilised crude petroleum oil produced from that particular onshore field for the purposes of the definition of pre‑threshold onshore oil, all oil that was, before that date, exempt onshore oil produced from that exempt onshore field is to be taken into account.

(2) For the purposes of this Act, a relevant accumulation shall be taken to be developed when petroleum, within the meaning of section 5B, is recovered from the accumulation for the purpose of:

(a) the sale of the petroleum; or

(b) the production from the petroleum of a product for sale.

(3) Without affecting the meaning of any reference to a month in any other provision of this Act or in any other Act, a reference in section 6AB, 6B, 6C, 6CA, 6D or 6E to a month is a reference to one of the 12 months of a calendar year.

(4) The physical characteristics of fuel oil are:

(a) a density equal to or greater than 920.0 kg/cubic metre at 15 degrees Celsius as determined by either ASTM D1298 or ASTM D4052; and

(b) a carbon residue, on the whole sample, of at least 2.0 percent mass as determined by ASTM D189 (Conradson Carbon Residue) or by ASTM D4530 (Carbon Residue‑Micro Method); and

(c) a minimum kinematic viscosity of 10 centistokes (millimetres squared per second) at 50 degrees Celsius as determined by ASTM D445.

(5) In subsection (4), a reference to ASTM followed by a number is a reference to a test so numbered as prescribed by the American Society for Testing and Materials and set out in Section 5 of the Annual Book of ASTM Standards (1986 revision) published in 1986 by the American Society for Testing and Materials at Philadelphia, Pennsylvania in the United States of America.

(6) Exempt oils and hydraulic fluids are:

(a) food grade white mineral oil that complies with:

(i) Sec. 21 CFR 172.878 of Title 21, Volume 1 of the United States Code of Federal Regulations (regulations made by the Food and Drug Administration of the United States); and

(ii) Sec. 21 CFR 178.3620 (a) of Title 21, Volume 1 of the United States Code of Federal Regulations (regulations made by the Food and Drug Administration of the United States); and

(b) polyglycol brake fluids that meet the requirements of Australian Standard AS 1960.1—2005 Motor vehicle brake fluids—Non‑petroleum type; and

(c) aromatic process oils that meet all of the criteria in the following table:

Column 1 Property | Column 2 Test Method | Column 3 Value |

Density at 15°C | ATSM D1298 or D4502 | 0.9gm/cm3 minimum |

Aniline point | ASTM D611 | 70°C maximum |

Refractive index at 20°C | ASTM D1298 or D1747 | 1.490 minimum |

Pour point | ASTM D97 | ‑9°C minimum |

Viscosity index | ASTM D2270 | 80 maximum |

3A Ministerial guidelines relating to fields

(1) The Resources Minister may, by legislative instrument signed by the Minister, make guidelines to be taken into account by the CEO in making By‑laws prescribing a field for the purposes of the definition of onshore field or exempt offshore field.

(2) In making By‑laws for a purpose described in subsection (1), the CEO must have regard to the guidelines in force at the time.

4 Time of imposition of Duties of Excise

The time of imposition of the Duties of Excise imposed by this Act is the twenty‑fifth day of March, One thousand nine hundred and twenty at nine o’clock in the forenoon reckoned according to the standard time in the State of Victoria, and this Act shall be deemed to have come into operation at that time.

5 Duties of Excise

(1) The Duties of Excise specified in the Schedule are hereby imposed in accordance with the Schedule, as from the time of the imposition of such duties or such later dates as are mentioned in the Schedule in regard to any particular items, and such duties shall be deemed to have been imposed at such time or dates, and shall be charged, collected, and paid to the use of the King for the purposes of the Commonwealth, on the following goods, namely:

(a) all goods dutiable under the Schedule and manufactured or produced in Australia after the time or dates when such duties are deemed to have been imposed; and

(b) all goods dutiable under the Schedule and manufactured or produced in Australia before the time or dates when such duties are deemed to have been imposed, and which were at that time or those dates subject to the CEO’s control, or in the stock, custody, or possession of, or belonging to, any distiller or manufacturer thereof, and on which no duty of Excise had been paid before the time or dates when such duties are deemed to have been imposed.

Note: Sections 6A and 6AA effectively change certain rates of duty that appear on the face of the Schedule.

(2) Where a section of another Act, whether passed before or after the commencement of this subsection, amends the Schedule to this Act, then, unless the contrary intention appears:

(a) that section imposes duties of Excise in accordance with the Schedule as so amended;

(b) where that section comes, came, or is deemed to have come, into operation on a particular day, the duties of Excise so imposed shall be charged, collected and paid:

(i) on all goods dutiable under the Schedule, as amended and in force on that day, and manufactured or produced in Australia on or after that day; and

(ii) on all goods dutiable under the Schedule, as amended and so in force, and manufactured or produced in Australia before that day, being goods:

(A) that, on that day, were subject to the CEO’s control, or, on that day, were in the stock, custody or possession of, or belonged to, a manufacturer or producer of the goods; and

(B) on which no duty of Excise had been paid before that day; and

(c) where that section comes, came, or is deemed to have come, into operation at a particular time, the duties of Excise so imposed shall be charged, collected and paid:

(i) on all goods dutiable under the Schedule, as amended and in force at that time, and manufactured or produced in Australia at or after that time; and

(ii) on all goods dutiable under the Schedule, as amended and in force at that time, and manufactured or produced in Australia before that time, being goods:

(A) that, at that time, were subject to the CEO’s control, or, at that time were in the stock, custody or possession of, or belonged to, the manufacturer or producer of the goods; and

(B) on which no duty of Excise had been paid before that time.

5B Petroleum

(1) In this section:

petroleum means petroleum oil or petroleum gas and includes condensate or liquid petroleum gas.

prescribed petroleum means petroleum other than stabilized oil.

production area means:

(a) a prescribed production area within the meaning of section 6B; or

(b) a prescribed new production area within the meaning of section 6C; or

(ba) a prescribed condensate production area within the meaning of section 6CA; or

(c) a prescribed intermediate production area within the meaning of section 6D.

stabilized oil means stabilized crude petroleum oil.

(2) Subject to subsections (3) and (3A), for the purposes of this Act, where a mixing of 2 or more kinds of petroleum has occurred and the resulting mixture takes on the essential character of petroleum of one of those kinds (in this subsection referred to as petroleum of the principal kind), the petroleum in the mixture shall be deemed to be petroleum of the principal kind.

(3) For the purposes of this Act, where a person enters for home consumption a mixture of, or obtained from, stabilized oil and prescribed petroleum (other than condensate), the petroleum in the mixture shall be deemed to be stabilized oil.

Note: A mixture of, or obtained from, stabilized oil and condensate is covered by subsection (2).

(3A) For the purposes of this Act, if a person enters for home consumption a mixture of, or obtained from, condensate and prescribed petroleum, the petroleum in the mixture is taken to be condensate.

Note: A mixture of, or obtained from, stabilized oil and condensate is covered by subsection (2).

(4) For the purposes of this Act, where stabilized oil or condensate is obtained from prescribed petroleum produced from a particular production area, that oil or condensate (as the case requires) shall be taken to have been produced from that production area.

(4A) For the purposes of this Act, where stabilized oil or condensate is obtained from prescribed petroleum produced from a Resource Rent Tax area, that oil or condensate (as the case requires) shall be taken to have been produced from that area.

(5) For the purposes of this Act, where a quantity of stabilized oil consists of oil obtained from prescribed petroleum produced from different production areas:

(a) the prescribed petroleum produced from each of those production areas shall be deemed to have resulted in the production of a discrete part of that quantity of stabilized oil; and

(b) the part of that quantity of stabilized oil that is to be taken to have been obtained from prescribed petroleum produced from such a production area is so much of that quantity of stabilized oil as bears to that quantity the same proportion as the quantity of prescribed petroleum produced from that production area bears to the total quantity of prescribed petroleum produced from all the production areas from which that quantity of stabilized oil was so obtained.

6A Indexation of CPI indexed rates

(1) If the indexation factor for an indexation day is greater than 1, each CPI indexed rate is, on that day, replaced by the rate of duty worked out using the formula:

Note: For indexation factor see subsection (3). For CPI indexed rate and indexation day see subsection (10).

(2) The amount worked out under subsection (1) is to be rounded to the same number of decimal places as the CPI indexed rate was on the day before the indexation day (rounding up if the next decimal place is 5 or more).

Indexation factor

(3) The indexation factor for an indexation day is the number worked out using the formula:

Note: For index number, reference quarter and base quarter see subsection (10).

(4) The indexation factor is to be worked out to 3 decimal places (rounding up if the fourth decimal place is 5 or more).

Effect of delay in publication of index number

(5) If the index number for the most recent reference quarter before the indexation day is published by the Statistician on a day (the publication day) that is not at least 5 days before the indexation day, then, despite subsection (1), any replacement of a CPI indexed rate under subsection (1) happens on the fifth day after the publication day.

Effect of Excise Tariff alteration

(6) If an Excise Tariff alteration proposed in the Parliament proposes to substitute, on and after a particular day, a rate for a CPI indexed rate, treat that substitution as having had effect on and after that day for the purposes of this section.

Changes to CPI index reference period and publication of substituted index numbers

(7) Amounts are to be worked out under this section:

(a) using only the index numbers published in terms of the most recently published index reference period for the Consumer Price Index; and

(b) disregarding index numbers published in substitution for previously published index numbers (except where the substituted numbers are published to take account of changes in the index reference period).

Application of replacement rate

(8) If a CPI indexed rate is replaced under this section on a particular day, the replacement rate applies in relation to goods entered for home consumption on or after that day.

Publication of replacement rate

(9) The CEO must, on or as soon as practicable after the day a CPI indexed rate is replaced under this section, publish a notice in the Gazette advertising the replacement rate and the goods it applies to.

Definitions

(10) In this section:

base quarter means the June quarter or December quarter that has the highest index number of all the June quarters and December quarters that occur:

(a) before the most recent reference quarter before the indexation day; and

(b) after the June quarter of 1983.

CPI indexed rate means:

(a) a rate of duty set out in item 1, 2 or 3 of the Schedule; or

(b) a rate of duty set out in item 10 of the Schedule, other than in:

(i) subitem 10.6 or 10.17; or

(ii) subitem 10.7, 10.12, 10.20, 10.21 or 10.30; or

(c) the rate set out in step 3 of the method statement in subsection 6G(1) (about duty payable on blended goods).

December quarter means a period of 3 months starting on 1 October.

indexation day means each 1 February and 1 August.

index number, for a quarter, means the All Groups Consumer Price Index number that is the weighted average of the 8 capital cities and is published by the Statistician in relation to that quarter.

June quarter means a period of 3 months starting on 1 April.

reference quarter means the June quarter or December quarter.

6AAA Rounding of fuel duty rates

(1) Despite subsection 6A(2), the amount to be worked out under subsection 6A(1) in respect of an indexation day for a CPI indexed rate covered by subsection (3) of this section is to be rounded to 3 decimal places (rounding up if the next decimal place is 5 or more).

(2) For the purposes of section 6A, determine the CPI indexed rate on the day before the indexation day as mentioned in subsection 6A(1) on the assumptions that:

(a) the operation of subsection (1) of this section was disregarded in respect of all previous indexation days (if any); and

(b) subsection 6A(2) permitted amounts worked out under subsection 6A(1) in respect of those indexation days to be rounded to 5 decimal places (rounding up if the next decimal place was 5 or more).

(3) This subsection covers the following CPI indexed rates:

(a) a rate of duty set out in item 10 of the Schedule, other than in:

(i) subitem 10.6 or 10.17; or

(ii) subitem 10.7, 10.12, 10.20, 10.21 or 10.30;

(b) the rate set out in step 3 of the method statement in subsection 6G(1) (about duty payable on blended goods).

(4) In this section:

CPI indexed rate has the same meaning as in section 6A.

indexation day has the same meaning as in section 6A.

6AA Indexing of tobacco duty rate under subitem 5.1 of the Schedule

(1) If the indexation factor for an indexation day is at least 1, the rate of duty set out in subitem 5.1 of the Schedule (the tobacco duty rate) is, on that day, replaced by the rate of duty worked out using the formula:

Note: For indexation factor see subsections (3) and (5), for indexation day see subsection (12) and for additional factor see subsection (6).

(2) The amount worked out under subsection (1) is to be rounded to 5 decimal places (rounding up if the sixth decimal place is 5 or more).

Indexation factor

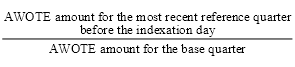

(3) The indexation factor for an indexation day is the number worked out using the formula:

Note: For AWOTE amount, reference quarter and base quarter see subsection (12).

(4) The indexation factor is to be worked out to 3 decimal places (rounding up if the fourth decimal place is 5 or more).

(5) Despite subsection (3), treat the indexation factor for 1 September 2014, 1 September 2015, 1 September 2016, 1 September 2017, 1 September 2018, 1 September 2019 or 1 September 2020 as 1 if, on that day, it would otherwise be less than 1.

Additional factor

(6) The additional factor for an indexation day is:

(a) 1.125, if the indexation day is 1 September 2014, 1 September 2015, 1 September 2016, 1 September 2017, 1 September 2018, 1 September 2019 or 1 September 2020; or

(b) 1, for each other indexation day.

Effect of delay in publication of AWOTE amount

(7) If the AWOTE amount for the most recent reference quarter before the indexation day is published by the Statistician on a day (the publication day) that is not at least 5 days before the indexation day, then, despite subsection (1), any replacement of a tobacco duty rate under subsection (1) happens on the fifth day after the publication day.

Effect of Excise Tariff alteration

(8) If an Excise Tariff alteration proposed in the Parliament proposes to substitute, on and after a particular day, a rate for a tobacco duty rate, treat that substitution as having had effect on and after that day for the purposes of this section.

Publication of substituted AWOTE amounts

(9) If the Statistician publishes an estimate of full‑time adult average weekly ordinary time earnings for persons in Australia for a period for which such an estimate was previously published by the Statistician, the publication of the later estimate is to be disregarded for the purposes of this section.

Application of replacement rate

(10) If a tobacco duty rate is replaced under this section on a particular day, the replacement rate applies in relation to goods entered for home consumption on or after that day.

Publication of replacement rate

(11) The CEO must, on or as soon as practicable after the day a tobacco duty rate is replaced under this section, publish a notice in the Gazette advertising the replacement rate and the goods it applies to.

Definitions

(12) In this section:

AWOTE amount, for a quarter, means the estimate of the full‑time adult average weekly ordinary time earnings for persons in Australia for the middle month of the quarter published by the Statistician in relation to that month.

base quarter means the June quarter or December quarter that has the highest AWOTE amount of all the June quarters and December quarters that occur:

(a) before the most recent reference quarter before the indexation day; and

(b) after the December quarter of 2012.

December quarter means a period of 3 months starting on 1 October.

indexation day means each 1 March and 1 September.

June quarter means a period of 3 months starting on 1 April.

reference quarter means the June quarter or December quarter.

6AAB Tobacco duty rate under subitem 5.5 of the Schedule

(1) For the purposes of subitem 5.5 of the Schedule, the applicable rate on a day is the amount worked out using the formula:

(2) The weight conversion factor is:

(a) for a day on or after the first replacement day and before the second replacement day—0.000775; or

(b) for a day on or after the second replacement day and before the third replacement day—0.00075; or

(c) for a day on or after the third replacement day and before the fourth replacement day—0.000725; or

(d) for a day on or after the fourth replacement day—0.0007.

Rounding

(3) The amount worked out under subsection (1) is to be rounded to 2 decimal places (rounding up if the third decimal place is 5 or more).

Replacement days

(4) For the purposes of this section, the first replacement day is:

(a) 1 September 2017; or

(b) if, in relation to the indexation day that is 1 September 2017, subsection 6AA(7) has the effect of replacing a rate of duty on a later day—that later day.

(5) For the purposes of this section, the second replacement day is:

(a) 1 September 2018; or

(b) if, in relation to the indexation day that is 1 September 2018, subsection 6AA(7) has the effect of replacing a rate of duty on a later day—that later day.

(6) For the purposes of this section, the third replacement day is:

(a) 1 September 2019; or

(b) if, in relation to the indexation day that is 1 September 2019, subsection 6AA(7) has the effect of replacing a rate of duty on a later day—that later day.

(7) For the purposes of this section, the fourth replacement day is:

(a) 1 September 2020; or

(b) if, in relation to the indexation day that is 1 September 2020, subsection 6AA(7) has the effect of replacing a rate of duty on a later day—that later day.

Application of applicable rate

(8) If the applicable rate changes on a particular day, the changed rate applies in relation to goods entered for home consumption on or after that day.

Publication

(9) The CEO must, on or as soon as practicable after the day the rate of duty set out in subitem 5.1 of the Schedule is replaced under section 6AA, publish a notice in the Gazette advertising:

(a) the rate of duty under subitem 5.5 of the Schedule on that day; and

(b) the goods to which subitem 5.5 of the Schedule applies.

6AAC Duty payable on blended tobacco goods

(1) Work out the duty payable under this Act on goods (the blended tobacco goods) that would, apart from this section, be classified to subitem 5.1 or 5.5 of the Schedule and that consist of constituents that are classified to either of those subitems, or to subitem 5.8 of the Schedule because of a previous operation of this section, as follows:

Method statement

Step 1. Work out the amount of duty that would, apart from this section, be payable on the blended tobacco goods.

Step 2. Add up the amount of duty previously payable on each constituent that is classified to subitem 5.1, 5.5 or 5.8 of the Schedule.

Step 3. Subtract the result of step 2 from the result of step 1.

Step 4. The duty payable on the blended tobacco goods is:

(a) the result of step 3; or

(b) if the result of step 3 is less than zero—zero.

(2) If a constituent of the blended tobacco goods was imported, assume for the purposes of subsection (1) that:

(a) the constituent was manufactured in Australia when it was imported; and

(b) if customs duty was paid on the constituent—there was a payment of Excise duty equal to the lesser of the following amounts (or either of them if they are equal):

(i) the amount of Excise duty that would have been payable on the constituent had it been manufactured in Australia when it was imported;

(ii) the amount of the customs duty paid.

6AB Applicable petroleum prices

For the purposes of section 6B, 6C, 6CA or 6D, at any particular time the applicable petroleum price for a month occurring after 30 June 1997 in respect of stabilized crude petroleum oil or condensate, obtained from a production area, that is a prescribed production area, a prescribed new production area, a prescribed condensate production area or a prescribed intermediate production area, as the case requires, for the purposes of that section, is:

(a) if at that time the final VOLWARE price for stabilized crude petroleum oil or condensate (as the case requires) for the month and an oil producing region that constitutes or includes that production area has been determined under section 7 of the Petroleum Excise (Prices) Act 1987—that final VOLWARE price; or

(b) if at that time the final VOLWARE price for stabilized crude petroleum oil or condensate (as the case requires) has not been so determined—the interim VOLWARE price for stabilized crude petroleum oil or condensate (as the case requires) determined under that section for the month and an oil producing region that constitutes or includes that production area.

6AC Application of section 6B, 6C, 6CA or 6D to different oil producing regions

If:

(a) a final VOLWARE price or an interim VOLWARE price for stabilized crude petroleum oil or condensate (as the case requires) has been, or is taken to have been, determined under the Petroleum Excise (Prices) Act 1987 for a month and an oil producing region; and

(b) that oil producing region is constituted by or includes:

(i) a particular prescribed production area within the meaning of section 6B; or

(ii) a particular prescribed new production area within the meaning of section 6C; or

(iii) a particular prescribed condensate production area within the meaning of section 6CA; or

(iv) a particular prescribed intermediate production area within the meaning of section 6D;

that determination is taken to have effect, and, at all material times to have had effect, in the application of that section in respect of stabilized crude petroleum or condensate (as the case requires) obtained from that production area, as if it were also a determination of that price made in respect of that particular production area.

6B Duties of excise on old oil

Definitions

(1) In this section:

adjusted previous year’s duty, in relation to a prescribed production area in relation to a month of a financial year, means the amount of duty that, at the end of the financial year immediately preceding the financial year in which that month occurs, would have been payable in respect of old oil produced from that area and entered for home consumption during that preceding year if, for the prices that were, at the end of that preceding year, the applicable petroleum prices for all of the months of that preceding year, there had been substituted the prices that are, at the end of that first‑mentioned month, the respective applicable petroleum prices for all of those months.

non‑adjusted previous year’s duty, in relation to a prescribed production area in relation to a month of a financial year, means the amount of duty that, at the end of the financial year immediately preceding the financial year in which that month occurs, would have been payable in respect of old oil produced from that area and entered for home consumption during that preceding year if, for the prices that were, at the end of that preceding year, the applicable petroleum prices for all of the months of that preceding year, there had been substituted the prices that were, immediately before the commencement of that first‑mentioned month, the respective applicable petroleum prices for all of those months.

old oil means stabilised crude petroleum oil in respect of which subitem 20.7 of the Schedule applies.

prescribed production area means a petroleum production area prescribed by by‑laws (which, without limiting the generality of the foregoing, may be a relevant accumulation, a well, an oilfield or a gas field).

Introduction

(2) The amount of duty in respect of old oil ascertained in accordance with this section shall be ascertained by reference to the prescribed production area from which the oil is produced and to the month of a financial year during which the oil is entered for home consumption.

The amount of duty

(3) Subject to subsection (3A), the amount of duty in respect of old oil produced from a prescribed production area and entered for home consumption during a month of a financial year commencing on or after 1 July 2001 is the amount worked out using the formula:

where:

credited adjustment amount is the credited adjustment amount (if any) for that area and that month, worked out in accordance with subsection (5C).

debited adjustment amount is the debited adjustment amount (if any) for that area and that month, worked out in accordance with subsection (5B).

duty paid is the amount of duty (if any) paid in respect of old oil produced from that area and entered for home consumption during the period starting at the start of that financial year and ending at the end of that month.

notional duty is the amount of notional duty in respect of old oil produced from that area and entered for home consumption during the period starting at the start of that financial year and ending at the end of that month, worked out in accordance with subsection (4).

Disregarding certain amounts when working out amount of duty

(3A) In working out, for the purposes of subsection (3), the amount of duty paid in respect of old oil produced from a prescribed production area and entered for home consumption during a period starting at the start of a financial year and ending at the end of a month of that year, the following amounts are to be disregarded:

(a) any increases in the amount of duty paid as a result of the addition of debited adjustment amounts for that area for any of the preceding months of that year;

(b) any decreases in that amount as a result of the subtraction of credited adjustment amounts for that area for any of those months.

The total amount of notional duty

(4) The amount of notional duty in respect of old oil produced from a particular prescribed production area and entered for home consumption during a particular period is the sum of the amounts of notional duty in respect of:

(a) the quantity (if any) of the oil that exceeds A 4B but does not exceed A 6B; and

(b) the quantity (if any) of the oil that exceeds A 6B but does not exceed A 8B; and

(c) the quantity (if any) of the oil that exceeds A 8B but does not exceed A 10B; and

(d) the quantity (if any) of the oil that exceeds A 10B but does not exceed A 12B; and

(e) the quantity (if any) of the oil that exceeds A 12B;

where:

A is the number of days in the period.

B is:

(a) where the period is in a year in which there are 365 days—136.98630 kilolitres; or

(b) where the period is in a year in which there are 366 days—136.61202 kilolitres.

The amount of notional duty for a quantity of oil—one petroleum price

(5) Subject to subsections (6) and (9), the amount of notional duty in respect of a quantity of oil referred to in subsection (4) is an amount equal to the relevant percentage (set out in subsection (7)) of the product of:

(a) the amount specified in the price that is, at the end of the period referred to in subsection (4) in relation to the quantity of oil, the applicable petroleum price for the month in which the period comes to an end; and

(b) the number of kilolitres in that quantity;

calculated to the nearest cent.

The debited adjustment amount

(5B) Where:

(a) during a month of a financial year, a VOLWARE price for stabilised crude petroleum oil for a month of the immediately preceding financial year and a particular prescribed production area is determined under section 7 of the Petroleum Excise (Prices) Act 1987; and

(b) the adjusted previous year’s duty for that prescribed production area for that first‑mentioned month is greater than the non‑adjusted previous year’s duty for that area for that first‑mentioned month;

there is a debited adjustment amount for that area for that first‑mentioned month, being an amount equal to the difference between that adjusted previous year’s duty and that non‑adjusted previous year’s duty.

The credited adjustment amount

(5C) Where:

(a) during a month of a financial year, a VOLWARE price for stabilised crude petroleum oil for a month of the immediately preceding financial year and a particular prescribed production area is determined under section 7 of the Petroleum Excise (Prices) Act 1987; and

(b) the adjusted previous year’s duty for that prescribed production area for that first‑mentioned month is less than the non‑adjusted previous year’s duty for that area for that first‑mentioned month;

there is a credited adjustment amount for that area for that first‑mentioned month, being an amount equal to the difference between that non‑adjusted previous year’s duty and that adjusted previous year’s duty.

The amount of notional duty for a quantity of oil—more than one petroleum price

(6) Where, at the end of a period in a financial year, the applicable petroleum prices for the months in which the period occurs and a particular prescribed production area are not all the same, the amount of the notional duty in respect of a quantity of oil referred to in subsection (4) produced from that production area and entered for home consumption during the period is an amount equal to the relevant percentage (set out in subsection (7)) of the sum of the amounts calculated in respect of each such applicable petroleum price in operation during the period in accordance with the formula:

where:

P is the amount specified in the applicable petroleum price.

Q is the number of kilolitres in the quantity of oil referred to in subsection (4).

K is the number of kilolitres of old oil produced from that production area and entered for home consumption during that part of the period during which the applicable petroleum price was in operation.

KT is the number of kilolitres of old oil produced from that production area and entered for home consumption during the period.

Relevant percentage for a quantity of oil

(7) For the purposes of subsections (5) and (6), the relevant percentage in relation to a quantity of oil referred to in subsection (4) is:

(a) in the case of a quantity to which paragraph 4(a) applies—20%; and

(b) in the case of a quantity to which paragraph 4(b) applies—30%; and

(c) in the case of a quantity to which paragraph 4(c) applies—40%; and

(d) in the case of a quantity to which paragraph 4(d) applies—50%; and

(e) in the case of a quantity to which paragraph 4(e) applies—55%.

Rounding the number of kilolitres in a quantity of oil

(8) For the purposes of subsections (5) and (6), the number of kilolitres in a quantity of oil shall be taken to be a number equal to:

(a) unless paragraph (b) applies—the number of kilolitres in that quantity calculated to 1 decimal place; or

(b) where the number of kilolitres in that quantity calculated to 2 decimal places ends in a number greater than 4—the number of kilolitres in that quantity calculated to 1 decimal place increased by 0.1.

The amount of notional duty—dealing with the first year of production

(9) Where no old oil produced from a particular prescribed production area was ever entered for home consumption before the expiration of the first month of a particular financial year, then, in ascertaining, in accordance with subsections (4), (5) and (7) or (4), (6) and (7), the notional duty in respect of old oil produced from that production area and entered for home consumption during a later month (in this subsection referred to as the relevant month) of that financial year, those subsections have effect in relation to the old oil as if each reference in a paragraph of subsection (4) to B were a reference to the product of B and the factor ascertained in accordance with the formula:

where:

G is the number of days in the period commencing on the day on which old oil produced from the prescribed production area was first entered for home consumption and ending on the expiration of the relevant month; and

H is the number of days in the period commencing on the first day of the financial year and ending on the expiration of the relevant month.

Interpretation of the Schedule

(10) The words set out after “, if higher,” in the column headed “Rate of Duty” in subitem 20.7 of the Schedule shall be deemed, for the purposes of this Act or any other law of the Commonwealth, to be a rate of duty.

6C Duties of excise on new oil

Definitions

(1) In this section:

adjusted previous year’s duty, in relation to a prescribed new production area in relation to a month of a financial year, means the amount of duty that, at the end of the financial year immediately preceding the financial year in which that month occurs, would have been payable in respect of new oil produced from that area and entered for home consumption during that preceding year if, for the prices that were, at the end of that preceding year, the applicable petroleum prices for all of the months of that preceding year, there had been substituted the prices that are, at the end of that first‑mentioned month, the respective applicable petroleum prices for all of those months.

non‑adjusted previous year’s duty, in relation to a prescribed new production area in relation to a month of a financial year, means the amount of duty that, at the end of the financial year immediately preceding the financial year in which that month occurs, would have been payable in respect of new oil produced from that area and entered for home consumption during that preceding year if, for the prices that were, at the end of that preceding year, the applicable petroleum prices for all of the months of that preceding year, there had been substituted the prices that were, immediately before the commencement of that first‑mentioned month, the respective applicable petroleum prices for all of those months.

prescribed new production area means a new petroleum production area prescribed by by‑laws (which, without limiting the generality of the foregoing, may be a relevant accumulation, a well, an oilfield or a gas field).

Introduction

(2) The amount of duty in respect of new oil ascertained in accordance with this section shall be ascertained by reference to the prescribed new production area from which the oil is produced and to the month of a financial year during which the oil is entered for home consumption.

The amount of duty

(3) Subject to subsection (3A), the amount of duty in respect of new oil produced from a prescribed new production area and entered for home consumption during a month of a financial year commencing on or after 1 July 2001 is the amount worked out using the formula:

where:

notional duty is the amount of notional duty in respect of new oil produced from that area and entered for home consumption during the period starting at the start of that financial year and ending at the end of that month, worked out in accordance with subsection (4).

debited adjustment amount is the debited adjustment amount (if any) for that area and that month, worked out in accordance with subsection (5A).

duty paid is the amount of duty (if any) paid in respect of new oil produced from that area and entered for home consumption during the period starting at the start of that financial year and ending at the end of that month.

credited adjustment amount is the credited adjustment amount (if any) for that area and that month, worked out in accordance with subsection (5B).

Disregarding certain amounts when working out amount of duty

(3A) In working out, for the purposes of subsection (3), the amount of duty paid in respect of new oil produced from a prescribed new production area and entered for home consumption during a period starting at the start of a financial year and ending at the end of a month of that year, the following amounts are to be disregarded:

(a) any increases in the amount of duty paid as a result of the addition of debited adjustment amounts for that area for any of the preceding months of that year;

(b) any decreases in that amount as a result of the subtraction of credited adjustment amounts for that area for any of those months.

The total amount of notional duty

(4) The amount of notional duty in respect of new oil produced from a particular prescribed new production area and entered for home consumption during a particular period is the sum of the amounts of notional duty in respect of:

(a) the quantity (if any) of the oil that exceeds A  10B but does not exceed A

10B but does not exceed A  12B;

12B;

(b) the quantity (if any) of the oil that exceeds A  12B but does not exceed A

12B but does not exceed A  14B;

14B;

(c) the quantity (if any) of the oil that exceeds A  14B but does not exceed A

14B but does not exceed A  16B; and

16B; and

(d) the quantity (if any) of the oil that exceeds A  16B;

16B;

where:

A is the number of days in the period.

B is:

(a) where the period in a year in which there are 365 days—136.98630 kilolitres; or

(b) where the period is in a year in which there are 366 days—136.61202 kilolitres.

The amount of notional duty for a quantity of oil—one petroleum price

(5) Subject to subsections (6) and (9), the amount of notional duty in respect of a quantity of oil referred to in subsection (4) is an amount equal to the relevant percentage (set out in subsection (7)) of the product of:

(a) the amount specified in the price that is, at the end of the period referred to in subsection (4) in relation to the quantity of oil, the applicable petroleum price for the month in which the period comes to an end; and

(b) the number of kilolitres in that quantity;

calculated to the nearest cent.

The debited adjustment amount

(5A) Where:

(a) during a month of a financial year, a VOLWARE price for stabilised crude petroleum oil for a month of the immediately preceding financial year and a particular prescribed new production area is determined under section 7 of the Petroleum Excise (Prices) Act 1987; and

(b) the adjusted previous year’s duty for that prescribed new production area for that first‑mentioned month is greater than the non‑adjusted previous year’s duty for that area for that first‑mentioned month;

there is a debited adjustment amount for that area for that first‑mentioned month, being an amount equal to the difference between that adjusted previous year’s duty and that non‑adjusted previous year’s duty.

The credited adjustment amount

(5B) Where:

(a) during a month of a financial year, a VOLWARE price for stabilised crude petroleum oil for a month of the immediately preceding financial year and a particular prescribed new production area is determined under section 7 of the Petroleum Excise (Prices) Act 1987; and

(b) the adjusted previous year’s duty for that prescribed new production area for that first‑mentioned month is less than the non‑adjusted previous year’s duty for that area for that first‑mentioned month;

there is a credited adjustment amount for that area for that first‑mentioned month, being an amount equal to the difference between that non‑adjusted previous year’s duty and that adjusted previous year’s duty.

The amount of notional duty for a quantity of oil—more than one petroleum price

(6) Where, at the end of a period in a financial year, the applicable petroleum prices for the months in which the period occurs and a particular prescribed new production area are not all the same, the amount of the notional duty in respect of a quantity of oil referred to in subsection (4) produced from that production area and entered for home consumption during the period is an amount equal to the relevant percentage (set out in subsection (7)) of the sum of the amounts calculated in respect of each such applicable petroleum price in operation during the period in accordance with the formula:

where:

P is the amount specified in the applicable petroleum price.

Q is the number of kilolitres in the quantity of oil referred to in subsection (4).

K is the number of kilolitres of new oil produced from that production area and entered for home consumption during that part of the period during which the applicable petroleum price was in operation.

KT is the number of kilolitres of new oil produced from that production area and entered for home consumption during the period.

Relevant percentage for a quantity of oil

(7) For the purposes of subsections (5) and (6), the relevant percentage in relation to a quantity of oil referred to in subsection (4) is:

(a) in the case of a quantity to which paragraph 4(a) applies—10%; and

(b) in the case of a quantity to which paragraph 4(b) applies—15%; and

(c) in the case of a quantity to which paragraph 4(c) applies—20%; and

(d) in the case of a quantity to which paragraph 4(d) applies—30%.

Rounding the number of kilolitres in a quantity of oil

(8) For the purposes of subsections (5) and (6), the number of kilolitres in a quantity of oil shall be taken to be a number equal to:

(a) unless paragraph (b) applies—the number of kilolitres in that quantity calculated to 1 decimal place; or

(b) where the number of kilolitres in that quantity calculated to 2 decimal places ends in a number greater than 4—the number of kilolitres in that quantity calculated to 1 decimal place increased by 0.1.

The amount of notional duty—dealing with the first year of production

(9) When no new oil produced from a particular prescribed new production area was ever entered for home consumption before the expiration of the first month of a particular financial year, then, in ascertaining, in accordance with subsections (4), (5) and (7) or (4), (6) and (7), the notional duty in respect of new oil produced from the production area and entered for home consumption during a later month (in this subsection referred to as the relevant month) of that financial year, those subsections have effect in relation to the new oil as if each reference in a paragraph of subsection (4) to B were a reference to the product of B and the factor ascertained in accordance with the formula:

where:

M is the number of days in the period commencing on the day on which new oil produced from the prescribed new production area was first entered for home consumption and ending on the expiration of the relevant month; and

N is the number of days in the period commencing on the first day of the financial year and ending on the expiration of the relevant month.

Interpretation of the Schedule

(10) The words set out after “, if higher,” in the column headed “Rate of Duty” in subitem 20.5 of the Schedule shall be deemed, for the purposes of this Act or any other law of the Commonwealth, to be a rate of duty.

6CA Duties of excise on condensate

Definitions

(1) In this section:

adjusted previous year’s duty, in relation to a prescribed condensate production area in relation to a month of a financial year, means the amount of duty that, at the end of the financial year immediately preceding the financial year in which that month occurs, would have been payable in respect of condensate produced from that area and entered for home consumption during that preceding year if, for the prices that were, at the end of that preceding year, the applicable petroleum prices for all of the months of that preceding year, there had been substituted the prices that are, at the end of that first‑mentioned month, the respective applicable petroleum prices for all of those months.

non‑adjusted previous year’s duty, in relation to a prescribed condensate production area in relation to a month of a financial year, means the amount of duty that, at the end of the financial year immediately preceding the financial year in which that month occurs, would have been payable in respect of condensate produced from that area and entered for home consumption during that preceding year if, for the prices that were, at the end of that preceding year, the applicable petroleum prices for all of the months of that preceding year, there had been substituted the prices that were, immediately before the commencement of that first‑mentioned month, the respective applicable petroleum prices for all of those months.

prescribed condensate production area has the meaning given by subsection (1A).

(1A) Prescribed condensate production area means any of the following:

(a) a condensate production area prescribed by by‑laws (which, without limiting the generality of the foregoing, may be a relevant accumulation, a well, an oilfield or a gas field);

(b) the Rankin Trend (see subsection (1B)).

Note: A by‑law may be expressed to commence before the day it is registered under the Legislation Act 2003 (see subsection 12(1A) of that Act).

(1B) The Rankin Trend means the area that includes the following:

(a) the reservoirs, or groups of reservoirs, known as:

(i) North Rankin; and

(ii) Perseus; and

(iii) Searipple; and

(iv) Goodwyn; and

(v) Keast/Dockrell; and

(vi) Echo/Yodel;

(b) other reservoirs, or groups of reservoirs, (if any) that are specified in the regulations made for the purposes of this paragraph.

(1C) Before the Governor‑General makes a regulation specifying a reservoir, or a group of reservoirs, for the purposes of paragraph (1B)(b):

(a) the Resources Minister must be satisfied that the reservoir, or the group of reservoirs, is part of the same field as a reservoir or group of reservoirs mentioned in paragraph (1B)(a); and

(b) if the Resources Minister is so satisfied—the Resources Minister must consider the effect of specifying the reservoir, or the group of reservoirs, on the efficient exploitation of the resource related to the reservoir, or to the group of reservoirs.

(1D) Subsection 12(2) (retrospective application of legislative instruments) of the Legislation Act 2003 does not apply to regulations specifying a reservoir, or a group of reservoirs, for the purposes of paragraph (1B)(b) of this section.

(1E) Subsection (1D) does not apply to regulations that create, modify or otherwise affect a provision that makes a person liable to an offence or civil penalty.

Introduction

(2) The amount of duty in respect of condensate ascertained in accordance with this section is to be ascertained by reference to the prescribed condensate production area from which the condensate is produced and to the month of a financial year during which the condensate is entered for home consumption.

The amount of duty

(3) Subject to subsection (4), the amount of duty in respect of condensate produced from a prescribed condensate production area and entered for home consumption during a month of a financial year is the amount worked out using the formula:

where:

credited adjustment amount is the credited adjustment amount (if any) for that area and that month, worked out in accordance with subsection (8).

debited adjustment amount is the debited adjustment amount (if any) for that area and that month, worked out in accordance with subsection (7).

duty paid is the amount of duty (if any) paid in respect of condensate produced from that area and entered for home consumption during the period starting at the start of that financial year and ending at the end of that month.

notional duty is the amount of notional duty in respect of condensate produced from that area and entered for home consumption during the period starting at the start of that financial year and ending at the end of that month, worked out in accordance with subsection (5).

Disregarding certain amounts when working out amount of duty

(4) In working out, for the purposes of subsection (3), the amount of duty paid in respect of condensate produced from a prescribed condensate production area and entered for home consumption during a period starting at the start of a financial year and ending at the end of a month of that year, the following amounts are to be disregarded:

(a) any increases in the amount of duty paid as a result of the addition of debited adjustment amounts for that area for any of the preceding months of that year;

(b) any decreases in that amount as a result of the subtraction of credited adjustment amounts for that area for any of those months.

The total amount of notional duty

(5) The amount of notional duty in respect of condensate produced from a particular prescribed condensate production area and entered for home consumption during a particular period is the sum of the amounts of notional duty in respect of:

(a) the quantity (if any) of the condensate that exceeds A 10B but does not exceed A 12B;

(b) the quantity (if any) of the condensate that exceeds A 12B but does not exceed A 14B;

(c) the quantity (if any) of the condensate that exceeds A 14B but does not exceed A 16B; and

(d) the quantity (if any) of the condensate that exceeds A 16B;

where:

A is the number of days in the period.

B is:

(a) where the period in a year in which there are 365 days—136.98630 kilolitres; or

(b) where the period is in a year in which there are 366 days—136.61202 kilolitres.

The amount of notional duty for a quantity of condensate—one petroleum price

(6) Subject to subsections (9) and (12), the amount of notional duty in respect of a quantity of condensate referred to in subsection (5) is an amount equal to the relevant percentage (set out in subsection (10)) of the product of:

(a) the amount specified in the price that is, at the end of the period referred to in subsection (5) in relation to the quantity of condensate, the applicable petroleum price for the month in which the period comes to an end; and

(b) the number of kilolitres in that quantity;

calculated to the nearest cent.

The debited adjustment amount

(7) If:

(a) during a month of a financial year, a VOLWARE price for condensate for a month of the immediately preceding financial year and a particular prescribed condensate production area is determined under section 7 of the Petroleum Excise (Prices) Act 1987; and

(b) the adjusted previous year’s duty for that prescribed condensate production area for that first‑mentioned month is greater than the non‑adjusted previous year’s duty for that area for that first‑mentioned month;

there is a debited adjustment amount for that area for that first‑mentioned month, being an amount equal to the difference between that adjusted previous year’s duty and that non‑adjusted previous year’s duty.

The credited adjustment amount

(8) If:

(a) during a month of a financial year, a VOLWARE price for condensate for a month of the immediately preceding financial year and a particular prescribed condensate production area is determined under section 7 of the Petroleum Excise (Prices) Act 1987; and

(b) the adjusted previous year’s duty for that prescribed condensate production area for that first‑mentioned month is less than the non‑adjusted previous year’s duty for that area for that first‑mentioned month;

there is a credited adjustment amount for that area for that first‑mentioned month, being an amount equal to the difference between that non‑adjusted previous year’s duty and that adjusted previous year’s duty.

The amount of notional duty for a quantity of condensate—more than one petroleum price

(9) If, at the end of a period in a financial year, the applicable petroleum prices for the months in which the period occurs and a particular prescribed condensate production area are not all the same, the amount of the notional duty in respect of a quantity of condensate referred to in subsection (5) produced from that production area and entered for home consumption during the period is an amount equal to the relevant percentage (set out in subsection (10)) of the sum of the amounts calculated in respect of each such applicable petroleum price in operation during the period in accordance with the formula:

where:

K is the number of kilolitres of condensate produced from that production area and entered for home consumption during that part of the period during which the applicable petroleum price was in operation.

KT is the number of kilolitres of condensate produced from that production area and entered for home consumption during the period.

P is the amount specified in the applicable petroleum price.

Q is the number of kilolitres in the quantity of condensate referred to in subsection (5).

Relevant percentage for a quantity of condensate

(10) For the purposes of subsections (6) and (9), the relevant percentage in relation to a quantity of condensate referred to in subsection (5) is:

(a) in the case of a quantity to which paragraph (5)(a) applies—10%; and

(b) in the case of a quantity to which paragraph (5)(b) applies—15%; and

(c) in the case of a quantity to which paragraph (5)(c) applies—20%; and

(d) in the case of a quantity to which paragraph (5)(d) applies—30%.

Rounding the number of kilolitres in a quantity of condensate

(11) For the purposes of subsections (6) and (9), the number of kilolitres in a quantity of condensate is taken to be a number equal to:

(a) unless paragraph (b) applies—the number of kilolitres in that quantity calculated to one decimal place; or

(b) if the number of kilolitres in that quantity calculated to 2 decimal places ends in a number greater than 4—the number of kilolitres in that quantity calculated to one decimal place increased by 0.1.

The amount of notional duty—dealing with the first year of production

(12) When no condensate produced from a particular prescribed condensate production area was ever entered for home consumption before the end of the first month of a particular financial year, then, in ascertaining, in accordance with subsections (5), (6) and (10) or (5), (9) and (10), the notional duty in respect of condensate produced from the production area and entered for home consumption during a later month (the relevant month) of that financial year, those subsections have effect in relation to the condensate as if each reference in a paragraph of subsection (5) to B were a reference to the product of B and the factor ascertained in accordance with the formula:

where:

M is the number of days in the period commencing on the day on which condensate produced from the prescribed condensate production area was first entered for home consumption and ending on the end of the relevant month.

N is the number of days in the period commencing on the first day of the financial year and ending on the end of the relevant month.

(13) Subsection 12(2) (retrospective application of legislative instruments) of the Legislation Act 2003 does not apply to a by‑law prescribing a condensate production area.

(13A) Despite section 169 of the Excise Act 1901, a by‑law prescribing a condensate production area may have the effect of imposing duty, in relation to condensate entered for home consumption before the date on which the by‑law is published in the Gazette, at a rate higher than the rate of duty payable in respect of the condensate on the day on which the condensate was entered for home consumption.

Interpretation of the Schedule

(14) The words set out after “, if higher,” in the column headed “Rate of Duty” in subitem 21.3 of the Schedule are taken, for the purposes of this Act or any other law of the Commonwealth, to be a rate of duty.

6D Duties of excise on intermediate oil

Definitions

(1) In this section:

adjusted previous year’s duty, in relation to a prescribed intermediate production area in relation to a month of a financial year, means the amount of duty that, at the end of the financial year immediately preceding the financial year in which that month occurs, would have been payable in respect of intermediate oil produced from that area and entered for home consumption during that preceding year if, for the prices that were, at the end of that preceding year, the applicable petroleum prices for all of the months of that preceding year, there had been substituted the prices that are, at the end of that first‑mentioned month, the respective applicable petroleum prices for all of those months.

non‑adjusted previous year’s duty, in relation to a prescribed intermediate production area in relation to a month of a financial year, means the amount of duty that, at the end of the financial year immediately preceding the financial year in which that month occurs, would have been payable in respect of intermediate oil produced from that area and entered for home consumption during that preceding year if, for the prices that were, at the end of that preceding year, the applicable petroleum prices for all of the months of that preceding year, there had been substituted the prices that were, immediately before the commencement of that first‑mentioned month, the respective applicable petroleum prices for all of those months.

prescribed intermediate production area means an intermediate petroleum production area prescribed by by‑laws (which, without limiting the generality of the foregoing, may be a relevant accumulation, a well, an oilfield or a gas field).

Introduction

(2) The amount of duty in respect of intermediate oil ascertained in accordance with this section shall be ascertained by reference to the prescribed intermediate production area from which the oil is produced and to the month of a financial year during which the oil is entered for home consumption.

The amount of duty

(3) Subject to subsection (3A), the amount of duty in respect of intermediate oil produced from a prescribed intermediate production area and entered for home consumption during a month of a financial year commencing on or after 1 July 1997 is the amount worked out using the formula:

where:

notional duty is the amount of notional duty in respect of intermediate oil produced from that area and entered for home consumption during the period starting at the start of that financial year and ending at the end of that month, worked out in accordance with subsection (4).

debited adjustment amount is the debited adjustment amount (if any) for that area and that month, worked out in accordance with subsection (5A).

duty paid is the amount of duty (if any) paid in respect of intermediate oil produced from that area and entered for home consumption during the period starting at the start of that financial year and ending at the end of that month.

credited adjustment amount is the credited adjustment amount (if any) for that area and that month, worked out in accordance with subsection (5B).

Disregarding certain amounts when working out amount of duty

(3A) In working out, for the purposes of subsection (3), the amount of duty paid in respect of intermediate oil produced from a prescribed intermediate production area and entered for home consumption during a period starting at the start of a financial year and ending at the end of a month of that year, the following amounts are to be disregarded:

(a) any increases in the amount of duty paid as a result of the addition of debited adjustment amounts for that area for any of the preceding months of that year;

(b) any decreases in that amount as a result of the subtraction of credited adjustment amounts for that area for any of those months.

The total amount of notional duty

(4) The amount of notional duty in respect of intermediate oil produced from a particular prescribed intermediate production area and entered for home consumption during a particular period is the sum of the amounts of notional duty in respect of:

(a) the quantity (if any) of the oil that exceeds A  6B but does not exceed A

6B but does not exceed A  8B;

8B;

(b) the quantity (if any) of the oil that exceeds A  8B but does not exceed A

8B but does not exceed A  10B;

10B;

(c) the quantity (if any) of the oil that exceeds A  10B but does not exceed A

10B but does not exceed A  12B; and

12B; and

(d) the quantity (if any) of the oil that exceeds A  12B;

12B;

where:

A is the number of days in the period.

B is:

(a) where the period is in a year in which there are 365 days—136.98630 kilolitres; or

(b) where the period is in a year in which there are 366 days—136.61202 kilolitres.

The amount of notional duty for a quantity of oil—one petroleum price

(5) Subject to subsections (6) and (9), the amount of notional duty in respect of a quantity of oil referred to in subsection (4) is an amount equal to the relevant percentage (set out in subsection (7)) of the product of:

(a) the amount specified in the price that is, at the end of the period referred to in subsection (4) in relation to the quantity of oil, the applicable petroleum price for the month in which the period comes to an end; and

(b) the number of kilolitres in that quantity;

calculated to the nearest cent.

The debited adjustment amount

(5A) Where:

(a) during a month of a financial year, a VOLWARE price for stabilized crude petroleum oil for a month of the immediately preceding financial year and a particular prescribed intermediate production area is determined under section 7 of the Petroleum Excise (Prices) Act 1987; and

(b) the adjusted previous year’s duty for that prescribed intermediate production area for that first‑mentioned month is greater than the non‑adjusted previous year’s duty for that area for that first‑mentioned month;

there is a debited adjustment amount for that area for that first‑mentioned month, being an amount equal to the difference between that adjusted previous year’s duty and that non‑adjusted previous year’s duty.

The credited adjustment amount

(5B) Where:

(a) during a month of a financial year, a VOLWARE price for stabilized crude petroleum oil for a month of the immediately preceding financial year and a particular prescribed intermediate production area is determined under section 7 of the Petroleum Excise (Prices) Act 1987; and

(b) the adjusted previous year’s duty for that prescribed intermediate production area for that first‑mentioned month is less than the non‑adjusted previous year’s duty for that area for that first‑mentioned month;

there is a credited adjustment amount for that area for that first‑mentioned month, being an amount equal to the difference between that non‑adjusted previous year’s duty and that adjusted previous year’s duty.

The amount of notional duty for a quantity of oil—more than one petroleum price

(6) Where, at the end of a period in a financial year, the applicable petroleum prices for the months in which the period occurs and a prescribed intermediate production area are not all the same, the amount of the notional duty in respect of a quantity of oil referred to in subsection (4) produced from that production area and entered for home consumption during the period is an amount equal to the relevant percentage (set out in subsection (7)) of the sum of the amounts calculated in respect of each such applicable petroleum price in operation during the period in accordance with the formula:

where:

P is the amount specified in the applicable petroleum price.

Q is the number of kilolitres in the quantity of oil referred to in subsection (4).

K is the number of kilolitres of intermediate oil produced from that production area and entered for home consumption during that part of the period during which the applicable petroleum price was in operation.

KT is the number of kilolitres of intermediate oil produced from that production area and entered for home consumption during the period.

Relevant percentage for a quantity of oil

(7) For the purposes of subsections (5) and (6), the relevant percentage in relation to a quantity of oil referred to in subsection (4) is:

(a) in the case of a quantity to which paragraph (4)(a) applies—15%;

(b) in the case of a quantity to which paragraph (4)(b) applies—30%;

(c) in the case of a quantity to which paragraph (4)(c) applies—50%; and

(d) in the case of a quantity to which paragraph (4)(d) applies—55%.

Rounding the number of kilolitres in a quantity of oil

(8) For the purposes of subsections (5) and (6), the number of kilolitres in a quantity of oil shall be taken to be a number equal to:

(a) unless paragraph (b) applies—the number of kilolitres in that quantity calculated to 1 decimal place; or

(b) where the number of kilolitres in that quantity calculated to 2 decimal places ends in a number greater than 4—the number of kilolitres in that quantity calculated to 1 decimal place increased by 0.1.

The amount of notional duty—dealing with the first year of production

(9) Where no intermediate oil produced from a particular prescribed intermediate production area was ever entered for home consumption before the expiration of the first month of a particular financial year, then, in ascertaining, in accordance with subsections (4), (5) and (7) or (4), (6) and (7), the notional duty in respect of intermediate oil produced from that production area and entered for home consumption during a later month (in this subsection referred to as the relevant month) of that financial year, those subsections have effect in relation to the intermediate oil as if each reference in a paragraph of subsection (4) to B were a reference to the product of B and the factor ascertained in accordance with the formula:

where:

R is the number of days in the period commencing on the day on which intermediate oil produced from the prescribed intermediate production area was first entered for home consumption and ending on the expiration of the relevant month; and