Superannuation Supervisory Levy Imposition Act 1998

No. 60, 1998

An Act to impose a levy on trustees of certain superannuation entities

Superannuation Supervisory Levy Imposition Act 1998

No. 60, 1998

An Act to impose a levy on trustees of certain superannuation entities

Contents

1 Short title..................................1

2 Commencement..............................1

3 Act binds the Crown............................2

4 External Territories............................2

5 Definitions.................................2

6 Imposition of superannuation industry supervisory levy.......3

7 Amount of levy...............................3

8 Calculation of indexation factor.....................4

9 Regulations.................................5

Superannuation Supervisory Levy Imposition Act 1998

No. 60, 1998

An Act to impose a levy on trustees of certain superannuation entities

[Assented to 29 June 1998]

The Parliament of Australia enacts:

This Act may be cited as the Superannuation Supervisory Levy Imposition Act 1998.

(1) This Act commences on the commencement of the Australian Prudential Regulation Authority Act 1998.

(2) If this Act commences during a financial year (but not on 1 July of that financial year), this Act has effect in relation to that financial year subject to the modifications specified in the regulations.

This Act binds the Crown in each of its capacities.

This Act extends to each external Territory.

In this Act, unless the contrary intention appears:

indexation factor means the indexation factor calculated under section 8.

index number, in relation to a quarter, means the All Groups Consumer Price Index number, being the weighted average of the 8 capital cities, published by the Australian Statistician in respect of that quarter.

levy imposition day, in relation to a trustee of a superannuation entity for a financial year, means:

(a) if the superannuation entity is a superannuation entity on 1 July of the financial year—that day; or

(b) in any other case—the day, during the financial year, on which the superannuation entity becomes a superannuation entity.

statutory upper limit means:

(a) in relation to the first financial year that ends after this Act commences—$500,000; or

(b) in relation to a later financial year—the amount calculated by multiplying the statutory upper limit for the previous financial year by the indexation factor for the later financial year.

superannuation entity means an entity that:

(a) is a superannuation entity within the meaning of the Superannuation Industry (Supervision) Act 1993; and

(b) is not an excluded superannuation fund within the meaning of that Act.

trustee, in relation to a superannuation entity, means the person who is the trustee of the entity for the purposes of the Superannuation Industry (Supervision) Act 1993.

Levy payable in accordance with subsection 8(6) of the Financial Institutions Supervisory Levies Collection Act 1998 is imposed.

(1) Subject to subsection (2), the amount of levy payable by a trustee of a superannuation entity for a financial year is:

(a) unless paragraph (b) or (c) applies—the amount that, for the financial year, is the levy percentage of the superannuation entity’s asset value on 30 June of the previous financial year; or

(b) if the amount worked out under paragraph (a) exceeds the maximum levy amount for the financial year—the maximum levy amount; or

(c) if the amount worked out under paragraph (a) is less than the minimum levy amount for the financial year—the minimum levy amount.

Note: The levy percentage, maximum levy amount, minimum levy amount and the method of working out the superannuation entity’s asset value, are as determined under subsection (3).

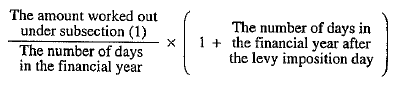

(2) If the levy imposition day for the trustee of a superannuation entity for the financial year is later than 1 July in the financial year, the amount of levy payable by the trustee for the financial year is the amount worked out using the following formula:

(3) The Treasurer is, in writing, to determine:

(a) the maximum levy amount for each financial year; and

(b) the minimum levy amount for each financial year; and

(c) the levy percentage for each financial year; and

(d) how a superannuation entity’s asset value is to be worked out.

(4) An amount determined under subsection (3) as the maximum levy amount must not exceed the statutory upper limit as at the time when the determination is made.

(5) A determination under subsection (3) is a disallowable instrument for the purposes of section 46A of the Acts Interpretation Act 1901.

(1) The indexation factor for a financial year is the number worked out by dividing the index number for the March quarter immediately preceding that financial year by the index number for the March quarter immediately preceding that first‑mentioned March quarter.

(2) The indexation factor is to be calculated to 3 decimal places, but increased by .001 if the 4th decimal place is more than 4.

(3) Calculations under subsection (1):

(a) are to be made using only the index numbers published in terms of the most recently published reference base for the Consumer Price Index; and

(b) are to be made disregarding index numbers that are published in substitution for previously published index numbers (where the substituted numbers are published to take account of changes in the reference base).

The Governor‑General may make regulations for the purposes of subsection 2(2).

[Minister's second reading speech made in—

House of Representatives on 26 March 1998

Senate on 13 May 1998]

(30/98)