A New Tax System (Wine Equalisation Tax) Act 1999

No. 62, 1999

A New Tax System (Wine Equalisation Tax) Act 1999

No. 62, 1999

A New Tax System (Wine Equalisation Tax) Act 1999

No. 62, 1999

An Act about a tax, relating to certain alcoholic beverages, to implement A New Tax System, and for related purposes

Part 1—Introduction

Division 1—Preliminary

1‑1.................................Short title

1‑2.............................Commencement

1‑3How the wine tax law applies to things outside Australia and things happening before commencement

1‑4........States and Territories are bound by the wine tax law

Division 2—Overview of the wine tax legislation

2‑1..........................What this Act is about

2‑5.........................Liability to tax (Part 2)

2‑10............................Quoting (Part 3)

2‑15........................Wine tax credits (Part 4)

2‑20.....................Payment of wine tax (Part 5)

2‑25.........................Miscellaneous (Part 6)

2‑30...................Interpretative provisions (Part 7)

2‑35Administration, collection and recovery provisions (Part VI of the Taxation Administration Act 1953)

Division 3—Defined terms

3‑1...................When defined terms are identified

3‑5.....................When terms are not identified

3‑10.............Identifying the defined term in a definition

Division 4—Status of Guides and other non‑operative material

4‑1....................Non‑operative material

4‑5...........................Explanatory sections

4‑10..............................Other material

Part 2—Wine tax

Division 5—General rules for taxability

5‑1.......................What this Division is about

5‑5.............General rules for taxing assessable dealings

5‑10Sale time brought forward if purchaser uses the wine before title passes

5‑15Royalty‑inclusive sale (AD2c and AD12c) or AOU (AD3d and AD13d)

5‑20............Indirect marketing sale (AD2d and AD12d)

5‑25.Untaxed sale (AD2e and AD12e) or AOU (AD3a and AD13a)

5‑30................Local entry of imported wine (AD10)

5‑35Time of local entry if wine entered for home consumption before importation

5‑40Reductions in wine tax for some importations that are free of customs duty

Division 7—Exemptions

7‑1.......................What this Division is about

7‑5...Exemption for dealings that are GST‑free supplies

7‑10.....................Exemptions based on quoting

7‑15Exemptions based on Schedule 4 to the Customs Tariff Act 1995

7‑20.Exemption for local entry if wine has been taxed while in bond

Division 9—Taxable value

9‑1.......................What this Division is about

Subdivision 9‑A—General rules for working out taxable value

9‑5......How to work out the taxable value of a taxable dealing

9‑10Agreement with Commissioner regarding calculation of taxable value

Subdivision 9‑B—Notional wholesale selling price

9‑25The 2 methods of working out notional wholesale selling prices for retail dealings with grape wine

9‑30Working out notional wholesale selling prices for retail dealings with wine that is not grape wine

9‑35......................The half retail price method

9‑40................The average wholesale price method

9‑45.......Notional wholesale selling prices for other dealings

Subdivision 9‑C—Additions to taxable value

9‑65..Taxable dealing with wine that is the contents of a container

9‑70Assessable dealings with wine that involve the payment of an associated royalty

9‑75................Assessable dealing with wine in bond

9‑80Amounts not to be added if they are already included in the taxable value

Part 3—Quoting

Division 13—Quoting for dealings in wine

13‑1......................What this Division is about

13‑5.................Standard grounds for quoting ABN

13‑10......Additional quoting grounds in special circumstances

13‑15............................Periodic quoting

13‑20...............Manner in which quote must be made

13‑25...Incorrect quote nevertheless effective for certain purposes

13‑30Quote not effective for certain purposes if there are grounds for believing it was improperly made

13‑35...................Improper quoting is an offence

Part 4—Wine tax credits

Division 17—Wine tax credits

17‑1......................What this Division is about

17‑5.....................Wine tax credit entitlements

17‑10.....................Claims for wine tax credits

17‑15Commissioner not required to consider credit claims for less than $200

17‑20Wine tax credits to be applied against tax liabilities and excess refunded

17‑25..............Excess wine tax credits must be repaid

17‑30Clawback of CR15 wine tax credit on later recovery of bad debt

17‑35Clawback of CR8 wine tax credit on later sale of defective wine

17‑40...Agreement with Commissioner regarding wine tax credits

17‑45.........Notifying disallowance of wine tax credit claim

Part 5—Payments and refunds of wine tax

Division 21—Inclusion of wine tax and wine tax credits in net amounts

21‑1......................What this Division is about

21‑5....................Wine tax added to net amounts

21‑10....................Attribution rules for wine tax

21‑15..........Wine tax credits subtracted from net amounts

Division 23—Wine tax on customs dealings

23‑1......................What this Division is about

23‑5.............Payment of wine tax on customs dealings

23‑10...........Application of Division 165 of the GST Act

Part 6—Miscellaneous

Division 27—Miscellaneous

27‑1......Application of this Act to cider, perry, mead and sake

27‑5....Wine tax must be specified on invoice for wholesale sales

27‑10Alteration of wine tax liability or wine tax credit if affected by non‑arm’s length transaction

27‑15.................Apportionment of global amounts

27‑20..........Commonwealth etc. not liable to pay wine tax

27‑25............Cancellation of exemptions from wine tax

27‑30.................Application of the Criminal Code

27‑35..............................Regulations

Part 7—Interpreting this Act

Division 29—Rules for interpreting this Act

29‑1......................What forms part of this Act

29‑5.................What does not form part of this Act

29‑10..Explanatory sections, and their role in interpreting this Act

Division 31—Meaning of some important concepts

Subdivision 31‑A—Wine

31‑1............................Meaning of wine

Subdivision 31‑B—Grape wine

31‑5........................Meaning of grape wine

Subdivision 31‑C—Borne wine tax and wine tax borne

31‑10.........Meanings of borne wine tax and wine tax borne

Subdivision 31‑D—Obtaining wine under quote etc.

31‑15.............Meaning of obtain wine under quote etc.

Subdivision 31‑E—Approved forms

31‑20.....................Meaning of approved form

Division 33—Dictionary

33‑1................................Dictionary

A New Tax System (Wine Equalisation Tax) Act 1999

No. 62, 1999

An Act about a tax, relating to certain alcoholic beverages, to implement A New Tax System, and for related purposes

This Act may be cited as the A New Tax System (Wine Equalisation Tax) Act 1999.

This Act commences on 1 July 2000.

(1) The *wine tax law extends to acts, omissions, matters and things outside *Australia (except where a contrary intention appears).

(2) The *wine tax law applies to acts and omissions happening before or after the commencement of this Act (except where there is an express statement to the contrary).

The *wine tax law binds the Crown in right of each of the States, of the Australian Capital Territory and of the Northern Territory. However, it does not make the Crown liable to be prosecuted for an offence.

This Act is about the wine equalisation tax (or wine tax).

The wine tax is a single stage tax applying (in most cases) to dealings in wine at the wholesale level. In almost all dealings to which it applies, the GST will also apply.

Note 1: Wine is widely defined in Subdivision 31‑A. It can apply to beverages fermented from any fruit or vegetable. The wine tax also extends to cider, perry, mead and sake (see section 27‑1).

Note 2: The wine tax is imposed by 3 Acts:

(a) the A New Tax System (Wine Equalisation Tax Imposition—General) Act 1999; and

(b) the A New Tax System (Wine Equalisation Tax Imposition—Customs) Act 1999; and

(c) the A New Tax System (Wine Equalisation Tax Imposition—Excise) Act 1999.

Part 2 sets out the rules that establish the liability for the wine tax. The broad aim of the wine tax law is to tax the last wholesale sale of wine (usually the sale from the last wholesaler to the retailer).

Part 3 is about quoting. The system of quoting is designed to avoid wine tax becoming payable on earlier sales.

Part 4 is about the entitlement to, and claiming of, wine tax credits. The system of wine tax credits deals (among other things) with situations where wine tax has become payable more than once on the same wine.

Part 5 provides for amounts of wine tax, and wine tax credits, to be included in net amounts under the GST system. This has the effect of incorporating the wine tax into the payments and refunds system for the GST. However, the wine tax is paid together with customs duty (where appropriate).

Part 6 deals with miscellaneous matters.

Part 7 contains the Dictionary, which sets out a list of all the terms that are defined in this Act. It also sets out the meanings of some important concepts and rules on how to interpret this Act.

Part VI of the Taxation Administration Act 1953 contains provisions relating to the administration of the wine tax, and to collection and recovery of amounts of wine tax.

(1) Many of the terms used in the law relating to the wine tax are defined.

(2) Most defined terms in this Act are identified by an asterisk appearing at the start of the term: as in “*taxable dealing”. The footnote that goes with the asterisk contains a signpost to the Dictionary definitions starting at section 33‑1.

(1) Once a defined term has been identified by an asterisk, later occurrences of the term in the same subsection are not usually asterisked.

(2) Terms are not asterisked in the non‑operative material contained in this Act.

Note: The non‑operative material is described in Division 4.

(3) The following basic terms used throughout the Act are not identified with an asterisk.

Common definitions that are not asterisked | |

Item | This term: |

1 | amount |

2 | Commissioner |

3 | entity |

4 | price |

5 | wine |

6 | wine tax |

7 | you |

Within a definition, the defined term is identified by bold italics.

In addition to the operative provisions themselves, this Act contains other material to help you identify accurately and quickly the provisions that are relevant to you and to help you understand them.

This other material falls into 2 main categories.

One category is the explanatory section in many Divisions. Under the section heading “What this Division is about”, a short explanation of the Division appears in boxed text.

Explanatory sections form part of this Act but are not operative provisions. In interpreting an operative provision, explanatory sections may only be considered for limited purposes. They are set out in section 29‑10.

The other category consists of material such as notes and examples. These also form part of the Act. They are distinguished by type size from the operative provisions (except for formulas), but are not kept separate from them.

Liability for wine tax centres around the concept of an assessable dealing. This concept is defined in the Assessable Dealings Table and the sections following the table.

(1) The *Assessable Dealings Table sets out all the *assessable dealings that can be subject to wine tax.

(2) If the time of an *assessable dealing (as specified in column 4 of the table) is on or after 1 July 2000, and no exemption applies under Division 7, then:

(a) the dealing is a *taxable dealing; and

(b) the entity specified in column 3 is the entity liable to the tax; and

(c) the tax becomes payable at the time of the dealing, as specified in column 4.

However, the dealing is not a taxable dealing unless the entity specified in column 3 is *registered or *required to be registered.

Note: Under Part 5, amounts of wine tax are included in your net amount under the GST system.

(3) To calculate the amount of the tax:

(a) determine the *taxable value of the dealing under Division 9; and

(b) multiply the result by 29%.

Note: The amount of tax is reduced for some importations (e.g. accompanied baggage of passengers) that are free of customs duty (see section 5‑40).

(4) The table does not apply to a dealing with wine unless the wine is *assessable wine immediately before the time of the dealing, and is in *Australia at the time of the dealing.

Assessable Dealings Table | ||||

Column 1 No. | Column 2 *Assessable dealing | Column 3 *Entity liable | Column 4 Time of dealing | Column 5 Normal taxable value |

Part A—Australian Wine | ||||

AD1a | *wholesale sale by an entity that *manufactured the wine in the course of any business | seller | time of sale | the *price (excluding wine tax and *GST) for which the wine was sold |

AD1b | *wholesale sale by an entity that is not the *manufacturer of the wine | seller | time of sale | the *price (excluding wine tax and *GST) for which the wine was sold |

AD2a | *retail sale by an entity that *manufactured the wine in the course of any business | seller | time of sale | the *notional wholesale selling price |

AD2b | *retail sale by an entity that is not the *manufacturer of the wine, but that *obtained the wine under quote; excludes case covered by AD2d | seller | time of sale | the *notional wholesale selling price |

AD2c | *royalty‑inclusive sale | seller | time of sale | the amount that would be the *notional wholesale purchase price of the wine if the *manufacturer had incurred the *eligible royalty costs |

AD2d | *indirect marketing sale | seller | time of sale | the *notional wholesale selling price |

AD2e | *untaxed sale by an entity that is not the *manufacturer of the wine | seller | time of sale | the *notional wholesale selling price |

AD3a | *untaxed AOU by an entity that is not the *manufacturer of the wine | applier | time of *AOU | the *notional wholesale selling price |

AD3b | *AOU by an entity that manufactured the wine in the course of any business | applier | time of *AOU | the *notional wholesale selling price |

AD3c | *AOU by an entity that is not the *manufacturer of the wine, but that *obtained the wine under quote | applier | time of *AOU | (a) the purchase *price (excluding *GST), if the wine was *purchased under quote; (b) in other cases, the *notional wholesale selling price |

AD3d | *royalty‑inclusive AOU | applier | time of *AOU | the amount that would be the *notional wholesale purchase price of the wine if the *manufacturer had incurred the *eligible royalty costs |

AD4b | removal from a *customs clearance area of *airport shop goods purchased by a *relevant traveller from an *inwards duty free shop | *relevant traveller | time of removal | the *price for which the wine was purchased by the *relevant traveller |

Assessable Dealings Table | ||||

Column 1 No. | Column 2 *Assessable dealing | Column 3 *Entity liable | Column 4 Time of dealing | Column 5 Normal taxable value |

Part B—Imported Wine | ||||

AD10 | *local entry | entity that makes the *local entry | time of *local entry | the *GST importation value |

AD11b | *wholesale sale by any entity | seller | time of sale | the *price (excluding wine tax and *GST) for which the wine was sold |

AD12b | *retail sale by an entity that *obtained the wine under quote; excludes case covered by AD12d | seller | time of sale | the *notional wholesale selling price |

AD12c | *royalty‑inclusive sale | seller | time of sale | the amount that would be the *notional wholesale purchase price of the wine if the entity that *imported the wine had incurred the *eligible royalty costs |

AD12d | *indirect marketing sale | seller | time of sale | the *notional wholesale selling price |

AD12e | *untaxed sale | seller | time of sale | the *notional wholesale selling price |

AD13a | *untaxed AOU | applier | time of *AOU | the*notional wholesale selling price |

AD13c | *AOU by an entity that *obtained the wine under quote | applier | time of *AOU | (a) if the wine was *purchased under quote: the purchase *price (excluding *GST); (b) if the wine was *locally entered under quote by the applier: the *GST importation value |

AD13d | *royalty‑inclusive AOU | applier | time of *AOU | the amount that would be the *notional wholesale purchase price of the wine if the entity that *imported the wine had incurred the *eligible royalty costs |

AD14b | removal from a *customs clearance area of *airport shop goods purchased by a *relevant traveller from an *inwards duty free shop | *relevant traveller | time of renewal | the *price for which the wine was purchased by the *relevant traveller |

Note: The numbering of items in the table uses the following pattern:

For Australian wine, the dealings are divided into 4 groups:

Imported wine has an additional class of local entry (AD10). The other dealings with imported wine have a number that is 10 higher than the broadly corresponding dealing with Australian wine. For example, AD12b for imported wine corresponds to AD2b for Australian wine.

(1) This section applies to an *assessable dealing that consists of a sale, if the purchaser uses the wine after the time when the contract is made but before the time when title is to pass to the purchaser under the contract.

(2) The time when the purchaser first so uses the wine is taken to be the time of the sale for the purposes of the *wine tax law.

(1) A *retail sale, or an *AOU, of wine (the current wine) by you in the course of a business is a royalty‑inclusive sale or a royalty‑inclusive AOU respectively if the following conditions are met:

(a) *eligible royalty costs have been incurred at or before the time of the sale or AOU, or could reasonably be expected to be incurred after the time of the sale or AOU, by any or all of the following:

(i) you;

(ii) your associate;

(iii) any entity (other than the *manufacturer) under an arrangement with you or with your associate;

(b) the sale or AOU is not covered by another category of *assessable dealing in the *Assessable Dealings Table.

(2) Eligible royalty cost is a *royalty that is paid or payable in connection with the current wine, except where the amount was paid or payable by any entity before 24 March 1999.

A sale of *assessable wine is an indirect marketing sale if it is a *retail sale made by an entity (the marketer) that is not the *manufacturer of the wine and the sale is made:

(a) under an arrangement that provides for the sale of the wine to be made by an entity that is acting for the marketer but is not an employee of the marketer; or

(b) from premises that:

(i) are used, mainly for making retail sales of wine, by an entity or entities other than the marketer; and

(ii) are held out to be premises of, or premises used by, the other entity or entities.

(1) A *retail sale of wine by you is an untaxed sale unless:

(a) you *obtained the wine under quote; or

(b) the wine has previously passed through a taxing point; or

(c) the sale is an *indirect marketing sale.

(2) An *AOU, in the course of any business, by you is an untaxed AOU unless:

(a) you *obtained the wine under quote; or

(b) the wine has previously passed through a taxing point.

(3) For the purposes of this section, wine is taken to have passed through a taxing point only if:

(a) the wine has been the subject of a *taxable dealing; or

(b) the wine has been the subject of an *assessable dealing that was exempted because you could not be taxed or were entitled to an exemption arising outside the *wine tax law; or

(c) the wine has been the subject of sales tax within the meaning of the Sales Tax Assessment Act 1992.

(1) The Local Entry Table sets out the situations that amount to a local entry of *imported wine for the purposes of the *wine tax law. The rest of this section deals with situations involving the withdrawal of a customs entry, or multiple local entries of the same wine.

(2) The withdrawal of the customs entry underlying a formal local entry (the earlier local entry) usually has the effect that the earlier local entry is taken never to have happened. However, if:

(a) there is a later formal local entry after the withdrawal; and

(b) the tax on that later entry would be less than the tax on the earlier local entry;

then the earlier local entry is taken never to have been extinguished and the later entry is taken never to have happened.

(3) If a formal local entry happens after a deemed local entry, the formal local entry is taken never to have happened.

(4) If a deemed local entry happens after a formal local entry, the formal local entry is taken never to have happened.

(5) In this section:

customs entry means an entry for home consumption under the Customs Act 1901.

deemed local entry means a local entry that is not a formal local entry.

formal local entry means a local entry covered by *LE1 or *LE2 in the Local Entry Table.

Local Entry Table | |||

Column 1 No. | Column 2 Situation giving rise to local entry | Column 3 *Entity to be regarded as making the local entry | Column 4 Time when local entry is made (but see note) |

LE1 | the wine is taken to have been entered for home consumption under subsection 71A(6) of the Customs Act 1901 | owner (within the meaning of the Customs Act 1901) of the wine | when the wine is taken to have been entered for home consumption |

LE2 | the wine is taken to have been entered for home consumption under subsection 71A(7) of the Customs Act 1901 | owner (within the meaning of the Customs Act 1901) of the wine | when the wine is taken to have been entered for home consumption |

LE3 | the wine is delivered into home consumption under section 71 of the Customs Act 1901 | entity authorised under section 71 of the Customs Act 1901 to deliver the wine | when the wine is delivered into home consumption |

LE4 | the wine is sold under section 72, 87, 96, 206 or 207 of the Customs Act 1901 | entity that was the owner (within the meaning of the Customs Act 1901) of the wine immediately before the sale | when the wine is sold |

LE5 | the wine is delivered to an entity under section 208 of the Customs Act 1901 | entity to which the wine is delivered | when the wine is delivered |

LE6 | the wine is delivered to an entity under a court order made in an action under the Customs Act 1901 for condemnation or recovery of the wine | entity to which the wine is delivered | when the wine is delivered |

LE7 | the wine is delivered to an entity under a court order made in an action for a declaration that the wine is not forfeited under the Customs Act 1901 | entity to which the wine is delivered | when the wine is delivered |

LE8 | the wine has been seized under a warrant issued under section 203 of the Customs Act 1901, or under section 203B or 203C of that Act, and is delivered to an entity on the basis that it is not forfeited goods | entity to which the wine is delivered | when the wine is delivered |

LE9 | delivery of the wine is authorised under subsection 209(6) of the Customs Act 1901 | entity to which the wine is delivered or is to be delivered | when the authorisation is made |

LE10 | a demand is made under section 35A or 149 of the Customs Act 1901 in relation to the wine | entity on which the demand is made | when the demand is made |

LE11 | the wine is treated as entered for home consumption under subsection 96A(12) of the Customs Act 1901 | entity treated under section 96A of the Customs Act 1901 as having entered the wine for home consumption | when the wine is treated as having been entered for home consumption |

LE12 | the wine is taken out of a warehouse under a permission granted under section 97 of the Customs Act 1901 and is not returned to the warehouse before the expiration of the period specified in the permission | entity to which the permission is given | when the wine is taken out of the warehouse |

LE13 | the wine is delivered, under regulations made for the purposes of paragraph 27‑35(2)(a), to an entity that has given a security or undertaking for the payment of wine tax that may become payable on the wine | entity to which the wine is delivered | when the wine is delivered |

LE14 | the wine is taken into home consumption in accordance with a permission granted under section 77D of the Customs Act 1901 | entity to which the permission is granted | when the wine is taken into home consumption |

LE15 | the wine is not covered by any other item in this table but is *imported into Australia, and is not entered for home consumption as required under the Customs Act 1901 | owner (within the meaning of the Customs Act 1901) of the wine | when the wine is *imported into Australia |

Despite column 4 of the *Local Entry Table, if wine is deemed to be entered for home consumption under the Customs Act 1901 at a time before the wine is *imported, the *local entry of the wine is taken to occur immediately after the time of importation.

If:

(a) a *taxable dealing with wine is a *customs dealing; and

(b) a proportion of the value of the wine is not liable to *customs duty because of by‑laws made for the purposes of item 15 in Part I of Schedule 4 to the *Customs Tariff;

the amount of wine tax on the dealing is an amount equal to the amount worked out under subsection 5‑5(3) and then reduced by the same proportion.

In some circumstances, a dealing with wine is exempt from wine tax even if it is an assessable dealing.

An *assessable dealing is not taxable if the dealing is a *supply that is *GST‑free (other than because of Subdivision 38‑D (child care) of the *GST Act).

(1) A sale is not taxable if the purchaser *quotes for the sale at or before the time of the sale.

(2) A *customs dealing is not taxable if the entity that would, apart from this subsection, be liable for the wine tax on the dealing *quotes for the dealing at or before the time of the dealing.

(1) A *customs dealing is not taxable if it is an *importation of wine covered by item 17, 18A, 18B, 18C, 21, 23A, 23B, 24, 25A, 25B, 25C, 32A, 32B, 33A, 33B or 34 in Schedule 4 to the *Customs Tariff.

(2) To avoid doubt, a reference to wine that is covered by an item in Schedule 4 to the *Customs Tariff includes a reference to wine to which that item would apply if the wine were dutiable goods within the meaning of the Customs Act 1901.

A *local entry of wine is not taxable if you or anyone else became liable to tax on a previous *assessable dealing with the wine while it was in bond or under the control of *Customs.

In most cases, the taxable value of an assessable dealing is multiplied by the rate of wine tax to calculate the amount of wine tax.

(1) The general rules for calculating the taxable value are set out in the *Assessable Dealings Table.

(2) In some cases, the *Assessable Dealings Table refers to the *notional wholesale selling price as the *taxable value. Subdivision 9‑B sets out how to work out the notional wholesale selling price.

(3) In some cases, amounts must be added to the amount set out in the *Assessable Dealings Table. These additions are set out in Subdivision 9‑C.

(4) In working out the *taxable value of wine, any rebate, refund or other payment or credit made by a State or Territory in respect of the wine is to be disregarded.

(1) The Commissioner may enter into an agreement with you about calculating the *taxable values of particular *taxable dealings for which you are liable for the wine tax.

(2) So far as the agreement is inconsistent with this Act, the agreement prevails.

(1) There are 2 methods for working out the notional wholesale selling price for a *taxable dealing that is either:

(a) a *retail sale of *grape wine; or

(b) an *AOU connected with retail sales of wine that is grape wine.

(2) The *half retail price method is used unless you have chosen under subsection (3) to use the *average wholesale price method.

(3) You may choose to use the *average wholesale price method if, during the *tax period in respect of which you are liable to pay wine tax on the dealing, at least 10% by value of all your sales of *grape wine that:

(a) is of the same vintage as the grape wine to which the dealing relates; and

(b) is produced from the same grape varieties, or the same blend of grape varieties, as the grape wine to which the dealing relates;

are *wholesale sales.

The notional wholesale selling price for a *taxable dealing that is either:

(a) a *retail sale of wine that is not *grape wine; or

(b) an *AOU connected with retail sales of wine that is not grape wine;

is worked out using the *half retail price method.

(1) The notional wholesale selling price for a *retail sale of *grape wine, worked out using the half retail price method, is 50% of the *price of the sale.

(2) The notional wholesale selling price for an *AOU connected with retail sales of grape wine, worked out using the half retail price method, is 50% of the *price for which you would normally have sold the wine if the sale were a *retail sale.

The notional wholesale selling price for a *retail sale of *grape wine, or for an *AOU connected with retail sales of grape wine, worked out using the average wholesale price method is the weighted average of the *prices (excluding wine tax and *GST) for *wholesale sales that you have made of grape wine that:

(a) is of the same vintage as the grape wine to which the retail sale or AOU relates; and

(b) is produced from the same grape varieties, or the same blend of grape varieties, as the grape wine to which the retail sale or AOU relates;

during the *tax period in respect of which you are liable to pay wine tax on the retail sale or AOU.

Example: If, during a tax period, you make 70% of wholesale sales of grape wine of a particular vintage and variety at $80 per dozen, and the remaining 30% at $90 per dozen, the weighted average of the wholesale prices for wholesale sales during the tax period is:

![]()

The notional wholesale selling price for a taxable dealing with wine that is neither:

(a) a *retail sale of wine; nor

(b) an *AOU connected with retail sales of wine;

is the *price (excluding wine tax and *GST) for which you could reasonably have been expected to sell the wine by wholesale under an arm’s length transaction.

(1) This section deals with situations in which a *container is associated with wine (the contents) that is the subject of a *taxable dealing. The aim of this section is to ensure that the *taxable value will include a component for the container, even though the parties may have allocated a separate amount to the container.

(2) If:

(a) the *taxable value of the dealing is calculated by reference to the *price (excluding wine tax and *GST) for which the contents were sold; and

(b) the parties have allocated a separate amount to the *container;

then the taxable value is *increased by so much of the value of the container as is recouped by the seller in connection with the sale of the contents.

(3) If the *taxable value of the dealing is not calculated as mentioned in subsection (2), then the taxable value is *increased by so much of the value of the *container as could reasonably be expected to have been recouped by you in connection with a hypothetical sale of the contents at the time of the actual *taxable dealing with the contents.

(1) If a *royalty is paid or payable, or likely to be paid or payable, in connection with any of the following events in respect of particular wine:

(a) the *manufacture of the wine;

(b) the *importation or *local entry of the wine;

(c) a sale of the wine;

then the *taxable value of any *taxable dealing with that wine that happens at or after that event includes the amount or value of the royalty.

(2) Royalty is any amount to the extent to which it is paid or payable (whether or not periodically) as consideration for any of the following things (or for the right to do them):

(a) doing anything that would be an infringement of copyright if it were done without the licence of the copyright owner;

(b) making, using, exercising or vending an invention (each of those terms having the meaning it has in the Patents Act 1990);

(c) using a design that is of a kind capable of being registered under the Designs Act 1906 (whether or not it is registered under that Act or under any other law);

(d) using a trade mark that is of a kind capable of being registered under the Trade Marks Act 1995 (whether or not it is registered under that Act or under any other law), but not including a mark that relates to a service;

(e) using confidential information;

(f) using machinery, implements, apparatus or other equipment;

(g) *supplying scientific, technical, industrial, commercial or other knowledge or information;

(h) supplying assistance that is ancillary to, and is supplied as a means of enabling the application or enjoyment of, any matter covered by paragraphs (a) to (g);

(i) a total or partial forbearance in respect of any matter covered by paragraphs (a) to (h).

Terms used in paragraph (a) of this definition have the same meaning as in the Copyright Act 1968.

If a *taxable dealing happens while the wine is in bond or otherwise subject to the control of *Customs, the *taxable value is *increased by the amount of *customs duty to which the wine would have been subject if it had been entered for home consumption under the Customs Act 1901 at the time of the taxable dealing.

This Subdivision does not add any amount to the *taxable value so far as it would already be included in the taxable value.

In certain circumstances you can quote for a dealing with wine. This is designed to avoid the wine tax becoming payable on sales preceding the last wholesale sale. (Under section 7‑10, wine tax is not payable on a sale for which the purchaser has quoted.)

(1) You are entitled to *quote your *ABN for a dealing with wine if, at the time of quoting, you have the intention of dealing with the wine in any of the following ways:

(a) selling the wine by *wholesale, or by *indirect marketing sale, while the wine is in *Australia;

(b) selling the wine, by any kind of sale, while it is in Australia (this ground is available only if you are mainly a wholesaler at the time of quoting);

(c) using the wine as a material in *manufacture or other treatment or processing, whether or not it relates to or results in other wine;

(d) making a *supply of the wine that will be *GST‑free.

(2) However, you are not entitled to *quote unless you are *registered.

(3) For the purposes of paragraph (1)(b), you are mainly a wholesaler at the quoting time only if:

(a) *wholesale sales and *indirect marketing sales account for more than half of the total value of all sales of *assessable wine by you during the 12 months ending at the quoting time; or

(b) you have an expectation (based on reasonable grounds) that wholesale sales and indirect marketing sales will account for more than half of the total value of all sales of assessable wine by you during the 12 months starting at the quoting time.

For this purpose, the value of a sale of wine is the *price for which the wine is sold.

The Commissioner may (if you are *registered) authorise you to *quote your *ABN in special circumstances in which you would not otherwise be entitled to quote.

(1) You may make a periodic *quote under this section for purchases that you propose to make from an entity (the supplier) during the period, not exceeding 12 months, covered by the periodic quote.

(2) If you make such a periodic *quote on or before the first day of the period to which the quote relates, you are treated as having quoted your *ABN for all purchases during the period from the *supplier, other than purchases in respect of which you have notified the supplier in accordance with subsection (3).

(3) If you are not entitled to *quote for a particular purchase from the *supplier during the period, you must notify the supplier of that fact at or before the time of the purchase. The notification must be in the *approved form.

(4) You are guilty of an offence if you contravene subsection (3).

Maximum penalty: 20 penalty units.

Note 1: Chapter 2 of the Criminal Code sets out the general principles of criminal responsibility.

Note 2: See section 4AA of the Crimes Act 1914 for the current value of a penalty unit.

(5) Section 13‑30 applies to a *quote that you are treated as having made under subsection (2) of this section for a particular purchase.

(1) A *quote (including a periodic quote) must be made in the *approved form.

(2) A *quote for a dealing is not effective unless it is made at or before the time of the dealing.

If you *quote in circumstances in which you are not entitled to quote, or the quote is not in the *approved form, the quote is nevertheless:

(a) effective for the purposes of Subdivision 31‑D; and

(b) effective for the purpose of section 7‑10, unless section 13‑30 applies.

A *quote is not effective, so far as it would have resulted in an exemption or a ground for a *CR6 wine tax credit, if at the time of the quote the entity to which the quote is made has reasonable grounds for believing that:

(a) you are not entitled to quote in the particular circumstances; or

(b) the quote is not made in the *approved form; or

(c) the quote is false or misleading in a material particular (either because of something stated in the quote or something left out).

You must not, in relation to any dealing with wine:

(a) quote an *ABN for the purposes of this Act:

(i) in circumstances in which you are not entitled to quote; or

(ii) in contravention of subsection 13‑20(1); or

(b) in any other way falsely quote an ABN.

Maximum penalty: 20 penalty units.

Note 1: Chapter 2 of the Criminal Code sets out the general principles of criminal responsibility.

Note 2: See section 4AA of the Crimes Act 1914 for the current value of a penalty unit.

Note 3: Section 23 of the A New Tax System (Australian Business Number) Act 1999 provides penalties for misuse of ABNs.

Wine tax credits can arise in a number of circumstances. Generally speaking, they prevent wine tax applying more than once to the same goods.

Note: If you are in the GST system, wine tax credits are included in your net amounts (see Part 5). If you are not in the GST system, you can claim wine tax credits under this Part.

(1) The *Wine Tax Credit Table sets out the situations in which you are entitled to a *wine tax credit.

(2) You are not entitled to a *wine tax credit for an amount of tax for which a wine tax credit entitlement has previously arisen (whether for you or another entity).

(3) You are not entitled to a *wine tax credit unless you make a claim for the wine tax credit under section 17‑10.

Wine Tax Credit Table | ||||

No. | Summary of ground | Details of ground | Amount of *wine tax credit | Time *wine tax credit arises |

CR1 | Tax overpaid | You have paid an amount as wine tax that was not legally payable. | the amount overpaid, to the extent that you have not *passed it on | when the amount became overpaid |

CR2 | You have *borne wine tax, even though entitled to *quote | You have *borne wine tax on a *tax‑bearing dealing for which you were entitled to *quote (whether or not you quoted). You have not sold the wine. If you have applied the wine to own use, the *AOU would not have been taxable, assuming it were an *assessable dealing. | the *wine tax borne, to the extent that you have not *passed it on | time of the *tax‑bearing dealing |

CR3 | You are liable to tax because *quote ineffective under section 13‑30 | You have become liable to wine tax on an *assessable dealing (or have lost an entitlement to a *CR6 wine tax credit) because section 13‑30 applied to an otherwise fully effective *quote that was made to you. | the wine tax payable on the *assessable dealing (or the amount to which the *CR6 wine tax credit would have related), to the extent that you have not *passed it on | time of the *assessable dealing (or time *CR6 wine tax credit would have arisen) |

CR4 | Avoiding double tax on the same wine | You have become liable to wine tax on an *assessable dealing (the current dealing), but have *borne wine tax on the wine before the time of the current dealing. | the wine tax previously *borne on the wine | time of the current dealing |

CR5 | Ensuring exemption where latest *assessable dealing is non‑taxable | *Assessable dealing (the current dealing) is not taxable (for any reason except section 7‑20). You: (a) would be liable to the wine tax on the current dealing if it were taxable; and (b) have *borne wine tax on the wine before the time of the current dealing. | the wine tax previously *borne on the wine | time of the current dealing |

CR6 | Tax excluded from sale *price of tax‑paid wine sold to *quoting purchaser | You have sold wine, to a purchaser who *quoted on the sale, for a *price that excluded some or all of the wine tax previously *borne by you on the wine. | the wine tax excluded from sale *price | time of sale |

CR7 | Ensuring no double tax in respect of *containers | You are liable to the wine tax on an *assessable dealing with wine that is the contents of a *container. You have *borne wine tax on the container. | the *wine tax borne on the *container | time of the *assessable dealing |

CR8 | Replacement of defective wine | You have *borne wine tax on *assessable wine used for the purpose of replacing other wine because of defects in the other wine. | *wine tax borne on replacement wine | time of replacement |

CR9 | Tax excluded from sale *price of tax‑paid wine sold to purchaser for *export | You have sold wine to a purchaser who, at the time of sale, had the intention of *exporting the wine (otherwise than as *accompanied baggage) while it was still *assessable wine. The *price excluded some or all of the wine tax previously *borne by you on the wine. | the wine tax excluded from sale *price | time of sale |

CR10 | Wine *exported by you while still *assessable wine | Wine on which you have *borne wine tax has been *exported by you while still *assessable wine. | the *wine tax borne | time of *export |

CR11 | Wine sold for tax‑exclusive *price to *eligible Australian traveller who subsequently *exported it | You sold wine to an *eligible Australian traveller in accordance with the *prescribed rules for export sales for a *price that excluded some or all of the wine tax previously *borne by you on the wine. The wine has been *exported by the purchaser within the time, and in the manner, prescribed by the regulations. | wine tax excluded from sale *price | time of *export |

CR12 | Wine sold for tax‑exclusive *price to *eligible foreign traveller | You sold wine to an *eligible foreign traveller, in accordance with the *prescribed rules for export sales, for a *price that excluded some or all of the wine tax previously *borne by you on the wine. | wine tax excluded from sale *price | time of sale |

CR13 | Refund of *customs duty following destruction of *imported wine | You have become liable to wine tax on a *local entry of wine that was *imported under a contract of sale. You rejected the wine for non‑compliance with the contract and the wine was destroyed under *Customs supervision. The Commissioner is satisfied that the destruction is or would be ground for remission of *customs duty on the wine. | wine tax payable on the *local entry | time of destruction of the wine |

CR14 | Drawback of *customs duty on *imported wine | You have become liable to wine tax on a *local entry of wine for which drawback of *customs duty has been allowed under section 168 of the Customs Act 1901 (or, in the Commissioner’s opinion, would have been allowed if wine had been liable to duty). | wine tax payable on the *local entry | time when drawback was allowed (or would have been allowed) |

CR15 | Sale *price written off as bad debt | You have: (a) paid wine tax on an *assessable dealing that is a sale and later written off some or all of the *price for which the wine was sold; or (b) paid wine tax on an assessable dealing that is a *local entry (other than an *LE4) and later written off some or all of the price for which the wine was first sold by you after the local entry. | a proportion of the wine tax paid that is equal to the proportion of the debt written off | time of writing off |

(1) If you are *registered or *required to be registered, you may make a claim for a *wine tax credit by including the amount of the wine tax credit in the *reduction of your *net amount for the*tax period in question under section 21‑15.

(2) If you are not *registered or *required to be registered, you may make a claim for a *wine tax credit in the *approved form. The claim must be accompanied by such supporting evidence as the Commissioner requires.

(3) A claim under subsection (2) must be lodged with the Commissioner within 4 years after the time when the *wine tax credit arises.

The Commissioner is not required to consider a claim under subsection 17‑10(2) for a *wine tax credit if the total amount claimed is less than $200.

If you have claimed under subsection 17‑10(2) a *wine tax credit to which you are entitled, the Commissioner must apply the wine tax credit as follows:

(a) the Commissioner may apply the wine tax credit against any liability that you have under the *wine tax law or under any other Act of which the Commissioner has the general administration;

(b) the Commissioner must refund any excess to you.

If the amount applied by the Commissioner under section 17‑20 is more than the amount of the *wine tax credit to which you are properly entitled, the excess is to be treated as if it were wine tax that became payable, and due for payment, by you at the time when it was applied.

Note: The main effect of treating the amount as if it were tax is to apply the collection and recovery rules in Part VI of the Taxation Administration Act 1953.

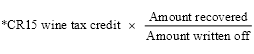

(1) A *wine tax credit under *CR15 in relation to an amount written off by you as a bad debt is subject to the condition that you are liable to pay an amount under this section if you later recover some or all of the amount written off.

(2) The amount payable by you is calculated using the following formula:

(3) The amount is to be treated as if it were wine tax that became payable by you at the time of recovery of the bad debt, and, for the purposes of Part 5, were attributable to the *tax period in which the recovery happened.

Note: The main effect of treating the amount as if it were wine tax is to apply the collection and recovery rules in Part VI of the Taxation Administration Act 1953.

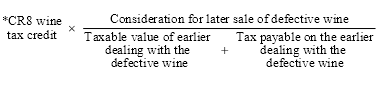

(1) A *wine tax credit under *CR8 for wine tax on wine that was used to replace defective wine is subject to the condition that you are liable to pay an amount under this section if you later sell the defective wine.

(2) The amount payable by you is calculated using the following formula:

(3) The amount is to be treated as if it were wine tax that became payable by you at the time of the later sale of the defective wine, and, for the purposes of Part 5, were attributable to the *tax period in which the later sale happened.

Note: The main effect of treating the amount as if it were wine tax is to apply the collection and recovery rules in Part VI of the Taxation Administration Act 1953.

(1) The Commissioner may enter into an agreement with you regarding the manner of calculating and claiming *wine tax credits to which you are entitled.

(2) So far as the agreement is inconsistent with this Act, the agreement prevails.

If the Commissioner decides to disallow the whole or a part of a claim for a *wine tax credit, the Commissioner must notify you of the decision.

Note: Disallowing the whole or a part of a claim for a wine tax credit is a reviewable wine tax decision (see Division 7 of Part VI of the Taxation Administration Act 1953).

Wine tax (except wine tax on customs dealings) is added to net amounts under the GST Act. Wine tax credits are subtracted from those net amounts.

Note: Division 165 (Anti‑avoidance) of the GST Act will cover avoidance schemes relating to wine tax so far as they affect net amounts, because such schemes affect amounts payable under the GST Act.

(1) Your *net amount for a *tax period is *increased by adding the sum of all of the amounts of wine tax (if any) that are attributable to that tax period.

(2) However, this section does not apply to wine tax payable on *customs dealings.

Note: This section has the effect of incorporating your liability for the wine tax (other than wine tax on customs dealings) into the amount of GST that you are liable to pay under Division 33 of the GST Act, or into the amount of refund to which you are entitled under Division 35 of the GST Act.

(1) The wine tax payable by you on a *taxable dealing that is a *supply is attributable to the same *tax period, or tax periods, applying to you as the tax period or tax periods to which:

(a) if the supply is a *taxable supply—the taxable supply is attributable; or

(b) if the supply is not a taxable supply—the supply would be attributable if it were a taxable supply.

For the basic rules on attribution of taxable supplies, see section 29‑5 of the GST Act.

(2) The wine tax payable by you on a *taxable dealing that is not a *supply is attributable to the *tax period during which the time of dealing occurs, as specified in column 4 of the *Assessable Dealings Table.

Your *net amount for a *tax period is *reduced by subtracting the sum of all of the amounts of *wine tax credits (if any) to which you are entitled that arise during that tax period.

Note 1: This section has the effect of incorporating your entitlement to wine tax credits into the amount of GST that you are liable to pay under Division 33 of the GST Act, or into the amount of refund to which you are entitled under Division 35 of the GST Act.

Note 2: If you are not registered or required to be registered (and therefore do not have net amounts), you can claim wine tax credits to which you are entitled directly from the Commissioner (see subsection 17‑10(2)).

Wine tax on a customs dealing is not included in net amounts. Generally speaking, it is paid together with customs duty. (This is consistent with payment of GST on taxable importations.)

Amounts of wine tax on *customs dealings are to be paid to the Commonwealth:

(a) at the same time, at the same place, and in the same manner, as *customs duty is payable on the wine in question (or would be payable if the wine were subject to customs duty); or

(b) in the circumstances specified in the regulations, within such further time specified in the regulations, and at the place and in the manner specified in the regulations.

Note: The regulations could (for example) allow for deferral of payments to coincide with payments of net amounts.

Division 165 of the *GST Act applies to amounts that are payable under this Division as if they were amounts payable under the GST Act.

(1) This Act applies in relation to cider, perry, mead and sake in the same way that it applies in relation to wine (other than *grape wine).

(2) However, this section does not apply to any beverage of a kind referred to in paragraph 31‑1(2)(a), (b), (c) or (d).

(1) If you sell wine by *wholesale at a *price that includes wine tax that you have or will become liable to pay on the wine, you must specify the amount of the tax on any invoice given to the purchaser.

(2) You are guilty of an offence if you contravene this section.

Maximum penalty: 20 penalty units.

Note 1: Chapter 2 of the Criminal Code sets out the general principles of criminal responsibility.

Note 2: See section 4AA of the Crimes Act 1914 for the current value of a penalty unit.

(1) This section applies to you if:

(a) you (or your *associate) has been a party to a non‑arm’s length transaction; and

(b) if the transaction had instead been an arm’s length transaction, it would have been the case (or could reasonably be expected to have been the case) that:

(i) your liability to wine tax on the non‑arm’s length transaction, or any other transaction, would have been *increased; or

(ii) your entitlement to a *wine tax credit in connection with the non‑arm’s length transaction, or any other transaction, would have been *reduced.

(2) The liability or *wine tax credit is taken always to have been the amount that it would have been (or could reasonably be expected to have been) if it had been based on an arm’s length transaction instead of on the non‑arm’s length transaction.

(1) If there is a need to know the *price for which particular wine was sold, but the parties have not allocated a particular amount to the wine, the price for which the wine was sold is (for the purposes of the *wine tax law) the price for which the wine could reasonably be expected to have been sold if it had been sold separately.

(2) Similarly, if there is a need to know how much of a global amount relates to some other element of a transaction, but the parties have not allocated a particular amount to that element, the amount to be allocated to that element (for the purposes of the *wine tax law) is the amount that could reasonably be expected to have been allocated to that element if that element had been the only subject matter of the transaction.

(1) The Commonwealth and *Commonwealth entities are not liable to pay wine tax payable under this Act. However, it is the Parliament’s intention that the Commonwealth and Commonwealth entities should:

(a) be notionally liable to pay wine tax payable under this Act; and

(b) be notionally entitled to *wine tax credits arising under this Act.

(2) The *Finance Minister may give such written directions as are necessary or convenient for carrying out or giving effect to subsection (1) and, in particular, may give directions in relation to the transfer of *money within an account, or between accounts, operated by the Commonwealth or a *Commonwealth entity.

(3) Directions under subsection (2) have effect, and must be complied with, despite any other Commonwealth law.

(4) Commonwealth entity means:

(a) an Agency (within the meaning of the Financial Management and Accountability Act 1997); or

(b) a Commonwealth authority (within the meaning of the Commonwealth Authorities and Companies Act 1997);

that cannot be made liable to taxation by a Commonwealth law.

(1) This section cancels the effect of a provision of another Act that would have the effect of exempting a person from liability to pay wine tax payable under this Act.

(2) The cancellation does not apply if the provision of the other Act:

(a) commences after this section commences; and

(b) refers specifically to wine tax payable under this Act.

The Criminal Code applies to all offences against this Act.

(1) The Governor‑General may make regulations prescribing matters:

(a) required or permitted by this Act to be prescribed; or

(b) necessary or convenient to be prescribed for carrying out or giving effect to this Act.

(2) In particular, the regulations may make provision:

(a) allowing wine to be brought into *Australia, on a temporary basis, without the payment of wine tax;

(b) relating to the service of documents under, or for the purposes of, the *wine tax law (including the service of process in proceedings for the recovery of tax or other amounts payable under the wine tax law);

(c) for penalties for offences against the regulations by way of fines of up to $1,000.

(1) These all form part of this Act:

the headings to the Parts, Divisions and Subdivisions of this Act;

*explanatory sections;

the headings to the sections and subsections of this Act;

the notes and examples (however described) that follow provisions of this Act.

(2) The asterisks used to identify defined terms form part of this Act. However, if a term is not identified by an asterisk, disregard that fact in deciding whether or not to apply to that term a definition or other interpretation provision.

These do not form part of this Act:

footnotes and endnotes;

Tables of Subdivisions.

(1) An explanatory section is:

(a) any section that is the first section in a Division and that has as its heading “What this Division is about”; or

(b) any section in Division 2, 3 or 4.

(2) *Explanatory sections form part of this Act, but they are not operative provisions. In interpreting an operative provision, an explanatory section may only be considered:

(a) in determining the purpose or object underlying the provision; or

(b) to confirm that the provision’s meaning is the ordinary meaning conveyed by its text, taking into account its context in this Act and the purpose or object underlying the provision; or

(c) in determining the provision’s meaning if the provision is ambiguous or obscure; or

(d) in determining the provision’s meaning if the ordinary meaning conveyed by its text, taking into account its context in this Act and the purpose or object underlying the provision, leads to a result that is manifestly absurd or is unreasonable.

(1) Wine includes any fruit wine or vegetable wine.

Note: The wine tax also applies to cider, perry, mead and sake in the same way that it applies to wine (see section 27‑1).

(2) However, wine does not include:

(a) beverages that do not contain more than 1.15% by volume of ethyl alcohol; or

(b) *beer; or

(c) spirits, liqueurs or spirituous liquors; or

(d) beverages that contain beer, spirits (other than spirits for fortifying wine or other beverages), liqueurs or spirituous liquors.

(3) For the purpose of paragraph (3)(a), the volume of ethyl alcohol in beverages is to be measured at 20°C and is to be calculated on the basis that the specific gravity of ethyl alcohol is 0.79067 (at 20°C in a vacuum).

(4) Beer means any fermented liquor (whether or not the liquor contains sugar, glucose or any other substance) that:

(a) is brewed from a mash (whether or not the mash contains malt); and

(b) contains hops (including any substance prepared from hops) or other bitters.

Note: The concept of grape wine is used in Subdivision 9‑B to work out the taxable value of retail transactions involving wine produced from grapes. In the case of grape wine, you can choose to use the average wholesale price method of working out taxable values.

(1) Grape wine is wine that:

(a) is the product of the complete or partial fermentation of fresh grapes or products derived solely from fresh grapes; and

(b) complies with any requirements of the regulations relating to any of the following:

(i) the substances that may be added to grape wine;

(ii) the substances that may be used in the production of grape wine;

(iii) the composition of grape wine.

(2) A beverage does not cease to be the product of the complete or partial fermentation of fresh grapes or products derived solely from fresh grapes merely because:

(a) it has, by complete or partial fermentation of contained sugars, become surcharged with carbon dioxide; or

(b) grape spirit, brandy, or both grape spirit and brandy, have been added to it.

(1) This section sets out the 2 situations in which an entity is taken to have borne wine tax on wine.

(2) An entity is taken to have borne wine tax on wine if the entity has become liable to wine tax on an *assessable dealing with the wine. However, the wine tax for which the entity has become liable is not counted to the extent to which it has been the basis of a *wine tax credit entitlement.

(3) An entity is taken to have borne wine tax on wine if the entity purchased the wine for a *price that included wine tax. However, the amount of wine tax borne is to be *reduced by any amount of the wine tax included in that price that has been refunded or *wine tax credited to the entity.

(1) This section sets out the circumstances in which wine is taken to be obtained by an entity under quote.

(2) An entity purchases wine under quote if the entity *quotes on the purchase of the wine, and either:

(a) the sale is an *assessable dealing by the seller that is exempted from tax only because of the quote; or

(b) on the basis of the quote, the seller agrees to exclude tax from the *price of the wine.

(3) An entity locally enters wine under quote if the entity *quotes on the *local entry of the wine and the local entry is exempted from tax only because of the quote.

(4) An entity obtains wine under quote if:

(a) the entity *purchases, or *locally enters, the wine under quote as described in subsection (2) or (3); or

(b) the entity *quotes on a *customs dealing with the wine and the dealing is exempted from tax only because of the quote; or

(c) the entity has obtained a *CR2 wine tax credit for *wine tax borne on a dealing with the wine.

(1) A notice, application or other document is in the approved form if:

(a) it is in the form approved in writing by the *Commissioner in relation to that kind of notice, application or other document; and

(b) it contains the information that the form requires, and such further information as the Commissioner requires; and

(c) it is given, to the entity to which it is required to be given, in the manner (if any) that the Commissioner requires; and

(d) it is, if required by this Act to be given to the Commissioner, lodged at the place that the Commissioner requires.

(2) The *Commissioner may combine in the same approved form more than one notice, application or other document.

In this Act, unless the contrary intention appears:

ABN has the meaning given by section 41 of the A New Tax System (Australian Business Number) Act 1998.

accompanied baggage, in relation to the *export of wine, means wine that is exported on a flight or voyage on which the owner of the wine is a passenger.

AD1a means the *assessable dealing of that name in the *Assessable Dealings Table, and AD1b, AD2a etc. have corresponding meanings.

airport shop goods has the same meaning as in the Customs Act 1901.

amount includes a nil amount.

AOU means *application to own use.

AOU connected with retail sales of wine means an *AOU that:

(a) is constituted by consuming wine or giving wine away; and

(b) is connected with making, or attempting to make, *retail sales of wine.

AOU connected with retail sales of grape wine has the meaning given by subsection 9‑25(4).

application to own use, in relation to wine, includes any of the following:

(a) consuming the wine;

(b) giving the wine away, or transferring property in the wine under a contract that is not a contract of sale;

(c) granting any right or permission to use the wine;

(d) if an entity other than the owner has *locally entered the wine—anything done by the entity that would be an application to own use of the wine by the owner if it had been done by the owner;

but does not include:

(e) selling the wine or consigning it for sale by consignment; or

(f) if the wine is *imported wine—anything done with it after *importation and before it is locally entered.

approved form has the meaning given by Subdivision 31‑E.

assessable dealing means any dealing covered by the *Assessable Dealings Table.

Assessable Dealings Table means the table in section 5‑5.

assessable wine means *Australian wine or *imported wine.

associate has the meaning given by section 318 of the Income Tax Assessment Act 1936.

Australia has the meaning given by section 195‑1 of the *GST Act.

Australian wine means wine that has been *manufactured in *Australia, but does not include *imported wine.

average wholesale price method for working out the *notional wholesale selling price of a *taxable dealing is the method set out in section 9‑40.

beer has the meaning given by subsection 31‑1(4).

borne wine tax has the meaning given by Subdivision 31‑C.

Commissioner means the Commissioner of Taxation.

Commonwealth entity has the meaning given by subsection 27‑20(4).

company means:

(a) a body corporate; or

(b) any other unincorporated association or body of persons;

but does not include a *partnership.

container means:

(a) packaging in which, or with which, any property (the contents) is packed or secured, in the ordinary course of a business, for the purpose of the marketing or delivery of the contents; and

(b) ancillary items that are packed or secured with the contents and are intended, and reasonably necessary, to allow or facilitate the use of the contents.

CR1 means the wine tax credit ground of that name in the *Wine Tax Credit Table, and CR2, CR3 etc. have corresponding meanings.

Customs means the Australian Customs Service.

customs clearance area means an area that is designated or set aside for the performance of functions under the Customs Act 1901.

customs dealing means *AD4b, *AD10 or *AD14b.

customs duty means any duty of customs imposed by that name under a law of the Commonwealth, other than:

(a) the A New Tax System (Goods and Services Tax Imposition—Customs) Act 1999; or

(b) the A New Tax System (Wine Equalisation Tax Imposition—Customs) Act 1999.

Customs Tariff means the Customs Tariff Act 1995 as amended by any Act, and as proposed to be amended by Customs Tariff Proposals introduced into the House of Representatives.

eligible Australian traveller means an entity defined to be an eligible Australian traveller by regulations made for the purposes of this definition.

eligible foreign traveller means an entity defined to be an eligible foreign traveller by regulations made for the purposes of this definition.

eligible royalty cost has the meaning given by subsection 5‑15(2).

entity has the meaning given in section 195‑1 of the *GST Act.

explanatory section has the meaning given by section 29‑10.

export, in relation to wine, means export the wine from *Australia, and, in relation to an *eligible Australian traveller, includes taking the wine out of Australia as *accompanied baggage.

Finance Minister means the Minister administering the Financial Management and Accountability Act 1997.

grape wine has the meaning given by Subdivision 31‑B.

GST has the meaning given by section 195‑1 of the *GST Act.

GST Act means the A New Tax System (Goods and Services Tax ) Act 1999.

GST‑free has the meaning given by section 195‑1 of the *GST Act.

GST importation value of a *local entry is an amount equal to what would be the value of the local entry, for the purposes of the *GST Act, if it were a taxable importation within the meaning of section 195‑1 of that Act.

For the basic rules on the value of taxable importations, see section 13‑20 of the GST Act.

half‑retail price method for working out the *notional wholesale selling price of a *taxable dealing is:

(a) if the dealing is a *retail sale—the method set out in subsection 9‑35(1); or

(b) if the dealing is an *AOU connected with retail sales of grape wine—the method set out in subsection 9‑35(2).

import means *import goods into Australia.

importation of goods into Australia has the meaning given by section 195‑1 of the *GST Act.

imported wine means wine that has been *imported (whether or not the wine was *manufactured in *Australia).

increase includes increase from nil.

indirect marketing sale has the meaning given by section 5‑20.

inwards duty free shop has the same meaning as in section 96B of the Customs Act 1901.

LE1 means the *local entry of that name in the *Local Entry Table, and LE2, LE3 etc. have corresponding meanings.

local entry has the meaning given by section 5‑30.

Local Entry Table means the table in section 5‑30.

locally enter wine under quote has the meaning given by subsection 31‑15(3).

manufacture includes the following:

(a) production;

(b) combining parts or ingredients so as to form an article or substance that is commercially distinct from the parts or ingredients;

(c) applying a treatment to foodstuffs as a process in preparing them for human consumption;

but does not include any prescribed combination of parts or ingredients.

manufacturer, in relation to particular wine, means the entity that (not as an employee) *manufactured the wine, whether or not the entity owned the materials out of which the wine was manufactured.

money has the meaning given by section 195‑1 of the *GST Act.

net amount has the meaning given by section 195‑1 of the *GST Act.

notional wholesale purchase price, in relation to wine, means the *price (excluding wine tax and *GST) for which you could reasonably have been expected to purchase the wine by wholesale under an arm’s length transaction.

notional wholesale selling price has the meaning given by Subdivision 9‑B.

obtain wine under quote has the meaning given by Subdivision 31‑D.

partnership has the meaning given by section 995‑1 of the *ITAA 1997.

passed on, in relation to an amount of tax that has been *borne by an entity, does not include an amount that the entity has passed on to another entity, but has later refunded to that other entity.

prescribed rules for export sales means the rules prescribed by the regulations setting out conditions that must be complied with in order for dealings with wine to be exempted, or otherwise relieved from wine tax, on the basis of the *export, or intended export, of the wine.

price has the meaning given by section 9‑75 of the *GST Act.

purchase wine under quote has the meaning given by subsection 31‑15(2).

quote means quote an *ABN.

reduce includes reduce to nil.

registered has the meaning given by section 195‑1 of the *GST Act.

relevant traveller has the same meaning as in section 96B of the Customs Act 1901.

required to be registered has the meaning given by section 195‑1 of the *GST Act.

retail sale means any sale that is not a *wholesale sale.

royalty has the meaning given by subsection 9‑70(2).

royalty‑inclusive AOU has the meaning given by section 5‑15.

royalty‑inclusive sale has the meaning given by section 5‑15.

sale includes barter or exchange.

supply has the meaning given by section 9‑10 of the *GST Act.

taxable dealing means an *assessable dealing that happens on or after 1 July 2000 for which no exemption is available under Division 7.

taxable supply has the meaning given by section 195‑1 of the *GST Act.

taxable value means the taxable value that applies under Division 9.

tax‑bearing dealing, in relation to an amount of *wine tax borne by an entity, means the dealing through which, or because of which, the tax was borne.

tax period has the meaning given by section 195‑1 of the *GST Act.

untaxed AOU has the meaning given by subsection 5‑25(2).

untaxed sale has the meaning given by subsection 5‑25(1).

wholesale sale means a sale to an entity that purchases for the purpose of resale, but does not include a sale of wine from stock in a retail store (or retail section of a store) to make up for a temporary shortage of stock of the purchaser, if the wine is of a kind that:

(a) is usually *manufactured by the purchaser; or

(b) is usually purchased by the purchaser for resale.

wine has the meaning given by Subdivision 31‑A.

wine tax means tax that is payable under the *wine tax law and imposed as wine equalisation tax by any of these:

(a) the A New Tax System (Wine Equalisation Tax Imposition—General) Act 1999; or

(b) the A New Tax System (Wine Equalisation Tax Imposition—Customs) Act 1999; or

(c) the A New Tax System (Wine Equalisation Tax Imposition—Excise) Act 1999.

wine tax borne has the meaning given by Subdivision 31‑C.

wine tax credit means a wine tax credit under Part 4.

Wine Tax Credit Table means the table in section 17‑5.

wine tax law means:

(a) this Act; and

(b) any Act that imposes wine tax; and

(c) the A New Tax System (Wine Equalisation Tax and Luxury Car Tax Transition) Act 1999 so far as it relates to the Acts covered by paragraphs (a) and (b); and

(d) the Taxation Administration Act 1953, so far as it relates to any Act covered by paragraphs (a) to (c); and

(e) any other Act, so far as it relates to any Act covered by paragraphs (a) to (d) (or to so much of that Act as is covered); and

(f) regulations under an Act, so far as they relate to any Act covered by paragraphs (a) to (e) (or to so much of that Act as is covered).

you: if a provision of this Act uses the expression you, it applies to entities generally, unless its application is expressly limited.

Note: The expression you is not used in provisions that apply only to entities that are not individuals.

[Minister’s second reading speech made in—

House of Representatives on 24 March 1999

Senate on 31 March 1999]

(56/99)