A New Tax System (Closely Held Trusts) Act 1999

No. 70, 1999

A New Tax System (Closely Held Trusts) Act 1999

No. 70, 1999

A New Tax System (Closely Held Trusts) Act 1999

No. 70, 1999

An Act to implement A New Tax System by amending the income tax law in respect of certain closely held trusts, and for related purposes

Contents

1 Short title...................................

2 Commencement...............................

3 Schedule(s)..................................

Schedule 1—Basic amendments

Income Tax Assessment Act 1936

Schedule 2—Consequential amendments

Part 1—Income Tax Assessment Act 1936

Part 2—Income Tax Assessment Act 1997

Part 3—Superannuation Contributions Tax (Assessment and Collection) Act 1997

A New Tax System (Closely Held Trusts) Act 1999

No. 70, 1999

An Act to implement A New Tax System by amending the income tax law in respect of certain closely held trusts, and for related purposes

[Assented to 8 July 1999]

The Parliament of Australia enacts:

This Act may be cited as the A New Tax System (Closely Held Trusts) Act 1999.

This Act commences on the day on which it receives the Royal Assent.

Each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

Income Tax Assessment Act 1936

1 Subsection 97(1)

Omit “Where”, substitute “Subject to Division 6D, where”.

2 After Division 6C of Part III

Insert:

Division 6D—Provisions relating to certain closely held trusts

102UA What this Division is about

(1) The main purpose of this Division is to ensure that the trustee of a closely held trust with a trustee beneficiary advises the Commissioner of the ultimate beneficiaries of certain net income and tax‑preferred amounts of the trust soon after the end of the year of income. This will allow the Commissioner to check whether the assessable income of the ultimate beneficiaries correctly includes any required share of that net income, and whether the net assets of the ultimate beneficiaries reflect the receipt of the tax‑preferred amounts.

(2) To achieve this purpose, the Division:

(a) provides for the trustee to correctly identify the ultimate beneficiaries within a specified period after the end of the year of income; and

(b) if the trustee fails to do so, provides for taxation at a penalty rate (in the case of net income) or offences under the Taxation Administration Act 1953 (in the case of tax‑preferred amounts).

(3) This Division also provides that, where there are in fact no ultimate beneficiaries of net income of the closely held trust, there will also be taxation at a penalty rate.

In this Division:

closely held trust has the meaning given by subsection 102UC(1).

correct UB statement has the meaning given by section 102UG.

listed person has the meaning given by section 102UF.

present entitlement has a meaning affected by section 102UJ.

tax offset has the same meaning as in the Income Tax Assessment Act 1997.

tax‑preferred amount has the meaning given by section 102UI.

trustee beneficiary has the meaning given by section 102UD.

UB statement period has the meaning given by section 102UH.

ultimate beneficiary has the meaning given by section 102UE.

ultimate beneficiary non‑disclosure tax means tax payable under paragraph 102UK(2)(a) or 102UM(2)(a).

(1) A closely held trust is:

(a) a trust where an individual has, or up to 20 individuals have between them, directly or indirectly, and for their own benefit, fixed entitlements to a 75% or greater share of the income, or a 75% or greater share of the capital, of the trust; or

(b) a discretionary trust;

except where the trust is an excluded trust.

Trustees of discretionary trusts treated as individuals

(2) For the purposes of paragraph (1)(a), if:

(a) a trustee of a discretionary trust holds a fixed entitlement to a share of the income or capital of the trust mentioned in that paragraph directly or indirectly; and

(b) no person holds that fixed entitlement directly or indirectly through the discretionary trust;

the trustee is taken to hold that fixed entitlement directly or indirectly as an individual and for the individual’s own benefit.

Individuals treated as single individual

(3) For the purposes of paragraph (1)(a), all of the following are taken to be a single individual:

(a) an individual, whether or not the individual holds fixed entitlements directly in the trust mentioned in that paragraph;

(b) the individual’s relatives;

(c) in relation to any fixed entitlements in respect of which other individuals are nominees of the individual or of the individual’s relatives—those other individuals.

Definitions

(4) In this section:

discretionary trust means a trust that is not a fixed trust within the meaning of section 272‑65 of Schedule 2F.

excluded trust means:

(a) a trust to which paragraph (b), (c) or (d) of the definition of excepted trust in section 272‑100 of Schedule 2F applies; or

(b) a unit trust whose units are listed on the Australian Stock Exchange Limited.

fixed entitlement has the meaning given by sections 272‑5, 272‑10, 272‑15 and 272‑40 of Schedule 2F.

indirectly has the meaning given by section 272‑20 of Schedule 2F.

A person is a trustee beneficiary of a closely held trust if the person is a beneficiary of the trust in the capacity of trustee of another trust.

(1) This section states when a person is an ultimate beneficiary in respect of the whole or part (the head trust amount) of:

(a) a share of the net income of a closely held trust for a year of income that is included in the assessable income of a trustee beneficiary of the trust under section 97; or

(b) a share of a tax‑preferred amount of a closely held trust to which a trustee beneficiary of the trust is presently entitled at the end of a year of income.

Present entitlement cases

(2) A person is an ultimate beneficiary in respect of the head trust amount if the person is a listed person and:

(a) is the trustee beneficiary; or

(b) is presently entitled to the head trust amount indirectly through one or more interposed partnerships or trusts (other than any that are ultimate beneficiaries).

No present entitlement

(3) A person is an ultimate beneficiary in respect of the head trust amount if:

(a) the person:

(i) is the trustee beneficiary; or

(ii) is the trustee of a trust who is presently entitled to the head trust amount indirectly through one or more interposed partnerships or trusts (other than any that are ultimate beneficiaries); and

(b) no beneficiary of the trust of which the person is trustee is presently entitled to the head trust amount indirectly as a beneficiary of that trust.

Full absorption of head trust amount

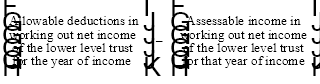

(4) If the head trust amount is the whole or part of a share of the net income of the closely held trust, a person is also an ultimate beneficiary in respect of the head trust amount if:

(a) the person is the trustee of another closely held trust (the lower level trust); and

(b) the person:

(i) is the trustee beneficiary; or

(ii) is presently entitled to the head trust amount indirectly through one or more interposed partnerships or trusts (other than as ultimate beneficiaries); and

(c) the head trust amount is not greater than the amount worked out using the formula:

Exclusion of trustee of closely held trust

(5) The trustee of the closely held trust cannot, in the capacity of trustee of that trust, be an ultimate beneficiary of the head trust amount.

For the purposes of subsection 102UE(2), a person is a listed person if the person is:

(a) an individual (other than in the capacity of trustee of a trust); or

(b) a company (other than in the capacity of trustee of a trust); or

(c) the trustee of a trust that is not a closely held trust; or

(d) a pooled superannuation trust within the meaning of section 48 of the Superannuation Industry (Supervision) Act 1993, in relation to the year of income concerned; or

(e) a complying superannuation fund, within the meaning of section 45 of that Act, in relation to the year of income concerned; or

(f) a complying approved deposit fund, within the meaning of section 47 of that Act, in relation to the year of income concerned; or

(g) an institution all of whose income of the year of income concerned is exempt under section 50‑5 of the Income Tax Assessment Act 1997; or

(h) a fund, authority or institution in Australia that is mentioned in section 30‑15 of the Income Tax Assessment Act 1997.

Share of net income case

(1) This section applies if:

(a) a share of the net income of a closely held trust for a year of income is included in the assessable income of a trustee beneficiary of the trust under section 97; and

(b) there are one or more ultimate beneficiaries in respect of the whole or a part (the head trust amount) of the share.

Tax‑preferred amount case

(2) This section also applies if:

(a) a trustee beneficiary of a closely held trust is presently entitled at the end of a year of income to a share of a tax‑preferred amount of the trust; and

(b) there are one or more ultimate beneficiaries in respect of the whole or a part (also the head trust amount) of the share.

Correct UB statement

(3) If this section applies, the trustee of the closely held trust makes a correct UB statement about the head trust amount if the trustee correctly states in writing:

(a) how much of the head trust amount is attributable to each ultimate beneficiary; and

(b) whether the ultimate beneficiary is an ultimate beneficiary by virtue of subsection 102UE(2), (3) or (4); and

(c) for each ultimate beneficiary who is a resident at the end of the year of income—the ultimate beneficiary’s name and tax file number; and

(d) for each ultimate beneficiary who is not a resident at the end of the year of income—the ultimate beneficiary’s name and address.

The UB statement period, for the trustee of a trust in relation to a year of income, is the period from the end of the year of income until the end of the period within which the trustee is required to furnish to the Commissioner the trust’s return of income for the year of income.

The expression tax‑preferred amount of a trust means:

(a) income of the trust that is not included in its assessable income in working out its net income; or

(b) capital of the trust.

Indirect present entitlement to a share of net income

(1) For the purposes of this Division, if a person is presently entitled indirectly through one or more interposed partnerships or trusts to a share of the income of a trust derived in a year of income, the person is presently entitled indirectly through the one or more partnerships or trusts to that share of the net income of the trust.

Note: Section 95A is relevant in determining whether a person is presently entitled to a share of the income of a trust.

Extended concept of present entitlement to capital of a trust

(2) For the purposes of this Division, section 95A applies in relation to capital of a trust in the same way as it applies to income of the trust.

Subdivision C—Ultimate beneficiary non‑disclosure tax on share of net income

102UK Ultimate beneficiary non‑disclosure tax where no correct UB statement

(1) This section applies if:

(a) a share of the net income of a closely held trust for a year of income is included in the assessable income of a trustee beneficiary of the trust under section 97; and

(b) there are one or more ultimate beneficiaries in respect of the whole or a part of the share of the net income; and

(c) during the UB statement period in relation to the year of income, the trustee of the closely held trust does not make and give to the Commissioner a correct UB statement about the whole or the part of the share.

Consequences of section applying

(2) If this section applies:

(a) either:

(i) if the trustee of the closely held trust is the only person in the trustee group (see subsection (3))—the trustee is liable to pay tax; or

(ii) if the trustee of the closely held trust is not the only person in the trustee group—the persons in the trustee group are jointly and severally liable to pay tax;

as imposed by the A New Tax System (Ultimate Beneficiary Non‑disclosure Tax) Act (No. 1) 1999, on the whole or the part of the share of the net income, other than on any amount in respect of which the trustee did make and give to the Commissioner a correct UB statement during the UB statement period; and

Note: Provisions dealing with the payment etc. of the tax under paragraph (a) (known as ultimate beneficiary non‑disclosure tax) are set out in Subdivision D.

Trustee group

(3) The trustee group consists of the following:

(a) the trustee of the closely held trust;

(b) if the trustee of the closely held trust is a company—the directors of the company.

102UL Exclusion of directors of closely held trust from liability to pay tax

(1) This section applies if a director of a company that is the trustee of the closely held trust is included in the trustee group under section 102UK.

Director not taking part in statement decision because of illness or other good reason

(2) If, because of illness or for some other good reason, the director did not take part in any decision not to make the correct UB statement, the director is not included in the trustee group.

Director otherwise not taking part in statement decision

(3) If:

(a) the director did not take part in any decision not to make the correct UB statement; and

(b) either:

(i) the director was not aware of the proposal to make such a decision; or

(ii) the director was aware and took reasonable steps to prevent the making of the decision;

the director is not included in the trustee group.

Director taking part in statement decision

(4) If:

(a) the director took part in any decision not to make a correct UB statement; and

(b) the director voted against, or otherwise disagreed with the decision; and

(c) the director took reasonable steps to ensure that a correct UB statement would be made;

the director is not included in the trustee group.

(5) If:

(a) no decision was made not to make a correct UB statement; and

(b) either:

(i) the director, because of illness or for some other good reason, was not involved in the management of the company during the UB statement period in relation to the year of income; or

(ii) the director took reasonable steps to ensure that a correct UB statement would be made;

the director is not included in the trustee group.

102UM Ultimate beneficiary non‑disclosure tax where no ultimate beneficiary

(1) This section applies if:

(a) a share of the net income of a closely held trust for a year of income is included in the assessable income of a trustee beneficiary of the trust under section 97; and

(b) there is no ultimate beneficiary in respect of the whole or a part of the share of the net income.

Consequences of section applying

(2) If this section applies:

(a) either:

(i) if the trustee of the closely held trust is the only person in the trustee group (see subsection (3))—the trustee is liable to pay tax; or

(ii) if the trustee of the closely held trust is not the only person in the trustee group—the persons in the trustee group are jointly and severally liable to pay tax;

as imposed by the A New Tax System (Ultimate Beneficiary Non‑disclosure Tax) Act (No. 2) 1999, on the whole or the part of the share of the net income; and

Note: Provisions dealing with the payment etc. of the tax under paragraph (a) (known as ultimate beneficiary non‑disclosure tax) are set out in Subdivision D.

(b) except for the purposes of sections 99, 99A and 99B and this Division, the whole or the part of the share of the net income is not included in the assessable income of the trustee beneficiary under section 97.

Trustee group

(3) The trustee group consists of the following:

(a) the trustee of the closely held trust;

(b) if the trustee of the closely held trust is a company—the directors of the company.

Subdivision D—Payment etc. of ultimate beneficiary non‑disclosure tax

102UN Amount of ultimate beneficiary non‑disclosure tax reduced by notional tax offset

(1) This section applies to ultimate beneficiary non‑disclosure tax that a trustee group would otherwise be liable to pay on the whole or part of a share of the net income of a closely held trust.

(2) The amount of the ultimate beneficiary non‑disclosure tax is reduced by the amount of any tax offset to which the trustee of the closely held trust would be entitled in an assessment under section 99A if it were assumed that the trustee were assessed and liable to pay tax under that section on the whole or the part of the share of the net income.

102UO Payment of ultimate beneficiary non‑disclosure tax

Due date

(1) Ultimate beneficiary non‑disclosure tax is due and payable at the end of:

(a) 21 days after the UB statement period concerned ends; or

(b) such later day as the Commissioner, in special circumstances, allows.

Debt due

(2) Ultimate beneficiary non‑disclosure tax, when it becomes due and payable, is a debt due to the Commonwealth and payable to the Commissioner.

102UP Additional tax for late payment

(1) Subject to subsection (2), if any ultimate beneficiary non‑disclosure tax remains unpaid at the end of 60 days after the day when it became due and payable, additional tax, by way of penalty, is due and payable at the rate of 16% per annum on the amount unpaid, calculated from the end of that period.

Remission of additional tax

(2) Where additional tax is due and payable by a person or persons under subsection (1) in relation to an amount of ultimate beneficiary non‑disclosure tax, the Commissioner may remit the additional tax or a part of it if he or she is satisfied as mentioned in subsection (3), (4) or (5).

Remission criteria

(3) The Commissioner may remit the additional tax or part if satisfied that:

(a) the circumstances that contributed to the delay in payment of the ultimate beneficiary non‑disclosure tax were not due to, or caused directly or indirectly by, an act or omission of the person or persons; and

(b) the person or persons have taken reasonable action to mitigate, or mitigate the effects of, those circumstances.

Remission criteria

(4) The Commissioner may remit the additional tax or part if satisfied that:

(a) the circumstances that contributed to the delay in payment of the ultimate beneficiary non‑disclosure tax were due to, or caused directly or indirectly by, an act or omission of the person or persons; and

(b) the person or persons have taken reasonable action to mitigate, or mitigate the effects of, those circumstances; and

(c) having regard to the nature of those circumstances, it would be fair and reasonable to remit the additional tax or the part of the additional tax.

Remission criteria

(5) The Commissioner may remit the additional tax or part if satisfied that there are special circumstances by reason of which it would be fair and reasonable to do so.

Effect of court judgment

(6) Where judgment is given by, or entered in, a court for the payment of:

(a) an amount of ultimate beneficiary non‑disclosure tax; or

(b) an amount that includes an amount of ultimate beneficiary non‑disclosure tax;

then:

(c) the ultimate beneficiary non‑disclosure tax is not taken, for the purposes of subsection (1), to have ceased to be due and payable by reason only of the giving or entering of the judgment; and

(d) if the judgment debt carries interest, the additional tax that would, but for this paragraph, be payable under this section in relation to the ultimate beneficiary non‑disclosure tax is reduced by:

(i) in a case to which paragraph (a) applies—the amount of the interest; or

(ii) in a case to which paragraph (b) applies—the percentage of the interest worked out using the formula:

![]()

Any unpaid ultimate beneficiary non‑disclosure tax, and any unpaid additional tax payable under section 102UP, may be sued for and recovered in a court of competent jurisdiction by the Commissioner suing in his or her official name.

(1) The Commissioner may give a person or persons, by post or otherwise, a notice specifying:

(a) the amount of any ultimate beneficiary non‑disclosure tax that the Commissioner has ascertained is payable by the person or persons; and

(b) the day on which that tax became or will become due and payable.

Effect of notice on liability etc.

(2) The amount of the liability of a person or persons to ultimate beneficiary non‑disclosure tax, and the due date for payment of the tax, are not dependent on, or in any way affected by, the giving of a notice.

Amendment of notice

(3) The Commissioner may at any time amend a notice. An amended notice is a notice for the purposes of this section.

Inconsistency between notices

(4) If there is an inconsistency between notices that relate to the same subject matter, the later notice prevails to the extent of the inconsistency.

Objections

(5) A person who is or persons who are dissatisfied with a notice made in relation to the person or persons may object against it in the manner set out in Part IVC of the Taxation Administration Act 1953.

102US Evidentiary effect of notice of liability

(1) The production of:

(a) a notice given under section 102UR; or

(b) a document that is signed by the Commissioner and appears to be a copy of such a notice;

is conclusive evidence that:

(c) the notice was duly given; and

(d) the amount of ultimate beneficiary non‑disclosure tax specified in the notice became due and payable by the person or persons to whom it was given on the day specified.

(2) Subsection (1) does not apply in proceedings under Part IVC of the Taxation Administration Act 1953 on a review or appeal relating to the review.

Subdivision E—Making correct UB statement about ultimate beneficiaries of tax‑preferred amounts

102UT Requirement to make correct UB statement about ultimate beneficiaries of tax‑preferred amounts

(1) If, at the end of a year of income, a trustee beneficiary of a closely held trust is presently entitled to a share of a tax‑preferred amount of the trust, the trustee of the closely held trust must, during the UB statement period, make and send to the Commissioner a statement of either of the following kinds, or statements of the following kinds, covering the whole of the share of the tax‑preferred amount:

(a) a correct UB statement;

(b) a correct statement in writing that there is no ultimate beneficiary.

(2) For the purposes of the Taxation Administration Act 1953, if the trustee contravenes the requirement in subsection (1) of this section to make and send a statement to the Commissioner, then, subject to subsection (3) of this section, the trustee is guilty of an offence against section 8C of that Act.

(3) The trustee is not guilty of an offence against section 8C of the Taxation Administration Act 1953 as a result of a contravention of the requirement if:

(a) the trustee did not know all the information required to be included in the statement or statements; and

(b) the trustee had taken reasonable steps to ascertain the information that he or she did not know; and

(c) if the trustee did know some of the information, he or she included it in a statement or statements that he or she sent to the Commissioner during the UB statement period.

(4) The only burden of proof that the trustee bears in respect of subsection (3) is the burden of adducing or pointing to evidence that suggests a reasonable possibility that the matter in question existed.

Subdivision F—Special provisions about tax file numbers

102UU Ultimate beneficiary may quote tax file number to trustee of closely held trust

An ultimate beneficiary in respect of the whole or part of:

(a) a share of the net income of a closely held trust for a year of income that is included in the assessable income of a trustee beneficiary of the trust under section 97; or

(b) a share of a tax‑preferred amount of a closely held trust to which a trustee beneficiary of the trust is presently entitled at the end of a year of income;

may quote his or her tax file number to the trustee of the closely held trust in connection with that trustee making a correct UB statement about that share.

Note: Section 8WA of the Taxation Administration Act 1953 makes it an offence for a person to require or request another person to quote the other person’s tax file number unless provision is made by a taxation law for the other person to quote the number.

102UV Trustee of closely held trust may record etc. tax file number

(1) This section applies if an ultimate beneficiary in respect of the whole or part of:

(a) a share of the net income of a closely held trust for a year of income that is included in the assessable income of a trustee beneficiary of the trust under section 97; or

(b) a share of a tax‑preferred amount of a closely held trust to which a trustee beneficiary of the trust is presently entitled at the end of a year of income;

quotes his or her tax file number to the trustee of the closely held trust in connection with that trustee making a correct UB statement about that share.

(2) Section 8WB of the Taxation Administration Act 1953 does not prohibit the trustee of the closely held trust from:

(a) recording the tax file number or maintaining such a record; or

(b) using the tax file number in a manner connecting it with the identity of the ultimate beneficiary; or

(c) divulging or communicating the tax file number to a third person;

in connection with that trustee making a correct UB statement about that share.

3 Application

(1) This item affects the following references in provisions of Division 6D of Part III of the Income Tax Assessment Act 1936 as amended by this Schedule:

(a) references in sections 102UK, 102UM, 102UU and 102UV to a share of the net income of a closely held trust being included in the assessable income of the trustee beneficiary of the trust under section 97 of the Income Tax Assessment Act 1936;

(b) references in sections 102UT, 102UU and 102UV to a trustee beneficiary of a closely held trust being presently entitled to a share of a tax‑preferred amount of the trust.

Note: Because the references concerned are in the operative provisions of the new Division, this item determines when the amendments made by this Schedule will commence to apply.

(2) In the case of the references in paragraph (1)(a) of this item, the references only apply where the present entitlement to the share of income, mentioned in section 97 of the Income Tax Assessment Act 1936 in relation to the share of the net income concerned, arose after 4 pm, by legal time in the Australian Capital Territory, on 13 August 1998.

(3) In the case of the references in paragraph (1)(b) of this item, the references only apply where the present entitlement to the share of the tax‑preferred amount concerned arose after 4 pm, by legal time in the Australian Capital Territory, on 13 August 1998.

4 Transitional—extension of statement deadline

If the end of the UB statement period mentioned in Division 6D of Part III of the Income Tax Assessment Act 1936 as amended by this Schedule occurs before the commencement of this Schedule, the end of the UB statement period is taken instead to occur when 90 days have elapsed after the commencement of this Schedule.

Schedule 2—Consequential amendments

Part 1—Income Tax Assessment Act 1936

1 Paragraph 26(b)

Omit “and” (last occurring).

2 At the end of paragraph 26(b)

Add:

or (iii) amounts on which ultimate beneficiary non‑disclosure tax is payable under Division 6D; and

3 At the end of subparagraph 47A(18)(d)(ii)

Add:

or (G) the trustee of a trust estate where ultimate beneficiary non‑disclosure tax is payable under Division 6D on the whole or part of the net income of the trust estate;

4 At the end of paragraph 47A(18)(d)

Add:

(vi) if sub‑subparagraph (ii)(G) applies:

(A) the trust estate was a resident trust estate (within the meaning of Division 6) in relation to the assessment year of income; and

(B) the whole or a part (which whole or part is in this subsection also called the actual taxpayer’s portion of the original assessable amount) of the whole or the part of the share of the net income is attributable (either directly or indirectly through one or more interposed partnerships or trusts) to the original assessable amount;

5 After subsection 86(2)

Insert:

(2A) This section does not apply in working out a share of the net income of a closely held trust for the purposes of applying paragraph 102UK(2)(a) or 102UM(2)(a) (which deals with ultimate beneficiary non‑disclosure tax). However, this subsection does not as a result affect the way in which a share of the net income of a closely held trust is worked out for the purposes of applying paragraph 102UK(2)(b) or 102UM(2)(b).

6 Subsection 102AAE(2)

Omit “either of”, substitute “one of”.

7 After paragraph 102AAE(2)(b)

Insert:

(c) both of the following conditions are satisfied:

(i) ultimate beneficiary non‑disclosure tax is payable under Division 6D on the whole or part (the net income amount) of a share of the net income of the trust estate of the trust’s year of income;

(ii) the whole or part of the net income amount is attributable to the item part;

8 After subsection 102AAM(4)

Insert:

(4A) If:

(a) paragraph 102UK(2)(b) or 102UM(2)(b) has the effect that the whole or a part of a share of the net income of a trust estate (the first trust estate) is not included in the assessable income of the trustee of another trust estate (the second trust estate); and

(b) the whole or the part of the share (which whole or part is in this subsection called the taxpayer’s portion of the distributed amount of the non‑resident trust’s year of income) is attributable (either directly or indirectly through one or more interposed partnerships or trusts) to the distributed amount of the non‑resident trust’s year of income; and

(c) if paragraph 102UK(2)(b) or 102UM(2)(b) were ignored, the second trust estate would be an interposed trust mentioned in applying subparagraph (4)(b)(iii) or (iv) of this section; and

(d) this subsection does not also apply to the trustee of a trust interposed between the first trust estate and the non‑resident trust;

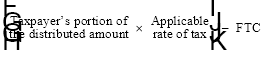

the trustee of the first trust estate is liable to pay interest to the Commissioner in respect of the taxpayer’s portion of the distributed amount of the non‑resident trust’s year of income, calculated under subsection (5), on the amount calculated using the formula:

where:

applicable rate of tax has the meaning given by subsection (10).

FTC [Foreign tax credit] means so much of any credit under Division 18 to which the trustee of the first trust would be entitled, in respect of the taxpayer’s portion of the distributed amount of the non‑resident trust’s year of income, if the taxpayer’s portion of the distributed amount of the non‑resident trust’s income were an amount in respect of which the trustee were liable to be assessed and to pay tax under section 99A.

taxpayer’s portion of the distributed amount means the taxpayer’s portion of the distributed amount of the non‑resident trust’s year of income.

9 At the end of subparagraph 102AAU(1)(c)(i)

Add:

(C) on which ultimate beneficiary non‑disclosure tax is payable under Division 6D; or

10 At the end of subsection 128B(3)

Add:

; or (l) income derived by a trustee that, because of paragraph 102UK(2)(b) or 102UM(2)(b), is not included in the assessable income of a trustee beneficiary of the trust estate.

11 Subsection 170(10)

After “section 100A,”, insert “Subdivision C of Division 6D of Part III, section”.

12 Application

(1) The amendments made by items 1 to 7 and 9 apply to ultimate beneficiary non‑disclosure tax that becomes payable at any time after the commencement of this Part.

(2) The amendment made by item 8 applies to net income of a trust estate of the year of income in which 13 August 1998 occurred, and all later years of income.

(3) The amendment made by item 10 applies to income derived either before or after the commencement of this Part.

Part 2—Income Tax Assessment Act 1997

13 After paragraph 42‑295(3)(b)

Insert:

(ba) you are the trustee of a trust, ultimate beneficiary non‑disclosure tax is payable under Division 6D of Part III of that Act (provisions relating to certain closely held trusts) on the whole or a part of a share of the net income of the trust and the amount mentioned in paragraph (2)(b) is included in that whole or part; or

14 Application

The amendment made by this Part applies to assessments for the income year in which 13 August 1998 occurred, and all later income years.

Part 3—Superannuation Contributions Tax (Assessment and Collection) Act 1997

15 Section 43 (paragraph (aa) of the definition of adjusted taxable income)

Omit “subsection 271‑105(1) of Schedule 2F to”, substitute “paragraphs 102UK(2)(b) and 102UM(2)(b) of, and subsection 271‑105(1) of Schedule 2F to,”.

16 Application

The amendment made by this Part applies to the calculation of adjusted taxable income for the financial year that began on 1 July 1998 or a later financial year.

[Minister’s second reading speech made in—

House of Representatives on 13 May 1999

Senate on 21 June 1999]

(84/99)