A New Tax System (Family Assistance) Act 1999

No. 80, 1999

A New Tax System (Family Assistance) Act 1999

No. 80, 1999

A New Tax System (Family Assistance) Act 1999

No. 80, 1999

An Act to implement A New Tax System by providing assistance to families, and for related purposes

Contents

Part 1—Preliminary

1 Short title...................................

2 Commencement...............................

Part 2—Interpretation

Division 1—Definitions

3 Definitions..................................

Division 2—Immunisation rules

4 Minister’s power to make determinations for the purposes of the definition of immunised

5 Meaning of conscientious objection

6 Immunisation requirements........................

7 Minister may make determinations in relation to the immunisation requirements

Division 3—Various interpretative provisions

8 Extended meaning of Australian resident—hardship and special circumstances

9 Session of care................................

10 Effect of absence of child from care of approved child care service.

11 Minister may make determinations in relation to the absence of child from child care

12 Effect of absence of child from care of registered carer........

13 School holidays...............................

14 Meaning of satisfies the work/training/study test

15 Work/training/study test—recognised work or work related commitments

16 Work/training/study test—recognised training commitments.....

17 Work/training/study test—recognised study commitments......

18 Meaning of school child

19 Maintenance income............................

Division 4—Approved care organisations

20 Approval of organisations providing residential care services to young people

Part 3—Eligibility for family assistance

Division 1—Eligibility for family tax benefit

Subdivision A—Eligibility of individuals for family tax benefit in normal circumstances

21 When an individual is eligible for family tax benefit in normal circumstances

22 When an individual is an FTB child of another individual.......

23 Effect of FTB child ceasing to be in individual’s care without consent

24 Effect of certain absences of FTB child etc. from Australia......

25 Effect of FTB child being in individual’s care for less than 10% of a period

26 Only 1 member of a couple eligible for family tax benefit.......

27 Extension of meaning of FTB child in a blended family case.....

28 Eligibility for family tax benefit of members of a couple in a blended family

29 Eligibility for family tax benefit of separated members of a couple for period before separation

30 Only 1 individual eligible for family tax benefit at the same time..

Subdivision B—Eligibility of individuals for family tax benefit where death occurs

31 Continued eligibility for family tax benefit if an FTB child dies...

32 Eligibility for a single amount of family tax benefit if an FTB child dies

33 Eligibility for family tax benefit if an eligible individual dies.....

Subdivision C—Eligibility of approved care organisations for family tax benefit

34 When an approved care organisation is eligible for family tax benefit

35 When an approved care organisation is not eligible for family tax benefit

Division 2—Eligibility for maternity allowance

Subdivision A—Eligibility of individuals for maternity allowance in normal circumstances

36 When an individual is eligible for maternity allowance in normal circumstances

37 Only one individual eligible for maternity allowance in respect of a child

Subdivision B—Eligibility of individuals for maternity allowance where death occurs

38 What happens if an individual eligible for maternity allowance dies.

Division 3—Eligibility for maternity immunisation allowance

Subdivision A—Eligibility of individuals for maternity immunisation allowance in normal circumstances

39 When an individual is eligible for maternity immunisation allowance in normal circumstances

Subdivision B—Eligibility of individuals for maternity immunisation allowance where death occurs

40 What happens if an individual eligible for maternity immunisation allowance dies

Division 4—Eligibility for child care benefit

Subdivision A—Eligibility for child care benefit by instalment for care provided by approved child care service in normal circumstances

41 When an individual is conditionally eligible for child care benefit by instalment to an approved child care service

42 When an individual is eligible for child care benefit by instalment to an approved child care service

Subdivision B—Eligibility for child care benefit for past periods for care provided by approved child care service in normal circumstances

43 When an individual is eligible for child care benefit..........

44 Individual not eligible for child care benefit if service eligible under Subdivision C

Subdivision C—Eligibility for child care benefit for care provided by approved child care service in special circumstances

45 When an approved child care service is eligible for child care benefit for an initial 13 week period

46 When an approved child care service is conditionally eligible for child care benefit by instalment

47 When an approved child care service is eligible for child care benefit by instalment

48 Minister’s determinations..........................

Subdivision D—Eligibility for child care benefit for past periods of care provided by registered carers

49 When an individual is eligible for child care benefit..........

Subdivision E—Limitations on eligibility for child care benefit

50 No multiple eligibility for same care...................

51 Person not eligible for child care benefit if child in care under a welfare law or child in exempt class of children

52 When eligibility for child care benefit for care provided by an approved child care service is limited to 20 hours per week

53 Determinations for the purposes of section 52..............

54 When eligibility for child care benefit for care provided by an approved child care service limited to 50 hours per week

55 Determinations for the purposes of section 54..............

56 Rules about the making of determinations under sections 52 to 55..

Subdivision F—Eligibility for child care benefit where death occurs

57 Eligibility for child care benefit if an eligible individual dies.....

Part 4—Rate of family assistance

Division 1—Family tax benefit

58 Rate of family tax benefit..........................

59 Secretary may make determination where individual is FTB child of 2 people who are not members of the same couple

60 Sharing family tax benefit between members of a couple in a blended family

61 Sharing family tax benefit between separated members of a couple for period before separation

62 Effect on individual’s rate of the individual’s absence from Australia

63 Effect on family tax benefit rate of FTB child’s absence from Australia

64 Calculation of rate of family tax benefit for death of FTB child...

65 Calculation of single amount for death of FTB child..........

Division 2—Maternity allowance

66 Amount of maternity allowance......................

Division 3—Maternity immunisation allowance

67 Amount of maternity immunisation allowance.............

68 When the maternity immunisation allowance is shared........

Division 4—Child care benefit

Subdivision A—Care provided by approved child care service

69 Application of Subdivision to parts of sessions of care.........

70 Rate of child care benefit for care provided by approved child care service

71 Rate of child care benefit in special circumstances...........

72 Weekly limit on benefit for care provided by approved child care service

Subdivision B—Care provided by registered carer

73 Rate of child care benefit for care provided by registered carer....

74 Weekly limit on benefit for care provided by registered carer.....

Division 5—Indexation

75 Indexation of amounts used in rate calculations.............

Schedule 1—Family Tax Benefit Rate Calculator

Part 1—Overall rate calculation process

1 Overall rate calculation process......................

2 Higher income free area..........................

Part 2—Part A rate (Method 1)

Division 1—Overall rate calculation process

3 Method of calculating Part A rate.....................

4 Base rate...................................

5 Family tax benefit advance to individual.................

6 Family tax benefit advance to partner...................

Division 2—Standard rate

7 Standard rate.................................

8 Base FTB child rate.............................

9 FTB child rate—recipient of other periodic payments.........

10 Effect of maintenance rights........................

11 Sharing family tax benefit (determination under subsection 59(1))..

Division 3—Rent assistance

12 Rent assistance children..........................

13 Eligibility for rent assistance........................

14 Rate of rent assistance............................

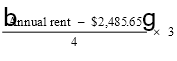

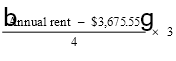

15 Annual rent..................................

16 Rent paid by a member of a couple....................

Division 4—Income test

17 Application of income test to pension and benefit recipients and their partners

18 Income test..................................

19 Income free area...............................

Division 5—Maintenance income test

20 Effect of maintenance income on family tax benefit rate.......

21 Maintenance income of members of couple to be added........

22 How to calculate an individual’s maintenance income free area...

23 Only maintenance actually received taken into account in applying clause 22

24 Apportionment of capitalised maintenance income...........

Part 3—Part A rate (Method 2)

Division 1—Overall rate calculation process

25 Method of calculating Part A rate.....................

Division 2—Standard rate

26 Standard rate.................................

27 Sharing family tax benefit (determination under subsection 59(1))..

Division 3—Income test

28 Income test..................................

Part 4—Part B rate

Division 1—Overall rate calculation process

29 Method of calculating Part B rate.....................

Division 2—Standard rate

30 Standard rate.................................

31 Sharing family tax benefit (determination under subsection 59(1))..

Division 3—Income test

32 Income test..................................

33 Income free area...............................

Part 5—Common provisions

Division 1—Large family supplement

34 Eligibility for large family supplement..................

35 Rate of large family supplement......................

Division 2—Multiple birth allowance

36 Eligibility for multiple birth allowance..................

37 Rate of multiple birth allowance......................

38 Sharing multiple birth allowance between 2 people (determination under subsection 59(1))

Schedule 2—Child care benefit rate calculator

Part 1—Overall rate calculation process

1 Method of calculating rate of child care benefit.............

2 Adjustment percentage...........................

3 Number of children in care of a particular kind.............

Part 2—Standard hourly rate

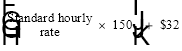

4 Standard hourly rate—basic meaning...................

Part 3—Multiple child %

5 Multiple child %...............................

Part 4—Taxable income %

6 Income thresholds..............................

7 Method of calculating taxable income %.................

8 Taxable income % if adjusted taxable income exceeds lower income threshold and if neither individual nor partner on income support

9 Income threshold..............................

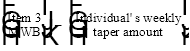

10 Taper %....................................

11 Maximum weekly benefit.........................

12 Minimum taxable income %........................

Schedule 3—Adjusted taxable income

1 Adjusted taxable income relevant to family tax benefit and child care benefit

2 Adjusted taxable income..........................

3 Adjusted taxable income of members of couple.............

4 Adjusted fringe benefits total.......................

5 Target foreign income............................

6 Net rental property loss...........................

7 Tax free pension or benefit.........................

8 Deductible child maintenance expenditure................

Schedule 4—Indexation and adjustment of amounts

Part 1—Preliminary

1 Analysis of Schedule............................

2 Indexed and adjusted amounts.......................

Part 2—Indexation

3 CPI Indexation Table............................

4 Indexation of amounts...........................

5 Indexation factor...............................

6 Rounding off indexed amounts......................

Part 3—Adjustment of other rates

7 Adjustment of FTB child rates.......................

Part 4—Transitional indexation provision

8 Transitional indexation of amounts used to calculate family assistance rates

A New Tax System (Family Assistance) Act 1999

No. 80, 1999

An Act to implement A New Tax System by providing assistance to families, and for related purposes

[Assented to 8 July 1999]

The Parliament of Australia enacts:

This Act may be cited as the A New Tax System (Family Assistance) Act 1999.

(1) This Act commences, or is taken to have commenced:

(a) after all the provisions listed in subsection (2) have commenced; and

(b) on the last day on which any of those provisions commenced.

(2) These are the provisions:

(a) section 1‑2 of the A New Tax System (Goods and Services Tax) Act 1999;

(b) section 2 of the A New Tax System (Goods and Services Tax Imposition—Excise) Act 1999;

(c) section 2 of the A New Tax System (Goods and Services Tax Imposition—Customs) Act 1999;

(d) section 2 of the A New Tax System (Goods and Services Tax Imposition—General) Act 1999;

(e) section 2 of the A New Tax System (Goods and Services Tax Administration) Act 1999.

(1) In this Act, unless the contrary intention appears:

absence, in relation to care provided for a child by an approved child care service, does not include any period of absence:

(a) before the service has started providing care for the child; or

(b) after the service has stopped providing care for the child (otherwise than temporarily).

adjusted taxable income has the meaning given by Schedule 3.

aged care resident has the same meaning as in the Social Security Act 1991.

amount of rent paid or payable has the same meaning as in the Social Security Act 1991.

approved care organisation means an organisation approved by the Secretary under section 20.

Australian Immunisation Handbook means the latest edition of the Australian Immunisation Handbook published by the Australian Government Publishing Service.

Australian resident has the same meaning as in the Social Security Act 1991.

authorised party, in relation to the adoption of a child, means a person or agency that, under the law of the State, Territory or foreign country whose courts have jurisdiction in respect of the adoption, is authorised to conduct negotiations or arrangements for the adoption of children.

base FTB child rate, in relation to an FTB child of an individual whose Part A rate of family tax benefit is being worked out using Part 2 of Schedule 1, has the meaning given by clause 8 of that Schedule.

base rate, in relation to an individual whose Part A rate of family tax benefit is being worked out using Part 2 of Schedule 1, has the meaning given by clause 4 of that Schedule.

benefit received by an individual has a meaning affected by paragraph 19(2)(b).

capitalised maintenance income, in relation to an individual, means maintenance income of the individual:

(a) that is neither a periodic amount nor a benefit provided on a periodic basis; and

(b) the amount or value of which exceeds $1,500.

child care benefit means the benefit for which a person is eligible under Division 4 of Part 3.

child support means financial support under the Child Support (Assessment) Act 1989 and includes financial support:

(a) by way of lump sum payment; or

(b) by way of transfer or settlement of property.

conscientious objection, in relation to the immunisation of a child, has the meaning given by section 5.

CPC rate has the same meaning as in the Social Security Act 1991.

current figure, as at a particular time and in relation to an amount that is to be indexed or adjusted under Schedule 4, means:

(a) if the amount has not yet been indexed or adjusted under Schedule 4 before that time—the amount; and

(b) if the amount has been indexed or adjusted under Schedule 4 before that time—the amount most recently substituted for the amount under Schedule 4 before that time.

disability expenses maintenance has the meaning given by subsection 19(3).

family assistance means:

(a) family tax benefit; or

(b) maternity allowance; or

(c) maternity immunisation allowance; or

(d) child care benefit.

family law order means:

(a) a parenting order within the meaning of section 64B of the Family Law Act 1975; or

(b) a family violence order within the meaning of section 60D of that Act; or

(c) a State child order registered under section 70D of that Act; or

(d) an overseas child order registered under section 70G of that Act.

family member, in relation to an individual, means:

(a) the partner, father or mother of the individual; or

(b) a sister, brother or child (including an adopted child) of the individual.

family tax benefit means the benefit for which a person is eligible under Division 1 of Part 3.

FTB advance rate, in relation to an individual whose Part A rate of family tax benefit is being worked out using Part 2 of Schedule 1, means half the amount that would be the FTB child rate for an FTB child who has not turned 18 under clause 26 of that Schedule if:

(a) the person’s Part A rate were to be worked out using Part 3 of that Schedule; and

(b) clause 27 of that Schedule did not apply.

FTB child has the meaning given by Subdivision A of Division 1 of Part 3.

illness separated couple has the same meaning as in the Social Security Act 1991.

immunised, in relation to a child, means the child is immunised in accordance with:

(a) a standard vaccination schedule determined under section 4; or

(b) a catch up vaccination schedule determined under section 4.

Income Tax Assessment Act means the Income Tax Assessment Act 1997.

income year has the same meaning as in the Income Tax Assessment Act.

index number has the same meaning as in the Social Security Act 1991.

ineligible homeowner has the same meaning as in the Social Security Act 1991.

lower income threshold for child care benefit has the meaning given by subclause 6(2) of Schedule 2.

maintenance includes child support.

maintenance agreement means a written agreement (whether made within or outside Australia) that provides for the maintenance of a person (whether or not it also makes provision in relation to other matters), and includes such an agreement that varies an earlier maintenance agreement.

maintenance income, in relation to an individual, means:

(a) child maintenance—that is, the amount of a payment or the value of a benefit that is received by the individual for the maintenance of an FTB child of the individual and is received from:

(i) a parent of the child; or

(ii) the partner or former partner of a parent of the child; or

(b) partner maintenance—that is, the amount of a payment or the value of a benefit that is received by the individual for the individual’s own maintenance and is received from the individual’s partner or former partner; or

(c) direct child maintenance—that is, the amount of a payment or the value of a benefit that is received by an FTB child of the individual for the child’s own maintenance and is received from:

(i) a parent of the child; or

(ii) the partner or former partner of a parent of the child;

but does not include disability expenses maintenance.

maternity allowance means the allowance for which an individual is eligible under Division 2 of Part 3.

maternity immunisation allowance means the allowance for which an individual is eligible under Division 3 of Part 3.

medical practitioner means a person registered or licensed as a medical practitioner under a State or Territory law that provides for the registration or licensing of medical practitioners.

meets the immunisation requirements has the meaning given by section 6.

member of a couple has the same meaning as in the Social Security Act 1991.

non‑standard hours family day care means hours of care provided by a family day care service at times that are identified in the service’s conditions of approval as being non‑standard hours of the service.

partner has the same meaning as in the Social Security Act 1991.

part‑time family day care means standard hours family day care provided by a family day care service for a child in a week during which the service provides a total of less than 50 hours of standard hours family day care for the child.

payment or benefit received from an individual has a meaning affected by paragraph 19(2)(c).

prescribed educational scheme has the same meaning as in the Social Security Act 1991.

principal home has the same meaning as in the Social Security Act 1991.

received from has a meaning affected by paragraph 19(2)(a).

receiving, in relation to a social security payment, has the same meaning as in the Social Security Act 1991.

recognised immunisation provider has the same meaning as in section 46A of the Health Insurance Act 1973.

recognised study commitments has the meaning given by section 17.

recognised training commitments has the meaning given by section 16.

recognised work or work related commitments has the meaning given by section 15.

registered parenting plan means a parenting plan registered under section 63E of the Family Law Act 1975.

rent has the same meaning as in the Social Security Act 1991.

rent assistance child has the meaning given by subclause 12(2) of Schedule 1.

respite care couple has the same meaning as in the Social Security Act 1991.

satisfies the work/training/study test has the meaning given by section 14.

school child has the meaning given by section 18.

school holiday session means a session of care provided by an outside school hours care service during school holidays.

service pension has the same meaning as in the Social Security Act 1991.

session of care has the meaning given by a determination in force under section 9.

social security benefit has the same meaning as in the Social Security Act 1991.

social security payment has the same meaning as in the Social Security Act 1991.

social security pension has the same meaning as in the Social Security Act 1991.

standard advance period means:

(a) a period that starts on 1 January and ends on the following 30 June; or

(b) a period that starts on 1 July and ends on the following 31 December.

standard hours family day care means hours of care provided by a family day care service at times that are identified in the service’s conditions of approval as being standard hours of care.

stillborn child means a child:

(a) who weighs at least 400 grams at delivery or whose period of gestation was at least 20 weeks; and

(b) who has not breathed since delivery; and

(c) whose heart has not beaten since delivery.

taxable income has the same meaning as in the Income Tax Assessment Act.

temporarily separated couple has the same meaning as in the Social Security Act 1991.

undertaking full‑time study has the same meaning as in the Social Security Act 1991.

upper income threshold for child care benefit has the meaning given by subclause 6(3) of Schedule 2.

week concerned for an hour of care is the week (beginning on a Monday) in which the hour occurs.

youth allowance means a payment under Part 2.11 of the Social Security Act 1991.

(2) Expressions used in this Act that are defined in the A New Tax System (Family Assistance) (Administration) Act 1999 have the same meaning as in that Act.

4 Minister’s power to make determinations for the purposes of the definition of immunised

(1) The Minister must, for the purpose of the definition of immunised in section 3, determine:

(a) one or more standard vaccination schedules for the immunisation of children; and

(b) one or more catch up vaccination schedules for the immunisation of children who have not been immunised in accordance with a standard vaccination schedule.

(2) A determination under this section is a disallowable instrument for the purposes of section 46A of the Acts Interpretation Act 1901.

5 Meaning of conscientious objection

An individual has a conscientious objection to a child being immunised if the individual’s objection is based on a personal, philosophical, religious or medical belief involving a conviction that vaccination under the latest edition of the standard vaccination schedule should not take place.

(1) This section states when the child of an individual (the adult) meets the immunisation requirements for the purposes of determining whether the adult is eligible for:

(a) maternity immunisation allowance under Division 3 of Part 3; or

(b) child care benefit under Division 4 of Part 3.

Child immunised

(2) The child meets the immunisation requirements if the child has been immunised.

Conscientious objection

(3) The child meets the immunisation requirements if a recognised immunisation provider has certified in writing that he or she has discussed with the adult the benefits and risks of immunising the child and the adult has declared in writing that he or she has a conscientious objection to the child being immunised.

(4) The child meets the immunisation requirements if:

(a) the child is an FTB child of another individual (whether or not the child is also an FTB child of the adult); and

(b) a recognised immunisation provider has certified in writing that he or she has discussed with the other individual the benefits and risks of immunising the child and the other individual has declared in writing that he or she has a conscientious objection to the child being immunised.

Medical contraindication

(5) The child meets the immunisation requirements if a recognised immunisation provider has certified in writing that the immunisation of the child would be medically contraindicated under the specifications set out in the Australian Immunisation Handbook.

Natural immunity

(6) The child meets the immunisation requirements if a medical practitioner has certified in writing that the child does not require immunisation because the child has contracted a disease or diseases and as a result has developed a natural immunity.

Child is in an exempt class of children

(7) The child meets the immunisation requirements if the child is in a class exempted from the requirement to be immunised by a determination under subsection 7(1).

Other circumstances

(8) The child meets the immunisation requirements if a determination in force under subsection 7(2) provides that the child meets the immunisation requirements.

7 Minister may make determinations in relation to the immunisation requirements

Exemption from immunisation requirements

(1) The Minister may determine that children included in a specified class are exempt from the requirement to be immunised.

Meeting the immunisation requirements

(2) The Minister may determine that children included in a specified class meet the immunisation requirements in circumstances specified in the determination.

Disallowable instrument

(3) A determination under this section is a disallowable instrument for the purposes of section 46A of the Acts Interpretation Act 1901.

Division 3—Various interpretative provisions

8 Extended meaning of Australian resident—hardship and special circumstances

(1) The Secretary may determine that an individual who is not an Australian resident is taken to be an Australian resident for the purposes of Division 4 of Part 3 (eligibility for child care benefit).

(2) The Secretary may make a determination under subsection (1) if the Secretary is satisfied that:

(a) hardship would be caused to the individual if the individual were not treated as an Australian resident; or

(b) because of the special circumstances of the particular case, the individual should be treated as an Australian resident.

(3) In making a determination under subsection (1), the Secretary must comply with any guidelines in force under subsection (4) in relation to the making of such determinations.

(4) The Minister may make guidelines relating to the making of determinations under subsection (1).

(5) Guidelines under subsection (4) are disallowable instruments for the purposes of section 46A of the Acts Interpretation Act 1901.

(1) The Minister must determine what constitutes a session of care for the purposes of this Act.

(2) A determination under subsection (1) may also deal with how a session of care that starts on one day and ends on another day is to be treated for the purposes of this Act.

(3) A determination under this section is a disallowable instrument for the purposes of section 46A of the Acts Interpretation Act 1901.

10 Effect of absence of child from care of approved child care service

Absence from part of a session

(1) For the purposes of this Act, if a child is absent from part only of a session of care provided by an approved child care service, the service is taken to have provided that part of the session of care to the child.

Absence from all of a session provided by an occasional care service

(2) For the purposes of this Act, if:

(a) a child is absent from all of a session of care that would otherwise have been provided to the child by an occasional care service; and

(b) the absence occurs in circumstances specified in a determination under subsection 11(1) as permitted circumstances for the purpose of this subsection;

the service is taken to have provided the session of care to the child.

Absence from all of a session provided by other services

(3) For the purposes of this Act, if:

(a) a child is absent from all of a session of care that would otherwise have been provided to the child by an approved child care service (except an occasional care service); and

(b) one of the following applies:

(i) the absence is due to the illness of the child, the individual in whose care the child is, that individual’s partner, or another individual with whom the child lives and a medical certificate covering that illness is obtained from a medical practitioner and given to the service;

(ii) the absence is due to the child’s attendance at a pre‑school;

(iii) the absence is due to alternative care arrangements being made for the child because the child does not have to be at school on a pupil‑free day;

(iv) the absence occurs in circumstances specified in a determination under subsection 11(1) as permitted circumstances for the purpose of this subparagraph;

(v) the absence occurs on a permitted absence day (see subsection (4));

the service is taken to have provided the session of care to the child.

Permitted absence days

(4) For the purposes of subparagraph (3)(b)(v), a permitted absence day is a day that meets the following requirements:

(a) the child is absent from all of one or more sessions of care provided by the approved child care service on the day (even if the child is not absent from some or all of another session or sessions of care provided by the service or another service on the day);

(b) the child’s absence from all of the one or more sessions of care is not covered by subparagraph (3)(b)(i), (ii), (iii) or (iv);

(c) before the day, not more than 30 permitted absence days in relation to the service and the child have elapsed in the same calendar year.

11 Minister may make determinations in relation to the absence of child from child care

Absences from care in permitted circumstances

(1) The Minister may determine that specified circumstances are permitted circumstances for the purpose of subsection 10(2) or subparagraph 10(3)(b)(iv).

Disallowable instrument

(2) A determination under this section is a disallowable instrument for the purposes of section 46A of the Acts Interpretation Act 1901.

12 Effect of absence of child from care of registered carer

For the purposes of Subdivision D of Division 4 of Part 3, and of the application of Subdivision B of Division 4 of Part 4 in relation to that Subdivision, if a child is absent from all or part of a period of care that would otherwise have been provided to the child by a registered carer, the carer is taken to have provided care to the child during the period of absence.

The Secretary may, by notice given to an outside school hours care service, determine that a specified day or days that are not school holidays in the State or Territory in which the service is located are taken to be school holidays for the purposes of the definition of school holiday session in section 3.

14 Meaning of satisfies the work/training/study test

(1) An individual satisfies the work/training/study test if:

(a) the individual has recognised work or work related commitments; or

(b) the individual has recognised training commitments; or

(c) the individual has recognised study commitments.

(2) The Minister may determine that individuals included in a specified class are exempt from the requirements of paragraphs (1)(a), (b) and (c).

(3) An individual covered by a determination under subsection (2) is taken to satisfy the work/training/study test while the determination is in force.

(4) A determination under this section is a disallowable instrument for the purposes of section 46A of the Acts Interpretation Act 1901.

15 Work/training/study test—recognised work or work related commitments

(1) An individual has recognised work or work related commitments if the individual:

(a) is in paid work (whether or not the individual performs the work as an employee); or

(b) receives a carer payment under Part 2.5 of the Social Security Act 1991; or

(c) receives carer allowance for a disabled adult (within the meaning of section 952 of the Social Security Act 1991) under Part 2.19 of that Act.

(2) The Minister may determine that individuals included in a specified class are individuals who are taken to have recognised work or work related commitments for the purposes of this section.

(3) A determination under this section is a disallowable instrument for the purposes of section 46A of the Acts Interpretation Act 1901.

16 Work/training/study test—recognised training commitments

An individual has recognised training commitments if the individual is undertaking a training course for the purpose of improving his or her work skills and/or employment prospects.

17 Work/training/study test—recognised study commitments

An individual has recognised study commitments if the individual:

(a) receives youth allowance and is undertaking full‑time study; or

(b) receives austudy payment under the Social Security Act 1991; or

(c) receives a pensioner education supplement under the Social Security Act 1991; or

(d) receives assistance under the scheme known as the ABSTUDY scheme; or

(e) is undertaking any other course of education for the purposes of improving his or her work skills and/or employment prospects.

(1) A child is a school child for the purposes of this Act if the child is attending primary or secondary school, or is on a break from school (for example, school holidays) and will be attending primary or secondary school after that break.

(2) The Minister may determine that children in a specified class are to be treated as though they were attending primary or secondary school for the purposes of this Act.

(3) The Minister may determine that children in a specified class are to be treated as though they were not attending primary or secondary school for the purposes of this Act.

(4) A determination under subsection (2) or (3) is a disallowable instrument for the purposes of section 46A of the Acts Interpretation Act 1901.

(1) For the purposes of the definition of capitalised maintenance income in section 3, an amount is a periodic amount if it is:

(a) the amount of one payment in a series of related payments, even if the payments are irregular in time and amount; or

(b) the amount of a payment making up for arrears in such a series.

(2) For the purposes of the definitions of maintenance income and disability expenses maintenance in section 3:

(a) a payment received under subsection 76(1) of the Child Support (Registration and Collection) Act 1988 in relation to a registered maintenance liability (within the meaning of that Act) is taken to be received from the individual who is the payer (within the meaning of that Act) in relation to the liability; and

(b) a reference to a benefit received by an individual includes a reference to a benefit received by the individual because of a payment made to, or a benefit conferred on, another individual (including a payment made or benefit conferred under a liability owed to the other individual); and

(c) a reference to a payment or benefit received from an individual includes a reference to a payment or benefit received:

(i) directly or indirectly from the individual; and

(ii) out of any assets of, under the control of, or held for the benefit of, the individual; and

(iii) from the individual under or as a result of a court order, a court registered or approved maintenance agreement or otherwise.

(3) A payment or benefit is disability expenses maintenance of an individual if:

(a) the payment or benefit is provided for expenses arising directly from:

(i) a physical, intellectual or psychiatric disability; or

(ii) a learning difficulty;

of an FTB child of the individual; and

(b) the disability or difficulty is likely to be permanent or to last for an extended period; and

(c) the payment or benefit is received:

(i) by the individual for the maintenance of the FTB child; or

(ii) by the FTB child for the child’s own maintenance; and

(d) the payment or benefit is received from:

(i) a parent of the child; or

(ii) the partner or former partner of a parent of the child.

Division 4—Approved care organisations

20 Approval of organisations providing residential care services to young people

(1) The Secretary may approve an organisation that co‑ordinates or provides residential care services to young people in Australia as an approved care organisation for the purposes of this Act.

Revocation

(2) The Secretary may revoke an approval under subsection (1).

Part 3—Eligibility for family assistance

Division 1—Eligibility for family tax benefit

Subdivision A—Eligibility of individuals for family tax benefit in normal circumstances

21 When an individual is eligible for family tax benefit in normal circumstances

(1) An individual is eligible for family tax benefit if:

(a) the individual has at least 1 FTB child (see section 22 and later provisions); and

(b) the individual is an Australian resident; and

(c) the individual’s rate of family tax benefit, worked out under Division 1 of Part 4, is greater than nil.

(2) However, the individual is not eligible for family tax benefit if another provision of this Subdivision so provides.

22 When an individual is an FTB child of another individual

(1) An individual is an FTB child of another individual (the adult) in any of the cases set out in this section.

Individual aged under 18

(2) The individual is an FTB child of the adult if:

(a) the individual is aged under 18; and

(b) the adult is legally responsible (whether alone or jointly with someone else) for the day‑to‑day care, welfare and development of the individual; and

(c) the individual is in the adult’s care; and

(d) the individual is an Australian resident or is living with the adult.

(3) The individual is an FTB child of the adult if:

(a) the individual is aged under 18; and

(b) a family law order or registered parenting plan is in force in relation to the individual; and

(c) under the order or plan, the adult is someone with whom the individual is supposed to live or someone with whom the individual is supposed to have contact; and

(d) the individual is in the adult’s care; and

(e) the individual is an Australian resident or is living with the adult.

While the individual is an FTB child of the adult under this subsection, the individual cannot be an FTB child of anyone else.

(4) The individual is an FTB child of the adult if:

(a) the individual is aged under 18; and

(b) the individual is in the adult’s care; and

(c) the individual is not in the care of anyone with the legal responsibility for the day‑to‑day care, welfare and development of the individual; and

(d) the individual is an Australian resident or is living with the adult.

Individual aged 18-20

(5) The individual is an FTB child of the adult if:

(a) the individual has turned 18 but is aged under 21; and

(b) the individual is in the adult’s care; and

(c) the individual is an Australian resident or is living with the adult.

Individual aged 21‑24 undertaking full‑time study

(6) The individual is an FTB child of the adult if:

(a) the individual has turned 21 but is aged under 25; and

(b) the individual is in the adult’s care; and

(c) the individual is an Australian resident or is living with the adult; and

(d) the individual is undertaking full‑time study.

Exceptions

(7) However, the individual cannot be an FTB child of the adult in the cases set out in this table:

When the individual is not an FTB child of the adult at a particular time | ||

| If the individual is aged: | then the individual cannot be an FTB child of the adult if: |

1 | 5 or more and less than 16 | (a) the individual is not undertaking full‑time study and the individual has adjusted taxable income, for the income year in which the particular time occurs, that equals or exceeds the cut‑out amount (see subsection (8)); or (b) the adult is the individual’s partner |

2 | 16 or more | (a) the individual has adjusted taxable income, for the income year in which the particular time occurs, that equals or exceeds the cut-out amount (see subsection (8)); or (b) the adult is the individual’s partner |

3 | any age | the individual, or someone on behalf of the individual, is at the particular time receiving: (a) a social security pension; or (b) a social security benefit; or (c) payments under a program included in the programs known as Labour Market Programs; or (d) payments under a prescribed educational scheme |

Definition

(8) In subsection (7):

cut‑out amount means the sum of:

(a) the amount specified in column 2 of item 2 of the table in clause 30 of Schedule 1 divided by 0.3; and

(b) the amount specified in clause 33 of that Schedule.

23 Effect of FTB child ceasing to be in individual’s care without consent

(1) This section applies if:

(a) an individual is an FTB child of another individual (the adult) under subsection 22(2) or (3); and

(b) an event occurs in relation to the child without the adult’s consent that prevents the child being in the adult’s care; and

(c) the adult takes reasonable steps to have the child again in the adult’s care.

When the child remains an FTB child of the adult

(2) The child is an FTB child of the adult for that part of the qualifying period (see subsection (5)) for which the child would have been an FTB child of the adult under subsection 22(2) or (3) if the child had not ceased to be in the adult’s care.

When the child is an FTB child of another individual

(3) If the child would have been an FTB child of any other individual under subsection 22(2) or (3) during any part of the qualifying period if the event had not occurred, the child is an FTB child of the other individual.

(4) Except as provided in subsection (2) or (3), the child cannot (in spite of section 22) be an FTB child of any individual during the qualifying period.

Definition of qualifying period

(5) In this section:

qualifying period means the period beginning when the child ceases to be in the adult’s care and ending at the earliest of the following times:

(a) if the child again comes into the adult’s care at a later time—that later time;

(b) after 14 weeks pass since the child ceased to be in the adult’s care;

(c) if:

(i) the adult is a parent of the child; and

(ii) no family law order or registered parenting plan is in force in relation to the child; and

(iii) the child comes into the care of the other parent at a later time;

that later time.

24 Effect of certain absences of FTB child etc. from Australia

Absence from Australia of FTB child

(1) If:

(a) either:

(i) an FTB child leaves Australia; or

(ii) a child born outside Australia is an FTB child at birth; and

(b) the child continues to be absent from Australia for more than 3 years;

the child is not, during that absence from Australia, an FTB child at any time after the period of 3 years beginning on the first day of the child’s absence from Australia.

(2) If:

(a) an FTB child who has been absent from Australia for more than 26 weeks, but less than 3 years, comes to Australia; and

(b) the child leaves Australia less than 26 weeks later;

for the purposes of subsection (1), the child is taken not to have come to Australia.

(3) If:

(a) a child is not an FTB child because of the application of subsection (1) or a previous application of this subsection; and

(b) the child comes to Australia; and

(c) the child leaves Australia less than 26 weeks after coming to Australia;

the child is not an FTB child at any time during the absence from Australia referred to in paragraph (c).

Maximum period of eligibility for family tax benefit while individual overseas

(4) If an individual leaves Australia, the maximum period for which the individual can be eligible for family tax benefit during that absence from Australia is the period of 3 years beginning on the first day of that absence.

(5) If:

(a) an individual who has been absent from Australia for more than 26 weeks, but less than 3 years, returns to Australia; and

(b) the child leaves Australia again less than 26 weeks later;

the child is taken not to have returned to Australia for the purposes of subsection (4).

(6) If:

(a) an individual is eligible for family tax benefit while the individual is absent from Australia; and

(b) the individual then ceases to be eligible for family tax benefit because of the application of subsection (4) or a previous application of this subsection; and

(c) the individual returns to Australia; and

(d) the individual leaves Australia again less than 26 weeks after returning to Australia;

the individual is not eligible for family tax benefit at any time during the absence from Australia referred to in paragraph (d).

25 Effect of FTB child being in individual’s care for less than 10% of a period

If:

(a) the Secretary is satisfied there has been, or will be, a pattern of care for an individual (the child) for a period in which the child was, or will be, an FTB child of 2 or more other individuals at different times during the period; and

(b) one of those other individuals (the adult) makes a claim under Part 3 of the A New Tax System (Family Assistance) (Administration) Act 1999 for payment of family tax benefit in respect of the child for some or all of that period; and

(c) the Secretary is satisfied the child was, or will be, in the adult’s care for less than 10% of that period;

then:

(d) the adult is not eligible for family tax benefit in respect of the child for any part of that period; and

(e) the Secretary may determine that another one of those individuals is eligible for family tax benefit in respect of the child for the part (if any) of that period during which the adult would have been eligible for family tax benefit in respect of the child apart from this section.

26 Only 1 member of a couple eligible for family tax benefit

(1) For any period when 2 individuals who are members of a couple would otherwise be eligible at the same time for family tax benefit in respect of one or more FTB children, only one member is eligible.

(2) The member who is eligible is the one determined by the Secretary to be eligible, having regard to:

(a) whether one member of the couple is the primary carer for the child or children; and

(b) whether the members have made a written agreement nominating one of them as the member who can make a claim under Part 3 of the A New Tax System (Family Assistance) (Administration) Act 1999 for payment of family tax benefit in respect of the child or children.

27 Extension of meaning of FTB child in a blended family case

If:

(a) 2 individuals are members of the same couple; and

(b) either or both of the individuals have a child (the qualifying child) from another relationship (whether before or after the 2 individuals became members of that couple);

each qualifying child that is an FTB child of one member of the couple while the 2 individuals are members of that couple is taken also to be an FTB child of the other member of the couple.

28 Eligibility for family tax benefit of members of a couple in a blended family

(1) If the Secretary is satisfied that:

(a) 2 individuals who are members of the same couple (person A and person B) would each be eligible for family tax benefit for 2 or more FTB children during a period but for subsection 26(1); and

(b) at least one of the children is a child of a previous relationship of person A; and

(c) at least one of the other children is:

(i) a child of the relationship between person A and person B; or

(ii) a child of a previous relationship of person B;

the Secretary may:

(d) determine that person A and person B are both eligible for family tax benefit for the children for the period; and

(e) determine person A’s and person B’s percentage of the family tax benefit for the children, such that each of those percentages is a multiple of 5%.

(2) The Secretary cannot make a determination under subsection (1) for a past period if person A or person B has been paid family tax benefit for the period.

(3) For the purposes of this section:

(a) an FTB child of an individual is a child of a previous relationship of an individual who is a member of a couple if the child is an immediate child of that individual but not of the individual’s partner; and

(b) a child is a child of the relationship of 2 individuals who are members of a couple if the child is an immediate child of both members of the couple; and

(c) an FTB child of an individual is an immediate child of the individual if:

(i) the child is the natural or adopted child of the individual; or

(ii) the individual is legally responsible for the child.

29 Eligibility for family tax benefit of separated members of a couple for period before separation

If the Secretary is satisfied that:

(a) 2 individuals are not members of the same couple (person A and person B); and

(b) during a period in the past when person A and person B were members of the same couple, they had an FTB child or children; and

(c) but for subsection 26(1), person A and person B would both be eligible for family tax benefit for the FTB child or children for that period;

the Secretary may:

(d) determine that person A and person B are both eligible for family tax benefit for the child or children for that period; and

(e) determine person A’s and person B’s percentage of the family tax benefit for the child or children for that period, such that each of those percentages is a multiple of 5%.

30 Only 1 individual eligible for family tax benefit at the same time

(1) If, apart from this section, 2 or more individuals (none of whom are members of the same couple and none of whom are living together) would, at the same time, be eligible for family tax benefit in respect of an FTB child, only one individual is eligible.

(2) The individual who is eligible is the one determined by the Secretary to be eligible, having regard to the living arrangements for the child.

Subdivision B—Eligibility of individuals for family tax benefit where death occurs

31 Continued eligibility for family tax benefit if an FTB child dies

(1) This section applies if:

(a) an individual is eligible for family tax benefit (except under section 33) in respect of one or more FTB children; and

(b) one of the FTB children dies; and

(c) in a case where the individual is eligible for family tax benefit in respect of more than one FTB child immediately before the child died—the individual’s rate of family tax benefit would decrease as a result of the child’s death.

Individual remains eligible for family tax benefit for 14 weeks after the death of the child

(2) The individual is eligible for family tax benefit, at a rate worked out under section 64, for each day in the period of 14 weeks beginning on the day the child died. This subsection has effect subject to subsection (3) of this section and to section 32.

14 weeks reduced in certain circumstances

(3) The period for which the individual is eligible for family tax benefit under subsection (2) does not include:

(a) if the child was undertaking full‑time study at the time the child died—any day on which the child would have been aged 25 if the child had not died; or

(b) in any other case—any day on which the child would have been aged 21 if the child had not died.

Eligibility during the period to which subsection (2) applies is sole eligibility

(4) Except as mentioned in subsection (2), the individual is not eligible for family tax benefit in respect of any FTB children of the individual during the period to which subsection (2) applies.

32 Eligibility for a single amount of family tax benefit if an FTB child dies

Instalment case

(1) If:

(a) the individual to whom section 31 applies was, immediately before the child concerned died, entitled to be paid family tax benefit by instalment; and

(b) the individual, on any day (the request day) during the period (the section 31 accrual period) for which the individual is eligible for family tax benefit under that section, makes a claim, under Part 3 of the A New Tax System (Family Assistance) (Administration) Act 1999, for payment of family tax benefit because of the death of a person, stating that the individual wishes to become eligible for a single amount of family tax benefit under this subsection;

then:

(c) the individual is eligible for a single amount of family tax benefit worked out under subsection 65(1); and

(d) the period for which the individual is eligible for family tax benefit under subsection 31(2) does not include the lump sum period mentioned in subsection 65(1).

Other cases

(2) If:

(a) the individual to whom section 31 applies was, immediately before the child concerned died, not entitled to be paid family tax benefit by instalment; and

(b) the period of 14 weeks beginning on the day the child died extends over 2 income years;

then:

(c) the individual is eligible for a single amount of family tax benefit for the period falling in the second of those income years worked out under subsection 65(3); and

(d) the period for which the individual is eligible for family tax benefit under subsection 31(2) does not include the period falling in the second of those income years.

33 Eligibility for family tax benefit if an eligible individual dies

Eligibility other than because of the death of an FTB child

(1) If:

(a) an individual is eligible for an amount (the subject amount) of family tax benefit (except because of section 31 or 32 applying in relation to the death of an FTB child); and

(b) the individual dies; and

(c) before the individual died, the subject amount had not been paid to the individual (whether or not a claim under Part 3 of the A New Tax System (Family Assistance) (Administration) Act 1999 had been made); and

(d) another individual makes a claim under that Part for payment of family tax benefit because of the death of a person, stating that he or she wishes to become eligible for the subject amount; and

(e) the Secretary considers that the other individual ought to be eligible for the subject amount;

the other individual is eligible for the subject amount and no‑one else is, or can become, eligible for or entitled to be paid that amount.

Eligibility because of the death of an FTB child

(2) If:

(a) an individual dies; and

(b) either:

(i) before the individual’s death, the individual was eligible for an amount (the subject amount) of family tax benefit under section 31 or 32 in relation to the death of an FTB child and the subject amount had not been paid to the individual (whether or not a claim under Part 3 of the A New Tax System (Family Assistance) (Administration) Act 1999 had been made); or

(ii) the individual died at the same time as the FTB child and would have been so eligible for the subject amount if the individual had not died; and

(c) another individual makes a claim under that Part for payment of family tax benefit because of the death of a person, stating that the individual wishes to become eligible for the subject amount; and

(d) the Secretary considers that the other individual ought to be eligible for the subject amount;

the other individual is eligible for the subject amount and no‑one else is, or can become, eligible for or entitled to be paid that amount.

Subdivision C—Eligibility of approved care organisations for family tax benefit

34 When an approved care organisation is eligible for family tax benefit

(1) An approved care organisation is eligible for family tax benefit in respect of an individual if:

(a) the individual:

(i) is aged under 21; or

(ii) is aged under 25 and is undertaking full‑time study; and

(b) the individual is a client of the organisation; and

(c) the individual is an Australian resident.

(2) However, an approved care organisation is not eligible for family tax benefit in respect of an individual in the cases set out in section 35.

Expanded meaning of client of an organisation

(3) For the purposes of paragraph (1)(b), if:

(a) an organisation that is not an approved care organisation is providing residential care services to young people in Australia; and

(b) an approved care organisation is co‑ordinating the provision of those services;

the young people are taken to be clients of the approved care organisation.

35 When an approved care organisation is not eligible for family tax benefit

(1) An approved care organisation is not eligible for family tax benefit in respect of an individual in the cases set out in this table:

When an approved care organisation is not eligible for family tax benefit at a particular time | ||

| If the individual is aged: | then the approved care organisation is not eligible for family tax benefit in respect of the individual if: |

1 | 5 or more and less than 16 | (a) the individual is not undertaking full‑time study; and (b) the individual has adjusted taxable income, for the income year in which the particular time occurs, that equals or exceeds the cut‑out amount (see subsection (3)) |

2 | 16 or more | the individual has adjusted taxable income, for the income year in which the particular time occurs, that equals or exceeds the cut-out amount (see subsection (3)) |

3 | any age | the individual, or someone on behalf of the individual, is at the particular time receiving: (a) a social security pension; or (b) a social security benefit; or (c) payments under a program included in the programs known as Labour Market Programs; or (d) payments under a prescribed educational scheme |

(2) An approved care organisation is also not eligible for family tax benefit in respect of an individual if anyone else is eligible for family tax benefit in respect of the individual.

Definition

(3) In subsection (1):

cut‑out amount means the sum of:

(a) the amount specified in column 2 of item 2 of the table in clause 30 of Schedule 1 divided by 0.3; and

(b) the amount specified in clause 33 of that Schedule.

Division 2—Eligibility for maternity allowance

Subdivision A—Eligibility of individuals for maternity allowance in normal circumstances

36 When an individual is eligible for maternity allowance in normal circumstances

(1) An individual is eligible for maternity allowance in respect of a child in any of the 4 cases set out in this section.

Parent of child

(2) First, an individual is eligible for maternity allowance in respect of a child if:

(a) the individual is a parent of the child; and

(b) the individual is eligible for family tax benefit in respect of the child at any time within the period of 13 weeks starting on the day of the child’s birth and the individual’s Part A rate at that time is greater than nil.

Child entrusted to care of individual

(3) Second, an individual is eligible for maternity allowance in respect of a child if:

(a) the individual is not a parent of the child; and

(b) the child is entrusted to the care of the individual or the individual’s partner within the period of 13 weeks starting on the day of the child’s birth; and

(c) the child continues, or is likely to continue, in that care for not less than 13 weeks; and

(d) the individual is eligible for family tax benefit in respect of the child at any time within the period of 13 weeks starting on the day of the child’s birth and the individual’s Part A rate at that time is greater than nil.

Stillborn child

(4) Third, an individual is eligible for maternity allowance in respect of a child if:

(a) the child is a stillborn child; and

(b) the individual would have been eligible for family tax benefit in respect of the child, at any time within the period of 13 weeks starting on the day of the child’s birth, if the child had not been a stillborn child and the individual’s Part A rate at that time would have been greater than nil.

Adoption

(5) Fourth, an individual is eligible for maternity allowance in respect of a child if:

(a) as part of the process for the adoption of the child by the individual, the child is entrusted to the care of the individual by an authorised party; and

(b) the child is not more than 26 weeks of age at the time the child is entrusted to the care of the individual; and

(c) the individual is eligible for family tax benefit in respect of the child at any time within the period of 13 weeks starting on the day the child is entrusted to the care of the individual and the individual’s Part A rate at that time is greater than nil.

37 Only one individual eligible for maternity allowance in respect of a child

(1) Only one individual is eligible for maternity allowance in respect of a child.

(2) If 2 or more individuals would otherwise be eligible for maternity allowance in respect of the same child, the individual who is eligible is the one determined by the Secretary to be eligible.

Subdivision B—Eligibility of individuals for maternity allowance where death occurs

38 What happens if an individual eligible for maternity allowance dies

If:

(a) an individual is eligible for maternity allowance (the subject allowance) in respect of a child; and

(b) the individual dies; and

(c) before the individual died, the subject allowance had not been paid to the individual (whether or not a claim under Part 3 of the A New Tax System (Family Assistance) (Administration) Act 1999 had been made); and

(d) another individual makes a claim under that Part for payment of maternity allowance because of the death of a person, stating that he or she wishes to become eligible for the subject allowance; and

(e) the Secretary considers that the other individual ought to be eligible for the subject allowance;

the other individual is eligible for the subject allowance and no‑one else is, or can become, eligible for or entitled to be paid that allowance.

Division 3—Eligibility for maternity immunisation allowance

Subdivision A—Eligibility of individuals for maternity immunisation allowance in normal circumstances

39 When an individual is eligible for maternity immunisation allowance in normal circumstances

(1) An individual is eligible for maternity immunisation allowance in respect of a child in any of the 3 cases set out in this section.

Child alive within 18 months of birth

(2) First, an individual is eligible for maternity immunisation allowance in respect of a child who is alive at the end of 18 months after the date of the child’s birth if:

(a) the Secretary is satisfied that the child meets the immunisation requirements set out in section 6 on any day before the child turns 2; and

(b) on the later of the following days (the qualifying day):

(i) the day the child turned 18 months;

(ii) the earliest day to which paragraph (a) applies;

one of the following applies:

(iii) the child is an FTB child of the individual and maternity allowance has been paid in respect of the child;

(iv) the individual is eligible for family tax benefit in respect of the child and the individual’s Part A rate is greater than nil;

(v) the Secretary is satisfied there is a pattern of care for the child for a period, that started before the qualifying day and that will end after that day, in which the child was, or will be, an FTB child of the individual.

Stillborn child

(3) Second, an individual is eligible for maternity immunisation allowance in respect of a child that is a stillborn child if the individual is entitled to maternity allowance in respect of the child.

Child dies within 2 years of birth

(4) Third, an individual is eligible for maternity immunisation allowance in respect of a child who is born alive but dies within 2 years if one of the following applies:

(a) the child was an FTB child of the individual on the day of the child’s death and someone has been paid or is entitled to be paid maternity allowance in respect of the child;

(b) on the day of the child’s death, the individual was eligible for family tax benefit in respect of the child and the individual’s Part A rate was greater than nil;

(c) the Secretary is satisfied that, on the day of the child’s death, there was a pattern of care for the child for a period, that started before that day and that would have ended after that day if the child had not died, in which the child was, or would have been, an FTB child of the individual.

Subdivision B—Eligibility of individuals for maternity immunisation allowance where death occurs

40 What happens if an individual eligible for maternity immunisation allowance dies

If:

(a) an individual is eligible for maternity immunisation allowance (the subject allowance) in respect of a child; and

(b) the individual dies; and

(c) before the individual died, the subject allowance had not been paid to the individual (whether or not a claim under Part 3 of the A New Tax System (Family Assistance) (Administration) Act 1999 had been made); and

(d) another individual makes a claim under that Part for payment of maternity immunisation allowance because of the death of a person, stating that he or she wishes to become eligible for the subject allowance; and

(e) the Secretary considers that the other individual ought to be eligible for the subject allowance;

the other individual is eligible for the subject allowance and no‑one else is, or can become, eligible for or entitled to be paid that allowance.

Division 4—Eligibility for child care benefit

Subdivision A—Eligibility for child care benefit by instalment for care provided by approved child care service in normal circumstances

41 When an individual is conditionally eligible for child care benefit by instalment to an approved child care service

(1) An individual is conditionally eligible for child care benefit by instalment to an approved child care service if:

(a) the individual, or the individual’s partner, has an FTB child; and

(b) the individual, or the individual’s partner, is:

(i) an Australian resident; or

(ii) undertaking a course of study in Australia and receiving financial assistance directly from the Commonwealth for the purpose of undertaking that study; and

(c) the service is not providing a session of care to the child for which the service is eligible for child care benefit under section 45; and

(d) a determination is not in force under Part 3 of the A New Tax System (Family Assistance) (Administration) Act 1999 that the service is conditionally eligible for child care benefit by instalment in respect of the child.

Secretary may determine that child is an FTB child

(2) The Secretary may determine that, because of special circumstances, a child who is not an FTB child of an individual is taken to be an FTB child of the individual for the purposes of paragraph (1)(a).

Section subject to Subdivision E

(3) This section is subject to Subdivision E (which deals with limits on eligibility).

42 When an individual is eligible for child care benefit by instalment to an approved child care service

(1) An individual is eligible for child care benefit by instalment to an approved child care service if:

(a) during the whole or part of an instalment period (see subsection (4)), a determination is in force under Part 3 of the A New Tax System (Family Assistance) (Administration) Act 1999 that the individual is conditionally eligible for child care benefit by instalment to the service in respect of a child; and

(b) during the next instalment period, the service gives the Secretary, in accordance with a form and in a manner approved by the Secretary:

(i) a statement of an amount of child care benefit in respect of the instalment period as mentioned in subsection (2); and

(ii) details of the basis on which the statement of the amount was made; and

(iii) any other information required by the Secretary; and

(c) the Secretary is satisfied that the amount of child care benefit set out in the statement under subparagraph (b)(i) was correctly calculated on the basis detailed under subparagraph (b)(ii).

Statement under paragraph (1)(b)

(2) The statement under paragraph (1)(b) must set out the amount of child care benefit the service considers the individual would be entitled to be paid, in respect of the sessions of care covered by subsection (3), on the assumption that the individual had instead made a claim under Part 3 of the A New Tax System (Family Assistance) (Administration) Act 1999 on the basis of eligibility under Subdivision B of this Division, and in applying that Subdivision for that purpose:

(a) subparagraph 43(1)(d)(ii) (which relates to immunisation requirements) is to be disregarded; and

(b) the CCB % that is to be used in calculating the individual’s rate of child care benefit under Schedule 2 is the CCB % specified in the determination.

(3) For the purposes of subsection (2), the sessions of care are those provided by the service to the child:

(a) while the determination was in force during the instalment period; and

(b) to which Subdivision E (which deals with limits on eligibility) does not apply.

Instalment period

(4) In this section:

instalment period means:

(a) if paragraph (b) does not apply—a quarter beginning on any 1 January, 1 April, 1 July or 1 October; or

(b) if the approved child care service is covered by a determination under subsection (5)—the period specified in the determination.

(5) The Secretary may determine that a specified period, that is not a quarter, is the instalment period for the purposes of this section for approved child care services of a particular kind. Such a determination does not come into force until the end of the instalment period in which it is made.

Subdivision B—Eligibility for child care benefit for past periods for care provided by approved child care service in normal circumstances

43 When an individual is eligible for child care benefit

(1) An individual is eligible for child care benefit in respect of a session of care provided to a child by an approved child care service if:

(a) the child is an FTB child of the individual, or of the individual’s partner, during the session; and

(b) the care is provided in Australia; and

(c) the individual, or the individual’s partner, has incurred a liability to pay for the session (whether or not the liability has been discharged); and

(d) when a claim by the individual for payment of child care benefit in respect of the session is determined in accordance with Part 3 of the A New Tax System (Family Assistance) (Administration) Act 1999:

(i) the individual, or the individual’s partner, is an Australian resident or is undertaking a course of study in Australia and receiving financial assistance directly from the Commonwealth for the purpose of undertaking that course; and

(ii) where the child is aged under 7 at that time and the session is not a school holiday session—the child meets the immunisation requirements set out in section 6; and

(e) the session starts on or after the commencement of this Act; and

(f) a determination is not in force during the session under Part 3 of the A New Tax System (Family Assistance) (Administration) Act 1999 that the individual is conditionally eligible for child care benefit by instalment to the approved child care service.

Secretary may determine that child is an FTB child

(2) The Secretary may determine that, because of special circumstances, a child who is not an FTB child of an individual is taken to be an FTB child of the individual for the purposes of paragraph (1)(a).

Exceptions

(3) This section is subject to section 44 and Subdivision E (which limit eligibility).

44 Individual not eligible for child care benefit if service eligible under Subdivision C

General rule

(1) An individual is not eligible for child care benefit under this Subdivision in respect of a session of care provided to a child if the approved child care service providing the session of care is eligible for child care benefit under Subdivision C in respect of the same session of care.

Exception

(2) Subsection (1) does not apply to a session of care if the session is covered by a determination under subsection (3).

Ministerial determination

(3) The Minister may determine that subsection (1) does not apply in specified circumstances to sessions of care provided by approved child care services.

Disallowable instrument

(4) A determination under this section is a disallowable instrument for the purposes of section 46A of the Acts Interpretation Act 1901.

Subdivision C—Eligibility for child care benefit for care provided by approved child care service in special circumstances

45 When an approved child care service is eligible for child care benefit for an initial 13 week period

(1) An approved child care service is eligible for child care benefit for a session of care provided by the service to a child if:

(a) at the time the care is provided, the service believes the child is at risk of serious abuse or neglect; or

(b) the child is in an individual’s care immediately before the session is provided and, at the time the care is provided, the service believes the individual is experiencing hardship of a kind specified in a determination in force under subsection 48(1).

Exceptions

(2) However, the service is not so eligible for child care benefit for the session of care if:

(a) the session is provided after 13 special‑circumstances‑rate weeks (see subsection (3)) have passed, whether or not in a continuous period, in the same calendar year as that in which the session is provided; or

(b) when the session is provided, a determination is in force under Part 3 of the A New Tax System (Family Assistance) (Administration) Act 1999 that an individual is conditionally eligible for child care benefit by instalment to the approved child care service in respect of the child.

Special‑circumstances‑rate week