Taxation Laws Amendment Act (No. 7) 1999

No. 117, 1999

Taxation Laws Amendment Act (No. 7) 1999

No. 117, 1999

Taxation Laws Amendment Act (No. 7) 1999

No. 117, 1999

An Act to amend the law relating to taxation

Contents

1 Short title...................................

2 Commencement...............................

3 Schedule(s)..................................

Schedule 1—Company Law Review Amendments

Part 1—Income Tax Assessment Act 1936

Part 2—Taxation Laws Amendment (Company Law Review) Act 1998

Part 3—Application of amendments

Schedule 2—Restructuring of certain managed investment schemes

Income Tax (Transitional Provisions) Act 1997

Income Tax Assessment Act 1997

Taxation Laws Amendment Act (No. 7) 1999

No. 117, 1999

An Act to amend the law relating to taxation

[Assented to 22 September 1999]

The Parliament of Australia enacts:

This Act may be cited as the Taxation Laws Amendment Act (No. 7) 1999.

(1) Subject to subsection (2), this Act commences on the day on which it receives the Royal Assent.

(2) Schedule 1 is taken to have commenced immediately after the commencement of section 1 of the Taxation Laws Amendment (Company Law Review) Act 1998.

Subject to section 2, each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

Schedule 1—Company Law Review Amendments

Part 1—Income Tax Assessment Act 1936

1 Subsection 6(1) (definition of share capital account)

Repeal the definition, substitute:

share capital account has the meaning given by section 6D.

2 After section 6CA

Insert:

6D Meaning of share capital account

(1) A share capital account is:

(a) an account which the company keeps of its share capital; or

(b) any other account (whether or not called a share capital account), created on or after 1 July 1998, where the first amount credited to the account was an amount of share capital.

(2) If a company has more than one account covered by subsection (1), the accounts are taken, for the purposes of this Act, to be a single account.

Note: Because the accounts are taken to be a single account (the combined share capital account) tainting any of the accounts has the effect of tainting the combined share capital account.

(3) However, an account that is tainted for the purposes of Division 7B of Part IIIAA is not a share capital account for the purposes of this Act other than for the purposes of:

(a) the definition of paid‑up share capital in subsection 6(1); and

(b) subsection 44(1B); and

(c) section 46H; and

(d) subsection 159GZZZQ(5); and

(e) Division 7B of Part IIIAA; and

(f) subsection 160ZA(7A).

3 Subsection 160ARDM(2)

Omit “if the amount is a debt transferred under a debt/equity swap (within the meaning of section 63E)”, substitute:

if the amount:

(a) could be identified in the books of the company as an amount of share capital at all times before it was credited to the share capital account; or

(b) is:

(i) a debt transferred under a debt/equity swap; and

(ii) does not exceed the lesser of the value of the shares issued by the debtor and the amount of the debt (or part of the debt) being extinguished under the debt/equity swap.

4 At the end of section 160ARDM

Add:

(3) For the purposes of this section, a debt/equity swap occurs if, under an arrangement (defined in subsection (4)), a taxpayer discharges, releases or otherwise extinguishes the whole or part of a debt owed to the taxpayer in return for the issue by the debtor to the taxpayer of shares (other than redeemable preference shares) in the debtor.

(4) In this section:

arrangement means any agreement, arrangement, understanding, promise, undertaking or scheme, whether express or implied, and whether or not enforceable, or intended to be enforceable, by legal proceedings.

Part 2—Taxation Laws Amendment (Company Law Review) Act 1998

5 Subsection 2(2)

Omit “24, 55”, substitute “23, 24, 54, 55”.

6 Item 3 of Schedule 1

Omit “a day to be fixed by Proclamation”, substitute “1 July 1998”.

7 At the end of Schedule 2

Add:

9 Transitional—merging tainted share premium accounts

(1) This item applies if, apart from this item, a company’s share capital account would become tainted under Division 7B of Part IIIAA of the Income Tax Assessment Act 1936 because the amount (the tainted amount) standing to the credit of a tainted share premium account becomes part of the company’s share capital under Schedule 5 to the Company Law Review Act 1998.

(2) The share capital account is only tainted as a result of the tainted amount becoming part of the share capital account when the balance of the share capital account is equal to the net tainted amount.

Note: This does not prevent the share capital account from becoming tainted under section 160ARDM of the Income Tax Assessment Act 1936 as a result of other amounts being transferred to it.

(3) No franking debit arises under section 160ARDQ of the Income Tax Assessment Act 1936 as a result of the share capital account becoming tainted under subitem (2).

(4) Where:

(a) before a distribution that consists of one or more amounts the share capital account is not tainted; but

(b) after the distribution the share capital account is tainted;

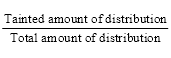

the following proportion of each of the amounts is taken to have been paid from a tainted share account:

where:

tainted amount of distribution is the difference between the net tainted amount immediately before the distribution and the net tainted amount immediately after the distribution.

Note: Certain distributions from tainted share capital accounts will be unfranked dividends for which no section 46 or 46A rebate is available.

(5) In this item:

net tainted amount, in relation to an account, means the lesser of:

(a) the tainted amount;

(b) the lowest balance of the share capital account at any time after the commencement of this item.

tainted share premium account, in relation to a company, means an account, whether or not called a share premium account:

(a) to which the company has, in respect of premiums received by the company on shares issued by it, credited amounts, being the respective amounts of the premiums; and

(b) for which either of the following conditions is satisfied:

(i) any other amount is standing to the credit of the account;

(ii) an amount has been credited to the account in respect of a premium received by the company on a share issued by it (not being an amount that has been so credited immediately after the receipt by the company of the premium) which could not at all times be identified in the books of the company as such a premium.

Part 3—Application of amendments

8 Application of amendments

(1) The amendments made by items 1 and 2 of this Schedule apply to things done after the commencement of this item where the relevant company has shares with no par value.

(2) The amendments made by items 3 and 4 of this Schedule apply where, after the commencement of this item, an amount is transferred to the share capital account of a company with shares with no par value.

Schedule 2—Restructuring of certain managed investment schemes

Income Tax (Transitional Provisions) Act 1997

1 Division 960 (before Subdivision 960‑M)

Insert:

960‑100 Effect of this Subdivision

This Subdivision has effect for the purposes of the Income Tax Assessment Act 1936, the Income Tax Assessment Act 1997, the Taxation Administration Act 1953 and this Act.

960‑105 Entities, and members of entities, benefiting from the application of this Subdivision

(1) This Subdivision applies to an entity if, and only if:

(a) the entity is a managed investment scheme for the purposes of the Corporations Law; and

(b) the scheme has been or is registered by the Australian Securities and Investments Commission under section 601EB of the Corporations Law; and

(c) the entity was a managed investment scheme as mentioned in paragraph (a) at all times from the commencement of 1 July 1998 until the registration of the scheme as mentioned in paragraph (b); and

(d) the entity was the same kind of entity immediately before, and immediately after, the scheme was so registered; and

(e) changes to the scheme that were necessary to be made to enable the scheme to be registered as mentioned in paragraph (b) were made during the period beginning on 1 July 1998 and ending on 30 June 2000 (the transition period); and

(f) the membership of the scheme did not alter as a result of the changes; and

(g) where any other changes were or are made to the scheme during the transition period:

(i) the other changes were or are made only for the purpose of improving the administration or operation of the scheme; and

(ii) there were no increases in the values of the interests of any members of the scheme as a result of the other changes or, if there were any such increases, they applied proportionately to the values of the interests of all the members of the scheme; and

(iii) no reductions in the values of the interests of any members of the scheme occurred as a result of the other changes; and

(iv) the membership of the scheme did not alter as a result of the other changes.

(2) If this Subdivision applies to an entity under subsection (1), it also applies to a member of the entity, in relation to the member’s interests in the entity, if, and only if, the member was a member:

(a) immediately before the changes referred to in subsection (1) were made or, if the changes were made at different times, immediately before the first of the changes was made; and

(b) immediately after the changes referred to in subsection (1) were made or, if the changes were made at different times, immediately after the last of the changes was made.

960‑110 No taxation consequences to result from changes to managed investment scheme

Despite the changes made as mentioned in subsection 960‑105(1) to the managed investment scheme constituted by an entity to which this Subdivision applies:

(a) the entity is taken, immediately after the changes were made or, if the changes were made at different times, immediately after the last of the changes was made, to be the same entity as existed immediately before the changes were made or, if the changes were made at different times, immediately before the first of the changes was made; and

(b) the legal ownership of the assets of the entity is taken not to have altered as a result of the changes; and

(c) the beneficial ownership of the interests in the entity of a member of the entity to whom this Subdivision applies in relation to those interests is taken not to have altered as a result of the changes; and

(d) without limiting by implication any other effect of the above paragraphs, the changes are taken not to have resulted in a CGT event in respect of the entity, or in respect of a member of the entity in relation to the member’s interests in the entity.

Income Tax Assessment Act 1997

2 Section 4‑5 (note)

Repeal the note, substitute:

Note 1: The expression you is not used in provisions that apply only to entities that are not individuals.

Note 2: For circumstances in which the identity of an entity that is a managed investment scheme for the purposes of the Corporations Law is not affected by changes to the scheme, see Subdivision 960‑E of the Income Tax (Transitional Provisions) Act 1997.

[Minister’s second reading speech made in—

House of Representatives on 13 May 1999

Senate on 30 June 1999]

(87/99)