An Act to implement A New Tax System by amending legislation relating to indirect tax, and by amending other legislation consequentially on indirect tax reform, and for other purposes

[Assented to 22 December 1999]

The Parliament of Australia enacts:

This Act may be cited as the A New Tax System (Indirect Tax and Consequential Amendments) Act 1999.

(1) Subject to this section, this Act commences on the day on which it receives the Royal Assent.

Schedule 1—GST, Luxury Car Tax and Wine Equalisation Tax

(2) Part 1 of Schedule 1 (other than items 127 and 133) commences immediately after the commencement of the A New Tax System (Goods and Services Tax) Act 1999.

(3) Part 2 of Schedule 1 (other than items 187, 189 and 190) commences immediately after the commencement of the A New Tax System (Luxury Car Tax) Act 1999.

(4) Part 3 of Schedule 1 (other than items 232 and 235) commences immediately after the commencement of the A New Tax System (Wine Equalisation Tax) Act 1999.

(5) Items 127, 133, 187, 189, 190, 232 and 235 of Schedule 1 commence, or are taken to have commenced, on 1 July 2000, or immediately after the commencement of item 9 of Schedule 3 to the A New Tax System (Pay As You Go) Act 1999, whichever is later.

Schedule 2—Customs Act

(6) Item 5 of Schedule 2 commences on the day on which this Act receives the Royal Assent if, and only if, this Act receives the Royal Assent before the day on which Schedule 2 to the Customs Legislation Amendment Act (No. 2) 1999 commences.

Note: The rest of Part 1 of Schedule 2 commences on Royal Assent.

(7) Part 2 of Schedule 2 commences immediately after the commencement of the A New Tax System (Goods and Services Tax) Act 1999.

(8) Part 3 of Schedule 2 commences on the day on which this Act receives the Royal Assent, or immediately after the commencement of Schedule 2 to the Customs Legislation Amendment Act (No. 2) 1999, whichever is later.

Schedule 3—Income Tax Assessment Act 1997

(9) Schedule 3 commences immediately after the commencement of the A New Tax System (Goods and Services Tax) Act 1999.

Note: Schedule 4 commences on Royal Assent.

Schedule 5—Tax Administration Acts

(10) Schedule 5 (other than items 2 and 3) commences immediately after the commencement of the A New Tax System (Indirect Tax Administration) Act 1999.

(11) Items 2 and 3 of Schedule 5 commence immediately after the commencement of the A New Tax System (Goods and Services Tax Administration) Act 1999.

Schedule 6—Indirect Tax Transition Acts

(12) Schedule 6 (other than items 13 and 14) commences, or is taken to have commenced, immediately after the commencement of the A New Tax System (Goods and Services Tax Transition) Act 1999.

(13) Items 13 and 14 of Schedule 6 commence immediately after the commencement of the A New Tax System (Wine Equalisation Tax and Luxury Car Tax Transition) Act 1999.

Schedule 7—Tradex Scheme

(14) If the Tradex Scheme Act 1999 commences before 1 July 2000:

(a) Part 1 of Schedule 7 commences, or is taken to have commenced, on the day on which that Act commences; and

(b) Part 2 of Schedule 7 commences immediately after the commencement of the A New Tax System (Goods and Services Tax) Act 1999.

(15) If the Tradex Scheme Act 1999 commences on 1 July 2000:

(a) Part 1 of Schedule 7 is taken never to have commenced; and

(b) Part 2 of Schedule 7 commences immediately after the commencement of the A New Tax System (Goods and Services Tax) Act 1999.

(16) If the Tradex Scheme Act 1999 commences after 1 July 2000:

(a) Part 1 of Schedule 7 is taken never to have commenced; and

(b) Part 2 of Schedule 7 commences on the day on which that Act commences.

Schedule 8—Other Acts

(17) Schedule 8 commences immediately after the commencement of the A New Tax System (Goods and Services Tax) Act 1999.

Subject to section 2, each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

Part 1—Amendment of the A New Tax System (Goods and Services Tax) Act 1999

1 At the end of Division 1

Add:

1‑4 States and Territories are bound by the GST law

The *GST law binds the Crown in right of each of the States, of the Australian Capital Territory and of the Northern Territory. However, it does not make the Crown liable to be prosecuted for an offence.

2 Subsection 3‑5(3) (after table item 8)

Insert:

3 Subsection 9‑10(2)

Omit all the words from and including “However” to and including “that is a supply of money.”.

4 At the end of section 9‑10

Add:

(4) However, a supply does not include a supply of *money unless the money is provided as *consideration for a supply that is a supply of money.

5 Paragraph 9‑15(3)(b)

Omit “a payment made as”, substitute “making”.

6 Subsection 9‑25(4)

After “property” (last occurring), insert “, or the land to which the real property relates,”.

7 Section 9‑39 (table item 8, 2nd column)

After “taxes”, insert “, fees and charges”.

8 At the end of section 9‑75

Add:

(2) However, if the taxable supply is of a *luxury car, the value of the taxable supply is as follows:

where:

luxury car tax value has the meaning given by section 5‑20 of the A New Tax System (Luxury Car Tax) Act 1999.

9 After section 9‑80

Insert:

9‑85 Value of taxable supplies to be expressed in Australian currency

(1) For the purposes of this Act, the *value of a *taxable supply is to be expressed in Australian currency.

(2) In working out the *value of a *taxable supply, any amount of the *consideration for the supply that is expressed in a currency other than Australian currency is to be treated as if it were an amount of Australian currency worked out in the manner determined by the Commissioner.

10 Section 9‑99 (after table item 4)

Insert:

4A | Offshore supplies other than goods or real property | Division 84 |

11 Section 9‑99 (table item 6)

Repeal the item.

12 Subsection 11‑10(2)

Omit all the words from and including “However” to and including “that is a supply of money.”.

13 At the end of section 11‑10

Add:

(3) However, an acquisition does not include an acquisition of *money unless the money is provided as *consideration for a supply that is a supply of money.

14 At the end of section 11‑15

Add:

(4) An acquisition is not treated, for the purposes of paragraph (2)(a), as relating to making supplies that would be *input taxed if:

(a) the only reason it would (apart from this subsection) be so treated is because it relates to making *financial supplies; and

(b) your *annual turnover of financial supplies does not exceed the lesser of:

(i) $50,000 or such other amount specified in the regulations; or

(ii) 5% of your *annual turnover (treating supplies that are input taxed as part of your annual turnover).

15 Subsection 11‑30(2)

Repeal the subsection.

16 Section 11‑99 (after table item 8)

Insert:

8A | Offshore supplies other than goods or real property | Division 84 |

17 Subsections 13‑5(1) and (2)

Repeal the subsections, substitute:

(1) You make a taxable importation if:

(a) goods are imported; and

(b) you enter the goods for home consumption (within the meaning of the Customs Act 1901).

However, the importation is not a taxable importation to the extent that it is a *non‑taxable importation.

Note: There is no registration requirement for taxable importations, and the importer need not be carrying on an enterprise.

18 Paragraph 13‑20(2)(a)

Omit “customs value (for the purposes of Division 2 of Part VIII of the Customs Act 1901)”, substitute “*customs value”.

19 Subparagraph 13‑20(2)(b)(i)

Repeal the subparagraph, substitute:

(i) for the *international transport of the goods to their *place of consignment in Australia; and

20 At the end of subsection 13‑20(2)

Add:

; and (d) any *wine tax payable in respect of the *local entry of the goods.

21 At the end of section 13‑20

Add:

(3) The Commissioner may, in writing:

(a) determine the way in which the amount paid or payable for a specified kind of transport or insurance is to be worked out for the purposes of paragraph (2)(b); and

(b) in relation to importations of a specified kind or importations to which specified circumstances apply, determine that the amount paid or payable for a specified kind of transport or insurance is taken, for the purposes of that paragraph, to be zero.

22 Section 13‑99 (table item 4)

Repeal the item.

23 At the end of section 15‑10

Add:

(4) An importation is not treated, for the purposes of paragraph (2)(a), as relating to making supplies that would be *input taxed if:

(a) the only reason it would (apart from this subsection) be so treated is because it relates to making *financial supplies; and

(b) your *annual turnover of financial supplies does not exceed the lesser of:

(i) $50,000 or such other amount specified in the regulations; or

(ii) 5% of your *annual turnover (treating supplies that are input taxed as part of your annual turnover).

24 Subsection 15‑25(2)

Repeal the subsection.

25 Section 15‑99 (after table item 2)

Insert:

2A | Non‑deductible expenses | Division 69 |

26 Section 17‑99 (after table item 12)

Insert:

12A | Simplified accounting methods for retailers | Division 123 |

27 At the end of section 19‑5

Add:

Note: This section is an explanatory section.

28 At the end of section 19‑10

Add:

(4) However, the return of a thing supplied, or part of a thing supplied, to its supplier is not an *adjustment event if the return is for the purpose of repair or maintenance.

29 Paragraph 19‑75(a)

Omit “plus”, substitute “minus”.

30 Paragraph 19‑75(b)

Omit “minus”, substitute “plus”.

31 At the end of section 25‑10

Add:

(2) The *Australian Business Registrar must enter in the *Australian Business Register the date on which your *registration takes or took effect.

32 At the end of section 25‑60

Add:

(2) The *Australian Business Registrar must enter in the *Australian Business Register the date on which the cancellation of your *registration takes effect.

33 Subsection 27‑30(1)

Repeal the subsection, substitute:

(1) For the purpose of ensuring the effective operation of this Division where:

(a) you become *registered or *required to be registered; or

(b) the tax periods applying to you have changed;

the Commissioner may, by written notice given to you, determine that a period specified in the notice is a tax period that applies to you.

Note: Determining under this section a tax period applying to you is a reviewable GST decision (see Division 7 of Part VI of the Taxation Administration Act 1953).

34 Subsection 27‑40(1)

Repeal the subsection, substitute:

(1) If:

(a) an individual dies or becomes bankrupt; or

(b) any other entity goes into liquidation or receivership or for any reason ceases to exist;

the individual’s or entity’s tax period at the time is taken to have ceased at the end of the day before the death, bankruptcy, liquidation or receivership.

(1A) If an entity ceases to *carry on any *enterprise, the entity’s tax period at the time is taken to have ceased at the end of the day on which the cessation occurred.

35 Section 27‑99 (after table item 1)

Insert:

1A | Representatives of incapacitated entities | Division 147 |

36 At the end of section 29‑15

Add:

(2) However, if paragraph 33‑15(b) applies to payment of the GST on the importation, the input tax credit is attributable to the tax period in which the liability for the GST arose.

37 Subsection 29‑40(1)

Repeal the subsection, substitute:

(1) If:

(a) your *annual turnover does not exceed the *cash accounting turnover threshold; or

(b) for income tax purposes, you account for your income using the receipts method; or

(c) each of the *enterprises that you *carry on is an enterprise of a kind that the Commissioner determines, in writing, to be a kind of enterprise in respect of which a choice to *account on a cash basis may be made under this section;

you may choose to account on a cash basis, with effect from the first day of the tax period that you choose.

38 Subsection 29‑40(2)

Omit all the words from and including “whether or not”, substitute “whether or not paragraph (1)(a), (b) or (c) applies”.

39 Paragraph 29‑40(3)(a)

Omit “$500,000”, substitute “$1,000,000”.

40 Subparagraph 29‑45(1)(b)(ii)

Omit “and”.

41 Subparagraph 29‑45(1)(b)(iii)

Repeal the subparagraph.

42 At the end of subsection 29‑70(1)

Add:

However, the Commissioner may treat as a tax invoice a particular document that is not a tax invoice.

43 At the end of subsection 29‑75(1)

Add:

However, the Commissioner may treat as an adjustment note a particular document that is not an adjustment note.

44 At the end of section 31‑10

Add:

(2) However, if the tax period ends during the first 7 days of a month, you must give the *GST return to the Commissioner:

(a) on or before the 21st day of that month; or

(b) within such further period as the Commissioner allows.

45 At the end of section 31‑20

Add:

(2) The Commissioner may direct that a *GST return given under this section need not state your *net amount for a tax period for which a GST return has been given under section 31‑15.

46 At the end of subsection 31‑25(2)

Add “, unless the Commissioner is satisfied that it is not practicable for you to lodge your returns electronically”.

47 At the end of section 33‑15

Add:

(2) An officer of Customs (within the meaning of subsection 4(1) of the Customs Act 1901) may refuse to deliver the goods concerned unless the GST has been paid.

48 Section 33‑99 (after table item 4)

Insert:

4A | Importations without entry for home consumption | Division 114 |

49 After subsection 35‑10(1)

Insert:

(1A) The account must be an account maintained in Australia.

50 Section 37‑1 (after table item 29)

Insert:

29A | Simplified accounting methods for retailers | Division 123 |

51 At the end of paragraphs 38‑4(1)(c) and (d)

Add “for human consumption”.

52 After paragraph 38‑4(1)(g)

Insert:

(ga) unprocessed cow’s milk; or

53 Subsection 38‑10(1) (table item 12)

Repeal the item, substitute:

54 Paragraph 38‑50(1)(a)

Omit “prohibited except”, substitute “restricted, but may be supplied”.

55 Subsections 38‑50(2) and (3)

Repeal the subsections, substitute:

(2) A supply of a drug or medicinal preparation is GST‑free if, under a *State law or a *Territory law in the State or Territory in which it is supplied, the supply of the drug or medicinal preparation to an *individual for private or domestic use or consumption is restricted but may be made by:

(a) a *medical practitioner, *dental practitioner or pharmacist; or

(b) any other person permitted by or under that law to do so.

(3) Subsection (2) does not cover the supply of a drug or medicinal preparation of a kind specified in the regulations.

56 Paragraph 38‑50(5)(a)

Omit “subsection (3)”, substitute “subsection (2)”.

57 At the end of section 38‑50

Add:

(6) A supply of a drug or medicinal preparation is GST‑free if:

(a) the drug or medicinal preparation is the subject of an approval under paragraph 19(1)(a) of the Therapeutic Goods Act 1989, and any conditions to which the approval is subject have been complied with; or

(b) the drug or medicinal preparation is supplied under an authority under subsection 19(5) of that Act, and the supply is in accordance with any regulations made for the purposes of subsection 19(7) of that Act; or

(c) the drug or medicinal preparation is exempted from the operation of Part 3 of that Act under regulation 12A of the Therapeutic Goods Regulations.

(7) A supply of a drug or medicinal preparation covered by this section is GST‑free if, and only if:

(a) the drug or medicinal preparation is for human use or consumption; and

(b) the supply is to an *individual for private or domestic use or consumption.

58 Subsection 38‑55(2)

Omit “, or a supply of re‑insurance of such insurance,”.

59 At the end of section 38‑55

Add:

(3) However, a supply of re‑insurance is not GST‑free under this section.

60 Subsection 38‑185(1) (table item 1, 3rd column)

After “from Australia”, insert “before, or”.

61 Subsection 38‑185(1) (table item 2, 3rd column)

After “from Australia”, insert “before, or”.

62 Subsection 38‑185(1) (table item 3, 3rd column)

Omit “of taking”, substitute “after taking”.

63 Subsection 38‑185(1) (table item 4, 3rd column)

Omit “within 60 days (or such further period as the Commissioner allows) after”, substitute “before, or within 60 days (or such further period as the Commissioner allows) after,”.

64 Subsection 38‑185(1) (table item 5, 3rd column)

After “stores” (wherever occurring), insert “, or spare parts,”.

65 At the end of section 38‑185

Add:

(3) Without limiting items 1 and 2 in the table in subsection (1), a supplier of goods is treated, for the purposes of those items, as having exported the goods from Australia if:

(a) before the goods are exported, the supplier supplies them to an entity that is not *registered or *required to be registered; and

(b) that entity exports the goods from Australia; and

(c) the goods have been entered for export within the meaning of section 113 of the Customs Act 1901; and

(d) since their supply to that entity, the goods have not been altered or used in any way, except to the extent (if any) necessary to prepare them for export; and

(e) the supplier has sufficient documentary evidence to show that the goods were exported.

However, if the goods are reimported into Australia, the supply is not GST‑free unless the reimportation is a *taxable importation.

66 After section 38‑185

Insert:

38‑187 Lease etc. of goods for use outside Australia

A supply of goods is GST‑free if:

(a) the supply is by way of lease or hire; and

(b) the goods are used outside Australia.

Note: If goods are leased or hired and used partly in Australia and partly outside Australia, the supply could be taxable to the extent that the goods are used in Australia (see section 9‑5).

67 Paragraph 38‑250(1)(b)

Repeal the paragraph, substitute:

(b) the supply is for *consideration that:

(i) if the supply is a supply of accommodation—is less than 75% of the *GST inclusive market value of the supply; or

(ii) if the supply is not a supply of accommodation—is less than 50% of the GST inclusive market value of the supply.

68 Paragraph 38‑250(2)(b)

Repeal the paragraph, substitute:

(b) the supply is for *consideration that:

(i) if the supply is a supply of accommodation—is less than 75% of the cost to the supplier of providing the accommodation; or

(ii) if the supply is not a supply of accommodation—is less than 50% of the consideration the supplier provided, or was liable to provide, for acquiring the thing supplied.

69 Subdivision 38‑I (heading)

Repeal the heading, substitute:

Subdivision 38‑I—Water, sewerage and drainage

70 After section 38‑295

Insert:

38‑300 Drainage

A supply of a service that consists of draining storm water is GST‑free.

71 Section 38‑355 (table item 1, 2nd column)

After “Transport”, insert “of passengers”.

72 Section 38‑355 (table item 1, 3rd column)

Omit “or goods”.

73 Section 38‑355 (table item 5)

Repeal the item, substitute:

5 | Transport etc. of goods | the *international transport of goods: (a) from their *place of export in Australia to a destination outside Australia; or (b) from a place outside Australia to their *place of consignment in Australia; or (c) from a place outside Australia to the same or another place outside Australia. However, paragraph (a) or (b) only applies to the transport of the goods within Australia if it is supplied by the supplier of the transport of the goods from or to Australia (whichever is relevant). |

74 Section 38‑355 (table item 6, 3rd column)

Omit “transport, loading or handling”, substitute “the *international transport”.

75 Section 38‑355 (table item 7, 3rd column)

Omit “transport, loading or handling”, substitute “the *international transport”.

76 Subparagraphs 38‑510(1)(a)(i) and (ii)

Repeal the subparagraphs, substitute:

(i) the person holding the position of Managing Director of the nominated company (within the meaning of Part 2 of the Hearing Services and AGHS Reform Act 1997); or

(ii) an officer or employee of that company who is authorised in writing by the Managing Director for the purposes of this section;

77 Subsection 42‑5(1)

Omit “34”, substitute “64”.

78 After subsection 42‑5(1)

Insert:

(1A) An importation of a container is a non‑taxable importation if:

(a) goods covered by item 34 in Schedule 4 to the Customs Tariff Act 1995 are imported in or on the container; and

(b) the container will be exported from Australia without being put to any other use.

79 Subsection 42‑5(2)

Omit all the words from and including “includes”, substitute “includes a reference to goods to which that item would apply apart from the operation of subsection 18(1) of that Act”.

80 Section 42‑10

Repeal the section.

81 Section 48‑1

After “90% owned group”, insert “, and in some cases other entities (such as non‑profit bodies),”.

82 At the end of section 48‑1

Add:

Note: Provisions for members of GST groups apply for the wine equalisation tax (see Subdivision 21‑B of the A New Tax System (Wine Equalisation Tax) Act 1999) and the luxury car tax (see Subdivision 16‑A of the A New Tax System (Luxury Car Tax) Act 1999).

83 Subsection 48‑10(2)

Omit “paragraph (1)(a)”, substitute “paragraph (1)(b)”.

84 Paragraph 48‑40(2)(a)

Repeal the paragraph, substitute:

(a) a supply that an entity makes to another *member of the same *GST group is treated as if it were not a *taxable supply, unless:

(i) it is a taxable supply because of Division 84 (which is about offshore supplies other than goods or real property); or

(ii) the entity is a participant in a *GST joint venture and acquired the thing supplied from the *joint venture operator for the joint venture; and

85 At the end of section 51‑1

Add:

Note: Provisions for participants in GST joint ventures apply for the wine equalisation tax (see Subdivision 21‑C of the A New Tax System (Wine Equalisation Tax) Act 1999) and the luxury car tax (see Subdivision 16‑B of the A New Tax System (Luxury Car Tax) Act 1999).

86 Paragraphs 51‑10(d) and (e)

Repeal the paragraphs.

87 Paragraph 51‑10(f)

Omit “; and”.

88 Paragraph 51‑10(g)

Repeal the paragraph.

89 Division 81 (heading)

Repeal the heading, substitute:

Division 81—Payments of taxes, fees and charges

90 Section 81‑1

Omit “and other” (wherever occurring), substitute “, fees and”.

91 Section 81‑5 (heading)

Repeal the heading, substitute:

81‑5 Payments of taxes etc. can constitute consideration

92 Subsection 81‑5(1)

After “tax” (wherever occurring), insert “, fee or charge”.

93 Subsection 81‑5(2)

After “tax”, insert “, fee or charge”.

94 Section 81‑10 (heading)

Repeal the heading, substitute:

81‑10 Supplies need not be connected with Australia if the consideration is the payment of tax etc.

95 Subsection 81‑10(1)

After “tax”, insert “, fee or charge”.

96 After section 84‑10

Insert:

84‑12 The amount of GST on offshore intangible supplies

(1) The amount of GST on a supply that is a *taxable supply because of section 84‑5 is 10% of the *price of the supply.

(2) This section has effect despite section 9‑70 (which is about the amount of GST on taxable supplies).

84‑13 The amount of input tax credits relating to offshore intangible supplies

(1) The amount of the input tax credit for a *creditable acquisition that relates to a supply that is a *taxable supply because of section 84‑5 is as follows:

where:

extent of consideration is the extent to which you provide, or are liable to provide, the *consideration for the acquisition, expressed as a percentage of the total consideration for the acquisition.

extent of creditable purpose is the extent to which the *creditable acquisition is for a *creditable purpose, expressed as a percentage of the total purpose of the acquisition.

full input tax credit is 11/10 of what would have been the amount of the input tax credit for the acquisition if:

(a) the supply had been a *taxable supply otherwise than because of section 84‑5; and

(b) the acquisition had been made solely for a creditable purpose; and

(c) you had provided, or had been liable to provide, all of the consideration for the acquisition.

(2) This section has effect despite sections 11‑25 and 11‑30 (which are about the amount of input tax credits for creditable acquisitions).

97 At the end of Division 93

Add:

93‑25 Food packaging that was supplied GST‑free

This Division does not apply to the acquisition of a *returnable container if the supply of the container to the entity from which you acquired it was a supply of packaging that was *GST‑free under section 38‑6.

98 Section 108‑1

Omit “customs duty or”.

99 Subsection 108‑5(1)

Omit “goods that are in bond or otherwise subject to the control of Customs”, substitute “*excisable goods that are in bond”.

100 Paragraph 108‑5(1)(b)

Repeal the paragraph, substitute:

(b) the amount of *excise duty to which the goods would have been subject if they had been entered for home consumption under the Excise Act 1901 at the time the supply first became a supply *connected with Australia.

101 Section 114‑5

Omit all the words from and including “The circumstances” to and including “section 13‑5”, substitute:

You make a taxable importation if:

(a) the circumstances referred to in the third column of the following table occur; and

(b) you are referred to in the fourth column of the table as the importer in relation to those circumstances.

However, there is not a taxable importation to the extent that the importation to which the circumstances relate is a *non‑taxable importation.

102 Section 114‑5 (table items 7, 8 and 9)

Repeal the items.

103 Section 114‑5 (table item 10, 3rd column)

Omit “under section 203 of the Customs Act 1901”, substitute “under a warrant issued under section 203 of the Customs Act 1901, or under section 203B or 203C of that Act,”.

104 Section 114‑5 (table items 11 and 12)

Repeal the items.

105 Section 114‑5 (at the end of the table)

Add:

16 | Goods not entered for home consumption when required | Goods not covered by any other item of this table are imported into Australia, and: (a) if they are required to be entered under section 68 of the Customs Act 1901—they are not entered in accordance with that requirement; or (b) in any other case—a requirement under that Act relating to their importation has not been complied with | The person who fails to comply with that requirement. |

106 At the end of section 114‑5

Add:

(2) This section has effect despite section 13‑5.

107 At the end of Division 114

Add:

114‑10 Goods that have already been entered for home consumption etc.

Once goods have been:

(a) entered for home consumption within the meaning of the Customs Act 1901; or

(b) taken to be imported because of the application of an item in the table in section 114‑5;

they cannot subsequently be taken to be imported because of the application of an item in the table, unless they have been exported from Australia since they were so entered or taken to be imported.

114‑15 Payments of amounts of GST where security for payment of customs duty is forfeited

(1) If:

(a) a circumstance relating to goods is an importation of the goods into Australia because of an item of the table in section 114‑5; and

(b) security has been given under the Customs Act 1901 for payment of *customs duty in respect of the goods; and

(c) the security is forfeited;

any GST payable on the importation is to be paid when the security is forfeited.

(2) This section has effect despite section 33‑15 (which is about payments of amounts of GST on importations).

114‑20 Payments of amounts of GST where delivery into home consumption is authorised under section 71 of the Customs Act

(1) If:

(a) the delivery of goods into home consumption in accordance with an authorisation under section 71 of the Customs Act 1901 is an importation into Australia because of item 1, 2, 3 or 4 of the table in section 114‑5; and

(b) information was provided under section 71 of that Act in connection with the granting of the authorisation;

any GST payable on the importation is to be paid when the information was provided/on or before the granting of the authorisation.

(2) This section has effect despite sections 33‑15 (which is about payments of amounts of GST on importations) and 114‑15.

108 Paragraph 117‑5(1)(a)

Repeal the paragraph, substitute:

(a) the cost, as determined by the Chief Executive Officer of the Australian Customs Service, of materials, labour and other charges involved in the repair or renovation; and

109 Paragraph 117‑5(1)(c)

Omit “(other than the amount of GST payable on the importation)”.

110 Section 117‑10

Repeal the section.

111 Before Division 126

Insert:

Division 123—Simplified accounting methods for retailers

123‑1 What this Division is about

The Commissioner can create simplified accounting methods that some retailers can choose to apply with a view to reducing their costs of complying with the requirements of the GST.

123‑5 Commissioner may determine simplified accounting methods

(1) The Commissioner may determine in writing an arrangement (to be known as a simplified accounting method) that:

(a) specifies the kinds of *retailers to whom it is available; and

(b) provides a method for working out *net amounts of retailers to whom the method applies.

(2) The kinds of *retailer specified under paragraph (1)(a) must all be kinds of retailers that:

(a) sell *food; or

(b) make supplies that are *GST‑free under Subdivision 38‑G (Non‑commercial activities of charitable institutions etc.);

in the course or furtherance of *carrying on their *enterprise.

123‑10 Choosing to apply a simplified accounting method

(1) You may, by notifying the Commissioner in the *approved form:

(a) choose to apply a *simplified accounting method if you are a *retailer of the kind to whom the method is available; or

(b) revoke your choice to apply the method.

(2) However, you:

(a) cannot revoke the choice within 12 months after the day on which you made the choice; and

(b) cannot make a further choice within 12 months after the day on which you revoked a previous choice; and

(c) cannot choose to apply a *simplified accounting method in addition to another simplified accounting method.

(3) Your choice to apply a *simplified accounting method has effect from the start of the tax period specified in your notice.

(4) Your choice to apply a *simplified accounting method ceases to have effect:

(a) if you cease to be a *retailer of the kind to whom the method is available—from the start of the tax period occurring after the day on which you cease to be such a retailer; or

(b) if you revoke your choice to apply the method—from the start of the tax period specified in your notice of revocation.

123‑15 Net amounts

(1) If you are a *retailer who has chosen to apply a *simplified accounting method, the net amount for a tax period during which the choice has effect is worked out using the method provided for by the method.

(2) This section has effect despite section 17‑5 (which is about net amounts).

112 Subsection 129‑5(2)

Omit “does not exceed”, substitute “exceeds”.

113 Section 135‑1

Omit “of input taxed supplies (if any) that will be made in running the concern”, substitute “(if any) of supplies that will be made in running the concern and that will not be taxable supplies or GST‑free supplies”.

114 Paragraph 135‑5(1)(b)

Omit “*input taxed”, substitute “neither *taxable supplies nor *GST‑free supplies”.

115 Subsection 135‑5(2)

Repeal the subsection, substitute:

(2) The amount of the increasing adjustment is as follows:

where:

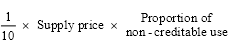

proportion of non‑creditable use is the proportion of all the supplies made through the *enterprise that you intend will be supplies that are neither *taxable supplies nor *GST‑free supplies, expressed as a percentage worked out on the basis of the *prices of those supplies.

supply price means the *price of the supply in relation to which the increasing adjustment arises.

116 Paragraph 135‑10(1)(a)

Omit “*input taxed”, substitute “neither *taxable supplies nor *GST‑free supplies”.

117 Paragraph 135‑10(1)(b)

Omit “*input taxed”, substitute “neither taxable supplies nor GST‑free supplies”.

118 At the end of Division 147

Add:

147‑25 Tax periods of representatives

(1) If a *representative of an *incapacitated entity is required to be registered in that capacity, the tax periods applying to the representative in that capacity are the same tax periods that apply to the incapacitated entity.

(2) This section has effect despite Division 27 (which is about how to work out the tax periods that apply).

119 Subsection 156‑15(1)

Repeal the subsection, substitute:

(1) If:

(a) a *taxable supply is made for a period or on a progressive basis; and

(b) the supply is made for *consideration that is to be provided on a progressive or periodic basis; and

(c) the whole of a progressive or periodic component of the supply would not be *connected with Australia if it were a separate supply;

that component is treated as if it were a separate supply that is not connected with Australia.

120 After section 156‑20

Insert:

156‑22 Leases etc. treated as being on a progressive or periodic basis

For the purposes of this Division, a supply or acquisition by way of lease, hire or similar arrangement is to be treated as a supply or acquisition that is made on a progressive or periodic basis, for the period of the lease, hire or arrangement.

121 Section 156‑25

After “This Division”, insert “(other than section 156‑15)”.

122 Subsection 171‑5(1)

Repeal the subsection, substitute:

(1) An amount of GST on a *taxable importation of goods is not payable if:

(a) a security or undertaking described in section 162 of the Customs Act 1901 has been given; and

(b) the provisions of the regulations mentioned in paragraph 162(3)(a) of that Act are complied with; and

(c) the goods are exported within the relevant period mentioned in paragraph 162(3)(b) of that Act.

Note: Section 162 of the Customs Act 1901 allows delivery of imported goods if the importer gives a security or undertaking to pay any customs duty, GST and luxury car tax relating to the importation.

(1A) An amount of GST on a *taxable importation of goods is not payable if:

(a) a security or undertaking described in section 162A of the Customs Act 1901 has been given; and

(b) the goods are not dealt with in contravention of regulations made for the purposes of that section; and

(c) either:

(i) the goods are exported within the relevant period mentioned in paragraph 162A(5)(b) of that Act; or

(ii) if the goods are described in subsection 162A(5A)—the goods are exported before the end of the relevant day mentioned in paragraph 162A(5A)(b).

Note: Section 162A of the Customs Act 1901 allows delivery of imported goods if the importer gives a security or undertaking to pay any customs duty, GST and luxury car tax relating to the importation.

123 After subsection 177‑1(2)

Insert:

(2A) The directions given under subsection (2) may also take account of the provisions of the A New Tax System (Goods and Services Tax Transition) Act 1999.

124 Paragraph 177‑10(1)(a)

Repeal the paragraph.

125 Section 182‑15 (heading)

Repeal the heading, substitute:

182‑15 Schedules 1, 2 and 3

126 Section 182‑15

Omit “Schedules 1 and 2”, substitute “Schedules 1, 2 and 3”.

127 Division 186

Repeal the Division.

128 At the end of section 188‑15

Add:

Supplies must be connected with Australia

(3) In working out your current annual turnover, disregard any supplies that are not *connected with Australia.

129 At the end of section 188‑20

Add:

Supplies must be connected with Australia

(3) In working out your projected annual turnover, disregard any supplies that are not *connected with Australia.

130 After section 188‑20

Insert:

188‑22 Settlements of insurance claims to be disregarded

In working out your *current annual turnover or your *projected annual turnover, disregard any supply that you have made to the extent that the *consideration for the supply is a payment of *money, or a supply, by an insurer in settlement of a claim under an *insurance policy.

Note: Under Subdivision 78‑B, your settlements of insurance claims can be treated as constituting supplies by insured entities.

131 Section 188‑30

Repeal the section, substitute:

188‑30 The value of non‑taxable supplies

For the purposes only of this Division, the value of a supply that is not a *taxable supply is taken to be 11/10 of what would be the *value of the supply if it were a taxable supply.

For the basic rules on the value of taxable supplies, see Subdivision 9‑C.

132 At the end of Division 188

Add:

188‑35 The value of loans

To the extent that a supply is constituted by a loan of *money, any repayment of the principal, and any obligation to repay the principal, is to be disregarded in working out the value of the supply.

133 Section 195‑1 (definition of approved form)

Repeal the definition, substitute:

approved form has the meaning given by section 995‑1 of the *ITAA 1997.

134 Section 195‑1

Insert:

Australian Business Register means the register established under section 24 of the A New Tax System (Australian Business Number) Act 1999.

135 Section 195‑1

Insert:

Australian Business Registrar means the Registrar of the *Australian Business Register.

136 Section 195‑1 (definition of Australian tax)

Repeal the definition.

137 Section 195‑1

Insert:

Australian tax, fee or charge means:

(a) a tax (however described) imposed under an *Australian law; or

(b) a fee or charge (however described) imposed under an Australian law and payable to an *Australian government agency.

138 Section 195‑1 (definition of cash accounting turnover threshold)

Omit “subsection 29‑40(2)”, substitute “subsection 29‑40(3)”.

139 Section 195‑1 (at the end of the definition of current annual turnover)

Add:

Note: This meaning is affected by section 188‑22.

140 Section 195‑1 (definition of customs duty)

Repeal the definition, substitute:

customs duty means any duty of customs imposed by that name under a law of the Commonwealth, other than:

(a) the A New Tax System (Goods and Services Tax Imposition—Customs) Act 1999; or

(b) the A New Tax System (Wine Equalisation Tax Imposition—Customs) Act 1999; or

(c) the A New Tax System (Luxury Car Tax Imposition—Customs) Act 1999.

141 Section 195‑1 (paragraphs (b) and (c) of the definition of essential prerequisite)

After “the entry to”, insert “, or the commencement of the practice of,”.

142 Section 195‑1 (definition of excisable goods)

Omit “section 4”, substitute “subsection 4(1)”

143 Section 195‑1 (paragraph (a) of the definition of first aid or life saving course)

Repeal the paragraph, substitute:

(a) principally involves training individuals in one or more of the following:

(i) first aid, resuscitation or other similar life saving skills;

(ii) surf life saving;

(iii) aero‑medical rescue; and

144 Section 195‑1 (paragraph (b) of the definition of first aid or life saving course)

Omit “non‑profit”.

145 Section 195‑1

Insert:

freight container means a container within the meaning of the Customs Convention on Containers, 1972, signed in Geneva on 2 December 1972, as affected by any amendment of the Convention that has come into force.

146 Section 195‑1 (definition of import)

Omit “*import”, substitute “import”.

147 Section 195‑1 (definition of importation of goods into Australia)

Repeal the definition.

148 Section 195‑1

Insert:

international transport means:

(a) in relation to the export of goods—the transport of the goods from their *place of export in Australia to a destination outside Australia (including loading and handling within Australia that is part of that transport); or

(b) in relation to the import of goods—the transport of the goods from a place outside Australia to their *place of consignment in Australia (excluding loading and handling within Australia).

149 Section 195‑1

Insert:

local entry has the meaning given by section 5‑30 of the A New Tax System (Wine Equalisation Tax) Act 1999.

150 Section 195‑1

Insert:

luxury car tax has the meaning given by section 27‑1 of the A New Tax System (Luxury Car Tax) Act 1999.

151 Section 195‑1 (definition of new residential premises)

Repeal the definition, substitute:

new residential premises means *residential premises that:

(a) have not previously been sold as residential premises and have not previously been the subject of a *long‑term lease; or

(b) have been created through *substantial renovations of a building; or

(c) have been built, or contain a building that has been built, to replace demolished premises on the same land.

To avoid doubt, if the residential premises are *new residential premises because of paragraph (b) or (c) of this definition, the new residential premises include land of which the new residential premises are a part.

152 Section 195‑1 (definition of partly creditable land transport)

Repeal the definition.

153 Section 195‑1

Insert:

place of consignment of goods means:

(a) if the goods are posted to Australia—the place in Australia to which the goods are addressed; or

(b) in any other case—the port or airport of final destination as indicated on the *transportation document.

154 Section 195‑1

Insert:

place of export of goods means:

(a) if the goods were posted from Australia—the place from which they were posted; or

(b) if paragraph (a) does not apply and the goods were packed in a *freight container—the place where they were so packed; or

(c) if the goods are self transported goods—the place, or last place, from which the goods departed Australia; or

(d) if paragraphs (a), (b) and (c) do not apply—the place, or first place, where the goods were placed on board a ship or aircraft for export from Australia.

155 Section 195‑1 (definition of potential residential land)

After “contain any”, insert “buildings that are”.

156 Section 195‑1 (at the end of the definition of projected annual turnover)

Add:

Note: This meaning is affected by sections 188‑22 and 188‑25.

157 Section 195‑1 (definition of residential premises)

Repeal the definition, substitute:

residential premises means land or a building that:

(a) is occupied as a residence; or

(b) is intended to be occupied, and is capable of being occupied, as a residence;

and includes a *floating home.

158 Section 195‑1

Insert:

retailer means an entity that, in the course or furtherance of *carrying on its *enterprise, sells *goods to people who buy them for private or domestic use or consumption.

159 Section 195‑1

Insert:

simplified accounting method means an arrangement in respect of which a determination under section 123‑5 is in force.

160 Section 195‑1 (definition of special education course)

Repeal the definition, substitute:

special education course means a course of education that provides special programs designed specifically for children with disabilities or students with disabilities (or both).

161 Section 195‑1

Insert:

substantial renovations of a building are renovations in which all, or substantially all, of a building is removed or replaced. However, the renovations need not involve removal or replacement of foundations, external walls, interior supporting walls, floors, roof or staircases.

162 Section 195‑1 (at the end of the definition of tax period)

Add “or 147‑25”.

163 Section 195‑1 (definition of taxable importation)

Omit “subsection 13‑5(1)”, substitute “subsections 13‑5(1) and 114‑5(1)”.

164 Section 195‑1

Insert:

transportation document includes the following:

(a) a consignment note;

(b) a house bill of lading;

(c) an ocean bill of lading;

(d) a house air waybill;

(e) a master air waybill;

(f) a sea waybill;

(g) a straight line air waybill;

(h) a sub‑master air waybill;

(i) other similar documents.

165 Section 195‑1 (at the end of the definition of value)

Add:

; and (d) value of a supply includes the meaning given by section 188‑35.

166 Section 195‑1

Insert:

wine tax has the meaning given by section 33‑1 of the A New Tax System (Wine Equalisation Tax) Act 1999.

167 Clause 1 of Schedule 2 (table item 14)

Omit “bottled”.

168 Schedule 3 (note)

Repeal the note, substitute:

Note 1: GST‑free supplies of medical aids and appliances are dealt with in section 38‑45.

Note 2: The second column of the table is not operative (see section 182‑15).

Part 2—Amendment of the A New Tax System (Luxury Car Tax) Act 1999

169 Paragraph 5‑10(3)(b)

Omit “imported”, substitute “*entered for home consumption”.

170 Paragraph 5‑20(1)(b)

After “tax”, insert “, fee or charge”.

171 After subsection 5‑20(1)

Insert:

(1A) If the supply of the *car is *GST‑free (to an extent) because of Subdivision 38‑P of the *GST Act, the *luxury car tax value of the car includes an amount equal to the amount of *GST that was not payable because of Subdivision 38‑P.

172 Subsection 7‑10(1)

Repeal the subsection, substitute:

(1) You make a taxable importation of a luxury car if:

(a) the *luxury car is *imported; and

(b) you *enter the car for home consumption.

Note: There is no registration requirement for taxable importations, and the importer need not be carrying on an enterprise.

173 Subsection 7‑10(4)

Omit all the words from and including “includes”, substitute “includes a reference to a car to which that item would apply apart from the operation of subsection 18(1) of the Customs Tariff Act 1995”.

174 Section 7‑15 (subparagraph (b)(i) of the definition of luxury car tax value)

Repeal the subparagraph, substitute:

(i) for the *international transport of the car and any car parts, accessories or attachments covered by subsection 7‑10(2) to their *place of consignment in Australia; and

175 Section 7‑15 (at the end of the definition of luxury car tax value)

Add:

; and (e) if the *importation of the car is *GST‑free (to an extent) because of paragraph 13‑10(b) of the *GST Act in conjunction with Subdivision 38‑P of that Act—an amount equal to the amount of *GST that was not payable because of paragraph 13‑10(b) and Subdivision 38‑P.

176 At the end of section 7‑15

Add:

(2) The Commissioner may, in writing:

(a) determine the way in which the amount paid or payable for a specified kind of transport or insurance is to be worked out for the purposes of paragraph (b) of the definition of luxury car tax value in subsection (1); and

(b) in relation to importations of a specified kind or importations to which specified circumstances apply, determine that the amount paid or payable for a specified kind of transport or insurance is taken, for the purposes of that paragraph, to be zero.

177 At the end of section 13‑20

Add:

(2) An officer of Customs (within the meaning of subsection 4(1) of the Customs Act 1901) may refuse to deliver the goods concerned unless the luxury car tax has been paid.

178 Subsection 13‑25(1)

Repeal the subsection, substitute:

(1) An amount of luxury car tax on a *taxable importation of a luxury car is not payable if:

(a) a security or undertaking described in section 162 of the Customs Act 1901 has been given; and

(b) the provisions of the regulations mentioned in paragraph 162(3)(a) of that Act are complied with; and

(c) the car is exported within the relevant period mentioned in paragraph 162(3)(b) of that Act.

Note: Section 162 of the Customs Act 1901 allows delivery of imported goods if the importer gives a security or undertaking to pay any customs duty, GST and luxury car tax relating to the importation.

(1A) An amount of luxury car tax on a *taxable importation of a luxury car is not payable if:

(a) a security or undertaking described in section 162A of the Customs Act 1901 has been given; and

(b) the car is not dealt with in contravention of regulations made for the purposes of that section; and

(c) either:

(i) the car is exported within the relevant period mentioned in paragraph 162A(5)(b) of that Act; or

(ii) if the car is goods described in subsection 162A(5A)—the car is exported before the end of the relevant day mentioned in paragraph 162A(5A)(b).

Note: Section 162A of the Customs Act 1901 allows delivery of imported goods if the importer gives a security or undertaking to pay any customs duty, GST and luxury car tax relating to the importation.

179 At the end of section 15‑5

Add:

(4) However, the return of a *luxury car to its supplier is not an *adjustment event if the return is for the purpose of repair or maintenance.

180 At the end of paragraph 15‑40(1)(c)

Add “, or the whole or a part of the debt has been due for 12 months or more”.

181 At the end of paragraph 15‑40(2)(a)

Add “taking into account any previous *luxury car tax adjustments for the supply”.

182 Paragraph 15‑40(2)(b)

Repeal the paragraph, substitute:

(b) the amount of luxury car tax (if any) that would be payable if the *price of the supply of the car (disregarding any previous *luxury car tax adjustments for the supply) was reduced by an amount equal to the sum of:

(i) the amount or amounts of the debt written off as bad; and

(ii) the amount of the debt that has been due for 12 months or more (other than amounts already written off).

183 Paragraph 15‑45(1)(a)

Omit “written off as bad”.

184 Paragraph 15‑45(1)(b)

Repeal the paragraph, substitute:

(b) you recover the whole or a part of the amount or amounts of the debt that have been written off as bad or due for 12 months or more.

185 Subsection 15‑45(2)

Repeal the subsection, substitute:

(2) The increasing luxury car tax adjustment is equal to:

(a) the amount of luxury car tax (if any) that would be payable if the *price of the supply of the car (disregarding any previous *luxury car tax adjustments for the supply) was reduced by the sum of:

(i) the amount or amounts of the debt previously written off as bad; and

(ii) the amount of the debt that has been due for 12 months or more (other than amounts already written off);

and then increased by an amount equal to the amount or amounts recovered; minus

(b) the amount of luxury car tax (if any) payable on the supply of the luxury car, taking into account any previous *luxury car tax adjustments for the supply.

186 After Division 15

Insert:

Division 16—GST groups and GST joint ventures

16‑1 What this Division is about

The representative member of a GST group deals with all of the luxury car tax liabilities and entitlements of the group. The joint venture operator of a GST joint venture deals with the luxury car tax liabilities and entitlements arising from the operator’s dealings on behalf of the other participants in the joint venture.

Subdivision 16‑A—Members of GST groups

16‑5 Who is liable for luxury car tax

(1) Luxury car tax payable on a *taxable supply of a luxury car, or a *taxable importation of a luxury car, for which a *member of a *GST group would (apart from this section) be liable:

(a) is payable by the *representative member; and

(b) is not payable by the member that would otherwise be liable (unless the member is the representative member).

(2) However, if the member is not the *representative member of the *GST group, this section only applies to luxury car tax payable on a *taxable importation of a luxury car if the tax is payable at a time when luxury car tax on *taxable supplies of luxury cars is normally payable by the representative member.

(3) This section has effect despite sections 5‑5 and 7‑5 (which are about liability for luxury car tax).

16‑10 Luxury car tax adjustments

(1) Any *luxury car tax adjustment that a *member of a *GST group has is to be treated as if:

(a) that member did not have the adjustment (unless that member is the *representative member); and

(b) the representative member had the adjustment.

(2) This section has effect despite section 13‑10 (which is about the effect of luxury car tax adjustments on net amounts).

Subdivision 16‑B—Participants in GST joint ventures

16‑15 Who is liable for luxury car tax

(1) Luxury car tax payable on a *taxable supply of a luxury car, or a *taxable importation of a luxury car, that the *joint venture operator of a *GST joint venture makes, on behalf of another *participant in the joint venture, in the course of activities for which the joint venture was entered into:

(a) is payable by the joint venture operator; and

(b) is not payable by the other participant.

(2) This section has effect despite sections 5‑5 and 7‑5 (which are about liability for luxury car tax).

16‑20 Luxury car tax adjustments

(1) Any *luxury car tax adjustment relating to any supply or *importation that the *joint venture operator of a *GST joint venture makes, on behalf of another *participant in the joint venture, in the course of activities for which the joint venture was entered into is to be treated as if:

(a) the other participant did not have the adjustment; and

(b) the joint venture operator had the adjustment.

(2) This section has effect despite section 13‑10 (which is about the effect of *luxury car tax adjustments on net amounts).

16‑25 Additional net amounts relating to GST joint ventures

The additional net amount relating to a *GST joint venture in section 51‑45 of the *GST Act:

(a) is increased by the amount of any luxury car tax on *taxable supplies of luxury cars for which the *joint venture operator is liable because of section 16‑15; and

(b) is increased or decreased (as the case requires) by the amount of any *luxury car tax adjustments that are adjustments of the joint venture operator because of section 16‑20.

187 Division 25 (heading)

Repeal the heading, substitute:

Division 25—Luxury cars

188 Subsection 25‑1(3)

Omit “year in which the supply of the car occurred”, substitute:

year in which:

(a) the supply of the car occurred; or

(b) the car was *entered for home consumption.

189 Section 25‑5

Repeal the section.

190 Section 27‑1 (definition of approved form)

Repeal the definition, substitute:

approved form has the meaning given by section 995‑1 of the *ITAA 1997.

191 Section 27‑1 (definition of Australian tax)

Repeal the definition.

192 Section 27‑1

Insert:

Australian tax, fee or charge has the meaning given by section 195‑1 of the *GST Act.

193 Section 27‑1

Insert:

enter for home consumption has the same meaning as in the Customs Act 1901.

194 Section 27‑1

Insert:

GST group has the meaning given by section 48‑5 of the *GST Act.

195 Section 27‑1

Insert:

GST joint venture has the meaning given by section 51‑5 of the *GST Act.

196 Section 27‑1 (definition of import)

Repeal the definition, substitute:

import means import goods into *Australia.

197 Section 27‑1

Insert:

international transport of a *car and any *car parts, accessories or attachments covered by subsection 7‑10(2) has the meaning given by section 195‑1 of the *GST Act.

198 Section 27‑1

Insert:

joint venture operator, for a *GST joint venture, has the meaning given by section 195‑1 of the *GST Act.

199 Section 27‑1

Insert:

member, in relation to a *GST group, has the meaning given by section 195‑1 of the *GST Act.

200 Section 27‑1

Insert:

participant, in relation to a *GST joint venture, has the meaning given by section 195‑1 of the *GST Act.

201 Section 27‑1

Insert:

place of consignment of a *car and any *car parts, accessories or attachments covered by subsection 7‑10(2) has the meaning given by section 195‑1 of the *GST Act.

202 Section 27‑1

Insert:

representative member, for a *GST group, has the meaning given by section 195‑1 of the *GST Act.

Part 3—Amendment of the A New Tax System (Wine Equalisation Tax) Act 1999

203 Section 2‑1 (note 1)

Repeal the note, substitute:

Note 1: Wine is widely defined in Subdivision 31‑A. It can apply to beverages fermented from any fruit or vegetable. It also extends to cider, perry, mead and sake.

204 Subsection 5‑5(2)

Omit “the dealing is not a taxable dealing unless”, substitute “an assessable dealing (other than a *customs dealing) is a taxable dealing only if”.

205 Subsection 5‑5(2) (note)

After “wine tax”, insert “, on assessable dealings (other than customs dealings),”.

206 Subsection 5‑5(4) (table item AD4b, 4th column)

Omit “time of removal”, substitute “time at which wine tax is payable under section 23‑5”.

207 Subsection 5‑5(4) (table item AD10, 4th column)

Omit “time of *local entry”, substitute “time at which wine tax is payable under section 23‑5”.

208 Subsection 5‑5(4) (table item AD14b, 4th column)

Omit “time of renewal”, substitute “time at which wine tax is payable under section 23‑5”.

209 At the end of subsection 5‑25(3)

Add:

; or (d) section 5 of the Sales Tax Amendment (Transitional) Act 1992 applies to the wine (whether or not the wine would, but for that section, have been subject to sales tax under the Sales Tax Assessment Act 1992).

210 Subsection 5‑30(5) (Local Entry Table, column 4)

Repeal the column.

211 Subsection 5‑30(5) (table item LE4, 2nd column)

Omit “87, 96, 206 or 207”, substitute “87 or 96”.

212 Subsection 5‑30(5) (table item LE4, 3rd column)

Omit “was the owner (within the meaning of the Customs Act 1901) of the wine immediately before the sale”, substitute “bought the wine”.

213 Subsection 5‑30(5) (table item LE13)

Repeal the item.

214 Subsection 5‑30(5) (table item LE15)

Omit “into Australia” (wherever occurring).

215 Sections 5‑35 and 5‑40

Repeal the sections.

216 Section 7‑5

Repeal the section, substitute:

7‑5 Exemption for dealings that are GST‑free supplies or non‑taxable importations

An *assessable dealing is not taxable if the dealing is:

(a) a *supply that is *GST‑free (other than because of Subdivision 38‑D (child care) of the *GST Act); or

(b) a *local entry relating to an *importation that is a *non‑taxable importation.

217 Subsection 7‑15(1)

After “item”, insert “15,”.

218 Subsection 7‑15(1)

Omit “, 23A, 23B, 24, 25A, 25B, 25C, 32A, 32B, 33A, 33B or 34”, substitute “, 24 or 33B”.

219 Subsection 7‑15(2)

Omit all the words from and including “includes”, substitute “includes a reference to goods to which that item would apply apart from the operation of subsection 18(1) of the Customs Tariff Act 1995”.

220 Section 17‑5 (table item CR9)

Repeal the item.

221 Section 17‑5 (table items CR11 and CR12)

Repeal the items, substitute:

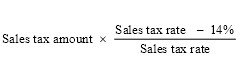

CR11 | Tax excluded from sale *price of *GST‑free supply of tax paid wine | You sold wine for a *price that excluded some or all of the wine tax previously *borne by you on the wine, and the sale was a *GST‑free supply of the wine. | wine tax excluded from sale *price | time of sale |

222 Subsection 17‑5(3) (table item CR13, 3rd column)

Omit “under *Customs supervision”.

223 Before section 21‑1

Insert:

Table of Subdivisions

21‑A General

21‑B Members of GST groups

21‑C Participants in GST joint ventures

224 After section 21‑1

Insert:

Subdivision 21‑A—General

225 Subsection 21‑5(1)

After “(if any)”, insert “payable by you”.

226 At the end of Division 21

Add:

Subdivision 21‑B—Members of GST groups

21‑40 Who is liable for wine tax

(1) Wine tax payable on a *taxable dealing for which a *member of a *GST group would (apart from this section) be liable to the tax:

(a) is payable by the *representative member; and

(b) is not payable by the member that would be so liable (unless the member is the representative member).

(2) However, if the member is not the *representative member of the *GST group, this section only applies to wine tax payable on a *customs dealing if the tax is payable at a time when wine tax on *taxable dealings is normally payable by the representative member.

(3) This section has effect despite subsection 5‑5(2) (which is about liability for wine tax).

21‑45 Who is entitled to wine tax credits

(1) If a *member of a *GST group would (apart from this section) be entitled to a *wine tax credit:

(a) the *representative member is entitled to the wine tax credit; and

(b) the member that would be so entitled is not entitled to the wine tax credit (unless the member is the representative member).

(2) This section has effect despite section 17‑5 (which is about entitlement to wine tax credits).

Subdivision 21‑C—Participants in GST joint ventures

21‑70 Who is liable for wine tax

(1) Wine tax payable on a *taxable dealing that the *joint venture operator of a *GST joint venture makes, on behalf of another *participant in the joint venture, in the course of activities for which the joint venture was entered into:

(a) is payable by the joint venture operator; and

(b) is not payable by the other participant.

(2) This section has effect despite subsection 5‑5(2) (which is about liability for wine tax).

21‑75 Who is entitled to wine tax credits

(1) If a *participant in a *GST joint venture would (apart from this section) be entitled to a *wine tax credit relating to a *taxable dealing that the *joint venture operator of the joint venture makes on the participant’s behalf:

(a) the joint venture operator is entitled to the wine tax credit; and

(b) the participant that would be so entitled is not entitled to the wine tax credit (unless the participant is the joint venture operator).

(2) This section has effect despite section 17‑5 (which is about entitlement to wine tax credits).

21‑80 Additional net amounts relating to GST joint ventures

The additional net amount relating to a *GST joint venture in section 51‑45 of the *GST Act:

(a) is increased by the amount of any wine tax on *taxable dealings for which the *joint venture operator is liable because of section 21‑70; and

(b) is decreased by the amount of any *wine tax credits to which the joint venture operator is entitled because of section 21‑75.

227 At the end of section 23‑5

Add:

(2) An officer of Customs (within the meaning of subsection 4(1) of the Customs Act 1901) may refuse to deliver the goods concerned unless the wine tax has been paid.

228 Section 27‑1

Repeal the section.

229 After subsection 27‑20(2)

Insert:

(2A) The directions given under subsection (2) may also take account of the provisions of the A New Tax System (Wine Equalisation Tax and Luxury Car Tax Transition) Act 1999.

230 Paragraph 27‑35(2)(a)

Repeal the paragraph.

231 Subdivisions 31‑A and 31‑B

Repeal the Subdivisions, substitute:

Subdivision 31‑A—Wine

31‑1 Meaning of wine

(1) Wine means any of these:

(a) *grape wine;

(b) *grape wine products;

(c) *fruit or vegetable wine;

(d) *cider or perry;

(e) *mead;

(f) *sake.

(2) However, wine does not include beverages that do not contain more than 1.15% by volume of ethyl alcohol.

31‑2 Meaning of grape wine

(1) Grape wine is a beverage that:

(a) is the product of the complete or partial fermentation of fresh grapes or products derived solely from fresh grapes; and

(b) complies with any requirements of the regulations, made for the purposes of section 31‑8, relating to grape wine.

(2) A beverage does not cease to be the product of the complete or partial fermentation of fresh grapes or products derived solely from fresh grapes merely because grape spirit, brandy, or both grape spirit and brandy, have been added to it.

Note: The concept of grape wine is used in Subdivision 9‑B to work out the taxable value of retail transactions involving wine produced from grapes. In the case of grape wine, you can choose to use the average wholesale price method of working out taxable values.

31‑3 Meaning of grape wine product

Grape wine product is a beverage that:

(a) contains at least 700 millilitres of *grape wine per litre; and

(b) has not had added to it, at any time, any ethyl alcohol from any other source, except:

(i) grape spirit; or

(ii) alcohol used in preparing vegetable extracts (including spices, herbs and grasses); and

(c) contains at least 8% by volume of ethyl alcohol, but not more than 22% by volume of ethyl alcohol; and

(d) complies with any requirements of the regulations, made for the purposes of section 31‑8, relating to grape wine products.

31‑4 Meaning of fruit or vegetable wine

Fruit or vegetable wine is a beverage that:

(a) is the product of the complete or partial fermentation of the juice or must of:

(i) fruit or vegetables; or

(ii) products derived solely from fruit or vegetables; and

(b) has not had added to it, at any time, any ethyl alcohol from any other source, except as specified in the regulations; and

(c) has not had added to it, at any time, any liquor or substance that gives colour or flavour, except as specified in the regulations; and

(d) contains at least 8% by volume of ethyl alcohol, but not more than 22% by volume of ethyl alcohol; and

(e) complies with any requirements of the regulations, made for the purposes of section 31‑8, relating to fruit or vegetable wine.

31‑5 Meaning of cider or perry

Cider or perry is a beverage that:

(a) is the product of the complete or partial fermentation of the juice or must of apples or pears; and

(b) has not had added to it, at any time, any ethyl alcohol from any other source, except as specified in the regulations; and

(c) has not had added to it, at any time, any liquor or substance (other than water or the juice or must of apples or pears) that gives colour or flavour, except as specified in the regulations; and

(d) complies with any requirements of the regulations, made for the purposes of section 31‑8, relating to cider or perry.

31‑6 Meaning of mead

Mead is a beverage that:

(a) is the product of the complete or partial fermentation of honey; and

(b) has not had added to it, at any time, any ethyl alcohol from any other source, except as specified in the regulations; and

(c) has not had added to it, at any time, any liquor or substance (other than honey) that gives colour or flavour, except as specified in the regulations; and

(d) complies with any requirements of the regulations, made for the purposes of section 31‑8, relating to mead.

31‑7 Meaning of sake

Sake is a beverage that:

(a) is the product of the complete or partial fermentation of rice; and

(b) has not had added to it, at any time, any ethyl alcohol from any other source, except as specified in the regulations; and

(c) has not had added to it, at any time, any liquor or substance that gives colour or flavour, except as specified in the regulations; and

(d) complies with any requirements of the regulations, made for the purposes of section 31‑8, relating to sake.

31‑8 Requirements for types of wine

(1) The regulations may specify requirements for these types of wine:

(a) *grape wine;

(b) *grape wine products;

(c) *fruit or vegetable wine;

(d) *cider or perry;

(e) *mead;

(f) *sake.

(2) The requirements for a particular type of wine may relate to any of the following:

(a) the substances that may be added to that type of wine;

(b) the quantities in which those substances may be added to that type of wine;

(c) the substances that must not be added to that type of wine;

(d) the substances that may be used in the production of that type of wine;

(e) the quantities in which those substances may be used in the production of that type of wine;

(f) the substances that must not be used in the production of that type of wine;

(g) the composition of that type of wine.

31‑9 Measuring alcoholic content

For the purposes of this Subdivision, the volume of ethyl alcohol in beverages is to be measured at 20°C and is to be calculated on the basis that the specific gravity of ethyl alcohol is 0.79067 (at 20°C in a vacuum).

232 Subdivision 31‑E

Repeal the Subdivision.

233 Section 33‑1 (definition of accompanied baggage)

Repeal the definition.

234 Section 33‑1 (definition of AOU connected with retail sales of grape wine)

Repeal the definition.

235 Section 33‑1 (definition of approved form)

Repeal the definition, substitute:

approved form has the meaning given by section 995‑1 of the *ITAA 1997.

236 Section 33‑1 (definition of beer)

Repeal the definition.

237 Section 33‑1

Insert:

cider or perry has the meaning given by section 31‑5.

238 Section 33‑1 (definition of eligible Australian traveller)

Repeal the definition.

239 Section 33‑1 (definition of eligible foreign traveller)

Repeal the definition.

240 Section 33‑1 (definition of export)

Omit “, and, in relation to an *eligible Australian traveller, includes taking the wine out of Australia as *accompanied baggage”.

241 Section 33‑1

Insert:

fruit or vegetable wine has the meaning given by section 31‑4.

242 Section 33‑1 (definition of grape wine)

Omit “Subdivision 31‑B”, substitute “section 31‑2”.

243 Section 33‑1

Insert:

grape wine product has the meaning given by section 31‑3.

244 Section 33‑1

Insert:

GST group has the meaning given by section 48‑5 of the *GST Act.

245 Section 33‑1 (definition of GST importation value)

After “the local entry”, insert “(disregarding any wine tax payable in respect of the local entry)”.

246 Section 33‑1

Insert:

GST joint venture has the meaning given by section 51‑5 of the *GST Act.

247 Section 33‑1 (definition of import)

Omit “*import”, substitute “import”.

248 Section 33‑1 (definition of importation of goods into Australia)

Repeal the definition.

249 Section 33‑1

Insert:

joint venture operator, for a *GST joint venture, has the meaning given by section 195‑1 of the *GST Act.

250 Section 33‑1

Insert:

mead has the meaning given by section 31‑6.

251 Section 33‑1

Insert:

member, in relation to a *GST group, has the meaning given by section 195‑1 of the *GST Act.

252 Section 33‑1

Insert:

non‑taxable importation has the meaning given by section 13‑10 and Division 42 of the *GST Act.

253 Section 33‑1

Insert:

participant, in relation to a *GST joint venture, has the meaning given by section 195‑1 of the *GST Act.

254 Section 33‑1

Insert:

representative member, for a *GST group, has the meaning given by section 195‑1 of the *GST Act.

255 Section 33‑1

Insert:

sake has the meaning given by section 31‑7.

Part 1—Amendments commencing on Royal Assent

1 Subsection 4(1)

Insert:

GST has the meaning given by section 195‑1 of the GST Act.

2 Subsection 4(1)

Insert:

GST Act means the A New Tax System (Goods and Services Tax) Act 1999.

3 Subsection 4(1)

Insert:

luxury car tax has the meaning given by section 27‑1 of the Luxury Car Tax Act.

4 Subsection 4(1)

Insert:

Luxury Car Tax Act means the A New Tax System (Luxury Car Tax) Act 1999.

5 Paragraph 71F(6)(b)

Omit “duty”, substitute “any duty, fee, charge or tax”.

6 Paragraphs 71F(6)(c) and (d)

Omit “duty”, substitute “the unpaid duty, fee, charge or tax (as appropriate)”.

7 Application

The amendments of subsection 71F(6) of the Customs Act 1901 made by this Part apply in relation to import entries communicated to Customs after the commencement of this Part.

8 At the end of subsection 162A(1)

Add “, GST or luxury car tax”.

Note: The heading to section 162A is altered by adding at the end “, GST and luxury car tax”.

9 Saving of regulations

Regulations that were made for the purposes of subsection 162A(1) of the Customs Act 1901 and in force immediately before the amendment of that subsection by this Part continue in force as if they had been made for the purposes of that subsection as amended by this Part. This does not prevent amendment or repeal of the regulations.

10 Subsection 162A(2)

Repeal the subsection, substitute:

(2) The CEO may accept a security given by a person for the payment of, or an undertaking by a person to pay, all of the following in relation to specified goods that are described in regulations made for the purposes of subsection (1) and that may be imported after a particular date or during a particular period:

(a) the duty, if any, that may become payable on the goods;

(b) the GST that may become payable on the taxable importation (as defined in the GST Act), if any, that is associated with the import of the goods;

(c) if a taxable importation of a luxury car (as defined in the Luxury Car Tax Act) is associated with the import of the goods—the luxury car tax that may become payable on that taxable importation.

If the CEO accepts the security or undertaking, a Collector may grant to a person who imports some or all of the specified goods permission to take delivery of the goods without payment of duty, GST or luxury car tax.

11 Saving of permissions

A permission granted under subsection 162A(2) of the Customs Act 1901 and in force immediately before the commencement of the amendments of section 162A of that Act by this Part continues in force as if the permission had been granted under that section as amended by this Part.

12 At the end of subsection 162A(5)

Add:

Note: GST and luxury car tax are not payable if duty is not payable because of subsection (5) (or would not be payable because of that subsection if it were otherwise payable). See section 171‑5 of the GST Act and section 13‑25 of the Luxury Car Tax Act.

13 Subsection 162A(7)

Omit all the words from and including “until” to and including “imported”, substitute:

until:

(a) no duty is, or may become, payable on goods to which the security relates that have been imported; and

(b) no GST is, or may become, payable on the taxable importation (as defined in the GST Act), if any, that is associated with the import of the goods; and

(c) no luxury car tax is, or may become, payable on the taxable importation of a luxury car (as defined the Luxury Car Tax Act), if any, that is associated with the import of the goods.

14 Subsection 162A(8)

Repeal the subsection, substitute:

(8) If the circumstances described in paragraph (5)(a) or (b) or (5A)(a) or (b) exist in relation to the goods:

(a) a security relating to the goods may be enforced; and

(b) if an undertaking has been given to pay the amount of the duty (if any), GST (if any) and luxury car tax (if any) associated with the import of the goods—the amount may be recovered at any time in a court of competent jurisdiction by proceedings in the name of:

(i) the CEO; or

(ii) the Regional Director for a State or Territory.

15 Application