A New Tax System (Tax Administration) Act (No. 1) 2000

No. 44, 2000

A New Tax System (Tax Administration) Act (No. 1) 2000

No. 44, 2000

A New Tax System (Tax Administration) Act (No. 1) 2000

No. 44, 2000

1 Short title...................................

2 Commencement...............................

3 Schedule(s)..................................

Schedule 1—PAYG instalments and trusts

Taxation Administration Act 1953

Schedule 2—Fringe benefits tax instalments

Fringe Benefits Tax Assessment Act 1986

Taxation Administration Act 1953

Schedule 3—Consequential amendments relating to collection and recovery rules

A New Tax System (Family Assistance) (Administration) Act 1999

A New Tax System (Luxury Car Tax) Act 1999

A New Tax System (Tax Administration) Act 1999

A New Tax System (Wine Equalisation Tax) Act 1999

Fringe Benefits Tax Assessment Act 1986

Higher Education Funding Act 1988

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Petroleum Resource Rent Tax Assessment Act 1987

Social Security Act 1991

Social Security (Administration) Act 1999

Student Assistance Act 1973

Superannuation Contributions Tax (Assessment and Collection) Act 1997

Superannuation Contributions Tax (Members of Constitutionally Protected Superannuation Funds) Assessment and Collection Act 1997

Taxation Administration Act 1953

Termination Payments Tax (Assessment and Collection) Act 1997

Tobacco Charges Assessment Act 1955

Trust Recoupment Tax Assessment Act 1985

Veterans’ Entitlements Act 1986

Wool Tax (Administration) Act 1964

Schedule 4—Miscellaneous amendments

A New Tax System (Indirect Tax Administration) Act 1999

A New Tax System (Pay As You Go) Act 1999

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Schedule 5—Consequential amendment of Chapter 6 (the Dictionary) of the Income Tax Assessment Act 1997

A New Tax System (Tax Administration) Act (No. 1) 2000

No. 44, 2000

An Act to implement A New Tax System by amending the law about taxation, and for related purposes

[Assented to 3 May 2000]

This Act may be cited as the A New Tax System (Tax Administration) Act (No. 1) 2000.

(1) Subject to this section, this Act commences, or is taken to have commenced, immediately after the commencement of section 1 of the A New Tax System (Tax Administration) Act 1999.

(2) Schedule 2 (except items 2, 5, 9 and 10 and subitem 11(2)) commences on 1 April 2000.

(3) Items 2, 5, 9 and 10, and subitem 11(2), of Schedule 2 commence on 1 April 2001.

(4) Item 34 of Schedule 3 commences, or is taken to have commenced, on 1 July 2000, immediately after the commencement of item 49 of Schedule 11 to the A New Tax System (Tax Administration) Act 1999.

(5) Item 35 of Schedule 3 commences, or is taken to have commenced, on 1 July 2000, immediately after the commencement of item 58 of Schedule 11 to the A New Tax System (Tax Administration) Act 1999.

(6) Items 46 and 47 of Schedule 3 commence, or are taken to have commenced:

(a) immediately after the commencement of item 6 of Schedule 2 to the Youth Allowance Consolidation Act 2000; or

(b) immediately after the commencement of section 1 of the A New Tax System (Tax Administration) Act 1999;

whichever is the later.

(7) Item 48 of Schedule 3 commences, or is taken to have commenced:

(a) on 20 March 2000; or

(b) immediately after the commencement of section 1 of the A New Tax System (Tax Administration) Act 1999;

whichever is the later.

(8) Item 68 of Schedule 3 commences, or is taken to have commenced, immediately after the commencement of Schedule 12 to the A New Tax System (Tax Administration) Act 1999.

(9) Items 39, 40, 52, 53, 73 and 74 of Schedule 3 commence, or are taken to have commenced, on 1 July 2000.

(10) Item 1 of Schedule 4 to this Act commences, or is taken to have commenced, on 1 July 2000, immediately before the commencement of Schedule 1 to the A New Tax System (Indirect Tax Administration) Act 1999.

(11) Items 4 to 9 of Schedule 4 to this Act commence, or are taken to have commenced, on 1 July 2000, immediately after the commencement of the amendments of the Income Tax Assessment Act 1936 made by Part 1 of Schedule 5 to the A New Tax System (Tax Administration) Act 1999.

Subject to section 2, each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

1 Section 45‑10 in Schedule 1 (note)

Repeal the note, substitute:

Note 1: Section 45‑450 provides for how this Part applies to a trustee covered by any of items 6 to 12 of the table in section 9‑1 of the Income Tax Assessment Act 1997. In most respects, the trust is treated like a company.

Note 2: This Part also applies to a trustee covered by item 5 of the table in section 9‑1 of the Income Tax Assessment Act 1997, but only to the extent set out in section 45‑455, and the rest of Subdivision 45‑N, in this Schedule.

2 Paragraph 45‑115(1)(b) in Schedule 1

Omit “under subsection 45‑320(5)”.

3 Subsection 45‑120(1) in Schedule 1 (note 1)

Omit “An amount of statutory income is not”, substitute “No other amount is”.

4 Subsection 45‑120(1) in Schedule 1 (note 2)

After “the period”, insert “(except in some cases)”.

5 Subparagraph 45‑215(1)(b)(ii) in Schedule 1

Omit “the amount notified to you by the Commissioner”, substitute “worked out”.

6 At the end of section 45‑260 in Schedule 1

Add:

Exception for corporate limited partnerships

(4) Your instalment income for the current period does not include an amount for a partnership that is a *corporate limited partnership for the income year that is or includes that period.

Note: Your instalment income will still include a distribution by the partnership that is ordinary income. See section 45‑120.

7 Subdivision 45‑I in Schedule 1 (heading)

Repeal the heading, substitute:

8 Group heading before section 45‑280 in Schedule 1

Repeal the heading.

9 Subsection 45‑280(2) in Schedule 1

Repeal the subsection, substitute:

(2) For the purposes of the formula in subsection (1):

your assessable income from the trust for the last income year means so much of a share of the trust’s net income for an income year as:

(a) Division 6 of Part III of the Income Tax Assessment Act 1936 included in your assessable income for the most recent income year:

(i) that ended before the start of the current period; and

(ii) for which you have an assessment, or for which the Commissioner has notified you that you do not have a taxable income; and

(b) is not attributable to a *capital gain made by the trust.

Note: For exceptions to paragraph (b), see section 45‑290.

10 At the end of section 45‑280 in Schedule 1

Add:

Exception for corporate unit trusts and public trading trusts

(4) Your instalment income for the current period does not include an amount for a trust if the trustee is liable to be assessed, and to pay tax, under section 102K or 102S of the Income Tax Assessment Act 1936 for the income year that is or includes that period.

Note: Your instalment income will still include a distribution by the trust that is ordinary income. See section 45‑120.

11 After section 45‑280 in Schedule 1

Insert:

(1) This section sets out cases where paragraph (b) of the definition of your assessable income from the trust for the last income year in subsection 45‑280(2) does not apply.

(2) It does not apply in the case of:

(a) an eligible ADF (as defined in section 267 of the Income Tax Assessment Act 1936) for the income year that is or includes the current period; or

(b) an eligible superannuation fund (as defined in that section) for that year; or

(c) a pooled superannuation trust (as defined in that section) for that year.

(3) It does not apply in the case of a *life insurance entity or *registered organisation to the extent that the share of the trust’s net income is included in the *CS/RA class of its assessable income for the income year that is or includes the current period.

Note: The CS/RA class relates to the Complying Superannuation/Roll‑over Annuity aspect of the entity’s business.

12 Group heading before section 45‑300 in Schedule 1

Repeal the heading.

13 Section 45‑300 in Schedule 1

Repeal the section.

14 Subsection 45‑405(1) in Schedule 1

Omit “under Subdivision 45‑J”.

15 Subsection 45‑405(2) in Schedule 1

Omit “in applying Subdivision 45‑J”.

16 At the end of Division 45 in Schedule 1

Add:

Table of sections

Trustees to whom this Part applies

45‑450 Trustees to whom a single instalment rate is given

45‑455 Trustees to whom several instalment rates are given

45‑460 Rest of Subdivision applies only to multi‑rate trustees

45‑465 Meaning of instalment income

45‑468 Multi‑rate trustee may pay quarterly instalments on the basis of GDP‑adjusted notional tax

How Commissioner works out instalment rate and notional tax for a multi‑rate trustee

45‑470 Working out instalment rate

45‑473 Commissioner must notify you of notional tax

45‑475 Working out your notional tax

45‑480 Working out your adjusted taxable income

45‑483 Meaning of reduced beneficiary’s share and reduced no beneficiary’s share

45‑485 Working out your adjusted withholding income

How Commissioner works out benchmark instalment rate and benchmark tax for a multi‑rate trustee

45‑525 When Commissioner works out benchmark instalment rate and benchmark tax

45‑530 How Commissioner works out benchmark instalment rate

45‑535 Working out your benchmark tax

(1) This Part (except Subdivision 45‑D) applies to a trustee covered by any of items 6 to 12 of the table in section 9‑1 of the Income Tax Assessment Act 1997.

Note: Subdivision 45‑D is about quarterly payers who pay on the basis of GDP‑adjusted notional tax.

(2) Such a trustee is called a single‑rate trustee.

(3) This Part (except Subdivision 45‑D) applies to the trustee of a trust that is a *corporate unit trust, or a *public trading trust, for an income year as if the trustee had a taxable income for the income year equal to the net income of the trust for the income year.

Trustee previously assessed in respect of beneficiary

(1) This Part also applies for an income year (the current year), to the trustee of a trust, in respect of a beneficiary of the trust, if for a previous income year the trustee of the trust was liable to be assessed, and to pay tax, under subsection 98(1) or (2) of the Income Tax Assessment Act 1936 in respect of that beneficiary.

(2) However, this Part does not apply for the current year to the trustee in respect of that beneficiary if:

(a) for that previous income year the trustee was liable to be assessed, and to pay tax, under subsection 98(1) of the Income Tax Assessment Act 1936 in respect of that beneficiary; and

(b) that beneficiary will no longer be under a legal disability, or it is reasonable to expect that he or she will no longer be under a legal disability, at the end of the current year.

Trustee previously assessed under section 99 or 99A

(3) This Part also applies for an income year to the trustee of a trust if for a previous income year the trustee was liable to be assessed, and to pay tax, under section 99 or 99A of the Income Tax Assessment Act 1936.

Multiple applications of this Part to the same trustee for the same income year

(4) The application of this Part for an income year, to the trustee of a trust, in respect of a beneficiary of the trust, because of subsection (1), is distinct from, and additional to, each of the following:

(a) the application of this Part for that income year, to the trustee of the trust, in respect of another beneficiary;

(b) the application of this Part for that income year, to the trustee of the trust, because of subsection (3);

(c) the application of this Part for that income year to a beneficiary of the trust.

(5) The application of this Part for an income year, to the trustee of a trust, because of subsection (3), is distinct from, and additional to, each of the following:

(a) the application of this Part for that income year, to the trustee of the trust, in respect of a beneficiary of the trust, because of subsection (1);

(b) the application of this Part for that income year to a beneficiary of the trust.

(6) A multi‑rate trustee is a trustee to whom this Part applies because of this section.

The rest of this Subdivision applies to you if, and only if, you are a *multi‑rate trustee. (It applies instead of Subdivisions 45‑J and 45‑K.)

Note: Except as provided in the rest of this Subdivision or elsewhere, this Part applies according to its terms to a multi‑rate trustee. For example, a multi‑rate trustee can become an annual payer under Subdivision 45‑E.

Your instalment income for a period is the whole of the trust’s *instalment income for that period.

Subdivision 45‑D (about quarterly payers who pay on the basis of GDP‑adjusted notional tax) applies to you in the same way as it applies to an individual.

(1) An instalment rate that the Commissioner gives you must be the percentage worked out to 2 decimal places (rounding up if the third decimal place is 5 or more) using the formula:

However, the instalment rate must be a nil rate if either component of the formula is nil.

(2) For the purposes of the formula in subsection (1):

base assessment instalment income means so much of the assessable income of the trust, as worked out for the purposes of the *base assessment, as the Commissioner determines is *instalment income of the trust for the *base year.

(3) The base assessment is the latest assessment for the most recent income year for which an assessment has been made of the tax payable by you:

(a) under subsection 98(1) or (2) of the Income Tax Assessment Act 1936 in respect of the same beneficiary; or

(b) under section 99 or 99A of the Income Tax Assessment Act 1936;

as appropriate.

(4) However, if the Commissioner is satisfied that there is a later income year for which no tax is payable as mentioned in subsection (3), the base assessment is the latest return or other information from which an assessment of tax so payable for that income year would have been made.

(5) The base year is the income year to which the *base assessment relates.

(1) When the Commissioner gives you the instalment rate, he or she must also notify you of the amount of your *notional tax, as worked out for the purposes of working out the instalment rate.

(2) The Commissioner may incorporate notice of the instalment rate and the amount of your *notional tax in notice of your assessment.

Notional tax if no withholding income

(1) Your notional tax is your *adjusted tax (worked out under section 45‑340) on your *adjusted taxable income (worked out under section 45‑480) for the *base year.

Notional tax if trust has withholding income

(2) However, your notional tax (as worked out under subsection (1)) is reduced if the trust’s assessable income for the *base assessment includes amounts in respect of *withholding payments (except *non‑quotation withholding payments).

(3) It is reduced (but not below nil) by your *adjusted tax (worked out under section 45‑340) on your *adjusted withholding income (worked out under section 45‑485) for the *base year.

Commissioner may take into account actual and proposed changes to the law

(4) Subsections 45‑325(4) and (5) apply for the purposes of working out your *notional tax under this section.

(1) Your adjusted taxable income for the *base year is worked out using the formula:

(2) For the purposes of the formula in subsection (1):

adjusted net income of the trust means the net income of the trust, as worked out for the purposes of the *base assessment and:

(a) reduced by any *net capital gain included in the trust’s assessable income as so worked out; and

(b) increased by any deductions for *tax losses that were made in so working out that net income; and

(c) reduced by the amount of any tax loss, to the extent that it can be carried forward for working out the trust’s net income for the next income year.

reduced net income of the trust means the net income of the trust, as worked out for the purposes of the *base assessment and reduced by any *net capital gain included in the trust’s assessable income as so worked out.

relevant share means the *reduced beneficiary’s share, or the *reduced no beneficiary’s share, as appropriate, of the net income of the trust, as worked out for the purposes of the *base assessment.

(1) If the trustee of a trust is liable to be assessed, and to pay tax, for an income year under subsection 98(1) or (2) of the Income Tax Assessment Act 1936 in respect of a particular beneficiary, the reduced beneficiary’s share of the net income is the amount on which the trustee is so liable to be assessed and to pay tax, except so much of that amount as is attributable to a *net capital gain included in the trust’s assessable income for that income year.

(2) If the trustee of a trust is liable to be assessed, and to pay tax, for an income year under section 99 or 99A of the Income Tax Assessment Act 1936, the reduced no beneficiary’s share of the net income is the amount on which the trustee is so liable to be assessed and to pay tax, except so much of that amount as is attributable to a *capital gain made by the trust during that income year.

(1) Your adjusted withholding income for the *base year is worked out using the formula:

(2) For the purposes of the formula in subsection (1):

net withholding income of the trust means:

• the total of the amounts included in the trust’s assessable income for the *base assessment in respect of *withholding payments (except *non‑quotation withholding payments);

reduced by:

• the trust’s deductions for that year, as used in making that assessment, to the extent that they reasonably relate to those amounts.

reduced net income of the trust has the meaning given by subsection 45‑480(2).

relevant share has the meaning given by subsection 45‑480(2).

(1) The Commissioner may work out your *benchmark instalment rate for an income year (the variation year) if, under section 45‑205, you choose an instalment rate to work out the amount of your instalment for an *instalment quarter in that year.

(2) The Commissioner may work out your *benchmark tax for an income year (the variation year) if, under paragraph 45‑112(1)(b) or (c), the amount of your instalment for an *instalment quarter in an income year is worked out on the basis of your estimate of your *benchmark tax for that income year.

(3) The Commissioner may work out your *benchmark tax for an income year (the variation year) if, under paragraph 45‑115(1)(c) or 45‑175(1)(b), you estimate the amount of your annual instalment for that year.

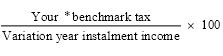

(1) Your benchmark instalment rate for the variation year is the percentage worked out to 2 decimal places (rounding up if the third decimal place is 5 or more) using the formula:

However, your benchmark instalment rate is a nil rate if either component of the formula is nil.

(2) For the purposes of the formula in subsection (1):

variation year instalment income means so much of the trust’s assessable income for the variation year as the Commissioner determines is *instalment income for that year.

Benchmark tax if no withholding income

(1) Your benchmark tax is your *adjusted assessed tax (worked out under section 45‑375) on the *reduced beneficiary’s share, or the *reduced no beneficiary’s share, as appropriate, of the net income of the trust for the variation year.

Benchmark tax if you had withholding income

(2) However, your benchmark tax (as worked out under subsection (1)) is reduced if the trust’s assessable income for the variation year includes amounts in respect of *withholding payments.

(3) It is reduced (but not below nil) by the total amount of the credits to which you are entitled for the variation year under section 18‑25 (for amounts withheld from the withholding payments).

Repeal the section, substitute:

(1) An employer is entitled to a credit when the Commissioner:

(a) makes an assessment of the tax payable by the employer for a year of tax; or

(b) determines that no tax is payable.

Note: The employer’s first return for the year of tax is treated as an assessment: see section 72.

(2) The credit is equal to:

• the total of each instalment (if any) payable by the employer for the year of tax;

reduced by:

• the total of any credits the employer has claimed under section 112A because of one or more instalments of tax for the year of tax.

Note: An employer can claim a credit under section 112A in some cases where the amount by reference to which an instalment is worked out reduces during the year of tax.

(3) The making of the assessment or determination, and the resulting credit entitlement, do not affect the liability to pay an instalment.

Note: How the credit is applied is set out in Division 3 of Part IIB of the Taxation Administration Act 1953.

2 Subsections 110(1), (2) and (3)

Repeal the subsections, substitute:

(1) An employer’s notional tax amount for a year of tax (the current year) as at a particular time (the test time) is worked out using the table, except as provided in subsections (3), (4) and (5).

Working out an employer’s notional tax amount | ||

Item | In this case: | The notional tax amount is: |

1 | No other item applies | the amount of the employer’s tax for the most recent year of tax (the base year) for which the Commissioner has made an assessment before the test time. |

2 | Before the test time, the Commissioner has determined that no tax is payable by the employer for a year of tax, and there is no later year of tax for which the Commissioner has made an assessment of the employer’s tax before the test time | nil |

3 | There is no year of tax for which the Commissioner has, before the test time, made an assessment of the employer’s tax or determined that no tax is payable by the employer | nil |

4 | The notional tax amount would otherwise be worked out under item 1 and: (a) the rate of tax declared by the Parliament for the current year is different from the rate declared for the base year; and (b) the regulations provide for varying the notional tax amount of employers for the current year | if the test time is before the prescribed day—the notional tax amount worked out under item 1; or if the test time is on and after the prescribed day—that amount as varied in accordance with the regulations. |

Note: The employer’s first return for the year of tax is treated as an assessment: see section 72.

(3) The Commissioner may determine that the employer’s notional tax amount for the current year is such amount as the Commissioner estimates will be the tax payable by the employer for that year, if the Commissioner has reason to believe that that tax will exceed:

(a) if the notional tax amount would otherwise be worked out under item 1 or 4 of the table in subsection (1)—the amount of the employer’s tax for the base year; or

(b) if the notional tax amount would otherwise be worked out under item 2 or 3 of the table in subsection (1)—nil.

Repeal the subsection, substitute:

(1) The amount of an instalment of tax of an employer for a year of tax that becomes due and payable on the 21st day after the end of a quarter is the amount worked out using this formula, if the amount is positive:

Otherwise, the amount of the instalment is nil.

Note: If the notional tax amount is too small, the instalment may not be payable: see subsection (2).

(1A) For the purposes of the formula in subsection (1):

notional tax amount means the employer’s notional tax amount for the year of tax, as at the end of the last day of that quarter.

previous credits means the total of any credits the employer has claimed under section 112A because of one or more instalments of tax for the same year of tax that became due and payable before that day.

previous instalments means the total of any instalments of tax for the same year of tax that became due and payable by the employer before that day.

After “year of tax” (first occurring), insert “that would otherwise become due and payable by an employer on the 21st day after the end of a quarter”.

Omit “or (2)”.

6 At the end of subsection 111(2)

Add:

; and (c) unless that quarter is the first quarter in the year of tax—because of one or more previous applications of this subsection, the instalment that would otherwise have become due and payable by the employer on the 21st day after the end of the previous quarter is not payable.

7 Subsections 112(4), (4A) and (5)

Repeal the subsections.

Insert:

(1) If an amount worked out using the formula in subsection 111(1) is negative, the employer is entitled to claim a credit equal to that amount, expressed as a positive amount.

Note: This will happen if the notional tax amount has reduced since the end of an earlier quarter because, for example, the employer has made an estimate under section 112 of its tax for the current year.

(2) A claim for a credit must be made in the approved form on or before the 21st day after the end of the quarter.

Note: How the credit is applied is set out in Division 3 of Part IIB of the Taxation Administration Act 1953.

(1) An employer is liable to pay the general interest charge under this section if:

(a) in order to determine the amount of an instalment of tax (the underpaid instalment) of the employer for a year of tax, an amount (whether positive, negative or nil) (the actual amount) was worked out using the formula in subsection 111(1); and

(b) because of subsection 110(5), the notional tax amount used in working out the actual amount was an estimate by the employer under subsection 112(1); and

(c) that notional tax amount is less than 90% of the employer’s tax assessed for the year of tax; and

(d) that assessed tax has become due and payable.

Note: Paragraph (1)(b) is not satisfied if the notional tax amount used in working out the actual amount was estimated tax worked out under subsection 112(3) because the Commissioner disagrees with the employer’s estimate.

(2) The employer is liable to pay the charge, for each day in the GIC period, on the amount (if any) by which the actual amount is less than the amount (whether positive, negative or nil) worked out using the formula:

(3) For the purposes of the formula in subsection (2):

minimum tax amount means the lesser of:

(a) the amount that, apart from subsection 110(5), would have been the notional tax amount used in working out the actual amount; and

(b) the employer’s tax assessed for the year of tax.

previous credits means the total of any credits the employer has claimed under section 112A because of one or more instalments of tax for the same year of tax that became due and payable before that day.

previous instalments means the total of any instalments of tax for the same year of tax that became due and payable by the employer before the day on which the underpaid instalment became due and payable (or would have become due and payable if the actual amount had been positive).

(4) The amount of the general interest charge is taken to be additional tax payable under this section.

Repeal the note, substitute:

Note: This will happen if the notional tax amount has reduced since the end of an earlier quarter because, for example:

10 Subsection 136(1)

Insert:

notional tax amount has the meaning given by section 110.

11 Application of amendments

(1) The amendments made by this Schedule (except items 2, 5, 9 and 10) apply in relation to instalments of tax for the year of tax starting on 1 April 2000 and all later years of tax.

(2) The amendments made by items 2, 5, 9 and 10 apply in relation to instalments of tax for the year of tax starting on 1 April 2001 and all later years of tax.

12 Subsection 8AAB(5) (table item 2)

Omit “112”, substitute “112B”.

1 Section 225

Omit “for the purpose of enabling the collection of tax”, substitute “or Subdivision 260‑A in Schedule 1 to the Taxation Administration Act 1953, for the purpose of enabling the collection of an amount”.

2 Section 13‑20 (note)

Renumber as note 1.

3 At the end of section 13‑20

Add:

Note 2: For provisions about collection and recovery of luxury car tax on taxable importations of luxury cars, see Part 4‑15 in Schedule 1 to the Taxation Administration Act 1953 and Division 3 of Part VI of that Act.

4 After subitem 2(4) of Schedule 2

Insert:

(4A) Despite subitems (2), (3) and (4), nothing can be done under Subdivision 255‑B, 255‑C or 260‑A in Schedule 1 to the Taxation Administration Act 1953 before 1 July 2000.

5 Section 23‑5 (note)

Renumber as note 1.

6 At the end of section 23‑5

Add:

Note 2: For provisions about collection and recovery of wine tax on customs dealings, see Part 4‑15 in Schedule 1 to the Taxation Administration Act 1953 and Division 3 of Part VI of that Act.

7 Subsection 101(1)

Omit “92, 93, 94, 95, 100, 129, 130 and 131”, substitute “93, 100 and 129”.

8 Subsection 101(2)

Omit “94, 95, 100, 129, 130 and 131”, substitute “100 and 129”.

9 Saving

A reference to section 92, 94, 130 or 131 of the Fringe Benefits Tax Assessment Act 1986 (the FBTA Act) in an item in Part 3 of Schedule 2 to the A New Tax System (Tax Administration) Act 1999 includes a reference to that section as it had effect, before its repeal, because of section 101 of the FBTA Act.

10 At the end of section 103

Add:

Note: For provisions about collection and recovery of instalments of fringe benefits tax, see Part 4‑15 in Schedule 1 to the Taxation Administration Act 1953.

11 Subsection 106U(1)

After “(Assessment Act)”, insert “, and Part 4‑15 in Schedule 1 to the Taxation Administration Act 1953,”.

12 Subsection 106U(1)

Omit “that Act”, substitute “the Assessment Act”.

13 At the end of subsection 106U(1)

Add:

Note: Part 4‑15 in Schedule 1 to the Taxation Administration Act 1953 deals with collection and recovery of amounts on and after 1 July 2000, replacing some provisions in Division 1 of Part VI of the Income Tax Assessment Act 1936.

Note: The heading to section 106U is altered by omitting “Income Tax Assessment Act” and substituting “tax legislation”.

14 After subsection 128C(1)

Insert:

Application

(1A) The Commissioner must not exercise his or her power under subsection (1) on or after 1 July 2000.

(1B) Subsections (2) and (5) do not apply in relation to withholding tax that becomes due and payable on or after 1 July 2000.

Note: For provisions about collection and recovery of withholding tax and other amounts on or after 1 July 2000, see Part 4‑15 in Schedule 1 to the Taxation Administration Act 1953.

15 Subsection 128C(9)

Repeal the subsection.

16 After subsection 128NB(3)

Insert:

Application

(3A) The Commissioner must not exercise his or her power under paragraph (3)(b) on or after 1 July 2000.

Note: For provisions about collection and recovery of tax on or after 1 July 2000, see Part 4‑15 in Schedule 1 to the Taxation Administration Act 1953.

17 At the end of section 160ARDZ

Add:

Application

(3) The Commissioner must not exercise his or her power under paragraph (1)(b) on or after 1 July 2000.

(4) Subsection (2) does not apply in relation to untainting tax that becomes due and payable on or after 1 July 2000.

Note: For provisions about collection and recovery of untainting tax on or after 1 July 2000, see Part 4‑15 in Schedule 1 to the Taxation Administration Act 1953.

18 At the end of section 160ARDZB

Add:

Application

(2) Subsection (1) does not apply in relation to any untainting tax or additional tax that becomes due and payable on or after 1 July 2000.

Note: For provisions about collection and recovery of untainting tax and additional tax on or after 1 July 2000, see Part 4‑15 in Schedule 1 to the Taxation Administration Act 1953.

19 At the end of section 204

Add:

Note: For provisions about collection and recovery of income tax and related amounts, see Part 4‑15 in Schedule 1 to the Taxation Administration Act 1953.

20 Subsection 205(3)

Omit “other provision of this Act”, substitute “provision of this or any other Act”.

21 Subsection 206(3)

Omit “other provision of this Act”, substitute “provision of this or any other Act”.

22 Paragraph 208(3)(b)

Omit “other provision of this Act”, substitute “provision of this or any other Act”.

23 Paragraph 209(3)(b)

Omit “other provision of this Act”, substitute “provision of this or any other Act”.

24 Subsection 214(3)

Omit “other provision of this Act”, substitute “provision of this or any other Act”.

25 Subsection 215(7)

Omit “other provision of this Act”, substitute “provision of this or any other Act”.

26 Subsection 216(4)

Omit “other provision of this Act”, substitute “provision of this or any other Act”.

27 Subsection 218(8)

Omit “other provision of this Act”, substitute “provision of this or any other Act”.

28 Subsection 220(9)

After “section”, insert “(including the extended operation that this section has because of any provision of this or any other Act)”.

29 Paragraph 221AZKC(5)(a)

Omit “section 206”, substitute “Subdivision 255‑B in Schedule 1 to the Taxation Administration Act 1953”.

30 Paragraph 221AZKC(5)(b)

Omit “section 206”, substitute “Subdivision 255‑B in Schedule 1 to the Taxation Administration Act 1953”.

31 Subsection 221AZKC(8)

Omit “206, 208, 209, 214, 254, 255, 258 and 259”, substitute “254 and 255”.

32 Subsection 221R(1A)

Repeal the subsection (except the note), substitute:

Application

(1A) Subsection (1) does not apply in relation to:

(a) an amount payable under this Division that becomes due and payable on or after 1 July 2000; or

(b) an amount that becomes due and payable on or after that day, and is taken to be income tax for the purposes of this Division because of any provision of this or any other Act.

33 At the end of section 221YHZW

Add:

Application

(2) The Commissioner must not exercise his or her power under paragraph (1)(b) on or after 1 July 2000.

Note: For provisions about collection and recovery of TFN withholding tax on or after 1 July 2000, see Part 4‑15 in Schedule 1 to the Taxation Administration Act 1953.

34 Subsection 222AFA(5)

Omit “Part 4‑10 in Schedule 1 to the Taxation Administration Act 1953”, substitute “Part 4‑15 in Schedule 1 to the Taxation Administration Act 1953,”.

35 Subsection 222ANA(4)

Omit “Part 4‑10”, substitute “Part 4‑15”.

36 Paragraph 258(3)(b)

Omit “other provision of this Act”, substitute “provision of this or any other Act”.

37 Paragraph 259(3)(b)

Omit “other provision of this Act”, substitute “provision of this or any other Act”.

38 Subsection 3‑5(3)

Omit “Division 1 (sections 204 to 220) of Part VI of the Income Tax Assessment Act 1936”, substitute “sections 204, 213, 214A and 219 of the Income Tax Assessment Act 1936 and Part 4‑15 in Schedule 1 to the Taxation Administration Act 1953”.

39 Subsection 65(5)

Repeal the subsection.

40 Saving

Despite the repeal of subsection 65(5) of the Petroleum Resource Rent Tax Assessment Act 1987 by item 39, that subsection continues to have effect in relation to an exercise of the Commissioner’s power under section 84 of that Act before 1 July 2000.

41 Subsection 65(12)

Omit “83, 84, 86, 87, 88, 89, 92, 109, 110 and 111”, substitute “92 and 109”.

42 Saving

A reference to section 83, 84, 86, 88, 89, 110 or 111 of the Petroleum Resource Rent Tax Assessment Act 1987 (the PRRTA Act) in an item in Part 3 of Schedule 2 to the A New Tax System (Tax Administration) Act 1999 includes a reference to that section as it had effect, before its repeal, because of subsection 65(12) of the PRRTA Act.

43 Subsection 93(1)

Omit “84, 85, 86, 87, 92, 109, 110 and 111”, substitute “85, 92 and 109”.

44 Saving

A reference to section 84, 86, 110 or 111 of the Petroleum Resource Rent Tax Assessment Act 1987 (the PRRTA Act) in an item in Part 3 of Schedule 2 to the A New Tax System (Tax Administration) Act 1999 includes a reference to that section as it had effect, before its repeal, because of subsection 93(1) of the PRRTA Act.

45 At the end of section 95

Add:

Note: For provisions about collection and recovery of an instalment of tax, see Part 4‑15 in Schedule 1 to the Taxation Administration Act 1953.

46 Subsection 1061ZZFG(1)

After “Part IVC of”, insert “, and Part 4‑15 in Schedule 1 to,”.

47 At the end of subsection 1061ZZFG(1)

Add:

Note 1: Part 4‑15 in Schedule 1 to the Taxation Administration Act 1953 deals with collection and recovery of amounts on and after 1 July 2000, replacing some provisions in Division 1 of Part VI of the Income Tax Assessment Act 1936.

Note 2: FS assessment debts are also collected through the Pay As You Go (PAYG) system of collecting income tax: see Parts 2‑1, 2‑5 and 2‑10 in Schedule 1 to the Taxation Administration Act 1953.

48 Subsection 238(1)

Omit “for the purpose of enabling the collection of tax”, substitute “or Subdivision 260‑A in Schedule 1 to the Taxation Administration Act 1953, for the purpose of enabling the collection of an amount”.

49 Subsection 12ZN(1)

After “Part IVC of”, insert “, and Part 4‑15 in Schedule 1 to,”.

Note: The heading to section 12ZN is altered by omitting “the Income Tax Assessment Act” and substituting “tax legislation”.

50 At the end of subsection 12ZN(1)

Add:

Note 1: Part 4‑15 in Schedule 1 to the Taxation Administration Act 1953 deals with collection and recovery of amounts on and after 1 July 2000, replacing some provisions in Division 1 of Part VI of the Income Tax Assessment Act 1936.

Note 2: FS assessment debts are also collected through the Pay As You Go (PAYG) system of collecting income tax: see Parts 2‑1, 2‑5 and 2‑10 in Schedule 1 to the Taxation Administration Act 1953.

51 At the end of subsection 15(4)

Add:

Note: For provisions about collection and recovery of superannuation contributions surcharge and other related amounts, see Part 4‑15 in Schedule 1 to the Taxation Administration Act 1953.

52 Subsection 15(8)

Omit “or within such further period as the Commissioner allows”.

53 Saving

Despite the amendment of subsection 15(8) of the Superannuation Contributions Tax (Members of Constitutionally Protected Superannuation Funds) Assessment and Collection Act 1997 made by item 52, anything done under that subsection before 1 July 2000 continues to have effect on and after that day as if that subsection had not been so amended.

54 At the end of subsection 15(8)

Add:

Note: For provisions about collection and recovery of superannuation contributions surcharge and other related amounts, see Part 4‑15 in Schedule 1 to the Taxation Administration Act 1953.

Repeal the subsection, substitute:

(1) If there is an RBA deficit debt on an RBA at the end of a day, the tax debtor is liable to pay to the Commonwealth the amount of the debt. The amount is due and payable at the end of that day.

Note: For provisions about collection and recovery of the amount, see Part 4‑15 in Schedule 1.

Note: The heading to section 8AAZH is replaced by the heading “Liability for RBA deficit debt”.

56 Section 14ZQ (paragraphs (a), (d) and (eb) of the definition of delayed administration (beneficiary) objection)

Repeal the paragraphs.

57 Section 14ZQ (paragraph (g) of the definition of delayed administration (beneficiary) objection)

Repeal the paragraph, substitute:

(g) subsection 260‑145(5) in Schedule 1 (because of paragraph (a) of that subsection).

58 Section 14ZQ (paragraphs (a), (d) and (eb) of the definition of delayed administration (trustee) objection)

Repeal the paragraphs.

59 Section 14ZQ (paragraph (g) of the definition of delayed administration (trustee) objection)

Repeal the paragraph, substitute:

(g) subsection 260‑145(5) in Schedule 1 (because of paragraph (b) of that subsection).

60 Paragraph 14ZW(1)(ab)

Omit “subsection 98(3) of the Fringe Benefits Tax Assessment Act 1986”, substitute “subsection 260‑145(5) in Schedule 1 (because of paragraph (a) of that subsection)”.

61 Paragraph 14ZW(1)(ac)

Omit “subsection 98(7) of the Fringe Benefits Tax Assessment Act 1986”, substitute “subsection 260‑145(5) in Schedule 1 (because of paragraph (b) of that subsection)”.

62 Saving

The amendments made by items 56 to 61 do not apply to anything done under:

(a) a provision specified in a paragraph that is repealed or amended by item 56, 57, 58 or 59; or

(b) that provision as it continues to have effect because of item 134 of Schedule 2 to the A New Tax System (Tax Administration) Act 1999.

63 Subsection 47(3)

Omit “Unless the Commissioner has extended the time to pay the penalty, or permitted it to be paid by instalments, the”, substitute “The”.

64 Subsection 47(3) (note)

Repeal the note.

65 At the end of section 16‑70 in Schedule 1

Add:

Note: For provisions about collection and recovery of amounts payable to the Commissioner under this Part, see Part 4‑15.

66 At the end of section 45‑15 in Schedule 1

Add:

Note 5: For provisions about collection and recovery of amounts you are liable to pay under this Part, see Part 4‑15.

67 Section 45‑75 in Schedule 1

Omit “208, 209, 214, 254, 255, 258 and 259”, substitute “254 and 255”.

68 At the end of section 298‑15 in Schedule 1

Add:

Note: For provisions about collection and recovery of the penalty, see Part 4‑15.

69 At the end of subsection 11(2)

Add:

Note: For provisions about collection and recovery of termination payments surcharge and other related amounts, see Part 4‑15 in Schedule 1 to the Taxation Administration Act 1953.

70 Subsection 17(1)

Omit “Subject to subsection (2) of this section and section 23, charge”, substitute “Charge”.

71 Subsection 17(1A)

Omit “Subject to subsection (2) of this section and section 23, additional”, substitute “Additional”.

72 Subsection 4(6)

After “Assessment Act”, insert “, or subsection 255‑5(2) in Schedule 1 to the Taxation Administration Act 1953,”.

Note: The heading to section 4 is altered by omitting “Assessment Act” and substituting “tax legislation”.

73 Subsection 4(8)

Repeal the subsection.

74 Saving

Despite the repeal of subsection 4(8) of the Trust Recoupment Tax Assessment Act 1985 by item 73, that subsection continues to have effect in relation to a person who dies before 1 July 2000.

75 Subsection 58J(1)

Omit “for the purposes of enabling the collection of tax”, substitute “or Subdivision 260‑A in Schedule 1 to the Taxation Administration Act 1953, for the purpose of enabling the collection of an amount”.

76 Subsection 58J(2)

Omit “for the purposes of enabling the collection of tax”, substitute “or Subdivision 260‑A in Schedule 1 to the Taxation Administration Act 1953, for the purpose of enabling the collection of an amount”.

77 At the end of section 58J

Add:

Note: The power of the Commissioner of Taxation to issue a notice in relation to collection of tax under section 218 of the Income Tax Assessment Act 1936 ceases on and after 1 July 2000. On and after that day, he or she may issue a similar notice under Subdivision 260‑A in Schedule 1 to the Taxation Administration Act 1953.

Note: The heading to section 58J is altered by omitting “—section 218 of the Income Tax Assessment Act”.

78 Subsection 36(1)

Omit “Subject to section 37, tax”, substitute “Tax”.

79 Subsection 36(2)

Omit “Subject to section 37, additional”, substitute “Additional”.

Repeal the item, substitute:

1 Subsection 8AAB(5) (after table item 17)

Insert:

17AA | 40 | Taxation Administration Act 1953 |

After “Division 12”, insert “(except section 12‑190)”.

3 After subitem 3(1) of Schedule 1

Insert:

(1A) Section 12‑190 in Schedule 1 to the Taxation Administration Act 1953 applies to a payment made on or after 1 July 2000, but only if some or all of the supply is made on or after that day. (When a supply is made is determined for the purposes of this subitem in the same way as for the purposes of the A New Tax System (Goods and Services Tax Transition) Act 1999.)

Omit all the words after “to have”, substitute “made a TFN declaration in relation to the trustee that has effect under Division 3.”.

5 Application

The amendment made by item 4 applies to a person who quotes his or her tax file number before, at or after the item’s commencement.

6 Section 202DI

Omit all the words after “to have”, substitute “made a TFN declaration in relation to the provider of the RSA that has effect under Division 3.”.

Note: The heading to section 202DI is altered by inserting “of” after “taxation”.

7 Application

The amendment made by item 6 applies to a person who quotes his or her tax file number before, at or after the item’s commencement.

8 Subsection 202DJ(1)

Omit “has quoted his or her tax file number as mentioned in subregulation 98(8) or regulation 100 of the Income Tax Regulations,”, substitute “has made a TFN declaration in relation to the trustee of the entity, scheme or fund, or the RSA provider, that states his or her tax file number, and has effect under Division 3 (except a declaration that includes a statement mentioned in subsection 202CB(2)),”.

9 Saving

The amendment made by item 8 applies to a person who, immediately before that item’s commencement, is taken to have quoted his or her tax file number to a trustee or an RSA provider because of subsection 202DJ(1) of the Income Tax Assessment Act 1936, as if that person had made a TFN declaration in relation to the trustee or the RSA provider as mentioned in that subsection as amended by that item.

After “221AZKC”, insert “, 221AZKEA”.

Insert:

If an instalment taxpayer’s assessment for the 1999‑2000 year of income is amended on one or more occasions, sections 221AZKB and 221AZKC apply, and are taken always to have applied, as if the taxpayer’s assessed tax for that year had always been the total of:

(a) the tax payable for that year; and

(b) the amount of interest (if any) payable under section 102AAM for that year;

as shown in the notice of the taxpayer’s latest assessment for that year.

Note: This may affect how much of the final instalment can be deferred, and the number and amounts of quarterly payments by which the taxpayer must pay off the deferred amount.

12 At the end of section 221AZKE

Add:

(2) Subsection (1) also has effect for the purposes of section 221AZKEA as applying to the entity.

(3) In this section:

entity has the meaning given by section 960‑100 of the Income Tax Assessment Act 1997.

13 Subsection 2‑15(3) (after item 4 of the table headed “Key participants in the income tax system”)

Insert:

4A. | foreign resident | section 995‑1 |

14 Subsections 26‑25(1) and (2)

Repeal the subsections, substitute:

(1) You cannot deduct under this Act interest (within the meaning of Division 11A of Part III of the Income Tax Assessment Act 1936) or a *royalty if:

(a) Subdivision 12‑F in Schedule 1 to the Taxation Administration Act 1953 requires you to withhold an amount from the interest or royalty; and

(b) either:

(i) you fail to withhold the amount; or

(ii) after withholding the amount, you fail to comply with section 16‑70 in that Schedule in relation to that amount.

(2) You cannot deduct under this Act interest (within the meaning of Division 11A of Part III of the Income Tax Assessment Act 1936), or a *royalty, that is in the form of a *non‑cash benefit if:

(a) section 14‑5 or 14‑10 in Schedule 1 to the Taxation Administration Act 1953 requires you to pay an amount to the Commissioner before providing the benefit, because of Subdivision 12‑F in that Schedule; and

(b) you fail to pay the amount as required by that section.

Omit “a payment of”.

Omit “, for”, substitute “for”.

17 Subsection 8AAB(5) (after table item 17F)

Insert:

17GA | 45‑232 in Schedule 1 | Taxation Administration Act 1953 |

Omit “and liability”, substitute “, liability”.

After “(HECS)”, insert “and liability to repay financial supplement debts under the Student Financial Supplement Scheme (SFSS)”.

20 After paragraph 11‑1(c) in Schedule 1

Insert:

(da) amounts of liabilities to the Commonwealth under Part 2B.3 of the Social Security Act 1991; and

(db) amounts of liabilities to the Commonwealth under Division 6 of Part 4A of the Student Assistance Act 1973; and

21 Section 12‑215 in Schedule 1

Omit all the words before paragraph (a), substitute:

An entity that receives a payment of a *dividend of a company that is an Australian resident must withhold an amount from the dividend if:

22 Paragraph 12‑215(b) in Schedule 1

After “is”, insert “or becomes”.

23 At the end of section 12‑215 in Schedule 1

Add:

(2) The entity must withhold the amount:

(a) if the foreign resident is so entitled when the entity receives the payment—immediately after the entity receives the payment; or

(b) if the foreign resident becomes so entitled after the entity receives the payment—immediately after the foreign resident becomes so entitled.

24 Section 12‑250 in Schedule 1

Omit all the words before paragraph (a), substitute:

An entity that receives a payment of interest (within the meaning of Division 11A of Part III of the Income Tax Assessment Act 1936) must withhold an amount from the payment if:

25 Paragraph 12‑250(b) in Schedule 1

After “is”, insert “or becomes”.

26 At the end of section 12‑250 in Schedule 1

Add:

(2) The entity must withhold the amount:

(a) if the foreign resident is so entitled when the entity receives the payment—immediately after the entity receives the payment; or

(b) if the foreign resident becomes so entitled after the entity receives the payment—immediately after the foreign resident becomes so entitled.

27 Section 12‑285 in Schedule 1

Omit all the words before paragraph (a), substitute:

An entity that receives a payment of a *royalty must withhold an amount from the payment if:

28 Paragraph 12‑285(b) in Schedule 1

After “is”, insert “or becomes”.

29 At the end of section 12‑285 in Schedule 1

Add:

(2) The entity must withhold the amount:

(a) if the foreign resident is so entitled when the entity receives the payment—immediately after the entity receives the payment; or

(b) if the foreign resident becomes so entitled after the entity receives the payment—immediately after the foreign resident becomes so entitled.

30 After paragraph 15‑30(c) in Schedule 1

Insert:

(da) the rates specified in section 1061ZZFA (about repayments of accumulated FS debts) of the Social Security Act 1991; and

(db) the rates specified in section 12ZK (about repayments of accumulated FS debts) of the Student Assistance Act 1973; and

31 Paragraph 15‑50(1)(b) in Schedule 1

Omit “11‑1(b) or (c)”, substitute “11‑1(b), (c), (da) or (db)”.

32 Section 16‑5 in Schedule 1 (note 2)

Omit “immediately after receiving the payment”, substitute “at the time required by that section”.

33 Section 16‑165 in Schedule 1

Repeal the section, substitute:

(1) Within 14 days after an entity (the payer) makes an *eligible termination payment that includes one or more retained amounts mentioned in subsection 27AC(2) of the Income Tax Assessment Act 1936, the payer must:

(a) give a *payment summary that covers the retained amount or amounts to the recipient of the payment (the recipient); and

(b) give a copy of the summary to the Commissioner.

(The summary must cover only the retained amount or amounts.)

Note: The payer must give the payment summary even if the payment is not covered by section 12‑85.

Exceptions

(2) Subsection (1) does not apply if the *eligible termination payment:

(a) is of a kind mentioned in paragraph (a) or (jaa) of the definition of eligible termination payment in subsection 27A(1) of the Income Tax Assessment Act 1936; and

(b) is a CGT exempt component within the meaning of that subsection.

(3) Subsection (1) also does not apply if the *eligible termination payment:

(a) is a death benefit of a kind set out in item 2 or 4 of Table 1 in subsection 27AAA(2) of the Income Tax Assessment Act 1936; and

(b) is made to a person who is a dependant (within the meaning of paragraph (b) of the definition of dependant in subsection 27A(1) of that Act) of the deceased taxpayer concerned.

34 Paragraph 16‑170(1)(f) in Schedule 1

Repeal the paragraph, substitute:

(f) specifies the retained amount or amounts (if any) mentioned in subsection 16‑165(1) that it covers; and

(g) is in the *approved form.

35 At the end of section 45‑5 in Schedule 1

Add:

; and (d) amounts of liabilities to the Commonwealth under Part 2B.3 of the Social Security Act 1991; and

(e) amounts of liabilities to the Commonwealth under Division 6 of Part 4A of the Student Assistance Act 1973.

36 After subsection 45‑120(2) in Schedule 1

Insert:

(2A) The instalment income of a *life insurance entity or *registered organisation for a period also includes its *statutory income, to the extent that the statutory income:

(a) is reasonably attributable to that period; and

(b) is included in the *CS/RA class of its assessable income for the income year that is or includes that period.

Note: The CS/RA class relates to the Complying Superannuation/Roll‑over Annuity aspect of the entity’s business.

37 At the end of section 45‑330 in Schedule 1

Add:

Special rule for life insurance entities and registered organisations

(3) The adjusted taxable income of a *life insurance entity or *registered organisation for the *base year is worked out as follows:

Method statement

Step 1. Recalculate each component of the taxable income for the *base assessment (except the *CS/RA component), disregarding any *capital gains.

Step 2. Add up the components recalculated under step 1.

Step 3. Add to the step 2 result the *CS/RA component for the *base assessment.

Step 4. Add to the step 3 result the deductions for *tax losses used in making the *base assessment.

Step 5. Reduce the step 4 result by the amount of any *tax loss, to the extent that the life insurance entity or registered organisation can carry it forward to the next income year.

38 Section 45‑340 in Schedule 1 (after step 3 of the method statement)

Insert:

Step 3A. The amount (if any) that you would have been liable to pay for the *base year by way of an *FS assessment debt if your taxable income for the base year had been your *adjusted taxable income, or your *adjusted withholding income, for that year is worked out.

39 Section 45‑340 in Schedule 1 (step 4 of the method statement)

Omit “and 3”, substitute “, 3 and 3A”.

40 Section 45‑375 in Schedule 1 (after step 3 of the method statement)

Insert:

Step 3A. The amount (if any) that you would have been liable to pay for the variation year by way of an *FS assessment debt if your taxable income for that year had been your *adjusted assessed taxable income for that year is worked out.

41 Section 45‑375 in Schedule 1 (step 4 of the method statement)

Omit “and 3”, substitute “, 3 and 3A”.

42 Group heading before section 360‑60 in Schedule 1

Repeal the heading, substitute:

43 Section 360‑60 (heading) in Schedule 1

Repeal the heading, substitute:

44 Subsection 360‑60(1) in Schedule 1

Repeal the subsection, substitute:

(1) A person who is authorised to perform a function, or exercise a power, of the Commissioner under this Division must do so only at places approved by the Commissioner.

45 Section 360‑75 in Schedule 1 (table item 35)

Repeal the item.

46 Section 360‑75 in Schedule 1 (after table item 50)

Insert:

53 | section 52‑150 | Family assistance payments |

47 After paragraph 360‑80(a) in Schedule 1

Insert:

(ba) a fee or commission you incur as mentioned in section 25‑7 (for advice about family tax benefit) of the Income Tax Assessment Act 1997; or

48 Section 360‑85 in Schedule 1 (table item 10)

Repeal the item.

Insert:

adjusted tax on *adjusted taxable income or on *adjusted withholding income has the meaning given by section 45‑340 in Schedule 1 to the Taxation Administration Act 1953.

2 Subsection 995‑1(1) (definition of adjusted taxable income)

Omit “section 45‑330”, substitute “sections 45‑330 and 45‑480”.

3 Subsection 995‑1(1) (definition of adjusted withholding income)

Omit “section 45‑335”, substitute “sections 45‑335 and 45‑485”.

4 Subsection 995‑1(1) (definition of base assessment)

Omit “section 45‑320”, substitute “sections 45‑320 and 45‑470”.

5 Subsection 995‑1(1) (definition of base year)

Omit “section 45‑320”, substitute “sections 45‑320 and 45‑470”.

6 Subsection 995‑1(1) (definition of benchmark instalment rate)

Omit “section 45‑360”, substitute “sections 45‑360 and 45‑530”.

7 Subsection 995‑1(1) (definition of benchmark tax)

Omit “section 45‑365”, substitute “sections 45‑365 and 45‑535”.

Insert:

Commissioner’s instalment rate has the meaning given by section 45‑115 in Schedule 1 to the Taxation Administration Act 1953.

Insert:

CS/RA class of the assessable income of a *life insurance entity or *registered organisation has the meaning given by section 116CE or 116GD of the Income Tax Assessment Act 1936.

Insert:

CS/RA component of the taxable income of a *life insurance entity or *registered organisation has the meaning given by section 110 or 116E of the Income Tax Assessment Act 1936.

11 Subsection 995‑1(1) (definition of instalment income)

Omit “and 45‑280”, substitute “, 45‑280, 45‑285 and 45‑465”.

Insert:

FS assessment debt means an FS assessment debt under:

(a) subsection 19AB(2) of the Social Security Act 1991; or

(b) the Student Assistance Act 1973 as in force at a time on or after 1 July 1998.

Insert:

majority control has the meaning given by section 45‑145 in Schedule 1 to the Taxation Administration Act 1953.

Insert:

multi‑rate trustee has the meaning given by section 45‑455 in Schedule 1 to the Taxation Administration Act 1953.

15 Subsection 995‑1(1) (definition of notional tax)

Omit “section 45‑325”, substitute “sections 45‑325 and 45‑475”.

Insert:

reduced beneficiary’s share of a trust’s net income for an income year has the meaning given by section 45‑483 in Schedule 1 to the Taxation Administration Act 1953.

Insert:

reduced no beneficiary’s share of a trust’s net income for an income year has the meaning given by section 45‑483 in Schedule 1 to the Taxation Administration Act 1953.

Insert:

single‑rate trustee has the meaning given by section 45‑450 in Schedule 1 to the Taxation Administration Act 1953.

[Minister’s second reading speech made in—

House of Representatives on 9 December 1999

Senate on 16 March 2000]

(245/99)