Indirect Tax Legislation Amendment Act 2000

No. 92, 2000

Indirect Tax Legislation Amendment Act 2000

No. 92, 2000

Indirect Tax Legislation Amendment Act 2000

No. 92, 2000

An Act to implement A New Tax System by amending legislation relating to indirect tax, and by amending other legislation consequential on indirect tax reform, and for related purposes

Contents

1 Short title...................................

2 Commencement...............................

3 Schedule(s)..................................

Schedule 1—Non‑profit bodies

A New Tax System (Goods and Services Tax) Act 1999

Taxation Administration Act 1953

Schedule 2—GST‑free supplies

A New Tax System (Goods and Services Tax) Act 1999

Schedule 3—Supplies involving non‑residents

A New Tax System (Goods and Services Tax) Act 1999

Schedule 4—Agents

A New Tax System (Goods and Services Tax) Act 1999

Taxation Administration Act 1953

Schedule 5—Financial supplies

A New Tax System (Goods and Services Tax) Act 1999

Schedule 6—Calculating amounts of GST

A New Tax System (Goods and Services Tax) Act 1999

A New Tax System (Goods and Services Tax Transition) Act 1999

Taxation Administration Act 1953

Schedule 7—Joint ventures

A New Tax System (Australian Business Number) Act 1999

A New Tax System (Goods and Services Tax) Act 1999

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Schedule 8—Insurance

A New Tax System (Goods and Services Tax) Act 1999

A New Tax System (Goods and Services Tax Transition) Act 1999

Schedule 9—Administration

A New Tax System (Goods and Services Tax) Act 1999

Taxation Administration Act 1953

Taxation (Interest on Overpayments and Early Payments) Act 1983

Schedule 9A—Producer rebates under the wine equalisation tax

A New Tax System (Wine Equalisation Tax) Act 1999

Schedule 10—Alcoholic beverages

A New Tax System (Goods and Services Tax Transition) Act 1999

Sales Tax Assessment Act 1992

Schedule 10A—Trading periods spanning midnight on 30 June 2000

A New Tax System (End of Sales Tax) Act 1999

A New Tax System (Goods and Services Tax Transition) Act 1999

A New Tax System (Wine Equalisation Tax and Luxury Car Tax Transition) Act 1999

Schedule 11—Other amendments

A New Tax System (Australian Business Number) Act 1999

A New Tax System (Goods and Services Tax) Act 1999

A New Tax System (Goods and Services Tax Transition) Act 1999

A New Tax System (Luxury Car Tax) Act 1999

Customs Act 1901

Taxation Administration Act 1953

Indirect Tax Legislation Amendment Act 2000

No. 92, 2000

An Act to implement A New Tax System by amending legislation relating to indirect tax, and by amending other legislation consequential on indirect tax reform, and for related purposes

[Assented to 30 June 2000]

The Parliament of Australia enacts:

This Act may be cited as the Indirect Tax Legislation Amendment Act 2000.

(1) Subject to this section, this Act commences immediately after the commencement of Part 1 of Schedule 1 to the A New Tax System (Indirect Tax and Consequential Amendments) Act (No. 2) 1999.

(2) Section 1 and this section, and Schedules 10 and 10A (other than item 5 of Schedule 10A), commence on the day on which this Act receives the Royal Assent.

(3) Items 10, 10A and 11 of Schedule 1, item 10 of Schedule 4, items 8, 9 and 10 of Schedule 6, item 33 of Schedule 7 and item 17 of Schedule 11 commence immediately after the commencement of items 7 to 23 of Schedule 8 to the A New Tax System (Indirect Tax and Consequential Amendments) Act (No. 2) 1999.

(4) Item 7 of Schedule 6, items 6 and 7 of Schedule 8, item 1 of Schedule 10 and items 13A to 16E of Schedule 11 commence immediately after the commencement of Schedule 2 to the A New Tax System (Indirect Tax and Consequential Amendments) Act (No. 2) 1999.

(5) Items 1, 2 and 3 of Schedule 7 and items 1 and 2 of Schedule 11 commence immediately after the commencement of Schedule 4 to the A New Tax System (Indirect Tax and Consequential Amendments) Act (No. 2) 1999.

(6) Schedule 9A and item 5 of Schedule 10A commence immediately after the commencement of Part 3 of Schedule 1 to the A New Tax System (Indirect Tax and Consequential Amendments) Act (No. 2) 1999.

(7) Item 16F of Schedule 11 commences immediately after the commencement of Part 2 of Schedule 11 to the A New Tax System (Indirect Tax and Consequential Amendments) Act (No. 2) 1999.

Subject to section 2, each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

A New Tax System (Goods and Services Tax) Act 1999

1 Subsection 9‑30(3)

Repeal the subsection, substitute:

Supplies that would be both GST‑free and input taxed

(3) To the extent that a supply would, apart from this subsection, be both *GST‑free and *input taxed:

(a) the supply is GST‑free and not input taxed, unless the provision under which it is input taxed requires the supplier to have chosen for its supplies of that kind to be input taxed; or

(b) the supply is input taxed and not GST‑free, if that provision requires the supplier to have so chosen.

Note: Subdivisions 40‑E (School tuckshops and canteens) and 40‑F (Fund‑raising events conducted by charitable institutions etc.) require such a choice.)

1A Section 9‑39 (after table item 5)

Insert:

5A | GST religious groups | Division 49 |

1B Section 11‑99 (after table item 6)

Insert:

6A | GST religious groups | Division 49 |

1C Section 17‑99 (after table item 8)

Insert:

8A | GST religious groups | Division 49 |

1D Section 19‑99 (before table item 1)

Insert:

1A | GST religious groups | Division 49 |

2 After subsection 27‑15(2)

Insert:

(2A) Paragraph (1)(d) does not apply to an entity that meets the requirements of subsection 63‑5(2) for choosing to apply Division 63 (whether or not the entity chooses to apply that Division).

2A Subsection 29‑40(2)

Omit “or any *gift‑deductible entity”, substitute “, any *gift‑deductible entity or any *government school”.

2B Section 37‑1 (after table item 15)

Insert:

15A | GST religious groups | Division 49 |

2C Paragraphs 38‑250(1)(a) and (2)(a)

Omit “or a *gift‑deductible entity”, substitute “, a *gift‑deductible entity or a *government school”.

2D Paragraph 38‑255(a)

Omit “or a *gift‑deductible entity”, substitute “, a *gift‑deductible entity or a *government school”.

2E Section 38‑255

Omit “or gift‑deductible entity” (wherever occurring), substitute “, gift‑deductible entity or government school”.

2F Paragraph 38‑270(a)

Omit “or a *gift‑deductible entity”, substitute “, a *gift‑deductible entity or a *government school”.

2G Paragraph 40-130(2)(a)

Repeal the paragraph.

3 At the end of Division 40

Add:

Subdivision 40‑F—Fund‑raising events conducted by charitable institutions etc.

40‑160 Fund‑raising events conducted by charitable institutions etc.

A supply is input taxed if:

(a) the supplier is a charitable institution, a trustee of a charitable fund, a *gift‑deductible entity or a *government school; and

(b) the supply is made in connection with a *fund‑raising event; and

(c) the supplier chooses to have all supplies that it makes in connection with the event treated as input taxed; and

(d) the event is referred to in the supplier’s records as an event that is treated as input taxed.

40‑165 Meaning of fund‑raising event

(1) Any of these is a fund‑raising event if it is conducted for the purpose of fund‑raising and it does not form any part of a series or regular run of like or similar events:

(a) a fete, ball, gala show, dinner, performance or similar event;

(b) an event comprising sales of goods if:

(i) each sale is for a *consideration that does not exceed $20 or such other amount as the regulations specify; and

(ii) selling such goods is not a normal part of the supplier’s *business;

(c) an event that the Commissioner decides, on an application by the supplier in writing, to be a fund‑raising event.

Note: Refusing an application for a decision under this paragraph is a reviewable GST decision (see Division 7 of Part VI of the Taxation Administration Act 1953).

(2) Paragraph (1)(b) does not apply to an event that involves the sale of alcoholic beverages or tobacco products.

(3) The Commissioner must not make a decision under paragraph (1)(c) unless satisfied that:

(a) the supplier is not in the *business of conducting such events; and

(b) the proceeds from conducting the event are for the direct benefit of the supplier’s charitable or non‑profit purposes.

(4) The Commissioner may determine, in writing, the frequency with which events may be held without forming any part of a series or regular run of like or similar events for the purposes of subsection (1).

4 Subsection 48‑10(2) (note)

Repeal the note, substitute:

Note 1: For the membership requirements of non‑profit sub‑entities, see section 63‑50.

Note 2: For the membership requirements of a GST group of government related entities, see section 149‑25.

4A After Division 48

Insert:

Division 49—GST religious groups

Table of Subdivisions

49‑A Approval of GST religious groups

49‑B Consequences of approval of GST religious groups

49‑C Administrative matters

49‑1 What this Division is about

Some registered charitable bodies can be approved as a GST religious group. Transactions between members of the group are then excluded from the GST.

Subdivision 49‑A—Approval of GST religious groups

49‑5 Approval of GST religious groups

The Commissioner must approve 2 or more entities as a *GST religious group if:

(a) the entities jointly apply, in the *approved form, for approval as a GST religious group; and

(b) each of the entities *satisfies the membership requirements for that GST religious group; and

(c) the application nominates one of the entities to be the *principal member for the group; and

(d) the entity so nominated is an *Australian resident.

A group of entities that is so approved is a GST religious group.

Note: Refusing an application for approval under this section is a reviewable GST decision (see Division 7 of Part VI of the Taxation Administration Act 1953).

49‑10 Membership requirements of a GST religious group

An entity satisfies the membership requirements of a *GST religious group, or a proposed GST religious group, if:

(a) the entity is *registered; and

(b) the entity is endorsed as exempt from income tax under Subdivision 50‑B of the *ITAA 1997; and

(c) all the other members of the GST religious group or proposed GST religious group are so endorsed; and

(d) the entity and all those other members are part of the same religious organisation; and

(e) the entity is not a member of any other GST religious group.

Subdivision 49‑B—Consequences of approval of GST religious groups

49‑30 Supplies between members of GST religious groups

(1) A supply that a *member of a *GST religious group makes to another member of the same GST religious group is treated as if it were not a *taxable supply.

(2) This section has effect despite section 9‑5 (which is about what are taxable supplies).

49‑35 Acquisitions between members of GST religious groups

(1) An acquisition that a *member of a *GST religious group makes from another member of the same GST religious group is treated as if it were not a *creditable acquisition.

(2) This section has effect despite section 11‑5 (which is about what are creditable acquisitions).

(1) An *adjustment event cannot arise in relation to:

(a) a supply that a *member of a *GST religious group makes to another member of the same GST religious group; or

(b) an acquisition that a member of a GST religious group makes from another member of the same GST religious group.

(2) This section has effect despite section 19‑10 (which is about what are adjustment events).

49‑45 Changes in the extent of creditable purpose

(1) An *adjustment cannot arise under Division 129 in relation to an acquisition that a *member of a *GST religious group makes from another member of the same GST religious group.

(2) This section has effect despite section 129‑5 (which is about when adjustments can arise under Division 129).

49‑50 GST religious groups treated as single entities for certain purposes

(1) Despite sections 49‑35, 49‑40 and 49‑45, a *GST religious group is treated as a single entity, and not as a number of entities corresponding to the *members of the GST religious group, for the purposes of working out:

(a) whether acquisitions or importations by a member are for a *creditable purpose; and

(b) the amounts of any input tax credits to which the member is entitled; and

(c) whether the member has any *adjustments; and

(d) the amounts of any such adjustments.

(2) This section has effect despite section 11‑25 (which is about the amount of input tax credits) and section 17‑10 (which is about the effect of adjustments on net amounts).

Subdivision 49‑C—Administrative matters

49‑70 Changing the membership etc. of GST religious groups

Changes made on application

(1) The Commissioner must, if the *principal member of a *GST religious group applies to the Commissioner in the *approved form, do one or more of these (as requested in the application):

(a) approve, as an additional *member of the GST religious group, another entity that *satisfies the membership requirements for the GST religious group;

(b) revoke the approval of one of the members of the GST religious group as a member of the group;

(c) approve another member of the GST religious group to replace the applicant as the principal member of the group.

Note: Refusing an application for approval or revocation under this subsection is a reviewable GST decision (see Division 7 of Part VI of the Taxation Administration Act 1953).

Changes made without application

(2) The Commissioner must revoke the approval of one of the *members of a *GST religious group if satisfied that the member does not *satisfy the membership requirements for the GST religious group.

Note: Revoking under this subsection an approval under this Division is a reviewable GST decision (see Division 7 of Part VI of the Taxation Administration Act 1953).

49‑75 Revoking the approval of GST religious groups

Revoking on application

(1) The Commissioner must, if the principal member of a *GST religious group applies to the Commissioner in the *approved form, revoke the approval of the group as a GST religious group.

Note: Refusing an application for revocation under this subsection is a reviewable GST decision (see Division 7 of Part VI of the Taxation Administration Act 1953).

Revoking without application

(2) The Commissioner must revoke the approval of the *GST religious group if satisfied that none of its members, or only one of its members, *satisfies the membership requirements for that GST religious group.

Note: Revoking under this subsection the approval of a GST group is a reviewable GST decision (see Division 7 of Part VI of the Taxation Administration Act 1953).

49‑80 Notification by principal members

The principal member of a *GST religious group must notify the Commissioner of any circumstances under which the Commissioner must:

(a) revoke the approval of one of the *members of the group under subsection 49‑70(2); or

(b) revoke the approval of the group under subsection 49‑75(2).

The notification may (in appropriate cases) be in the form of an application under subsection 49‑70(1) or 49‑75(1). The notification, or application, must be given to the Commissioner within 21 days after the circumstances occurred.

49‑85 Date of effect of approvals and revocations

(1) The Commissioner must decide the date of effect of any approval, or any revocation of an approval, under this Division.

(2) The date of effect may be the day of the decision, or a day before or after that day. However, it must be a day on which, for all the *members of the *GST religious group in question, a tax period begins.

Note: Deciding under this section the date of effect of any approval, or any revocation of an approval, under this Division is a reviewable GST decision (see Division 7 of Part VI of the Taxation Administration Act 1953).

49‑90 Notification by the Commissioner

The Commissioner must give notice of any decision that he or she makes under this Division:

(a) if the decision relates to the approval of 2 or more entities as a *GST religious group—to the entity nominated in the application for approval to be the *principal member of the group; or

(b) otherwise—to the principal member of the *GST religious group to which the decision relates.

4B Paragraph 63‑5(2)(a)

Omit “or a *gift‑deductible entity”, substitute “, a *gift‑deductible entity or a *government school”.

5 At the end of Division 63

Add:

63‑50 Membership requirements of GST groups

A *non‑profit sub‑entity satisfies the membership requirements for a *GST group, or a proposed GST group, if:

(a) it is *registered; and

(b) it has the same tax periods applying to it as the tax periods applying to all the other members of the GST group or proposed GST group; and

(c) it accounts on the same basis as all those other members; and

(d) it is not a *member of any other GST group; and

(e) each of the other members of the GST group or proposed GST group is either:

(i) the entity of which the non‑profit sub‑entity is a branch; or

(ii) another branch of that entity that is a non‑profit sub‑entity.

6 At the end of section 111‑1

Add “The entitlement extends to charitable bodies and government schools reimbursing their volunteers.”.

7 After section 111‑15

Insert:

111‑18 Application of Division to volunteers working for charitable institutions etc.

If:

(a) a charitable institution, a trustee of a charitable fund, a *gift‑deductible entity or a *government school reimburses an individual for an expense he or she incurs; and

(b) the expense is directly related to his or her activities as a volunteer of the institution, fund, gift‑deductible entity or government school;

this Division applies to the institution, fund, gift‑deductible entity or government school as if:

(c) the individual were an employee of the institution, fund, gift‑deductible entity or government school; and

(d) his or her activities in connection with incurring the expense were activities as such an employee.

7A Section 195‑1 (note at the end of the definition of creditable acquisition)

After “sections”, insert “49‑35,”.

8 Section 195‑1

Insert:

fund‑raising event has the meaning given by section 40‑165.

8A Section 195‑1

Insert:

government school means a *school that:

(a) supplies any of these kinds of *education courses:

(i) *pre‑school courses;

(ii) full‑time *primary courses;

(iii) full‑time *secondary courses;

(whether or not the school supplies any other education courses); and

(b) is conducted by or on behalf of an *Australian government agency;

and includes a proposed school that will meet the requirements of paragraphs (a) and (b) once it starts operation.

8B Section 195‑1

Insert:

GST religious group has the meaning given by section 49‑5.

8C Section 195‑1 (definition of member)

Repeal the definition, substitute:

member means:

(a) in relation to a *GST group—an entity, a *non‑profit sub‑entity or a *government related entity currently approved as one of the members of the group under section 48‑5 or paragraph 48‑70(1)(a); or

(b) in relation to a *GST religious group—an entity currently approved as one of the members of the group under section 49‑5 or paragraph 49‑70(1)(a).

8D Section 195‑1

Insert:

principal member, for a *GST religious group, is the *member of the group nominated as mentioned in paragraph 49‑5(c), or approved as a replacement principal member for the group under paragraph 49‑70(1)(c).

8E Section 195‑1 (definition of satisfies the membership requirements)

Repeal the definition, substitute:

satisfies the membership requirements:

(a) in relation to a *GST group—has the meaning given by section 48‑10 or 149‑25; or

(b) in relation to a *GST religious group—has the meaning given by section 49‑10.

8F Section 195‑1 (note at the end of the definition of taxable supply)

After “sections”, insert “49‑30,”.

9 Section 195‑1 (definition of satisfies the membership requirements)

Omit “or 149‑25”, substitute “, 63‑50 or 149‑25”.

Taxation Administration Act 1953

10 Subsection 62(2) (after table item 18)

Insert:

18A | refusing an application for a decision that an event is a fund‑raising event | paragraph 40‑165(1)(c) |

10A Subsection 62(2) (after table item 24)

Insert:

24A | refusing an application for approval | section 49‑5 |

24B | refusing an application for approval or revocation | subsection 49‑70(1) |

24C | revoking an approval under Division 49 | subsection 49‑70(2) |

24D | refusing an application for revocation | subsection 49‑75(1) |

24E | revoking the approval of a GST religious group | subsection 49‑75(2) |

24F | deciding the date of effect of any approval, or any revocation of an approval, under Division 49 | section 49‑85 |

11 After subsection 70(1A)

Insert:

(1B) If you choose under section 40‑160 of the GST Act to have treated as input taxed all the supplies you make in connection with a fund‑raising event, you must:

(a) keep records that record your choice; and

(b) retain those records for at least 5 years after making the choice.

A New Tax System (Goods and Services Tax) Act 1999

1 After section 38‑95

Insert:

38‑97 Lease etc. of curriculum related goods

A supply by way of lease or hire of goods is GST‑free if:

(a) the goods are for use directly or principally by a student in undertaking a *pre‑school course, *primary course or *secondary course in which the student is enrolled; and

(b) the entity supplying the course leases or hires the goods; and

(c) at all times while the lease or hiring has effect, the entity supplying the course has the right to decide who uses goods and the use to which the goods are put; and

(d) the lease or hiring is not part of an arrangement that includes:

(i) a transfer of ownership of the goods; or

(ii) an agreement to transfer ownership of the goods; or

(iii) imposing an obligation, or conferring a right, to transfer ownership of the goods.

2 Section 38‑100

After “section 38‑95”, insert “, or a supply by way of lease or hire that is covered by section 38‑97”.

3 Section 38‑290 (heading)

Repeal the heading, substitute:

38‑290 Sewerage and sewerage‑like services

4 At the end of section 38‑290

Add:

(2) A supply that consists of removing waste matter from *residential premises is GST‑free if:

(a) the premises are not serviced by sewers; and

(b) the waste matter is of a kind that would normally be removed using sewers if the premises were serviced by sewers.

(3) A supply that consists of servicing a domestic self‑contained sewage system is GST‑free.

4A Section 38‑415

Repeal the section, substitute:

38‑415 Supplies through inwards duty free shops

A supply is GST‑free if the supply is a sale of *airport shop goods through an *inwards duty free shop to a *relevant traveller.

5 Subsection 38‑475(1)

After “interest in, or”, insert “the lease by an *Australian government agency of or”.

6 Section 38‑480

After “interest in, or”, insert “the lease by an *Australian government agency of or”.

7 Section 195‑1 (definition of medical service)

Repeal the definition, substitute:

medical service means:

(a) a service for which medicare benefit is payable under Part II of the Health Insurance Act 1973; or

(b) any other service supplied by or on behalf of a *medical practitioner or *approved pathology practitioner that is generally accepted in the medical profession as being necessary for the appropriate treatment of the *recipient of the supply.

8 Section 195‑1 (paragraph (b) of the definition of relevant traveller)

Omit “imported or *excisable goods”, substitute “*airport shop goods”.

Schedule 3—Supplies involving non‑residents

A New Tax System (Goods and Services Tax) Act 1999

1 Section 9‑69 (after table item 4)

Insert:

4A | Non‑residents making supplies connected with Australia | Division 83 |

2 Section 9‑99 (after table item 4)

Insert:

4AA | Non‑residents making supplies connected with Australia | Division 83 |

3 Section 25‑49 (after table item 2)

Insert:

3 | Non‑residents making supplies connected with Australia | Division 83 |

4 Section 29‑99 (after table item 3)

Insert:

4 | Non‑residents making supplies connected with Australia | Division 83 |

5 Section 37‑1 (after table item 20A)

Insert:

20B | Non‑residents making supplies connected with Australia | Division 83 |

6 After section 38‑187

Insert:

38‑188 Tooling used by non‑residents to manufacture goods for export

A supply of goods is GST‑free if:

(a) the *recipient of the supply is a *non‑resident, and is not *registered or *required to be registered; and

(b) the goods are jigs, patterns, templates, dies, punches and similar machine tools to be used in Australia solely to manufacture goods that will be for export from Australia.

8 Subsection 38‑190(1) (table item 2)

Repeal the item, substitute:

2 | Supply to *non‑resident outside Australia. | a supply that is made to a *non‑resident who is not in Australia when the thing supplied is done, and: (a) the supply is neither a supply of work physically performed on goods situated in Australia when the work is done nor a supply directly connected with *real property situated in Australia; or (b) the *non‑resident acquires the thing in *carrying on the non‑resident’s *enterprise, but is not *registered or *required to be registered. |

9 Subsection 38‑190(1) (table item 3, 3rd column)

Omit “directly connected with goods situated in Australia when the thing supplied is done, or”, substitute “of work physically performed on goods situated in Australia when the thing supplied is done, or a supply directly connected”.

10 At the end of subsection 38‑190(2)

Add “and would not be *GST‑free”.

11 At the end of section 38‑190

Add:

(4) A supply is taken, for the purposes of item 3 in that table, to be a supply made to a *recipient who is not in Australia if:

(a) it is a supply under an agreement entered into, whether directly or indirectly, with an *Australian resident; and

(b) the supply is provided, or the agreement requires it to be provided, to another entity outside Australia.

12 After section 81‑10

Insert:

Division 83—Non‑residents making supplies connected with Australia

83‑1 What this Division is about

The GST on taxable supplies made by non‑residents can, with the agreement of the recipients, be “reverse charged” to the recipients.

83‑5 “Reverse charge” on supplies made by non‑residents

(1) The GST on a *taxable supply is payable by the *recipient of the supply, and is not payable by the supplier, if:

(a) the supplier is a *non‑resident; and

(b) the supplier does not make the supply through an *enterprise that the supplier *carries on in Australia; and

(c) the recipient is *registered or *required to be registered; and

(d) the supplier and the recipient agree that the GST on the supply be payable by the recipient.

(2) However, this section does not apply to:

(a) a supply that is not *connected with Australia but that is a *taxable supply because of Division 84 (which is about offshore supplies other than goods or real property); or

(b) a taxable supply made by a *non‑resident through a *resident agent.

Note: GST on these taxable supplies is payable by the resident agent: see section 57‑5.

(3) This section has effect despite section 9‑40 (which is about liability for the GST).

83‑10 Recipients who are members of GST groups

(1) If section 83‑5 applies to a *taxable supply but the *recipient of the supply is a *member of a *GST group, the GST on the supply:

(a) is payable by the *representative member; and

(b) is not payable by the member (unless the member is the representative member).

(2) This section has effect despite section 83‑5.

83‑15 Recipients who are participants in GST joint ventures

(1) If section 83‑5 applies to a *taxable supply but the *recipient of the supply is a *participant in a *GST joint venture and the supply is made, on the recipient’s behalf, by the *joint venture operator of the GST joint venture in the course of activities for which the joint venture was entered into, the GST on the supply:

(a) is payable by the joint venture operator; and

(b) is not payable by the participant.

(2) This section has effect despite section 83‑5.

83‑20 The amount of GST on “reverse charged” supplies made by non‑residents

(1) The amount of GST on a supply to which section 83‑5, 83‑10 or 83‑15 applies is 10% of the *price of the supply.

(2) This section has effect despite section 9‑70 (which is about the amount of GST on taxable supplies).

83‑25 When non‑residents must apply for registration

(1) A *non‑resident need not apply to be *registered under this Act if the non‑resident’s *annual turnover would not meet the *registration turnover threshold but for the *taxable supplies of the non‑resident that are taxable supplies to which section 83‑5 applies.

(2) It does not matter whether the *non‑resident is *required to be registered.

(3) This section has effect despite section 25‑1 (which is about when entities must apply for registration).

83‑30 When the Commissioner must register non‑residents

(1) The Commissioner need not *register a *non‑resident if the Commissioner is satisfied that the non‑resident’s *annual turnover would not meet the *registration turnover threshold but for the *taxable supplies of the non‑resident that are taxable supplies to which section 83‑5 applies.

(2) It does not matter whether the *non‑resident is *required to be registered.

(3) This section has effect despite section 25‑5 (which is about when the Commissioner must register an entity).

83‑35 Tax invoices not required for “reverse charged” supplies made by non‑residents

(1) A *non‑resident is not required to issue a *tax invoice for a *taxable supply of the non‑resident that is a taxable supply to which section 83‑5 applies.

(2) Subsection (1) has effect despite section 29‑70 (which is about the requirement to issue tax invoices).

(3) Subsection 29‑10(3) does not apply in relation to a *creditable acquisition made by an entity as a result of being the *recipient of a *taxable supply to which section 83‑5 applies.

13 After section 188‑22

Insert:

188‑23 Supplies “reverse charged” under Division 83 not to be included in a recipient’s turnover

To avoid doubt, if the GST on a *taxable supply is, under Division 83, payable by the *recipient of the supply, that supply is disregarded in working out the *current annual turnover or the *projected annual turnover of the recipient.

A New Tax System (Goods and Services Tax) Act 1999

1 Section 9‑39 (before table item 1)

Insert:

1A | Agents and insurance brokers | Division 153 |

2 Section 9‑99 (before table item 1)

Insert:

1A | Agents and insurance brokers | Division 153 |

3 Section 11‑99 (before table item 1)

Insert:

1A | Agents and insurance brokers | Division 153 |

4 At the end of section 153‑1

Add “It also allows in some cases a supply or acquisition made through an agent to be treated as 2 separate supplies or acquisitions.”.

5 After section 153‑1

Insert:

6 At the end of subsection 153‑15(2)

Add:

Note: If Subdivision 153‑B is to apply to the supply, only your agent can issue the tax invoice: see subsection 153‑55(3).

7 Subsections 153‑25(1) and (2)

Omit “this Division”, substitute “this Subdivision”.

8 After section 153‑25

Insert:

Subdivision 153‑B—Principals and agents as separate suppliers or acquirers

153‑50 Arrangements under which agents are treated as suppliers or acquirers

An entity (the principal) may, in writing, enter into an arrangement with another entity (the agent) under which:

(a) the agent will, on the principal’s behalf:

(i) make supplies to third parties; or

(ii) make acquisitions from third parties; or

(iii) make both supplies to third parties and acquisitions from third parties; and

(b) the kinds of supplies or acquisitions, or the kinds of supplies and acquisitions, to which the arrangement applies are specified; and

(c) for the purposes of the GST law:

(i) the agent will be treated as making the supplies to the third parties, or acquisitions from the third parties, or both; and

(ii) the principal will be treated as making corresponding supplies to the agent, or corresponding acquisitions from the agent, or both; and

(d) in the case of supplies to third parties:

(i) the agent will issue to the third parties, in the agent’s own name, all the *tax invoices and *adjustment notes relating to those supplies; and

(ii) the principal will not issue to the third parties any tax invoices and adjustment notes relating to those supplies; and

(e) the arrangement ceases to have effect if the principal or the agent, or both of them, cease to be *registered.

153‑55 The effect of these arrangements on supplies

(1) A *taxable supply that the principal makes to a third party through the agent is taken to be a supply that is a taxable supply made by the agent to the third party, and not by the principal, if:

(a) the supply is of a kind to which the arrangement applies; and

(b) the supply is made in accordance with the arrangement; and

(c) both the principal and the agent are *registered.

(2) In addition, the principal is taken to make a supply that is a *taxable supply to the agent. This supply is taken:

(a) to be a supply of the same thing as is supplied in the taxable supply (the agent’s supply) that the agent is taken to make; and

(b) to have a *value equal to 10/11 of the amount that is payable to the principal by the agent in respect of the agent’s supply.

The agent is taken to make a corresponding *creditable acquisition from the principal.

(3) If the principal pays, or is liable to pay, an amount, as a commission or similar payment, to the agent for the agent’s supply to the third party:

(a) for the purpose of paragraph (2)(b), the amount payable by the agent to the principal is taken to be reduced by the amount the principal pays, or is liable to pay, to the agent; and

(b) the supply by the agent to the principal, to which the principal’s payment or liability relates, is not a *taxable supply.

(4) However, this section no longer applies, and is taken never to have applied, if the principal issues to the third party, in the principal’s own name, any *tax invoice or *adjustment note relating to the supply.

(5) This section has effect despite section 9‑5 (which is about what are taxable supplies), section 9‑75 (which is about the value of taxable supplies) and section 11‑5 (which is about what are creditable acquisitions).

153‑60 The effect of these arrangements on acquisitions

(1) An acquisition that the principal makes from a third party through the agent is taken to be a *creditable acquisition made by the agent from the third party, and not by the principal, if:

(a) the acquisition is of a kind to which the arrangement applies; and

(b) the acquisition is made in accordance with the arrangement; and

(c) both the principal and the agent are *registered.

(2) In addition, the agent is taken to make a supply that is a *taxable supply to the principal. This supply is taken:

(a) to be a supply of the same thing as is acquired in the *creditable acquisition (the agent’s acquisition) that the agent is taken to make; and

(b) to have a *value equal to 10/11 of the amount that is payable to the agent by the principal in respect of the agent’s acquisition.

The principal is taken to make a corresponding acquisition from the agent, and the acquisition is taken to be a creditable acquisition if, apart from this section, the principal’s acquisition from the third party would have been a creditable acquisition.

(3) If the principal pays, or is liable to pay, an amount, as a commission or similar payment, to the agent for the agent’s acquisition from the third party:

(a) for the purpose of paragraph (2)(b), the amount payable by the principal to the agent is taken to be increased by the amount the principal pays, or is liable to pay, to the agent; and

(b) the supply by the agent to the principal, to which the principal’s payment or liability relates, is not a *taxable supply.

(4) This section has effect despite section 11‑5 (which is about what are creditable acquisitions), section 11‑10 (which is about what are acquisitions), section 9‑5 (which is about what are taxable supplies) and section 9‑75 (which is about the value of taxable supplies).

153‑65 Determinations that supplies or acquisitions are taken to be under these arrangements

(1) The Commissioner may determine in writing that supplies or acquisitions of a specified kind that any entity (the agent) makes on behalf of any other entity (the principal) to or from third parties are taken to be supplies or acquisitions:

(a) that are of a kind to which an arrangement of a kind referred to in section 153‑50 applies; and

(b) that are made in accordance with that arrangement.

(2) The determination has effect accordingly, unless either the agent or the principal notifies the other in writing, or both notify each other in writing, that:

(a) any supplies that the agent makes to third parties on the principal’s behalf are not supplies to which such an arrangement applies; and

(b) any acquisitions that the agent makes from third parties on the principal’s behalf are not acquisitions to which such an arrangement applies.

9 Before section 188‑25

Insert:

188‑24 Supplies to which Subdivision 153‑B applies

(1) In working out your *current annual turnover or your *projected annual turnover, you may choose to treat the *value of any *taxable supply that, under subsection 153‑55(1), you are taken to make as an agent as being an amount equal to the difference between:

(a) what is, apart from this section, the value of the supply; and

(b) the value of the taxable supply that, under subsection 153‑55(2), is taken to be made to you in relation to the taxable supply that you are taken to make.

(2) In working out your *current annual turnover or your *projected annual turnover, you may choose to treat the *value of any *taxable supply that, under subsection 153‑60(2), you are taken to make as an agent as being an amount equal to the difference between:

(a) what is, apart from this section, the value of the supply; and

(b) 10/11 of the *consideration you provided or are liable to provide for the *creditable acquisition that, under subsection 153‑60(1), you are taken to make and that relates to that supply.

Taxation Administration Act 1953

10 After subsection 70(1)

Insert:

(1AA) Subsection (1) requires a record of an arrangement entered into under section 153‑50 of the GST Act to be kept and retained by the party entering into the arrangement as principal. It does not require such a record to be kept or retained by the party entering into the arrangement as agent.

(1AB) Subsection (1) requires records of a notice given under subsection 153‑65(2) of the GST Act to be kept and retained by both the entity giving the notice and the entity receiving it.

A New Tax System (Goods and Services Tax) Act 1999

1 Paragraph 11‑15(4)(b)

Repeal the paragraph, substitute:

(b) you do not *exceed the financial acquisitions threshold.

2 At the end of section 11‑15

Add:

(5) An acquisition is not treated, for the purposes of paragraph (2)(a), as relating to making supplies that would be *input taxed to the extent that:

(a) the acquisition relates to making a *financial supply consisting of a borrowing; and

(b) the borrowing relates to you making supplies that are not input taxed.

2A Section 11‑99 (after table item 3)

Insert:

3A | Financial supplies (acquisitions and importations to provide fringe benefits) | Division 71 |

3 Paragraph 15‑10(4)(b)

Repeal the paragraph, substitute:

(b) you do not *exceed the financial acquisitions threshold.

4 At the end of section 15‑10

Add:

(5) An importation is not treated, for the purposes of paragraph (2)(a), as relating to making supplies that would be *input taxed to the extent that:

(a) the importation relates to making a *financial supply consisting of a borrowing; and

(b) the borrowing relates to you making supplies that are not input taxed.

4A Section 15‑99 (before table item 1)

Insert:

1A | Financial supplies (acquisitions and importations to provide fringe benefits) | Division 71 |

4B Section 37‑1 (before table item 11)

Insert:

10B | Financial supplies (acquisitions and importations to provide fringe benefits) | Division 71 |

5 After subsection 70‑5(1)

Insert:

(1A) However, an acquisition is not a reduced credit acquisition if, without this Division applying, an entity is entitled to an input tax credit for the acquisition.

Note: Acquisitions relating to financial supplies can give rise to input tax credits: see subsections 11‑15(4) and (5).

5A After Division 70

Insert:

Division 71—Financial supplies (acquisitions and importations to provide fringe benefits)

71‑1 What this Division is about

Financial suppliers may not be entitled to input tax credits for acquisitions or importations they make to provide fringe benefits to their employees.

Note: Under the Fringe Benefits Tax Assessment Act 1986, a lower rate of fringe benefits tax is payable for providing fringe benefits without entitlement to input tax credits.

71‑5 Acquisitions by financial suppliers to provide fringe benefits

(1) An acquisition that solely or partly relates to making *financial supplies is not a *creditable acquisition to the extent that the acquisition would (but for this section) be a *GST‑creditable benefit on the provision of which *fringe benefits tax is payable.

(2) However, this section applies only if you *exceed the financial acquisitions threshold.

(3) This section has effect despite section 11‑5 (which is about what is a creditable acquisition).

71‑10 Importations by financial suppliers to provide fringe benefits

(1) An importation that solely or partly relates to making *financial supplies is not a *creditable importation to the extent that the importation would (but for this section) be a *GST‑creditable benefit on the provision of which *fringe benefits tax is payable.

(2) However, this section applies only if you *exceed the financial acquisitions threshold.

(3) This section has effect despite section 15‑5 (which is about what is a creditable importation).

6 Subsection 129‑5(2)

Omit all the words after “unless”, substitute “you *exceed the financial acquisitions threshold”.

7 After section 188‑35

Insert:

Division 189—Exceeding the financial acquisitions threshold

189‑1 What this Division is about

You can be entitled to input tax credits for your acquisitions relating to financial supplies (even though financial supplies are input taxed) if you do not exceed the financial acquisitions threshold.

189‑5 Exceeding the financial acquisitions threshold—current acquisitions

General

(1) You exceed the financial acquisitions threshold at a time during a particular month if, assuming that all the *financial acquisitions you have made, or are likely to make, during the 12 months ending at the end of that month were made solely for a *creditable purpose, either or both of the following would apply:

(a) the amount of all the input tax credits to which you would be entitled for those acquisitions would exceed $50,000 or such other amount specified in the regulations;

(b) the amount of the input tax credits referred to in paragraph (a) would be more than 10% of the total amount of the input tax credits to which you would be entitled for all your acquisitions and importations during that 12 months (including the financial acquisitions).

Members of GST groups

(2) If you are a *member of a *GST group, you exceed the financial acquisitions threshold at a time during a particular month if, assuming that all the *financial acquisitions you or any other member of the group have made, or are likely to make, during the 12 months ending at the end of that month were made solely for a *creditable purpose, either or both of the following would apply:

(a) the amount of all the input tax credits to which you or any other member of the group would be entitled for those acquisitions would exceed $50,000 or such other amount specified in the regulations;

(b) the amount of the input tax credits referred to in paragraph (a) would be more than 10% of the total amount of the input tax credits to which you or any other member of the group would be entitled for all acquisitions and importations of any member of the group during that 12 months (including the financial acquisitions).

189‑10 Exceeding the financial acquisitions threshold—future acquisitions

General

(1) You exceed the financial acquisitions threshold at a time during a particular month if, assuming that all the *financial acquisitions you have made, or are likely to make, during that month and the next 11 months were made solely for a *creditable purpose, either or both of the following would apply:

(a) the amount of all the input tax credits to which you would be entitled for those acquisitions would exceed $50,000 or such other amount specified in the regulations;

(b) the amount of the input tax credits referred to in paragraph (a) would be more than 10% of the total amount of the input tax credits to which you would be entitled for all your acquisitions and importations during those months (including the financial acquisitions).

Members of GST groups

(2) If you are a *member of a *GST group, you exceed the financial acquisitions threshold at a time during a particular month if, assuming that all the *financial acquisitions you or any other member of the group have made, or are likely to make, during that month and the next 11 months were made solely for a *creditable purpose, either or both of the following would apply:

(a) the amount of all the input tax credits to which you or any other member of the group would be entitled for those acquisitions would exceed $50,000 or such other amount specified in the regulations;

(b) the amount of the input tax credits referred to in paragraph (a) would be more than 10% of the total amount of the input tax credits to which you or any other member of the group would be entitled for all acquisitions and importations of any member of the group during those months (including the financial acquisitions).

189‑15 Meaning of financial acquisition

A financial acquisition is an acquisition that relates to the making of a *financial supply (other than a financial supply consisting of a borrowing).

8 Section 195‑1 (definition of annual turnover of financial supplies)

Repeal the definition.

9 Section 195‑1

Insert:

exceed the financial acquisitions threshold has the meaning given by Division 189.

10 Section 195‑1

Insert:

financial acquisition has the meaning given by section 189‑15.

10A Section 195‑1

Insert:

fringe benefits tax means tax imposed by the Fringe Benefits Tax Act 1986.

10B Section 195‑1

Insert:

GST‑creditable benefit has the meaning given by section 149A of the Fringe Benefits Tax Assessment Act 1986.

11 Section 195‑1 (definition of reduced credit acquisition)

Omit “subsection 70‑5(1)”, substitute “section 70‑5”.

Schedule 6—Calculating amounts of GST

A New Tax System (Goods and Services Tax) Act 1999

1 After section 9‑85

Insert:

9‑90 Rounding of amounts of GST

One taxable supply recorded on an invoice

(1) If the amount of GST on a *taxable supply that is the only taxable supply recorded on a particular *invoice would, apart from this section, be an amount that includes a fraction of a cent, the amount of GST is rounded to the nearest cent (rounding 0.5 cents upwards).

Several taxable supplies recorded on an invoice

(2) If 2 or more *taxable supplies are recorded on the same *invoice, the total amount of GST on the supplies is:

(a) what would be the amount of GST if it were worked out by:

(i) working out the GST on each of the supplies (without rounding the amounts to the nearest cent); and

(ii) adding the amounts together and, if the total is an amount that includes a fraction of a cent, rounding it to the nearest cent (rounding 0.5 cents upwards); or

(b) the amount worked out using the following method statement:

Method statement

Step 1. Work out, for each *taxable supply, what would, apart from this section, be the amount of GST on the supply.

Step 2. If the amount for the supply has more decimal places than the number of decimal places allowed by the accounting system used to work out the amount, round the amount (up or down as appropriate) to that number of decimal places.

Note: Subsection (4) gives further details of this rounding.

Step 3. Work out the sum of the amounts worked out under step 1 and (if applicable) step 2 for each supply.

Step 4. If the sum under step 3 includes a fraction of a cent, round the sum to the nearest cent (rounding 0.5 cents upwards).

(3) Whether to use paragraph (2)(a) or paragraph (2)(b) to work out the total amount of GST on the supplies is a matter of choice for:

(a) the supplier if the amount is being worked out to ascertain the supplier’s liability for GST; or

(b) the *recipient of the supplies if the amount is being worked out to ascertain the recipient’s entitlement to input tax credits.

(4) In applying step 2 of the method statement in subsection (2), if:

(a) the number of decimal places in the amount for the supply exceeds by one decimal place the number of decimal places allowed by the accounting system used to work out the amount; and

(b) the last digit of the amount (before rounding) is 5;

the amount is rounded upwards to that number of decimal places.

Taxable supplies divided into items

(5) If one or more *taxable supplies recorded on the same *invoice are divided into 2 or more items:

(a) subsection (1) does not apply; and

(b) subsection (2) applies as if each such item represented a separate taxable supply.

Taxable supplies recorded on documents other than invoices

(6) If one or more *taxable supplies, none of which are recorded on an *invoice, are recorded on a document that is not an invoice, this section applies as if the document were an invoice.

2 After section 17‑10

Insert:

17‑15 Working out net amounts using approved forms

(1) You may choose to work out your *net amount for a tax period in the way specified in an *approved form if you use the form to notify the Commissioner of that net amount. The amount so worked out is treated as your net amount for the tax period.

Note: Choosing to use section 17‑5 to work out your net amount does not mean your GST return is not in the approved form: see subsection 31‑15(3).

(2) This section has effect despite section 17‑5.

3 At the end of section 31‑15

Add:

(3) The fact that, in your *GST return for the *tax period, your *net amount for the *tax period is worked out:

(a) in the way specified in section 17‑5; and

(b) not in the way specified in the *approved form for a GST return;

does not prevent your GST return for the tax period being treated as being in the approved form.

4 At the end of subsection 66‑50(3)

Add:

Note: Section 9‑90 (rounding of amounts of GST) can apply to amounts of GST worked out using this section.

5 At the end of subsection 75‑10(4)

Add:

Note: Section 9‑90 (rounding of amounts of GST) can apply to amounts of GST worked out using this section.

6 At the end of subsection 84‑12(2)

Add:

Note: Section 9‑90 (rounding of amounts of GST) can apply to amounts of GST worked out using this section.

A New Tax System (Goods and Services Tax Transition) Act 1999

7 After section 24A

Insert:

24B Commissioner may make determinations relating to rounding

(1) The Commissioner may determine in writing a way in which amounts of GST for taxable supplies recorded on invoices may be rounded for the purposes of:

(a) subsection 9‑90(1) of the GST Act; and

(b) subparagraph 9‑90(2)(a)(ii) of the GST Act; and

(c) step 4 in the method statement in subsection 9‑90(2) of the GST Act.

(2) However, the determination only applies:

(a) to the entity specified in the determination; and

(b) to taxable supplies attributable under the GST Act to tax periods that end on or before the day specified in the determination.

(3) The entity may round amounts of GST, for the purposes of the provisions referred to in paragraphs (1)(a), (b) and (c):

(a) in the way specified in the determination; or

(b) in the way specified in the provisions referred to in those paragraphs.

(4) The day specified under paragraph (2)(b) must not be later than 30 June 2002.

(5) An entity may apply to the Commissioner in writing for a determination under this section.

Note: Refusing an application for a determination under this section, and making determinations under this section, are reviewable GST transitional decisions (see Division 7 of Part VI of the Taxation Administration Act 1953).

(6) If one or more taxable supplies, none of which are recorded on an invoice, are recorded on a document that is not an invoice, this section applies as if the document were an invoice.

Taxation Administration Act 1953

8 After paragraph 62(1)(c)

Insert:

or (d) a reviewable GST transitional decision relating to you;

9 Subsection 62(1) (note)

Omit “and subsection (3) lists reviewable indirect tax decisions under this Part”, substitute “, subsection (3) lists reviewable indirect tax decisions under this Part and subsection (3A) lists reviewable GST transitional decisions under the A New Tax System (Goods and Services Tax Transition) Act 1999”.

10 After subsection 62(3)

Insert:

(3A) A decision under section 24B of the A New Tax System (Goods and Services Tax Transition) Act 1999 refusing an application for a determination under that section, or making a determination under that section, is a reviewable GST transitional decision.

A New Tax System (Australian Business Number) Act 1999

1 After subsection 37(1)

Insert:

(1A) Paragraph (1)(f) does not include a *non‑entity joint venture.

2 Section 41 (at the end of the definition of company)

Add “or a *non‑entity joint venture”.

3 Section 41

Insert:

non‑entity joint venture means an arrangement that the Registrar is satisfied is a contractual arrangement:

(a) under which 2 or more parties undertake an economic activity that is subject to the joint control of the parties; and

(b) that is entered into to obtain individual benefits for the parties, in the form of a share of the output of the arrangement rather than joint or collective profits for all the parties.

A New Tax System (Goods and Services Tax) Act 1999

4 Section 51‑1

Omit “Companies”, substitute “Entities”.

5 Subsections 51‑5(1) and (2)

Omit “*companies”, substitute “entities”.

6 Paragraphs 51‑5(1)(c), (d) and (e) and 51‑10(b)

Omit “companies”, substitute “entities”.

7 Paragraphs 51‑5(1)(e), 51‑45(2)(b) and (c), 51‑70(1)(c) and 51‑90(a)

Omit “company”, substitute “entity”.

8 Section 51‑10

Omit “A *company”, substitute “An entity”.

9 Section 51‑10

Omit “company”, substitute “entity”.

10 Subsections 51‑30(1), 51‑35(1) and 51‑40(1)

Omit “*company”, substitute “entity”.

11 Paragraphs 51‑30(2)(a), 51‑40(1)(b), 51‑45(2)(a), 51‑70(1)(a) and 51‑110(1)(b)

Omit “*company”, substitute “entity”.

12 After subsection 51‑45(2)

Insert:

(2A) However, while an election made by the *joint venture operator under section 51‑52 has effect:

(a) Division 17 applies to the joint venture operator as if the joint venture operator had an additional *net amount, relating to all the *GST joint ventures for which the joint venture operator is the joint venture operator, for each tax period; and

(b) that additional net amount is worked out by aggregating what would be the additional *net amounts relating to each GST joint venture under subsection (2) if that subsection applied.

13 After subsection 51‑50(2)

Insert:

(2A) However, while an election made by the *joint venture operator under section 51‑52 has effect:

(a) the joint venture operator must, in relation to all the *GST joint ventures for which the joint venture operator is the joint venture operator, give to the Commissioner a single *GST return for each tax period applying to the joint venture operator; and

(b) the *net amount stated in such a return must be the net amount relating to all those *GST joint ventures.

14 After section 51‑50

Insert:

51‑52 Consolidation of GST returns relating to GST joint ventures

Electing to consolidate GST returns

(1) The *joint venture operator of 2 or more *GST joint ventures may, by notifying the Commissioner in the *approved form, elect to give to the Commissioner consolidated *GST returns relating to all the GST joint ventures of the joint venture operator.

(2) The election takes effect on the day specified in the notice. However, the day specified must be the first day of a tax period applying to the *joint venture operator that has not already ceased when the notice is given.

Withdrawal of elections

(3) The *joint venture operator may, by notifying the Commissioner in the *approved form, withdraw the election.

(4) The withdrawal takes effect on the day specified in the notice. However, the day specified:

(a) must be the first day of a tax period applying to the *joint venture operator that has not already ceased when the notice is given; and

(b) must not be a day occurring earlier than 12 months after the election took effect.

Disallowance of elections

(5) The Commissioner may disallow the election if the Commissioner is satisfied that the *joint venture operator has a history of failing to comply with the joint venture operator’s obligations (either as a joint venture operator or in any other capacity) under a *taxation law.

Note: Disallowing an election is a reviewable GST decision (see Division 7 of Part VI of the Taxation Administration Act 1953).

(6) The disallowance is taken to have had effect from the start of the tax period in which the disallowance occurs.

15 Subsection 51‑55(1)

Omit “a *GST joint venture”, substitute “one or more *GST joint ventures”.

16 Paragraph 51‑55(1)(a)

Omit “the GST joint venture”, substitute “that GST joint venture or those GST joint ventures”.

17 Section 51‑60

Omit “a *GST joint venture”, substitute “one or more *GST joint ventures”.

18 Section 51‑60

Omit “the GST joint venture”, substitute “that GST joint venture or those GST joint ventures”.

19 Paragraph 51‑90(a)

Omit “*companies”, substitute “entities”.

20 After subsection 184‑1(1)

Insert:

(1A) Paragraph (1)(f) does not include a *non‑entity joint venture.

21 Section 195‑1 (at the end of the definition of company)

Add “or a *non‑entity joint venture”.

22 Section 195‑1 (definition of joint venture operator)

Omit “*company”, substitute “entity”.

23 Section 195‑1 (definition of participant)

Omit “a *company”, substitute “an entity”.

24 Section 195‑1

Insert:

minerals has the meaning given by section 330‑25 of the *ITAA 1997.

25 Section 195‑1

Insert:

non‑entity joint venture has the meaning given by subsection 995‑1(1) of the *ITAA 1997.

Income Tax Assessment Act 1936

26 Subsection 6(1) (at the end of the definition of company)

Add “or non‑entity joint ventures”.

27 Subsection 6(1)

Insert:

non‑entity joint venture has the meaning given by subsection 995‑1(1) of the Income Tax Assessment Act 1997.

Income Tax Assessment Act 1997

28 After subsection 960‑100(1)

Insert:

(1A) Paragraph (1)(e) does not include a *non‑entity joint venture.

29 Subsection 995‑1(1) (at the end of the definition of company)

Add “or a *non‑entity joint venture”.

30 Subsection 995‑1(1)

Insert:

non‑entity joint venture means an arrangement that the Commissioner is satisfied is a contractual arrangement:

(a) under which 2 or more parties undertake an economic activity that is subject to the joint control of the parties; and

(b) that is entered into to obtain individual benefits for the parties, in the form of a share of the output of the arrangement rather than joint or collective profits for all the parties.

Taxation Administration Act 1953

31 Section 8AAZA (at the end of the definition of company)

Add “or a non‑entity joint venture”.

32 Section 8AAZA

Insert:

non‑entity joint venture has the meaning given by subsection 995‑1(1) of the Income Tax Assessment Act 1997.

33 Subsection 62(2) (after table item 25)

Insert:

25A | disallowing an election to consolidate GST returns relating to GST joint ventures | subsection 51‑52(5) |

A New Tax System (Goods and Services Tax) Act 1999

1 Section 38‑355 (table item 6, 3rd column, paragraph (b))

Repeal the paragraph, substitute:

(b) insuring the *international transport of goods from their *place of export in Australia to a destination outside Australia; or (c) insuring: (i) the transport of goods from a place outside Australia to their *place of consignment in Australia; and (ii) the subsequent transport of those goods within Australia, if it is an integral part of the transport of goods from the place outside Australia to the place of consignment in Australia; including loading and handling within Australia that is part of that transport; or (d) insuring the transport of goods from a place outside Australia to the same or another place outside Australia.

|

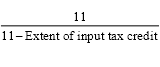

2 Subsection 78‑15(4) (method statement)

Repeal the method statement, substitute:

Method statement

Step 1. Add together:

(a) the sum of the payments of *money (if any) made in settlement of the claim; and

(b) the *GST inclusive market value of the supplies (if any) made by the insurer in settlement of the claim (other than supplies that would have been *taxable supplies but for section 78‑25).

Step 2. If any payments of excess were made to the insurer under the *insurance policy in question, subtract from the step 1 amount the sum of all those payments.

Step 3. Multiply the step 1 amount, or (if step 2 applies) the step 2 amount, by the following:

where:

extent of input tax credit has the meaning given by subsection (2).

3 Subparagraph 78‑50(1)(c)(i)

Omit “the insurance policy was supplied”, substitute “a claim was first made under the insurance policy since the last payment of a premium”.

4 After paragraph 78‑100(2)(c)

Insert:

(ca) those payments that that entity makes or is liable to make are treated as a premium it has paid; and

5 At the end of section 78‑100

Add:

(3) However, if the entity treated as the entity insured:

(a) is liable to make payments referred to in paragraph (2)(c); and

(b) has not made all those payments;

for the purposes of sections 78‑10 and 78‑15, the entity’s entitlement to an input tax credit for the premium paid is taken to be what its entitlement would have been if it had made all those payments.

A New Tax System (Goods and Services Tax Transition) Act 1999

6 After subsection 23(1)

Insert:

(1A) If, because of subsection (1), you are not entitled to an input tax credit for an acquisition you make, section 29‑70 of the GST Act (which is about tax invoices) does not apply in relation to the supply to which the acquisition relates.

7 Section 23A

Repeal the section.

A New Tax System (Goods and Services Tax) Act 1999

1 Paragraph 31‑15(1)(d)

Omit “section 31‑30”, substitute “section 388‑75 in Schedule 1 to the Taxation Administration Act 1953”.

2 At the end of subsection 31‑25(1)

Add:

Note: Section 388‑75 in Schedule 1 to the Taxation Administration Act 1953 deals with signing returns.

3 Subsection 31‑25(2)

Omit “unless the Commissioner is satisfied that it is not practicable for you to lodge your returns electronically”, substitute “unless the Commissioner otherwise approves”.

4 Subsection 31‑25(2) (note 2)

Omit “288‑5”, substitute “388‑80”.

5 Section 31‑30

Repeal the section.

6 Subsection 33‑10(2) (note 2)

Omit “288‑15 in that Schedule”, substitute “8AAZMA in that Act”.

7 After section 35‑5

Insert:

Your entitlement to be paid an amount under section 35‑5 arises when you give the Commissioner a *GST return under section 31‑5 or 31‑20.

8 Section 165‑80

Repeal the section.

9 Section 195‑1 (definition of approved form)

Repeal the definition, substitute:

approved form has the meaning given by section 388‑50 in Schedule 1 to the Taxation Administration Act 1953.

10 Section 195‑1 (definition of electronic signature)

Repeal the definition, substitute:

electronic signature has the meaning given by subsection 995‑1(1) of the Income Tax Assessment Act 1997.

11 Section 195‑1 (definition of GST return)

Omit “, 31‑25 and 31‑30”, substitute “and 31‑25 of this Act and section 388‑75 in Schedule 1 to the Taxation Administration Act 1953”.

Taxation Administration Act 1953

12 Section 8AAZA

Insert:

RBA group means a GST group under Division 48 of the A New Tax System (Goods and Services Tax) Act 1999.

13 Subsection 8AAZLA(1)

After “the entity”, insert “or, if the entity is a member of an RBA group, to an RBA of another member of the group”.

14 Subsection 8AAZLB(1)

After “the entity”, insert “or, if the entity is a member of an RBA group, against a non‑RBA tax debt of another member of the group”.

15 Sections 42 to 46

Repeal the sections.

16 After section 288‑35 in Schedule 1

Insert:

288‑40 Penalty for failing to register or cancel registration

You are liable to an administrative penalty of 20 penalty units if you fail to apply for registration, or to apply for cancellation of registration, as required by the *GST Act.

Note: See section 4AA of the Crimes Act 1914 for the current value of a penalty unit.

288‑45 Penalty for failing to issue tax invoice or adjustment note

(1) You are liable to an administrative penalty of 20 penalty units if you fail to issue a tax invoice as required by section 29‑70 of the *GST Act.

(2) You are liable to an administrative penalty of 20 penalty units if you fail to issue an adjustment note as required by section 29‑75 of the *GST Act.

Note: See section 4AA of the Crimes Act 1914 for the current value of a penalty unit.

288‑50 Penalty for both principal and agent issuing certain documents

An entity is liable to an administrative penalty of 20 penalty units if both the entity and its agent issue:

(a) separate tax invoices relating to the same taxable supply, contrary to subsection 153‑15(2) of the *GST Act; or

(b) separate adjustment notes for the same decreasing adjustment, contrary to subsection 153‑20(2) of that Act.

Note: See section 4AA of the Crimes Act 1914 for the current value of a penalty unit.

Taxation (Interest on Overpayments and Early Payments) Act 1983

17 Subsection 3(1) (at the end of the definition of relevant tax)

Add:

; or (o) GST assessed under the A New Tax System (Goods and Services Tax) Act 1999.

18 Application of amendments

(1) Subject to this item, the amendments made by this Schedule apply to things done on or after 1 July 2000.

(2) Those amendments do not apply to a return, statement, notice or other document, or a statement made or scheme entered into, in relation to the year starting on 1 July 1999 or an earlier year.

Schedule 9A—Producer rebates under the wine equalisation tax

A New Tax System (Wine Equalisation Tax) Act 1999

1 At the end of section 17‑1

Add “Producer rebates under Division 19 are a form of wine tax credit.”.

2 Section 17‑5 (after table item CR8)

Insert:

CR9 | *Producer rebate | You make an *assessable dealing in circumstances that entitle you to a *producer rebate under Division 19. | the amount of the *producer rebate under Division 19 | immediately before the end of the financial year in which the *assessable dealing occurs |

3 After Division 17

Insert:

19‑1 What this Division is about

Wine producers are entitled to a rebate for certain retail sales and AOUs of wine. The rebate tapers off when these sales and AOUs exceed a particular value. The rebate is provided in the form of a wine tax credit.

Note: Credit ground CR9 is producer rebates.

19‑5 Entitlement to producer rebates

Retail sales

(1) You are entitled to a *producer rebate for *rebatable wine in respect of a *financial year if:

(a) you are the *producer of the wine; and

(b) you are liable to wine tax for a *retail sale of the wine during the financial year; and

(c) the sale is from premises to which your *producer’s licence relates; and

(d) the sale does not contravene the *State law or *Territory law under which the licence was issued, or any conditions to which the licence is subject.

(2) A sale of wine by mail order or on the Internet is taken to be a sale from particular premises for the purposes of paragraph (1)(c) if the wine is sold under the *producer’s licence to which those premises relate.

AOUs

(3) You are also entitled to a *producer rebate for *rebatable wine in respect of a *financial year if:

(a) you are the *producer of the wine; and

(b) you are liable to wine tax for an *AOU of the wine during the financial year.

Exceptions

(4) However, you are not entitled to the rebate for the wine if:

(a) in the case of a *retail sale—you sell the wine in the course of providing, to the purchaser of the wine, other *food that is for consumption on the *premises from which it is supplied; or

(b) in the case of a retail sale—the sale is by mail order or on the Internet and a commission is payable to a third party for the sale, or a third party deducts an amount as commission from the proceeds of the sale; or

(c) in any case—in the *financial year in which the sale or *AOU occurs, your *annual rebatable turnover for the *producer’s licence under which the sale or AOU took place is more than $580,000.

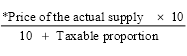

19‑10 Amount of producer rebates

(1) If the *annual rebatable turnover of a *producer of *rebatable wine for a particular *producer’s licence in a *financial year is $300,000 or less, the amount of the *producer rebates to which you are entitled in respect of that licence for that financial year is 14% of that turnover.

(2) If the *annual rebatable turnover of a *producer of *rebatable wine for a particular *producer’s licence in a *financial year is more than $300,000, the amount of the *producer rebates to which you are entitled in respect of that licence for that financial year is:

![]()

19‑15 Estimating amounts of producer rebates for each tax period

(1) The Commissioner may determine in writing how a *producer of *rebatable wine may work out estimates of amounts of *producer rebates that the producer may claim for the producer’s *tax periods during a *financial year (other than the last tax period of a financial year).

(2) An amount worked out in accordance with the determination, for one of the *tax periods applying to you, is treated as an amount of a *wine tax credit:

(a) to which you are entitled; and

(b) that arises during that tax period (even though under section 17‑5 it would arise at a later time).

(3) The amount of the *producer rebate to which you are entitled in respect of the *financial year is taken to be reduced by the sum of the amounts worked out under subsection (2) that you claim for *tax periods during the financial year.

(4) However, if the sum of the amounts worked out under subsection (2) that you claim for *tax periods during the *financial year exceeds the amount of the *producer rebate to which you are entitled in respect of the financial year:

(a) you are liable to pay an amount equal to that excess; and

(b) the amount is to be treated as if it were wine tax payable by you at the end of the financial year, and, for the purposes of Part 5, were attributable to the last tax period of the financial year.

19‑20 Annual rebatable turnover

The *annual rebatable turnover of a *producer of *rebatable wine for a particular *producer’s licence in a *financial year is the sum of:

(a) the *notional wholesale selling prices of all *retail sales of rebatable wine the producer makes in that financial year that are sales:

(i) made under the licence; and

(ii) to which subsection 19‑5(1) applies; and

(b) the notional wholesale selling prices of all *AOUs of rebatable wine the producer makes in that financial year that are AOUs:

(i) made under the licence; and

(ii) to which subsection 19‑5(3) applies.

4 Section 33‑1

Insert:

annual rebatable turnover has the meaning given by section 19‑20.

5 Section 33‑1

Insert:

financial year means a period of 12 months beginning on 1 July.

6 Section 33‑1

Insert:

food has the meaning given by section 38‑4 of the *GST Act.

7 Section 33‑1

Insert:

ITAA 1997 means the Income Tax Assessment Act 1997.

8 Section 33‑1

Insert:

premises, in relation to a supply of *food (other than wine), has the meaning given by section 38‑5 of the *GST Act.

9 Section 33‑1

Insert:

producer, of *rebatable wine, means an entity that:

(a) *manufactures the wine, or supplies to another entity the grapes, other fruit, vegetables or honey from which the wine is manufactured; and

(b) holds a *producer’s licence.

10 Section 33‑1

Insert:

producer rebate means a rebate to which a *producer of *rebatable wine is entitled under Division 19.

11 Section 33‑1

Insert:

producer’s licence means a licence, issued under a *State law or a *Territory law, to make *retail sales of wine from particular premises:

(a) as a wine producer or a vigneron; or

(b) in a similar capacity determined in writing by the Commissioner.

12 Section 33‑1

Insert:

rebatable wine means *grape wine, *grape wine products, *fruit or vegetable wine or *mead.

13 Section 33‑1

Insert:

State law has the meaning given by section 995‑1 of the *ITAA 1997.

14 Section 33‑1

Insert:

Territory law has the meaning given by section 995‑1 of the *ITAA 1997.

Schedule 10—Alcoholic beverages

A New Tax System (Goods and Services Tax Transition) Act 1999

1A After section 16A

Insert:

16AB Special GST credit for certain alcoholic beverages on which duty has decreased

(1) This section applies to goods if:

(a) you are entitled to a special credit under section 16 in respect of the goods; and

(b) they are goods mentioned in subsection 15A(1) (alcoholic beverages) of the Sales Tax (Exemptions and Classifications) Act 1992; and

(c) either:

(i) an amount of excise duty or customs duty (the old duty amount) in respect of the goods was paid before 1 July 2000; or

(ii) the goods were delivered into home consumption before 1 July 2000 under a permission given under subsection 61C(1) of the Excise Act 1901 or granted under subsection 69(3) of the Customs Act 1901, and an amount of excise duty or customs duty (the old duty amount) was or is payable in respect of the goods; and

(d) were excise duty or customs duty (whichever is applicable) instead to become payable on the goods immediately after 1 July 2000, the amount of that duty (the new duty amount) would be less than the old duty amount.

(2) The amount of the special credit in respect of the goods is increased by an amount equal to the difference between the old duty amount and the new duty amount.