Governor‑General Legislation Amendment Act 2001

No. 57, 2001

Governor‑General Legislation Amendment Act 2001

No. 57, 2001

Governor‑General Legislation Amendment Act 2001

No. 57, 2001

An Act to amend legislation in respect of the Governor‑General, and for related purposes

Contents

1 Short title...................................

2 Commencement...............................

3 Schedule(s)..................................

Schedule 1—Amendment of the Governor‑General Act 1974

Part 1—Salary

Part 2—Superannuation matters

Schedule 2—Amendment of taxation legislation

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Governor-General Legislation Amendment Act 2001

No. 57, 2001

An Act to amend legislation in respect of the Governor-General, and for related purposes

[Assented to 28 June 2001]

The Parliament of Australia enacts:

This Act may be cited as the Governor‑General Legislation Amendment Act 2001.

This Act commences on the day on which it receives the Royal Assent.

Each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

1 Section 3

Omit “$58,000”, substitute “$310,000”.

2 Transitional provision

The amendment made by this Part does not have effect during the continuance in office of the person holding office as Governor‑General immediately before the commencement of this Act.

3 Subsection 2A(2)

Insert:

assessment has the same meaning as in the Superannuation Contributions Tax (Assessment and Collection) Act 1997.

4 Subsection 2A(2)

Insert:

basic rate, at a particular time, in relation to a particular person, means 60% of the salary of the Chief Justice of Australia at that time, reduced by the amount of any pension or retiring allowance payable to that person at that time, whether by virtue of a law or otherwise out of money provided in whole or part by Australia, a State or a Territory.

5 Subsection 2A(2)

Insert:

notice of assessment, in respect of a person, means a notice given under subsection 15(8) of the Superannuation Contributions Tax (Assessment and Collection) Act 1997 to the person or to the person’s spouse, or to the legal personal representative of the person or the person’s spouse, stating that a person is liable to pay an amount of surcharge on surchargeable contributions for the person.

6 Subsection 2A(2)

Insert:

surcharge has the same meaning as in the Superannuation Contributions Tax (Assessment and Collection) Act 1997.

7 Subsection 2A(2) (definition of surcharge deduction amount)

Omit all the words from and including “means”, substitute:

means:

(c) for the purposes of calculating the prescribed percentage before the payment of the allowance has commenced—the amount by which the person’s surcharge debt account was in debit when the allowance became payable; or

(d) for the purposes of calculating the prescribed percentage after the payment of the allowance has commenced—the amount of surcharge on surchargeable contributions for the person which the trustee is liable to pay because of the operation of subsection 4(4).

8 Subsection 2A(2)

Insert:

surchargeable contributions, for a person, means surchargeable contributions within the meaning of the Superannuation Contributions Tax (Assessment and Collection) Act 1997 that are attributable to the operation of this Act in respect of the person.

9 Paragraphs 4(3)(a) and (b)

Repeal the paragraphs, substitute:

(a) if the person’s surcharge debt account was in debit when the allowance became payable to the person—a rate equal to 85% of the basic rate or the prescribed percentage of the basic rate at the relevant time, whichever is higher; or

(b) if the person’s surcharge debt account was not in debit when the allowance became payable to the person, whichever of the following rates is applicable:

(i) if a notice of assessment in respect of the person has been given before the relevant time—a rate equal to 85% of the basic rate or the prescribed percentage of the basic rate at that time, whichever is higher;

(ii) if a notice of assessment in respect of the person has not been given before the relevant time, and subsection (3AA) does not apply to the person at that time—a rate equal to 85% of the basic rate at that time;

(iii) if a notice of assessment in respect of the person has not been given before the relevant time, and subsection (3AA) applies to the person at that time—the basic rate at that time.

Note: For prescribed percentage, see subsection (3B).

10 After subsection 4(3)

Insert:

(3AA) This subsection applies to a person at a particular time (the relevant time) if, before the relevant time:

(a) the trustee of the Scheme (within the meaning of section 5A); and

(b) the person or, if the person is deceased, the person’s spouse or spouses or legal personal representative;

have reached a written agreement that a notice of assessment is not likely to be given in respect of the person.

11 Subsection 4(3A)

Repeal the subsection, substitute:

(3A) The rate of the allowance payable at any time (the relevant time) to a spouse of a deceased person who held office as Governor‑General is the amount worked out using the formula:

where:

adjustment amount means the amount of any pension or retiring allowance that would have been payable to the deceased person at the relevant time if the deceased person had not died, whether by virtue of a law or otherwise out of money provided in whole or part by Australia, a State or a Territory.

allowance rate means:

(a) if the person died while holding office as Governor‑General—the rate that would be applicable at the relevant time to the deceased person under subsection (3) if he or she had not died but had ceased to hold that office; or

(b) if the deceased person died after ceasing to hold office as Governor‑General—the rate that would be applicable at the relevant time to the deceased person under subsection (3) if he or she had not died.

reduction amount means the amount of any pension or retiring allowance payable to the spouse of the deceased person at the relevant time, whether by virtue of a law or otherwise out of money provided in whole or part by Australia, a State or a Territory.

12 Subsection 4(3B)

Repeal the subsection, substitute:

(3B) In subsection (3):

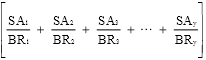

prescribed percentage, in relation to a person who has held office as Governor‑General, means the percentage worked out in accordance with the formula:

![]()

where:

SAt means the amount worked out in accordance with the formula:

where:

basic rate has the meaning given by section 2A.

BR1 is the basic rate at the time when the prescribed percentage is first calculated, and BR2, BR3 etc. have corresponding meanings for any later time when the prescribed percentage is calculated.

SA1 is the surcharge adjustment at the time when the prescribed percentage is first calculated, and SA2, SA3 etc. have corresponding meanings for any later time when the prescribed percentage is calculated.

surcharge adjustment means the amount obtained by dividing the person’s surcharge deduction amount by the conversion factor applicable to the person under the determination referred to in subsection (3C).

13 Subsection 4(4)

Repeal the subsection, substitute:

(4) If:

(a) a person ceases to hold office as Governor‑General; and

(b) after the person ceases to hold office, a notice of assessment (including an amended assessment) in respect of the person is given to the person, the person’s spouse or the legal personal representative of the person or the person’s spouse; and

(c) apart from this section, a person would be liable to pay surcharge under the assessment in accordance with the Superannuation Contributions Tax (Assessment and Collection) Act 1997;

the trustee of the Scheme (within the meaning of section 5A) is liable to pay the surcharge under the assessment mentioned in paragraph (b), and any general interest charge in respect of the surcharge, to the Commissioner of Taxation, and the liability of any other person to pay the surcharge or general interest charge, as the case requires, is discharged.

(5) Despite subsection (4), the trustee of the Scheme is not liable to pay the surcharge unless the person, the person’s spouse or the legal personal representative of the person or the person’s spouse gives the notice of assessment to the trustee of the Scheme.

(6) If, after an allowance became payable to a person under this section, a notice of assessment (including an amended assessment) of the person’s surcharge is given to the trustee of the Scheme as mentioned in subsection (5), the trustee must calculate or recalculate, as the case requires, the prescribed percentage of the basic rate in accordance with subsection (3B).

(7) Amounts payable under subsection (4) are to be paid out of the Consolidated Revenue Fund, which is appropriated accordingly.

14 Application provision

The repeals and amendments made by this Schedule do not apply to a person who held office as Governor‑General before 20 August 1996.

1 Subparagraph 97(3)(c)(i)

Omit “, 51‑15”.

2 Subsection 102AAE(2)

Omit “, 51‑15”.

3 Section 51‑15

Repeal the section.

4 Application

(1) The repeal and amendments made by this Schedule apply in relation to income derived on or after 29 June 2001 (the commencing day).

(2) However, the repeal and amendments do not apply in relation to income derived on or after the commencing day by a State Governor who held that office immediately before the commencing day.

[Minister’s second reading speech made in—

House of Representatives on 6 June 2001

Senate on 20 June 2001]

(108/01)