Superannuation Contributions Taxes and Termination Payments Tax Legislation Amendment Act 2001

No. 96, 2001

An Act to amend the law relating to superannuation contributions taxes and termination payments tax, and for related purposes

Superannuation Contributions Taxes and Termination Payments Tax Legislation Amendment Act 2001

No. 96, 2001

An Act to amend the law relating to superannuation contributions taxes and termination payments tax, and for related purposes

Contents

1 Short title

2 Commencement

3 Schedule(s)

Schedule 1—Amendment of the Superannuation Contributions Tax (Assessment and Collection) Act 1997

Schedule 2—Amendment of the Superannuation Contributions Tax (Members of Constitutionally Protected Superannuation Funds) Assessment and Collection Act 1997

Schedule 3—Amendment of the Termination Payments Tax (Assessment and Collection) Act 1997

Superannuation Contributions Taxes and Termination Payments Tax Legislation Amendment Act 2001

No. 96, 2001

An Act to amend the law relating to superannuation contributions taxes and termination payments tax, and for related purposes

[Assented to 15 August 2001]

The Parliament of Australia enacts:

This Act may be cited as the Superannuation Contributions Taxes and Termination Payments Tax Legislation Amendment Act 2001

(1) Subject to this section, this Act commences on the day on which it receives the Royal Assent.

(2) Schedule 1 is taken to have commenced on 5 June 1997, immediately after the commencement of the Superannuation Contributions Tax (Assessment and Collection) Act 1997.

(3) Schedule 2 is taken to have commenced on 7 December 1997, immediately after the commencement of the Superannuation Contributions Tax (Members of Constitutionally Protected Superannuation Funds) Assessment and Collection Act 1997.

(4) Schedule 3 is taken to have commenced on 5 June 1997, immediately after the commencement of the Termination Payments Tax (Assessment and Collection) Act 1997.

Subject to section 2, each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

1 After section 7

Insert:

7A Adjusted taxable income—first case

(1) This section applies to a member for a financial year if:

(a) no payments that were eligible termination payments for the purposes of Subdivision AA of Division 2 of Part III of the Income Tax Assessment Act because of paragraph (a) of the definition of eligible termination payment in subsection 27A(1) of that Act were made to or for the member in the financial year; or

(b) one or more such payments were so made but the total of the reduced amounts of the payments (other than payments that were rolled over before 1 July 1997) was equal to or greater than the amount specified in subsection 5(2) of the Superannuation Contributions Tax Imposition Act 1997 as altered under section 7 of that Act for the financial year.

(2) The reduced amount of an eligible termination payment is the amount (if any) remaining after deducting from the amount of the payment the amount of any post‑June 1994 invalidity component or CGT exempt component of the payment or any part of the payment that was made from an employee share acquisition scheme.

(3) The adjusted taxable income of the member for the financial year is the sum of:

(a) the member’s taxable income of the year of income comprising the financial year less any amounts included in the member’s assessable income of that year of income:

(i) that were eligible termination payments for the purposes of Subdivision AA of Division 2 of Part III of the Income Tax Assessment Act (other than amounts that were such payments because of paragraph (a) of the definition of eligible termination payment in subsection 27A(1) of that Act); or

(ii) that were so included under section 26AC or under subsection 26AD(2), (3) or (4) of the Income Tax Assessment Act in respect of a bona fide redundancy amount, an early retirement scheme amount or an invalidity amount as defined in section 159S of that Act; and

(b) in respect of the financial year beginning on 1 July 1996 or the following financial year—the amount (if any) by which the amount worked out under paragraph (a) would be increased if it were instead worked out ignoring subsection 271‑105(1) of Schedule 2F to the Income Tax Assessment Act; and

(c) in respect of the financial year beginning on 1 July 1998 or a later financial year—the amount (if any) by which the amount worked out under paragraph (a) would be increased if it were instead worked out ignoring paragraphs 102UK(2)(b) and 102UM(2)(b) of, and subsection 271‑105(1) of Schedule 2F to, the Income Tax Assessment Act; and

(d) the member’s surchargeable contributions for the financial year; and

(e) in respect of a financial year beginning on or after 1 July 1999—if the member is an employee (within the meaning of the Fringe Benefits Tax Assessment Act 1986) who has a reportable fringe benefits total (as defined in that Act) for the year of income comprising the financial year—the reportable fringe benefits total for the year of income.

7B Adjusted taxable income—second case

(1) This section applies to a member for a financial year if:

(a) one or more payments that were eligible termination payments for the purposes of Subdivision AA of Division 2 of Part III of the Income Tax Assessment Act because of paragraph (a) of the definition of eligible termination payment in subsection 27A(1) of that Act were made to or for the member in the financial year; and

(b) the total of the reduced amounts of the payments (other than payments that were rolled over before 1 July 1997) was less than the amount specified in subsection 5(2) of the Superannuation Contributions Tax Imposition Act 1997 as altered under section 7 of that Act for the financial year.

(2) The reduced amount of an eligible termination payment is the amount (if any) remaining after deducting from the amount of the payment the amount of any post‑June 1994 invalidity component or CGT exempt component of the payment or any part of the payment that was made from an employee share acquisition scheme.

(3) The adjusted taxable income of the member for the financial year is the sum of:

(a) the member’s taxable income of the year of income comprising the financial year less any of the following amounts included in the member’s assessable income of that year of income:

(i) amounts that were eligible termination payments for the purposes of Subdivision AA of Division 2 of Part III of the Income Tax Assessment Act;

(ii) amounts that were so included under section 26AC or under subsection 26AD(2), (3) or (4) of the Income Tax Assessment Act in respect of a bona fide redundancy amount, an early retirement scheme amount or an invalidity amount as defined in section 159S of that Act; and

(b) in respect of the financial year beginning on 1 July 1996 or the following financial year—the amount (if any) by which the amount worked out under paragraph (a) would be increased if it were instead worked out ignoring subsection 271‑105(1) of Schedule 2F to the Income Tax Assessment Act; and

(c) in respect of the financial year beginning on 1 July 1998 or a later financial year—the amount (if any) by which the amount worked out under paragraph (a) would be increased if it were instead worked out ignoring paragraphs 102UK(2)(b) and 102UM(2)(b) of, and subsection 271‑105(1) of Schedule 2F to, the Income Tax Assessment Act; and

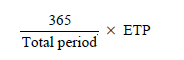

(d) in respect of each eligible termination payment referred to in subsection (1)—whichever of the following amounts is appropriate:

(i) if the post‑20 August 1996 period is less than 365 days—the amount (excluding any cents, cent or fraction of a cent included in that amount) worked out using the formula:

(ii) otherwise—the amount (excluding any cents, cent or fraction of a cent included in that amount) worked out using the formula:

where:

ETP means:

(a) if no part of the payment was rolled‑over—so much of the amount of the payment as is included in the member’s taxable income of the year of income comprising the financial year; or

(b) if any of the payment was rolled‑over—the sum of:

(i) so much of the part (if any) of the payment that was not rolled‑over as is included in the member’s taxable income of the year of income comprising the financial year; and

(ii) so much of the part of the payment that was rolled‑over after 30 June 1997 as would have been included in that taxable income if that part of the payment had not been rolled‑over.

post‑20 August 1996 period means the number of days in the period of the member’s employment for which the eligible termination payment was made that occurred after 20 August 1996.

total period means the number of days in the period of the member’s employment for which the eligible termination payment was made; and

(e) the member’s surchargeable contributions for the financial year less any amounts included in those surchargeable contributions because of subparagraph 8(2)(c)(iii); and

(f) in respect of a financial year beginning on or after 1 July 1999—if the member is an employee (within the meaning of the Fringe Benefits Tax Assessment Act 1986) who has a reportable fringe benefits total (as defined in that Act) for the year of income comprising the financial year—the reportable fringe benefits total for the year of income.

2 Subparagraph 8(2)(c)(iii)

Repeal the subparagraph, substitute:

(iii) subject to subsection (2A), constitute amounts accrued after 20 August 1996 that are eligible termination payments under paragraph (a) of the definition of eligible termination payment in subsection 27A(1) of that Act and are rolled‑over on or after 1 July 1997; and

3 Subsection 8(2A)

Omit all the words before the formula, substitute:

If an eligible termination payment within the meaning of subparagraph (2)(c)(iii) has been made or is made to or for a taxpayer after 20 August 1996, surcharge is payable only on the part of the reduced amount of the eligible termination payment that is worked out using the formula:

4 Subsection 8(2A)

Insert:

reduced amount of an eligible termination payment is the amount remaining after deducting from the amount of the payment any post‑June 1994 invalidity component or CGT exempt component of the payment or any part of the payment that was made from an employee share acquisition scheme.

5 Subparagraph 13(7)(a)(i)

Omit “and the total of so much of those amounts as are specified roll‑over amounts referred to in subparagraph 8(2)(c)(iii)”.

6 Section 43 (definition of adjusted taxable income)

Repeal the definition, substitute:

adjusted taxable income has the meaning given by section 7A or 7B, whichever is applicable.

7 Section 43

Insert:

rolled‑over has the meaning given by paragraph 27A(13)(a) of the Income Tax Assessment Act.

8 Section 43 (definition of specified roll‑over amount)

Repeal the definition.

9 Amendment of assessments

Nothing in the Superannuation Contributions Tax (Assessment and Collection) Act 1997 prevents the amendment of an assessment of surcharge on a member’s surchargeable contributions for a financial year for the purpose of giving effect to an amendment of that Act made by this Schedule if the Commissioner has sufficient information to satisfy himself or herself that the amendment is required or permitted for that purpose and the amendment does not increase the amount of surcharge payable in respect of those contributions.

1 Subparagraph 9(2)(c)(iii)

Repeal the subparagraph, substitute:

(iii) subject to subsection (3), constitute amounts accrued after 20 August 1996 that are eligible termination payments under paragraph (a) of the definition of eligible termination payment in subsection 27A(1) of that Act and are rolled‑over on or after 1 July 1997; and

2 Subsection 9(3)

Omit all the words before the formula, substitute:

If an eligible termination payment within the meaning of subparagraph (2)(c)(iii) has been made or is made to or for a taxpayer after 20 August 1996, surcharge is payable only on the part of the reduced amount of the eligible termination payment that is worked out using the formula:

3 Subsection 9(3)

Insert:

reduced amount of an eligible termination payment is the amount remaining after deducting from the amount of the payment any post‑June 1994 invalidity component or CGT exempt component of the payment or any part of the payment that was made from an employee share acquisition scheme.

4 Subparagraph 12(5)(a)(i)

Omit “and the total of so much of those amounts as are specified roll‑over amounts referred to in subparagraph 9(2)(c)(iii)”.

5 Section 38 (definition of adjusted taxable income)

Repeal the definition, substitute:

adjusted taxable income has the same meaning as in the Superannuation Contributions Tax (Assessment and Collection) Act 1997.

6 Section 38

Insert:

rolled‑over has the meaning given by paragraph 27A(13)(a) of the Income Tax Assessment Act.

7 Section 38 (definition of specified roll‑over amount)

Repeal the definition.

8 Amendment of assessments

Nothing in the Superannuation Contributions Tax (Members of Constitutionally Protected Superannuation Funds) Assessment and Collection Act 1997 prevents the amendment of an assessment of surcharge on a member’s surchargeable contributions for a financial year for the purpose of giving effect to an amendment of that Act made by this Schedule or Schedule 1 if the Commissioner has sufficient information to satisfy himself or herself that the amendment is required or permitted for that purpose and the amendment does not increase the amount of surcharge payable in respect of those contributions.

1 Subsection 8(1)

Omit “Termination payments surcharge”, substitute “Subject to subsection (1A), termination payments surcharge”.

2 After subsection 8(1)

Insert:

No surcharge is payable on excessive part of termination payments

(1A) In the case of a termination payment made after 7.30 pm by legal time in the Australian Capital Territory on 22 May 2001, surcharge is not payable on any part of the payment that the Commissioner has determined under section 140R of the Income Tax Assessment Act to be in excess of the RBLs of the taxpayer.

3 Section 9

Repeal the section, substitute:

9 Surcharge payable only on part of certain termination payments

(1) This section applies if a termination payment has been or is made to or for a taxpayer after 20 August 1996.

(2) In the case of a termination payment made at or before 7.30 pm by legal time in the Australian Capital Territory on 22 May 2001, surcharge is payable only on the part of the termination payment that is worked out using the formula:

(3)In the case of a termination payment made after 7.30 pm by legal time in the Australian Capital Territory on 22 May 2001, surcharge is payable only on the part of the termination payment that is worked out using the formula:

(4) For the purposes of this section:

excessive component means the part (if any) of the termination payment that the Commissioner has determined under section 140R of the Income Tax Assessment Act to be in excess of the RBLs of the taxpayer.

post‑20 August 1996 period means the number of days in the period of the taxpayer’s employment for which the termination payment was made that occurred after 20 August 1996.

total period means the number of days in the period of the taxpayer’s employment for which the termination payment was made.

4 Application

The amendments made by this Schedule apply only to payments made after 7.30 pm by legal time in the Australian Capital Territory on 22 May 2001.

5 Amendment of assessments

Nothing in the Termination Payments Tax (Assessment and Collection) Act 1997 prevents the amendment of an assessment of surcharge on termination payments made to or for a taxpayer for a financial year for the purpose of giving effect to an amendment of that Act made by this Schedule or Schedule 1 if the Commissioner has sufficient information to satisfy himself or herself that the amendment is required or permitted for that purpose and the amendment does not increase the amount of surcharge payable in respect of those termination payments.

[Minister’s second reading speech made in—

House of Representatives on 21 June 2001

Senate on 7 August 2001]

(112/01)