PART II—AMENDMENT OF THE CRIMES (TAXATION OFFENCES) ACT 1980

Principal Act

3. The Crimes (Taxation Offences) Act 19801 is in this Part referred to as the Principal Act.

Interpretation

4. Section 3 of the Principal Act is amended by inserting after paragraph (a) of the definition of “income tax” in subsection (1) the following paragraph:

“(aa) any amount payable to the Commissioner under Part IIIaa of the Income Tax Assessment Act;”.

PART III—AMENDMENT OF THE INCOME TAX ASSESSMENT ACT 1936

Principal Act

5. The Income Tax Assessment Act 19362 is in this Part referred to as the Principal Act.

Dividends paid instead of interest under certain short-term finance arrangements

6. Section 46c of the Principal Act is amended by inserting “(not being a debt dividend for the purposes of section 46d)” before “paid to the shareholder” in the definition of “debt dividend” in subsection (1).

7. Before section 47 of the Principal Act the following section is inserted:

Dividends paid instead of interest

“46d. (1) In this section, unless the contrary intention appears:

‘arrangement’ means any agreement, arrangement or understanding, whether formal or informal, whether express or implied and whether or not enforceable, or intended to be enforceable, by legal proceedings;

‘associate’ has the same meaning as in section 26aab;

‘commencing time’ means 1 o’clock in the afternoon, by legal time in the Australian Capital Territory, on 10 December 1986;

‘finance’ includes money raised by the issue of shares;

‘finance arrangement’, in relation to a company, means an arrangement entered into or carried out by any of the parties to the arrangement for the purpose, or for purposes that included the purpose:

(a) of enabling the company or an associate of the company to obtain finance (whether by way of renewal or otherwise); or

(b) of enabling the company or an associate of the company to obtain an extension of the period for which finance was obtained under an earlier arrangement;

‘loan’ includes the provision of credit or any other form of financial accommodation;

‘unfranked part’, in relation to a dividend (including a dividend that is not a frankable dividend within the meaning of section 160apa), means so much of the dividend as has not been franked in accordance with section 160aqf.

“(2) A dividend is a debt dividend for the purposes of this section if, and only if:

(a) the dividend is paid to a shareholder after the commencing time in respect of a share in a company (whether the company is a resident or a non-resident);

(b) the dividend is paid:

(i) in respect of a share issued after the commencing time; or

(ii) under a finance arrangement entered into after the commencing time; and

(c) having regard to:

(i) the manner in which the amount of dividends in respect of the share was to be calculated;

(ii) the conditions applicable to the payment of dividends in respect of the share; and

(iii) any other relevant matters;

the payment of the dividend may reasonably be regarded as equivalent to the payment of interest on a loan.

“(3) A shareholder is not entitled to, and shall not be allowed, a rebate under section 46 or 46a in respect of:

(a) a debt dividend paid before 1 July 1987; or

(b) the unfranked part of a debt dividend paid on or after 1 July 1987.”.

Distributions by liquidator

8. Section 47 of the Principal Act is amended by inserting after subsection (1) the following subsection:

“(1a) A reference in subsection (1) to income derived by a company includes a reference to:

(a) an amount included in the assessable income of the company otherwise than under section 160zo; or

(b) an amount that would be included in the assessable income of the company under section 160zo if:

(i) a reference in Part IIIa to the indexed cost base of an asset were a reference to the cost base of an asset;

(ii) section 160zc had not been enacted; and

(iii) for the purposes of Part IIIa:

(A) a net capital gain were taken to have accrued to a taxpayer in respect of a year of income if a capital gain or capital gains accrued to the taxpayer during the year of income; and

(B) the amount of the net capital gain that, under sub-subparagraph (A), is taken to have accrued to the taxpayer in respect of a year of income were an amount equal to the capital gain or the sum of the capital gains referred to in that sub-subparagraph.”.

Modified application of Act in relation to certain unit trusts

9. Section 102l of the Principal Act is amended by inserting in subsection (2) “and section 46d” before “apply”.

Modified application of Act in relation to certain unit trusts

10. Section 102t of the Principal Act is amended by inserting in subsection (2) “and section 46d” before “apply”.

Liability to withholding tax

11. Section 128b of the Principal Act is amended:

(a) by omitting from paragraph (1) (a) “,other than a non-resident who carries on business in Australia at or through a permanent establishment of the non-resident in Australia”; and

(b) by inserting after paragraph (3) (g) the following paragraph:

“(ga) income that consists of so much of a dividend as has been franked in accordance with section 160aqf;”.

Certain income not included in assessable income

12. Section 128d of the Principal Act is amended by inserting “paragraph 128b (3) (ga),” after “would, but for”.

Repeal of Division 11b of Part III

13. Division 11b of Part III of the Principal Act is repealed.

14. After Part III of the Principal Act the following Part is inserted:

“PART IIIaa—FRANKING OF DIVIDENDS

“Division 1—Interpretation

Interpretation

“160apa. In this Part, unless the contrary intention appears:

‘adjusted amount’, in relation to another amount (in this definition called the ‘basic amount’), means the amount calculated in accordance with the formula:

where:

BA is the basic amount; and

CR is the applicable general company tax rate;

‘amended assessment’ does not include an assessment that would not be an amended assessment except for section 171;

‘amended company tax assessment’ means an amended assessment of company tax;

‘applicable general company tax rate’ means:

(a) in relation to:

(i) the payment of a company tax instalment payable by a company for a year of income;

(ii) an assessment or amended assessment of the company tax payable by a company for a year of income;

(iii) a foreign tax credit allowable in respect of tax paid or payable by a company in respect of income derived in a year of income;

the general company tax rate for the year of tax to which the year of income relates;

(b) in relation to:

(i) the liability of a company to pay franking deficit tax for a franking year; or

(ii) an offset that relates to franking deficit tax payable by a company for a franking year;

the general company tax rate for:

(iii) if the franking year is a year of tax—that year of tax; or

(iv) in any other case—the year of tax in which the franking year ends; or

(c) in relation to:

(i) the payment during a financial year of a franked dividend to a shareholder in a company; or

(ii) a trust amount or partnership amount that relates, directly or indirectly, to the payment during a financial year of a franked dividend to a shareholder in a company;

the general company tax rate for that financial year;

‘approved form’ means a form approved by the Commissioner for the purposes of the provision in which the expression occurs;

‘committed future dividends’, in relation to a company at a particular time (in this definition called the ‘current time’) in a franking year, means:

(a) frankable dividends in respect of which the following conditions are satisfied at the current time:

(i) the amount of the dividends is fixed;

(ii) the rights to be paid the dividends are set out in the company’s constituent document;

(iii) the dividends are to be paid after the current time and before the end of the franking year to shareholders in the company; or

(b) frankable dividends that, under a resolution made before or at the current time, are to be paid before the end of the franking year to shareholders in the company, other than dividends having a reckoning day before the current time;

‘company tax’ means tax assessed on the taxable income of a company;

‘company tax instalment’ means an instalment of tax payable under Division 1a of Part VI;

‘data processing device’ means any article or material from which information is capable of being reproduced with or without the aid of any other article or device;

‘director’, in relation to a company, includes any person occupying or acting in the position of director of the company, by whatever name called and whether or not validly appointed to occupy, or duly authorised to act in, the position;

‘dividend statement’ means a statement under section 160aqh;

‘eligible year of income’ means the year of income commencing on 1 July 1986 or a subsequent year of income;

‘estimated debit’ means an estimated debit specified in an estimated debit determination;

‘estimated debit determination’ means a determination made by the Commissioner under section 160aqd;

‘flow-on franking amount’ means:

(a) in relation to a trust amount—so much of the trust amount as is attributable to:

(i) a franked dividend included in the assessable income of the trust estate;

(ii) the flow-on franking amount in relation to another trust amount included in the assessable income of the trust estate; or

(iii) the flow-on franking amount in relation to a partnership amount that is included in, or allowed as a deduction from, the assessable income of the trust estate; and

(b) in relation to a partnership amount—so much of the partnership amount as is attributable to:

(i) a franked dividend included in the assessable income of the partnership; or

(ii) the flow-on franking amount in relation to a trust amount included in the assessable income of the partnership;

‘foreign tax credit’ means a credit within the meaning of Division 19 of Part III;

‘frankable dividend’ means:

(a) a dividend within the meaning of section 6; or

(b) a distribution that is deemed to be a dividend by subsection 47 (1) otherwise than by the operation of subsection 47 (2a);

being in either case a dividend paid by a company to a shareholder on or after 1 July 1987, but does not include:

(c) a dividend for which the reckoning day is before 1 July 1987;

(d) a dividend for which a deduction is allowable under section 120; or

(e) a dividend to which paragraph 24j (2) (a) applies that is deemed by section 24j to be derived from sources in a prescribed Territory (as defined in paragraph 24ba (a));

‘franked amount’, in relation to a dividend, means so much of the dividend as has been franked in accordance with section 160aqf;

‘franked dividend’ means a dividend the whole or part of which has been franked in accordance with section 160aqf;

‘franking account assessment’ means the ascertainment of the franking account balance and of any franking deficit tax payable;

‘franking account balance’, in relation to a company, means:

(a) if the company has a franking surplus—the amount of that surplus;

(b) if the company has a franking deficit—the amount of that deficit; and

(c) in any other case—nil;

‘franking additional tax’ means additional tax payable under Division 11;

‘franking additional tax assessment’ means the ascertainment of franking additional tax;

‘franking assessment’ means:

(a) a franking account assessment; or

(b) a franking additional tax assessment;

‘franking deficit’ means a deficit calculated under section 160apj;

‘franking deficit tax’ means tax payable in accordance with section 160aqj;

‘franking surplus’ means a surplus calculated under section 160apj;

‘franking year’, in relation to a company, means:

(a) if the Commissioner determines under section 160aph that a period is to be treated as a franking year in relation to the company—that period;

(b) if paragraph (a) does not apply and the company is an early balancing company for the purposes of subsection 221ab (1)—the substituted instalment period referred to in that subsection; or

(c) in any other case—a financial year;

‘general company tax rate’ means the rate of tax imposed on taxable incomes of companies, other than companies that are registered organisations within the meaning of Division 8a of Part III;

‘liability reduction action’, in relation to a company, means action seeking:

(a) a reduction in an amount of company tax;

(b) an entitlement to a foreign tax credit or an increase in such an entitlement; or

(c) an entitlement to an offset or an increase in such an entitlement;

‘offset’ means an amount applied in accordance with Subdivision C of Division 5 in reduction of company tax payable by a company;

‘offset determination’ means a determination under Subdivision C of Division 5 of the entitlement of a company to an offset;

‘ordinary assessment’ means an assessment under this Act other than this Part;

‘ordinary return’ means a return under this Act other than this Part;

‘original assessment date’ means:

(a) in relation to a franking assessment other than an amended assessment—the day on which the assessment was made; and

(b) in relation to a franking assessment that is the first or a subsequent amendment of an assessment to which paragraph (a) applies—the day on which the original assessment was made;

‘original company tax assessment’ means an assessment, other than an amended assessment, of company tax;

‘paid’, in relation to an amount payable to the Commissioner under this Act, includes discharged by the application of a credit or other amount by the Commissioner;

‘partnership amount’ means an amount included in, or allowed as a deduction from, the assessable income of a partner under section 92;

‘potential rebate amount’ means:

(a) in relation to a trust amount (in this paragraph called the ‘current trust amount’):

(i) where the flow-on franking amount in relation to the current trust amount is attributable to a franked dividend included in the assessable income of the trust estate—the amount calculated in accordance with the formula:

where

CF is the number of dollars in the flow-on franking amount in relation to the current trust amount;

PR is the amount included in the assessable income of the trust estate under section 160aqt in relation to the franked dividend; and

TF is the number of dollars in so much of the net income of the trust estate as is attributable to the franked dividend;

(ii) where the flow-on franking amount in relation to the current trust amount is attributable to the flow-on franking amount in relation to another trust amount (in this subparagraph called the ‘earlier trust amount’)—the amount calculated in accordance with the formula:

where:

CF is the number of dollars in the flow-on franking amount in relation to the current trust amount;

EPR is the potential rebate amount in relation to the earlier trust amount; and

TF is the number of dollars in so much of the net income of the trust estate as is attributable to the flow-on franking amount in relation to the earlier trust amount; or

(iii) where the flow-on franking amount in relation to the current trust amount is attributable to the flow-on franking amount in relation to a partnership amount— the amount calculated in accordance with the formula:

where:

CF is the number of dollars in the flow-on franking amount in relation to the current trust amount;

PR is the potential rebate amount in relation to the partnership amount; and

TF is the number of dollars in so much of the net income of the trust estate as is attributable to the flow-on franking amount in relation to the partnership amount; or

(b) in relation to a partnership amount:

(i) where the flow-on franking amount in relation to the partnership amount is attributable to a franked dividend included in the assessable income of the partnership—the amount calculated in accordance with the formula:

where:

CF is the number of dollars in the flow-on franking amount in relation to the partnership amount;

PR is the amount included in the assessable income of the partnership under section 160aqt in relation to the franked dividend; and

TF is the number of dollars in so much of the net income of the partnership or of the partnership loss as is attributable to the franked dividend; or

(ii) where the flow-on franking amount in relation to the partnership amount is attributable to the flow-on franking amount in relation to a trust amount—the amount calculated in accordance with the formula:

where:

CF is the number of dollars in the flow-on franking amount in relation to the partnership amount;

PR is the potential rebate amount in relation to the trust amount; and

TF is the number of dollars in so much of the net income of the partnership or of the partnership loss as is attributable to the flow-on franking amount in relation to the trust amount;

‘reckoning day’, in relation to a dividend paid to a shareholder in a company, means:

(a) if the dividend is paid under a resolution under which other dividends are payable to shareholders in the company—the day on which the first dividend is paid under that resolution; or

(b) in any other case—the day on which the dividend is paid;

‘resolution’, in relation to the payment of dividends to a shareholder in a company, means:

(a) an authorisation;

(b) a declaration;

(c) a resolution; or

(d) an agreement;

given or made by:

(e) the company; or

(f) all or any of the directors of the company;

in accordance with the rules governing the payment of dividends by the company, that those dividends be paid;

‘taxation officer’ means a person exercising powers, or performing functions under, pursuant to or in relation to this Act or the regulations;

‘termination time’ means:

(a) in relation to the taking of liability reduction action by a company:

(i) if the action is a request for consideration of a matter by a particular court or tribunal:

(A) if proceedings in relation to the matter terminate in a manner favourable to the company—the time of service by the Commissioner of a notice of an assessment or determination made by the Commissioner giving effect to the determination of the matter by that court or tribunal; or

(B) in any other case—the time when that matter is determined by that court or tribunal; or

(ii) if the action is a request for consideration of a matter by the Commissioner:

(A) if the Commissioner makes a decision on the matter in a manner favourable to the company—the time of service by the Commissioner of a notice of an assessment or determination made by the Commissioner giving effect to the Commissioner’s decision on the matter; or

(B) in any other case—the time of service by the Commissioner of a notice of the Commissioner’s decision on that matter;

(b) in relation to the payment of a company tax instalment or company tax instalments—the time of service by the Commissioner of notice of the application (whether by credit, refund or both) of the instalment or instalments in accordance with section 221AI; or

(c) in relation to an estimated debit—the termination time ascertained under paragraph (a) or (b) in relation to the application by the company for the determination by the Commissioner of the debit;

‘trust amount’, in relation to a trust estate, means:

(a) a share of the net income of the trust estate that is included in the assessable income of a beneficiary under section 97, 98a or 100;

(b) a share of the net income of the trust estate in respect of which the trustee is liable to be assessed under section 98; or

(c) the net income, or a part of the net income, of the trust estate in respect of which the trustee is liable to be assessed under section 99 or 99a;

‘withholding income’ means income to which section 128b would apply but for paragraph 128b (3) (ga).

Reference to company not to include trustee

“160abp. A reference in this Part to a company does not include a reference to a company in the capacity of a trustee.

Liquidators

“160apc. A reference in this Part to a company includes a reference to the liquidator of a company.

Interim dividends

“160apd. For the purposes of this Part, interim dividends that are to be paid at or before a particular time shall be taken to be payable at or before that time.

What constitutes a class of shares

“160ape. (1) Subject to subsection (2), a share in a company shall be taken for the purposes of this Part to be in the same class as another share in the company if, and only if, the shares have the same nominal value.

“(2) A share in a company shall not be taken for the purposes of this Part to be in the same class as another share in the company if different rights are attached to the shares, under the constituent document of the company, in respect of all or any of the following:

(a) the receipt of dividends;

(b) the receipt of any distribution of capital of the company;

(c) the exercise of the voting power in the company.

Deemed separate dividend resolutions

“160apf. For the purposes of this Part, a resolution that, but for this section, would be a single resolution in relation to dividends to be paid in respect of shares of 2 or more classes shall be treated as being separate resolutions in relation to the dividends to be paid in respect of the shares of each of those classes.

Sufficient residence for company in year of income

“160apg. For the purposes of this Part, a company is sufficiently resident in a year of income if, and only if:

(a) the company is a resident for more than one-half of the year of income; or

(b) the company is a resident at all times during the year of income when the company exists.

Commissioner may determine that period be treated as a franking year

“160aph. (1) For the purpose of ensuring the effective operation of this Part in relation to companies whose accounting periods change, where:

(a) a company that is an early balancing company for the purposes of subsection 221ab (1) adopts a different accounting period; or

(b) a company becomes, or ceases to be, an early balancing company for the purposes of that subsection;

the Commissioner may, by notice in writing served on the company, determine that a period specified in the notice shall be treated as a franking year in relation to the company.

“(2) The period specified in the notice may:

(a) commence earlier than the date of service of the notice; and

(b) be shorter or longer than a period of 12 months.

“Division 2—Franking Surplus or Deficit

“Subdivision A—Ascertainment of Surplus or Deficit

Ascertainment of surplus or deficit

“160apj. (1) The franking surplus of a company at a particular time in a franking year is the amount by which the total of the franking credits of the company arising in the franking year and before that time exceeds the total of the franking debits of the company arising in the franking year and before that time.

“(2) The franking deficit of a company at a particular time in a franking year is the amount by which the total of the franking debits of the company arising in the franking year and before that time exceeds the total of the franking credits of the company arising in the franking year and before that time.

“Subdivision B—Franking Credits

Residence requirement for credit to arise in relation to year of income

“160apk. A franking credit of a company does not arise in relation to:

(a) the payment of a company tax instalment for a year of income;

(b) an assessment or amended assessment of company tax for a year of income; or

(c) a foreign tax credit allowable in respect of tax paid or payable by the company in respect of income derived in a year of income;

unless the company is sufficiently resident in the year of income.

Carry forward of franking surplus

“160apl. Where a company has a franking surplus at the end of a franking year, there arises at the beginning of the next franking year a franking credit of the company equal to that franking surplus.

Payment of company tax instalment

“160apm. Where, on a particular day, a company tax instalment payable by a company for an eligible year of income is paid, there arises on that day a franking credit of the company equal to the adjusted amount in relation to the amount paid.

Receipt of company tax assessment

“160apn. Where, on a particular day, the Commissioner serves on a company a notice of an original company tax assessment for an eligible year of income, there arises on that day a franking credit of the company equal to the adjusted amount in relation to the company tax.

Receipt of franked dividends

“160app. Where:

(a) on a particular day, a franked dividend is paid to a shareholder being a company; and

(b) the company is a resident at the time the dividend is paid;

there arises on that day a franking credit of the company equal to the franked amount of the dividend.

Receipt of franked dividends through trusts and partnerships

“160apq. Where:

(a) a trust amount or partnership amount is included in, or a partnership amount is allowed as a deduction from, the assessable income of a company; and

(b) there is a flow-on franking amount in relation to the trust amount or the partnership amount;

there arises, at the end of the year of income of the trustee or partnership to which the trust amount or partnership amount relates, a franking credit of the company equal to the amount calculated in accordance with the formula:

where:

CR is the applicable general company tax rate; and

PR is the potential rebate amount in relation to the trust amount or partnership amount.

Amended company tax assessment increasing tax

“160apr. Where:

(a) on a particular day, the Commissioner serves on a company a notice of an amended company tax assessment for an eligible year of income; and

(b) the amendment increases the company tax of the company;

there arises on that day a franking credit of the company equal to the adjusted amount in relation to the amount of the increase.

Reduction of offset

“160aps. Where, on a particular day, the Commissioner serves on a company a notice of a determination reducing an offset to which the company is entitled, there arises on that day a franking credit of the company equal to the adjusted amount in relation to the amount of the reduction.

Reduction of foreign tax credit

“160apt. Where, on a particular day, the Commissioner serves on a company a notice of a determination reducing a foreign tax credit allowable in respect of tax paid or payable by the company in respect of income derived in an eligible year of income, there arises on that day a franking credit of the company equal to the adjusted amount in relation to the amount of the reduction.

Lapsing of estimated debit

“160apu. On the day on which the termination time in relation to an estimated debit of a company occurs, there arises a franking credit of the company equal to the estimated debit.

Substituted estimated debit determination

“160apv. Where, on a particular day, the Commissioner serves on a company a notice of an estimated debit determination that is in substitution for an earlier determination, there arises on that day a franking credit of the company equal to the amount of the franking debit that arose because of the earlier determination.

“Subdivision C—Franking Debits

Residence requirement for debit to arise in relation to year of income

“160apw. A franking debit of a company does not arise in relation to:

(a) the payment of a company tax instalment for a year of income;

(b) an amended assessment of company tax for a year of income; or

(c) a foreign tax credit allowable in respect of tax paid or payable by the company in respect of income derived in a year of income;

unless the company is sufficiently resident in the year of income.

Under-franking

“160apx. Where:

(a) the required franking amount for a frankable dividend paid by a company on a particular day is not less than 10% of the amount of the dividend; and

(b) that required franking amount exceeds the franked amount of the dividend;

there arises on that day a franking debit of the company equal to the excess referred to in paragraph (b).

Application of company tax instalment

“160apy. Where:

(a) under section 221aI, the Commissioner applies (whether by credit, refund or both) the whole or a part of an amount of a company tax instalment paid by a company for an eligible year of income; and

(b) on a particular day, the Commissioner serves on the company a notice specifying the amount so applied;

there arises on that day a franking debit of the company equal to the adjusted amount in relation to the amount specified in the notice.

Amended company tax assessment reducing tax

“160apz. Where:

(a) on a particular day, the Commissioner serves on a company a notice of an amended company tax assessment for an eligible year of income; and

(b) the amendment reduces the company tax of the company;

there arises on that day a franking debit of the company equal to the adjusted amount in relation to the amount of the reduction.

Allowance of offset

“160aq. Where, on a particular day, the Commissioner serves on a company a notice of:

(a) a determination that the company is entitled to an offset; or

(b) a determination increasing the amount of an offset to which the company is entitled;

there arises on that day a franking debit of the company equal to the adjusted amount in relation to:

(c) if paragraph (a) applies—the offset; or

(d) if paragraph (b) applies—the amount of the increase.

Allowance of foreign tax credit

“160aqa. Where, on a particular day, the Commissioner serves on a company a notice of:

(a) a determination that a foreign tax credit is allowable in respect of tax paid or payable by the company in respect of income derived in an eligible year of income; or

(b) a determination increasing such a foreign tax credit;

there arises on that day a franking debit of the company equal to the adjusted amount in relation to:

(c) if paragraph (a) applies—the foreign tax credit; or

(d) if paragraph (b) applies—the amount of the increase.

Payment of franked dividends

“160aqb. Where, on a particular day, a company pays a franked dividend, there arises on that day a franking debit of the company equal to the franked amount of the dividend.

Estimated debit determination

“160aqc. Where, on a particular day, the Commissioner serves on a company notice of an estimated debit determination, there arises on that day a franking debit of the company equal to the estimated debit specified in the notice.

“Division 3—Estimated Debits

Determination of estimated debit

“160aqd. (1) Where a company:

(a) has taken liability reduction action; or

(b) has paid a company tax instalment or company tax instalments;

the company may lodge an application with the Commissioner for:

(c) the determination of an estimated debit in relation to the liability reduction action or in relation to the payment of the instalment or instalments; or

(d) the determination of such an estimated debit in substitution for an earlier determination.

“(2) The application:

(a) shall be made before the termination time;

(b) shall be in the approved form; and

(c) shall specify the amount of the estimated debit being applied for.

“(3) The Commissioner:

(a) may determine an estimated debit not greater than the amount specified in the application; and

(b) shall serve notice of any such determination on the company.

“(4) Where:

(a) a company lodges an application with the Commissioner on a particular day (in this subsection called the ‘application day’); and

(b) at the end of the twenty-first day after the application day, the Commissioner has neither:

(i) served notice of an estimated debit determination on the company; nor

(ii) refused to make an estimated debit determination; the Commissioner shall be deemed, on the twenty-second day after the application day, to have:

(c) determined an estimated debit in accordance with the application; and

(d) served notice of the determination on the company.

“(5) A notice of an estimated debit determination has no effect if it is served after the termination time.

“Division 4—Required Franking Amount

Ascertainment of required franking amount

“160aqe. (1) For the purposes of this Part, the required franking amount for a dividend (in this section called the ‘current dividend’) paid during a franking year (in this section called the ‘current franking year’) to a shareholder in a company is so much of the dividend as does not exceed:

(a) if only one provisional required franking amount applies under the following provisions of this section—that provisional required franking amount; or

(b) in any other case—the greater or greatest of the provisional required franking amounts applicable under the following provisions of this section (whether or not 2 such amounts are applicable under the same subsection).

“(2) The amount calculated in accordance with the following formula is a provisional required franking amount:

where:

CD is the amount of the current dividend;

CFD is the number of dollars in the total amount of the committed future dividends of the company at the beginning of the reckoning day for the current dividend (other than dividends included in component TD);

RFS is the number of dollars in the amount of the franking surplus of the company at the beginning of the reckoning day for the current dividend being that franking surplus reduced, for each frankable dividend (in this definition called an ‘earlier dividend’) payable to a shareholder in the company that:

(a) has a reckoning day earlier than the reckoning day for the current dividend; and

(b) has not been paid before the reckoning day for the current dividend;

by the greater of:

(c) the amount that will be the franked amount of the earlier dividend; or

(d) the required franking amount for the earlier dividend;

SDD is the number of dollars in the total amount of frankable dividends that:

(a) are paid or payable to shareholders in the company; and

(b) have the same reckoning day as the current dividend; (other than dividends included in component CFD or component TD); and

TD is:

(a) if the current dividend is paid under a resolution—the total amount of the frankable dividends paid or payable under the resolution to shareholders in the company; or

(b) in any other case—the amount of the current dividend.

“(3) Where:

(a) a franked dividend having a reckoning day earlier in the franking year than the reckoning day for the current dividend has been paid to a shareholder in the company;

(b) the franked amount of that earlier franked dividend exceeded the required franking amount for that earlier franked dividend; and

(c) at the beginning of that earlier reckoning day, the current dividend was a committed future dividend;

the amount calculated in accordance with the following formula is a provisional required franking amount:

where:

CD is the amount of the current dividend;

EFA is the number of dollars in the franked amount of the earlier franked dividend; and

EFD is the number of dollars in the amount of the earlier franked dividend.

“(4) Where:

(a) a franked dividend other than the current dividend is paid on the reckoning day for the current dividend;

(b) the other dividend and the current dividend are not paid under the same resolution;

(c) the reckoning day for the other dividend is the same as the reckoning day for the current dividend; and

(d) the required franking amount for that other franked dividend, calculated without regard to this subsection, is less than the franked amount of that other franked dividend;

the amount calculated in accordance with the following formula is a provisional required franking amount:

where:

CD is the amount of the current dividend;

OFA is the number of dollars in the franked amount of the other dividend; and

OFD is the number of dollars in the amount of the other dividend.

“Division 5—Franking of Dividends

“Subdivision A—Franking

What constitutes franking

“160aqf. (1) Where:

(a) a frankable dividend (in this subsection called the ‘current dividend’) is paid to a shareholder in a company;

(b) the company is a resident at the time of payment;

(c) if the current dividend is paid under a resolution:

(i) before the reckoning day for the current dividend, the company makes a declaration that each dividend to which the resolution relates is a franked dividend to the extent of a percentage (not exceeding 100%) specified in the declaration in relation to the dividend; and

(ii) the percentage so specified is the same for each of the dividends to which the resolution relates; and

(d) if the current dividend is not paid under a resolution—the company makes a declaration before the reckoning day for the current dividend that the current dividend is a franked dividend to the extent of a percentage (not exceeding 100%) specified in the declaration;

the current dividend shall be taken to have been franked to the extent of the amount calculated in accordance with the formula:

where:

CD is the amount of the current dividend; and

SP is the percentage specified in the declaration in relation to the dividend.

“(2) A declaration made for the purposes of this section cannot be varied or revoked.

Combined class of dividends to be equally franked

“160aqg. (1) The dividends paid during a franking year to shareholders in a company that satisfy the following conditions shall be taken to constitute a combined class of dividends:

(a) the dividends are paid in respect of shares of the same class (in this subsection called the ‘applicable class’);

(b) each of the dividends is paid under a resolution, but not all the dividends are paid under the same resolution;

(c) for each resolution to which paragraph (b) applies, the dividends to which the resolution relates are to be paid on only some of the shares of the applicable class.

“(2) Dividends that constitute a combined class of dividends shall be taken for the purposes of section 160aqf to have been paid under the resolution under which the first of those dividends was paid and not under any other resolution.

Company to give dividend statement to shareholders

“160aqh. A company that is a resident at the time of payment of a frankable dividend to a shareholder in the company shall, before or at the time of payment of the dividend, give to the shareholder a statement in the approved form setting out:

(a) if the dividend is not a franked dividend—a declaration to that effect;

(b) if the dividend is a franked dividend:

(i) the franked amount of the dividend;

(ii) the amount of the dividend reduced by the franked amount of the dividend;

(iii) the amount calculated in relation to the dividend in accordance with the formula in section 160aqt (whether or not that section applies to the dividend); and

(iv) any amount deducted from the dividend under section 221yl; and

(c) in either case—such other information in relation to the dividend as is required by the approved form to be set out.

“Subdivision B—Franking Deficit Tax

Liability to franking deficit tax

“160aqj. Where a company has a franking deficit at the end of a franking year, the company is liable to pay tax equal to the amount calculated in accordance with the formula:

where:

CR is the applicable general company tax rate; and

FD is the amount of the franking deficit.

“Subdivision C—Franking Deficit Tax to Offset Company Tax

Entitlement to offset

“160aqk. (1) Subject to this Subdivision, where:

(a) a company has become liable to pay franking deficit tax for a franking year; and

(b) after the end of the franking year:

(i) the Commissioner serves on the company a notice of an original company tax assessment for an eligible year of income in which the company was sufficiently resident; or

(ii) the Commissioner serves on the company a notice of an amended company tax assessment for an eligible year of income in which the company was sufficiently resident, being an amendment that increases the company tax of the company;

the Commissioner shall determine that the company is entitled to an offset in relation to that company tax or increased company tax equal to the amount specified in the determination, being the lesser of the following amounts:

(c) the amount of the franking deficit tax, reduced by any part of it that has been previously applied under this Subdivision;

(d) the amount of the company tax, or increased company tax, reduced by any foreign tax credits allowable in respect of tax paid or payable by the company in respect of income derived in the eligible year of income.

“(2) Where a company becomes entitled to an offset in relation to company tax or increased company tax, the company’s liability to pay that company tax, or increased company tax, shall be reduced by the amount of the offset.

Amendment of determination

“160aql. (1) The Commissioner may at any time amend an offset determination in such manner as the Commissioner thinks necessary.

“(2) For the purposes of this Act, an amended determination shall be treated like a determination.

Notice of determination

“160aqm. (1) The Commissioner shall serve notice in writing of an offset determination on the company to which it relates.

“(2) The notice may be included in a notice of assessment.

Determination not part of assessment

“160aqn. An offset determination does not form part of an assessment.

Evidence of determination

“160aqp. The production of:

(a) a notice of an offset determination; or

(b) a document signed by the Commissioner, a Second Commissioner or a Deputy Commissioner purporting to be a copy of an offset determination;

is conclusive evidence of:

(c) the due making of the determination; and

(d) except in proceedings on appeal against the determination, that the determination is correct.

Reviews and appeals

“160aqq. (1) Division 2 of Part V applies, with appropriate changes, in relation to offset determinations.

“(2) The fact that an appeal or reference in respect of an offset determination is pending does not prevent recovery of any amount that may be affected by the determination.

Recovery of excess offsets

“160aqr. Where, because of an amendment of an offset determination, the amount, or the sum of the amounts, applied by the Commissioner as an offset to which a company is entitled exceeds the amount of the offset to which the company is entitled, the Commissioner may recover the amount of the excess as if it were company tax due and payable by the company.

Refunds of amounts overpaid

“160aqs. Section 172 applies for the purposes of this Subdivision as if a reference in that section to an assessment included a reference to an offset determination.

“Division 6—Tax Effects for Shareholders

“Subdivision A—Assessable Income of Certain Shareholders

Extra amount to be included in assessable income where franked dividend paid

“160aqt. (1) Where:

(a) a franked dividend is paid in a year of income to a shareholder in a company;

(b) the shareholder is:

(i) a natural person who is resident at the time of payment of the dividend;

(ii) a trustee; or

(iii) a partnership; and

(c) the dividend is not exempt income of the shareholder;

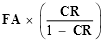

the assessable income of the shareholder of the year of income shall include the amount calculated in accordance with the formula:

where:

CR is the applicable general company tax rate; and

FA is the franked amount of the dividend.

“(2) An amount included in the assessable income of a shareholder under this section in relation to a dividend is in addition to any other

amount included in that assessable income in relation to the dividend under any other provision of this Act.

“(3) For the purposes of this Act, an amount shall not be taken to be directly or indirectly attributable to, or to be in respect of, a franked dividend only because it is directly or indirectly attributable to, or is in respect of, an amount included in assessable income under this section.

“Subdivision B—Franking Rebate for Certain Shareholders

Franking rebate

“160aqu. Where:

(a) an amount is included under section 160aqt in the assessable income of a shareholder of a year of income; and

(b) the shareholder is not:

(i) a partnership; or

(ii) a trustee other than:

(A) the trustee of a superannuation fund who is liable to be assessed under section 121cc, 121da or 121dab in respect of the investment income or taxable income of the fund; or

(B) the trustee of an ineligible approved deposit fund who is liable to be assessed under section 121daa in respect of income of the fund;

the shareholder is entitled to a rebate of tax in the shareholder’s assessment in respect of income of the year of income equal to the amount so included in the shareholder’s assessable income.

“Division 7—Dividends Paid to Trusts and Partnerships

“Subdivision A—Preliminary

Division to be applied separately to each dividend

“160aqv. This Division applies separately in relation to each franked dividend paid to a shareholder being a trustee or partnership.

Allocation of section 160aqt amount

“160aqw. (1) For the purposes of this Act, a section 160aqt amount shall be included in any relevant trust amounts and partnership amounts in the same proportions as persons are liable to be assessed, or would, but for section 128d, be liable to be assessed, directly or indirectly, in respect of the franked dividend to which the section 160aqt amount relates.

“(2) A reference in this section to a section 160aqt amount is a reference to:

(a) an amount included under section 160aqt in the assessable income of a trustee or partnership; or

(b) an amount attributable to an amount so included.

“Subdivision B—Rebates for Beneficiaries, Trustees and Partners

Franking rebate for certain beneficiaries

“160aqx. Where:

(a) a trust amount is included in the assessable income of a taxpayer of a year of income;

(b) the taxpayer is a natural person other than a trustee; and

(c) there is a flow-on franking amount in relation to the trust amount;

the taxpayer is entitled to a rebate of tax in the taxpayer’s assessment in respect of income of the year of income of an amount equal to the potential rebate amount in relation to the trust amount.

Franking rebate in trustee’s assessment

“160aqy. Where:

(a) a trustee is liable to be assessed under section 98 (other than subsection 98 (3)), or under section 99 or 99a, on a trust amount; and

(b) there is a flow-on franking amount in relation to the trust amount; the trustee is entitled to a rebate in that assessment of an amount equal to the potential rebate amount in relation to the trust amount.

Franking rebate for certain partners

“160aqz. Where:

(a) a partnership amount is included in, or allowable as a deduction from, the assessable income of a taxpayer of a year of income;

(b) the taxpayer is a natural person other than a trustee; and

(c) there is a flow-on franking amount in relation to the partnership amount;

the taxpayer is entitled to a rebate of tax in the taxpayer’s assessment in respect of income of the year of income of an amount equal to the potential rebate amount in relation to the partnership amount.

“Subdivision C—Adjustments in Relation to Section 160aqt Amounts for Companies and Non-residents

Adjustment where franking credit arises

“160ar. (1) Where:

(a) a trust amount is included in the assessable income of a company of a year of income; and

(b) a franking credit arises under section 160apq in relation to the trust amount;

an amount equal to so much of the potential rebate amount in relation to the trust amount as does not exceed the trust amount is allowable as a deduction from the assessable income of the company of the year of income.

“(2) Where:

(a) a partnership amount is included in, or allowable as a deduction from, the assessable income of a company of a year of income; and

(b) a franking credit arises under section 160apq in relation to the partnership amount;

the potential rebate amount in relation to the partnership amount is allowable as a deduction from the assessable income of the company of the year of income.

Adjustment for non-resident beneficiary

“160ara. Where:

(a) a trust amount is included in the assessable income of a taxpayer of a year of income;

(b) the taxpayer is:

(i) a natural person; or

(ii) a company; other than a trustee; and

(c) the trust amount would, but for section 128d, include withholding income;

there shall be allowed as a deduction from the assessable income of the taxpayer of the year of income an amount equal to the lesser of:

(d) the trust amount; and

(e) the amount that would be the potential rebate amount in relation to the trust amount if section 128d did not apply.

Adjustment where trustee assessed for non-resident beneficiary “160arb. Where:

(a) a trustee is liable to be assessed under section 98 on a trust amount; and

(b) the trust amount would, but for section 128d, include withholding income;

the trust amount shall be reduced by so much of the amount that would be the potential rebate amount in relation to the trust amount if section 128d did not apply as does not exceed the trust amount.

Adjustment where trustee assessed for company

“160arc. Where:

(a) a trustee is liable to be assessed under subsection 98 (3) on a trust amount; and

(b) there is a flow-on franking amount in relation to the trust amount;

the trust amount shall be reduced by so much of the potential rebate amount in relation to the trust amount as does not exceed the trust amount.

Adjustment for non-resident partner

“160ard. Where:

(a) a partnership amount is included in, or allowable as a deduction from, the assessable income of a taxpayer of a year of income;

(b) the taxpayer is:

(i) a natural person; or

(ii) a company;

other than a trustee; and

(c) the partnership amount would, but for section 128d, include withholding income;

there shall be allowed as a deduction from the assessable income of the taxpayer of the year of income an amount equal to the amount that would be the potential rebate amount in relation to the partnership amount if section 128d did not apply.

“Division 8—Returns and Assessments

“Subdivision A—Returns

Annual returns

“160are. (1) The Commissioner may, by notice published in the Gazette, require each company to which the notice applies to:

(a) furnish a return in relation to the franking year specified in the notice; and

(b) furnish to the Commissioner, with the return, a copy of each declaration made for the purposes of section 160aqf in respect of frankable dividends paid to shareholders in the company during that franking year.

“(2) A return under subsection (1) shall be furnished within the time required by the notice or such further time as the Commissioner allows.

Further returns etc.

“160arf. (1) Where the Commissioner, by notice in writing served on a company, requires the company to furnish a return in relation to a franking year, the company shall furnish the return within the time specified in the notice, whether or not the company has furnished, or is or was required to furnish, a return under section 160are or this section in respect of that franking year.

“(2) Where the Commissioner, by notice in writing served on a company, requires the company to furnish to the Commissioner a copy of each declaration made for the purposes of section 160aqf in relation to frankable dividends paid to shareholders in the company during a period specified in the notice, the company shall furnish the copies within the time specified in the notice, whether or not the company has furnished, or is or was required

to furnish, those copies under any other provision of this Act in respect of that period.

Requirements for returns

“160arg. A return under this Part shall:

(a) be in the form provided or authorised by the Commissioner for the purposes of that section;

(b) be furnished in accordance with the regulations;

(c) be signed on behalf of the company furnishing the return; and

(d) contain such information as is required for the due completion of the form of return.

“Subdivision B—Assessments

First return deemed to be an assessment

“160arh. Where:

(a) at a particular time (in this section called the ‘return time’), a return (in this section called the ‘first return’) under this Part in relation to a company in relation to a franking year is furnished; and

(b) before the return time, no return has been furnished, and no franking account assessment has been made, in relation to the company in relation to the franking year;

the following provisions have effect:

(c) the Commissioner shall be deemed at the return time to have made an assessment (in this section called the ‘deemed assessment’) of:

(i) the franking account balance of the company for the franking year; and

(ii) any franking deficit tax payable by the company for the franking year;

being those respective amounts as specified in the first return;

(d) the first return shall be deemed to be a notice of the deemed assessment and to be under the hand of the Commissioner;

(e) the notice referred to in paragraph (d) shall be deemed to have been served on the company at the return time.

Part-year assessment

“160arj. (1) The Commissioner may at any time make an assessment of the franking account balance of a company at a particular time during a franking year and, if the company has a franking deficit at that time, of the franking deficit tax payable by the company.

“(2) In making an assessment under subsection (1), the Commissioner shall apply this Part as if the beginning and end of the period to which the assessment relates were the beginning and end respectively of a franking year.

Default assessment

“160ark. Where a company has not furnished a return in respect of a franking year, the Commissioner may make an assessment of:

(a) the franking account balance of the company at the end of the franking year; and

(b) any franking deficit tax payable by the company for the franking year.

Assessment of franking additional tax

“160arl. The Commissioner shall make an assessment of franking additional tax payable by a company.

Notice of franking assessment

“160arm. (1) As soon as practicable after a franking assessment is made in respect of a company, the Commissioner shall serve notice of the assessment in writing on the company.

“(2) Notice of a franking assessment made in respect of a company may be included in notice of any other assessment made in respect of the company under this Act.

Amendment of assessments

“160arn. (1) The Commissioner may, at any time within a period of 3 years after the original assessment date in relation to a franking account assessment, amend the assessment by making such alterations or additions as the Commissioner thinks necessary.

“(2) Subject to this section, the Commissioner may, after the end of 3 years after the original assessment date in relation to a franking account assessment, amend the assessment by making such alterations or additions as the Commissioner thinks necessary.

“(3) Where:

(a) a company does not make a full and true disclosure of all the material facts necessary for a franking account assessment;

(b) the Commissioner makes such an assessment; and

(c) there is an under-assessment;

the Commissioner may:

(d) where the Commissioner is of the opinion that the under-assessment is due to fraud or evasion—at any time; or

(e) in any other case—within 6 years after the original assessment date in relation to the assessment;

amend the assessment by making such alterations or additions as the Commissioner thinks necessary.

“(4) No amendment reducing a franking account assessment shall be made after the end of 3 years after the original assessment date.

“(5) Where a franking account assessment has been amended under this section in any particular, the Commissioner may, within 3 years of the date that the amended assessment is made, make such further amendment of the assessment in or in respect of that particular as, in the Commissioner’s opinion, is necessary to effect such reduction in the assessment as is just.

“(6) Where a company:

(a) applies, within 3 years after the original assessment date in relation to a franking account assessment, for an amendment of the assessment; and

(b) supplies to the Commissioner within that period all information needed by the Commissioner for the purposes of determining the application made by the company;

the Commissioner may amend the assessment, notwithstanding that that period has ended.

“(7) Nothing in this section prevents the amendment of a franking account assessment:

(a) in order to give effect to a decision on a review or appeal; or

(b) by way of reducing the assessment in any particular pursuant to an objection made under this Act or pending an appeal or review.

“(8) The Commissioner may at any time amend a franking additional tax assessment.

“(9) Except as otherwise provided, an amended franking assessment is a franking assessment for all purposes of this Act.

“(10) In this section:

(a) a reference to reducing a franking account assessment is a reference to doing either or both of the following:

(i) increasing a franking surplus (including an increase from a nil franking account balance);

(ii) reducing a franking deficit (including a reduction resulting in a nil franking account balance) and the franking deficit tax payable in respect of the franking deficit;

(b) a reference to increasing a franking account assessment is a reference to doing either or both of the following:

(i) reducing a franking surplus (including a reduction resulting in a nil franking account balance);

(ii) increasing a franking deficit (including an increase from a nil franking account balance) and the franking deficit tax payable in respect of the franking deficit; and

(c) a reference to an under-assessment is a reference to a franking account assessment that would have to be increased in order to be correct.

Validity of assessment

“160arq. The validity of a franking assessment is not affected because any of the provisions of this Act have not been complied with.

Refunds of amounts overpaid

“160arr. Section 172 applies for the purposes of this Part as if references in that section to tax included references to franking deficit tax and franking additional tax.

“Subdivision C—Miscellaneous

Evidence

“160ars. Section 177 applies to a franking assessment or a return under this Part as it applies to an ordinary assessment or ordinary return.

“Division 9—Objections, Reviews and Appeals

Objections, reviews and appeals

“160art. (1) Subject to this section, Division 2 of Part V (other than section 193) applies in relation to a franking assessment as it applies in relation to an ordinary assessment.

“(2) For the purposes of this section:

(a) the reference in paragraph 190 (b) to an assessment being excessive is a reference to an assessment being incorrect; and

(b) a reference in section 201 to income tax includes a reference to franking deficit tax and franking additional tax.

“Division 10—Collection and Recovery

Due date for payment of franking deficit tax

“160aru. (1) Subject to subsection (2), franking deficit tax assessed for a franking year becomes due and payable, or shall be deemed to have become due and payable, as the case requires, on the last day of the month following the end of the franking year.

“(2) Franking deficit tax payable because of an assessment under section 160arj is due and payable on the date specified in the notice of assessment as the date on which it is due and payable.

Due date for payment of franking additional tax

“160arv. Franking additional tax is due and payable on the date specified in the notice of assessment of the franking additional tax as the date on which it is due and payable.

Miscellaneous provisions relating to collection and recovery

“160arw. (1) In sections 205, 206, 207, 208, 209, 213, 214, 215 and 218, ‘income tax’ or ‘tax’ includes franking deficit tax and franking additional tax.

“(2) Where:

(a) the Commissioner amends a franking account assessment (in this subsection called the ‘former assessment’) made under section 160arh or 160ark in relation to a company for a franking year;

(b) the franking deficit tax payable under the amended assessment exceeds the franking deficit tax payable under the former assessment; and

(c) the whole or a part (which whole or part is in this subsection called the ‘non-penalised amount’) of the excess referred to in paragraph (b) relates to a matter in respect of which the company is not liable (otherwise than because of the operation of subsection 8ze (1) of the Taxation Administration Act 1953 or section 160asb of this Act) to pay franking additional tax under section 160as;

the additional tax under section 207 in so far as it:

(d) would relate to so much of the unpaid amount referred to in subsection 207 (1) as is attributable to the non-penalised amount; and

(e) would be calculated in respect of the period:

(i) commencing on:

(A) the day on which franking deficit tax would, but for section 206 have become due and payable by the company in respect of the franking year; or

(b) the original assessment date;

whichever is the later; and

(ii) ending on the thirtieth day after the day on which the amended assessment was made;

shall be calculated as if the reference in section 207 to 20% per annum were a reference to such rate of interest as is, or such rates of interest as are, applicable under regulations made for the purposes of paragraph 10 (1) (b) of the Taxation (Interest on Overpayments) Act 1983.

“(3) Until regulations are made for the purposes of paragraph 10 (1) (b) of the Taxation (Interest on Overpayments) Act 1983, the rate of interest applicable for the purposes of subsection (2) of this section is 14.026% per annum.

“Division 11—Additional Tax by way of Penalty

Penalty for over-franking

“160arx. Where:

(a) the franking deficit of a company at the end of a franking year is more than 10% of the total of the franking credits arising during the franking year; and

(b) the franked amount of a dividend paid during the franking year to a shareholder in the company exceeded the required franking amount for that dividend;

the company is liable to pay, by way of penalty, additional tax equal to 30% of the franking deficit tax payable by the company for the franking year.

Penalty for setting out incorrect amounts in dividend statements

“160ary. (1) Where:

(a) a company gives to a shareholder in the company a dividend statement that is reasonably likely to cause the shareholder to believe that:

(i) if section 160aqt were to apply to the shareholder, an amount would be included in the assessable income of the shareholder under this Part because of the payment of the dividend; or

(ii) if section 160aqu were to apply to the shareholder, the shareholder would be entitled to a rebate of tax under this Part because of the payment of the dividend; and

(b) if section 160aqt or section 160aqu, as the case may be, were to apply to the shareholder:

(i) the amount that would be included in the assessable income of the shareholder under section 160aqt because of the payment of the dividend would be greater than the amount referred to in subparagraph (a) (i) of this subsection; or

(ii) the rebate to which the shareholder would be entitled under section 160aqu because of the payment of the dividend would be less than the amount of the rebate referred to in subparagraph (a) (ii) of this subsection;

the company is liable to pay, by way of penalty, additional tax equal to:

(c) if subparagraph (a) (i) applies—half of the amount of the excess referred to in subparagraph (b) (i); or

(d) if subparagraph (a) (ii) applies—the amount of the shortfall referred to in subparagraph (b) (ii).

“(2) For the purposes of this section:

(a) a nil amount shall be taken to be an amount; and

(b) a reference to a dividend statement includes a reference to a document purporting to be a dividend statement.

Penalty for failure to furnish return

“160arz. Where a company refuses or fails to furnish, when and as required under this Act to do so, a return, or any information, relating to a franking year, being a return relating to or information relating to, or to the affairs of, the company, the company is liable to pay, by way of penalty, additional tax equal to double the amount of the franking deficit tax payable by the company for the franking year.

Penalty for false or misleading statements

“160as. (1) Where:

(a) a company:

(i) makes a statement to a taxation officer that is false or misleading in a material particular; or

(ii) omits from a statement made to a taxation officer any matter or thing without which the statement is misleading in a material particular; and

(b) the franking deficit tax properly payable by the company exceeds the franking deficit tax that would have been payable by the company if it were assessed on the basis that the statements were not false or misleading, as the case may be;

the company is liable to pay, by way of penalty, additional tax equal to double the amount of the excess.

“(2) A reference in this section to a statement made to a taxation officer is a reference to a statement made to a taxation officer orally, in writing, in a data processing device or in any other form and, without limiting the generality of the foregoing, includes a statement:

(a) made in an application, certificate, declaration, notification, objection, return or other document made, given or furnished, or purporting to be made, given or furnished, under or pursuant to this Act or the regulations;

(b) made in answer to a question asked of a person under or pursuant to this Act or the regulations;

(c) made in any information furnished, or purporting to be furnished, under or pursuant to this Act or the regulations; or

(d) made in a document furnished to a taxation officer otherwise than under or pursuant to this Act or the regulations;

but does not include a statement made in a document produced pursuant to paragraph 264 (1) (b).

Minimum amount of additional tax

“160asa. Where, but for this section, an amount of franking additional tax of less than $20 would be payable by a person in respect of an act or omission, that amount shall be increased to $20.

Remission of additional tax

“160asb. The Commissioner may, in the Commissioner’s discretion, remit the whole or any part of the franking additional tax payable by a company but, for the purposes of the application of subsection 33 (1) of the Acts Interpretation Act 1901 to the power of remission conferred by this section, nothing in this Act prevents the exercise of the power at a time before the franking additional tax assessment is made.

“Division 12—Records, Information and Tax Agents

Company to keep records

“160asc. Section 262a applies for the purposes of this Part as if:

(a) a reference to a person carrying on a business were a reference to a company;

(b) a reference to income and expenditure were a reference to matters relevant to ascertaining the franking account balance;

(c) a reference to assessable income and allowable deductions were a reference to the franking account balance; and

(d) paragraph (2) (a) of that section were omitted.

Power of Commissioner to obtain information

“160asd. Section 264 applies for the purposes of this Part as if the reference in paragraph (1) (b) of that section to a person’s income or assessment were a reference to a matter relevant to the administration or operation of this Part.

Tax agents

“160ase. Part VIIa applies in relation to a return furnished, or objection lodged, for the purposes of this Part as it applies to an income tax return or objection.”.

Amount of instalment of tax

15. Section 221ae of the Principal Act is amended by inserting in subsection (3) “, section 160aqk” after “Part III”.

Estimated income tax

16. Section 221ag of the Principal Act is amended by omitting subsection (8) and substituting the following subsection:

“(8) A reference in this section to the amount of income tax that is or will be payable by a company in respect of its taxable income of a year of income shall be read as a reference to the amount of the income tax that is or will be so payable after deducting:

(a) any credits to which the company is or will be entitled under:

(i) section 45, subsection 98a (2), Division 18 of Part III or Division 3a of this Part; or

(ii) the Income Tax (International Agreements) Act 1953; and

(b) any offset to which the company is or will be entitled under section 160aqk.”.

Interpretation

17. Section 251r of the Principal Act is amended by omitting from subsection (7) “and Division 17 of Part III” and substituting “, Division 17 of Part III and sections 160aqu, 160aqx, 160aqy and 160aqz”.

Application of amendments

18. (1) In this section:

“commencing time” means 1 o’clock in the afternoon, by legal time in the Australian Capital Territory, on 10 December 1986.

(2) The amendment made by section 8 does not apply to a distribution by a liquidator in the course of winding up a company where the winding up commenced before the commencing time.

(3) Where:

(a) money or property of a company is distributed to a shareholder in the company after the commencing time; and

(b) the distribution is deemed by subsection 47 (2a) of the Principal Act to be, for the purposes of section 47 of the Principal Act, a distribution to a shareholder by a liquidator in the course of winding up the company;

subsection (2) of this section applies in relation to the distribution as if the winding up had commenced after the commencing time.

(4) The amendment made by paragraph 11 (a) applies to dividends paid to a shareholder on or after 1 July 1987.

(5) The repeal made by section 13 applies in relation to income of the year of income commencing on 1 July 1986 and of all subsequent years of income.

Amendment of assessments

19. Nothing in section 170 of the Principal Act prevents the amendment of an assessment made before the commencement of this section for the purpose of giving effect to this Part.

PART IV—REPEAL OF THE INCOME TAX (NON-RESIDENT COMPANIES) ACT 1978

Repeal

20. The Income Tax (Non-Resident Companies) Act 1978 is repealed.

Application

21. The Income Tax Assessment Act 1936 applies in relation to the tax that was imposed by the Act repealed by this Part as if that repealed Act were still in force.

PART V—AMENDMENT OF THE TAXATION ADMINISTRATION ACT 1953

Principal Act

22. The Taxation Administration Act 19533 is in this Part referred to as the Principal Act.

Penalty taxes to be alternative to prosecution for certain offences

23. Section 8ze of the Principal Act is amended by inserting after paragraph (3) (d) the following paragraph:

“(da) section 160ary, 160arz or 160as of the Income Tax Assessment Act 1936;”.

Modification of limitation laws applying to the recovery of tax debts

24. Section 14zka of the Principal Act is amended by inserting after subparagraph (2) (b) (iv) the following subparagraph:

“(iva) Division 11 of Part IIIaa of the Income Tax Assessment Act 1936;”.

PART VI—AMENDMENT OF THE TAXATION (INTEREST ON OVERPAYMENTS) ACT 1983

Principal Act

25. The Taxation (Interest on Overpayments) Act 19834 is in this Part referred to as the Principal Act.

Interpretation

26. Section 3 of the Principal Act is amended by omitting “or subsection 160al (1)” from subparagraph (a) (i) of the definition of “objection” in subsection (1) and substituting “, subsection 160al (1) or section 160aqq or 160art”.

Entitlement to interest

27. Section 9 of the Principal Act is amended by adding at the end the following subsections:

“(6) Where:

(a) at a particular time, a company pays an amount of franking deficit tax;

(b) at a later time (in this subsection called the ‘offset time’), the company becomes entitled to an offset that is attributable, in whole or in part, to so much of the company’s franking deficit tax liability as was discharged by the payment of that amount; and

(c) as a result of a decision to which this Act applies (being a decision made after the offset time), the whole or part of the amount paid by the company is overpaid;

the amount paid by the company shall be taken to have been applied, at the offset time, against a liability of the company to the Commonwealth as a result of that decision.

“(7) An expression used in subsection (6) and in Part IIIaa of the Income Tax Assessment Act 1936 has the same meaning in that subsection as it has in that Part of that Act.”.

NOTES

1. No. 156, 1980, as amended. For previous amendments, see No. 123, 1984; No. 47, 1985; Nos. 41, 48, 76 and 154, 1986; and Nos. 58 and 61, 1987.

2. No. 27, 1936, as amended. For previous amendments, see No. 88, 1936; No. 5, 1937; No. 46, 1938; No. 30, 1939; Nos. 17 and 65, 1940; Nos. 58 and 69, 1941; Nos. 22 and 50, 1942; No. 10, 1943; Nos. 3 and 28, 1944; Nos. 4 and 37, 1945; No. 6, 1946; Nos. 11 and 63, 1947; No. 44, 1948; No. 66, 1949; No. 48, 1950; No. 44, 1951; Nos. 4, 28 and 90, 1952; Nos. 1, 28, 45 and 81, 1953; No. 43, 1954; Nos. 18 and 62, 1955; Nos. 25, 30 and 101, 1956; Nos. 39 and 65, 1957; No. 55, 1958; Nos. 12, 70 and 85, 1959; Nos. 17, 18, 58 and 108, 1960; Nos. 17, 27 and 94, 1961; Nos. 39 and 98, 1962; Nos. 34 and 69, 1963; Nos. 46, 68, 110 and 115, 1964; Nos. 33, 103 and 143, 1965; Nos. 50 and 83, 1966; Nos. 19, 38, 76 and 85, 1967; Nos. 4, 70, 87 and 148, 1968; Nos. 18, 93 and 101, 1969; No. 87, 1970; Nos. 6, 54 and 93, 1971; Nos. 5, 46, 47, 65 and 85, 1972; Nos. 51, 52, 53, 164 and 165, 1973; No. 216, 1973 (as amended by No. 20, 1974); Nos. 26 and 126, 1974; Nos. 80 and 117, 1975; Nos. 50, 53, 56, 98, 143, 165 and 205, 1976; Nos. 57, 126 and 127, 1977; Nos. 36, 57, 87, 90, 123, 171 and 172, 1978; Nos. 12, 19, 27, 43, 62, 146, 147 and 149, 1979; Nos. 19, 24, 57, 58, 124, 133, 134 and 159, 1980; Nos. 61, 92, 108, 109, 110, 111, 154 and 175, 1981; Nos. 29, 38, 39, 76, 80, 106 and 123, 1982; Nos. 14, 25, 39, 49, 51, 54 and 103, 1983; Nos. 14, 42, 47, 63, 76, 115, 124, 165 and 174, 1984; No. 123, 1984 (as amended by No. 65, 1985); Nos. 47, 49, 104, 123 and 168, 1985; No. 173, 1985 (as amended by No. 49, 1986); Nos. 41, 46, 48, 49, 51, 52, 90, 109, 112 and 154, 1986; and Nos. 58, 61 and 62, 1987.

3. No. 1, 1953, as amended. For previous amendments, see Nos. 28, 39, 40 and 52, 1953; No. 18, 1955; No. 39, 1957; No. 95, 1959; No. 17, 1960; No. 75, 1964; No. 155, 1965; No. 93, 1966; No. 120, 1968; No. 216, 1973; No. 133, 1974; No. 37, 1976; Nos. 19 and 59, 1979; Nos. 39 and 117, 1983; No. 123, 1984; No. 65, 1985 (as amended by No. 193, 1985); Nos. 4, 47, 104, 123 and 168, 1985; and Nos. 41, 46, 48, 49, 112, 144 and 154, 1986.

4. No. 12, 1983, as amended. For previous amendments, see No. 123, 1984; Nos. 4, 47, 49 and 123, 1985; Nos. 41, 46, 48 and 154, 1986; and Nos. 58 and 61, 1987.

[Minister’s second reading speech made in—

House of Representatives on 2 April 1987

Senate on 27 May 1987]