(4) Part VII shall be deemed to have come into operation on 6 November 1987.

(5) Part VIII shall be deemed to have come into operation on the commencement of section 51 of the Taxation Laws Amendment Act (No. 4) 1987.

(6) Part IX shall be deemed to have come into operation on the commencement of the Taxation Laws Amendment (Fringe Benefits and Substantiation) Act 1987.

PART II—AMENDMENT OF THE AUSTRALIAN CAPITAL TERRITORY TAXATION (ADMINISTRATION) ACT 1969

Principal Act

3. In this Part, “Principal Act” means the Australian Capital Territory Taxation (Administration) Act 19691.

Interpretation

4. Section 4 of the Principal Act is amended:

(a) by omitting “, or a debenture of,” from paragraph (a) of the definition of “marketable security” in subsection (1);

(b) by omitting “share, debenture” from the definition of “marketable security” in subsection (1) and substituting “share”.

Application of amendments

5. (1) The amendments made by this Part, insofar as they relate to the tax imposed by the Australian Capital Territory Tax (Purchases of Marketable Securities) Act 1969, apply in relation to a purchase of a marketable security where the purchase is made after 15 July 1987.

(2) The amendments made by this Part, insofar as they relate to the tax imposed by the Australian Capital Territory Tax (Sales of Marketable Securities) Act 1969, apply in relation to a sale of a marketable security where the sale is made after 15 July 1987.

(3) The amendments made by this Part, insofar as they relate to the tax imposed by the Australian Capital Territory Tax (Transfers of Marketable Securities) Act 1986, apply in relation to a transfer of a marketable security effected by an instrument of transfer that appears to have been executed by the transferor, or by any of the transferors, after the commencement of that Act (including an instrument that appears to have been executed by the transferee, or by any of the transferees, before the commencement of that Act).

(4) The amendments made by this Part, insofar as they relate to stamp duty imposed by the Australian Capital Territory Stamp Duty Act 1969, apply in relation to an instrument executed after 15 July 1987.

(5) The amendments made by this Part, insofar as they relate to section 58g of the Principal Act as amended by this Act, apply in relation to the registration of a transfer where the registration is made after 15 July 1987 and, for the purposes of the application of paragraphs 58g (1) (b) and (c) of that Act to a registration made on or before that date, the amendments made by this Part shall be disregarded.

PART III—AMENDMENT OF THE INCOME TAX ACT 1986 Principal Act

6. In this Part, “Principal Act” means the Income Tax Act 19862.

Imposition of income tax

7. Section 5 of the Principal Act is amended by inserting in subsection (2) “128nb,” after “128na,”.

PART IV—AMENDMENT OF THE INCOME TAX ASSESSMENT ACT 1936

Principal Act

8. In this Part, “Principal Act” means the Income Tax Assessment Act 19363.

Certain sea installations and offshore areas to be treated as part of Australia

9. Section 6aa of the Principal Act is amended:

(a) by omitting subsections (1) and (2) and substituting the following subsections:

“(1) For all purposes of this Act related directly or indirectly to:

(a) the exploration for minerals in, or the exploitation of the natural resources (being minerals) of:

(i) an eligible external Territory;

(ii) a Petroleum Act adjacent area;

(iii) an Installations Act adjacent area by means of a sea installation installed in that area; or

(iv) the Papua New Guinea offshore area;

whether the exploration or exploitation is by the taxpayer concerned or by another person;

(b) the carrying on of an environment related activity in:

(i) an eligible external Territory;

(ii) a Petroleum Act adjacent area;

(iii) an Installations Act adjacent area by means of a sea installation installed in that area; or

(iv) the Papua New Guinea offshore area;

whether the activity is carried on by the taxpayer concerned or by another person; or

(c) acts, matters, circumstances and things touching, concerning, arising out of or connected with any such exploration, exploitation or environment related activity;

including purposes in relation to the application of this Act in respect of income or profits derived from any such exploration, exploitation, environment related activity, act, matter, circumstance or thing, or in respect of dividends paid wholly or partly out of any such profits, the provisions of this Act have effect, subject to this section, as if:

(d) the whole of each eligible external Territory and each Petroleum Act adjacent area were, and at all times had been, a part of Australia;

(e) each sea installation, when installed in the Installations Act adjacent area, were a part of Australia; and

(f) the Papua New Guinea offshore area were, and at all times had been, a part of Papua New Guinea.

“(2) Where a company carries on business that:

(a) consists of exploration or exploitation, or an environment related activity, of a kind referred to in subsection (1); or

(b) arises out of or is connected with any such exploration, exploitation or environment related activity (whether by that company or by another person);

the company shall, for the purposes of the definition of ‘resident’ or ‘resident of Australia’ in subsection 6 (1), be deemed to be carrying on business in Australia.”;

(b) by inserting after subsection (3a) the following subsections:

“(3b) Subject to subsection (3c), this section does not operate so as to include in the assessable income of a person any income derived before 15 October 1987 that would not have been so included if section 9 of the Taxation Laws Amendment Act 1988 had not come into operation.

“(3c) This section shall be taken to have applied as if the reference in paragraph (4) (a) of this section, as in force during the period commencing when the Petroleum (Submerged Lands) Amendment Act 1980 came into operation and ending immediately before this subsection came into operation, to the Petroleum (Submerged Lands) Act 1967-1974 had instead been a reference to the Petroleum (Submerged Lands) Act 1967 as in force immediately before the Petroleum (Submerged Lands) Amendment Act 1980 came into operation.”;

(c) by omitting paragraphs (4) (a), (b) and (c) and substituting the following paragraphs:

“(a) ‘eligible external Territory’ means the area, whether land or water, within the territorial limits of:

(i) the Territory of Ashmore and Carrier Islands;

(ii) the Coral Sea Islands Territory; or

(iii) the Territory of Heard and McDonald Islands;

and includes the space above and below that area;

(b) ‘environment related activity’ has the same meaning as in the Sea Installations Act 1987; and

(c) ‘Installations Act adjacent area’ means an area that is an adjacent area for the purposes of the Sea Installations Act 1987;”;

(d) by adding at the end of subsection (4) the following word and paragraph:

“; and (e) ‘Petroleum Act adjacent area’ means an area that is an adjacent area for the purposes of the Petroleum (Submerged Lands) Act 1967.”;

(e) by adding at the end the following subsection:

“(5) Where, if the definition of ‘sea installation’ in subsection 4 (1) of the Sea Installations Act 1987:

(a) extended to include:

(i) resources industry fixed structures and resources industry mobile units, within the meaning of subsections 4 (2) and (3) of that Act;

(ii) partly constructed structures (including pipelines) or vessels that, when completed, are intended to be, or could be, structures or units referred to in subparagraph (i); and

(iii) the remains of structures (including pipelines) or vessels that have been structures, units or vessels referred to in subparagraph (i) or (ii); and

(b) did not include fishing boats, fishing equipment and pearling vessels;

a structure or vessel, or structures or vessels, would, by section 6 of that Act, be deemed for the purposes of that Act to be a sea installation installed in a particular area, the structure or vessel, or the structures or vessels, shall be taken for the purposes of this section to be a sea installation installed in that area.”.

Interpretation

10. Section 24b of the Principal Act is amended by adding at the end the following subsection:

“(5) For the purposes of this Division (other than section 24c), the adjacent area, within the meaning of the Sea Installations Act 1987, in

relation to a prescribed Territory shall, after the commencement of this subsection, be taken to be part of the prescribed Territory.”.

Interpretation

11. Section 27a of the Principal Act is amended:

(a) by inserting “or (aa)” after “(a)” in paragraph (a) of the definition of “eligible service period” in subsection (1);

(b) by omitting “or (c)” from paragraph (b) of the definition of “eligible service period” in subsection (1) and substituting “, (ba), (c), (ca), (da), (db), (ga) or (gb)”;

(c) by omitting “eligible annuity” (wherever occurring) from paragraph (d) of the definition of “eligible service period” in subsection (1) and substituting “qualifying annuity”;

(d) by inserting after paragraph (a) of the definition of “eligible termination payment” in subsection (1) the following paragraph:

“(aa) any payment made to the taxpayer in consequence of the termination of any employment of another person, where:

(i) the payment is made after the death of the other person;

(ii) the taxpayer was not a dependant of the other person at the time of the death of the other person and is not a dependant of the other person at the time of payment;

(iii) the payment is made to the taxpayer otherwise than as trustee of the estate of the other person; and

(iv) the payment is not a payment:

(a) to which paragraph (ba) applies:

(b) of an annuity, or supplement, to which section 27h applies; or

(c) from a fund in relation to which section 121da applies, or has applied, in relation to the year of income commencing on 1 July 1984 or any subsequent year of income;”;

(e) by omitting from subparagraph (b) (ii) of the definition of “eligible termination payment” in subsection (1) “or (e)” and substituting “, (da), (e) or (ga)”;

(f) by inserting after paragraph (b) of the definition of “eligible termination payment” in subsection (1) the following paragraph:

“(ba) any payment made to the taxpayer from a superannuation fund by reason that another person was a member of the fund, where:

(i) the payment is made after the death of the other person;

(ii) the taxpayer was not a dependant of the other person at the time of the death of the other person

and is not a dependant of the other person at the time of payment;

(iii) the payment is made to the taxpayer otherwise than as trustee of the estate of the other person; and

(iv) the payment is not:

(a) income of the taxpayer;

(b) a payment to which paragraph (d), (db), (e), (f) or (gb) applies; or

(c) a benefit to which subsection 26af (1), 26afa (1) or 26afb (2) or (3) applies;

reduced by any amount that has been or will be included in the assessable income of any person under subsection 26af (2), 26afa (3) or 26afb (5) in respect of the transfer to the taxpayer of a right to receive the payment or any part of the payment;”;

(g) by inserting after paragraph (c) of the definition of “eligible termination payment” in subsection (1) the following paragraph:

“(ca) any payment made to the taxpayer by the trustee of an approved deposit fund by reason that another person was a depositor with the fund, where:

(i) the payment is made after the death of the other person;

(ii) the taxpayer was not a dependant of the other person at the time of the death of the other person and is not a dependant of the other person at the time of payment;

(iii) the payment is made to the taxpayer otherwise than as trustee of the estate of the other person; and

(iv) the payment is not income of the taxpayer;”;

(h) by inserting after paragraph (d) of the definition of “eligible termination payment” in subsection (1) the following paragraphs:

“(da) a payment (in this paragraph called the ‘capital payment’) made after the death of the taxpayer to the trustee of the estate of the taxpayer where:

(i) the capital payment is made by reason that the taxpayer was a member of a superannuation fund (whether or not the capital payment is made from the fund); and

(ii) at some time after the death of the taxpayer, a person had a right to elect to receive a superannuation pension (whether or not from the person making the capital payment) in lieu of the capital payment being made to the trustee;

reduced by the amount that would have been the unused undeducted purchase price in relation to the superannuation pension;

(db) a payment (in this paragraph called the ‘capital payment’) made to the taxpayer after the death of another person (in this paragraph called the ‘deceased person’) where:

(i) the capital payment is made by reason that the deceased person was a member of a superannuation fund (whether or not the capital payment is made from the fund);

(ii) the capital payment is made to the taxpayer otherwise than as trustee of the estate of the deceased person; and

(iii) at some time after the death of the deceased person, the taxpayer or another person had a right to elect to receive a superannuation pension (whether or not from the person making the capital payment) in lieu of the capital payment being made to the taxpayer;

reduced by the amount that would have been the unused undeducted purchase price in relation to the superannuation pension;”;

(j) by omitting “eligible” from paragraph (g) of the definition of “eligible termination payment” in subsection (1) and substituting “qualifying”;

(k) by inserting after paragraph (g) of the definition of “eligible termination payment” in subsection (1) the following paragraphs:

“(ga) a payment (in this paragraph called the ‘capital payment’) made after the death of the taxpayer to the trustee of the estate of the taxpayer where:

(i) the capital payment is made by reason that the taxpayer was a member of a superannuation fund (whether or not the capital payment is made from the fund); and

(ii) at some time after the death of the taxpayer a person had a right to elect to receive an annuity (whether or not from the person making the capital payment) in lieu of the capital payment being made to the trustee;

reduced by the amount that would have been the unused undeducted purchase price in relation to the annuity (having regard only to contributions made to the fund);

(gb) a payment (in this paragraph called the ‘capital payment’) made to the taxpayer after the death of another person (in this paragraph called the ‘deceased person’) where:

(i) the capital payment is made by reason that the deceased person was a member of a superannuation

fund (whether or not the capital payment is made from the fund);

(ii) the capital payment is made to the taxpayer otherwise than as trustee of the estate of the deceased person; and

(iii) at some time after the death of the deceased person, the taxpayer or another person had a right to elect to receive an annuity (whether or not from the person making the capital payment) in lieu of the capital payment being made to the taxpayer;

reduced by the amount that would have been the unused undeducted purchase price in relation to the annuity (having regard only to contributions made to the fund);”;

(m) by omitting “eligible” from paragraph (h) of the definition of “eligible termination payment” in subsection (1) and substituting “qualifying”;

(n) by omitting “eligible” from paragraph (j) of the definition of “eligible termination payment” in subsection (1) and substituting “qualifying”;

(p) by inserting “or, as the case requires, the fund member referred to in the applicable paragraph of the definition of ‘eligible termination payment’ ” after “the taxpayer” in subparagraph (a) (i) of the definition of “relevant service period” in subsection (1);

(q) by inserting “or the fund member, as the case may be,” after “the taxpayer” in subparagraph (a) (ii) of the definition of “relevant service period” in subsection (1);

(r) by inserting “or, as the case requires, the fund member referred to in the applicable paragraph of the definition of ‘eligible termination payment’ ” after “the taxpayer” (first occurring) in paragraph (b) of the definition of “relevant service period” in subsection (1);

(s) by inserting “or the fund member, as the case may be,” after “the taxpayer” in subparagraph (b) (i) of the definition of “relevant service period” in subsection (1);

(t) by inserting “or the fund member, as the case may be,” after “the taxpayer” in subparagraph (b) (ii) of the definition of “relevant service period” in subsection (1);

(u) by inserting “or, as the case requires, the depositor referred to in the applicable paragraph of the definition of ‘eligible termination payment’ ” after “the taxpayer” (first occurring) in paragraph (c) of the definition of “relevant service period” in subsection (1);

(w) by inserting “or the depositor, as the case may be,” after “the taxpayer” (second occurring) in paragraph (c) of the definition of “relevant service period” in subsection (1);

(y) by omitting from subsection (1) the definition of “dependant” and substituting the following definition:

“ ‘dependant’, in relation to a person:

(a) in subparagraph (3) (a) (ii), subsections (5), (5c) and (7) and paragraph (12) (a), includes:

(i) another person who is or was the spouse of the person; and

(ii) any child of the person; and

(b) in any other case, includes:

(i) another person who is or was a spouse of the person; and

(ii) any child of the person, being a child who has not attained the age of 18 years;”;

(z) by omitting from subsection (1) the definition of “eligible annuity” and substituting the following definition:

“ ‘eligible annuity’, in relation to a taxpayer, means:

(a) an annuity payable under a superannuation policy within the meaning of Division 8; or

(b) an annuity in respect of which the following conditions are satisfied:

(i) the annuity:

(a) is an immediate annuity purchased on or before 9 December 1987; or

(b) is an annuity whose purchase price consists wholly of a rolled-over amount or rolled-over amounts;

(ii) if the annuity contract permits a residual capital value to become payable after the 65th anniversary of the birth of the taxpayer—the contract does not permit the residual capital value to exceed the purchase price of the annuity;

(iii) if the annuity is payable for a term of years certain and the annuity contract permits a commutation payment or payments to become payable after the 65th anniversary of the birth of the taxpayer—the contract does not permit the total of such payments to exceed the reduced purchase price of the annuity;

(iv) if the annuity is payable until:

(a) the death of a particular person or of the last to die of 2 or more persons; or

(b) the end of a term of years certain;

whichever last occurs, and the annuity contract permits a commutation payment or payments to become payable after the 65th anniversary

of the birth of the taxpayer and before the end of that term of years certain—the contract does not permit the total of such payments to exceed the reduced purchase price of the annuity;

(v) if the annuity contract permits any annuity income to be derived in respect of a period commencing after the 65th anniversary of the birth of the taxpayer—the Commissioner is satisfied that there will not be any unreasonable deferral of the derivation of any of that income, having regard to the following matters:

(a) to the extent to which the amounts of that annuity income will depend on the amount of income that may be derived by the person paying the annuity—the respective times of derivation of those amounts of annuity income and of the income of the person paying the annuity;

(b) to the extent to which the amounts of that annuity income are not dependent on the amount of income that may be derived by the person paying the annuity—the relative sizes of the annual entitlements to that annuity income;

(c) such other matters as the Commissioner considers relevant;

(vi) if the annuity is a deferred annuity—the annuity contract requires the annuity to become an immediate annuity not later than the 65th anniversary of the birth of the taxpayer;”;

(za) by inserting in subsection (1) the following definitions:

“ ‘qualifying annuity’ means:

(a) an annuity purchased after 12 January 1987 that has at any time been:

(i) an eligible annuity in relation to any taxpayer; or

(ii) the subject of an eligible policy within the meaning of Division 8 or 8a;

(b) an annuity that:

(i) was purchased on or before 12 January 1987; and

(ii) is an eligible annuity within the meaning of this section as in force immediately before the commencement of section 11 of the Taxation Laws Amendment Act 1988; or

(c) an immediate annuity purchased on or before 9 December 1987;

‘reduced purchase price’, in relation to an annuity, means the purchase price of the annuity, reduced by the total of the amounts excluded from assessable income under paragraph 27h (1) (a) as deductible amounts in relation to the annuity;”;

(zb) by inserting in subsection (1) the following definition:

“ ‘spouse’, in relation to a person, includes another person who, although not legally married to the person, lives with the person on a bona fide domestic basis as the husband or wife of the person;”;

(zc) by inserting after subsection (4) the following subsection:

“(4a) Where:

(a) but for this subsection, an amount (in this subsection called the ‘gross amount’) would, in relation to a deceased taxpayer, be the amount of an eligible termination payment to which paragraph (h) of the definition of ‘eligible termination payment’ in subsection (1) applies because of it having been made to the trustee of the estate of the deceased taxpayer; and

(b) the annuity to which the payment relates was a roll-over annuity at the time of death of the deceased taxpayer;

the gross amount shall be reduced by such amount (if any) as the Commissioner considers appropriate having regard to the extent to which the dependants of the deceased taxpayer may reasonably be expected to benefit from the estate.”;

(zd) by inserting after subsection (5b) the following subsection:

“(5ba) Paragraph (j) of the definition of ‘eligible termination payment’ in subsection (1) does not apply to a payment made to a taxpayer of the residual capital value of an annuity if:

(a) the taxpayer was, at the time of death of the deceased person to whom the annuity was payable, a dependant of that person or is a dependant of that person at the time of payment; and

(b) the annuity was a roll-over annuity at the time of death of the person to whom the annuity was payable.”;

(ze) by inserting after subsection (7) the following subsection:

“(7a) For the purposes of this Subdivision, an annuity shall be taken to be presently payable at all times after, but not before, the commencement of the first period in respect of which the annuity is payable.”;

(zf) by omitting paragraph (12) (c) and substituting the following paragraph:

“(c) paid to a life assurance company or registered organisation in respect of the purchase of an annuity that:

(i) is an eligible annuity in relation to the taxpayer; and

(ii) is for the benefit of the taxpayer or for the benefit of dependants of the taxpayer in the event of the death of the taxpayer.”;

(zg) by inserting after subsection (12a) the following subsections:

“(12b) Notwithstanding subsection (12), an eligible termination payment to which paragraph (aa), (ba) or (ca) of the definition of ‘eligible termination payment’ in subsection (1) applies is not a qualifying eligible termination payment.

“(12c) Notwithstanding subsection (12), where:

(a) an eligible termination payment is an eligible termination payment in relation to a taxpayer (in this subsection called the ‘receiving taxpayer’) because of the application of paragraph (g) or (h) of the definition of ‘eligible termination payment’ in subsection (1) to a payment (in this subsection called the ‘capital payment’) made to the receiving taxpayer;

(b) the capital payment:

(i) is made in relation to an annuity that:

(a) has been an eligible annuity in relation to any taxpayer under paragraph (b) of the definition of ‘eligible annuity’ in subsection (1);

(b) has a purchase price that consists wholly or partly of a rolled-over amount or rolled-over amounts; and

(c) was previously payable to a person who has died; and

(ii) is made to the receiving taxpayer after the death of the deceased person; and

(c) the receiving taxpayer was not the spouse of the deceased person at the time of death of the deceased person;

the eligible termination payment is not a qualifying eligible termination payment.

“(12d) Notwithstanding subsection (12), where:

(a) paragraph (j) of the definition of ‘eligible termination payment’ in subsection (1) applies to an eligible termination payment in relation to a taxpayer (in this subsection called the ‘receiving taxpayer’);

(b) the annuity referred to in that paragraph is an annuity:

(i) that has been an eligible annuity in relation to any taxpayer under paragraph (b) of the definition of ‘eligible annuity’ in subsection (1); and

(ii) whose purchase price consists wholly or partly of a rolled-over amount or rolled-over amounts; and

(c) the receiving taxpayer was not, at the time of death of the person to whom the annuity was payable, the spouse of that person;

the eligible termination payment is not a qualifying eligible termination payment.”.

Expenditure on scientific research

12. Section 73a of the Principal Act is amended by inserting after subsection (2) the following subsection:

“(2a) Subsection (2) does not apply to expenditure incurred by a taxpayer in the construction of a building or part of a building, in the making of an alteration or addition to a building or in the acquisition of a building or part of a building unless:

(a) either of the following subparagraphs applies:

(i) that construction or making commenced, or that acquisition occurred, before 21 November 1987;

(ii) any contract in respect of that construction, making or acquisition was entered into before 21 November 1987; and

(b) if the expenditure was incurred after 20 November 1987—the taxpayer intended, on 20 November 1987, that:

(i) scientific research, being research related to a business carried on by the taxpayer for the purpose of gaining or producing assessable income, would be carried on by or on behalf of the taxpayer in the building; and

(ii) the building, part of the building, alteration or addition, as the case may be, would be of use for scientific research purposes only.”.

Expenditure on research and development activities

13. Section 73b of the Principal Act is amended:

(a) by inserting in subsection (1) the following definitions:

“ ‘associate’ has the same meaning as in section 26aab;

‘non-associate’, in relation to an eligible company, means a person who is not an associate of the company;”;

(b) by inserting after subsection (1) the following subsection:

“(1a) For the purpose of determining whether a person is an associate of another person within the meaning of this section, the definition of ‘relative’ in subsection 6 (1) and the definition of ‘associate’ in subsection 26aab (14) apply as if a reference in the definition concerned to the spouse of a person included a reference to another person who, although not legally married to the person, lives with the person on a bona fide domestic basis as the husband or wife of the person.”;

(c) by adding at the end of paragraph (2) (f) “or”;

(d) by omitting paragraph (2) (g);

(e) by inserting after subsection (2) the following subsection:

“(2a) For the purposes of the definition of ‘research and development activities’ in subsection (1), activities carried on by or on behalf of an eligible company by way of the development of computer software shall not be taken to be systematic, investigative or experimental activities unless the computer software is developed for the purpose, or for purposes that include the purpose, of sale, rent, licence, hire or lease to 2 or more non-associates of the company (counting a non-associate of the company and the associates of such a non-associate together as one person).”;

(f) by inserting after subsection (5) the following subsection:

“(5a) This section does not apply to expenditure incurred by an eligible company in the acquisition or construction of a building or of an extension, alteration or improvement to a building unless:

(a) in the case of acquisition—any contract in respect of that acquisition was entered into before 21 November 1987;

(b) in the case of construction—either of the following subparagraphs applies:

(i) that construction commenced before 21 November 1987;

(ii) any contract in respect of that construction was entered into before 21 November 1987; and

(c) if the expenditure was incurred after 20 November 1987—the company intended, on 20 November 1987, that the building, or the extension, alteration or improvement to the building, as the case may be, would be for use by the company exclusively for the purpose of the carrying on by or on behalf of the company of research and development activities.”.

Money paid on shares in management and investment companies

14. Section 77f of the Principal Act is amended:

(a) by omitting from subsection (1) the definition of “prescribed share capital”;

(b) by omitting from paragraphs (2) (e) and (13) (a) and (b) “prescribed share capital” and substituting “share capital”.

Transfer of loss within company group

15. Section 80g of the Principal Act is amended:

(a) by omitting from subsection (5) “subsection (5a)” and substituting “subsections (5a) and (5b)”;

(b) by omitting from paragraph (5a) (a) “1986” and substituting “1984”;

(c) by inserting after subsection (5a) the following subsection:

“(5b) For the purposes of subsection (1), where:

(a) at a time (in this subsection called the ‘issue time’) in the year of income commencing on 1 July 1984 or in a subsequent year of income, a company (in this subsection called the ‘shelf company’) issued shares (in this subsection called the ‘newly issued shares’) to another company or companies;

(b) immediately before the issue time, a person or persons held other shares in the shelf company;

(c) immediately after the issue time, the shelf company redeemed all the shares in the shelf company other than the newly issued shares; and

(d) the shelf company was dormant, within the meaning of Part VI of the Companies Act 1981, throughout the period (in this subsection called the ‘dormant period’) commencing on the day on which the shelf company was incorporated and ending immediately before the issue time;

the shelf company shall be taken not to have been in existence during the dormant period.”.

Deductions for superannuation contributions by eligible persons

16. Section 82aat of the Principal Act is amended by adding at the end the following subsection:

“(3) A deduction is not allowable under this section in respect of so much of a contribution made after 12 January 1987 as is deemed by section 27d to have been expended in making a payment as mentioned in paragraph 27a (12) (a).”.

Interpretation

17. Section 110 of the Principal Act is amended:

(a) by omitting the definition of “eligible policy” and substituting the following definition:

“ ‘eligible policy’ means:

(a) a superannuation policy;

(b) a life assurance policy in relation to an immediate annuity, being an immediate annuity in respect of which the following conditions are satisfied:

(i) the annuity was purchased after 9 December 1987;

(ii) the purchase price does not consist wholly of a rolled-over amount or rolled-over amounts within the meaning of Subdivision aa of Division 2;

(iii) if the annuity contract permits a residual capital value to be payable—the contract does not

permit the residual capital value to exceed the purchase price of the annuity;

(iv) if the annuity is payable for a term of years certain—the annuity contract does not permit the total of any commutation payments to exceed the reduced purchase price of the annuity;

(v) if the annuity is payable until:

(a) the death of a particular person or of the last to die of 2 or more persons; or

(b) the end of a term of years certain;

whichever last occurs, and the annuity contract permits a commutation payment or payments to become payable before the end of that term of years certain—the contract does not permit the total of such payments to exceed the reduced purchase price of the annuity;

(vi) the Commissioner is satisfied there will not be any unreasonable deferral of the derivation of any annuity income, having regard to the following matters:

(a) to the extent to which the amounts of that annuity income will depend on the amount of income that may be derived by the person paying the annuity—the respective times of derivation of those amounts of annuity income and of the income of the person paying the annuity;

(b) to the extent to which the amounts of that annuity income are not dependent on the amount that may be derived by the person paying the annuity—the relative sizes of the annual entitlements to that annuity income;

(c) such other matters as the Commissioner considers relevant;

(c) a life assurance policy in relation to an annuity that was purchased after 12 January 1987 and comes within paragraph (b) of the definition of ‘eligible annuity’ in subsection 27a (1); or

(d) a life assurance policy in relation to an annuity that comes within paragraph (b) or (c) of the definition of ‘qualifying annuity’ in subsection 27a (1);”;

(b) by omitting the definitions of “deferred annuity” and “roll-over annuity”;

(c) by inserting the following definition:

“‘reduced purchase price’, in relation to an annuity, has the same meaning as in Subdivision aa of Division 2;”;

(d) by adding at the end the following subsection:

“(2) For the purposes of this Division, an annuity shall be taken to be presently payable at all times after, but not before, the beginning of the first period in respect of which the annuity is payable.”.

Interpretation

18. Section 116e of the Principal Act is amended:

(a) by omitting the definition of “eligible policy” and substituting the following definition:

“ ‘eligible policy’ means:

(a) a superannuation policy;

(b) a policy in relation to an immediate annuity, being an immediate annuity in respect of which the following conditions are satisfied:

(i) the annuity was purchased after 9 December 1987;

(ii) the purchase price does not consist wholly of a rolled-over amount or rolled-over amounts within the meaning of Subdivision aa of Division 2;

(iii) if the annuity contract permits a residual capital value to be payable—the contract does not permit the residual capital value to exceed the purchase price of the annuity;

(iv) if the annuity is payable for a term of years certain—the annuity contract does not permit the total of any commutation payments to exceed the reduced purchase price of the annuity; and

(v) if the annuity is payable until:

(a) the death of a particular person or of the last to die of 2 or more persons; or

(b) the end of a term of years certain;

whichever last occurs, and the annuity contract permits a commutation payment or payments to become payable before the end of that term of years certain—the contract does not permit the total of such payments to exceed the reduced purchase price of the annuity;

(vi) the Commissioner is satisfied there will not be any unreasonable deferral of the derivation of

any annuity income, having regard to the following matters:

(a) to the extent to which the amounts of that annuity income will depend on the amount of income that may be derived by the person paying the annuity—the respective times of derivation of those amounts of annuity income and of the income of the person paying the annuity;

(b) to the extent to which the amounts of that annuity income are not dependent on the amount that may be derived by the person paying the annuity—the relative sizes of the annual entitlements to that annuity income;

(c) such other matters as the Commissioner considers relevant;

(c) a policy in relation to an annuity that was purchased after 12 January 1987 and comes within paragraph (b) of the definition of ‘eligible annuity’ in subsection 27a (1); or

(d) a policy in relation to an annuity that comes within paragraph (b) or (c) of the definition of ‘qualifying annuity’ in subsection 27a (1);”;

(b) by omitting the definitions of “deferred annuity”, “eligible annuity” and “roll-over annuity”;

(c) by inserting the following definitions:

“ ‘qualifying annuity’ has the same meaning as in Subdivision aa of Division 2;

‘reduced purchase price’, in relation to an annuity, has the same meaning as in Subdivision aa of Division 2;”;

(d) by adding at the end the following subsection:

“(2) For the purposes of this Division, an annuity shall be taken to be presently payable at all times after, but not before, the beginning of the first period in respect of which the annuity is payable.”.

Assessable income of registered organisations

19. Section 116g of the Principal Act is amended by omitting from subsection (2) “eligible” and substituting “qualifying”.

20. After section 128ad of the Principal Act the following section is inserted:

Interpretation provisions relating to offshore banking units

“128ae. (1) In this Division, unless the contrary intention appears:

‘offshore banking unit’ means a person in relation to whom a declaration is in force under subsection (2);

‘offshore borrowing’ means a borrowing from:

(a) a non-resident in any currency; or

(b) a resident in a currency other than Australian currency;

‘offshore loan’ means a loan to:

(a) a person who is a non-resident, where it would reasonably be expected that:

(i) the person would continue to be a non-resident during the term of the loan; and

(ii) interest payable during the term of the loan would not be, in whole or in part, an outgoing incurred by the person in carrying on business in Australia at or through a permanent establishment of the person in Australia; or

(b) an offshore banking unit;

‘prevailing borrowing rate’, in relation to a person who is or has been an offshore banking unit, in relation to a particular time, means the effective annual interest rate that the Commissioner considers was payable by the person on borrowings at or about that time or, where there were none, by offshore banking units generally at or about that time;

‘prevailing borrowing term’, in relation to a person who is or has been an offshore banking unit, in relation to a particular time, means the period that the Commissioner considers was the usual term of borrowings by the person at or about that time or, where there were none, by offshore banking units generally at or about that time;

‘tax exempt loan money’ means an amount that is tax exempt loan money under this section;

‘transfer to a person’ includes apply an amount for the benefit of a person.

“(2) The Treasurer may, by notice published in the Gazette, declare a person being:

(a) a savings bank or trading bank as defined by subsection 5 (1) of the Banking Act 1959;

(b) a public authority constituted by a law of a State, being a public authority that carries on the business of State banking; or

(c) a person whom the Treasurer is satisfied is appropriately authorised to carry on business as a dealer in foreign exchange;

to be an offshore banking unit for the purposes of this Division.

“(3) A declaration under subsection (2) shall not come into force before the day on which the notice containing the declaration is published in the Gazette.

“(4) Where:

(a) a person who is an offshore banking unit makes an offshore borrowing; and

(b) the lender would, but for section 128gb, be liable to pay withholding tax on income consisting of interest on the offshore borrowing;

then, for the purposes of this Division, the amount borrowed is tax exempt loan money of the person.

“(5) Where:

(a) a person who is or has been an offshore banking unit makes an offshore loan of tax exempt loan money; and

(b) the loan is repaid;

the amount repaid is, for the purposes of this Division, deemed to be tax exempt loan money of the person.

“(6) Where a person who is an offshore banking unit borrows tax exempt loan money from a person who is or has been an offshore banking unit, the amount borrowed is, for the purposes of this Division, deemed to be tax exempt loan money of the first-mentioned person.

“(7) Where a person who is or has been an offshore banking unit transfers an amount of tax exempt loan money to another person, the following provisions have effect for the purposes of this Division:

(a) subject to subsections (10) and (11), the amount transferred ceases to be tax exempt loan money of the person; and

(b) the amount transferred does not, except under subsection (6), become tax exempt loan money of the other person.

“(8) Where a person who is or has been an offshore banking unit transfers to another person an amount that, in the opinion of the Commissioner, includes tax exempt loan money, so much of the amount transferred as the Commissioner considers was tax exempt loan money is deemed, for the purposes of this Division, to have been tax exempt loan money of the person.

“(9) Where a person who is or has been an offshore banking unit deals with an amount of tax exempt loan money of the person under the person’s internal accounting arrangements in such a way that the amount becomes available for possible transfer to other persons (other than by way of an offshore loan or repayment of an offshore borrowing), the following provisions have effect for the purposes of this Division:

(a) the person is, when the amount so becomes available, deemed to make a transfer of the amount to another person, other than by way of an offshore loan or repayment of an offshore borrowing;

(b) any actual transfer of the amount by the person to another person shall be disregarded.

“(10) For the purposes of this Division, where a person who is or has been an offshore banking unit transfers tax exempt loan money to another person in exchange for an equivalent amount in a different currency:

(a) the amount received in exchange shall be taken to be the same money as was transferred; and

(b) the transfer shall be taken not to have occurred.

“(11) For the purposes of this Division, where a person who is or has been an offshore banking unit transfers tax exempt loan money to another person by way of a deposit for the purposes of temporary safe-keeping pending the making of an offshore loan or repayment of an offshore borrowing:

(a) the amount held on deposit and upon being repaid shall be taken to be the same money as was transferred; and

(b) the transfer shall be taken not to have occurred.

“(12) For the purposes of this section, an amount:

(a) deposited in an account with a bank or other financial institution; or

(b) paid by way of consideration for the issue of a security;

shall be taken to have been lent to, and borrowed by, the bank, financial institution or issuer of the security.”.

Liability to withholding tax

21. Section 128b of the Principal Act is amended:

(a) by omitting from subsection (1) “subsection (3)” and substituting “subsections (3) and (3a)”;

(b) by omitting from subparagraph (3) (h) (iv) “or 128ga” and substituting “, 128ga or 128gb”;

(c) by inserting after subsection (3) the following subsection:

“(3a) If section 112a provides for the exclusion from assessable income of a percentage of a dividend derived by a non-resident who carries on business in Australia at or through a permanent establishment of the non-resident in Australia, this section does not apply to that percentage of so much of the dividend as has not been franked in accordance with section 160aqf.”.

Certain income not included in assessable income

22. Section 128d of the Principal Act is amended by omitting “or section 128ga” and substituting “, section 128ga or section 128gb”.

23. After section 128ga of the Principal Act the following section is inserted:

Division not to apply to interest payments on offshore borrowings by offshore banking units

“128gb. (1) This section applies to interest paid by a person in respect of an offshore borrowing of the person if, when the borrowing took place, the person was an offshore banking unit (whether or not the person is an offshore banking unit when the interest is paid).

“(2) Tax is not payable in accordance with this Division in respect of interest to which this section applies.

“(3) Where:

(a) under an arrangement:

(i) a person (in this subsection called the ‘conduit bank’) is to make an offshore borrowing from another person (in this subsection called the ‘foreign lender’); and

(ii) the conduit bank is to make an offshore loan to another person (in this subsection called the ‘real borrower’) of the same or a similar amount;

(b) but for this subsection, this section would apply to interest on the offshore borrowing; and

(c) the rate of interest payable on the offshore borrowing is the same as or, in the opinion of the Commissioner, similar to the rate of interest payable in respect of the offshore loan;

this section does not apply to interest on the offshore borrowing.

“(4) In subsection (3):

‘arrangement’ means any agreement, arrangement or understanding, whether formal or informal, whether express or implied and whether or not enforceable, or intended to be enforceable, by legal proceedings.”.

24. After section 128na of the Principal Act the following section is inserted:

Special tax payable in respect of certain dealings by current and former offshore banking units

“128nb. (1) Where a person who is or has been an offshore banking unit transfers to another person an amount of tax exempt loan money, other than by way of:

(a) an offshore loan; or

(b) repayment of an offshore borrowing;

the person is liable to pay income tax, as imposed by the Income Tax (Offshore Banking Units) (Withholding Tax Recoupment) Act 1988, on the lost withholding tax amount in respect of the transfer.

“(2) For the purposes of subsection (1), the lost withholding tax amount in respect of the transfer is an amount ascertained in accordance with the formula:

where:

IWT rate is the rate declared by the Parliament in respect of income to which subsection 128b (5) applies;

PB rate is the prevailing borrowing rate in relation to the person at the time of the transfer;

PB term is the number of years in the prevailing borrowing term in relation to the person at the time of the transfer; and

TA is the amount of tax exempt loan money transferred.

“(3) Tax under this section is due and payable by the person liable to pay the tax at the end of:

(a) 21 days after the end of the month in which the transfer to which it relates takes place; or

(b) such further period as the Commissioner, in special circumstances, allows.

“(4) Section 128c (other than subsections (1) and (4aa)) applies, in addition to its application apart from this subsection, as if references in that section to withholding tax were references to tax payable under this section.

“(5) The Commissioner may remit the whole or part of an amount of tax payable under this section in relation to the transfer of an amount of tax exempt loan money to another person if:

(a) the Commissioner is satisfied that:

(i) the liability to pay the amount of tax arose because the person mistakenly believed, on reasonable grounds, that the other person was a non-resident or an offshore banking unit, that interest payable to the person in respect of the amount transferred would be an outgoing of a particular kind or that the amount transferred was not tax exempt loan money; and

(ii) the person had taken reasonable steps to ascertain the matter to which the mistaken belief related; or

(b) the Commissioner is satisfied that there are special circumstances justifying the remission of the whole or part of the amount of tax.”.

Stripped securities

25. Section 159gz of the Principal Act is amended by omitting from subsection (4) “proportion of and substituting “proportion as”.

Rebate in respect of amounts assessable under section 26ah

26. Section 160aab of the Principal Act is amended:

(a) by omitting “or” from the end of paragraph (1) (e);

(b) by adding at the end of subsection (1) the following word and paragraph:

“; or (g) the State Government Insurance Corporation established by a law of Western Australia.”.

Rebate for money paid on shares for the purposes of petroleum exploration, prospecting or mining

27. Section 160aca of the Principal Act is amended by inserting “(being that Act as in force immediately before the Petroleum (Submerged Lands) Amendment Act 1980 came into operation)” after “Petroleum (Submerged Lands) Act 1967” in the definition of “adjacent area” in subsection (1).

Interpretation

28. Section 160ae of the Principal Act is amended:

(a) by omitting from paragraph (3) (e) “or” (last occurring);

(b) by inserting after paragraph (3) (e) the following paragraph:

“(ea) interest that is offshore banking income; or”;

(c) by adding at the end the following subsections:

“(4) In this Division, ‘offshore banking income’ means:

(a) income (being interest, fees, commission or other amounts) derived by a person in respect of offshore banking transfers of the person; or

(b) income consisting of dividends paid to a person by a company out of profits derived from the making of offshore banking transfers.

“(5) Where, if all offshore borrowings made by persons when they were offshore banking units were taken to be tax exempt loan money of the persons for the purposes of Division 11a, an offshore loan, or other transfer, of an amount by a person would, for the purposes of that Division, be an offshore loan, or other transfer, of tax exempt loan money of the person, the offshore loan, or other transfer, of the amount is an offshore banking transfer of the person for the purposes of subsection (4).

“(6) Expressions used in subsection (5) that are also used in Division 11a have the same respective meanings in that subsection as in that Division.”.

Credits in respect of foreign tax

29. Section 160af of the Principal Act is amended by omitting subsection (7) and substituting the following subsection:

“(7) Notwithstanding the preceding provisions of this section, where the foreign income derived by a taxpayer in a year of income consists of any 2 or more of the following classes of income:

(a) interest income;

(b) offshore banking income;

(c) other income;

the following provisions have effect:

(d) this section does not apply in relation to the taxpayer in relation to the foreign income as a whole but, instead, applies in relation to the

taxpayer separately in relation to each of the 2 or more classes of income;

(e) for the purposes of this section as so applying in relation to each of the 2 or more classes of income, that class of the income shall be treated as the whole of the foreign income.”.

30. After section 160afa of the Principal Act the following section is inserted:

Certain dividends deemed to be offshore banking income

160afaa. (1) Where:

(a) a dividend is paid by a foreign company to a taxpayer in a year of income; and

(b) at any time in the year of income, the foreign company is related to the taxpayer or would be related to the taxpayer if the taxpayer were an Australian company;

then, for the purposes of this Division, so much of the dividend as does not exceed the amount then standing in the transferred offshore banking income pool of the foreign company shall be deemed to be offshore banking income derived by the taxpayer.

“(2) For the purposes of subsection (1), the foreign company shall be deemed to have at a particular time a transferred offshore banking income pool consisting of the sum of all amounts of transferred offshore banking income of the company derived at or before that time, reduced by the sum of all amounts deemed under subsection (1) to be offshore banking income derived by the taxpayer before that time.

“(3) In subsection (2), ‘transferred offshore banking income’, in relation to the foreign company, means any income derived by the company, where:

(a) the right to receive the income was transferred or assigned to the company by the taxpayer; and

(b) the income would, but for the transfer or assignment of the right, have been offshore banking income of the taxpayer.”.

Losses of previous years

31. Section 160afd of the Principal Act is amended by omitting subsection (6) and substituting the following subsection:

“(6) For the purposes of this section:

(a) interest income constitutes a single class of income;

(b) offshore banking income constitutes a single class of income; and

(c) all other income constitutes a single class of income.”.

Transfer of excess credit within company group

32. Section 160afe of the Principal Act is amended:

(a) by omitting from subsection (6) “subsection (6a)” and substituting “subsections (6a) and (6b)”;

(b) by omitting from paragraph (6a) (a) “1986” and substituting “1987”;

(c) by inserting after subsection (6a) the following subsection:

“(6b) For the purposes of subsection (2), where:

(a) at a time (in this subsection called the ‘issue time’) in the year of income commencing on 1 July 1987 or in a subsequent year of income, a company (in this subsection called the ‘shelf company’) issued shares (in this subsection called the ‘newly issued shares’) to another company or companies;

(b) immediately before the issue time, a person or persons held other shares in the shelf company;

(c) immediately after the issue time, the shelf company redeemed all the shares in the shelf company other than the newly issued shares; and

(d) the shelf company was dormant, within the meaning of Part VI of the Companies Act 1981, throughout the period (in this subsection called the ‘dormant period’) commencing on the day on which the shelf company was incorporated and ending immediately before the issue time;

the shelf company shall be taken not to have been in existence during the dormant period.”;

(d) by omitting subsection (8) and substituting the following subsection:

“(8) This section applies only to the following 2 classes of income:

(a) interest income;

(b) all other income other than offshore banking income.”.

Transfer of net capital loss within company group

33. Section 160zp of the Principal Act is amended:

(a) by omitting from subsection (6) “subsection (6a)” and substituting “subsections (6a) and (6b)”;

(b) by omitting from paragraph (6a) (a) “1986” and substituting “1985”;

(c) by inserting after subsection (6a) the following subsection:

“(6b) For the purposes of subsection (1), where:

(a) at a time (in this subsection called the ‘issue time’) in the year of income commencing on 1 July 1985 or in a subsequent year of income, a company (in this subsection called the ‘shelf company’) issued shares (in this subsection called the ‘newly issued shares’) to another company or companies;

(b) immediately before the issue time, a person or persons held other shares in the shelf company;

(c) immediately after the issue time, the shelf company redeemed all the shares in the shelf company other than the newly issued shares; and

(d) the shelf company was dormant, within the meaning of Part VI of the Companies Act 1981, throughout the period (in this subsection called the ‘dormant period’) commencing on the day on which the shelf company was incorporated and ending immediately before the issue time;

the shelf company shall be taken not to have been in existence during the dormant period.”.

Transfer of asset to wholly-owned company

34. Section 160zzn of the Principal Act is amended:

(a) by inserting in subparagraph (7) (b) (i) “the” before “indexed”;

(b) by omitting from subparagraph (7) (b) (ii) “asset” (first occurring) and substituting “shares or securities”.

Transfer of asset between companies in the same group

35. Section 160zzo of the Principal Act is amended:

(a) by omitting from subsection (8) “subsection (8a)” and substituting “subsections (8a) and (8b)”;

(b) by omitting from paragraph (8a) (a) “1986” and substituting “1985”;

(c) by inserting after subsection (8a) the following subsection:

“(8b) For the purposes of subsection (3), where:

(a) at a time (in this subsection called the ‘issue time’) in the year of income commencing on 1 July 1985 or in a subsequent year of income, a company (in this subsection called the ‘shelf company’) issued shares (in this subsection called the ‘newly issued shares’) to another company or companies;

(b) immediately before the issue time, a person or persons held other shares in the shelf company;

(c) immediately after the issue time, the shelf company redeemed all the shares in the shelf company other than the newly issued shares; and

(d) the shelf company was dormant, within the meaning of Part VI of the Companies Act 1981, throughout the period (in this subsection called the ‘dormant period’) commencing on the day on which the shelf company was incorporated and ending immediately before the issue time;

the shelf company shall be taken not to have been in existence during the dormant period.”.

36. After section 160zzp of the Principal Act the following sections are inserted in Division 17 of Part IIIa:

Exchange of units in a unit trust for shares in a company

“160zzpa. (1) This section applies where:

(a) under a scheme that:

(i) is for the reorganisation of the affairs of a unit trust; and

(ii) was entered into, or commenced to be carried out, after 9 December 1987;

2 or more taxpayers (in this section called the ‘exchanging taxpayers’), being the holders of all the units (in this section called the ‘exchange units’) in the unit trust, dispose of all the exchange units to a company (in this section called the ‘interposed company’), not being a company in the capacity of a trustee of a trust estate;

(b) the consideration in respect of each of the disposals consists only of non-redeemable shares (in this section called the ‘replacement shares’) in the interposed company;

(c) the total number of replacement shares is equal to, or is a multiple of, the total number of exchange units;

(d) in the case of each exchanging taxpayer—all of the exchange units held by the taxpayer are disposed of at the same time (in this section called the ‘exchanging taxpayer’s disposal time’);

(e) immediately after the time (in this section called the ‘completion time’) of the disposals or, if the disposals occurred at different times, the last of the disposals:

(i) the exchanging taxpayers are the owners of all the shares in the interposed company; and

(ii) the interposed company holds all the units in the unit trust;

(f) if the exchanging taxpayer’s disposal time in relation to a particular exchanging taxpayer occurred before the completion time—the taxpayer was the owner of the replacement shares concerned at all times during the period commencing immediately after the exchanging taxpayer’s disposal time and ending at the completion time;

(g) the unit trust is a resident unit trust in relation to the year of income of the unit trust in which the completion time occurred;

(h) the interposed company is a resident of Australia at the completion time and, if the disposals occurred at different times, at all times during the period commencing at the time of the first of the disposals and ending at the completion time;

(j) in the case of an exchanging taxpayer in the capacity of a trustee of a trust estate—immediately after the exchanging taxpayer’s disposal time, the taxpayer holds the replacement shares concerned upon the same trust as the taxpayer held the exchange units that were disposed of to the interposed company;

(k) immediately after the completion time, each exchanging taxpayer owned the replacement shares in the interposed company in the same proportion as the taxpayer held the exchange units in the unit trust that were disposed of to the interposed company;

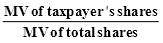

(m) in the case of each exchanging taxpayer—the ratio calculated in accordance with the formula:

where:

MV of taxpayer’s shares is so much of the market value, immediately after the completion time, of the replacement shares owned by the taxpayer immediately after that time as is attributable to the exchange units held by the interposed company; and

MV of total shares is so much of the market value of all the replacement shares, immediately after the completion time, as is attributable to the exchange units held by the interposed company;

is the same as the ratio calculated in accordance with the formula:

where:

MV of taxpayer’s units is the market value, immediately before the exchanging taxpayer’s disposal time, of the exchange units held by the taxpayer immediately before that time; and

MV of total units is the market value of all the exchange units immediately before the exchanging taxpayer’s disposal time;

(n) the interposed company has, by notice in writing given to the Commissioner within 2 months after the completion time, or within such further time as the Commissioner allows, elected that this subsection apply in respect of all the disposals; and

(p) the notice referred to in paragraph (n) is accompanied by a declaration, in a form approved by the Commissioner, with respect to the operation of this section.

“(2) If:

(a) either of the following conditions is satisfied in relation to a particular exchanging taxpayer:

(i) the taxpayer is a resident of Australia;

(ii) each disposal of an exchange unit by the taxpayer constitutes a disposal of a taxable Australian asset; and

(b) the taxpayer has elected that this subsection is to apply in respect of the disposal of all the exchange units held by the taxpayer;

this Part (other than this section) does not apply in respect of the disposal of those units and:

(c) if all the exchange units held by the taxpayer were acquired by the taxpayer before 20 September 1985—the taxpayer shall be deemed, for the purposes of this Part, to have acquired the replacement shares concerned before 20 September 1985;

(d) if:

(i) some, but not all, of the exchange units held by the taxpayer were acquired by the taxpayer before 20 September 1985;

(ii) the taxpayer, in the notice of election, nominates, as pre-CGT shares, such of the replacement shares acquired by the taxpayer as are specified in the notice; and

(iii) the number of replacement shares nominated by the taxpayer does not exceed the number calculated in accordance with the formula:

where:

Pre CGT units is the number of exchange units acquired by the taxpayer before 20 September 1985;

Shares is the number of replacement shares owned by the taxpayer immediately after the completion time; and

Total units is the number of exchange units that the taxpayer disposed of to the interposed company;

the taxpayer shall be deemed, for the purposes of this Part, to have acquired the nominated shares before 20 September 1985;

(e) each replacement share acquired by the taxpayer that is not deemed by paragraph (c) or (d) to have been acquired by the taxpayer before 20 September 1985 shall be taken to be a post-20 September 1985 replacement share for the purposes of paragraph (g) and subsection (3);

(f) each exchange unit that was acquired by the taxpayer on or after 20 September 1985 shall be taken to be a post-20 September 1985 exchange unit for the purposes of paragraph (g); and

(g) in the case of a post-20 September 1985 replacement share—the taxpayer shall be deemed to have paid or given as consideration in respect of the acquisition of the share an amount equal to:

(i) for the purpose of ascertaining whether a capital gain accrued to the taxpayer in the event of a subsequent disposal of the share by the taxpayer—the amount calculated in accordance with the formula:

where:

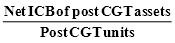

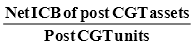

ICB of post CGT units is the sum of the amounts that would have been the indexed cost bases to the taxpayer of post-20 September 1985 exchange units for the purposes of this Part if this Part had applied in respect of the disposal of the units by the taxpayer to the interposed company; and

Post CGT shares is the number of post-20 September 1985 replacement shares owned by the taxpayer immediately after the completion time; or

(ii) for the purposes of ascertaining whether the taxpayer incurred a capital loss in the event of a subsequent disposal of the share by the taxpayer—the amount calculated in accordance with the formula:

where:

RCB of post CGT units is the sum of the amounts that would have been the reduced cost bases to the taxpayer of post-20 September 1985 exchange units for the purposes of this Part if this Part had applied in respect of the disposal of the units by the taxpayer to the interposed company; and

Post CGT shares is the number of post-20 September 1985 replacement shares owned by the taxpayer immediately after the completion time.

“(3) If a post-20 September 1985 replacement share is disposed of by an exchanging taxpayer within 12 months after the earliest day, being a day after 19 September 1985, on which any exchange unit was acquired by the taxpayer, the reference in paragraph (2) (g) to the indexed cost bases to the taxpayer of units is a reference to the cost bases to the taxpayer of the units.

“(4) An election by a taxpayer under subsection (2) shall be made by notice in writing given to the Commissioner on or before the date of lodgment of the return of income of the taxpayer for the year of income in which the disposal of the exchange units concerned took place, or within such further period as the Commissioner allows.

“(5) If:

(a) any of the assets of the unit trust, as at the completion time, were acquired by the trustee of the unit trust before 20 September 1985;

(b) the interposed company, by notice in writing accompanying the notice referred to in paragraph (1) (n), nominates, as pre-CGT units, such of the exchange units held by the company immediately after the completion time as are specified in the notice; and

(c) the number of exchange units nominated by the company does not exceed the number calculated in accordance with the formula:

where:

Net value of pre CGT assets is the number of dollars in the market value of the assets referred to in paragraph (a) as at the completion time reduced by the number of dollars in the

liabilities of the unit trust as at that time to the extent that those liabilities are attributable to those assets;

Units is the number of exchange units held by the company immediately after the completion time; and

Net value of total assets is the number of dollars in the market value of the assets of the unit trust as at the completion time reduced by the number of dollars in the liabilities of the unit trust as at that time;

the units so nominated shall be deemed, for the purposes of this Part, to have been acquired by the interposed company before 20 September 1985.

“(6) Any other exchange units held by the interposed company immediately after the completion time shall be taken to be post-20 September 1985 exchange units for the purposes of subsections (7) and (8).

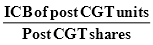

“(7) The interposed company shall be deemed to have paid or given as consideration in respect of the acquisition of each post-20 September 1985 exchange unit an amount equal to:

(a) for the purpose of ascertaining whether a capital gain accrued to the company in the event of a subsequent disposal of the unit by the company—the amount calculated in accordance with the formula:

where:

Net ICB of post CGT assets is the sum of the amounts that would have been the indexed cost bases to the trustee of the unit trust, for the purposes of this Part, of such of the assets of the unit trust, as at the completion time, as were acquired by the trustee on or after 20 September 1985 if those assets of the trust had been disposed of by the trustee at the completion time, being that sum reduced by the liabilities of the unit trust as at the completion time to the extent that those liabilities are attributable to those assets; and

Post CGT units is the number of post-20 September 1985 exchange units held by the company immediately after the completion time; or

(b) for the purposes of ascertaining whether the company incurred a capital loss in the event of a subsequent disposal of the unit by the company—the amount calculated in accordance with the formula:

where:

Net RCB of post CGT assets is the sum of the amounts that would have been the reduced cost bases to the trustee of the unit trust, for the purposes of this Part, of such of the assets of the unit trust, as at the completion time, as were acquired by the trustee on or after 20 September 1985 if those assets had been disposed of by the trustee at the completion time,

being that sum reduced by the liabilities of the unit trust as at the completion time to the extent that those liabilities are attributable to those assets; and

Post CGT units is the number of post-20 September 1985 exchange units held by the company immediately after the completion time.

“(8) If a post-20 September 1985 exchange unit is disposed of by the interposed company within 12 months after the day on which the unit was acquired by the company, the reference in paragraph (7) (a) to the indexed cost bases to the trustee of assets is a reference to the cost bases to the trustee of the assets.

“(9) For the purposes of this section, a share issued by a company shall be taken to be a non-redeemable share unless:

(a) the share is, or at the option of the company is to be, liable to be redeemed; or

(b) the share was issued under, or as part of, an agreement or arrangement, whether oral or in writing and whether entered into before or after the commencement of this section, that had the purpose, or purposes that included the purpose, of enabling the company, by means of the redemption, purchase or cancellation, or of a reduction in the paid-up value, of that share or of any other share in the company, to pay, transfer or apply to, on behalf of or at the direction of the person to whom the share was issued or any other person, whether upon the exercise of an option by the company or by any other person or not, any money or other property other than shares in the company.

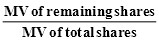

“(10) Where:

(a) immediately after the completion time, the exchanging taxpayers are the owners of some, but not all, of the shares in the interposed company;

(b) the number of the remaining shares does not exceed 5; and

(c) the Commissioner is of the opinion that, having regard to:

(i) the ratio calculated in accordance with the formula:

where:

MV of remaining shares is the number of dollars in the market value of the remaining shares immediately after the completion time; and

MV of total shares is the number of dollars in the market value of the replacement shares immediately after the completion time; and

(ii) such other matters as the Commissioner considers relevant; it would be unreasonable not to treat the exchanging taxpayers as being the owners of all the shares in the interposed company;

the following provisions have effect:

(d) the exchanging taxpayers shall be treated, for the purposes of subparagraph (1) (e) (i), as if, immediately after the completion time, they were the owners of all the shares in the interposed company;

(e) the remaining shares shall be disregarded for the purposes of the application of paragraph (1) (k).

“(11) For the purposes of this section, the liabilities of the unit trust, as at the completion time, to the extent that, apart from this subsection, they are not attributable to the assets of the unit trust as at the completion time (in this subsection called the ‘general liabilities’), shall be taken to be attributable to particular assets of the unit trust, as at that time, to the extent calculated in accordance with the formula:

where:

General liabilities is the amount of the general liabilities;

MV of particular assets is the number of dollars in the market value, as at the completion time, of the particular assets as at that time; and

MV of total assets is the number of dollars in the market value, as at the completion time, of the assets of the unit trust as at that time.

Redemption or cancellation of units in a unit trust in exchange for shares in a company

“160zzpb. (1) This section applies where:

(a) all of the following conditions are satisfied in relation to a scheme for the reorganisation of the affairs of a unit trust:

(i) the scheme was entered into, or commenced to be carried out, after 9 December 1987;

(ii) under the scheme, a company (in this section called the ‘interposed company’), not being a company in the capacity of a trustee of a trust estate, acquires not more than 5 units (in this section called the ‘formal units’) in the unit trust;

(iii) the interposed company did not hold any other units in the unit trust at any time before the acquisition of the formal units;

(iv) the remaining units (in this section called the ‘exchange units’) in the unit trust are held by 2 or more taxpayers (in this section called the ‘exchanging taxpayers’);

(v) under the scheme, all the exchange units are redeemed or cancelled;

(vi) under the scheme, the trustee of the unit trust issues to the interposed company 2 or more units (in this section called the ‘scheme units’) in the unit trust;

(vii) the number of scheme units issued to the interposed company equals, or is a multiple of, the number of exchange units that were redeemed or cancelled;

(b) the consideration in respect of each of the redemptions or cancellations consists only of newly issued non-redeemable shares (in this section called the ‘replacement shares’) in the interposed company;

(c) the total number of replacement shares is equal to, or is a multiple of, the total number of exchange units;

(d) in the case of each exchanging taxpayer—all of the exchange units held by the taxpayer are redeemed or cancelled at the same time (in this section called the ‘exchanging taxpayer’s disposal time’);

(e) immediately after the time (in this section called the ‘completion time’) of the redemptions or cancellations or, if the redemptions or cancellations occurred at different times, the last of the redemptions or cancellations:

(i) the exchanging taxpayers are the owners of all the shares in the interposed company; and

(ii) the interposed company holds all the units in the unit trust;

(f) if the exchanging taxpayer’s disposal time in relation to a particular exchanging taxpayer occurred before the completion time—the taxpayer was the owner of the replacement shares concerned at all times during the period commencing immediately after the exchanging taxpayer’s disposal time and ending at the completion time;

(g) the unit trust is a resident unit trust in relation to the year of income of the unit trust in which the completion time occurred;

(h) the interposed company is a resident of Australia at the completion time and, if the redemptions or cancellations occurred at different times, at all times during the period commencing at the time of the first of the redemptions or cancellations and ending at the completion time;

(j) in the case of an exchanging taxpayer in the capacity of a trustee of a trust estate—immediately after the exchanging taxpayer’s disposal time, the taxpayer holds the replacement shares concerned upon the same trust as the taxpayer held the exchange units that were redeemed or cancelled;

(k) immediately after the completion time, each exchanging taxpayer owned the replacement shares in the interposed company in the same proportion as the taxpayer held the exchange units in the unit trust that were redeemed or cancelled;

(m) in the case of each exchanging taxpayer—the ratio calculated in accordance with the formula:

where:

MV of taxpayer’s shares is so much of the market value, immediately after the completion time, of the replacement shares owned by the taxpayer immediately after that time as is attributable to the scheme units held by the interposed company; and

MV of total shares is so much of the market value of all the replacement shares, immediately after the completion time, as is attributable to the scheme units held by the interposed company;

is the same as the ratio calculated in accordance with the formula:

where: