PART II—AMENDMENT OF THE INCOME TAX ASSESSMENT ACT 1936

Principal Act

3. In this Part, “Principal Act” means the Income Tax Assessment Act 19361.

Expenditure on scientific research

4. Section 73a of the Principal Act is amended by omitting “Health, by the Secretary to the Department of Science or by the Secretary to the Department of Employment and Industrial Relations” from the definition of “an approved research institute” in subsection (6) and substituting “Community Services and Health or by the Secretary to the Department of Employment, Education and Training”.

Repeal of sections 115 and 116

5. (1) Sections 115 and 116 of the Principal Act are repealed.

(2) The amendment made by subsection (1) applies to assessments in respect of income of the year of income commencing on 1 July 1988 and of all subsequent years of income.

6. After Division 16h of Part III of the Principal Act the following Division is inserted:

“Division 16j—Effect of Cancellation of Subsidiary’s Shares in Holding Company

Interpretation—general

“159gzzzc. (1) In this Division:

‘associate’ has, subject to subsection (2), the same meaning as in subsection 26aab (14);

‘cancellation’ includes redemption;

‘disposal’ includes cancellation;

‘entity’ means a company, a partnership or a trust estate;

‘pre-cancellation period’, in relation to a cancellation of shares to which this Division applies, means the period beginning when the holding company concerned became a holding company of the subsidiary concerned and ending at the time of the cancellation;

‘security’ means stock, a bond or debenture, or any other document evidencing the indebtedness of a person, whether or not the debt is secured.

“(2) For the purposes of the definition of ‘associate’ in subsection (1), any reference in subsection 26aab (14), or in any other provision of this Act that has effect for the purposes of that subsection, to the spouse of a person (in this subsection called the ‘relevant person’) shall be taken:

(a) to include a reference to a person who is living with the relevant person as the husband or wife of the relevant person on a bona fide domestic basis although not legally married to the relevant person; but

(b) not to include a reference to a person who is legally married to the relevant person but is living separately and apart from the relevant person on a permanent basis.

“(3) For the purposes of this Division, a company is:

(a) a subsidiary of another company; or

(b) the holding company of another company;

if the first-mentioned company is such for the purposes of the Companies Act 1981 or a corresponding law in force in a State or Territory.

“(4) For the purposes of this Division, a reference to an interest in an entity is a reference to a legal or equitable interest in:

(a) if the entity is a company—shares in the company;

(b) if the entity is a partnership—capital or profits of the partnership;

(c) if the entity is a trust estate—corpus or income of the trust estate; or

(d) in any case—securities issued by the entity.

Meaning of “eligible entity”, “eligible interest” and “eligible proportion”

“159gzzzd. For the purposes of this Division, where a holding company holds interests in a subsidiary of the holding company either directly or indirectly through interposed entities:

(a) a reference to an eligible entity in relation to the holding company and the subsidiary is a reference to the holding company or any of the interposed entities;

(b) a reference to an eligible interest of an eligible entity is a reference to any interest held by the eligible entity directly in the subsidiary or directly in any other eligible entity in relation to the holding company and the subsidiary; and

(c) a reference to the eligible proportion in relation to an eligible interest of an eligible entity is a reference to the proportion of the total interests held directly in the subsidiary by all persons and entities that is represented by:

(i) if the eligible entity holds the eligible interest directly in the subsidiary—the eligible interest; or

(ii) if, by virtue of holding the eligible interest, the eligible entity holds an interest in the subsidiary indirectly through another eligible entity or other eligible entities—that interest in the subsidiary.

Share cancellations to which this Division applies

“159gzzze. Where a holding company cancels shares in itself that are held by a subsidiary of that company, this Division applies to the cancellation of the shares.

Effect on subsidiary of share cancellations to which this Division applies

“159gzzzf. (1) Where:

(a) this Division applies to a cancellation of shares; and

(b) apart from this section, either:

(i) the subsidiary concerned would not receive or be entitled to receive any consideration in respect of the cancellation; or

(ii) the consideration that the subsidiary concerned would receive or be entitled to receive in respect of the cancellation would be less than the adjusted market value of the shares;

the following provisions have effect for the purposes of this Act:

(c) where subparagraph (b) (i) applies—the subsidiary shall be taken to have received or to be entitled to receive, as consideration in respect of the cancellation, an amount equal to the adjusted market value of the shares;

(d) where subparagraph (b) (ii) applies—the amount of the consideration that the subsidiary receives or is entitled to receive in respect of the cancellation shall be taken to be increased by an amount so that it equals the adjusted market value of the shares.

“(2) For the purposes of subsection (1), the adjusted market value of the shares is the amount that would have been their market value at the time of the cancellation if the cancellation did not occur and was never proposed to occur.

Pre-cancellation disposals of eligible interests

“159gzzzg. (1) Where:

(a) this Division applies to a cancellation of shares;

(b) during the pre-cancellation period, there is a disposal of an eligible interest held by an eligible entity in relation to the holding company and the subsidiary concerned; and

(c) apart from this section, either:

(i) the eligible entity would not have received or been entitled to receive any consideration in respect of the disposal; or

(ii) the consideration that the eligible entity would have received or been entitled to receive in respect of the disposal would have been less than the adjusted market value of the eligible interest;

the following provisions have effect for the purposes of this Act:

(d) where subparagraph (c) (i) applies—the eligible entity shall be taken to have received or to have been entitled to receive, as

consideration in respect of the disposal, an amount equal to the adjusted market value of the eligible interest;

(e) where subparagraph (c) (ii) applies—the amount of the consideration that the eligible entity received or was entitled to receive in respect of the disposal shall be taken to be increased by an amount so that it equals the adjusted market value of the eligible interest.

“(2) For the purposes of subsection (1), the adjusted market value of the eligible interest is the amount that would have been its market value at the time of the disposal if the cancellation of the shares to which this Division applies did not occur and was never proposed to occur.

Post-cancellation disposals of eligible interests etc.

“159gzzzh. (1) Where:

(a) as a result of the application of section 159gzzzf in relation to a cancellation of shares, the subsidiary concerned is taken to have received or to be entitled to receive an amount of consideration or an increase in an amount of consideration (which amount or increase is in this section called the ‘cancellation adjustment amount’) in relation to the cancellation of the shares; and

(b) an eligible entity in relation to the holding company and the subsidiary concerned holds an eligible interest at the time of the share cancellation;

then this section applies in relation to the eligible interest.

“(2) For the purposes of this Act (other than Part IIIa):

(a) if the eligible interest is not trading stock—in determining:

(i) the amount of any deduction allowed or allowable to the eligible entity in respect of the acquisition of the eligible interest; or

(ii) the amount of any profit included in, or loss allowable as a deduction from, the assessable income of the eligible entity in respect of the acquisition and any subsequent disposal of the eligible interest;

the consideration in respect of the acquisition of the eligible interest shall be taken to have been reduced by the eligible interest’s eligible proportion of the cancellation adjustment amount; and

(b) if the eligible interest is trading stock—the consideration in respect of any subsequent disposal of the eligible interest shall be taken to be increased by the eligible interest’s eligible proportion of the cancellation adjustment amount.

“(3) For the purposes of Part IIIa:

(a) in determining whether a capital gain accrues to the eligible entity in the event of any subsequent disposal of the eligible interest—the eligible entity shall be taken to have:

(i) disposed of the eligible interest at the time of the share cancellation for a consideration equal to the indexed cost

base (or, where the actual disposal occurs within 12 months of the actual acquisition of the eligible interest, the cost base) to the eligible entity in respect of the eligible interest; and

(ii) immediately re-acquired the eligible interest for a consideration equal to the indexed cost base or the cost base, as the case may be, reduced by the eligible interest’s eligible proportion of the cancellation adjustment amount;

(b) in determining whether the eligible entity incurs a capital loss in the event of any subsequent disposal of the eligible interest—the eligible entity shall be taken to have:

(i) disposed of the eligible interest at the time of the share cancellation for a consideration equal to the reduced cost base to the eligible entity in respect of the eligible interest; and

(ii) immediately re-acquired the eligible interest for a consideration equal to the reduced cost base reduced by the eligible interest’s eligible proportion of the cancellation adjustment amount; and

(c) the reference in subsection 160z (3) to the day on which the eligible interest was acquired by the eligible entity shall be taken to be a reference to the day on which the eligible interest was actually acquired by the eligible entity.

“(4) Expressions used in subsection (3) that are also used in Part IIIA have the same respective meanings in that subsection as in that Part.

“(5) This section applies in relation to the acquisition or disposal of the eligible interest held by the eligible entity at the time of the share cancellation even if the entity was not an eligible entity, and the interest was not an eligible interest, at the time of the acquisition or disposal.

Additional application of sections 159gzzzg and 159gzzzh to associates

“159gzzzi. (1) Subject to this section, where a natural person is an associate of a holding company (otherwise than solely because of being the trustee of a trust estate), sections 159gzzzg and 159gzzzh apply (in addition to any application apart from this application of this section) as if references in those sections to:

(a) an eligible entity in relation to the holding company and the subsidiary concerned;

(b) an eligible interest of such an entity; or

(c) the eligible proportion in relation to such an interest;

were references to what would, if the natural person were a holding company in relation to the subsidiary, be respectively:

(d) an eligible entity in relation to the natural person and the subsidiary;

(e) an eligible interest of such an entity; or

(f) the eligible proportion in relation to such an interest.

“(2) For the purposes of applying section 159gzzzg or 159gzzzh in accordance with subsection (1):

(a) any interest of an entity that is an eligible interest for the purposes of the application of that section apart from subsection (1) shall be taken not to be an eligible interest; and

(b) any eligible interest of an eligible entity (including the natural person) held in the actual holding company referred to in subsection (1), or in any eligible entity interposed between the natural person and that holding company, shall be taken not to be an eligible interest.”.

Consideration in respect of disposal

7. Section 160zd of the Principal Act is amended by adding at the end the following subsection:

“(6) This section has effect subject to Division 16j of Part III.”.

Amendment of assessments

8. Section 170 of the Principal Act is amended by inserting in subsection (10) “159gzzzh (2),” before “159zj (2b)”.

9. After section 266 of the Principal Act the following Part is inserted:

“PART IX—TAXATION OF SUPERANNUATION BUSINESS AND RELATED BUSINESS

“Division 1—Preliminary

Interpretation

“267. (1) In this Part, unless the contrary intention appears:

‘actuary’ has the same meaning as in the Life Insurance Act 1945;

‘approved person’ means a person included in a class of persons for the time being approved by the Commissioner in writing for the purposes of this definition;

‘arm’s length premium’, in relation to an insurance policy, means the amount that the insured could reasonably be expected to be required to pay to obtain the insurance policy under a transaction where the parties to the transaction are dealing with each other at arm’s length in relation to the transaction;

‘complying ADF’, in relation to a year of income, means a fund in respect of which:

(a) the Insurance and Superannuation Commissioner has given a notice under section 14 of the OSS Act stating that the Insurance and Superannuation Commissioner is satisfied that the fund satisfied the approved deposit fund conditions in relation to the year of income; or

(b) the Insurance and Superannuation Commissioner has given a notice under section 15 of the OSS Act stating that the Insurance and Superannuation Commissioner is satisfied that the fund should be treated as if it had satisfied the approved deposit fund conditions in relation to the year of income;

‘complying superannuation fund’, in relation to a year of income, means a fund in respect of which:

(a) the Insurance and Superannuation Commissioner has given a notice under section 12 of the OSS Act stating that the Insurance and Superannuation Commissioner is satisfied that the fund satisfied the superannuation fund conditions in relation to the year of income; or

(b) the Insurance and Superannuation Commissioner has given a notice under section 13 of the OSS Act stating that the Insurance and Superannuation Commissioner is satisfied that the fund should be treated as if it had satisfied the superannuation fund conditions in relation to the year of income;

‘constitutionally protected fund’ has the meaning given by subsection 271 (2);

‘death or disability benefit’, in relation to a member of a complying superannuation fund, means:

(a) a benefit provided to a dependant of the member in the event of the death of the member;

(b) a benefit provided to the member in the event of the permanent disability of the member; or

(c) a benefit provided to the member, by way of income, during a period when the member is unable to perform the normal duties of the member’s employment, being a period not exceeding 2 years or, if the Commissioner approves in writing a longer period in relation to the fund, that period;

‘dependant’ has the same meaning as in the OSS Act;

‘eligible ADF’, in relation to a year of income, means a fund that is a complying ADF, or a non-complying ADF, in relation to the year of income;

‘eligible entity’, in relation to a year of income, means:

(a) a fund that is an eligible ADF in relation to the year of income;

(b) a fund that is an eligible superannuation fund in relation to the year of income; or

(c) a unit trust that is a PST in relation to the year of income;

‘eligible superannuation fund’, in relation to a year of income, means a fund that is a complying superannuation fund, or a non-complying superannuation fund, in relation to the year of income;

‘eligible termination payment’ has the same meaning as in Subdivision AA of Division 2 of Part III;

‘life assurance company’ has the same meaning as in Division 8 of Part III;

‘non-complying ADF’, in relation to a year of income, means a fund that, at all times during the year of income when the fund is in existence, is an approved deposit fund within the meaning of the OSS Act, but does not include a fund that is a complying ADF in relation to the year of income;

‘non-complying superannuation fund’, in relation to a year of income, means a fund that, at all times during the year of income when the fund is in existence, is:

(a) a provident, benefit, superannuation or retirement fund; or

(b) a superannuation fund within the meaning of the OSS Act;

but does not include a fund that is a complying superannuation fund in relation to the year of income;

‘normal assessable income’ means assessable income other than:

(a) special income; or

(b) taxable contributions;

‘OSS Act’ means the Occupational Superannuation Standards Act 1987;

‘OSS notice’ means a notice under the OSS Act;

‘pooled superannuation trust’ or ‘PST’, in relation to a year of income, means a unit trust in respect of which:

(a) the Insurance and Superannuation Commissioner has given a notice under section 15b of the OSS Act stating that the Insurance and Superannuation Commissioner is satisfied that the unit trust satisfied the pooled superannuation trust conditions in relation to the year of income; or

(b) the Insurance and Superannuation Commissioner has given a notice under section 15c of the OSS Act stating that the Insurance and Superannuation Commissioner is satisfied that the unit trust should be treated as if it had satisfied the pooled superannuation trust conditions in relation to the year of income;

‘registered organization’ has the same meaning as in Division 8a of Part III;

‘special component’:

(a) in relation to a complying ADF—has the meaning given by section 292;

(b) in relation to a complying superannuation fund—has the meaning given by section 284; or

(c) in relation to a PST —has the meaning given by section 298;

‘special income’ has the meaning given by section 273;

‘specified roll-over amount’, in relation to an eligible entity, means so much of an amount paid to the eligible entity as is required, by the operation of section 27d in relation to:

(a) an eligible termination payment that comes within paragraph (a) or (aa) of the definition of ‘eligible termination payment’ in subsection 27a (1); or

(b) an eligible termination payment made from a fund that is a constitutionally protected fund in relation to the year of income of the fund in which the payment is made;

to be regarded as being the application of some or all of an amount referred to in sub-subparagraph 27d (1) (b) (iii) (a);

‘standard component’:

(a) in relation to a complying ADF—has the meaning given by section 293;

(b) in relation to a complying superannuation fund—has the meaning given by section 285; or

(c) in relation to a PST—has the meaning given by section 299;

‘superannuation policy’ has the same meaning as in Division 8 of Part III;

‘taxable contribution’ has the meaning given by section 274;

‘unit trust’ has the same meaning as in Division 6c of Part III.

“(2) The Commissioner, in giving an approval for the purposes of paragraph (c) of the definition of ‘death or disability benefit’ in subsection (1), shall have regard to:

(a) any relevant approval given in relation to the fund concerned for the purposes of the definition of ‘superannuation fund’ in subsection 3 (1) of the OSS Act; and

(b) any other relevant circumstances.

“(3) A reference in this Part to a fund or unit trust shall, where appropriate, be read as a reference to the trustee of the fund or unit trust.

Trustees of funds not constituted as trusts

“268. Where, apart from this section, there is in relation to a fund no person who is a trustee of the fund for the purposes of this Part, the person, or each of the persons, who manages the fund shall be taken, for the purposes of this Part, to be the trustee, or a trustee, as the case requires, of the fund.

Issue, revocation etc. of OSS notices

“269. For the purposes of this Part, where an OSS notice is given in relation to a fund or unit trust in relation to a year of income:

(a) the notice shall be deemed to have been given at the beginning of the year of income; and

(b) if:

(i) the notice is revoked; or

(ii) the decision to give the notice is set aside;

the notice shall be deemed never to have been given.

Part to apply to government funds etc.

“270. A reference in this Part to a fund or unit trust includes a reference to a fund or unit trust established by:

(a) a law of the Commonwealth or of a State or Territory; or

(b) a public authority constituted by or under a law of the Commonwealth or of a State or Territory.

Part has effect subject to the Constitution

“271. (1) It is the intention of the Parliament that if, but for this section, this Part would have the effect that a law imposing taxation would impose tax on property of any kind belonging to a State within the meaning of section 114 of the Constitution, this Part shall not have that effect.

“(2) For the purposes of this Part, a fund is a constitutionally protected fund in relation to a year of income if subsection (1) applies to the fund in relation to any tax in relation to the year of income.

Assumption to be made in calculating taxable income

“272. The taxable income of an eligible entity shall be calculated as if the trustee were a taxpayer and a resident.

Special income

“273. (1) This section applies to income derived in a year of income by a fund or unit trust (in this section called the ‘entity’) that is a complying superannuation fund, a complying ADF or a PST in relation to the year of income.

“(2) A dividend paid to the entity by a company that is a private company in relation to the year of income of the company in which the dividend was paid is special income of the entity unless the Commissioner is of the opinion that it would be reasonable not to treat the dividend as special income of the entity, having regard to:

(a) the paid-up value of the shares in that company that are assets of the entity;

(b) the cost to the entity of the shares on which the dividend was paid by the company;

(c) the rate of the dividend paid to the entity by the company on the shares in the company that are assets of the entity;

(d) whether the company has paid a dividend on other shares in the company and, if so, the rate of that dividend;

(e) whether any shares have been issued by the company to the entity in satisfaction of, or of a part of, a dividend paid by the company and, if so, the circumstances of the issue of those shares; and

(f) any other matters that the Commissioner considers relevant.

“(3) For the purposes of subsection (2), income that, in the opinion of the Commissioner, was derived by the entity indirectly from a dividend paid by a company, being a private company in relation to the year of income of the company in which the dividend was paid, shall be deemed to have been a dividend paid to the entity by the company.

“(4) Income (other than a dividend to which subsection (2) applies) derived by the entity from a transaction is special income of the entity if the parties to the transaction were not dealing with each other at arm’s length in relation to the transaction and that income is greater than the income that might have been expected to have been derived by the entity from the transaction if those parties had been dealing with each other at arm’s length in relation to the transaction.

“(5) A reference in subsection (4) to a transaction includes a reference to a series of transactions.

“Division 2—Taxable Contributions

Taxable contributions

“274. (1) Subject to this Division, the following amounts paid to an eligible entity (other than a PST) are taxable contributions:

(a) if the eligible entity is an eligible superannuation fund:

(i) an amount in respect of which a deduction is allowable, or would but for subsection 73b (20) be allowable, under section 82aac to the person making the payment;

(ii) a contribution made by a person (in this section called the ‘contributor’) to obtain superannuation benefits for the contributor or, in the event of the death of the contributor, for dependants of the contributor, but not including so much of such a contribution as is deemed by section 27d to have been expended in making a payment as mentioned in paragraph 27a (12) (a);

(iii) a contribution made by an exempt entity (within the meaning of Division 6c of Part III) for the purpose of making provision for superannuation benefits for, or for dependants of, a person;

(iv) a specified roll-over amount;

(b) if the eligible entity is an eligible ADF—a specified roll-over amount.

“(2) Contributions to which subparagraph (1) (a) (ii) applies that are made to a complying superannuation fund in a year of income are not taxable contributions to the extent to which they are contributions covered by a notice under subsection 82aat (1a) given to the trustee of the fund before the date on which the trustee lodges the return of income of the fund of the year of income.

“(3) Contributions to which subparagraph (1) (a) (ii) applies that are made to a complying superannuation fund in a year of income are not taxable contributions if a notice under subsection (4) has been given in relation to the contributor in relation to the year of income before the date on which the trustee lodges the return of income of the fund of the year of income.

“(4) An approved person may give a notice to the trustee of a complying superannuation fund stating that the approved person is satisfied that, apart from subsection 82aas (3), a person specified in the notice (who may be the approved person) would not be an eligible person (within the meaning of Subdivision AB of Division 3 of Part III) in relation to a year of income specified in the notice.

“(5) The notice under subsection (4):

(a) shall be in the prescribed form;

(b) shall be given in the prescribed manner; and

(c) is irrevocable.

Transfer of taxable contributions

“275. (1) Where:

(a) the whole or a part of a taxable contribution made to a complying superannuation fund or a complying ADF in a year of income of the fund (in this section called the ‘fund’s year of income’):

(i) is applied by the trustee of the fund in the purchase of a superannuation policy from a life assurance company or registered organization (in this subsection called the ‘transferee’); or

(ii) is applied by the trustee of the fund in the purchase of units in a PST (in this subsection also called the ‘transferee’); and

(b) the trustee of the fund, with the consent of the transferee, gives to the Commissioner a notice stating that this section is to apply to the whole or a specified part of so much of the contribution as was so applied;

the amount to which the notice relates shall be taken, for the purposes of this Act:

(c) to be included in the assessable income of the transferee of the year of income of the transferee in which the end of the fund’s year of income occurs; and

(d) not to be included in the assessable income of the fund of the fund’s year of income.

“(2) The notice under paragraph (1) (b):

(a) shall be in the prescribed form;

(b) shall be given in the prescribed manner;

(c) shall be given on or before the date of lodgment of the return of income of the fund for the fund’s year of income; and

(d) is irrevocable.

Contribution notices given after return lodgment date

“276. (1) Subject to this section, if:

(a) a notice under subsection 82aat (1a) in relation to a contribution made to a fund in a year of income (in this section called the ‘contribution year’) is given to the trustee of the fund in a later year of income (in this section called the ‘notice year’) and on or after the date specified in subsection 274 (2); and

(b) apart from this section, the assessable income of the fund of the contribution year would include an amount (in this section called the ‘clawback amount’) that would not have been included if the notice had been given to the trustee before that date;

the clawback amount is allowable as a deduction from the assessable income of the fund of the notice year.

“(2) In determining whether paragraph (1) (b) is satisfied, section 275 shall be disregarded.

“(3) If the Commissioner is satisfied, having regard to the matters specified in subsection (4), that it would be appropriate for the clawback amount not to be included in the assessable income of the fund of the contribution year:

(a) so much of the contribution referred to in paragraph (1) (a) as is equal to the clawback amount shall be taken for the purposes of this Part (other than this section) never to have been a taxable contribution; and

(b) the clawback amount is not allowable as a deduction under subsection (1).

“(4) The matters to which the Commissioner is to have regard are:

(a) whether the clawback amount exceeds the amount that would be the taxable income of the fund of the notice year apart from this section;

(b) the amount of the rebates (if any) allowable to the trustee of the fund under Part IIIaa in relation to the notice year; and

(c) such other matters as the Commissioner considers relevant.

“(5) This section applies only once in respect of a particular contribution or part of a contribution.

Contributions treated as assessable in determining deductions

“277. In determining the deductions allowable from the assessable income of an eligible entity (other than a PST), any amount to which subsection 274 (1) applies shall be treated as if it were assessable income of the eligible entity (whether or not it is a taxable contribution).

“Division 3—Complying Superannuation Funds

Liability to taxation

“278. (1) The trustee of a complying superannuation fund is liable to pay tax on the taxable income of the fund of the year of income.

“(2) Except as provided by Division 11a of Part III, the income of a complying superannuation fund of the year of income is not subject to tax except as provided by this Part.

Deduction for premiums for death or disability cover

“279. (1) Where, in a year of income, the trustee of a complying superannuation fund pays a premium for an insurance policy that is, in whole or in part, in respect of a current or contingent liability of the fund to provide death or disability benefits for members of the fund, so much of the premium as is attributable to the liability is allowable as a deduction in respect of the year of income.

“(2) Where:

(a) during the whole or a part of a year of income, a complying superannuation fund is subject to a current or contingent liability to provide death or disability benefits for members of the fund; and

(b) that liability, to some extent, is not covered by an insurance policy;

the lowest arm’s length premium for an insurance policy in respect of that liability, to the extent to which it is not so covered, is an allowable deduction in respect of the year of income.

“(3) A deduction is not allowable under this section unless the return of the fund of the year of income is accompanied by a certificate by an actuary, in the prescribed form, with respect to the operation of this section.

No deduction in respect of benefits

“280. No deduction is allowable from the assessable income of a complying superannuation fund in respect of benefits.

Assessable income to include taxable contributions

“281. Subject to section 275, the assessable income of a complying superannuation fund of a year of income includes taxable contributions made to the fund in the year of income.

Exclusion from assessable income of amounts that accrued before 1 July 1988

“282. The assessable income of a complying superannuation fund of a year of income shall not include so much of any amount derived in the year of income as accrued to the fund before 1 July 1988.

Exemption of income attributable to current pensions

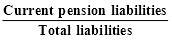

“283. (1) For each amount that, apart from this section, would be normal assessable income of a complying superannuation fund, the percentage (if any) calculated under subsection (2) is exempt from tax.

“(2) The percentage is calculated in accordance with the formula:

where:

Current pension liabilities is so much of the average liabilities of the fund of the year of income as, in the opinion of the Commissioner, represents liabilities to pay pensions during the year of income; and

Total liabilities is the average liabilities of the fund of the year of income.

“(3) An amount of income of a fund of a year of income is not exempt from tax under this section unless the return of the fund of the year of income is accompanied by a certificate by an actuary, in the prescribed form, with respect to the operation of this section.

Special component of taxable income

“284. The special component of the taxable income of a complying superannuation fund is the amount (if any) remaining after deducting from the special income:

(a) any allowable deductions that relate exclusively to the special income; and

(b) so much of any other allowable deductions as, in the opinion of the Commissioner, may appropriately be related to the special income.

Standard component of taxable income

“285. The standard component of the taxable income of a complying superannuation fund is the amount (if any) remaining after deducting the special component from the taxable income.

“Division 4—Non-complying Superannuation Funds

Liability to taxation

“286. (1) The trustee of a non-complying superannuation fund is liable to pay tax on the taxable income of the fund of the year of income.

“(2) Except as provided by Division 11a of Part III, the income of a non-complying superannuation fund of the year of income is not subject to tax except as provided by this Part.

No deduction in respect of benefits

“287. No deduction is allowable from the assessable income of a non-complying superannuation fund in respect of benefits.

Assessable income to include taxable contributions

“288. The assessable income of a non-complying superannuation fund of a year of income includes taxable contributions made to the fund in the year of income.

“Division 5—Complying Approved Deposit Funds

Liability to taxation

“289. (1) The trustee of a complying ADF is liable to pay tax on the taxable income of the fund of the year of income.

“(2) Except as provided by Division 11a of Part III, the income of a complying ADF of the year of income is not subject to tax except as provided by this Part.

Assessable income to include taxable contributions

“290. Subject to section 275, the assessable income of a complying ADF of a year of income includes taxable contributions made to the fund in the year of income.

Exclusion from assessable income of amounts that accrued before 1 July 1988

“291. The assessable income of a complying ADF of a year of income shall not include so much of any amount derived in the year of income as accrued to the fund before 1 July 1988.

Special component of taxable income

“292. The special component of the taxable income of a complying ADF is the amount (if any) remaining after deducting from the special income:

(a) any allowable deductions that relate exclusively to the special income; and

(b) so much of any other allowable deductions as, in the opinion of the Commissioner, may appropriately be related to the special income.

Standard component of taxable income

“293. The standard component of the taxable income of a complying ADF is the amount (if any) remaining after deducting the special component from the taxable income.

“Division 6—Non-complying Approved Deposit Funds

Liability to taxation

“294. (1) The trustee of a non-complying ADF is liable to pay tax on the taxable income of the fund of the year of income.

“(2) Except as provided by Division 11a of Part III, the income of a non-complying ADF of the year of income is not subject to tax except as provided by this Part.

Assessable income to include taxable contributions

“295. The assessable income of a non-complying ADF of a year of income includes taxable contributions made to the fund in the year of income.

“Division 7—Pooled Superannuation Trusts

Liability to taxation

“296. (1) The trustee of a PST is liable to pay tax on the taxable income of the trust of the year of income.

“(2) Except as provided by Division 11a of Part III, the income of a PST of the year of income is not subject to tax except as provided by this Part.

“(3) Subsection (2) does not affect any liability arising under paragraph 26 (b) or under Division 6 of Part III, in relation to a year of income, in relation to a unitholder that is not a complying ADF, a complying superannuation fund or a PST in relation to that year of income.

Exclusion from assessable income of amounts that accrued before 1 July 1988

“297. The assessable income of a PST of a year of income shall not include so much of any amount derived in the year of income as accrued to the trust before 1 July 1988.

Special component of taxable income

“298. The special component of the taxable income of a PST is the amount (if any) remaining after deducting from the special income:

(a) any allowable deductions that relate exclusively to the special income; and

(b) so much of any other allowable deductions as, in the opinion of the Commissioner, may appropriately be related to the special income.

Standard component of taxable income

“299. The standard component of the taxable income of a PST is the amount (if any) remaining after deducting the special component from the taxable income.

“Division 8—Miscellaneous

Rebates and provisional tax

“300. (1) The trustee of a fund that is an eligible superannuation fund or an eligible ADF in relation to a year of income:

(a) is entitled to a rebate as provided by section 160ab;

(b) is not entitled to a rebate as provided by section 46 or 46a; and

(c) except where the fund is a non-complying superannuation fund, or a non-complying ADF, in relation to the year of income, is not

liable to pay provisional tax under Division 3 of Part VI in respect of income of the fund.

“(2) The trustee of a PST:

(a) is entitled to a rebate as provided by section 160ab;

(b) is not entitled to a rebate as provided by section 46 or 46a; and

(c) is not liable to pay provisional tax under Division 3 of Part VI in respect of income of the PST.

Amendment of assessments

“301. Where:

(a) an assessment has been made in relation to a year of income; and

(b) a provision of this Part that is relevant to the assessment is dependent on a circumstance that occurs or may occur after the end of the year of income;

nothing in section 170 prevents the amendment of the assessment at any time for the purpose of giving effect to this Act in relation to the occurrence of that circumstance after the end of the year of income.”.

Other amendments relating to superannuation business and related business

10. The Principal Act is amended as set out in Schedule 1.

Application—Division 16j of Part III

11. (1) The amendment made by section 6 applies in relation to a cancellation of shares:

(a) in the case of a cancellation by resolution that is subject to confirmation by a court—where the order of the court confirming the resolution is or was made after 11 August 1988 (whether or not the cancellation has effect from an earlier date); and

(b) in any other case—after 11 August 1988.

(2) Where:

(a) if paragraph (1) (a) applies—the order of the court was made before 1 December 1988; or

(b) if paragraph (1) (b) applies—the cancellation of the shares took place before 1 December 1988;

the following provisions have effect:

(c) if the adjusted market value, referred to in subsection 159gzzzf (1) of the amended Act, in relation to the shares exceeds the consideration in respect of the acquisition of the shares then, for the purposes of the application of the amended Act (other than Part IIIa or section 159gzzzh) in relation to the cancellation:

(i) paragraph 159gzzzf (1) (c) of the amended Act has effect as if the reference in that paragraph to the adjusted market value of the shares were instead a reference to the amount of the consideration; and

(ii) paragraph 159gzzzf (1) (d) of the amended Act has effect as if the reference in that paragraph to an amount being increased so that it equals the adjusted market value of the shares were instead a reference to that amount being increased or decreased so that it equals the amount of the consideration;

(d) if the adjusted market value, referred to in subsection 159gzzzf (1) of the amended Act, in relation to the shares exceeds their indexed cost base to the subsidiary concerned or, where the shares were cancelled within 12 months of their acquisition, their cost base then, for the purposes of the application of Part IIIa of the amended Act in relation to the cancellation:

(i) paragraph 159gzzzf (1) (c) of the amended Act has effect as if the reference in that paragraph to the adjusted market value of the shares were instead a reference to the indexed cost base or cost base, as the case may be; and

(ii) paragraph 159gzzzf (1) (d) of the amended Act has effect as if the reference in that paragraph to an amount being increased so that it equals the adjusted market value of the shares were instead a reference to that amount being increased or decreased so that it equals the indexed cost base or the cost base, as the case may be.

(3) Expressions used in paragraph (2) (d) that are also used in Part IIIa of the amended Act have the same respective meanings in that paragraph as in that Part.

(4) In this section:

“amended Act” means the Principal Act as amended by this Act.

Application of superannuation and related amendments 12. (1) In this section:

“1 July 1988 year” means the year of income in which 1 July 1988 occurred.

(2) The following amendments of the Principal Act made by this Act apply to assessments in respect of income of the 1 July 1988 year and of all subsequent years of income:

(a) the amendment made by section 9;

(b) the amendments repealing paragraph 23 (jaa), sections 23fc and 23fd, and Division 9b of Part III, of the Principal Act;

(c) the amendment of section 160aab of the Principal Act.

(3) The amendments of sections 102m, 110, 121g, 121h and 124za of the Principal Act made by this Act apply in relation to a fund in relation to the 1 July 1988 year of the fund and in relation to all subsequent years of income.

(4) The amendment of the definition of “salary expenditure” in subsection 73b (1) of the Principal Act, and the amendments of Subdivision AA of Division 3 of Part III of the Principal Act, made by this Act:

(a) insofar as the amendments relate to contributions—apply in relation to contributions made on or after 1 July 1988; and

(b) insofar as they relate to amounts set apart—apply to amounts set apart after 30 November 1988.

(5) The amendments of Subdivision AB of Division 3 of Part III of the Principal Act made by this Act apply in relation to contributions made on or after 1 July 1988.

(6) The following amendments of the Principal Act made by this Act apply in relation to dividends paid on or after 1 July 1988:

(a) the amendments of sections 160aqt, 160aqu and 221yda;

(b) the amendment inserting section 160aqya.

Transitional—section 73a

13. Where, immediately before the commencement of this section, a body was, because of an approval for the purposes of section 73a of the Principal Act, an approved research institute within the meaning of that section of that Act, that body continues to be an approved research institute for the purposes of section 73a of the Principal Act as amended by this Act until that approval is withdrawn by any person or body empowered to give approvals for the purposes of that section of the Principal Act as so amended.

Transitional—superannuation and related amendments

14. (1) In this section:

“amended Act” means the Principal Act as amended by this Act;

“income” includes assessable income;

“1 July 1988 year” means the year of income in which 1 July 1988 occurred.

(2) Where:

(a) a taxpayer is the trustee of an eligible entity, within the meaning of Part IX of the amended Act, in relation to the taxpayer’s 1 July 1988 year; and

(b) any part of the taxpayer’s 1 July 1988 year occurred before 1 July 1988;

the following provisions have effect:

(c) subsection 160aab (5a) and Part IX of the amended Act do not apply to income derived by the entity before 1 July 1988;

(d) notwithstanding the repeal of paragraph 23 (jaa), sections 23fc and 23fd, Division 9b of Part III and subsection 160aab (5a) of the Principal Act, those provisions of the Principal Act continue to apply to the taxpayer’s 1 July 1988 year in relation to income

derived by the entity before 1 July 1988 as if they had not been repealed;

(e) for the purposes of Division 9b of Part III of the Principal Act as applied by paragraph (d), in determining whether section 121cc, 121da, 121daa or 121dab of the Principal Act applied in relation to the entity in relation to the 1 July 1988 year, so much of the year of income as occurred after 30 June 1988 shall be disregarded;

(f) where a particular amount (in this paragraph called the “deductible amount”):

(i) is allowable, or would be allowable but for paragraph (c), as a deduction in calculating the taxable income of the entity of the 1 July 1988 year in accordance with Part IX of the amended Act; and

(ii) if Division 9b of Part III of the Principal Act had not been repealed by this Act, would have been allowable as a deduction in calculating an amount (if any) upon which the trustee of the entity is liable to be assessed under that Division in respect of the 1 July 1988 year;

the Commissioner may, to such extent as the Commissioner considers reasonable, apportion the deductible amount so that:

(iii) a part of the deductible amount is allowable as a deduction in calculating the taxable income of the entity of the 1 July 1988 year in accordance with Part IX of the amended Act; and

(iv) the remainder of the deductible amount is allowable as a deduction in calculating an amount (if any) upon which the trustee of the entity is liable to be assessed under Division 9b of Part III of the Principal Act, in its application by virtue of this section, in respect of the 1 July 1988 year;

(g) where a particular amount (in this paragraph called the “deductible amount”):

(i) is allowable, or would be allowable but for paragraph (c), as a deduction in calculating the taxable income of the entity of the 1 July 1988 year in accordance with Part IX; and

(ii) if the amendments made by this Act had not been made, would not have been allowable as a deduction to the entity in respect of the 1 July 1988 year;

only so much of the deductible amount as the Commissioner considers reasonable is allowable as a deduction in calculating the taxable income of the entity of the 1 July 1988 year in accordance with Part IX of the amended Act;

(h) a reference in section 82aas of the Principal Act to a fund to which paragraph 23 (jaa) applies in relation to a year of income includes a reference to a fund to which that paragraph, in its application by virtue of this section, applies in relation to the 1 July 1988 year;

(j) notwithstanding the amendment of section 124za of the Principal Act made by this Act, that section, insofar as it relates to paragraph 23 (jaa) of the Principal Act, continues to apply in relation to a fund to which that paragraph, in its application by virtue of this section, applies in relation to the 1 July 1988 year, as if that amendment had not been made;

(k) notwithstanding the amendments of sections 121g and 121h of the Principal Act made by this Act, those sections continue to apply in relation to the entity in relation to the 1 July 1988 year, as if those amendments had not been made;

(m) a reference in section 121F of the amended Act to paragraph 23 (jaa) of the Principal Act includes a reference to that paragraph in its application, by virtue of this section, in relation to the 1 July 1988 year;

(n) a reference in section 121g of the Principal Act to section 121cc of the Principal Act includes a reference to that last-mentioned section in its application, by virtue of this section, in relation to the 1 July 1988 year;

(o) a reference in section 121h of the Principal Act to section 121db of the Principal Act includes a reference to that last-mentioned section in its application, by virtue of this section, in relation to the 1 July 1988 year;

(p) a reference in section 27a of the amended Act or section 82aac of the Principal Act to a fund to which section 121cc, 121 da or 121 dab of the Principal Act applies, or has applied, in relation to a year of income includes a reference to a fund to which the section concerned, in its application by virtue of this section, applies or has applied in relation to the 1 July 1988 year;

(q) a reference in section 160aqu of the Principal Act to a trustee of a fund who is liable to be assessed under section 121cc, 121da, 121daa or 121 dab of the Principal Act includes a reference to the trustee of a fund who is liable to be assessed under the section concerned in its application, by virtue of this section, to the 1 July 1988 year.

(3) In determining, for the purposes of subsection (2), whether income was derived by an entity before 1 July 1988, income that:

(a) is included in the assessable income of the entity under subsection 92 (1) or Division 6 of Part III of the amended Act; or

(b) is derived by the entity during, but not at a particular time during, a year of income;

shall be taken to have been derived by the entity at such time, or at such times and in such proportions, as the Commissioner considers reasonable having regard to:

(c) where paragraph (a) applies in respect of a partnership or a trust estate—the time, or the times, when income was derived by the

partnership or by the trustee of the trust estate, as the case may be; and

(d) in any case—any relevant matters.

(4) If, apart from the amendments made by this Act, a fund would have been a fund to which paragraph 23 (jaa) of the Principal Act applied in relation to the 1 July 1988 year or a later year of income that is earlier than the year of income commencing on 1 July 1990, the fund shall be taken, for the purposes of the amended Act, to be a complying superannuation fund (within the meaning of Part IX of the amended Act) in relation to the year of income concerned.

Amendment of assessments

15. Nothing in section 170 of the Principal Act prevents the amendment of an assessment made before the commencement of this section for the purpose of giving effect to this Act.

PART III —AMENDMENT OF OTHER ACTS IN CONNECTION WITH THE AMENDMENTS OF THE INCOME TAX ASSESSMENT ACT 1936 RELATING TO SUPERANNUATION BUSINESS AND RELATED BUSINESS

Amendment of other Acts

16. The Acts specified in Schedule 2 are amended as set out in that Schedule.

Application of amendment of the Fringe Benefits Tax Assessment Act 1986

17. The amendment made by this Act to the definition of “superannuation fund” in subsection 136 (1) of the Fringe Benefits Tax Assessment Act 1986 applies in relation to a fund in relation to the year of income of the fund in which 1 July 1988 occurred and in relation to all subsequent years of income.

Application of amendments of the Superannuation Act 1976

18. The amendments of the Superannuation Act 1976 made by this Act apply in relation to the year of income of the Fund in which 1 July 1988 occurred and in relation to all subsequent years of income.

–––––––––––

SCHEDULE 1 Section 10

OTHER AMENDMENTS OF THE INCOME TAX ASSESSMENT ACT 1936 RELATING TO SUPERANNUATION BUSINESS AND RELATED BUSINESS

Subsection 6 (1) (definition of “superannuation fund”):

Omit the definition, substitute the following definition:

“‘superannuation fund’ (except in Part IX) includes an eligible superannuation fund within the meaning of Part IX;”.

Section 6e:

Repeal the section.

Paragraph 23 (jaa):

Omit the paragraph.

Sections 23fc and 23fd:

Repeal the sections.

Subsection 26afb (1) (definition of “exempt fund”):

Omit the definition, substitute the following definition:

“ ‘exempt fund’ means:

(a) a fund to which section 23fc, as in force at any time before the commencement of section 1 of the Taxation Laws Amendment Act (No. 2) 1989, has applied in relation to any year of income; or

(b) a fund that is or has been a complying superannuation fund, within the meaning of Part IX, in relation to any year of income;”.

Subsection 27a (1) (subparagraph (a) (iii), and sub-subparagraph (aa) (iv) (c), of the definition of “eligible termination payment”):

Omit “applies, or has applied,”, substitute “, as in force at any time before the commencement of section 1 of the Taxation Laws Amendment Act (No. 2) 1989, has applied”.

Subsection 27a (1) (definition of “eligible termination payment”):

After subparagraph (a) (iii), insert the following subparagraph:

“(iiia) from a fund that is or has been a non-complying superannuation fund, within the meaning of Part IX, in relation to any year of income;”.

Subsection 27a (1) (sub-subparagraph (aa) (iv) (b) of the definition of “eligible termination payment”):

Omit “or” from the end of the sub-subparagraph.

SCHEDULE 1—continued

Subsection 27a (1) (subparagraph (aa) (iv) of the definition of “eligible termination payment”):

Add at the end the following word and sub-subparagraph:

“or (d) from a fund that is or has been a non-complying superannuation fund, within the meaning of Part IX, in relation to any year of income;”.

Subsection 27a (1) (definition of “superannuation fund”):

Before subparagraph (a) (i), insert the following subparagraphs:

“(ia) a fund to which paragraph 23 (jb) applies, or has applied, in relation to any year of income;

(iaa) a fund that is or has been a complying superannuation fund, within the meaning of Part IX, in relation to any year of income;”.

Subsection 27a (1) (subparagraph (a) (i) of the definition of “superannuation fund”):

Omit the subparagraph, substitute the following subparagraph:

“(i) a fund to which paragraph 23 (jaa) or section 23fc, 121cc or 121dab, as in force at any time before the commencement of section 1 of the Taxation Laws Amendment Act (No. 2) 1989, has applied in relation to any year of income;”.

Subsection 73b (1) (subparagraph (c) (i) of the definition of “salary expenditure”):

Omit “(other than expenditure by way of contributions to superannuation funds or expenditure that would, apart from subsection 82aac (2) or (3) or section 82aae, be allowable as a deduction to the company under section 82aac)”.

Subsections 82aaa (2) and (3):

Omit the subsections, substitute the following subsection:

“(2) For the purposes of this Subdivision, a director of a company shall be taken to be employed by the company.”.

Subsection 82aaa (5):

Omit the subsection.

Sections 82aab to 82aap (inclusive):

Repeal the sections, substitute the following section:

Deduction for contributions to eligible superannuation fund for employees

“82aac. Where:

(a) a taxpayer makes a contribution to a fund for the purpose of making provision for superannuation benefits for, or for dependants of, an eligible employee; and

SCHEDULE 1—continued

(b) the fund is an eligible superannuation fund, within the meaning of Part IX, in relation to the year of income of the fund in which the contribution is made;

the amount of the contribution is an allowable deduction in respect of the year of income of the taxpayer in which the contribution is made.”.

Section 82aar:

Omit “set apart or paid by a taxpayer as or”, substitute “paid by a taxpayer as a contribution”.

Section 82aar:

Add at the end the following subsection:

“(2) A deduction is not allowable under this Act in respect of an amount set apart by a taxpayer as a fund for the purpose of making provision for superannuation benefits for, or for dependants of, an employee or employees.”.

Subsection 82aas (1) (definition of “superannuation contributions”):

Omit “an eligible”, substitute “a complying”.

Subsection 82aas (1) (definition of “eligible superannuation fund”):

Omit the definition.

Subsection 82aas (1):

Insert the following definition:

“ ‘complying superannuation fund’ means a fund that is a complying superannuation fund, within the meaning of Part IX, in relation to the year of income;”.

Paragraph 82aat (1) (b):

Omit “section 23fc applies in relation to the fund”, substitute “the fund is a complying superannuation fund, within the meaning of Part IX,”.

After subsection 82aat (1):

Insert the following subsections:

“(1a) Subsection (1) does not apply to a contribution to the extent to which the contribution is specified in a notice under subsection (1b).

“(1b) A taxpayer may, at the time of making a contribution to a fund or at any later time, give to the trustee of the fund a notice in relation to the whole or a specified part of the contribution.

“(1c) The notice:

(a) shall be in the prescribed form;

(b) shall be given in the prescribed manner; and

SCHEDULE 1—continued

(c) is irrevocable.

“(1d) Nothing in section 170 prevents the amendment of an assessment at any time for the purpose of giving effect to subsection (1a) of this section.”.

Subsection 82aat (2):

Omit “$1,500”, substitute “$3,000”.

Section 102m (paragraph (b) of the definition of “exempt entity”):

Omit the paragraph, substitute the following paragraph:

“(b) the trustee of:

(i) an exempt life assurance fund;

(ii) a fund to which paragraph 23 (j) applies; or

(iii) a complying superannuation fund, a complying ADF, or a PST, within the meaning of Part IX;”.

Section 110 (definition of “exempt superannuation fund”):

Omit the definition, substitute the following definition:

“ ‘exempt superannuation fund’ means a fund that is a complying superannuation fund, within the meaning of Part IX, in relation to the year of income;”.

Division 9b of Part III:

Repeal the Division.

Subsection 121f (1) (paragraph (a) of the definition of “relevant exempting provision”):

Omit “, (jaa)”.

Subsection 121f (1) (paragraph (bb) of the definition of “relevant exempting provision”):

Omit the paragraph, substitute the following paragraph:

“(bb) paragraph 23 (jaa) or section 23fc or 23fd, as in force at any time before the commencement of section 1 of the Taxation Laws Amendment Act (No. 2) 1989”.

Paragraphs 121g (4) (c), (5) (c) and (6) (c):

Add at the end “and”.

Paragraphs 121g (4) (d), (5) (d) and (6) (d):

Omit the paragraphs.

Subsection 121h (3):

Omit the subsection.

Subsection 124za (1) (definition of “exempt body”):

Omit the definition, substitute the following definition:

SCHEDULE 1—continued

“ ‘exempt body’ means a body, association or fund to which paragraph 23 (d), (e), (ea), (eb), (ec), (f) (g), (h), (i), (j) or (k) applies.”.

Subsection 160aab (5a):

Omit the subsection, substitute the following subsection:

“(5a) A taxpayer being the trustee of an eligible entity within the meaning of Part IX is entitled in the taxpayer’s assessment in respect of income of a year of income to a rebate of tax equal to 29% of any eligible section 26ah amount included in the taxpayer’s assessable income of the year of income.”.

Section 160aqt:

Add at the end the following subsection:

“(4) For the purposes of subsection (1), in determining whether a dividend is exempt income, section 283 shall be disregarded.”.

Subparagraph 160aqu (b) (ii):

Omit the subparagraph, substitute the following subparagraph:

“(ii) a trustee other than the trustee of an eligible entity within the meaning of Part IX;”.

Section 160aqu:

Add at the end the following subsection:

“(2) For the purposes of subsection (1), in determining the amount included under section 160aqt in the assessable income of a shareholder, section 283 shall be disregarded.”.

After section 160aqy:

Insert the following section:

Franking rebate for trustees of superannuation funds, ADPs and PSTs

“160aqya. (1) Where:

(a) a trust amount is included in the assessable income of a taxpayer of a year of income;

(b) the taxpayer is the trustee of an eligible entity within the meaning of Part IX; and

(c) there is a flow-on franking amount in relation to the trust amount;

the taxpayer is entitled to a rebate of tax in the taxpayer’s assessment in respect of income of the year of income of an amount equal to the potential rebate amount in relation to the trust amount.

“(2) Where:

(a) a partnership amount is included in, or allowable as a deduction from, the assessable income of a taxpayer of a year of income;

(b) the taxpayer is a trustee of an eligible entity within the meaning of Part IX; and

SCHEDULE 1—continued

(c) there is a flow-on franking amount in relation to the partnership amount;

the taxpayer is entitled to a rebate of tax in the taxpayer’s assessment in respect of income of the year of income of an amount equal to the potential rebate amount in relation to the partnership amount.”.

Paragraph 221 yd a (1) (da) and subparagraph 221 yda (2) (a) (ii):

Insert “, 160aqya” after “160aqy”.

––––––––––––

SCHEDULE 2 Section 16

AMENDMENT OF OTHER ACTS IN CONNECTION WITH THE AMENDMENTS OF THE INCOME TAX ASSESSMENT ACT 1936 RELATING TO SUPERANNUATION BUSINESS AND RELATED BUSINESS

Fringe Benefits Tax Assessment Act 1986

Subsection 136 (1) (subparagraph (k) (i) of the definition of “fringe benefit”):

Insert “, (iiia)” after “(iii)”.

Subsection 136 (1) (subparagraph (k) (ii) of the definition of “fringe benefit”):

Insert “or (iiia)” after “(a) (iii)”.

Subsection 136 (1) (paragraph (a) of the definition of “superannuation fund”):

Omit the paragraph, substitute the following paragraph:

“(a) an eligible superannuation fund within the meaning of Part IX of the Income Tax Assessment Act 1936; or”.

Occupational Superannuation Standards Act 1987

Title:

Omit “and approved deposit funds”, substitute “, approved deposit funds and pooled superannuation trusts”.

Subsection 3 (1) (definitions of “protected document” and “protected information”):

Omit “or approved deposit fund”, substitute “, approved deposit fund or pooled superannuation trust”.

SCHEDULE 2—continued

Subsection 3(1) (definition of “year of income”):

Insert “or unit trust” after “fund” (wherever occurring).

Subsection 3 (1) (definition of “reviewable decision”):

Omit the definition, substitute the following definition:

“ ‘reviewable decision’ means:

(a) a decision of the Commissioner to give a notice in relation to a fund under section 12, 13, 14 or 15 stating that the Commissioner is not satisfied that the fund complied with the superannuation fund conditions or the approved deposit fund conditions, as the case may be, in relation to a year of income; or

(b) a decision of the Commissioner to give a notice in relation to a unit trust under section 15b or 15C stating that the Commissioner is not satisfied that the unit trust complied with the pooled superannuation trust conditions in relation to a year of income;”.

Subsection 3 (1) (definition of “fund affected by a reviewable decision”):

Omit the definition.

Subsection 3 (1):

Insert the following definitions:

“ ‘fund or unit trust affected by a reviewable decision’, in relation to a reviewable decision, means the fund or unit trust in relation to which the decision was made;

‘pooled superannuation trust’ means a unit trust that, under the regulations, is a unit trust to which this definition applies;

‘trustee’, in relation to a fund, has the same meaning as in Part IX of the Tax Act;

‘unit trust’ has the same meaning as in Part IX of the Tax Act;”.

After section 3:

Insert the following section:

Crown to be bound

“3a. (1) This Act binds the Crown in right of the Commonwealth, of each of the States, of the Northern Territory and of Norfolk Island.

“(2) Nothing in this Act renders the Crown in right of the Commonwealth, of a State, of the Northern Territory or of Norfolk Island liable to be prosecuted for an offence.”.

Section 4:

Add at the end the following subsection:

SCHEDULE 2—continued

“(5) Where any of the first regulations made for the purposes of the definition of ‘pooled superannuation trust’ in subsection 3 (1) or for the purposes of subsection 8a (1) specify a day (not being a day before 1 July 1988) before the date of notification of the regulations in the Gazette as the day on which specified regulations are to be taken to have come into operation, those regulations shall be taken to have come into operation on the day so specified.”.

After section 6:

Insert the following section:

Satisfaction of pooled superannuation trust conditions

“6a. A reference in this Act to a unit trust satisfying the pooled superannuation trust conditions in relation to a year of income is a reference to the following conditions being satisfied in relation to the unit trust in relation to the year of income:

(a) the unit trust was a pooled superannuation trust:

(i) if part of the year of income occurred before 1 July 1988— at all times during so much of the year of income as occurred on or after 1 July 1988 when the unit trust was in existence; or

(ii) in any other case—at all times during the year of income when the unit trust was in existence;

(b) at all times during the year of income when the unit trust was in existence and there were in force regulations for the purposes of subsection 8a (1) prescribing standards applicable to the unit trust, the unit trust complied with those standards;

(c) the trustees of the unit trust complied with:

(i) any requirement made in relation to the unit trust during the year of income by or under subsection 10 (1aa) or section 11; and

(ii) any requirement made in relation to the unit trust in relation to the year of income under subsection 10 (2).”.

Heading to Part II:

Omit “AND APPROVED DEPOSIT FUNDS”, substitute “, APPROVED DEPOSIT FUNDS AND POOLED SUPERANNUATION TRUSTS”.

Subsection 7 (3):

Omit “section 23fc, 121cc or 121d of”.

Subsection 8 (3):

Omit “section 23fd or 121daaa of”.

SCHEDULE 2—continued

After section 8:

Insert the following section:

Operating standards for pooled superannuation trusts

“8a. (1) The regulations may prescribe standards applicable to the operation of pooled superannuation trusts.

“(2) The standards that may be prescribed include, but are not limited to, standards relating to the following matters:

(a) the ownership and disposal of units in pooled superannuation trusts;

(b) the investment of assets of pooled superannuation trusts;

(c) the persons who may be trustees of pooled superannuation trusts;

(d) the number of trustees, and the composition of boards or committees of trustees, of pooled superannuation trusts;

(e) the keeping and retention of records in relation to pooled superannuation trusts;

(f) the financial and actuarial reports to be prepared in relation to pooled superannuation trusts;

(g) the disclosure of information to unitholders in pooled superannuation trusts;

(h) the matters required, permitted or not permitted to be included, from time to time, in the trust deeds of pooled superannuation trusts.

“(3) Nothing in the Tax Act limits the standards that may be prescribed.”.

After subsection 10 (1):

Insert the following subsection:

“(1aa) The trustees of a pooled superannuation trust established after the commencement of this subsection shall, within the prescribed period after establishment, give to the Commissioner the prescribed information.”.

Subsection 10 (1a):

Add at the end “or (1aa)”.

Subsections 10 (2) and 11 (2):

Omit “or an approved deposit fund”, substitute “, an approved deposit fund or a pooled superannuation trust”.

Subsection 11 (2):

Add at the end “or trust”.

Subsections 11 (3) and (4):

Insert “or trust” after “fund” (wherever occurring).

SCHEDULE 2—continued

After section 15a:

Insert the following sections:

Notices as to satisfaction of the pooled superannuation trust conditions

“15b. (1) Where:

(a) after the end of a year of income of a unit trust, the trustees of the unit trust give to the Commissioner, in relation to the year of income:

(i) a return, in a form approved by the Commissioner, in writing, for the purposes of this section, providing such information relating to the unit trust and to the unit trust’s satisfaction of the pooled superannuation trust conditions during the year of income as is required by the form to be provided;

(ii) a certificate by the trustees of the unit trust, in the prescribed form;

(iii) a certificate by an approved auditor, in the prescribed form; and

(iv) the prescribed application fee; and

(b) either:

(i) the return, certificates and fee referred to in paragraph (a) are received by the Commissioner on or before the day specified in the form of return as the day by which the return is to be given to the Commissioner; or

(ii) the return, certificates and fee referred to in that paragraph are received by the Commissioner, but are not all received until after the day referred to in subparagraph (i), and any prescribed late lodgment fee has also been received by the Commissioner;

subsection (3) applies in relation to the unit trust in relation to the year of income.

“(2) A certificate referred to in subparagraph (1) (a) (ii) or (iii) may be endorsed on a return referred to in subparagraph (1) (a) (i).

“(3) Where this subsection applies in relation to a unit trust in relation to a year of income, the Commissioner shall, subject to subsection (6), give notice in writing to the trustees of the unit trust stating whether the Commissioner is satisfied that the unit trust satisfied the pooled superannuation trust conditions in relation to the year of income, having regard to:

(a) the return and certificates given under subsection (1); and

(b) any other information available to the Commissioner.

“(4) If:

SCHEDULE 2—continued

(a) the Commissioner has, under this section or section 15c, given a notice to the trustees of a unit trust stating that the Commissioner is not satisfied that the unit trust satisfied the pooled superannuation trust conditions in relation to a year of income of the unit trust; and

(b) the Commissioner, after considering information that was not previously considered by the Commissioner, becomes satisfied that the unit trust so satisfied the pooled superannuation trust conditions;

the Commissioner shall give notice in writing to the trustees of the unit trust revoking the notice referred to in paragraph (a) and stating that the Commissioner is satisfied that the unit trust satisfied the pooled superannuation trust conditions in relation to the year of income.

“(5) If:

(a) the Commissioner has, under this section, given a notice to the trustees of a unit trust stating that the Commissioner is satisfied that the unit trust satisfied the pooled superannuation trust conditions in relation to a year of income of the unit trust; and

(b) the Commissioner, after considering information that was not previously considered by the Commissioner, ceases to be satisfied that the unit trust so satisfied the pooled superannuation trust conditions;

the Commissioner shall, subject to subsection (6), give notice in writing to the trustees of the unit trust revoking the notice referred to in paragraph (a) and stating that the Commissioner is not satisfied that the unit trust satisfied the pooled superannuation trust conditions in relation to the year of income.

“(6) Where:

(a) but for this subsection, the Commissioner would be required to give a notice stating that the Commissioner is not satisfied that a unit trust satisfied the pooled superannuation trust conditions in relation to a year of income; and

(b) the Commissioner decides to give a notice under subsection 15c (1) stating that the Commissioner is satisfied that the unit trust should be treated as if it had satisfied the pooled superannuation trust conditions in relation to the year of income;

the Commissioner is not required to give the notice referred to in paragraph (a).

“(7) A notice under this section stating that the Commissioner is not satisfied that a unit trust satisfied the pooled superannuation trust conditions in relation to a year of income shall set out the reasons why the Commissioner is not so satisfied.

“(8) The Commissioner shall advise the Commissioner of Taxation of particulars of all notices given under this section.

SCHEDULE 2—continued

Discretion to treat unit trusts as satisfying the pooled superannuation trust conditions

“15c. (1) Where, in relation to a unit trust in relation to a year of income of the unit trust:

(a) the trustees of the unit trust have not given the Commissioner the return, certificates and fee or fees referred to in subsection 15b (1), or the trustees of the unit trust have given the Commissioner the return, certificates and fee or fees referred to in that subsection but the Commissioner is not satisfied that the unit trust satisfied the pooled superannuation trust conditions; and

(b) the trustees of the unit trust satisfy the Commissioner that, because of special circumstances that existed in relation to the unit trust during the year of income, it would be reasonable for the unit trust to be treated as if it had satisfied the pooled superannuation trust conditions;

the Commissioner shall give notice in writing to the trustees of the unit trust stating that the Commissioner is satisfied that the unit trust should be treated as if it had satisfied the pooled superannuation trust conditions in relation to the year of income.

“(2) If:

(a) the Commissioner has given a notice under subsection (1) in relation to a unit trust in relation to a year of income of the unit trust; and

(b) the Commissioner, after considering information that was not previously considered by the Commissioner, becomes satisfied that the unit trust should not be treated as if it had satisfied the pooled superannuation trust conditions in relation to the year of income;

the Commissioner shall give notice in writing to the trustees of the unit trust revoking the notice referred to in paragraph (a) and stating that the Commissioner is not satisfied that the unit trust satisfied the pooled superannuation trust conditions in relation to the year of income.

“(3) A notice under this section stating that the Commissioner is not satisfied that a unit trust satisfied the pooled superannuation trust conditions in relation to a year of income shall set out the reasons why the Commissioner is not so satisfied.

“(4) The Commissioner shall advise the Commissioner of Taxation of particulars of all notices given under this section.”.

Subsection 16 (1):

Insert “or unit trust” after “fund” (wherever occurring).

Subsections 17 (1) and (2):

Insert “or unit trust” after “fund”.

SCHEDULE 2—continued

Subsection 19 (1):

Omit “and approved deposit funds”, substitute “, approved deposit funds and pooled superannuation trusts”.

Subsection 19 (2):

Omit “or approved deposit fund”, substitute “, approved deposit fund or pooled superannuation trust”.

Subsection 19 (2):

Add at the end “or trust, as the case requires”.

Superannuation Act 1976

Subsection 42 (5):

Omit “Income”, substitute “Subject to subsection (5c), income”.

Subsection 42 (5a):

Omit “subsection (5b)”, substitute “subsections (5b) and (5c)”.

After subsection 42 (5b):

Insert the following subsection:

“(5c) Subsections (5) and (5a) do not apply to taxation the liability to which arises under the Income Tax Assessment Act 1936”.

Taxation Administration Act 1953

Subsection 8w (1a):

Omit “or 15”, substitute “, 15, 15b or 15c”.

NOTE