Occupational Superannuation (Reasonable Benefit Limits) Amendment Act 1990

No. 61 of 1990

TABLE OF PROVISIONS |

PART 1—PRELIMINARY |

Section | |

1. | Short title |

2. | Commencement |

PART 2—AMENDMENTS OF THE OCCUPATIONAL

SUPERANNUATION STANDARDS ACT 1987 |

3. | Principal Act |

4. | Interpretation |

5. | Operating standards for superannuation funds |

6. | Operating standards for approved deposit funds |

7. | Pre-1 July 88 funding credits and debits |

8. | Insertion of new Part: |

PART IIIa—REASONABLE BENEFIT LIMITS |

| 15e. Interpretation |

| 15f. Approved deposit funds, life assurance companies and registered organisations to provide certain information |

| 15g. Payers to provide certain information |

| 15h. Quotation of tax file numbers |

| 15j. Notification of roll-over etc. |

| 15k. Determination of reasonable benefits |

| 15l. Interim determinations |

| 15m. Notification etc. of determinations |

| 15n. Amendment of interim determinations |

TABLE OF PROVISIONS—continued |

Section | |

| 15p. Payers may request information on previous benefits etc. |

| 15q. Persons may request copy of previous determinations |

| 15r. Discretion to treat payment etc. as within reasonable benefit limits |

| 15s. Deemed commutation of annuities and pensions |

| 15t. This Part to be taxation law |

| 15u. Recording of tax file numbers |

| 15v. Commissioner to observe Information Privacy Principles |

9. | Review of certain decisions |

10. | Statements to accompany notification of decisions |

11. | Commissioner may publish statistical information |

12. | Regulations |

| PART 3—AMENDMENTS OF THE INCOME TAX ASSESSMENT ACT 1936 |

13. | Principal Act |

14. | Interpretation |

15. | Components of an ETP |

16. | Taxed and untaxed elements of post-June 83 component |

17. | Assessable income to include certain superannuation and kindred payments |

18. | Amendment of assessments |

19. | Deduction for contributions to eligible superannuation fund for employees |

20. | Interpretation |

21. | Taxable contributions |

22. | Repeal of section 279c |

23. | No deduction in respect of benefits |

24. | Deduction for section 82aaq assessable amounts |

| PART 4—AMENDMENT OF THE TAXATION ADMINISTRATION ACT 1953 |

25. | Principal Act |

26. | Application of Part to the Occupational Superannuation Standards Act 1987 |

Commencement

2. (1) Section 1 and this section commence on the day on which this Act receives the Royal Assent.

(2) Section 7 is taken to have commenced on 30 June 1989.

(3) Sections 22, 23 and 24 commence on 1 July 1995.

(4) The remaining provisions of this Act commence on 1 July 1990.

PART 2—AMENDMENTS OF THE OCCUPATIONAL SUPERANNUATION STANDARDS ACT 1987

Principal Act

3. In this Part, “Principal Act” means the Occupational Superannuation Standards Act 19871.

Interpretation

4. Section 3 of the Principal Act is amended:

(a) by inserting before paragraph (a) of the definition of “reviewable decision” in subsection (1) the following paragraphs:

“(aa) a decision of the Commissioner under section 15k, 15l, 15n or 15r;

“(ab) a decision of the Commissioner refusing to make a determination under subsection 15f (3), 15g (10) or 15g (11);”;

(b) by omitting from paragraph (b) of the definition of “superannuation fund” in subsection (1) “either or both” (wherever occurring) and substituting “one or more”;

(c) by omitting subparagraph (b) (ii) of that definition and substituting the following subparagraphs:

“(ii) the provision of benefits for each member of the fund in the event of the member attaining a particular age (being an age not less than the age prescribed by the regulations) without having retired from any business, trade, profession, vocation, calling, occupation or employment in which the member is engaged;

“(iii) the provision of benefits for dependants of each member of the fund in the event of the death of the member, being a death occurring before:

(a) the member’s retirement from any business, trade, profession, vocation, calling, occupation or employment in which the member is engaged; or

(b) the member attains a particular age (being an age not less than the age prescribed for the purposes of subparagraph (ii)) without having retired from

any business, trade, profession, vocation, calling, occupation or employment in which the member is engaged;

whichever is earlier;”;

(d) by inserting the following definitions in subsection (1):

“ ‘life assurance company’ means:

(a) a company registered under section 19 of the Life Insurance Act 1945; or

(b) a public authority constituted by a law of a State or Territory, being an authority that carries on life insurance business within the meaning of subsection 4 (1) of that Act;

‘registered organisation’ means:

(a) an association registered under a law of a State or Territory as a trade union; or

(b) a society registered under a law of a State or Territory providing for the registration of friendly or benefit societies; or

(c) an association of employees that is registered as an organisation under the Industrial Relations Act 1988;”;

(e) by adding at the end the following subsections:

“(4) For the purposes of paragraph (c) of the definition of ‘approved purposes’ in subsection (1), a payment, upon the request of a depositor of an amount deposited with an approved deposit fund, from the fund to a life assurance company or registered organisation for the purchase of an annuity in the name of the depositor is taken to be a repayment of that amount to the depositor upon request.

“(5) A reference in subsection (4) to a depositor includes a reference to the legal personal representative of a depositor.”.

Operating standards for superannuation funds

5. Section 7 of the Principal Act is amended by inserting after paragraph (2) (b) the following paragraphs:

“(ba) the amount of contributions that a superannuation fund may accept;

(bb) the circumstances in which a superannuation fund may accept contributions;

(bc) the actuarial standards that will apply to superannuation funds that provide superannuation pensions within the meaning of section 27a of the Tax Act otherwise than by way of annuities from a life assurance company;”.

Operating standards for approved deposit funds

6. Section 8 of the Principal Act is amended by inserting after paragraph (2) (d) the following paragraph:

“(da) the form in which benefits may be paid out of approved deposit funds;”.

Pre-1 July 88 funding credits and debits

7. Section 15d of the Principal Act is amended by adding at the end the following subsection:

“(14) In this section:

‘fund’ includes a scheme for the payment of benefits upon retirement or death, being a scheme that is constituted by or under a law of the Commonwealth or of a State or Territory.”.

Insertion of new Part

8. After Part III of the Principal Act the following Part is inserted:

“PART IIIa—REASONABLE BENEFIT LIMITS

Interpretation

“15e. (1) In this Part:

‘annuity’ means an annuity purchased wholly or partly with rolled-over amounts;

‘concessional component’ has the same meaning as in section 27a of the Tax Act;

‘continuously non-complying ADF’ has the same meaning as in section 27a of the Tax Act;

‘eligible termination payment’ has the same meaning as in section 27a of the Tax Act;

‘Information Privacy Principle’ has the same meaning as in subsection 6 (1) of the Privacy Act 1988;

‘payer’ means an approved deposit fund (other than a continuously non-complying ADF), a superannuation fund, an employer, a life assurance company or a registered organisation that makes an eligible termination payment, a payment of a superannuation pension or a payment of an annuity;

‘private company’ has the same meaning as in subsection 6 (1) of the Tax Act;

‘reasonable benefit limits’, in relation to an eligible termination payment, a superannuation pension or an annuity, means the limits calculated in accordance with the regulations;

‘relative’ has the same meaning as in subsection 6 (1) of the Tax Act;

‘residual capital value’, in relation to an annuity or superannuation pension, means the capital amount payable on the termination of the annuity or superannuation pension, as the case may be;

‘rolled-over amount’ has the same meaning as in section 27a of the Tax Act;

‘roll-over period’ has the same meaning as in section 27a of the Tax Act;

‘superannuation fund’ has the same meaning as in section 27a of the Tax Act;

‘superannuation pension’ means:

(a) a pension payable from a superannuation fund; or

(b) a benefit that is:

(i) payable from a superannuation fund; and

(ii) determined, in writing, by the Commissioner to be a superannuation pension;

‘tax file number’ has the same meaning as in Part Va of the Tax Act;

‘undeducted contributions’ has the same meaning as in section 27a of the Tax Act;

‘year of income’ has the same meaning as in subsection 6 (1) of the Tax Act.

“(2) For the purposes of this Part, an employee is an associate of an employer if:

(a) the employee is a relative of the employer; or

(b) the employer is a company that is a private company in relation to a particular year of income and, at any time during that year of income:

(i) the employee, or a relative of the employee, was a director of the company; or

(ii) shares in the company were beneficially owned by, or held indirectly on behalf of or for the benefit of, the employee or a relative of the employee; or

(iii) the employee, or a relative of the employee, was a director of another company that is a private company in relation to the year of income of that other company that, in the Commissioner’s opinion, corresponded to the first-mentioned year of income and shares in the first- mentioned company were beneficially owned by, or held indirectly on behalf of or for the benefit of, the other company; or

(iv) the employee, or a relative of the employee, was the beneficial owner of shares in, or was a director of, another company that is a private company in relation to the year of income of that other company that, in the

Commissioner’s opinion, corresponded to the first mentioned year of income and shares in the other company were beneficially owned by, or held indirectly on behalf of or for the benefit of, the first-mentioned company; or

(v) the employee, or a relative of the employee, was the beneficial owner of shares in, or was a director of, another company that is a private company in relation to the year of income of that other company that, in the Commissioner’s opinion, corresponded to the first mentioned year of income and shares in the other company were beneficially owned by, or held indirectly on behalf of or for the benefit of, a person who beneficially owned shares in the first-mentioned company or on whose behalf or for whose benefit shares in the first-mentioned company were indirectly held.

“(3) For the purposes of this Part, a person is not taken to make an eligible termination payment to another person to the extent that:

(a) the other person does not receive the whole or a part of the payment; and

(b) the first-mentioned person, acting on the other person’s behalf:

(i) rolls-over so much of the payment as was not received to an approved deposit fund; or

(ii) rolls-over so much of the payment as was not received to a superannuation fund; or

(iii) uses so much of the payment as was not received in the purchase from a life assurance company or a registered organisation of an annuity (other than an annuity that is presently payable); or

(iv) uses so much of the payment as was not received in 2 or 3 of those ways.

Approved deposit funds, life assurance companies and registered organisations to provide certain information

“15f. (1) For the purposes of determining the reasonable benefit limits of a person in respect of whom there was on 15 February 1990 an amount deposited with an approved deposit fund or a rolled-over amount held by a life assurance company or a registered organisation, where, on 15 February 1990:

(a) an approved deposit fund (other than a continuously non–complying ADF) held an amount in respect of an amount deposited with it on or before that day in relation to a person; or

(b) a life assurance company or registered organisation held an

amount in respect of a rolled-over amount deposited with it on or before that day in relation to a person;

the approved deposit fund, life assurance company or registered organisation must, within such reasonable period after 1 July 1990 as is prescribed, give to the Commissioner, in such form as is approved in writing by the Commissioner, a notice containing such information as is prescribed concerning the amount held and the person’s identity.

“(2) A life assurance company or registered organisation that is required to give a notice to the Commissioner under subsection (1) is guilty of an offence if it fails to give the notice in accordance with that subsection.

Penalty: $15,000.

“(3) In spite of section 6, where an approved deposit fund:

(a) is required to give a notice to the Commissioner under subsection (1); and

(b) fails to give the notice in accordance with that subsection;

the fund is not taken to have satisfied the approved deposit fund conditions in relation to the year of income in which the last day of the period prescribed under that subsection occurs unless the Commissioner determines (on an application having been made by the fund) that the fund is taken to have satisfied those conditions in relation to that year of income.

“(4) Subsection (1) applies in relation to an amount held by an approved deposit fund, life assurance company or registered organisation on 15 February 1990 whether or not the fund, company or organisation still holds the amount, or any part of the amount, on 1 July 1990.

“(5) A notice given under subsection (1) is a protected document for the purposes of this Act, and information contained in such a document, or transmitted under that subsection, is protected information for those purposes.

“(6) Subsection 4b (3) of the Crimes Act 1914 does not apply in relation to an offence against subsection (2).

Payers to provide certain information

“15g. (1) Subject to subsections (4), (5) and (6), where:

(a) a payer makes an eligible termination payment to a person or commences to make payments of a superannuation pension to a person; or

(b) a payer commences to make payments of an annuity that is presently payable to a person;

the payer must, within the lodgment period, give to the Commissioner, in such form as is approved in writing by the Commissioner, a notice

containing such information as is prescribed, being information that concerns the payment, superannuation pension or annuity or that is necessary to enable a determination of the person’s reasonable benefit limits to be made under subsection 15k (1).

“(2) A payer (other than an approved deposit fund or a superannuation fund) that is required to give a notice to the Commissioner under subsection (1) is guilty of an offence if it fails to give the notice in accordance with that subsection.

Penalty: $3,000.

“(3) Where a notice is given to the Commissioner under subsection (1), the payer must, within such reasonable period as is prescribed, give to the person concerned, in such form as is approved in writing by the Commissioner, a notice containing such information as is prescribed concerning the payment, superannuation pension or annuity.

“(4) Where the payer of an eligible termination payment is an employer or a superannuation fund, subsection (1) does not apply unless the amount of the payment exceeds an amount prescribed for the purposes of this subsection.

“(5) Where:

(a) apart from this subsection, subsection (1) would apply to an eligible termination payment made to a person or the payment to a person of a superannuation pension or an annuity; and

(b) the payment was made as a result of the death of another person; and

(c) the person was a spouse or child of the other person; and

(d) the payment was made before the end of:

(i) the period of 6 months after the death of the other person; or

(ii) the period of 3 months after the grant of probate of the will, or the grant of letters of administration of the estate, of the other person;

whichever happens later;

subsection (1) does not apply to the payment.

“(6) Where:

(a) apart from this subsection, subsection (1) would apply to an eligible termination payment made to a person; and

(b) the payment was made as a result of the commutation to a lump sum of so much of an annuity or superannuation pension as was notified to the payer under section 15s as exceeding the reasonable benefit limits, being a lump sum equal to the excess amount specified in the notice;

subsection (1) does not apply to the payment.

“(7) Where, if this Part had commenced on 16 February 1990:

(a) a person would be a payer; and

(b) subsection (1) would apply to the person in relation to a payment made by the person during the period starting on that day and finishing at the end of 30 June 1990;

the person must, within the lodgment period, give to the Commissioner, in such form as is approved in writing by the Commissioner, a notice containing such information as is prescribed, being information that concerns the payment or that is necessary to enable a determination of the payee’s reasonable benefit limits to be made under subsection 15k(1).

“(8) Subsection (7) does not apply to a payment made by an employer to an employee who is not an associate of the employer.

“(9) A person (other than an approved deposit fund or a superannuation fund) that is required to give a notice to the Commissioner under subsection (7) is guilty of an offence if the person fails to give the notice in accordance with that subsection.

Penalty: $3,000.

“(10) In spite of section 5, where a superannuation fund:

(a) is required to give a notice to the Commissioner under subsection (1) or (7); and

(b) fails to give the notice in accordance with that subsection;

the fund is not taken to have satisfied the superannuation fund conditions in relation to the year of income in which the last day of the period prescribed under that subsection occurs unless the Commissioner determines (on an application having been made by the fund) that the fund is taken to have satisfied those conditions in relation to that year of income.

“(11) In spite of section 6, where an approved deposit fund:

(a) is required to give a notice to the Commissioner under subsection (1) or (7); and

(b) fails to give the notice in accordance with that subsection;

the fund is not taken to have satisfied the approved deposit fund conditions in relation to the year of income in which the last day of the period prescribed under that subsection occurs unless the Commissioner determines (on an application having been made by the fund) that the fund is taken to have satisfied those conditions in relation to that year of income.

“(12) A document provided under subsection (1) or (7) is a protected document for the purposes of this Act, and information contained in such a document, or transmitted under that subsection, is protected information for those purposes.

“(13) For the purposes of subsections (1) and (7), the lodgment period, in relation to giving a notice under one of those subsections, is:

(a) in the case of a notice under subsection (1)—such reasonable period as is prescribed for the purposes of this paragraph; or

(b) in the case of a notice under subsection (7)—such reasonable period after 1 July 1990 as is prescribed for the purposes of this paragraph; or

(c) in any case—if:

(i) the payer concerned has, within the period referred to in paragraph (a) or (b) (whichever is applicable), applied to the Commissioner for an extension of the lodgment period for the notice; and

(ii) the Commissioner, by written notice given to the payer, determines that the lodgment period should, in the special circumstances of the particular case, be extended;

the extended period as so determined.

Quotation of tax file numbers

“15h. (1) Where an approved deposit fund, life assurance company or registered organisation is obliged to give to the Commissioner a notice under section 15f concerning an amount held in relation to a person, the person may quote the person’s tax file number to the fund, company or organisation in connection with the giving of the notice.

“(2) Where:

(a) a payer makes an eligible termination payment to a person or commences to make payments of a superannuation pension to a person; or

(b) a payer commences to make payments of an annuity that is presently payable to a person;

the person may quote the person’s tax file number to the payer in connection with the payment, superannuation pension or annuity.

“(3) Where, during the period starting on 16 February 1990 and finishing at the end of 30 June 1990:

(a) a payer made an eligible termination payment to a person or commenced to make payments of a superannuation pension to a person; or

(b) a payer commenced to make payments of an annuity that was, at the time payments commenced, presently payable to a person;

the person may quote the person’s tax file number to the payer in connection with the payment, superannuation pension or annuity.

“(4) A person quotes a tax file number to a payer or other body by informing the payer or body of the number in a manner approved by the Commissioner.

“(5) The payer or other body may be so informed by the person or by another person acting for that person.

Notification of roll-over etc.

“15j. (1) Where:

(a) a person receives from a payer payment of an eligible termination payment; and

(b) within the roll-over period, the person:

(i) rolls-over the whole or a part of the payment to an approved deposit fund; or

(ii) rolls-over the whole or a part of the payment to a superannuation fund; or

(iii) uses the whole or a part of the payment in the purchase from a life assurance company or a registered organisation of an annuity (other than an annuity that is presently payable); or

(iv) uses the whole or a part of the payment in 2 or 3 of those ways;

the person must, within such reasonable period as is prescribed after the transaction referred to in paragraph (b) takes place, give to the Commissioner a notice containing such information as is prescribed, being information that concerns the transaction or that is necessary to enable a determination of the person’s reasonable benefit limits to be made under subsection 15k (1).

“(2) Where:

(a) a person becomes entitled to receive payment of an eligible termination payment from an approved deposit fund (other than a continuously non-complying ADF), a superannuation fund, an employer, a life assurance company or a registered organisation; and

(b) either:

(i) the entitlement arises out of the commutation of a superannuation pension, or an annuity, that was presently payable; or

(ii) the eligible termination payment represents the residual capital value of a superannuation pension or annuity; and

(c) the person receives part only, or none, of the payment; and

(d) the person:

(i) rolls-over so much of the payment as was not received to an approved deposit fund; or

(ii) rolls-over so much of the payment as was not received to a superannuation fund; or

(iii) uses so much of the payment as was not received in the purchase from a life assurance company or a registered organisation of an annuity (other than an annuity that is presently payable); or

(iv) uses so much of the payment as was not received in 2 or 3 of those ways;

the fund, employer, company or organisation referred to in paragraph (a) must, within such reasonable period as is prescribed after the transaction referred to in paragraph (d) takes place, give to the Commissioner a notice containing such information as is prescribed, being information that concerns the transaction or that is necessary to enable a determination of the person’s reasonable benefit limits to be made under subsection 15k (1).

Determination of reasonable benefits

“15k. (1) Subject to subsections (2) and (3), where the Commissioner receives a notice under subsection 15g (1) in relation to an eligible termination payment made to a person or the commencement of payment to a person of a superannuation pension or an annuity, the Commissioner must, within such period as is prescribed after receiving the notice, determine, in accordance with the regulations, whether the payment is in excess of the reasonable benefit limits and, if it is, the extent to which it is in excess of those limits.

“(2) The Commissioner must not make a determination under subsection (1) in relation to an eligible termination payment made to a person or the commencement of payment to a person of a superannuation pension or an annuity if the payer failed to provide to the Commissioner under subsection 15g (1) the person’s tax file number.

“(3) Where:

(a) the Commissioner receives a notice under subsection 15g (1) in relation to an eligible termination payment made to a person; and

(b) before the Commissioner makes a determination under subsection (1) in relation to the payment, the Commissioner receives a notice under section 15j that the person has, within the roll-over period:

(i) rolled over the whole of the payment to an approved deposit fund; or

(ii) rolled over the whole of the payment to a superannuation fund; or

(iii) used the whole of the payment in the purchase from a life assurance company or a registered organisation of an annuity (other than an annuity that is presently payable); or

(iv) used the whole of the payment in 2 or 3 of those ways;

the Commissioner must not make a determination under subsection (1) in relation to the payment.

“(4) Where:

(a) the Commissioner receives a notice under subsection 15g (1)

in relation to an eligible termination payment made to a person; and

(b) before the Commissioner makes a determination under subsection (1) in relation to the payment, the Commissioner receives a notice under section 15j that the person has, within the roll-over period:

(i) rolled over part of the payment to an approved deposit fund; or

(ii) rolled over part of the payment to a superannuation fund; or

(iii) used part of the payment in the purchase from a life assurance company or a registered organisation of an annuity (other than an annuity that is presently payable); or

(iv) used part of the payment in 2 or 3 of those ways;

the determination under subsection (1) in relation to the payment is to relate only to the part of the payment that has not been so rolled over or used.

“(5) Where:

(a) the Commissioner receives a notice under subsection 15g (1) in relation to an eligible termination payment made to a person; and

(b) the Commissioner makes a determination under subsection (1) in relation to the payment; and

(c) after the determination is made, the Commissioner receives a notice under section 15j that the person has, within the roll–over period:

(i) rolled over the whole of the payment to an approved deposit fund; or

(ii) rolled over the whole of the payment to a superannuation fund; or

(iii) used the whole of the payment in the purchase from a life assurance company or a registered organisation of an annuity (other than an annuity that is presently payable); or

(iv) used the whole of the payment in 2 or 3 of those ways; the Commissioner must revoke the determination.

“(6) Where:

(a) the Commissioner receives a notice under subsection 15g (1) in relation to an eligible termination payment made to a person; and

(b) the Commissioner makes a determination under subsection (1) in relation to the payment; and

(c) after the determination is made, the Commissioner receives a notice under section 15j that the person has, within the roll–over period:

(i) rolled over part of the payment to an approved deposit fund; or

(ii) rolled over part of the payment to a superannuation fund; or

(iii) used part of the payment in the purchase from a life assurance company or a registered organisation of an annuity (other than an annuity that is presently payable); or

(iv) used part of the payment in 2 or 3 of those ways;

the Commissioner must, within the prescribed time after receiving the notice under section 15j, revise the determination so that it relates only to the part of the payment that has not been so rolled over or used.

“(7) Where:

(a) the Commissioner has made a determination under subsection (1) in relation to the commencement of payment to a person of a superannuation pension or an annuity; and

(b) the person elects to commute the whole or a part of the superannuation pension or annuity within the period of time after that commencement that is prescribed as the period within which such an election may be made;

the Commissioner must, within the period of time after receiving notice of the commutation that is prescribed as the period within which the determination must be revised, revise the determination so that it takes the eligible termination payment arising from the commutation into account.

“(8) Where:

(a) the Commissioner has made a determination under subsection (1) in relation to the payment to a person of an eligible termination payment; and

(b) the Commissioner of Taxation has reduced the amount of the eligible termination payment under subsection 27a (4) or (4a) of the Tax Act;

the Commissioner must, within the prescribed time after the person has applied to the Commissioner for revision of the determination, revise the determination so that it takes the reduction into account.

“(9) The Commissioner may, at any time, revise a determination under subsection (1) by making any alteration that the Commissioner thinks necessary in order to:

(a) correct any error made by the Commissioner in making the determination; or

(b) take into account any further material information that has become available since the determination was made.

“(10) For the purposes of this Part, where a determination is revised under subsection (6), (7), (8) or (9), it is taken, as so revised, to be a determination made under subsection (1), but the determination, as so revised, must not be a determination that the Commissioner is not empowered to make under subsection (1).

Interim determinations

“15l. (1) Subject to subsection (3), where:

(a) the Commissioner, having received a notice under subsection 15g (1):

(i) is required to make a determination under subsection 15k (1); or

(ii) would, but for the operation of subsection 15k (2), be required to make such a determination;

in relation to an eligible termination payment or the payment of a superannuation pension or an annuity; and

(b) the Commissioner does not have sufficient information to make the determination;

the Commissioner must, within such period as is prescribed after receiving the notice, make an interim determination, in accordance with the method prescribed by the regulations, of whether the payment is in excess of the reasonable benefit limits and, if it is, of the extent to which it is in excess of those limits.

“(2) Without limiting the circumstances under which the Commissioner is taken not to have sufficient information under paragraph (1) (b) to make a determination, the Commissioner is taken, for the purposes of that paragraph, not to have sufficient information to make a determination if the notice concerned does not specify the tax file number of the person whose tax file number may be quoted to the payer concerned under section 15h.

“(3) Where the notice does not specify the person’s tax file number, the Commissioner’s interim determination must be to the effect that the whole of the amount of the payment that is counted towards the reasonable benefit limits is in excess of the reasonable benefit limits.

Notification etc. of determinations

“15m. (1) Where the Commissioner makes a determination under subsection 15k (1) or section 15l in relation to an eligible termination payment made to a person or the payment of a superannuation pension or an annuity to a person, the Commissioner:

(a) must give a copy of the determination, and a written statement setting out the basis on which the determination was made, to the person; and

(b) in the case of an interim determination—must include with the material referred to in paragraph (a) a notice:

(i) stating that the person may, within the prescribed period, apply to the Commissioner for an amendment of the interim determination; and

(ii) stating what additional information the Commissioner needs in order to make a determination under subsection 15k (1) and advising the person of the manner (as approved by the Commissioner) in which the person may provide the additional information; and

(iii) if the additional information is, or includes, the person’s tax file number, advising the person that, because the Commissioner has not been notified of the person’s tax file number, the interim determination is to the effect that the whole of the amount of the payment that is counted towards the reasonable benefit limits is in excess of the reasonable benefit limits; and

(c) may, if requested to do so by the Commissioner of Taxation, give a copy of the determination to the Commissioner of Taxation.

“(2) A request by the Commissioner of Taxation under paragraph (1) (c) may relate to a particular determination or a class of determinations.

Amendment of interim determinations

“15n. (1) Where:

(a) a person applies, in accordance with the regulations, for an amendment of an interim determination; and

(b) the Commissioner obtains any additional information necessary for the making of a determination under subsection 15k (1);

the Commissioner may, within the prescribed time after receiving the application, amend the interim determination in such manner (if any) as the Commissioner thinks necessary.

“(2) Where the Commissioner makes an interim determination and:

(a) no application under this section for an amendment of the interim determination is made within the prescribed period; or

(b) the Commissioner has not received, within the prescribed period:

(i) the additional information required under subparagraph 15m (1) (b) (ii); or

(ii) additional information that the Commissioner has agreed

is sufficient to enable the Commissioner to make a determination under subsection 15k (1);

the interim determination has effect as if it were a determination under subsection 15k (1).

“(3) An agreement by the Commissioner under subparagraph (2) (b) (ii) must not involve the Commissioner agreeing that sufficient information has been received to enable the Commissioner to make a determination under subsection 15k (1) if the tax file number of the person concerned has still not been provided to the Commissioner.

“(4) Where:

(a) the Commissioner makes an interim determination; and

(b) the interim determination has effect as mentioned in subsection (2); and

(c) in the circumstances provided for in the regulations, a person applies, in accordance with the regulations, for an amendment of the determination;

the Commissioner may amend the determination in such manner (if any) as the Commissioner thinks necessary.

“(5) Where the Commissioner amends a determination under this section, the Commissioner:

(a) must give a copy of the amended determination, and a written statement setting out the basis on which the determination was amended, to the person; and

(b) may, if requested to do so by the Commissioner of Taxation, give a copy of the amended determination to the Commissioner of Taxation.

“(6) A request by the Commissioner of Taxation under paragraph (5) (b) may relate to a particular amended determination or a class of amended determinations.

“(7) Where an interim determination is amended under this section, it has effect accordingly, but the interim determination, as so amended, must not be an interim determination that the Commissioner is not empowered to make under section 15l.

Payers may request information on previous benefits etc.

“15p. (1) Where a payer:

(a) makes an eligible termination payment to a person or commences to make payments of a superannuation pension to a person; or

(b) commences to make payments of an annuity that is presently payable to a person;

the payer may request the person to provide to the payer such information as is prescribed concerning any eligible termination

payments, and any payments of superannuation pension or annuity, previously made to the person by that payer or any other payer.

“(2) A request by a payer to a person in accordance with subsection (1) is not to be taken, for the purposes of section 8wa of the Taxation Administration Act 1953, to involve a requirement or request that the person quote his or her tax file number.

Persons may request copy of previous determinations

“15q. Where a person requests the Commissioner to provide to the person a copy of a determination made by the Commissioner under subsection 15k (1) or section 15l in relation to an eligible termination payment made to the person, or the payment of a superannuation pension or an annuity to the person, the Commissioner must provide a copy of that determination, and such information concerning that determination as is prescribed, to the person.

Discretion to treat payment etc. as within reasonable benefit limits

“15r. Where:

(a) part of an eligible termination payment, a superannuation pension or an annuity would, apart from this section, exceed the reasonable benefit limits; and

(b) the Commissioner is satisfied that, because of the special circumstances of the case, the whole or a part of the payment, superannuation pension or annuity should be treated as if it were within the reasonable benefit limits;

the Commissioner may make a determination under subsection 15k (1), or an interim determination under section 15l, accordingly.

Deemed commutation of annuities and pensions

“15s. (1) Where:

(a) a person purchases an annuity from a life assurance company or a registered organisation; and

(b) the Commissioner determines under subsection 15k (1) that the annuity exceeds the reasonable benefits limits;

the Commissioner must, by notice in writing, advise the company or organisation:

(c) that it must, within the period of one month after receipt of the notice:

(i) treat the annuity as if the person had commuted to a lump sum so much of the annuity as exceeds those limits, being a lump sum that is equal to the excess amount specified in the notice; and

(ii) advise the Commissioner that the annuity has been so treated; and

(d) of the offence and the penalty provided for in subsection (2).

“(2) The company or organisation must, within the period of one month after receipt of the advice:

(a) treat the annuity in the manner required by the Commissioner; and

(b) advise the Commissioner that the annuity has been so treated; and the company or organisation is guilty of an offence if it fails to comply with this subsection.

Penalty: $15,000.

“(3) Subsection (2) does not apply to a life assurance company or registered organisation unless:

(a) it is a foreign corporation within the meaning of paragraph 51 (xx) of the Constitution; or

(b) it is a trading corporation, within the meaning of that paragraph, formed within the limits of Australia; or

(c) it is a financial corporation, within the meaning of that paragraph, formed within the limits of Australia; or

(d) it is incorporated in a Territory, other than the Northern Territory.

“(4) In spite of section 5, where:

(a) a person commences to receive payments of a superannuation pension from a superannuation fund; and

(b) the Commissioner determines under subsection 15k (1) that the pension exceeds the reasonable benefit limits; and

(c) the Commissioner requests the fund, by notice in writing, that, within the period of one month after receipt of the request, it must:

(i) treat the pension as if the person had commuted to a lump sum so much of the pension as exceeds those limits, being a lump sum that is equal to the excess amount specified in the notice; and

(ii) advise the Commissioner that the pension has been so treated; and

(d) the superannuation fund fails to comply with the request;

the superannuation fund is not, while the pension remains payable, taken to have satisfied the superannuation fund conditions in relation to the year of income in which the day one month after the request was made occurs or in relation to any subsequent year of income.

“(5) Subsection 4b (3) of the Crimes Act 1914 does not apply in relation to an offence against subsection (2).

This Part to be taxation law

“15t. This Part is taken to be a taxation law for the purposes of section 69 of the Privacy Act 1988 and any guidelines in force under section 17 of that Act.

Recording of tax file numbers

“15u. In spite of section 8wb of the Taxation Administration Act 1953, the Commissioner may record a tax file number provided to the Commissioner under this Part or regulations made for the purposes of this Part.

Commissioner to observe Information Privacy Principles

“15v. The Commissioner must observe:

(a) guidelines in force under section 17 of the Privacy Act 1988; and

(b) the Information Privacy Principles.”.

Review of certain decisions

9. Section 16 of the Principal Act is amended:

(a) by inserting in subsection (1) being a decision referred to in paragraph (ab), (a), (b), (c) or (d) of the definition of ‘reviewable decision’ in subsection 3 (1),” after “Commissioner” (first occurring);

(b) by inserting after subsection (1) the following subsection:

“(1a) A person who is affected by a reviewable decision of the Commissioner, being a decision referred to in paragraph (aa) of the definition of ‘reviewable decision’ in subsection 3 (1), may, if dissatisfied with the decision, by notice given to the Commissioner within the period of 21 days after receiving notice of the decision, or within such further period as the Commissioner allows, request the Commissioner to reconsider the decision.”;

(c) by omitting from subsection (5) “trustees making the request” and substituting “applicant”;

(d) by omitting from subsection (5) “trustees” (last occurring) and substituting “applicant”;

(e) by omitting from subsection (5a) “to trustees” and substituting “to an applicant”;

(f) by omitting from subsection (5a) “the trustees” and substituting “the applicant”.

Statements to accompany notification of decisions

10. Section 17 of the Principal Act is amended:

(a) by inserting in subsection (1) or a person,” after “unit trust”;

(b) by inserting in paragraphs (1) (a) and (b) “or the person” after “trustees”;

(c) by inserting in subsection (2) or a person,” after “unit trust”;

(d) by inserting in subsection (2) “or the person” after “trustees” (last occurring).

Commissioner may publish statistical information

11. Section 19 of the Principal Act is amended:

(a) by adding at the end of subsection (1) “, or relating to payments made to persons”;

(b) by omitting subsection (2) and substituting the following subsection:

“(2) The Commissioner must not arrange for the publication of statistical information in a form that would:

(a) identify a superannuation fund, approved deposit fund or pooled superannuation trust and disclose information relating to the fund or trust, as the case requires; or

(b) identify a person to whom a payment has been made.”.

Regulations

12. Section 22 of the Principal Act is amended by omitting all the words after paragraph (b) and substituting the following:

“and, in particular:

(c) prescribing fees payable in respect of any matter under this Act; or

(d) prescribing methods for determining the reasonable benefit limits and for determining whether a part of an eligible termination payment or of the value of a superannuation pension or an annuity is within or exceeds those limits.”.

PART 3—AMENDMENTS OF THE INCOME TAX ASSESSMENT ACT 1936

Principal Act

13. In this Part, “Principal Act” means the Income Tax Assessment Act 19362.

Interpretation

14. Section 27a of the Principal Act is amended:

(a) by inserting in subsection (1) the following definitions:

“ ‘continuously non-complying ADF’ means an approved deposit fund:

(a) in the case of a fund that came into existence before 1 July 1988:

(i) that was an ineligible approved deposit fund within the meaning of section 121b of this Act, as in force at a time before 1 July 1988, in relation to the year of income commencing on 1 July 1987 and to each preceding year of income during which the fund was in existence; and

(ii) that has been a non-complying ADF in relation to the year of income commencing on 1 July 1988 and to each succeeding year of income; or

(b) in any other case—that has been a non-complying ADF in relation to each year of income since it came into existence;

‘excessive component’, in relation to an ETP, means the sum of:

(a) that part (if any) of the ETP that the Insurance and Superannuation Commissioner has determined exceeds the reasonable benefit limits; and

(b) that part (if any) of the ETP that represents the commutation to a lump sum of part of an annuity or pension in compliance with an advice or request of the Insurance and Superannuation Commissioner under section 15s of the Occupational Superannuation Standards Act 1987;

‘non-complying ADF’ has the same meaning as in Part IX;”;

(b) by omitting from paragraph (m) of the definition of “eligible termination payment” in subsection (1) “or” (last occurring);

(c) by adding at the end of the definition of “eligible termination payment” in subsection (1) the following word and paragraph:

“; or (p) a transfer of an amount from a fund that is a taxable contribution under subsection 274 (10), being a transfer that:

(i) was not made at the request of a member of the fund; and

(ii) either:

(a) was made by the fund for the purpose of ensuring that the fund remain a complying superannuation fund; or

(b) as a result of which the fund became such a fund.”;

(d) by inserting after subsection (3) the following subsection:

“(3a) A reference in the definition of ‘eligible termination payment’ in subsection (1) to an approved deposit fund does not include a reference to a continuously non-complying ADF.”;

(e) by inserting in paragraph (12) (a) “complying” before “superannuation fund”;

(f) by omitting from paragraph (12) (b) “an approved deposit fund that, at the time when the amount is paid, is maintained by an approved trustee or approved trustees” and substituting “a complying ADF”.

Components of an ETP

15. Section 27aa of the Principal Act is amended:

(a) by inserting after paragraph (1) (c) the following paragraph: “(ca) the excessive component;”;

(b) by omitting from paragraph (l) (d) “(ETP – C – NQ)” (wherever occurring) and substituting “(ETP – C – NQ – EC)”;

(c) by inserting in paragraph (1) (d) “EC is the amount of the excessive component;” after “NQ is the non-qualifying component;”;

(d) by adding at the end the following subsections:

“(3) Where:

(a) an ETP is made in relation to a taxpayer in a year of income; and

(b) the ETP consists of or includes a payment that is an eligible termination payment for the purposes of the Occupational Superannuation Standards Act 1987 to which subsection 15g (1) of that Act applies; and

(c) the Insurance and Superannuation Commissioner does not make, otherwise than because of the application of subsection 15k (3) of that Act, a determination of the reasonable benefit limits in relation to the ETP;

subsection (1) applies to the taxpayer as if paragraphs (l) (ca), (d) and (e) were replaced by the following paragraph:

‘(e) the excessive component, which is the ETP reduced by the other components.’.

“(4) Where:

(a) an ETP includes a non-qualifying component and an excessive component; and

(b) the amount of the excessive component is greater than the amount of the non-qualifying component; and

(c) subsection (3) does not apply to the ETP;

the amount of the excessive component is to be reduced by the amount of the non-qualifying component.

“(5) Where:

(a) an ETP includes a non-qualifying component and an excessive component; and

(b) the amount of the excessive component is less than or equal to the amount of the non-qualifying component; and

(c) subsection (3) does not apply to the ETP;

the ETP is taken not to include an excessive component.

“(6) For the purposes of paragraph (3) (c), the Insurance and Superannuation Commissioner is not, merely because a determination has been revoked under subsection 15k (5) of the Occupational Superannuation Standards Act 1987, taken not to have made the determination.”.

Taxed and untaxed elements of post-June 83 component

16. Section 27ab of the Principal Act is amended:

(a) by inserting in subparagraph (3) (b) (i) “and reduced by the amount of the excessive component (if any)” after “increased by the UUPP amount”;

(b) by inserting in subparagraph (3) (b) (ii) “reduced by the amount of the excessive component (if any)” after “the amount of the ETP”;

(c) by adding at the end the following subsection:

“(7) Where:

(a) subsection (6) applies to an ETP; and

(b) the ETP has an excessive component;

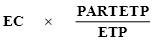

each of the parts of the ETP referred to in paragraphs (6) (a) and (b) are taken to include an excessive component of an amount calculated in accordance with the formula:

where:

EC is the excessive component of the ETP;

PART ETP is the part of the ETP referred to in paragraph (6) (a) or (b), as the case requires;

ETP is the amount of the ETP.”.

Assessable income to include certain superannuation and kindred payments

17. Section 27b of the Principal Act is amended by adding at the end the following subsection:

“(3) Where an ETP is made in relation to a taxpayer in a year of income, the assessable income of the taxpayer of the year of income includes the excessive component.”.

Amendment of assessments

18. Section 27J of the Principal Act is amended by adding at the end the following subsection:

“(2) Nothing in section 170 prevents the amendment of an assessment for the purpose of giving effect to a change to the excessive component of an ETP, whether as a result of a decision of the Tribunal or otherwise.”.

Deduction for contributions to eligible superannuation fund for employees

19. Section 82aac of the Principal Act is amended by adding at the end the following subsections:

“(2) A deduction is not allowable under subsection (1) in respect of contributions made by a taxpayer, or by a taxpayer and an associate of the taxpayer, in a year of income to more than 2 funds in respect of one employee.

“(3) In this section:

‘associate’, in relation to a person, has the same meaning as in section 26aab.”

Interpretation

20. Section 267 of the Principal Act is amended by inserting in subsection (1) the following definition:

“ ‘continuously non-complying superannuation fund’, in relation to a year of income, means a non-complying superannuation fund:

(a) in the case of a fund that came into existence before 1 July 1988:

(i) if the fund came into existence before 1 July 1964—the income of which was not exempt from tax in relation to any year of income commencing before that day; and

(ii) that was a fund to which section 121da of this Act, as in force at a time before 1 July 1988, applied in relation to the year of income commencing on 1 July 1987 and to each preceding year of income during which the fund was in existence; and

(iii) that has been a non-complying superannuation fund in relation to the year of income commencing on 1 July 1988 and to each succeeding year of income; or

(b) in any other case—that has been a non-complying superannuation fund in relation to each year of income since it came into existence;”.

Taxable contributions

21. Section 274 of the Principal Act is amended by adding at the end the following subsection:

“(10) Subject to this Division, the following transfers of amounts between superannuation funds are taxable contributions:

(a) a transfer of an amount from a complying superannuation fund to a non-complying superannuation fund;

(b) a transfer of an amount from a non-complying superannuation fund (other than a continuously non-complying superannuation fund) to a non-complying superannuation fund.”.

Repeal of section 279c

22. Section 279c of the Principal Act is repealed.

No deduction in respect of benefits

23. Section 280 of the Principal Act is amended by omitting “Subject to section 279c, no” and substituting “No”.

Deduction for section 82aaq assessable amounts

24. Section 286a of the Principal Act is amended by inserting “continuously” before “non-complying”.

PART 4—AMENDMENT OF THE TAXATION ADMINISTRATION ACT 1953

Principal Act

25. In this Part, “Principal Act” means the Taxation Administration Act 19533.

Application of Part to the Occupational Superannuation Standards Act 1987

26. Section 8aa of the Principal Act is amended by omitting paragraph (a) and substituting the following paragraph:

“(a) that Act, and regulations under that Act, were taxation laws; and”.

NOTES

1. No. 97, 1987, as amended. For previous amendments, see No. 138, 1987; and Nos. 97 and 105, 1989.

2. No. 27, 1936, as amended. For previous amendments, see No. 88, 1936; No. 5, 1937; No. 46, 1938; No. 30, 1939; Nos. 17 and 65, 1940; Nos. 58 and 69, 1941; Nos. 22 and 50, 1942; No. 10, 1943; Nos. 3 and 28, 1944; Nos. 4 and 37, 1945; No. 6, 1946; Nos. 11 and 63, 1947; No. 44, 1948; No. 66, 1949; No.

48, 1950; No. 44, 1951; Nos. 4, 28 and 90, 1952; Nos. 1, 28, 45 and 81, 1953; No. 43, 1954; Nos. 18 and 62, 1955; Nos. 25, 30 and 101, 1956; Nos. 39 and 65, 1957; No. 55, 1958; Nos. 12, 70 and 85, 1959; Nos. 17, 18, 58 and 108, 1960; Nos. 17, 27 and 94, 1961; Nos. 39 and 98, 1962; Nos. 34 and 69, 1963; Nos. 46, 68, 110 and 115, 1964; Nos. 33, 103 and 143, 1965; Nos. 50 and 83, 1966; Nos. 19, 38, 76 and 85, 1967; Nos. 4, 70, 87 and 148, 1968; Nos. 18, 93 and 101, 1969; No. 87, 1970; Nos. 6, 54 and 93, 1971; Nos. 5, 46, 47, 65 and 85, 1972; Nos. 51, 52, 53, 164 and 165, 1973; No. 216, 1973 (as amended by No. 20, 1974); Nos. 26 and 126, 1974; Nos. 80 and 117, 1975; Nos. 50, 53, 56, 98, 143, 165 and 205, 1976; Nos. 57, 126 and 127, 1977; Nos. 36, 57, 87, 90, 123, 171 and 172, 1978; Nos. 12, 19, 27, 43, 62, 146, 147 and 149, 1979; Nos. 19, 24, 57, 58, 124, 133, 134 and 159, 1980; Nos. 61, 92, 108, 109, 110, 111, 154 and 175, 1981; Nos. 29, 38, 39, 76, 80, 106 and 123, 1982; Nos. 14, 25, 39, 49, 51, 54 and 103, 1983; Nos. 14, 42, 47, 63, 76, 115, 124, 165 and 174, 1984; No. 123, 1984 (as amended by No. 65, 1985); Nos. 47, 49, 104, 123, 168 and 174, 1985; No. 173, 1985 (as amended by No. 49, 1986); Nos. 41, 46, 48, 51, 109, 112 and 154, 1986; No. 49, 1986 (as amended by No. 141, 1987); No. 52, 1986 (as amended by No. 141, 1987); No. 90, 1986 (as amended by No. 141, 1987); Nos. 23, 58, 61, 120, 145 and 163, 1987; No. 62, 1987 (as amended by No. 108, 1987); No. 108, 1987 (as amended by No. 138, 1987); No. 138, 1987 (as amended by No. 11, 1988); No. 139, 1987 (as amended by Nos. 11 and 78, 1988); Nos. 8, 11, 59, 75, 78, 80, 87, 95, 97, 127 and 153, 1988; Nos. 2, 11, 56, 70, 73, 97, 1989 (as amended by No. 105, 1989); Nos. 105, 107, 129, 163 and 167, 1989; and No. 20, 1990.

3. No. 1, 1953, as amended. For previous amendments, see Nos. 28, 39, 40 and 52, 1953; No. 18, 1955; No. 39, 1957; No. 95, 1959; No. 17, 1960; No. 75, 1964; No. 155, 1965; No. 93, 1966; No. 120, 1968; No. 216, 1973; No. 133, 1974; No. 37, 1976; Nos. 19 and 59, 1979; Nos. 39 and 117, 1983; No. 123, 1984; No. 65, 1985; (as amended by No. 193, 1985); Nos. 4, 47, 104, 123 and 168, 1985; Nos. 41, 46, 48, 112, 144 and 154, 1986; No. 49, 1986 (as amended by No. 141, 1987); Nos. 120 and 145, 1987; No. 62, 1987 (as amended by No. 108, 1987); No. 108, 1987 (as amended by No. 138, 1987); No. 138, 1987 (as amended by No. 11, 1988); Nos. 95 and 97, 1988; Nos. 105, 107, 124, 163 and 167, 1989; and No. 20, 1990.

[Minister’s second reading speech made in—

House of Representatives on 16 May 1990

Senate on 28 May 1990]