Taxation Laws Amendment Act (No. 4)

1990

No. 4 of 1991

An Act to amend the law relating to taxation

[Assented to 8 January 1991]

BE IT ENACTED by the Queen, and the Senate and the House of Representatives of the Commonwealth of Australia, as follows:

PART 1—PRELIMINARY

Short title

1. This Act may be cited as the Taxation Laws Amendment Act (No. 4) 1990.

Commencement

2. (1) Subject to this section, this Act commences on the day on which it receives the Royal Assent.

(2) Part 3 is taken to have commenced at the commencement of section 4 of the Taxation Laws Amendment Act (No. 2) 1990.

PART 2—AMENDMENT OF THE INCOME TAX ASSESSMENT

ACT 1936

Principal Act

3. In this Part, “Principal Act” means the Income Tax Assessment Act 19361.

Interpretation

4. Section 6 of the Principal Act is amended:

(a) by inserting in subsection (2) “(including subsection (2a) of this section)” after “reference in this Act”;

(b) by inserting after subsection (2) the following subsection:

“(2a) A reference in this Act to a year of income preceded by a figure referring to 2 years is a reference to the year of income commencing on 1 July in the first of those years (for example, ‘1990-91 year of income’ refers to the year of income commencing on 1 July 1990).”.

Alternative election in case of disposal, death or compulsory destruction of live stock

5. Section 36aaa of the Principal Act is amended by omitting from subsection (24) “destroyed” and substituting “disposed of”.

Gifts, pensions etc.

6. Section 78 of the Principal Act is amended:

(a) by inserting in subparagraph (1) (a) (xxxvi) “Royal” after “Australasia, the”;

(b) by omitting from subparagraph (1) (a) (lxxxiv) “Aid”.

Rebates for residents of isolated areas

7. Section 79a of the Principal Act is amended:

(a) by inserting in paragraph (2) (a) “, or of the special area in Zone B,” after “Zone A”;

(b) by omitting paragraphs (2) (b) and (c);

(c) by inserting after subsection (3e) the following subsection:

“(3f) For the purposes of this section, the census population of Nhulunbuy is taken to be less than 2,500.”.

8. After section 82kza of the Principal Act the following section is inserted:

Relief from substantiation requirements in special circumstances

“82kzaa. (1) Where:

(a) a taxpayer claims to have incurred an expense during a year of income; and

(b) having regard to:

(i) the nature and quality of evidence that the taxpayer has available to substantiate the claim; and

(ii) special circumstances affecting the taxpayer, including, but not limited to, the following:

(a) the extent to which the taxpayer attempted to comply with the substantiation sections;

(b) whether the taxpayer’s failure to comply with the substantiation sections was inadvertent or deliberate;

the Commissioner, in the course of reviewing the claim after the making of the assessment of the taxpayer’s taxable income of the year of income, is satisfied that:

(iii) the expense was incurred by the taxpayer during the year of income; and

(iv) it would be unreasonable for the substantiation sections to apply in relation to the taxpayer in relation to the expense; and

(c) the Commissioner’s review is undertaken:

(i) of the Commissioner’s own motion; or

(ii) in considering an objection against the assessment of the taxpayer’s taxable income of the year of income; or

(iii) in considering whether to make an amendment of the assessment of the taxpayer’s taxable income of the year of income in response to a request made by the taxpayer before the commencement of this section;

the substantiation sections do not apply in relation to the taxpayer in relation to the expense.

“(2) For the purposes of this section, the Commissioner is taken to have made an assessment of the taxpayer’s taxable income of the year of income if the Commissioner has served notice in respect of the taxpayer to the effect that:

(a) the taxpayer’s taxable income of the year of income is nil; or

(b) no tax is payable on the taxpayer’s taxable income of the year of income.

“(3) Where:

(a) a taxpayer makes an application under subsection 188 (1) or (2); and

(b) the period referred to in the subsection concerned ended before the commencement of this section;

the following provisions have effect:

(c) the Commissioner, the Tribunal or the Federal Court of Australia, as the case requires, when making a decision on the application, must disregard subsection (1) of this section;

(d) if the Commissioner, the Tribunal or the Federal Court of Australia, as the case requires, grants the application:

(i) the taxpayer’s objection has no effect to the extent that it relates to grounds based on subsection (1) of this section; and

(ii) the Tribunal or the Federal Court of Australia, when making a decision under paragraph 190 (a), must disregard subsection (1) of this section.

“(4) This section applies to an expense incurred before, at or after the commencement of this section.”.

Exploration and prospecting expenditure

9. Section 122jf of the Principal Act is amended by adding at the end of subsection (8) “that does not exceed the amount of the exempt income”.

Interpretation

10. Section 159gza of the Principal Act is amended by inserting the following definitions:

“ ‘foreign bank’ means a non-resident company that carries on a banking business;

‘nostro account’, in relation to a financial institution, means an account held by the financial institution with a foreign bank where both of the following conditions are satisfied:

(a) the account is maintained by the financial institution for the sole purpose of settling international transactions;

(b) the account is maintained on the basis that:

(i) amounts deposited to the account are held in the account for not more than 10 days; and

(ii) amounts advanced by way of an overdraft on the account are repaid within 10 days;

‘nostro amount’, in relation to a financial institution, means an amount owing by the financial institution where an amount representing the amount owing is:

(a) held in a nostro account in relation to the financial institution; or

(b) advanced by way of an overdraft on a nostro account in relation to the financial institution;

‘section 128f debenture amount’ has the meaning given by section 159gzja;

‘short-term trade credit amount’ has the meaning given by section 159gzjb;

‘vostro account’, in relation to a financial institution, means an account held by a foreign bank with the financial institution where both of the following conditions are satisfied:

(a) the account is maintained by the foreign bank for the sole purpose of settling international transactions;

(b) the account is maintained on the basis that:

(i) amounts deposited to the account are held in the account for not more than 10 days; and

(ii) amounts advanced by way of an overdraft on the account are repaid within 10 days;

‘vostro amount’, in relation to a financial institution, means an amount owing to the financial institution where an amount representing the amount owing is:

(a) held in a vostro account in relation to the financial institution; or

(b) advanced by way of an overdraft on a vostro account in relation to the financial institution;”.

Foreign debt

11. Section 159gzf of the Principal Act is amended by inserting in subsection (1) “(not including, in the case of a financial institution, a nostro amount)” after “owing by the company”.

Foreign equity

12. Section 159gzg of the Principal Act is amended:

(a) by omitting paragraph (1) (d) and substituting the following paragraph:

“(d) the balance outstanding at the end of the year of income on all amounts owing to the company by foreign controllers, or non-resident associates of foreign controllers, of the company, other than the following amounts:

(i) if the company is a financial institution:

(a) vostro amounts; or

(b) an amount standing to the credit of a nostro account in relation to the financial institution;

(ii) section 128f debenture amounts;

(iii) short-term trade credit amounts;”;

(b) by inserting in subsection (3) “(other than short-term trade credit amounts)” after “owing to the partnership”;

(c) by inserting in subsection (4) “(other than short-term trade credit amounts)” after “owing to the trustee of the trust estate”;

(d) by inserting in subsection (5) “(other than short-term trade credit amounts)” after “owing to the foreign investor”.

13. After section 159gzj of the Principal Act the following sections are inserted:

Section 128f debenture amount

“159gzja. For the purposes of this Division, an amount owing to a company as at a particular time is a section 128f debenture amount if all of the following paragraphs apply:

(a) the amount is owing to the company by a foreign controller, or a non-resident associate of a foreign controller, of the company (which foreign controller or associate is in this section called the ‘debtor’);

(b) the amount is owing in respect of a debenture issued by the company to the debtor not earlier than 30 days before that time;

(c) the debenture was issued to the debtor in the debtor’s capacity as a dealer, manager or underwriter in relation to the placement of the debentures concerned;

(d) the debtor disposes of the debenture within 30 days after the issue of the debenture;

(e) section 128f applies, or will apply, to any interest paid by the company in respect of the debenture.

Short-term trade credit amount

“159gzjb. (1) For the purposes of this Division, an amount owing to a resident company, to a partnership or to the trustee of a trust estate as at a particular time is a short-term trade credit amount if, and only if, all of the following paragraphs apply:

(a) the amount is owing to the company, partnership or trustee by a foreign controller, or a non-resident associate of a foreign controller, of the company, partnership or trust estate, as the case may be (which foreign controller or associate is in this subsection called the ‘trade debtor’);

(b) the company, partnership or trustee carries on a business of providing property or services at that time;

(c) in the course of carrying on that business, the company, partnership or trustee, as the case may be:

(i) provides property or services to the trade debtor; and

(ii) invoices the trade debtor for the provision of the property or services on terms that allow the trade debtor credit for a period not exceeding 30 days after the date of the invoice;

(d) the credit facility mentioned in subparagraph (c) (ii) is not extended or rolled-over.

“(2) For the purposes of this Division, an amount owing to a foreign investor as at a particular time is a short-term trade credit amount if, and only if, all of the following paragraphs apply:

(a) the amount is owing to the foreign investor by a non-resident associate (which non-resident associate is in this subsection called the ‘trade debtor’);

(b) the foreign investor carries on a business of providing property or services at that time;

(c) in the course of carrying on that business, the foreign investor:

(i) provides property or services to the trade debtor; and

(ii) invoices the trade debtor for the provision of the property or services on terms that allow the trade debtor credit for a period not exceeding 30 days after the date of the invoice;

(d) the credit facility mentioned in subparagraph (c) (ii) is not extended or rolled-over.

“(3) In this section:

‘provide’ has the same meaning as in section 21a;

‘services’ has the same meaning as in section 21a.”.

14. After section 159gzl of the Principal Act the following section is inserted:

Adjustment of foreign equity in certain cases involving resident holding companies of financial institutions

“159gzla. (1) For the purposes of determining the foreign equity in relation to a resident company (in this subsection called the ‘resident financial company’) in relation to a year of income, if all of the following conditions are satisfied at all times during the year of income when the resident financial company was in existence:

(a) the resident financial company is a bank within the meaning of the Banking Act 1959;

(b) apart from this subsection, the same foreign controller in relation to the resident financial company was the sole foreign controller in relation to the resident financial company;

(c) all of the following subparagraphs apply in relation to another resident company (in this subsection called the ‘resident holding company’):

(i) the resident holding company is not a financial institution;

(ii) there is no amount owing by the resident holding company in respect of which interest is or may become payable;

(iii) all of the shares in the resident holding company are beneficially owned by the foreign controller or by the foreign controller and an associate, or associates, of the foreign controller;

(iv) some, but not all, of the shares in the resident financial company are beneficially owned by the resident holding company;

the following provisions have effect:

(d) the resident holding company is to be treated, for the purposes of subsection 159gze (1), as if it were a non-resident;

(e) if, apart from this subsection, at the end of the year of income, the resident holding company owes one or more amounts to a foreign controller, or to a non-resident associate of a foreign controller, of the resident holding company (not being an amount in respect of which interest is or may become payable), then, the foreign equity in relation to the resident financial company in relation to the year of income is reduced by the amount, or the sum of the amounts, so owing.

“(2) Subject to subsection (3), for the purposes of this section, a company is to be taken to be in existence if it has been incorporated and has not been dissolved.

“(3) For the purposes of this section, if a company was dormant (within the meaning of Part VI of the Companies Act 1981) at all times during a period (in this subsection called the ‘dormant period’) commencing at the time of its incorporation, the company is to be taken not to have been in existence during the dormant period.”.

Resident companies

15. Section 159gzs of the Principal Act is amended:

(a) by inserting after paragraph (a) the following paragraph:

“(aa) subsection (2) does not apply; and”;

(b) by adding at the end the following subsections:

“(2) If:

(a) an amount of foreign debt interest is, apart from this Division, allowable as a deduction from the assessable income of a year of income of a taxpayer being a resident company; and

(b) the taxpayer makes an election, in accordance with subsection (5), that this subsection apply in relation to the taxpayer in relation to the year of income;

the proportion of the foreign debt interest calculated under subsection (3) is not so allowable as a deduction.

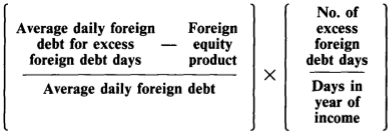

“(3) The proportion is calculated using the formula:

where:

Average daily foreign debt for excess foreign debt days is the average of the total foreign debt of the taxpayer in respect of each excess foreign debt day of the taxpayer that occurred in the year of income;

Foreign equity product is the foreign equity product of the taxpayer of the year of income;

Average daily foreign debt is the average of the total foreign debt of the taxpayer in respect of each day that occurred in the year of income;

No. of excess foreign debt days is the number of excess foreign debt days of the taxpayer that occurred in the year of income;

Days in year of income is the number of days in the year of income.

“(4) For the purposes of this section, if the total foreign debt of the taxpayer in respect of a particular day in a year of income exceeds the foreign equity product of the taxpayer of the year of income, the day is an excess foreign debt day of the taxpayer.

“(5) An election for the purposes of subsection (2) must be lodged with the Commissioner on or before the date of lodgment of the taxpayer’s return of income for the later of the following years of income:

(a) the year of income to which the election relates;

(b) the year of income in which this subsection commenced;

or within such further period as the Commissioner allows.”.

Resident company groups

16. Section 159gzt of the Principal Act is amended:

(a) by inserting after paragraph (1) (a) the following paragraph:

“(aa) subsection (3) does not apply; and”;

(b) by adding at the end the following subsections:

“(3) If:

(a) an amount of foreign debt interest is, apart from this Division, allowable as a deduction from the assessable income of a year of income of a taxpayer, being a member of a resident company group in relation to the year of income; and

(b) the member of the group that has foreign equity in relation to the year of income makes an election, in accordance with subsection (7), that this subsection apply in relation to the company group in relation to the year of income;

the proportion of the foreign debt interest calculated under subsection (4) is not so allowable as a deduction.

“(4) The proportion is calculated using the formula:

where:

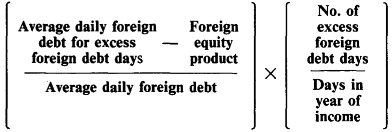

Average daily foreign debt for excess foreign debt days is the average of the aggregate of the total foreign debts of all the members of the company group in respect of each excess foreign debt day of such members that occurred in the year of income;

Foreign equity product is the foreign equity product of the year of income of the member of that group that has foreign equity in relation to the year of income;

Average daily foreign debt is the average of the aggregate of the total foreign debts of all of the members of the resident company group in respect of each day that occurred in the year of income;

No. of excess foreign debt days is the number of days that occurred in the year of income that are excess foreign debt days of the members of that group;

Days in year of income is the number of days in the year of income.

“(5) Where:

(a) the foreign equity of the member referred to in paragraph (3) (b) is attributable in part to profits arising from any transaction or transactions involving the member and any other member or members of the resident company group, being a transaction or transactions that were not arm’s length transactions; and

(b) if the transaction or transactions had been arm’s length transactions, the foreign equity of the member would have been less;

subsection (3) applies as if the lesser amount were substituted for the amount of the foreign equity.

“(6) For the purposes of this section, if the aggregate of the total foreign debts of all of the members of a resident company group in respect of a particular day in a year of income exceeds the foreign equity product of the year of income of the member of the resident company group that has foreign equity in relation

to the year of income, the day is an excess foreign debt day of each member of the group.

“(7) An election made by a member of a resident company group for the purposes of subsection (3) must be lodged with the Commissioner on or before the date of lodgment of the member’s return of income for the later of the following years of income:

(a) the year of income to which the election relates;

(b) the year of income in which this subsection commenced;

or within such further period as the Commissioner allows.”.

Partnerships

17. Section 159gzu of the Principal Act is amended:

(a) by inserting after paragraph (a) the following paragraph:

“(aa) subsection (2) does not apply; and”;

(b) by adding at the end the following subsections:

“(2) If:

(a) an amount of foreign debt interest is, apart from this Division, allowable as a deduction in calculating under section 90 the net income or partnership loss of a partnership of a year of income; and

(b) the partnership makes an election, in accordance with subsection (5), that this subsection apply in relation to the partnership in relation to the year of income;

the proportion of the foreign debt interest calculated under subsection (3) is not so allowable as a deduction.

“(3) The proportion is calculated using the formula:

where:

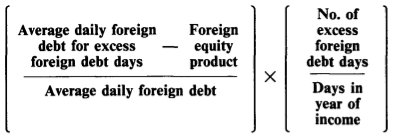

Average daily foreign debt for excess foreign debt days is the average of the total foreign debt of the partnership in respect of each excess foreign debt day of the partnership that occurred in the year of income;

Foreign equity product is the foreign equity product of the partnership of the year of income;

Average daily foreign debt is the average of the total foreign debt of the partnership in respect of each day that occurred in the year of income;

No. of excess foreign debt days is the number of excess foreign debt days of the partnership that occurred in the year of income;

Days in year of income is the number of days in the year of income.

“(4) For the purposes of this section, if the total foreign debt of the partnership in respect of a particular day in a year of income exceeds the foreign equity product of the partnership of the year of income, the day is an excess foreign debt day of the partnership.

“(5) An election made by a partnership for the purposes of subsection (2) must be lodged with the Commissioner on or before the date of lodgment of the return of income of the partnership for the later of the following years of income:

(a) the year of income to which the election relates;

(b) the year of income in which this subsection commenced;

or within such further period as the Commissioner allows.”.

Trust estates

18. Section 159gzv of the Principal Act is amended:

(a) by inserting after paragraph (a) the following paragraph:

“(aa) subsection (2) does not apply; and”;

(b) by adding at the end the following subsections:

“(2) If:

(a) an amount of foreign debt interest is, apart from this Division, allowable as a deduction in calculating under section 95 the net income of a trust estate of a year of income; and

(b) the trustee of the trust estate makes an election, in accordance with subsection (5), that this subsection apply in relation to the trust estate in relation to the year of income;

the proportion of the foreign debt interest calculated under subsection (3) is not so allowable as a deduction.

“(3) The proportion is calculated using the formula:

where:

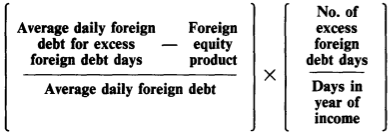

Average daily foreign debt for excess foreign debt days is the average of the total foreign debt of the trust estate in respect of each excess foreign debt day of the trust estate that occurred in the year of income;

Foreign equity product is the foreign equity product of the trust estate of the year of income;

Average daily foreign debt is the average of the total foreign debt of the trust estate in respect of each day that occurred in the year of income;

No. of excess foreign debt days is the number of excess foreign debt days of the trust estate that occurred in the year of income;

Days in year of income is the number of days in the year of income.

“(4) For the purposes of this section, if the total foreign debt of the trust estate in respect of a particular day in a year of income exceeds the foreign equity product of the trust estate of the year of income, the day is an excess foreign debt day of the trust estate.

“(5) An election made by a trustee for the purposes of subsection (2) must be lodged with the Commissioner on or before the date of lodgment of the return of income of the trust estate for the later of the following years of income:

(a) the year of income to which the election relates;

(b) the year of income in which this subsection commenced;

or within such further period as the Commissioner allows.”.

Foreign investors

19. Section 159gzw of the Principal Act is amended:

(a) by inserting after paragraph (a) the following paragraph:

“(aa) subsection (2) does not apply; and”;

(b) by adding at the end the following subsections:

“(2) If:

(a) an amount of foreign debt interest is, apart from this Division, allowable as a deduction from the assessable

income of a year of income of a taxpayer being a foreign investor; and

(b) the taxpayer makes an election, in accordance with subsection (5), that this subsection apply in relation to the taxpayer in relation to the year of income;

the proportion of the foreign debt interest calculated under subsection (3) is not so allowable as a deduction.

“(3) The proportion is calculated using the formula:

where:

Average daily foreign debt for excess foreign debt days is the average of the total foreign debt of the taxpayer in respect of each excess foreign debt day of the taxpayer that occurred in the year of income;

Foreign equity product is the foreign equity product of the taxpayer of the year of income;

Average daily foreign debt is the average of the total foreign debt of the taxpayer in respect of each day that occurred in the year of income;

No. of excess foreign debt days is the number of excess foreign debt days of the taxpayer that occurred in the year of income;

Days in year of income is the number of days in the year of income.

“(4) For the purposes of this section, if the total foreign debt of the taxpayer in respect of a particular day exceeds the foreign equity product of the taxpayer of the year of income, the day is an excess foreign debt day of the taxpayer.

“(5) An election for the purposes of subsection (2) must be lodged with the Commissioner on or before the date of lodgment of the taxpayer’s return of income for the later of the following years of income:

(a) the year of income to which the election relates;

(b) the year of income in which this subsection commenced;

or within such further period as the Commissioner allows.”.

20. After section 159gzzk of the Principal Act the following section is inserted:

Eligible gold mining expenditure—election regarding estimate of mine life for pre-changeover years

“159gzzka. (1) A taxpayer may, in accordance with subsection (3), elect that, in relation to all eligible gold mining expenditure in relation to any mining property incurred by the taxpayer before the changeover year, the notional writing-down assumptions are to include the assumption in subsection (2) of this section.

“(2) The assumption is that, in applying paragraph 122d (2) (a), 122db (2) (a), 122dd (2) (a), 122df (2) (a) or 122dg (3) (b) in relation to a year of income (in this subsection called the ‘pre-changeover year’) before the changeover year, the reference in that paragraph to the number of whole years in the estimated life of the mine or proposed mine to which the paragraph applies, on the mining property, as at the end of the pre-changeover year, is to be read as a reference to the sum of:

(a) the number of years of income occurring after the pre-changeover year but not after the changeover year; and

(b) the number of whole years in the estimated life of that mine or proposed mine as at the end of the changeover year.

“(3) The election must:

(a) be made in writing signed by or on behalf of the taxpayer; and

(b) be delivered to the Commissioner on or before the last day for the furnishing of the return of income of the changeover year or within such further time as the Commissioner allows.”.

Repeal of section 159gzzp

21. Section 159gzzp of the Principal Act is repealed.

Heading

22. The heading to Subdivision C of Division 16h of Part III of the Principal Act is amended by omitting “and related provisions”.

Repeal of section 159gzzza

23. Section 159gzzza of the Principal Act is repealed.

24. After section 159gzzzb of the Principal Act the following Subdivisions are inserted in Division 16h:

“Subdivision D—Part IIIa

Interpretation

“159gzzzba. Expressions used in this Subdivision that are also used in Part IIIa have the same respective meanings as in that Part.

Disposals of assets to which sections 159gzzzbc and 159gzzzbd apply

“159gzzzbb. Where:

(a) a taxpayer owns an asset at the end of 31 December 1990 (in this Subdivision called the ‘changeover time’); and

(b) before the changeover time, the asset was used by the taxpayer (other than on a prior holding of the asset) solely for the purpose of producing exempt income, where that use was principally for the purpose of producing income to which paragraph 23 (o) or subsection 23c (1) applied; and

(c) after the changeover time, the taxpayer disposes (which disposal is in this Subdivision called the ‘post-changeover disposal’) of the asset; and

(d) the asset was owned by the taxpayer at all times after the changeover time; and

(e) Part IIIa applies to the post-changeover disposal of the asset;

then sections 159gzzzbc and 159gzzzbd apply to the post-changeover disposal of the asset.

Capital gains adjustment

“159gzzzbc. (1) If the market value of the asset at the changeover time is greater than the amount that would be its indexed cost base if the taxpayer disposed of it at that time, then, for the purpose of determining under Part IIIa whether a capital gain accrues to the taxpayer in respect of the post-changeover disposal of the asset:

(a) the taxpayer is taken to have disposed of the asset at the changeover time for a consideration equal to the amount of that indexed cost base; and

(b) the taxpayer is taken to have immediately re-acquired the asset for a consideration equal to the market value of the asset at the changeover time; and

(c) the reference in subsection 160z (3) to the day on which the asset was acquired by the taxpayer is taken to be a reference to the day on which the asset was actually acquired by the taxpayer.

“(2) If the post-changeover disposal takes place within 12 months of the actual acquisition of the asset, subsection (1) has effect as if the references in that subsection to the asset’s indexed cost base were references to its cost base.

Capital loss adjustment

“159gzzzbd. If the market value of the asset at the changeover time is less than the amount that would be its reduced cost base if the taxpayer disposed of it at that time, then, for the purpose of determining under Part IIIa whether the taxpayer incurred a capital loss in respect of the post-changeover disposal of the asset:

(a) the taxpayer is taken to have disposed of the asset at the changeover time for a consideration equal to the amount of that reduced cost base; and

(b) the taxpayer is taken to have immediately re-acquired the asset for a consideration equal to the market value of the asset at the changeover time.

Notional deductions for section 160zk purposes

“159gzzzbe. (1) Where a taxpayer has incurred any eligible gold mining expenditure, within the meaning of Subdivision B, in relation to an asset, then, for the purposes of any application of subsection 160zk (1) in relation to a disposal of the asset by the taxpayer after 31 December 1990:

(a) notional deductions, within the meaning of Subdivision B, are taken to be deductions that have been allowed in respect of the expenditure; and

(b) where an amount is included in, or allowable as a deduction from, the assessable income of the taxpayer of a year of income in relation to the expenditure under section 122k in its application in accordance with section 159gzzo—the amount that, if section 159gzzo were disregarded, would have been included in the assessable income or allowable as a deduction under section 122k in relation to that expenditure is instead taken to have been so included in the assessable income or allowable as a deduction.

“(2) Where a taxpayer has incurred any eligible gold transport expenditure, within the meaning of Subdivision C, in relation to an asset, then, for the purposes of any application of subsection 160zk (1) in relation to a disposal of the asset by the taxpayer after 31 December 1990:

(a) notional deductions, within the meaning of Subdivision C, are taken to be deductions that have been allowed in respect of the expenditure; and

(b) where an amount is included in, or allowable as a deduction from, the assessable income of the taxpayer of a year of income in relation to the expenditure under section 123c in its application in accordance with section 159gzzz—the amount that, if section 159gzzz were disregarded, would have been included in the assessable income or allowable as a deduction under section 123c in relation to that expenditure is instead taken to have been so included in the assessable income or allowable as a deduction.

“Subdivision E—Subdivision B of Division 2

Interpretation

“159gzzzbf. In this Subdivision:

‘changeover year’, in relation to a taxpayer, means the year of income of the taxpayer in which 1 January 1991 occurs;

‘eligible trading stock’, in relation to a taxpayer at a particular time, means trading stock of the taxpayer that is on hand at that time where, if that time were the end of a year of income of the taxpayer, the value of the trading stock would not be required to be taken into account under section 28 in ascertaining whether or not the taxpayer has a taxable income for the year of income only because paragraph 23 (o) or subsection 23c (1) applies, or but for Subdivision A would apply, to income derived by the taxpayer at that time.

31.12.90 eligible trading stock to be taken into account for beginning-of-changeover-year valuation purposes

“159gzzzbg. (1) Subject to subsection (2), for the purposes of Subdivision B of Division 2 of Part III, the value of all eligible trading stock of a taxpayer on hand at the end of 31 December 1990, and of no other eligible trading stock of the taxpayer, is to be taken into account under section 28 as trading stock of the taxpayer on hand at the beginning of the changeover year in ascertaining whether or not the taxpayer has a taxable income for the changeover year.

“(2) Subsection (1) does not apply for the purposes of applying Subdivision B of Division 2 of Part III in determining the exempt income, or expenses incurred in deriving the exempt income, of the taxpayer for the changeover year.

Method of determining value of beginning-of-changeover-year trading stock

“159gzzzbh. (1) Where section 159gzzzbg applies to trading stock, then, for the purposes of ascertaining under Subdivision B of Division 2 of Part III the value of the trading stock to be taken into account at the beginning of the changeover year:

(a) the taxpayer may, in accordance with subsection (3), exercise any option, and give any notice, under section 31 in relation to the value of the trading stock at the end of the year of income before the changeover year as if that end of year occurred at the end of 31 December 1990; and

(b) if the taxpayer does not exercise an option under paragraph (a) in relation to particular trading stock, the value to be taken into account in accordance with that paragraph in relation to that trading stock is its cost price.

“(2) If:

(a) the taxpayer adopts, under Subdivision B of Division 2 of Part III, cost price as the basis of valuation in relation to any trading stock on hand at the end of the changeover year; and

(b) the value of that trading stock at the beginning of the changeover year was ascertained in accordance with paragraph (1) (a);

then, for the purposes of that Subdivision, the cost price of that trading stock is taken to be equal to the value at which it was taken into account in accordance with paragraph (1) (a).

“(3) The option or notice referred to in paragraph (1) (a) must:

(a) be exercised or given in writing signed by or on behalf of the taxpayer; and

(b) be delivered to the Commissioner before 1 March 1991 or within such further time as the Commissioner allows.

31.12.90 eligible trading stock to be taken into account for end-of-changeover-year valuation purposes in determining exempt income

“159gzzzbi. For the purposes of applying Subdivision B of Division 2 of Part III in determining the exempt income, or expenses incurred in deriving the exempt income, of a taxpayer for the changeover year:

(a) the value of all eligible trading stock of the taxpayer on hand at the end of 31 December 1990, and of no other eligible trading stock of the taxpayer, is to be taken into account under section 28 as trading stock of the taxpayer on hand at the end of the changeover year; and

(b) that value is taken to be the same at is ascertained in accordance with paragraph 159gzzzbh (1) (a).”.

25. Section 160apma of the Principal Act is repealed and the following section is substituted:

Initial payment of tax

“160apma. Where, on a particular day (in this section called the ‘payment day’) in a franking year (in this section called the ‘payment year’), a payment is made by a company in respect of an initial payment of tax that the company is required to make under section 221ap in respect of a year of income:

(a) if the payment day is in the year of income—there arises on the first day of the franking year next following the payment year a franking credit of the company equal to the adjusted amount in relation to the amount paid; or

(b) in any other case—there arises on the payment day a franking credit of the company equal to the adjusted amount in relation to the amount paid.”.

Application of initial payment of tax by a company

26. Section 160apya of the Principal Act is amended:

(a) by omitting “income is credited” and substituting “income is applied (whether by credit, refund or both)”;

(b) by omitting “payment is credited” and substituting “payment is applied”;

(c) by omitting “so credited” and substituting “so applied”.

27. After section 160apya of the Principal Act the following section is inserted:

Application of subsequent payments of tax before determination of taxable income

“160apyaa. If:

(a) after a company makes an initial payment of tax referred to in section 160apya in respect of a year of income and before the day on which the company makes a final payment of tax in respect of that year of income under section 221azd, the company makes a further payment on account of tax in respect of that year of income; and

(b) that further payment is applied (whether by credit, refund or both) by the Commissioner under section 221azf;

there arises, on the day on which that further payment is applied, a franking debit of the company equal to the adjusted amount in relation to the amount so applied.”.

28. After section 160apyb of the Principal Act the following section is inserted:

Waiver of franking deficit tax

“160apyc. Where subsection 160aqj (2) applies in relation to an initial payment of tax under section 221ap made by a company, there arises, on the day of that payment, a franking debit of the company equal to:

(a) if paragraph 160aqj (2) (c) applies—the adjusted amount in relation to the amount of the relevant franking deficit tax referred to in that paragraph; or

(b) if paragraph 160aqj (2) (d) applies—the adjusted amount in relation to so much of the amount of the relevant franking deficit tax referred to in that paragraph as is equal to the initial payment of tax.”.

When initial payment to be made

29. Section 221ap of the Principal Act is amended by adding at the end the following subsection:

“(2) An initial payment of tax is due and payable on the day referred to in subsection (1).”.

Additional payments to form part of initial payment

30. Section 221az of the Principal Act is amended:

(a) by omitting “An amount paid” and substituting “Subject to this section, an amount paid”;

(b) by adding at the end the following subsection:

“(2) An amount paid as mentioned in subsection 221ar (7) is not taken, for the purposes of Part IIIaa, to be, or to constitute part of, as the case requires, an initial payment of tax.”.

Schedule 2

31. Schedule 2 to the Principal Act is amended:

(a) by adding at the end of Part I:

“9. Lord Howe Island.”;

(b) by adding at the end of Part II:

“4. King Island, Tasmania.

5. All the islands in the group of islands known as the Furneaux Group, Tasmania.”.

Application of amendments

32. (1) In this section:

“amended Act” means the Principal Act as amended by this Act.

(2) The amendments made by section 5 apply in relation to live stock disposed of on or after 1 July 1987.

(3) The amendment made by paragraph 6 (a) applies to gifts made on or after 23 June 1970.

(4) The amendment made by paragraph 6 (b) applies to gifts made on or after 2 August 1989.

(5) The amendments made by sections 7 and 31 apply to assessments in respect of income of the 1990-91 year of income and of all subsequent years of income.

(6) The amendment made by section 9 applies to expenditure incurred after 15 August 1989.

(7) Subject to this section, the amendments made by section 11, paragraph 12 (a) and section 14 apply to assessments in respect of income of the 1987-88 year of income and of all subsequent years of income.

(8) Subparagraph 159gzg (1) (d) (iii) of the amended Act and the amendments made by paragraphs 12 (b), (c) and (d) and sections 15 to 19 (inclusive) of this Act apply to assessments in respect of income of the 1988-89 year of income and of all subsequent years of income.

(9) The amendments made by sections 21, 22, 23 and 24 (in so far as it provides for the insertion of Subdivision D in Division 16h of Part III of the Principal Act) apply to assets whether acquired before or after the commencement of those sections.

Transitional—section 160apx of the amended Act

33. (1) In this section:

“amended Act” means the Principal Act as amended by this Act.

(2) For the purposes of Part IIIaa of the amended Act, where:

(a) a franking debit (in this subsection called the “actual franking debit”) of a company arose under section 160apx of the Principal Act before the commencement of this section in relation to a dividend; and

(b) if sections 160apya, 160apyaa and 160apyc of the amended Act had been in force before the commencement of this section:

(i) no franking debit of the company would have arisen under section 160apx in relation to the dividend; or

(ii) a franking debit (in this subsection called the “notional franking debit”) of the company would have arisen under that section in relation to the dividend; and

(c) if subparagraph (b) (ii) applies—the actual franking debit exceeds the notional franking debit;

there arises on the date of commencement of this section a franking credit of the company equal to:

(d) if subparagraph (b) (i) applies—the actual franking debit; or

(e) if subparagraph (b) (ii) applies—the amount of the excess.

(3) A reference in this section to section 160apya of the amended Act does not include a reference to that section as it has effect by virtue of section 34 of this Act.

(4) A reference in this section to section 160apyaa of the amended Act does not include a reference to that section as it has effect by virtue of section 35 of this Act.

(5) A reference in this section to section 160apyc of the amended Act does not include a reference to that section as it has effect by virtue of section 36 of this Act.

Transitional—section 160apya of the amended Act

34. (1) In this section:

“amended Act” means the Principal Act as amended by this Act.

(2) In addition to the effect that section 160apya of the amended Act has apart from this section, that section also has the effect in relation to refunds that it would have if:

(a) that section applied to payments applied by the Commissioner before the commencement of this section; and

(b) the reference in that section to the day on which a payment was applied were a reference to the date of commencement of this section.

Transitional—section 160apyaa of the amended Act

35. (1) In this section:

“amended Act” means the Principal Act as amended by this Act.

(2) In addition to the effect that section 160apyaa of the amended Act has apart from this section, that section also has the effect that it would have if:

(a) that section applied to payments applied by the Commissioner before the commencement of this section; and

(b) the reference in that section to the day on which a payment was applied were a reference to the date of commencement of this section.

Transitional—section 160apyc of the amended Act

36. (1) In this section:

“amended Act” means the Principal Act as amended by this Act.

(2) In addition to the effect that section 160apyc of the amended Act has apart from this section, that section also has the effect that it would have if:

(a) that section applied to initial payments of tax made before the commencement of this section; and

(b) the reference in that section to the day of payment were a reference to the date of commencement of this section.

Amendment of assessments

37. Section 170 of the Principal Act does not prevent the amendment of an assessment made before the commencement of this section for the purpose of giving effect to this Act.

PART 3—AMENDMENT OF THE TAXATION LAWS

AMENDMENT ACT (NO. 2) 1990

Principal Act

38. In this Part, “Principal Act” means the Taxation Laws Amendment Act (No. 2) 19902.

Interpretation

39. Section 4 of the Principal Act is amended by omitting “ ‘exempt income’ “ and substituting “ ‘exempt debit’ ”.

NOTES

1. No. 27, 1936, as amended. For previous amendments, see No. 88, 1936; No. 5, 1937; No. 46, 1938; No. 30, 1939; Nos. 17 and 65, 1940; Nos. 58 and 69, 1941; Nos. 22 and 50, 1942; No. 10, 1943; Nos. 3 and 28, 1944; Nos. 4 and 37, 1945; No. 6, 1946; Nos. 11 and 63, 1947; No. 44, 1948; No. 66, 1949; No. 48, 1950; No. 44, 1951; Nos. 4, 28 and 90, 1952; Nos. 1, 28, 45 and 81, 1953; No. 43, 1954; Nos. 18 and 62, 1955; Nos. 25, 30 and 101, 1956; Nos. 39 and 65, 1957; No. 55, 1958; Nos. 12, 70 and 85, 1959; Nos. 17, 18, 58 and 108, 1960; Nos. 17, 27 and 94, 1961; Nos. 39 and 98, 1962; Nos. 34 and 69, 1963; Nos. 46, 68, 110 and 115, 1964; Nos. 33, 103 and 143, 1965; Nos. 50 and 83, 1966; Nos. 19, 38, 76 and 85, 1967; Nos. 4, 70, 87 and 148, 1968; Nos. 18, 93 and 101, 1969; No. 87, 1970; Nos. 6, 54 and 93, 1971; Nos. 5, 46, 47, 65 and 85, 1972; Nos. 51, 52, 53, 164 and 165, 1973; No. 216, 1973 (as amended by No. 20, 1974); Nos. 26 and 126, 1974; Nos. 80 and 117, 1975; Nos. 50, 53, 56, 98, 143, 165 and 205, 1976; Nos. 57, 126 and 127, 1977; Nos. 36, 57, 87, 90, 123, 171 and 172, 1978; Nos. 12, 19, 27, 43, 62, 146, 147 and 149, 1979; Nos. 19, 24, 57, 58, 124, 133, 134 and 159, 1980; Nos. 61, 92, 108, 109, 110, 111, 154 and 175, 1981; Nos. 29, 38, 39, 76, 80, 106 and 123, 1982; Nos. 14, 25, 39, 49, 51, 54 and 103, 1983; Nos. 14, 42, 47, 63, 76, 115, 124, 165 and 174, 1984; No. 123, 1984 (as amended by No. 65, 1985); Nos. 47, 49, 104, 123, 168 and 174, 1985; No. 173, 1985 (as amended by No. 49, 1986); Nos. 41, 46, 48, 51, 109, 112 and 154, 1986; No. 49, 1986 (as amended by No. 141, 1987); No. 52, 1986 (as amended by No. 141, 1987); No. 90, 1986 (as amended by No. 141, 1987); Nos. 23, 58, 61, 120, 145 and 163, 1987; No. 62, 1987 (as amended by No. 108, 1987); No. 108, 1987 (as amended by No. 138, 1987); No. 138, 1987 (as amended by No. 11, 1988); No. 139, 1987 (as amended by Nos. 11 and 78, 1988); Nos. 8, 11, 59, 75, 78, 80, 87, 95, 97, 127 and 153, 1988; Nos. 2, 11, 56, 70, 73, 97, 105, 107, 129, 163 and 167; 1989; No. 97, 1989 (as amended by No. 105, 1989); and Nos. 20, 35, 37, 45, 57, 58, 60 and 61, 1990.

2. No. 57, 1990.

[Minister’s second reading speech made in—

House of Representatives on 12 September 1990

Senate on 13 November 1990]