Export Market Development Grants

Amendment Act (No. 2) 1990

No. 8 of 1991

An Act to amend the Export Market Development Grants

Act 1974

[Assented to 21 January 1991]

The Parliament of Australia enacts:

Short title etc.

1. (1) This Act may be cited as the Export Market Development Grants Amendment Act (No. 2) 1990.

(2) In this Act, “Principal Act” means the Export Market Development Grants Act 19741.

Commencement

2. This Act is taken to have commenced on 1 July 1990.

Interpretation

3. Section 3 of the Principal Act is amended:

(a) by omitting “scientific or technical” from the definition of “know-how” in subsection (1);

(b) by inserting “or other” after “industrial” in the definition of “know-how” in subsection (1);

(c) by omitting paragraph (e) of the definition of “grant year” in subsection (1) and substituting the following paragraph:

“(e) the year commencing on 1 July 1990 or any of the 4 next succeeding years;”;

(d) by omitting from subsection (1) the definition of “eligible expenditure” and substituting the following definition:

“ ‘eligible expenditure’ has the meaning given by section 11a;”;

(e) by omitting from subsection (1) the definition of “eligible internal service” and substituting the following definition:

“ ‘eligible internal services’ means services that are eligible internal services because of regulations under subsection 43 (2b);”;

(f) by inserting in subsection (1) the following definitions:

“ ‘active grant year’, in relation to a claimant, means a grant year in respect of which a grant has been received, or is receivable, by the claimant;

‘approved activity, project or purpose’, in relation to an approved joint venture or approved consortium, means the activity, project or purpose specified under paragraph 40bd (2) (b) in the joint venture’s or consortium’s approval;

‘approved consortium’ means a group of persons that is approved by the Commission as an approved consortium under subsection 40bd (1);

‘approved joint venture’ means a group of persons that is approved by the Commission as an approved joint venture under subsection 40bd (1);

‘approved trading house’ means a person who is approved by the Commission as an approved trading house under subsection 40ba (1);

‘associated company’, in relation to a person, means a company that is, at any time during the relevant grant year, a company:

(a) whose operations are, or are able to be, controlled, either directly or indirectly, by the claimant; or

(b) which controls, or is able to control, either directly or indirectly, the operations of the claimant; or

(c) whose operations are controlled, or are able to be controlled, either directly or indirectly, by a person who controls or is able to control, or persons who control or are able to control, either directly or indirectly, the operations of the claimant;

‘eligible tourism services’ means services that are eligible tourism services because of regulations under subsection 43 (3b);

‘grant ceiling’ means:

(a) in relation to a person other than an approved trading house—$250,000; and

(b) in relation to an approved trading house—the amount prescribed by the regulations for the purposes of this paragraph;

‘new business’, in relation to an approved trading house, means business of the approved trading house that is new business in accordance with the guidelines under section 41;

‘nominated contact member’, in relation to an approved joint venture or approved consortium, means the member who is specified under paragraph 40bd (2) (c) in the joint venture’s or consortium’s approval;

‘permanent employee’, in relation to a person, means another person who has been a full-time employee of the person for a continuous period of not less than 5 years immediately preceding the time in relation to which the expression is used;

‘prescribed agent’ means:

(a) in relation to a person other than a company and unless paragraph (c) applies—the person or an employee of the person; or

(b) in relation to a person who is a company, or in relation to an association referred to in section 11b—a director, member of the governing body or employee of the company or association; or

(c) in relation to a partnership—any partner or employee of the partnership and, if any of the partners is a company, a director or employee of that company; or

(d) in relation to an approved joint venture or approved consortium—any of the following:

(i) a member of the joint venture or consortium;

(ii) an employee of a member of the joint venture or consortium;

(iii) if a member of the joint venture or consortium is a company—a director or employee of the company; or

(e) in relation to any person or in relation to an association referred to in section 11b—any other person determined by the Commission to be a person not at arm’s length with the person or association;

‘prescribed associate’ means:

(a) in relation to a person that is an unincorporated company—a member of the governing body of the company; or

(b) in relation to an association that is referred to in section 11b and is an unincorporated company—a member of the governing body of the company; or

(c) in relation to a partnership—a partner and, if a partner is a company, a director of that company; or

(d) in relation to a person or association referred to in section 11b—another person determined by the Commission to be a person not at arm’s length with the person or the association;

‘relative’, in relation to a person, means:

(a) a parent, grandparent, brother, sister, uncle, aunt, nephew, niece, lineal descendant or adopted child of that person or of his or her spouse; or

(b) the spouse of that person or of any other person specified in paragraph (a);”;

(g) by inserting after subsection (1) the following subsection:

“(1a) A reference in this Act to a qualifying export development activity is a reference to an activity in respect of which expenditure is qualifying export development expenditure under:

(a) section 11z if the claimant is a person other than an approved body, approved trading house, approved joint venture or approved consortium; or

(b) section 11za if the claimant is an approved body; or

(c) section 11zb if the claimant is an approved trading house; or

(d) section 11zc if the claimant is an approved joint venture or approved consortium.”;

(h) by inserting after subsection (9) the following subsection:

“(10) For the purposes of subsection (9), if an amount is paid by cheque or payment order, the amount is taken to be paid when the bank or financial institution on which the cheque or payment order is drawn debits the drawer’s account.”.

Export earnings

4. Section 3a of the Principal Act is amended:

(a) by inserting in subsection (1) “(other than an approved joint venture or approved consortium)” after “person” (first occurring);

(b) by inserting after subsection (2a) the following subsections:

“(2b) Subject to subsection (2e), a reference in this Act to an approved joint venture’s or approved consortium’s export earnings for a grant year is a reference to the sum of the export earnings of each of the members of the joint venture or

consortium for that grant year to the extent that those earnings are in respect of the approved activity, project or purpose of the joint venture or consortium.

“(2c) In working out a member’s export earnings for a grant year for the purposes of subsection (2b), disregard subsection (2).

“(2d) If a person who is not an Australian resident is a member of an approved joint venture or approved consortium, the Commission may, in writing, determine the percentage that, in the Commission’s opinion, is the person’s percentage share of the joint venture’s or consortium’s profits and losses.

“(2e) If a determination is made under subsection (2d), the joint venture’s or consortium’s export earnings for the grant year is to be reduced by the percentage specified in the determination.

“(2f) If:

(a) a person is a member of an approved joint venture or approved consortium; and

(b) the person makes a claim in respect of the person’s eligible expenditure for a grant year; and

(c) the claim is not made on behalf of the joint venture or consortium;

the person’s export earnings for the grant year, for the purposes of that claim, are to be taken into account only to the extent that they are not earnings in respect of the approved activity, project or purpose of the joint venture or consortium.

“(2g) A reference in this Act to an approved trading house’s export earnings for a grant year is a reference to export earnings of the trading house for the grant year to the extent that the earnings relate to new business of the trading house.”.

Repeal of section 4

5. Section 4 of the Principal Act is repealed.

6. After section 11 of the Principal Act the following Part is inserted:

“PART 1a—ELIGIBLE EXPENDITURE

“Division 1—General

Operation of this Part

“11a. (1) Expenditure is eligible expenditure of a person (other than an approved trading house, approved joint venture or approved consortium):

(a) only if it is incurred by the person; and

(b) only to the extent to which it is claimable expenditure (see Division 2); and

(c) only if it is qualifying export development expenditure for the particular person (see Division 4).

“(2) Expenditure is eligible expenditure of an approved trading house:

(a) only if it is incurred by the trading house; and

(b) only to the extent to which it is claimable expenditure (see Division 2); and

(c) only if it is qualifying export development expenditure for the trading house (see Division 4); and

(d) only if it is incurred in respect of new business of the trading house.

“(3) Subject to subsection (4), expenditure is eligible expenditure of an approved joint venture or approved consortium:

(a) only if it is incurred by a member of the joint venture or consortium; and

(b) only if it is incurred in respect of the approved activity, project or purpose of the joint venture or consortium; and

(c) only to the extent to which it is claimable expenditure (see Division 2); and

(d) only if the expenditure is qualifying export development expenditure for the joint venture or consortium (see Division 4).

“(4) A payment or set-off between members of an approved joint venture or approved consortium cannot be eligible expenditure of the joint venture or consortium.

“(5) Division 2 sets out the kinds of expenditure that are claimable.

“(6) Division 3 sets out expenditure that is not claimable.

“(7) Division 4 sets out the purposes for which the expenditure must be incurred to be qualifying export development expenditure: whether expenditure is qualifying export development expenditure depends on the status of the claimant.

“(8) Division 5 sets out the circumstances in which the amount of qualifying export development expenditure may be reduced by the Commission.

“(9) For the purposes of this Part, a person’s eligible expenditure includes expenditure that is taken to be eligible expenditure of the person under section 11b.

Subscriptions to industry associations etc.

“11b. Where:

(a) a person has paid an amount to an association as the whole or part of a subscription, contribution or levy; and

(b) the association is not an approved body or a company resident outside Australia; and

(c) the Commission is satisfied that the amount has been or will be applied:

(i) by way of claimable expenditure; and

(ii) in such a way that, had the amount been, or were it to be, applied by the person, the payment of the amount would be qualifying export development expenditure;

the amount is, for the purpose of this Part, taken to be an amount of eligible expenditure incurred by the person at the time when it was paid to the association.

“Division 2—Claimable expenditure

Expenses of agent

“11c. (1) Expenditure is claimable expenditure if:

(a) it is incurred by way of expenses of, contribution towards expenses of or payments made to, an agent for the purpose of:

(i) the carrying out of market research or the obtaining of market information; or

(ii) the advertising or other means of securing publicity or soliciting business; and

(b) it is not paid or payable to:

(i) a person for services performed by the person in Australia, or in the course of a visit from Australia to a place or places outside Australia, if the person is ordinarily employed in Australia by:

(a) the claimant; or

(b) an associated company; or

(c) a prescribed associate; or

(d) a director of the company if the claimant is a company; or

(e) a director of an associated company; or

(f) an associated company carrying on business in Australia; or

(g) an association referred to in section 11b; or

(ii) a prescribed associate who is a resident of Australia other than:

(a) a director of the company if the claimant is a company; or

(b) a director of an associated company; or

(c) an associated company carrying on business in Australia; or

(iii) a director of the company if the claimant is a company; or

(iv) a director of an associated company; or

(v) an associated company carrying on business in Australia.

“(2) Expenditure is claimable expenditure under this section only to the extent to which it relates to one or more of the following:

(a) eligible goods;

(b) eligible services;

(c) eligible internal educational services;

(d) eligible external governmental educational services;

(e) eligible industrial property rights;

(f) eligible know-how;

(g) eligible internal services;

(h) eligible tourism services.

“(3) In applying subsection (2), the Commission is to have regard to:

(a) the number of different types of goods, services or other things being promoted by the agent; and

(b) the allocation of the agent’s time; and

(c) any other matters that the Commission considers relevant.

“(4) Paragraph (1) (b) applies to expenditure of a member of an approved joint venture or approved consortium as if each member of the joint venture or consortium were a claimant for the grant.

Expenses associated with providing free samples or technical information

“11d. (1) Expenditure is claimable expenditure if:

(a) it is incurred by way of expenses (including costs of delivery) that, in the Commission’s opinion, are directly attributable to providing, without charge, samples or technical information to a person outside Australia; and

(b) those expenses are not payable to:

(i) a director of the company if the claimant is a company; or

(ii) a director of an associated company; or

(iii) an associated company carrying on business in Australia; or

(iv) a prescribed associate who is a resident of Australia.

“(2) Paragraph (1) (b) applies to expenditure of a member of an approved joint venture or approved consortium as if each member of the joint venture or consortium were a claimant for the grant.

“(3) Where:

(a) expenses are incurred in providing samples or technical information to a person outside Australia; and

(b) those expenses are payable to a person or prescribed associate referred to in paragraph (1) (b);

those expenses are taken to be directly attributable to the provision of the samples or technical information, but only to the extent that those expenses are, in the Commission’s opinion, expenses attributable to the actual cost of labour and materials involved in the provision of the samples or technical information.

Expenses for preparation of tenders and quotations (eligible services, eligible internal educational services, eligible external governmental educational services, eligible know-how, eligible internal services, eligible goods or eligible tourism services)

“11e. (1) Subject to subsection (2), expenditure is claimable expenditure if:

(a) it is incurred by way of expenses that, in the Commission’s opinion, are directly attributable to preparing or submitting a tender or quotation to a person resident outside Australia for the supply by the claimant of:

(i) eligible services; or

(ii) eligible internal educational services; or

(iii) eligible external governmental educational services; or

(iv) eligible know-how; or

(v) eligible internal services; or

(vi) eligible goods that are not of the same kind and specification as, or not similar to, goods that are being regularly dealt with by the claimant; or

(vii) eligible tourism services; and

(b) the expenses are not payable to:

(i) a director of the company if the claimant is a company; or

(ii) a director of an associated company; or

(iii) an associated company carrying on business in Australia; or

(iv) a prescribed associate who is a resident of Australia.

“(2) Paragraphs (1) (a) and (b) apply to expenditure of a member of an approved joint venture or approved consortium as if each member of the joint venture or consortium were a claimant for the grant.

“(3) Where:

(a) expenses are incurred in preparing or submitting a tender or quotation to a person outside Australia for the supply of the goods or services referred to in paragraph (1) (a); and

(b) those expenses are payable to a person or prescribed associate referred to in paragraph (1) (b);

the expenses are taken to be directly attributable to preparing or submitting a tender or quotation, but only to the extent that those expenses are, in the Commission’s opinion, expenses attributable to the actual cost of labour and materials involved in preparing or submitting the tender or quotation.

“(4) For the purposes of this section, preparing or submitting a tender or quotation includes making investigations and preparing information, designs, estimates or other material for the purposes of submitting the tender or quotation.

Expenses for packaging and labelling eligible goods

“11f. (1) Expenditure is claimable expenditure if:

(a) it is incurred by way of expenses that, in the Commission’s opinion, are directly attributable to:

(i) selecting or designing packaging and labelling; or

(ii) selecting or designing materials for packaging and labelling;

for use exclusively in connection with the export of eligible goods; and

(b) those expenses are not payable to:

(i) a director of the company if the claimant is a company; or

(ii) a director of an associated company; or

(iii) an associated company carrying on business in Australia; or

(iv) any other prescribed associate who is a resident of Australia.

“(2) Paragraph (1) (b) applies to expenditure of a member of an approved joint venture or approved consortium as if each member of the joint venture or consortium were a claimant for the grant.

“(3) Where:

(a) expenses are incurred:

(i) selecting or designing packaging and labelling; or

(ii) selecting or designing materials for packaging and labelling; and

(b) those expenses are payable to a person or prescribed associate referred to in paragraph (1) (b);

those expenses are taken to be directly attributable to the matters referred to in subparagraphs (3) (a) (i) and (ii), but only to the extent that those expenses are, in the Commission’s opinion, expenses attributable to the actual cost of labour and materials involved in:

(c) selecting or designing packaging and labelling; or

(d) selecting or designing materials for packaging and labelling.

Expenses for certain educational courses

“11g. (1) Expenditure is claimable expenditure if:

(a) it is incurred by way of expenses that, in the Commission’s opinion, are directly attributable to an educational course on international business development:

(i) for the claimant or a director, partner or employee of the claimant; and

(ii) that, in the Commission’s opinion, will assist the claimant to carry out qualifying export development activities;

other than amounts paid or payable:

(iii) as remuneration (whether by way of salary or otherwise) to the person undertaking the course; or

(iv) to a relative of the person undertaking the course; and

(b) those expenses are not payable to:

(i) a director of the company if the claimant is a company; or

(ii) a director of an associated company; or

(iii) an associated company carrying on business in Australia; or

(iv) a prescribed associate who is a resident of Australia.

“(2) Subparagraph (1) (a) (i) and paragraph (1) (b) apply to expenditure of a member of an approved joint venture or approved consortium as if each member of the joint venture or consortium were a claimant for the grant.

“(3) Where:

(a) expenses are incurred in respect of an educational course on international business development as referred to in paragraph (1) (a); and

(b) those expenses are payable to a person or prescribed associate referred to in paragraph (1) (b);

those expenses are taken to be directly attributable to the course, but only to the extent that those expenses are, in the Commission’s opinion, expenses attributable to the actual cost of labour and materials involved in the course.

Expenses for foreign language training

“11h. (1) Expenditure is claimable expenditure if:

(a) it is incurred by way of expenses that, in the Commission’s opinion, are directly attributable to foreign language training:

(i) for the claimant or a director, partner or employee of the claimant; and

(ii) that, in the Commission’s opinion, will assist the claimant to carry out qualifying export development activities;

other than amounts paid or payable:

(iii) as remuneration (whether by way of salary or otherwise)

to the person undertaking the training; or

(iv) to a relative of the person undertaking the training; and

(b) those expenses are not payable to:

(i) a director of the company if the claimant is a company; or

(ii) a director of an associated company; or

(iii) an associated company carrying on business in Australia; or

(iv) any other prescribed associate who is a resident of Australia.

“(2) Subparagraph (1) (a) (i) and paragraph (1) (b) apply to expenditure of a member of an approved joint venture or approved consortium as if each member of the joint venture or consortium were a claimant for the grant.

“(3) Where:

(a) expenses are incurred in respect of foreign language training as provided for in paragraph (1) (a); and

(b) those expenses are payable to a person or prescribed associate referred to in paragraph (1) (b);

those expenses are taken to be directly attributable to the training, but only to the extent that those expenses are, in the Commission’s opinion, expenses attributable to the actual cost of labour and materials involved in the training.

Expenses for foreign registration of eligible industrial property rights

“11j. (1) Subject to subsection (2), expenditure is claimable expenditure if:

(a) it is incurred by way of expenses (whether as payment of fees

or otherwise) that, in the Commission’s opinion, are directly attributable to obtaining, or seeking to obtain, under the law of a country outside Australia:

(i) the grant or registration; or

(ii) the extension of the term of registration; or

(iii) the extension of the period of registration;

of eligible industrial property rights; and

(b) those expenses are not payable to:

(i) a director of the company if the claimant is a company; or

(ii) a director of an associated company; or

(iii) an associated company carrying on business in Australia; or

(iv) a prescribed associate who is a resident of Australia.

“(2) Paragraph (1) (b) applies to expenditure of a member of an approved joint venture or approved consortium as if each member of the joint venture or consortium were a claimant for the grant.

“(3) Where:

(a) expenses are incurred in respect of the matters referred to in paragraph (1) (a); and

(b) those expenses are payable to a person or prescribed associate referred to in paragraph (1) (b);

those expenses are taken to be directly attributable to obtaining or seeking to obtain the matters referred to in paragraph (1) (a), but only to the extent that those expenses are, in the Commission’s opinion, expenses attributable to the actual cost of labour and materials involved in those matters.

Expenses for insurance to protect eligible industrial property rights

“11k. (1) Subject to subsection (2), expenditure is claimable expenditure if:

(a) it is incurred by way of premiums paid for insurance against costs likely to be incurred in respect of the protection of eligible industrial property rights obtained under the laws of countries outside Australia; and

(b) those expenses are not payable to:

(i) a director of the company if the claimant is a company; or

(ii) a director of an associated company; or

(iii) an associated company carrying on business in Australia; or

(iv) a prescribed associate who is a resident of Australia.

“(2) Paragraph (1) (b) applies to expenditure of a member of an approved joint venture or approved consortium as if each member of the joint venture or consortium were a claimant for the grant.

“(3) Where:

(a) expenses are incurred in respect of premiums paid for insurance; and

(b) those expenses are payable to a person or prescribed associate referred to in paragraph (1) (b);

those expenses are taken to be directly attributable to a payment of premiums for insurance but only to the extent that those expenses are, in the Commission’s opinion, expenses attributable to the actual cost of labour involved in the payment of those premiums.

Hotels, meals and entertainment expenses on overseas visits ($200 a day allowance)

“11l. (1) This section applies to a person who is:

(a) the claimant; or

(b) a prescribed agent of the claimant; or

(c) any other agent of the claimant;

but does not apply to a person who carries out the duties of a sales representative of the claimant outside Australia.

“(2) Subject to subsections (4) and (5), if:

(a) a person to whom this section applies commences a visit from a place in Australia to a place or places outside Australia; and

(b) the visit is undertaken primarily and principally for the purpose of undertaking qualifying export development activities of the claimant; and

(c) the activities do not consist mainly of attendance at or participation in:

(i) an educational course on international business development; or

(ii) a foreign language training course; or

(iii) a combination of the courses referred to in subparagraphs (i) and (ii); and

(d) the person’s fares for the visit are not made non-claimable by section 11u;

the claimant is taken, for the purposes of this Act, to have incurred, in the grant year in which the visit commences, $200 claimable expenditure in respect of each of the whole days elapsed during the visit.

“(3) For the purposes of subsection (2):

(a) a visit is to be taken to commence at the time when the vessel or aircraft on which the person is travelling departs from its last port of call or airport in Australia; and

(b) the number of whole days elapsed during a visit is to be calculated from the time when the visit commences until the time when the vessel or aircraft on which the person is travelling arrives at its first port of call or airport in Australia; and

(c) a whole day is to be a period of 24 hours.

“(4) The amount of claimable expenditure taken to be incurred under subsection (2) in respect of a person’s visit is not to exceed $4,200 ($200 a day for a maximum of 21 days).

“(5) If a person to whom this section applies undertakes, during the visit, qualifying export development activities on behalf of 2 or more claimants, each claimant is taken, for the purposes of this Act, to have incurred in the grant year in which the visit commences an amount of claimable expenditure equal to the claimant’s share of the $200 a day referred to in subsection (2).

“(6) The Commission is to determine each claimant’s share for the purposes of subsection (5) having regard to:

(a) the respective shares in which the claimants paid for, or contributed to, the person’s fares for the visit; and

(b) the time spent by the person in undertaking qualifying export development activities on behalf of each of the claimants; and

(c) any other matters that the Commission considers relevant.

Note: the claimable expenditure allowed under this section is intended to be instead of expenses on accommodation, sustenance and entertainment that are non-claimable expenditure because of the operation of section 11s.

Amounts paid to directors

“11m. (1) Where:

(a) an amount is paid or payable during a grant year by a claimant; and

(b) the claimant is a company; and

(c) the amount is paid or payable to:

(i) a director of the claimant company; or

(ii) a director of an associated company;

who is ordinarily carrying out the duties of a sales representative of the claimant outside Australia; and

(d) that amount would, but for subparagraphs 11c (1) (b) (iii) and (iv) be claimable expenditure; and

(e) that amount is incurred in respect of claimable expenditure of the claimant;

the Commission may, if it considers it appropriate to do so, treat the whole or part of the amount as claimable expenditure incurred by the claimant during that grant year.

“(2) Subsection (1) applies to expenditure of a member of an approved joint venture or approved consortium as if each member of the joint venture or consortium were a claimant for the grant.

“Division 3—Non-claimable expenditure

Capital expenditure

“11n. Expenditure of a capital nature is non-claimable expenditure unless it is either:

(a) expenses of the kind referred to in section 11f, 11j or 11k; or

(b) expenditure incurred in relation to disposals of the kind referred to in subsections 11z (8) and (9), 11za (5), 11zb (4), (5) and (6) and 11zc (7) and (8).

Expenses associated with International Trade Enhancement Scheme projects

“11p. Expenditure is non-claimable expenditure if it is incurred in relation to a project or activity that is, at the time when the expenditure is incurred, an approved project or activity for the purposes of the scheme known as the International Trade Enhancement Scheme.

Payments to approved trading house

“11q. Any expenditure by way of expenses of, contributions towards expenses of or payments made to, an approved trading house for the purposes of the undertaking by the approved trading house of a qualifying export development activity is non-claimable expenditure.

Non-claimable expenditure of approved trading house

“11r. Any expenditure incurred by an approved trading house in respect of:

(a) eligible goods; or

(b) eligible industrial property rights; or

(c) eligible know-how;

which, in the Commission’s opinion, was:

(d) derived directly or indirectly from; or

(e) dealt with on behalf of;

an affiliated company or an associated company, is non-claimable expenditure.

Certain travel expenses

“11s. (1) Travel, accommodation, sustenance or entertainment expenses in respect of or in relation to a visit by any person from a place (whether within or outside Australia) to another place or other places (whether within or outside Australia) are non-claimable expenditure unless the expenses are:

(a) fares; or

(b) accommodation or sustenance expenses that, in the Commission’s opinion, are directly attributable to:

(i) foreign language training as provided for in section 11h; or

(ii) an educational course on international business development as provided for in section 11g; or

(c) expenses for accommodation, sustenance or entertainment within Australia in respect of or in relation to a visit to Australia by a person who is not:

(i) the claimant; or

(ii) a prescribed agent of the claimant ordinarily employed or carrying out duties in Australia; or

(iii) a prescribed agent of the association ordinarily employed or carrying out duties in Australia; or

(d) expenses for accommodation, sustenance or entertainment incurred outside Australia in respect of or in relation to a visit by a person from a place outside Australia to another place or places outside Australia, if the person is carrying out the duties of a sales representative of the claimant outside Australia.

“(2) Paragraphs (1) (c) and (d) apply to expenditure of a member of an approved joint venture or approved consortium as if each member of the joint venture or consortium were a claimant for the grant.

Expenses for first class fares

“11t. Where:

(a) expenditure is incurred by way of first class travel fares; and

(b) the fares form part of the types of claimable expenditure set out in Division 2;

35% of those travel fare expenses are non-claimable expenditure.

Certain fares non-claimable

“11u. (1) If:

(a) a person is travelling outside Australia; and

(b) a relative of the person is, or relatives of the person are, travelling outside Australia at the same time;

the following provisions have effect:

(c) the claimant may nominate the person whose fares are to be claimable expenditure;

(d) the fares of the other person or persons are non-claimable expenditure.

“(2) For the purposes of subsection (1), ignore any relationship between:

(a) the claimant and any permanent employee of the claimant; and

(b) between any 2 permanent employees of the claimant; and

(c) between any 2 persons who do not meet at any time while they are travelling outside Australia and before they both return to Australia.

“(3) Subsections (1) and (2) apply to expenditure of a member of an approved joint venture or approved consortium as if that member were the claimant.

Miscellaneous non-claimable expenditure

“11v. Expenditure is non-claimable expenditure if it is incurred as:

(a) expenses of advertising in Australia; or

(b) commission or other remuneration, paid or payable, otherwise than by way of salary, retainer or fee, in respect of sales or other disposals; or

(c) remuneration by way of salary, retainer or fee, to the extent that the remuneration is determined, directly or indirectly, by reference to the extent or value of sales or other disposals made, or business obtained, by the person to whom the remuneration is paid or payable; or

(d) discounts and credits, or amounts in the nature of discounts or credits, allowed or paid in relation to sales and other disposals; or

(e) amounts paid or payable by way of tax, levy or other contribution under a law of Australia or of a State or internal Territory or to an authority or association in relation to the grant year in respect of which the amounts were paid or payable.

Agent (other than a prescribed agent) expenses

“11w. If:

(a) expenditure is incurred:

(i) by way of expenses of; or

(ii) by way of contributions towards expenses of; or

(iii) by way of payments made to;

an agent other than a prescribed agent; and

(b) that agent is an agent of the person for the purposes of the

undertaking by the agent of activities, the expenditure for which is claimable expenditure;

that expenditure is taken to be non-claimable expenditure unless the expenses incurred by that agent in respect of travel, accommodation, sustenance and entertainment (other than fares) in connection with those activities, are identified in any account rendered by or on behalf of the agent in respect of those activities.

Expenditure reduced by the Commission: eligible services outside Australia

“11x. (1) Expenditure, to the extent it is reduced by the Commission under subsection (2) or (3), is non-claimable expenditure.

“(2) Where:

(a) expenditure referred to in section 11e is incurred; and

(b) that expenditure relates to the supply of eligible services; and

(c) the services are not prescribed services in the construction industry; and

(d) the Commission is satisfied:

(i) that consideration for those services has accrued or will accrue; or

(ii) that, if those services were supplied, consideration for them would accrue;

to a person who is not resident and carrying on business in Australia;

the Commission must, for the purposes of this section, treat that expenditure as being reduced by an amount that the Commission, having regard to the extent to which the consideration for those services is consideration referred to in paragraph (d), considers appropriate.

“(3) Where:

(a) expenditure of the kind referred to in paragraph (2) (a) is incurred; and

(b) the expenditure relates to the supply of eligible services; and

(c) the services are prescribed services in the construction industry; and

(d) the Commission is satisfied:

(i) that consideration for those services has accrued or will accrue; or

(ii) that, if those services were supplied, consideration for them would accrue;

to a person who is not resident and carrying on business in Australia;

the Commission must, for the purposes of this section:

(e) if less than 20% but not less than 10% of the consideration for

those services is consideration within paragraph (d)—treat that expenditure as being reduced by an amount equal to 25% of that expenditure; or

(f) if less than 10% but not less than 5% of the consideration for those services is consideration within paragraph (d)—treat that expenditure as being reduced by an amount equal to 50% of that expenditure; or

(g) if less than 5% of the consideration for those services is consideration within paragraph (d)—disregard that expenditure.

“(4) For the purposes of subsections (2) and (3), where the business or affairs of a claimant who carries on business both in and outside Australia are so arranged that, in the Commission’s opinion, it is inappropriate to consider particular consideration for the supply by the claimant of services outside Australia:

(a) that has or will accrue; or

(b) that, if those services were supplied, would accrue;

to the claimant as consideration accruing to a person resident and carrying on business in Australia, the Commission must treat that consideration as accruing to a person other than a person resident and carrying on business in Australia.

“(5) In this section:

‘claimant’ includes:

(a) a consortium which has the following characteristics:

(i) all or the majority of the members are residents of Australia;

(ii) the membership includes the claimant;

(iii) it is formed to supply the relevant eligible services; or

(b) a consortium which is yet to be formed and which has the following characteristics:

(i) all or the majority of the members will be residents of Australia;

(ii) the membership will include the claimant;

(iii) either:

(a) it will be formed to supply the relevant eligible services; or

(b) if required to supply the relevant eligible services, it would be formed to do so.

‘prescribed services in the construction industry’ means civil engineering services or building services supplied by way of the construction, alteration or repair (other than routine maintenance) of:

(a) a building or other improvement to land (including submerged land); or

(b) a floating structure (other than a vessel of any description designed for use in navigation);

being services the consideration for which is not less than $200,000.

Expenditure associated with “X”-rated films

“11y. (1) Expenditure incurred directly or indirectly in relation to the export of a film is non-claimable expenditure unless, at the time the Commission determines the claim, the film:

(a) has been given a classification; and

(b) the classification is not an ‘X’ classification.

“(2) Subsection (1) does not apply to a film if:

(a) the film has not, at the time when the Commission determines the claim, been given a classification because the film is not yet completed; and

(b) the Commission has no reason to believe that the film might, if completed and submitted for classification:

(i) be refused classification; or

(ii) be given an ‘X’ classification.

“(3) If:

(a) expenditure on a film is disregarded under subsection (1); and

(b) the film is subsequently given a classification; and

(c) the classification is not an ‘X’ classification;

the expenditure is taken to be incurred at the time when the classification is given.

“(4) A reference in this section to classification of a film is a reference to censorship classification under the law of the Commonwealth, a State, the Australian Capital Territory or the Northern Territory.

“Division 4—Qualifying export development expenditure

Qualifying export development expenditure (person other than an approved body, approved trading house, approved joint venture or approved consortium)

“11z. (1) This section applies to persons other than an approved body, approved trading house, approved joint venture or approved consortium.

“(2) Expenditure is qualifying export development expenditure of a person to whom this section applies if, in the Commission’s opinion, it is incurred primarily and principally for the purpose of:

(a) creating or seeking opportunities for; or

(b) creating or increasing demand for;

the sale by that person for export, or the export and sale by that person, of eligible goods manufactured, produced, assembled or processed in Australia.

“(3) Expenditure is qualifying export development expenditure of a person to whom this section applies if, in the Commission’s opinion:

(a) that person manufactures, produces, assembles or processes eligible goods at the time the expenditure is incurred; and

(b) the expenditure is incurred primarily and principally for the purpose of:

(i) creating or seeking opportunities for; or

(ii) creating or increasing demand for;

the sale for export, or export and sale, of eligible goods manufactured, produced, assembled or processed in Australia by that person.

“(4) Expenditure is qualifying export development expenditure of a person to whom this section applies if, in the Commission’s opinion, it is incurred primarily and principally for the purpose of:

(a) creating or seeking opportunities for; or

(b) creating or increasing demand for;

the sale, outside Australia, of eligible goods manufactured, produced or assembled outside Australia wholly or principally out of materials or parts supplied by that person.

“(5) Expenditure is qualifying export development expenditure of a person to whom this section applies if:

(a) in the Commission’s opinion, it is incurred primarily and principally for the purpose of:

(i) creating or seeking opportunities for; or

(ii) creating or increasing demand for;

the supply, by that person, of eligible services outside Australia; and

(b) the supply by that person is for reward and in the course of carrying on business in Australia.

“(6) Expenditure is qualifying export development expenditure of a person to whom this section applies if:

(a) in the Commission’s opinion, it is incurred primarily and principally for the purpose of:

(i) creating or seeking opportunities for; or

(ii) creating or increasing demand for;

the supply, by that person, of eligible internal educational services to persons resident outside Australia; and

(b) the supply by that person is for reward and in the course of carrying on business in Australia.

“(7) Expenditure is qualifying export development expenditure of a person to whom this section applies if, in the Commission’s opinion, it is incurred primarily and principally for the purpose of:

(a) creating or seeking opportunities for; or

(b) creating or increasing demand for;

the supply, by the Commonwealth, a State, the Australian Capital Territory or the Northern Territory, for reward, of eligible external governmental educational services or eligible internal educational services.

“(8) Expenditure is qualifying export development expenditure of a person to whom this section applies if:

(a) in the Commission’s opinion, it is incurred primarily and principally for the purpose of:

(i) creating or seeking opportunities for; or

(ii) creating or increasing demand for;

the disposal, by that person, to persons resident outside Australia for use and enjoyment outside Australia of:

(iii) eligible industrial property rights owned by that person; or

(iv) eligible know-how owned by that person; and

(b) the disposal by that person is for reward and in the course of carrying on business in Australia.

“(9) If:

(a) a person to whom this section applies disposes of:

(i) eligible industrial property rights owned by the person; or

(ii) eligible know-how owned by the person; and

(b) the disposal by that person is for reward and in the course of carrying on business in Australia; and

(c) the disposal is to a person resident outside Australia for use and enjoyment outside Australia; and

(d) the person incurs expenditure which, in the Commission’s opinion, is incurred primarily and principally for the purpose of increasing the person’s return on the disposal;

that expenditure is qualifying export development expenditure.

“(10) The return referred to in subsection (9), may be a return receivable at or after the time of disposal and may be a return by way of royalty or licence fee or in any other form.

“(11) Expenditure is qualifying export development expenditure of a person to whom this section applies if:

(a) in the Commission’s opinion, it is incurred primarily and principally for the purpose of:

(i) creating or seeking opportunities for; or

(ii) creating or increasing demand for;

the supply by that person of eligible internal services; and

(b) the supply by that person is for reward and in the course of carrying on business in Australia.

“(12) Expenditure is qualifying export development expenditure of a person to whom this section applies if:

(a) in the Commission’s opinion, it is incurred primarily and principally for the purpose of:

(i) creating or seeking opportunities for; or

(ii) creating or increasing demand for;

the supply, by that person of eligible tourism services; and

(b) the supply by that person is for reward and in the course of carrying on business in Australia.

Qualifying export development expenditure (approved body)

“11za. (1) This section applies to an approved body.

“(2) Expenditure is qualifying export development expenditure of an approved body if, in the Commission’s opinion, it is incurred by the approved body primarily and principally for the purpose of:

(a) creating or seeking opportunities for; or

(b) creating or increasing demand for;

the sale for export, or export and sale, of eligible goods manufactured, produced, assembled or processed in Australia.

“(3) Expenditure is qualifying export development expenditure of an approved body if:

(a) in the Commission’s opinion, it is incurred primarily and principally for the purpose of:

(i) creating or seeking opportunities for; or

(ii) creating or increasing demand for;

the supply, by other persons of:

(iii) eligible services outside Australia; or

(iv) eligible internal educational services; or

(v) eligible internal services; or

(vi) eligible tourism services; and

(b) the supply, by those other persons is for reward and in the course of carrying on business in Australia.

“(4) Expenditure is qualifying export development expenditure of an approved body if, in the Commission’s opinion, it is incurred primarily and principally for the purpose of:

(a) creating or seeking opportunities for; or

(b) creating or increasing demand for;

the supply, by the Commonwealth, a State, the Australian Capital Territory or the Northern Territory, for reward, of eligible external governmental educational services or eligible internal educational services.

“(5) Expenditure is qualifying export development expenditure of an approved body if:

(a) in the Commission’s opinion, it is incurred primarily and principally for the purpose of:

(i) creating or seeking opportunities for; or

(ii) creating or increasing demand for;

the disposal, by other persons, to persons resident outside Australia for use and enjoyment outside Australia of:

(iii) eligible industrial property rights owned by those other persons; or

(iv) eligible know-how owned by those other persons; and

(b) the disposal by those other persons is for reward and in the course of carrying on business in Australia.

“(6) If:

(a) a person disposes of:

(i) eligible industrial property rights owned by the person; or

(ii) eligible know-how owned by the person; and

(b) the disposal by that person is for reward and in the course of carrying on business in Australia; and

(c) the disposal is to a person resident outside Australia for use and enjoyment outside Australia; and

(d) an approved body incurs expenditure which, in the Commission’s opinion, is incurred primarily and principally for the purpose of increasing the person’s return on the disposal;

that expenditure is qualifying export development expenditure.

“(7) The return referred to in subsection (6), may be a return receivable at or after the time of disposal and may be a return by way of royalty or licence fee or in any other form.

Qualifying export development expenditure (approved trading house)

“11zb. (1) This section applies to approved trading houses.

“(2) Expenditure is qualifying export development expenditure of an approved trading house if, in the Commission’s opinion, it is incurred primarily and principally for the purpose of:

(a) creating or seeking opportunities for; or

(b) creating or increasing demand for;

the sale by the approved trading house for export, or the export and sale by the approved trading house, of eligible goods manufactured, produced, assembled or processed in Australia.

“(3) Expenditure is qualifying export development expenditure of an approved trading house if, in the Commission’s opinion, it is incurred primarily and principally for the purpose of:

(a) creating or seeking opportunities for; or

(b) creating or increasing demand for;

the sale, outside Australia, of eligible goods manufactured, produced or assembled outside Australia wholly or principally out of materials or parts supplied by the approved trading house.

“(4) Expenditure is qualifying export development expenditure of an approved trading house if:

(a) in the Commission’s opinion, it is incurred primarily and principally for the purpose of:

(i) creating or seeking opportunities for; or

(ii) creating or increasing demand for;

the disposal, by the approved trading house, to persons resident outside Australia for use and enjoyment outside Australia of:

(iii) eligible industrial property rights owned by the approved trading house; or

(iv) eligible know-how owned by the approved trading house; and

(b) the disposal, by the approved trading house, is for reward and in the course of carrying on business in Australia.

“(5) Expenditure is qualifying export development expenditure of an approved trading house if:

(a) in the Commission’s opinion, it is incurred primarily and principally for the purpose of:

(i) creating or seeking opportunities for; or

(ii) creating or increasing demand for;

the disposal, by other persons, to persons resident outside Australia, for use and enjoyment outside Australia, of:

(iii) eligible industrial property rights owned by those other persons; or

(iv) eligible know-how owned by those other persons; and

(b) the disposal by those other persons is for reward and in the course of carrying on business in Australia.

“(6) If:

(a) an approved trading house disposes of:

(i) eligible industrial property rights owned by the trading house; or

(ii) eligible know-how owned by the trading house; and

(b) the disposal by the trading house is for reward and in the course of carrying on business in Australia; and

(c) the disposal is to a person resident outside Australia for use and enjoyment outside Australia; and

(d) the trading house incurs expenditure which, in the Commission’s opinion, is incurred primarily and principally for the purpose of increasing the trading house’s return on the disposal;

that expenditure is qualifying export development expenditure.

“(7) If:

(a) a person disposes of:

(i) eligible industrial property rights owned by the person; or

(ii) eligible know-how owned by the person; and

(b) the disposal by that person is for reward and in the course of carrying on business in Australia; and

(c) the disposal is to a person resident outside Australia for use and enjoyment outside Australia; and

(d) an approved trading house incurs expenditure which, in the Commission’s opinion, is incurred primarily and principally for the purpose of increasing the person’s return on the disposal;

that expenditure is qualifying export development expenditure.

“(8) The return referred to in subsection (6) or (7) may be a return receivable at or after the time of disposal and may be a return by way of royalty or licence fee or in any other form.

Qualifying export development expenditure (approved joint venture and approved consortium)

“11zc. (1) Expenditure is qualifying export development expenditure for an approved joint venture or approved consortium if, in the Commission’s opinion, the expenditure is incurred primarily and principally for the purpose of:

(a) creating or seeking opportunities for; or

(b) creating or increasing demand for;

the sale by a member of the joint venture or consortium for export, or the export and sale by a member of the joint venture or consortium, of eligible goods manufactured, produced, assembled or processed in Australia.

“(2) Expenditure is qualifying export development expenditure for an approved joint venture or approved consortium if, in the Commission’s opinion:

(a) a member of the joint venture or consortium manufactures, produces, assembles or processes eligible goods at the time when the expenditure is incurred; and

(b) the expenditure is incurred primarily and principally for the purpose of:

(i) creating or seeking opportunities for; or

(ii) creating or increasing demand for;

the sale for export, or export for sale, of eligible goods manufactured, produced, assembled or processed by a member of the joint venture or consortium in Australia.

“(3) Expenditure is qualifying export development expenditure for an approved joint venture or approved consortium if, in the Commission’s opinion, the expenditure is incurred primarily and principally for the purpose of:

(a) creating or seeking opportunities for; or

(b) creating or increasing demand for;

the sale, outside Australia, of eligible goods manufactured, produced, assembled or processed outside Australia wholly or principally out of materials or parts supplied by a member of the joint venture or consortium.

“(4) Expenditure is qualifying export development expenditure for an approved joint venture or approved consortium if:

(a) in the Commission’s opinion, the expenditure is incurred primarily and principally for the purpose of:

(i) creating or seeking opportunities for; or

(ii) creating or increasing demand for;

the supply by a member of the joint venture or consortium of eligible services; and

(b) the supply by a member of the joint venture or consortium is for reward and in the course of carrying on business in Australia.

“(5) Expenditure is qualifying export development expenditure for an approved joint venture or approved consortium if:

(a) in the Commission’s opinion, the expenditure is incurred primarily and principally for the purpose of:

(i) creating or seeking opportunities for; or

(ii) creating or increasing demand for;

the supply by a member of the joint venture or consortium of eligible internal educational services to persons resident outside Australia; and

(b) the supply by a member of the joint venture or consortium is for reward and in the course of carrying on business in Australia.

“(6) Expenditure is qualifying export development expenditure for an approved joint venture or approved consortium if, in the Commission’s opinion, it is incurred primarily and principally for the purpose of:

(a) creating or seeking opportunities for; or

(b) creating or increasing demand for;

the supply, by the Commonwealth, a State, the Australian Capital Territory or the Northern Territory, for reward, of eligible external governmental educational services or eligible internal educational services.

“(7) Expenditure is qualifying export development expenditure for an approved joint venture or approved consortium if:

(a) in the Commission’s opinion, the expenditure is incurred primarily and principally for the purpose of:

(i) creating or seeking opportunities for; or

(ii) creating or increasing demand for;

the disposal by a member of the joint venture or consortium to persons resident outside Australia for use and enjoyment outside Australia, of:

(iii) eligible industrial property rights owned by a member of the joint venture or consortium; or

(iv) eligible know-how owned by a member of the joint venture or consortium; and

(b) the disposal by a member of the joint venture or consortium is for reward and in the course of carrying on business in Australia.

“(8) If:

(a) a member of an approved joint venture or approved consortium disposes of:

(i) eligible industrial property rights owned by a member of the joint venture or consortium; or

(ii) eligible know-how owned by a member of the joint venture or consortium; and

(b) the disposal by that member is for reward and in the course of carrying on business in Australia; and

(c) the disposal is to a person resident outside Australia for use and enjoyment outside Australia; and

(d) that member incurs expenditure which, in the Commission’s opinion, is incurred primarily and principally for the purpose of increasing the member’s return on the disposal;

that expenditure is qualifying export development expenditure for the approved joint venture or approved consortium of which the person is a member.

“(9) The return referred to in subsection (8) may be a return receivable at or after the time of disposal and may be a return by way of royalty or licence fee or in any other form.

“(10) Expenditure is qualifying export development expenditure for an approved joint venture or approved consortium if:

(a) in the Commission’s opinion, the expenditure is incurred primarily and principally for the purpose of:

(i) creating or seeking opportunities for; or

(ii) creating or increasing demand for;

the supply by a member of the joint venture or consortium of eligible internal services; and

(b) the supply by a member of the joint venture or consortium is for reward and in the course of carrying on business in Australia.

“Division 5—Reduction of qualifying export development expenditure

Reduction where expenditure is unreasonable

“11zd. (1) Where the Commission is of the opinion that the amount of any claimable expenditure claimed in respect of a qualifying export development activity may exceed the amount that would reasonably be expected to be payable for the purpose or purposes for which the expenditure was incurred, the Commission may:

(a) notify the claimant, in writing, that it is of that opinion and of its reasons for being of that opinion; and

(b) request the claimant, within the period specified by the Commission in the notice, to provide information to the Commission to establish if the amount of expenditure was reasonably payable for the purpose or purposes for which that expenditure was incurred.

“(2) Where:

(a) a claimant receives a notice under subsection (1); and

(b) a claimant fails, within the period specified in the notice, to provide information that establishes to the satisfaction of the

Commission, that the amount or part of the amount of the expenditure to which the notice relates was reasonably payable for the purpose or purposes for which the expenditure was incurred;

the Commission may, for the purposes of this Act, by determination in writing, treat the qualifying export development expenditure as reduced by that amount or that part of that amount.

Certain qualifying export development expenditure ignored

“11ze. (1) Subject to subsection (2), where qualifying export development expenditure incurred by a person (in this section called the ‘claimant’):

(a) has been, or is to be, paid or reimbursed to the claimant by:

(i) another person; or

(ii) the government of the Commonwealth; or

(iii) the government of a State; or

(iv) the government of the Australian Capital Territory; or

(v) the government of the Northern Territory; or

(vi) any other government; or

(b) is incurred in respect of a qualifying export development activity, for which the claimant has been, or is to be paid by:

(i) another person; or

(ii) the government of the Commonwealth; or

(iii) the government of a State; or

(iv) the government of the Australian Capital Territory; or

(v) the government of the Northern Territory; or

(vi) any other government;

that qualifying export development expenditure in relation to that claimant is to be ignored.

“(2) Subsection (1) does not apply:

(a) where eligible external governmental educational services or eligible internal educational services are supplied for reward to persons resident outside Australia by:

(i) the Commonwealth; or

(ii) a State; or

(iii) the Australian Capital Territory; or

(iv) the Northern Territory; or

(b) to a payment or reimbursement between members of an approved joint venture or approved consortium in respect of qualifying export development expenditure of the joint venture or consortium; or

(c) to a payment to, or reimbursement of, an approved trading house.

“(3) For the purposes of this section, qualifying export development expenditure is taken to be reimbursed to a person where:

(a) a claimant incurs any qualifying export development expenditure; and

(b) the Commission is satisfied that:

(i) there is an agreement or arrangement between the claimant and another person; and

(ii) under that agreement or arrangement, consideration received or receivable by the claimant for the disposal of:

(a) any eligible goods; or

(b) any eligible services; or

(c) any eligible internal educational services; or

(d) any eligible external governmental educational services; or

(e) any eligible industrial property rights; or

(f) any eligible know-how; or

(g) any eligible internal services; or

(h) any eligible tourism services;

was or is more than it would have been if that expenditure had not been incurred; and

(iii) a purpose of or an effect of the agreement or arrangement, would, but for this section, be to allow the claimant to claim a grant in respect of expenditure for which the claimant will be compensated by the increased consideration.

“(4) Subsection (3) is not intended to limit the meaning of ‘reimbursed’ for the purposes of this section.

“(5) Expenditure which, under subsection (3), is taken to have been reimbursed to a claimant by another person, must, for the purposes of this section, be taken to have been reimbursed either:

(a) to the extent of; or

(b) to the extent of an amount determined by the Commission to be a reasonable estimate of;

the amount by which the consideration referred to in subparagraph (3) (b) (ii) was or is greater, by reason of that expenditure, than it would otherwise have been.”.

Grants

7. Section 12 of the Principal Act is amended by adding at the end the following subsection:

“(3) A grant in respect of eligible expenditure of an approved joint venture or approved consortium is to be paid to the nominated contact member.”.

Claims for grants

8. Section 13 of the Principal Act is amended by inserting after subsection (1) the following subsection:

“(1a) A claim for a grant in respect of eligible expenditure of an approved joint venture or approved consortium is to be made on behalf of the joint venture or consortium by the nominated contact member.”.

9. Section 14 of the Principal Act is repealed and the following section is substituted:

Eligibility for grant

“14. (1) Subject to subsections (2), (4), (6), (7), (8) and (9), a claimant is eligible for a grant in respect of a grant year if:

(a) the claimant has incurred eligible expenditure in the grant year; and

(b) the amount of the claimant’s eligible expenditure for the grant year is $30,000 or more; or

(c) in respect of a claimant in his or her first grant year after the commencement of this section and who elects in writing that this paragraph apply, the sum of the amount of the claimant’s eligible expenditure for that grant year and for the year immediately preceding that grant year is $30,000 or more.

“(2) Grants are not payable to:

(a) the Commonwealth, a State, the Australian Capital Territory or the Northern Territory; or

(b) an authority or association declared by the regulations to be a body to which grants are not payable.

“(3) Paragraph (2) (a) does not apply to a grant in relation to:

(a) eligible external governmental educational services; or

(b) eligible internal educational services; or

(c) health care services that are eligible internal services.

“(4) Subject to subsection (3), a grant is not payable to a person in respect of eligible expenditure incurred by that person at a time when that person was not a resident of Australia.

“(5) Subsection (4) is to be disregarded in working out whether a grant is payable in respect of eligible expenditure of an approved joint venture or approved consortium.

“(6) In determining the grant entitlement, for the purposes of this Act, of an authority or association that is declared by the regulations to be, except in respect of a particular business activity carried on by that authority or association, a body to which grants are not payable, any eligible expenditure incurred, or export earnings received, by that authority or association in respect of any other business activity carried on by that authority or association is to be disregarded.

“(7) A grant is not payable to a person (other than an approved trading house, approved joint venture or approved consortium) in respect of a particular grant year if either of the following paragraphs applies:

(a) if the person is a body corporate that has an affiliated company in relation to the grant year, the affiliated company is not an approved trading house and the affiliated company has made a claim in respect of the grant year—the aggregate of the export earnings in the grant year of the person, and the relevant export earnings in the grant year of every body corporate that was an affiliated company in relation to the grant year (other than an approved trading house) and has made a claim in respect of the grant year, exceeds $25,000,000;

(b) in any other case—the person’s export earnings for the grant year exceed $25,000,000.

“(8) A grant is not payable in respect of the eligible expenditure of an approved joint venture or approved consortium for a grant year if the joint venture’s or consortium’s export earnings for the grant year exceed $25,000,000.

“(9) Subject to subsections (10), (11), (12), (13) and (14), a grant is not payable to a claimant if the claimant has received grants in respect of 8 or more grant years.

“(10) Subsection (9) does not apply to:

(a) an approved body; or

(b) an approved trading house.

“(11) In applying subsection (9) to a claim made by a member of an approved joint venture or approved consortium on the member’s own behalf, a grant received in respect of eligible expenditure of the joint venture or consortium is taken not to have been received by the member.

“(12) In applying subsection (9) to a claim made on behalf of an approved joint venture or approved consortium, a grant received by a

member of the joint venture or consortium in the member’s own right is taken not to have been received by the joint venture or consortium.

“(13) In applying subsection (9), disregard a grant if:

(a) the grant relates to a grant year before the grant year that starts on 1 July 1990; and

(b) the grant was solely in respect of eligible expenditure in respect of services that were eligible tourism services for the purposes of this Act at the time when the expenditure was incurred.

“(14) In applying subsection (9), disregard a grant if:

(a) the grant relates to a grant year before the grant year that started on 20 May 1985; and

(b) the grant:

(i) was for $3,500 or less; or

(ii) was made to an educational institution specified in Schedule 7 to the Export Market Development Grants Regulations.

“(15) In subsection (7):

‘relevant export earnings’, in relation to a body corporate that was an affiliated company in relation to another body corporate in relation to a grant year, means the export earnings of the first-mentioned body corporate while it was such an affiliated company.”.

10. Section 16 of the Principal Act is repealed and the following sections are substituted:

Amount of grant

“16. (1) This is how to work out the amount of a claimant’s grant for a grant year if the claimant is neither an approved body nor an approved trading house:

(a) first, work out the claimant’s provisional grant amount for that grant year using subsection (3); and

(b) then, work out the claimant’s ceiling adjusted grant amount using subsection (5); and

(c) then, work out the export performance adjusted grant amount using subsection (6): this is the amount of the claimant’s grant for that grant year.

“(2) This is how to work out the amount of a claimant’s grant for a grant year if the claimant is an approved body or an approved trading house:

(a) first, work out the claimant’s provisional grant amount using subsection (3); and

(b) then, work out the claimant’s ceiling adjusted grant amount

using subsection (5): this is the amount of the claimant’s grant for that grant year.

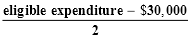

“(3) A claimant’s provisional grant amount for a grant year is the amount worked out using the formula:

where eligible expenditure is the eligible expenditure incurred by the claimant during that grant year.

“(4) Where paragraph 14 (1) (c) applies to a claimant in his or her first grant year, the formula for calculating the provisional grant income for that year is:

“(5) A claimant’s ceiling adjusted grant amount is:

(a) the claimant’s grant ceiling if the claimant’s provisional grant amount is greater than the claimant’s grant ceiling; or

(b) the claimant’s provisional grant amount in any other case.

“(6) A claimant’s export performance adjusted grant amount for a grant year is:

(a) if the grant year is the claimant’s first or second active grant year—the claimant’s ceiling adjusted grant amount; or

(b) if the grant year is the claimant’s third active grant year or a later active grant year—the amount worked out as follows:

(i) first, work out the amount of the claimant’s export earnings for the grant year;

(ii) then, work out the number of active grant years the claimant has had (including the current grant year);

(iii) then, use that number to work out the claimant’s export performance percentage for the grant year in accordance with the table at the end of this subsection;

(iv) then, apply the export performance percentage to the claimant’s export earnings for the grant year: the result is called the export performance limit;

(v) then, compare the claimant’s ceiling adjusted grant amount with the export performance limit;

(vi) if the claimant’s ceiling adjusted grant amount is greater than the export performance limit—the export performance adjusted grant amount is equal to the export performance limit;

(vii) if the claimant’s ceiling adjusted grant amount is less than or equal to the export performance limit—the export performance adjusted grant amount is equal to the ceiling adjusted grant amount.

TABLE |

EXPORT PERFORMANCE PERCENTAGE |

item | number of active grant years | factor |

1 | 3 | 40% |

2 | 4 | 20% |

3 | 5 | 10% |

4 | 6 | 7.5% |

5 | 7 | 5% |

6 | 8 | 5% |

“(7) In working out the number of active grant years a claimant has had for the purposes of subparagraph (6) (b) (ii), disregard a grant if:

(a) the grant relates to a grant year before the grant year that starts on 1 July 1990; and

(b) the grant was solely in respect of eligible expenditure in respect of services that were eligible tourism services for the purposes of this Act at the time when the expenditure was incurred.

“(8) In working out the number of active grant years a claimant has had for the purposes of subparagraph (6) (b) (ii), disregard a grant if:

(a) the grant relates to a grant year before the grant year that started on 20 May 1985; and

(b) the grant:

(i) was for $3,500 or less; or

(ii) was made to an educational institution specified in Schedule 7 to the Export Market Development Grants Regulations.

Carry forward of unmatched eligible expenditure

“16a. (1) A claimant has unmatched eligible expenditure for a grant year if the claimant’s export performance adjusted grant amount (see subsection 16 (6)) is less than the claimant’s ceiling adjusted grant amount (see subsection 16 (5)).

“(2) If a claimant has unmatched eligible expenditure for a grant year, the amount of the unmatched eligible expenditure is:

“(3) If:

(a) a claimant has unmatched eligible expenditure for a grant year (in this section called ‘Grant Year 1’); and

(b) for the claimant’s next active grant year (in this subsection called ‘Grant Year 2’) either:

(i) the claimant’s provisional grant amount is both:

(a) less than the claimant’s grant ceiling; and

(b) less than the claimant’s export performance limit for Grant Year 2; or

(ii) both:

(a) the claimant’s eligible expenditure (apart from this subsection) is less than $30,000; and

(b) the sum of the claimant’s eligible expenditure for Grant Year 2 (apart from this subsection) and the claimant’s unmatched eligible expenditure for Grant Year 1 is greater than $30,000;

so much of the unmatched eligible expenditure for Grant Year 1 as does not exceed the carry-forward ceiling is taken into account for the purposes of this Act as if it had been incurred in Grant Year 2.

“(4) For the purposes of subsection (3), the claimant’s carry-forward ceiling is:

(a) if subparagraph (3) (b) (i) applies to the claimant—the amount worked out using the formula:

where:

‘relevant limit’ is whichever is the lesser of the claimant’s grant ceiling and the claimant’s export performance limit for Grant Year 2;

‘provisional grant amount’ is the claimant’s provisional grant amount for Grant Year 2 (apart from this subsection); or

(b) if subparagraph (3) (b) (ii) applies to the claimant—the amount worked out using the formula:

where:

‘threshold shortfall’ is the difference between the claimant’s eligible expenditure for Grant Year 2 and $30,000;

‘relevant limit’ is whichever is the lesser of the claimant’s grant ceiling and the claimant’s export performance limit for Grant Year 2.

“(5) If subsection (3) applies to unmatched eligible expenditure for Grant Year 1, the amount of that unmatched expenditure is, for the purposes of the application of this section to a later grant year, reduced by the amount taken to have been incurred in Grant Year 2.

“(6) If:

(a) for the claimant’s next active grant year (in this subsection called ‘Grant Year 3’) after Grant Year 2 either:

(i) the claimant’s provisional grant amount apart from this section is both:

(a) less than the claimant’s grant ceiling; and

(b) less than the claimant’s export performance limit for Grant Year 3; or

(ii) both:

(a) the claimant’s eligible expenditure is less than $30,000; and

(b) the sum of the claimant’s eligible expenditure for Grant Year 3 and the claimant’s unmatched eligible expenditure for Grant Year 1 is greater than $30,000; and

(b) the claimant has unmatched eligible expenditure for Grant Year 1;

the unmatched eligible expenditure is taken into account as if it has been incurred in Grant Year 3.

“(7) If subsections (3) and (6) would, but for this subsection, both apply to treat unmatched eligible expenditures for 2 grant years as if they had been incurred in the same later grant year, subsection (6) applies first and subsection (3) only applies after subsection (6) has had its effect.”.

Change in ownership of business etc.

11. Section 19 of the Principal Act is amended:

(a) by adding at the end of paragraph (c) “or”;