Taxation Laws Amendment Act (No. 3) 1991

No. 216 of 1991

An Act to amend the law relating to taxation

[Assented to 24 December 1991]

The Parliament of Australia enacts:

PART 1—PRELIMINARY

Short title

1. This Act may be cited as the Taxation Laws Amendment Act (No. 3) 1991.

Commencement

2. (1) Subject to this section, this Act commences on the day on which it receives the Royal Assent.

(2) Section 11 and subsection 89 (2) are taken to have commenced on 22 January 1991.

(3) Sections 40 and 42 commence, or are taken to have commenced, as the case requires, on the commencement of the Life Insurance Policy Holders' Protection Levies Collection Act 1991.

(4) Sections 45 to 66 (inclusive) and sections 90 and 93 to 101 (inclusive) (other than sections 47, 52, 53 and 59, subsection 90 (2) and section 97) are taken to have commenced on 21 August 1991.

(5) Sections 47, 52, 53 and 59, subsection 90 (2) and section 97 are taken to have commenced at 3 p.m., by standard time in the Australian Capital Territory, on 20 August 1991.

(6) Subsection 82 (2) commences on the day after the day on which this Act receives the Royal Assent.

(7) Subject to subsection (8), section 107 commences on a day to be fixed by Proclamation.

(8) If section 107 does not commence under subsection (7) within the period of 6 months beginning on the day on which this Act receives the Royal Assent, it commences on the first day after the end of that period.

(9) Part 9 is taken to have commenced on 1 July 1991.

(10) Subject to subsection (11), sections 112 to 117 (inclusive) commence on a day to be fixed by Proclamation.

(11) If sections 112 to 117 (inclusive) do not commence under subsection (10) within the period of 6 months beginning on the day on which this Act receives the Royal Assent, they commence on the first day after the end of that period.

PART 2—AMENDMENT OF THE CHILD SUPPORT

(REGISTRATION AND COLLECTION) ACT 1988

Principal Act

3. In this Part, "Principal Act" means the Child Support (Registration and Collection) Act 19881.

Duty of employer to make deductions from salary or wages

4. Section 46 of the Principal Act is amended:

(a) by omitting from subsection (1) "subsection (3)" and substituting "this section";

(b) by adding at the end the following subsection:

"(9) Subsection (1) has, and is taken to have had, no effect to the extent (if any) that it is inconsistent with paragraph 72 (iii) or 103 (iii) of the Constitution.".

PART 3—AMENDMENT OF THE FRINGE BENEFITS TAX

ASSESSMENT ACT 1986

Principal Act

5. In this Part, "Principal Act" means the Fringe Benefits Tax Assessment Act 19862.

Living-away-from-home allowance benefits

6. Section 30 of the Principal Act is amended by adding at the end the following subsection:

"(2) If:

(a) at a particular time after 10 October 1991, in respect of the employment of an employee of an employer, the employer pays an allowance to the employee; and

(b) the employee's usual place of employment is on an oil rig, or other petroleum or gas installation, at sea; and

(c) the employee is provided with residential accommodation at or near that usual place of employment; and

(d) the allowance is expressed to be paid as a living-away-from-home allowance; and

(e) no part of the allowance is covered by subsection (1); and

(f) it would be concluded that the whole or a part of the allowance is in the nature of compensation to the employee for disadvantages to which the employee is subject, during a period, by reason that the employee is required to live away from his or her usual place of residence in order to perform the duties of that employment;

the payment of the whole of the allowance constitutes a benefit provided by the employer to the employee at that time.".

Taxable value of living-away-from-home allowance fringe benefits

7. Section 31 of the Principal Act is amended by omitting all the words after "year of tax" and substituting the following word and paragraphs:

"is:

(a) if the fringe benefit is covered by subsection 30 (1)—the amount of the recipients allowance reduced by:

(i) any exempt accommodation component; and

(ii) any exempt food component; or

(b) if the fringe benefit is covered by subsection 30 (2)—the amount of the recipients allowance.".

Amendment of assessments

8. Section 74 of the Principal Act does not prevent the amendment of an assessment made before the commencement of this section for the purpose of giving effect to the amendments made by this Part.

PART 4—AMENDMENT OF THE INCOME TAX ASSESSMENT ACT 1936

Principal Act

9. In this Part, "Principal Act" means the Income Tax Assessment Act 19363.

Exemption of pay and allowances of members of Defence Force serving in operational areas

10. Section 23ac of the Principal Act is amended:

(a) by omitting from subsection (1), paragraph (2) (a) and subsections (3) and (6) "the operational area" (wherever occurring) and substituting "an operational area";

(b) by inserting in paragraphs (2) (b) and (c) "the operational area is covered by subsection (6) and" after "if;

(c) by inserting after paragraph (2) (c) the following paragraph:

"(ca) if the operational area is covered by subsection (6a)— there is in force a certificate in writing issued by the Chief of the Defence Force to the effect that the allotment concerned was in response to Iraq's invasion of Kuwait;";

(d) by inserting in paragraph (3) (b) "at the earlier of the end of 9 June 1991 and" after "ended";

(e) by adding at the end of subsections (4) and (5) "or (ca)";

(f) by inserting after subsection (6) the following subsection:

"(6A) For the purposes of this section, the area comprising Iraq and Kuwait is taken to have become an operational area on 23 February 1991.";

(g) by inserting "or (6a)" after "(6)" in the definition of "operational area" in subsection (7).

Exemption of certain pensions

11. Section 23ad of the Principal Act is amended:

(a) by omitting "woman" from paragraph (c) of the definition of "prescribed person" in subsection (1) and substituting "person";

(b) by omitting paragraph (b) of the definition of "wife's pension" in subsection (1) and substituting the following paragraph:

"(b) a spouse's service pension payable under Part III of the Veterans' Entitlements Act 1986 to the spouse of a veteran (within the meaning of that Part), being a male veteran who has turned 65 or a female veteran who has turned 60;".

Exemption of certain income derived in respect of approved overseas projects

12. Section 23af of the Principal Act is amended by omitting from paragraph (15) (b) "the whole or a part of.

Exemption of income earned in overseas employment

13. Section 23ag of the Principal Act is amended by omitting from paragraph (6f) (b) "the whole or a part of ".

Exemption of amounts paid out of attributed income

14. Section 23ai of the Principal Act is amended by adding at the end of the definition of "trust" in subsection (3) ", but does not include a trust covered by subsection 371 (7)".

Interpretation

15. Section 24a of the Principal Act is amended by inserting the following definitions:

" 'bereavement Subdivision' means:

(a) any of the following Subdivisions of the Social Security Act 1991:

(i) Subdivision A of Division 9 of Part 2.2;

(ii) Subdivision A of Division 10 of Part 2.3;

(iii) Subdivision B of Division 9 of Part 2.5;

(iv) Subdivision B of Division 9 of Part 2.6;

(v) Subdivision A of Division 9 of Part 2.9;

(vi) Subdivision A of Division 9 of Part 2.10;

(vii) Subdivision A of Division 10 of Part 2.16; or

(b) any of the following Subdivisions of the Veterans' Entitlements Act 1986:

(i) Subdivision F of Division 3 of Part III;

(ii) Subdivision F of Division 4 of Part III;

(iii) Subdivision G of Division 6 of Part III; (Subdivisions providing for bereavement payments);

'exclusion provision' means:

(a) paragraph 82 (1) (e), 135 (1) (e), 146f (1) (e), 237 (1) (e), 303 (1) (e), 449 (1) (e), 501 (1) (e) or 822 (1) (e) of the Social Security Act 1991; or

(b) paragraph 36p (1) (e), 37p (1) (e) or 39r (1) (e) of the Veterans' Entitlements Act 1986;

(paragraphs excluding payments to a person under bereavement Subdivision if person's pension or allowance after partner's death is not less than those payments);".

Age pension

16. Section 24abc of the Principal Act is amended by adding at the end the following subsection:

"(5) If:

(a) a taxpayer's partner died; and

(b) the taxpayer would have been qualified for payments under a bereavement Subdivision but for an exclusion provision (taxpayer's pension or allowance increased on partner's death to such an extent that no bereavement payments); and

(c) the taxpayer derives payments of age pension under Part 2.2 of the Social Security Act 1991 on one or more of the 7 pension paydays after the death;

then those payments on that payday or each of those paydays are not treated under subsection (1) but as follows:

(d) the supplementary amounts are exempt;

(e) so much of the balance as exceeds what would have been the balance (payments less supplementary amounts) if the partner had not died is exempt;

(f) the rest of the balance is not exempt.".

17. Section 24abd of the Principal Act is repealed and the following section is substituted:

Disability support pension

"24abd. (1) Payments of disability support pension under Part 2.3 of the Social Security Act 1991 are exempt.

"(2) Subsection (1) has effect subject to subsection (4) (which deals with taxpayers who derive bereavement lump sum payments under section 146h of the Social Security Act 1991).

"(3) Payments under sections 146g, 146k, 146p and 146q of the Social Security Act 1991 (which deal with bereavement payments) are exempt.

"(4) If a taxpayer derives a payment under section 146h of the Social Security Act 1991:

(a) so much of the sum of that payment and other payments under the Social Security Act 1991 derived by the taxpayer on pension paydays that occurred during the bereavement lump sum period as does not exceed the tax-free amount calculated using the exempt bereavement payment calculator A in section 24abzb is exempt; and

(b) the balance of the sum is not exempt.".

18. After section 24abd of the Principal Act the following sections are inserted:

Pharmaceutical allowance

"24abda. Payments of pharmaceutical allowance under Part 2.22 of the Social Security Act 1991 are exempt.

Advance pharmaceutical supplement

"24abdb. Payments of advance pharmaceutical supplement under Part 2.23 of the Social Security Act 1991 are exempt.

Disaster relief payment

"24abdc. Payments of disaster relief payment under Part 2.24 of the Social Security Act 1991 are exempt.".

Carer pension

19. Section 24abf of the Principal Act is amended:

(a) by omitting from subsection (1) "pensioner" (wherever occurring) and substituting "person";

(b) by adding at the end the following subsections:

"(5) If:

(a) a taxpayer's partner died; and

(b) the taxpayer would have been qualified for payments under a bereavement Subdivision but for an exclusion provision (taxpayer's pension or allowance increased on partner's death to such an extent that no bereavement payments); and

(c) the taxpayer derives payments of carer pension under Part 2.5 of the Social Security Act 1991 on one or more of the 7 pension paydays after the death;

then those payments on that payday or each of those paydays are not treated under subsection (1) but as follows:

(d) the supplementary amounts are exempt;

(e) so much of the balance as exceeds what would have been the balance (payments less supplementary amounts) if the partner had not died is exempt;

(f) the rest of the balance is not exempt.

"(6) Subsection (5) does not apply to a payday on which item 3 or 4 of subsection (1) applies to the taxpayer (payments exempt).".

Sole parent pension

20. Section 24abg of the Principal Act is amended by adding at the end the following subsection:

"(5) If:

(a) a taxpayer's partner died; and

(b) the taxpayer would have been qualified for payments under a bereavement Subdivision but for an exclusion provision (taxpayer's pension or allowance increased on partner's death to such an extent that no bereavement payments); and

(c) the taxpayer derives payments of sole parent pension under Part 2.6 of the Social Security Act 1991 on one or more of the 7 pension paydays after the death;

then those payments on that payday or each of those paydays are not treated under subsection (1) but as follows:

(d) the supplementary amounts are exempt;

(e) so much of the balance as exceeds what would have been the balance (payments less supplementary amounts) if the partner had not died is exempt;

(f) the rest of the balance is not exempt.".

Repeal of section 24abj

21. Section 24abj of the Principal Act is repealed.

22. Sections 24abl and 24abm of the Principal Act are repealed and the following sections are substituted:

Job search allowance

"24abl. (1) The treatment of payments of job search allowance under Part 2.11 of the Social Security Act 1991 is as follows:

(a) the supplementary amount is exempt;

(b) the balance is not exempt.

"(2) Payments under sections 592 and 592a of the Social Security Act 1991 (which deals with bereavement payments) are exempt.

Newstart allowance

"24abm. (1) The treatment of payments of newstart allowance under Part 2.12 of the Social Security Act 1991 is as follows:

(a) the supplementary amount is exempt;

(b) the balance is not exempt.

"(2) Payments under section 660o and 660p of the Social Security Act 1991 (which deals with bereavement payments) are exempt.".

23. Section 24abo of the Principal Act is repealed and the following section is substituted:

Sickness allowance

"24abo. (1) The treatment of payments of sickness allowance under Part 2.14 of the Social Security Act 1991 is as follows:

(a) the supplementary amount is exempt;

(b) the balance is not exempt.

"(2) Payments under section 728s and 728t of the Social Security Act 1991 (which deals with bereavement payments) are exempt.".

Special needs age pension

24. Section 24abq of the Principal Act is amended by adding at the end the following subsection:

"(3) If:

(a) a taxpayer's partner died; and

(b) the taxpayer would have been qualified for payments under a bereavement Subdivision but for an exclusion provision (taxpayer's pension or allowance increased on partner's death to such an extent that no bereavement payments); and

(c) the taxpayer derives payments of special needs age pension under section 772 of the Social Security Act 1991 on one or more of the 7 pension paydays after the death;

then those payments on that payday or each of those paydays are not treated under subsection (1) but as follows:

(d) the supplementary amounts are exempt;

(e) so much of the balance as exceeds what would have been the balance (payments less supplementary amounts) if the partner had not died is exempt;

(f) the rest of the balance is not exempt.".

25. Section 24abr of the Principal Act is repealed and the following section is substituted:

Special needs disability support pension

"24abr. (1) Payments of special needs disability support pension under section 773 of the Social Security Act 1991 are exempt.

"(2) Subsection (1) has effect subject to section 24abv (which deals with bereavement payments).".

Special needs wife pension

26. Section 24abs of the Principal Act is amended by adding at the end the following subsections:

"(3) If:

(a) a taxpayer's partner died; and

(b) the taxpayer would have been qualified for payments under a bereavement Subdivision but for an exclusion provision (taxpayer's pension or allowance increased on partner's death to such an extent that no bereavement payments); and

(c) the taxpayer derives payments of special needs wife pension under section 774 of the Social Security Act 1991 on one or more of the 7 pension paydays after the death;

then those payments on that payday or each of those paydays are not treated under that subsection but as follows:

(d) the supplementary amounts are exempt;

(e) so much of the balance as exceeds what would have been the balance (payments less supplementary amounts) if the partner had not died is exempt;

(f) the rest of the balance is not exempt.

"(4) Subsection (3) does not apply to a payday on which item 4 of subsection (1) applies to the taxpayer (payments exempt).".

Age service pension

27. Section 24ace of the Principal Act is amended by adding at the end the following subsection:

"(5) If:

(a) a taxpayer's partner died; and

(b) the taxpayer would have been qualified for payments under a bereavement Subdivision but for an exclusion provision (taxpayer's pension or allowance increased on partner's death to such an extent that no bereavement payments); and

(c) the taxpayer derives payments of age service pension under Division 3 of Part III of the Veterans' Entitlements Act 1986 on one or more of the 7 pension paydays after the death;

then those payments on that day or each of those days are not treated under subsection (1) but as follows:

(d) the supplementary amounts are exempt;

(e) so much of the balance as exceeds what would have been the balance (payments less supplementary amounts) if the partner had not died is exempt;

(f) the rest of the balance is not exempt.".

Invalidity service pension

28. Section 24acf of the Principal Act is amended by adding at the end the following subsections:

"(5) If:

(a) a taxpayer's partner died; and

(b) the taxpayer would have been qualified for payments under a bereavement Subdivision but for an exclusion provision (taxpayer's pension or allowance increased on partner's death to such an extent that no bereavement payments); and

(c) the taxpayer derives, payments of invalidity service pension under Division 4 of Part III of the Veterans' Entitlements Act 1986 on one or more of the 7 pension paydays after the death;

then those payments on that payday or each of those paydays are not treated under subsection (1) but as follows:

(d) the supplementary amounts are exempt;

(e) so much of the balance as exceeds what would have been the balance (payments less supplementary amounts) if the partner had not died is exempt;

(f) the rest of the balance is not exempt.

"(6) Subsection (5) does not apply to a payday on which item 2 of subsection (1) applies to the taxpayer (payments exempt).".

Partner service pension

29. Section 24acg of the Principal Act is amended by omitting from subsection (1) "wife service pension" and substituting "partner service pension".

Carer service pension

30. Section 24ach of the Principal Act is amended by adding at the end the following subsections:

"(5) If:

(a) a taxpayer's partner died; and

(b) the taxpayer would have been qualified for payments under a bereavement Subdivision but for an exclusion provision (taxpayer's pension or allowance increased on partner's death to such an extent that no bereavement payments); and

(c) the taxpayer derives payments of carer service pension under Division 6 of Part III of the Veterans' Entitlements Act 1986 on one or more of the 7 pension paydays after the death;

then those payments on that payday or each of those paydays are not treated under that subsection but as follows:

(d) the supplementary amounts are exempt;

(e) so much of the balance as exceeds what would have been the balance (payments less supplementary amounts) if the partner had not died is exempt;

(f) the rest of the balance is not exempt.

"(6) Subsection (5) does not apply to a payday on which item 3 or 5 of subsection (1) applies to the taxpayer (payments exempt).".

31. After section 26ah of the Principal Act the following section is inserted:

Investment-related lottery winnings to be included in assessable income

"26aj. (1) If:

(a) either:

(i) a loan benefit is provided to a taxpayer, or to another person, in respect of a year of income (in this subsection called the 'current year of income'); or

(ii) an amount (other than loan principal) is paid or credited to a taxpayer, or to another person, during a year of income (in this subsection also called the 'current year of income'); or

(iii) other property or services are provided to a taxpayer, or to another person, during a year of income (in this subsection also called the 'current year of income'); and

(b) the making of a loan, the payment or crediting of the amount,

or the provision of the property or services, as the case may be, is by way of winnings from:

(i) betting (including pool betting); or

(ii) a lottery or other form of gambling; or

(iii) a game with prizes; and

(c) the chance to participate in the betting, lottery, gambling or game (in this subsection called the 'betting chance') was provided:

(i) wholly or partly in respect of an investment held by the taxpayer in or with a third person (who may be an associate of the taxpayer) (in this subsection called the 'investment body'); or

(ii) wholly or partly in relation directly or indirectly to such an investment; and

(d) the betting, lottery, gambling or game was organised by, or on behalf of:

(i) the investment body (either acting alone or together with one or more other persons); or

(ii) an associate of the investment body (either acting alone or together with one or more other persons); and

(e) if the recipient of the loan benefit, amount or property or services, as the case may be, is a person other than the taxpayer—either:

(i) the other person is an associate of the taxpayer; or

(ii) the loan benefit, amount or property or services, as the case may be, is provided under an arrangement to which the taxpayer, or an associate of the taxpayer, is a party; and

(f) no part of the value of the betting chance is included in the assessable income of the taxpayer of any year of income; and

(g) the provision of the betting chance is neither:

(i) a fringe benefit within the meaning of the Fringe Benefits Tax Assessment Act 1986; nor

(ii) a benefit that, apart from paragraph (g) of the definition of 'fringe benefit' in subsection 136 (1) of the Fringe Benefits Tax Assessment Act 1986, would be a fringe benefit within the meaning of that Act;

then:

(h) if subparagraph (a) (i) applies—the taxpayer's assessable income of the current year of income includes the amount (if any) by which the benchmark amount of interest in relation to the loan in respect of the current year of income exceeds the amount of interest that has accrued on the loan in respect of the current year of income; or

(i) if subparagraph (a) (ii) applies—the taxpayer's assessable income of the current year of income includes the amount paid or credited; or

(j) if subparagraph (a) (iii) applies—the taxpayer's assessable income of the current year of income includes the arm's length value of the property or services, reduced by the recipient's contribution (if any).

"(2) If:

(a) apart from this subsection, an amount (in this subsection called the 'gross assessable amount') is included in a taxpayer's assessable income of a year of income under paragraph (1) (h) in respect of a loan benefit; and

(b) assuming that:

(i) the recipient of the loan benefit had, on the last day of the period (in this subsection called the 'loan period') during the year of income when the recipient was under an obligation to repay the whole or any part of the loan, incurred and paid unreimbursed interest (in this subsection called the 'gross interest'), in respect of the loan, in respect of the loan period; and

(ii) the amount of the gross interest was equal to the benchmark amount of interest in relation to the loan in respect of the year of income;

a once-only deduction (in this subsection called the 'gross deduction') would, or would apart from section 82A, and Subdivision F of Division 3, have been allowable to the recipient in respect of the gross interest;

the gross assessable amount is reduced by:

(c) if no interest accrued on the loan in respect of the loan period— the amount of the gross deduction; or

(d) in any other case—the amount worked out using the formula:

where:

'Gross deduction' means the amount of the gross deduction;

'Reducing amount' means the amount (if any) that would, or that would apart from section 82a, and Subdivision F of Division 3, have been allowable as a once-only deduction to the recipient in respect of the interest that accrued on the loan in respect of the loan period if that interest had been incurred and paid by the recipient on the last day of the loan period.

"(3) If:

(a) apart from this subsection, an amount (in this subsection called the 'gross assessable amount') is included in a taxpayer's

assessable income of a year of income under paragraph (1) (j) in respect of the provision of property or services; and

(b) assuming that:

(i) the recipient of the property or services had, at the time the property or services were provided, incurred and paid unreimbursed expenditure in respect of the provision of the property or services; and

(ii) the expenditure was equal to the amount of the arm's length value of the property or services;

a once-only deduction would, or would apart from section 82a, and Subdivision F of Division 3, have been allowable to the recipient in respect of a percentage (in this subsection called the 'deductible percentage') of the expenditure;

the gross assessable amount is reduced by the deductible percentage.

"(4) For the purposes of the application of this section to a taxpayer, if a person (in this subsection called the 'provider') makes a loan to another person (who may be the taxpayer) (in this subsection called the 'recipient'):

(a) the making of the loan is taken to constitute a loan benefit provided by the provider to the recipient; and

(b) that loan benefit is taken to be provided in respect of each year of income of the taxpayer during the whole or part of which the recipient is under an obligation to repay the whole or any part of the loan.

"(5) For the purposes of this section, if a person (in this subsection called the 'provider') makes a deferred interest loan (in this subsection called the 'principal loan') to another person (in this subsection called the 'recipient'):

(a) the provider is taken, at the end of:

(i) the period of 6 months commencing on the day on which the principal loan was made; and

(ii) each subsequent period of 6 months;

(being in either case a period during the whole of which the recipient is under an obligation to repay the whole or any part of the principal loan) to have made a loan (in this subsection called the 'deemed loan') to the recipient; and

(b) the amount of the deemed loan is equal to the amount by which the interest (in this subsection called the 'accrued interest') that has accrued on the principal loan in respect of that period exceeds the amount (if any) paid in respect of the accrued interest before the end of that period; and

(c) if any part of the accrued interest becomes payable or is paid after the time when the deemed loan is taken to have been made, the deemed loan is to be reduced accordingly; and

(d) the deemed loan is taken to have been made at a nil rate of interest.

"(6) For the purposes of this section, if no interest is payable in respect of a loan, a nil rate of interest is taken to be payable in respect of the loan.

"(7) For the purposes of this section, a person is taken to be under an obligation to pay or repay an amount even though the amount is not due for payment or repayment.

"(8) For the purposes of this section, if a person does anything that results in the creation of property in another person, the first-mentioned person is taken to have provided that property to the other person at the time when the property comes into existence.

"(9) For the purposes of this section, if:

(a) a particular mode of application of money by a taxpayer in relation to another person (in this subsection called the 'investment body') would not, apart from this subsection, be an investment; and

(b) a chance to participate in:

(i) betting (including pool betting); or

(ii) a lottery or other form of gambling; or

(iii) a game with prizes;

is provided to the taxpayer or a third person:

(iv) wholly or partly in respect of the mode of application of money by the taxpayer; or

(v) wholly or partly in relation directly or indirectly to the mode of application of money by the taxpayer; and

(c) if a cash payment had been provided by the investment body to the taxpayer instead of that chance, the payment would constitute, to any extent, a return on an investment held by the taxpayer in or with the investment body;

the mode of application of money is taken to be an investment held by the taxpayer with the investment body.

"(10) If a ballot is held to determine the order in which loans are to be made by a Starr-Bowkett building society to its members, then the making of a loan in accordance with the ballot is not covered by paragraph (1) (b).

"(11) In this section:

'arm's length value', in relation to property or services, means:

(a) the amount that the recipient could reasonably have been expected to have been required to pay to obtain the property or services from the provider under a transaction where the parties to the transaction are dealing with each other at arm's length in relation to the transaction; or

(b) if such an amount cannot be practically determined—such amount as represents a reasonable valuation of the property or services;

'arrangement' means:

(a) any agreement, arrangement, understanding, promise or undertaking, whether express or implied, and whether or not enforceable, or intended to be enforceable, by legal proceedings; and

(b) any scheme, plan, proposal, action, course of action or course of conduct, whether unilateral or otherwise;

'associate' has the same meaning in relation to a person as that expression has in relation to a person in section 26aab;

'benchmark amount of interest', in relation to a loan, in relation to a year of income, means the amount of interest that would have accrued on the loan in respect of the year of income if the interest was calculated on the daily balance of the loan at the benchmark interest rate in relation to the year of income;

'benchmark interest rate', in relation to a year of income, means the predominant per cent per annum interest rate on new, variable interest rate housing loans to individuals for owner-occupation that is specified, for the June immediately preceding the financial year to which the year of income relates, in the 'Interest Rates and Yields: Banks' table in the Statistical Directory of the Reserve Bank of Australia Bulletin dated July in that financial year;

'deferred interest loan' means a loan in respect of which interest is payable at a rate exceeding nil, other than:

(a) a loan where the whole of the interest is due for payment within 6 months after the loan is made; or

(b) a loan where:

(i) the interest is payable by instalments; and

(ii) the intervals between instalments do not exceed 6 months; and

(iii) the first instalment is due for payment within 6 months after the loan is made;

'investment' means any mode of application of money for the purpose of gaining a return;

'loan' includes:

(a) an advance of money; and

(b) the provision of credit or any other form of financial accommodation; and

(c) the payment of an amount for, on account of, on behalf of or at the request of a person where there is an obligation (whether express or implied) to repay the amount; and

(d) a transaction (whatever its terms or form) which in substance effects a loan of money;

'loan benefit' has the meaning given by subsection (4);

'once-only deduction', in relation to expenditure, means a deduction in a year of income in respect of a percentage of the expenditure where no deduction is allowable in respect of a percentage of the expenditure in any other year of income;

'person' means any of the following:

(a) a company;

(b) a partnership;

(c) a person in the capacity of trustee;

(d) any other person;

'provide':

(a) in relation to property—includes dispose of (whether by assignment, declaration of trust or otherwise); and

(b) in relation to services—includes allow, confer, give, grant or perform;

'recipient's contribution', in relation to property or services, means the amount of any consideration paid to the provider by the recipient in respect of the provision of the property or services, reduced by the amount of any reimbursement paid to the recipient in respect of that consideration;

'return', in relation to an investment, includes interest, income or profit;

'services' includes any benefit, right (including a right in relation to, and an interest in, real or personal property), privilege or facility and, without limiting the generality of the foregoing, includes a right, benefit, privilege, service or facility that is, or is to be, provided under:

(a) an arrangement for or in relation to:

(i) the performance of work (including work of a professional nature), whether with or without the provision of property; or

(ii) the provision of, or the use of facilities for, entertainment, recreation or instruction; or

(iii) the conferring of rights, benefits or privileges for which remuneration is payable in the form of a royalty, tribute, levy or similar exaction; or

(b) a contract of insurance; or

(c) an arrangement for or in relation to the lending of money;

'unreimbursed expenditure' means expenditure no part of which has been reimbursed;

'unreimbursed interest' means interest no part of which has been reimbursed.".

Divisible deductions

32. Section 50g of the Principal Act is amended:

(a) by inserting in paragraph (1) (a) "82bb," after "77f,";

(b) by inserting after paragraph (2) (ja) the following paragraphs:

"(jb) if:

(i) a divisible deduction is allowable to the company in relation to the year of income under section 82bb in respect of allowable environmental impact expenditure incurred by the company at a particular time (in this paragraph called the 'expenditure time'); and

(ii) the expenditure time occurred:

(a) during the year of income; and

(b) before the end of the relevant period;

the amount worked out using the following formula is taken to be an allowable deduction in respect of that relevant period:

where:

'Divisible deduction' means the amount of the divisible deduction;

'Post-expenditure days in relevant period' means the number of whole days in the relevant period that occurred after the expenditure time;

'Post-expenditure days in year' means the number of whole days in the year of income that occurred after the expenditure time;

(jc) if:

(i) a divisible deduction is allowable to the company in relation to the year of income under section 82bb in respect of allowable environmental impact expenditure incurred by the company; and

(ii) the year of income is not the year of income in which the expenditure was incurred;

the amount worked out using the following formula is taken to be an allowable deduction in respect of that relevant period:

where:

'Divisible deduction' means the amount of the divisible deduction;

'Days in relevant period' means the number of whole days in the relevant period;".

Tax-related expenses

33. Section 69 of the Principal Act is amended by inserting in subsection (6) ", other than subsection 51 (1)" after "section 51" (first occurring).

Deductions for petroleum resource rent tax payments

34. Section 72a of the Principal Act is amended:

(a) by inserting in subsections (1) and (2) ", or an instalment of petroleum resource rent tax," after "rent tax";

(b) by inserting after subsection (2) the following subsection:

"(2a) A reference in subsections (1) and (2) to a payment of an amount of petroleum resource rent tax does not include a reference to a payment under paragraph 99 (c) of the Petroleum Tax Act.";

(c) by inserting in paragraphs (3) (a) and (4) (a) ", or instalment of petroleum resource rent tax," after "rent tax";

(d) by inserting in paragraphs (3) (a) and (4) (a) ", or would apart from subsection (2a) have been allowable," after "allowable";

(e) by inserting after paragraph (3) (a) the following paragraph:

"(aa) under paragraph 99 (d) of the Petroleum Tax Act, the Commissioner credits an amount paid by a taxpayer in respect of an instalment of petroleum resource rent tax, where a deduction for that amount has been allowed or is allowable to the taxpayer for a year of income; or";

(f) by omitting from subparagraphs (3) (b) (i) and (4) (b) (i) Petroleum Resource Rent Tax Assessment Act 1987" and substituting "Petroleum Tax Act";

(g) by inserting in subsections (3) and (4) "credited," after "received,";

(h) by inserting after paragraph (4) (a) the following paragraph:

"(aa) under paragraph 99 (d) of the Petroleum Tax Act, the Commissioner credits an amount paid by a taxpayer as agent or trustee in respect of an instalment of petroleum resource rent tax, where a deduction for that amount has been allowed or is allowable to the taxpayer for a year of income; or";

(i) by omitting subsection (5) and substituting the following subsection:

"(5) In this section:

'instalment of petroleum resource rent tax' means an instalment of tax payable under Division 2 of Part VIII of the Petroleum Tax Act;

'petroleum resource rent tax' means tax imposed by the Petroleum Resource Rent Tax Act 1987, as assessed under the Petroleum Tax Act;

'Petroleum Tax Act' means the Petroleum Resource Rent Tax Assessment Act 1987.".

Expenditure on research and development activities

35. Section 73b of the Principal Act is amended:

(a) by omitting "during the deduction period" from the definitions of "building expenditure", "contracted expenditure", "plant expenditure", "research and development expenditure" and "salary expenditure" in subsection (1) (wherever occurring) and substituting "on or after 1 July 1985";

(b) by omitting "during the period commencing on 20 November 1987 and ending at the end of the deduction period" from paragraph (c) of the definition of "contracted expenditure" in subsection (1) and substituting "on or after 20 November 1987";

(c) by omitting "during the period concerned" (last occurring) in the definition of "contracted expenditure" in subsection (1) and substituting "on or after the date concerned, or during the period concerned, as the case may be";

(d) by omitting "and before the end of the deduction period" from the definition of "core technology expenditure" in subsection (i);

(e) by omitting from subsection (1) the definition of "deduction period";

(f) by omitting from subsection (4) "and before 1 July 1995";

(g) by omitting subsection (16).

Recouped expenditure on research and development activities

36. Section 73c of the Principal Act is amended by omitting from paragraph (2) (a) "during the deduction period" and substituting "on or after 1 July 1985".

Gifts, pensions etc.

37. Section 78 of the Principal Act is amended:

(a) by omitting subparagraphs (1) (a) (xiii), (xxviii), (xxix), (xxxiv), (lxiv), (lxix) and (xcii);

(b) by inserting after subparagraph (1) (a) (cvi) the following subparagraph:

"(cvii) a fund that, when the gift is made, is on the register kept under section 78aa;".

38. After section 78 of the Principal Act the following section is inserted:

Register of Cultural Organisations

"78aa. (1) In this section:

'Arts Department' means the Department of the Arts, Sport, the Environment, Tourism and Territories;

'Arts Minister' means the Minister for the Arts, Tourism and Territories;

'body' means:

(a) a body corporate (including an incorporated association); or

(b) a trust established by a deed or will; or

(c) an unincorporated body established for a public purpose by the Commonwealth, a State or a Territory;

'cultural organisation' means a body with all of the following characteristics:

(a) its principal purpose, or each of its principal purposes, is a cultural purpose;

(b) it does not pay any of its profits or financial surplus, or give any of its property, to its shareholders, members, beneficiaries, controllers or owners, as the case requires;

(c) it has a public fund:

(i) to which gifts of money or property for its cultural purpose or purposes are to be made; and

(ii) to which any interest on money in the fund is to be credited; and

(iii) to which any money derived from the property given to the fund is to be paid; and

(iv) that does not receive any other money or property; and

(v) that is used only to support the body's cultural purpose or purposes;

(d) it has agreed to give the Arts Department, at 6 monthly intervals, statistical data about gifts to that fund during the last 6 months;

(e) it complies with any rules made from time to time by the Treasurer and the Arts Minister to ensure that gifts to that fund are used only to support its cultural purpose or purposes;

'cultural purpose' means the promotion of any of the following:

(a) literature;

(b) music;

(c) one or more of the performing arts;

(d) one or more of the visual arts;

(e) one or more crafts;

(f) design;

(g) film;

(h) video;

(i) television;

(j) radio;

(k) community arts;

(l) Aboriginal arts;

(m) movable cultural heritage;

'gift fund', in relation to a cultural organisation, means the organisation's fund described in paragraph (c) of the definition of 'cultural organisation';

'promotion', in relation to an activity or other matter listed in the definition of cultural purpose, includes:

(a) production, presentation, publication or preservation in relation to the matter; and

(b) the provision of accommodation for the purpose of the matter; and

(c) training in relation to the matter;

'register' means the Register of Cultural Organisations required by subsection (2).

"(2) The Arts Department must keep a register, to be known as the Register of Cultural Organisations, listing such cultural organisations and their gift funds as are required to be on the register because of this section.

"(3) If the Arts Minister is satisfied that a body has all the characteristics of a cultural organisation, he or she is to certify to the Treasurer in writing that the body is a cultural organisation.

"(4) If the Arts Minister has certified to the Treasurer that a body is a cultural organisation, they may, in their discretion, direct the Arts Department in writing to enter the organisation and its gift fund on the register on a specified day on or after the day on which the direction is given.

"(5) In considering whether to give a direction, the Treasurer and the Arts Minister are to take into account the policies and budgetary priorities of the Australian Government.

"(6) If:

(a) before the commencement of this section, the Treasurer and the Arts Minister, or the Arts Minister, announced that a specified body would be entered on the register with effect from a specified day after 24 March 1991 (however the announcement was expressed); and

(b) the Arts Minister is satisfied that, on that commencement, the body had all the characteristics of a cultural organisation (whether or not it had them when the announcement was made);

then:

(c) the Arts Minister is to certify to the Treasurer in writing that the body is a cultural organisation; and

(d) the Treasurer and the Arts Minister are to direct the Arts Department in writing to enter the organisation and its gift fund on the register; and

(e) for the purposes of the application of this Act in relation to the organisation:

(i) the register is taken to have been established on the specified day; and

(ii) the organisation and its gift fund are taken to have been entered on the register on the specified day; and

(iii) if the gift fund was created after the specified day—gifts made to the organisation before the fund's creation are taken to have been made to that fund.

"(7) If:

(a) before the commencement of this section, the Treasurer and the Arts Minister, or the Arts Minister, announced that a specified body would be entered on the register with effect from a specified day after 24 March 1991 (however the announcement was expressed); and

(b) the Arts Minister is not satisfied that, on that commencement, the body had all the characteristics of a cultural organisation (whether or not it had them when the announcement was made);

then, for the purposes of the application of this Act in relation to the body:

(c) the register is taken to have been established on the specified day; and

(d) the body is taken to have been, on the specified day, a cultural organisation with a gift fund; and

(e) the body and its gift fund are taken to have been:

(i) entered on the register on the specified day; and

(ii) removed from the register on the commencement of this section; and

(f) gifts to the body are taken to have been gifts to its gift fund.

"(8) The Treasurer and the Arts Minister may, in their discretion, direct the Arts Department in writing to remove a cultural organisation and its gift fund from the register on a specified day on or after the day on which the direction is given.".

39. After section 82aq of the Principal Act the following Subdivision is inserted:

"Subdivision C—Deductions for expenditure on environmental impact studies

Objects of Subdivision

"82b. The objects of this Subdivision are:

(a) to provide for the deductibility of allowable environmental impact expenditure (section 82bb); and

(b) to allow property used for eligible environmental impact activities to be treated as if it were used for the purpose of producing assessable income (section 82bg).

Interpretation

"82ba. In this Subdivision:

'allowable environmental impact expenditure' has the meaning given by section 82bc;

'eligible environmental impact activity' has the meaning given by section 82bd;

'environment' includes all aspects of the surroundings of humans, whether affecting them as individuals or in social groupings;

'income-producing project', in relation to a taxpayer, means a project that is, or is to be, carried out for the purpose, or for purposes that include the purpose, of producing assessable income (other than assessable income attributable to section 160z) of the taxpayer of any year of income;

'project' includes a proposed project.

Deduction of allowable environmental impact expenditure

"82bb. (1) Subject to this Subdivision, if a taxpayer incurs allowable environmental impact expenditure during a year of income (in this section called the 'current year of income') in connection with an income-producing project of the taxpayer, then:

(a) if:

(i) a decision is made before the end of the current year of income to abandon the project; or

(ii) the project ends before the end of the current year of income;

the expenditure is an allowable deduction for the current year of income; or

(b) if it is not practicable to readily estimate, as at the end of the current year of income, the time when the project will end— 10% of the expenditure is an allowable deduction for:

(i) the current year of income; and

(ii) each of the 9 subsequent years of income; or

(c) if:

(i) none of the above paragraphs apply; and

(ii) it is practicable to readily estimate, as at the end of the current year of income, the year of income (in this paragraph called the 'final year of income') in which the end of the project will occur; and

(iii) the final year of income is one of the 9 years of income subsequent to the current year of income;

equal parts of the expenditure are respectively allowable deductions for:

(iv) the current year of income; and

(v) the final year of income; and

(vi) each of the intervening years of income (if any); or

(d) if:

(i) none of the above paragraphs apply; and

(ii) it is practicable to readily estimate, as at the end of the current year of income, the year of income (in this paragraph called the 'final year of income') in which the end of the project will occur; and

(iii) the final year of income is later than the 9th year of income subsequent to the current year of income;

10% of the expenditure is an allowable deduction for:

(iv) the current year of income; and

(v) each of the 9 subsequent years of income.

"(2) A provision of this Act (including a provision of section 51, other than subsection 51 (1)) that expressly prevents or restricts the operation of section 51 applies in the same way to this section.

Allowable environmental impact expenditure

"82bc. (1) A reference in this Subdivision to allowable environmental impact expenditure of a taxpayer in connection with an income-producing project of the taxpayer is a reference to expenditure (whether of a capital nature or otherwise) incurred by the taxpayer on or after 12 March 1991 to the extent that the expenditure is in respect of eligible environmental impact activities in relation to the project.

"(2) Expenditure is taken not to be allowable environmental impact expenditure to the extent to which a deduction is allowable in respect of that expenditure under a provision of this Act other than section 82bb.

"(3) Expenditure is taken not to be allowable environmental impact expenditure to the extent to which the expenditure is taken into account in calculating an amount of depreciation that is allowable as a deduction.

Eligible environmental impact activities

"82bd. A reference in this Subdivision to an eligible environmental impact activity in relation to an income-producing project is a reference to:

(a) undertaking a study; or

(b) preparing or obtaining a report or other documentation; or

(c) carrying out any other activity;

for the sole or dominant purpose of evaluating the impact, or likely impact, of the project on the environment.

No deduction where expenditure is recouped

"82be. (1) Section 82bb does not apply, and is to be taken never to have applied, to expenditure if:

(a) the taxpayer, whether before or after the commencement of this subsection, receives, or becomes entitled to receive, a recoupment of, or grant in respect of, the expenditure; and

(b) the amount of the recoupment or the grant is not, and will not be, included in the assessable income of the taxpayer of any year of income.

"(2) For the purposes of subsection (1), if a taxpayer receives, or becomes entitled to receive, an amount that constitutes to an unspecified extent a recoupment of, or a grant in respect of, expenditure, then so much of that amount as is reasonable is taken to be a recoupment of, or grant in respect of, that expenditure, as the case requires.

"(3) Section 170 does not prevent the amendment of an assessment at any time for the purpose of giving effect to this section.

Transactions between persons not at arm's length

"82bf. If:

(a) a person has incurred expenditure in connection with a transaction where the parties to the transaction are not dealing with each other at arm's length in relation to the transaction; and

(b) deductions are or have been allowable under this Subdivision in respect of the expenditure; and

(c) the amount of the expenditure is greater or less than is reasonable;

the amount of the expenditure is taken, for all purposes of the application of this Act in relation to the parties to the transaction, to be the amount that would have been reasonable if the parties were dealing with each other at arm's length.

Property used for eligible environmental impact activities taken to be used for the purpose of producing assessable income

"82bg. (1) For the purposes of this Act, if property is used by a taxpayer on or after 12 March 1991 for eligible environmental impact activities in relation to an income-producing project of the taxpayer, that use of the property by the taxpayer is taken to be for the purpose of producing assessable income of the taxpayer.

"(2) Subsection (1) has effect subject to a provision of this Act that expressly provides that a particular use of property is not taken to be for the purpose of producing assessable income.".

40. Before section 110 of the Principal Act the following heading is inserted:

"Subdivision A—General provisions".

Expenses of general management

41. Section 113 of the Principal Act is amended by inserting in subsection (4) ", other than subsection 51 (1)" after "section 51" (first occurring).

42. After section 116d of the Principal Act the following Subdivision is inserted:

"Subdivision B—Tax treatment of matters relating to life insurance policy holders' protection levies

Interpretation

"116da. In this Subdivision:

'Collection Act' means the Life Insurance Policy Holders' Protection Levies Collection Act 1991;

'final winding-up payment' has the same meaning as in the Collection Act;

'grant' has the same meaning as in the Collection Act;

'protection levy' has the same meaning as in the Collection Act;

'winding-up advance' has the same meaning as in the Collection Act.

Deduction for protection levy

"116db. Protection levy incurred by a taxpayer is an allowable deduction for the year of income in which the protection levy is incurred.

Deduction for protection levy relates to non-fund assessable income

"116dc. For the purposes of Subdivision A, a deduction allowable to a taxpayer under section 116db is taken to relate exclusively to non-fund assessable income of the taxpayer.

Assessable income to include winding-up advances and final winding-up payments

"116dd. The assessable income of a taxpayer of a year of income includes a winding-up advance or a final winding-up payment payable to the taxpayer in the year of income.

Winding-up advances and final winding-up payments to be non-fund assessable income

"116de. For the purposes of Subdivision A, an amount included in a taxpayer's assessable income under section 116dd is taken to be non-fund assessable income of the taxpayer.

Tax treatment of transfer of equity in Fund

"116df. If:

(a) a scheme covered by section 19 of the Collection Act makes provision for a transfer of the kind mentioned in that section; and

(b) the transferee pays or gives consideration to the transferor in respect of the transfer;

then:

(c) the amount or value of the consideration is included in the assessable income of the transferor for the year of income in which it was incurred by the transferee; and

(d) for the purposes of Subdivision A, an amount included in a taxpayer's assessable income under paragraph (c) is taken to be non-fund assessable income of the taxpayer; and

(e) the amount or value of the consideration is a deduction allowable to the transferee for the year of income in which it was incurred; and

(f) for the purposes of Subdivision A, a deduction allowable to a taxpayer under paragraph (e) is taken to relate exclusively to non-fund assessable income of the taxpayer.

Grant exempt from income tax

"116dg. A grant is exempt from income tax.

Amendment of assessments—remission or refund of protection levy

"116dh. (1) Section 170 does not prevent the amendment of an assessment for the purpose of giving effect to section 116db.

"(2) The following are examples of situations which could result in such an amendment being made:

(a) the remission of the whole or a part of an amount of protection levy;

(b) the refund or other application of an overpayment of protection levy.

"(3) For the purposes of section 116db, the effect of a remission of protection levy is that the amount remitted is taken never to have been incurred.

Assessability provisions not to affect meaning of "fund assessable income" when used in Subdivision A

"116dj. Section 116de and paragraph 116df (d) are enacted for the avoidance of doubt and do not, by implication, affect the meaning of 'fund assessable income' when used in Subdivision A.

This Subdivision to be primary code for tax treatment of matters relating to protection levy

"116dk. If any of the following events happen:

(a) a taxpayer incurs protection levy;

(b) a taxpayer derives a winding-up advance or a final winding-up payment;

(c) a transfer of the kind mentioned in section 19 of the Collection Act;

(d) the payment or giving of consideration in respect of such a transfer by the transferee to the transferor;

(e) the remission of the whole or a part of an amount of protection levy;

(f) the refund or other application of an overpayment of protection levy;

the event is to be ignored in determining:

(g) whether an amount is included in the assessable income of a taxpayer under a provision of this Act other than this Subdivision or Part IIIa; or

(h) whether an amount is allowable as a deduction to a taxpayer under a provision of this Act other than this Subdivision; or

(i) whether Part IIIa applies in respect of the disposal of an asset.".

Exploration and prospecting expenditure

43. Section 122j of the Principal Act is amended by omitting from subsection (1) and subparagraph (4d) (b) (i) "on any mining tenements".

Deduction of expenditure on rehabilitation-related activities

44. Section 124ba of the Principal Act is amended by inserting in subsection (2) ", other than subsection 51 (1)" after "section 51" (first occurring).

Application of credits

45. Section 160an of the Principal Act is amended by inserting after subsection (3) the following subsection:

"(3a) Subsection (3) does not apply for the purposes of Division 2 of Part IIIaa (which deals with franking credits and debits).".

Interpretation

46. Section 160apa of the Principal Act is amended:

(a) by omitting subparagraph (a) (i) of the definition of "applicable general company tax rate";

(b) by inserting "company" after "on account of in subparagraph (a) (ib) of the definition of "applicable general company tax rate";

(c) by inserting after subparagraph (a) (ib) of the definition of "applicable general company tax rate" the following subparagraphs:

"(iba) the payment of a final payment of tax in respect of a year of income under section 221azd;

(ibb) the making of a payment by a company of, or on account of, company tax in respect of a year of income where the payment is covered by section 160apmd;";

(d) by inserting after subparagraph (a) (ic) of the definition of "applicable general company tax rate" the following subparagraphs:

"(id) the payment of a refund to a company of an amount paid by the company in respect of a year of income where the refund is covered by section 160apyba;

(ie) the application by the Commissioner of an amount paid by a company in respect of a year of income where the application is covered by section 160apyba;";

(e) by omitting "assessment or" from subparagraph (a) (ii) of the definition of "applicable general company tax rate";

(f) by omitting "the formula" from paragraph (aa) of the definition of "applicable general company tax rate" and substituting "a formula";

(g) by omitting subparagraph (aa) (i) of the definition of "applicable general company tax rate" and substituting the following subparagraph:

"(i) sections 160apvba to 160apvd (inclusive);";

(h) by omitting "160aqch" from subparagraph (aa) (ii) of the definition of "applicable general company tax rate" and substituting "160aqcl";

(i) by inserting "(except as provided by subsection 160an (3a))" after "includes" in the definition of "paid";

(j) by omitting paragraph (b) of the definition of "termination time" and substituting the following paragraph:

"(b) in relation to the payment of an initial payment of tax under section 221ap in respect of a year of income— the earlier of the following times:

(i) the time at which the company receives an amount as a refund of that payment under whichever of the following provisions is applicable:

(a) subsection 221aq (3);

(b) subsection 221ar (6);

(c) subsection 221au (4);

(ii) whichever of the following is applicable:

(a) if the company is required to make a payment under section 221azd in respect of the year of income—the day on which that payment is made;

(b) in any other case—on the day that would have been applicable under subparagraph 166a (a) (i) if the company had been required to make such a payment under section 221azd; or";

(k) by omitting the definition of "company tax instalment";

(l) by omitting the definition of "liability reduction action" and substituting the following definition:

" 'liability reduction action', in relation to a company, means action seeking a reduction in an amount of company tax;".

47. After section 160apka of the Principal Act the following section is inserted:

No credits of a registered organization

"160apkb. A franking credit of a registered organization does not arise after 3 p.m., by standard time in the Australian Capital Territory, on 20 August 1991.".

Repeal of section 160apm

48. Section 160apm of the Principal Act is repealed.

Subsequent payments of tax before determination of taxable income

49. Section 160apmb of the Principal Act is amended by inserting "company" after "on account of.

50. After section 160apmb of the Principal Act the following sections are inserted:

Final payment of tax

"160apmc. If, on a particular day, a company makes a final payment of tax in respect of a year of income under section 221azd, there arises on that day a franking credit of the company equal to the adjusted amount in relation to the amount of that payment.

Payments of tax made after the final payment of tax

" 160apmd. If, on a particular day:

(a) a company makes a payment of, or on account of, company tax in respect of an eligible year of income; and

(b) that payment is not covered by section 160apma, 160apmb or 160apmc;

there arises, on the day on which that payment is made, a franking credit of the company equal to the adjusted amount in relation to the amount of that payment.".

Repeal of sections 160apn and 160apna

51. Sections 160apn and 160apna of the Principal Act are repealed.

Receipt of franked dividends

52. Section 160app of the Principal Act is amended by omitting subsection (4).

Receipt of franked dividends through trusts and partnerships

53. Section, 160apq of the Principal Act is amended by omitting subsection (2).

54. After section 160apq of the Principal Act the following sections are inserted:

Payment of excess offset

"160apqa. If, on a particular day, a company makes a payment of an excess amount that:

(a) is covered by section 160aqr; and

(b) relates to an offset to which the company is entitled;

there arises on that day a franking credit of the company equal to the adjusted amount in relation to the amount of the payment.

Payment of excess foreign tax credit

"160apqb. If, on a particular day, a company makes a payment of an excess amount that:

(a) is covered by subsection 160an (5); and

(b) relates to a foreign tax credit allowable in respect of tax paid or payable by the company in respect of income derived by the company in an eligible year of income;

there arises on that day a franking credit of the company equal to the adjusted amount in relation to the amount of the payment.".

Repeal of sections 160apr, 160aps and 160apt

55. Sections 160apr, 160aps and 160apt of the Principal Act are repealed.

56. Sections 160apva and 160apvb of the Principal Act are repealed and the following sections are substituted:

Life assurance companies—credit reducing section 160apyba debit

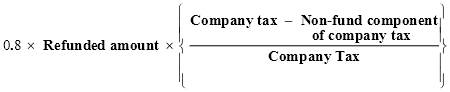

"160apvba. (1) If, on a particular day, a franking debit of a life assurance company arises under section 160apyba in relation to the refund or application of an amount paid by the company in respect of a year of income, there arises on that day a franking credit of the company worked out under subsection (2) of this section.

"(2) The amount of the franking credit is equal to the adjusted amount in relation to the amount calculated using the formula:

where:

'Refunded/applied amount' means the amount refunded or applied;

'Company tax' means the company tax assessed to the company for the year of income;

'Non-fund component of company tax' means so much of the company tax assessed to the company for the year of income as is attributable to the non-fund component.

Life assurance companies—credit reducing section 160apybb debit

"160apvbb. (1) If, on a particular day, a franking debit of a life assurance company arises under section 160apybb in relation .to the payment or application of a foreign tax credit in respect of tax paid or payable by a company in respect of a year of income, there arises on that day a franking credit of the company worked out under subsection (2) of this section.

"(2) The amount of the franking credit is equal to the adjusted amount in relation to the amount calculated using the formula:

where:

'Foreign tax credit paid or applied' means the amount paid or applied;

'Non-fund component of foreign tax credit paid or applied' means so much of the foreign tax credit paid or applied as is attributable to the non-fund component in relation to the year of income.".

Life assurance companies—credits reducing section 160apyb debit

57. Section 160apvc of the Principal Act is amended:

(a) by omitting from subsection (1) "in this section" and substituting "in subsection (2) of this section";

(b) by adding at the end the following subsections:

"(3) If:

(a) on a particular day, a franking debit of a life assurance company arises under section 160apyb in relation to an amount received as a refund in relation to a year of income; and

(b) on or after that day, a notice of an original company tax assessment for the year of income is served, or deemed to be served, on the company;

there arises, on the day on which the notice is served or deemed to be served, a franking credit of the company worked out under subsection (4) of this section.

"(4) The amount of the franking credit is equal to the adjusted amount in relation to the amount calculated using the formula:

where:

'Refunded amount' means the amount received as a refund;

'Company tax' means the company tax assessed to the company for the year of income;

'Non-fund component of company tax' means so much of the company tax assessed to the company for the year of income as is attributable to the non-fund component.".

58. Section 160apve of the Principal Act is repealed and the following sections are substituted:

Life assurance companies—credit reducing subsection 160aqcd (1) debit

"160apvf. If:

(a) on a particular day, a franking debit of a life assurance company arises under subsection 160aqcd (1) in relation to an initial payment of tax in respect of a year of income; and

(b) on or after that day, a notice of an original company tax assessment for the year of income is served, or deemed to be served, on the company;

there arises, on the day on which the notice is served or deemed to be served, a franking credit of the company equal to the amount of the franking debit.

Life assurance companies—credit reducing subsection 160aqce (1) debit

"160apvg. If:

(a) on a particular day, a franking debit of a life assurance company arises under subsection 160aqce (1) in relation to a further payment on account of tax in respect of a year of income; and

(b) on or after that day, a notice of an original company tax assessment for the year of income is served, or deemed to be served, on the company;

there arises, on the day on which the notice is served or deemed to be served, a franking credit of the company equal to the amount of the franking debit.".

59. After section 160apwa of the Principal Act the following section is inserted:

No debits of a registered organization

"160apwb. A franking debit of a registered organization does not arise after 3 p.m., by standard time in the Australian Capital Territory, on 20 August 1991.".

Repeal of sections 160apy, 160apya and 160apyaa

60. Sections 160apy, 160apya and 160apyaa of the Principal Act are repealed.

61. After section 160apyb of the Principal Act the following sections are inserted:

Refunds of company tax

"160apyba. If:

(a) a company makes a payment covered by section 160apma, 160apmb, 160apmc or 160apmd; and

(b) either:

(i) the company receives an amount as a refund of that payment (not being a refund covered by section 160apyb); or

(ii) the Commissioner applies the payment against a liability of the company; and

(c) the amount refunded or applied, as the case may be, is not attributable to a reduction of company tax covered by section 160apz;

there arises, on the day on which the company receives the refund, or on the day on which that payment is applied, as the case may be, a franking debit of the company equal to the adjusted amount in relation to the amount received or applied, as the case requires.

Foreign tax credits—actual payment or application against non-franking credit liabilities

"160apybb. If:

(a) a company receives a payment of a foreign tax credit under subsection 160an (1); or

(b) a foreign tax credit to which a company is entitled is applied

by the Commissioner under subsection 160an (2) against a liability of the company other than:

(i) a liability for company tax in respect of an eligible year of income; or

(ii) a liability under Division 1b of Part VI; or

(iii) a liability under subsection 160an (5); or

(iv) a liability under section 160aqr;

there arises, on the day on which the payment is made, or on the day on which that credit is applied, as the case may be, a franking debit of the company equal to the adjusted amount in relation to the amount paid or applied, as the case requires.".

Repeal of sections 160aq and 160aqa

62. Sections 160aq and 160aqa of the Principal Act are repealed.

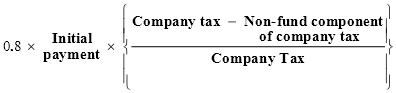

Life assurance companies—debits reducing section 160apma credit

63. Section 160aqcd of the Principal Act is amended:

(a) by omitting from subsection (1) "in this section" and substituting "in subsection (2) of this section";

(b) by adding at the end the following subsections:

"(3) If:

(a) on a particular day, a franking credit of a life assurance company arises under section 160apma in relation to an initial payment of tax that the company is required to make under section 221ap in respect of a year of income; and

(b) on or after that day, a notice of an original company tax assessment for the year of income is served, or deemed to be served, on the company;

there arises, on the day on which the notice is served or deemed to be served, a franking debit of the company worked out under subsection (4) of this section.

"(4) The amount of the franking debit is equal to the adjusted amount in relation to the amount calculated using the formula:

where:

'Initial payment' means the initial payment of tax;

'Company tax' means the company tax assessed to the company for the year of income;

'Non-fund component of company tax' means so much of the company tax assessed to the company for the year of income as is attributable to the non-fund component.".

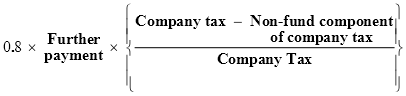

Life assurance companies—debits reducing section 160apmb credit

64. Section 160aqce of the Principal Act is amended:

(a) by omitting from subsection (1) "in this section" and substituting "in subsection (2) of this section";

(b) by adding at the end the following subsections:

"(3) If:

(a) on a particular day, a franking credit of a life assurance company arises under section 160apmb in relation to a further payment on account of tax in respect of a year of income; and

(b) on or after that day, a notice of an original company tax assessment for the year of income is served, or deemed to be served, on the company;

there arises, on the day on which the notice is served or deemed to be served, a franking debit of the company worked out under subsection (4) of this section.

"(4) The amount of the franking debit is equal to the adjusted amount in relation to the amount calculated using the formula:

where:

'Further payment' means the amount of the further payment;

'Company tax' means the company tax assessed to the company for the year of income;

'Non-fund component of company tax' means so much of the company tax assessed to the company for the year of income as is attributable to the non-fund component.".

65. Sections 160aqcf, 160aqcg and 160aqch of the Principal Act are repealed and the following sections are substituted:

Life assurance companies—debit reducing section 160apmc credit

"160aqcj. (1) If, on a particular day, a franking credit of a life assurance company arises under section 160apmc in relation to a final payment of tax in respect of a year of income, there arises on that day a franking debit of the company worked out under subsection (2) of this section.

"(2) The amount of the franking debit is equal to the adjusted amount in relation to the amount calculated using the formula:

where:

'Final payment' means the amount of the final payment;

'Company tax' means the tax assessed to the company for the year of income;

'Non-fund component of company tax' means so much of the company tax assessed to the company for the year of income as is attributable to the non-fund component.

Life assurance companies—debit reducing section 160apmd credit

"160aqck. (1) If, on a particular day, a franking credit of a life assurance company arises under section 160apmd in relation to a payment of, or on account of, company tax in respect of a year of income, there arises on that day a franking debit of the company worked out under subsection (2) of this section.

"(2) The amount of the franking debit is equal to the adjusted amount in relation to the amount calculated using the formula:

where:

'Payment' means the amount of the payment;

'Company tax' means the company tax assessed to the company for the year of income;

'Non-fund component of company tax' means so much of the company tax assessed to the company for the year of income as is attributable to the non-fund component.

Life assurance companies—debit reducing section 160apqb credit

"160aqcl. (1) If, on a particular day, a franking credit of a life assurance company arises under section 160apqb in relation to a payment of an excess amount in respect of a foreign tax credit allowable in relation to a year of income, there arises on that day a franking debit of the company worked out under subsection (2) of this section.

"(2) The amount of the franking debit is equal to the adjusted amount in relation to the amount calculated using the formula:

where:

'Excess amount' means the amount of the excess;

'Non-fund component of excess amount' means so much of the excess amount as is attributable to the non-fund component in relation to the year of income.

Life assurance companies—debit reducing subsection 160apvc (1) credit

"160aqcm. If:

(a) on a particular day, a franking credit of a life assurance company arises under subsection 160apvc (1) in relation to an amount received as a refund in relation to a year of income; and

(b) on or after that day, a notice of an original company tax assessment for the year of income is served, or deemed to be served, on the company;

there arises, on the day on which the notice is served or deemed to be served, a franking debit of the company equal to the amount of the franking credit.".

Determination of estimated debit

66. Section 160aqd of the Principal Act is amended:

(a) by omitting from paragraph (1) (b) "a company tax instalment or company tax instalments or";

(b) by omitting from paragraph(1) (c) "of the instalment or instalments or";

(c) by inserting after subsection (1) the following subsection:

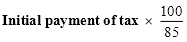

"(1a) An estimated debit in relation to an initial payment of tax must relate to the refund of that payment under subsection 221aq (3), 221ar (6) or 221au (4).".

67. After section 160w of the Principal Act the following section is inserted:

Deemed disposal and re-acquisition of valueless shares in companies in liquidation

"160wa. (1) For the purposes of this Part, if:

(a) a taxpayer owns a share in a company as at a particular time (in this subsection called the 'test time') after 11 November 1991; and

(b) there is a liquidator of the company; and