Taxation Laws Amendment Act (No. 2) 1992

No. 80 of 1992

TABLE OF PROVISIONS

| PART 1—PRELIMINARY |

Section | |

1. | Short title |

2. | Commencement |

| PART 2—AMENDMENT OF THE INCOME TAX ASSESSMENT ACT 1936 |

3. | Principal Act |

4. | Interpretation |

5. | Exemption of pay and allowances of members of Defence Force serving in operational areas |

6. | Exemption of foreign branch profits of Australian companies |

7. | Repeal of section 55 and substitution of new section: |

| 55. Annual depreciation percentage |

8. | Calculation of depreciation |

9. | Special depreciation on property used for basic iron or steel production |

10. | Depreciation roll-over relief for unpooled property where CGT roll-over relief allowed under section 160ZZM, 160ZZMA, 160ZZN, 160ZZNA or 160ZZO or where election for roll-over relief made under section 59AA |

11. | Calculation of depreciation—pooled property |

12. | Expenditure on research and development activities |

13. | Recouped expenditure on research and development activities |

14. | Reduction of deductions |

15. | Gifts, pensions etc. |

16. | Deduction for contributions to eligible superannuation fund for employees |

17. | Interpretation |

TABLE OF PROVISIONS—continued

Section | |

18. | Deduction in respect of new plant installed on or after 1 January 1976 |

19. | Interpretation |

20. | Exemption of income attributable to certain policies etc. |

21. | Insertion of new section: |

| 112C. Exemption of income attributable to policies issued by foreign permanent establishments |

22. | Residual amounts |

23. | Assets to which Part applies |

24. | Asset passing to personal representative or beneficiary |

25. | Part applies in respect of disposals of assets |

26. | Asset bequeathed to tax-advantaged person etc. |

27. | Capital gains and capital losses |

28. | Consideration in respect of disposal |

29. | Transfer of net capital loss within company group |

30. | Election to treat grant of long term lease as disposal of freehold interest or head lease |

31. | Payments for variation of lease |

32. | Consideration for disposal |

33. | Insertion of new section: |

| 160ZYJA. Employee share trusts |

34. | Conversion of note not to constitute disposal |

35. | Conversion of note not to constitute disposal |

36. | Involuntary disposal |

37. | Asset received as a result of involuntary disposal |

38. | Transfer of asset between spouses upon breakdown of marriage |

39. | Transfer of assets from company or trust to spouse upon breakdown of marriage |

40. | Transfer of asset to wholly-owned company |

41. | Transfer of partnership assets to wholly-owned company |

42. | Transfer of asset between companies in the same group |

43. | Exchange of shares in the same company |

44. | Principal residence |

45. | Exemption of part of gain attributable to goodwill |

46. | Insertion of new section: |

| 160ZZRAA. Calculation of ‘exemption threshold’ for purposes of section 160ZZR |

47. | Interpretation |

48. | Shares in, and loans to, transferor—deemed disposal and re-acquisition |

49. | Equity interest in transferee—compensatory increase in cost base etc. |

50. | When asset acquired |

51. | Keeping of records |

52. | Interpretation |

53. | Prescribed persons |

54. | Interpretation |

55. | Widely distributed finance shares |

56. | Insertion of new section: |

| 327B Transitional finance shares |

57. | Direct attribution interest in a CFC or CFT |

58. | Direct attribution account interest in a company |

59. | Notional allowable deduction for eligible finance share dividends, widely distributed finance share dividends and transitional finance share dividends |

60. | Additional notional exempt income—unlisted or listed country CFC |

61. | Elections under CGT roll-over provisions |

62. | Roll-overs—asset disposals |

63. | Tainted sales income |

64. | Assessability in respect of certain dividends deemed to be paid by a CFC under section 47A |

65. | Application of amendments—general |

66. | Application of amendments—depreciation |

67. | Application of amendments—capital gains tax |

68. | Application of amendments—CFCs |

69. | Transitional—sections 160J and 160ZZQ of the amended Act |

TABLE OF PROVISIONS—continued

Section | |

70. | Transitional—section 160ZYZ of the Principal Act |

71. | Transitional—section 160ZZBB of the Principal Act |

72. | Transitional—Division 19A of Part IIIA of the Principal Act |

73. | Transitional—subsection 160ZZS(2A) of the amended Act |

74. | Transitional—Part X record-keeping offences |

75. | Amendment of assessments |

| PART 3—DEFERRAL OF INITIAL PAYMENTS OF COMPANY TAX FOR 1991-92 |

| Division 1—Interpretation |

76. | Interpretation |

| Division 2—Deferral of initial payments of tax for 1991-92 |

77. | 9-week deferral of initial payments of tax for 1991-92 |

| Division 3—Deferred initial payments of tax for 1991-92 to be offset by prior payments of franking deficit tax |

78. | Deferred initial payments of tax for 1991-92 to be offset by prior payments of franking deficit tax |

79. | IP offset provision to be ignored in calculating certain company tax thresholds |

80. | Eliminated or reduced initial payments of tax to be treated as fully paid for credit/refund purposes |

81. | Franking credits and debits—effect of elimination or reduction of initial payment of tax |

82. | Reduction of liability for franking deficit tax |

83. | No refunds of amounts of franking deficit tax overpaid because of the FDT reduction provision |

84. | Reduction of liability for franking deficit tax does not give rise to a franking credit under section 160APQA of the Assessment Act |

Taxation Laws Amendment Act (No. 2) 1992

No. 80 of 1992

An Act to amend the law relating to taxation

An Act to amend the law relating to taxation

[Assented to 30 June 1992]

The Parliament of Australia enacts:

PART 1—PRELIMINARY

Short title

1. This Act may be cited as the Taxation Laws Amendment Act (No. 2) 1992.

Commencement

2.(1) Subject to this section, this Act commences on the day on which it receives the Royal Assent.

(2) If the day (in this subsection called the “TLAA day”) on which the Taxation Laws Amendment Act 1992 receives the Royal Assent is a later day than the day on which this Act receives the Royal Assent, sections 7, 8, 9, 10, 11, 18, 22, 54 to 59 (inclusive), subsection 60(1), section 66, subsections 68(1), (2), (3) and (4) and section 74 commence on the day after the TLAA day.

(3) Subsections 52(2) and 53(2) commence on the day after the day on which this Act receives the Royal Assent.

PART 2—AMENDMENT OF THE INCOME TAX ASSESSMENT ACT 1936

Principal Act

3. In this Part, “Principal Act” means the Income Tax Assessment Act 19361.

Interpretation

4. Section 6 of the Principal Act is amended by omitting subparagraph (a)(iii) of the definition of “resident” or “resident of Australia” in subsection (1) and substituting the following subparagraph:

“(iii) who is:

(A) a member of the superannuation scheme established by deed under the Superannuation Act 1990; or

(B) an eligible employee for the purposes of the Superannuation Act 1976; or

(C) the spouse, or a child under 16, of a person covered by sub-subparagraph (A) or (B); and”.

Exemption of pay and allowances of members of Defence Force serving in operational areas

5. Section 23AC of the Principal Act is amended:

(a) by inserting after paragraph (2)(ca) the following paragraph:

“(cb) if the operational area is Cambodia—there is in force a certificate in writing issued by the Chief of the Defence Force to the effect that the allotment concerned was in respect of the member’s service as part of:

(i) the group called the United Nations Advance Mission in Cambodia; or

(ii) the group called the United Nations Transitional Authority in Cambodia;”;

(b) by inserting after subsection 23AC(2) the following subsections:

“(2A) A certificate issued in accordance with paragraph (2)(cb) shall cease to have force only in accordance with a certificate of revocation signed by the Chief of the Defence Force.

“(2B) A certificate of revocation made in accordance with subsection (2A) is a disallowable instrument for the purposes of section 46A of the Acts Interpretation Act 1901.”;

(c) by omitting from paragraph (3)(b) “9 June 1991” and

substituting “the termination date (if any) applicable to the operational area”;

(d) by omitting “or (ca)” from subsections (4) and (5) and substituting “, (ca) or (cb)”;

(e) by inserting after subsection (6A) the following subsection:

“(6B) For the purposes of this section, the area comprising Cambodia is taken to have become an operational area on 20 October 1991.”;

(f) by inserting in subsection (7) the following definition:

“ ‘termination date’, in relation to an operational area covered by subsection (6) or (6A), means 9 June 1991;”;

(g) by omitting “or (6A)” from the definition of “operational area” in subsection (7) and substituting “, (6A) or (6B)”.

Exemption of foreign branch profits of Australian companies

6. Section 23AH of the Principal Act is amended:

(a) by omitting subsection (3) and substituting the following subsection:

“(3) If:

(a) the original taxpayer in relation to the foreign branch income is the trustee of a trust estate or a partnership; and

(b) the following conditions are satisfied in relation to another taxpayer (in this subsection called the ‘actual taxpayer’):

(i) the actual taxpayer is a company;

(ii) either:

(A) the actual taxpayer is a beneficiary of the trust estate or a partner in the partnership; or

(B) one or more partnerships or trusts are interposed between the original taxpayer and the actual taxpayer; and

(c) assuming that:

(i) the foreign branch income derived by the original taxpayer was the only amount included in the original taxpayer’s assessable income of the year of income; and

(ii) no deductions were allowable to the original taxpayer for the year of income; and

(iii) in a case where one or more partnerships or trusts are interposed between the original taxpayer and the actual taxpayer:

(A) the only amounts that are included in the assessable incomes of those interposed

partnerships and trusts are amounts that are attributable (either directly or indirectly through one or more interposed trusts or partnerships) to the foreign branch income; and

(B) no deductions were allowable to any of the interposed partnerships or trusts;

the following conditions would have been satisfied in relation to the actual taxpayer:

(iv) an amount would have been included in the assessable income of the actual taxpayer of a year of income under subsection 92(1) or section 97, 98A or 100;

(v) the whole or a part of the amount so included in the actual taxpayer’s assessable income would have been attributable (either directly or indirectly through one or more interposed trusts or partnerships) to the foreign branch income;

then, for the purposes of the application of Divisions 5 and 6 to the actual taxpayer in relation to any year of income:

(d) the assessable income of the original taxpayer does not include so much of the foreign branch income as is attributable to a period when the actual taxpayer was a resident; and

(e) section 160AFD does not apply to a loss incurred by the original taxpayer to the extent that the loss is attributable to:

(i) any foreign branch income derived by the original taxpayer during any year of income; or

(ii) any foreign branch capital gain which accrued to the original taxpayer during any year of income.”;

(b) by omitting subsections (9) and (9A) and substituting the following subsections:

“(9) If:

(a) the original taxpayer in relation to the foreign branch capital gain is the trustee of a trust estate; and

(b) the following conditions are satisfied in relation to another taxpayer (in this subsection called the ‘actual taxpayer’):

(i) the actual taxpayer is a company;

(ii) either:

(A) the actual taxpayer is a beneficiary of the trust estate; or

(B) one or more partnerships or trusts are

interposed between the original taxpayer and the actual taxpayer; and

(c) assuming that:

(i) the only amount included in the original taxpayer’s assessable income of the year of income concerned is an amount (in this subsection called the ‘foreign branch capital gain amount’) attributable to the foreign branch capital gain; and

(ii) no deductions were allowable to the original taxpayer for that year of income; and

(iii) no capital loss was incurred by the original taxpayer under Part IIIA during that year of income; and

(iv) in a case where one or more partnerships or trusts are interposed between the original taxpayer and the actual taxpayer:

(A) the only amounts that are included in the assessable incomes of those interposed partnerships and trusts are amounts that are attributable (either directly or indirectly through one or more interposed trusts or partnerships) to the foreign branch capital gain amount; and

(B) no deductions were allowable to any of the interposed partnerships or trusts; and

(C) no capital losses were incurred by any of the interposed partnerships or trusts under Part IIIA;

the following conditions would have been satisfied in relation to the actual taxpayer:

(v) an amount would have been included in the assessable income of the actual taxpayer of a year of income under subsection 92(1) or section 97, 98A or 100;

(vi) the whole or a part of the amount so included in the actual taxpayer’s assessable income would have been attributable (either directly or indirectly through one or more interposed trusts or partnerships) to the foreign branch capital gain amount;

then, for the purposes of the application of Divisions 5 and 6 to the actual taxpayer in relation to any year of income:

(d) the assessable income of the original taxpayer does not include so much of the foreign branch capital gain as is attributable to a period when the actual taxpayer was a resident; and

(e) section 160AFD does not apply to a loss incurred by the original taxpayer to the extent that the loss is attributable to:

(i) any foreign branch capital gain which accrued to the original taxpayer during any year of income; or

(ii) any foreign branch income derived by the original taxpayer during any year of income.

“(9A) If:

(a) a taxpayer (in this subsection called the ‘original taxpayer’), being the trustee of a trust estate, disposes of an asset; and

(b) a loss of a capital nature is incurred by the original taxpayer in respect of the disposal; and

(c) if, instead, a gain or profit of a capital nature had accrued to the original taxpayer in respect of the disposal, that gain or profit (which gain or profit is in this subsection called the ‘notional foreign branch capital gain’) would be a foreign branch capital gain; and

(d) a capital loss is incurred by the original taxpayer under Part IIIA in respect of the disposal of the asset; and

(e) the following conditions are satisfied in relation to another taxpayer (in this subsection called the ‘actual taxpayer’):

(i) the actual taxpayer is a company;

(ii) either:

(A) the actual taxpayer is a beneficiary of the trust estate; or

(B) one or more partnerships or trusts are interposed between the original taxpayer and the actual taxpayer; and

(f) assuming that:

(i) the only amount included in the original taxpayer’s assessable income of the year of income concerned is an amount (in this subsection called the ‘notional foreign branch capital gain amount’) attributable to the notional foreign branch capital gain; and

(ii) no deductions were allowable to the original taxpayer for that year of income; and

(iii) no capital loss was incurred by the original taxpayer under Part IIIA during that year of income; and

(iv) in a case where one or more partnerships or trusts are interposed between the original taxpayer and the actual taxpayer:

(A) the only amounts that are included in the

assessable incomes of those interposed partnerships and trusts are amounts that are attributable (either directly or indirectly through one or more interposed trusts or partnerships) to the notional foreign branch capital gain amount; and

(B) no deductions were allowable to any of the interposed partnerships or trusts; and

(C) no capital losses were incurred by any of the interposed partnerships or trusts under Part IIIA;

the following conditions would have been satisfied in relation to the actual taxpayer:

(v) an amount would have been included in the assessable income of the actual taxpayer of a year of income under subsection 92(1) or section 97, 98A or 100;

(vi) the whole or a part of the amount so included in the actual taxpayer’s assessable income would have been attributable (either directly or indirectly through one or more interposed trusts or partnerships) to the notional foreign branch capital gain amount; and

then, for the purposes of the application of Divisions 5 and 6 to the actual taxpayer in relation to any year of income, the assessable income of the original taxpayer is to be worked out on the basis that no such capital loss had been incurred by the original taxpayer.”.

7. Section 55 of the Principal Act is repealed and the following section is substituted:

Annual depreciation percentage

“55.(1) The annual depreciation percentage for a unit of property owned by a taxpayer is worked out as follows.

“(2) [Step 1: 100% depreciation] If:

(a) either:

(i) the cost of the property does not exceed $300 or such higher amount as is prescribed; or

(ii) the effective life of the property is less than 3 years; and

(b) the taxpayer does not nominate, in accordance with subsection (8), an annual depreciation percentage less than 100%;

the annual depreciation percentage is 100%.

“(3) [Step 2: scientific research] If:

(a) step 1 does not apply; and

(b) the property is used by the taxpayer for the purposes of scientific research only; and

(c) either:

(i) the effective life of the property is 5 years or more; or

(ii) the property is an eligible motor vehicle or an eligible artwork; and

(d) the property was acquired by the taxpayer before 1 July 1995; and

(e) the taxpayer does not nominate, in accordance with subsection (8), an annual depreciation percentage less than 50%;

the annual depreciation percentage is 50%.

“(4) [Step 3: employee amenities] If:

(a) neither step 1 nor 2 applies; and

(b) the property is used by the taxpayer principally for the purpose of providing clothing cupboards, first aid, rest-room or recreational facilities, or meals or facilities for meals:

(i) for persons employed by the taxpayer in a business carried on by the taxpayer for the purpose of producing assessable income; or

(ii) for the care of children of those persons; and

(c) either:

(i) the effective life of the property is 5 years or more; or (ii) the property is an eligible motor vehicle or an eligible artwork; and

(d) the taxpayer does not nominate, in accordance with subsection (8), an annual depreciation percentage less than 50%;

the annual depreciation percentage is 50%.

“(5) [Step 4: general rates] If:

(a) none of steps 1, 2 and 3 apply; and

(b) the property is not an eligible motor vehicle; and

(c) the property is not an eligible artwork; and

(d) the taxpayer does not nominate, in accordance with subsection (8), an annual depreciation percentage less than the percentage worked out using the following table;

the annual depreciation percentage is worked out using the following table:

Years in effective life | Annual depreciation percentage |

3 to fewer than 5 | 60% |

5 to fewer than 6⅔ | 40% |

6⅔ to fewer than 10 | 30% |

10 to fewer than 13 | 25% |

13 to fewer than 30 | 20% |

30 or more | 10% |

“(6) [Step 5: special broadbanded rates for eligible motor vehicles] If:

(a) none of steps 1, 2, 3 and 4 apply; and

(b) the property is an eligible motor vehicle; and

(c) the taxpayer does not nominate, in accordance with subsection (8), an annual depreciation percentage less than the percentage worked out using the following table;

the annual depreciation percentage is worked out using the following table:

Years in effective life | Annual depreciation percentage |

3 to fewer than 5 | 50% |

5 to fewer than 6⅔ | 30% |

6⅔ to fewer than 10 | 22.5% |

10 to fewer than 13 | 15% |

13 to fewer than 20 | 11.25% |

20 to fewer than 40 | 7.5% |

40 or more | 3.75% |

“(7) [Step 6: special loaded rates for eligible artworks] If:

(a) none of steps 1, 2, 3, 4 and 5 apply; and

(b) the property is an eligible artwork; and

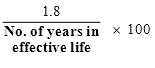

(c) the taxpayer does not nominate, in accordance with subsection (8), an annual depreciation percentage less than the percentage calculated (to 2 decimal places) using the following formula;

the annual depreciation percentage is the percentage calculated (to 2 decimal places) using the formula:

where:

‘No. of years in effective life’ means the number (calculated to 2 decimal places) of years in the effective life of the property.

“(8) A taxpayer may nominate a percentage as the annual depreciation percentage for a specified unit of property in respect of which depreciation is allowable to the taxpayer for a specified year of income if the nominated percentage is less than the percentage that would otherwise be that annual depreciation percentage.

“(9) In this section:

‘eligible artwork’ means:

(a) a painting, sculpture, drawing, engraving or photograph; or

(b) a reproduction of any such thing; or

(c) property of a description, or of a use, similar to anything covered by paragraph (a) or (b);

‘eligible motor vehicle’ means a motor vehicle (including a vehicle known as a four wheel drive vehicle) that is:

(a) a motor car, station wagon, panel van, utility truck or similar vehicle; or

(b) a motor cycle or similar vehicle; or

(c) any other road vehicle designed to carry a load of less than one tonne or fewer than 9 passengers;

‘scientific research’ has the same meaning as in section 73A.”.

Calculation of depreciation

8. Section 56 of the Principal Act is amended by omitting paragraphs (1)(a) and (b) and substituting the following paragraphs:

“(a) the annual depreciation percentage fixed under section 55 of the depreciated value of that unit at the beginning of the year of income; or

(b) if the taxpayer has elected under subsection (1AA) that this paragraph be applied to the unit of property:

(i) if the annual depreciation percentage fixed under section 55 is less than 100%—the percentage worked out using the following formula (rounded to the nearest whole percentage, with 0.5% rounded up) of the cost of the unit:

where:

‘Annual depreciation percentage’ is the annual depreciation percentage fixed under section 55; or

(ii) if the annual depreciation percentage fixed under section 55 is 100%—100% of the cost of the unit.”.

Special depreciation on property used for basic iron or steel production

9. Section 57AK of the Principal Act is amended by inserting in paragraph (5)(a) “as in force immediately before the commencement of section 1 of the Taxation Laws Amendment Act (No. 2) 1992,” after “55,”.

Depreciation roll-over relief for unpooled property where CGT roll-over relief allowed under section 160ZZM, 160ZZMA, 160ZZN, 160ZZNA or 160ZZO or where election for roll-over relief made under section 59AA

10. Section 58 of the Principal Act is amended by omitting from paragraph (4)(d) “2A” and substituting “2”.

Calculation of depreciation—pooled property

11. Section 62AAP of the Principal Act is amended by omitting “1.5 ×” from the formula in subsection (1).

Expenditure on research and development activities

12.(1) Section 73B of the Principal Act is amended by omitting paragraph (3A)(b) and substituting the following paragraph:

“(b) either:

(i) each other partner was:

(A) an eligible company; or

(B) a body corporate that was, or is taken to have been, registered under section 39F of the Industry Research and Development Act 1986 as a research agency in respect of the class of research and development activities on which the expenditure was incurred; or

(ii) the partnership was designated as a Co-operative Research Centre under the program known as the Co-operative Research Centres Program;”.

(2) Section 73B of the Principal Act is amended:

(a) by inserting after paragraph (3A)(d) the following paragraph: “(da) if the partnership is not designated as a Co-operative Research Centre under the program known as the Co-operative Research Centres Program—subsections 73C(2A) and 73D(2A) do not apply in relation to the expenditure that a partner is so taken to have incurred;”;

(b) by inserting in paragraph (1)(f) “, (da)” after “(d)”.

Recouped expenditure on research and development activities

13. Section 73C of the Principal Act is amended by inserting after subsection (2) the following subsection:

“(2A) A reference in this section to a recoupment of, or a grant in respect of, the whole or any part of expenditure incurred by an eligible company on research and development activities that formed or form part of a particular project carried on by or on behalf of the company does not include a reference to a recoupment or grant where the recoupment or grant is made:

(a) by or from the Commonwealth; and

(b) under the program known as the Co-operative Research Centres Program.”.

Reduction of deductions

14. Section 73D of the Principal Act is amended by inserting after subsection (2) the following subsection:

“(2A) A reference in this section to a recoupment of, or a grant in respect of, any of the expenditure incurred by an eligible company on research and development activities that formed or form part of a particular project carried on by or on behalf of the company does not include a reference to a recoupment or grant where the recoupment or grant is made:

(a) by or from the Commonwealth; and

(b) under the program known as the Co-operative Research Centres Program.”.

Gifts, pensions etc.

15. Section 78 of the Principal Act is amended by omitting subparagraph (1)(a)(xlvii) and substituting the following subparagraph:

“(xlvii) the World Wide Fund for Nature Australia;”.

Deduction for contributions to eligible superannuation fund for employees

16. Section 82AAC of the Principal Act is amended by inserting after subsection (2) the following subsection:

“(2A) The rule in subsection (2) does not apply, and is taken never to have applied, in relation to contributions made in a year of income in respect of a particular employee if:

(a) the taxpayer claims, or the taxpayer and the associates of the taxpayer claim, deductions for contributions made to 3 funds only; and

(b) the following conditions are satisfied in relation to any one of those funds:

(i) the fund was established by a law of the Commonwealth, a State or a Territory;

(ii) the fund was in existence at the beginning of 1 July 1990.”.

Interpretation

17. Section 82AAS of the Principal Act is amended by omitting from subsection (1) the definition of “unsupported eligible person” and substituting the following definition:

“ ‘unsupported eligible person’, in relation to a year of income, means a person who is an eligible person in relation to the year of income where:

(a) the person would have been an eligible person in relation to the year of income if subsection (2A) had not been enacted; or

(b) superannuation agreement contributions were made in relation to the person during the year of income in connection with particular employment of, or particular services rendered by, the person and either:

(i) both:

(A) the person’s assessable income of the year of income includes one or more amounts that were derived from that employment or those services; and

(B) the total of the amounts mentioned in sub-subparagraph (A) is less than 10% of the person’s assessable income of the year of income; or

(ii) the person’s assessable income of the year of income does not include any amount that was derived from that employment or those services;”.

Deduction in respect of new plant installed on or after 1 January 1976

18. Section 82AB of the Principal Act is amended by omitting from paragraph (5B)(b) “57AG or” and substituting “57AG, as in force immediately before the commencement of section 1 of the Taxation Laws Amendment Act 1992, or section”.

Interpretation

19. Section 110 of the Principal Act is amended by omitting all the words after “reduced” in the definitions of “modified 160Z gain amount” and “ordinary 160Z gain amount” in subsection (1) and substituting the following words and paragraphs:

“in accordance with the following steps:

(a) if, assuming that the gain were instead income derived during the year of income in which the gain accrued, the whole or a part of the income would have been exempt from tax under

section 112C—reduce the gain by so much of the income as is so exempt;

(b) if the step mentioned in paragraph (a) applies and any part of the gain remains after taking that step—further reduce the remainder of the gain by the proportion of that remainder that would be calculated using the formula in section 112A;

(c) if the step mentioned in paragraph (a) does not apply—reduce the gain by the proportion of the gain that would be calculated using the formula in section 112A;”.

Exemption of income attributable to certain policies etc.

20. Section 112A of the Principal Act is amended:

(a) by inserting in subsection (1) “eligible” before “income derived”;

(b) by omitting from subsection (1) “and eligible non-resident policies” and substituting “(other than eligible non-resident policies)”;

(c) by inserting in subsection (1) “(other than eligible non-resident policies)” after “all policies”;

(d) by omitting from subsection (2) “(other than eligible nonresident policies)”;

(e) by omitting subsection (5) and substituting the following subsection:

“(5) In this section:

‘accounts’ has the same meaning as in Part X;

‘eligible income’, in relation to a company, means income that is not:

(a) exempt from tax under a provision of this Act other than this section; or

(b) derived from the assets described in the accounts of a business carried on by the company at or through a permanent establishment of the company in a foreign country as assets of that business;

‘policy’ means a life assurance policy.”.

21. Before section 113 of the Principal Act the following section is inserted:

Exemption of income attributable to policies issued by foreign permanent establishments

“112C.(1) This section applies to an amount of income derived by a life assurance company during a year of income where:

(a) the income was derived in carrying on a particular business in a particular foreign country at or through a permanent establishment of the company in the foreign country (which business is in this section called the ‘PE business’); and

(b) the income was derived from the assets:

(i) included in an Australian statutory fund of the company or in any other fund maintained by the company in respect of its life assurance business; and

(ii) described in the accounts of the PE business as assets of the PE business; and

(c) the income was derived from sources in a foreign country or foreign countries;

and the amount of income is reduced in proportion to the extent (if any) that the assets were not held to cover liabilities referable to policies issued in the course of carrying on the PE business.

“(2) For each amount of income, the proportion calculated using the following formula is exempt from tax:

Calculated liabilities for eligible non-resident policies |

Total calculated liabilities |

where:

‘Calculated liabilities for eligible non-resident policies’ means so much of the calculated liabilities of the company at the end of the year of income as, in the opinion of the Commissioner, is referable to eligible non-resident policies that:

(a) are included in that fund; and

(b) were issued in the course of carrying on the PE business;

‘Total calculated liabilities’ means so much of the calculated liabilities of the company at the end of the year of income as, in the opinion of the Commissioner, is referable to policies that:

(a) are included in that fund; and

(b) were issued in the course of carrying on the PE business.

“(3) In this section:

‘accounts’ has the same meaning as in Part X;

‘policy’ means a life assurance policy.”.

Residual amounts

22. Section 159GF of the Principal Act is amended by inserting in subparagraph (1)(a)(iii) “, as in force immediately before the commencement of section 1 of the Taxation Laws Amendment Act 1992,” after “57AG”.

Assets to which Part applies

23. Section 160A of the Principal Act is amended by adding at the end “or an interest in such a motor vehicle”.

Asset passing to personal representative or beneficiary

24. Section 160J of the Principal Act is amended:

(a) by omitting “court,” from subparagraph (b)(ii) and substituting “court; or”;

(b) by inserting after subparagraph (b)(ii) the following subparagraph:

“(iii) under a deed of arrangement where:

(A) the deed was entered into in settlement of a claim to participate in the distribution of the estate of the deceased person; and

(B) the consideration (if any) given by the beneficiary for the asset consisted of the variation or waiver of a claim to one or more other assets that formed part of that estate;”.

Part applies in respect of disposals of assets

25. Section 160L of the Principal Act is amended:

(a) by omitting from paragraphs (3)(a) and (4)(a) “immediately before its disposal” and substituting “throughout the period when the asset was owned by the taxpayer”;

(b) by omitting from paragraph (5)(a) “immediately before the disposal” and substituting “throughout the period when the asset was a partnership asset of the partnership”.

Asset bequeathed to tax-advantaged person etc.

26. Section 160Y of the Principal Act is amended:

(a) by omitting from subsection (2) “the following provisions” and substituting “subsections (3) and (4)”;

(b) by inserting after subsection (2) the following subsection:

“(2A) If:

(a) a person died after 2 April 1992; and

(b) an asset that formed part of the estate of the deceased person and was acquired by the deceased person on or after 20 September 1985 has passed to a beneficiary in the estate of the deceased person; and

(c) the deceased person was a resident; and

(d) the beneficiary is a non-resident; and

(e) the asset is not a taxable Australian asset;

section 160X does not apply in respect of the asset but subsections (3) and (4) of this section have effect.”.

Capital gains and capital losses

27.(1) Section 160Z of the Principal Act is amended:

(a) by omitting paragraph (9)(b) and substituting the following paragraph:

“(b) in the case of a taxpayer being a company:

(i) section 50H operates so as to deem a disqualifying event in relation to the company to have occurred at a time during the year of income; and

(ii) the company does not pass the continuity of business test set out in subsection (9A) in relation to that time;”;

(b) by inserting after subsection (9) the following subsection:

“(9A) For the purposes of paragraph (9)(b), a company passes the continuity of business test in relation to a time (in this subsection called the ‘event time’) during a year of income if, and only if:

(a) the company carried on at all times during the year of income the same business as it carried on immediately before the event time; and

(b) the company did not, at any time during the year of income, derive income from:

(i) a business of a kind that it did not carry on immediately before the event time; or

(ii) a transaction of a kind that it had not entered into in the course of its business operations before the event time.”.

(2) Section 160Z of the Principal Act is amended by inserting in subsection (5) “or 160ZT(1A)” after “160ZM(2)”.

Consideration in respect of disposal

28. Section 160ZD of the Principal Act is amended by inserting in subsection (2) “, the disposal is not by way of the expiry of the asset” after “asset” (first occurring).

Transfer of net capital loss within company group

29. Section 160ZP of the Principal Act is amended by omitting subsection (9) and substituting the following subsections:

“(9) If:

(a) section 50H operates so as to deem a disqualifying event in relation to the loss company to have occurred at a time during the loss year; and

(b) the loss company does not pass the continuity of business test set out in subsection (9A) in relation to that time;

no part of a net capital loss incurred by that company in respect of that year is capable of being specified in a notice under paragraph (7)(c).

“(9A) For the purposes of subsection (9), a company passes the continuity of business test in relation to a time (in this subsection called the ‘event time’) during a year of income if, and only if:

(a) the company carried on at all times during the year of income the same business as it carried on immediately before the event time; and

(b) the company did not, at any time during the year of income, derive income from:

(i) a business of a kind that it did not carry on immediately before the event time; or

(ii) a transaction of a kind that it had not entered into in the course of its business operations before the event time.”.

Election to treat grant of long term lease as disposal of freehold interest or head lease

30. Section 160ZSA of the Principal Act is amended:

(a) by omitting from paragraph (1)(e) “subsection 160ZT(1) does not” and substituting “subsections 160ZT(1), (1A) and (1B) do not”;

(b) by omitting from paragraph (1)(f) “subsection 160ZT(1)” and substituting “subsections 160ZT(1), (1A) and (1B)”.

Payments for variation of lease

31. Section 160ZT of the Principal Act is amended by omitting subsection (1) and substituting the following subsections:

“(1) For the purposes of this Part, if the lessor under a lease of property incurs expenditure in obtaining the consent of the lessee to the variation or waiver of any of the terms of the lease, the lessor is taken to have incurred a capital loss equal to the amount of that expenditure.

“(1A) For the purposes of this Part, if:

(a) the lessor under a lease of property incurs expenditure in obtaining the consent of the lessee to the variation or waiver of any of the terms of the lease; and

(b) the lessee receives an amount (in this subsection called the ‘consent amount’) from the lessor in respect of the giving by the lessee of consent to the variation or waiver; and

(c) the lease was acquired by the lessee on or after 20 September 1985;

then:

(d) if, assuming that the lessee had disposed of the lease at the time the waiver or variation was made, the indexed cost base to the lessee of the lease would not have exceeded the consent amount—the lessee is taken:

(i) to have disposed of the lease at that time for a consideration equal to the consent amount; and

(ii) to have immediately re-acquired the lease for no consideration; or

(e) if, assuming that the lessee had disposed of the lease at the time the waiver or variation was made, the indexed cost base to the lessee of the lease would have exceeded the consent amount—the lessee is taken to have disposed of the lease at that time for a consideration equal to the amount of that indexed cost base and to have immediately re-acquired the lease:

(i) for the purpose of ascertaining whether a capital gain accrued to the lessee in the event of a subsequent disposal of the lease by the lessee—for a consideration equal to the amount by which that indexed cost base exceeded the consent amount; or

(ii) for the purpose of ascertaining whether the lessee incurred a capital loss in the event of a subsequent disposal of the lease by the lessee—for a consideration equal to the amount by which the amount that, if the lessee had disposed of the lease at the time the waiver or variation was made, would have been the reduced cost base to the lessee in respect of the lease exceeds the consent amount.

“(1B) If the lessee disposed of the lease (otherwise than because of the application of subsection (1A)) within 12 months after the lessee acquired the lease (otherwise than because of the application of subsection (1A)), subsection (1A) has effect as if the references in that subsection to the indexed cost base to the lessee in respect of the lease were references to the cost base to the lessee in respect of the lease.”.

Consideration for disposal

32. Section 160ZV of the Principal Act is amended by omitting from subsection (2) “be deemed” (last occurring).

33. After section 160ZYJ of the Principal Act the following section is inserted:

Employee share trusts

“160ZYJA.(1) For the purposes of this Part, if:

(a) either:

(i) an amount is included in the assessable income of a

taxpayer under section 26AAC as a result of the acquisition by the taxpayer of a share in a company; or (ii) apart from subsection 26AAQ4F), an amount would have been included in the assessable income of a taxpayer under section 26AAC as a result of the acquisition by the taxpayer of a share in a company; and

(b) the share was acquired by the taxpayer under the terms of a trust deed under which a trustee is required or authorised to sell, or otherwise to transfer, shares in a company to employees of the company or of another company or to relatives of those employees; and

(c) if an amount was paid by the taxpayer as consideration for the share—that amount is equal to or less than the indexed cost base to the trustee of the share;

this Part does not apply in respect of the disposal by the trustee of the share to the taxpayer.

“(2) For the purposes of this Part, if:

(a) any of the following apply:

(i) an amount is included in the assessable income of a taxpayer under subsection 26AAC(8C) as a result of the acquisition by the taxpayer of a right to acquire shares in a company; or

(ii) apart from subsection 26AAC(4F), an amount would have been included in the assessable income of a taxpayer under subsection 26AAC(8C) as a result of the acquisition by the taxpayer of a right to acquire shares in a company; or

(iii) an amount is included in the assessable income of a taxpayer under subsection 26AAC(7) or (8) as a result of the disposal by the taxpayer or an associate of the taxpayer of a right to acquire shares in a company; or

(iv) both:

(A) an amount is included in the assessable income of a taxpayer under section 26AAC as a result of the acquisition by the taxpayer or an associate of the taxpayer of shares in a company; and

(B) the shares were acquired as a result of the exercise or operation of a right to acquire shares in the company; and

(b) the right was acquired, or originally acquired, by the taxpayer under the terms of a trust deed under which a trustee is required or authorised to sell, or otherwise to transfer, shares in a company to employees of the company or of another company or to relatives of those employees; and

(c) if an amount was paid by the taxpayer as consideration for the

right—that amount is equal to or less than the indexed cost base to the trustee of the right;

this Part does not apply in respect of the disposal by the trustee of the right to the taxpayer.

“(3) For the purposes of this Part, if:

(a) an amount is included in the assessable income of the trustee of the estate of a deceased person under subsection 26AAC(9) as a result of the acquisition by the trustee of shares in a company; and

(b) the shares were acquired as a result of the exercise or operation of a right to acquire shares in the company; and

(c) the right was acquired by the deceased person under the terms of a trust deed under which a trustee (in this subsection called the ‘scheme trustee’) is required or authorised to sell, or otherwise to transfer, shares in a company to employees of the company or of another company or to relatives of those employees; and

(d) if an amount was paid by the deceased person as consideration for the right—that amount is equal to or less than the indexed cost base to the scheme trustee of the right;

this Part does not apply in respect of the disposal by the scheme trustee of the right to the deceased person.

“(4) If:

(a) the trustee mentioned in subsection (1) disposed of the share to the taxpayer within 12 months after the share was acquired by the trustee; or

(b) the trustee mentioned in subsection (2) disposed of the right to the taxpayer within 12 months after the right was acquired by the trustee; or

(c) the scheme trustee mentioned in subsection (3) disposed of the right to the deceased person within 12 months after the right was acquired by the scheme trustee;

the reference in paragraph (1)(c), (2)(c) or (3)(d) to the indexed cost base to the trustee or to the scheme trustee, as the case may be, is to be read as a reference to the cost base to the trustee or to the scheme trustee, as the case requires.

“(5) Section 170 does not prevent the amendment of an assessment at any time for the purpose of giving effect to this section.

“(6) In spite of section 160E, in this section:

‘associate’ has the same meaning as in section 26AAC;

‘employee’ has the same meaning as in section 26AAC”.

Conversion of note not to constitute disposal

34. Section 160ZYZ of the Principal Act is amended by omitting “A” and substituting “For the purposes of this Part, a”.

Conversion of note not to constitute disposal

35. Section 160ZZBB of the Principal Act is amended by omitting “A” and substituting “For the purposes of this Part, a”.

Involuntary disposal

36.(1) Section 160ZZK of the Principal Act is amended by inserting in paragraph (1)(b) “(or such extended period as the Commissioner in special circumstances allows)” before “before”.

(2) Section 160ZZK of the Principal Act is amended by inserting after paragraph (1)(b) the following paragraph:

“(ba) in the case of the acquisition of a replacement asset—the replacement asset is not trading stock of the taxpayer immediately after its acquisition by the taxpayer;”.

Asset received as a result of involuntary disposal

37. Section 160ZZL of the Principal Act is amended by inserting after paragraph (1)(a) the following paragraph:

“(aa) the replacement asset is not trading stock of the taxpayer immediately after its acquisition by the taxpayer;”.

Transfer of asset between spouses upon breakdown of marriage

38. Section 160ZZM of the Principal Act is amended:

(a) by omitting from paragraph (1)(b) “country,” and substituting “country; or”;

(b) by inserting after paragraph (1)(b) the following paragraph:

“(ba) an order of a court under a law of a State or Territory or of a foreign country relating to the breakdown of de facto marriages;”.

Transfer of assets from company or trust to spouse upon breakdown of marriage

39. Section 160ZZMA of the Principal Act is amended by adding at the end of paragraph (1)(b) the following word and subparagraph:

“or (iii) an order of a court under a law of a State or Territory or of a foreign country relating to the breakdown of de facto marriages.”.

Transfer of asset to wholly-owned company

40. Section 160ZZN of the Principal Act is amended:

(a) by inserting in subparagraph (2)(a)(i) “(in this section called a ‘roll-over asset’)” after “asset”;

(b) by inserting in subparagraphs (2)(a)(ii), (iii) and (iv) and (4)(a)(i), (ii), (iii) and (iv) “(in this section also called a ‘roll-over asset’)” after “asset” (first occurring);

(c) by inserting after paragraph (2)(c) the following paragraphs:

“(caa) the roll-over asset is not trading stock of the company immediately after its acquisition by the company;

(cab) if:

(i) the roll-over asset is:

(A) a right to which Division 10 or 10A applies; or

(B) an option to which Division 11, 11A or 13 applies; or

(C) a convertible note to which Division 12 or 12A applies; and

(ii) as a result of the exercise of the right or option, or the conversion of the convertible note, the company acquires another asset (in this paragraph called the ‘derived asset’);

the derived asset is not trading stock of the company immediately after its acquisition by the company; and”;

(d) by inserting in paragraphs (2)(ba), (e) and (f), (4)(ba), (c), (e) and (f) and subsection (8) “roll-over” before “asset” (wherever occurring);

(e) by omitting from subsections (3), (5), (5A), (7) and (9) “an asset” and substituting “a roll-over asset”;

(f) by omitting “and” from the end of paragraph (4)(c);

(g) by inserting after paragraph (4)(c) the following paragraphs:

“(ca) the roll-over asset is not trading stock of the company immediately after its acquisition by the company;

(cb) if:

(i) the roll-over asset is:

(A) a right to which Division 10 or 10A applies; or

(B) an option to which Division 11, 11A or 13 applies; or

(C) a convertible note to which Division 12 or 12A applies; and

(ii) as a result of the exercise of the right or option, or the conversion of the convertible note, the company acquires another asset (in this paragraph called the ‘derived asset’);

the derived asset is not trading stock of the company immediately after its acquisition by the company; and”;

(h) by adding at the end the following subsection:

“(10) Section 170 does not prevent the amendment of an assessment at any time for the purpose of giving effect to paragraph (2)(cab) or (4)(cb).”.

Transfer of partnership assets to wholly-owned company

41. Section 160ZZNA of the Principal Act is amended:

(a) by inserting after paragraph (2)(d) the following paragraphs:

“(da) the eligible asset is not trading stock of the company immediately after its acquisition by the company; and (db) if:

(i) the eligible asset is:

(A) a right to which Division 10 or 10A applies; or

(B) an option to which Division 11, 11A or 13 applies; or

(C) a convertible note to which Division 12 or 12A applies; and

(ii) as a result of the exercise of the right or option, or the conversion of the convertible note, the company acquires another asset (in this paragraph called the ‘derived asset’);

the derived asset is not trading stock of the company immediately after its acquisition by the company; and”;

(b) by adding at the end the following subsection:

“(15) Section 170 does not prevent the amendment of an assessment at any time for the purpose of giving effect to paragraph (2)(db).”.

Transfer of asset between companies in the same group

42. Section 160ZZO of the Principal Act is amended:

(a) by inserting in subparagraph (1)(a)(i) “(in this section called a ‘roll-over asset’)” after “asset”;

(b) by inserting in subparagraphs (1)(a)(ii), (iii) and (iv) “(in this section also called a ‘roll-over asset’)” after “asset” (first occurring);

(c) by inserting after paragraph (1)(b) the following paragraphs:

“(ba) the roll-over asset is not trading stock of the transferee immediately after its acquisition by the transferee;

(bb) if:

(i) the roll-over asset is:

(A) a right to which Division 10 or 10A applies; or

(B) an option to which Division 11, 11A or 13 applies; or

(C) a convertible note to which Division 12 or 12A applies; and

(ii) as a result of the exercise of the right or option, or the conversion of the convertible note, the transferee acquires another asset (in this paragraph called the ‘derived asset’);

the derived asset is not trading stock of the transferee immediately after its acquisition by the transferee;”;

(d) by inserting in paragraphs (1)(e), (f), (g) and (h) and subsection (2D) “roll-over” before “asset” (wherever occurring);

(e) by omitting from subsections (2) and (9) “an asset” and substituting “a roll-over asset”;

(f) by adding at the end the following subsection:

“(9A) Section 170 does not prevent the amendment of an assessment at any time for the purpose of giving effect to paragraph (1)(bb).”.

Exchange of shares in the same company

43. Section 160ZZP of the Principal Act is amended:

(a) by omitting “and” from the end of paragraph (1)(f);

(b) by inserting after paragraph (1)(f) the following paragraph:

“(fa) the total paid-up share capital of the company immediately after the new shares were issued equals the total paid-up share capital of the company immediately before the redemption or cancellation; and”.

Principal residence

44.(1) Section 160ZZQ of the Principal Act is amended:

(a) by inserting after subsection (1) the following subsection:

“(1AA) For the purposes of this section, if:

(a) land or a dwelling is acquired or disposed of under a contract entered into at a particular time; and

(b) legal ownership of the land or dwelling does not pass until a later time;

then, in spite of any other provision of this Part, the ownership of the land or dwelling is to be worked out on the basis of the legal ownership.”;

(b) by omitting “and” from the end of subparagraph (5)(b)(iii);

(c) by adding at the end of paragraph (5)(b) the following subparagraph:

“(iv) a dwelling was on the land at the relevant time and, after that time, the taxpayer:

(A) repaired or renovated the dwelling; or

(B) commenced to repair or renovate the dwelling

but died before the repairs or renovations were completed; and”;

(d) by omitting from paragraph (5)(c) “or (iii)(A)” and substituting “, (iii)(A) or (iv)(A)”;

(e) by omitting from subparagraphs (5)(c)(i) and (ii) and sub-subparagraph (5)(e)(i)(A) “or the erection of the dwelling was completed” and substituting “, the erection of the dwelling was completed or the repair or renovation of the dwelling was completed, as the case requires”;

(f) by omitting from subparagraph (5)(d)(ii) and paragraph (5)(f) “or (iii)(B)” and substituting “, (iii)(B) or (iv)(B)”;

(g) by inserting after subparagraph (5AA)(a)(i) the following subparagraph:

“(ia) if:

(A) subparagraph (5)(b)(iv) applies; and

(B) the dwelling was occupied by the taxpayer or another person after the relevant time; and

(C) the dwelling ceased to be so occupied for the purpose of allowing the repairs or renovations to be carried out;

the date on which the dwelling ceased, or last ceased, to be so occupied; or”;

(h) by adding at the end of subsection (5AA) the following word and paragraph:

“; and (c) a taxpayer who has, whether before or after the commencement of this paragraph, entered into a contract or contracts for the repair or renovation of a dwelling is taken to have commenced to repair or renovate the dwelling at the time when the contract or the first contract was entered into.”.

(2) Section 160ZZQ of the Principal Act is amended:

(a) by omitting from subparagraph (6)(b) “court,” and substituting “court; or”;

(b) by inserting after paragraph (6)(b) the following paragraph:

“(c) under a deed of arrangement where:

(i) the deed was entered into in settlement of a claim to participate in the distribution of the estate of the deceased person; and

(ii) the consideration (if any) given by the taxpayer for the dwelling consisted of the variation or waiver of a claim to one or more other assets that formed part of that estate.”.

Exemption of part of gain attributable to goodwill

45. Section 160ZZR of the Principal Act is amended:

(a) by omitting from paragraphs (1)(b) and (c) “$1,000,000” and substituting “the exemption threshold for the year of income in which the disposal takes place”;

(b) by omitting from subsection (1) “one-fifth” and substituting “half;

(c) by adding at the end of subsection (2) the following word and paragraph:

“; and (c) the expression ‘exemption threshold’ has the meaning given by section 160ZZRAA.”.

46. After section 160ZZR of the Principal Act the following section is inserted:

Calculation of ‘exemption threshold’ for purposes of section 160ZZR [Calculation in accordance with section]

“160ZZRAA.(1) For the purposes of section 160ZZR, the exemption threshold for a year of income is calculated as follows.

[Exemption threshold before 1993-94]

“(2) The exemption threshold for years of income before the 1993-94 year of income is $2,000,000.

[Exemption threshold from 1993-94 onwards]

“(3) For each later year of income, the exemption threshold is calculated by:

(a) taking the exemption threshold for the year of income before it (ignoring any application of paragraph (d)); and

(b) multiplying the exemption threshold by the indexation factor for the later year of income (see subsection (4)); and

(c) rounding the result to the nearest $1,000 or multiple of $1,000 (rounding upwards an amount ending in $500); and

(d) if the result is less than $2,000,000—increasing it to $2,000,000.

[Calculating the indexation factor in subsection (3)]

“(4) The indexation factor for the later year of income is calculated, to 3 decimal places, using the following formula:

sum of index numbers for quarters in period 1 |

sum of index numbers for quarters in period 2 |

where

‘index number’, for a quarter, means the All Groups Consumer Price Index number, being the weighted average of the 8 capital cities, published by the

(ignoring any later number that may be published by the Australian Statistician in substitution for it);

‘period 1’ means the period of 12 months ending on 31 March immediately before the later year of income (ignoring any substituted accounting period);

‘period 2’ means the period of 12 months immediately before period 1.

[Indexation factor: rounding]

“(5) If the indexation factor would end with a number greater than 4 if it were calculated to 4 decimal places (instead of 3 decimal places as mentioned in subsection (4)), then the indexation factor must be increased by 0.001.

[Indexation factor: change in CPI reference base]

“(6) For the purposes of applying the formula component ‘index number’, if at any time, whether before or after the commencement of this section, the Australian Statistician has changed or changes the reference base for the Consumer Price Index, then, after the change only index numbers published in terms of the new base are to be used.

[Publication of indexation factor and exemption threshold]

“(7) Before the beginning of each year of income (ignoring any substituted accounting period) the Commissioner must publish by written notice the indexation factor and the exemption threshold for the year of income.”.

Interpretation

47. Section 160ZZRA of the Principal Act is amended by inserting the following definitions:

“ ‘consideration’, in relation to the disposal of the first asset, means consideration worked out as if subsection 160ZD(2) had not been enacted;

‘subsidiary’ has the same meaning as in section 160ZZO;”.

Shares in, and loans to, transferor—deemed disposal and re-acquisition

48. Section 160ZZRE of the Principal Act is amended by adding at the end the following subsection:

“(6) If:

(a) at the first asset disposal time, a taxpayer (in this subsection called the ‘second taxpayer’) held an asset, being:

(i) a share in the transferor that was acquired by the second taxpayer on or after 20 September 1985 (in this subsection called a ‘post-CGT share’); or

(ii) a loan to the transferor that was acquired by the second taxpayer on or after 20 September 1985 (in this subsection called a ‘post-CGT loan’); and

(b) either:

(i) at the first asset disposal time, the second taxpayer held a share in the transferor that was acquired by the second taxpayer before 20 September 1985; or

(ii) whichever of the following is applicable:

(A) in the case of a post-CGT share—at the first asset disposal time, the second taxpayer held shares in the transferor belonging to 2 or more classes of shares;

(B) in the case of a post-CGT loan—at the first asset disposal time, the second taxpayer held 2 or more loans to the transferor; and

(c) the application of subsection (3) to the post-CGT share, or the application of subsection (4) to the post-CGT loan, as the case may be, would be unreasonable;

then:

(d) in the case of a post-CGT share—subsection (3) does not apply to the post-CGT share; and

(e) in the case of a post-CGT loan—subsection (4) does not apply to the post-CGT loan; and

(f) the cost base, the indexed cost base or the reduced cost base of the post-CGT share or the post-CGT loan to the second taxpayer is reduced by such amount (if any) as is reasonable having regard to:

(i) the circumstances in which the post-CGT share or the post-CGT loan was acquired by the second taxpayer; and

(ii) the extent (if any) to which the market value of the post-CGT share or the post-CGT loan was reduced as a result of the disposal of the first asset at the first asset disposal time.”.

Equity interest in transferee—compensatory increase in cost base etc.

49. Section 160ZZRH of the Principal Act is amended by inserting in paragraph (d) “160ZZRE(6) or” after “subsection”.

When asset acquired

50. Section 160ZZS of the Principal Act is amended:

(a) by inserting after subsection (1) the following subsection:

“(1A) If subsection (1) applies so as to deem an asset to have been acquired by a taxpayer after 19 September 1985:

(a) the time when the taxpayer is taken, for the purposes of this Part, to have acquired the asset is the time when the natural persons who, immediately before 20 September 1985, held majority underlying interests in the asset ceased, or first ceased, to hold those interests; and

(b) the taxpayer is taken to have acquired the asset for a consideration equal to the market value of the asset as at the time mentioned in paragraph (a).”;

(b) by inserting after subsection (2) the following subsection:

“(2A) For the purposes of this section (and for the purposes of the application of Subdivision G of Division 3 of Part III to this section), the following are taken to be natural persons:

(a) a body politic;

(b) a company that is, by the terms of the company’s constituent document, prohibited from making any distribution, whether in money, property or otherwise, to its members.”.

Keeping of records

51. Section 160ZZU of the Principal Act is amended:

(a) by inserting in subsections (3) and (3A) “(assuming that paragraph 160ZZO(1)(bb) had not been enacted)” after “section 160ZZO applies”;

(b) by inserting in paragraphs (3)(a) and (3A)(a) “(assuming that paragraph 160ZZO(1)(bb) had not been enacted)” after “disposal”;

(c) by omitting from paragraphs (3)(b) and (c), (3A)(b) and (c) and (6)(b) and (c) “earlier” and substituting “earliest”;

(d) by inserting after subparagraphs (3)(b)(i) and (3A)(b)(i) the following subparagraph:

“(ia) if section 160ZZO does not actually apply to the disposal but would have applied if paragraph 160ZZO(1)(bb) had not been enacted—the time when the derived asset mentioned in that paragraph was acquired by the transferee;”;

(e) by inserting in paragraphs (3A)(c) and (6)(c) “, (ia)” before “or (ii)”.

Interpretation

52.(1) Section 251R of the Principal Act is amended by omitting from subsection (6A) “or (c)” and substituting “, (c), (ca) or (cb)”.

(2) Section 251R of the Principal Act is amended by inserting in subsection (6A) “, (caa)” after “(ca)”.

Prescribed persons

53.(1) Section 251U of the Principal Act is amended by omitting from paragraph (3)(b) “or (c)” and substituting “, (c), (ca) or (cb)”.

(2) Section 251U of the Principal Act is amended by inserting in paragraph (3)(b) “, (caa)” after “(ca)”.

Interpretation

54. Section 317 of the Principal Act is amended by inserting the following definitions:

“ ‘transitional finance share’ has the meaning given by section 327B;

‘transitional finance share dividend’ means a dividend in respect of a transitional finance share.”.

Widely distributed finance shares

55. Section 327A of the Principal Act is amended by inserting after subsection (1) the following subsection:

[Extended meaning of ‘widely distributed finance shares’—funding of transitional finance shares]

“(1A) For the purposes of this Part, if:

(a) apart from this subsection, shares (in this subsection called the ‘test shares’) in a company are not widely distributed finance shares; and

(b) as a result of the operation of subsection 327B(3) in relation to the shares:

(i) the shares are taken to be widely distributed finance shares for the purposes of section 327B; and

(ii) shares in another company are transitional finance shares;

the test shares are taken to be, and to have been, widely distributed finance shares.”.

56. After section 327A of the Principal Act the following section is inserted:

Transitional finance shares

[Meaning of ‘transitional finance shares’]

“327B.(1) For the purposes of this Part, shares (in this subsection called the ‘test shares’) in a company (in this subsection called the ‘second company’) are transitional finance shares at a particular time (in this subsection called the ‘test time’) if all of the following conditions are satisfied:

(a) the test time is before 1 July 1998;

(b) the test shares are finance shares;

(c) during a period (in this subsection called the ‘primary issue period’) ending before the IP time, another company (in this subsection called the ‘first company’) issued widely distributed finance shares;

(d) the issue of the widely distributed finance shares comprised the whole of a common issue of shares by the first company;

(e) the issue of the test shares comprised the whole of a common issue of shares by the second company;

(f) the test shares were simultaneously issued to the first company by the second company at, or within a reasonable time after, the end of the primary issue period;

(g) the widely distributed finance shares were issued by the first company for the sole purpose of funding the first company’s acquisition of the test shares;

(h) assuming that the test shares had been issued at the end of the primary issue period, the following conditions would have been satisfied at all times during the period commencing at the end of the primary issue period and ending at the test time:

(i) the rights and obligations relating to the widely distributed finance shares are substantially similar to the rights and obligations relating to the test shares;

(ii) the first company and the second company are under common ownership;

(i) if, on the assumption that the dividends in respect of the test shares were instead payments of the interest, referred to in subsection (2), to which they may reasonably be regarded as equivalent, the following conditions would have been satisfied in relation to that interest:

(i) the interest that accrued during the 24-month period ending at the test time accrued at intervals not exceeding 12 months;

(ii) the interest that accrued during the 12-month period commencing 24 months before the test time was paid not later than 12 months after it accrued;

(iii) the dividends paid in respect of the widely distributed finance shares during the 12-month period ending at the test time are wholly attributable to the interest that accrued during the 12-month period ending at the time the dividends were paid;

(iv) the total amount of dividends paid in respect of the widely distributed finance shares during the 12-month period ending at the test time is equal to, or approximately equal to, the total amount of interest to which the dividends are attributable.

[Meaning of ‘finance shares’]

“(2) For the purposes of this section, shares in a company are finance shares if, and only if, having regard to:

(a) the manner in which the amount of dividends in respect of the shares was to be calculated; and

(b) the conditions applicable to the payment of dividends in respect of the shares; and

(c) any other relevant matters;

the payment of the dividends in respect of the shares may reasonably be regarded as equivalent to the payment of interest on a loan.

[Modification of ‘widely distributed finance shares’]

“(3) For the purposes of this section, in determining whether shares are widely distributed finance shares, if an asset is held by an entity as trustee for another entity who is absolutely entitled to the asset against the trustee, paragraph 327A(2)(b) has effect as if:

(a) the asset were vested in the other entity instead of the trustee; and

(b) if the asset is a share—any dividends paid in respect of the share were paid to the other entity instead of to the trustee.

[Meaning of ‘under common ownership’]

“(4) For the purposes of this section, 2 companies are under common ownership at a particular time if, and only if:

(a) another company (in this subsection called the third company’) holds eligible share interests in each of the companies; and

(b) the aggregate of the eligible share interests in each company held by the third company is 90% or more.

[Meaning of ‘eligible share interest’]

“(5) For the purposes of this section, a person holds an eligible share interest in a company at a particular time equal to the percentage of the company’s total paid-up share capital (excluding finance shares) beneficially owned by the person at that time.

[Extended meaning of ‘eligible share interest’: tiers of companies]

“(6) For the purposes of this section, if:

(a) a person holds an eligible share interest (including an eligible share interest that is taken to be held because of one or more previous applications of this subsection) in a company (in this subsection called the ‘first level company’); and

(b) the first level company holds an eligible share interest in another company (in this subsection called the ‘second level company’);

the person is taken to hold an eligible share interest in the second level company equal to the percentage calculated using the formula:

where:

‘First level percentage’ means the percentage of the eligible share interest held by the person in the first level company;

‘Second level percentage’ means the percentage of the eligible share interest held by the first level company in the second level company.

[Definitions]

“(7) In this section:

‘eligible share interest’ has the meaning given by subsections (5) and (6);

‘finance share’ has the meaning given by subsection (2);

‘under common ownership’ has the meaning given by subsection (4);

‘widely distributed finance share’ has a meaning affected by subsection (3).”.

Direct attribution interest in a CFC or CFT

57. Section 356 of the Principal Act is amended by omitting from subsection (4) “and widely distributed finance shares” and substituting “, widely distributed finance shares and transitional finance shares”.

Direct attribution account interest in a company

58. Section 366 of the Principal Act is amended by omitting from subsection (5) “and widely distributed finance shares” and substituting “, widely distributed finance shares and transitional finance shares”.

Notional allowable deduction for eligible finance share dividends, widely distributed finance share dividends and transitional finance share dividends

59. Section 394 of the Principal Act is amended:

(a) by omitting from paragraph (a) “or a widely distributed finance share dividend” and substituting “, a widely distributed finance share dividend or a transitional finance share dividend”;

(b) by inserting in paragraph (b) “or subsection 327B(2)” after “327A(3)(b)”.

Additional notional exempt income—unlisted or listed country CFC

60.(1) Section 402 of the Principal Act is amended by inserting in paragraphs (2)(c) and (d) “or a transitional finance share dividend” after “widely distributed finance share dividend”.

(2) Section 402 of the Principal Act is amended:

(a) by omitting from paragraph (2)(d) “that other” and substituting “the eligible CFC and the other”;

(b) by inserting after paragraph (2)(d) the following paragraph:

“(da) an amount that is taken by section 47A to be a dividend paid to the eligible CFC in the eligible period by another company, where the eligible taxpayer is an attributable taxpayer in relation to the eligible CFC and the other company when the dividend is taken to be paid;”.

Elections under CGT roll-over provisions

61. Section 421 of the Principal Act is amended:

(a) by omitting “For” and substituting “Subject to this section, for”;

(b) by adding at the end the following subsections:

“(2) Except in accordance with subsection (3), subsection (1) does not apply to an election in respect of the disposal of an asset if the disposal is, or apart from an election in accordance with subsection 438(3A) would be, taken into account in determining under Division 8 whether the eligible CFC passes the active income test in relation to the eligible period.

“(3) If an election is made under a CGT roll-over provision in accordance with subsection 438(3A), that election also has effect as if it were made under the CGT roll-over provision in accordance with subsection (1) of this section.”.

Roll-overs—asset disposals

62. Section 438 of the Principal Act is amended:

(a) by inserting after subsection (2) the following subsections:

“(2A) If:

(a) a CGT roll-over provision applies to the disposal of the asset (in this subsection called the ‘original asset’) by the company; and

(b) the disposal is not to another entity; and

(c) the company acquires another asset (in this subsection called the ‘replacement asset’) that is referred to in the CGT roll-over provision as being by way of replacement of, substitution for, or consideration for the disposal of, the original asset (whether or not exactly those expressions are used);

the following provisions have effect:

(d) the company is not taken to have:

(i) derived any gains; or

(ii) incurred any loss;

in respect of the disposal of the original asset; and

(e) the company is taken to have paid, as consideration to acquire the replacement asset, the sum of:

(i) the consideration (if any) paid or payable by the company to acquire the original asset; and

(ii) the expenditure (if any) incurred by the company in making improvements to the original asset.

“(2B) For the purposes of subsections (2) and (2A), if an asset is disposed of by being cancelled, redeemed or consolidated

into another asset, the disposal is taken not to be to another entity.”;

(b) by inserting after subsection (3) the following subsection:

“(3A) For the purposes of applying Part IIIA in relation to a statutory accounting period as mentioned in paragraph (3)(b), any election that may be made by the company, or by the company and another entity, apart from this section under any of the CGT roll-over provisions:

(a) on or before the date of lodgment of a particular return of income; or

(b) within such period as the Commissioner allows; is to be given instead:

(c) before the end of the period of 2 months after the end of the statutory accounting period; or

(d) within such further period as the Commissioner allows.”.

Tainted sales income

63. Section 447 of the Principal Act is amended:

(a) by omitting from paragraphs (1)(a) and (b) “both” and substituting “all”;

(b) by adding at the end of paragraphs (1)(a) and (b) the following subparagraph:

“(iii) if the goods were altered by the company—the income does not pass the substantial alteration test set out in subsection (4).”;

(c) by adding at the end of subsection (1) the following paragraphs:

“(c) income from the sale of goods (in this paragraph called the ‘manufactured goods’) by the company where all of the following conditions are satisfied:

(i) the manufactured goods were manufactured by the company;

(ii) any of the raw materials or goods from which the manufactured goods were manufactured were sold to the company by another entity;

(iii) either of the following sub-subparagraphs applies at the time of the sale to the company of the raw materials or goods from which the manufactured goods were manufactured:

(A) the entity who sold to the company the raw materials or goods from which the manufactured goods were manufactured was an associate of the company and a Part X Australian resident;

(B) the raw materials or goods from which the