Customs Legislation Amendment

Act 1993

No. 8 of 1994

An Act to amend the Customs Act 1901 and the

Anti-Dumping Authority Act 1988, and for related purposes

[Assented to 18 January 1994]

The Parliament of Australia enacts:

PART 1—PRELIMINARY

Short title

1. This Act may be cited as the Customs Legislation Amendment Act 1993.

Commencement

2.(1) Sections 1, 2, 3, 4, 5, 6, 7 and 14, subsection 16(1) and sections 18 and 21 commence on the day on which this Act receives the Royal Assent.

(2) Section 8 is taken to have commenced on 1 September 1992.

(3) Sections 11, 12 and 13 commence 28 days after the day on which this Act receives the Royal Assent.

(4) Section 15, subsection 16(2) and section 23, so far as it relates to item 3 of Schedule 2, are taken to have commenced on 1 November 1992.

(5) Section 17 commences, or is taken to have commenced, 14 days after the day on which the Customs Tariff Amendment Act (No. 2) 1993 receives or received the Royal Assent.

(6) Section 23, so far as it relates to item 1 of Schedule 2, is taken to have commenced on 18 August 1992.

(7) Section 23, so far as it relates to item 2 of Schedule 2, is taken to have commenced on 1 January 1993.

(8) Subject to subsection (9), the remaining provisions of this Act commence on a day or days to be fixed by Proclamation.

(9) If a provision mentioned in subsection (8) does not commence under that subsection within 6 months after the day on which this Act receives the Royal Assent, it commences on the first day after the end of that period.

Application of Division 1A of Part VIII of the Customs Act

3. Division 1A of Part VIII of the Customs Act 1901 as amended by this Act applies in respect of goods that are entered for home consumption after section 10 of this Act commences.

PART 2—AMENDMENTS OF THE CUSTOMS ACT 1901

Principal Act

4. In this Part, “Principal Act” means the Customs Act 19011.

Definitions

5. Section 4 of the Principal Act is amended by omitting from subsection (1) the definition of “Place outside Australia” and substituting the following definition:

“ ‘place outside Australia’ includes.

(a) the waters in Area A of the Zone of Cooperation; or

(b) a resources installation in Area A;

but does not include:

(c) any other area of waters outside Australia; or

(d) any other installation outside Australia; or

(e) a ship outside Australia; or

(f) a reef or an uninhabited island outside Australia;”.

Arrival report

6. Section 64AA of the Principal Act is amended:

(a) by omitting from subsection (1) “within the meaning of section 130C” and substituting “and of the personal effects of the crew”;

(b) by adding at the end the following subsection:

“(3) In this section:

‘ship’s stores’ means ship’s stores within the meaning of section 130C.”.

Authority to deal with goods entered under section 71A

7. Section 71B of the Principal Act is amended:

(a) by omitting from subparagraph (2)(b)(i) “that, subject to payment of any designated amount, the goods will be cleared” and substituting “that the goods are cleared”;

(b) by omitting from subparagraph (3)(c)(i) “that, subject to payment of any designated amount, the goods will be cleared” and substituting “that the goods are cleared”;

(c) by omitting paragraph (4)(b) and substituting the following paragraph:

“(b) a payment of any duty, sales tax or other charge payable at the time of entry on the goods covered by the import entry advice together with all administrative charges associated with the making of that entry;”;

(d) by inserting after subsection (4) the following subsection:

“(4A) Without limiting the generality of the reference in subsection (4) to administrative charges associated with the making of an entry, that reference includes, in relation to a documentary import entry, an amount specified in the regulations as a fee payable for assistance provided in preparing the entry for use in a Customs computer system.”.

Withdrawal of import entries

8. Section 71F of the Principal Act is amended by adding at the end the following subsection:

“(6) If:

(a) an import entry is communicated to Customs; and

(b) duty remains unpaid in respect of goods covered by the entry for 30 days starting on the day on which the import entry advice in respect of those goods is communicated; and

(c) after that period ends, the Collector gives written notice to the owner of the goods requiring payment of duty within a further period set out in the notice; and

(d) duty is not paid within the further period;

the import entry is taken to have been withdrawn under subsection (1).”.

Repeal of section 151

9. Section 151 of the Principal Act is repealed.

Insertion of new Division

10. After Division 1 of Part VIII of the Principal Act the following Division is inserted:

“Division 1A—Rules of origin of preference claim goods

Purpose of Division

“153A.(1) The purpose of this Division is to set out rules for determining whether goods are the produce or manufacture:

(a) of a particular country other than Australia; or

(b) of a Developing Country but not of a particular Developing Country.

“(2) Goods are not the produce or manufacture of a country other than Australia unless, under the rules as so set out, they are its produce or manufacture.

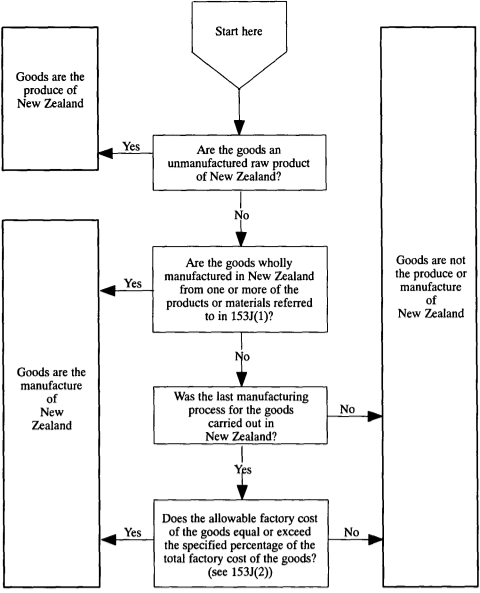

“(3) Diagrams and explanatory notes illustrating certain operations of this Division in relation to New Zealand are set out in Schedule VII. Details are as follows:

(a) Diagram 1 is a decision diagram for working out whether goods are the produce or manufacture of New Zealand;

(b) Diagram 2 gives an example of goods that are last processed in New Zealand to show, in particular, how allowable expenditure on materials, allowable factory cost and total factory cost are worked out.

Definitions

“153B. In this Division:

‘allowable factory cost’, in relation to preference claim goods and to the factory at which the last process of their manufacture was performed, means the sum of:

(a) the allowable expenditure of the factory on materials in respect of the goods worked out under section 153D; and

(b) the allowable expenditure of the factory on labour in respect of the goods worked out under section 153F; and

(c) the allowable expenditure of the factory on overheads in respect of the goods worked out under section 153G;

‘Developing Country’ has the same meaning as in the Customs Tariff Act 1987 and includes a place that, for the purposes of that Act, is to be treated as a Developing Country;

‘factory’, in relation to preference claim goods, means:

(a) if the goods are claimed to be the manufacture of a particular preference country—the place in that country where the last process in the manufacture of the goods was performed; and

(b) if the goods are claimed to be the manufacture of a preference country that is a Developing Country but not a particular Developing Country—the place in Papua New Guinea or in a Forum Island Country where the last process in the manufacture of the goods was performed;

‘Forum Island Country’ has the same meaning as in the Customs Tariff Act 1987;

‘inner container’ includes any container into which preference claim goods are packed, other than a shipping or airline container, pallet or other similar article;

‘manufacturer’, in relation to preference claim goods, means the person undertaking the last process in their manufacture;

‘materials’, in relation to preference claim goods, means:

(a) if the goods are unmanufactured raw products—those products; and

(b) if the goods are manufactured goods—all matter or substances used or consumed in the manufacture of the goods (other than that matter or those substances that are treated as overheads); and

(c) in either case—the inner containers in which the goods are packed;

‘person’ includes partnerships and unincorporated associations;

‘preference claim goods’ means goods that are claimed, when they are entered for home consumption, to be the produce or manufacture of a preference country;

‘preference country’ has the same meaning as in the Customs Tariff Act 1987;

‘qualifying area’, in relation to particular preference claim goods, means:

(a) if the goods are claimed to be the manufacture of New Zealand—New Zealand and Australia; or

(b) if the goods are claimed to be the manufacture of Canada—Canada and Australia; or

(c) if the goods are claimed to be the manufacture of Papua New Guinea—Papua New Guinea, the Forum Island Countries, New Zealand and Australia; or

(d) if the goods are claimed to be the manufacture of a Forum Island Country—the Forum Island Countries, Papua New Guinea, New Zealand and Australia; or

(e) if the goods are claimed to be the manufacture of a particular Developing Country—the Developing Country, Papua New Guinea, the Forum Island Countries, the other Developing Countries and Australia; or

(f) if the goods are claimed to be the manufacture of a Developing Country but not a particular Developing Country—Papua New Guinea, the Forum Island Countries, the Developing Countries and Australia; or

(g) if the goods are claimed to be the manufacture of a country that is not a preference country—that country and Australia;

‘total factory cost’, in relation to preference claim goods, means the sum of:

(a) the total expenditure of the factory on materials in respect of the goods, worked out under section 153C; and

(b) the allowable expenditure of the factory on labour in respect of the goods, worked out under section 153F; and

(c) the allowable expenditure of the factory on overheads in respect of the goods, worked out under section 153G.

Total expenditure of factory on materials

“153C. The total expenditure of a factory on materials in respect of preference claim goods is the cost to the manufacturer of the materials in the form they are received at the factory, worked out under section 153E.

Allowable expenditure of factory on materials

Allowable expenditure of a factory on materials to be worked out under subsections (2) to (8)

“153D.(1) The allowable expenditure of a factory on materials in respect of preference claim goods in the form those materials are received at the factory is to be worked out under subsections (2) to (8) inclusive.

Goods wholly or partly manufactured from materials imported from outside the qualifying area

“(2) If:

(a) preference claim goods (other than goods wholly manufactured from unmanufactured raw products) are manufactured, in whole or in part, from particular materials; and

(b) those particular materials, in the form they are received at the factory, are imported from a country outside the qualifying area;

there is no allowable expenditure of the factory on those particular materials.

Goods wholly or partly manufactured from unmanufactured raw products of a country inside the qualifying area

“(3) If:

(a) preference claim goods are manufactured, in whole or in part, from particular materials; and

(b) those particular materials, in the form they are received at the factory, are the unmanufactured raw products of a country inside the qualifying area;

the allowable expenditure of the factory on those particular materials is the cost to the manufacturer of those particular materials, worked out under section 153E.

Goods wholly or partly manufactured from materials imported from outside the qualifying area—intervening manufacture

“(4) If:

(a) preference claim goods are manufactured, in whole or in part, from particular materials; and

(b) other materials (‘contributing materials’) have been incorporated in those particular materials; and

(c) those contributing materials were imported into a country in the qualifying area from a country outside the qualifying area; and

(d) after their importation and to achieve that incorporation, those contributing materials have been subjected to a process of manufacture, or a series of processes of manufacture, in the qualifying area without any intervening exportation to a country outside that area;

the allowable expenditure of the factory on those particular materials in the form they are received at the factory does not include any part of the cost of those particular materials to the manufacturer, worked out under section 153E, that is attributable to the cost of those contributing materials in the form in which the contributing materials were received by the person who subjected them to their first manufacturing process in the qualifying area after importation.

Intervening export of contributing materials

“(5) If contributing materials within the meaning of subsection (4) are, after their importation into a country in the qualifying area and before their incorporation into the particular materials from which preference claim goods are manufactured, subsequently exported to a country outside that area, then, on their reimportation into a country in the qualifying area, subsection (2) or (4), as the case requires, applies as if that subsequent reimportation were the only importation of those materials.

Goods claimed to be the manufacture of New Zealand—special rule

“(6) If:

(a) goods claimed to be the manufacture of New Zealand are manufactured, in whole or in part, from particular materials; and

(b) under subsection (4), the allowable expenditure of the factory on those particular materials would be at least 50% of the total expenditure of the factory on those particular materials worked out in accordance with section 153C;

then, despite subsection (4), the allowable expenditure of the factory on those particular materials is taken to be that total expenditure.

Waste or scrap

“(7) If:

(a) materials are imported into a country; and

(b) the subjecting of those materials to a process of manufacture gives rise to waste or scrap; and

(c) that waste or scrap is fit only for the recovery of raw materials;

any raw materials that are so recovered in that country are to be treated, for the purposes of this section, as if they were unmanufactured raw products of that country.

Transhipment

“(8) If, in the course of their exportation from one country to another country, materials are transhipped, that transhipment is to be disregarded for the purpose of determining, under this section, the country from which the materials were exported.

Calculation of the cost of materials received at a factory

Purpose of section

“153E.(1) This section sets out, for the purposes of sections 153C and 153D, the rules for working out the cost of materials in the form they are received at a factory.

General rule

“(2) Subject to this section, the cost of materials received at a factory is the amount paid or payable by the manufacturer in respect of the materials in the form they are so received.

Customs and excise duties and certain other taxes to be disregarded

“(3) Any part of the cost of materials in the form they are received at a factory that represents:

(a) a customs or excise duty; or

(b) a tax in the nature of a sales tax, a goods and services tax, an anti-dumping duty or a countervailing duty;

imposed on the materials by a country in the qualifying area is to be disregarded.

Comptroller may require artificial elements of cost to be disregarded

“(4) If the Comptroller is satisfied that materials in the form they are received at a factory incorporate other materials solely for the purpose of artificially raising the cost of the first-mentioned materials, the Comptroller may, by written notice given to the importer of preference claim goods in which those other materials are incorporated, require the part of the cost that is, in the Comptroller’s opinion, reasonably attributable to those other materials to be disregarded.

Comptroller may require cost over normal market value to be disregarded

“(5) If the Comptroller is satisfied that the cost to the manufacturer of materials in the form they are received at a factory exceeds, by an amount determined by the Comptroller, the normal market value of the materials, the Comptroller may, by written notice given to the importer of preference claim goods in which those materials are incorporated, require the excess to be disregarded.

Comptroller may determine cost of certain materials received at a factory

“(6) If the Comptroller is satisfied:

(a) that materials in the form they are received at a factory are so received:

(i) free of charge; or

(ii) at a cost that is less than the normal market value of the materials; and

(b) that the receipt of the materials free of charge or at a reduced cost has been arranged, directly or indirectly, by a person who will be the importer of preference claim goods in which those materials are incorporated;

the Comptroller may, by written notice given to the importer, require that an amount determined by the Comptroller to be the difference between the cost, if any, paid by the manufacturer and the normal market value be treated as the amount, or a part of the amount, paid by the manufacturer in respect of the materials.

Effect of determination

“(7) If the Comptroller gives a notice to the importer of preference claim goods under subsection (4), (5) or (6) in respect of materials incorporated in those goods, the cost of the materials to the manufacturer must be determined having regard to the terms of that notice.

Allowable expenditure of factory on labour

Calculation of allowable expenditure of factory on labour

“153F.(1) Allowable expenditure of a factory on labour in respect of preference claim goods means the sum of the part of each cost prescribed for the purposes of this subsection:

(a) that is incurred by the manufacturer of the goods; and

(b) that relates, directly or indirectly, and wholly or partly, to the manufacture of the goods; and

(c) that can reasonably be allocated to the manufacture of the goods.

Regulations may specify manner of working out cost

“(2) Regulations prescribing a cost for the purposes of subsection (1) may also specify the manner of working out that cost.

Allowable expenditure of factory on overheads

Calculation of allowable expenditure of factory on overheads

“153G.(1) Allowable expenditure of a factory on overheads in respect of preference claim goods means the sum of the part of each cost prescribed for the purposes of this subsection:

(a) that is incurred by the manufacturer of the goods; and

(b) that relates, directly or indirectly, and wholly or partly, to the manufacture of the goods; and

(c) that can reasonably be allocated to the manufacture of the goods.

Regulations may specify manner of working out cost

“(2) Regulations prescribing a cost for the purposes of subsection (1) may also specify the manner of working out that cost.

Unmanufactured goods

“153H. Goods claimed to be the produce of a country are the produce of that country if they are its unmanufactured raw products.

Manufactured goods originating in New Zealand

Rule for certain goods wholly manufactured in New Zealand

“153J.(1) Goods claimed to be the manufacture of New Zealand are the manufacture of that country if they are wholly manufactured in New Zealand from one or more of the following:

(a) unmanufactured raw products;

(b) materials wholly manufactured in Australia or New Zealand or Australia and New Zealand;

(c) materials imported into New Zealand that the Comptroller has determined, by Gazette notice, to be manufactured raw materials of New Zealand.

Rule for other manufactured goods last processed in New Zealand

“(2) Goods claimed to be the manufacture of New Zealand are the manufacture of that country if:

(a) the last process in their manufacture was performed in New Zealand; and

(b) having regard to their qualifying area, their allowable factory cost is not less than the specified percentage of their total factory cost.

Specified percentage

“(3) The specified percentage of the total factory cost of goods referred to in subsection (2) is:

(a) unless paragraph (b) applies—50%; or

(b) if the goods are of a kind for which the Comptroller has determined, by Gazette notice, that another percentage is appropriate—that percentage.

Modification of section 153J in special circumstances

When 50% in subsection 153J(3) can be read as 48%

“153K.(1) If the Comptroller is satisfied:

(a) that the allowable factory cost of preference claim goods in a shipment of such goods that are claimed to originate in New Zealand is at least 48% but not 50% of the total factory cost of those goods; and

(b) that the allowable factory cost of those goods would be at least 50% of the total factory cost of those goods if an unforeseen circumstance had not occurred; and

(c) that the unforeseen circumstance is unlikely to continue;

the Comptroller may determine, in writing, that section 153J has effect:

(d) for the purpose of the shipment of goods that is affected by that unforeseen circumstance; and

(e) for the purposes of any subsequent shipment of similar goods that is so affected during a period specified in the determination;

as if the reference in subsection 153J(3) to 50% were a reference to 48%.

Effect of determination

“(2) If the Comptroller makes a determination then, in relation to all preference claim goods imported into Australia that are covered by that determination, section 153J has effect in accordance with the determination.

Comptroller may revoke determination

“(3) If:

(a) the Comptroller makes a determination; and

(b) the Comptroller becomes satisfied that the unforeseen circumstance giving rise to the determination no longer continues;

the Comptroller may, by written notice, revoke the determination despite the fact that the period referred to in the determination has not ended.

Definition of “similar goods”

“(4) In this section:

‘similar goods’, in relation to goods in a particular shipment, means goods:

(a) that are contained in another shipment that is imported by the same importer; and

(b) that undergo the same process or processes of manufacture as the goods in the first-mentioned shipment.

Manufactured goods originating in Papua New Guinea or a Forum Island Country

Rule for certain goods wholly manufactured in Papua New Guinea

“153L.(1) Goods claimed to be the manufacture of Papua New Guinea are the manufacture of that country if they are wholly manufactured in Papua New Guinea from one or more of the following:

(a) unmanufactured raw products;

(b) materials wholly manufactured in Australia or Papua New Guinea or Australia and Papua New Guinea;

(c) materials imported into Papua New Guinea that the Comptroller has determined, by Gazette notice, to be manufactured raw materials of Papua New Guinea.

Rule for manufactured goods last processed in PNG or a Forum Island Country if qualifying area does not include New Zealand

“(2) Goods claimed to be the manufacture of Papua New Guinea or of a Forum Island Country are the manufacture of that country if:

(a) the last process in their manufacture was performed in that country; and

(b) if their qualifying area did not include New Zealand—their allowable factory cost would be not less than the specified percentage of their total factory cost.

Rule for manufactured goods last processed in PNG or a Forum Island Country if qualifying area includes New Zealand

“(3) Goods claimed to be the manufacture of Papua New Guinea or of a Forum Island Country are the manufacture of that country, if:

(a) the last process in their manufacture was performed in the country; and

(b) they are partly manufactured from materials:

(i) that are the produce or manufacture of New Zealand; and

(ii) that can lawfully be imported into Australia in any quantity; and

(iii) that, if they are imported, attract the ‘Free’ rate of customs duty under sections 22, 24, 26 and 27 of the Customs Tariff Act 1987; and

(c) having regard to their qualifying area, their allowable factory cost is not less than the specified percentage of their total factory cost; and

(d) if their qualifying area did not include New Zealand or Australia—their allowable factory cost would be at least 25% of their total factory cost.

Specified percentage

“(4) The specified percentage of the total factory cost of goods referred to in subsection (2) or (3) is:

(a) unless paragraph (b) applies—50%; or

(b) if the goods are of a kind for which the Comptroller has determined, by Gazette notice, that a lesser percentage is appropriate—that percentage.

Manufactured goods originating in a particular Developing Country

“153M. Goods claimed to be the manufacture of a particular Developing Country are the manufacture of that country if:

(a) the last process in their manufacture was performed in that country; and

(b) having regard to their qualifying area, their allowable factory cost is at least 50% of their total factory cost.

Manufactured goods originating in a Developing Country but not in any particular Developing Country

“153N. Goods claimed to be the manufacture of a Developing Country, but not of any particular Developing Country, are the manufacture of a Developing Country, but not a particular Developing Country, if:

(a) the last process in their manufacture was performed in Papua New Guinea or a Forum Island Country; and

(b) they are not the manufacture of Papua New Guinea or a Forum Island Country under section 153L; and

(c) having regard to their qualifying area, their allowable factory cost is at least 50% of their total factory cost.

Manufactured goods originating in Canada

General rule

“153P.(1) Despite section 153H and subsections (2) and (3), goods claimed to be the produce or manufacture of Canada are not the produce or manufacture of that country unless:

(a) they have been shipped to Australia from Canada; and

(b) either:

(i) they have not been transhipped; or

(ii) the Comptroller is satisfied that, when they were shipped from Canada, their intended destination was Australia.

Rule for certain manufactured goods wholly manufactured in Canada

“(2) Goods claimed to be the manufacture of Canada are the manufacture of that country if they are wholly manufactured in Canada from one or more of the following:

(a) unmanufactured raw products;

(b) materials wholly manufactured in Australia or Canada or Australia and Canada;

(c) materials imported into Canada that the Comptroller has determined, by Gazette notice, to be manufactured raw materials of Canada.

Rule for other manufactured goods last processed in Canada

“(3) Goods claimed to be the manufacture of Canada are the manufacture of that country if:

(a) the last process in their manufacture was performed in Canada; and

(b) having regard to their qualifying area, their allowable factory cost is not less than the specified percentage of their total factory cost.

Specified percentage

“(4) The specified percentage of the total factory cost of goods referred to in subsection (3) is:

(a) if the goods are of a kind commercially manufactured in Australia—75%; or

(b) if the goods are of a kind not commercially manufactured in Australia—25%.

Manufactured goods originating in a country that is not a preference country

Rule for certain goods wholly manufactured in a country that is not a preference country

“153Q.(1) Goods claimed to be the manufacture of a country that is not a preference country are the manufacture of that country if they are wholly manufactured in that country from one or more of the following:

(a) unmanufactured raw products;

(b) materials wholly manufactured in Australia or the country or Australia and the country;

(c) materials imported into the country that the Comptroller has determined, by Gazette notice, to be manufactured raw materials of the country.

Rule for other manufactured goods last processed in a country that is not a preference country

“(2) Goods claimed to be the manufacture of a country that is not a preference country are the manufacture of that country if:

(a) the last process in their manufacture was performed in that country; and

(b) having regard to their qualifying area, their allowable factory cost is not less than the specified percentage of their total factory cost.

Specified percentage

“(3) Subject to subsection (4), the specified percentage of the total factory cost of goods referred to in subsection (2) is:

(a) if the goods are of a kind commercially manufactured in Australia—75%; or

(b) if the goods are of a kind not commercially manufactured in Australia—25%.

Special rule for Christmas Island, Cocos (Keeling) Islands and Norfolk Island

“(4) If the country that is not a preference country is Christmas Island, Cocos (Keeling) Islands or Norfolk Island, the specified percentage of the total factory cost of goods referred to in subsection (2) is:

(a) if the goods are of a kind commercially manufactured in Australia—50%; or

(b) if the goods are of a kind not commercially manufactured in Australia—25%.

Are goods commercially manufactured in Australia?

Comptroller may determine that goods are, or are not, commercially manufactured in Australia

“153R.(1) For the purposes of sections 153P and 153Q, the Comptroller may, by Gazette notice, determine that goods of a specified kind are, or are not, commercially manufactured in Australia.

Effect of determination

“(2) If such a determination is made, this Division has effect accordingly.

Rule against double counting

“153S. In determining the allowable factory cost or the total factory cost of preference claim goods, a cost incurred, whether directly or indirectly, by the manufacturer of the goods must not be taken into account more than once.

May be different rules of origin for anti-dumping purposes so far as New Zealand is concerned

“153T.(1) Regulations and determinations made under this Division, to the extent that they determine whether or not goods are the produce or manufacture of New Zealand, may make different provision for the purposes:

(a) of Part XVB; and

(b) of this Act (other than Part XVB).

“(2) Subsection (1) does not limit by implication the application of subsection 33(3A) of the Acts Interpretation Act 1901 in relation to this section.”.

Power of officers to inspect commercial documents in certain circumstances

11. Section 214AA of the Principal Act is amended:

(a) by omitting subparagraphs (1)(a)(i) and (ii) and substituting the following subparagraphs:

“(i) to take goods into home consumption under section 69 or 70; or

(ii) to take goods into home consumption, to warehouse goods, or to tranship goods, under section 71B; or

(iii) to deal with goods under section 114C; and”;

(b) by omitting from paragraph (1)(b) “connection with an entry of those goods under section 71A or section 114” and substituting:

“connection with:

(i) a return under paragraph 69(5)(c) or 70(7)(a) in respect of goods referred to in subparagraph (a)(i); or

(ii) an entry under section 71A in respect of goods referred to in subparagraph (a)(ii); or

(iii) an entry under section 114 in respect of goods referred to in subparagraph (a)(iii)”;

(c) by omitting from paragraph (1)(c) “the goods have been so entered” and substituting “the return has been given or the entry communicated to Customs, as the case requires”.

Power of officers to inspect commercial documents in other circumstances

12. Section 214AB of the Principal Act is amended by omitting from subsection (2) “the entry of goods” and substituting “a return given to Customs under section 69 or 70 or an entry communicated to Customs under section 71A or 114”.

Commercial documents to be kept

13. Section 240 of the Principal Act is amended:

(a) by inserting after subsection (1) the following subsection:

“(1AA) A person who is the owner of goods imported into Australia must keep all the relevant commercial documents relating to the goods:

(a) that come into the person’s possession or control before, or come into the person’s possession or control on or after, a return is given to Customs under section 69 or 70 in relation to those goods; and

(b) that are necessary to enable a Collector to satisfy himself or herself of the correctness of the particulars shown in the return;

until the end of the period of 5 years after the giving of the return.

Penalty: 20 penalty units.”;

(b) by inserting in subsections (2), (3) and (4) “, (1AA)” after “subsection (1)”;

(c) by inserting in subsection (6) “(1AA),” after “(1),”.

Processing requests for revocation of TCOs

14. Section 269SC of the Principal Act is amended by inserting after subsection (1) the following subsection:

“(1A) As soon as practicable after receiving a request for revocation of a TCO, the Comptroller must publish a Gazette notice stating:

(a) that the request has been lodged; and

(b) the date that the request was lodged; and

(c) the full particulars of the TCO to which the request relates.”.

Effect of revocation on goods in transit and capital equipment on order

15. Section 269SG of the Principal Act is amended:

(a) by inserting in subsection (1) “or (4)” after “269SC(3)”;

(b) by inserting in subsection (2) “or (4)” after “269SC(3)”;

(c) by omitting from subsection (4) “the Comptroller” and substituting “an officer of Customs”;

(d) by inserting in subsection (4) “or (4)” after “269SC(3)”.

Internal review

16.(1) Section 269SH of the Principal Act is amended by inserting after subsection (3) the following subsection:

“(3A) As soon as practicable after receiving a request for reconsideration of a decision that leads to the making of a TCO or that refuses to revoke a TCO, the Comptroller must publish a Gazette notice stating:

(a) that the request has been lodged; and

(b) the date that the request was lodged; and

(c) the full particulars of the TCO to which the request relates.”.

(2) Section 269SH of the Principal Act is further amended:

(a) by omitting from paragraph (4)(c) “subsection (6)” and substituting “subsection (7)”;

(b) by omitting from subsection (12) “(9)” and substituting “(10)”.

Interpretation

17. Section 273F of the Principal Act is amended by omitting subsection (2) and substituting the following subsection:

“(2) Unless the contrary intention appears, a reference in this Part to an item of a Customs Tariff includes a reference to a heading and a subheading in Schedule 3 to the Customs Tariff Act 1987.”.

Review of decisions under Customs Tariff Act

18. Section 273H of the Principal Act is amended by omitting from subsection (1) “the Minister or”.

Insertion of new section

19. After section 273K of the Principal Act, the following section is inserted:

Entry and transmission of information by computer

“273L. If this Act requires or permits information (including information in the form of particular words) to be entered or transmitted by computer, the information may be entered or transmitted by computer in an encoded form chosen by Customs.”.

Addition of new Schedule

20. After Schedule VI to the Principal Act the Schedule included in Schedule 1 to this Act is added.

PART 3—AMENDMENTS OF THE ANTI-DUMPING AUTHORITY ACT 1988

Principal Act

21. In this Part, “Principal Act” means the Anti-Dumping Authority Act 19882.

Anti-dumping measures not to apply to goods of New Zealand origin

22. Section 3A of the Principal Act is amended by omitting from subsection (2) “Section 151” and substituting “Division 1A of Part VIII”.

PART 4—MISCELLANEOUS

Further amendments of other Acts

23. The Acts specified in Schedule 2 are amended as set out in that Schedule.

SCHEDULE 1 Section 20

“SCHEDULE VII Section 153A

DIAGRAMS AND EXPLANATORY NOTES ILLUSTRATING

OPERATION OF DIVISION 1A OF PART VIII

DIAGRAM 1

Decision diagram for working out whether preference claim goods are the produce or manufacture of New Zealand

SCHEDULE 1—continued

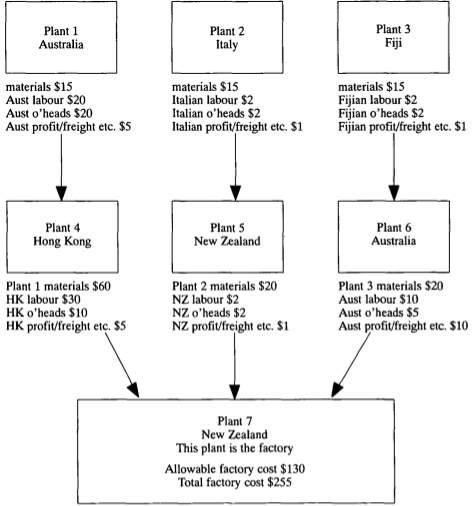

DIAGRAM 2

An example of possible inputs into goods last processed in New Zealand and claimed to be the manufacture of that country

[An explanation of the calculations to determine whether the goods are properly so claimed appears in the notes to the diagram.]

Plant 4 materials $105 (Allowable expenditure on materials nil)

Plant 5 materials $25 (Allowable expenditure on materials $5)

Plant 6 materials $45 (Allowable expenditure on materials $45)

NZ labour $60

NZ o’heads $20

SCHEDULE 1—continued

Notes relating to diagram 2

Goods imported into Australia after last process in the factory (ie Plant 7) are claimed to be the manufacture of New Zealand. This claim will be correct if the allowable factory cost of these preference claim goods is at least 50% of their total factory cost.

To work out both of these factory costs, we must first work out the allowable expenditure of the factory on the 3 manufactured materials that make up the preference claim goods. We will also need to take into account 3 other amounts, namely the total expenditure of the factory on materials, and the allowable expenditure of the factory on labour, and on overheads.

Working out allowable expenditure on materials (see section 153D)

• The allowable expenditure of the factory on particular manufactured materials in the form they are received from Plant 4 is nil because the materials are imported from outside the qualifying area (ie Hong Kong). (See subsection 153D(2)). This is so even though the manufactured materials themselves incorporate goods originating inside the qualifying area (ie Plant 1 in Australia).

• The allowable expenditure of the factory on particular manufactured materials in the form they are received from Plant 5 is not $25 but $5. This is because:

— the cost of contributing materials imported into the qualifying area from outside that area (ie Plant 2 in Italy) and subsequently processed is excluded under subsection 153D(4) from the working out of that allowable expenditure; and

— subsection 153D(6) does not apply.

• The allowable expenditure of the factory on particular manufactured materials in the form they are received from Plant 6 is the full cost to the manufacturer of $45. It is true that contributing materials are imported into the qualifying area from outside that area (ie Plant 3 in Fiji) and subsequently processed. However, the cost of those contributing materials is not required to be excluded under subsection 153D(4) from the working out of that allowable expenditure because subsection 153D(6) applies.

SCHEDULE 1—continued

Working out allowable factory cost (see section 153B)

Allowable expenditure of the factory on materials from Plants 4, 5 and 6 (Nil + $5 + $45) | $50 |

PLUS allowable expenditure of the factory on labour | $60 |

PLUS allowable expenditure of the factory on overheads | $20 |

TOTAL | $130 |

Working out total factory cost (see section 153B)

Total expenditure of the factory on materials from Plants 4, 5 and 6 ($105 + $25 + $45) | $175 |

PLUS allowable expenditure of the factory on labour | $60 |

PLUS allowable expenditure of the factory on overheads | $20 |

TOTAL | $255 |

CONCLUSION: Since allowable factory cost is at least 50% of total factory cost, goods are the manufacture of New Zealand. (See subsection 153J(2)).”.

SCHEDULE 2 Section 23

AMENDMENTS OF OTHER ACTS

Customs Legislation Amendment Act 1992

1. Paragraph 21(a):

Omit “ ‘mining operation’ ”, substitute “ ‘mining operations’ ”.

Customs Legislation (Anti-Dumping Amendments) Act 1992

2. Paragraph 4(a):

Omit “ ‘anti-dumping duty’ ”, substitute “ ‘dumping duty’ ”.

Customs Legislation (Tariff Concessions and Anti-Dumping) Amendment Act 1992

3. Subsection 20(6):

Omit “subsection (4)”, substitute “subsection (5)”.

NOTES

1. No. 6, 1901, as amended. For previous amendments, see No. 21, 1906; Nos. 9 and 36, 1910; No. 19, 1914; No. 10, 1916; No. 41, 1920; No. 19, 1922; No. 12, 1923; No. 22, 1925; No. 6, 1930; Nos. 7 and 45, 1934; No. 7, 1935; No. 85, 1936; No. 54, 1947; No. 45, 1949; Nos. 56 and 80, 1950; No. 56, 1951; No. 108, 1952; No. 47, 1953; No. 66, 1954; No. 37, 1957; No. 54, 1959; Nos. 42 and 111, 1960; No. 48, 1963; Nos. 29, 82 and 133, 1965; No. 28, 1966; No. 54, 1967; Nos. 14 and 104, 1968; Nos. 12 and 134, 1971; Nos. 162 and 216, 1973; Nos. 28 and 120, 1974; Nos. 56, 77 and 107, 1975; Nos. 41, 91 and 174, 1976; No. 154, 1977; Nos. 36 and 183, 1978; Nos. 92, 116, 177 and 180, 1979; Nos. 13, 15, 110 and 171, 1980; Nos. 45, 64, 67, 152 and 157, 1981; Nos. 48, 51, 80, 81, 115 and 137, 1982; No. 81, 1982; Nos. 19, 39 and 101, 1983; Nos. 2, 22, 63, 72 and 165, 1984; Nos. 39, 40 and 175, 1985; Nos. 10, 34 and 149, 1986; Nos. 51, 76, 81, 104 and 141, 1987; Nos. 63, 66 and 76, 1988; Nos. 23, 24, 79, 108 and 174, 1989; Nos. 5, 6, 11, 70, 79 and 111, 1990; Nos. 28, 82, 120 and 123, 1991; and Nos. 34, 89, 104, 164, 207, 209, 210 and 221, 1992.

2. No. 72, 1988, as amended. For previous amendments, see No. 174, 1989; No. 70, 1990; No. 122, 1991; and Nos. 89, 94 and 207, 1992.

[Minister’s second reading speech made in—

[Minister’s second reading speech made in—

Senate on 31 August 1993

House of Representatives on 16 November 1993]