(5) Part 2 of Schedule 10 is taken to have commenced immediately after the commencement of item 60 of Schedule 1 to the Taxation Laws Amendment Act (No. 4) 1994.

(6) Item 3 of Schedule 10 is taken to have commenced on the day on which Part 2 of Schedule 5 to the Taxation Laws Amendment Act (No. 4) 1994 commenced.

(7) Items 4 to 6 of Schedule 10 are taken to have commenced immediately after the commencement of Part 3 of Schedule 6.

(8) Item 7 of Schedule 10 is taken to have commenced immediately after the commencement of section 92 of the Taxation Laws Amendment Act (No. 3) 1994.

(9) Item 8 of Schedule 10 is taken to have commenced immediately after the commencement of section 130 of the Taxation Laws Amendment Act (No. 3) 1994.

(10) Part 5 of Schedule 10 is taken to have commenced immediately after the commencement of Division 9 of Part 2 of the Taxation Laws Amendment (Superannuation) Act 1992.

Schedules

3. The Acts and regulations specified in the Schedules to this Act are amended in accordance with the applicable items in the Schedules, and the other items in the Schedules have effect according to their terms

—————

SCHEDULE 1 Section 3

AMENDMENTS RELATING TO STATE/TERRITORY BODIES

PART 1—STATE/TERRITORY BODIES

Division 1—Income Tax Assessment Act 1936

Subdivision A—Certain State/Territory bodies exempt from tax

1. After Division 1AA of Part III:

Insert:

“Division 1AB—Certain State/Territory bodies exempt from income tax

“Subdivision A—Exemption for certain State/Territory bodies

Key principle

“24AK.

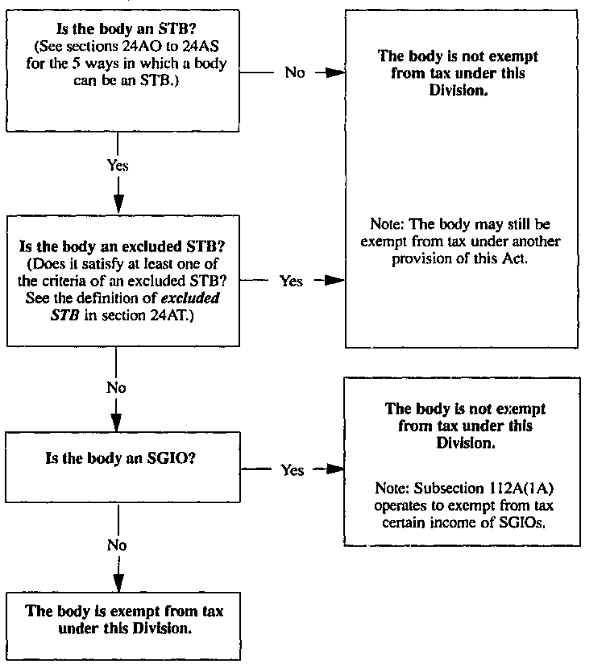

A body that is a State/Territory body (an STB) is exempt from income tax under this Division unless it is an excluded STB. There are 5 different ways in which a body can be an STB. |

Diagram—guide to work out if body is exempt under this Division

“24AL. The following diagram is a guide to help work out whether a body is exempt from income tax under this Division:

SCHEDULE 1—continued

SCHEDULE 1—continued

Certain STBs exempt from tax

“24AM. The income of a State/Territory body (an STB) is exempt from income tax unless section 24AN applies to the STB.

Certain STBs not exempt from tax under this Division

“24AN. Income derived by an STB is not exempt from income tax under this Division if, at the time that it is derived, the STB is an excluded STB or an SGIO.

Notes: 1. For the definition of excluded STB see section 24AT.

2. Even though an excluded STB is not exempt from income tax under this Division, it may still be exempt under another provision of this Act.

3. Subsection 112A(1A) operates to exempt certain income of SGIOs.

First way in which a body can be an STB

“24AO. A body is an STB if:

(a) it is a company limited solely by shares; and

(b) all the shares in it are beneficially owned by one or more government entities.

Note: For the definition of government entity see section 24AT. Note that an excluded STB is not a government entity.

Second way in which a body can be an STB

“24AP. A body is an STB if:

(a) it is established by State or Territory legislation; and

(b) it is not a company limited solely by shares; and

(c) the legislation provides that it must distribute all of its profits (if any) only to one or more government entities; and

(d) if the legislation makes provision as to the way its net assets may be distributed if it is dissolved or wound up—the provision is that, if it is dissolved, all of its net assets (if any) must be distributed only to one or more government entities.

Third way in which a body can be an STB

“24AQ. A body is an STB if:

(a) it is established by State or Territory legislation; and

(b) it is not a company limited solely by shares; and

(c) die legislation gives the power to appoint or dismiss its governing person or body only to one or more government entities.

Fourth way in which a body can be an STB

“24AR. A body is an STB if:

(a) it is established by State or Territory legislation; and

SCHEDULE 1—continued

(b) it is not a company limited solely by shares; and

(c) the legislation gives the power to direct its governing person or body as to the conduct of its affairs only to one or more government entities.

Fifth way in which a body can be an STB

“24AS. A body is an STB if:

(a) it is not a company limited solely by shares; and

(b) it is not established by State or Territory legislation; and

(c) all the legal and beneficial interests (including, but not limited to, interests as to income, profits, dividends, capital and distributions of capital) in it are held only by one or more government entities; and

(d) all the rights or powers (if any) to vote, appoint or dismiss its governing person or body and direct its governing person or body as to the conduct of its affairs are held only by one or more government entities.

What do excluded STB, government entity and Territory mean?

“24AT. In this Division:

excluded STB means an STB that:

(a) at a particular time, is prescribed as an excluded STB in relation to that time; or

(b) is a municipal corporation or other local governing body (within the meaning of paragraph 23(d)); or

(c) is a public educational institution (within the meaning of paragraph 23(e)); or

(d) is a public hospital (within the meaning of paragraph 23(ea)); or

(e) is a superannuation fund;

government entity means:

(a) a State; or

(b) a Territory; or

(c) another STB that is not an excluded STB;

Territory means the Northern Territory or the Australian Capital Territory.

Governor, Minister and Department Head taken to be a government entity

“24AU. For the purposes of sections 24AQ, 24AR and 24AS, if the power to appoint, dismiss or direct the governing body is given to, or is held by:

SCHEDULE 1—continued

(a) a Governor of a State; or

(b) a Minister of the Crown of a State; or

(c) a Minister of a Territory; or

(d) the head of a Department of a State or a Territory; or

(e) any combination of paragraphs (a) to (d);

the power is taken to be given to, or held by, a government entity.

Regulations prescribing excluded STBs

States and Territories to consent to STBs being excluded STBs

“24AV.(1) The regulations may prescribe that an STB is an excluded STB only if all States and Territories consent to the STB being so prescribed.

Regulations prescribing excluded STBs may be retrospective

“(2) Despite section 48 of the Acts Interpretation Act 1901, a regulation prescribing an STB as an excluded STB may provide that the STB is an excluded STB in relation to a time before the day of the notification of the regulation in the Gazette.

“Subdivision B—Body ceasing to be an STB

Body ceasing to be an STB

“24AW. This Act applies in relation to a body for a year of income (the cessation year) in which the body ceases to be an STB as if:

(a) the cessation were, for the purposes of Subdivision B of Division 2A, a disqualifying event that, by reason of section 50H, is taken to have occurred; and

(b) the references in that Subdivision to ‘company’ were references to ‘body’; and

(c) subsection 50A(2) did not apply in relation to that disqualifying event; and

(d) if the body is not a company—there were no other disqualifying events for the body in the cessation year; and

(e) for the purposes of section 50D, the amount of any notional loss incurred in the relevant period before the cessation were taken to be nil; and

(f) paragraph 50F(l)(c) were amended by omitting ‘79E,’ and ‘80,’; and

(g) deductions allowable under sections 79E and 80 were taken, under section 50G, to be allowable in respect of the relevant period before the cessation and not in respect of any other relevant period;

(h) for the purposes of Subdivision B of Division 2A, the application of Part IIIA were modified in accordance with section 24AX.

SCHEDULE 1—continued

Special provisions relating to capital gains and losses

Period after cessation date—prior net capital losses to be disregarded

“24AX.(1) In determining if an amount is to be included in the assessable income of the body under Part IIIA for a relevant period that occurred after the cessation, any net capital losses incurred before the cessation are to be disregarded.

Special cases where net capital gain before cessation and net capital loss after cessation

“(2) Subsections (3) and (4) apply if:

(a) a net capital gain accrued in the relevant period before the cessation; and

(b) if the period from the cessation until the end of the year of income were treated as a year of income—a net capital loss would have accrued in that period.

Special case 1—gain exceeds loss

“(3) If this subsection applies and the net capital gain exceeds the net capital loss:

(a) the amount that is to be included in the assessable income of the body for the relevant period that occurred before the cessation as a result of the net capital gain accruing to the body is taken to be the amount by which the net capital gain exceeds the net capital loss; and

(b) no net capital gain is taken to have accrued, and no net capital loss is taken to have been incurred, in any relevant period in the cessation year after the cessation; and

(c) in determining if a net capital gain accrued to, or a net capital loss was incurred by, the body for the year following the cessation year, no net capital loss is taken to have been incurred by the body in the cessation year.

Special case 2—loss equal to or exceeds gain

“(4) If this subsection applies and the net capital gain does not exceed the net capital loss:

(a) no amount is to be included in the assessable income of the body for any relevant period in the cessation year as a result of a net capital gain accruing to the body; and

(b) in determining if a net capital gain accrued to, or a net capital loss was incurred by, the body for the year following the cessation year, the net capital loss that the body incurred in the cessation year is taken to be the amount (if any) by which the net capital loss exceeds the net capital gain.

SCHEDULE 1—continued

Losses from STB years not carried forward

“24AY.(1) If a body is an STB on the last day of a year of income in which it incurs a loss (within the meaning of section 79E or 79F), the loss is not allowable as a deduction from the body’s assessable income of a later year of income unless the body is an STB on the first day of that later year of income.

Note: This section prevents losses from years prior to the cessation year from being carried forward to years after the cessation year.

“(2) This section only applies to losses incurred in the 1995-96 year of income or a later year of income.

Effect of unfunded superannuation liabilities

“24AYA.(1) This section applies to a deduction under section 82AAC in respect of a contribution made in relation to a person who was an employee of a prescribed excluded STB when it ceased to be an STB.

“(2) A deduction to which this section applies is not allowable to the body for any year of income unless the requirements of subsections (3) and (4) are complied with.

“(3) For the deduction to be allowable, the body must obtain a certificate by an authorised actuary stating the actuarial value, as at the time the body ceases to be an STB, of liabilities of the STB to provide superannuation benefits for, or for dependants of, employees of the body, where the liabilities:

(a) accrued after 30 June 1995 and before the time when the body ceased to be an STB; and

(b) were, according to actuarial principles, unfunded at that time.

“(4) The certificate must be in a form approved in writing by the Commissioner. The body must obtain the certificate:

(a) before the date of lodgment of its return of income of the year of income in which the body ceased to be an STB; or

(b) within such further time as the Commissioner allows.

“(5) If the body obtains the certificate, a deduction to which this section applies is nevertheless not allowable for a year of income if the sum of all deductions to which this section applies for the year of income is less than or equal to the unfunded liability limit (see subsection (6)) for the year of income.

“(6) If the sum is greater than that limit, so much of the deduction as is worked out using the following formula is not allowable:

SCHEDULE 1—continued.

Amount of deduction | X | Unfunded liability limit for the year of income |

Sum of all deductions to which this section applies for the year of income |

where:

Unfunded liability limit for a year of income is:

(a) if the year of income is the one in which the body ceases to be an STB—the actuarial value of the liabilities set out in the actuary’s certificate; or

(b) in any other case—that actuarial value as reduced by the total amount of deductions to which this section applies that, because of subsection (5), have not been allowable to the body for all previous years of income.

“(7) Expressions used in this section that are also used in section 82AAC have the same respective meanings as in that section.

Meaning of relevant period and prescribed excluded STB

“24AZ. In this Subdivision:

prescribed excluded STB means an STB that is an excluded STB as a result of regulations made for the purposes of paragraph (a) of the definition of excluded STB in section 24AT;

relevant period has the same meaning as in Subdivision B of Division 2A.”.

Subdivision B—Consequential amendments

2. Subsection 6(1) (definition of SGIO):

Omit “a public authority”, substitute “an STB (within the meaning of Division 1AB of Part III)”.

3. Paragraph 23(d):

After “public authority” insert “(other than an STB within the meaning of Division 1AB)”.

4. Subsections 46(9) and 46A(16):

Add at the end “or Division 1AB”,

5. Section 51AD:

Add at the end:

“(21) For the purposes of determining if this section applies to property, the income of a prescribed excluded STB (within the meaning of Division 1AB) is taken to be exempt.”.

SCHEDULE 1—continued

6. Subsection 73CB(6):

Add at the end:

“; or (c) an STB (within the meaning of Division 1AB).”.

7. Paragraph 73C(2)(b):

After “or a Territory” insert an STB (within the meaning of Division 1AB)”.

8. Section 102M (definition of exempt entity):

After paragraph (a) insert:

“(aa) an STB (within the meaning of Division 1AB) the income of which is wholly exempt from tax;”.

9. Section 121F (definition of relevant exempting provision):

After paragraph (bb) insert:

“(be) section 24AM;”.

10. Subsection 124ZA(1) (definition of exempt body):

Omit the definition, substitute:

“exempt body means :

(a) a body, association or fund to which paragraph 23(d), (e), (ea), (eb), (ec), (f), (g), (h), (i), (j) or (k) applies; or

(b) an STB (within the meaning of Division 1AB) the income of which is wholly exempt from tax;”.

11. Subsection 159GE(1) (definition of exempt public body):

After paragraph (a) insert:

“or (aa) an STB (within the meaning of Division 1AB) the income of which is wholly exempt from tax; or”.

12 After section 159GE:

Insert:

Division applies to certain State/Territory bodies

“159GEA. In addition to any other operation that this Division has, this Division operates as if the references to an exempt public body included a reference to a prescribed excluded STB (within the meaning of Division 1AB).”.

13. Subsection 160K(1) (definition of relevant exempting provision):

After paragraph (bb) insert:

“(bca) section 24AM;”.

SCHEDULE 1—continued

14. Subsection 269B(1):

Omit “section 23G”, substitute “sections 23G and 24AM”.

Division 2—Development Allowance Authority Act 1992

15. Subsection 93D(1) (definition of government body):

Omit the definition, substitute the following definition:

“government body means:

(a) the Commonwealth, a State or a Territory; or

(b) a body to which paragraph 23(d) of the Tax Act applies; or

(c) an STB (within the meaning of Division 1AB of Part III of the Tax Act) the income of which is wholly exempt from tax;”.

Division 3—Application of amendments made by this Part

16. Application

The amendments made by items 5 and 12 of this Part apply to income derived on or after 1 July 1995. All other amendments made by this Part apply to income derived on or after 1 July 1994.

SCHEDULE 1—continued

PART 2—SALES TAX (EXEMPTIONS AND CLASSIFICATIONS) ACT 1992

17. Object

The object of this Part is to exempt certain State and Territory bodies from sales tax.

18. Section 3:

Insert the following definitions:

“excluded STB has the meaning given by subsection 3D(6);

State/Territory body has the meaning given by section 3D;”.

19. Before section 4:

Insert in Part 2:

State/Territory bodies

First way in which a body can be a State/Territory body

“3D.(1) A body is a State/Territory body if:

(a) it is a company limited solely by shares; and

(b) all the shares in it are beneficially owned by one or more government entities.

Note. For the definition of government entity see subsection (6). Note that an excluded STB is not a government entity.

Second way in which a body can be a State/Territory body

“(2) A body is a State/Territory body if:

(a) it is established by State or Territory legislation; and

(b) it is not a company solely limited by shares; and

(c) the legislation provides that it must distribute all of its profits (if any) only to one or more government entities; and

(d) if the legislation makes provision as to the way its net assets may be distributed if it is dissolved or wound up—the provision is that, if it is dissolved, all of its net assets (if any) must be distributed only to one or more government entities.

Third way in which a body can be a State/Territory body

“(3) A body is a State/Territory body if:

(a) it is established by State or Territory legislation; and

(b) it is not a company solely limited by shares; and

(c) the legislation gives the power to appoint or dismiss its governing person or body only to one or more government entities.

SCHEDULE 1—continued

Fourth way in which a body can be a State/Territory body

“(4) A body is a State/Territory body if:

(a) it is established by State or Territory legislation: and

(b) it is not a company solely limited by shares; and

(c) the legislation gives the power to direct its governing person or body as to the conduct of its affairs only to one or more government entities.

Fifth way in which a body can be a State/Territory body

“(5) A body is a State/Territory body if:

(a) it is not a company solely limited by shares; and

(b) it is not established by State or Territory legislation; and

(c) all the legal and beneficial interests (including, but not limited to, interests as to income, profits, dividends, capital and distributions of capital) in it are held only by one or more government entities; and

(d) all the rights or powers (if any) to vote, appoint or dismiss its governing person or body and direct its governing person or body as to the conduct of its affairs are held only by one or more government entities.

What do excluded STB, government entity and Territory mean?

“(6) In this section:

excluded STB means a State/Territory body that:

(a) at a particular time, is prescribed as an excluded State/Territory body in relation to that time; or

(b) is a municipal corporation or other local governing body (within the meaning of paragraph 23(d) of the Income Tax Assessment Act 1936); or

(c) is a public educational institution (within the meaning of paragraph 23(e) of that Act); or

(d) is a public hospital (within the meaning of paragraph 23(ea) of that Act);

government entity means:

(a) a State; or

(b) a Territory; or

(c) another State/Territory body that is not an excluded State/Territory body;

Territory means the Northern Territory or the Australian Capital Territory.

SCHEDULE 1—continued

Governor, Minister and Department Head taken to be a government entity

“(7) For the purposes of subsections (3), (4) and (5), if the power to appoint, dismiss or direct the governing body is given to, or is held by:

(a) a Governor of a State; or

(b) a Minister of the Crown of a State; or

(c) a Minister of a Territory; or

(d) the Head of a Department of a State or a Territory; or

(e) any combination of paragraphs (a) to (d);

the power is taken to be given to, or held by, a government entity.

States and Territories to consent to State/Territory bodies being excluded STBs

“(8) The regulations may prescribe that a State/Territory body is an excluded STB only if all States and Territories consent to the State/Territory body being so prescribed.”.

20. After Item 126 in the Table of Contents in Schedule 1:

Insert:

“126A. State/Territory bodies”.

21. Subitem 126(2) of Schedule 1:

Omit the subitem, substitute:

“(2) This Item does not cover goods for use by:

(a) a Commonwealth-controlled authority within the meaning of section 130 of the Assessment Act; or

(b) a State/Territory body”.

22. After Item 126 of Schedule 1:

Insert:

Item 126A: [State/Territory bodies]

“Goods for use by a State/Territory body other than an excluded STB.”.

23. Paragraph 127(1)(c) of Schedule 1:

Add at the end:

“other than such a board or trust that is a State/Territory body”.

24. Application

The amendments made by this Part apply to dealings with goods after the commencement of this item.

SCHEDULE 1—continued

25. Transitional—periodic quotes by State/Territory bodies

If, before the commencement of this item, a State/Territory body (other than an excluded STB) has made a periodic quote under section 85 of the Sales Tax Assessment Act 1992 on the basis that goods will be used to satisfy exemption Item 126 or 127, then, after the commencement of this Item, the periodic quote is taken to have been made on the basis that goods will be used to satisfy exemption Item 126A.

——————

SCHEDULE 2 Section 3

EMPLOYEE SHARE SCHEMES

PART 1—INCOME TAX ASSESSMENT ACT 1936

Division 1—Insertion of Division 13A in Part III

1. After Division 13 of Part III:

Insert:

“Division 13A—Employee share schemes

“Subdivision A—Key principle and overview of Division

The key principle

“139.

This Division provides for the taxation treatment of shares and rights acquired under employee share schemes. . |

Any discount from the market price of the shares or rights is assessable. However, 2 alternative concessions are available for shares or rights provided under schemes that satisfy certain requirements. |

The first concession is that the discount will not be included in the employee’s assessable income until a later year of income. |

The second concession is that the employee may make an election that reduces the amount assessed. Additional requirements must be satisfied to obtain this concession. |

SCHEDULE 2—continued

Overview of Division

“139A. The following table summarises the contents of this Division:

OVERVIEW |

Subdivision | Coverage |

A | Key principle and overview |

B | The basic requirement that the discount be included in assessable income |

C | Key concepts: employee share scheme, discount, cessation time, qualifying shares, qualifying rights and exemption conditions |

D | Special provisions |

E | Elections |

F | Special provisions about the market value of a share or right |

G | Definitions (including a list of all terms defined in the Division) |

“Subdivision B—Inclusion of discount in assessable income

Discount to be included in assessable income

“139B.(1) If a taxpayer has acquired a share or right under an employee share scheme, the assessable income of the taxpayer includes the discount given in relation to the share or right.

Note: Employee share scheme is defined in section 139C.

When the discount is to be included

“(2) Unless subsection (3) applies, the discount is included in the taxpayer’s assessable income of the year of income in which the share or right is acquired.

“(3) If the share or right is a qualifying share or right and the taxpayer has not made an election under section 139E for the year of income in which the share or right is acquired, the discount is included in the taxpayer’s assessable income of the year of income in which the cessation time (see sections 139CA and 139CB) occurs.

Reduction of amounts included—elections

“139BA.(1) This section applies if a taxpayer has made an election under section 139E for a year of income and the exemption conditions (see section 139CE) are satisfied in relation to shares or rights covered by the

SCHEDULE 2—continued

election. It applies to the total amount otherwise included in a taxpayer’s assessable income for the year of income under section 139B in respect of those shares or rights.

“(2) The total amount is only included in the assessable income to the extent that it is greater than $500.

“Subdivision C—Key concepts: employee share scheme, discount, cessation time, qualifying shares and rights and exemption conditions

Employee share schemes

“139C.(1) A taxpayer acquires a share or right under an employee share scheme if the share or right is acquired by the taxpayer in respect of, or for or in relation directly or indirectly to, any employment of the taxpayer or an associate of the taxpayer.

“(2) A taxpayer acquires a share or right under an employee share scheme if the share or right is acquired by the taxpayer in respect of, or for or in relation directly or indirectly to, any services provided by the taxpayer or an associate of the taxpayer.

“(3) The taxpayer does not acquire a share or right under an employee share scheme if the consideration for the acquisition is equal to, or more than, the market value of the share or right at the time that it is acquired.

“(4) The taxpayer does not acquire a share under an employee share scheme if the taxpayer acquires the share as the result of exercising a right that the taxpayer acquired under an employee share scheme.

“(5) The taxpayer does not acquire a share or right under an employee share scheme if the taxpayer is a trust whose sole activities are obtaining shares, or rights to acquire shares, and providing those shares or rights to employees of a company or to associates of those employees.

Cessation time—shares

“139CA.(1) The cessation time for a share is the time when the taxpayer acquires the share if:

(a) there is no restriction preventing the taxpayer from disposing of the share before a particular time; and

(b) the scheme under which the share was acquired did not have any conditions that could result in the taxpayer forfeiting ownership of the share.

“(2) If subsection (1) does not apply, the cessation time for a share is the earliest of the following:

SCHEDULE 2—continued

(a) the time when the taxpayer disposes of the share;

(b) the later of:

(i) the time when any restriction preventing the taxpayer from disposing of the share ceases to have effect; and

(ii) the time when any condition that could result in the taxpayer forfeiting ownership of shares ceases to have effect;

(c) the time when the employment in respect of which the share was acquired ceases;

(d) the end of the 10 year period starting when the taxpayer acquired the share.

“(3) For the purposes of subsection (2), a taxpayer only ceases the employment in respect of which the share was acquired when the taxpayer is no longer employed by any of the following:

(a) the employer of the taxpayer in that employment;

(b) a holding company of the employer;

(c) a subsidiary of the employer or of a holding company of the employer.

Cessation time—rights

“139CB.(1) The cessation time for a right is the earliest of the following:

(a) the time when the taxpayer disposes of the right (other than by exercising it);

(b) the time when the employment in respect of which the right was acquired ceases;

(c) if the right is exercised and there is a restriction preventing the taxpayer from disposing of the share acquired as a result of the exercise of the right or a condition that could result in the taxpayer forfeiting ownership of the share—the time when the last such restriction or condition ceases to have effect;

(d) if the right is exercised and there is no such restriction or condition—the time when the right is exercised;

(e) the end of the 10 year period starting when the taxpayer acquired the right.

“(2) For the purposes of subsection (1), a taxpayer only ceases the employment in respect of which the right was acquired when the taxpayer is no longer employed by any of the following:

(a) the employer of the taxpayer in that employment;

(b) a holding company of the employer;

SCHEDULE 2—continued

(c) a subsidiary of the employer or of a holding company of the employer.

Calculation of discount

“139CC.(1) This section sets out how to calculate the discount given in relation to a share or right.

Case 1—discount covered by subsection 139B(2)

“(2) If subsection 139B(2) applies to the discount, the discount is the market value of the share or right at the time when it was acquired by the taxpayer less any consideration paid or given by the taxpayer as consideration for the acquisition of the share or right.

Case 2—discount covered by subsection 139B(3)—share or right disposed of at arm’s length within 30 days

“(3) If subsection 139B(3) applies to the discount, and the share or right (or any share acquired as a result of the exercise of the right) is disposed of by the taxpayer in an arm’s length transaction at the cessation time or within 30 days after the cessation time, the discount is:

(a) the amount or value of any consideration received by the taxpayer for the disposal;

reduced by:

(b) the amount or value of any consideration paid or given by the taxpayer as consideration for the acquisition of the share or right; and

(c) for a right that has been exercised—the amount or value of any consideration paid or given to exercise the right.

Case 3—discount covered by subsection 139B(3)—share or right not disposed of at arm’s length within 30 days

“(4) If subsection 139B(3) applies to the discount, and the share or right (or any share acquired as a result of the exercise of the right) is not disposed of by the taxpayer in an arm’s length transaction at the cessation time or within 30 days after the cessation time, the discount is:

(a) the market value of the share or right (or the share acquired as a result of the exercise of the right) at the cessation time;

reduced by:

(b) the amount of any consideration paid or given by the taxpayer as consideration for the acquisition of the share or right; and

(c) for a right that has been exercised—the amount of any consideration paid or given by the taxpayer to exercise the right.

SCHEDULE 2—continued

Meaning of qualifying shares and qualifying rights

“139CD.(1) For the purposes of this Division:

(a) a share in a company is a qualifying share if the 6 conditions below are satisfied; and

(b) a right to acquire a share in a company is a qualifying right if the first, second, third, fifth and sixth of the 6 conditions below are satisfied.

Note: Section 139DF excludes certain shares from being qualifying shares.

“(2) The first condition is that the share or right is acquired by a taxpayer under an employee share scheme.

“(3) The second condition is that the company is the employer of the taxpayer or a holding company of the employer of the taxpayer.

“(4) The third condition is that all the shares available for acquisition under the scheme are ordinary shares and all the rights available for acquisition under the scheme are rights to acquire ordinary shares.

“(5) The fourth condition is that, at the time the share was acquired, at least 75% of the employees of the employer were, or at some earlier time had been, entitled to acquire:

(a) shares or rights under the scheme; or

(b) shares or rights in the employer, or a holding company of the employer, under another employee share scheme.

“(6) The fifth condition is that, immediately after the acquisition of the share or right, the taxpayer does not hold a legal or beneficial interest in more than 5% of the shares in the company.

“(7) The sixth condition is that, immediately after the acquisition of the share or right, the taxpayer is not in a position to cast, or control the casting of, more than 5% of the maximum number of votes that might be cast at a general meeting of the company.

“(8) The Commissioner may determine that the fourth condition (see subsection (5)) is taken to have been satisfied in relation to a share or a right if the Commissioner considers that the employer has done everything reasonably practicable to ensure that the condition was satisfied.

Exemption conditions

“139CE.(1) This section sets out the 3 exemption conditions that must be satisfied for section 139B A to apply to a share or right acquired under an employee share scheme.

“(2) The first condition is that the scheme did not have any conditions that could result in any recipient forfeiting ownership of shares or rights acquired under it.

SCHEDULE 2—continued

“(3) The second condition is that the scheme was operated so that no recipient would be permitted to dispose of a share or right (the scheme share or scheme right) acquired under it, or of a share acquired as a result of a scheme right, before the earlier of the following times:

(a) the end of the period of 3 years after the time of the acquisition of the scheme share or scheme right;

(b) the time when the taxpayer ceased, or first ceased, to be employed by the employer.

“(4) The third condition is that both the employee share scheme and any scheme for the provision of financial assistance in respect of acquisitions of shares or rights under the employee share scheme are operated on a non -discriminatory basis (see section 139GE).

“(5) For the purposes of subsection (3), a taxpayer only ceases the employment in respect of which the share or right was acquired when the taxpayer is no longer employed by any of the following:

(a) the employer of the taxpayer in that employment;

(b) a holding company of the employer;

(c) a subsidiary of the employer or of a holding company of the employer.

“Subdivision D—Special provisions

Discount assessable to associate if share acquired by taxpayer in respect of associate’s employment

“139D.(1) This section applies if:

(a) a taxpayer has acquired a share or right under an employee share scheme; and

(b) the share or right was acquired by the taxpayer in respect of, or for or in relation directly or indirectly to, any employment of, or services rendered by, an associate of the taxpayer; and

(c) apart from this section, an amount would be included in respect of the acquisition in the assessable income of the taxpayer of a year of income under this Division.

“(2) If this section applies, the amount is included in the associate’s assessable income of the year of income instead of in the taxpayer’s assessable income.

Acquisition of legal interest in shares or rights—

certain discounts not assessable

“139DA. If:

SCHEDULE 2—continued

(a) a taxpayer has acquired the legal interest in a share or right; and

(b) the taxpayer, or an associate of the taxpayer, is required to include an amount under section 139B in the taxpayer’s or the associate’s assessable income as a result of the acquisition; and

(c) the taxpayer, or the associate, is, or would apart from section 139BA be, required to include an amount under section 139B in his or her assessable income as a result of the acquisition of the beneficial interest in the share or right;

the taxpayer, or the associate, is not required to include the amount mentioned in paragraph (b).

No deduction until share or right acquired

“139DB. If, at a particular time, a person (the provider) provides another person with money or other property:

(a) under an arrangement; and

(b) for the purpose of enabling another person (the ultimate beneficiary) to acquire, directly or indirectly, a share or right, under an employee share scheme;

then, for the purpose of determining when any deduction is allowable to the provider in respect of provision of the money or other property, the provider is taken to have provided it not before the time when the ultimate beneficiary acquires the share or right.

Note: The amount included in assessable income for the acquisition of an interest in a share is the same as for the acquisition of the share—see Subdivision F and section 139G.

Deduction for provider of certain qualifying shares or rights

“139DC.(1) A taxpayer is entitled to an allowable deduction in the taxpayer’s assessment in respect of income of a year of income (the benefit year) if the taxpayer provides one or more qualifying shares or qualifying rights to another person in the benefit year that satisfy the following conditions:

(a) the exemption conditions (see section 139CE);

(b) the condition that no amount has been allowed, is allowable, or will be allowable, as a deduction in the assessment of the taxpayer in respect of income of any year of income in respect of expenditure incurred in providing the share or right.

“(2) The amount of the deduction in respect of the shares or rights provided by the taxpayer to the person in the benefit year is the lesser of:

(a) $500; and

SCHEDULE 2—continued

(b) the sum of the market values, at the time that the share or right is provided, of each qualifying share or qualifying right that satisfies the conditions in subsection (1) reduced by the sum of any amounts paid by the person as consideration for those shares or rights.

Note: Only one deduction is allowable under this section in respect of each person to whom the taxpayer provided shares or rights in a year.

No benefit where rights lost

“139DD.(1) For the purposes of this Division, a right to acquire a share in a company is never acquired by a taxpayer if the following 2 requirements are satisfied.

“(2) The first requirement is that the taxpayer loses the right without having exercised it.

“(3) The second requirement is that the company is the employer of the taxpayer or a holding company of the employer of the taxpayer.

“(4) Section 170 does not prevent the amendment of an assessment at any time for the purpose of giving effect to this section.

Amount not assessable under section 21A or paragraph 26(e)

“139DE. Section 21A and paragraph 26(e) do not apply to:

(a) a share or right that a taxpayer acquires under an employee share scheme; or

(b) any share acquired by a taxpayer as a result of a right covered by paragraph (a).

Anti-avoidance—certain shares and rights not qualifying shares and qualifying rights

“139DF.(1) Despite any other provision of this Part, a share in a company, or a right to acquire a share in a company, acquired by a taxpayer is not a qualifying share or right if:

(a) the predominant business of the company (whether or not stated in its constituent documents) is the acquisition, sale or holding of shares, securities or other investments (whether directly or indirectly through one or more companies, partnerships or trusts); and

(b) the taxpayer is employed by the company and is also employed by another company; and

(c) the company and the other company are members of the same company group.

“(2) A company is a member of the same company group as another company if one of the companies is a holding company of the other or if another company is a holding company of both companies.

SCHEDULE 2—continued

“Subdivision E—Elections

Taxpayer may make election

“139E.(1) A taxpayer may make an election under this section that subsection 139B(2) applies for a year of income. The election covers each qualifying share or qualifying right acquired in that year by the taxpayer.

How and when election must be made

“(2) The election must be in writing in a form approved by the Commissioner and be made before the taxpayer lodges his or her return of income for the year of income, or within such further time as the Commissioner allows.

“Subdivision F—Special provisions about the market value of a share or right

Meaning of market value of a share or right

“139F. This Subdivision sets out how to determine the market value of a share or right to acquire a share on a particular day.

Listed shares or rights—market value

“139FA. If the share or right is quoted on a stock market of an approved stock exchange on that day, the market value is:

(a) if there was at least one transaction on that stock market in shares or rights of that class during the one week period before that day—the weighted average of the prices at which those shares or rights were traded on that stock market during the one week period before that day; or

(b) if there were no transactions on that stock market in that one week period in such shares or rights—the last price at which an offer was made on that stock market in that period to buy such a share or right.

Unlisted shares—market value

“139FB.(1) If the share is not quoted on an approved stock exchange on that day, the market value is the arm’s length value of the share:

(a) as specified in a written report, in a form approved by the Commissioner, given to the person from whom the taxpayer acquires the share by a person who is a qualified person in relation to valuing the share (see section 139FG); or

(b) as calculated in accordance with any other method approved in writing by the Commissioner as a reasonable method of calculating the arm’s length value of unlisted shares.

SCHEDULE 2—continued

Partly paid unlisted shares

“(2) Without limiting the factors that must be taken into account in valuing, under paragraph (1)(a), a share that is partly paid, the qualified person must take into account:

(a) the amount of the par value of the share that is already paid; and

(b) the amount and timing of future calls; and

(c) rights to dividends that arise from holding the share.

Unlisted rights—market value

“139FC. If the right is not quoted on an approved stock exchange on that day, the market value is the greater of:

(a) the market value, on the particular day, of the share that may be acquired by exercising the right, less the lowest amount that must be paid to exercise the right to acquire the share; and

whichever of the following applies:

(b) if the right can not be exercised more than 10 years after the day when the right was acquired—subject to section 139FE, the value determined in accordance with regulations for the purpose of this paragraph or, if no such regulations are in force, the value determined in accordance with sections 139FJ to 139FN;

(c) if the right can be exercised more than 10 years after the day when the right was acquired—the greater of:

(i) the arm’s length value of the right as specified in a written report, in a form approved by the Commissioner, given to the person from whom the taxpayer acquires the right by a suitably qualified valuer; and

(ii) the value that would have been determined under paragraph (b) if the right could be exercised 10 years after the particular day.

Conditions and restrictions to be disregarded

“139FD. In determining the market value of a share or right under section 139FB or 139FC, the share or right, and any share that may be acquired as a consequence of the exercise or operation of the right, is taken not to be subject to any conditions or restrictions.

Value of right nil or can not be determined

“139FE. If the lowest amount that must be paid to exercise a right to acquire a share is nil or can not be determined, the market value of the right on a particular day is the same as the market value of the share on that day.

SCHEDULE 2—continued

Value of legal and beneficial interests

“139FF. To avoid doubt, if a person acquires either the beneficial interest or the legal interest in a share or right, the value that is applicable for the purposes of this Division is the value of the share or right, not the value of the interest in the share or right.

Notes: 1. It is the value of the share or right that is relevant because the taxpayer is taken to have acquired the share or right—see section 139G.

2. Double taxation is avoided by section 139DA.

Meaning of qualified person

“139FG. A person is a qualified person in relation to valuing a share in a company if the person is registered as a company auditor under a law in force in a State or a Territory, and is not:

(a) a director, secretary or employee of the company; or

(b) a partner, employer or employee of a person referred to in paragraph

(a); or

(c) a partner or employee of an employee of a person so referred to.

Meaning of published price where multiple quotation

“139FH. If a share or right is quoted on a day on 2 or more approved stock markets, the published price on that day of that share or right is the published price on whichever of those stock markets is nominated by the taxpayer.

Provision of information about market value

“139FI. If a taxpayer requests the person from whom he or she acquired a share or right to provide information necessary for the taxpayer to calculate the market value of the share or right at a particular time, the person must take all reasonable steps to provide that information within 30 days after the request.

Outline of remainder of Subdivision

“139FJ. The remainder of this Subdivision sets out the method of calculating, for the purposes of paragraph 139FC(b), the market value, on a particular day, of a right to acquire a share.

Step 1—calculate the calculation percentage

“139FK. Apply the following formula. The result is the calculation percentage.

Market value, on the particular day, of the share that is the subject of the right | X | 100% |

Amount, or lowest amount, that must be paid to exercise the right |

SCHEDULE 2—continued

Step 2—how to use calculation percentage

1f calculation percentage is less than 50%

“139FL.(1) 1f the calculation percentage is less than 50%, the market value of the right is nil.

1f calculation percentage is equal to or greater than 50% but less than 110%

“(2) If the calculation percentage is equal to, or greater than, 50% but less than 110%, go to the instructions for using Table 1 in section 139FM that are set out below that Table.

If calculation percentage is equal to or greater than 110%

“(3) If the calculation percentage is equal to, or greater than, 110%, go to the instructions for using Table 2 in section 139FN that are set out below that Table.

Table 1 and instructions

Table 1

“139FM.(1) The following is Table 1:

Exercise period (months) | Calculation percentage |

50% to 60% | 60% to 70% | 70% to 75% | 75% to 80% | 80% to 85% | 85% to 90% | 90% to 92.5% | 92.5% to 95% |

108 to 120 | 0.6% | 2.1% | 4.8% | 6.7% | 8.9% | 11.4% | 14.1% | 15.5% |

96 to 108 | 0.4% | 1.5% | 4.0% | 5.8% | 7.9% | 10.3% | 13.0% | 14.5% |

84 to 96 | 0.2% | 1.1% | 3.2% | 4.8% | 6.8% | 9.2% | 11.8% | 13.3% |

72 to 84 | 0.1% | 0.7% | 2.4% | 3.8% | 5.6% | 7.9% | 10.5% | 11.9% |

60 to 72 | 0.0% | 0.4% | 1.6% | 2.8% | 4.4% | 6.5% | 9.0% | 10.4% |

48 to 60 | 0.0% | 0.1% | 0.9% | 1.8% | 3.1% | 4.9% | 7.3% | 8.6% |

36 to 48 | 0.0% | 0.0% | 0.4% | 0.9% | 1.9% | 3.3% | 5.4% | 6.6% |

24 to 36 | 0.0% | 0.0% | 0.1% | 0.3% | 0.8% | 1.8% | 3.4% | 4.4% |

18 to 24 | 0.0% | 0.0% | 0.0% | 0.1% | 0.4% | 1.0% | 2.3% | 3.2% |

12 to 18 | 0.0% | 0.0% | 0.0% | 0.0% | 0.1% | 0.4% | 1.3% | 2.0% |

9 to 12 | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.2% | 0.8% | 1.3% |

6 to 9 | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.3% | 0.7% |

3 to 6 | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.2% |

0 to 3 | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% |

SCHEDULE 2—continued

Table 1—continued

Exercise period (months) | Calculation percentage |

95% to 97.5% | 97.5% to 100% | 100% to 102.5% | 102.5% to 105% | 105% to 107.5% | 107.5% to 110% |

108 to 120 | 16.9% | 18.4% | 20.0% | 21.5% | 23.1% | 24.7% |

96 to 108 | 15.9% | 17.5% | 19.0% | 20.6% | 22.2% | 23.9% |

84 to 96 | 14.8% | 16.3% | 17.9% | 19.5% | 21.2% | 22.9% |

72 to 84 | 13.4% | 15.0% | 16.6% | 18.2% | 19.9% | 21.7% |

60 to 72 | 11.8% | 13.4% | 15.0% | 16.7% | 18.5% | 20.3% |

48 to 60 | 10.1% | 11.6% | 13.2% | 14.9% | 16.7% | 18.6% |

36 to 48 | 8.0% | 9.5% | 11.1% | 12.9% | 14.7% | 16.5% |

24 to 36 | 5.7% | 7.1% | 8.7% | 10.4% | 12.2% | 14.1% |

18 to 24 | 4.4% | 5.7% | 7.2% | 8.9% | 10.8% | 12.7% |

12 to 18 | 2.9% | 4.1% | 5.6% | 7.3% | 9.1% | 11.2% |

9 to 12 | 2.2% | 3.3% | 4.7% | 6.3% | 8.2% | 10.3% |

6 to 9 | 1.4% | 2.3% | 3.6% | 5.3% | 7.2% | 9.4% |

3 to 6 | 0.5% | 1.2% | 2.4% | 4.1% | 6.1% | 8.4% |

0 to 3 | 0.1% | 0.4% | 1.3% | 3.0% | 5.3% | 7.8% |

Instructions for using Table 1

“(2) From Table 1, select the percentage (the Table 1 percentage) that corresponds to:

(a) the period, in months, from the particular day until the last day on which the right may be exercised (the exercise period); and

(b) the calculation percentage;

and then multiply the amount, or lowest amount, that must be paid to exercise the right by the Table 1 percentage. The result is the market value of the right.

SCHEDULE 2—continued

Table 2 and instructions

Table 2

“139FN.(1) The following is Table 2:

Exercise period (months) | Column 1 | Column 2 |

108 to 120 | 24.7% | 0.6% |

96 to 108 | 23.9% | 0.6% |

84 to 96 | 22.9% | 0.7% |

72 to 84 | 21.7% | 0.7% |

60 to 72 | 20.3% | 0.7% |

48 to 60 | 18.6% | 0.7% |

36 to 48 | 16.5% | 0.8% |

24 to 36 | 14.1% | 0.8% |

18 to 24 | 12.7% | 0.8% |

12 to 18 | 11.2% | 0.9% |

9 to 12 | 10.3% | 0.9% |

6 to 9 | 9.4% | 0.9% |

3 to 6 | 8.4% | 0.9% |

0 to 3 | 7.8% | 1.0% |

Instructions for using Table 2—calculating the base percentage

“(2) From column 1 of Table 2, select the percentage that corresponds to the period, in months, from the particular day until the last day on which the right may be exercised. This percentage is called the base percentage.

Instructions for using Table 2—calculating the additional percentage

“(3) From column 2 of Table 2, select the percentage that corresponds to the exercise period (the exercise period). This percentage is called the additional percentage.

Instructions for using Table 2—calculating the excess

“(4) Work out the result of the following formula. Disregard any fraction. The result is called the excess.

100 | X | | Calculation | - | 110% | |

percentage |

SCHEDULE 2—continued

Instructions for using Table 2—calculating the market value

“(5) The market value of the right is the amount worked out using the following formula:

Amount or lowest amount that must be paid to exercise the right | X | | Base percentage | + |

| Excess | + | Additional | | |

| Percentage |

Note: If:

(a) the exercise period; or

(b) the calculation percentage in relation to a particular right;

is the top of one range in Table 1 or 2 and is also the bottom of another range in that Table, it is taken to be in the lower range and not in the higher range.

“Subdivision G—Definitions

Meaning of acquiring or providing a share or right

“139G. A person acquires a share or right if:

(a) another person transfers the share or right to that person (other than, in the case of a share, by issuing the share to that person); or

(b) in the case of a share—another person allots the share to that person; or

(c) in the case of a right—another person creates the right in that person; or

(d) the person otherwise acquires a legal interest in the share or right from another person; or

(e) the person acquires a beneficial interest in the share or right from another person.

In those circumstances, the other person provides the share or right.

Meaning of employee and employer

“139GA. The expressions employee and employer have the same meanings as in section 221 A.

Meaning of permanent employee

“139GB.(1) Subject to subsections (2) and (3), permanent employee of a company is:

(a) a full-time employee of the company; or

(b) a permanent part-time employee of the company;

with at least 36 months service (whether continuous or non-continuous).

SCHEDULE 2—continued

“(2) A person is not a permanent employee of the company at any time when the person is a director of the company.

“(3) A person is not a permanent employee at any time when the person:

(a) is an exempt visitor within the meaning of section 517 of the Income Tax Assessment Act 1936; or

(b) is not a resident within the meaning of that Act; or

(c) is not physically present in Australia.

“(4) For the purposes of subsection (1), the length of a person’s service includes any period when the person is, in accordance with the terms and conditions of that service:

(a) absent on recreation leave; or

(b) absent from work because of accident or illness.

“(5) In paragraph (4)(a), recreation leave does not include:

(a) long service leave, furlough, extended leave or leave of a similar kind (however described); or

(b) leave without pay or on reduced pay.

Meaning of holding company

“139GC. The expression holding company has the same meaning as in the Corporations Law.

Meaning of approved stock exchange

“139GD. A stock exchange is an approved stock exchange if:

(a) the stock exchange is named in regulations made for the purposes of this section; or

(b) if no such regulations are in force—the stock exchange is an approved stock exchange within the meaning of Part XI.

Meaning of associate

“139GE. The expression associate has the same meaning as it would have in section 26AAB if:

(a) the following paragraph were inserted before paragraph (14)(a) of that section:

“(aa) a company where the taxpayer holds (whether directly or indirectly through one or more interposed companies, partnerships or trusts) a share in the company, or a right to acquire a share in the company;”; and

(b) ‘paragraph (a)’ wherever occurring in subsection (14) were omitted and ‘paragraph (aa) or (a)’ were substituted.

SCHEDULE 2—continued

Meaning of conducting a scheme on a non-discriminatory basis

“139GF.( 1) This section sets out the conditions that must be satisfied for the employee share scheme mentioned in subsection 139CE(4) or a scheme for the provision of financial assistance in respect of acquisitions of shares or rights under the employee share scheme to be operated on a non-discriminatory basis.

Non-discriminatory employee share scheme

“(2) The employee share scheme is operated on a non-discriminatory basis if, and only if, the following conditions are satisfied in relation to all offers to acquire shares or rights under the scheme:

(a) participation in the scheme is open to at least 75% of permanent employees of the employer;

(b) the time for acceptance of each offer is reasonable;

(c) the essential features of each offer are the same for at least 75% of permanent employees of the employer.

Essential features of offer

“(3) The essential features of an offer for an employee share scheme are:

(a) the consideration for the acquisition of the share or right concerned (whether that consideration is determined by reference to the value of the share or right or otherwise); and

(b) the number of shares or rights, the minimum number of shares or rights or the maximum number of shares or rights, offered to each employee, as the case may be; and

(c) the time for acceptance of the offer; and

(d) the steps taken for the circulation of information about the offer.

Non-discriminatory financial assistance schemes

“(4) The scheme for the provision of financial assistance in respect of acquisitions of shares or rights under the employee share scheme is operated on a non-discriminatory basis if, and only if, the following conditions are satisfied in relation to all financial assistance provided under the scheme:

(a) the time for taking up each offer of assistance is reasonable;

(b) the essential features of each offer of assistance are the same for at least 75% of permanent employees of the employer.

Essential features of offer of financial assistance

“(5) The essential features of an offer of financial assistance are:

(a) the terms and conditions of the offer; and

SCHEDULE 2—continued

(b) the amount, the minimum amount, or the maximum amount, of assistance offered to each employee, as the case may be.

“(6) The Commissioner may determine that the condition mentioned in paragraph (2)(a), (2)(c) or (4)(b) is taken to have been satisfied in relation to a scheme if the Commissioner considers that the employer has done everything reasonably practicable to ensure that the condition was satisfied.

Meaning of provision of financial assistance

“139GG. The expression provision of financial assistance includes the making of a loan, giving of a guarantee, provision of security, release of an obligation and forgiving of a debt.

Index of definitions

“139GH. The following table lists the definitions in this Division and shows their location:

Definition | Provision |

Acquiring a share or right | 139G |

Approved stock exchange | 139GD |

Associate | 139GE |

Cessation time - rights | 139CB |

Cessation time - shares | 139CA |

Discount | 139CC |

Employee | 139GA |

Employee share scheme | 139C |

Employer | 139GA |

Exemption conditions | 139CE |

Financial assistance | 139GG |

Holding company | 139GC |

Market value of a share or right | Subdivision F |

Non-discriminatory schemes | 139GF |

Permanent employee | 139GB |

Providing a share or right | 139G |

Published price | 139FH |

Qualified person | 139FG |

Qualifying shares and qualifying rights | 139CD |

SCHEDULE 2—continued

Division 2—Other amendments of the Income Tax Assessment Act 1936

2. Subsection 26AAC(4):

Omit “This section” and substitute “Subject to subsection (4AA), this section”.

3. After subsection 26AAC(4):

Insert:

“(4AA) This section does not apply to an acquisition by a taxpayer of a share in a company, or of a right to acquire a share in a company, if:

(a) an amount is, or apart from section 139BA would be, included in the assessable income of the taxpayer under Division 13A in relation to the acquisition; or

(b) in the case of a share—the share was acquired as a result of the exercise of a right and this section did not apply in relation to the acquisition of the right.”.

4. Subsection 27A(1) (definition of eligible termination payment):

Add at the end:

“; or (q) amounts included in the assessable income of the taxpayer under Division 13A;”.

5. Section 160AZA (Main Index entry relating to Employee’s shares):

Omit “160ZYJA”, substitute “160ZYJE”.

6. Division 9 of Part IIIA (heading):

Add at the end: “— section 26AAC”.

7 After Division 9 of Part IIIA:

Insert:

“Division 9A—Employees' shares—Division 13A of Part III

Shares or rights under employee share scheme

“160ZYJB.(1) This section applies if an amount is, or apart from section 139BA would be, included in a taxpayer’s assessable income under Division 13 A of Part III as a result of the taxpayer acquiring a share or right.

“(2) If subsection 139CC(2) applies, the taxpayer is taken for the purposes of this Part to have paid, at the time when the share or right is acquired by the taxpayer, as consideration in respect of the acquisition, the greater of:

SCHEDULE 2—continued

(a) the amount paid by the taxpayer as consideration in respect of the acquisition; and

(b) the market value of the share or right at the time of the acquisition.

Note: Market Value is defined in Subdivision F of Division 13A of Part III.

“(3) If subsection 139CC(3) applies, this Part does not apply in respect of the disposal mentioned in that subsection.

“(4) If subsection 139CC(4) applies, the taxpayer is taken for the purposes of this Part to have paid, at the cessation time, an amount equal to the market value of the share or right at that time as consideration in respect of the acquisition.

Note: Cessation time is defined in sections 139CA and 139CB.

Shares or rights under employee share scheme—associates

“160ZYJC.(1) This section applies if an amount is included in a taxpayer’s assessable income under Division 13A of Part III as a result of an associate of the taxpayer acquiring a share or right.

Note: Associate is defined in section 139GE.

“(2) The associate is taken for the purposes of this Part to have paid, at the time when the share or right is acquired by the associate, as consideration in respect of the acquisition, the greater of:

(a) the amount paid by the associate as consideration in respect of the acquisition; and

(b) the market value of the share or right at the time of the acquisition.

Employee share trusts

“160ZYJD.(1) For the purposes of this Part, if:

(a) an amount is, or apart from section 139BA would be, included in a taxpayer’s assessable income under Division 13A of Part III as a result of the acquisition by the taxpayer of a share or right in a company; and

(b) the share or right was acquired by the taxpayer under the terms of a trust deed under which the trustee is required or authorised to sell, or otherwise to transfer, the share, or right, to:

(i) an employee of the company or of another company;

(ii) an associate of such an employee; and

(c) either no amount was paid by the taxpayer as consideration for the share or, if an amount was paid, that amount is equal to or less than the indexed cost base to the trustee of the share or right;

this Part does not apply in respect of the disposal by the trustee of the share or right to the taxpayer.

Note: Employee is defined in section 139GA.

SCHEDULE 2—continued

“(2) If the trust disposed of the share or right within 12 months after the share or right was acquired by the trust, the reference in paragraph (1)(c) to the indexed cost base to the trustee is to be read as a reference to the cost base to the trustee.

Terms have same meaning as in Division 13A of Part III

“160ZYJE. Despite section 160E, associate, cessation time, employee and market value have the same meaning in this Division as in Division 13A of Part III.”.

8. After section 530:

Insert in Division 16 of Part XI:

Reduction of foreign investment fund income because of employee share scheme shares or rights

“530A.(1) If:

(a) a taxpayer acquired a qualifying share or right under an employee share scheme and has not made an election under section 139E for the year of income in which the share or right is acquired; and

(b) there is a period (the reduction period) forming the whole or part of a notional accounting period of a FIF in respect of which the following conditions are satisfied:

(i) the taxpayer holds the share or right;

(ii) the share or right is an interest in the FIF;

(iii) the cessation time for the share or right has not occurred;

the foreign investment fund income of the taxpayer for the notional accounting period is to be reduced by an amount equal to any increase in the market value of the share or right during the reduction period.

“(2) In the section, cessation time, market value, qualifying right and qualifying share have the same meanings as in Division 13A of Part III.”.

SCHEDULE 2—continued

PART 2—FRINGE BENEFITS TAX ASSESSMENT ACT 1986

9. Subsection 136(1) (definition of fringe benefit):

After paragraph (h), insert:

“(ha) a benefit constituted by the acquisition by a person of a share or right under an employee share scheme (within the meaning of Division 13 A of Part III of the Income Tax Assessment Act 1936);

(hb) a benefit constituted by the acquisition by a trust of money or other property where the sole activities of the trust are obtaining shares, or rights to acquire shares, in a company (the employer), or a holding company (within the meaning of the Corporations Law) of the employer, and providing those shares or rights to employees of the employer;”.

SCHEDULE 2—continued

PART 3—SUPERANNUATION ENTITIES (TAXATION) ACT 1987

10. After section 20:

Insert:

Transitional—altered definition of eligible termination payment

“21. Part IIIA, including that Part as applying because of section 69 of the Taxation Laws Amendment (Superannuation) Act 1992, applies in relation to payments received after 24 December 1991 as if the definition of eligible termination payment in section 21A of the Tax Act did not cover amounts that, disregarding that definition, would be included in a taxpayer’s assessable income under section 26AAC or Division 13A of Part III of the Tax Act.”.

SCHEDULE 2—continued

PART 4—APPLICATION AND TRANSITIONAL

11. Application of amendments

(1) Subject to this section, the amendments made by this Schedule apply to the acquisition of a share, or right to acquire a share, if it occurs after 6 p.m. by legal time in the Australian Capital Territory on 28 March 1995.

(2) The amendments made by this Schedule do not apply to the acquisition of a share where the share was acquired as a result of the exercise of a right that:

(a) was acquired at or before 6 p.m. by legal time in the Australian Capital Territory on 28 March 1995; or

(b) is covered by subitem (3), (4) or (5).

(3) Subject to item 12, the amendments made by this Schedule do not apply to the acquisition of a share or right before 1 July 1995 where:

(a) the share or right was acquired as a result of an offer, or an invitation, made at or before 6 p.m. by legal time in the Australian Capital Territory on 28 March 1995; and

(b) the offer or invitation was made to employees of a company to acquire shares, or rights to acquire shares, in the company or in a holding company of the company.

(4) Subject to item 12, the amendments made by this Schedule do not apply to the acquisition of a share or right before 1 July 1996 where:

(a) the offer or invitation is to acquire shares, or rights to acquire shares, in a public company; and

(b) the share or right is acquired as a result of an offer, or an invitation, to employees of the public company or a subsidiary of the public company; and

(c) if the approval of shareholders is required for the scheme under which the offer or invitation was made—the scheme was approved by shareholders of the public company before 6 p.m. by legal time in the Australian Capital Territory on 28 March 1995.

(5) A taxpayer may make an election that the amendments made by this Schedule do not apply to the acquisition of particular shares or rights where:

(a) the total market value, when acquired, of the shares or rights covered by the election, does not exceed $1000; and

(b) the shares or rights were acquired before 1 July 1995 as a result of an offer, or an invitation, made at or before 6 p.m. by legal time in the Australian Capital Territory on 28 March 1995.

(6) For the purposes of subitem (5), the market value of a right is taken to be the same as the market value of the share to which it relates.

SCHEDULE 2—continued

(7) In this item:

public company means:

(a) a public company within the meaning of the Corporations Law; or

(b) a company established by Commonwealth, State or Territory legislation; or

(c) a company listed on an approved stock exchange.

Note: Approved stock exchange is defined in section 139GD of the Income Tax Assessment Act 1936.

subsidiary has the same meaning as in the Corporations Law.

12. Taxpayer may elect that amendments apply

The amendments made by this Schedule apply to the acquisition of a share or right by a taxpayer if:

(a) apart from subitem 11(3) or 11(4), the amendments would apply to the acquisition; and

(b) the taxpayer elects that the amendments apply to the acquisition.

13. Application of amendments—election that amendments apply

A taxpayer may make an election that the amendments made by this Schedule apply to the acquisition of a share, or a right to acquire a share, if the acquisition occurs after 7.30 p.m. by legal time in the Australian Capital Territory on 10 May 1994 and at or before 6 p.m. by legal time in the Australian Capital Territory on 28 March 1995.

14. Elections

An election under this Part must be in writing in a form approved by the Commissioner and be made before the later of:

(a) the end of 90 days after the commencement of this item; and

(b) the time when the taxpayer lodges his or her return for the 1994-95 year of income;

or within such further time as the Commissioner allows.

15. Transitional—subsection 139CD(5)

For the purposes of subsection 139CD(5) of the Income Tax Assessment Act 1936, a share or right is taken to be acquired under an employee share scheme if it would have been so acquired if item 11 of this Schedule provided that the amendments made by this Schedule applied to shares or rights acquired at any time before or after the commencement of this item.

—————

SCHEDULE 3 Section 3

VARIOUS AMENDMENTS OF THE INCOME TAX ASSESSMENT ACT 1936

PART 1—REFUNDS OF TFN AMOUNTS DEDUCTED IN ERROR

1. Paragraph 221YHZC(1A)(f):

Omit all the words from and including “reconciling” to and including “in respect of those deductions”, substitute “making the reconciliation required by subsection (1AA) and stating the total amount of refunds made by the investment body under subsection 221YHZDA(1) or paragraph 221YHZDAC(1)(d) in respect of deductions made in error during the financial year.”.

2. After subsection 221YHZC(1A):

Insert:

“(1AA) For the purposes of paragraph (1A)(f):

(a) the total of the amounts of all deductions made by the investment body during the financial year from unattributed income in respect of Part VA investments;

is to be reconciled with:

(b) the sum of:

(i) all amounts paid to the Commissioner under subsection 221YHZD(1A) in respect of those deductions; and

(ii) all amounts recorded under paragraph 221YHZD(1AB)(c) as being offset against amounts to be paid to the Commissioner in respect of those deductions.”.

3. Subsection 221YHZD(1A):

Omit “An investment body”, substitute “Subject to subsection (1AB), an investment body”.

4. After subsection 221YHZD(1AA):

Insert:

“(1AB) Subject to subsection (1AC), if:

(a) in discharging a liability under subsection 221YHZDA(1) or paragraph 221YHZDAC(1)(d), an investment body refunds to a person the whole or part of the amount of a deduction made in error during a financial year; and

SCHEDULE 3—continued

(b) the investment body is, apart from this subsection, required under subsection (1A) of this section to pay to the Commissioner an amount (the amount to be remitted) deducted, or purportedly deducted, during the same financial year from a payment of income to that person or to any other person; and

(c) the investment body makes a record to the effect that it offsets the whole or part of the refund against the amount to be remitted;

the amount to be remitted is reduced by the whole or the part of the refund.

“(1AC) The investment body must not record under paragraph (1AB)(c) that it offsets any part of a refund that:

(a) it has previously recorded under that paragraph; or

(b) it has applied to recover from the Commissioner under subsection 221YHZDA(1) or paragraph 221 YHZDAC(1)(d).”.

5. Paragraph 221YHZDA(1)(a):

After “deduction” insert “after the commencement of Part 1 of Schedule 3 to the Taxation Laws Amendment Act (No. 2) 1995".

6. Paragraph 221YHZDA(1)(a):

Omit “this Division”, substitute “subsection 221YHZC(1A)”.

7. Paragraph 221YHZDA(1)(a):

Add at the end “and”.

8. Subsection 221YHZDA(1):

After paragraph (c), insert the following word and paragraphs:

“and (d) the person has applied to the investment body for a refund of the excess amount on the basis of the error, or the investment body has otherwise become aware of the error, before the end of 15 July in the financial year after the one in which the deduction was made; and

(e) any information requested by the investment body under subsection (1A) has been given to it, or the time for making such a request (see subsection (1B)) has passed without such a request being made;”.

Note: The heading to section 221YHZDA is altered by omitting “in certain cases” and substituting “made in error—pre-16 July cases”.

9. Subsection 221YHZDA(1):

Omit “the excess amount from the Commissioner as a debt due to the investment body”, substitute “from the Commissioner, as a debt due to the investment body, so much of the excess amount as it has not recorded as being offset under paragraph 221YHZD(1AB)(c)”.

SCHEDULE 3—continued

10. After subsection 221YHZDA(1):

Insert:

“(1A) If, when the person makes the application mentioned in paragraph (1)(d), or when the investment body otherwise becomes aware of the error, the investment body does not have a record of:

(a) the person’s tax file number; or

(b) the basis on which the person was taken to have quoted his or her tax file number to the investment body in connection with the person’s investment;

the investment body may request the person to give the investment body the tax file number or evidence of the basis on which the person was taken to have quoted the tax file number.

“(1B) The request must be made within 7 working days (of the investment body) after it receives the person’s application for the refund or it otherwise becomes aware of the error.”.

11. Subsection 221YHZDA(2):

Omit the subsection, substitute:

“(2) If the investment body is liable to pay the excess amount to the person under subsection (1), the person is not entitled to a credit under section 221YHZK in respect of the excess amount.”.

12. After section 221YHZDA:

Insert:

Refund of deductions made in error—post-15 July cases

Application for refund

“221YHZDAA.(1) If:

(a) an investment body in relation to a Part VA investment has made a deduction after the commencement of this section, purportedly under subsection 221YHZC(1A), from income paid, in respect of a particular financial year, to a person in connection with the investment; and

(b) the amount deducted has been paid to the Commissioner; and

(c) the whole or a part of the amount of the deduction (the excess amount) was made in error; and

(d) the person did not apply to the investment body for a refund of the excess amount on the basis of the error, and the investment body did not otherwise become aware of the error, before the end of 15 July in the financial year after the one in which the deduction was made;

SCHEDULE 3—continued

the person may apply in writing to the Commissioner for a refund under this section.

Conditions for refund

“(2) If:

(a) the application states:

(i) if the person has a tax file number—that tax file number; or

(ii) if the person does not have a tax file number and was taken to have quoted a tax file number to the investment body before the deduction was made—the basis on which the person was taken to have quoted the tax file number; and

(b) the Commissioner is satisfied that the person is entitled to make the application under subsection (1); and

(c) the Commissioner considers that:

(i) it is unlikely that the person will become entitled to a credit under section 221YHZK in respect of the excess amount before the end of the financial year after the one in which the deduction was made; or

(ii) the person would suffer hardship if the Commissioner did not refund the excess amount; or

(iii) it would otherwise be fair and reasonable to refund the excess amount;

the Commissioner must refund the excess amount to the person.

No credit in respect of refund

“(3) A person is not entitled to a credit under section 221YHZK in respect of an amount refunded under subsection (2) of this section.

Special provision covering pre-1 July 1995 deductions

“221YHZDAB. If:

(a) immediately before the commencement of this section, an investment body was liable, under subsection 221YHZDA(1) as in force at that time, to pay to a person the whole or part of the amount of a deduction made in error; and

(b) the deduction was made on or before 30 June 1995; and