Chapter 3—Specialist liability rules

Part 3‑5—Corporate taxpayers and corporate distributions

Division 164—Non‑share capital accounts for companies

Guide to Division 164

164‑1 What this Division is about

A company that issues non‑share equity interests will have a notional account called a non‑share capital account. This account records contributions to the company in relation to those non‑share equity interests and returns made by the company of those contributions.

A non‑share distribution that represents a return of contributions is not taxed as a dividend (subject to the anti‑avoidance provisions dealing with dividend substitution). In certain circumstances a company may use its share capital account as the source for such distributions.

Table of sections

Operative provisions

164‑5 Object

164‑10 Non‑share capital account

164‑15 Credits to non‑share capital account

164‑20 Debits to non‑share capital account

Operative provisions

164‑5 Object

(1) This Division provides for the *non‑share capital account through which a company records contributions made to it in respect of *non‑share equity interests and returns by it of those contributions.

(2) This allows a *non‑share distribution to be characterised as either:

(a) a *non‑share dividend; or

(b) a *non‑share capital return.

164‑10 Non‑share capital account

(1) A company has a non‑share capital account if:

(a) the company issues a *non‑share equity interest in the company on or after 1 July 2001; or

(b) the company has issued a non‑share equity interest in the company before 1 July 2001 that is still in existence on 1 July 2001; or

(c) a *debt interest in the company changes at a particular time (the change time) to an *equity interest in the company because of subsection 974‑110(1) or (2); or

(d) the following conditions are satisfied in relation to an interest in the company:

(i) immediately before subsection 974‑75(4) ceases to have effect, the interest is taken to be a debt interest in the company because of that subsection;

(ii) the interest is an equity interest in the company at the time (the change time) that is immediately after that cessation;

(iii) subsection 974‑75(6) does not apply to the interest in relation to the income year that includes the change time; or

(e) the following conditions are satisfied in relation to an interest in the company:

(i) subsection 974‑75(6) applies to the interest in relation to a particular income year;

(ii) that subsection does not apply to the interest in relation to the next income year;

(iii) the interest is an equity interest in the company at the time (the change time) that is the start of that next income year.

(2) The account continues in existence even if the company ceases to have any *non‑share equity interests on issue.

(3) The balance of the account cannot fall below nil.

(4) The only credits and debits that may be made to the account are those provided for in sections 164‑15 and 164‑20.

164‑15 Credits to non‑share capital account

(1) If the company issues a *non‑share equity interest in the company on or after 1 July 2001, there is a credit to the *non‑share capital account equal to:

where:

amount received is the *market value, when it is provided, of the consideration the company receives for the issue of the interest.

share capital account credit is the amount of any credit made to the company’s *share capital account in respect of the issue of the interest.

Note: The issue of a non‑share equity interest can give rise to a credit to the company’s share capital account if the interest consists, for example, of a stapled security that includes a share in the company’s capital.

(2) If paragraph 164‑10(1)(c), (d) or (e) applies in relation to a particular interest in the company, there is a credit to the *non‑share capital account at the change time referred to in that paragraph of an amount equal to:

where:

amount received is the *market value, when it was provided, of the consideration the company received for the issue of the interest.

amount returned is so much of the amount received as has been returned to a holder of the interest before the change time.

share capital account credit is the amount of any credit made to the company’s *share capital account in respect of the issue of the interest.

(3) If the company has a *non‑share capital account at the beginning of 1 July 2001 because of a *non‑share equity interest the company issued before 1 July 2001, there is a credit to the non‑share capital account on that day for each non‑share equity interest in the company that:

(a) was issued before 1 July 2001; and

(b) is still in existence on 1 July 2001.

(4) The amount of the credit under subsection (3) is:

where:

amount received is the *market value, when it is provided, of the consideration the company receives for the issue of the interest.

return of amount received is the sum of the amounts paid before 1 July 2001 by way of return, in whole or in part, of the amount received.

share capital account credit is the sum of any amounts credited before 1 July 2001 to the company’s *share capital account in respect of the issue of the interest.

(5) To avoid doubt, if:

(a) it appears that a credit to the company’s *non‑share capital account has arisen under this section because an interest in the company appears to be, or have become, an *equity interest at a time in a particular income year; and

(b) because subsection 974‑75(6) or 974‑110(1A) is subsequently found to apply in relation to the interest and that income year, the interest was not in fact, or did not in fact become, an equity interest at that time;

the credit referred to in paragraph (a) is taken never to have arisen.

164‑20 Debits to non‑share capital account

(1) The company may debit the whole or a part of a *non‑share distribution against the company’s *non‑share capital account:

(a) to the extent to which the distribution is made as consideration for the surrender, cancellation or redemption of a *non‑share equity interest in the company; or

(b) to the extent to which:

(i) the distribution is made in connection with a reduction in the *market value of a non‑share equity interest in the company; and

(ii) the amount of the distribution is equal to the amount of the reduction in market value.

(2) The total of the amounts debited to the account in respect of a particular *non‑share equity interest must not exceed the total of the amounts credited to the account in respect of the interest.

(3) If:

(a) an *equity interest in the company changes at a particular time (the change time) to a *debt interest in the company because of subsection 974‑110(1) or (2); or

(b) an equity interest in the company changes to a debt interest in the company, with effect from a time (the change time) that is the start of a particular income year, because of subsection 974‑110(1A); or

(c) the following conditions are satisfied in relation to an interest in the company:

(i) subsection 974‑75(6) does not apply to the interest in relation to a particular income year;

(ii) the interest is an equity interest in the company at the end of that income year;

(iii) subsection 974‑75(6) applies to the interest from the time (the change time) that is the start of the next income year;

there is, or is taken to have been, a debit to the *non‑share capital account at the change time equal to:

where:

credits in relation to the interest is the sum of all the credits that have been made to the *non‑share capital account in relation to the interest before the change time.

debits in relation to the interest is the sum of all the debits that have been made to the *non‑share capital account in relation to the interest before the change time.

(4) To avoid doubt, if:

(a) it appears that a debit to the company’s *non‑share capital account has arisen because an interest in the company appears to be, or have become, a *debt interest at a time in a particular income year; and

(b) because subsection 974‑75(6) or 974‑110(1A) is subsequently found not to apply in relation to the interest and that income year, the interest was not in fact, or did not in fact become, a debt interest at that time;

the debit referred to in paragraph (a) is taken never to have arisen.

Division 165—Income tax consequences of changing ownership or control of a company

Table of Subdivisions

Guide to Division 165

165‑A Deducting tax losses of earlier income years

165‑B Working out the taxable income and tax loss for the income year of the change

165‑CA Applying net capital losses of earlier income years

165‑CB Working out the net capital gain and the net capital loss for the income year of the change

165‑CC Change of ownership or control of company that has an unrealised net loss

165‑CD Reductions after alterations in ownership or control of loss company

165‑C Deducting bad debts

165‑D Tests for finding out whether the company has maintained the same owners

165‑E The same business test

165‑F Special provisions relating to ownership by non‑fixed trusts

Guide to Division 165

165‑1 What this Division is about

A change in the ownership or control of a company can affect:

• whether it can deduct its tax losses of earlier income years; and

• how it calculates its taxable income and tax loss for the income year of the change; and

• whether it can deduct debts owed to it that are written off as bad.

Subdivision 165‑A—Deducting tax losses of earlier income years

Guide to Subdivision 165‑A

165‑5 What this Subdivision is about

A company cannot deduct a tax loss unless:

(a) it has the same owners and the same control throughout the period from the start of the loss year to the end of the income year; or

(b) it satisfies the same business test by carrying on the same business, entering into no new kinds of transactions and conducting no new kinds of business.

Note: The exceptions mentioned in this section apply differently in relation to designated infrastructure project entities: see section 415‑35.

Table of sections

Operative provisions

165‑10 To deduct a tax loss

165‑12 Company must maintain the same owners

165‑13 Alternatively, the company must satisfy the same business test

165‑15 The same people must control the voting power, or the company must satisfy the same business test

165‑20 When company can deduct part of a tax loss

Operative provisions

165‑10 To deduct a tax loss

A company cannot deduct a *tax loss unless either:

(a) it meets the conditions in section 165‑12 (which is about the company maintaining the same owners); or

Note: See section 165‑215 for a special alternative to these conditions.

(b) it meets the condition in section 165‑13 (which is about the company satisfying the same business test).

Note: In the case of a widely held or eligible Division 166 company, Subdivision 166‑A modifies how this Subdivision applies, unless the company chooses otherwise.

165‑12 Company must maintain the same owners

Ownership test period

(1) In determining whether section 165‑10 prevents a company from deducting a *tax loss, the ownership test period is the period from the start of the *loss year to the end of the income year.

Note: See section 165‑255 for the rule about incomplete test periods.

Voting power

(2) There must be persons who had *more than 50% of the voting power in the company at all times during the *ownership test period.

Note 1: See section 165‑150 to work out who had more than 50% of the voting power.

Note 2: Subdivision 167‑B has special rules for working out voting power in a company whose shares do not all carry the same voting rights, or do not carry all of the voting rights in the company.

Rights to dividends

(3) There must be persons who had rights to *more than 50% of the company’s dividends at all times during the *ownership test period.

Note 1: See section 165‑155 to work out who had rights to more than 50% of the company’s dividends.

Note 2: Subdivision 167‑A has special rules for working out rights to dividends in a company whose shares do not all carry the same rights to dividends.

Rights to capital distributions

(4) There must be persons who had rights to *more than 50% of the company’s capital distributions at all times during the *ownership test period.

Note 1: See section 165‑160 to work out who had rights to more than 50% of the company’s capital distributions.

Note 2: Subdivision 167‑A has special rules for working out rights to capital distributions in a company whose shares do not all carry the same rights to capital distributions.

When to apply the primary test

(5) To work out whether a condition in this section was satisfied at all times during the *ownership test period, apply the primary test for that condition unless subsection (6) requires the alternative test to be applied.

Note: For the primary test, see subsections 165‑150(1), 165‑155(1) and 165‑160(1).

When to apply the alternative test

(6) Apply the alternative test for that condition if one or more other companies beneficially owned *shares or interests in shares in the company at any time during the *ownership test period.

Note: For the alternative test, see subsections 165‑150(2), 165‑155(2) and 165‑160(2).

Conditions in subsections (2), (3) and (4) may be treated as having been satisfied in certain circumstances

(7) If any of the conditions in subsections (2), (3) and (4) have not been satisfied, those conditions are taken to have been satisfied if:

(a) they would have been satisfied except for the operation of section 165‑165; and

(b) the company has information from which it would be reasonable to conclude that less than 50% of the *tax loss has been reflected in deductions, capital losses, or reduced assessable income, that occurred, or could occur in future, because of the happening of any *CGT event in relation to any *direct equity interests or *indirect equity interests in the company during the *ownership test period.

(7A) If the company is:

(a) a *non‑profit company; or

(b) a *mutual affiliate company; or

(c) a *mutual insurance company;

during the whole of the *ownership test period, the conditions in subsections (3) and (4) are taken to have been satisfied by the company.

Time of happening of CGT event

(8) The happening of a *CGT event in relation to a *direct equity interest or *indirect equity interest in the company that results in the failure of the company to satisfy a condition in subsection (2), (3) or (4) is taken, for the purposes of paragraph (7)(b), to have occurred during the *ownership test period.

165‑13 Alternatively, the company must satisfy the same business test

(1) This section sets out the condition that a company must meet to be able to deduct the *tax loss if:

(a) the company fails to meet a condition in subsection 165‑12(2), (3) or (4); or

(b) it is not practicable to show that the company meets the conditions in those subsections.

Note Other provisions may treat the company as meeting, or failing to meet, the conditions in subsections 165‑12(2), (3) and (4).

(2) The company must satisfy the *same business test for the income year (the same business test period). Apply the test to the *business the company carried on immediately before the time (the test time) shown in the relevant item of the table.

Test time |

Item | If: | The test time is: |

1 | It is practicable to show there is a period that meets these conditions: (a) the period starts at the start of the *ownership test period or, if the company came into being during the *loss year, at the time the company came into being; (b) the company would meet the conditions in subsections 165‑12(2), (3) and (4) if the period were the ownership test period for the purposes of this Act | The latest time that it is practicable to show is in the period |

2 | Item 1 does not apply and the company was in being throughout the *loss year | The start of the loss year |

3 | Item 1 does not apply and the company came into being during the *loss year | The end of the loss year |

For the same business test: see Subdivision 165‑E.

165‑15 The same people must control the voting power, or the company must satisfy the same business test

(1) Even if a company meets the conditions in section 165‑12 or 165‑13, it cannot deduct the *tax loss if:

(a) for some or all of the part of the *ownership test period that started at the end of the *loss year, a person controlled, or was able to control, the voting power in the company (whether directly, or indirectly through one or more interposed entities); and

(b) for some or all of the *loss year, that person did not control, and was not able to control, that voting power (directly, or indirectly in that way); and

(c) that person began to control, or became able to control, that voting power (directly, or indirectly in that way) for the purpose of:

(i) getting some benefit or advantage in relation to how this Act applies; or

(ii) getting such a benefit or advantage for someone else;

or for purposes including that purpose.

Note: A person can still control the voting power in a company that is in liquidation etc.: see section 165‑250.

(2) However, that person’s control of the voting power, or ability to control it, does not prevent the company from deducting the *tax loss if the company satisfies the *same business test for the income year (the same business test period).

(3) Apply the *same business test to the *business that the company carried on immediately before the time (the test time) when the person began to control that voting power, or became able to control it.

For the same business test: see Subdivision 165‑E.

165‑20 When company can deduct part of a tax loss

(1) If section 165‑10 (which is about deducting a tax loss) prevents a company from deducting a *tax loss, the company can deduct the part of the tax loss that was incurred during a part of the loss year.

(2) However, the company can do this only if, assuming that part of the *loss year had been treated as the whole of the loss year for the purposes of section 165‑10, the company would have been entitled to deduct the *tax loss.

Subdivision 165‑B—Working out the taxable income and tax loss for the income year of the change

Guide to Subdivision 165‑B

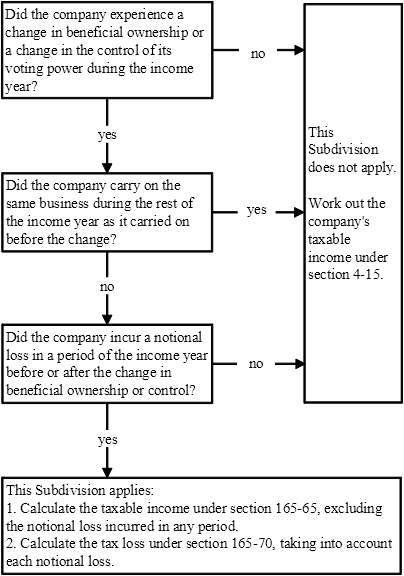

165‑23 What this Subdivision is about

A company that has not had the same ownership and control during the income year, and has not satisfied the same business test, works out its taxable income and tax loss under this Subdivision.

Table of sections

165‑25 Summary of this Subdivision

165‑30 Flow chart showing the application of this Subdivision

When a company must work out its taxable income and tax loss under this Subdivision

165‑35 On a change of ownership, unless the company satisfies the same business test

165‑37 Who has more than a 50% stake in the company during a period

165‑40 On a change of control of the voting power in the company, unless the company satisfies the same business test

Working out the company’s taxable income

165‑45 First, divide the income year into periods

165‑50 Next, calculate the notional loss or notional taxable income for each period

165‑55 How to attribute deductions to periods

165‑60 How to attribute assessable income to periods

165‑65 How to calculate the company’s taxable income for the income year

Working out the company’s tax loss

165‑70 How to calculate the company’s tax loss for the income year

Special rules that apply if the company is in partnership

165‑75 How to calculate the company’s notional loss or notional taxable income for a period when the company was a partner

165‑80 How to calculate the company’s share of a partnership’s notional loss or notional net income for a period if both entities have the same income year

165‑85 How to calculate the company’s share of a partnership’s notional loss or notional net income for a period if the entities have different income years

165‑90 Company’s full year deductions include a share of partnership’s full year deductions

165‑25 Summary of this Subdivision

(1) The company calculates its taxable income for the income year in this way:

Method statement

Step 1. Divide the income year into periods: each change in ownership or control is a dividing point between periods.

Step 2. Treat each period as if it were an income year and work out the notional loss or notional taxable income for that period.

Step 3. Work out the taxable income for the year of the change by adding up:

each notional taxable income; and

any full year amounts (amounts of assessable income not taken into account at Step 2);

and then subtracting any full year deductions (deductions not taken into account at Step 2).

Note: Do not take into account any notional loss.

(2) As well as a taxable income, the company will have a tax loss. It is the total of:

• each notional loss; and

• excess full year deductions of particular kinds.

(3) Special rules apply if the company was in partnership at some time during the income year.

For the special rules that apply if the company was in partnership: see sections 165‑75 to 165‑90.

165‑30 Flow chart showing the application of this Subdivision

Note: If the company was a partner during the income year, special rules apply to calculating a notional loss or notional taxable income.

When a company must work out its taxable income and tax loss under this Subdivision

165‑35 On a change of ownership, unless the company satisfies the same business test

A company must calculate its taxable income and *tax loss under this Subdivision unless:

(a) there are persons who had *more than a 50% stake in the company during the whole of the income year; or

Note: See section 165‑220 for a special alternative to the condition in this paragraph.

(b) there is only part of the income year (a part that started at the start of the income year) during which the same persons had *more than a 50% stake in the company, but the company satisfies the *same business test for the rest of the income year (the same business test period); or

(c) the company was a *designated infrastructure project entity during the whole of the income year.

Note: See subsection 415‑35(7) if there is only part of the income year during which the company was a designated infrastructure project entity.

For the purposes of paragraph (b), apply the *same business test to the *business that the company carried on immediately before the time (the test time) when that part ended.

Note 1: For the same business test, see Subdivision 165‑E.

Note 2: In the case of a widely held or eligible Division 166 company, Subdivision 166‑B modifies how this Subdivision applies, unless the company chooses otherwise.

165‑37 Who has more than a 50% stake in the company during a period

(1) If:

(a) there are persons who had *more than 50% of the voting power in the company during the whole of a period (the ownership test period) consisting of the income year or a part of it; and

(b) there are persons who had rights to *more than 50% of the company’s dividends during the whole of the ownership test period; and

(c) there are persons who had rights to *more than 50% of the company’s capital distributions during the whole of the ownership test period;

those persons had more than a 50% stake in the company during the ownership test period.

Note: Division 167 has special rules for working out rights to voting power, dividends and capital distributions in a company whose shares do not all carry the same rights to those matters.

(2) To work out whether a condition in subsection (1) was satisfied during the *ownership test period, apply the primary test for that condition unless subsection (3) requires the alternative test to be applied.

For the primary tests: see subsections 165‑150(1), 165‑155(1)

and 165‑160(1).

(3) Apply the alternative test for that condition if one or more other companies beneficially owned *shares, or interests in shares, in the company at any time during the *ownership test period.

For the alternative tests: see subsections 165‑150(2), 165‑155(2)

and 165‑160(2).

Conditions in subsection (1) may be treated as having been satisfied in certain circumstances

(4) If any of the conditions in subsection (1) have not been satisfied, those conditions are taken to have been satisfied if:

(a) they would have been satisfied except for the operation of section 165‑165; and

(b) the company has information from which it would be reasonable to conclude that less than 50% of the *notional loss for the *ownership test period has been reflected in deductions, capital losses, or reduced assessable income, that occurred, or could occur in future, because of the happening of any *CGT event in relation to any *direct equity interests or *indirect equity interests in the company during that period.

(4A) If the company is:

(a) a *non‑profit company; or

(b) a *mutual affiliate company; or

(c) a *mutual insurance company;

during the whole of the *ownership test period, the conditions in paragraphs (1)(b) and (c) are taken to have been satisfied by the company.

Time of happening of CGT event

(5) The happening of a *CGT event in relation to a *direct equity interest or *indirect equity interest in the company that results in the failure of the company to satisfy a condition in subsection (1) is taken, for the purposes of paragraph (4)(b), to have occurred during the *ownership test period.

165‑40 On a change of control of the voting power in the company, unless the company satisfies the same business test

(1) A company must calculate its taxable income and tax loss under this Subdivision if, during the income year, a person begins to control, or becomes able to control, the voting power in the company (whether directly, or indirectly through one or more interposed entities) for the purpose, or for purposes including the purpose, of:

(a) getting some benefit or advantage in relation to how this Act applies; or

(b) getting such a benefit or advantage for someone else.

Note 1: A person can still control the voting power in a company that is in liquidation etc.: see section 165‑250.

Note 2: Subdivision 167‑B has special rules for working out voting power in a company whose shares do not all carry the same voting rights, or do not carry all of the voting rights in the company.

(2) However, that person’s control of the voting power, or ability to control it, does not require the company to calculate its taxable income under this Subdivision if the company satisfies the *same business test for the rest of the income year (the same business test period).

(3) Apply the *same business test to the *business that the company carried on immediately before the time (the test time) when the person began to control that voting power, or became able to control it.

For the same business test: see Subdivision 165‑E.

Working out the company’s taxable income

165‑45 First, divide the income year into periods

(1) Divide the income year into periods as follows.

(2) The first period starts at the start of the income year. Each later period starts immediately after the end of the previous period.

(3) The last period ends at the end of the income year. Each period (except the last) ends at the earlier of:

(a) the latest time that would result in persons having *more than a 50% stake in the company during the whole of the period; or

(b) the earliest time when a person begins to control, or becomes able to control, the voting power in the company (whether directly, or indirectly through one or more interposed entities) for the purpose, or for purposes including the purpose, of:

(i) getting some benefit or advantage to do with how this Act applies; or

(ii) getting such a benefit or advantage for someone else.

Note: See section 165‑255 for the rule about incomplete periods.

(4) However, what would otherwise be 2 or more successive periods are treated as a single period if the company satisfies the *same business test for all of them, considered as a single period (the same business test period). Apply the same business test to the *business the company carried on immediately before the end of the first of the periods (the test time).

Note 1: For the same business test, see Subdivision 165‑E.

Note 2: See section 165‑225 for a special alternative to subsections (3) and (4) of this section.

165‑50 Next, calculate the notional loss or notional taxable income for each period

(1) The company has a *notional loss for a period if the deductions attributed to the period under section 165‑55 exceed the assessable income attributed to the period under section 165‑60. The notional loss is the amount of the excess.

For a period during which the company was in partnership,

the notional loss is worked out under section 165‑75.

(2) On the other hand, if that assessable income exceeds those deductions, the company has a notional taxable income for the period, equal to the excess.

For a period during which the company was in partnership,

the notional taxable income is worked out under section 165‑75.

(3) If the company has a *notional loss for none of the periods in the income year, this Subdivision has no further application, and the company’s taxable income for the income year is calculated in the usual way.

The usual way of working out taxable income is set out in section 4‑15.

165‑55 How to attribute deductions to periods

(1) The company’s deductions for the income year are attributed to periods in the income year as follows.

(2) The following deductions are attributed to each period in proportion to the length of the period:

(a) deductions for the decline in value of a *depreciating asset;

See Division 40.

(b) deductions for *exploration or prospecting, or *mining capital expenditure, in connection with mining or quarrying;

See section 40‑80 and Subdivisions 40‑H and 40‑I.

(c) deductions for expenditure, deductions for which are spread over 2 or more income years, but not:

(i) deductions for exploration or prospecting, or capital expenditure, in connection with mining or quarrying; or

See Subdivision 40‑I.

(ii) *full year deductions (see subsection (5));

(d) deductions for expenditure of capital monies in connection with an Australian *film.

See former section 124ZAFA of the Income Tax Assessment Act 1936.

(3) All other deductions (except *full year deductions) are attributed to periods as if each period were an income year.

(4) *Full year deductions are not attributed to any of the periods. They are brought in at a later stage of the process of calculating the company’s taxable income for the income year.

(5) These are full year deductions:

(a) deductions for bad debts under section 8‑1 (about general deductions) or section 25‑35 (about bad debts);

(b) deductions for losses on debt/equity swaps under section 63E of the Income Tax Assessment Act 1936;

(c) deductions, so far as they are allowable under Division 8 (which is about deductions) because Subdivision H (Period of deductibility of certain advance expenditure) of Division 3 of Part III of the Income Tax Assessment Act 1936 applies to the company in relation to the income year;

(fa) deductions for payments of pensions, gratuities or retiring allowances under section 25‑50;

(fb) deductions for gifts under Division 30;

(f) deductions for *tax losses of earlier income years.

See Division 36.

(6) However, a deduction for the balance of capital expenditure is not a full year deduction if the deduction results from the disposal, loss, lapse, termination of use or destruction of the property.

165‑60 How to attribute assessable income to periods

(1) The company’s assessable income for the income year is attributed to periods in the income year as follows.

(2) The following amounts are attributed to periods so far as they are reasonably attributable to those periods:

(a) amounts included in the company’s assessable income under section 97 (Beneficiary of a trust estate who is not under a legal disability) of the Income Tax Assessment Act 1936; or

(b) amounts included in the company’s assessable income under section 98A (Non‑resident beneficiaries assessable in respect of certain income) of the Income Tax Assessment Act 1936.

(2A) However, so much of an amount included in the company’s assessable income under section 97 or 98A of the Income Tax Assessment Act 1936 as is a *capital gain that forms part of a *net capital gain is not attributed to a period.

(3) The following items of assessable income are attributed to each period in proportion to the length of the period:

(a) insurance recoveries for loss of *live stock or trees;

See section 385‑130.

(b) amounts included in assessable income as a result of elections relating to the forced disposal of live stock;

See Subdivision 385‑E and section 385‑160.

(c) recoupment of mains electricity connection expenditure.

See items 1.16 and 2.5 in section 20‑30, which lists deductions for which recoupments are assessable under Subdivision 20‑A.

(4) An amount included in the company’s assessable income under section 385‑135 (Election to defer including profit on second wool clip) is attributed to the period when the wool would ordinarily have been shorn.

(5) An amount included in the company’s assessable income that is a *dividend under:

(a) section 65 (Payments to associated persons); or

(c) section 109 (Excessive payments to shareholders and associates);

of the Income Tax Assessment Act 1936 is attributed to the period when the amount was paid or credited, whichever occurred first.

(6) All other items of assessable income (except *full year amounts) are attributed to periods as if each period were an income year.

(6A) A *net capital gain is not attributed to a period.

Note: This is because Subdivision 165‑CB provides for how the company must work out its net capital gain for the income year.

(7) Full year amounts are amounts referred to in paragraphs (2)(a) and (b), so far as they are not reasonably attributable to a period, but do not include any part of a *capital gain that forms part of a *net capital gain. Full year amounts are brought in at a later stage of the process of calculating the company’s taxable income for the income year.

165‑65 How to calculate the company’s taxable income for the income year

(1) The company’s taxable income for the income year is calculated as follows.

(2) Add up the *notional taxable incomes (if any) worked out under section 165‑50 or 165‑75.

Note: A notional loss for a period is not taken into account, but counts towards the company’s tax loss for the income year.

(3) Add the *full year amounts referred to in subsection 165‑60(7) (if any) and any *net capital gain of the company for the income year.

(4) Subtract the company’s *full year deductions of these kinds:

(a) deductions for bad debts under section 8‑1 (about general deductions) or section 25‑35 (about bad debts);

(c) deductions, so far as they are allowable under Division 8 (which is about deductions) because Subdivision H (Period of deductibility of certain advance expenditure) of Division 3 of Part III of the Income Tax Assessment Act 1936 applies to the company in relation to the income year;

unless they exceed the total of the *notional taxable incomes and the *full year amounts. (If they equal or exceed that total, the company does not have a taxable income for the income year.)

(5) If an amount remains, subtract from it the company’s other *full year deductions, in the order shown in subsection 165‑55(5), unless they exceed the amount remaining. (If they equal or exceed that amount, the company does not have a taxable income for the income year.)

(6) If an amount remains, it is the company’s taxable income for the income year.

Working out the company’s tax loss

165‑70 How to calculate the company’s tax loss for the income year

(1) The company’s tax loss for the income year is calculated as follows.

(2) Total the *notional losses worked out under section 165‑50 or 165‑75.

(3) Add to the total in subsection (2) the amount (if any) by which the company’s *full year deductions of these kinds:

(a) deductions for bad debts under section 8‑1 (about general deductions) or section 25‑35 (about bad debts);

(c) deductions, so far as they are allowable under Division 8 (which is about deductions) because Subdivision H (Period of deductibility of certain advance expenditure) of Division 3 of Part III of the Income Tax Assessment Act 1936 applies to the company in relation to the income year;

exceed the total of:

(d) the *notional taxable incomes (if any); and

To work out the notional taxable income: see section 165‑50.

(e) the *full year amounts referred to in section 165‑60 (if any); and

(f) any *net capital gain of the company for the income year.

(4) If the company *derived exempt income, subtract its *net exempt income (worked out under section 36‑20).

(5) Any amount remaining is the company’s tax loss for the income year, which is called a loss year.

Note: The meanings of tax loss and loss year are modified by section 36‑55 for a corporate tax entity that has an amount of excess franking offsets.

To find out how much of the tax loss can be deducted in later income years: see Subdivision 165‑A.

To find out how to deduct it: see section 36‑17.

Special rules that apply if the company is in partnership

165‑75 How to calculate the company’s notional loss or notional taxable income for a period when the company was a partner

(1) This section applies if at any time during a period the company was a partner in one or more partnerships.

(2) The company has a *notional loss for the period if the total (the loss total) of:

(a) the deductions attributed to the period under section 165‑55; and

(b) the *company’s share of each *notional loss (if any) of a partnership for the period;

exceeds the total (the income total) of:

(c) the assessable income attributed to the period under section 165‑60; and

(d) the *company’s share of each *notional net income (if any) of a partnership for the period.

The notional loss is the amount of the excess.

Note: A notional loss is taken into account in working out the company’s tax loss under section 165‑70.

(3) On the other hand, if the income total exceeds the loss total, the company has a notional taxable income for the period, equal to the excess.

Note: A notional taxable income is taken into account in working out the company’s taxable income under section 165‑65.

(4) If the company has a *notional taxable income for all periods in the income year, this Subdivision has no further application, and the company’s taxable income for the income year is calculated in the usual way.

Note: The usual way of working out taxable income is set out in section 4‑15.

165‑80 How to calculate the company’s share of a partnership’s notional loss or notional net income for a period if both entities have the same income year

(1) This section applies if at any time during a period the company is a partner in a partnership that has an income year that starts and ends when the company’s income year starts and ends.

(2) The partnership’s notional loss or notional net income for the period is calculated in the same way as the *notional loss or *notional taxable income of a company.

(3) The company’s share is calculated by dividing:

• the company’s interest in the partnership’s net income or partnership loss of the income year;

by

• the amount of that net income or partnership loss;

and expressing the result as a percentage.

(4) However, if the partnership had neither a net income nor a partnership loss, the company’s share is a percentage that is fair and reasonable having regard to the extent of the company’s interest in the partnership.

165‑85 How to calculate the company’s share of a partnership’s notional loss or notional net income for a period if the entities have different income years

(1) This section applies if at any time during a period the company is a partner in a partnership that has an income year that starts and ends at a different time from when the company’s income year starts and ends.

(2) So much of the partnership’s net income or partnership loss of an income year as was *derived during the period is a notional net income or notional loss of the partnership for the period. (For the purposes of this subsection, the partnership’s net income or partnership loss is calculated without taking account of the partnership’s *full year deductions for that income year.)

Note: The partnership’s full year deductions are dealt with in section 165‑90.

(3) The company’s share is calculated by dividing:

• the company’s interest in the partnership’s net income or partnership loss of that income year;

by

• the amount of that net income or partnership loss;

and expressing the result as a percentage.

165‑90 Company’s full year deductions include a share of partnership’s full year deductions

(1) This section applies if at any time during the income year the company is a partner in a partnership that has one or more *full year deductions for the income year of the partnership that corresponds to the income year of the company.

(2) The partnership’s *full year deductions are treated as full year deductions of the company, but only to the extent of the *company’s share.

(3) If the partnership’s income year is the same as the company’s, the company’s share is calculated by dividing:

• the company’s interest in the partnership’s net income or partnership loss of the income year;

by

• the amount of that net income or partnership loss;

and expressing the result as a percentage.

(4) However, if the partnership had neither a net income nor a partnership loss, the company’s share is a percentage that is fair and reasonable having regard to the extent of the company’s interest in the partnership.

(5) If the partnership’s income year does not start and end at the same time as the company’s income year, the company’s share is a percentage that is fair and reasonable having regard to all relevant circumstances.

Subdivision 165‑CA—Applying net capital losses of earlier income years

Guide to Subdivision 165‑CA

165‑93 What this Subdivision is about

In working out its net capital gain for an income year, a company cannot apply a net capital loss for an earlier income year unless:

(a) it has the same owners and the same control from the start of the loss year to the end of the income year; or

(b) it satisfies the same business test by carrying on the same business, entering into no new kinds of transactions and conducting no new kinds of business.

Table of sections

Operative provisions

165‑96 When a company cannot apply a net capital loss

Operative provisions

165‑96 When a company cannot apply a net capital loss

(1) In working out its *net capital gain for the *current year, a company cannot apply a *net capital loss it has for an earlier income year if Subdivision 165‑A would prevent it from deducting the loss for the current year if:

(a) the loss were a *tax loss of the company for that earlier income year; and

(b) section 165‑20 (about deducting part of a tax loss) were disregarded.

Note 1: A company’s net capital gain for an income year is usually worked out under section 102‑5.

Note 2: Subdivision 165‑A deals with the deductibility of a company’s tax loss for an earlier income year if there has been a change in the ownership or control of the company in the period from the start of the loss year to the end of the income year.

Note 3: Subdivision 165‑F may affect the application of Subdivision 165‑A.

(2) If subsection (1) prevents the company from applying the *net capital loss, it can apply the part of the loss that it made during a part of that earlier income year, but only if, assuming that part of that income year had been treated as the whole of it, the company would have been entitled to apply the net capital loss.

Subdivision 165‑CB—Working out the net capital gain and the net capital loss for the income year of the change

Guide to Subdivision 165‑CB

165‑99 What this Subdivision is about

A company that has not had the same ownership and control during the income year, and has not satisfied the same business test, works out its net capital gain and net capital loss under this Subdivision.

Table of sections

When a company must work out its net capital gain and net capital loss under this Subdivision

165‑102 On a change of ownership, or of control of voting power, unless the company satisfies the same business test

Working out the company’s net capital gain and net capital loss

165‑105 First, divide the income year into periods

165‑108 Next, calculate the notional net capital gain or notional net capital loss for each period

165‑111 How to work out the company’s net capital gain

165‑114 How to work out the company’s net capital loss

When a company must work out its net capital gain and net capital loss under this Subdivision

165‑102 On a change of ownership, or of control of voting power, unless the company satisfies the same business test

A company must calculate its *net capital gain and *net capital loss for the income year under this Subdivision if:

(a) it must calculate its taxable income and *tax loss for the income year under Subdivision 165‑B; or

Note: Subdivision 165‑F may affect the application of Subdivision 165‑B.

(b) it would be required to calculate them under that Subdivision but for subsection 165‑50(3) (about cases where that Subdivision would make no difference to the taxable income).

Note: In the case of a widely held or eligible Division 166 company, Subdivision 166‑B modifies how this Subdivision applies, unless the company chooses otherwise.

Working out the company’s net capital gain and net capital loss

165‑105 First, divide the income year into periods

Divide the income year into periods according to section 165‑45 (which is about working out the company’s taxable income under Subdivision 165‑B).

165‑108 Next, calculate the notional net capital gain or notional net capital loss for each period

(1) The company has a notional net capital gain for a period if the total of the *capital gains it made during the period exceeds the total of the *capital losses it made during the period. The notional net capital gain is the amount of the excess.

(2) On the other hand, if the total of those losses exceeds the total of those gains, the company has a notional net capital loss for the period, equal to the excess.

(3) If the company has a *notional net capital loss for none of the periods in the income year, this Subdivision has no further application, and the company’s *net capital gain for the income year is calculated in the usual way.

The usual way of working out the net capital gain is set out in section 102‑5.

Trust’s capital gain attributed to company beneficiary

(4) If some or all (the attributable amount) of an amount included in the company’s assessable income for the income year under:

(a) section 97 (Beneficiary of a trust estate who is not under a legal disability) of the Income Tax Assessment Act 1936; or

(b) section 98A (Non‑resident beneficiaries assessable in respect of certain income) of that Act;

is attributable to a *capital gain that the trust made at a particular time during the period, this section applies to the attributable amount as if it were a *capital gain made by the company at that time.

165‑111 How to work out the company’s net capital gain

The company’s net capital gain for the income year is worked out in this way:

Working out the company’s net capital gain

Step 1. Add up the *notional net capital gains (if any) worked out under section 165‑108.

Note: A notional net capital loss for a period is not taken into account, but counts towards the company’s net capital loss for the income year.

Step 2. Add to the Step 1 amount so much of each amount included in the company’s assessable income for the income year under:

(a) section 97 (Beneficiary of a trust estate who is not under a legal disability) of the Income Tax Assessment Act 1936; or

(b) section 98A (Non‑resident beneficiaries assessable in respect of certain income) of that Act;

as is attributable to a *capital gain that the trust made outside the income year.

Note: This is relevant only if the trust has an income year that starts and ends at a different time from when the company’s income year starts and ends.

Step 3. If the Step 2 amount is more than zero, reduce it by applying any unapplied *net capital losses from previous income years. (If this reduces it to zero, the company has no net capital gain for the income year.)

Note: To apply net capital losses: see section 102‑15.

Step 4. If the Step 3 amount is more than zero, it is the company’s net capital gain.

Note : For exceptions and modifications to these rules: see section 102‑30.

165‑114 How to work out the company’s net capital loss

The company’s net capital loss for the income year is worked out in this way:

Working out the company’s net capital loss

Step 1. Add up the *notional net capital losses (if any) worked out under section 165‑108.

Step 2. If the Step 1 amount is more than zero, it is the company’s net capital loss.

Note: For exceptions and modifications to these rules: see section 102‑30.

Subdivision 165‑CC—Change of ownership or control of company that has an unrealised net loss

Guide to Subdivision 165‑CC

165‑115 What this Subdivision is about

If a change occurs in the ownership or control of a company that has an unrealised net loss, the company cannot, to the extent of the unrealised net loss, have capital losses taken into account, or deduct revenue losses, in respect of CGT events that happen to CGT assets that it owned at the time of the change, unless it satisfies the same business test.

165‑115AA Special rules to save compliance costs

(1) A company is exempt from these rules if, at the time of the change in ownership or control, it (together with certain related entities) has a net asset value of not more than $6,000,000 under the test in section 152‑15 (for small business CGT relief).

(2) In working out whether it has an unrealised net loss, a company can choose to work out the market value of each of its assets individually, or of all of its assets together.

(3) If a company works out the market value of each of its assets individually, it may choose to exclude every asset that it acquired for less than $10,000, in which case:

(a) unrealised losses and gains on the excluded assets will not be taken into account in calculating the company’s unrealised net loss; and

(b) losses on the excluded assets will be allowed without the company being subject to the same business test.

Table of sections

Operative provisions

165‑115A Application of Subdivision

165‑115B What happens when the company makes a capital loss or becomes entitled to a deduction in respect of a CGT asset after a changeover time

165‑115BAWhat happens when a CGT event happens after a changeover time to a CGT asset of the company that is trading stock

165‑115BBOrder of application of assets: residual unrealised net loss

165‑115C Changeover time—change in ownership of company

165‑115D Changeover time—change in control of company

165‑115E What is an unrealised net loss

165‑115F Notional gains and losses

Operative provisions

165‑115A Application of Subdivision

Application

(1) This Subdivision applies to a company if:

(a) a changeover time has occurred or occurs in relation to the company after the commencement time; and

(b) at the changeover time the company had an unrealised net loss (see section 165‑115E); and

(c) either of the following applies:

(i) the company makes a *capital loss, or apart from this Subdivision would be entitled to a deduction, in respect of a *CGT event that happens to a *CGT asset referred to in subsection (1A);

(ii) the company makes a *trading stock loss in respect of a CGT asset referred to in subsection (1A) that is an item of *trading stock; and

(d) the company would not, at the changeover time, satisfy the maximum net asset value test under section 152‑15.

CGT assets in respect of which Subdivision applies

(1A) The *CGT assets for the purposes of paragraph (1)(c) are:

(a) any CGT asset that the company owned at the changeover time; and

(b) any CGT asset that the company did not own at the changeover time but had owned at a previous time, where:

(i) a deferral event referred to in subsection 170‑255(1) happened before the changeover time; and

(ii) the deferral event involved the company as the originating company referred to in that subsection; and

(iii) the deferral event would have resulted in the company making a *capital loss, or becoming entitled to a deduction, in respect of the CGT asset except for section 170‑270; and

(iv) the company is not taken to have made a capital loss at or before the changeover time, or to have become entitled to a deduction at that time, under section 170‑275 in respect of the asset.

Company may choose to disregard CGT assets acquired for less than $10,000

(1B) A company may choose, for the purposes of the application of this Subdivision to it in respect of a particular changeover time, that every *CGT asset that has been acquired by it for less than $10,000 is to be disregarded.

However, the choice does not affect the application of the *global method of working out whether the company has an unrealised net loss (see subsection 165‑115E(2)).

Time for making choice

(1C) A choice under subsection (1B) must be made on or before:

(a) the day on which the company lodges its *income tax return for the income year in which the relevant changeover time occurred; or

(b) such later day as the Commissioner allows.

Trading stock loss

(1D) A company is taken to have made a trading stock loss in respect of an asset that is an item of *trading stock if, and only if:

(a) one of the following applies:

(i) the company *disposes of the item;

(ii) the item stops being trading stock (within the meaning of section 70‑80);

(iii) the item is revalued under Division 70; and

(b) if subparagraph (a)(i) or (ii) applies—the item’s *market value at the time when it is disposed of or stops being trading stock is less than:

(i) in respect of an item that has been valued under Division 70—its latest value under the Division; or

(ii) otherwise—its cost at that time; and

(c) if subparagraph (a)(iii) applies—the item’s value under the revaluation is less than:

(i) in respect of an item that has previously been valued under Division 70—its latest value under that Division before the revaluation; or

(ii) otherwise—its cost at the time of the revaluation.

The difference worked out under paragraph (b) or (c), as the case may be, constitutes the amount of the *trading stock loss.

Commencement time

(2) For the purposes of this Subdivision, the commencement time of a company is:

(a) if the company was in existence at 1 pm (by legal time in the Australian Capital Territory) on 11 November 1999—that time; or

(b) if the company came into existence after that time—the time when it came into existence.

Reference time

(2A) For the purposes of the application of this Subdivision to a company in relation to a particular time (the test time), the reference time is:

(a) if no changeover time occurred in respect of the company before the test time—the commencement time; or

(b) otherwise—the time immediately after the last changeover time that occurred in respect of the company before the test time.

Asset owned at more than one changeover time

(3) If:

(a) 2 or more changeover times have occurred or occur in relation to a company; and

(b) the company owned a particular asset at more than one of those changeover times;

this Subdivision applies to the company in respect of that asset only in relation to the later or latest of those changeover times.

Note: For changeover time see sections 165‑115C and 165‑115D.

165‑115B What happens when the company makes a capital loss or becomes entitled to a deduction in respect of a CGT asset after a changeover time

Where capital loss or deduction is equal to or less than residual unrealised net loss

(1) If the *capital loss or deduction referred to in subparagraph 165‑115A(1)(c)(i) is equal to or less than the company’s residual unrealised net loss at the time of the occurrence of the event that resulted in the capital loss or entitled the company to the deduction:

(a) the capital loss is taken to have been a *net capital loss; or

(b) the deduction is taken to have been a *tax loss;

of the company for the income year immediately before the income year in which the changeover time occurred.

Where capital loss or deduction is greater than residual unrealised net loss

(2) If the *capital loss or deduction referred to in subparagraph 165‑115A(1)(c)(i) is greater than the company’s residual unrealised net loss at the time of the occurrence of the event that resulted in the capital loss or entitled the company to the deduction:

(a) the part of the capital loss that is equal to the residual unrealised net loss is taken to have been a *net capital loss; or

(b) the part of the deduction that is equal to the residual unrealised net loss is taken to have been a *tax loss;

of the company for the income year immediately before the income year in which the changeover time occurred.

Company does not meet certain conditions in relation to net capital loss or tax loss

(3) The company is taken not to have met, at the changeover time, the conditions in subsections 165‑12(2), (3) and (4) in relation to the *net capital loss or the *tax loss. The changeover time is the test time for applying section 165‑13 to the company.

Need to meet same business test

(4) The effect of subsection (3) is that the company cannot apply the *net capital loss (see section 165‑10 as it applies because of section 165‑96), or deduct the *tax loss (see section 165‑10), unless it meets the condition in section 165‑13 (the same business test).

Consequences for net capital loss

(5) The *net capital loss cannot be applied against *capital gains made in an income year before the income year in which the company made the capital loss referred to in subparagraph 165‑115A(1)(c)(i).

Consequences for tax loss

(6) The *tax loss cannot be deducted from assessable income *derived in an income year before the income year in which the company would have been entitled to the deduction referred to in subparagraph 165‑115A(1)(c)(i).

Note: For changeover time see sections 165‑115C and 165‑115D.

165‑115BA What happens when a CGT event happens after a changeover time to a CGT asset of the company that is trading stock

Application

(1) This section applies to the company if, after the changeover time, the company makes a *trading stock loss in respect of an item of *trading stock as mentioned in subparagraph 165‑115A(1)(c)(ii).

Where trading stock loss is equal to or less than residual unrealised net loss

(2) If the *trading stock loss is equal to or less than the company’s residual unrealised net loss at the time of the occurrence of the trading stock loss, the amount of the trading stock loss is to be included in the company’s assessable income.

Where trading stock loss is greater than unrealised net loss

(3) If the *trading stock loss is greater than the company’s residual unrealised net loss at the time of the occurrence of the trading stock loss, the part of the trading stock loss that is equal to the residual unrealised net loss is to be included in the company’s assessable income.

No increase in assessable income if company satisfies the same business test

(4) Neither subsection (2) nor (3) applies to the company if the company meets the condition in section 165‑13 (the same business test).

Assumptions for purposes of same business test

(5) In determining whether the company meets the condition in section 165‑13, assume:

(a) that the *trading stock loss (if subsection (2) applies) or the part of the trading stock loss (if subsection (3) applies) is a *net capital loss of the company for the income year immediately before the income year in which the changeover time occurred; and

(b) that the company failed, at the changeover time, to meet the condition in subsections 165‑12(2), (3) and (4) in relation to the net capital loss referred to in paragraph (a); and

(c) that the changeover time is the test time; and

(d) that the same business test period is the income year in which the loss occurred.

165‑115BB Order of application of assets: residual unrealised net loss

Order in which assets are to be applied

(1) In applying subsection 165‑115B(2) or 165‑115BA(3) in respect of assets that the company owned at the changeover time:

(a) the company’s *capital losses are taken to have been made, the company is taken to have become entitled to deductions and the company is taken to have made *trading stock losses in the order in which the events that resulted in the capital losses, deductions or trading stock losses occurred; and

(b) if 2 or more such events occurred at the same time, they are taken to have occurred in such order as the company determines.

Residual unrealised net loss

(2) The company’s residual unrealised net loss, at the time of an event (the relevant event) that resulted in the company making a *capital loss, becoming entitled to a deduction or making a *trading stock loss, in respect of an asset, is the amount worked out using the following formula:

where:

previous capital losses, deductions or trading stock losses means the total of the following:

(a) capital losses that the company made, deductions to which the company became entitled, or *trading stock losses that the company made, as a result of events earlier than the relevant event in respect of assets that the company owned at the *changeover time;

(b) each reduction that section 715‑105 (as applying to the company as the *head company of a *consolidated group or *MEC group) makes in respect of such an asset because an entity ceased before the time of the relevant event to be a *subsidiary member of the group (but counting only the greater or greatest such reduction if 2 or more are made for the same asset);

or nil if there are none.

unrealised net loss means the company’s unrealised net loss at the last changeover time that occurred before the relevant event.

Note: For changeover time see sections 165‑115C and 165‑115D.

165‑115C Changeover time—change in ownership of company

(1) A time (the test time) is a changeover time in respect of a company if:

(a) persons who had *more than 50% of the voting power in the company at the reference time do not have more than 50% of that voting power immediately after the test time; or

(b) persons who had rights to *more than 50% of the company’s dividends at the reference time do not have rights to more than 50% of those dividends immediately after the test time; or

(c) persons who had rights to *more than 50% of the company’s capital distributions at the reference time do not have rights to more than 50% of those distributions immediately after the test time.

Note 1: See section 165‑150 to work out who had more than 50% of the voting power in the company.

Note 2: See section 165‑155 to work out who had rights to more than 50% of the company’s dividends.

Note 3: See section 165‑160 to work out who had rights to more than 50% of the company’s capital distributions.

Note 4: For reference time see subsection 165‑115A(2A).

Note 5: Division 167 has special rules for working out rights to voting power, dividends and capital distributions in a company whose shares do not all carry the same rights to those matters.

(2) To work out whether paragraph (1)(a), (b) or (c) applied at a particular time, apply the primary test unless subsection (3) requires the alternative test to be applied.

Note: For the primary test see subsections 165‑150(1), 165‑155(1) and 165‑160(1).

(3) Apply the alternative test if one or more other companies beneficially owned *shares or interests in shares in the company at any time during the period from the reference time to the *test time.

Note: For the alternative test see subsections 165‑150(2), 165‑155(2) and 165‑160(2).

(4) A *test time that would, apart from this subsection, be a changeover time in respect of the company because of the application of subsection (1) is taken not to be a changeover time if:

(a) that subsection would not have applied except for the operation of section 165‑165; and

(b) the company has information from which it would be reasonable to conclude that less than 50% of the company’s unrealised net loss at the test time has been reflected in deductions, capital losses, or reduced assessable income, that occurred, or could occur in future, because of the happening of any *CGT event in relation to any *direct equity interests or *indirect equity interests in the company during the period from the reference time to the test time.

(4A) If the company is:

(a) a *non‑profit company; or

(b) a *mutual affiliate company; or

(c) a *mutual insurance company;

during the whole of the period from the reference time to the *test time, the test time is taken not to be a *changeover time in respect of the company because of the application of paragraphs (1)(b) and (c).

(5) The happening of any *CGT event in relation to a *direct equity interest or *indirect equity interest in the company that results in the time of the happening of the event being a changeover time in respect of the company is taken, for the purposes of paragraph (4)(b), to have occurred during the period referred to in that paragraph.

165‑115D Changeover time—change in control of company

(1) A time (the test time) is also a changeover time in respect of a company if, at the test time:

(a) a person or persons who did not control, and were not able to control, the voting power in the company at the reference time began to control, or became able to control, that voting power immediately after the test time; and

(b) that person or those persons so began, or became able, to control that voting power for the purpose of:

(i) getting some benefit or advantage in relation to how this Act applies; or

(ii) getting such a benefit or advantage for someone else;

or for purposes including that purpose.

Note 1: A person can still control the voting power in a company that is in liquidation etc.: see section 165‑250.

Note 2: Subdivision 167‑B has special rules for working out voting power in a company whose shares do not all carry the same voting rights, or do not carry all of the voting rights in the company.

(2) In this section:

control of the voting power in a company means control of that voting power either directly, or indirectly through one or more interposed entities.

165‑115E What is an unrealised net loss

(1) The question whether a company has an unrealised net loss at a particular time (the relevant time) is worked out in this way (the individual asset method), unless the company chooses to work it out using the *global method (set out in subsection (2)).

Method statement

Step 1. Work out under section 165‑115F in respect of each *CGT asset that the company owned at the relevant time any notional capital gain or notional revenue gain or any notional capital loss or notional revenue loss that the company has at that time in respect of the asset.

The sum of the notional capital gains is the company’s unrealised capital gain at the relevant time.

The sum of the notional capital losses is the company’s unrealised capital loss at the relevant time.

The sum of the notional revenue gains is the company’s unrealised revenue gain at the relevant time.

The sum of the notional revenue losses is the company’s unrealised revenue loss at the relevant time.

Step 2. Add up the unrealised capital gain and the unrealised revenue gain at the relevant time. The total is the unrealised gross gain at that time.

Step 3. Add up the unrealised capital loss and the unrealised revenue loss at the relevant time. The total is the unrealised gross loss at that time.

Step 4. If the unrealised gross loss at the relevant time exceeds the unrealised gross gain at that time, the excess is the company’s preliminary unrealised net loss at that time.

Step 5. Add up the company’s preliminary unrealised net loss and any *capital loss, deduction or share of a deduction disregarded under section 170‑270 in relation to an asset referred to in paragraph 165‑115A(1A)(b). The total is the company’s unrealised net loss at the relevant time.

(2) The global method of working out whether the company has an unrealised net loss at the relevant time is as follows:

Method statement

Step 1. Work out the total *market value of all *CGT assets that the company owned at the relevant time (including those it *acquired for less than $10,000), using a valuation method that would generally be regarded as appropriate in the circumstances.

Step 2. Work out the total of the *cost bases of those *CGT assets at the relevant time.

Note: If a CGT asset that the company owned at the relevant time was also trading stock or a revenue asset at that time, see subsection (3) of this section.

Step 3. If the step 2 amount exceeds the step 1 amount, the excess is the company’s preliminary unrealised net loss at the relevant time.

Step 4. Add up the company’s preliminary unrealised net loss and any *capital loss, deduction or share of a deduction disregarded under section 170‑270 in relation to an asset referred to in paragraph 165‑115A(1A)(b). The total is the company’s unrealised net loss at the relevant time.

(3) If:

(a) a *CGT asset that the company owned at the relevant time was also *trading stock or a *revenue asset at that time; and

(b) the asset’s *cost base at the relevant time is less than the amount that would be compared under section 165‑115F with the asset’s *market value in working out a notional revenue gain or notional revenue loss that the company has at the relevant time in respect of the asset;

then, for the purposes of step 2 of the method statement in subsection (2) of this section, the amount that would be so compared is to be taken into account instead of that cost base.

(4) A choice to use the *global method must be made on or before:

(a) the day on which the company lodges its *income tax return for the income year in which the relevant time occurred; or

(b) such later day as the Commissioner allows.

165‑115F Notional gains and losses

(1) This section applies for the purpose of calculating whether a company has at a particular time (the relevant time) a notional capital gain, a notional capital loss, a notional revenue gain or a notional revenue loss in respect of a *CGT asset that it owned at that time.

(2) The calculation is to be made on the assumption that the company disposed of the asset at its *market value at the relevant time.

(3) In relation to an asset other than an item of *trading stock:

(a) if the company would make a *capital gain in respect of the disposal of the asset—the company has at the relevant time in respect of the asset a notional capital gain equal to the amount of the capital gain; or

(b) if an amount (other than a capital gain) would be included in the company’s assessable income in respect of the disposal of the asset—the company has at the relevant time in respect of the asset a notional revenue gain equal to the amount so included; or

(c) if the company would make a *capital loss in respect of the disposal of the asset—the company has at the relevant time in respect of the asset a notional capital loss equal to the amount of the capital loss; or

(d) if the company would be entitled to a deduction in respect of the disposal of the asset—the company has at the relevant time in respect of the asset a notional revenue loss equal to the amount of the deduction.

(4) In relation to an asset that is an item of *trading stock:

(a) if the item’s *market value at the relevant time exceeds:

(i) in respect of an item that has been valued under Division 70—the item’s latest valuation under that Division; or

(ii) otherwise—the *cost of the item at the relevant time;

the company has at the relevant time in respect of the article a notional revenue gain equal to the excess; or

(b) if the item’s market value at the relevant time is less than:

(i) in respect of an item that has been valued under Division 70—the item’s latest valuation under that Division; or

(ii) otherwise—the *cost of the item at the relevant time;

the company has at the relevant time in respect of the article a notional revenue loss equal to the difference.

(5) A company may choose that this section is to apply to the company at the relevant time in respect of an asset to which subsection (6) applied at that time as if references to the *market value of the asset were references to its *written down value.

(6) This subsection applies to an asset at the relevant time if:

(a) the asset is a *depreciating asset (not a building or structure) for whose decline in value the company has deducted or can deduct an amount; and

(b) the expenditure incurred by the company to *acquire the asset was less than $1,000,000 (the expenditure can include the giving of property: see section 103‑5); and

(c) it would be reasonable for the company to conclude that the *market value of the asset at that time was not less than 80% of its *written down value at that time.

Subdivision 165‑CD—Reductions after alterations in ownership or control of loss company

Guide to Subdivision 165‑CD

165‑115GA What this Subdivision is about

This Subdivision prevents multiple recognition of a company’s losses when significant equity and debt interests that entities (not individuals) have in the company are realised.

165‑115GB When adjustments must be made

(1) The operation of this Subdivision is triggered at an alteration time, which is when:

(a) an alteration takes place in the ownership or control of the company; or

(b) a liquidator or administrator of the company declares that shares or financial instruments are worthless (CGT event G3).

(2) An alteration time is the trigger for making reductions and other adjustments to the reduced cost base of significant equity and debt interests in the company that are owned by an entity (not an individual) that, alone or with its associates, has a controlling stake in the company and either:

(a) has a *direct equity interest or *indirect equity interest of at least 10% in the company; or

(b) is owed a debt of at least $10,000 by the company or by another entity that has a significant equity or debt interest in the company.

Deductions that relate to such interests held as trading stock or otherwise on revenue account are also reduced.

(3) Adjustments may also be made when such an entity’s interests in the company are partly realised within 12 months before an alteration time or if, under an arrangement, such interests are realised partly within that period or at the alteration time and partly at an earlier time.

(4) However, entities in which there are no interests in respect of which the company’s losses have been, or can be, duplicated are not affected by this Subdivision.

165‑115GC How adjustments are calculated

(1) Adjustments are based on the overall loss of the company. This comprises its realised losses and unrealised losses on CGT assets.

(2) Special rules, directed at saving compliance costs, apply to determine whether unrealised losses have to be counted at an alteration time and, if so, how to work them out.

(3) The company may not have to calculate its unrealised losses if the alteration time is not also a changeover time for the purposes of Subdivision 165‑CC (about change of ownership or control of a company that has an unrealised net loss), and the company has no realised losses.

(4) The company does not have to count unrealised losses at an alteration time if (together with certain related entities) it has a net asset value of not more than $6,000,000 under the test in section 152‑15 (for small business CGT relief).

(5) In working out its unrealised losses on CGT assets, the company can choose to work out the *market value of each of its assets individually, or of all of its assets together.