Export Market Development Grants Act 1997

No. 57, 1997

An Act relating to the grant of financial assistance to provide incentives for the development of export markets

[Assented to 30 April 1997]

The Parliament of Australia enacts:

Part 1—Preliminary

1 Short title

This Act may be cited as the Export Market Development Grants Act 1997.

2 Commencement

This Act commences on 1 July 1997.

3 Object of Act

The object of this Act is to bring benefits to Australia by encouraging the creation, development and expansion of foreign markets for Australian goods, services, intellectual property and know-how. It does so by providing for an assistance scheme under which small and medium Australian exporters committed to and capable of seeking out and developing export business are repaid part of their expenses incurred in promoting those products.

Part 2—Entitlement to grant

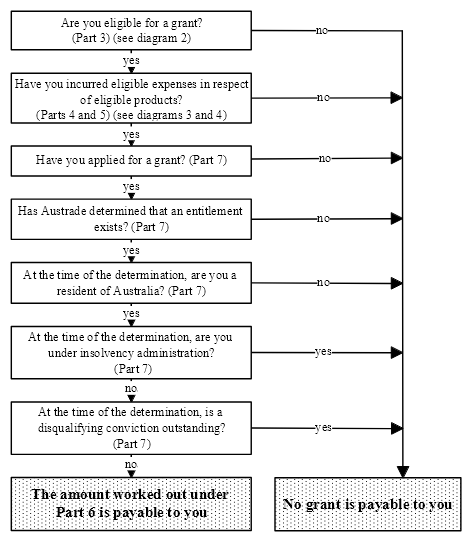

4 Entitlement to grant

Subject to this Act, a person that:

(a) is eligible under Part 3 for a grant in respect of a grant year; and

(b) has incurred eligible expenses in that grant year in relation to eligible products; and

(c) has applied for a grant in accordance with Part 7;

is entitled to a grant in respect of that grant year in the amount worked out under Part 6.

Note: For eligible expenses, grant year, eligible products and grant see section 107.

Part 3—Persons eligible for a grant

Division 1—General

5 Object of Part

(1) This Part defines who is eligible for a grant.

(2) The underlying principle is that only small or medium Australian businesses that:

(a) are developing export markets for eligible products; and

(b) have a prospect of success in their export enterprise;

should be eligible for a grant.

Note: For grant and eligible products see section 107.

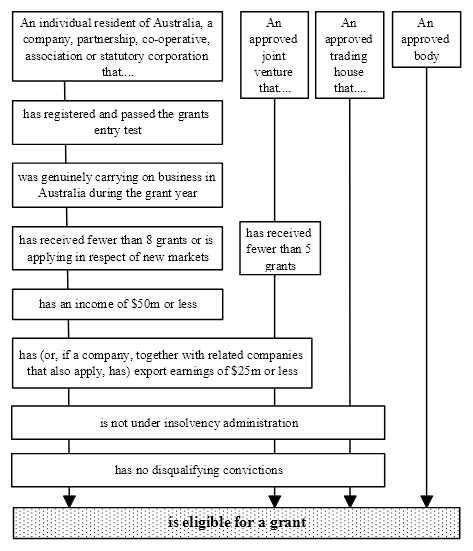

6 Who is eligible for a grant?

(1) Each of the following:

(a) an individual who is a resident of Australia;

(b) a body incorporated under the Corporations Law;

(c) an association or co-operative incorporated under an Australian law;

(d) a partnership regulated by an Australian law;

(e) a joint venture approved by Austrade under section 89;

(f) a trading house approved by Austrade under section 89;

(g) a body corporate established for a public purpose by or under an Australian law;

is eligible for a grant in respect of a grant year if it satisfies the conditions applicable to it under section 7.

(2) A body approved by Austrade under section 89 is eligible for a grant in respect of a grant year.

Note: For Austrade, Australian law, grant and grant year see section 107. For resident of Australia see section 114.

7 General rules for eligibility

Person other than approved joint venture, approved trading house or trustee

(1) A person referred to in subsection 6(1) (other than an approved joint venture, an approved trading house or a person acting in the capacity of trustee of a trust estate) is eligible for a grant in respect of a grant year if the following conditions are satisfied:

(a) the person was, in Austrade’s opinion, genuinely carrying on business in Australia during the grant year;

(b) in the case of an individual, he or she was a resident of Australia during the time in the grant year when he or she was, in Austrade’s opinion, carrying on business in Australia;

(c) subject to section 8, the person is not a grantee in respect of 8 or more previous grant years;

(d) the person’s income for the grant year is not more than $50,000,000;

(e) the person’s export earnings for the grant year (together with, in the case of a body corporate, the export earnings for the grant year of each related company (if any) that applies for a grant in respect of the grant year), are not more than $25,000,000;

(f) the person is not, when the person applies for the grant, disqualified under section 13 from receiving a grant because the person, or an associate of the person, is under insolvency administration;

(g) there are no disqualifying convictions outstanding against the person under section 17 when the person applies for the grant;

(h) if Division 5 applies to the person—the person has been registered under section 19 and has passed the grants entry test.

Note: For person, grant, grant year, Austrade, resident of Australia, grantee, income, export earnings, related company, associate, under insolvency administration and grants entry test see section 107.

Approved joint venture

(2) An approved joint venture is eligible for a grant in respect of a grant year if it satisfies the following conditions:

(a) it is not a grantee in respect of 5 or more previous grant years;

(b) its export earnings for the grant year are not more than $25,000,000;

(c) no associate of the joint venture is under insolvency administration when the joint venture applies for the grant;

(d) there are no disqualifying convictions outstanding against the joint venture under section 17 when the joint venture applies for the grant.

Note: For approved joint venture, grant, grant year, Austrade, grantee, export earnings, associate and under insolvency administration see section 107.

Approved trading house

(3) An approved trading house is eligible for a grant in respect of a grant year if:

(a) neither the trading house nor any associate of the trading house is under insolvency administration when the trading house applies for the grant; and

(b) there are no disqualifying convictions outstanding against the trading house under section 17 when the trading house applies for the grant.

Note: For approved trading house, grant and grant year see section 107.

Trustees

(4) A person acting as trustee of a trust estate is eligible for a grant in respect of a grant year if the following conditions are satisfied:

(a) the person provides to Austrade, on request, the following information:

(i) a declaration of beneficial and ultimate control of the trust estate, including by trustees; and

(ii) a declaration of the identities of the beneficiaries of the trust estate, including in the case of individuals, their countries of residence and, in the case of beneficiaries which are not individuals, their countries of incorporation or registration, as the case may be; and

(iii) details of any relationships with other entities; and

(iv) the percentage distribution of income within the trust; and

(v) any changes during the grant year in relation to information provided under subparagraphs (i), (ii), (iii) or (iv);

(b) subject to section 8, the person is not a grantee in respect of 8 or more previous years;

(c) the income of the person from the trust business during the grant year is not more than $50,000,000;

(d) the export earnings of the person during the grant year are not more than $25,000,000;

Note: Section 10 provides that only earnings from the trust business are to be taken into account.

(e) neither the person, nor (in the case of a company) any of its directors, is under insolvency administration when the person applies for the grant;

(f) none of the beneficiaries of the trust estate, nor (in the case of a beneficiary other than an individual) any associate of the beneficiary, is under insolvency administration when the person applies for the grant;

(g) there are no disqualifying convictions outstanding against either the person or any beneficiary of the trust estate under section 17 when the person applies for the grant;

(h) if Division 5 applies to the person—the person (in the capacity of trustee for the trust estate) has been registered under section 19 and has passed the grants entry test.

Note: For person, grant year, Austrade, grantee, income, export earnings, associate under insolvency administration and grants entry test see section 107.

8 Grantees in respect of previous grant years

(1) In determining for the purposes of paragraph 7(1)(c), (2)(a) or (4)(b) whether a person is a grantee in respect of a grant year, any of the following grants paid to the person is to be disregarded:

(a) a grant of $3,500 or less in respect of a claim period before the grant year that started on 20 May 1985;

(b) in the case of a person that was, for the purposes of the repealed Act, a body specified in Schedule 7 to the Export Market Development Grants Regulations made under that Act—any grant to that person in respect of a claim period before the grant year that started on 20 May 1985;

(c) a grant:

(i) in respect of a claim period before the grant year that started on 1 July 1990; and

(ii) that was solely in respect of eligible expenditure (within the meaning of the repealed Act) for eligible tourism services (within the meaning of that Act);

(d) in the case of a person that has applied for a grant in the capacity of trustee of a trust estate—any grant paid to the person otherwise than in that capacity;

(e) in the case of a person that has applied for a grant in the person’s own right—any grant paid to the person in the person’s capacity as trustee of a trust estate.

Note: For grantee and repealed Act see section 107.

(2) Paragraph 7(1)(c) does not apply to an applicant if the applicant is applying for a grant only in respect of eligible expenses that were incurred for eligible promotional activities carried out to further approved promotional purposes in a new market for the person.

Note: For eligible expenses, eligible promotional activity and approved promotional purpose see section 107. For new market see section 113.

(3) In subsection (1):

claim period has the same meaning as in the repealed Act.

grant includes a grant under the repealed Act.

Division 2—Export earnings

9 Object of Division

This Division explains the meaning of export earnings.

10 Export earnings—general

(1) Subject to subsections (3), (5) and (6) and section 12, the export earnings of a person (other than an approved joint venture) for a grant year are worked out by ascertaining from the following table, and adding up, the relevant earnings of the person for the eligible products referred to in column 2 of the table.

Note: For person, approved joint venture, grant year and eligible product see section 107.

Export earnings |

Column 1

Item | Column 2

Eligible products | Column 3

Relevant earnings |

1 | eligible goods: (a) sold at any time in Australia by the person; and (b) exported by the person during the grant year | so much of the amount or value of the consideration received, or receivable, for the sale and export of the goods as is attributable to the free on board value of the goods |

2 | eligible goods: (a) exported by the person at any time; and (b) sold outside Australia by the person during the grant year | the amount or value of the consideration that would be, under item 1, relevant earnings for those goods if the goods had been sold in Australia |

3 | an eligible external service supplied at any time by the person | the amount or value of the consideration received during the year for the supply of that service less so much of the consideration as is, in Austrade’s opinion, paid, or payable, outside Australia in relation to that service |

4 | an eligible internal service supplied at any time by the person | the amount or value of the consideration received during the year for the supply of that service |

5 | an eligible tourism service (indirect tourism service) supplied by the person: (a) to another person that is a resident of Australia (inbound tour operator); but (b) for supply by the inbound tour operator, in the course of trade, to a person that is not a resident of Australia | 20% of the amount or value of the consideration received during the year for the supply of the service to the inbound tourist operator |

6 | if the person is an inbound tour operator—an indirect tourism service supplied at any time by the person to a person that is not a resident of Australia | 80% of the amount or value of the consideration received during the grant year for the supply of that service |

7 | an eligible tourism service (other than an indirect tourism service) supplied at any time by the person to a person that is not a resident of Australia | the amount or value of the consideration received during the year for the supply of that service |

8 | eligible intellectual property or know‑how disposed of at any time by the person | the amount or value of the consideration received during the year for that disposal |

Note: For eligible goods, export, supply, Australia, Austrade, eligible external service, eligible internal service, eligible tourism service, disposal, eligible intellectual property and eligible know-how see section 107. See also sections 109, 110 and 111.

(2) For the purposes of subsection (1):

(a) the date of export of goods exported under a bill of lading or an air waybill is the earlier of:

(i) the date shown on the bill of lading or air waybill; and

(ii) the date on which the goods are received for shipment at the port or airport of export; and

(b) the date of export of goods sold as stores for use on ships or aircraft leaving Australia is the date of the sale; and

(c) the date of export of goods (for example, ships or aircraft) that are taken out of Australia under their own power for the purpose of being exported is the date on which the goods leave Australia; and

(d) the date of export of any other goods is the date on which they are received for shipment at the port or airport of export.

(3) Any consideration for the sale, supply or disposal of an eligible product in the following circumstances is to be disregarded in working out the export earnings of the person:

(a) a sale, supply or disposal of an eligible product in the course of trade with New Zealand;

(b) a sale, supply or disposal of an eligible product in the course of trade with a foreign country that has been declared by the Minister, in writing, to be subject to trade sanctions;

(c) if the person is a member of an approved joint venture—a sale, supply or disposal of an eligible product that relates directly to the approved activity, project or purpose of the joint venture.

Note: For eligible product, approved joint venture and approved activity, project or purpose see section 107. For foreign country see section 22 of the Acts Interpretation Act 1901.

(4) A declaration under paragraph (3)(b) is a disallowable instrument for the purposes of section 46A of the Acts Interpretation Act 1901.

(5) In working out the export earnings of a person that has applied for a grant in the capacity of trustee of a trust estate, disregard any earnings of the person that are not derived from the business carried on for the purposes of the trust estate.

(6) In working out the export earnings of a person that:

(a) has applied for a grant in the person’s own right; but

(b) is also a trustee, or a beneficiary, of a trust estate;

disregard any earnings of the person from the business carried on for the purposes of the trust estate.

11 Export earnings—approved joint venture

Subject to section 12, the export earnings of an approved joint venture for a grant year are the sum of the export earnings of all members of the joint venture whose income for the grant year is not more than $50,000,000, excluding any export earnings of a member that:

(a) are not in respect of the approved activity, project or purpose of the joint venture; or

(b) were earned at a time during the grant year when the member was not a resident of Australia.

Note: For approved joint venture, grant year, income and approved activity, project or purpose see section 107. For resident of Australia see section 114.

12 Export earnings—adjustments by Austrade

If Austrade adjusts under section 96 the amount that, apart from this section, would be (under section 10 or 11, as the case may be) the export earnings of a person for a grant year, that amount as so adjusted is taken to be the person’s export earnings for the grant year.

Division 3—Insolvency administration

13 Persons disqualified from receiving a grant

For the purposes of paragraph 7(1)(f), a person specified in column 2 of an item in the following table is disqualified from receiving a grant if the circumstances specified in column 3 of that item apply.

Persons disqualified from receiving a grant |

Column 1

Item | Column 2

Person | Column 3

Circumstance bringing disqualification |

1 | individual | the individual is under insolvency administration |

2 | body corporate other than a body referred to in paragraph 6(1)(g) | the body corporate or an associate of the body corporate is under insolvency administration |

3 | partnership or body corporate referred to in paragraph 6(1)(g) | an associate of the partnership or of the body corporate is under insolvency administration |

Note: For associate see section 107.

14 When is an individual under insolvency administration?

An individual is under insolvency administration only if:

(a) the individual is in any of the following situations under the Bankruptcy Act 1966:

(i) the individual is a bankrupt in respect of a bankruptcy from which he or she has not been discharged;

(ii) property of the individual is subject to control under section 50 or Division 2 of Part X of that Act;

(iii) the individual has, in the previous 3 years, executed a deed of assignment or deed of arrangement under Part X of that Act;

(iv) creditors of the individual have, in the previous 3 years, accepted a composition under Part X of that Act; or

(b) the individual is in a situation of a kind referred to in paragraph (a) under the law of an external Territory or a foreign country.

Note: For external Territory and foreign country see sections 17 and 22 respectively of the Acts Interpretation Act 1901.

15 When is a body corporate under insolvency administration?

(1) Subject to subsection (2), a body corporate is under insolvency administration only if:

(a) it is in any of the following situations under the Corporations Law:

(i) the body corporate is being wound up;

(ii) there is a receiver, receiver and manager, or other controller, of property of the body corporate who has functions or powers in connection with managing the body corporate;

(iii) the body corporate is under administration or official management;

(iv) the body corporate has executed a deed of company arrangement that has not yet terminated;

(v) the body corporate has entered into a compromise or arrangement with another person and the administration of the compromise or arrangement has not been concluded; or

(b) the body corporate is in a situation of a kind referred to in paragraph (a) under the law of an external Territory or a foreign country.

Note: For external Territory and foreign country see sections 17 and 22 respectively of the Acts Interpretation Act 1901.

(2) Despite subsection (1), a body corporate that, apart from this subsection, would be under insolvency administration is taken not to be under insolvency administration if there is in force a certificate given by the person administering the body corporate stating that the body corporate is able to pay all its debts as and when they become due and payable.

Note: For person administering the body corporate see subsection (3).

(3) In subsection (2):

person administering a body corporate means whichever of the following has been appointed in relation to the body corporate:

(a) the liquidator or provisional liquidator of the body corporate;

(b) the receiver, receiver and manager, or other controller, of property of the body corporate;

(c) the administrator, or the official manager, of the body corporate;

(d) the administrator of the deed of company arrangement executed by the body corporate;

(e) the administrator of any compromise or arrangement into which the body corporate has entered;

(f) a person exercising, under the law of an external Territory or a foreign country, the same functions and the same powers as a person referred to in one of paragraphs (a) to (e).

Division 4—Outstanding disqualifying convictions

16 Disqualifying convictions

(1) For the purposes of this Act, a disqualifying conviction is:

(a) in relation to an individual—a conviction of the individual for a relevant offence; or

(b) in relation to a body corporate—a conviction of the body corporate or of an associate of the body corporate for a relevant offence; or

(c) in relation to a partnership or an approved joint venture—a conviction of an associate of the partnership or of the joint venture for a relevant offence.

Note: For associate see section 107.

(2) In this section:

relevant offence means:

(a) an offence that under subsection 229(3) of the Corporations Law disqualifies a person from managing a corporation; or

(b) an offence against section 29A, 29B, 29C or 29D of the Crimes Act 1914 that relates to an application for a grant; or

(c) an offence against section 39 of the repealed Act; or

(d) an offence under:

(i) section 5, 6, 7 or 7A or subsection 86(1) of the Crimes Act 1914; or

(ii) a provision of a law of a State or Territory that corresponds to any of those provisions;

that relates to an offence referred to in paragraph (a), (b) or (c).

Note: For repealed Act see section 107.

17 When is a disqualifying conviction outstanding?

A disqualifying conviction in respect of a person remains outstanding against the person for the period starting on the day on which the conviction was recorded and ending:

(a) if the conviction was for a term of imprisonment—5 years after the individual convicted was released from prison; or

(b) in any other case—5 years after the day on which the conviction was recorded.

Division 5—Registration and grants entry test

18 Persons affected by Division

(1) Subject to subsections (2) and (3), this Division applies to a person (other than an approved body, approved joint venture or approved trading house) that intends to apply for a grant in respect of a grant year unless:

(a) the person is a grantee in respect of any previous grant year; or

(b) the person’s application for a grant in respect of the immediately preceding grant year is pending.

Note: For person and grantee see section 107.

(2) If the person intends to apply for a grant in the capacity of trustee of a trust estate, then, for the purposes of subsection (1), disregard:

(a) any grant previously paid or payable to the person; and

(b) any application for a grant made by the person;

otherwise than in that capacity.

(3) If the person intends to apply for a grant in the person’s own right, then, for the purposes of subsection (1), disregard:

(a) any grant previously paid or payable to the person; and

(b) any application for a grant made by the person;

in the capacity of trustee of a trust estate.

19 Registration

(1) The person must, before the end of the grant year, apply to Austrade to be registered for the purposes of this Act.

(2) The application must be in a form, and must be made in a manner, approved by Austrade.

(3) The application is taken not to have been made until it has been received by:

(a) Austrade; or

(b) a person appointed by Austrade to receive applications under this section.

(4) Austrade must:

(a) register the person; and

(b) as soon as practicable, notify the person, in writing, of the registration.

20 Taking of grants entry test

(1) A person that:

(a) has been registered under section 19; and

(b) has not passed the grants entry test under the repealed Act;

must take a test under this section. The test is to be taken at such time as Austrade considers to be appropriate to apply the test.

Note: For repealed Act see section 107.

(2) The purpose of the test is to find out whether the export enterprise in relation to which the person is seeking a grant has a prospect of success.

(3) Austrade is to decide whether the person has passed the test.

(4) If a person has not passed the test, Austrade must tell the person in writing which requirement of the test the person has not satisfied.

21 Requirements of grants entry test

(1) Austrade may determine in writing the requirements that a person must satisfy to pass the grants entry test.

(2) The determination may require the person to supply particular information from:

(a) existing documents to be given to Austrade; or

(b) documents to be prepared and given to Austrade.

(3) A determination under subsection (1) is a disallowable instrument for the purposes of section 46A of the Acts Interpretation Act 1901.

22 Austrade may request information relevant to grants entry test

(1) Austrade may, by written notice given to a person that has taken the grants entry test, request the person to give to Austrade, within the period and in the manner specified in the notice, information about any matter specified in the notice that Austrade requires to decide whether the person has passed the test.

(2) The period specified in the notice must not be less than 28 days.

(3) Austrade may refrain from deciding whether the person has passed the test, if the person does not give to Austrade the information requested.

(4) This section does not, by implication, limit subsection 72(1).

Part 4—Eligible products

23 Object of Part

(1) This Part sets out the conditions to be satisfied in deciding if a particular product (whether goods, services, intellectual property or know‑how) is an eligible product.

(2) The underlying principle is that a product should be eligible only if it is substantially of Australian origin.

24 Eligible goods

(1) Subject to subsection (3), goods made in Australia are eligible goods if they meet the 50% Australian content rule, that is, at least 50% of the free on board value of the goods is attributable to:

(a) components that were manufactured or produced in Australia; and

(b) the cost of labour performed on the goods in Australia; and

(c) the overheads incurred in Australia in connection with the making of the goods; and

(d) any mark‑up included in the free on board value of the goods.

(2) Subject to subsection (3), goods made outside Australia are eligible goods if they meet the 75% Australian content rule, that is, at least 75% of the value of the components used in the making of the goods is attributable to goods that meet the 50% Australian content rule.

(3) Despite subsections (1) and (2):

(a) particular goods made in Australia that meet the 50% Australian content rule; and

(b) particular goods made outside Australia that meet the 75% Australian content rule;

are not eligible goods if Austrade has determined, in writing, having regard to all the facts available to it, that the Australian input in those goods is not sufficient to ensure that Australia will derive a significant net benefit from their export.

(4) In addition:

(a) particular goods made in Australia that do not meet the 50% Australian content rule; and

(b) particular goods made outside Australia that do not meet the 75% Australian content rule;

are eligible goods if Austrade has determined, in writing, having regard to all the facts available to it, that the Australian input in those goods is sufficient to ensure that Australia will derive a significant net benefit from their export.

Note: For goods made in Australia and goods made outside Australia see section 107.

25 Eligible services

(1) Subject to subsection (4), an internal service is an eligible internal service if the service is supplied in Australia to a person that is not a resident of Australia.

Note: For internal service see section 107. For resident of Australia see section 114.

(2) Subject to subsection (4), a tourism service is an eligible tourism service if:

(a) the service is supplied in Australia to a person that is not a resident of Australia; or

(b) the service is supplied in Australia:

(i) to a person that is a resident of Australia; but

(ii) for supply by that person, in the course of trade, to a person that is not a resident of Australia.

Note: For tourism service see section 107. For resident of Australia see section 114.

(3) Subject to subsection (4), an external service is an eligible external service if the service is supplied outside Australia to a person that is not a resident of Australia.

Note: For external service see section 107. For resident of Australia see section 114.

(4) Despite subsection (1), (2) or (3) (as the case requires):

(a) a particular internal service; or

(b) a particular tourism service; or

(c) a particular external service;

that, apart from this subsection, would be an eligible internal service, an eligible tourism service or an eligible external service (as the case may be), is not such a service if Austrade determines, in writing, having regard to all the facts available to it, that the Australian input in the service is not sufficient to ensure that Australia will derive a significant net benefit from the supply of the service.

26 Eligible intellectual property

Intellectual property is eligible intellectual property if Austrade is satisfied:

(a) in the case of rights relating to a trade mark—that the trade mark:

(i) was first used in Australia; or

(ii) has increased in significance or value because of its use in Australia; or

(b) in the case of rights relating to any other thing—that the thing resulted to a substantial extent from research or work done in Australia.

Note: For intellectual property see section 107.

27 Eligible know‑how

(1) Know‑how is eligible know‑how if Austrade is satisfied that it resulted to a substantial extent from research or work done in Australia.

(2) In subsection (1):

know‑how means private knowledge, information or expertise relating to commercial or industrial operations that:

(a) is of commercial value; and

(b) is imparted for the purpose of enabling the recipient to carry out a particular activity.

Part 5—Eligible expenses

Division 1—General

28 Object of Part

(1) This Part defines what are the eligible expenses of an applicant for a grant.

(2) The underlying principle is that only expenses relating to specific promotional activities genuinely incurred by applicants for the purpose of marketing eligible products in foreign countries should qualify.

29 Eligible expenses—general

Subject to section 30, expenses incurred by an applicant for a grant in respect of a grant year are eligible expenses if the following conditions are satisfied:

(a) the expenses are, under section 33, claimable expenses in respect of an eligible promotional activity;

(b) if the applicant is an approved trading house or an approved joint venture—the expenses are related to the approved activity, project or purpose of the trading house or of the joint venture (as the case may be);

(c) the expenses were incurred (within the meaning of Division 3) by the applicant:

(i) if the applicant is not a grantee in respect of any previous grant year—during the grant year or the immediately preceding year; or

(ii) in any other case—during the grant year;

(d) the expenses, together with other expenses of the applicant that satisfy paragraphs (a) to (c), add up to $20,000 or more.

Note: For grant, grant year and grantee see section 107.

30 Eligible expenses—adjustments by Austrade

If Austrade adjusts under section 96 the amount that, apart from this section, would be (under section 29) the eligible expenses of an applicant for the grant year, that amount as so adjusted is taken to be the applicant’s eligible expenses for the grant year.

Division 2—Claimable expenses in respect of eligible promotional activities

Subdivision 1—General

31 Object of Division

This Division explains:

(a) what is an eligible promotional activity; and

(b) what are claimable expenses in respect of such an activity.

32 Meaning of agent

In this Division, a reference to an agent of an applicant does not include a representative of the applicant referred to in item 1 of the table in section 33.

Subdivision 2—Eligible promotional activity and claimable expenses defined

33 Claimable expenses in respect of eligible promotional activities

(1) The activity specified in column 2 of an item in the following table is an eligible promotional activity in relation to an applicant.

(2) The expenses specified in column 3 of an item in the following table, to the extent to which they are not excluded expenses under Subdivision 4, are claimable expenses of the applicant in respect of the activity specified in column 2 of that item.

Claimable expenses in respect of eligible promotional activities |

Column 1 Item | Column 2 Activity | Column 3 Expenses |

1 | maintaining an overseas representative on a long term basis in a foreign country to the extent to which the representative is maintained for an approved promotional purpose | so much of the expenses incurred by the applicant in a grant year in: (a) maintaining the representative; and (b) meeting the expenses incurred by the representative in soliciting business for the applicant; that, together with similar expenses (if any) incurred in respect of other representatives during the grant year, does not exceed $200,000 |

2 | any visit (marketing visit) made by the applicant or its agent to any place in or outside Australia to the extent to which the visit is made for an approved promotional purpose | all expenses: (a) incurred by the applicant in payments to persons that, in Austrade’s opinion, were not closely related to the applicant; and (b) that are allowable expenses under section 34 |

3 | any communication by the applicant or its agent with a potential buyer or a distributor, representative or consultant to the extent to which the communication is made for an approved promotional purpose | all reasonable expenses incurred by the applicant in payments to persons that, in Austrade’s opinion, were not closely related to the applicant |

4 | the provision, primarily for an approved promotional purpose, of free samples to a person that is not a resident of Australia, as follows: (a) provision outside Australia of samples relating to any eligible product of the applicant; (b) provision in Australia of samples relating to eligible tourism services supplied by the applicant | all reasonable expenses incurred by the applicant that are attributable to the actual cost of providing the samples |

5 | participation by the applicant or its agent in a trade fair, or the provision by the applicant or its agent of promotional literature or other advertising material, to the extent to which this is done for an approved promotional purpose | all reasonable expenses incurred by the applicant in payments to persons that, in Austrade’s opinion, were not closely related to the applicant |

6 | engaging as a consultant on a short term basis (either in or outside Australia) a person that, in Austrade’s opinion, is not closely related to the applicant, to the extent to which the person undertakes market research, or marketing activities, related to an approved promotional purpose | all reasonable expenses incurred by the applicant |

Note 1: For approved promotional purpose see Subdivision 3. For reasonable expenses see section 35.

Note 2: Austrade’s decisions whether a person is not closely related to an applicant are subject to guidelines determined by the Minister under section 101.

34 Expenses relating to a marketing visit

(1) This section sets out the allowable expenses of an applicant in respect of a marketing visit (see item 2 of the table in section 33).

(2) Subject to subsection (6), the following expenses in respect of any air travel reasonably undertaken by the applicant or its agent are allowable:

(a) if the applicant has paid first class air fares in respect of the travel—65% of those fares; or

(b) in any other case—the total amount of the air fares.

(3) Subject to subsection (6), all transport expenses (other than air fares) in respect of any travel reasonably undertaken by the applicant or its agent are allowable.

(4) If the visit is made to a place outside Australia:

(a) the applicant is taken, for the purposes of this subsection, to have incurred general expenses of $200 in respect of each day (working day) during the visit that was primarily devoted to furthering the approved promotional purpose for which the visit was made; and

(b) subject to subsections (5) and (6), those expenses are allowable in respect of each working day in the visit.

(5) Expenses are not allowable under subsection (4) in respect of more than 21 working days.

(6) If an agent (first agent) of the applicant who is a relative of:

(a) the applicant; or

(b) another agent of the applicant;

meets the applicant or the other agent (as the case requires) outside Australia while both:

(c) the first agent; and

(d) the applicant or other agent;

are making marketing visits outside Australia, the expenses of only one of them (being the one nominated by the applicant) are allowable expenses of the applicant. However, this subsection does not apply if the first agent, or (in a case where 2 agents meet outside Australia) each of the agents, has been working on a full-time basis for the applicant for the immediately preceding 5 years.

Note: For relative see section 107.

35 What are reasonable expenses?

(1) Austrade is to determine for the purposes of section 33 whether any expenses incurred by the applicant are reasonable.

(2) If it appears to Austrade that any expenses incurred by the applicant in respect of an eligible promotional activity may not be reasonable, Austrade must:

(a) notify the applicant, in writing, that it is of that opinion and of its reasons for being of that opinion; and

(b) ask the applicant to establish, within the period specified by Austrade, that the amount of the expenses was reasonably payable for the activity for which the expenses were incurred.

(3) If Austrade determines that any expenses of the applicant are not reasonable:

(a) Austrade must determine the amount that it considers to be reasonable for those expenses; and

(b) expenses in that amount are taken to be the reasonable expenses of the applicant for the purposes of this Division.

(4) In making a determination under subsection (1), Austrade must take into consideration any information given by the applicant in answer to Austrade’s request under paragraph (2)(b).

Subdivision 3—Approved promotional purposes

36 Object of Subdivision

This Subdivision explains what are approved promotional purposes.

37 Approved promotional purpose—eligible products

For the purposes of section 33, an eligible promotional activity in relation to an applicant is for an approved promotional purpose if it is carried out for the purpose of creating, seeking or increasing demand or opportunity in a foreign country for any of the following:

(a) eligible goods owned by the applicant and that the applicant intends to sell for export or to export and sell;

(b) if the applicant is making goods in Australia—eligible goods:

(i) made in Australia by the applicant; and

(ii) that any person intends to sell for export or to export and sell;

(c) eligible goods made outside Australia:

(i) the Australian content of which is made up wholly or principally from components supplied by the applicant; and

(ii) that any person intends to sell outside Australia;

(d) if the applicant is not an approved body or an approved trading house—eligible services supplied by the applicant;

(e) if the applicant is not an approved body—eligible intellectual property or eligible know‑how:

(i) owned by the applicant; and

(ii) that the applicant intends to dispose of;

(f) if the applicant is an approved body or approved trading house—eligible intellectual property or eligible know‑how:

(i) owned by another person; and

(ii) that the other person intends to dispose of;

(g) if the applicant is an approved body:

(i) eligible goods made in Australia and that any other person intends to sell for export or to export and sell; or

(ii) eligible services supplied by another person.

Note: For foreign country see section 22 of the Acts Interpretation Act 1901. For export, goods made in Australia and goods made outside Australia see section 107. For sell see section 109 and for dispose see section 111.

38 Approved promotional purpose—return on disposal of eligible intellectual property etc.

(1) If the applicant is not an approved body, then, for the purposes of section 33, an eligible promotional activity in relation to the applicant is also for an approved promotional purpose if it is carried out for the purpose of increasing the applicant’s return on the disposal by the applicant of eligible intellectual property or eligible know‑how.

(2) If the applicant is an approved body or approved trading house, then, for the purposes of section 33, an eligible promotional activity in relation to the applicant is also for an approved promotional purpose if it is carried out for the purpose of increasing another person’s return on the disposal by the other person of eligible intellectual property or eligible know‑how, to a third party.

(3) The return referred to in subsection (1) or (2):

(a) may be a return receivable at or after the time of disposal of the intellectual property or know‑how; and

(b) must be a return by way of royalty or licence fee.

Subdivision 4—Excluded expenses

39 Object of Subdivision

This Subdivision sets out the expenses that are excluded expenses for the purposes of subsection 33(2).

40 Guide to Subdivision

The following table lists the types of expenses that are excluded expenses and the sections dealing with them.

List of excluded expenses |

Column 1 Item | Column 2 Expense | Column 3 Section |

1 | Capital expenses | 41 |

2 | Expenses incurred when applicant not resident of Australia | 42 |

3 | Expenses related to trade with New Zealand | 43 |

4 | Expenses incurred in breach of trade sanction | 44 |

5 | Expenses (other financial assistance schemes) | 45 |

6 | Expenses for which applicant is paid | 46 |

7 | Expenses disclosed after submitting application | 47 |

8 | Taxes etc. | 48 |

9 | Expenses incurred as commission, discounts etc. | 49 |

10 | Expenses (new markets) | 50 |

11 | Expenses that involve payments to approved trading houses | 51 |

12 | Expenses of approved trading house | 52 |

13 | Expenses of approved joint venture | 53 |

14 | Expenses of applicant carrying on business in different capacities | 54 |

15 | Expenses incurred by applicant to increase return on disposal of eligible intellectual property etc. to a related company | 55 |

16 | Expenses relating to illegal activities | 56 |

17 | Expenses associated with “X”‑rated films | 57 |

41 Capital expenses

Expenses of an applicant that are of a capital nature are excluded.

42 Expenses incurred when applicant not resident of Australia

Expenses that were incurred by an applicant (other than an approved joint venture) at a time when the applicant was not a resident of Australia are excluded.

Note: For resident of Australia see section 114.

43 Expenses related to trade with New Zealand

Expenses of an applicant are excluded if they were incurred in respect of an eligible promotional activity related to trade with New Zealand.

44 Expenses incurred in breach of trade sanction

Expenses of an applicant are excluded if they were incurred in respect of an eligible promotional activity related to trade with a country that has been declared, for the purposes of paragraph 10(3)(b), to be subject to trade sanctions.

45 Expenses (other financial assistance schemes)

Expenses of an applicant are excluded if they were incurred for an eligible promotional activity related to an approved promotional purpose that was, when the expenses were incurred, approved for the purposes of a scheme (other than the scheme provided for under this Act):

(a) administered by Austrade; and

(b) making provision for financial assistance.

46 Expenses for which applicant is paid

(1) Expenses of an applicant in respect of an eligible promotional activity related to a particular approved promotional purpose are excluded to the extent (if any) to which the applicant has been paid, or is entitled to be paid, any consideration for any thing done by the applicant to further that purpose.

(2) For the purposes of subsection (1), any action by the applicant to write off, waive or otherwise release a person from, an obligation to pay any consideration is to be disregarded.

47 Expenses disclosed after submitting application

(1) This section applies if:

(a) on one or more occasions after applying for a grant in respect of a grant year, but before Austrade determines whether the applicant is entitled to the grant, an applicant discloses to Austrade eligible expenses (undisclosed expenses) that were not disclosed in the application; and

(b) the total amount of the undisclosed expenses is more than 10% of the amount of the eligible expenses disclosed in the application (disclosed expenses).

(2) The undisclosed expenses of the applicant are excluded to the extent to which they exceed 10% of the disclosed expenses.

48 Taxes etc.

(1) Subject to subsection (2), expenses of an applicant are excluded if they were incurred in payment of a tax, levy or other contribution under an Australian law.

Note: For Australian law see section 107.

(2) Subsection (1) does not apply to charge imposed by the Passenger Movement Charge Act 1978.

49 Expenses incurred as commission, discounts etc.

(1) Expenses of an applicant are excluded if they were incurred as:

(a) commission or other remuneration paid, otherwise than by way of salary, retainer or fee, in respect of commercial transactions relating to eligible products; or

(b) remuneration by way of salary, retainer or fee, to the extent that the remuneration is determined, directly or indirectly, by reference to the extent or value of any commercial transactions relating to eligible products that the person to whom the remuneration is paid has entered into; or

(c) discounts and credits, or amounts equivalent to discounts or credits, allowed or paid in relation to commercial transactions relating to eligible products.

Note: For commercial transaction see subsection (2).

(2) In subsection (1):

commercial transaction, in relation to an eligible product, means:

(a) the sale, supply or disposal of the product; and

(b) in the case of eligible intellectual property or eligible know‑how—the obtaining of an increased return on the disposal of the intellectual property or know-how.

50 Expenses (new markets)

(1) This section applies to an applicant (other than an approved body, approved joint venture or approved trading house) that is a grantee in respect of 8 or more previous grant years.

(2) Expenses of the applicant are excluded to the extent (if any) to which they relate to a market that is not a new market for the applicant.

Note: For new market see section 113.

51 Expenses that involve payments to an approved trading house

Expenses of an applicant in respect of an eligible promotional activity are excluded if:

(a) they consist of payments to an approved trading house to cover its expenses relating to the activity; and

(b) the approved trading house is an eligible applicant for a grant in respect of its eligible expenses relating to the activity.

Note: For approved trading house see section 107.

52 Expenses of approved trading house

(1) Expenses of an approved trading house are excluded if they were incurred in respect of an eligible promotional activity relating to the promotion of an eligible product owned by a person that is, in Austrade’s opinion, closely related to the approved trading house.

Note: Austrade’s decisions whether a person is closely related to an approved trading house are subject to guidelines determined by the Minister under section 101.

(2) Expenses of an approved trading house are excluded to the extent (if any) to which they were incurred in breach of any condition to which its approval as a trading house is subject.

53 Expenses of approved joint venture

(1) Expenses of an approved joint venture in respect of a grant year are excluded to the extent (if any) to which they were incurred by:

(a) a member of the joint venture at a time when the member was not a resident of Australia; or

(b) a member of the joint venture whose income for the grant year exceeds $50,000,000.

(2) Expenses of an approved joint venture are excluded to the extent (if any) to which they were incurred in breach of any condition to which its approval as a joint venture is subject.

Note: For approved joint venture and income see section 107. For resident of Australia see section 114.

54 Expenses of applicant carrying on business in different capacities

(1) If an applicant has applied for a grant in the capacity of trustee of a trust estate, any expenses of the applicant incurred otherwise than in that capacity are excluded.

(2) If an applicant that has applied for a grant in the applicant’s own right is also a trustee of a trust estate, any expenses of the applicant incurred in the capacity of trustee of the trust estate are excluded.

55 Expenses incurred by applicant to increase return on disposal of eligible intellectual property etc. to a related company

Expenses of an applicant are excluded if they were incurred in respect of an eligible promotional activity aimed at increasing the

applicant’s return on the disposal of eligible intellectual property or eligible know-how to a related company.

56 Expenses relating to illegal activities

Expenses of an applicant in respect of an eligible promotional activity related to a particular approved promotional purpose are excluded if any thing done in furthering the purpose:

(a) was, at the time when it was done, an offence against a law of the place where it was done; or

(b) would have been, at that time, an offence against an Australian law if it had been done in Australia.

Note: For Australian law see section 107.

57 Expenses associated with “X”‑rated films

(1) Expenses of an applicant are excluded if they were incurred in respect of an eligible promotional activity carried out for an approved promotional purpose relating to a film that has an “X” classification.

(2) Expenses of an applicant are excluded if:

(a) they were incurred in respect of an eligible promotional activity carried out for an approved promotional purpose relating to a film; and

(b) the film has not been given a classification; and

(c) Austrade has reason to believe the film will be refused classification or given an “X” classification.

(3) A reference in this section to classification of a film is a reference to censorship classification under an Australian law.

Note: For Australian law see section 107.

Division 3—When are expenses incurred?

58 General rule

(1) Subject to section 59, an expense is taken to have been incurred by an applicant only at the time when the amount of the expense is acquitted.

(2) For the purposes of subsection (1), the amount of an expense incurred by an applicant is taken to have been acquitted at the time when that amount:

(a) is paid off; or

(b) is set off, with the written consent of the person (creditor) to whom it is payable, against money owed by the creditor or another person to the applicant.

(3) For the purposes of subsection (2), if an amount is paid by cheque or payment order, the amount is taken to be paid when the bank or financial institution on which the cheque or payment order is drawn debits the drawer’s account.

(4) For the purposes of subsection (2), the transfer or issue to a person of shares in a company does not constitute an acquittal.

59 Expenses relating to goods etc. provided during grant year

If:

(a) apart from this section, the amount of an expense for goods or services would be taken to have been incurred during a grant year; and

(b) those goods or services, or some of them, were not provided before the end of the grant year;

the amount, or the part of the amount relating to the goods or services that were not so provided, is to be taken, if Austrade so determines, to be incurred only when the goods or services are provided.

Part 6—Amount of grant

Division 1—General

60 Object of Part

This Part sets out how to work out the amount payable to an applicant that is entitled to a grant in respect of a grant year.

61 Guide to Part

(1) Division 2 deals with the first part of the calculation process. It explains how to work out the maximum amount (the provisional grant amount) that each applicant entitled to a grant in respect of a grant year could receive.

(2) As, however, the amount available to meet all payments of grant falling due in a financial year is fixed, it follows that in some years there may not be sufficient funds to meet all provisional grant entitlements in full.

(3) Division 3 sets out the capping mechanism to be used in such circumstances to ensure that all applicants entitled to a grant receive a share of the amount available for distribution. Under the system to be applied, applicants whose provisional grant amount does not exceed a predetermined amount set by the Minister under section 68 (the initial payment ceiling amount) will not be affected and will receive their full entitlement. Only those who would have been entitled to higher amounts will have their prospective entitlements reduced.

(4) Division 4 gives power to Austrade to determine some of the factors (such as the initial payment ceiling amount) that are used in the calculation process.

Division 2—How to work out an applicant’s provisional grant amount

62 Guide to Division

An applicant’s provisional grant amount for a grant year is to be worked out under section 63 unless:

(a) Division 3 of Part 8 (Applicant party to transaction resulting in applicant obtaining grant etc.) applies; or

(b) the applicant is a member of a related company group.

Sections 64 and 65 deal with these 2 cases.

63 General rule

(1) Subject to subsections (2), (3) and (4), an applicant’s provisional grant amount for a grant year is 50% of the applicant’s eligible expenses for the grant year less $7,500.

(2) If the applicant’s eligible expenses for the grant year do not include expenses in respect of any communication with a potential buyer or a distributor, representative or consultant (see item 3 of the table in section 33), then, subject to subsection (4), the applicant’s provisional grant amount for the grant year is the sum of:

(a) the amount worked out under subsection (1) in relation to the applicant; and

(b) 3% of that amount.

(3) If an applicant, other than an approved body or approved trading house, is a grantee in respect of 3 or more grant years (including the grant year in respect of which the calculation is being made), then, subject to subsection (4), the applicant’s provisional grant amount for the grant year is the lesser of the following amounts:

(a) the amount that would be the applicant’s provisional grant amount under subsection (1) or (2) (as the case may be) if this subsection did not apply to the applicant;

(b) the amount obtained by multiplying the applicant’s export earnings for the grant year by the relevant percentage applicable to the applicant in accordance with the following table.

|

Relevant percentage |

Column 1

Item

| Column 2 Number of grant years in respect of which applicant is a grantee | Column 3

Percentage

|

1 | 3 | 40% |

2 | 4 | 20% |

3 | 5 | 10% |

4 | 6 | 7.5% |

5 | 7 or more | 5% |

Note: For grantee and export earnings see section 107.

(4) An applicant’s provisional grant amount for a grant year may not exceed:

(a) if the applicant is an approved trading house—$500,000; or

(b) in any other case—$200,000.

Note: For approved trading house see section 107.

64 Applicant party to transaction resulting in applicant obtaining grant etc.

If Austrade adjusts under Division 3 of Part 8 the amount that, apart from this section, would be the applicant’s provisional grant amount, that amount as so adjusted is taken to be the applicant’s provisional grant amount for the grant year.

65 Applicant is a member of a related company group

(1) This section applies to an applicant other than an approved trading house if:

(a) the applicant is a body corporate; and

(b) at the end of the grant year the applicant was a member of a related company group (other than an approved joint venture); and

(c) other members of the group have also applied for a grant in respect of the grant year; and

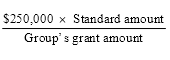

(d) the group’s grant amount exceeds $250,000.

Note: For related company group and approved joint venture see section 107. For group’s grant amount see subsection (3).

(2) The applicant’s provisional grant amount for the grant year is worked out by using the formula:

(3) In this section:

group’s grant amount means the amount obtained by:

(a) working out the amount that would be (under section 63 or 64) the provisional grant amount of each of the members of the related company group that have applied for a grant in respect of the grant year if this section did not apply to the member; and

(b) adding up all those amounts.

standard amount means the amount that would be (under section 63 or 64) the applicant’s provisional grant amount for the grant year if this section did not apply to the applicant.

Division 3—How to work out amount of grant

66 Object of Division

This Division sets out how to work out the actual amount that an applicant entitled to a grant in respect of a grant year will receive.

67 Amount of grant

(1) If an applicant is entitled to a grant in respect of a grant year, the amount of the grant is worked out in accordance with the following subsections.

(2) If the applicant’s provisional grant amount for the grant year does not exceed the initial payment ceiling amount for the grant year, the amount of the grant is equal to the applicant’s provisional grant amount.

(3) If the applicant’s provisional grant amount for the grant year exceeds the initial payment ceiling amount for the grant year:

(a) multiply the amount of the excess by the payout factor for the grant year; and

(b) add the amount obtained under paragraph (a) to the initial payment ceiling amount.

The result is the amount of grant payable to the applicant for the grant year.

Note 1: For initial payment ceiling amount, provisional grant amount and payout factor see section 107.

Note 2: The payout factor for the grant year will only be known after the balance distribution date for the year following the grant year (See subsections 69(1) and (2)).

Division 4—Initial payment ceiling amount, balance distribution date and payout factor

68 Determination of initial payment ceiling amount etc.

(1) The Minister may, from time to time, determine in writing:

(a) the amount that is the initial payment ceiling amount for:

(i) the grant year (initial year) immediately preceding the year that is current when the determination comes into force; and

(ii) each grant year following the initial year; and

(b) the date:

(i) in the grant year that is current when the determination comes into force; and

(ii) in each subsequent grant year;

that is the balance distribution date for that year.

(2) The balance distribution date for the grant year that is current when the determination comes into force must be later than the date on which the determination comes into force.

(3) A determination under subsection (1) is a disallowable instrument for the purposes of section 46A of the Acts Interpretation Act 1901.

69 Payout factor

(1) For the purposes of subsection 67(3), Austrade must, in respect of each grant year:

(a) work out in accordance with the regulations; and

(b) determine in writing;

the payout factor that, in calculating the amount payable to each applicant:

(c) entitled to receive a grant in respect of that year; and

(d) whose provisional grant amount in respect of that year exceeds the initial payment ceiling amount for that year;

is to be used to adjust the amount of the excess.

Note: For provisional grant amount and initial payment ceiling amount see section 107.

(2) The determination must be made as soon as practicable after the balance distribution date for the following year.

(3) The purpose, in applying the payout factor, is to ensure that the amount of each grant payable in respect of the grant year is capped at the appropriate level so that all payments of grant that become due in the year following the grant year are able to be met from the money available for that purpose.

(4) The regulations may prescribe the method for working out the factor that will be the payout factor for a grant year.

Part 7—Application for, and payment of, grant

Division 1—Applying for a grant

70 How to apply for a grant

(1) A person that is eligible for a grant in respect of a grant year may make an application to Austrade for the grant.

(2) The application must:

(a) be in a form, and be made in a manner, approved by Austrade; and

(b) be made within 5 months after the end of the grant year.

(3) If the person is an approved joint venture, the application must be made on behalf of the joint venture by the nominated contact member.

Note: For grant, grant year, approved joint venture and nominated contact member see section 107.

71 Application made when Austrade etc. receives it

An application is not taken to have been made until it has been received by:

(a) Austrade; or

(b) a person appointed by Austrade to receive applications under this section.

72 Austrade may ask applicant etc. for further information etc.

(1) Austrade may:

(a) by written notice given to an applicant, ask the applicant; or

(b) if the applicant is a body corporate that was a member of a related company group as at the end of the grant year to which the application relates—by written notice given to each body corporate that was a member of the group, ask each of these bodies;

to give to Austrade specified information, or to make available to Austrade specified books, records or documents, that Austrade may require to perform its functions under this Act.

(2) Austrade may, by written notice to the applicant, ask the applicant to give to Austrade any written consent (whether of the applicant or of any associate of the applicant) specified in the notice that Austrade requires to enable criminal records to be checked for the purposes of applying Division 4 of Part 3 and section 86 to the applicant.

Note: Part VIIC of the Crimes Act 1914 exempts a person from having to disclose spent convictions.

(3) If Austrade makes a form available for the purpose of making an application for a grant, the form must contain an explanation of the effect of subsections (1) and (2) and paragraph 73(b). If Austrade does not make such a form available, Austrade must give to each applicant a document that contains an explanation of the effect of those provisions.

73 Grounds on which Austrade may refuse to consider application

Austrade may refuse to consider an application if:

(a) the application is not in accordance with subsection 70(2); or

(b) the applicant, or (if the applicant is a body corporate that was a member of a related company group) a related company, has not complied with a request of Austrade under section 72; or

(c) an individual who has helped, in a prescribed capacity, to prepare the application has not complied with a request of Austrade under section 79.

Note: For prescribed capacity see subsection 74(2).

Division 2—Disqualified individual not to help in preparing application

74 Application of Division

(1) This Division applies to an application for a grant made to Austrade if:

(a) it has been prepared for the applicant by an export market development grants consultant; and

(b) an individual helped, in a prescribed capacity, to prepare the application.

Note: For export market development grants consultant see section 107. For prescribed capacity see subsection (2).

(2) For the purposes of this Part, an individual helps to prepare an application in a prescribed capacity if:

(a) either:

(i) any work done by the individual in preparing the application involves forming an opinion (whether formal or informal) about the operation of the law on a matter dealt with by the application; or

(ii) the individual manages or supervises (directly or indirectly) work mentioned in subparagraph (i); and

(b) the work, management or supervision (as the case may be) is performed by or on behalf of an export market development grants consultant.

75 Application taken not to have been made if individual helps, in a prescribed capacity, to prepare it

If the individual who helped to prepare the application:

(a) is, at the time when the application is made, disqualified from preparing applications; or

(b) becomes disqualified from preparing applications at any time during the period beginning when the application is made

and ending immediately before Austrade determines whether the applicant is entitled to a grant;

the application is taken for the purposes of this Act (other than this Division) not to have been made.

76 Austrade must notify applicant that application taken not to have been made

If the application is taken (under section 75) not to have been made, Austrade must, as soon as practicable after becoming aware of that fact, give to the applicant a written notice:

(a) stating that the application is taken not to have been made; and

(b) setting out the effect of section 77.

77 When applicant may make fresh application

(1) If an application (first application) is taken (under section 75) not to have been made, the applicant may make a fresh application under subsection 70(1) if:

(a) when the first application was made, the individual concerned was not yet disqualified; or

(b) when the first application was made:

(i) the individual concerned was disqualified; but

(ii) the applicant neither knew, nor had reasonable grounds to suspect, that the individual was disqualified.

(2) The fresh application must be made within:

(a) 90 days after the applicant receives the notice referred to in section 76; or

(b) 5 months after the end of the grant year;

whichever is the later.

78 Disqualified individual

(1) If an individual has been convicted of:

(a) an offence that under subsection 229(3) of the Corporations Law disqualifies a person from managing a corporation; or

(b) an offence against section 29A, 29B, 29C or 29D of the Crimes Act 1914 that relates to an application for a grant; or

(c) an offence against section 39 of the repealed Act; or

(d) an offence under:

(i) section 5, 6, 7 or 7A or subsection 86(1) of the Crimes Act 1914; or

(ii) a provision of a law of a State or Territory that corresponds to any of those provisions;

that relates to an offence referred to in paragraph (a), (b) or (c);

the individual is disqualified from preparing applications for the disqualification period.

(2) For the purposes of this section, the disqualification period is the period starting on the day on which the conviction was recorded and ending:

(a) if the conviction was for a term of imprisonment—5 years after the individual convicted was released from prison; or

(b) in any other case—5 years after the day on which the conviction was recorded.

79 Consent to enable check of criminal records

Austrade may, by written notice to an individual who has helped, in a prescribed capacity, to prepare an application, ask the individual to give to Austrade any written consent that Austrade requires to enable criminal records to be checked for the purposes of applying this Division to the individual.

Note 1: For prescribed capacity see subsection 74(2).

Note 2: Part VIIC of the Crimes Act 1914 exempts a person from having to disclose spent convictions.

Division 3—Determining entitlement to, and making payment of, grant

Subdivision 1—Duties of Austrade

80 Austrade must determine applicant’s entitlement to grant etc.

(1) Austrade must:

(a) subject to section 73, consider each application for a grant; and

(b) determine whether the applicant is entitled to a grant; and

(c) if Austrade determines that the applicant is entitled to a grant—determine the amount of the grant as soon as practicable.

(2) The applicant becomes entitled to the grant when Austrade makes the determination under paragraph (1)(b).

Subdivision 2—When grant payable

81 Payment where applicant becomes entitled to grant before balance distribution date

(1) If Austrade’s determination that an applicant is entitled to a grant in respect of a grant year (first determination) is made before the balance distribution date for the year following the grant year, the following provisions apply.

Note: For balance distribution date see section 107.

(2) If the applicant’s provisional grant amount for the grant year does not exceed the initial payment ceiling amount for the grant year, the grant becomes (subject to section 83) payable to the applicant when Austrade determines the amount of the grant under paragraph 80(1)(c).

Note: For the amount of the grant see subsection 67(2).

(3) If the applicant’s provisional grant amount for the grant year exceeds the initial payment ceiling amount for the grant year:

(a) the applicant is, on the making of the first determination (but subject to section 83), entitled to be paid an advance on account of the grant equal to the initial payment ceiling amount; and

(b) subject to section 83, the grant becomes payable to the applicant when Austrade determines the amount of the grant under paragraph 80(1)(c).

Note 1: The amount of the grant may be determined in this case only after the balance distribution date for the year following the grant year. The applicant is then entitled to receive the amount of the grant less any advance on account of the grant paid to the applicant. For the amount of the grant see subsection 67(3).

Note 2: Subdivision 3 sets out the circumstances in which a grant is not payable to an applicant.

82 Payment where applicant becomes entitled to grant after balance distribution date

If Austrade’s determination that the applicant is entitled to a grant in respect of a grant year is made after the balance distribution date for the year following the grant year, then, subject to section 83, the grant becomes payable:

(a) if Austrade determines the amount of the grant before the 1 July next following the balance distribution date—on that 1 July; or

(b) in any other case—on the day on which the amount of the grant is determined.

Note 1: For the amount of the grant see section 67.

Note 2: Subdivision 3 sets out the circumstances in which a grant is not payable to an applicant.

83 Payment of grant—applicant member of a related company group

(1) If section 65 applies to an applicant for a grant, the grant, or an advance on account of the grant, becomes payable to the applicant when:

(a) Austrade’s determination under paragraph 80(1)(c) in relation to the applicant; and

(b) Austrade’s determination under paragraph 80(1)(c) in relation to each company that:

(i) is related to the applicant; and

(ii) has also applied for a grant;

have been finalised.

Note: For related company see section 107. For finalised see subsection (2).

(2) For the purposes of subsection (1), a determination under paragraph 80(1)(c) is finalised when:

(a) the determination; and

(b) any decision of a court affecting that determination;

may no longer be, or is not, subject to a review by, or an appeal to, another court.

(3) In subsection (2):

court includes the Administrative Appeals Tribunal.

Note: Subdivision 3 sets out the circumstances in which a grant is not payable to an applicant.

84 Payment of grant—approved joint venture

A grant, or an advance on account of a grant, that is payable to an approved joint venture is to be paid to the nominated contact member.

Note: For nominated contact member see section 107.

Subdivision 3—Circumstances in which grant not payable

85 Person not resident of Australia

(1) Despite Subdivision 2, a grant, or an advance on account of a grant, is not payable to a person if, at the time when, or at any time after, the person becomes entitled to the grant or advance, the person ceases to be a resident of Australia.

(2) Subsection (1) does not affect the validity of a payment of grant, or of an advance on account of grant, to the person before the person ceased to be a resident of Australia.

Note: For resident of Australia see section 114.

86 Disqualifying conviction outstanding against grantee etc.

(1) Despite Subdivision 2, a grant, or an advance on account of a grant, is not payable to a person if, at the time when, or at any time after, the person becomes entitled to the grant or advance, there is a disqualifying conviction outstanding against:

(a) if paragraph (b) does not apply—the person; or

(b) if the person is entitled to the grant or advance in the capacity of trustee of a trust estate—the person or any beneficiary of the trust estate.

(2) Subsection (1) does not affect the validity of a payment of grant, or of an advance on account of grant, to the person at a time when there was no disqualifying conviction outstanding against the person, or the person or any beneficiary of the trust estate, as the case may be.

Note: For disqualifying conviction see section 107.

87 Grantee etc. under insolvency administration

(1) Despite Subdivision 2, a grant, or an advance on account of a grant, is not payable to a person if, at the time when, or at any time after, the person becomes entitled to the grant or advance:

(a) if paragraph (b) does not apply—the person or (where applicable) an associate of the person; or

(b) if the person is entitled to the grant or advance in the capacity of trustee of a trust estate:

(i) the person or (where applicable) an associate of the person; or

(ii) any beneficiary of the trust estate or (where applicable) an associate of the beneficiary;

is under insolvency administration.

(2) Subsection (1) does not affect the validity of a payment of grant, or of an advance on account of grant, to the person at a time when:

(a) if paragraph (1)(a) applies to the person—neither the person, nor any associate of the person; or

(b) if paragraph (1)(b) applies to the person—neither the person nor any other person referred to in that paragraph;

was under insolvency administration.

Note: For associate and under insolvency administration see section 107.

Part 8—Miscellaneous

Division 1—Approved bodies, approved trading houses and approved joint ventures

88 Applications for approval

(1) Any of the following:

(a) a body corporate established for a public purpose by or under an Australian law;

(b) a co-operative;

(c) any other body corporate representing the interests of an industry or of a substantial part of an industry;

may apply to Austrade for approval as an approved body.

(2) A group of persons may apply to Austrade for approval as a joint venture.

(3) A person (other than a joint venture) may apply to Austrade for approval as an approved trading house.

(4) The application must be in writing and in accordance with a form approved by Austrade.

89 Approval

(1) Subject to section 92, Austrade must deal with the application in accordance with the regulations.

(2) A decision of Austrade to approve, or not to approve, the applicant must be in writing.

Note: Subsection 33(3) of the Acts Interpretation Act 1901 provides that a power conferred on a person to make an instrument (such as a written approval) includes the power to cancel or vary the instrument.

(3) Subject to subsections (4) and (5), an approval must specify the conditions (if any) to which the approval is subject.

(4) An approval of a group of persons as a joint venture must:

(a) specify the activity, project or purpose for which the group is approved; and

(b) specify the member of the group who is the nominated contact member for the purposes of applications and payments of grant.

Only a resident of Australia may be specified as a nominated contact member.

(5) An approval of a person as a trading house must specify the activity, project or purpose for which the person is approved.