Taxation Laws Amendment Act (No. 3) 1997

No. 147, 1997

Taxation Laws Amendment Act (No. 3) 1997

No. 147, 1997

Taxation Laws Amendment Act (No. 3) 1997

No. 147, 1997

An Act to amend the law relating to taxation

Contents

1 Short title..................................1

2 Commencement..............................1

3 Schedule(s).................................3

4 Amendment of income tax assessments.................3

Schedule 1—CGT exemption: disposing of small business retirement assets 4

Part 1—Amendment of the Income Tax Assessment Act 1936 4

Division 1—Amendment of CGT provisions 4

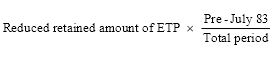

Division 2—Amendment of superannuation‑related provisions 19

Part 2—Amendment of the Terminations Payments Tax (Assessment and Collection) Act 1997 22

Part 3—Application 22

Schedule 2—Sale of mining rights 22

Income Tax Assessment Act 1936 22

Income Tax Assessment Act 1997 22

Schedule 3—Family tax initiative 22

Income Tax Assessment Act 1936 22

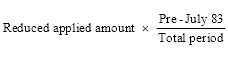

Schedule 4—Dividend imputation and tax exempt entities 22

Part 1—Amendment of the Income Tax Assessment Act 1936 22

Part 2—Application 22

Schedule 5—Principal residence exemption from CGT 22

Part 1—Amendment of the Income Tax Assessment Act 1936 22

Division 1—Dwellings acquired from deceased persons: extension of 12 month rule to 2 years 22

Division 2—Dwellings acquired from deceased persons: partial exemptions from CGT 22

Division 3—Dwellings acquired from deceased persons: status of residence at time of death 22

Division 4—Status of dwelling when first used for producing assessable income 22

Part 2—Application 22

Schedule 6—Treatment of payments made under firearms surrender arrangements 22

Part 1—Amendment of the Income Tax Assessment Act 1936 22

Part 2— Amendment of the Income Tax Assessment Act 1997 22

Schedule 7—Remote area housing 22

Fringe Benefits Tax Assessment Act 1986 22

Schedule 8—Depreciation of lessor’s fixtures 22

Income Tax Assessment Act 1936 22

Schedule 9—Increase in age limit for superannuation contributions 22

Part 1—Amendment of the Superannuation Guarantee (Administration) Act 1992 22

Part 2—Amendment of the Small Superannuation Accounts Act 1995 22

Schedule 10—Rebate for superannuation contributions made on behalf of a low‑income or non-working spouse 22

Income Tax Assessment Act 1936 22

Schedule 11—Research and development 22

Income Tax Assessment Act 1936 22

Taxation Laws Amendment Act (No. 3) 1996 22

Schedule 12—Sales tax 22

Sales Tax (Exemptions and Classifications) Act 1992 22

Schedule 13—Subsidiary company liquidations and capital gains tax 22

Part 1—Amendment of the Income Tax Assessment Act 1936 22

Part 2—Application 22

Schedule 14—Gains and losses 22

Part 1—Income Tax Assessment Act 1936 (revenue losses) 22

Part 2—Income Tax Assessment Act 1936 (capital gains and capital losses) 22

Part 3—Income Tax Assessment Act 1936 (capital gains tax definitions) 22

Part 4—Income Tax Assessment Act 1997 (revenue losses) 22

Part 5—Income Tax (Consequential Amendments) Act 1997 22

Schedule 15—Deductions for gifts 22

Part 1—Amendment of the Income Tax Assessment Act 1936 22

Part 2—Amendment of the Income Tax Assessment Act 1997 22

Schedule 16—Technical amendments 22

Taxation Laws Amendment Act 1993 22

Taxation Laws Amendment Act (No. 3) 1994 22

Taxation Laws Amendment Act (No. 4) 1995 22

Taxation Laws Amendment Act (No. 3) 1996 22

Taxation Laws Amendment Act (No. 2) 1997 22

Taxation Laws Amendment (Private Health Insurance Incentives) Act 1997 22

Schedule 17—Employee share schemes 22

Income Tax Assessment Act 1936 22

Taxation Laws Amendment Act (No. 3) 1997

No. 147, 1997

An Act to amend the law relating to taxation

[Assented to 14 October 1997]

The Parliament of Australia enacts:

This Act may be cited as the Taxation Laws Amendment Act (No. 3) 1997.

(1) Subject to this section, this Act commences on the day on which it receives the Royal Assent.

(2) Item 4 of Schedule 6 commences, or is taken to have commenced, immediately after the commencement of item 76 of Schedule 6 to the Tax Law Improvement Act 1997.

(3) Part 2 of Schedule 6 commences, or is taken to have commenced, immediately after the commencement of the Income Tax Assessment Act 1997.

(4) Items 2 and 5 of Schedule 10 commence immediately after the later of the commencement of item 1 of that Schedule or the Retirement Savings Accounts Act 1997.

(5) Schedule 11 is taken to have commenced immediately after the commencement of item 38 of Schedule 4 to the Taxation Laws Amendment Act (No. 3) 1996.

(6) Schedule 12 is taken to have commenced at 7.00 pm, by legal time in the Australian Capital Territory, on 7 November 1996.

(7) Part 4 of Schedule 14 commences, or is taken to have commenced, on 1 July 1997, immediately after the commencement of the Income Tax Assessment Act 1997.

(8) Part 5 of Schedule 14 commences, or is taken to have commenced, on 1 July 1997, immediately after the commencement of the Income Tax (Consequential Amendments) Act 1997.

(9) Part 2 of Schedule 15 commences at the later of:

(a) the start of the day on which this Act receives the Royal Assent; and

(b) immediately after the commencement of Schedule 1 to the Tax Law Improvement Act 1997.

(10) Item 1 of Schedule 16 is taken to have commenced immediately after the commencement of section 44 of the Taxation Laws Amendment Act 1993.

(11) Items 2 and 3 of Schedule 16 are taken to have commenced immediately after the commencement of Part 1 of the Schedule to the Taxation Laws Amendment Act (No. 3) 1994.

(12) Item 4 of Schedule 16 is taken to have commenced immediately after the commencement of item 1 of Schedule 2 to the Taxation Laws Amendment Act (No. 4) 1995.

(13) Items 5 and 6 of Schedule 16 are taken to have commenced immediately after the commencement of item 134 of Schedule 2 to the Taxation Laws Amendment Act (No. 4) 1995.

(14) Item 7 of Schedule 16 is taken to have commenced immediately after the commencement of item 74 of Schedule 4 to the Taxation Laws Amendment Act (No. 3) 1996.

(15) Item 8 of Schedule 16 is taken to have commenced immediately after the commencement of item 9 of Schedule 1 to the Taxation Laws Amendment Act (No. 2) 1997.

(16) Item 9 of Schedule 16 is taken to have commenced immediately after the commencement of item 1 of Schedule 3 to the Taxation Laws Amendment (Private Health Insurance Incentives) Act 1997.

Subject to section 2, each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

Section 170 of the Income Tax Assessment Act 1936 does not prevent the amendment of an assessment made before the commencement of this section for the purposes of giving effect to this Act.

1 Section 160AZA (Sub Index—Exemptions, after entry relating to principal residence)

Insert:

Small business retirement assets | Division 17B of Part IIIA |

2 After section 160ZZPQ

Insert:

A taxpayer must not make an election under paragraph 160ZZPQ(1)(f) in respect of the disposal of an asset if the taxpayer has previously made an election under Division 17B in respect of the disposal.

3 After Division 17A of Part IIIA

Insert:

Broadly, a capital gain accruing on the disposal of an asset by a small business is exempt from tax under this Part, if the proceeds of the disposal are used in connection with the retirement of an individual, or 2 individuals, who control that business. The amount of the gain will be treated as a special kind of eligible termination payment made to the individuals.

Sole traders and partnerships

(1) For a taxpayer who is an individual (carrying on business as a sole trader or as a partner in a partnership) to get an exemption, and for the other consequences set out in this Division to apply, the conditions in Subdivision B must be satisfied.

Companies and trusts

(2) For a taxpayer that is a private company or trust to get an exemption, and for the other consequences set out in this Division to apply, the conditions in Subdivision C must be satisfied.

Lifetime exemption limit

(3) There is a lifetime limit of $500,000 on the total of amounts that may be exempt in relation to a particular individual under this Division (see section 160ZZPZN). The single limit applies to all exempt amounts involving the individual, whether under Subdivision B or C.

Previous years’ net capital losses

(4) An exemption under this Division is not available to the extent that the taxpayer has net capital losses from previous years of income available to set off against the capital gain (see Subdivision D).

Definitions

(5) Definitions of various expressions used in the Division are in Subdivision E.

The consequences set out in section 160ZZPZE apply to a taxpayer who is an individual if the conditions in section 160ZZPZD are met.

First condition

(1) The first condition is that:

(a) the requirements of paragraphs 160ZZPQ(1)(a) to (d) must be satisfied in relation to the disposal of an asset by the taxpayer other than as a trustee; and

(b) the taxpayer must receive all of the actual consideration (see section 160ZZPZO), if any, in respect of the disposal within the period beginning one year before, and ending 2 years after, the disposal.

The whole of the actual consideration mentioned in paragraph (b) need not be received all at once; parts of the actual consideration may be received at different times during the period.

Second condition

(2) The second condition is that:

(a) the taxpayer must elect in writing, on or before the date of lodgment of the taxpayer’s return of income for the year of income mentioned in paragraph 160ZZPQ(1)(a), that this Division is to apply to the taxpayer in respect of the disposal; and

(b) the election must specify an amount as the asset’s CGT exempt amount; and

(c) that amount must not be greater than the amount of the capital gain concerned (possibly as reduced by Subdivision D, which deals with previous years’ net capital losses); and

(d) the asset’s CGT exempt amount must not exceed the individual’s CGT retirement exemption limit (see section 160ZZPZN) immediately before the election is made; and

(e) the taxpayer must not have already made an election under section 160ZZPQ in respect of the disposal.

(1) If the conditions in section 160ZZPZD are met, the following consequences apply.

Capital gain reduced by asset’s CGT exempt amount

(2) The amount of the capital gain that otherwise would have accrued to the taxpayer in respect of the disposal of the asset concerned is reduced (but not below nil) by the asset’s CGT exempt amount.

Other CGT exemptions/concessions are not available

(3) Divisions 15, 17, 17A, 18 and 19 do not apply in respect of the disposal.

Proceeds of disposal taken to be an ETP

(4) Also, for each amount the taxpayer receives as actual consideration in respect of the disposal at a particular time, an ETP of that amount (but possibly reduced by subsection (5)) is taken, for the purposes of this Act, to have been made in relation to the taxpayer at the later of the following times:

(a) the time the election is made;

(b) the time the actual consideration is received.

Note: For the rules about ETPs (eligible termination payments), see Subdivision AA of Division 2 of Part III.

No ETP to the extent that the total actual consideration received exceeds the asset’s CGT exempt amount

(5) However, if the sum of:

(a) the amount of the actual consideration; and

(b) the total amount of any actual consideration the taxpayer received earlier in respect of the disposal;

exceeds the asset’s CGT exempt amount, the amount of the ETP is reduced by the amount of the excess.

Note: In some cases, this will reduce the amount of the ETP to nil.

Example: Assume that the asset’s CGT exempt amount is $1,000. Assume that the taxpayer receives an amount of actual consideration of $300, and has previously received $900 as actual consideration in respect of the disposal. The sum of that actual consideration is $1,200, which exceeds the asset’s CGT exempt amount by $200. Therefore the amount of this ETP is reduced by $200 to $100.

(1) If the taxpayer was under 55 immediately before the disposal, an amount equal to the amount of each ETP that is taken to have been made under subsection 160ZZPZE(4) must be rolled over (within the meaning of Subdivision AA of Division 2 of Part III, but assuming that paragraph 27A(12)(c) had not been enacted) by the taxpayer.

(2) If the taxpayer does not comply with subsection (1), the election is taken never to have been made.

Note: Because making the election is a condition (see paragraph 160ZZPZD(2)(a)), the taxpayer will lose the benefit of this Subdivision in such a case.

The consequences set out in section 160ZZPZJ apply to a taxpayer that is a company (other than a public company) or a trust (other than a publicly traded unit trust) if either:

(a) the single‑controller conditions set out in section 160ZZPZH are met; or

(b) the dual‑controller conditions set out in section 160ZZPZI are met.

(1) This section sets out the conditions that are the single-controller conditions.

First condition

(2) The first condition is that:

(a) the requirements of paragraphs 160ZZPQ(1)(a) to (d) must be satisfied in relation to the disposal of an asset by the taxpayer; and

(b) the taxpayer must receive all of the actual consideration (see section 160ZZPZO), if any, in respect of the disposal within the period beginning one year before, and ending 2 years after, the disposal.

The whole of the actual consideration mentioned in paragraph (b) need not be received all at once; parts of the actual consideration may be received at different times during the period.

Second condition

(3) The second condition is that, immediately before the disposal, there must be one, and only one, controlling individual (see section 160ZZPZP) of the taxpayer.

Third condition

(4) The third condition is that:

(a) the taxpayer must elect in writing, on or before the date of lodgment of the taxpayer’s return of income for the year of income mentioned in paragraph 160ZZPQ(1)(a), that this Division is to apply to the taxpayer in respect of the disposal; and

(b) the election must specify an amount as the asset’s CGT exempt amount; and

(c) that amount must not be greater than the amount of the capital gain concerned (possibly as reduced by Subdivision D, which deals with previous years’ net capital losses); and

(d) the asset’s CGT exempt amount must not exceed the controlling individual’s CGT retirement exemption limit (see section 160ZZPZN) immediately before the election is made; and

(e) the taxpayer must not have already made an election under section 160ZZPQ in respect of the disposal.

Fourth condition

(5) The fourth single-controller condition is that, within:

(a) 7 days after making the election; or

(b) 7 days after the taxpayer receives the whole or a part (the payment amount) of the actual consideration as mentioned in paragraph (2)(b);

whichever comes later, the taxpayer must make an ETP in relation to the controlling individual whose amount is at least equal to the payment amount.

Note: The payment amount may be reduced under subsection (8).

If there are 2 or more ETPs required

(6) If, at a particular time, subsection (5) requires a taxpayer to make 2 or more ETPs to the controlling individual (whether or not by the same time), the taxpayer may meet that requirement either:

(a) by making separate ETPs whose amounts are in total at least equal to the sum of the payment amounts; or

(b) by making a single ETP whose amount is at least equal to the sum of the payment amounts.

Fifth condition

(7) The fifth condition is that, if the controlling individual was under 55 immediately before the disposal, an amount, in relation to the ETP, at least equal to the payment amount must be rolled over (within the meaning of Subdivision AA of Division 2 of Part III, reading references in that Subdivision to “the taxpayer” as references to the controlling individual instead, and assuming that paragraph 27A(12)(c) had not been enacted) by the controlling individual.

Note: The payment amount may be reduced under subsection (8).

ETP not required to the extent that the total actual consideration received exceeds the asset’s CGT exempt amount

(8) However, if the sum of:

(a) the payment amount; and

(b) the total amount of any actual consideration the taxpayer received, as mentioned in paragraph (2)(b), earlier in respect of the disposal;

exceeds the asset’s CGT exempt amount, the payment amount is reduced, for the purposes of subsections (5), (6) and (7), by the amount of the excess.

Note: In some cases, this will reduce that amount to nil.

Example: Assume that the asset’s CGT exempt amount is $1,000. Assume that the taxpayer receives a payment amount of $300, and has previously received $900 as actual consideration in respect of the disposal. The sum of those amounts is $1,200, which exceeds the asset’s CGT exempt amount by $200. Therefore the amount of this payment amount is reduced by $200 to $100.

(1) This section sets out the conditions that are the dual-controller conditions.

First condition

(2) The first condition is that:

(a) the requirements of paragraphs 160ZZPQ(1)(a) to (d) must be satisfied in relation to the disposal of an asset by the taxpayer; and

(b) the taxpayer must receive all of the actual consideration (see section 160ZZPZO), if any, in respect of the disposal within the period beginning one year before, and ending 2 years after, the disposal.

The whole of the actual consideration mentioned in paragraph (b) need not be received all at once; parts of the actual consideration may be received at different times during the period.

Second condition

(3) The second condition is that, immediately before the disposal, there must be 2 controlling individuals (see section 160ZZPZP) of the taxpayer.

Third condition

(4) The third condition is that:

(a) the taxpayer must elect in writing, on or before the date of lodgment of the taxpayer’s return of income for the year of income mentioned in paragraph 160ZZPQ(1)(a), that this Division is to apply to the taxpayer in respect of the disposal; and

(b) the election must specify an amount as the asset’s CGT exempt amount; and

(c) that amount must not be greater than the amount of the capital gain concerned (possibly as reduced by Subdivision D, which deals with previous years’ net capital losses); and

(d) the election must specify the percentages (the exemption percentages) of the asset’s CGT exempt amount that are to be regarded as attributable to each of the 2 controlling individuals. One of the percentages may be nil, but the 2 percentages must add up to 100%; and

(e) for each of the 2 controlling individuals, the individual’s exemption percentage of the asset’s CGT exempt amount must not exceed that individual’s CGT retirement exemption limit immediately before the election is made; and

Example: Fiona is a controlling individual of a taxpayer. Her exemption percentage is 10% (which means that the other controlling individual’s exemption percentage must be 90%). Fiona’s CGT retirement exemption limit is $500,000. To determine whether paragraph (e) is complied with, she would take 10% of the asset’s CGT exempt amount and see whether that amount exceeds $500,000.

(f) the taxpayer must not have already made an election under section 160ZZPQ in respect of the disposal.

Fourth condition

(5) The conditions in subsections 160ZZPZH(5) to (8) are also dual‑controller conditions, except that the subsections apply separately in respect of each of the 2 controlling individuals as if:

(a) each were the only controlling individual; and

(b) references (other than in paragraph (5)(b) and subsection (8)) to the payment amount were, in relation to each controlling individual, instead a reference to the following amount:

![]()

(1) If the conditions in section 160ZZPZH or 160ZZPZI are met, the following consequences apply.

Capital gain reduced by asset’s CGT exempt amount

(2) The amount of the capital gain that otherwise would have accrued in respect of the disposal concerned is reduced (but not below nil) by the asset’s CGT exempt amount.

Other CGT exemptions/concessions are not available

(3) Divisions 15, 17, 17A, 18 and 19 do not apply in respect of the disposal.

Treatment of ETP

(4) Any ETP, or part of an ETP, the taxpayer makes, to the extent required to comply with subsection 160ZZPZH(5) (including as it is applied by subsection 160ZZPZI(5)):

(a) is taken, for the purposes of this Act, to consist solely of a CGT exempt component; and

(b) is not an allowable deduction of the taxpayer.

Note: For the rules about ETPs (eligible termination payments), see Subdivision AA of Division 2 of Part III.

(1) If:

(a) immediately before the disposal of the asset concerned, there was only one controlling individual of the taxpayer; and

(b) at any time during the period (the ownership period) from the later of:

(i) the start of the 1992-93 year of income; and

(ii) the time when the taxpayer acquired the asset;

until immediately before the disposal, the individual was not the controlling individual of the taxpayer;

the asset’s CGT exempt amount is reduced by the following amount:

(2) However, if, disregarding subparagraph (1)(b)(i), the asset’s CGT exempt amount would be reduced by a lesser amount, the asset’s CGT exempt amount is instead reduced by that lesser amount.

If there are 2 controlling individuals

(3) If, immediately before the disposal, there were 2 controlling individuals of the taxpayer, the asset’s CGT exempt amount is reduced by the sum of the amounts, worked out for each controlling individual, using the formula:

(1) This section applies if:

(a) a taxpayer makes one or more elections under paragraph 160ZZPZD(2)(a), 160ZZPZH(4)(a) or 160ZZPZI(4)(a) in respect of disposals of assets during a particular year of income (the current year); and

(b) the taxpayer incurred one or more net capital losses in respect of years of income before the current year, but after the 1994-95 year of income, that have not been fully applied under section 160ZC in respect of years of income before the current year; and

(c) the losses would, apart from this Division, be fully or partly applied in determining whether a net capital gain accrues to the taxpayer in respect of the current year (if sufficient capital gains accrue in the current year). The extent to which a loss would be so applied is called the unapplied loss.

Capital gains are reduced

(2) The capital gain in respect of each of the disposals is reduced (but not below nil) by an amount (the reduction amount) equal to so much of the total amount of the unapplied losses as has not already (see subsection (4)) been applied in reducing other capital gains under this subsection for the current year or an earlier year of income.

Losses are also reduced, in the order in which they were incurred

(3) The net capital losses are reduced (but not below nil) by the reduction amount, in the order in which the taxpayer incurred the losses.

Order of reduction of capital gains is the order in which elections were made

(4) Capital gains in respect of disposals are to be reduced under subsection (2) in the order in which the taxpayer made the elections as mentioned in paragraph (1)(a) in respect of the disposals.

This section applies before other net capital loss provisions

(5) For any given year of income, this section is to be applied in reduction of net capital losses before section 160ZC and Division 17A are to be applied in relation to those losses.

Example

(6) The following is an example of how this section works:

Example: Assume that a taxpayer has net capital losses from previous years of income of $200 and $300 (incurred in that order). Assume that the taxpayer made elections in respect of the disposal of assets A, B and C (in that order) and that the amounts of the respective capital gains were $200, $400 and $700.

First, the capital gain in respect of asset A is reduced to nil by the $200 loss. (Note that the election for asset A must therefore specify nil as that asset’s CGT exempt amount.) The $300 loss is then applied against the capital gain in respect of asset B, reducing it to $100.

Now that all of the total amount of the losses has been applied, the capital gain in respect of asset C is not reduced under this section.

In this Division:

actual consideration has the meaning given by section 160ZZPZO.

asset has the same meaning as in Division 17A.

CGT retirement exemption limit has the meaning given by section 160ZZPZN.

controlling individual has the meaning given by section 160ZZPZP.

ETP means an eligible termination payment within the meaning of section 27A.

pattern of distributions test has the meaning given by subsection 160ZZPZQ(1).

public company has the same meaning as in Division 17A.

publicly traded unit trust has the same meaning as in Division 17A.

test year has the meaning given by subsection 160ZZPZQ(2).

trust has the same meaning as in Division 17A.

(1) An individual’s CGT retirement exemption limit at a particular time is the amount worked out as follows:

![]()

where:

previous elections means elections under paragraph 160ZZPZD(2)(a), 160ZZPZH(4)(a) or 160ZZPZI(4)(a) made before the particular time by:

(a) the individual; or

(b) a company or trust whose controlling individual, or one of whose controlling individuals, was the individual.

If there are 2 controlling individuals

(2) If the individual was one of 2 controlling individuals of a company or trust that made a previous election, only the individual’s exemption percentage (see paragraph 160ZZPZI(4)(d)) of the CGT exempt amount specified in the election is to be taken into account under subsection (1).

(1) For the purposes of this Division, actual consideration means consideration disregarding the effect of subsection 160ZD(2).

(2) For the purposes of this Division, if the actual consideration in respect of the disposal of an asset is an obligation to pay money or do any other thing, the actual consideration is taken to be received when the money is paid or the other thing is done.

(1) This section sets out the meaning of controlling individual of (in turn) a company, a fixed trust and any other trust.

Companies

(2) An individual is the controlling individual of a company at a particular time if, at that time, the individual:

(a) is an employee (see subsection (6)) of the company; and

(b) holds all of the legal and equitable interests in shares that carry (between them) the right to exercise at least 50% of the voting power in the company; and

(c) holds all of the legal and equitable interests in shares that carry (between them) the right to receive at least 50% of any dividends that the company may pay; and

(d) holds all of the legal and equitable interests in shares that carry (between them) the right to receive at least 50% of any distribution of capital of the company.

Control of fixed trusts

(3) An individual is the controlling individual of a fixed trust (see subsection (5)) at a particular time if, at that time, the individual:

(a) is an employee (see subsection (6)) of the trust; and

(b) has, for his or her own benefit, entitlements to at least a 50% share of the income of the trust; and

(c) has, for his or her own benefit, entitlements to at least a 50% share of the capital of the trust.

Control of other trusts

(4) An individual is the controlling individual of a trust, other than a fixed trust, at a particular time (the test time) if:

(a) the individual is an employee (see subsection (6)) of the trust at the test time; and

(b) the trust passes the pattern of distributions test, for the test year, in relation to the individual (see section 160ZZPZQ).

Fixed trust

(5) A trust is a fixed trust if persons have entitlements to all of the income and capital of the trust.

Employee

(6) In this section:

employee has the same meaning as in the Superannuation Guarantee (Administration) Act 1992, except that subsection 12(11) of that Act is to be disregarded.

Redeemable shares to be disregarded

(7) For the purposes of subsection (2), a person who, at a particular time, holds a legal or equitable interest in a share:

(a) that is liable to be redeemed; or

(b) that, at the option of the company that issued it, is liable to be redeemed;

is taken not to hold the interest at that time.

(1) A trust passes the pattern of distributions test for the test year (see subsection (2)) in relation to an individual if:

(a) during the test year, the trust made a distribution of income, a distribution of capital or both; and

(b) if the trust made at least one such distribution of income—the trust distributed to the individual, for the individual’s benefit, at least a 50% share of all distributions of income made by the trust during the test year; and

(c) if the trust made at least one such distribution of capital—the trust distributed to the individual, for the individual’s benefit, at least a 50% share of all distributions of capital made by the trust during the test year.

Test year

(2) For the purposes of subsection (1), the test year is:

(a) if the test time concerned (see subsection 160ZZPZP(4)) is in the same year of income as the disposal concerned—the year of income immediately before that year of income; or

(b) in any other case—the year of income in which the test time occurs.

4 Subsection 27A(1)

Insert:

CGT exempt component, in relation to an ETP, means:

(a) if the ETP is covered by subsection 160ZZPZE(4)—the amount of the ETP; or

(b) if the whole or a part of the ETP is taken by subsection 160ZZPZJ(4) to consist solely of a CGT exempt component—the amount of that component.

5 Subsection 27A(1) (paragraph (h) of the definition of eligible termination payment)

Omit “or”.

6 Subsection 27A(1) (after paragraph (j) of the definition of eligible termination payment)

Insert:

or (jaa) an amount that is taken to be an ETP by subsection 160ZZPZE(4);

7 After paragraph 27AA(1)(ca)

Insert:

(cb) the CGT exempt component;

8 Subparagraph 27AA(1)(d)(i) (formula)

Repeal the formula, substitute:

9 Subparagraph 27AA(1)(d)(i) (after the definition of EC)

Insert:

CGT is the CGT exempt component.

10 Subparagraph 27AA(1)(d)(ii)

Repeal the subparagraph, substitute:

(ii) the amount represented by the component:

![]()

in subparagraph (i), reduced by the undeducted contributions;

11 Subsection 27AA(3)

Omit “paragraphs (1)(ca), (d) and (e)”, substitute “paragraphs (1)(ca), (cb), (d) and (e)”.

12 Subsection 27AB(1) (table item 1)

Omit “(fe) or (ff)”, substitute “(fe), (ff) or (jaa)”.

13 After paragraph 27AC(2)(c)

Insert:

(ca) the retained amount of the CGT exempt component is so much of the CGT exempt component as was not rolled‑over; and

14 Subparagraph 27AC(2)(d)(i) (formula)

Repeal the formula, substitute:

15 Subparagraph 27AC(2)(d)(i) (before the definition of Pre‑July 83)

Insert:

Reduced retained amount of ETP is the retained amount of the ETP, reduced by the sum of the amounts listed in subsection (2A).

16 Subparagraph 27AC(2)(d)(ii)

Repeal the subparagraph, substitute:

(ii) the retained amount of the ETP, reduced by the sum of the amounts listed in subsection (2A) and further reduced by the retained amount of the undeducted contributions; and

17 After subparagraph 27AC(2)(e)(ii)

Insert:

(iia) the retained amount of the CGT exempt component of the ETP; and

18 After subsection 27AC(2)

Insert:

Reduced retained amount of ETP

(2A) For the purposes of subparagraphs (2)(d)(i) and (ii), the amounts are as follows:

(a) the retained amount of the concessional component of the ETP;

(b) the retained amount of the post‑June 1994 invalidity component of the ETP;

(c) the retained amount of the CGT exempt component of the ETP;

(d) the non-qualifying component of the ETP;

(e) the excessive component of the ETP.

19 After subparagraph 27CB(1)(b)(i)

Insert:

(ia) a CGT exempt component;

20 After sub-subparagraph 27D(1)(b)(iii)(D)

Insert:

(DA) a CGT exempt component;

21 After paragraph 27D(5)(aa)

Insert:

(ab) the notional CGT exempt component, which is the amount (including a nil amount) specified in the taxpayer’s election under subsection (1) as the extent to which the taxpayer wishes the applied amount to be regarded as consisting of the eligible component covered by sub-subparagraph (1)(b)(iii)(DA);

22 Subparagraph 27D(5)(c)(i) (formula)

Repeal the formula, substitute:

23 Subparagraph 27D(5)(c)(i) (before the definition of Pre‑July 83)

Insert:

Reduced applied amount is the applied amount, reduced by the sum of the amounts listed in subsection (5A).

24 Subparagraph 27D(5)(c)(ii)

Repeal the subparagraph, substitute:

(ii) the applied amount, reduced by the sum of the amounts listed in subsection (5A) and further reduced by the amount of the notional undeducted contributions;

25 After subsection 27D(5)

Insert:

(5A) For the purposes of subparagraphs (5)(c)(i) and (ii), the amounts are as follows:

(a) the notional concessional component;

(b) the notional post‑June 1994 invalidity component;

(c) the notional CGT exempt component.

26 Section 140C

Insert:

CGT exempt component has the same meaning as in section 27A.

27 Section 140C (at the end of the definition of payer)

Add “and, if the benefit is an ETP covered by subsection 160ZZPZE(4), includes the taxpayer mentioned in that subsection”.

28 At the end of section 140H

Add:

; and (g) a reference to the CGT exempt component of the amount rolled over is a reference to so much of the ETP as is taken, because of section 27D, to consist of an amount to which sub-subparagraph 27D(1)(b)(iii)(DA) applies.

29 Subparagraph 140M(1)(a)(iii)

Omit “and”.

30 After subparagraph 140M(1)(a)(iii)

Insert:

(iv) a payer makes an ETP, consisting in whole or in part of a CGT exempt component, in relation to a person; and

31 At the end of section 140M

Add:

ETPs covered by subsection 160ZZPZE(4)—special rules

(6) If an ETP is taken to have been made to a person under subsection 160ZZPZE(4):

(a) the ETP is taken to be an ETP to which subsection (1) of this section applies; and

(b) for the purposes of this section, the person is taken to be the payer of the ETP; and

(c) paragraph (3)(b) of this section does not apply in relation to the ETP; and

(d) the notice mentioned in subsection (1) must be given to the Commissioner before the end of the 14th day of the month after the payment month mentioned in subparagraph (3)(b)(i), or before the end of such further period as the Commissioner allows.

32 At the end of section 140N

Add:

Automatic quotation of TFN for certain CGT exempt ETPs

(4) If:

(a) the ETP is covered by subsection 160ZZPZE(4); and

(b) the person has a tax file number;

the person is taken to have quoted the tax file number to the payer when the ETP was made.

Note: The reason for this rule is that, in such cases, the person and the payer are the same person.

33 At the end of section 140P

Add:

(3) This section does not apply if the benefit is an ETP covered by subsection 160ZZPZE(4).

Note: The reason for this exception is that, in such cases, the recipient and the payer are the same person.

34 At the end of section 140ZH

Add:

; and (d) 100% of the retained amount of the CGT exempt component of the ETP.

35 Subparagraph 140ZJ(1)(a)(ii)

Omit “or”, substitute “and”.

36 After subparagraph 140ZJ(1)(a)(ii)

Add:

(iii) 100% of the retained amount of the CGT exempt component of the ETP; or

37 Paragraph 140ZJ(1)(b)

After “in any other case—”, insert “the sum of 100% of the retained amount of the CGT exempt component of the ETP and”.

38 After section 140ZJ

Insert:

The RBL amount of an ETP covered by subsection 160ZZPZE(4) is 100% of the retained amount of the CGT exempt component of the ETP.

39 Subparagraph 140ZM(a)(iii)

Omit “or”

40 After subparagraph 140ZM(a)(iii)

Add:

(iv) 100% of the retained amount of the CGT exempt component; or

41 After subparagraph 140ZM(b)(iii)

Add:

(iv) 100% of the retained amount of the CGT exempt component;

42 Subsection 140ZO(1) (definition of Undeducted purchase price)

Repeal the definition, substitute:

Undeducted purchase price means the undeducted purchase price of the pension, reduced by so much of the purchase price of the pension as is taken, because of section 27D, to consist of an amount to which sub-subparagraph 27D(1)(b)(iii)(DA) applies.

43 Subsection 140ZO(3) (definition of Excess undeducted purchase price)

Repeal the definition, substitute:

Excess undeducted purchase price means the amount by which the undeducted purchase price of the new pension (as reduced by so much of the purchase price of the pension as is taken, because of section 27D, to consist of an amount to which sub-subparagraph 27D(1)(b)(iii)(DA) applies) exceeds the undeducted purchase price of the old pension (as reduced in the same way).

44 Subsection 7(2)

After “invalidity payment”, insert “or CGT exempt component”.

45 Application

The amendments made by this Schedule apply to disposals of assets on or after 1 July 1997.

1 Paragraph 23(pa)

Omit all the words from and including “where” (first occurring) to “except that—”, substitute:

where:

(i) those rights to mine were acquired by the person before 7.30 pm, by legal time in the Australian Capital Territory, on 20 August 1996; and

(ia) the income was derived before 20 August 2001; and

(ib) the person, on or before 20 August 1996 was a bona fide prospector, that is to say:

(A) a person (other than a company) who has personally carried out the whole or the major part of the field work of prospecting for gold or for the prescribed metal or prescribed mineral, as the case may be, in that area, or has contributed to the expenditure incurred in the work of prospecting and development in that area; or

(B) a company which has itself carried out the whole or the major part of such field work;

except that:

(ii) where the income was derived under a contract for the sale, transfer or assignment of the rights to mine entered into after 7.30 pm, by legal time in the Australian Capital Territory, on 20 August 1996, this paragraph only applies to so much of the income derived as would have been derived if those rights had been sold for their market value at that time; and

2 Subsection 330-60(1)

Omit “If you are a *genuine prospector, your *ordinary income (for the 1997-98 income year or a later income year)”, substitute “Your *ordinary income”.

3 Subsection 330-60(1)

After “income tax”, insert:

if:

(d) you acquired those rights before 7.30 pm, by legal time in the Australian Capital Territory, on 20 August 1996; and

(e) you *derive the *ordinary income before 20 August 2001; and

(f) you were a *genuine prospector on or before 20 August 1996, and you are one when you derive the ordinary income.

4 After subsection 330-60(1)

Insert:

(1A) If you *derived the *ordinary income under a contract for the sale, transfer or assignment of the rights entered into after 7.30 pm, by legal time in the Australian Capital Territory, on 20 August 1996, the exemption applies only to:

(a) so much of the ordinary income as you would have derived if those rights had been sold for their market value at that time;

reduced by:

(b) any amounts you incurred before that time that you have deducted or can deduct for an earlier income year under Division 10 of Part III of the Income Tax Assessment Act 1936 in respect of expenditure on exploration or prospecting (within the meaning of section 122J or 122JF of that Act) in that area.

5 Subsection 330-60(2)

Omit “The exemption”, substitute “If subsection (1A) does not apply, the exemption”.

6 Paragraph 330-60(2)(b)

Omit “section 122J”, substitute “Division 10 of Part III”.

7 Paragraph 330-60(2)(b)

Omit “that section”, substitute “section 122J or 122JF of that Act”.

1 Subsection 23AF(17A) (at the end of the definition of notional gross tax)

Add:

and (c) Division 5 of Part II of the Income Tax Rates Act 1986 did not apply in relation to the taxpayer.

2 After subsection 23AF(17C)

Insert:

Family tax initiative adjustment

(17D) If:

(a) the income of a taxpayer of a year of income consists of an amount that is exempt from tax under this section; and

(b) apart from this subsection, section 20C, 20D or 20E of the Income Tax Rates Act 1986 would apply in relation to the taxpayer;

then:

(c) those sections of the Income Tax Rates 1986 do not apply to the taxpayer in relation to the year; and

(d) the amount of tax payable by the person is reduced by the amount worked out using the formula:

![]()

(17E) In subsection (17D):

lowest marginal rate means the lowest rate set out in column 2 of the table in clause 1 of Part I of Schedule 7 to the Income Tax Rates Act 1986.

tax free threshold increase means the sum of the amounts by which, subject to Division 5 of Part II of the Income Tax Rates Act 1986, the amount of $5,400 set out in column 1 of the table in clause 1 of Part I of Schedule 7 to that Act would be taken to be increased in relation to the taxpayer in respect of the year of income under sections 20C and 20D of that Act if those sections applied to the taxpayer.

3 Subsection 23AG(3) (at the end of the definition of notional gross tax)

Add:

and (c) Division 5 of Part II of the Income Tax Rates Act 1986 did not apply in relation to the taxpayer.

4 After subsection 23AG(5)

Insert:

Family tax initiative adjustment

(5A) If:

(a) the income of a taxpayer of a year of income consists of an amount that is exempt from tax under this section; and

(b) apart from this subsection, section 20C, 20D or 20E of the Income Tax Rates Act 1986 would apply in relation to the taxpayer;

then:

(c) those sections of the Income Tax Rates Act 1986 do not apply to the taxpayer in relation to the year; and

(d) the amount of tax payable by the person is reduced by the amount worked out using the formula:

![]()

(5B) In subsection (5A):

lowest marginal rate means the lowest rate set out in column 2 of the table in clause 1 of Part I of Schedule 7 to the Income Tax Rates Act 1986.

tax free threshold increase means the sum of the amounts by which, subject to Division 5 of Part II of the Income Tax Rates Act 1986, the amount of $5,400 set out in column 1 of the table in clause 1 of Part I of Schedule 7 to that Act would be taken to be increased in relation to the taxpayer in respect of the year of income under sections 20C and 20D of that Act if those sections applied to the taxpayer.

5 Application

The amendments made by this Schedule apply in relation to the 1996‑97 year of income and to all later years of income.

1 After section 160AQCN

Insert:

(1) This section applies if:

(a) at a particular time (the transition time), all of the income of a company (the exempt company) is wholly exempt from income tax; and

(b) at the transition time, another company (the former subsidiary) ceases to be a subsidiary (as defined in section 57-125 of Schedule 2D) of the exempt company; and

(c) immediately before the transition time, the former subsidiary was not itself wholly exempt from income tax; and

(d) immediately before the transition time, all of the income of every company that beneficially owned shares in the former subsidiary was wholly exempt from income tax.

Note: If the exempt company itself ceases to be wholly exempt from income tax, it and its subsidiaries will be covered by similar rules under Schedule 2D (treatment of tax exempt entities that become taxable).

Cancellation of surplus

(2) Subject to subsection (4), if, immediately before the transition time, the former subsidiary has a class A franking surplus, a class B franking surplus or a class C franking surplus, then the surplus is reduced to nil at the transition time.

Cancellation of credit/debit

(3) Subject to subsection (4), if:

(a) at any time after the transition time, there arises a franking credit or a franking debit of the former subsidiary; and

(b) the franking credit or franking debit is to any extent attributable to the period, or to an event taking place, before the transition time;

the franking credit or franking debit is to that extent taken not to have arisen.

Cases where subsections (2) and (3) do not apply

(4) If:

(a) one or more class A franking debits, class B franking debits or class C franking debits of the former subsidiary arise after the transition time; and

(b) any of the debits is to an extent (the amount of which is the pre-transition time component of the debit) attributable to the period, or to an event taking place, before the transition time; and

(c) immediately before the transition time:

(i) there was a class A franking surplus, class B franking surplus or class C franking surplus of the former subsidiary that was less than the total of the pre-transition time components of all of the debits of that class; or

(ii) there was no class A franking surplus, there was no class B franking surplus or there was no class C franking surplus of the former subsidiary;

then:

(d) in a case covered by subparagraph (c)(i)—subsection (2) does not apply to the surplus or surpluses concerned; and

(e) in any case—subsection (3) does not apply to the debits of the class or classes concerned.

States and Territories

(5) The reference in paragraph (1)(a) to a company all of whose income is wholly exempt from income tax includes a reference to a State or Territory.

2 At the end of Schedule 2D

Add:

Cancellation of surplus

(1) Subject to subsections (3) and (4), if, immediately before the transition time, the transition taxpayer or a subsidiary (see section 57‑125) of the transition taxpayer has a class A franking surplus, a class B franking surplus or a class C franking surplus, then the surplus is reduced to nil at the transition time.

Cancellation of credit/debit

(2) Subject to subsections (3) and (4), if:

(a) at any time after the transition time, there arises a franking credit or a franking debit of the transition taxpayer or of a subsidiary of the transition taxpayer; and

(b) the franking credit or franking debit is to any extent attributable to a period, or to an event taking place, before the transition time;

the franking credit or franking debit is to that extent taken not to have arisen.

Cases where subsections (1) and (2) do not apply to the transition taxpayer

(3) If:

(a) one or more class A franking debits, class B franking debits or class C franking debits of the transition taxpayer arise after the transition time; and

(b) any of the debits is to an extent (the amount of which is the pre-transition time component of the debit) attributable to the period, or to an event taking place, before the transition time; and

(c) immediately before the transition time:

(i) there was a class A franking surplus, class B franking surplus or class C franking surplus of the transition taxpayer that was less than the total of the pre-transition time components of all of the debits of that class; or

(ii) there was no class A franking surplus, there was no class B franking surplus or there was no class C franking surplus of the transition taxpayer;

then:

(d) in a case covered by subparagraph (c)(i)—subsection (1) does not apply to the surplus or surpluses concerned; and

(e) in any case—subsection (2) does not apply to the debits of the class or classes concerned.

Cases where subsections (1) and (2) do not apply to a subsidiary

(4) If:

(a) one or more class A franking debits, class B franking debits or class C franking debits of a subsidiary of the transition taxpayer arise after the transition time; and

(b) any of the debits is to an extent (the amount of which is the pre-transition time component of the debit) attributable to the period, or to an event taking place, before the transition time; and

(c) immediately before the transition time:

(i) there was a class A franking surplus, class B franking surplus or class C franking surplus of the subsidiary that was less than the total of the pre-transition time components of all of the debits of that class; or

(ii) there was no class A franking surplus, there was no class B franking surplus or there was no class C franking surplus of the subsidiary;

then:

(d) in a case covered by subparagraph (c)(i)—subsection (1) does not apply to the surplus or surpluses concerned; and

(e) in any case—subsection (2) does not apply to the debits of the class or classes concerned.

Definitions

(5) In this section, the following expressions have the same meaning as in Part IIIAA:

class A franking debit |

class A franking surplus |

class B franking debit |

class B franking surplus |

class C franking debit |

class C franking surplus |

franking credit |

franking debit. |

(1) A company (the subsidiary company) is a subsidiary of another company (the holding company) if all the shares in the subsidiary company are beneficially owned by:

(a) the holding company; or

(b) one or more subsidiaries of the holding company; or

(c) the holding company and one or more subsidiaries of the holding company.

(2) A company (other than the subsidiary company) is a subsidiary of the holding company if, and only if:

(a) it is a subsidiary of the holding company; or

(b) it is a subsidiary of a subsidiary of the holding company;

because of any other application or applications of this section.

3 Application

The amendments made by Part 1 apply if the transition time is after 2 July 1995.

1 Paragraph 160ZZQ(14)(b), subparagraph 160ZZQ(15)(b)(i) and paragraphs 160ZZQ(18)(b) and (20)(b)

Omit “12 months”, substitute “2 years”.

2 Subsection 160ZZQ(17)

Omit “subsection (21)”, substitute “subsections (20A) and (21)”.

3 Paragraph 160ZZQ(17)(a)

Omit all the words after “is disposed of”.

4 After paragraph 160ZZQ(17)(a)

Insert:

(aa) the disposal is not covered by subsection (13), (13A) or (14);

5 Subparagraph 160ZZQ(17)(b)(i)

Omit “portion only”, substitute “the whole or a portion”.

6 Subparagraphs 160ZZQ(17)(b)(ii) and (iii)

Omit “part only”, substitute “the whole or part”.

7 Subsection 160ZZQ(17) (formula, definition of B)

Repeal the definition, substitute:

B is the sum of the following:

(d) the number of days (if any) in the relevant period during which the taxpayer owned the dwelling (disregarding section 160X), but the dwelling was not the taxpayer’s sole or principal residence;

(e) if the deceased person acquired the dwelling on or after 20 September 1985—the number of days (if any) in the period during which the deceased person owned the dwelling, but the dwelling was not the deceased person’s sole or principal residence;

(f) the number of days (if any) in the period mentioned in paragraph (13)(d) during which the dwelling was not the sole or principal residence of any of the persons mentioned in subparagraphs (13)(d)(i) and (ii).

8 After paragraph 160ZZQ(17A)(a)

Insert:

(aa) the disposal is not covered by subsection (13), (13A) or (14);

9 Subparagraphs 160ZZQ(17A)(b)(i) and (ii)

Omit “part only”, substitute “the whole or part”.

10 Subsection 160ZZQ(17A) (formula, definition of B)

Repeal the definition, substitute:

B is the sum of the following:

(d) the number of days (if any) in the period from the deceased person’s death to the disposal of the dwelling during which the dwelling was not the taxpayer’s sole or principal residence;

(e) if the deceased person acquired the dwelling on or after 20 September 1985—the number of days (if any) in the period during which the deceased person owned the dwelling, but the dwelling was not the deceased person’s sole or principal residence.

11 After paragraph 160ZZQ(19)(a)

Insert:

(aa) the disposal is not covered by subsection (15);

12 Subparagraphs 160ZZQ(19)(b)(i) and (ii)

Omit “part only”, substitute “the whole or part”.

13 Subsection 160ZZQ(19) (formula, definition of B)

Repeal the definition, substitute:

B is the sum of the following:

(d) the number of days (if any) in the period mentioned in subparagraph (15)(b)(ii) during which the dwelling was not the sole or principal residence of any of the persons mentioned in sub-subparagraphs (15)(b)(ii)(A) and (B);

(e) if the deceased person acquired the dwelling on or after 20 September 1985—the number of days (if any) in the period during which the deceased person owned the dwelling, but the dwelling was not the deceased person’s sole or principal residence.

14 Subsection 160ZZQ(20A)

After “Where”, insert “both subsections (17) and (18),”.

15 Paragraph 160X(5)(a)

Omit “if the asset was acquired by the deceased person before 20 September 1985—the asset”, substitute:

if:

(i) the deceased person acquired the asset before 20 September 1985; or

(ii) the asset is a dwelling that was, immediately before the person’s death, the person’s sole or principal residence for the purposes of section 160ZZQ and was not, for the purposes of that section, then being used for the purpose of gaining or producing assessable income;

the asset.

16 At the end of paragraph 160X(5)(a)

Add:

Note: In certain cases, a dwelling may be taken to have been a person’s sole or principal residence, and any use for the purpose of gaining or producing assessable income may be disregarded, for the purposes of section 160ZZQ: see subsection 160ZZQ(11).

17 Paragraph 160X(5)(b)

Omit “if the asset was acquired by the deceased person on or after 20 September 1985,”, substitute “in any other case—”.

18 Paragraphs 160ZZQ(13)(c), (13A)(c), (14)(c) and (15)(c)

Omit “throughout the period during which the dwelling was owned by”, substitute “immediately before the death of”.

19 Subparagraph 160ZZQ(17)(b)(ii)

Omit “referred to in that paragraph” (last occurring), substitute “during which the deceased person owned the dwelling”.

20 At the end of subsection 160ZZQ(17)

Add:

Note: The number of days worked out under paragraphs (e) and (j) is modified in some cases: see subsection (20AA).

21 Subparagraph 160ZZQ(17A)(b)(ii)

Omit “referred to in that paragraph” (last occurring), substitute “during which the deceased person owned the dwelling”.

22 At the end of subsection 160ZZQ(17A)

Add:

Note: The number of days worked out under paragraphs (e) and (h) is modified in some cases: see subsection (20AA).

23 Subsection 160ZZQ(18)

Omit “referred to in paragraph (14)(c)” (wherever occurring), substitute “during which the deceased person owned the dwelling”.

24 Subparagraph 160ZZQ(19)(b)(ii)

Omit “referred to in that paragraph”, substitute “during which the deceased person owned the dwelling”.

25 At the end of subsection 160ZZQ(19)

Add:

Note: The number of days worked out under paragraphs (e) and (h) is modified in some cases: see subsection (20AA).

26 Subsection 160ZZQ(20)

Omit “referred to in paragraph (15)(c)” (wherever occurring), substitute “during which the deceased person owned the dwelling”.

27 After subsection 160ZZQ(20A)

Insert:

(20AA) For the purposes of subsections (17), (17A) and (19), if, immediately before the death of the deceased person concerned, the dwelling concerned:

(a) was the deceased person’s sole or principal residence; and

(b) was not being used for the purpose of gaining or producing assessable income;

then:

(c) the number of days mentioned in paragraphs (17)(e), (17A)(e) or (19)(e) (as appropriate) is taken to be nil; and

(d) the number of days mentioned in paragraphs (17)(j), (17A)(h) or (19)(h) (as appropriate) is worked out from and including the date of the death, instead of the date on which the deceased person acquired the dwelling.

28 After paragraph 160ZZQ(20B)(b)

Insert:

and (ba) subparagraph 160X(5)(a)(ii) does not apply to the taxpayer’s acquisition of the dwelling;

29 At the end of subsection 160ZZQ(21)

Add:

; and (f) if subsection (13), (13A), (14) or (15) would have applied in respect of the disposal—the extent to which, and the period for which, the dwelling was used for the purpose of gaining or producing assessable income in the period during which both:

(i) the deceased person mentioned in whichever of those subsections would have applied owned the dwelling; and

(ii) the dwelling was the deceased person’s sole or principal residence.

Note: This paragraph means that, in determining the amount of the capital gain or capital loss, the Commissioner must have regard to certain use of the dwelling for the purpose of gaining or producing assessable income before the death. However, this rule is subject to subsection (22).

30 At the end of section 160ZZQ

Add:

(22) If:

(a) apart from subsection (21), subsection (13), (13A), (14), (15), (17), (17A), (18), (19), (20) or (20C) would apply in respect of the disposal of a dwelling; and

(b) during all or part of the period (the exemption period) mentioned in paragraph (21)(b), the dwelling was the sole or principal residence of the deceased person mentioned in whichever of those subsections would have applied; and

(c) immediately before the deceased person’s death, the dwelling:

(i) was the deceased person’s sole or principal residence; and

(ii) was not being used for the purpose of gaining or producing assessable income;

then:

(d) in having regard to the matter mentioned in paragraph (21)(e), the Commissioner must disregard so much of the exemption period as occurred before the death; and

(e) paragraph (21)(f) does not apply in respect of the disposal.

Note: This means that, in determining the amount of the capital gain or capital loss under subsection (21), the Commissioner must disregard any use of the dwelling before the death for the purpose of gaining or producing assessable income.

(23) To avoid doubt, for the purposes of subsection (21), a period may consist of a particular instant in time.

31 Paragraph 160ZZQ(11)(a)

After “the taxpayer”, insert “(disregarding subsection (20D))”.

32 Subsection 160ZZQ(11)

Omit “(other than this subsection)”, substitute “(other than this subsection and subsection (20D))”.

33 After subsection 160ZZQ(20C)

Insert:

(20D) Despite subparagraphs (20C)(a)(ii) and (iii) and subsection 160X(5), if:

(a) a taxpayer acquires a dwelling on or after 20 September 1985; and

(b) for the first time (the first income time) since the acquisition, the dwelling begins to be used for the purpose of gaining or producing assessable income; and

(c) assuming that the taxpayer had disposed of the dwelling immediately before the first income time, the disposal would have been covered by any of the following provisions:

(i) subsection (12) or (13A);

(ii) subsection (13);

(iii) if subparagraph (15)(b)(ii) would then have applied to the dwelling—subsection (15);

(iv) subparagraph (20C)(b)(i); and

(d) the taxpayer later disposes of the dwelling; and

(e) that later disposal is not covered by:

(i) subsection (14); or

(ii) if subparagraph (15)(b)(i) applies to the disposal—subsection (15);

then:

(f) for the purposes of this Part, the taxpayer is taken to have acquired the dwelling at the first income time for a consideration equal to its market value at that time; and

(g) for the purposes of this section, the taxpayer is taken not to have acquired the dwelling as a beneficiary in, or a trustee of, the estate of a deceased person; and

(h) if subparagraph (c)(ii) or (iii) of this subsection applies—throughout the period mentioned in paragraph (13)(d) or subparagraph (15)(b)(ii) (as appropriate) during which the dwelling was the sole or principal residence of any one or more of the following:

(i) the person who was, immediately before the deceased person’s death, the deceased person’s spouse;

(ii) a person who, under the deceased person’s will, had a right to occupy the dwelling;

the dwelling is taken, for the purposes of this section, to have been the taxpayer’s sole or principal residence.

Note: This means that, in applying this Part to the disposal, the period before the first income time (including any time when a deceased person owned the dwelling ) is to be disregarded. Subsection (12) or (16) might apply to the disposal (subject to subsection (21), which deals with use of the dwelling for the purpose of gaining or producing assessable income).

34 Application

(1) The amendments made by Divisions 1 and 2 of Part 1 apply to disposals of dwellings after 7.30 pm, by legal time in the Australian Capital Territory, on 20 August 1996.

(2) The amendments made by Division 3 of Part 1 apply to assets that pass to the legal personal representative of a deceased person, to a beneficiary in the estate of a deceased person or to a trustee of the estate of a deceased person, after 7.30 pm, by legal time in the Australian Capital Territory, on 20 August 1996.

(3) The amendments made by Division 4 of Part 1 apply to a dwelling owned by a taxpayer if:

(a) for the first time since the taxpayer acquired the dwelling, it is used for the purpose of gaining or producing assessable income; and

(b) that time is after 7.30 pm, by legal time in the Australian Capital Territory, on 20 August 1996.

1 Subsection 6(1)

Insert:

firearms surrender arrangements means:

(a) Commonwealth, State or Territory legislation; or

(b) administrative arrangements of a State or a Territory;

implementing the agreement arising from the meeting of the Police Ministers held on 10 May 1996 concerning the surrender of prohibited firearms.

2 After paragraph 23(jc)

Insert:

(jd) the income derived by way of compensation under firearms surrender arrangements for any loss of business;

Note: Firearms surrender arrangements has the meaning given by subsection 6(1).

3 After subsection 51(2A)

Insert:

(2B) Where a taxpayer derives assessable income as a result of the surrender of an item of trading stock under firearms surrender arrangements, the excess, if any, of the amount of that income over the acquisition cost is an allowable deduction in the year of income in which that income is derived.

Note: Firearms surrender arrangements has the meaning given by subsection 6(1).

4 After subsection 53I(2)

Insert:

(3) Also, the provisions mentioned in subsection (1) continue to apply for the operation of subsection 59(2AAA) for the 1997-98 year of income and for later years of income in which proceeds are derived as a result of firearms surrender arrangements.

Note: Firearms surrender arrangements has the meaning given by subsection 6(1).

5 After subsection 59(2)

Insert:

(2AAA) For the purposes of the application of subsection (2), the taxpayer’s assessable income does not include any amount by which consideration receivable under firearms surrender arrangements exceeds the depreciated value of a surrendered item of property.

Note: Firearms surrender arrangements has the meaning given by subsection 6(1).

6 Subsection 79E(12) (definition of exempt income)

After “to which”, insert “paragraph 23(jd),”.

7 Subsection 79E(12) (definition of exempt income)

After “23AK”, insert “, subsection 59(2AAA)”.

8 After subsection 160Z(6)

Insert:

(6A) Nothing in this Part operates to deem a capital gain to have accrued to a taxpayer during the year of income where the relevant disposal related to an asset for which the taxpayer received consideration under firearms surrender arrangements.

Note: Firearms surrender arrangements has the meaning given by subsection 6(1).

9 Application

The amendments made by this Part apply in respect of years of income in which proceeds are derived as a result of firearms surrender arrangements.

Note: Firearms surrender arrangements has the meaning given by subsection 6(1) of the Income Tax Assessment Act 1936.

10 Section 12-5 (after table item headed “financial arrangements”)

Insert:

firearms surrender payments |

|

.................................... | 51(2B) |

11 Before paragraph 36-20(3)(a)

Insert:

(aa) paragraph 23(jd) (Income derived by way of compensation under firearms surrender arrangements).

12 After paragraph 36-20(3)(e)

Insert:

(ea) subsection 59(2AAA) (Excess of consideration over depreciated value of property surrendered under firearms surrender arrangements);

13 Application

The amendments made by this Part apply in respect of years of income in which proceeds are derived as a result of firearms surrender arrangements.

Note: Firearms surrender arrangements has the meaning given by subsection 6(1) of the Income Tax Assessment Act 1936.

1 At the end of Division 13 of Part III

Add:

A benefit that would, apart from this section, be a remote area housing fringe benefit is an exempt benefit if:

(a) the benefit is provided by an employer who is, for the purposes of the Income Tax Assessment Act 1936, carrying on a business of primary production; and

(b) the benefit is provided to an employee of the employer; and

(c) the employee is employed in that business of primary production; and

(d) the benefit is provided in respect of that employment.

2 Subsection 59(1)

After “remote area housing fringe benefit”, insert “, or a benefit that apart from section 58ZA would be a remote area housing fringe benefit,”.

3 Application

The amendments made by this Schedule apply to assessments for the FBT year beginning on 1 April 1997 and for all later FBT years.

1 At the end of subsection 54AA(1)

Add:

; and (f) section 54AB does not apply.

2 After section 54AA

Insert:

(1) This section applies if:

(a) a taxpayer (the lessor) enters into a lease with another person (the lessee) under which a right to use a unit of property that is plant or articles within the meaning of section 54 is granted to the lessee; and

(b) the property is a fixture on the land of a person other than the lessor and therefore the lessor is not the owner of the property; and

(c) if the property were not a fixture, the lessor would be the owner of the property; and

(d) under sections 54AC and 54AD, the lessor is an eligible lessor in relation to the property.

(2) If this section applies, the provisions of this Act relating to depreciation apply as if the lessor were the owner of the property instead of any other person.

(3) Also, section 51AD and Division 16D apply in relation to property to which this section applies as if the lessor were the owner of the property instead of any other person.

(4) For the purposes of this section and sections 54AC and 54AD:

lease means:

(a) any arrangement to let a unit of property (other than realty) on hire under which a right to use the property is granted by the owner to another person for a monetary or other consideration; or

(b) a renewal of such an arrangement;

but does not include a hire purchase agreement.

Right of removal

(1) Where a unit of property is a fixture on land owned by the lessee of the property, then, for the purposes of subsection 54AB(1), the lessor is an eligible lessor in relation to that property if:

(a) the lessor has a right, in addition to any other right, to sever and remove the property from the land in the event of default under, or termination of, the lease (a right to remove); and

(b) the property can be removed without causing substantial damage to the property or to the land.

Effective right of removal

(2) Where the property is a fixture on land owned by a person other than the lessee, then, for the purposes of subsection 54AB(1), the lessor is an eligible lessor in relation to the property if:

(a) the lessee has a right to sever and remove the property from the land; and

(b) the property can be removed without causing substantial damage to the property or to the land; and

(c) under the lease, the lessor has a right against the lessee to recover the property (an effective right to remove).

Lessor not an eligible lessor if right to remove, or effective right to remove, is lost

(3) The lessor is not an eligible lessor in relation to the property if:

(a) although the lessor has a right to remove, or an effective right to remove, the property, the lease expires or is otherwise terminated without the lessor exercising that right; or

(b) there is an event of default under the lease and the lessor ceases to have a right to remove, or an effective right to remove, the property; or

(c) the lessor disposes of his or her interest in the lease, including the residual interest in the property; or

(d) the lessee discharges his or her obligations under the lease and the property is not returned to the lessor; or

(e) the property is lost or destroyed.

(1) Subject to subsection (2), a lessor is not an eligible lessor in relation to a unit of property for the purposes of subsection 54AB(1) if, at any time before the lease was entered into, the lessee or an associate of the lessee owned the property and used it or held it for use.

(2) Subsection (1) does not apply if:

(a) the property was first owned and used or held for use by the lessee or an associate of the lessee no more than 6 months before the lessor acquired the property; and

(b) the lessor acquired the property from the lessee or an associate of the lessee; and

(c) the property was not a fixture at the time that it was first owned and used or held for use by the lessee or an associate of the lessee; and

(d) at the time the property was first owned and used or held for use by the lessee or an associate of the lessee, there was an arrangement in existence providing for the property to be sold to the lessor and then leased to the lessee.

(3) For the purposes of subsections (1) and (2), a person (the seller) is taken to have sold property and another person (the purchaser) is taken to have acquired property where the seller purports to sell the property to the purchaser but does not because the property is a fixture on land.

(4) If the conditions in subsection (2) are satisfied, the cost of the property to the lessor, for the purposes of working out the property’s depreciated value under section 62, is taken to be the lesser of:

(a) the sum of:

(i) the amount that would have been the depreciated value of the property of the lessee or an associate of the lessee at the time the lessor acquired it; and

(ii) any amount included in the assessable income of the lessee or associate under section 59 as a result of the sale; or

(b) the consideration paid by the lessor for the property.

(5) For the purposes of this section:

associate has the same meaning as in section 318.

(1) A lessor who is not an eligible lessor in relation to a unit of property under section 54AB because one or more of the conditions in subsection 54AC(3) is satisfied, is taken to have disposed of the property for the purposes of section 59 or 59AA for the amount of consideration set out in this section.

(2) If:

(a) the lease expires or is otherwise terminated without the lessor exercising his or her right to remove, or effective right to remove, the property; or

(b) there is an event of default under the lease and the lessor ceases to have a right to remove, or an effective right to remove, the property; or

(c) the lessee discharges his or her obligations under the lease and the property is not returned to the lessor;

the lessor is taken to have disposed of the property for a consideration equal to:

(d) if the parties to the lease are dealing at arm’s length and there is any termination or residual amount received or receivable under the lease in respect of the property—that termination or residual amount; or

(e) if the parties to the lease are dealing at arm’s length and there is no termination or residual amount received or receivable under the lease in respect of the property—any amount received or receivable by way of compensation in lieu of recovery of the property; or

(f) if the parties to the lease are not dealing at arm’s length—the market value of the property immediately before the time of disposal referred to in paragraph (a), (b) or (c) worked out as if it were removed from the land.

(3) If the lessor disposes of his or her interest in the lease including the residual interest in the property, the lessor is taken to have disposed of the property for a consideration equal to:

(a) if the parties to the disposal are dealing at arm’s length—the part of the disposal price that is reasonably attributable to the property; or

(b) if the parties to the disposal are not dealing at arm’s length—the market value immediately before the time of disposal worked out as if the property were removed from the land.

(4) If the property is lost or destroyed, the lessor is taken to have disposed of the property for the sum of any amounts received or receivable in relation to its loss or destruction.

3 Application

The amendments made by this Schedule apply in relation to units of property first used on or after 1 July 1996 for the purposes of producing assessable income of the lessor of the property.

1 Paragraph 27(1)(a)

Omit “65”, substitute “70”.

2 Application

The amendment made by this Part applies in relation to the 1997-98 year and all later years.

3 Section 30

Omit “65”, substitute “70”.

4 Application

The amendment made by this Part applies to deposits made for a period of employment where:

(a) the deposit is made on or after 1 July 1997; and

(b) the period of employment to which the deposit relates starts on or after 1 July 1997.

1 After Subdivision AAC of Division 17 of Part III

Insert:

(1) This section applies if the following conditions are satisfied in relation to a taxpayer and in relation to a year of income of the taxpayer:

(a) the taxpayer has a spouse in relation to whom he or she makes one or more eligible spouse contributions; and

(b) the taxpayer and his or her spouse are residents at the time that the taxpayer makes the eligible spouse contribution; and

(c) the spouse’s assessable income is less than $13,800.

Note: For the meaning of eligible spouse contribution, see section 159TC.

(2) The taxpayer is entitled to a rebate of tax in the taxpayer’s assessment for the year of income equal to 18% of the lesser of:

(a) $3,000 reduced by $1 for every $1 of the amount (if any) by which the spouse’s assessable income of that year exceeds $10,800; or

(b) the total of the eligible spouse contributions made in relation to the spouse by the taxpayer in that year.

If, in relation to a year of income, a taxpayer qualifies for the rebate under section 159T in respect of more than one spouse, the total of rebates under that section for which the taxpayer qualifies is equal to the lesser of:

(a) the sum of the rebate amounts for which the taxpayer qualifies in relation to each spouse; or

(b) $540.

A taxpayer who qualifies for a rebate under section 159T in respect of an eligible spouse may quote the tax file number of the spouse. The taxpayer must obtain the consent of the spouse to the quotation.

For the purposes of this Subdivision:

complying superannuation fund has the same meaning as in Part IX.

dependant has the same meaning as in the Superannuation Industry (Supervision) Act 1993.

eligible spouse contributions, in relation to a taxpayer, means contributions made by the taxpayer where:

(a) the contributions are made in relation to a person who is the taxpayer’s spouse at the time those contributions are made; and

(b) the contributions are made to a fund that is a complying superannuation fund in relation to the year of income of the fund in which the contributions are made; and

(c) the contributions are made to obtain superannuation benefits for the spouse or, in the event of the death of the spouse, for dependants of the spouse; and