Taxation Laws Amendment Act (No. 1) 1998

No. 16, 1998

Taxation Laws Amendment Act (No. 1) 1998

No. 16, 1998

Taxation Laws Amendment Act (No. 1) 1998

No. 16, 1998

An Act to amend the law relating to taxation, and for related purposes

Contents

1 Short title..................................1

2 Commencement..............................1

3 Schedule(s).................................2

4 Amendment of income tax assessments.................2

Schedule 1—Capital gains tax roll‑over relief for small businesses 3

Part 1—Amendments relating to disposals of shares or units in unit trusts 3

Income Tax Assessment Act 1936 3

Part 2—Technical amendments 16

Income Tax Assessment Act 1936 16

Schedule 2—Amendment of the Sales Tax Assessment Act 1992 25

Schedule 3—Land transport facilities 48

Part 1—Insertion of new Division 396 48

Income Tax Assessment Act 1997 48

Part 2—Other amendments 63

Income Tax Assessment Act 1997 63

Part 3—Transitional and application provisions 66

Schedule 4—Removing exemption for CRAFT Scheme payments 68

Income Tax Assessment Act 1997 68

Schedule 5—Technical amendments of the Income Tax Assessment Act 1997 69

Schedule 6—Technical amendments of the Income Tax Assessment Act 1936 76

Schedule 7—Technical amendments of the Income Tax (Transitional Provisions) Act 1997 76

Schedule 8—Technical amendments of the Income Tax (Consequential Amendments) Act 1997 76

Schedule 9—Technical amendments of other Acts 76

Financial Corporations (Transfer of Assets and Liabilities) Act 1993 76

Schedule 10—“Catch‑up” amendments 76

Part 1—Amendment of the Income Tax Assessment Act 1997 76

Part 2—Amendment of the Income Tax Assessment Act 1936 76

Part 3—Amendment of the Airports (Transitional) Act 1996 76

Part 4—Amendment of the Civil Aviation Legislation Amendment Act 1995 76

Part 5—Amendment of the Federal Airports Corporation Act 1986 76

Schedule 11—Amendments to improve further the readability of the Income Tax Assessment Act 1997 76

Part 1—Asterisking in operative provisions 76

Part 2—Removing asterisks from Guide material 76

Part 3—Removing asterisks from non‑operative material outside Guides 76

Part 4—Making Guide status more obvious 76

Part 5—Application of amendments made by this Schedule 76

Taxation Laws Amendment Act (No. 1) 1998

No. 16, 1998

An Act to amend the law relating to taxation, and for related purposes

[Assented to 16 April 1998]

The Parliament of Australia enacts:

This Act may be cited as the Taxation Laws Amendment Act (No. 1) 1998.

(1) Subject to subsection (2), this Act commences on the day on which it receives the Royal Assent.

(2) Items 35, 46, 47, 50, 51 and 54 of Schedule 1 commence immediately after the commencement of item 17 of that Schedule.

(2) Schedule 8 is taken to have commenced immediately before 1 July 1997.

Subject to section 2, each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

4 Amendment of income tax assessments

Section 170 of the Income Tax Assessment Act 1936 does not prevent the amendment of an assessment made before the commencement of this section for the purposes of giving effect to this Act.

Schedule 1—Capital gains tax roll‑over relief for small businesses

Part 1—Amendments relating to disposals of shares or units in unit trusts

Income Tax Assessment Act 1936

1 Division 17A of Part IIIA (heading)

Repeal the heading, substitute:

Division 17A—Roll‑over relief for certain disposals of assets related to small businesses

2 Subsection 160ZZPK(1)

Insert:

approved asset has the meaning given by subsections 160ZZPT(1AA) to (1AC).

3 Subsection 160ZZPK(1)

Insert:

controlling individual has the meaning given by section 160ZZPNA.

4 Subsection 160ZZPK(1) (at the end of the definition of gross non‑goodwill roll‑over amount)

Add “or (3A)”.

5 Subsection 160ZZPK(1)

Insert:

resident unit trust has the same meaning as in section 102Q.

6 Subsection 160ZZPK(1) (at the end of the definition of roll‑over asset)

Add “, (8) or (9)”.

7 Before paragraph 160ZZPL(7)(a)

Insert:

(aa) the asset is not a share in a company or a unit in a unit trust; and

8 At the end of section 160ZZPL

Add:

(8) A share in a company is a roll‑over asset in respect of a taxpayer who is an individual (other than an individual acting as a trustee) in respect of a year of income if:

(a) the company is, in respect of the year of income, a private company that is a resident; and

(b) the share is disposed of by the taxpayer in the year of income; and

(c) the taxpayer is the controlling individual of the company at the disposal test time; and

(d) the threshold criteria set out in section 160ZZPP are complied with at the disposal test time.

(9) A unit in a unit trust is a roll‑over asset in respect of a taxpayer who is an individual (other than an individual acting as a trustee) in respect of a year of income if:

(a) the unit trust is a resident unit trust, but is not a publicly traded unit trust, in respect of the year of income; and

(b) the unit is disposed of by the taxpayer in the year of income; and

(c) the taxpayer is the controlling individual of the trust at the disposal test time; and

(d) the threshold criteria set out in section 160ZZPP are complied with at the disposal test time.

9 At the end of Subdivision A of Division 17A of Part IIIA

Add:

160ZZPNA Controlling individual

Explanation of section

(1) This section sets out the meaning of controlling individual of a company and of a unit trust.

Control of companies

(2) An individual is the controlling individual of a company at a particular time if, at that time, the individual:

(a) is a director and an employee (see subsection (4)) of the company; and

(b) holds all of the legal and equitable interests in shares that carry (between them) the right to exercise at least 50% of the voting power in the company; and

(c) holds all of the legal and equitable interests in shares that carry (between them) the right to receive at least 50% of any dividends that the company may pay; and

(d) holds all of the legal and equitable interests in shares that carry (between them) the right to receive at least 50% of any distribution of capital of the company.

Control of unit trusts

(3) An individual is the controlling individual of a unit trust at a particular time if, at that time, the individual:

(a) is an employee (see subsection (4)) of the trust; and

(b) has, for his or her benefit, entitlements to at least a 50% share of the income of the trust; and

(c) has, for his or her benefit, entitlements to at least a 50% share of the capital of the trust.

Employee

(4) In this section:

employee has the same meaning as in the Superannuation Guarantee (Administration) Act 1992, except that subsection 12(11) of that Act is to be disregarded.

Redeemable shares to be disregarded

(5) For the purposes of subsection (2), a person who, at a particular time, holds a legal or equitable interest in a share:

(a) that is liable to be redeemed; or

(b) that, at the option of the company that issued it, is liable to be redeemed;

is taken not to hold the interest at that time.

Individual becoming director or employee within 3 months

(6) If an individual:

(a) nominates a replacement asset that is a share in a private company or a unit in a unit trust; and

(b) becomes a director and employee of the company, or an employee of the trust, as the case may be, within 3 months after he or she acquires the share or unit;

the individual is taken, for the purposes of this Division, to have been such a director and employee, or such an employee, as the case may be, at all times during that period.

10 Subdivision B of Division 17A of Part IIIA (heading)

Repeal the heading, substitute:

Subdivision B—How roll‑over relief is available on the disposal of an asset

11 Section 160ZZPO

Repeal the section, substitute:

160ZZPO What this Subdivision is about

This Subdivision sets out the way in which roll‑over relief is given to a taxpayer in respect of a year of income in which certain assets (roll‑over assets) are disposed of by the taxpayer.

If certain threshold criteria and other conditions are satisfied, capital gains do not accrue in respect of the disposals and net roll‑over amounts are worked out for the roll‑over assets.

The taxpayer may then nominate certain replacement assets in respect of the net roll‑over amounts and is to apportion the net roll‑over amounts to replacement assets in accordance with various rules.

The amounts apportioned are taken to reduce the cost base of the replacement assets.

12 Subsection 160ZZPP (note)

Omit “paragraph 160ZZPL(7)(b)”, substitute “paragraphs 160ZZPL(7)(b), (8)(d) and (9)(d)”.

13 Paragraphs 160ZZPQ(1)(c) and (d)

Repeal the paragraphs, substitute:

(c) where the roll‑over asset is neither a share in a company nor a unit in a unit trust:

(i) the roll‑over asset was an active asset at the disposal test time or, if it was not an active asset at that time because the relevant business had ceased to be carried on, the cessation occurred not earlier than 12 months before that time; and

(ii) the roll‑over asset was an active asset during more than one‑half of the period in which it was owned by the taxpayer; and

14 Subsection 160ZZPQ(3)

Repeal the subsection, substitute:

Calculation of gross non‑goodwill roll‑over amount for assets other than shares or units

(3) If the roll‑over asset is none of the following:

(a) goodwill;

(b) a share in a company;

(c) a unit in a unit trust;

an amount (the gross non‑goodwill roll‑over amount) equal to the notional capital gain is taken for the purposes of this Division to apply to the taxpayer in respect of the year of income in which the disposal occurred.

Calculation of gross non‑goodwill roll‑over amount for shares or units

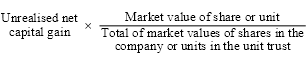

(3A) If the roll‑over asset is a share in a company or a unit in a unit trust, an amount (the gross non‑goodwill roll‑over amount) equal to the lesser of the following amounts is taken for the purposes of this Division to apply to the taxpayer in respect of the year of income in which the disposal occurred:

(a) an amount equal to the notional capital gain;

(b) the amount worked out using the formula:

Amount taken to be capital gain

(3B) If the gross non‑goodwill roll‑over amount is the amount worked out under paragraph (3A)(b), an amount equal to the difference between the notional capital gain and the amount worked out under that paragraph is taken to be a capital gain that accrued to the taxpayer in the year of income in which the disposal occurred.

Unrealised net capital gain from active assets

(3C) Subject to subsection (3D), for the purposes of paragraph (3A)(b), the unrealised net capital gain is the total of the capital gains (after deducting any capital losses) that would accrue to the company or trust at the time of the disposal, as the case may be, if all assets of the company or trust that:

(a) either:

(i) were active assets at that time; or

(ii) had ceased to be active assets because of the cessation of the relevant business of the company or trust not earlier than 12 months before that time; and

(b) had been active assets during more than one‑half of the period in which they were owned by the company or were assets of the trust, as the case may be;

were disposed of at that time and the consideration for the disposal of each asset was an amount equal to the market value of the asset.

Certain assets to be disregarded in calculating unrealised net capital gain

(3D) In calculating the unrealised net capital gain referred to in subsection (3C), no regard is to be had to any asset that had been nominated by the company or trust as a replacement asset for the purposes of this Division and was acquired by the company or trust less than 5 years before the time of the disposal of the roll‑over asset.

15 Subsection 160ZZPT(1)

Omit all the words after “one or more”, substitute “approved assets (a replacement asset or replacement assets) that were acquired by the taxpayer within the period beginning one year before, and ending 2 years after, the last disposal by the taxpayer of any roll‑over asset in that year of income”.

16 After subsection 160ZZPT(1)

Insert:

Active asset may be nominated

(1AA) An active asset is an approved asset.

Certain shares may be nominated

(1AB) A share in a company is an approved asset in respect of a taxpayer if:

(a) the taxpayer is an individual (other than an individual who is acting as a trustee); and

(b) the company is, in respect of a year of income in which the share is acquired by the taxpayer, a private company that is a resident; and

(c) the taxpayer is the controlling individual of the company immediately after the share is acquired by the taxpayer; and

(d) the total of the market values of all the active assets of the company at the time of the acquisition of the share by the taxpayer is not less than 80% of the total of the market values of all the company’s assets at that time.

Certain units in unit trusts may be nominated

(1AC) A unit in a unit trust is an approved asset in respect of a taxpayer if:

(a) the taxpayer is an individual (other than an individual who is acting as a trustee); and

(b) the trust is, in respect of a year of income in which the unit is acquired by the taxpayer, a resident unit trust that is not a publicly traded unit trust; and

(c) the taxpayer is the controlling individual of the trust immediately after the unit is acquired by the taxpayer; and

(d) the total of the market values of all the active assets of the trust at the time of the acquisition of the unit by the taxpayer is not less than 80% of the total of the market values of all the assets of the trust at that time.

17 Subsections 160ZZPV(2) and (3)

Repeal the subsections, substitute:

(2) If this section applies, the following provisions have effect:

(a) the taxpayer must apportion the total net roll‑over amount among the nominated replacement assets in such manner as the taxpayer determines but so that the amount apportioned to a particular asset does not exceed the lesser of:

(i) the cost base of the asset; and

(ii) if the asset is a share in a company or a unit in a unit trust—the maximum apportionment amount for the share or unit worked out under subsection (3);

(b) if an amount is apportioned to an asset that is not a depreciable asset—the cost base of the asset is taken, from the time of its acquisition by the taxpayer, to have been reduced by the amount;

(c) if an amount is apportioned to an asset that is a depreciable asset and section 160ZZPX does not apply in relation to the asset before it is disposed of—the amount is taken to be a capital gain that accrues to the taxpayer during the year of income in which the asset is disposed of;

(d) if the amount apportioned to assets under paragraph (a) is less than the total net roll‑over amount—an amount equal to the difference is taken to be a capital gain that accrued to the taxpayer during the disposal year of income.

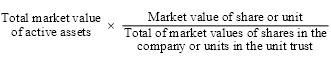

(3) The maximum apportionment amount for a share in a particular company or a unit in a particular unit trust is:

where:

active assets are those assets of the company or trust that were active assets of the company or trust, as the case may be, at the time of the acquisition of the shares or units.

market value means the market value at that time.

18 Subsections 160ZZPW(5) and (6)

Repeal the subsections, substitute:

(5) If this section applies, the following provisions also have effect:

(a) the taxpayer must apportion the residual net roll‑over amount among the nominated non‑goodwill replacement assets in such manner as the taxpayer determines but so that the amount apportioned to a particular asset does not exceed the lesser of:

(i) the cost base of the asset; and

(ii) if the asset is a share in a company or a unit in a unit trust—the maximum apportionment amount for the share or unit worked out under subsection (6);

(b) if an amount is apportioned to an asset that is not a depreciable asset—the cost base of the asset is taken, from the time of its acquisition by the taxpayer, to have been reduced by the amount;

(c) if an amount is apportioned to an asset that is a depreciable asset and section 160ZZPX does not apply in relation to the asset before it is disposed of—the amount is taken to be a capital gain that accrues to the taxpayer during the year of income in which the asset is disposed of;

(d) if the amount apportioned to assets under paragraph (a) is less than the residual net roll‑over amount—an amount equal to the difference is taken to be a capital gain that accrued to the taxpayer during the disposal year of income.

(6) The maximum apportionment amount for a share in a particular company or a unit in a particular unit trust is:

where:

active assets are those assets of the company or trust that were active assets of the company or trust, as the case may be, at the time of the acquisition of the shares or units.

market value means the market value at that time.

19 After section 160ZZPX

Insert:

160ZZPXA Change of circumstances of company or unit trust

Change of circumstances to which section applies

(1) This section applies if:

(a) there is a roll‑over asset in respect of a taxpayer in respect of a year of income; and

(b) there is a net roll‑over amount that applies to the taxpayer in respect of the year of income; and

(c) a replacement asset is nominated by the taxpayer under section 160ZZPT in respect of the net roll‑over amount; and

(d) the replacement asset is a share in a company or a unit in a unit trust; and

(e) at a time (the change time) after the taxpayer nominated the replacement asset:

(i) the taxpayer ceases to be the controlling individual of the company or trust; or

(ii) the total of the market values of the active assets of the company or trust falls below 80% of the total of the market values of all the assets owned by the company or the assets of the trust, as the case may be; or

(iii) the company ceases to be a private company that is a resident, the trust ceases to be a resident unit trust or the trust becomes a publicly traded unit trust, as the case may be; and

(f) the replacement asset is owned by the taxpayer immediately after the change time.

Exception

(2) Subparagraph (1)(e)(ii) does not apply if the total of the market values of the active assets referred to in that subparagraph fell below the percentage so referred to only because of changes in the market values of assets owned by the company or trust at the time of the nomination.

Capital gain accrues when change of circumstances occurs

(3) An amount (the adjustment amount) equal to the amount that was apportioned to the asset by the taxpayer under section 160ZZPV or 160ZZPW, as the case may be, is taken to be a capital gain that accrued to the taxpayer in the year of income in which the relevant change time occurred.

Consideration to be increased

(4) The cost base of the asset is increased, at the change time, by the adjustment amount.

20 Paragraph 160ZZPZD(1)(a)

Omit “to (d)”, substitute “to (c)”.

21 After paragraph 160ZZPZD(1)(a)

Insert:

(aa) the asset is a roll‑over asset within the meaning of subsection 160ZZPL(7); and

22 Paragraph 160ZZPZH(2)(a)

Omit “to (d)”, substitute “to (c)”.

23 After paragraph 160ZZPZH(2)(a)

Insert:

(aa) the asset is a roll‑over asset within the meaning of subsection 160ZZPL(7); and

24 Paragraph 160ZZPZI(2)(a)

Omit “to (d)”, substitute “to (c)”.

25 After paragraph 160ZZPZI(2)(a)

Insert:

(aa) the asset is a roll‑over asset within the meaning of subsection 160ZZPL(7); and

26 Application of amendments

The amendments made by this Part apply to disposals of assets on or after 1 July 1997.

Income Tax Assessment Act 1936

27 Subsection 160ZZPK(1)

Insert:

consideration, in respect of the acquisition of an asset, means the amount that is that consideration within the meaning of section 160ZH.

28 Subsection 160ZZPK(1)

Insert:

incidental costs to a taxpayer of the acquisition of an asset means the amount constituting those costs within the meaning of section 160ZH.

29 Subsection 160ZZPK(1) (definition of total goodwill cost base)

Repeal the definition, substitute:

total goodwill cost base, in relation to a taxpayer in relation to a disposal year of income, means the amount that, apart from this Division, would be:

(a) the sum (worked out at the time of acquisition) of the consideration in respect of, and the incidental costs to the taxpayer of, the acquisition of the replacement goodwill asset nominated by the taxpayer in respect of a net goodwill roll‑over amount that applies to the taxpayer in respect of that year of income; or

(b) if the taxpayer nominated 2 or more replacement goodwill assets in respect of such a net goodwill roll‑over amount—the sum (worked out at the time of the relevant acquisition) of the considerations in respect of, and the incidental costs to the taxpayer of, the acquisition of those replacement goodwill assets.

30 Subsection 160ZZPK(1) (definition of total non‑goodwill cost base)

Repeal the definition.

31 After subsection 160ZZPL(3)

Insert:

Subsection 157(3) to be disregarded

(3A) In determining for the purposes of this section whether a taxpayer is carrying on a business, subsection 157(3) is to be disregarded.

32 Subsection 160ZZPL(5)

After “roll‑over asset”, insert “that is an intangible asset and”.

Note: The heading to subsection 160ZZPL(5) is replaced by “Exception for intangible roll‑over asset whose value has been enhanced by the taxpayer”.

33 After subsection 160ZZPN(2)

Insert:

Where Public Trustee is trustee of discretionary trust

(2A) Subparagraph (2)(c)(i) does not apply to the first entity if the trustee of the trust referred to in that subparagraph is the Public Trustee of a State or Territory acting in that capacity.

34 Paragraph 160ZZPN(3)(c)

After “is”, insert “not”.

35 Section 160ZZPO

Omit “base”, substitute “of the acquisition”.

36 Subsection 160ZZPP(2)

Repeal the subsection.

37 Subsection 160ZZPP(3)

Omit “or an associate of the taxpayer”.

38 After paragraph 160ZZPP(4)(a)

Insert:

Note: The assets of a taxpayer do not include shares, units or other interests in entities connected with the taxpayer (see subsection 160ZZPL(2)).

39 Paragraph 160ZZPP(4)(c)

Repeal the paragraph.

40 Paragraph 160ZZPQ(1)(e)

Repeal the paragraph, substitute:

(e) if the roll‑over asset was nominated as a replacement asset under a previous application of this Division—the roll‑over asset was acquired by the taxpayer more than 5 years before the disposal test time; and

41 Paragraph 160ZZPR(2)(b)

Repeal the paragraph, substitute:

(b) then, in reduction of any net capital losses that:

(i) the taxpayer is taken to have incurred in respect of years of income (applicable years of income) earlier than the disposal year of income but not earlier than the 1995‑96 year of income; and

(ii) would, apart from this Division, be applied in determining whether a net capital gain accrues to the taxpayer in respect of the disposal year of income (if sufficient capital gains were to accrue in the disposal year of income).

42 At the end of paragraph 160ZZPS(2)(b)

Add:

; and (iii) would, apart from this Division, be applied in determining whether a net capital gain accrues to the taxpayer in respect of the disposal year of income (if sufficient capital gains were to accrue in the disposal year of income).

43 Before subsection 160ZZPT(2)

Insert:

When nomination to be made

(1A) A nomination of a replacement asset must be made before the end of 2 years after the last disposal by the taxpayer of any roll‑over asset in the year of income to which the net roll‑over amount relates.

44 Paragraphs 160ZZPU(2)(a) and (b)

Repeal the paragraphs, substitute:

(a) the taxpayer must apportion the whole of the net goodwill roll‑over amount among the nominated replacement assets in such manner as the taxpayer determines but so that the amount apportioned to a particular asset does not exceed the sum of:

(i) the amount that, at the time of the acquisition of the asset, was the consideration in respect of the acquisition of the asset; and

(ii) the amount that, at that time, was the total of the incidental costs to the taxpayer of the acquisition of the asset; and

(b) if an amount is apportioned to an asset—the amount is to be applied, at the time of the acquisition of the asset by the taxpayer, in reduction of the following amounts in such proportions as the taxpayer determines:

(i) the amount that, at the time of the acquisition of the asset, was the consideration in respect of the acquisition of the asset;

(ii) the amount that, at that time, was the total of the incidental costs to the taxpayer of the acquisition of the asset.

45 Paragraphs 160ZZPU(3)(a) and (b)

Repeal the paragraphs, substitute:

(a) the taxpayer must apportion so much of the net goodwill roll‑over amount as is equal to the total goodwill cost base among the nominated replacement assets so that the amount apportioned to a particular asset does not exceed the sum of:

(i) the amount that, at the time of the acquisition of the asset, was the consideration in respect of the acquisition of the asset; and

(ii) the amount that, at that time, was the total of the incidental costs to the taxpayer of the acquisition of the asset;

(b) if an amount is apportioned to an asset—the consideration in respect of the acquisition of the asset and the incidental costs to the taxpayer of the acquisition of the asset are each taken, at the time of the acquisition of the asset by the taxpayer, to be nil;

46 Paragraphs 160ZZPV(2)(a) and (b)

Repeal the paragraphs, substitute:

(a) the taxpayer must apportion the total net roll‑over amount among the nominated replacement assets in such manner as the taxpayer determines but so that the amount apportioned to a particular asset does not exceed the lesser of:

(i) the sum of the acquisition amounts set out in subsection (2B); and

(ii) if the asset is a share in a company or a unit in a unit trust—the maximum apportionment amount for the share or unit worked out under subsection (3);

(b) if an amount is apportioned to an asset that is not a depreciable asset—the amount is to be applied in reduction of the acquisition amounts for the asset in such proportions as the taxpayer determines;

47 After subsection 160ZZPV(2)

Insert:

(2A) The reductions set out in paragraph (2)(b) are taken to have been made at the time of the acquisition of the asset by the taxpayer.

(2B) The acquisition amounts for an asset are:

(a) the amount that, at the time of the acquisition of the asset, was the consideration in respect of the acquisition of the asset; and

(b) the amount that, at that time, was the total of the incidental costs to the taxpayer of the acquisition of the asset.

48 Paragraphs 160ZZPW(3)(a) and (b)

Repeal the paragraphs, substitute:

(a) the taxpayer must apportion the whole of the net goodwill roll‑over amount among the replacement assets that are nominated in respect of the net goodwill roll‑over amount in such manner as the taxpayer determines but so that the amount apportioned to a particular asset does not exceed the sum of:

(i) the amount that, at the time of the acquisition of the asset, was the consideration in respect of the acquisition of the asset; and

(ii) the amount that, at that time, was the total of the incidental costs to the taxpayer of the acquisition of the asset;

(b) if an amount is apportioned to an asset—the amount is to be applied, at the time of the acquisition of the asset by the taxpayer, in reduction of the following amounts in such proportions as the taxpayer determines:

(i) the amount that, at the time of the acquisition of the asset, was the consideration in respect of the acquisition of the asset;

(ii) the amount that, at that time, was the total of the incidental costs to the taxpayer of the acquisition of the asset.

49 Paragraphs 160ZZPW(4)(a) and (b)

Repeal the paragraphs, substitute:

(a) the taxpayer must apportion so much of the net goodwill roll‑over amount as is equal to the total goodwill cost base among the replacement assets that are nominated in respect of the net goodwill roll‑over amount so that the amount apportioned to a particular asset does not exceed the sum of:

(i) the amount that, at the time of the acquisition of the asset, was the consideration in respect of the acquisition of the asset; and

(ii) the amount that, at that time, was the total of the incidental costs to the taxpayer of the acquisition of the asset; and

(b) if an amount is apportioned to an asset—the consideration in respect of the acquisition of the asset and the incidental costs to the taxpayer of the acquisition of the asset are each taken, at the time of the acquisition of the asset by the taxpayer, to be nil; and

50 Paragraphs 160ZZPW(5)(a) and (b)

Repeal the paragraphs, substitute:

(a) the taxpayer must apportion the residual net roll‑over amount among the nominated non‑goodwill replacement assets in such manner as the taxpayer determines but so that the amount apportioned to a particular asset does not exceed the lesser of:

(i) the sum of the acquisition amounts set out in subsection (5B); and

(ii) if the asset is a share in a company or a unit in a unit trust—the maximum apportionment amount for the share or unit worked out under subsection (6);

(b) if an amount is apportioned to an asset that is not a depreciable asset—the amount is to be applied in reduction of the acquisition amounts for the asset in such proportions as the taxpayer determines;

51 After subsection 160ZZPW(5)

Insert:

(5A) The reductions set out in paragraph (5)(b) are taken to have been made at the time of the acquisition of the asset by the taxpayer.

(5B) The acquisition amounts for an asset are:

(a) the amount that, at the time of the acquisition of the asset, was the consideration in respect of the acquisition of the asset; and

(b) the amount that, at that time, was the total of the incidental costs to the taxpayer of the acquisition of the asset; and

52 Subparagraph 160ZZPX(1)(d)(i)

Before “ceases”, insert “if the replacement asset is not a share in a company or a unit in a unit trust—”.

53 Subsection 160ZZPX(3)

Repeal the subsection, substitute:

Consideration to be increased

(3) If the replacement asset is not a depreciable asset, the amount that, at the time of the acquisition of the asset, was the consideration in respect of the acquisition of the asset is to be increased, at the change time, by the adjustment amount.

54 Subsection 160ZZPXA(4)

Omit “cost base”, substitute “amount that, at the time of the acquisition of the asset, was the consideration in respect of the acquisition”.

55 Subsection 160ZZPY(3)

Repeal the subsection, substitute:

Consideration to be increased

(3) If the replacement asset is not a depreciable asset, the amount that, at the time of the acquisition of the asset, was the consideration in respect of the acquisition of the asset is taken, for the purposes of the application of this Part in relation to the person who acquired the asset, to be increased, from the time of the acquisition, by the adjustment amount.

56 Paragraph 160ZZPZ(1)(b)

Omit “section 160ZZPX”, substitute “sections 160ZZPX and 160ZZPXA”.

57 Paragraph 160ZZPZ(2)(b)

Omit “section 160ZZPX”, substitute “sections 160ZZPX and 160ZZPXA”.

58 Application of amendments

(1) The amendments made by items 32, 35 and 44 to 51 and 53 to 55 apply to disposals of assets after 23 October 1997.

(2) The amendment made by item 40 applies in respect of roll‑over assets acquired after 23 October 1997.

(3) The amendments made by items 31, 33, 34, 36 to 39, 41 to 43, 52, 56 and 57 apply to disposals of assets on or after 1 July 1997.

Schedule 2—Amendment of the Sales Tax Assessment Act 1992

Insert:

accredited has the meaning given by Division 2 of Part 7A.

Insert:

authorisation has the meaning given by Division 3 of Part 7A.

3 Section 5

Insert:

Part 7A goods has the meaning given by section 91C.

Insert:

tax file number has the meaning given by section 202A of the Income Tax Assessment Act 1936.

Add:

(4) Part 7A goods that have been the subject of a taxable dealing are taken not to have passed through a taxing point if the Commissioner believes that:

(a) tax has not been paid, and is unlikely to be paid, in respect of the dealing; and

(b) the person who is liable to pay that tax does not intend to pay the tax; and

(c) at the time of the dealing the taxpayer referred to in subsection (1) or (2) was aware, or could reasonably have been expected to be aware, that the tax had not been paid and was unlikely to be paid.

Add:

(3) Subsections (1) and (2) do not apply if the quote is not effective because of section 91S.

Add:

(2) Subsection (1) does not apply if the quote is not effective because of section 91S.

8 At the end of subsection 29(4)

Add:

; or (e) the current goods are Part 7A goods.

9 Subsection 29(7) (at the end of the definition of countable dealing)

Add:

; (c) a dealing with Part 7A goods.

Insert:

56A No credits for certain dealings with Part 7A goods

(1) A claimant is not entitled to a credit in respect of a dealing with Part 7A goods if the Commissioner believes that:

(a) tax has not been paid, and is unlikely to be paid, in respect of the dealing; and

(b) the taxpayer who is liable to pay that tax does not intend to pay the tax; and

(c) the claimant is aware, or could reasonably be expected to be aware, that the tax has not been paid and is unlikely to be paid.

(2) A claimant is not entitled to a CR26 credit in respect of a dealing with Part 7A goods if the Commissioner believes that:

(a) the amount withheld under section 91X has not been paid, and is unlikely to be paid, in respect of the dealing; and

(b) the taxpayer who is liable to pay that amount does not intend to pay the amount; and

(c) the claimant is aware, or could reasonably be expected to be aware, that the amount has not been paid and is unlikely to be paid.

11 After subsection 61(2)

Insert:

(2A) In addition to the returns required under subsections (1) and (2), a person who becomes liable to tax in respect of a dealing with Part 7A goods during a month must lodge a return within 21 days after the end of the month, or such further time as the Commissioner allows.

Omit “and (2)”, substitute “, (2) and (2A)”.

13 At the end of subsection 63(3)

Add “or a dealing with Part 7A goods”.

Note: The heading to section 63 is altered by inserting “or a dealing with Part 7A goods” after “dealing”

Insert:

64A Normal due date for payment of tax (other than tax on a customs dealing)

Tax that is payable by a person in respect of dealings (other than customs dealings) with Part 7A goods during a month becomes due for payment at the end of the 21st day after the end of that month, or at such later time as the Commissioner determines.

15 Subsection 69(2) (definition of tax)

After “includes”, insert “amounts payable under Part 7A,”.

16 Subsection 70(2) (definition of tax)

After “includes”, insert “amounts payable under Part 7A,”.

17 Subsection 71(3) (definition of tax)

After “includes”, insert “amounts payable under Part 7A,”.

18 Subsection 72(8) (definition of tax)

After “includes”, insert “amounts payable under Part 7A,”.

19 Subsection 73(7) (definition of tax)

After “includes”, insert “amounts payable under Part 7A,”.

20 Subsection 74(10) (after paragraph (a) of the definition of sales tax debt)

Insert:

(aa) an amount payable under Part 7A;

21 Subsection 76(3) (definition of tax)

After “includes”, insert “amounts payable under Part 7A,”.

Omit “$2,000”, substitute “20 penalty units”.

Insert:

Part 7A—Additional requirements for dealings with certain goods

Division 1—Purpose, overview and interpretation

This Part establishes a system of additional requirements for dealings with certain goods for the purpose of overcoming problems of sales tax evasion.

This Part establishes a system of additional requirements for dealings with certain goods. These goods are called Part 7A goods.

This Part establishes a system of accrediting persons (see Division 2).

Most quotes in relation to dealings with Part 7A goods must be authorised by the Commissioner. An authorisation will only be given where the person quoting is accredited (see Division 3).

In addition, sales tax must be withheld by the purchaser of goods in certain transactions (see Division 4).

(1) Part 7A goods are goods that, if imported, would be covered by a description and corresponding tariff classification specified in the following table:

Part 7A goods | ||

Item | Description of goods | Tariff classification |

1 | Personal computers | 8471.41.00 |

2 | Laptops, Notebooks, Palmtops | 8471.30.00 |

3 | Monitors | 8471.60.00 |

4 | Keyboards | 8471.60.00 |

5 | Printers (dot matrix, ink-jet or laser) | 8471.60.00 |

6 | CD‑ROM drives | 8471.90.00 |

7 | Modems | 8517.50.10 |

8 | Computer components (Motherboards, CPUs, memory, disk drives (hard and floppy), controller cards) | 8473.30.00 |

(2) Goods are also Part 7A goods if they are prescribed for the purposes of this subsection.

(3) However, goods are not Part 7A goods if they are prescribed for the purposes of this subsection.

(4) In subsection (1):

tariff classification means the tariff classification under which the goods are classified for the purposes of the Customs Tariff Act 1995.

91D When a person is relevant to an application

A person (the relevant person) is relevant to an application made by another person (the applicant) if:

(a) the applicant is accustomed or under an obligation, or might reasonably be expected, to act in accordance with the directions, instructions or wishes of the relevant person; or

(b) the applicant is a company and the directors of the applicant are accustomed or under an obligation, or might reasonably be expected, to act in accordance with the directions, instructions or wishes of the relevant person; or

(c) the applicant is a company and the relevant person is a director of the company; or

(d) the applicant is a trust and the relevant person is a trustee of the trust; or

(e) the applicant is a partnership and the relevant person is a partner in the partnership.

(2) Paragraphs (1)(a) and (b) apply:

(a) whether the obligation is formal or informal; and

(b) whether the directions, instructions or wishes are, or might reasonably be expected to be, communicated directly or through interposed companies, partnerships or trusts.

Only certain registered persons or other persons may be accredited (section 91F).

To be accredited, people must also meet a number of conditions or be exempted from meeting particular conditions by the Commissioner (section 91G).

Even if people meet the conditions, the Commissioner has a discretion to refuse to accredit persons (section 91K).

Accreditation may be withdrawn by the Commissioner (section 91J).

A person who is accredited must comply with requirements about record‑keeping and advising the Commissioner of certain matters (sections 91N and 91P).

91F Who may apply for accreditation

Registered persons

(1) A registered person may apply for accreditation.

People who grant certain leases

(2) A person (whether or not registered) may apply for accreditation if he or she has granted, or intends to grant, leases of Part 7A goods:

(a) that are eligible long‑term leases or eligible short‑term leases; or

(b) in relation to which section 32 would apply.

People who can quote under section 84

(3) A person (whether or not registered) who the Commissioner has allowed to quote under section 84 for a dealing with Part 7A goods may apply for accreditation.

Others may apply if Commissioner allows

(4) Any other person may, with the agreement of the Commissioner, apply for accreditation.

91G Requirements for accreditation

(1) To be accredited, a person must satisfy all of the following requirements other than those that the Commissioner exempts the person from satisfying.

(2) The first requirement is that the person must have conducted the business activities in respect of which accreditation has been sought at or from established premises that were advertised to the public as being premises from which the business was carried on.

(3) The second requirement is that the person must have a tax file number and must have quoted that tax file number in relation to each account maintained by the person for business purposes with a financial institution.

(4) The third requirement is that, if the person is an individual, the person must conduct all financial transactions relating to the business through a bank account that is, or bank accounts that are, separate from any private or domestic account maintained by the person.

(5) The fourth requirement is that the person, and each person who is relevant to the person’s application, must have satisfactorily complied with his or her obligations under Acts administered by the Commissioner for the period of 3 years before the date of the application.

(6) The fifth requirement is that the person must have maintained records in English in relation to the period of 3 years before the date of the application including details of purchases and sales of goods, the names of suppliers and customers, details of purchases and sales in relation to which sales tax was not paid and details of credits claimed. The records must be located in Australia and may be kept and retained in written or electronic form.

(7) The sixth requirement is that:

(a) if the person is an individual—the person; or

(b) if the person is a company—at least one director of the company; or

(c) if the person is a trust—the trustee of the trust; or

(d) if the person is a partnership—at least one partner in the partnership;

is an Australian citizen or is the holder of a permanent visa (within the meaning of the Migration Act 1958).

(8) The seventh requirement is that, in the period of 3 years before the date of the application:

(a) the person has not, whether in Australia or another country, been convicted of any offence, or been subject to any penalty, in relation to taxation requirements, customs requirements, the misdescription of goods, trade practices, fair trading or the defrauding of a government; or

(b) if the person is not an individual—no person who is relevant to the person’s application, whether in Australia or another country, has been convicted of any offence, or been subject to any penalty, in relation to taxation requirements, customs requirements, the misdescription of goods, trade practices, fair trading or the defrauding of a government.

(9) The eighth requirement is that:

(a) the person has not been refused accreditation or had his or her accreditation revoked in the previous 3 years; or

(b) if the person is not an individual—no person who is relevant to the person’s application has been refused accreditation or had his or her accreditation revoked in the previous 3 years.

(10) The ninth requirement is that:

(a) the person has not, in the previous 3 years, been a person who is relevant to another person’s application at a time when the other person’s application did not satisfy the previous eight requirements; or

(b) if the person is not an individual—no person who is relevant to the person’s application has, in the previous 3 years, been a person who is relevant to another person’s application at a time when the other person’s application did not satisfy the previous eight requirements.

91H Application for accreditation

(1) An application for accreditation must be in a form approved in writing by the Commissioner for the purpose and must contain the information necessary for the proper completion of the form.

Electronic applications

(2) An approval given by the Commissioner of a form of application may require or permit the application to be given on a specified kind of data processing device, or by way of electronic transmission, in accordance with specified software requirements.

(1) If the Commissioner receives an application that is properly made under section 91H and the applicant satisfies all necessary tests under section 91G, the Commissioner must accredit the applicant unless the Commissioner exercises his or her discretion under section 91K.

(2) Once granted, accreditation remains in force until the end of any period specified by the Commissioner unless it is revoked under section 91L.

(3) The accreditation may be given in writing or by way of electronic transmission.

91K Commissioner’s discretion to refuse accreditation

The Commissioner may refuse to accredit a person if:

(a) the Commissioner has reasonable grounds for believing that sales tax will not be, or is unlikely to be, paid in relation to transactions with Part 7A goods dealt with by the person; or

(b) the person’s application is false or misleading in a material particular (either because of something stated in the application or something left out);

and the Commissioner believes that the refusal would assist in achieving the purpose of this Part.

91L Revocation of accreditation

(1) The Commissioner may, by written notice given to a person, revoke the person’s accreditation at a particular time if the Commissioner believes that, if the person made an application at that time:

(a) the person would not be covered by section 91F; or

(b) the person would not satisfy all of the requirements in section 91G; or

(c) the Commissioner would exercise his or her discretion under section 91K.

(2) If a person requests the Commissioner to revoke his or her accreditation, the Commissioner must revoke the person’s accreditation.

91M Review of decisions on accreditation

A person who is affected by a decision:

(a) under section 91J or 91K to refuse to accredit; or

(b) under section 91L to revoke accreditation;

and is dissatisfied with the decision may object against the decision in the manner set out in Part IVC of the Taxation Administration Act 1953.

91N Accredited persons to advise Commissioner of certain matters

(1) This section applies if, at a particular time, a person who is accredited becomes aware that, if the person made an application for accreditation at that time:

(a) the person would not be covered by section 91F; or

(b) the person would not satisfy all of the requirements in section 91G.

(2) If this section applies, the accredited person must notify the Commissioner of that fact and provide the Commissioner with details of circumstances that cause this section to apply. The notification and the details must be given in writing within 7 days of the time mentioned in subsection (1).

Offence of contravening subsection (2)

(3) A person who contravenes subsection (2) is guilty of an offence punishable on conviction by a fine not exceeding 50 penalty units.

91P Additional information about transactions

In addition to any returns required under section 61, the Commissioner may direct a person to give to the Commissioner such information as the Commissioner:

(a) requires in respect of dealings by the person with Part 7A goods; or

(b) if the person is accredited—considers is relevant to the person’s accreditation.

91Q Commissioner may publicise who is accredited

(1) The Commissioner may publish, or otherwise publicise, the names, accreditation numbers and registration numbers of persons who are accredited or whose accreditation is revoked.

(2) In addition, the Commissioner may, if requested:

(a) advise a person whether or not another person is accredited and, if so, whether the person is registered; and

(b) if the information is required for the purposes of section 91S, advise a person whether or not a person who is not accredited is registered.

(3) This section operates despite anything in this Act or the Taxation Administration Act 1953.

Division 3—Authorisation of certain transactions

This Division provides for the Commissioner to authorise quotations in respect of particular dealings with goods. Without an authorisation, the quote will not be effective.

Authorisations may be sought, and may be given, in any way that the Commissioner decides. This could be orally or by way of electronic transmission.

The authorisation may be given in relation to a particular dealing or may be a standing authorisation that applies to specified kinds of dealings.

91S Quote not effective without authorisation

(1) A quote in relation to a dealing with Part 7A goods is only effective if:

(a) the person quoting is accredited and the quote is authorised by the Commissioner; or

(b) the quote is a quote of an exemption declaration, the dealing is not a local entry and the person making the quote intends to use the goods so as to satisfy an exemption item (other than a prescribed exemption item); or

(c) the dealing is not a local entry and the person making the quote:

(i) is registered; and

(ii) is not acquiring the goods for resale; and

(iii) satisfies the low purchase value test (see subsections (2) and (3)) in relation to that dealing; or

(d) the quote is made in prescribed circumstances; or

(e) the person accepting the quote satisfies the Commissioner that he or she was satisfied on reasonable grounds that paragraph (a), (b), (c) or (d) applied.

(2) For a person to satisfy the low purchase value test in relation to a dealing (the current dealing), the total of the value of:

(a) the current dealing; and

(b) all other acquisitions of Part 7A goods for which the person quoted in the 12 months before the current dealing;

must be less than $6,000 or such other amount as is prescribed.

(3) In addition, the person must have an expectation (based on reasonable grounds) that the total of the value of all acquisitions of Part 7A goods by the person in the 12 months after the current dealing for which the person will quote will be less than $6,000 or such other amount as is prescribed.

(4) For a person (the seller) to be satisfied that another person (the purchaser) satisfies the low purchase value test in relation to a dealing, the seller must obtain from the purchaser a signed statement, in a form approved in writing by the Commissioner, that the purchaser satisfies the low purchase value test in relation to the dealing.

(5) A person must not, in relation to any dealing with goods, falsely represent that the person satisfies the low purchase value test in relation to that dealing.

Penalty: 50 penalty units.

91T Method of obtaining authorisation

(1) A person who wants an authorisation in relation to a quote for a dealing must seek the authorisation in a manner approved in writing by the Commissioner.

(2) The person may seek authorisation in relation to a single quote or in relation to quotes for a class of dealings. An authorisation in relation to a class of dealings is a standing authorisation.

(3) Without limiting the Commissioner’s power under subsection (1), the Commissioner may approve authorisations being sought orally or by way of electronic transmission.

91U Giving of authorisation by Commissioner

(1) If a person seeks an authorisation in relation to a single dealing, the Commissioner must give the authorisation unless:

(a) the person making the quote is not accredited; or

(b) the quote would not be effective even if the Commissioner authorised it; or

(c) the Commissioner considers that there are reasonable grounds for believing that sales tax will not be, or is unlikely to be, paid in relation to the dealing or in relation to other dealings with those Part 7A goods.

Example: The Commissioner may believe that sales tax will not be paid in relation to a later sale to a retailer that is made by the person who buys the goods from the person making the application.

(2) If a person seeks a standing authorisation, the Commissioner may give the standing authorisation if the Commissioner considers that there are reasonable grounds for believing that sales tax will be paid in relation to all dealings that would be covered by the standing authorisation and in relation to other dealings with the goods covered by those dealings.

(3) The Commissioner may also, on his or her own initiative, give a person a standing authorisation covering such dealings as the Commissioner determines if the Commissioner considers that there are reasonable grounds for believing that sales tax will be paid in relation to all dealings that would be covered by the standing authorisation.

(4) A standing authorisation does not cover a quote if:

(a) the person making the quote is not accredited; or

(b) the quote would not be effective even if the Commissioner authorised it.

(5) The Commissioner may, by written notice, revoke a standing authorisation.

(6) A person who is affected by a decision:

(a) to refuse to authorise a transaction; or

(b) to refuse to give a standing authorisation; or

(c) to revoke a standing authorisation;

and is dissatisfied with the decision may object against the decision in the manner set out in Part IVC of the Taxation Administration Act 1953.

(7) In determining that there are reasonable grounds for believing that sales tax will not be, or is unlikely to be, paid in relation to transactions with Part 7A goods dealt with by the person, the Commissioner is not limited to considering dealings to which the person is a party.

An authorisation may be given in such form, including orally or by way of electronic transmission, as the Commissioner considers appropriate.

Division 4—Withholding of sales tax on dealings with Part 7A goods

This Division provides for the withholding of sales tax from payments in respect of certain dealings with Part 7A goods. The dealings are those where an accredited person or a retailer purchases goods from an unaccredited person.

It also sets out the way in which the tax, and associated forms, must be sent to the Commissioner.

(1) If an accredited person makes a payment to a person in respect of a taxable dealing that is the purchase of Part 7A goods for the purpose of resale from a person who is not accredited, the accredited person must deduct the withholding amount from the payment.

(2) If, after the day prescribed for the purposes of this subsection, a person who is a retailer in relation to particular Part 7A goods makes a payment to a person in respect of a taxable dealing that is the purchase of those Part 7A goods from a person who is not accredited, the retailer must deduct the withholding amount from the payment.

(3) Subsections (1) and (2) do not apply if the accredited person, or the retailer (as the case requires):

(a) took reasonable steps to determine whether the other person was accredited; and

(b) as a result, reasonably believed that the other person was accredited.

(4) A person, other than a government body, who contravenes this section is guilty of an offence punishable on conviction by a maximum fine of 20 penalty units.

91Y Working out the withholding amount

(1) The withholding amount for a payment that is made in respect of the purchase of Part 7A goods where the purchase involves only Part 7A goods and an invoice is given for the purchase is:

(2) In any other case, the withholding amount for a payment that is made in respect of the purchase of Part 7A goods is:

(3) In this section:

notional wholesale selling price has the same meaning as in Table 1 in Schedule 1.

Schedule 4 rate is the rate of tax that applies to taxable dealings with goods covered by Schedule 4 to the Exemptions and Classifications Act.

91Z Reporting and remitting amounts

(1) A person who makes one or more payments covered by section 91X in a month must send all amounts deducted under section 91X from the payments to the Commissioner within 21 days after the end of the month (or such longer period as the Commissioner allows).

(2) The person must also:

(a) complete and sign a withholding advice form in respect of the amounts; and

(b) make 2 copies of the form; and

(c) give a copy of the form to the seller; and

(d) send the form to the Commissioner within 21 days after the end of the month (or such longer period as the Commissioner allows).

(3) The person must keep the copies of all of the forms that the person is required to make under this section (other than those copies required to be given to the seller or sent to the Commissioner) for at least 5 years after the end of the financial year in which the payments to which the copies relate were made. The copies must be kept in Australia.

(4) A person, other than a government body, who contravenes subsection (1) is guilty of an offence punishable on conviction by imprisonment for 12 months. In addition, the court may order the person to pay to the Commissioner as a penalty an amount not greater than the amount required to be deducted under section 91X from any payment to which the contravention relates.

(5) A person, other than a government body, who contravenes subsection (2) or (3) is guilty of an offence punishable on conviction by a fine of 20 penalty units.

91ZA Refund of deductions in certain cases

(1) If a person has applied for a refund and the Commissioner is satisfied that:

(a) a deduction was made from a payment to the applicant; and

(b) the whole or a part of the amount of the deduction (the relevant amount) was made due to an act or omission of the applicant or another person; and

(c) having regard to:

(i) the purposes of this Division; and

(ii) the nature of the act or omission referred to in paragraph (b); and

(iii) such other matters (if any) as the Commissioner thinks fit;

it would be fair and reasonable to refund the relevant amount to the applicant, the Commissioner must refund the relevant amount to the applicant.

(2) No person is entitled to a credit in respect of an amount refunded under subsection (1).

(3) A person who is affected by a decision to refuse to refund an amount under subsection (1) and is dissatisfied with the decision may object against the decision in the manner set out in Part IVC of the Taxation Administration Act 1953.

91ZB Failure to make deductions from payments

(1) A person, other than a government body, who refuses or fails, at the time of making a payment, to deduct from the payment the amount required to be deducted under this Division, is liable to pay to the Commissioner, by way of penalty:

(a) an amount (the undeducted amount) equal to the amount that the person failed to deduct; and

(b) an amount equal to 16% per annum of so much of the undeducted amount as remains unpaid, worked out from the end of the period within which the person, had the person deducted the required amount, would have been required to pay the amount to the Commissioner.

(2) A government body, other than the Commonwealth, that refuses or fails, at the time of making a payment, to deduct from the payment the amount required to be deducted under this Division, is liable to pay to the Commissioner, by way of penalty, an amount equal to 16% per annum of the amount that the body refused or failed to deduct in respect of the period:

(a) starting at the end of the period within which the body, had it deducted the required amount, would have been required to pay the amount to the Commissioner; and

(b) ending on the day on which the whole of the amount payable by the body under this subsection in respect of the undeducted amount is paid.

91ZC Failure to pay amounts deducted to Commissioner

(1) Where an amount (the principal amount) payable to the Commissioner by a person other than the Commonwealth under subsection 91Z(1) remains unpaid at the end of the period within which it is required to be paid:

(a) the principal amount continues to be payable by the person to the Commissioner; and

(b) the person is liable to pay to the Commissioner, by way of penalty, the amount worked out under subsection (2) or (3).

(2) If the person is not a government body, the amount is the sum of:

(a) an amount (the relevant penalty amount) equal to 20% of the principal amount; and

(b) an amount at the rate of 16% per annum of the sum of so much of the principal amount as remains unpaid and so much of the relevant penalty amount as remains unpaid, worked out from the end of that period.

(3) If the person is a government body, the amount is 16% per annum of so much of the principal amount as remains unpaid, worked out from the end of that period.

(1) In this Division:

government body means the Commonwealth, a State, a Territory or an authority of the Commonwealth, a State or a Territory.

(2) For the purposes of this Division, a person is a retailer of particular Part 7A goods if:

(a) the person is mainly a retailer in relation to the Part 7A goods; and

(b) the person did not manufacture the Part 7A goods; and

(c) the person will not use the Part 7A goods as raw materials in manufacturing.

(3) A person is mainly a retailer in relation to particular Part 7A goods if the person sells Part 7A goods and:

(a) wholesale sales and indirect marketing sales of Part 7A goods do not account for more than half of the total value of all sales of Part 7A goods by the person during the 12 months ending at the time of the relevant dealing with the particular Part 7A goods; or

(b) the person has an expectation (based on reasonable grounds) that wholesale sales and indirect marketing sales of Part 7A goods will not account for more than half of the total value of all sales of Part 7A goods by the person during the 12 months starting at the time of the relevant dealing with the particular Part 7A goods.

For this purpose, the value of a sale of goods is the price for which the goods are sold.

Division 5—General provisions about offences

(1) A person must not, in relation to any dealings with goods:

(a) falsely represent that the person is an accredited person; or

(b) falsely represent that a quote is authorised under section 91U.

Penalty: 20 penalty units.

(2) Strict liability applies to subsection (1).

Note: For strict liability, see section 6.1 of the Criminal Code.

91ZF Application of the Criminal Code

Chapter 2 of the Criminal Code applies to all offences against this Part.

24 Schedule 1 (at the end of Table 3)

Add:

CR26 | Credit for amounts withheld on Part 7A goods | Claimant has become liable to tax on an assessable dealing with Part 7A goods and another person has withheld an amount in respect of that dealing under section 91X. | the amount withheld | the later of the time when the claimant pays the tax on the assessable dealing and the time when the Commissioner receives the form under subsection 91Z(2) in respect of the amount withheld |

(1) The amendment made by item 5 applies in relation to dealings after 23 October 1997.

(2) The amendment made by item 10 applies in relation to credits applied for after 23 October 1997.

(3) Divisions 3 and 4 of Part 7A of the Sales Tax Assessment Act 1992 apply to dealings on or after a date to be prescribed.

26 Transitional—record keeping requirements

For the purposes of applications made within 3 years after the commencement of this item, subsection 91G(6) applies as if the requirement for the records to have been kept in English was limited to records that are kept after the commencement of this item.

Schedule 3—Land transport facilities

Part 1—Insertion of new Division 396

Income Tax Assessment Act 1997

Insert:

[The next Division is Division 396]

Division 396—Land transport facilities borrowings

Guide to Division 396

396‑A Key operative provisions

396‑B What LTF interest is covered?

396‑C Projects, borrowers and lenders

396‑D Application, approval and agreement process

396‑E Miscellaneous

396‑5 What this Division is about

A lender can get a tax offset for certain interest it derives on an approved borrowing by another entity for the construction of land transport facilities.

For a borrowing to be approved:

(a) the borrower must apply to the Commissioner; and

(b) the Minister for Transport and Regional Development must approve the application; and

(c) that Minister, the borrower and each of the lenders must enter into an agreement.

The total of tax offsets available under this Division for an income year is subject to a limit.

Where a tax offset is given for interest, the borrower cannot deduct the interest.

Subdivision 396‑A—Key operative provisions

396‑10 What this Subdivision is about

This Subdivision provides for:

(a) the tax offset for the lender; and

(b) deductions not to be allowed to the borrower.

It also provides for a cap to be set on the amount of tax offsets approved for each income year.

Operative provisions

396‑15 Tax offset for LTF interest on land transport facilities borrowings

396‑20 Maximum amount of tax offsets

396‑25 Borrower cannot deduct LTF interest for which lender has tax offset

[This is the end of the Guide.]

396‑15 Tax offset for LTF interest on land transport facilities borrowings

(1) An entity that is a lender under a *land transport facilities borrowings agreement is entitled to a *tax offset for *LTF interest covered by the agreement.

Amount of tax offset

(2) The amount of the tax offset is worked out using the formula:

![]()

However, the amount cannot exceed any amount specified in the *land transport facilities borrowings agreement as the maximum *tax offset for that lender for the income year for that agreement.

(3) In subsection (2):

LTF interest covered by agreement means the amount of *LTF interest that is covered by the *land transport facilities borrowings agreement and that is derived by the entity in the income year.

396‑20 Maximum cost to Commonwealth

The maximum net cost to the Commonwealth of *tax offsets to be approved under this Division for an income year (after taking into account deductions that are reduced) is the amount determined, by written notice, by the Treasurer.

Note: The maximum amount is taken into account under subsection 396‑70(5) in approving projects.

396‑25 Borrower cannot deduct LTF interest for which lender has tax offset

(1) The total of amounts that an entity that is a borrower under a *land transport facilities borrowings agreement can deduct for an income year for *LTF interest covered by the agreement is reduced by:

(2) In subsection (1):

tax offset entitlement is the total of the amounts of *tax offset worked out under subsection 396‑15(2) for LTF interest that is covered by the agreement and that is derived by a lender in the income year.

(3) If the amount by which deductions for an income year are to be reduced by subsection (1) (or by a previous operation of this subsection) exceeds the total of those deductions:

(a) the deductions are reduced to nil; and

(b) the total amount that the borrower can deduct for the next income year for *LTF interest covered by the agreement is reduced by the total of:

(i) that excess; and

(ii) the amount worked out for that next income year using the formula in subsection (1).

Note: This can happen where interest is incurred by the borrower in an income year after the income year in which it is derived by the lender.

Subdivision 396‑B—What LTF interest is covered?

This Subdivision sets out the interest for which a tax offset can be obtained.

Operative provisions

396‑30 What is LTF interest?

396‑35 Interest covered by land transport facilities borrowings agreement

396‑40 Interest ceasing to be covered by a land transport facilities borrowings agreement

[This is the end of the Guide.]

(1) LTF interest, in relation to a borrower, is:

(a) a payment of interest, or in the nature of interest, made or liable to be made by the borrower, for which the borrower is, apart from this Division, entitled to a deduction; or

(b) an amount allowable as a deduction to the borrower under section 159GT of the Income Tax Assessment Act 1936 in relation to a *borrowing that is covered by a *land transport facilities borrowings agreement.

Note: Section 159GT deals with certain securities.

(2) LTF interest, in relation to a lender, is:

(a) a payment of interest, or in the nature of interest, made or liable to be made to the lender, that is included in the lender’s assessable income for an income year; or

(b) an amount included in the assessable income of the lender under section 159GQ of the Income Tax Assessment Act 1936 in relation to a *borrowing that is covered by a *land transport facilities borrowings agreement.

Note: Section 159GQ deals with certain securities.

396‑35 Interest covered by land transport facilities borrowings agreement

(1) *LTF interest that is derived by an entity is covered by a *land transport facilities borrowings agreement if:

(a) the entity is a lender under the agreement; and

(b) the LTF interest arises under a *borrowing that is covered by the agreement when the interest is derived.

(2) *LTF interest that is incurred by an entity is covered by a *land transport facilities borrowings agreement if:

(a) the entity is the borrower under the agreement; and

(b) the LTF interest arises under a *borrowing that is covered by the agreement at the time that the LTF interest is incurred.

396‑40 Interest ceasing to be covered by a land transport facilities borrowings agreement

*LTF interest ceases to be covered by a *land transport facilities borrowing agreement if the borrower or a lender breaches the agreement and the Minister for Transport and Regional Development decides:

(a) that the breach is a material breach of the agreement; and

(b) not to agree to vary the agreement in a way that would cause the breach to no longer be a breach.

Subdivision 396‑C—Projects, borrowers and lenders

This Subdivision explains the projects that can be approved and who can be approved as borrowers or lenders.

Where a project and a borrower are approved, a land transport facilities borrowings agreement is entered into under Subdivision 396‑D.

Operative provisions

396‑45 What projects can be approved?

396‑50 Who can be approved as a borrower?

396‑55 Who can be a lender?

[This is the end of the Guide.]

396‑45 What projects can be approved?

(1) To be approved, a project must be the construction of a *land transport facility or the construction or acquisition of one or more *related facilities.

(2) A land transport facility is a road, tunnel, bridge, or railway line, in Australia, that is to be used for the transport of the public or their goods at a charge to them (whether the transport is by the member of the public concerned or by another entity).

(3) Related facilities are facilities in Australia that are reasonably necessary for a *land transport facility to be able to operate for the purpose for which it was constructed.

(4) The following are examples of *related facilities:

(a) *plant and other equipment (for example, rolling stock in the case of a railway) for use in operating the *land transport facility;

(b) buildings or other structures from which staff are to operate the land transport facility;

(c) buildings or other structures for storing freight, cargo, plant, fuel, stores or equipment;

(d) stations or passenger or freight terminals;

(e) maintenance facilities.

(5) A road, road bridge or road tunnel to provide access to a *land transport facility that is a railway is not a related facility (or part of the land transport facility itself).

(6) A railway, railway bridge or railway tunnel to provide access to a *land transport facility that is a road is not a related facility (or part of the land transport facility itself).

Note: Items 20 and 21 of Schedule 3 to the Taxation Laws Amendment Act (No. 1) 1998 treat certain facilities as if they were land transport facilities or related facilities.

396‑50 Who can be approved as a borrower?

(1) An entity can only be approved as a borrower in relation to a particular project if the entity is:

(a) an incorporated body; or

(b) a *corporate limited partnership; or

(c) a *corporate unit trust; or

(d) a *public trading trust;

and intends to continue to be that type of entity for the period covered by the agreement.

(2) An entity cannot be approved as a borrower if the entity is making the *borrowing in partnership with another entity.

(3) An entity cannot be approved as a borrower if the entity:

(a) is a government body (within the meaning of subsection 93D(1) of the Development Allowance Authority Act 1992); or

(b) is government owned (within the meaning of subsection 93I(3) of that Act);

unless the entity is covered by subsection 93I(4) of that Act.

A lender must be an Australian resident for the whole of an income year to be entitled to a *tax offset under this Division for that income year.

Subdivision 396‑D—Application, approval and agreement process

This Subdivision sets out the process for applications to be made and approved and agreements to be entered into.

Operative provisions

396‑60 Applications

396‑65 Minister or Commissioner may seek more information

396‑70 Minister for Transport and Regional Development to consider applications

396‑75 Selection criteria

396‑80 Land transport facilities borrowings agreements

396‑85 Conditions to be in all agreements

396‑90 Variation of agreements

[This is the end of the Guide.]

(1) An entity that wants to be approved as a borrower in relation to a particular project must give a written application to the Commissioner.

(2) The application must be in a form approved in writing by the Commissioner and must contain all information that is required for proper completion of the form.

Electronic applications

(3) An approval by the Commissioner of a form of application may require or permit the application to be given on a specified kind of data processing device, or by way of electronic transmission, in accordance with specified software requirements.

396‑65 Minister or Commissioner may seek more information

(1) The Minister for Transport and Regional Development or the Commissioner may, in writing, ask an applicant to provide additional information for the purpose of determining the applicant’s application.

(2) The Minister for Transport and Regional Development does not have to consider, or further consider, the application until the additional information has been provided.

396‑70 Minister for Transport and Regional Development to consider applications

(1) The Minister for Transport and Regional Development is to consider applications and to decide:

(a) whether to approve the borrower and the project; and

(b) if so, whether to set a maximum amount of *tax offsets for the project for each income year covered by the approval.

(2) A decision to approve a borrower and a project must be in writing and must specify:

(a) the borrower; and

(b) the project; and

(c) the income years covered by the approval; and

(d) if a maximum amount of *tax offsets for the project for each income year covered by the approval is set—the maximum amount for each income year.

The amount may be different for different years.

(3) The decision may include conditions to which the approval is subject.

(4) The approval must not cover an income year that starts more than 5 years after the first *borrowing is made in respect of the project.

(5) In making a decision under paragraphs (1)(a) and (1)(b), the Minister for Transport and Regional Development must attempt to ensure that the maximum net cost referred to in section 396‑20 for any income year will not be exceeded.

(6) For the purposes of subsection (5), where no maximum amount is specified in relation to a project, the Minister for Transport and Regional Development is to take account of the expected amount of tax offsets for that project.