Tax Laws Amendment (2004 Measures No. 7) Act 2005

No. 41, 2005

An Act to amend the law relating to taxation, and for related purposes

Tax Laws Amendment (2004 Measures No. 7) Act 2005

No. 41, 2005

An Act to amend the law relating to taxation, and for related purposes

Contents

1 Short title

2 Commencement

3 Schedule(s)

4 Amendment of assessments

Schedule 1—25% entrepreneurs’ tax offset

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Schedule 2—STS accounting method

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Schedule 3—Employee share schemes

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Schedule 4—FBT exemption thresholds for long service award benefits

Fringe Benefits Tax Assessment Act 1986

Schedule 5—Petroleum exploration incentives

Petroleum Resource Rent Tax Assessment Act 1987

Schedule 6—Consolidation

Part 1—Application

Part 2—Amount of certain liabilities for purpose of calculating allocable cost amount on exit

Income Tax Assessment Act 1997

Part 3—Ensuring no double reduction in working out step 3 of allocable cost amount on entry

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Part 4—Bad debts

Division 1—Main amendment

Income Tax Assessment Act 1997

Division 2—Consequential amendments

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Part 5—Insurance companies

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Schedule 7—STS roll‑over

Income Tax Assessment Act 1997

Schedule 8—Family trust elections

Income Tax Assessment Act 1936

Schedule 9—Non‑commercial loans

Part 1—Amendment commencing on 29 June 2004

Income Tax Assessment Act 1936

Part 2—Amendments commencing on Royal Assent

Income Tax Assessment Act 1936

Schedule 10—Technical corrections and amendments

Part 1—Technical corrections and amendments commencing on Royal Assent

A New Tax System (Goods and Services Tax) Act 1999

A New Tax System (Wine Equalisation Tax) Act 1999

Fringe Benefits Tax Assessment Act 1986

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

New Business Tax System (Consolidation and Other Measures) Act 2003

Petroleum Resource Rent Tax Assessment Act 1987

Product Grants and Benefits Administration Act 2000

Superannuation Guarantee (Administration) Act 1992

Taxation Administration Act 1953

Taxation Laws Amendment Act (No. 5) 2002

Venture Capital Act 2002

Part 2—Technical corrections and amendments commencing otherwise than on Royal Assent

A New Tax System (Pay As You Go) Act 1999

Energy Grants (Credits) Scheme (Consequential Amendments) Act 2003

Fringe Benefits Tax Assessment Act 1986

Income Tax Assessment Act 1997

New Business Tax System (Consolidation) Act (No. 1) 2002

New Business Tax System (Consolidation and Other Measures) Act 2003

Taxation Laws Amendment (Company Law Review) Act 1998

Taxation Laws Amendment (Research and Development) Act 2001

Tax Laws Amendment (2004 Measures No. 2) Act 2004

Part 3—Removal of link notes

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Taxation Administration Act 1953

Venture Capital Act 2002

Schedule 11—Film tax offset amendments

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Tax Laws Amendment (2004 Measures No. 7) Act 2005

No. 41, 2005

An Act to amend the law relating to taxation, and for related purposes

[Assented to 1 April 2005]

The Parliament of Australia enacts:

This Act may be cited as the Tax Laws Amendment (2004 Measures No. 7) Act 2005.

(1) Each provision of this Act specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Note: This table relates only to the provisions of this Act as originally passed by the Parliament and assented to. It will not be expanded to deal with provisions inserted in this Act after assent.

(2) Column 3 of the table contains additional information that is not part of this Act. Information in this column may be added to or edited in any published version of this Act.

Each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

Section 170 of the Income Tax Assessment Act 1936 does not prevent the amendment of an assessment made before the commencement of this section for the purposes of giving effect to this Act.

1 Section 13‑1 (after table item headed “eligible termination payments (ETPs)”)

Insert:

entrepreneurs’ tax offset |

| |

see simplified tax system |

| |

2 Section 13‑1 (table item headed “partnerships”)

After “dividends”, insert “and simplified tax system”.

3 Section 13‑1 (after table item headed “sickness benefits”)

Insert:

simplified tax system |

| |

25% entrepreneurs’ tax offset...................... | Subdivision 61‑J | |

4 Section 13‑1 (table item headed “trusts”)

After “dividends”, insert “and simplified tax system”.

5 After Subdivision 61‑I

Insert:

This Subdivision provides a 25% tax offset on your income tax liability related to the business income of a business in the simplified tax system with annual group turnover of less than $75,000.

Your entitlement to the offset varies depending on what kind of entity you are. The amount of your offset varies depending on whether the annual group turnover is $50,000 or less or is more than $50,000.

You may be entitled to more than 1 tax offset. For example, if you are an individual STS taxpayer running your own business, you may be entitled to a tax offset under section 61‑505. If you are also a beneficiary of a trust that is an STS taxpayer, you may be entitled to a tax offset under section 61‑520.

Table of sections

Operative provisions

61‑505 25% entrepreneurs’ tax offset: individual or company

61‑510 25% entrepreneurs’ tax offset: partner in a partnership

61‑515 25% entrepreneurs’ tax offset: trustee of a trust

61‑520 25% entrepreneurs’ tax offset: beneficiary of a trust

61‑525 Meaning of net STS income and STS annual turnover

Entitlement

(1) You are entitled to a *tax offset for an income year if:

(a) you are an individual or a company; and

(b) you are an *STS taxpayer for the year; and

(c) your *STS group turnover for the year is less than $75,000; and

(d) you have *net STS income for the year.

Amount

(2) The amount of your *tax offset is worked out in this way:

Method statement

Step 1. Work out your taxable income for the income year.

Step 2. Work out 25% of your basic income tax liability for the year (as worked out in step 2 of the method statement in subsection 4‑10(3)).

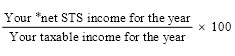

Step 3. Work out the percentage (the STS percentage) using the formula:

If that percentage is more than 100%, the STS percentage is 100%.

Step 4. If your *STS group turnover for the year is $50,000 or less, multiply the amount at step 2 by the STS percentage: the result is the amount of your *tax offset.

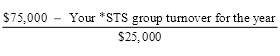

Step 5. If your *STS group turnover for the year is more than $50,000, work out the fraction (the STS phase‑out fraction) using the formula:

The amount of your *tax offset is worked out using the formula:

![]()

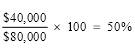

Example: A company runs a local sports business. The company is an STS taxpayer for the year. The company’s STS group turnover for the year is $50,000, the company’s net STS income for the year is $40,000 and the company’s taxable income for the year is $80,000.

The company is entitled to a tax offset.

The amount of the offset is worked out in this way:

The step 1 amount is $80,000.

The step 2 amount is $6,000: 25% of the company’s basic income tax liability of $24,000 ($80,000 multiplied by the 30% company tax rate).

The step 3 STS percentage is:

The amount of the company’s tax offset (step 4) is:

![]()

Entitlement

(1) You are entitled to a *tax offset for an income year if:

(a) you are a partner in a partnership during the year; and

(b) the partnership is an *STS taxpayer for the year; and

(c) the partnership’s *STS group turnover for the year is less than $75,000; and

(d) the partnership has *net STS income for the year; and

(e) your assessable income for the year includes a share (your net STS income share) of that net STS income.

Amount

(2) The amount of your *tax offset is worked out in this way:

Method statement

Step 1. Work out your taxable income for the income year.

Step 2. Work out 25% of your basic income tax liability for the year (as worked out in step 2 of the method statement in subsection 4‑10(3)).

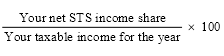

Step 3. Work out the percentage (the STS percentage) using the formula:

If that percentage is more than 100%, the STS percentage is 100%.

Step 4. If the partnership’s *STS group turnover for the year is $50,000 or less, multiply the amount at step 2 by the STS percentage: the result is the amount of your *tax offset.

Step 5. If the partnership’s *STS group turnover for the year is more than $50,000, work out the fraction (the STS phase‑out fraction) using the formula:

The amount of your *tax offset is worked out using the formula:

![]()

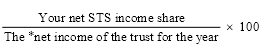

Entitlement

(1) You are entitled to a *tax offset for an income year if:

(a) you are a trustee of a trust during the year; and

(b) the trust is an *STS taxpayer for the year; and

(c) the trust’s *STS group turnover for the year is less than $75,000; and

(d) the trust has *net STS income for the year; and

(e) you are liable to be assessed under section 98, 99 or 99A of the Income Tax Assessment Act 1936 on a share (your net STS income share) of that net STS income.

Amount

(2) The amount of your *tax offset is worked out in this way:

Method statement

Step 1. Work out the *net income of the trust for the income year.

Step 2. Work out 25% of the amount of income tax you are liable to pay for the year on that *net income (apart from any *tax offsets).

Step 3. Work out the percentage (the STS percentage) using the formula:

If that percentage is more than 100%, the STS percentage is 100%.

Step 4. If the trust’s *STS group turnover for the year is $50,000 or less, multiply the amount at step 2 by the STS percentage: the result is the amount of your *tax offset.

Step 5. If the trust’s *STS group turnover for the year is more than $50,000, work out the fraction (the STS phase‑out fraction) using the formula:

The amount of your *tax offset is worked out using the formula:

![]()

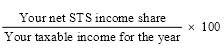

Entitlement

(1) You are entitled to a *tax offset for an income year if:

(a) you are a beneficiary of a trust during the year; and

(b) the trust is an *STS taxpayer for the year; and

(c) the trust’s *STS group turnover for the year is less than $75,000; and

(d) the trust has *net STS income for the year; and

(e) your assessable income for the year includes a share (your net STS income share) of that net STS income.

Amount

(2) The amount of your *tax offset is worked out in this way:

Method statement

Step 1. Work out your taxable income for the income year.

Step 2. Work out 25% of your basic income tax liability for the year (as worked out in step 2 of the method statement in subsection 4‑10(3)).

Step 3. Work out the percentage (the STS percentage) using the formula:

If that percentage is more than 100%, the STS percentage is 100%.

Step 4. If the trust’s *STS group turnover for the year is $50,000 or less, multiply the amount at step 2 by the STS percentage: the result is the amount of your *tax offset.

Step 5. If the trust’s *STS group turnover for the year is more than $50,000, work out the fraction (the STS phase‑out fraction) using the formula:

The amount of your *tax offset is worked out using the formula:

![]()

Net STS income

(1) An entity’s net STS income for an income year is the amount by which the entity’s *STS annual turnover for the year is more than the sum of the entity’s deductions attributable to that turnover.

STS annual turnover

(2) An entity’s STS annual turnover for an income year is the sum of the *value of the business supplies the entity made in the year.

(3) To the extent that the *taxable supplies an entity makes in an income year includes *gambling supplies, use an amount equal to 11 times the entity’s *global GST amount for those supplies rather than the *value of the business supplies in working out the entity’s *STS annual turnover.

(4) In working out the *value of the business supplies made by an entity, disregard:

(a) any *supply made to the extent that the consideration for the supply is a payment or a supply by an insurer in settlement of a claim under an insurance policy; and

(b) to the extent that a supply is constituted by a loan—any repayment of principal, and any obligation to repay principal.

6 At the end of section 328‑5

Add:

Note: If you choose to become an STS taxpayer, you may be entitled to the 25% entrepreneurs’ tax offset: see Subdivision 61‑J.

7 Subsection 328‑365(1) (note)

Omit “Note”, substitute “Note 1”.

8 At the end of subsection 328‑365(1)

Add:

Note 2: If you choose to become an STS taxpayer, you may be entitled to the 25% entrepreneurs’ tax offset: see Subdivision 61‑J.

9 Subsection 995‑1(1)

Insert:

net STS income has the meaning given by section 61‑525.

10 Subsection 995‑1(1)

Insert:

STS annual turnover has the meaning given by section 61‑525.

11 Application

The amendments made by items 1 to 10 apply to assessments for the first income year starting on or after 1 July 2005 and later income years.

12 Section 45‑340 in Schedule 1 (before paragraph (a) of step 1 of the method statement)

Insert:

(aaa) Subdivision 61‑J of the Income Tax Assessment Act 1997 (the 25% entrepreneurs’ tax offset); or

13 Application

The amendment made by item 12 applies in relation to the calculation of an entity’s adjusted tax:

(a) for a base year that is the first income year starting on or after 1 July 2005 or is a later income year; and

(b) only for the purposes of a PAYG instalment period that includes, or starts after, the day on which this Act receives the Royal Assent.

1 Subsection 6‑5(4) (note)

Repeal the note.

2 Subsection 8‑1(3) (note 1)

Omit “Note 1”, substitute “Note”.

3 Subsection 8‑1(3) (note 2)

Repeal the note.

4 Subsection 70‑15(3) (note 1)

Omit “Note 1”, substitute “Note”.

5 Subsection 70‑15(3) (note 2)

Repeal the note.

6 Section 328‑5

Omit “3”.

7 Section 328‑5

Omit:

• you use a cash accounting system for ordinary income, general deductions and deductions for tax‑related expenses and repairs; and

8 Section 328‑10

Repeal the section.

9 Subdivision 328‑C

Repeal the Subdivision.

10 Before Division 330

Insert:

Table of sections

328‑115 When you stop using the STS accounting method

328‑120 Continuing to use the STS accounting method

328‑125 Meaning of STS accounting method

328‑440 Becoming an STS taxpayer after stopping to be one

(1) This section sets out what happens to your ordinary income and general deductions, and deductions under section 25‑5 or 25‑10 of the Income Tax Assessment Act 1997, if:

(a) you are an STS taxpayer for an income year and for the following income year (the changeover year); and

(b) you were using the STS accounting method for the income year before the changeover year; and

(c) you change to an accruals accounting method for the changeover year.

(2) This section also sets out what happens to your ordinary income and general deductions, and deductions under section 25‑5 or 25‑10 of the Income Tax Assessment Act 1997, if:

(a) you stop being an STS taxpayer for an income year (also the changeover year); and

(b) you were using the STS accounting method for the income year before the changeover year; and

(c) you change to an accruals accounting method for the changeover year.

(3) Any ordinary income that, apart from paragraph 328‑105(1)(a) of the Income Tax Assessment Act 1997, you would have derived before the changeover year (while you were an STS taxpayer) and you have not included in your assessable income because you have not received it is included in your assessable income for the changeover year.

(4) Any general deductions, and deductions under section 25‑5 or 25‑10 of the Income Tax Assessment Act 1997, that, apart from paragraph 328‑105(1)(b) of that Act, you would have incurred before the changeover year (while you were an STS taxpayer) and that you have not deducted because you have not paid them can be deducted for the changeover year.

If you were an STS taxpayer for your first income year that started before 1 July 2005, you can continue to use the STS accounting method for your first income year starting on or after 1 July 2005 and later income years while you continue to be an STS taxpayer.

In sections 328‑115 and 328‑120, STS accounting method means the accounting method that was required by the Income Tax Assessment Act 1997 to be used by STS taxpayers for the 2004‑05 income year.

Subsection 328‑440(3) of the Income Tax Assessment Act 1997 does not apply to you, during the period of 5 years starting on 1 July 2005, if you chose to stop being an STS taxpayer for an income year before your first income year starting on or after 1 July 2005.

11 Application

The amendments made by this Schedule apply to assessments for the first income year starting on or after 1 July 2005 and later income years.

1 Section 139A (after table item dealing with Subdivision D)

Insert:

DA | Takeovers and restructures |

2 Subsection 139C(4)

After “The taxpayer does not”, insert “(except for the purposes of Subdivision DA)”.

3 Paragraph 139CA(2)(b)

Before “the later of”, insert “subject to subsection (4),”.

4 At the end of section 139CA

Add:

(4) Paragraph (2)(b) does not apply in relation to a share that, because of section 139DQ, is treated, for the purposes of this Division, as if it were a continuation of a share acquired under an employee share scheme.

Note: Subdivision DA can affect whether the taxpayer is treated as having disposed of a share or ceased employment.

5 Paragraphs 139CB(1)(c) and (d)

Before “if the right is exercised”, insert “subject to subsection (3),”.

6 After paragraph 139CB(1)(d)

Insert:

(da) if subsection (3) applies—the time when the taxpayer disposes of the share referred to in paragraph (3)(b);

7 At the end of section 139CB

Add:

Note: Subdivision DA can affect whether the taxpayer is treated as having disposed of a right or ceased employment.

(3) Paragraphs (1)(c) and (d) do not apply in relation to a right if:

(a) a share has been or is acquired as a result of the exercise of the right; and

(b) because of section 139DQ, another share is treated, for the purposes of this Division, as if it were a continuation of that share.

8 At the end of section 139CC

Add:

Note: Section 139DS can affect the amount of consideration that the taxpayer is treated as having paid or given.

9 After subsection 139DD(2)

Insert:

(2A) To avoid doubt, the taxpayer does not lose the right if, because of section 139DQ, another right is treated, for the purposes of this Division, as if it were a continuation of that right.

10 After subsection 139DD(3)

Insert:

(3A) To avoid doubt, the company does not cease to be the employer of the taxpayer or a holding company of the employer of the taxpayer if, because of section 139DQ, the taxpayer’s employment by another company is treated, for the purposes of this Division, as if it were a continuation of that employment.

11 After Subdivision D of Division 13A of Part III

Insert:

The object of this Subdivision is to allow this Division to continue to apply, in appropriate circumstances, to 100% takeovers or restructures of companies that have employee share schemes.

Treating acquisitions as continuations of existing shares etc.

(1) To the extent that:

(a) a taxpayer acquires:

(i) shares in a company (the new company) that can reasonably be regarded as matching shares in another company (the old company) that the taxpayer had acquired under an employee share scheme; or

(ii) rights in a company (the new company) that can reasonably be regarded as matching rights in another company (the old company) that the taxpayer had acquired under an employee share scheme; and

(b) the acquisition occurs in connection with a 100% takeover, or a restructure, of the old company; and

(c) as a result of the takeover or restructure, the taxpayer ceased to hold the shares or rights in the old company;

then, if the conditions in section 139DR are met, the matching shares or rights are treated, for the purposes of this Division, as if they were a continuation of the shares or rights in the old company.

Note: In determining to what extent something can reasonably be regarded as matching shares or rights in the old company, one of the factors to consider is the respective market values of that thing and of those shares or rights.

Treating acquisitions as disposals of existing shares etc.

(2) However, to the extent that, in connection with the takeover or restructure, the taxpayer acquires anything that:

(a) can reasonably be regarded as matching shares or rights in the old company that the taxpayer had acquired under an employee share scheme; but

(b) is not a matching share or right to which subsection (1) applies;

the taxpayer is treated, for the purposes of this Division, as having disposed of shares, or disposed of rights (other than by exercising them), that the taxpayer held, under an employee share scheme, in the old company immediately before the takeover or restructure.

Treating new employment as continuation of existing employment

(3) If subsection (1) applies, any employment of the taxpayer in:

(a) the new company; or

(b) a holding company of the new company; or

(c) a subsidiary of the new company or of a holding company of the new company;

is treated, for the purposes of this Division, as a continuation of the employment in respect of which he or she acquired the shares or rights in the old company or in a subsidiary of the old company.

(1) The first condition is that, immediately before the takeover or restructure, the taxpayer held shares or rights in the old company under an employee share scheme.

(2) The second condition is that, at or about the time the taxpayer acquires the matching shares or rights, the taxpayer is an employee of:

(a) the new company; or

(b) a holding company of the new company; or

(c) a subsidiary of the new company or of a holding company of the new company.

(3) The third condition is that:

(a) to the extent that the matching shares or rights are shares, they are ordinary shares; or

(b) to the extent that the matching shares or rights are rights, they are rights to acquire ordinary shares.

(4) The fourth condition is that, if subsection 139DQ(1) did not apply, the cessation time, for the shares or rights in the old company to which the matching shares or rights relate, would occur as a result of the takeover or restructure.

(5) The fifth condition is that, at the time the taxpayer acquires the matching shares or rights, the taxpayer does not hold a legal or beneficial interest in more than 5% of the shares of the new company.

(6) The sixth condition is that, at that time, the taxpayer is not in a position to cast, or control the casting of, more than 5% of the maximum number of votes that may be cast at a general meeting of the new company.

(1) If:

(a) subsection 139DQ(1) applies to shares or rights that the taxpayer has acquired; and

(b) the taxpayer had paid or given consideration (the original consideration) for an acquisition, under an employee share scheme, of any of the shares or rights in the old company (the original shares or rights);

the taxpayer is treated as having paid or given, for any of the apportionable assets for the original shares or rights, consideration of an amount worked out by spreading the original consideration proportionately among all the apportionable assets according to their market values immediately after the takeover or restructure.

Note: Subsection 139FA(4) alters the meaning of market value of a share or right for the purposes of this section.

(2) The apportionable assets for the original shares or rights are:

(a) all matching shares or rights held by the taxpayer that are treated because of this Division as a continuation of the original shares or rights; and

(b) anything else that the taxpayer acquired in connection with the takeover or restructure and that can reasonably be regarded as matching the original shares or rights; and

(c) in the case of a restructure—any shares or rights in the old company that the taxpayer held immediately before, and continues to hold immediately after, the restructure and that can reasonably be regarded as matching the original shares or rights.

12 At the end of section 139FA

Add:

(4) This section applies for the purposes of section 139DS as if references in this section to the one week period up to and including that day were references to the period consisting of that day.

13 Section 139GC

Omit “Corporations Law”, substitute “Corporations Act 2001”.

14 After section 139GC

Insert:

The expression subsidiary has the same meaning as in the Corporations Act 2001.

A 100% takeover of a company by another company is an arrangement that is intended to result in the company becoming a 100% subsidiary of the other company, or of a holding company or subsidiary of the other company.

A restructure of a company is a change in the ownership, or the structure of the ownership, of the company as a result of which some or all shares or rights held in the company under an employee share scheme immediately before the change:

(a) are replaced; or

(b) could reasonably be regarded as having been replaced;

wholly or partly by shares or rights in one or more other companies.

15 Section 139GH (before the table item dealing with Acquiring a share or right)

Insert:

100% takeover | 139GCB |

16 Section 139GH (at the end of the table)

Add:

Restructure | 139GCC |

Subsidiary | 139GCA |

17 Subsection 130‑80(1)

Repeal the subsection, substitute:

(1) This section sets out what happens if you:

(a) *acquire a *share or right at a discount (within the meaning of Subdivision C of Division 13A of Part III of the Income Tax Assessment Act 1936) under an *employee share scheme; or

(b) acquire a share or right that, because of section 139DQ of that Act, is treated, for the purposes of Division 13A of Part III of that Act, as if it were a continuation of a share or right acquired under an employee share scheme.

18 After subsection 130‑83(1)

Insert:

(1A) If:

(a) a *CGT event happens in relation to the *share or right (the original share or right); and

(b) it happens in connection with an acquisition (within the meaning of Subdivision C of Division 13A of Part III of the Income Tax Assessment Act 1936) of another share or right (the matching share or right); and

(c) under section 139DQ of the Income Tax Assessment Act 1936 the matching share or right is treated, for the purposes of Division 13A of Part III of that Act, as if it were a continuation of the original share or right;

any *capital gain or *capital loss you make from the CGT event is disregarded.

19 Section 130‑90 (heading)

Repeal the heading, substitute:

20 Subsection 130‑90(3)

Repeal the subsection, substitute:

(3) Either:

(a) the individual, *associate or affiliate company must have acquired the *share or right under an *employee share scheme; or

(b) the share or right must, because of section 139DQ of the Income Tax Assessment Act 1936, be a share or right that is treated, for the purposes of Division 13A of Part III of that Act, as if it were a continuation of a share or right acquired under an employee share scheme.

21 At the end of Subdivision 130‑D

Add:

If:

(a) a *CGT event happens in relation to a *share or right (the original share or right); and

(b) it happens in connection with an acquisition (within the meaning of Subdivision C of Division 13A of Part III of the Income Tax Assessment Act 1936) of another share or right (the matching share or right) by the beneficiary of an *employee share trust; and

(c) under section 139DQ of the Income Tax Assessment Act 1936 the matching share or right is treated, for the purposes of Division 13A of Part III of that Act, as if it were a continuation of the original share or right;

any *capital gain or *capital loss the trustee of the employee share trust makes from the CGT event is disregarded.

22 Application

(1) The amendments made by this Schedule apply, and are taken to have applied, to acquisitions of shares or rights on or after 1 July 2004.

(2) In this item:

acquisition, of a share or right, has the same meaning as in Division 13A of Part III of the Income Tax Assessment Act 1936.

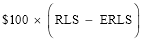

1 Paragraph 58Q(1)(c) (formula)

Repeal the formula, substitute:

![]()

2 Paragraph 58Q(1)(d) (formula)

Repeal the formula, substitute:

![]()

3 Application

The amendments made by this Schedule apply to FBT years beginning on or after 1 April 2005.

1 Section 2

Insert:

designated frontier area means that block or those blocks that constitute both:

(a) an area or part of an area:

(i) specified in section 36A; or

(ii) specified in an instrument made under subsection 36B(1); and

(b) an exploration permit area.

2 Section 2

Insert:

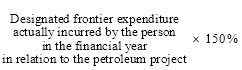

designated frontier expenditure, in relation to a petroleum project and a financial year, means exploration expenditure that is actually incurred:

(a) by a person in that year where the eligible exploration or recovery area in relation to the project is a designated frontier area; and

(b) during the original period of the exploration permit concerned (before the permit is first renewed or ceases to be in force);

other than exploration expenditure that is incurred in evaluating or delineating a petroleum pool (within the meaning of the Petroleum (Submerged Lands) Act 1967) that has been discovered in a designated frontier area.

3 Section 2

Insert:

uplifted frontier expenditure has the meaning given by section 36C.

4 After section 36

Insert:

For the purposes of the definition of designated frontier area, the following areas are specified:

(a) Area T04‑5, as first gazetted in the Tasmanian Government Gazette on 5 May 2004 under subsection 20(1) of the Petroleum (Submerged Lands) Act 1967;

(b) Areas W04‑2, W04‑4, W04‑15 and W04‑16, as first gazetted in the Western Australia Government Gazette on 30 March 2004 under subsection 20(1) of the Petroleum (Submerged Lands) Act 1967;

(c) Area NT04‑3, as first gazetted in the Northern Territory Government Gazette on 14 April 2004 under subsection 20(1) of the Petroleum (Submerged Lands) Act 1967.

Note: An amount of exploration expenditure incurred in respect of an area that is specified under this section might be increased by 150% (before the GDP factor or the augmented bond rate is applied to the amount under the Schedule): see section 36C.

(1) For the purposes of the definition of designated frontier area, the Minister administering the Petroleum (Submerged Lands) Act 1967 may designate, in writing, up to (and including) 20% of potential exploration permit areas as frontier areas.

Note: An amount of exploration expenditure incurred in respect of an area that is specified under this section might be increased by 150% (before the GDP factor or the augmented bond rate is applied to the amount under the Schedule): see section 36C.

(2) The Minister must not specify new areas for a calendar year after 2008.

(3) The Minister must publish an instrument made under subsection (1) in the Gazette.

(4) An instrument made under subsection (1) is not a legislative instrument for the purposes of the Legislative Instruments Act 2003.

(5) The Minister may, by signed instrument, delegate his or her power under subsection (1) to an SES employee or an acting SES employee in the Minister’s Department.

Note: The expressions SES employee and acting SES employee are defined in section 17AA of the Acts Interpretation Act 1901.

(6) In this section:

potential exploration permit area means an area or areas constituted by a block or blocks in respect of which applications for exploration permits have been invited, but not yet granted, under Division 2 of Part III of the Petroleum (Submerged Lands) Act 1967.

For the purposes of this Act, the amount of uplifted frontier expenditure that a person is taken to have incurred in a financial year in relation to a petroleum project is worked out as follows:

5 Subsection 45C(9)

Omit “, within 60 days of being given the notice, lodge with the Commissioner a written objection against the decision setting out fully and in detail the grounds on which the person relies”, substitute “object against the decision in the manner set out in Part IVC of the Taxation Administration Act 1953”.

6 Subsection 45C(10)

Repeal the subsection.

7 Clause 1 of the Schedule (definition of incurred exploration expenditure amount)

Repeal the definition, substitute:

incurred exploration expenditure amount, in relation to a petroleum project that is not a combined project and in relation to a financial year, means the sum of the following:

(a) any amounts of exploration expenditure (other than designated frontier expenditure) actually incurred by the person in the financial year in relation to the project;

(b) any amounts of uplifted frontier expenditure that the person is taken by section 36C to have incurred in the financial year in relation to the project;

(c) any amounts of expenditure that the person is taken by subparagraph 48(1)(a)(ia) or paragraph 48A(5)(c) to have incurred in the financial year in relation to the project.

Note: The effect of subsections 35A(2), 35B(2) and 45D(3) must be taken into account when working out an incurred exploration expenditure amount.

8 Clause 1 of the Schedule

Insert:

incurred exploration expenditure amount, in relation to a petroleum project that is a combined project and in relation to a financial year, means the sum of the following:

(a) any amounts of:

(i) exploration expenditure (other than designated frontier expenditure) actually incurred by the person; and

(ii) uplifted frontier expenditure that the person is taken by section 36C to have incurred;

in the financial year in relation to the project (not being amounts incurred before the project combination certificate in relation to the project came into force);

(b) any amounts of expenditure that the person is taken by subparagraph 48(1)(a)(ia) or paragraph 48A(5)(c) to have incurred in the financial year in relation to the project;

(c) if the project combination certificate came into force during the financial year:

(i) any amounts of exploration expenditure (other than designated frontier expenditure) actually incurred by the person in the financial year; and

(ii) any amounts of uplifted frontier expenditure that the person is taken by section 36C to have incurred in the financial year; and

(iii) any amounts of exploration expenditure that the person is taken by section 48 or 48A to have incurred in the financial year;

in relation to the pre‑combination projects.

Note: The effect of subsections 35A(2), 35B(2) and 45D(3) must be taken into account when working out an incurred exploration expenditure amount.

9 Paragraph 15(1)(a) of the Schedule

After “incurred exploration expenditure”, insert “, or is taken to have incurred uplifted frontier expenditure,”.

10 Subclause 15(1) of the Schedule

Omit “all of the exploration expenditure is non‑transferable expenditure”, substitute “the total of the amounts of exploration expenditure (other than designated frontier expenditure), and uplifted frontier expenditure, is taken to be non‑transferable expenditure”.

11 Paragraph 15(2)(b) of the Schedule

Repeal the paragraph, substitute:

(b) the total of:

(i) any amounts of exploration expenditure (other than designated frontier expenditure) actually incurred by the person; and

(ii) any amounts of uplifted frontier expenditure taken to be incurred by the person in respect of designated frontier expenditure actually incurred by the person;

in relation to the notional project in the financial year exceeds the excess referred to in paragraph (a) by an amount (the non‑transferable amount);

12 Subclause 15(2) of the Schedule

Omit “so much of the exploration expenditure as equals the non‑transferable amount is non‑transferable expenditure”, substitute “so much of the expenditure as equals the non‑transferable amount is taken to be non‑transferable expenditure”.

13 Paragraph 15(3)(b) of the Schedule

Omit “the exploration expenditure incurred”, substitute “any exploration expenditure (other than designated frontier expenditure) incurred, or any uplifted frontier expenditure taken to be incurred,”.

14 Paragraph 15(4)(c) of the Schedule

Repeal the paragraph, substitute:

(c) add amounts in accordance with the following rules:

(i) start with the oldest amount of any exploration expenditure (other than designated frontier expenditure) incurred, or any uplifted frontier expenditure taken to be incurred, by the person in the financial year;

(ii) add to that, in order starting with the next oldest amount, each of the other amounts incurred, or taken to be incurred, by the person in the financial year;

(iii) if adding an amount of expenditure would make the total exceed the non‑transferable amount, add only so much of the amount as makes the total equal the non‑transferable amount and do not add any later amount of expenditure;

15 Paragraph 15(4)(d) of the Schedule

Omit “subparagraphs (c)(i) and (ii)”, substitute “paragraph (c)”.

16 Paragraph 16(c) of the Schedule

Repeal the paragraph, substitute:

(c) the total of:

(i) any amounts of exploration expenditure (other than designated frontier expenditure) actually incurred by the person; and

(ii) any amounts of uplifted frontier expenditure taken to be incurred by the person in respect of designated frontier expenditure actually incurred by the person;

in relation to the notional project during the period starting on 1 July 1990 and ending at the end of the assessable year;

17 Application

(1) The amendments made by this Schedule (other than items 5 and 6) apply in respect of any exploration expenditure incurred (whether before or after this Schedule commences) where the eligible exploration or recovery area is a designated frontier area.

(2) The amendments made by items 5 and 6 apply in respect of any objection made (whether before or after that item commences) that has not yet been finally determined or otherwise disposed of.

1 Application

The amendments made by this Schedule apply on and after 1 July 2002.

2 At the end of section 711‑45

Add:

Adjustment where amount of liability differed for purpose of calculating allocable cost amount on entry

(8) If:

(a) a leaving entity’s liability mentioned in any preceding subsection was taken into account in working out the *allocable cost amount for a *subsidiary member (whether or not the leaving entity) of the old group in accordance with Division 705 (the entry ACA); and

(b) the amount (the entry amount) of the liability that was so taken into account is different from the amount (the exit amount) of the liability taken into account in applying the subsection; and

(c) the entry ACA was different from what it would have been if the exit amount, instead of the entry amount, had been taken into account in working it out;

then, for the purpose of applying the subsection, the liability is taken to be of an amount equal to the entry amount.

3 Subsection 705‑90(6)

Repeal the subsection, substitute:

Undistributed profits must have accrued to joined group

(6) Next, work out the extent to which the undistributed profits that satisfy the requirements of subsection (3) accrued to the joined group before the joining time (subsection (7) states what it means for a profit to accrue to the joined group before the joining time). The result is the step 3 amount.

4 Paragraph 701‑30(2)(a)

Omit “, and paragraph (6)(b),”.

5 At the end of Division 709

Add:

An entity can deduct a bad debt that:

(a) has for a period been owed to a member of a consolidated group; and

(b) has for another period been owed to an entity that was not a member of that group;

only if each entity that has been owed the debt for such a period could have deducted the debt had it been written off as bad at the end of the period. This applies even if the debt is owed to the same entity for different periods.

Table of sections

Application and object

709‑205 Application of this Subdivision

709‑210 Object of this Subdivision

Limit on deduction of bad debt

709‑215 Limit on deduction of bad debt

(1) This Subdivision affects whether an entity (the claimant) that is or has been a *member of a *consolidated group and writes off a debt, or part of a debt, as bad may deduct the debt or part if the conditions in subsection (2) exist.

(2) The conditions are that, in the time starting when the debt was incurred (whether to the claimant or another entity) and ending when the claimant wrote off the debt or part:

(a) the debt was owed to an entity (whether the claimant or another entity) for a period (a debt test period) when the entity was a *member of a *consolidated group; and

(b) the debt was owed to an entity (whether the claimant or another entity) for a period (also a debt test period) when the entity was a not a member of that group.

Note 1: The debt must have been owed to the claimant for at least one of the debt test periods for the claimant to have been able to write it off.

Note 2: One effect of section 701‑1 (Single entity rule) is that a debt is taken to be owed to the head company of a consolidated group while the debt is owed to a subsidiary member of the group.

(3) Ignore section 701‑5 (Entry history rule) and section 701‑40 (Exit history rule) in identifying a debt test period.

Note: Subsection (3) does not affect sections 701‑5 and 701‑40 so far as they operate to treat the debt, or part of the debt, as having been included in the claimant’s assessable income. That inclusion is generally a condition under section 25‑35 for the claimant to be able to deduct the debt.

(4) This Subdivision does not apply in relation to a debt merely because it is assigned:

(a) from an entity that is a *member of a *consolidated group to an entity that is not a member of that group; or

(b) from an entity that is not a member of a consolidated group to an entity that is a member of a consolidated group; or

(c) from an entity that is a member of a consolidated group to an entity that is a member of another consolidated group.

This subsection has effect despite subsections (1) and (2).

Note: There is not an assignment of a debt from one entity to another merely because section 701‑1 (Single entity rule) starts or ceases to apply in relation to the entities so that the debt ceases to be a debt owed to one entity and becomes a debt owed to the other entity.

The main object of this Subdivision is to ensure that the claimant can deduct the debt, or part of it, only if each entity that was owed the debt for a debt test period could have deducted the debt if it had been written off as bad at the end of the period.

(1) The claimant can deduct the debt, or part of the debt, if, and only if:

(a) section 8‑1 or 25‑35 permits the deduction (ignoring subsection 25‑35(5) and the provisions mentioned in that subsection); and

(b) the condition in subsection (2) is met for each debt test period.

(2) The condition is that the entity that was owed the debt for the debt test period could have deducted the debt for an income year (the debt test income year) starting and ending at the times identified in subsection (3) if:

(a) the entity had written off the debt as bad at the end of the period; and

(b) these provisions (the modified provisions) had effect as described in this section:

(i) sections 165‑123 and 165‑126 (which are about conditions that must be met for a company to be able to deduct a bad debt);

(ii) sections 266‑35, 266‑85, 266‑120, 266‑160 and 267‑25 in Schedule 2F to the Income Tax Assessment Act 1936 (which are about conditions that must be met for certain kinds of trusts to be able to deduct a bad debt);

(iii) other provisions of this Act so far as they relate to a section listed in subparagraph (i) or (ii); and

(c) these provisions did not apply:

(i) subsections 165‑120(2) and (3);

(ii) section 267‑65 in Schedule 2F to the Income Tax Assessment Act 1936.

Note 1: Some of the other provisions of this Act that relate to a section listed in subparagraph (2)(b)(i) are sections 165‑120, 165‑129 and 165‑132 and Subdivision 166‑C.

Note 2: Some of the other provisions of this Act that relate to a section listed in subparagraph (2)(b)(ii) are sections 266‑40, 266‑45, 266‑90, 266‑125, 266‑165, 267‑30, 267‑35, 267‑40 and 267‑45 in Schedule 2F to the Income Tax Assessment Act 1936.

Debt test income year

(3) The table shows when the debt test income year starts and ends.

Start and end of debt test income year | |||

| If: | The start of the debt test income year is: | The end of the debt test income year is: |

1 | Both these conditions are met: (a) the entity that is owed the debt for the debt test period is the claimant; (b) the period ends at the time (the write‑off time) the claimant actually writes off the debt or part of the debt | The later of these times (or either of them if they are the same): (a) the start of the income year in which the write‑off time occurs; (b) the start of the debt test period | The end of the income year in which the write‑off time occurs |

2 | Either: (a) the entity that is owed the debt for the debt test period is not the claimant; or (b) that entity is the claimant but that period ends before the claimant actually writes off the debt or part of the debt | The later of these times (or either of them if they are the same): (a) 12 months before the end of the debt test period; (b) the start of the debt test period | The end of the debt test period |

Continuity periods, ownership test periods and test periods

(4) For the purposes of subsection (2), the modified provisions have effect as if:

(a) the *first continuity period started at the start time shown in the table and ended at the start of the debt test income year; and

(b) the *second continuity period were the debt test income year or, for the purposes of section 165‑123 and Subdivision 166‑C defining periods by reference to the second continuity period, the period:

(i) starting at the start of the debt test income year; and

(ii) ending at the end time shown in the table; and

(c) each section listed in subparagraph (2)(b)(ii) specified that the test period identified in the section:

(i) started at the start time shown in the table; and

(ii) ended at the end time shown in the table.

Start time and end time | |||

| If: | The start time is: | The end time is: |

1 | All these conditions are met: (a) the entity that is owed the debt for the debt test period is the claimant; (b) the period ends at the time (the write‑off time) the claimant actually writes off the debt or part of the debt; (c) the claimant is the *head company of a *consolidated group at the write‑off time | The start of the debt test period | The end of the income year in which the write‑off time occurs |

2 | All these conditions are met: (a) the entity that is owed the debt for the debt test period is the claimant; (b) the period ends at the time (the write‑off time) the claimant actually writes off the debt or part of the debt; (c) the claimant is not the *head company of a *consolidated group at the write‑off time | Just before the start of the debt test period | The end of the income year in which the write‑off time occurs |

3 | The debt test period: (a) starts at a time other than a time when the entity that is owed the debt for the period ceases to be a *member of a *consolidated group; and (b) ends when the entity becomes a member of such a group; (whether or not the entity was the *head company of another such group during the period) | The start of the debt test period | Just after the end of the debt test period |

4 | Both these conditions are met: (a) the entity that is owed the debt for the debt test period is the *head company of a *consolidated group; (b) the period ends when: (i) a *subsidiary member of the group becomes a *member of another consolidated group; or (ii) the entity ceases to be the head company of the group without becoming a member of another consolidated group | The start of the debt test period | The end of the debt test period |

5 | The debt test period: (a) starts when the entity that is owed the debt for the period ceases to be a *member of a *consolidated group; and (b) ends later when the entity becomes a member of a consolidated group | Just before the start of the debt test period | Just after the end of the debt test period |

(5) For the purposes of subsection (2), the modified provisions have effect as if section 267‑25 in Schedule 2F to the Income Tax Assessment Act 1936 applied in relation to debts whether they were incurred in the income year or an earlier income year.

Test time for same business test under section 165‑126

(6) For the purposes of subsection (2), the modified provisions have effect as if subsection 165‑126(2) specified that the test time were the later of these times (or either of them if they are the same):

(a) the first time at which it is not practicable to show that the company will meet the conditions in section 165‑123 (as modified by this section);

(b) the time just after the start of the debt test period.

Business at and just after the end of the debt test period

(7) If:

(a) the debt test period ends when the entity that was owed the debt for the period becomes a *member of a *consolidated group; and

(b) under the modified provisions, the *business that the entity carried on at or just after the end of the period is relevant to the question whether the entity could have deducted the debt as described in subsection (2);

those provisions have effect for the purposes of that subsection as if the entity carried on at those times the business it carried on just before the end of the period.

6 At the end of subsection 266‑35(1) in Schedule 2F

Add:

Note: Subdivision 709‑D of the Income Tax Assessment Act 1997 modifies how this section operates in relation to a trust that used to be a member of a consolidated group and that writes off as bad a debt that used to be owed to a member of the group.

7 At the end of subsection 266‑85(3) in Schedule 2F

Add:

Note: Subdivision 709‑D of the Income Tax Assessment Act 1997 modifies how this section operates in relation to a trust that used to be a member of a consolidated group and that writes off as bad a debt that used to be owed to a member of the group.

8 At the end of subsection 266‑120(1) in Schedule 2F

Add:

Note: Subdivision 709‑D of the Income Tax Assessment Act 1997 modifies how this section operates in relation to a trust that used to be a member of a consolidated group and that writes off as bad a debt that used to be owed to a member of the group.

9 At the end of subsection 266‑160(2) in Schedule 2F

Add:

Note: Subdivision 709‑D of the Income Tax Assessment Act 1997 modifies how this section operates in relation to a trust that used to be a member of a consolidated group and that writes off as bad a debt that used to be owed to a member of the group.

10 At the end of subsection 267‑25(1) in Schedule 2F

Add:

Note: Subdivision 709‑D of the Income Tax Assessment Act 1997 affects the application of this section to a trust that used to be a member of a consolidated group and that writes off as bad a debt that used to be owed to a member of the group.

11 At the end of subsection 267‑65(1) in Schedule 2F

Add:

Note: Subdivision 709‑D of the Income Tax Assessment Act 1997 modifies how this section operates in relation to a trust that used to be a member of a consolidated group and that writes off as bad a debt that used to be owed to a member of the group.

12 Section 12‑5 (table item headed “bad debts”)

After:

debt/equity swaps .......................... | 63E, 63F |

insert:

deduction of a debt that used to be owed to a member of a consolidated group by an entity that used to be a member of the group | Subdivision 709‑D |

13 Subsection 25‑35(5) (at the end of the table)

Add:

6 | An entity that used to be a member of a consolidated group can deduct a bad debt that used to be owed to a member of the group only if certain conditions are met | Subdivision 709‑D

|

14 At the end of subsection 165‑120(1)

Add:

Note 3: Subdivision 709‑D modifies how this Subdivision operates in relation to a company that used to be a member of a consolidated group and that writes off as bad a debt that used to be owed to a member of the group.

15 Subsection 995‑1(1) (definition of test time)

After “707‑135,”, insert “709‑215,”.

16 After Division 707

Insert:

Table of Subdivisions

709‑D Deducting bad debts

Table of sections

709‑200 Application of Subdivision 709‑D of the Income Tax Assessment Act 1997

Subdivision 709‑D of the Income Tax Assessment Act 1997 applies on and after 1 July 2002.

17 At the end of section 67‑25

Add:

Life insurance company’s subsidiary joining consolidated group

(5) The *tax offset available under subsection 713‑545(5) is subject to the refundable tax offset rules.

18 Subsection 320‑175(2) (notes)

Repeal the notes, substitute:

Note 1: The time when a life insurance company joins or leaves a consolidated group is also a valuation time: see sections 713‑525 and 713‑585.

Note 2: A life insurance company that fails to comply with this section is liable to an administrative penalty: see section 288‑70 in Schedule 1 to the Taxation Administration Act 1953.

19 Subsection 320‑230(2) (notes)

Repeal the notes, substitute:

Note 1: The time when a life insurance company joins or leaves a consolidated group is also a valuation time: see sections 713‑525 and 713‑585.

Note 2: A life insurance company that fails to comply with this section is liable to an administrative penalty: see section 288‑70 in Schedule 1 to the Taxation Administration Act 1953.

20 Group heading before section 713‑505

Repeal the heading, substitute:

21 Section 713‑510

Repeal the section, substitute:

(1) An entity cannot be a *subsidiary member of a *consolidated group or *consolidatable group of which a *life insurance company is a *member if:

(a) the life insurance company owns, either directly or indirectly through one or more interposed entities, all the *membership interests in the entity and either:

(i) some, but not all, of the membership interests described in subsection (3) (the key interests) are *virtual PST assets of the life insurance company; or

(ii) some, but not all, of the key interests are *segregated exempt assets of the life insurance company; or

(b) the life insurance company owns, either directly or indirectly through one or more interposed entities, only some of the membership interests in the entity and any of the key interests are virtual PST assets or segregated exempt assets of the life insurance company.

Note: The entity could, however, be a member of another consolidated group or consolidatable group.

(2) An entity cannot continue to be a *subsidiary member of a *consolidated group of which a *life insurance company is a *member if:

(a) the life insurance company owns, either directly or indirectly through one or more interposed entities, all the *membership interests in the entity and, had the entity not been a subsidiary member of the group, either:

(i) some, but not all, of the membership interests described in subsection (3) (the key interests) would be *virtual PST assets of the life insurance company; or

(ii) some, but not all, of the key interests would be *segregated exempt assets of the life insurance company; or

(b) the life insurance company owns, either directly or indirectly through one or more interposed entities, only some of the membership interests in the entity and, had the entity not been a subsidiary member of the group, any of the key interests would be virtual PST assets or segregated exempt assets of the life insurance company.

(3) The key interests are the *membership interests the *life insurance company owns directly in:

(a) the entity; or

(b) an interposed entity.

(1) This section affects how paragraph 320‑15(1)(h) and section 320‑85 apply if:

(a) a *life insurance company becomes a *subsidiary member of a *consolidated group at a time (the joining time); and

(b) just before the joining time, the life insurance company had one or more liabilities under the *net risk components of life insurance policies.

Note: Paragraph 320‑15(1)(h) and section 320‑85 both operate on the basis of a comparison of the value of the company’s liabilities under the net risk components of life insurance policies at the end of the current year with the value of those liabilities at the end of the previous year, so that:

(a) that paragraph includes an amount in the company’s assessable income for the current year if the value at the end of the current year is less than the value at the end of the previous income year; and

(b) that section allows a deduction for the current year if the value at the end of the current year is more than the value at the end of the previous income year.

(2) The object of this section is to ensure that the *head company of the *consolidated group bears the income tax consequences relating to a change in *value of the liabilities only after the joining time.

Note: The life insurance company bears the income tax consequences relating to a change in value of the liabilities before the joining time, because section 701‑30 ensures that paragraph 320‑15(1)(h) and section 320‑85 apply in relation to a part of the income year before that time when the company was not a subsidiary member of a consolidated group as if that part were an income year.

(3) Paragraph 320‑15(1)(h) and section 320‑85 apply for the head company core purposes set out in section 701‑1 (Single entity rule) as if the *value of the liabilities at the end of the last income year ending before the joining time were the value of the liabilities (for the *life insurance company) just before the joining time.

22 Before section 713‑515

Insert:

23 Section 713‑515 (heading)

Repeal the heading, substitute:

24 Section 713‑520 (heading)

Repeal the heading, substitute:

25 Sections 713‑525 and 713‑530

Repeal the sections, substitute:

Division 320 has effect as if the time when a *life insurance company becomes a *subsidiary member of a *consolidated group were a *valuation time for the purposes of sections 320‑175 and 320‑230.

Note: This means that there must be a valuation of the virtual PST assets and virtual PST liabilities under section 320‑175 (with the consequences set out in section 320‑180), and a valuation of the segregated exempt assets and exempt life insurance policy liabilities under section 320‑230 (with the consequences set out in section 320‑235), as at that time.

(1) This section applies if:

(a) a *life insurance company becomes a *member of a *consolidated group at a time (the joining time); and

(b) just before the joining time, the life insurance company had either:

(i) a *tax loss of the *complying superannuation class; or

(ii) a *net capital loss from *virtual PST assets.

(2) This Act operates (except so far as the contrary intention appears) for the purposes of income years ending after the joining time as if:

(a) the *head company of the *consolidated group had made the loss for the income year in which the joining time occurs; and

(b) the *life insurance company had not made the loss for the income year for which it made the loss.

(3) The *head company is not prevented from *utilising the loss for the income year in which the joining time occurs merely because this Act operates as if the head company had made the loss for that year.

(4) Division 707 does not apply in relation to the *net capital loss or the *tax loss at the joining time.

(1) This section applies if:

(a) a *life insurance company becomes a *member of a *consolidated group at a time (the joining time); and

(b) at the joining time, the life insurance company owns, either directly or indirectly through one or more interposed entities, all the *membership interests in yet another entity (the life insurance subsidiary) that becomes a *subsidiary member of the group at that time; and

(c) all the following membership interests are *virtual PST assets of the life insurance company:

(i) the membership interests (if any) that the life insurance company owns directly in the life insurance subsidiary;

(ii) the membership interests (if any) that the life insurance company owns directly in the interposed entities; and

(d) the *head company of the group makes a *tax loss or *net capital loss under Subdivision 707‑A because of a transfer from the life insurance subsidiary.

(2) This Act operates for the purposes of income years ending after the transfer as if:

(a) the *tax loss were of the *complying superannuation class; or

(b) the *net capital loss were from *virtual PST assets.

(3) Subdivisions 707‑B, 707‑C and 707‑D do not affect the *utilisation of the loss by the *head company of the *consolidated group.

(1) This section applies if:

(a) a *life insurance company becomes a *member of a *consolidated group at a time (the joining time); and

(b) at the joining time, the life insurance company owns, either directly or indirectly through one or more interposed entities, all the *membership interests in yet another entity (the life insurance subsidiary) that becomes a *subsidiary member of the group at that time; and

(c) all the following membership interests are *segregated exempt assets of the life insurance company:

(i) the membership interests (if any) that the life insurance company owns directly in the life insurance subsidiary;

(ii) the membership interests (if any) that the life insurance company owns directly in the interposed entities.

(2) A *tax loss or *net capital loss of the life insurance subsidiary for an income year ending before the joining time cannot be *utilised by the life insurance subsidiary for an income year ending after that time.

Note: This prevents the loss from being transferred to the head company of the consolidated group under Subdivision 707‑A (because it means the life insurance subsidiary could not have utilised the loss for the trial year). As a result, section 707‑150 prevents any other entity from utilising the loss for an income year ending after the joining time.

(1) This section applies if:

(a) a *life insurance company becomes a *member of a *consolidated group at a time (the joining time); and

(b) at the joining time, the life insurance company owns, either directly or indirectly through one or more interposed entities, *membership interests in yet another entity (the life insurance subsidiary) that becomes a *subsidiary member of the group at that time; and

(c) the life insurance subsidiary’s *franking account is in surplus just before the joining time.

(2) Paragraph 709‑60(2)(b) does not apply in relation to the life insurance subsidiary.

(3) A *franking credit arises at the joining time in the *franking account of the *head company of the group. The amount of the credit is the amount worked out under subsection (4).

(4) The amount is equal to the amount of the *franking credit that would arise in the *life insurance company’s *franking account just before the joining time under item 5 of the table in subsection 219‑15(2) if:

(a) the life insurance subsidiary made a *franked distribution to the life insurance company just before the joining time; and

(b) the amount of the franking credit on the distribution were equal to the surplus mentioned in paragraph (1)(c).

(5) The *head company of the group is entitled to a *tax offset for the income year in which the joining time occurs. The amount of the tax offset is:

(a) if all the *membership interests (if any) that the *life insurance company owns directly in the life insurance subsidiary, and all the membership interests (if any) that the life insurance company owns directly in interposed entities, are *segregated exempt assets of the life insurance company—the surplus mentioned in paragraph (1)(c), reduced by the amount worked out under subsection (4); or

(b) if all the membership interests (if any) that the life insurance company owns directly in the life insurance subsidiary, and all the membership interests (if any) that the life insurance company owns directly in interposed entities, are *virtual PST assets of the life insurance company—the amount worked out under subsection (6); or

(c) otherwise—nil.

(6) The amount is worked out using the following formula (or is nil if it would otherwise be negative):

where:

complying superannuation class tax rate means the rate of tax in respect of the *complying superannuation class of the taxable income of a *life insurance company for the income year in which the joining time occurs (see paragraph 23A(b) of the Income Tax Rates Act 1986).

ordinary class tax rate means the rate of tax in respect of the *ordinary class of the taxable income of a life insurance company for the income year in which the joining time occurs (see subparagraph 23A(a)(ii) of the Income Tax Rates Act 1986).

Sections 709‑70 and 709‑75 do not apply in relation to a *subsidiary member of a *consolidated group if:

(a) the subsidiary member is a *life insurance company; or

(b) a life insurance company that is a *member of the group owns *membership interests, either directly or indirectly through one or more interposed entities, in the subsidiary member.

Conditions for sections 713‑555 and 713‑560 to apply

(1) Sections 713‑555 and 713‑560 apply only if both the conditions in subsections (2) and (3) are met.

Note: Each of those sections sets out extra conditions that must also be met for the section to apply.

(2) The first condition is that there is a time (the fusion time) when it starts to be the case that both these entities (the fused entities) are *members of a single *consolidated group:

(a) a *life insurance company;

(b) an entity (the policyholder) holding an *exempt life insurance policy (the fused entities’ policy) that:

(i) was issued when the policyholder and the life insurance company were not both members of a single consolidated group; and

(ii) provided for the life insurance company to pay an *immediate annuity to the policyholder.

(3) The second condition is that the *head company of the *consolidated group determines the following amounts:

(a) the total *transfer value of the head company’s *segregated exempt assets;

(b) the amount of the head company’s *exempt life insurance policy liabilities;

as at a time (the determination time) that is the fusion time or, if the head company does not determine those amounts as at the fusion time, the first time after the fusion time as at which the head company determines those amounts.

Note: If the life insurance company becomes a subsidiary member of the consolidated group, that company’s segregated exempt assets become segregated exempt assets of the head company of the group because of section 701‑5 (Entry history rule) and section 713‑505 (Head company treated as a life insurance company).

Object of sections 713‑555 and 713‑560

(4) The object of sections 713‑555 and 713‑560 is to ensure that the *head company of the *consolidated group:

(a) does not have excessive amounts included in its assessable income because section 701‑1 (Single entity rule) treats the fused entities as one so liabilities under the fused entities’ policy do not contribute to the amount of the head company’s *exempt life insurance policy liabilities as at the determination time; and

(b) has amounts included in its assessable income, or is allowed deductions, to reflect what would have happened to the fused entities if they had not both been *members of the group at any time between the fusion time and the determination time when they were both members of the group.

Application

(1) This section applies if:

(a) as at the determination time, the total *transfer value of the *segregated exempt assets of the *head company of the *consolidated group exceeds the amount of that company’s *exempt life insurance policy liabilities, wholly or partly because:

(i) those assets include assets out of which exempt life insurance policy liabilities attributable to the fused entities’ policy were to have been discharged; and

(ii) while both the fused entities are members of the group, the liability to pay the *annuity is taken not to exist for the head company core purposes set out in section 701‑1 (Single entity rule), because one or more applications of that section treat the fused entities as one entity; and

(b) because of that excess, the head company transfers under subsection 320‑235(1) or 320‑250(2), from its segregated exempt assets, assets (the policy assets) whose total transfer value equals the amount of the excess attributable to the matters described in subparagraphs (a)(i) and (ii).

However, this section does not apply if the policyholder ceases to be a *member of the consolidated group between the fusion time and the determination time.

Note: Subsections 320‑235(1) and 320‑250(2) require a life insurance company to transfer assets from its segregated exempt assets if, at certain times, the total transfer value of the segregated exempt assets exceeds the amount of the company’s exempt life insurance policy liabilities.

Policy assets’ transfer value not included in assessable income

(2) Paragraph 320‑15(1)(f) does not apply to the transfer of the policy assets.

Note: Paragraph 320‑15(1)(f) includes in a life insurance company’s assessable income the transfer values of assets transferred by the company from the company’s segregated exempt assets under subsection 320‑235(1) or 320‑250(2).

Extra assessable income if policy is not a qualifying security

(3) If the fused entities’ policy is not a qualifying security (as defined in section 159GP of the Income Tax Assessment Act 1936), the assessable income of the *head company of the *consolidated group for the income year in which the company transfers the policy assets includes the amount worked out using the formula:

![]()

where:

reduced purchase price of the annuity means the reduced purchase price of the *annuity as at the determination time worked out under Subdivision AA of Division 2 of Part III of the Income Tax Assessment Act 1936 as if the determination time (rather than the fusion time) had been the first time at which both the fused entities were *members of the *consolidated group.

Assessable income or deduction if policy is a qualifying security

(4) If the fused entities’ policy is a qualifying security (as defined in section 159GP of the Income Tax Assessment Act 1936), section 159GS (Balancing adjustment on transfer of qualifying security) of that Act applies as if:

(a) the *head company of the *consolidated group:

(i) had been the holder (as defined in section 159GP of that Act) of the policy; and

(ii) had transferred the policy when it transferred the policy assets; and

(b) the transfer price had equalled the total *transfer value of the policy assets; and

(c) the determination time (rather than the fusion time) had been the first time at which both the fused entities were *members of the consolidated group.

Note: If the policyholder becomes a subsidiary member of the consolidated group, section 701‑5 (Entry history rule) treats the head company as if anything that had happened to the policyholder before it became a subsidiary member of the group had happened to the head company.

Application

(1) This section applies if there is a period (the gap) between:

(a) the fusion time; and

(b) the determination time or the time at which the policyholder ceases to be a *member of the *consolidated group, whichever is earlier;

when the fused entities are both members of the consolidated group.

Continuation of exempt life insurance policy during the gap

(2) For the head company core purposes mentioned in section 701‑1 (Single entity rule), Division 320 applies in relation to the fused entities’ policy as if it continued to be an *exempt life insurance policy during the gap, even though both the fused entities were *members of the *consolidated group.

Transfer from segregated assets to provide for annuity payments

(3) During the gap, the *head company of the *consolidated group may transfer an asset from the head company’s *segregated exempt assets to provide for payments of the *immediate annuity under the fused entities’ policy.

Effect of transfer

(4) If the *head company of the *consolidated group transfers an asset under subsection (3):

(a) section 320‑255 applies to the asset in the same way as that section applies to an asset transferred under subsection 320‑250(2); and

(b) whichever one of subsections (5) and (6) is relevant affects the *head company of the *consolidated group for the income year in which the gap occurs.

Income if policy is not a qualifying security

(5) If the fused entities’ policy is not a qualifying security (as defined in section 159GP of the Income Tax Assessment Act 1936), the *head company’s assessable income includes the amount that, if the fused entities had not been *members of the *consolidated group:

(a) would have been included in the policyholder’s assessable income under section 27H of that Act in connection with the policy; and

(b) would have been derived in the gap.

Income or deduction if policy is a qualifying security

(6) If the fused entities’ policy is a qualifying security (as defined in section 159GP of the Income Tax Assessment Act 1936):

(a) the *head company’s assessable income includes the amount (if any) that, if the fused entities had not been *members of the *consolidated group:

(i) would have been included in the policyholder’s assessable income under section 159GQ of that Act in connection with the policy; and

(ii) would have been attributable to the gap; or

(b) the head company may deduct the amount (if any) that, if the fused entities had not been members of the consolidated group:

(i) would have been a deduction allowable to the policyholder under section 159GQ of that Act in connection with the policy; and

(ii) would have been attributable to the gap.

(1) This section affects how paragraph 320‑15(1)(h) and section 320‑85 apply if:

(a) a *life insurance company ceases to be a *subsidiary member of a *consolidated group at a time (the leaving time); and

(b) at the leaving time, the *life insurance company has one or more liabilities under the *net risk components of life insurance policies.

Note: Paragraph 320‑15(1)(h) and section 320‑85 both operate on the basis of a comparison of the value of a life insurance company’s liabilities under the net risk components of life insurance policies at the end of the current year with the value of those liabilities at the end of the previous year, so that:

(a) that paragraph includes an amount in the company’s assessable income for the current year if the value at the end of the current year is less than the value at the end of the previous income year; and

(b) that section allows a deduction for the current year if the value at the end of the current year is more than the value at the end of the previous income year.