Tax Laws Amendment (2006 Measures No. 1) Act 2006

No. 32, 2006

An Act to amend the law relating to taxation, and for related purposes

Tax Laws Amendment (2006 Measures No. 1) Act 2006

No. 32, 2006

An Act to amend the law relating to taxation, and for related purposes

Contents

1 Short title

2 Commencement

3 Schedule(s)

Schedule 1—Foreign source income exemptions for temporary residents

Part 1—Main amendments

Income Tax Assessment Act 1997

Part 2—Other amendments

Fringe Benefits Tax Assessment Act 1986

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Schedule 2—Business related costs

Part 1—Capital allowances amendments

Income Tax Assessment Act 1997

Part 2—CGT amendments

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Part 3—Application

Schedule 3—Promotion and implementation of schemes

Part 1—Main amendments

Taxation Administration Act 1953

Part 2—Consequential amendments

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Part 3—Application

Schedule 4—Vouchers

A New Tax System (Goods and Services Tax) Act 1999

Tax Laws Amendment (2006 Measures No. 1) Act 2006

No. 32, 2006

An Act to amend the law relating to taxation, and for related purposes

[Assented to 6 April 2006]

The Parliament of Australia enacts:

This Act may be cited as the Tax Laws Amendment (2006 Measures No. 1) Act 2006.

This Act commences on the day on which it receives the Royal Assent.

Each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

1 At the end of Division 768

Add:

This Subdivision modifies the general tax rules for people in Australia who are temporary residents, whether Australian residents or foreign residents.

Generally foreign income derived by temporary residents is non‑assessable non‑exempt income and capital gains and losses they make are also disregarded for CGT purposes. There are some exceptions for employment‑related income and capital gains on shares and rights acquired under employee share schemes.

Temporary residents are also partly relieved of record‑keeping obligations in relation to the controlled foreign company and foreign investment fund rules.

Interest paid by temporary residents is not subject to withholding tax and may be non‑assessable non‑exempt income for a foreign resident.

Table of sections

Operative provisions

768‑905 Objects

768‑910 Income derived by temporary resident

768‑915 Certain capital gains and capital losses of temporary resident to be disregarded

768‑920 Capital gains and losses on employee shares and rights where taxation of discount not deferred

768‑925 Notional gain or loss

768‑930 Adjustment to notional gain or loss

768‑935 Adjustment for share or right acquired under employee share scheme

768‑940 Adjustment for derived share

768‑945 Amending assessment to take account of effect on capital gain or loss of recalculating discount

768‑950 Individual becoming an Australian resident

768‑955 Temporary resident who ceases to be temporary resident but remains an Australian resident

768‑960 Temporary resident not attributable taxpayer for purposes of controlled foreign companies rules

768‑965 Exemption of temporary resident from taxation in respect of foreign investment fund income

768‑970 Modification of rules for accruals system of taxation of certain non‑resident trust estates

768‑975 Calculation of beneficiary’s share of net income of non‑resident trust estate

768‑980 Interest paid by temporary resident

The objects of this Subdivision are to:

(a) provide *temporary residents with tax relief on most foreign source income and capital gains; and

(b) relieve the burdens associated with complying with certain record‑keeping obligations and interest withholding tax obligations.

(1) The following are *non‑assessable non‑exempt income:

(a) the *ordinary income you *derive directly or indirectly from a source other than an *Australian source if you are a *temporary resident when you derive it;

(b) your *statutory income (other than a *net capital gain) from a source other than an Australian source if you are a temporary resident when you derive it.

This subsection has effect subject to subsections (3) and (5).

Note: A capital gain or loss you make may be disregarded under section 768‑915.

(2) For the purposes of paragraph (1)(b):

(a) if you have statutory income because a particular circumstance occurs, you derive the statutory income at the time when the circumstance occurs; and

(b) if you have statutory income because a number of circumstances occur, you derive the statutory income at the time when the last of those circumstances occurs.

Exception to subsection (1)

(3) However, the following are not *non‑assessable non‑exempt income under subsection (1):

(a) the *ordinary income you *derive directly or indirectly from a source other than an *Australian source to the extent that it is remuneration, for employment undertaken, or services provided, while you are a *temporary resident;

(b) your *statutory income (other than a *net capital gain) from a source other than an Australian source to the extent that it relates to employment undertaken, or services provided, while you are a temporary resident;

(c) an amount included in your assessable income under Division 86;

(d) an amount that, but for subsection (1), would be included in your assessable income under Division 13A of Part III of the Income Tax Assessment Act 1936.

Note: This subsection only makes an amount not non‑assessable non‑exempt income under subsection (1). It does not prevent that amount from being non‑assessable non‑exempt income under some other provision of this Act or the Income Tax Assessment Act 1936.

Section 26AAC employee share schemes

(4) This subsection applies if:

(a) an amount would otherwise be included in your assessable income under section 26AAC of the Income Tax Assessment Act 1936 (about shares and rights acquired by employees); and

(b) the applicable time mentioned in subsection 26AAC(15) of that Act for the relevant *share occurs while you are a *temporary resident.

(5) If subsection (4) applies, the amount is *non‑assessable non‑exempt income to the extent to which you acquired the relevant *share under a scheme for the acquisition of shares by employees in respect of, or for or in relation (directly or indirectly) to:

(a) any employment you undertook outside Australia; or

(b) any services you provided outside Australia;

prior to becoming a *temporary resident.

(6) Subsection (5) does not limit paragraph (1)(b).

A *capital gain or *capital loss you make from a *CGT event is disregarded if:

(a) you are a *temporary resident when, or immediately before, the CGT event happens; and

(b) you would not make a capital gain or loss from the CGT event if you were a foreign resident when, or immediately before, the CGT event happens.

Note: Division 136 deals with capital gains and capital losses by foreign residents.

When this section applies

(1) This section applies to a *share or right if:

(a) you *acquire the share or right under an *employee share scheme; and

(b) you engage in employment, or render services, that affect the holding or acquisition of the shares or rights while you are a *temporary resident; and

(c) the share or right does not have the *necessary connection with Australia; and

(d) either:

(i) the share or right is not a *qualifying share or *qualifying right; or

(ii) the share or right is a qualifying share or qualifying right and you have made an election under section 139E of the Income Tax Assessment Act 1936 covering the share or right; and

(e) a *CGT event happens in relation to the share or right; and

(f) if the CGT event is CGT event I1—you are not a temporary resident immediately before the event happens; and

(g) you would make a *capital gain or *capital loss from the CGT event, and the capital gain or capital loss would not be disregarded, if you were an Australian resident (but not a temporary resident) when the CGT event happens; and

(h) this section has not previously applied to you in relation to a CGT event in relation to the share or right.

Note: Paragraph (a)—section 139DQ of the Income Tax Assessment Act 1936 applies for the purposes of this Subdivision to treat a matching share or right issued as part of a 100% takeover or restructure as a continuation of the share or right it matches.

(2) This section also applies to a *share (the derived share) if:

(a) you *acquire a right (the original right) under an *employee share scheme; and

(b) you engage in employment, or render services, that affect the holding or acquisition of the original right, or the derived share, while you are a *temporary resident; and

(c) you acquire the derived share by exercising the original right; and

(d) the derived share does not have the *necessary connection with Australia; and

(e) either:

(i) the original right is not a *qualifying right; or

(ii) the original right is a qualifying right and you have made an election under section 139E of the Income Tax Assessment Act 1936 covering the original right; and

(f) a *CGT event happens in relation to the derived share; and

(g) if the CGT event is CGT event I1—you are not a temporary resident immediately before the event happens; and

(h) you would make a *capital gain or *capital loss from the CGT event, and the capital gain or capital loss would not be disregarded, if you were an Australian resident (but not a temporary resident) when the CGT event happens; and

(i) this section has not previously applied to you in relation to the original right or the derived share.

Note: Paragraph (a)—section 139DQ of the Income Tax Assessment Act 1936 applies for the purposes of this Subdivision to treat a matching share or right issued as part of a 100% takeover or restructure as a continuation of the share or right it matches.

(3) To avoid doubt, paragraph (1)(e) or (2)(f) applies:

(a) even if you are not a *temporary resident when the *CGT event happens; and

(b) whether you are an Australian resident or a foreign resident when the CGT event happens.

Capital gain or loss

(4) If you are a *temporary resident or a foreign resident when the *CGT event happens, you make a *capital gain or *capital loss from the CGT event.

Note: If you are an Australian resident (but not a temporary resident) when the CGT event occurs, neither Division 136 nor section 768‑915 prevents you having a capital gain or capital loss.

(5) Subsection (4) has effect despite Division 136 and section 768‑915.

Amount of capital gain or capital loss for temporary residents and foreign residents

(6) If you are a *temporary resident or a foreign resident when the *CGT event happens, the amount of the *capital gain or *capital loss is the amount of your adjusted notional gain or loss worked out under subsection (9).

Amount of capital gain or capital loss for Australian residents

(7) If you are an Australian resident (but not a *temporary resident) when the *CGT event happens, the amount of the *capital gain or *capital loss is the sum of:

(a) the amount that would be the amount of your capital gain or capital loss if this section did not apply to you; and

(b) the amount of your adjusted notional gain or loss worked out under subsection (9).

Example: George, a New Zealander, is granted shares (with a total market value at the time of $100,000) under an employee share scheme on 20 January 2006. He comes to Australia as a temporary resident on 1 January 2007 and completes the rest of the employment to which the shares relate in Australia. George elects to have the discount assessed in that income year. He then ceases to be a temporary resident but remains an Australian resident on 8 May 2008. At that time the shares have a market value of $80,000. George disposes of the shares on 30 June 2009 for $115, 000. George’s capital gain for the purpose of paragraph (a) would be $35,000. Assume that the amount of the loss that accrued up to 8 May 2008 that is to be counted for the purpose of paragraph (b) is $9,000. For the year ending 30 June 2009, George would, as a result of subsection (7), make a capital gain of $26,000 (being $35,000 less $9,000).

(8) If subsection (7) applies to the *CGT event, subsections 136‑40(3) and 768‑955(3) do not apply for the purposes of applying Division 115 in relation to the CGT event.

Adjusted notional gain or loss

(9) To work out your adjusted notional gain or loss:

(a) work out your notional gain or loss using section 768‑925; and

(b) adjust your notional gain or loss using sections 768‑930, 768‑935 and 768‑940.

(1) Your notional gain or loss is the *capital gain or *capital loss you would have had in relation to the *CGT event if, for the whole of the period set by subsections (2) and (3), you:

(a) had been an Australian resident; and

(b) had not been a *temporary resident.

(2) The period starts:

(a) in the case of section 768‑920 applying to the *share or right in relation to which the *CGT event happens because of subsection 768‑920(1):

(i) if the share or right was acquired from an *employee share trust—when you first acquired a beneficial interest in the share or right; or

(ii) if subparagraph (i) does not apply—when you *acquired that share or right; and

(b) in the case of section 768‑920 applying to the *share in relation to which the *CGT event happens because of subsection 768‑920(2):

(i) if the share was acquired from an *employee share trust—when you first acquired a beneficial interest in the original right; or

(ii) if subparagraph (i) does not apply—when you *acquired the original right.

(3) The period ends when the *CGT event happens.

(4) If you are an Australian resident (but not a *temporary resident) when the *CGT event happens, your notional gain or loss is reduced by the amount of the *capital gain or *capital loss that you would have made in relation to the *CGT event if section 768‑920 did not apply to you.

(1) If section 768‑920 applies to the *share or right in relation to which the *CGT event happens because of subsection 768‑920(1), adjust your notional gain or loss by:

(a) firstly, applying the factor worked out under subsection 768‑935(1), (2) or (3) to the amount of your notional gain or loss; and

(b) secondly, applying the factor worked out under subsection 768‑935(4) to the amount worked out under paragraph (a).

(2) If section 768‑920 applies to the *share in relation to which the *CGT event happens because of subsection 768‑920(2), adjust your notional gain or loss by:

(a) firstly, applying the factor worked out under subsection 768‑940(1), (2) or (3) to the amount of your notional gain or loss; and

(b) secondly, applying the factor worked out under subsection 768‑940(4) to the amount worked out under paragraph (a).

(1) If:

(a) the *CGT event happens on or after the *cessation time for the share or right; and

(b) when, or immediately before, the CGT event happens you are either:

(i) a foreign resident; or

(ii) an Australian resident who is a temporary resident;

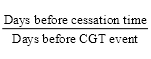

the factor to be applied for the purposes of paragraph 768‑930(1)(a) is:

where:

days before cessation time is the number of days in the period that:

(a) starts on the day on which you *acquired the *share or right or, if you acquired the share or right from an *employee share trust, on the day on which you first acquired a beneficial interest in the share or right; and

(b) ends on the *cessation time for the share or right.

days before CGT event is the number of days in the period that:

(a) starts on the day on which you *acquired the *share or right or, if you acquired the share or right from an *employee share trust, on the day on which you first acquired a beneficial interest in the share or right; and

(b) ends on the day on which the *CGT event happens.

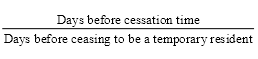

(2) If:

(a) the *CGT event happens on or after the *cessation time for the share or right; and

(b) when, or immediately before, the CGT event happens you are an Australian resident (but not a *temporary resident);

the factor to be applied for the purposes of paragraph 768‑930(1)(a) is:

where:

days before cessation time is the number of days in the period that:

(a) starts on the day on which you *acquired the *share or right or, if you acquired the share or right from an *employee share trust, on the day on which you first acquired a beneficial interest in the share or right; and

(b) ends on the *cessation time for the share or right.

days before ceasing to be a temporary resident is the number of days in the period that:

(a) starts on the day on which you *acquired the *share or right or, if you acquired the share or right from an *employee share trust, on the day on which you first acquired a beneficial interest in the share or right; and

(b) ends on the day on which you cease to be a *temporary resident.

(3) The factor to be applied for the purposes of paragraph 768‑930(1)(a) is 1 if:

(a) the CGT event happens before the *cessation time for the *share or right; or

(b) you became an Australian resident who was not a *temporary resident before the cessation time for the share or right.

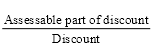

(4) The factor to be applied for the purposes of paragraph 768‑930(1)(b) is:

where:

assessable part of discount is the amount of the discount that:

(a) was included in your assessable income under Division 13A of Part III of the Income Tax Assessment Act 1936 in relation to the *share or right; or

(b) would have been included in your assessable income under that Division in relation to the share or right if subsection 139BA(2) of that Act were disregarded.

discount is the amount of the discount.

(1) If:

(a) the *CGT event happens on or after the *cessation time for the original right; and

(b) when, or immediately before, the CGT event happens you are either:

(i) a foreign resident; or

(ii) an Australian resident who is a *temporary resident;

the factor to be applied for the purposes of paragraph 768‑930(2)(a) is:

where:

days before cessation time is the number of days in the period that:

(a) starts on the day on which you *acquired the original right or, if you acquired the *share from an *employee share trust, on the day on which you first acquired a beneficial interest in the original right; and

(b) ends on the *cessation time for the original right.

days before CGT event is the number of days in the period that:

(a) starts on the day on which you *acquired the original right or, if you acquired the *share from an *employee share trust, on the day on which you first acquired a beneficial interest in the original right; and

(b) ends on the day on which the *CGT event happens.

(2) If:

(a) the *CGT event happens on or after the *cessation time for the original right; and

(b) when, or immediately before, the CGT event happens you are an Australian resident (but not a *temporary resident);

the factor to be applied for the purposes of paragraph 768‑930(2)(a) is:

where:

days before cessation time is the number of days in the period that:

(a) starts on the day on which you *acquired the original right or, if you acquired the *share from an *employee share trust, on the day on which you first acquired a beneficial interest in the original right; and

(b) ends on the *cessation time for the original right.

days before ceasing to be a temporary resident is the number of days in the period that:

(a) starts on the day on which you *acquired the original right or, if you acquired the *share from an *employee share trust, on the day on which you first acquired a beneficial interest in the original right; and

(b) ends on the day on which you cease to be a *temporary resident.

(3) The factor to be applied for the purposes of paragraph 768‑930(2)(a) is 1 if:

(a) the *CGT event happens before the *cessation time for the original right; or

(b) you became an Australian resident who was not a *temporary resident before the cessation time for the original right.

(4) The factor to be applied for the purposes of paragraph 768‑930(2)(b) is:

where:

assessable part of discount is the amount of the discount that:

(a) was included in your assessable income under Division 13A of Part III of the Income Tax Assessment Act 1936 in relation to the original right; or

(b) would have been included in your assessable income under that Division in relation to the original right if subsection 139BA(2) of that Act were disregarded.

discount is the amount of the discount.

(1) This section applies if:

(a) an amount is included in your assessable income, or you have a net capital loss, for a particular income year; and

(b) that amount is reduced, or increased, because of a change in the extent (if any) to which any of the following provisions of the Income Tax Assessment Act 1936 apply in relation to the amount during a subsequent income year:

(i) section 23AF;

(ii) section 23AG;

(iii) subsection 139B(1A).

(2) In paragraph (1)(b):

(a) the reference to an amount being reduced includes a reference to the amount being reduced to a nil amount; and

(b) the reference to an amount being increased includes a reference to the amount being increased from a nil amount.

(3) Section 170 of the Income Tax Assessment Act 1936 does not prevent the amendment of an assessment to take account of the effect that the reduction or increase has on the determination of the amount of a *capital gain or *capital loss under subsection 768‑920(6) or (7).

(4) If section 768‑920 applies to the *share or right in relation to which the *CGT event occurs because of subsection 768‑920(1), the amendment must be made before the end of the period of 4 years starting immediately after the income year during which the period of employment or service relating to the *acquisition of the share or right ends.

(5) If section 768‑920 applies to the *share or right in relation to which the *CGT event occurs because of subsection 768‑920(2), the amendment must be made before the end of the period of 4 years starting immediately after the income year during which the period of employment or service relating to the *acquisition of the original right ends.

Section 136‑40 does not apply to your becoming an Australian resident if you are a *temporary resident immediately after you become an Australian resident.

(1) If you are a *temporary resident and you then cease to be a temporary resident (but remain, at that time, an Australian resident), there are rules relevant to each *CGT asset that:

(a) you owned just before you ceased to be a temporary resident; and

(b) does not have the *necessary connection with Australia; and

(c) you *acquired on or after 20 September 1985.

(2) The first element of the *cost base and *reduced cost base of the asset (at the time you cease to be a *temporary resident) is its *market value at that time. This subsection has effect despite Subdivision 130‑D.

(3) Also, Parts 3‑1 and 3‑3 apply to the asset as if you had *acquired it at the time you ceased to be a *temporary resident.

(4) This section does not apply to a *share or right if:

(a) it is a *qualifying share or a *qualifying right; and

(b) you have not made an election under section 139E of the Income Tax Assessment Act 1936 covering the share or right; and

(c) the *cessation time for the share or right has not occurred.

For the purposes of Part X of the Income Tax Assessment Act 1936 (which deals with the attribution of income in respect of controlled foreign companies), you are taken not to be an *attributable taxpayer in relation to a *CFC or *CFT at any time you are a *temporary resident.

If you are a *temporary resident at the end of an income year, section 529 and Division 22 of Part XI of the Income Tax Assessment Act 1936 do not apply to you in relation to a *FIF or *FLP in respect of the notional accounting period of the FIF or FLP that ends in that income year.

At any time when you are a *temporary resident, you are taken not to be a resident for the purposes of section 102AAZD of the Income Tax Assessment Act 1936.

At any time when you are a *temporary resident, you are taken not to be a resident for the purposes of subsection 96C(6) of the Income Tax Assessment Act 1936.

Interest that is paid by a *temporary resident:

(a) is an amount to which section 128B (liability to withholding tax) of the Income Tax Assessment Act 1936 does not apply; and

(b) is *non‑assessable non‑exempt income if the interest is:

(i) *derived by a foreign resident; and

(ii) is not derived from carrying on *business in Australia at or through a *permanent establishment in Australia.

2 Subsection 995‑1(1)

Insert:

temporary resident: you are a temporary resident if:

(a) you hold a temporary visa granted under the Migration Act 1958; and

(b) you are not an Australian resident within the meaning of the Social Security Act 1991; and

(c) your *spouse is not an Australian resident within the meaning of the Social Security Act 1991.

However, you are not a temporary resident if you have been an Australian resident (within the meaning of this Act), and any of paragraphs (a), (b) and (c) are not satisfied, at any time after the commencement of this definition.

Note: The tests in paragraphs (b) and (c) are applied to ensure that holders of temporary visas who nonetheless have a significant connection with Australia are not treated as temporary residents for the purposes of this Act.

3 Subsection 136(1) (sub-subparagraph (j)(ii)(B) of the definition of fringe benefit)

Omit “an exempt visitor to Australia for the purposes of section 517 of that Act in relation to the year of income in which”, substitute “a temporary resident (within the meaning of the Income Tax Assessment Act 1997) when”.

4 At the end of subsection 96C(6)

Add:

Note: A temporary resident is taken not to be a resident for the purposes of this subsection: see section 768‑975 of the Income Tax Assessment Act 1997.

5 At the end of subsection 128B(2)

Add:

Note: An amount of interest paid to a person by a temporary resident is an amount to which this section does not apply: see section 768‑980 of the Income Tax Assessment Act 1997.

6 At the end of subsection 128B(2A)

Add:

Note: An amount of interest paid to a person by a temporary resident is an amount to which this section does not apply: see section 768‑980 of the Income Tax Assessment Act 1997.

7 At the end of section 128D

Add:

Note: An amount of interest paid to a person by a temporary resident is non‑assessable non‑exempt income: see section 768‑980 of the Income Tax Assessment Act 1997.

8 Subsection 139DQ(1)

After “this Division”, insert “and Subdivision 768‑R of the Income Tax Assessment Act 1997”.

9 Subsection 139DQ(2)

After “this Division”, insert “and Subdivision 768‑R of the Income Tax Assessment Act 1997”.

10 Subsection 139DQ(3)

After “this Division”, insert “and Subdivision 768‑R of the Income Tax Assessment Act 1997”.

11 Paragraphs 139GB(3)(a) and (b)

Repeal the paragraphs, substitute:

(a) is a temporary resident within the meaning of the Income Tax Assessment Act 1997; or

(b) is not a resident; or

12 Paragraph 274(1)(aa)

Omit “an exempt visitor to Australia for the purposes of section 517 in relation to”, substitute “a temporary resident within the meaning of the Income Tax Assessment Act 1997 at the end of”.

13 At the end of section 361

Add:

(3) Subsections (1) and (2) have effect subject to section 768‑960 of the Income Tax Assessment Act 1997.

14 Subsection 469(5)

Repeal the subsection, substitute:

(5) The operative provision does not apply, or its application is affected, in certain circumstances which are set out in:

(a) Divisions 2 to 15 of this Part; and

(b) section 768‑965 of the Income Tax Assessment Act 1997.

15 Division 10 of Part XI

Repeal the Division.

16 Section 11‑55 (table item headed “foreign aspects of income taxation”)

Before:

withholding tax, dividend royalty or interest subject to............. 128D |

insert:

income derived by temporary residents...................................... 768‑910 |

interest paid by temporary residents........................................... 768‑980 |

17 Section 11‑55 (after table item headed “tax loss transfers”)

Insert:

temporary residents |

|

see foreign aspects of income taxation |

|

18 Subsection 104‑160(6) (note 1)

Omit “section 104‑165”, substitute “section 104‑166”.

19 Subsection 104‑160(6) (after note 1)

Insert:

Note 1A: An individual may disregard the gain or loss if he or she was a temporary resident immediately before he or she stopped being an Australian resident: see section 768‑915.

20 Subsection 104‑165(1)

Repeal the subsection.

Note: The heading to section 104‑165 is replaced by the heading “Exception for individuals”.

21 After section104‑165

Insert:

Subsection 104‑165(1) continues to apply, despite its repeal by item 20 of Schedule 1 to the Tax Laws Amendment (2006 Measures No. 1) Act 2006, to an individual:

(a) who is in Australia on the day on which that item receives the Royal Assent; and

(b) who remains an Australian resident from that day until the time subsection 104‑165(1) is applied in respect of him or her.

22 Section 109‑55 (table item 15)

After “become an Australian resident”, insert “(but not a temporary resident)”.

23 Section 109‑55 (after table item 15)

Insert:

15A | You are a temporary resident, you then cease to be a temporary resident (but remain, at that time, an Australian resident) and you owned a CGT asset that you acquired on or after 20 September 1985 and that did not have the necessary connection with Australia | when you cease to be a temporary resident | section 768‑955 |

24 Section 112‑87 (table item 1)

After “becomes an Australian resident”, insert “(but not a temporary resident)”.

25 Section 112‑87 (after table item 1)

Insert:

1A | A temporary resident ceases to be a temporary resident (but remains, at that time, an Australian resident) | First element of cost base and reduced cost base | 768‑955 |

26 After paragraph 130‑80(4)(a)

Insert:

(aa) you are not a *temporary resident immediately after you become an Australian resident; and

27 Subsection 130‑80(4) (note)

Omit “Note”, substitute “Note 1”.

28 Subsection 130‑80(4) (note)

Omit “Section 136‑40 deals”, substitute “Sections 136‑40 and 768‑955 deal”.

29 At the end of subsection 130‑80(4)

Add:

Note 2: Paragraph (aa)—see also section 768‑920.

30 After paragraph 130‑83(4)(a)

Insert:

(aa) you are not a *temporary resident immediately after you become an Australian resident; and

31 Subsection 130‑83(4) (note)

Omit “Note”, substitute “Note 1”.

32 Subsection 130‑83(4) (note)

Omit “Section 136‑40 deals”, substitute “Sections 136‑40 and 768‑955 deal”.

33 After paragraph 130‑85(4)(a)

Insert:

(aa) you are not a *temporary resident immediately after you become an Australian resident; and

34 Subsection 130‑85(4) (note)

Omit “Note”, substitute “Note 1”.

35 Subsection 130‑85(4) (note)

Omit “Section 136‑40 deals”, substitute “Sections 136‑40 and 768‑955 deal”.

36 At the end of subsection 130‑85(4)

Add:

Note 2: Paragraph (aa)—see also section 768‑920.

37 At the end of subsection 136‑40(1)

Add:

Note: This section has effect subject to section 768‑950 (individuals who become Australian residents and are temporary residents immediately after they become Australian residents).

38 Subsection 995‑1(1)

Insert:

FLP has the same meaning as in Part XI of the Income Tax Assessment Act 1936.

39 Subsection 995‑1(1) (definition of notional accounting period)

Omit “section 486”, substitute “section 470”.

40 Application

(1) Sections 768‑910, 768‑945, 768‑960, 768‑965, 768‑970 and 768‑975 of the Income Tax Assessment Act 1997 apply for an income year that begins on or after the start‑up day.

(2) Sections 768‑915, 768‑920, 768‑925, 768‑930, 768‑935 and 768‑940 of the Income Tax Assessment Act 1997 and items 20 and 21 of this Schedule apply if the relevant CGT event happens on or after the start‑up day.

(3) For the purposes of sections 768‑920, 768‑925, 768‑930, 768‑935, 768‑940 and 768‑945 of the Income Tax Assessment Act 1997, items 8, 9 and 10 of this Schedule apply if:

(a) the relevant CGT event happens on or after the start‑up day; and

(b) the relevant matching shares or rights were acquired on or after 1 July 2004.

(4) Section 768‑950 of the Income Tax Assessment Act 1997 and items 26, 30 and 33 of this Schedule apply to an individual becoming an Australian resident on or after the start‑up day.

(5) Section 768‑955 of the Income Tax Assessment Act 1997 applies to an individual ceasing to be a temporary resident (but remaining an Australian resident) on or after the start‑up day.

(6) For the purposes of section 768‑955 of the Income Tax Assessment Act 1997, items 8, 9 and 10 of this Schedule apply if:

(a) the individual ceases to be a temporary resident (but remains an Australian resident) on or after the start‑up day; and

(b) the relevant CGT asset is a matching share or right that was acquired on or after 1 July 2004.

(7) Section 768‑980 of the Income Tax Assessment Act 1997 applies to a payment of interest made on or after the day on which this Act receives the Royal Assent.

(8) The amendments made by items 13, 14 and 15 of this Schedule apply for an income year that begins on or after the start‑up day.

(9) In this item:

start‑up day means the 1 July next following the day on which this Act receives the Royal Assent.

1 Subsection 12‑5(2) (before table item headed “leases”)

Insert:

lease, authority, licence, permit or quota |

|

expenditure to terminate...................... | 25‑110 |

2 At the end of Division 25

Add:

(1) You can deduct an amount for capital expenditure you incur to terminate a lease or licence (including an authority, permit or quota) that results in the termination of the lease or licence if the expenditure is incurred:

(a) in the course of *carrying on a *business; or

(b) in connection with ceasing to carry on a business.

(2) The amount you can deduct is 20% of the expenditure:

(a) for the income year in which the lease or licence is terminated; and

(b) for each of the next 4 income years.

Exceptions

(3) You cannot deduct any amount for expenditure you incur to terminate a lease that, in accordance with *accounting standards, or statements of accounting concepts made by the Australian Accounting Standards Board, is classified as a finance lease.

(4) If you incurred the expenditure under an *arrangement and:

(a) there is at least one other party to the arrangement with whom you did not deal at *arm’s length; and

(b) apart from this subsection, the amount of the expenditure would be more than the *market value of what it was for (assuming the termination did not occur and was never proposed to occur);

the amount of expenditure you take into account is that market value.

(5) You cannot deduct any amount for expenditure you incur to terminate a lease or licence if:

(a) after the termination, you or an *associate of yours enters into another lease or licence with the same party or an associate of that party; and

(b) the other lease or licence is of the same kind as the original one.

(6) You cannot deduct any amount for expenditure you incur to terminate a lease or licence to the extent that the expenditure is for the granting or receipt of another lease or licence in relation to the asset that was the subject of the original lease or licence.

3 Section 35‑5

Repeal the section, substitute:

(1) The object of this Division is to improve the integrity of the taxation system by:

(a) preventing losses from non‑commercial activities that are *carried on as *businesses by individuals (alone or in partnership) being offset against other assessable income; and

(b) preventing pre‑business capital expenditure and post‑business capital expenditure by individuals (alone or in partnership) in relation to non‑commercial activities being deductible under section 40‑880 (business related costs);

unless certain exceptions apply.

(2) This Division is not intended to apply to activities that do not constitute *carrying on a *business (for example, the receipt of income from passive investments).

4 Subsection 35‑10(2) (heading)

Repeal the heading, substitute:

Rules

5 After subsection 35‑10(2)

Insert:

(2A) You cannot deduct an amount under section 40‑880 (business related costs) for expenditure in relation to a *business activity you used to *carry on if you are an individual, either alone or in partnership (whether or not some other entity is a member of the partnership) unless:

(a) one of the tests set out in section 35‑30 (assessable income test), 35‑35 (profits test), 35‑40 (real property test) or 35‑45 (other assets test) was satisfied for the business activity; or

(b) the Commissioner has exercised the discretion set out in section 35‑55 for the business activity; or

(c) the exception in subsection (4) applied;

for the income year in which the business activity ceased to be carried on or an earlier income year.

(2B) If you are an individual, either alone or in partnership (whether or not some other entity is a member of the partnership), you cannot deduct an amount under section 40‑880 (business related costs) for expenditure in relation to a *business activity:

(a) you propose to *carry on; or

(b) another entity proposes to carry on if the other entity is not an individual, either alone or in partnership;

for an income year before the one in which the business activity starts to be carried on.

(2C) This section applies to an amount that you could have deducted, apart from paragraph (2B)(a), as if it were an amount attributable to the *business activity that you can deduct from assessable income from the activity for the income year in which the business activity starts to be *carried on.

(2D) You can deduct expenditure covered by paragraph (2B)(b) for the income year in which the *business activity starts to be *carried on.

6 Subsection 35‑10(4)

After “subsection (2)”, insert “, (2A) or (2B)”.

7 Subsection 35‑15(1)

Omit “section 35‑10”, substitute “subsection 35‑10(2)”.

8 Subsection 35‑20(1)

Omit “section 35‑10”, substitute “subsection 35‑10(2) or (2A)”.

9 Section 35‑30

Omit “rule in section 35‑10 does not apply”, substitute “rules in section 35‑10 do not apply”.

10 Subsection 35‑35(1)

Omit “rule in section 35‑10 does not apply”, substitute “rules in section 35‑10 do not apply”.

11 Subsection 35‑35(1)

Omit “subsection 35‑10(2)”, substitute “subsections 35‑10(2) and (2C)”.

12 Subsection 35‑35(2)

Omit “rule in section 35‑10 does not apply”, substitute “rules in section 35‑10 do not apply”.

13 Subsection 35‑35(2)

Omit “subsection 35‑10(2)”, substitute “subsections 35‑10(2) and (2C)”.

14 Subsection 35‑40(1)

Omit “rule in section 35‑10 does not apply”, substitute “rules in section 35‑10 do not apply”.

15 Subsection 35‑45(1)

Omit “rule in section 35‑10 does not apply”, substitute “rules in section 35‑10 do not apply”.

16 Subsection 35‑55(1)

Omit “section 35‑10”, substitute “subsection 35‑10(2)”.

17 Subparagraph 35‑55(1)(b)(ii)

Omit “subsection 35‑10(2)”, substitute “subsections 35‑10(2) and (2C)”.

18 At the end of section 35‑55 (after the note)

Add:

(2) The Commissioner may decide that the rule in subsection 35‑10(2B) does not apply to a *business activity for an income year if the Commissioner is satisfied that it would be unreasonable to apply that rule because special circumstances of the kind referred to in paragraph (1)(a) of this section prevented the activity from starting.

Note: This subsection is intended to provide for a case where a business activity would have begun to be carried on and satisfied one of the tests if it were not for the special circumstances.

19 Section 40‑10 (table item 2.3)

After “5 years”, insert “where the amounts are not otherwise taken into account and are not denied a deduction”.

20 At the end of section 40‑180

Add:

(3) The first element of *cost includes an amount you paid or are taken to have paid in relation to starting to *hold the *depreciating asset if that amount is directly connected with holding the asset.

(4) The first element of *cost of a *depreciating asset does not include an amount that forms part of the second element of cost of another depreciating asset.

21 Paragraph 40‑185(1)(b)

Omit “for holding the asset or receiving the benefit”, substitute “in relation to holding the asset or receiving the benefit”.

22 Subsection 40‑185(1) (example)

Omit “Example”, substitute “Example 1”.

23 Subsection 40‑185(1) (after example 1)

Insert:

Example 2: Laura travels overseas to purchase a purpose‑built vehicle for use in her trade. The purchase of the vehicle is the sole reason for the trip. Laura incurs expenses for airfares and accommodation. These expenses are included in the cost of the vehicle because they are “in relation to starting to hold” the vehicle.

24 Subsection 40‑190(2)

Repeal the subsection (not including the example or the note), substitute:

(2) The second element is:

(a) the amount you are taken to have paid under section 40‑185 for each economic benefit that has contributed to bringing the asset to its present condition and location from time to time since you started to *hold the asset; and

(b) expenditure you incur that is reasonably attributable to a *balancing adjustment event occurring for the asset.

25 Subsection 40‑190(2) (example)

Omit “Example”, substitute “Example 1”.

26 Subsection 40‑190(2) (before the note)

Insert:

Example 2: Leonie needed to replace one of her old depreciating assets that was fixed to her land with a new, more efficient one. Leonie paid a contractor a fee to demolish and remove the old asset. This resulted in a balancing adjustment event occurring for the old asset, and the fee forms part of the second element of the cost of the old asset that was demolished.

27 Before subsection 40‑190(3)

Insert:

(2A) Paragraph (2)(b) does not apply to a *balancing adjustment event referred to in item 6 or 11 of the table in subsection 40‑300(2).

28 Section 40‑315

Repeal the section.

29 Section 40‑825

After “5 years”, insert “if the amounts are not otherwise taken into account and are not denied a deduction”.

30 Section 40‑880

Repeal the section, substitute:

Object

(1) The object of this section is to make certain *business capital expenditure deductible over 5 years if:

(a) the expenditure is not otherwise taken into account; and

(b) a deduction is not denied by some other provision; and

(c) the business is, was or is proposed to be *carried on for a *taxable purpose.

Deduction

(2) You can deduct, in equal proportions over a period of 5 income years starting in the year in which you incur it, capital expenditure you incur:

(a) in relation to your *business; or

(b) in relation to a business that used to be *carried on; or

(c) in relation to a business proposed to be carried on; or

(d) to liquidate or deregister a company of which you were a *member, to wind up a partnership of which you were a partner or to wind up a trust of which you were a beneficiary, that carried on a business.

Limitations and exceptions

(3) You can only deduct the expenditure, for a *business that you *carry on, used to carry on or propose to carry on, to the extent that the business is carried on, was carried on or is proposed to be carried on for a *taxable purpose.

(4) You can only deduct the expenditure, for a *business that another entity used to *carry on or proposes to carry on, to the extent that:

(a) the business was carried on or is proposed to be carried on for a *taxable purpose; and

(b) the expenditure is in connection with:

(i) your deriving assessable income from the business; and

(ii) the business that was carried on or is proposed to be carried on.

(5) You cannot deduct anything under this section for an amount of expenditure you incur to the extent that:

(a) it forms part of the *cost of a *depreciating asset that you *hold, used to hold or will hold; or

(b) you can deduct an amount for it under a provision of this Act other than this section; or

(c) it forms part of the cost of land; or

(d) it is in relation to a lease or other legal or equitable right; or

(e) it would, apart from this section, be taken into account in working out:

(i) a profit that is included in your assessable income (for example, under section 6‑5 or 15‑15); or

(ii) a loss that you can deduct (for example, under section 8‑1 or 25‑40); or

(f) it could, apart from this section, be taken into account in working out the amount of a *capital gain or *capital loss from a *CGT event; or

(g) a provision of this Act other than this section would expressly make the expenditure non‑deductible if it were not of a capital nature; or

(h) a provision of this Act other than this section expressly prevents the expenditure being taken into account as described in paragraphs (a) to (f) for a reason other than the expenditure being of a capital nature; or

(i) it is expenditure of a private or domestic nature; or

(j) it is incurred in relation to gaining or producing *exempt income or *non‑assessable non‑exempt income.

(6) The exceptions in paragraphs (5)(d) and (f) do not apply to expenditure you incur to preserve (but not enhance) the value of goodwill if the expenditure you incur is in relation to a legal or equitable right and the value to you of the right is solely attributable to the effect that the right has on goodwill.

(7) You cannot deduct an amount under paragraph (2)(c) in relation to a *business proposed to be *carried on unless, having regard to any relevant circumstances, it is reasonable to conclude that the business is proposed to be carried on within a reasonable time.

(8) You cannot deduct anything under this section for an amount of expenditure that, because of a market value substitution rule, was excluded from the *cost of a *depreciating asset or the *cost base or *reduced cost base of a *CGT asset.

Note: Some examples of market value substitution rules are subsection 40‑180(2) (table item 8), subsection 40‑190(3) (table item 1) and sections 40‑765 and 112‑20.

(9) You cannot deduct anything under this section for an amount of expenditure you incur:

(a) by way of returning an amount you have received (except to the extent that the amount was included in your assessable income or taken into account in working out an amount so included); or

(b) to the extent that, for another entity, the amount is a *return on or of:

(i) an *equity interest; or

(ii) a *debt interest that is an obligation of yours.

31 Section 108‑17

Omit “non‑capital costs of ownership”, substitute “costs of ownership”.

32 Section 108‑30

Omit “non‑capital costs of ownership”, substitute “costs of ownership”.

33 Subsection 110‑25(1)

Omit “, subject to subsections (7), (8) and (9)”.

34 Subsection 110‑25(3)

Repeal the subsection (not including the note), substitute:

(3) The second element is the *incidental costs you incurred. These costs can include giving property: see section 103‑5.

35 Subsection 110‑25(4)

Omit “non‑capital costs of ownership of”, substitute “costs of owning”.

36 Subsection 110‑25(5)

Repeal the subsection (including the note), substitute:

(5) The fourth element is capital expenditure you incurred:

(a) the purpose or the expected effect of which is to increase or preserve the asset’s value; or

(b) that relates to installing or moving the asset.

The expenditure can include giving property: see section 103‑5.

Note: There are 3 situations involving leases in which this element is modified: see section 112‑80.

(5A) Subsection (5) does not apply to capital expenditure incurred in relation to goodwill.

37 Subsections 110‑25(7), (8), (9), (10) and (11)

Repeal the subsections.

38 Subsection 110‑25(12) (note 1)

Omit “subsection (5) of this section or”.

39 Subsection 110‑35(1)

Repeal the subsection, substitute:

(1) There are a number of incidental costs you may have incurred. Except for the ninth, they are costs you may have incurred:

(a) to *acquire a *CGT asset; or

(b) that relate to a *CGT event.

40 Paragraphs 110‑35(5)(a) and (b)

After “advertising”, insert “or marketing”.

41 At the end of section 110‑35

Add:

(7) The sixth is search fees relating to a *CGT asset.

(8) The seventh is the cost of a conveyancing kit (or a similar cost).

(9) The eighth is borrowing expenses (such as loan application fees and mortgage discharge fees).

(10) The ninth is expenditure that:

(a) is incurred by the *head company of a *consolidated group to an entity that is not a *member of the group; and

(b) reasonably relates to a *CGT asset *held by the head company; and

(c) is incurred because of a transaction that is between members of the group.

Example: Land is transferred by one company to another company. The companies are members of a consolidated group. Stamp duty is payable as a result of the transaction.

The transaction has no taxation consequences because of its intra‑group nature.

The stamp duty is included in the cost base and reduced cost base of the land.

Note: Intra‑group assets are not held by the head company because of the operation of subsection 701‑1(1) (the single entity rule). An example of an intra‑group asset is a debt owed by a member of the consolidated group to another member of the group.

42 After section 110‑35

Insert:

(1) The cost base of a *CGT asset *acquired at or before 11.45 am (by legal time in the Australian Capital Territory) on 21 September 1999 also includes indexation of the elements of the cost base (except the third element) if the requirements of Division 114 are met.

(2) However, for the purposes of working out the *capital gain of an entity mentioned in an item of the table from a *CGT event happening after 11.45 am (by legal time in the Australian Capital Territory) on 21 September 1999, the cost base includes indexation only if the entity mentioned in the item chooses that the cost base includes indexation.

Choice of indexation | ||

Item | For the purposes of working out the capital gain of this entity: | The cost base includes indexation only if this entity chooses so: |

1 | An individual | The individual |

2 | A *complying superannuation entity | The trustee of the complying superannuation entity |

3 | A trust | The trustee of the trust |

4 | A listed investment company | The company |

Note 1: Section 103‑25 specifies when you must make the choice and provides that the way you prepare your income tax return is evidence of your choice.

Note 2: For each CGT asset whose cost base you need to work out, you may either choose to index the expenditure included in the asset’s cost base or not make that choice. If you do not choose to index the expenditure, your net capital gain includes only part of your capital gain on the CGT asset as worked out on the basis of the cost base not including indexation and reduced by your capital losses.

(3) Also, for the purpose of working out the *capital gain of a *life insurance company from a *CGT event happening after 30 June 2000 in respect of a *CGT asset that is a *virtual PST asset, the cost base includes indexation only if the life insurance company chooses that the cost base includes indexation.

Note: Section 110‑25 of the Income Tax (Transitional Provisions) Act 1997 provides that, in working out the capital gain from a CGT event after 11.45 am on 21 September 1999 and before 1 July 2000 in respect of an asset of a life insurance company or registered organisation, the cost base includes indexation only if the company or organisation chooses it.

43 Section 110‑38

Before “Expenditure”, insert “(1)”.

44 At the end of section 110‑38

Add:

(2) Expenditure does not form part of any element of the cost base to the extent that it is a *bribe to a foreign public official or a *bribe to a public official.

(3) Expenditure does not form part of any element of the cost base to the extent that it is in respect of providing *entertainment.

(4) Expenditure does not form part of any element of the cost base to the extent that section 26‑5 prevents it being deducted (even if some other provision also prevents it being deducted).

Note: Section 26‑5 denies deductions for penalties.

45 After subsection 110‑55(9A)

Insert:

(9B) Expenditure does not form part of the reduced cost base to the extent that it is a *bribe to a foreign public official or a *bribe to a public official.

(9C) Expenditure does not form part of the reduced cost base to the extent that it is in respect of providing *entertainment.

(9D) Expenditure does not form part of the reduced cost base to the extent that section 26‑5 prevents it being deducted (even if some other provision also prevents it being deducted).

Note: Section 26‑5 denies deductions for penalties.

46 Section 114‑1 (note 3)

Omit “non‑capital costs of ownership”, substitute “costs of ownership”.

47 Subsections 114‑5(2) and (3)

Omit “for the purposes of section 110‑25”.

48 Subsection 960‑275(4)

Omit “non‑capital costs of ownership”, substitute “costs of ownership”.

49 Subsection 995‑1(1) (definition of incidental costs)

Repeal the definition, substitute:

incidental costs has the meaning given by section 110‑35.

50 Section 114‑5

Omit “section 110‑25 of”.

51 Application

(1) The amendments made by Part 1 of this Schedule apply to expenditure incurred on or after 1 July 2005.

(2) The amendments made by Part 2 of this Schedule apply to CGT events happening on or after 1 July 2005.

1 After Division 288 in Schedule 1

Insert:

Table of Subdivisions

290‑A Objects of this Division

290‑B Civil penalties

290‑C Injunctions

290‑D Voluntary undertakings

Table of sections

290‑5 Objects of this Division

The objects of this Division are:

(a) to deter the promotion of tax avoidance *schemes and tax evasion schemes; and

(b) to deter the implementation of schemes that have been promoted on the basis of conformity with a *product ruling in a way that is materially different from that described in the product ruling.

Table of sections

290‑50 Civil penalties

290‑55 Exceptions

290‑60 Meaning of promoter

290‑65 Meaning of tax exploitation scheme

Promoter of tax exploitation scheme

(1) An entity must not engage in conduct that results in that or another entity being a *promoter of a *tax exploitation scheme.

Implementing scheme otherwise than in accordance with ruling

(2) An entity must not engage in conduct that results in a *scheme that has been promoted on the basis of conformity with a *product ruling being implemented in a way that is materially different from that described in the product ruling.

Note: A scheme will not have been implemented in a way that is materially different from that described in a product ruling if the tax outcome for participants in the scheme is the same as that described in the ruling.

Civil penalty

(3) If the Federal Court of Australia is satisfied, on application by the Commissioner, that an entity has contravened subsection (1) or (2), the Court may order the entity to pay a civil penalty to the Commonwealth.

Amount of penalty

(4) The maximum amount of the penalty is the greater of:

(a) 5,000 penalty units (for an individual) or 25,000 penalty units (for a body corporate); and

(b) twice the consideration received or receivable (directly or indirectly) by the entity and *associates of the entity in respect of the *scheme.

Note: See section 4AA of the Crimes Act 1914 for the current value of a penalty unit.

Principles relating to penalties

(5) In deciding what penalty is appropriate for a contravention of subsection (1) or (2) by an entity, the Federal Court of Australia may have regard to all matters it considers relevant, including:

(a) the amount of the consideration received or receivable (directly or indirectly) by the entity and *associates of the entity in respect of the *scheme; and

(b) the deterrent effect that any penalty may have; and

(c) the amount of loss or damage incurred by scheme participants; and

(d) the nature and extent of the contravention; and

(e) the circumstances in which the contravention took place, including the deliberateness of the entity’s conduct and whether there was an honest and reasonable mistake of law; and

(f) the period over which the conduct extended; and

(g) whether the entity took any steps to avoid the contravention; and

(h) whether the entity has previously been found by the Court to have engaged in the same or similar conduct; and

(i) the degree of the entity’s cooperation with the Commissioner.

Recovery of penalty

(6) The penalty is a civil debt payable to the Commonwealth, and the Commissioner may, on behalf of the Commonwealth, enforce an order for an entity to pay the penalty as if it were an order made in civil proceedings against the entity to recover a debt due by the entity. The debt arising from the order is taken to be a judgment debt.

Reasonable mistake or reasonable precautions

(1) The Federal Court of Australia must not order the entity to pay a civil penalty if the entity satisfies the Court:

(a) that the conduct in respect of which the proceedings were instituted was due to a reasonable mistake of fact; or

(b) that:

(i) the conduct in respect of which the proceedings were instituted was due to the act or default of another entity, to an accident or to some other cause beyond the entity’s control; and

(ii) the entity took reasonable precautions and exercised due diligence to avoid the conduct.

(2) The other entity referred to in paragraph (1)(b) does not include someone who was an employee or agent of the entity when the alleged conduct occurred.

Reliance on advice from the Commissioner

(3) The Commissioner must not make an application under section 290‑50 for conduct referred to in subsection 290‑50(1) in relation to an entity’s involvement in a *scheme if:

(a) the scheme is based on treating a *taxation law as applying in a particular way; and

(b) that way agrees with:

(i) advice given to the entity or the entity’s agent by or on behalf of the Commissioner; or

(ii) a statement in a publication approved in writing by the Commissioner.

Time limitation

(4) The Commissioner must not make an application under section 290‑50 in relation to an entity’s involvement in a *tax exploitation scheme more than 4 years after the entity last engaged in conduct that resulted in the entity or another entity being a *promoter of the tax exploitation scheme.

(5) The Commissioner must not make an application under section 290‑50 in relation to an entity’s involvement in a *scheme that has been promoted on the basis of conformity with a *product ruling more than 4 years after the entity last engaged in conduct in relation to implementation of the scheme.

(6) However, the limitation in subsection (4) or (5) does not apply to a *scheme involving tax evasion.

Exception where entity does not know result of conduct

(7) The Federal Court of Australia must not order an entity to pay a civil penalty in relation to the entity’s engaging in conduct:

(a) that results in another entity being a *promoter of a *tax exploitation scheme; or

(b) that results in a *scheme that has been promoted on the basis of conformity with a *product ruling being implemented in a way that is materially different from that described in the product ruling;

if the entity satisfies the Court that the entity did not know, and could not reasonably be expected to have known, that the entity’s conduct would produce that result.

Employees

(8) The Commissioner must not make an application under section 290‑50 in relation to an individual’s involvement in a *scheme as an employee if the Federal Court of Australia has ordered the individual’s employer to pay a civil penalty under this Division in relation to the same scheme.

(1) An entity is a promoter of a *tax exploitation scheme if:

(a) the entity markets the scheme or otherwise encourages the growth of the scheme or interest in it; and

(b) the entity or an *associate of the entity receives (directly or indirectly) consideration in respect of that marketing or encouragement; and

(c) having regard to all relevant matters, it is reasonable to conclude that the entity has had a substantial role in respect of that marketing or encouragement.

(2) However, an entity is not a promoter of a *tax exploitation scheme merely because the entity provides advice about the *scheme.

(3) An employee is not to be taken to have had a substantial role in respect of that marketing or encouragement merely because the employee distributes information or material prepared by another entity.

(1) A *scheme is a tax exploitation scheme if, at the time of the conduct mentioned in subsection 290‑50(1):

(a) one of these conditions is satisfied:

(i) if the scheme has been implemented—it is reasonable to conclude that an entity that (alone or with others) entered into or carried out the scheme did so with the sole or dominant purpose of that entity or another entity getting a *scheme benefit from the scheme;

(ii) if the scheme has not been implemented—it is reasonable to conclude that, if an entity (alone or with others) had entered into or carried out the scheme, it would have done so with the sole or dominant purpose of that entity or another entity getting a scheme benefit from the scheme; and

(b) one of these conditions is satisfied:

(i) if the scheme has been implemented—it is not *reasonably arguable that the scheme benefit is available at law;

(ii) if the scheme has not been implemented—it is not reasonably arguable that the scheme benefit would be available at law if the scheme were implemented.

Note: The condition in paragraph (b) would not be satisfied if the implementation of the scheme for all participants were in accordance with binding advice given by or on behalf of the Commissioner of Taxation (for example, if that implementation were in accordance with a public ruling under this Act, or all participants had private rulings under this Act and that implementation were in accordance with those rulings).

(2) In deciding whether it is *reasonably arguable that a *scheme benefit would be available at law, take into account any thing that the Commissioner can do under a *taxation law.

Example: The Commissioner may cancel a tax benefit obtained by a taxpayer in connection with a scheme under section 177F of the Income Tax Assessment Act 1936.

Table of sections

290‑120 Conduct to which this Subdivision applies

290‑125 Injunctions

290‑130 Interim injunctions

290‑135 Delay in making ruling

290‑140 Discharge etc. of injunctions

290‑145 Certain limits on granting injunctions not to apply

290‑150 Other powers of the Federal Court unaffected

This Subdivision applies to conduct of the kind referred to in subsection 290‑50(1) or (2).

If an entity has engaged, is engaging or is proposing to engage in conduct to which this Subdivision applies or would apply, the Federal Court of Australia may, on the application of the Commissioner, grant an injunction:

(a) restraining the entity from engaging in the conduct; and

(b) if, in the Court’s opinion, it is desirable to do so—requiring the entity to do something.

The Federal Court of Australia may, before considering an application for an injunction under section 290‑125, grant an interim injunction restraining an entity from engaging in conduct to which this Subdivision applies.

If:

(a) an entity applied in writing to the Commissioner for a *product ruling in relation to a *scheme; and

(b) the Commissioner has neither made the ruling nor told the entity in writing that the Commissioner has declined to make the ruling;

the Commissioner must not make an application under section 290‑125 in relation to conduct or proposed conduct by an entity in relation to the scheme until the Commissioner makes the ruling or tells the entity in writing that the Commissioner has declined to make the ruling.

The Federal Court of Australia may discharge or vary an injunction granted under this Subdivision.

Restraining injunctions

(1) The power of the Federal Court of Australia under this Subdivision to grant an injunction restraining an entity from engaging in conduct of a particular kind may be exercised:

(a) if the Court is satisfied that the entity has engaged in conduct of that kind—whether or not it appears to the Court that the entity intends to engage again, or to continue to engage, in conduct of that kind; or

(b) if it appears to the Court that, if an injunction is not granted, it is likely that the entity will engage in conduct of that kind—whether or not the entity has previously engaged in conduct of that kind and whether or not there is an imminent danger of substantial damage to anyone if the entity engages in conduct of that kind.

Performance injunctions

(2) The power of the Federal Court of Australia under this Subdivision to grant an injunction requiring an entity to do something may be exercised:

(a) if the Court is satisfied that the entity has refused or failed to do that thing—whether or not it appears to the Court that the entity intends to refuse or fail again, or to continue to refuse or fail, to do that thing; or

(b) if it appears to the Court that, if an injunction is not granted, it is likely that the entity will refuse or fail to do that thing—whether or not the entity has previously refused or failed to do that act or thing and whether or not there is an imminent danger of substantial damage to anyone if the entity refuses or fails to do that act or thing.

The powers conferred on the Federal Court of Australia under this Subdivision are in addition to, and not instead of, any other powers of the Court, however conferred.

Table of sections

290‑200 Voluntary undertakings

(1) The Commissioner may accept a written undertaking given by an entity for the purposes of this section in connection with furthering the objects of this Division.

(2) The entity may withdraw or vary the undertaking at any time, but only with the consent of the Commissioner.

(3) If the Commissioner considers that the entity that gave the undertaking has breached any of its terms, the Commissioner may apply to the Federal Court of Australia for an order under subsection (4).

(4) If the Court is satisfied that the entity has breached a term of the undertaking, the Court may make one or both of the following orders:

(a) an order directing the entity to comply with that term of the undertaking;

(b) any other order that the Court considers appropriate.

2 At the end of Division 298 in Schedule 1

Add:

Table of sections

298‑80 Application of Subdivision

298‑85 Civil evidence and procedure rules for civil penalty orders

298‑90 Civil proceedings after criminal proceedings

298‑95 Criminal proceedings during civil proceedings

298‑100 Criminal proceedings after civil proceedings

298‑105 Evidence given in proceedings for penalty not admissible in criminal proceedings

298‑110 Civil double jeopardy

This Subdivision applies for the purposes of the provisions (the civil penalty provisions) set out in this table.

Application of Subdivision | ||

Item | Provision | Brief description |

1 | Division 290 | Civil penalties for the promotion and implementation of schemes |

The Federal Court of Australia must apply the rules of evidence and procedure for civil matters when hearing proceedings for a civil penalty order under the civil penalty provisions.

The Court must not make a civil penalty order under the civil penalty provisions against an entity if the entity has been convicted of an offence constituted by conduct that is substantially the same as the conduct in relation to which the civil penalty order would be made.

(1) Proceedings for a civil penalty order under the civil penalty provisions against an entity are stayed if:

(a) criminal proceedings are started or have already been started against the entity for an offence; and

(b) the offence is constituted by conduct that is substantially the same as the conduct in relation to which the civil penalty order would be made.

(2) The proceedings for the order may be resumed if the entity is not convicted of the offence. Otherwise, the proceedings for the order are dismissed.

Criminal proceedings may be started against an entity for conduct that is substantially the same as conduct in relation to which a civil penalty order under the civil penalty provisions could be made regardless of whether a civil penalty order has been made against the entity.

Evidence of information given or evidence of production of documents by an entity is not admissible in criminal proceedings against the entity if:

(a) the entity previously gave the evidence or produced the documents in proceedings for a civil penalty order under the civil penalty provisions against the entity (whether or not the order was made); and

(b) the conduct alleged to constitute the offence is substantially the same as the conduct in relation to which the civil penalty order was sought.

However, this does not apply to a criminal proceeding in respect of the falsity of the evidence given by the entity in the proceedings for the civil penalty order.

If an entity is ordered to pay a civil penalty under the civil penalty provisions in respect of particular conduct, the entity is not liable to a civil penalty under some other provision of a *Commonwealth law in respect of that conduct.

3 Subsection 995‑1(1)

Insert:

product ruling means a public ruling under the Taxation Administration Act 1953 that states that it is a product ruling.

4 Subsection 995‑1(1)

Insert:

promoter has the meaning given by section 290‑60 in Schedule 1 to the Taxation Administration Act 1953.

5 Subsection 995‑1(1)

Insert:

tax exploitation scheme has the meaning given by section 290‑65 in Schedule 1 to the Taxation Administration Act 1953.

6 Subsection 16‑35(1) in Schedule 1 (note 2)

After “administrative”, insert “and civil”.

7 Subsection 16‑43(2) in Schedule 1 (note)

After “administrative”, insert “and civil”.

8 Subsection 16‑140(3) in Schedule 1 (note 2)

After “administrative”, insert “and civil”.

9 Section 255‑1 in Schedule 1

Before “A tax‑related liability”, insert “(1)”.

10 At the end of section 255‑1 in Schedule 1

Add:

(2) A civil penalty under Division 290 is not a tax‑related liability.

11 Part 4‑25 in Schedule 1 (heading)

Repeal the heading, substitute:

12 Section 288‑10 in Schedule 1 (note 2)

After “administrative”, insert “and civil”.

13 Section 288‑20 in Schedule 1 (note 2)

After “administrative”, insert “and civil”.

14 Division 298 in Schedule 1 (heading)

Repeal the heading, substitute:

15 Section 298‑5 in Schedule 1

Repeal the section, substitute:

This Subdivision applies if:

(a) an administrative penalty is imposed on an entity by another Division in this Part; or

(b) a penalty is imposed on an entity by Subdivision 162‑D of the *GST Act.

16 Section 420‑5 in Schedule 1 (note 2)

After “administrative”, insert “and civil”.

17 Application

The amendments made by this Schedule apply in relation to conduct engaged in on or after the day on which this Act receives the Royal Assent.

1 At the end of subsection 29‑25(2)

Add:

; or (h) a supply or acquisition for which the GST treatment will be unknown until a later supply is made.

2 Section 100‑1 (note)

Omit “state a”, substitute “have a stated”.

3 Section 100‑5 (heading)

Repeal the heading, substitute:

4 Paragraph 100‑5(1)(a)

Omit “a monetary value stated on the voucher”, substitute “the *stated monetary value of the voucher”.

5 Paragraph 100‑5(1)(b)

Omit “that monetary value”, substitute “the stated monetary value of the voucher”.

6 Subsection 100‑5(2)

Omit “that monetary value”, substitute “the *stated monetary value of the voucher”.

7 After subsection 100‑5(2)

Insert:

(2A) The stated monetary value, in relation to a *voucher other than a *prepaid phone card or facility, means the monetary value stated on the voucher or in documents accompanying the voucher.

(2B) The stated monetary value, in relation to a *voucher that is a *prepaid phone card or facility, means the sum of:

(a) in any case—the monetary value stated on the voucher or in documents accompanying the voucher; and

(b) if the voucher is topped up after it is supplied—the monetary value of the top‑up stated on the voucher or in documents accompanying the top‑up.

However, disregard the monetary value stated on the voucher (or in documents accompanying the voucher) or top‑up (as the case requires), of any bonus supplies covered by the voucher or top‑up (as the case requires).

8 Subsection 100‑10(3)

Omit “a monetary value stated on the voucher”, substitute “the *stated monetary value of the voucher”.

9 After section 100‑10

Insert:

(1) To avoid doubt, the consideration for a *taxable supply of a thing acquired by fully redeeming a *voucher is taken to be the sum of:

(a) the *stated monetary value of the voucher, reduced by any amount of that value refunded to the holder of the voucher in respect of the supply; and

(b) any additional consideration provided for the supply.

(2) To avoid doubt, the consideration for a *taxable supply of a thing acquired by partly redeeming a *voucher is taken to be the sum of:

(a) the amount of the *stated monetary value of the voucher that the redemption represents; and

(b) any additional consideration provided for the supply.

(3) Subsections (1) and (2) have effect despite section 9‑15 (which is about consideration).

10 Paragraph 100‑15(1)(b)

Omit “a monetary value stated on the voucher”, substitute “the *stated monetary value of the voucher”.

11 Paragraph 100‑15(1)(c)

Before “redeemed”, insert “fully”.

12 Subsection 100‑15(2)

Repeal the subsection, substitute:

(2) The amount of the increasing adjustment is 1/11 of the *stated monetary value of the voucher to the extent that it was not redeemed.

13 After section 100‑15

Insert:

(1) An entity (the supplier) may, in writing, enter into an arrangement with another entity under which the other entity supplies (whether or not as an agent on the supplier’s behalf) a *voucher to a third party.

(2) If, under the arrangement, the supplier pays, or is liable to pay, an amount, as a commission or similar payment, to the other entity for the other entity’s supply, the supply by the other entity to the supplier, to which the supplier’s payment or liability relates, is treated as if it were not a *taxable supply.

(3) This section has effect despite section 9‑5 (which is about what are taxable supplies).

14 Section 100‑25

Repeal the section, substitute:

(1) A voucher is any:

(a) voucher, token, stamp, coupon or similar article; or

(b) *prepaid phone card or facility;

the redemption of which in accordance with its terms entitles the holder to receive supplies in accordance with its terms. However, a postage stamp is not a voucher.

(2) A prepaid phone card or facility is any article or facility supplied for the primary purpose of enabling the holder:

(a) to use, on a prepaid basis, telephone or like services supplied by a supplier of *telecommunications supplies; or

(b) to make, on a prepaid basis, acquisitions that are facilitated by using telephone or like services supplied by such a supplier.

15 Section 195‑1 (note to the definition of consideration)

After “100‑5”, insert “, 100‑12”.

16 Section 195‑1

Insert: