Tax Laws Amendment (2006 Measures No. 2) Act 2006

No. 58, 2006

An Act to amend the law relating to taxation, and for related purposes

Tax Laws Amendment (2006 Measures No. 2) Act 2006

No. 58, 2006

An Act to amend the law relating to taxation, and for related purposes

Contents

1 Short title

2 Commencement

3 Schedule(s)

4 Amendment of assessments

Schedule 1—F‑111 Deseal/Reseal Ex‑gratia Lump Sum Payments

Income Tax Assessment Act 1997

Schedule 2—Specific gift recipients

Income Tax Assessment Act 1997

Schedule 3—CGT treatment of options

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Schedule 4—Compulsory acquisition

Income Tax Assessment Act 1997

Schedule 5—Franking deficit tax

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Schedule 6—Choice of superannuation fund

Superannuation Guarantee (Administration) Act 1992

Schedule 7—Technical corrections and improvements

Part 1—Amendments commencing on Royal Assent

A New Tax System (Commonwealth‑State Financial Arrangements) Act 1999

A New Tax System (Goods and Services Tax) Act 1999

A New Tax System (Goods and Services Tax Transition) Act 1999

A New Tax System (Luxury Car Tax) Act 1999

A New Tax System (Wine Equalisation Tax) Act 1999

Commonwealth Places (Mirror Taxes) Act 1998

Fringe Benefits Tax Assessment Act 1986

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Income Tax Rates Act 1986

Income Tax (Transitional Provisions) Act 1997

Sales Tax Legislation Amendment Act (No. 1) 1999

Superannuation Guarantee (Administration) Act 1992

Taxation Administration Act 1953

Taxation Laws Amendment Act (No. 2) 2000

Part 2—Amendments commencing at other times

A New Tax System (Family Assistance) (Consequential and Related Measures) Act (No. 2) 1999

Fuel Tax Act 2006

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Taxation (Interest on Overpayments and Early Payments) Act 1983

Tax Laws Amendment (2004 Measures No. 1) Act 2004

Tax Laws Amendment (2004 Measures No. 2) Act 2004

Part 3—Amendments relating to asterisking

Division 1—Asterisking of “partnership”

Income Tax Assessment Act 1997

Division 2—Asterisking of “derived”

Income Tax Assessment Act 1997

Division 3—Asterisking of “market value”

Income Tax Assessment Act 1997

Division 4—Other asterisking amendments

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Part 4—Technical amendments relating to legislative instruments

A New Tax System (Goods and Services Tax) Act 1999

Commonwealth Places (Mirror Taxes) Act 1998

Energy Grants (Credits) Scheme Act 2003

Excise Act 1901

Excise Tariff Act 1921

Fringe Benefits Tax Assessment Act 1986

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Superannuation Contributions Tax (Assessment and Collection) Act 1997

Superannuation Contributions Tax (Members of Constitutionally Protected Superannuation Funds) Assessment and Collection Act 1997

Superannuation (Government Co‑contribution for Low Income Earners) Act 2003

Taxation Laws Amendment Act (No. 5) 2001

Tax Laws Amendment (2006 Measures No. 2) Act 2006

No. 58, 2006

An Act to amend the law relating to taxation, and for related purposes

[Assented to 22 June 2006]

The Parliament of Australia enacts:

This Act may be cited as the Tax Laws Amendment (2006 Measures No. 2) Act 2006.

(1) Each provision of this Act specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information | ||

Column 1 | Column 2 | Column 3 |

Provision(s) | Commencement | Date/Details |

1. Sections 1 to 4 and anything in this Act not elsewhere covered by this table | The day on which this Act receives the Royal Assent. | 22 June 2006 |

2. Schedules 1 to 4 | The day on which this Act receives the Royal Assent. | 22 June 2006 |

3. Schedule 5, items 1 to 3 | The day on which this Act receives the Royal Assent. | 22 June 2006 |

4. Schedule 5, items 4 and 5 | 1 July 2002. | 1 July 2002 |

5. Schedule 6 | The day on which this Act receives the Royal Assent. | 22 June 2006 |

6. Schedule 7, Part 1 | The day on which this Act receives the Royal Assent. | 22 June 2006 |

7. Schedule 7, item 171 | Immediately after the commencement of item 20 of Schedule 10 to the A New Tax System (Family Assistance) (Consequential and Related Measures) Act (No. 2) 1999. | 1 July 2000 |

8. Schedule 7, item 172 | Immediately after the commencement of the Fuel Tax Act 2006. | 1 July 2006 |

9. Schedule 7, item 173 | Immediately after the commencement of item 82 of Schedule 2 to the New Business Tax System (Miscellaneous) Act (No. 2) 2000. | 30 June 2000 |

10. Schedule 7, item 174 | 24 October 2002. | 24 October 2002 |

11. Schedule 7, item 175 | Immediately after the commencement of item 82 of Schedule 2 to the New Business Tax System (Miscellaneous) Act (No. 2) 2000. | 30 June 2000 |

12. Schedule 7, item 176 | 30 June 2004. | 30 June 2004 |

13. Schedule 7, item 177 | 24 December 1992. | 24 December 1992 |

14. Schedule 7, item 178 | 30 June 2004. | 30 June 2004 |

15. Schedule 7, items 179 to 188 | Immediately after the commencement of Schedule 7 to the Tax Laws Amendment (2004 Measures No. 1) Act 2004. | 1 July 2004 |

16. Schedule 7, item 189 | Immediately after the commencement of Schedule 5 to the Taxation Laws Amendment Act (No. 6) 1999. | 5 July 1999 |

17. Schedule 7, item 190 | Immediately after the commencement of item 82 of Schedule 2 to the New Business Tax System (Miscellaneous) Act (No. 2) 2000. | 30 June 2000 |

18. Schedule 7, item 191 | Immediately after the commencement of the New Business Tax System (Consolidation) Act (No. 1) 2002. | 24 October 2002 |

19. Schedule 7, item 192 | 30 June 2004. | 30 June 2004 |

20. Schedule 7, item 193 | Immediately after the A New Tax System (Pay As You Go) Act 1999 received the Royal Assent. | 22 December 1999 |

21. Schedule 7, items 194 to 209 | Immediately after the commencement of the Fuel Tax Act 2006. | 1 July 2006 |

22. Schedule 7, item 210 | Immediately before the commencement of Schedule 10 to the Tax Laws Amendment (2004 Measures No. 1) Act 2004. | 1 July 2005 |

23. Schedule 7, items 211 and 212 | Immediately after the commencement of Schedule 10 to the Tax Laws Amendment (2004 Measures No. 1) Act 2004. | 1 July 2005 |

24. Schedule 7, Parts 3 and 4 | The day on which this Act receives the Royal Assent. | 22 June 2006 |

Note: This table relates only to the provisions of this Act as originally passed by the Parliament and assented to. It will not be expanded to deal with provisions inserted in this Act after assent.

(2) Column 3 of the table contains additional information that is not part of this Act. Information in this column may be added to or edited in any published version of this Act.

Each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

Section 170 of the Income Tax Assessment Act 1936 does not prevent the amendment of an assessment if:

(a) the assessment was made before the commencement of this section; and

(b) the amendment is made within 4 years after that commencement; and

(c) the amendment is made for the purpose of giving effect to Schedule 4.

1 Section 11‑15 (table item headed “defence”)

After:

Defence Force member, compensation payments for loss of deployment allowance for warlike service |

|

insert:

F‑111 Deseal/Reseal Ex‑gratia Lump Sum Payments | 51‑5 |

2 Section 51‑5 (at the end of the table)

Add:

1.6 | a recipient of an ex‑gratia payment from the Commonwealth known as the F‑111 Deseal/Reseal Ex‑gratia Lump Sum Payment | the ex‑gratia payment | none |

3 Application

The amendments made by this Schedule apply in relation to the 2005‑2006 income year and later income years.

1 Subsection 30‑70(2) (at the end of the table)

Add:

8.2.10 | Playgroup Victoria Inc. | the gift must be made after 23 February 2006 |

2 Section 30‑105 (at the end of the table)

Add:

13.2.11 | St Michael’s Church Restoration Fund | the gift must be made after 23 February 2006 and before 24 February 2007 |

3 Section 30‑315 (after table item 86D)

Insert:

86DA | Playgroup Victoria Inc. | item 8.2.10 |

4 Section 30‑315 (after table item 112AF)

Insert:

112AG | St Michael’s Church Restoration Fund | item 13.2.11 |

1 Section 116‑65

Repeal the section, substitute:

(1) This section applies if:

(a) you granted, renewed or extended an option to create (including grant or issue) or *dispose of a *CGT asset; and

(b) another entity exercises the option; and

(c) because of the exercise of the option, you create (including grant or issue) or dispose of the CGT asset.

(2) The *capital proceeds from the creation (including grant or issue) or disposal include any payment you received for granting, renewing or extending the option.

(3) The payment can include giving property: see section 103‑5.

2 Section 116‑70

Repeal the section, substitute:

(1) This section applies if:

(a) you granted, renewed or extended an option; and

(b) the option requires you both to *acquire, and to create (including grant or issue) or *dispose of, a *CGT asset.

(2) The option is treated as 2 separate options and half of the *capital proceeds from the grant, renewal or extension is attributed to each option.

3 Subsection 134‑1(1)

Repeal the subsection, substitute:

(1) This table sets out the effects of the exercise of an option (including an option that has been renewed or extended) on the *cost bases and *reduced cost bases of the grantor and the entity that exercises the option (the grantee).

Exercise of options | ||

Item | In this situation: | Effect on cost base and reduced cost base: |

1 | Option binds grantor to: (a) *dispose of a *CGT asset; or (b) create (including grant or issue) a CGT asset (call option) | For the grantee The first element of the grantee’s *cost base and *reduced cost base for the CGT asset is what the grantee paid for the option (or to renew or extend it) plus any amount the grantee paid to exercise it For the grantor See section 116‑65 |

2 | Option binds grantor to *acquire a *CGT asset (put option) | For the grantor The first element of the grantor’s *cost base and *reduced cost base for the asset acquired is any amount paid to exercise the option reduced by any payment received by the grantor for the option (or to renew or extend it) For the grantee The second element of the grantee’s cost base and reduced cost base for the asset acquired by the grantor includes any payment the grantee made to acquire the option (or to renew or extend it) |

Note 1: If you granted, renewed or extended an option, CGT event C3 or D2 may happen.

Note 2: Item 1 in the table is modified for certain options granted before 20 September 1985: see section 134‑1 of the Income Tax (Transitional Provisions) Act 1997.

Note 3: Item 1 in the table is modified for shares or rights acquired at a discount (within the meaning of Subdivision C of Division 13A of Part III of the Income Tax Assessment Act 1936) under an employee share scheme—in certain circumstances you can be taken to have paid the market value for an option: see Subdivision 130‑D and section 112‑15.

4 Section 134‑1

Before “The modification in item 1”, insert “(1)”.

5 Section 134‑1

Omit “dispose of a CGT asset”, substitute “create (including grant or issue) or dispose of a CGT asset”.

6 At the end of section 134‑1

Add:

(2) This section does not apply to an option if:

(a) it has been renewed or extended; and

(b) the last renewal or extension occurred on or after 20 September 1985.

7 Application

The amendments made by this Schedule apply in relation to options exercised on or after 27 May 2005.

1 Paragraph 40‑365(2)(c)

Repeal the paragraph, substitute:

(c) the original asset is acquired by an entity (other than an Australian government agency or a *foreign government agency) under a power of compulsory acquisition conferred by a law covered under subsection (2A); or

(d) you dispose of the original asset to an entity (other than a foreign government agency) in circumstances meeting all of these conditions:

(i) the disposal takes place after a notice was served on you by or on behalf of the entity;

(ii) the notice invited you to negotiate with the entity with a view to the entity acquiring the asset by agreement;

(iii) the notice informed you that if the negotiations were unsuccessful, the asset would be compulsorily acquired by the entity;

(iv) the compulsory acquisition would have been under a power of compulsory acquisition conferred by a law covered under subsection (2A); or

(e) you dispose of land onto which the original asset was fixed to an entity (other than a foreign government agency) in circumstances meeting all of these conditions:

(i) a mining lease was compulsorily granted over the land;

(ii) the lease significantly affected your use of the land;

(iii) the lease was in force just before the disposal;

(iv) the entity to which you dispose of the land was the lessee under the lease; or

(f) you dispose of land onto which the original asset was fixed to an entity (other than a foreign government agency) in circumstances meeting all of these conditions:

(i) a mining lease would have been compulsorily granted over the land if you had not disposed of it;

(ii) that lease would have significantly affected your use of the land;

(iii) the entity to which you dispose of the land would have been the lessee under the lease.

2 After subsection 40‑365(2)

Insert:

(2A) A law is covered under this subsection if it is:

(a) an *Australian law (other than Chapter 6A of the Corporations Act 2001); or

(b) a *foreign law (other than a foreign law corresponding to Chapter 6A of the Corporations Act 2001).

3 After paragraph 124‑70(1)(a)

Insert:

(aa) it is compulsorily acquired by an entity (other than an Australian government agency or a *foreign government agency) under a power of compulsory acquisition conferred by a law covered under subsection (1A);

4 Paragraph 124‑70(1)(c)

Repeal the paragraph, substitute:

(c) you *dispose of it to an entity (other than a foreign government agency) in circumstances meeting all of these conditions:

(i) the disposal takes place after a notice was served on you by or on behalf of the entity;

(ii) the notice invited you to negotiate with the entity with a view to the entity acquiring the asset by agreement;

(iii) the notice informed you that if the negotiations were unsuccessful, the asset would be compulsorily acquired by the entity;

(iv) the compulsory acquisition would have been under a power of compulsory acquisition conferred by a law covered under subsection (1A);

(ca) you dispose of it to an entity (other than a foreign government agency) in circumstances meeting all of these conditions:

(i) the asset is land over which a mining lease was compulsorily granted;

(ii) the lease significantly affected your use of the land;

(iii) the lease was in force just before the disposal;

(iv) the entity to which you dispose of the land was the lessee under the lease;

(cb) you dispose of it to an entity (other than a foreign government agency) in circumstances meeting all of these conditions:

(i) the asset is land over which a mining lease would have been compulsorily granted if you had not disposed of it;

(ii) that lease would have significantly affected your use of the land;

(iii) the entity to which you dispose of the land would have been the lessee under the lease.

5 After subsection 124‑70(1)

Insert:

(1A) A law is covered under this subsection if it is:

(a) an *Australian law (other than Chapter 6A of the Corporations Act 2001); or

(b) a *foreign law (other than a foreign law corresponding to Chapter 6A of the Corporations Act 2001).

6 Application

(1) The amendments made by this Schedule apply in relation to CGT events that happen after 1 pm (by legal time in the Australian Capital Territory) on 11 November 1999.

(2) The amendments made by this Schedule apply in relation to balancing adjustment events that occur after 30 June 2001.

(3) Former section 42‑293 of the Income Tax Assessment Act 1997 applies in relation to balancing adjustment events that occurred during the period:

(a) starting just after 1 pm (by legal time in the Australian Capital Territory) on 11 November 1999; and

(b) ending just before 1 July 2001;

as if the amendments made by this Schedule to section 40‑365 of that Act were made (with any necessary changes) to former section 42‑293.

(4) To avoid doubt:

(a) those necessary changes to those amendments include the following:

(i) item 1 applies in relation to former paragraph 42‑293(2)(c);

(ii) references in item 1 to the original asset are taken to be references to the original plant;

(iii) item 2 applies in relation to former section 42‑293; and

(b) a choice under former subsection 42‑293(1) may be made after the commencement of this item in relation to those amendments; and

(c) the Commissioner may allow, after the commencement of this item, a further period under former subsection 42‑293(3) in relation to those amendments.

1 Subsection 205‑70(2) (method statement, steps 1 and 2)

Repeal the steps, substitute:

Step 1. Work out the total amount of *franking deficit tax that is covered by paragraph (1)(a).

Then, subject to subsections (5) and (6), reduce so much of it as is attributable to *franking debits to which subsection (8) applies by 30% if that part exceeds 10% of the total amount of *franking credits that arose in the entity’s *franking account for the relevant year.

Step 2. Work out the total amount of *franking deficit tax that is covered by paragraph (1)(b) for a previous income year.

Then, subject to subsections (5) and (6), reduce so much of it as is attributable to *franking debits to which subsection (8) applies by 30% if that part exceeds 10% of the total amount of *franking credits that arose in the entity’s *franking account for that previous income year.

2 At the end of section 205‑70

Add:

Commissioner’s discretion

(6) The 30% reductions in steps 1 and 2 of the method statement in subsection (2) do not apply in working out the amount of the *tax offset to which the entity is entitled for the relevant year if the Commissioner determines in writing, on application by the entity in the *approved form, that the excess referred to in those steps was due to events outside the control of the entity.

(7) A determination under subsection (6) is not a legislative instrument.

Applicable franking debits

(8) This subsection applies to *franking debits in the *franking account of an entity:

(a) that arise under table item 1, 3, 5 or 6 in section 205‑30 for an income year; and

(b) if the entity has franking debits covered by paragraph (a) for that income year—that arise under table item 2 in that section for that income year.

3 Application

The amendments made by items 1 and 2 apply to assessments for the 2004‑05 income year and later income years.

4 At the end of section 205‑70

Add:

(6) The 30% reductions for an entity in steps 2 and 3 of the method statement in subsection (3), and in steps 1, 2, 3 and 4 of the method statement in subsection (4), apply only to franking deficit tax that is attributable to franking debits of the entity:

(a) that arose under table item 1, 3, 5 or 6 in section 205‑30 of the Income Tax Assessment Act 1997 for the relevant income year; and

(b) if the entity has franking debits covered by paragraph (a) for the relevant income year—that arose under table item 2 in that section of that Act for the relevant income year.

(7) The 30% reductions in those steps do not apply in working out the amount of the tax offset to which an entity is entitled for the relevant year if the Commissioner determines in writing, on application by the entity in the approved form, that the excess referred to in those steps was due to events outside the control of the entity.

(8) A determination under subsection (7) is not a legislative instrument.

5 After section 205‑70

Insert:

(1) This section applies to events that occur on or after 1 July 2002 and before the start of the 2004‑05 income year.

(2) The 30% reductions for an entity in steps 1 and 2 of the method statement in subsection 205‑70(2) of the Income Tax Assessment Act 1997 apply only to franking deficit tax that is attributable to franking debits of the entity:

(a) that arose under table item 1, 3, 5 or 6 in section 205‑30 of the Income Tax Assessment Act 1997 for the relevant income year; and

(b) if the entity has franking debits covered by paragraph (a) for the relevant income year—that arose under table item 2 in that section of that Act for the relevant income year.

(3) The 30% reductions in steps 1 and 2 of the method statement in subsection 205‑70(2) of the Income Tax Assessment Act 1997 do not apply in working out the amount of the tax offset to which an entity is entitled for the relevant year if the Commissioner determines in writing, on application by the entity in the approved form, that the excess referred to in those steps was due to events outside the control of the entity.

(4) A determination under subsection (3) is not a legislative instrument.

1 After section 32Z

Insert:

(1) This section applies to an employer that is a corporation to which paragraph 51(xx) of the Constitution applies.

(2) A requirement in a law of a State or Territory that the employer make contributions to a superannuation fund on behalf of an employee is not enforceable to the extent that the employer instead makes the contributions on behalf of the employee, in compliance with this Part, to another superannuation fund that is a chosen fund.

2 Application

The amendment made by this Schedule applies to contributions made on or after 1 July 2006.

1 Subsection 5(6) (definition of Commonwealth entity)

Repeal the definition.

2 Paragraph 75‑11(2A)(e)

Omit “value of interest”, substitute “value of the interest”.

3 Subsection 126‑10(3)

Omit “Subdivision 38‑H”, substitute “section 38‑270”.

4 Application

The amendment made by item 3 applies to supplies made on or after 14 December 2004.

5 Subdivision 165‑C (heading)

Repeal the heading.

6 Subsection 177‑1(1)

Omit “*Commonwealth entities”, substitute “*untaxable Commonwealth entities”.

7 Subsection 177‑1(1)

Omit “Commonwealth entities should”, substitute “untaxable Commonwealth entities should”.

8 Subsection 177‑1(2)

Omit “a *Commonwealth entity”, substitute “an *untaxable Commonwealth entity”.

9 Subsection 177‑1(4)

Omit “a *Commonwealth entity” (first occurring), substitute “an *untaxable Commonwealth entity”.

10 Subsection 177‑1(4)

Omit “a *Commonwealth entity” (second and third occurring), substitute “an untaxable Commonwealth entity”.

11 Subsection 177‑1(5)

Repeal the subsection, substitute:

(5) Untaxable Commonwealth entity means:

(a) an Agency (within the meaning of the Financial Management and Accountability Act 1997); or

(b) a Commonwealth authority (within the meaning of the Commonwealth Authorities and Companies Act 1997);

that cannot be made liable to taxation by a Commonwealth law.

12 Paragraph 177‑3(a)

Omit “a *Commonwealth entity”, substitute “an *untaxable Commonwealth entity”.

13 Section 195‑1 (definition of Commonwealth entity)

Repeal the definition.

14 Section 195‑1 (definition of reduced credit land transport)

Repeal the definition.

15 Section 195‑1

Insert:

untaxable Commonwealth entity has the meaning given by section 177‑1.

16 Subsection 13(4A)

Omit “a Commonwealth entity” (wherever occurring), substitute “an untaxable Commonwealth entity”.

17 Subsection 14(5)

Omit “a Commonwealth entity” (wherever occurring), substitute “an untaxable Commonwealth entity”.

18 Subsection 21‑1(1)

Omit “*Commonwealth entities”, substitute “*untaxable Commonwealth entities”.

19 Subsection 21‑1(1)

Omit “Commonwealth entities” (last occurring), substitute “untaxable Commonwealth entities”.

20 Subsection 21‑1(2)

Omit “a *Commonwealth entity”, substitute “an *untaxable Commonwealth entity”.

21 Subsection 21‑1(4)

Repeal the subsection.

22 Section 27‑1 (definition of Commonwealth entity)

Repeal the definition.

23 Section 27‑1

Insert:

untaxable Commonwealth entity has the meaning given by section 177‑1 of the *GST Act.

24 Subsection 27‑20(1)

Omit “*Commonwealth entities”, substitute “*untaxable Commonwealth entities”.

25 Subsection 27‑20(1)

Omit “Commonwealth entities” (last occurring), substitute “untaxable Commonwealth entities”.

26 Subsection 27‑20(2)

Omit “a *Commonwealth entity”, substitute “an *untaxable Commonwealth entity”.

27 Subsection 27‑20(4)

Repeal the subsection.

28 Section 33‑1 (definition of Commonwealth entity)

Repeal the definition.

29 Section 33‑1

Insert:

untaxable Commonwealth entity has the meaning given by section 177‑1 of the *GST Act.

30 Clause 4 of Schedule 1

Repeal the clause, substitute:

The Stamp Act 1921 of Western Australia is a scheduled law.

31 Clause 6 of Schedule 1

Repeal the clause, substitute:

The Pay‑roll Tax Act 1971 of Tasmania is a scheduled law.

32 Subsection 136(1) (paragraph (e) of the definition of entertainment facility leasing expenses)

After “1936”, insert “or the Income Tax Assessment Act 1997”.

33 Subsection 136(1) (definition of entity) (the definition of entity inserted by item 3 of Schedule 7 to the Taxation Laws Amendment Act (No. 4) 2003)

Repeal the definition.

34 Section 162B

Omit “Income Tax Assessment Act 1936”, substitute “Income Tax Assessment Act 1997”.

35 Subsection 6(1)

Insert:

international tax sharing treaty:

(a) means an agreement between Australia and another country under which Australia and the other country share tax revenues from activities undertaken in an area identified by or under the agreement; and

(b) does not include an agreement within the meaning of the International Tax Agreements Act 1953.

36 Subsection 6(1) (definition of non‑equity share)

Repeal the definition (including the note), substitute:

non‑equity share has the same meaning as in the Income Tax Assessment Act 1997.

37 Subsection 23AK(3) (definition of trust)

Omit “605(9)”, substitute “605(11)”.

38 Application

The amendment made by item 37 applies to assessments for the 2001‑02 income year and later income years.

39 Subparagraph 46AC(1)(b)(i)

Omit “income year”, substitute “year of income”.

40 Paragraph 82AM(3)(c)

Omit “income year”, substitute “year of income”.

41 Subsection 92(2A)

Omit “income year”, substitute “year of income”.

42 Section 102AAB (definition of listed country trust estate)

Omit “same meaning as in Part X”, substitute “meaning given by section 102AAE”.

43 Paragraph 102AAM(10)(b)

Omit “Column 2 of”.

44 Section 121AS (note 6)

Omit “Subdivision 126‑D”, substitute “Subdivision 126‑E”.

45 Subsection 136AA(1) (definition of international tax sharing treaty)

Repeal the definition.

46 Subsection 160AF(8) (definition of relevant debt deduction)

Omit “an income year”, substitute “a year of income”.

47 Subsection 170(14) (definition of international tax sharing treaty)

Repeal the definition.

48 Subsection 177EA(19)

Omit “income year”, substitute “year of income”.

49 Subsection 372(2)

Omit “Subject to subsections (3) and (4)”, substitute “Subject to subsection (4)”.

50 Paragraph 544(1)(b)

Omit “from a group”, substitute “form a group”.

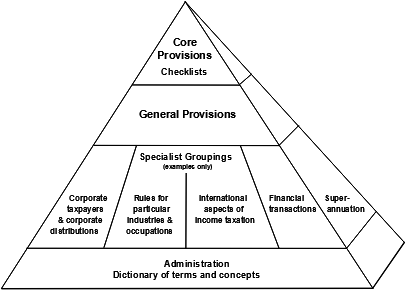

51 Section 2‑5 (pyramid)

Repeal the pyramid, substitute:

52 At the end of section 2‑5

Add:

Note: The Taxation Administration Act 1953 contains the provisions on collection and recovery of tax and provisions on administration.

53 At the end of subsection 4‑10(3)

Add:

Note: Division 63 explains what happens if your tax offsets exceed your basic income tax liability. How the excess is treated depends on the type of tax offset.

54 Subsection 4‑10(3A)

Repeal the subsection.

55 Application

The amendment made by item 54 applies to assessments for the 2006‑07 income year and later income years.

56 Subsection 6‑10(2) (note)

Repeal the note, substitute:

Note 1: Although an amount is statutory income because it has been included in assessable income under a provision of this Act, it may be made exempt income or non‑assessable non‑exempt income under another provision: see sections 6‑20 and 6‑23.

Note 2: Many provisions in the summary list in section 10‑5 contain rules about ordinary income. These rules do not change its character as ordinary income.

57 Section 11‑15 (table item headed “foreign aspects of income taxation”)

Omit:

Commonwealth sporting club or association, income of . | 23(c)(ii) |

58 Section 11‑15 (table item headed “foreign aspects of income taxation”)

Omit:

sporting club, British Commonwealth, income of ..... | 23(c)(ii) |

sports person, non‑resident, income of ...... | 23(c)(i) |

59 Section 13‑1 (table item headed “research and development”)

Omit “731”, substitute “73I”.

60 Subsection 26‑5(2) (note)

Repeal the note, substitute:

Note: See paragraph 25‑5(1)(ca) for the deductibility of penalties that arise under Subdivision 162‑D of the GST Act.

61 Subsection 30‑315(2) (table item 28A) (the table item 28A inserted by item 19 of Schedule 1 to the Taxation Laws Amendment Act (No. 4) 1999)

Renumber the item as 28AB.

62 Section 61‑496

Repeal the section, substitute:

(1) You may transfer your entitlement to so much of your *tax offset as is equal to the excess to the individual who was your *spouse as at the last day of the child care offset year.

Note: The excess part of a tax offset is worked out under Division 63.

(2) If you make a transfer:

(a) the transferee is entitled to the transferred part of the *tax offset for the child care offset year; and

(b) you are no longer entitled to the transferred part of the tax offset.

(3) A transfer cannot be revoked.

(4) If you die during the child care offset year, the reference to your *spouse in subsection (1) is taken to be a reference to your spouse just before your death.

63 Subsection 61‑497(1)

Omit “it is”, substitute “you have applied for it”.

64 After Division 61

Insert:

This Division sets out some rules that are common to all tax offsets.

Table of sections

63‑10 Priority rules

(1) If you have one or more *tax offsets for an income year, apply them against your basic income tax liability in the order shown in the table. To the extent that an amount of a tax offset remains, the table tells you what happens to it.

Order of applying tax offsets | ||

Item | Tax offset | What happens to any excess |

5 | *Tax offset under section 160AAAA of the Income Tax Assessment Act 1936 (tax offset for low income aged persons) | Your entitlement to it is transferred in accordance with regulations made under that Act |

10 | *Tax offset under section 160AAAB of the Income Tax Assessment Act 1936 (tax offset for low income aged persons—trustee assessed under section 98) | Your entitlement to it is transferred in accordance with regulations made under that Act |

15 | *Tax offset under section 160AAA of the Income Tax Assessment Act 1936 (tax offset in respect of certain pensions) | Your entitlement to it is transferred in accordance with regulations made under that Act |

20 | Any *tax offset not covered by another item in this table | You cannot get a refund of it, you cannot transfer it and you cannot carry it forward to a later income year |

25 | Child care *tax offset under Subdivision 61‑IA | You may transfer your entitlement to it to your *spouse (under sections 61‑496 and 61‑497) |

30 | Landcare and water facility *tax offset under the former Subdivision 388‑A | You may carry it forward to a later income year (under Division 65) |

35 | Foreign tax credit under Division 18 of Part III of the Income Tax Assessment Act 1936 | You may carry it forward to a later income year (under section 160AFE of that Act) |

40 | *Tax offset that is subject to the refundable tax offset rules in Division 67 | You can get a refund of the remaining amount |

45 | *Tax offset arising from payment of *franking deficit tax (see section 205‑70) | You may carry it forward to a later income year (under section 205‑70) |

Note 1: Section 13‑1 lists tax offsets.

Note 2: Former Division 388 was repealed by the New Business Tax System (Capital Allowances—Transitional and Consequential) Act 2001.

Note 3: Section 160AFE of the Income Tax Assessment Act 1936 also affects how much of a foreign tax credit can be applied against your basic income tax liability.

Note 4: The remaining amount of a carry forward tax offset may be reduced by section 65‑30 or 65‑35 to take account of net exempt income.

Note 5: Tax offsets mentioned in items 5 and 10 are more commonly referred to as the Senior Australians Tax Offset.

(2) Within each item, apply the tax offsets in the order in which they arose.

Note: This would be relevant if you have carry forward tax offsets of the same category for different income years.

65 Sections 65‑20 and 65‑25

Repeal the sections.

66 Section 65‑30

Omit “subsection 65‑25(1)”, substitute “Division 63”.

67 Subsection 65‑35(2)

Repeal the subsection, substitute:

(2) You apply a *tax offset that is carried forward to a later year in accordance with the priorities set out in Division 63 as if it were a tax offset for that later year.

68 Sections 67‑30 and 67‑35

Repeal the sections.

69 Application

The amendments made by items 62 to 68 apply to assessments for the 2006‑07 income year and later income years.

70 Subsections 70‑105(2) and (6)

Omit “person on whom”, substitute “entity on which”.

71 After subsection 87‑40(1)

Insert:

Agent rules do not apply

(1A) The rules in section 960‑105 (Certain entities treated as agents) do not apply to this section.

72 Section 109‑60 (table item 4A)

After “Division 326”, insert “of Schedule 2H”.

73 Section 112‑97 (table item 5A)

After “Division 326”, insert “of Schedule 2H”.

74 Section 112‑150 (table item 7) (the table item 7 inserted by item 2 of Schedule 11 to the Taxation Laws Amendment Act (No. 2) 2002)

Repeal the item.

75 Section 112‑150 (before table item 9)

Insert:

8 | Beneficiary becomes absolutely entitled to a share following a roll‑over under Subdivision 124‑M | Subdivision 126‑E |

76 Subsection 115‑45(2) (note)

Repeal the note, substitute:

Note: This section does not prevent a capital gain from being a discount capital gain if there are at least 300 members or beneficiaries of the company or trust and control of the company or trust is not and cannot be concentrated (see section 115‑50).

77 Subsection 124‑520(2)

After “Division 326”, insert “in Schedule 2H”.

78 Subsection 124‑780(1) (note 3)

Omit “Subdivision 126‑D”, substitute “Subdivision 126‑E”.

79 Subsection 124‑870(4) (note)

Omit “ut before”, substitute “but before”.

80 Subdivision 126‑D (the Subdivision 126‑D inserted by item 4 of Schedule 11 to the Taxation Laws Amendment Act (No. 2) 2002)

Reletter as Subdivision 126‑E.

81 Subdivision 126‑E (as relettered)

Relocate to after Subdivision 126‑D (the Subdivision 126‑D inserted by item 19 of Schedule 1 to the Family Law Legislation Amendment (Superannuation) (Consequential Provisions) Act 2001).

82 Group heading before section 126‑185

Repeal the heading, substitute:

83 Section 152‑200

Repeal the section, substitute:

This Subdivision tells you how to apply the small business CGT concessions mentioned in step 4 of the method statement in subsection 102‑5(1).

A capital gain is reduced by 50% if the basic conditions in Subdivision 152‑A are satisfied.

If the capital gain has already been reduced by the discount percentage, the 50% reduction under this Subdivision applies to that reduced gain.

The capital gain may be further reduced by the small business retirement exemption or a small business rollover, or both.

Alternatively, you may choose not to apply the 50% reduction and instead apply the small business retirement exemption or small business rollover.

None of these rules apply if the 15‑year exemption already applies to the capital gain, since such a gain is disregarded anyway.

84 Section 152‑300

Omit “The concession in section 152‑205 (small business 50% reduction) applies”, substitute “You may choose not to apply the concession in section 152‑205 (small business 50% reduction)”.

85 Section 152‑400

Omit “The concession in section 152‑205 (small business 50% reduction) applies”, substitute “You may choose not to apply the concession in section 152‑205 (small business 50% reduction)”.

86 Section 204‑45 (heading)

Repeal the heading, substitute:

87 Section 204‑45

After “paragraph 204‑30(3)(c)”, insert “(about distributions to favoured members)”.

88 Paragraph 205‑70(1)(c)

Omit “that offset exceeded the amount that would have been its income tax liability for that year if it did not have that offset (but had all its other tax offsets)”, substitute “some of the offset remained after applying section 63‑10 (tax offset priority rules)”.

89 Subsection 205‑70(2) (method statement, step 4)

Repeal the step, substitute:

Step 4. Work out the remaining amount of a *tax offset covered by paragraph (1)(c).

90 At the end of subsection 205‑70(2) (after the note)

Add:

Example: The following apply to a corporate tax entity that satisfies the residency requirement for an income year:

Under section 63‑10 (about tax offset priority rules), the foreign tax credit must be applied before the franking deficit offset is applied. As a result, that credit and $20,000 of the franking deficit offset combine to reduce the entity’s income tax liability to nil. The remaining $40,000 of the franking deficit offset will be included in a franking deficit offset for the next income year for which the entity satisfies the residency requirement.

91 Subsection 205‑70(3)

Repeal the subsection (including the note and the example).

92 Application

The amendments made by items 86 to 91 apply to assessments for the 2006‑07 income year and later income years.

93 Subsection 214‑25(2)

Repeal the subsection, substitute:

(2) The return must be in the *approved form.

94 Subsection 320‑134(3) (note)

Omit “assumptions mentioned in section 67‑30 (about getting a refund of a tax offset)”, substitute “tax offset priority rules in Division 63”.

95 Subsection 701‑55(5)

Omit “Part 3.1 or 3.3”, substitute “Part 3‑1 or 3‑3”.

96 Subparagraphs 701‑70(3)(a)(i) and (ii)

Omit “or”.

97 Subparagraph 701‑75(3)(a)(i)

Omit “or”.

98 Paragraphs 715‑270(5)(c), (d) and (e)

Reletter as paragraphs 715‑270(5)(a), (b) and (c).

99 Subsection 723‑110(3)

Renumber as subsection 723‑110(2).

100 Subparagraph 727‑465(b)(ii)

Omit “gaining entity.”, substitute “gaining entity;”.

101 Subsection 820‑120(4) (table items 3 and 4)

Renumber as table items 2 and 3.

102 Subsection 820‑225(3) (table items 3 and 4)

Renumber as table items 2 and 3.

103 Paragraph 900‑30(7)(b)

Omit “Income Tax Assessment Act 1997”, substitute “Income Tax Assessment Act 1936”.

104 At the end of Subdivision 960‑E

Add:

(1) This Act applies to an entity as if the entity were an agent of another entity (the principal) if:

(a) the principal is outside Australia; and

(b) the entity is in Australia and, on behalf of the principal, holds money of the principal or has control, receipt or disposal of money of the principal.

(2) This Act, or a provision of this Act, applies to an entity as if the entity were an agent of another entity if the Commissioner determines in writing that the entity is the agent or sole agent of the other entity for the purposes of this Act or of that provision.

(3) A determination under subsection (2) is not a legislative instrument.

105 At the end of Division 960

Add:

The expression “market value” is often used in this Act with its ordinary meaning.

However, in some cases that expression has a meaning affected by this Subdivision.

Table of sections

Operative provisions

960‑405 Effect of GST on market value of an asset

960‑410 Market value of non‑cash benefits

(1) The market value of an asset at a particular time is reduced by the amount of the *input tax credit (if any) to which you would be entitled assuming that:

(a) you had *acquired the asset at that time; and

(b) the acquisition had been solely for a *creditable purpose.

(2) Subsection (1) does not apply:

(a) to an asset the *supply of which cannot be a *taxable supply; or

(b) in working out the *market value of economic benefits, or of *equity or loan interests, for the purposes of Part 3‑95 (about value shifting).

Note: Some assets, such as shares, cannot be the subject of a taxable supply.

In working out the market value of a *non‑cash benefit, disregard anything that would prevent or restrict conversion of the benefit to money.

106 Subsection 995‑1(1) (paragraph (a) of the definition of adopted child)

Omit “the law of a State or Territory”, substitute “a *State law or *Territory law”.

107 Subsection 995‑1(1) (paragraph (b) of the definition of adopted child)

Omit “the law of a State or Territory”, substitute “a State law or Territory law”.

108 Subsection 995‑1(1) (definition of agent)

Repeal the subsection, substitute:

agent: this Act applies to some entities that are not agents in the same way as it applies to agents: see section 960‑105.

109 Subsection 995‑1(1) (definition of dividend)

Omit “subsections 6(1), (4) and (5)”, substitute “subsections 6(1) and (4)”.

110 Subsection 995‑1(1) (paragraph (a) of the definition of firearms surrender arrangements)

Repeal the paragraph, substitute:

(a) an *Australian law; or

111 Subsection 995‑1(1) (definition of foreign superannuation fund) (the definition of foreign superannuation fund inserted by item 18 of Schedule 10 to the Taxation Laws Amendment Act (No. 1) 1998)

Repeal the definition.

112 Subsection 995‑1(1) (definition of market value)

Repeal the definition, substitute:

market value has a meaning affected by Subdivision 960‑S.

113 Subsection 995‑1(1) (definition of non‑equity share)

Repeal the definition, substitute:

non‑equity share means a *share that is not an *equity interest in the company.

Note: A share will not be an equity interest if it is characterised as, or forms part of a larger interest that is characterised as, a debt interest under Subdivision 974‑B.

114 Paragraph 14(2)(c)

Omit “$630”, substitute “$594”.

115 Application

The amendment made by item 114 applies to assessments for the 2005‑06 income year and later income years.

116 Paragraph 1(b) of Part I of Schedule 7

Repeal the paragraph, substitute:

(b) for each part of the ordinary taxable income specified in the table—the rate applicable under the table.

117 Paragraph 1(b) of Part II of Schedule 7

Repeal the paragraph, substitute:

(b) for each part of the ordinary taxable income specified in the table—the rate applicable under the table.

118 Paragraph 2(b) of Part I of Schedule 10

Omit “column 1”, substitute “item 1”.

119 Application

The amendment made by item 118 applies to assessments for the 2003‑04 income year and later income years.

120 After section 40‑12

Insert:

(1) This section applies to a depreciating asset that is plant if:

(a) you entered into a contract to acquire the plant, you otherwise acquired it or you started to construct it before 11.45 am, by legal time in the Australian Capital Territory, on 21 September 1999; and

(b) you held it at the end of 30 June 2001; and

(c) on or after 1 July 2001:

(i) the plant is split into 2 or more depreciating assets; or

(ii) the plant is merged into another depreciating asset.

(2) For a case where the plant is split into 2 or more depreciating assets, the new Act applies as if you had acquired the assets into which it is split before the time mentioned in paragraph (1)(a) while you continue to hold those assets.

(3) For a case where the plant is merged into another depreciating asset, section 40‑125 of the new Act does not apply to the asset, or to your interest in the asset, into which it is merged while you continue to hold it.

121 Paragraphs 40‑75(1)(b) and (c)

Reletter as paragraphs 40‑75(1)(a) and (b).

122 Section 40‑95

Repeal the section.

123 Part 3‑35

Relocate to after Part 3‑6.

124 At the end of Subdivision 960‑E

Add:

A declaration made by the Commissioner for the purposes of paragraph (b) of the definition of agent in subsection 995‑1(1) of the Income Tax Assessment Act 1997 and in force immediately before the Tax Laws Amendment (2006 Measures No. 2) Act 2006 received the Royal Assent continues to have effect for the purposes of section 960‑105 of the Income Tax Assessment Act 1997.

125 Subsection 2(1)

Omit “(1)”.

126 Subsection 2(2)

Repeal the subsection.

127 Items 1 to 6, 9 and 10 of Schedule 2

Repeal the items.

128 Subitem 12(1) of Schedule 2

Repeal the subitem.

129 Subsection 31(1)

Omit “(1)”.

130 Subsection 31(1)

Omit “section 46”, substitute “this Act”.

131 Subsection 8AAB(5) (table item 17A)

Repeal the item.

132 After subsection 14ZW(1BA)

Insert:

(1BB) If:

(a) the taxation objection is against an assessment by the Commissioner of the amount of an administrative penalty under Division 284; and

(b) that penalty relates to an assessment of the person; and

(c) the person has longer than 60 days to lodge a taxation objection against the assessment referred to in paragraph (b);

the person must lodge the taxation objection within that longer period.

133 Application

The amendment made by item 132 applies to assessments of the amounts of administrative penalties made by the Commissioner after the day on which this Act receives the Royal Assent.

134 Section 18

Omit all the words after “in particular”, substitute “, prescribing penalties not exceeding a fine of 5 penalty units for offences against the regulations.”.

135 Section 16‑30 in Schedule 1

Repeal the section, substitute:

An entity (except an *exempt Australian government agency) that:

(a) fails to withhold an amount as required by Division 12; or

(b) fails to pay an amount to the Commissioner as required by Division 13 or 14;

is liable to pay to the Commissioner a penalty equal to that amount.

Note 1: An entity may become liable under this section in respect of a payment it made or received that is taken to have been subject to withholding tax as a result of a Commissioner’s determination under subsection 177F(2A) of the Income Tax Assessment Act 1936 (see also subsection 177F(2F) of that Act).

Note 2: Division 298 in this Schedule contains machinery provisions for administrative penalties.

136 Sections 16‑40 and 16‑43 in Schedule 1

Repeal the sections, substitute:

An *exempt Australian government agency that:

(a) fails to withhold an amount as required by Division 12 from a *withholding payment covered by Subdivision 12‑F (about dividend, interest or royalty payment); or

(b) fails to pay to the Commissioner an amount as required by Division 14 in respect of a withholding payment covered by that Subdivision;

is liable to pay to the Commissioner a penalty equal to that amount.

Note 1: An exempt Australian government agency may become liable under this section in respect of a payment it made or received that is taken to have been subject to withholding tax as a result of a Commissioner’s determination under subsection 177F(2A) of the Income Tax Assessment Act 1936 (see also subsection 177F(2F) of that Act).

Note 2: Division 298 in this Schedule contains machinery provisions for administrative penalties.

An *exempt Australian government agency that:

(a) fails to withhold an amount as required by Division 12 from a *withholding payment covered by Subdivision 12‑FB (about payments to foreign residents); or

(b) fails to pay to the Commissioner an amount as required by Division 14 in respect of a withholding payment covered by that Subdivision;

is liable to pay to the Commissioner a penalty equal to that amount.

Note: Division 298 in this Schedule contains machinery provisions for administrative penalties.

137 Sections 16‑45 and 16‑50 in Schedule 1

Repeal the sections.

138 Application

The amendments made by items 135 to 137 apply to administrative penalties imposed after the day on which this Act receives the Royal Assent.

139 Transitional

(1) If, under section 16‑45 in Schedule 1 to the Taxation Administration Act 1953 as in force immediately before the commencement of this item, the Commissioner has refused to any extent to remit to an entity an amount of penalty, the entity may, in the manner set out in Part IVC of that Act, object against the decision.

(2) The objection must be made before the end of 60 days after the day on which this Act receives the Royal Assent (the assent day).

(3) An objection that was purported to have been made against such a refusal before the assent day has effect as if it had been made under this item on the assent day.

140 Section 18‑5 in Schedule 1

Omit “A person”, substitute “An entity”.

141 Subsection 18‑15(1) in Schedule 1

Omit “A person”, substitute “An entity”.

142 Subsection 18‑15(1) in Schedule 1

Omit “the person” (wherever occurring), substitute “the entity”.

143 Subsection 18‑20(1) in Schedule 1

Omit “A person”, substitute “An entity”.

144 Subsection 18‑20(1) in Schedule 1

Omit “the person” (wherever occurring), substitute “the entity”.

145 Subsection 18‑25(1) in Schedule 1

Omit “A person”, substitute “An entity”.

146 Section 18‑27 in Schedule 1

Omit “A person”, substitute “An entity”.

147 Section 18‑27 in Schedule 1

Omit “the person’s”, substitute “the entity’s”.

148 Section 18‑27 in Schedule 1

Omit “the person”, substitute “the entity”.

149 Subsection 18‑30(1) in Schedule 1

Omit “A person”, substitute “An entity”.

150 Paragraph 18‑30(1)(a) in Schedule 1

Omit “the person’s”, substitute “the entity’s”.

151 Paragraph 18‑30(1)(b) in Schedule 1

Omit “the person”, substitute “the entity”.

152 Paragraph 18‑35(1)(b) in Schedule 1

Omit “section 16‑50”, substitute “section 298‑25”.

153 Subsection 18‑35(1) in Schedule 1

Omit “the person”, substitute “the entity”.

154 Paragraph 18‑35(2)(b) in Schedule 1

Omit “section 16‑45”, substitute “section 298‑20”.

155 Subsection 18‑40(1) in Schedule 1

Omit “the person”, substitute “the entity”.

156 Subsections 18‑42(1) and (2) in Schedule 1

Omit “the person”, substitute “the entity”.

157 Subsection 18‑42(3) in Schedule 1

Omit “section 16‑45”, substitute “section 298‑20”.

158 Paragraph 18‑45(1)(a) in Schedule 1

Omit “the person”, substitute “the entity”.

159 Paragraph 18‑45(1)(b) in Schedule 1

Omit “persons” (wherever occurring), substitute “entities”.

160 Paragraph 18‑45(2)(a) in Schedule 1

Omit “the person”, substitute “the entity”.

161 Paragraph 18‑45(2)(b) in Schedule 1

Omit “persons” (wherever occurring), substitute “entities”.

162 Subsection 18‑45(3) in Schedule 1

Omit “section 16‑45”, substitute “section 298‑20”.

163 Subparagraph 18‑75(1)(a)(ii) in Schedule 1

Omit “a person or persons”, substitute “an entity or entities”.

164 Subsection 250‑10(2) in Schedule 1 (table item 5)

Before “33‑5”, insert “33‑3,”.

165 Application

The amendment made by item 164 applies to GST returns, and net amounts, for tax periods ending on or after 22 February 2001.

166 Subsection 250‑10(2) in Schedule 1 (table item 100)

Repeal the item.

167 Paragraph 284‑225(3)(a) in Schedule 1

Omit “or the part of, it”, substitute “or the part of it,”.

168 At the end of section 298‑5 in Schedule 1

Add:

; or (c) an administrative penalty is imposed on an entity by a provision of Division 16 in this Schedule.

169 Subsection 340‑5(3) in Schedule 1

Repeal the subsection, substitute:

(3) The Commissioner may release you, in whole or in part, from the liability if you are an entity specified in the column headed “Entity” of the following table and the condition specified in the column headed “Condition” of the table is satisfied.

Entity and condition | ||

Item | Entity | Condition |

1 | an individual | you would suffer serious hardship if you were required to satisfy the liability |

2 | a trustee of the estate of a deceased individual | the dependants of the deceased individual would suffer serious hardship if you were required to satisfy the liability |

170 Items 14 to 17 of Schedule 6

Repeal the items.

171 Item 20 of Schedule 10

Repeal the item, substitute:

20 Subsection 159J(6) (paragraph (aad) of the definition of separate net income)

Repeal the paragraph, substitute:

(aad) does not include any part of benefit PP (partnered) paid under the Social Security Act 1991, as in force immediately before the commencement of item 1 of Schedule 10 to the A New Tax System (Family Assistance) (Consequential and Related Measures) Act (No. 2) 1999, that is exempt under section 52‑10 because of paragraph (e) of the item dealing with parenting payment (benefit PP (partnered)) in the table in section 52‑15 of the Income Tax Assessment Act 1997; and

172 Section 110‑5 (definition of untaxable Commonwealth entity)

Omit “to Commonwealth entity”.

173 Paragraphs 70B(2A)(b) and (c)

Repeal the paragraphs, substitute:

(b) segregated current pension assets (as defined in Part IX) of a complying superannuation fund (as defined in that Part).

174 Subsection 73BAG(1)

Omit “Subsections 73(23) and (24B)”, substitute “Subsections 73B(23) and (24B)”.

175 Paragraphs 92(2A)(b) and (c)

Repeal the paragraphs, substitute:

(b) a segregated current pension asset (as defined in Part IX) of a complying superannuation fund (as defined in that Part).

176 Section 94D (all the subsections after subsection 94D(3))

Repeal the subsections, substitute:

(4) The place of residence of a VCMP is the place at which the partnership has its central management and control.

(5) A limited partnership that is a foreign hybrid limited partnership in relation to a year of income because of subsection 830‑10(1) of the Income Tax Assessment Act 1997 is not a corporate limited partnership in relation to the year of income.

Note: As result, both the normal partnership provisions and special provisions relating to foreign hybrid limited partnerships will apply to the entity.

(6) If, for the purpose of applying this Act and the Income Tax Assessment Act 1997 in relation to a partner’s interest in a limited partnership, the partnership is a foreign hybrid limited partnership in relation to a year of income because of subsection 830‑10(2) of that Act, the partnership is not a corporate limited partnership in relation to the partner’s interest in relation to the year of income.

Note: As result, both the normal partnership provisions and special provisions relating to foreign hybrid limited partnerships will apply to the entity, but only in relation to the partner’s interest.

177 Section 94F

Omit “paragraph 94D(d)”, substitute “paragraph 94D(1)(d)”.

178 Paragraph 485AA(1)(a)

Omit “subsection 94D(5)”, substitute “subsection 94D(6)”.

179 Subparagraph 30‑125(1)(c)(i)

Omit “subsections (4) and (5)”, substitute “section 30‑130”.

180 Subparagraph 30‑125(1)(c)(ii)

Omit “subsections (4), (5) and (6)”, substitute “subsection (6) of this section and section 30‑130”.

181 Subparagraph 30‑125(2)(d)(i)

Omit “subsections (4) and (5)”, substitute “section 30‑130”.

182 Subparagraph 30‑125(2)(d)(ii)

Omit “subsections (4), (5) and (6)”, substitute “subsection (6) of this section and section 30‑130”.

183 Subsections 30‑125(4), (4A) and (5)

Repeal the subsections.

184 Subsection 30‑125(6)

After “gift fund”, insert “(see section 30‑130)”.

185 After section 30‑125

Insert:

(1) The entity must maintain for the principal purpose of the fund, authority or institution a fund (the gift fund):

(a) to which gifts of money or property for that purpose are to be made; and

(b) to which contributions described in item 7 or 8 of the table in section 30‑15 in relation to a *fund‑raising event held for that purpose are to be made; and

(c) to which any money received by the entity because of such gifts or contributions is to be credited; and

(d) that does not receive any other money or property.

(2) The entity must use the gift fund only for the principal purpose of the fund, authority or institution.

186 Subsections 30‑265(2) and (3)

Repeal the subsections, substitute:

(2) It must maintain a public fund that meets the requirements of section 30‑130, or would meet those requirements if the *environmental organisation were a fund, authority or institution.

187 Subsections 30‑289(2) and (3)

Repeal the subsections, substitute:

(2) It must maintain a public fund that meets the requirements of section 30‑130.

188 Subsections 30‑300(3) and (4)

Repeal the subsections, substitute:

(3) It must maintain a public fund that meets the requirements of section 30‑130, or would meet those requirements if the *cultural organisation were a fund, authority or institution.

189 Paragraphs 51‑35(c) and (d)

Repeal the paragraphs, substitute:

(c) a payment by an entity or authority on the condition that the student will (or will if required) become, or continue to be, an employee of the entity or authority;

(d) a payment by an entity or authority on the condition that the student will (or will if required) enter into, or continue to be a party to, a contract with the entity or authority that is wholly or principally for the labour of the student;

190 Section 118‑355

Repeal the section.

191 Subsection 701‑10(6)

Omit “*tax cost is set by this subsection”, substitute “*tax cost is set by this section”.

192 Paragraph 830‑10(1)(d)

Omit “subsection 94D(4)”, substitute “subsection 94D(5)”.

193 Subsection 995‑1(1) (definition of small withholder)

After “section 16‑105”, insert “in Schedule 1 to the Taxation Administration Act 1953”.

194 Subsection 3(1) (at the end of paragraphs (a), (b) and (c) of the definition of decision to which this Act applies)

Add “or”.

195 Subsection 3(1) (paragraph (ca) of the definition of decision to which this Act applies)

Repeal the paragraph, substitute:

(ca) in a case where the expression is used in relation to relevant tax of a kind referred to in items 5 to 50 of the table in section 3C—a decision of the Commissioner to amend an assessment made in relation to a taxpayer reducing the liability of the taxpayer to tax; or

196 Subsection 3(1) (at the end of paragraph (cb) of the definition of decision to which this Act applies)

Add “or”.

197 Subsection 3(1) (paragraph (d) of the definition of decision to which this Act applies)

Omit “paragraph (ka) or (na) of the definition of relevant tax”, substitute “item 120 of the table in section 3C”.

198 Subsection 3(1) (paragraph (e) of the definition of decision to which this Act applies)

Omit “paragraph (n) of the definition of relevant tax”, substitute “item 135 of the table in section 3C”.

199 Subsection 3(1) (at the end of paragraphs (a) and (b) of the definition of person)

Add “and”.

200 Subsection 3(1) (definition of relevant tax)

Repeal the definition, substitute:

relevant tax has the meaning given by section 3C.

201 At the end of Part I

Add:

In this Act:

relevant tax means any of these:

Relevant taxes | |

Item | Type of tax |

5 | Tax as defined in subsection 6(1) of the Tax Act |

10 | Additional tax under Part VII of the Tax Act |

15 | General interest charge under section 170AA of the Tax Act |

20 | Shortfall interest charge under Division 280 in Schedule 1 to the Taxation Administration Act 1953 |

25 | Interest under section 102AAM of the Tax Act |

30 | Provisional and additional tax under section 221YDB of the Tax Act |

35 | Instalments under section 221AZK of the Tax Act |

40 | Amounts that are treated under subsection 106U(1) of the Higher Education Funding Act 1988 as if they were income tax |

45 | Amounts that are treated under Subdivision 154‑D of the Higher Education Support Act 2003 as if they were income tax |

50 | Amounts that are treated under subsection 12ZN(1) of the Student and Youth Assistance Act 1973 as if they were income tax |

55 | Withholding tax as defined in subsection 6(1) of the Tax Act |

60 | An amount payable to the Commissioner under subsection 220AS(1) of the Tax Act |

65 | An amount payable to the Commissioner under subsection 221EAA(1) of the Tax Act |

70 | An amount payable to the Commissioner under subsection 221YHH(1) of the Tax Act |

75 | An amount payable to the Commissioner under subsection 221YHZC(3) or 221YHZD(2) of the Tax Act |

80 | An amount payable to the Commissioner under section 16‑80 in Schedule 1 to the Taxation Administration Act 1953 |

85 | An amount payable to the Commissioner under subsection 222AJA(3) of the Tax Act |

90 | An amount payable to the Commissioner under Subdivision 16‑A (other than section 16‑50) in Schedule 1 to the Taxation Administration Act 1953 |

95 | Trust recoupment tax, applied penalty tax or penalty tax, as defined in subsection 3(1) of the Trust Recoupment Tax Assessment Act 1985 |

100 | Duty or tax within the meaning of subsection 81(1) of the Australian Capital Territory Taxation (Administration) Act 1969 |

105 | Tax within the meaning of subsection 36(1) of the Debits Tax Administration Act 1982 |

110 | Tax, or additional tax, referred to in subsection 93(1) of the Fringe Benefits Tax Assessment Act 1986 |

115 | Tax within the meaning of subsection 27(1) of the Pay‑roll Tax (Territories) Assessment Act 1971 |

120 | Tax within the meaning of subsection 85(1) of the Petroleum Resource Rent Tax Assessment Act 1987 |

125 | Tax within the meaning of subsection 29(1) of the Sales Tax Assessment Act (No. 1) 1930 (including that subsection as applied by any other Act providing for the assessment of sales tax) |

130 | Tax within the meaning of section 68 of the Sales Tax Assessment Act 1992 |

135 | Charge within the meaning of subsection 18(1) of the Tobacco Charges Assessment Act 1955 |

140 | Tax within the meaning of subsection 38(1) of the Wool Tax (Administration) Act 1964 |

145 | Indirect tax within the meaning of subsection 995‑1(1) of the Income Tax Assessment Act 1997 |

150 | A penalty or charge payable under Subdivision 105‑D in Schedule 1 to the Taxation Administration Act 1953 |

155 | GST assessed under the A New Tax System (Goods and Services Tax) Act 1999 |

202 Sub‑subparagraph 10(1)(a)(iii)(A)

Omit “paragraph (a), (b), (c), (d), (e) or (g) of the definition of relevant tax in subsection 3(1)”, substitute “items 5 to 85, or 105, of the table in section 3C”.

203 Sub‑subparagraph 10(1)(a)(iii)(AA)

Omit “paragraph (a) of the definition of relevant tax in subsection 3(1)”, substitute “items 5 to 50 of the table in section 3C”.

204 Sub‑subparagraph 10(1)(a)(iii)(B)

Omit “paragraph (ba) of the definition of relevant tax in subsection 3(1)”, substitute “item 65 of the table in section 3C”.

205 Sub‑subparagraph 10(1)(a)(iii)(C)

Omit “paragraph (bb) of the definition of relevant tax in subsection 3(1)”, substitute “item 70 of the table in section 3C”.

206 Paragraph 10(1)(aa)

Omit “paragraph (a) of the definition of relevant tax in subsection 3(1)”, substitute “items 5 to 50 of the table in section 3C”.

207 Section 10A

Omit “paragraph (f) or (m) of the definition of relevant tax in subsection 3(1)”, substitute “item 100 or 125 of the table in section 3C”.

208 Subparagraph 12(1)(a)(i)

Omit “paragraph (a) of the definition of relevant tax in subsection 3(1)”, substitute “items 5 to 50 of the table in section 3C”.

209 Subparagraph 12(1)(a)(ii)

Omit “paragraph (f), (k), (m), (n) or (p) of the definition of relevant tax in subsection 3(1)”, substitute “item 100, 115, 125, 135 or 140 of the table in section 3C”.

210 Items 31 and 40 of Schedule 10

Repeal the items.

211 Item 41 of Schedule 10 (link note)

Repeal the link note.

212 Section 2 (table item 19)

Repeal the item, substitute:

19. Schedule 8, item 4 | Immediately after the commencement of Schedule 10 to the Tax Laws Amendment (2004 Measures No. 1) Act 2004. | 1 July 2005 |

213 Asterisking of “partnership”

The provisions of the Income Tax Assessment Act 1997 listed in the table are amended as set out in the table.

Asterisking amendments | |||

Item | Provision | Omit: | Substitute: |

1 | Subsection 165‑115Y(7) | *partnership | partnership |

2 | Paragraph 205‑15(2)(a) | *partnership | partnership |

3 | Subsection 208‑40(3) | *partnership | partnership |

4 | Paragraph 208‑45(1)(a) | *partnership | partnership |

5 | Subsection 208‑45(8) | *partnership | partnership |

6 | Paragraph 208‑155(3)(f) | *partnership | partnership |

7 | Paragraph 208‑155(4)(b) | *partnership | partnership |

8 | Paragraph 208‑155(5)(d) | *partnership | partnership |

9 | Paragraph 208‑155(6)(b) | *partnerships | partnerships |

10 | Subsection 208‑155(7) | *partnership | partnership |

11 | Subparagraph 210‑170(1)(b)(i) | *partnership | partnership |

12 | Subsection 219‑15(2) (table item 6) | *partnership | partnership |

13 | Paragraph 219‑15(3)(a) | *partnership | partnership |

14 | Paragraph 768‑550(2)(b) | *partnership | partnership |

214 Asterisking of “derived”

The provisions of the Income Tax Assessment Act 1997 listed in the table are amended as set out in the table.

Asterisking amendments | |||

Item | Provision | Omit: | Substitute: |

1 | Paragraph 26‑80(3)(aa) | derived | *derived |

2 | Paragraph 35‑25(b) | derived | *derived |

3 | Paragraph 40‑335(2)(b) | derive | *derive |

4 | Subsection 40‑460(1) | derive | *derive |

5 | Subsection 40‑830(6) | derive | *derive |

6 | Section 50‑45 (table item 9.4) | derived | *derived |

7 | Paragraph 50‑80(1)(c) | derived | *derived |

8 | Subsection 58‑10(3) | derive | *derive |

9 | Paragraph 110‑55(7)(b) | derived | *derived |

10 | Paragraph 115‑290(4)(c) | derive | *derive |

11 | Paragraph 152‑40(4)(e) | derive | *derive |

12 | Subsection 165‑115B(6) | derived | *derived |

13 | Paragraph 202‑45(b) | derived | *derived |

14 | Paragraph 204‑1(c) | derive | *derive |

15 | Paragraph 204‑30(1)(b) | derive | *derive |

16 | Subsections 204‑30(7), (8), (9) and (10) | derives | *derives |

17 | Paragraph 204‑80(1)(d) | derived | *derived |

18 | Paragraph 207‑55(1)(a) | derive | *derive |

19 | Paragraph 207‑120(2)(b) | derived | *derived |

20 | Paragraph 207‑128(1)(d) | derived | *derived |

21 | Paragraphs 208‑155(6)(b) and (7)(b) | derives | *derives |

22 | Paragraph 220‑205(1)(a) | derived | *derived |

23 | Subsection 320‑5(1) | derive | *derive |

24 | Section 320‑35 | derived | *derived |

25 | Subsection 320‑37(1) | derived (first occurring) | *derived |

26 | Subsection 320‑37(1A) | derived | *derived |

27 | Paragraph 320‑137(2)(a) | derived | *derived |

28 | Paragraphs 320‑141(1)(c) and (2)(a) | derived | *derived |

29 | Paragraphs 320‑143(1)(c) and (2)(a) | derived | *derived |

30 | Paragraph 320‑246(5)(a) | derived | *derived |

31 | Subsection 375‑872(1) | derived | *derived |

32 | Subsection 396‑15(3) (definition of LTF interest covered by agreement) | derived | *derived |

33 | Subsection 396‑25(2) (definition of tax offset entitlement) | derived | *derived |

34 | Subsection 396‑35(1) | derived | *derived |

35 | Paragraph 701‑70(1)(b) | deriving | *deriving |

36 | Subsection 701‑70(5) | derived | *derived |

37 | Subsection 701‑70(6) (definition of total arrangement assessable income) | derived | *derived |

38 | Paragraph 701‑70(7)(b) | derived | *derived |

39 | Paragraph 701‑75(1)(b) | deriving | *deriving |

40 | Subsection 701‑75(5) | derived | *derived |

41 | Subsection 701‑75(6) (definition of total arrangement assessable income) | derived | *derived |

42 | Paragraph 713‑560(5)(b) | derived | *derived |

43 | Subsection 716‑850(1) | derived | *derived |

44 | Paragraph 768‑545(3)(c) | derived | *derived |

45 | Subsection 775‑45(7) (table item 1) | derived | *derived |

46 | Subsection 960‑50(6) (table item 6) | derived (first occurring) | *derived |

47 | Subsection 995‑1(1) (definition of non‑copyright income) | derived | *derived |

215 Asterisking of “market value”

The provisions of the Income Tax Assessment Act 1997 listed in the table are amended as set out in the table.

Asterisking amendments | |||

Item | Provision | Omit: | Substitute: |

1 | Subsection 30‑15(2) (table items 1 and 2, column headed “How much you can deduct”) | market value (first occurring) | *market value |

2 | Subsection 30‑15(2) (table item 7, column headed “Type of gift or contribution”) | market value | *market value |

3 | Subsection 30‑215(3) (table item 4) | market value (first occurring) | *market value |

4 | Subsections 35‑40(2) and (3) | market value | *market value |

5 | Section 35‑50 | market value | *market value |

6 | Subsection 40‑350(2) | market value | *market value |

7 | Subparagraph 45‑5(1)(e)(iii) | market value | *market value |

8 | Paragraph 45‑5(4)(c) | market value | *market value |

9 | Subparagraph 45‑10(1)(f)(iii) | market value | *market value |

10 | Paragraph 45‑10(4)(c) | market value | *market value |

11 | Subsection 45‑15(1) | market value (first occurring) | *market value |

12 | Subsection 45‑20(1) | market value (first occurring) | *market value |

13 | Section 51‑5 (table item 1.1) | market value | *market value |

14 | Subsection 70‑70(2) | market value (first occurring) | *market value |

15 | Subsection 70‑90(1A) | market value | *market value |

16 | Paragraph 70‑120(2)(c) | market value | *market value |

17 | Paragraph 86‑75(2)(a) | market value | *market value |

18 | Paragraphs 87‑25(1)(b) and (2)(b) | market value | *market value |

19 | Subsection 104‑190(5) | market values | *market values |

20 | Paragraph 104‑220(1)(b) | market value | *market value |

21 | Subsection 104‑225(6) | *market value | market value |

22 | Subsection104‑225(6) | market value (first occurring) | *market value |

23 | Subsection 104‑230(6) | market value | *market value |

24 | Subparagraph 104‑530(3)(b)(ii) | market value | *market value |

25 | Paragraph 110‑25(2)(b) | market value | *market value |

26 | Subsection 112‑20(2) | market value (first occurring) | *market value |

27 | Paragraphs 115‑45(6)(b) and (7)(b) | market value | *market value |

28 | Subparagraph 115‑290(4)(c)(i) | market value | *market value |

29 | Subsection 116‑20(2) (table item F2) | market value (first occurring) | *market value |

30 | Subsection 116‑80(2) | market value (first occurring) | *market value |

31 | Subsections 118‑60(3) and (4) | market value | *market value |

32 | Subsection 118‑192(2) | market value | *market value |

33 | Subsection 122‑20(3) | market value (first occurring) | *market value |

34 | Paragraph 122‑20(3)(a) | *market value | market value |

35 | Subsection 122‑20(4) | market value | *market value |

36 | Subsection 122‑130(3) | market value (first occurring) | *market value |

37 | Paragraph 122‑130(3)(a) | *market value | market value |

38 | Subsection 122‑130(4) | market value | *market value |

39 | Subsection 122‑140(2) (table item 3) | market values (first occurring) | *market values |

40 | Paragraph 124‑240(d) | market value (first occurring) | *market value |

41 | Paragraph 124‑245(d) | market value (first occurring) | *market value |

42 | Subsection 124‑295(6) | market value (first occurring) | *market value |

43 | Subsection 124‑300(6) | market value (first occurring) | *market value |

44 | Subsection 124‑365(3) | market value (first occurring) | *market value |

45 | Subsection 124‑375(3) | market value (first occurring) | *market value |

46 | Paragraph 124‑380(3)(b) | market value (first occurring) | *market value |

47 | Subsection 124‑450(3) | market value (first occurring) | *market value |

48 | Subsection 124‑460(3) | market value (first occurring) | *market value |

49 | Paragraph 124‑465(3)(b) | market value (first occurring) | *market value |

50 | Paragraph 124‑780(5)(a) | market value (first occurring) | *market value |

51 | Paragraph 124‑781(4)(a) | market value (first occurring) | *market value |

52 | Paragraph 124‑782(3)(b) | market values | *market values |

53 | Subsection 124‑782(4) | market value | *market value |

54 | Paragraph 124‑784(2)(b) | market value | *market value |

55 | Subsection 124‑784(3) | market value | *market value |

56 | Subsection 124‑800(1) | market value | *market value |

57 | Paragraph 124‑860(7)(b) | market value | *market value |

58 | Subsection 128‑15(4) (table item 3) | market value (first occurring) | *market value |

59 | Subsection 128‑15(4) (table item 4) | *market value (last occurring) | market value |

60 | Subsection 130‑20(3) (table item 2) | market value | *market value |

61 | Subsections 130‑80(2) and (3) | market value | *market value |

62 | Subsection 152‑20(1) | market values | *market values |

63 | Subparagraph 152‑40(3)(b)(i) | market values | *market values |

64 | Subparagraph 152‑40(4)(e)(i) | market value | *market value |

65 | Subsection 152‑310(3) | market value | *market value |

66 | Subsection 152‑325(4) | market value | *market value |

67 | Subsections 164‑15(1), (2) and (4) (definition of amount received) | market value | *market value |

68 | Subparagraph 164‑20(1)(b)(i) | market value | *market value |

69 | Subsections 165‑115AA(2) and (3) | market value | *market value |

70 | Paragraph 165‑115A(1D)(b) | market value | *market value |

71 | Subsection 165‑115E(2) (method statement, step 1) | market value | *market value |

72 | Paragraph 165‑115E(3)(b) | market value | *market value |

73 | Subsection 165‑115F(2) | market value | *market value |

74 | Paragraph 165‑115F(4)(a) | market value | *market value |

75 | Subsections 165‑115GC(5), (6) and (7) | market value | *market value |

76 | Subsection 165‑115U(1B) (method statement, step 1) | market value | *market value |

77 | Paragraph 165‑115U(1C)(b) | market value | *market value |

78 | Subsections 165‑115V(3) and (6) | market value | *market value |

79 | Paragraph 165‑115V(7)(c) | market value | *market value |

80 | Subsection 165‑115W(1) (method statement, steps 1 and 2) | market value (first occurring) | *market value |

81 | Paragraphs 165‑115ZA(5)(b) and (9)(b) | market value | *market value |

82 | Paragraph 165‑115ZA(10)(d) | market value (first occurring) | *market value |

83 | Paragraph 165‑115ZB(6)(e) | market values | *market values |

84 | Subsection 165‑115ZB(7) | market value (first occurring) | *market value |

85 | Subsection 165‑115ZD(5) (table item 6) | market value (first occurring) | *market value |