Private Health Insurance Act 2007

No. 31, 2007

An Act to regulate private health insurance, and for related purposes

Private Health Insurance Act 2007

No. 31, 2007

An Act to regulate private health insurance, and for related purposes

Contents

Part 1‑1—Introduction

Division 1—Preliminary

1‑1.................................Short title

1‑5.............................Commencement

1‑10.......................Identifying defined terms

Division 3—Overview of this Act

3‑1..........................What this Act is about

3‑5...........................Incentives (Chapter 2)

3‑10..........Complying health insurance products (Chapter 3)

3‑15...................Private health insurers (Chapter 4)

3‑20.........................Enforcement (Chapter 5)

3‑25........................Administration (Chapter 6)

3‑30..........................Dictionary (Schedule 1)

Division 5—Constitutional matters

5‑1................................Meaning of insurance

5‑5........Act not to apply to State insurance within that State

5‑10..............Compensation for acquisition of property

Chapter 2—Incentives

Part 2‑1—Introduction

Division 15—Introduction

15‑1......................What this Chapter is about

Part 2‑2—Premiums reduction and incentive payments schemes

Division 20—Introduction

20‑1.........................What this Part is about

20‑5............Private Health Insurance (Incentives) Rules

Division 23—Premiums reduction scheme

Subdivision 23‑A—Amount of reduction

23‑1........................Reduction in premiums

23‑5...............................Meaning of incentive amount

23‑10Reduction after a person 65 years or over ceases to be covered by policy

Subdivision 23‑B—Participation in the premiums reduction scheme

23‑15 Registration as a participant in the premiums reduction scheme

23‑20...........................Refusal to register

23‑25....................................Pre‑1999 participants must keep information up to date

23‑30.........Participants who want to withdraw from scheme

23‑35......................Revocation of registration

23‑40.......................Variation of registration

23‑45.......Retention of applications by private health insurers

Division 26—The incentive payments scheme

Subdivision 26‑A—Amount of incentive payment

26‑1...................Payment in relation to premiums

26‑5Payment after a person 65 years or over ceases to be covered by policy

Subdivision 26‑B—Claiming payments under the incentive payments scheme

26‑10......Claim for payment under incentive payments scheme

26‑15.........................Withdrawal of claim

26‑20.........Determination of claim and payment of amount

26‑25...........Reconsideration of decision refusing a claim

26‑30.............Claimants to keep information up to date

Part 2‑3—Lifetime health cover

Division 31—Introduction

31‑1.........................What this Part is about

31‑5.....Private Health Insurance (Lifetime Health Cover) Rules

Division 34—General rules about lifetime health cover

34‑1Increased premiums for person who is late in taking out hospital cover

34‑5Increased premiums for person who ceases to have hospital cover after his or her lifetime health cover base day

34‑10...Increased premiums stop after 10 years’ continuous cover

34‑15..............................Meaning of hospital cover

34‑20..............................Meaning of permitted days without hospital cover

34‑25..............................Meaning of lifetime health cover base day

34‑30......................When a person is overseas

Division 37—Exceptions to the general rules about lifetime health cover

37‑1......................People born on or before 1 July 1934

37‑5..................People over 31 and overseas on 1 July 2000

37‑10.............................Hardship cases

37‑15............Increases cannot exceed 70% of base rates

37‑20..........................Joint hospital cover

Division 40—Administrative matters relating to lifetime health cover

40‑1..................Notification to insured people etc.

40‑5...Evidence of having had hospital cover, or of a person’s age

Chapter 3—Complying health insurance products

Part 3‑1—Introduction

Division 50—Introduction

50‑1......................What this Chapter is about

50‑5.....Private Health Insurance Rules relevant to this Chapter

Part 3‑2—Community rating

Division 55—Principle of community rating

55‑1.........................What this Part is about

55‑5....................Principle of community rating

55‑10............................Closed products

Part 3‑3—Requirements for complying health insurance products

Division 60—Introduction

60‑1.........................What this Part is about

Division 63—Basic rules about complying health insurance products

63‑1......Obligation to ensure products are complying products

63‑5...............................Meaning of complying health insurance product

63‑10..............................Meaning of complying health insurance policy

Division 66—Community rating requirements

66‑1...................Community rating requirements

66‑5.........................Premium requirement

66‑10..................Minister’s approval of premiums

66‑15...........Entitlement to benefits for general treatment

66‑20.Different amount of benefits depending on where people live

Division 69—Coverage requirements

69‑1........................Coverage requirements

69‑5...............................Meaning of cover

69‑10..............................Meaning of hospital‑substitute treatment

Division 72—Benefit requirements for policies that cover hospital treatment

72‑1..........................Benefit requirements

72‑5.......Rules requirement in relation to provision of benefits

72‑10..................Minimum benefits for prostheses

72‑15.................Ongoing listing fee for prostheses

72‑20.............................Other matters

Division 75—Waiting period requirements

75‑1.....................Waiting period requirements

75‑5...............................Meaning of waiting period

75‑10..............................Meaning of transfers

75‑15..............................Meaning of pre‑existing condition

Division 78—Portability requirements

78‑1........................Portability requirements

Division 81—Quality assurance requirements

81‑1...................Quality assurance requirements

Division 84—Enforcement of this Part

84‑1.......Offence: advertising, offering or insuring under non‑complying policies

84‑5Offence: directors and chief executive officers liable if systems not in place to prevent breaches

84‑10.....................Injunction in relation to non‑complying policies

84‑15...............Remedies for people affected by non‑complying policies

Part 3‑4—Obligations relating to complying health insurance products

Division 90—Introduction

90‑1.........................What this Part is about

Division 93—Giving information to consumers

93‑1.....Maintaining up to date standard information statements

93‑5...............................Meaning of standard information statement

93‑10........Making standard information statements available

93‑15...........Giving information to newly insured people

93‑20.................Keeping insured people up to date

93‑25.....Giving advance notice of detrimental changes to rules

93‑30.............Failure to give information to consumers

Division 96—Giving information to the Department, the Council and the Private Health Insurance Ombudsman

96‑1........Giving standard information statements on request

96‑5....Giving standard information statements for new products

96‑10.........Giving updated standard information statements

96‑15.............Giving additional information on request

96‑20Failure to give information to Department, Council or Private Health Insurance Ombudsman

96‑25Giving information required by the Private Health Insurance (Complying Product) Rules

Division 99—Transfer certificates

99‑1..........................Transfer certificates

Division 102—Private health insurers to offer cover for hospital treatment

102‑1..Private health insurers to offer cover for hospital treatment

Chapter 4—Private health insurers

Part 4‑1—Introduction

Division 110—Introduction

110‑1......................What this Chapter is about

Part 4‑2—Carrying on health insurance business

Division 115—Introduction

115‑1........................What this Part is about

115‑5The Private Health Insurance (Health Insurance Business) Rules

115‑10......Whether a business etc. is health insurance business

Division 118—Prohibition of carrying on health insurance business without registration

118‑1...Carrying on health insurance business without registration

118‑5...............................Injunctions

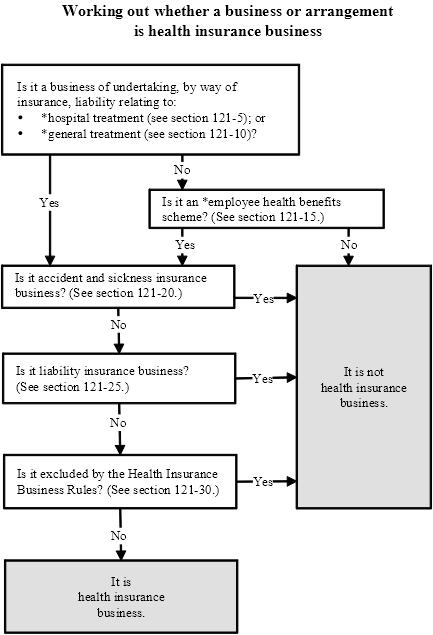

Division 121—What is health insurance business?

121‑1..............................Meaning of health insurance business

121‑5..............................Meaning of hospital treatment

121‑7..............Conditions on declarations of hospitals

121‑10.............................Meaning of general treatment

121‑15.............................Extension to employee health benefits schemes

121‑20......Exception: accident and sickness insurance business

121‑25..............Exception: liability insurance business

121‑30Exception: insurance business excluded by the Private Health Insurance (Health Insurance Business) Rules

Part 4‑3—Registration

Division 126—Registration

126‑1........................What this Part is about

126‑5........The Private Health Insurance (Registration) Rules

126‑10......................Applying for registration

126‑15..................Requesting further information

126‑20......................Deciding the application

126‑25.......................Notifying the decision

126‑30............Council can be taken to refuse application

126‑35.........Council to maintain record of registrations etc.

126‑40....................Changing registration status

126‑42...................Conversion to for profit status

126‑45....................Cancellation of registration

Part 4‑4—Health benefits funds

Division 131—Introduction

131‑1........................What this Part is about

131‑5..The Private Health Insurance (Health Benefits Fund) Rules

131‑10.............................Meaning of health benefits fund

131‑15.............................Meaning of health‑related business

Division 134—The requirement to have health benefits funds

134‑1.....Private health insurers must have health benefits funds

134‑5Notifying the Council when health benefits funds are established

134‑10..........................Inclusion of health‑related businesses in health benefits funds

Division 137—The operation of health benefits funds

137‑1...................Assets of health benefits funds

137‑5.................Payments to health benefits funds

137‑10.....Expenditure and application of health benefits funds

137‑15.............................Effect of non‑compliance with section 137‑10

137‑20................Investment of health benefits funds

137‑25Restriction on restructure, merger, acquisition or termination of health benefits funds

137‑30.........................Operation of health‑related businesses through health benefits funds

Division 140—The solvency standard for health benefits funds

140‑1..........................Purpose of Division

140‑5...............Council to establish solvency standard

140‑10...................Purpose of solvency standard

140‑15...............Compliance with solvency standard

140‑20.........................Solvency directions

Division 143—The capital adequacy standard for health benefits funds

143‑1..........................Purpose of Division

143‑5..........Council to establish capital adequacy standard

143‑10...............Purpose of capital adequacy standard

143‑15...........Compliance with capital adequacy standard

143‑20....................Capital adequacy directions

Division 146—Restructure, merger and acquisition of health benefits funds

146‑1................Restructure of health benefits funds

146‑5.........Merger and acquisition of health benefits funds

146‑10..............Consent of policy holders not required

146‑15.....................Other laws not overridden

Division 149—Termination of health benefits funds

Subdivision 149‑A—Approving the termination of health benefits funds

149‑1......................Applying for termination

149‑5...................Requesting further information

149‑10......................Deciding the application

149‑15............Council can be taken to refuse application

Subdivision 149‑B—Conducting the termination of health benefits funds

149‑20..........Conduct of funds during termination process

149‑25..............Insurers etc. to give reports to Council

149‑30.....Terminating managers displace management of funds

Subdivision 149‑C—Ending the termination of health benefits funds

149‑35......................Power to end termination

Subdivision 149‑D—Completing the termination of health benefits funds

149‑40..............Completion of the termination process

149‑45Distribution of remaining assets after completion of the termination process

149‑50..Liability of officers of insurers for loss to terminated funds

149‑55..................Report of terminating manager

149‑60......................Applying for winding up

Division 152—Duties and liabilities of directors etc.

152‑5.................Notices to remedy contraventions

152‑10..............Liability of directors in relation to non‑compliance with notices

152‑15....Council may sue in the name of private health insurers

Part 4‑5—Other obligations of private health insurers

Division 157—Introduction

157‑1........................What this Part is about

157‑5...The Private Health Insurance (Insurer Obligations) Rules

Division 160—Appointed actuaries

160‑1..............................Appointment

160‑5.....................Eligibility for appointment

160‑10..................Notification of appointment etc.

160‑15.....................Cessation of appointment

160‑20Compliance with the Private Health Insurance (Insurer Obligations) Rules

160‑25....................Powers of appointed actuary

160‑30..................Actuary’s obligations to report

160‑35.............Qualified privilege of appointed actuary

Division 163—Prudential standards

163‑1Private Health Insurance (Insurer Obligations) Rules to establish prudential standards

163‑5...............Compliance with prudential standards

163‑10.........Notice of breaches of prudential standards etc.

163‑15...............Directions to comply with standards

163‑20.................Failure to comply with directions

Division 166—Disqualified persons

166‑1Private health insurers not to allow disqualified persons to act as directors

166‑5..Disqualified persons must not act for private health insurers

166‑10.............................Effect of non‑compliance

166‑15...............................Who is a disqualified person?

166‑20..................Council may disqualify persons

166‑25...Council may determine that persons are not disqualified

Division 169—Reporting and notification requirements

169‑1.................Copies of reports to policy holders

169‑5.........Information to be given to the Council annually

169‑10.....Private health insurers to notify any changes to rules

169‑15Private health insurers to notify Department and Council about current chief executive officer

Division 172—Miscellaneous

172‑1 Private health insurers to comply with Council’s requirements

172-5 Agreements with medical practitioners

172‑10....Private health insurers to give information to Secretary

172‑15......Restrictions on payment of pecuniary penalties etc.

Chapter 5—Enforcement

Part 5‑1—Introduction

Division 180—Introduction

180‑1......................What this Chapter is about

Part 5‑2—General enforcement methods

Division 185—What this Part is about

185‑1..............................Introduction

185‑5..............................Meaning of enforceable obligation

185‑10.............................Meaning of Council‑supervised obligation

Division 188—Performance indicators

188‑1........................Performance indicators

Division 191—Explanation of private health insurer’s operations

191‑1Minister or Council may seek an explanation from a private health insurer

191‑5...........Writer must respond to insurer’s explanation

Division 194—Investigation of private health insurer’s operations

194‑1..Minister or Council may investigate a private health insurer

194‑5......................Notice to give information

194‑10...................Notice to produce documents

194‑15.......................Notice to give evidence

194‑20...........Offences in relation to investigation notices

194‑25........Authorisation to examine books and records etc.

194‑30...................Minister may consult Council

194‑35...Minister or Council must notify outcome of investigation

Division 197—Enforceable undertakings

197‑1Minister or Council may accept written undertakings given by a private health insurer

197‑5....................Enforcement of undertakings

Division 200—Ministerial and Council directions

200‑1..............Minister or Council may give directions

200‑5........................Direction requirements

Division 203—Remedies in the Federal Court

203‑1.......Minister or Council may apply to the Federal Court

203‑5....................Declarations of contravention

203‑10......................Pecuniary penalty order

203‑15.........................Compensation order

203‑20.......................Adverse publicity order

203‑25..............................Other order

203‑30..............Time limit for declarations and orders

203‑35 Civil evidence and procedure rules for declarations and orders

203‑40..........Civil proceedings after criminal proceedings

203‑45.........Criminal proceedings during civil proceedings

203‑50..........Criminal proceedings after civil proceedings

203‑55Evidence given in proceedings for penalty not admissible in criminal proceedings

203‑60........Minister or Council may require person to assist

203‑65Relief from liability for contravening an enforceable obligation

203‑70......................Powers of Federal Court

Division 206—Revoking entitlement to offer rebate as a premium reduction

206‑1...........Revocation of status of participating insurer

Part 5‑3—Enforcement of health benefits fund requirements

Division 211—Introduction

211‑1........................What this Part is about

211‑5..........................Purpose of this Part

211‑10The Private Health Insurance (Health Benefits Fund Enforcement) Rules

211‑15Limitation on external management and termination of health benefits funds

Division 214—Investigations into affairs of private health insurers

214‑1......Investigation of private health insurers by inspectors

214‑5.........................Powers of inspectors

214‑10..............Person may be represented by lawyer

214‑15..........Compliance with requirements of inspectors

214‑20.........................Access to premises

214‑25........................Reports of inspectors

214‑30......................Dissemination of reports

214‑35................Liability for publishing reports etc.

214‑40......................Delegation by inspectors

214‑45.................Records not to be concealed etc.

Division 217—External management of health benefits funds

Subdivision 217‑A—Preliminary

217‑1..........................Purpose of Division

217‑5......The basis of the law relating to external management

Subdivision 217‑B—Appointment of external managers

217‑10.............Council may appoint external managers

217‑15.........Grounds of appointment of external managers

217‑20.....External managers to displace management of funds

Subdivision 217‑C—Duties and powers of external managers

217‑25....................Duties of external managers

217‑30.............Additional powers of external managers

217‑35......Protection of property during external management

217‑40Rights of chargee, owner or lessor of property of fund under external management

Subdivision 217‑D—Procedure relating to voluntary deeds of arrangement

217‑45Matters that may be included in the Private Health Insurance (Health Benefits Fund Enforcement) Rules

Subdivision 217‑E—External managers’ reports to Council

217‑50..........External managers to give reports to Council

217‑55............Dealing with reports given to the Council

217‑60.......Court orders in respect of schemes of arrangement

Subdivision 217‑F—Miscellaneous

217‑65........When an external management begins and ends

217‑70Effect of things done during external management of health benefits funds

217‑75..................Disclaimer of onerous property

217‑80.........Application of provisions of Corporations Act

Division 220—Ordering the termination of health benefits funds

220‑1....Applications by external managers to the Federal Court

220‑5Orders made on applications for appointments of terminating managers

220‑10..................Binding nature of Court orders

220‑15.......................Notice of appointments

Chapter 6—Administration

Part 6‑1—Introduction

Division 230—Introduction

230‑1......................What this Chapter is about

Part 6‑2—Private Health Insurance Ombudsman

Division 235—Introduction

235‑1.....................Principal object of this Part

235‑5..........Private Health Insurance (Ombudsman) Rules

Division 238—Establishment and functions

238‑1Establishment of office of Private Health Insurance Ombudsman

238‑5.......Functions of Private Health Insurance Ombudsman

Division 241—Complaints

Subdivision 241‑A—Relevant complaints

241‑1.....................Who may make a complaint

241‑5.........Persons against whom complaints may be made

241‑10.......................Grounds for complaint

Subdivision 241‑B—Dealing with complaints

241‑15.....................Initial receipt of complaint

241‑20.................Ways of dealing with complaints

241‑25Referral to the Australian Competition and Consumer Commission

241‑30.......................Referral to other bodies

241‑35..............Deciding not to deal with a complaint

Subdivision 241‑C—Referral to subjects of complaints

241‑40.............Referral to the subject of the complaint

Subdivision 241‑D—Investigation of complaints

241‑45.....................Investigation of complaint

241‑50Minister may direct Private Health Insurance Ombudsman to investigate, or to continue to investigate, a complaint

Subdivision 241‑E—Recommendations and reports

241‑55...Recommendations as a result of referral or investigation

241‑60Report to Minister on outcome of investigation under Subdivision 241‑D

Subdivision 241‑F—Miscellaneous

241‑65.................Complainant to be kept informed

Division 244—Investigations

Subdivision 244‑A—Investigations

244‑1.......................Initiating investigations

244‑5................Investigations at Minister’s request

Subdivision 244‑B—Recommendations and reports

244‑10..........Recommendations as a result of investigation

244‑15Report to Minister on outcome of investigations under this Division

244‑20Consultation with Australian Competition and Consumer Commission

Division 247—Mediation

247‑1........................Conducting mediation

247‑5..........Participation in mediation may be compulsory

247‑10.......Medical practitioners may appoint representatives

247‑15................Conduct of compulsory mediation

247‑20............Admissibility of things said in mediation

247‑25.....................Appointment of mediators

Division 250—Information‑gathering

250‑1..............................Information‑gathering

250‑5........................Limits on information‑gathering

250‑10................Disclosure of personal information

Division 253—Provisions relating to the Private Health Insurance Ombudsman

253‑1...Appointment of the Private Health Insurance Ombudsman

253‑5.......................Validity of appointments

253‑10........................Acting appointments

253‑15...................Remuneration and allowances

253‑20........................Outside employment

253‑25..........................Leave of absence

253‑30..............................Resignation

253‑35....................Termination of appointment

253‑40Disclosure of interest by Private Health Insurance Ombudsman

253‑45...Statutory agency etc. for purposes of Public Service Act

253‑50............................Annual report

253‑55..............................Delegation

253‑60Private Health Insurance Ombudsman and staff not personally liable

Division 256—Miscellaneous

256‑1....................Protection from civil actions

256‑5.............................Victimisation

256‑10Giving information about the Private Health Insurance Ombudsman

Part 6‑3—Private Health Insurance Administration Council

Division 261—Introduction

261‑1........................What this Part is about

261‑5..........The Private Health Insurance (Council) Rules

Division 264—Continuation, purposes, functions and powers

264‑1.....................Continuation of the Council

264‑5......................Objectives of the Council

264‑10......................Functions of the Council

264‑15.................Report on private health insurers

264‑20................................Powers

264‑25.......................Directions by Minister

Division 267—Constitution and administration

267‑1.....................Constitution of the Council

267‑5......................Appointment of members

267‑10......................Meetings of the Council

267‑15.....................Delegation by the Council

267‑20.........................Modification of the Commonwealth Authorities and Companies Act 1997

Division 270—Members

270‑1......................Terms and conditions etc.

270‑5.......................Validity of appointments

270‑10........................Acting Commissioner

270‑15Deputy Commissioner to act as Commissioner in certain circumstances

270‑20.....Powers and duties of persons acting as Commissioner

270‑25...........Remuneration and allowances of members

270‑30..........................Leave of absence

270‑35..............................Resignation

270‑40....................Termination of appointment

270‑45.......................Disclosure of interests

Division 273—Chief Executive Officer and staff

273‑1.......................Chief Executive Officer

273‑5.................Duties of Chief Executive Officer

273‑10.........................Conflict of interests

273‑15........................Staff and consultants

273‑20..Remuneration and allowances of Chief Executive Officer

273‑25..........Leave of absence of Chief Executive Officer

Part 6‑4—Administration of premiums reduction and incentive payments schemes

Division 276—Introduction

276‑1........................What this Part is about

Division 279—Provisions applying only to premiums reduction scheme

Subdivision 279‑A—Reimbursement of private health insurers for premiums reduced under scheme

279‑1.........Participating insurers may claim reimbursement

279‑5.........................Participating insurers

279‑10......................Requirements for claims

279‑15.........Amounts payable to the private health insurer

279‑20..Notifying private health insurers if amount is not payable

279‑25..Additional payment if insurer claims less than entitlement

279‑30........Additional payment if insurer makes a late claim

279‑35.................Content and timing of application

279‑40.......................Decision on application

279‑45....................Reconsideration of decisions

Subdivision 279‑B—Powers of Medicare Australia CEO in relation to participating insurers

279‑50................Audits by Medicare Australia CEO

279‑55Medicare Australia CEO may require production of applications

Division 282—Provisions applying to premiums reduction scheme and incentive payments scheme

Subdivision 282‑A—When and how payments can be recovered

282‑1........................Recovery of payments

282‑5..................Interest on amounts recoverable

282‑10Medicare Australia CEO may set off debts against amounts payable

282‑15...Reconsideration of certain decisions under this Division

Subdivision 282‑B—Miscellaneous

282‑20.......Notification requirements—private health insurers

282‑25.......Use etc. of information relating to another person

282‑30.Information to be provided to the Commissioner of Taxation

282‑35..............................Delegation

282‑40............................Appropriation

Part 6‑5—External managers and terminating managers

Division 287—Introduction

287‑1........................What this Part is about

287‑5.......The Private Health Insurance (Management) Rules

Division 290—Powers of managers

290‑1.........................Powers of managers

290‑5Officers etc. not to perform functions etc. while fund is under management

290‑10........Managers act as agents of private health insurers

Division 293—Information concerning, and records and property of, health benefits funds

293‑1...................Directors etc. to help managers

293‑5.................Managers’ rights to certain records

293‑10Only manager can deal with property of fund under management

293‑15Order for compensation where officer involved in void transaction

Division 296—Provisions incidental to appointment of managers

296‑1.....................Remuneration of managers

296‑5.............Council may give directions to managers

296‑10............Termination of appointments of managers

296‑15....................Acts of managers valid etc.

296‑20...............................Indemnity

296‑25.........................Qualified privilege

Division 299—Miscellaneous

299‑1Time for doing act does not run while act prevented by this Division

299‑5........Continued application of other provisions of Act

299‑10Modifications of this Act in relation to health benefits funds under management

299‑15...........Order of Court to be binding on all persons

299‑20....................Jurisdiction of Federal Court

299‑25Private Health Insurance (Management) Rules dealing with various matters

Part 6‑6—Private health insurance levies

Division 304—Introduction

304‑1........................What this Part is about

304‑5.....Private Health Insurance (Levy Administration) Rules

304‑10.............................Meaning of private health insurance levy

Division 307—Collection and recovery of private health insurance levies

307‑1........When private health insurance levy must be paid

307‑5.........................Late payment penalty

307‑10............Payment of levy and late payment penalty

307‑15...........Recovery of levy and late payment penalty

307‑20Waiver of late payment penalty for levies other than collapsed insurer levy

307‑25Waiver of collapsed insurer levy and late payment penalty for that levy

307‑30.............................Other matters

Division 310—Returns, requesting information and keeping records

310‑1.....Returns must be lodged with Council and Department

310‑5......................Insurer must keep records

310‑10.........Council may request information from insurer

Division 313—Power to enter premises and search for documents

313‑1.......Authorised officer may enter premises with consent

313‑5......Authorised officer may enter premises under warrant

313‑10....................Announcement before entry

313‑15..............Executing a warrant to enter premises

313‑20.............................Identity cards

Part 6‑7—Private Health Insurance Risk Equalisation Trust Fund

Division 318—Private Health Insurance Risk Equalisation Trust Fund

318‑1.....Private Health Insurance Risk Equalisation Trust Fund

318‑5...Amounts to be paid into the Risk Equalisation Trust Fund

318‑10.........Operation of the Risk Equalisation Trust Fund

318‑15......Administration of the Risk Equalisation Trust Fund

Part 6‑8—Disclosure of information

Division 323—Disclosure of information

323‑1.............Prohibition on disclosure of information

323‑5...............Authorised disclosure: official duties

323‑10Authorised disclosure: sharing information about insurers among agencies

323‑15Authorised disclosure: sharing information about insurers other than among agencies

323‑20..............Authorised disclosure: public interest

323‑25Authorised disclosure: by the Secretary or Council if authorised by affected person

323‑30............Authorised disclosure: court proceedings

323‑35Authorised disclosure: Council’s public information and agency cooperation functions

323‑40Offence: disclosure of information obtained by certain authorised disclosures

323‑45..........Offence: soliciting disclosure of information

323‑50..........Offence: use etc. of unauthorised information

323‑55.......Offence: offering to supply protected information

Part 6‑9—Review of decisions

Division 328—Review of decisions

328‑1........................What this Part is about

328‑5......................AAT review of decisions

Part 6‑10—Miscellaneous

Division 333—Miscellaneous

333‑1........................Delegation by Minister

333‑5.......................Delegation by Secretary

333‑10...........................Approved forms

333‑15......................Signing approved forms

333‑20.....Private Health Insurance Rules made by the Minister

333‑25.....Private Health Insurance Rules made by the Council

333‑30..............................Regulations

Schedule 1—Dictionary

1 Dictionary

Private Health Insurance Act 2007

No. 31, 2007

An Act to regulate private health insurance, and for related purposes

[Assented to 30 March 2007]

The Parliament of Australia enacts:

This Act may be cited as the Private Health Insurance Act 2007.

This Act commences on 1 April 2007.

1‑10 Identifying defined terms

(1) Many of the terms in this Act are defined in the Dictionary in Schedule 1.

(2) Most of the terms that are defined in the Dictionary are identified by an asterisk appearing at the start of the term: as in “*health benefits fund”. The footnote with the asterisk contains a signpost to the Dictionary.

(3) An asterisk usually identifies the first occurrence of a term in a section (if not divided into subsections), subsection, definition, table item or diagram. Later occurrences of the term in the same provision are not usually asterisked.

(4) Terms are not asterisked in headings, notes, examples or guides.

(5) If a term is not identified by an asterisk, disregard that fact in deciding whether or not to apply to that term a definition or other interpretation provision.

(6) The following basic terms used throughout the Act are not identified with an asterisk:

Terms that are not identified with an asterisk | ||

Item | This term ... | is defined in ... |

1 | Council | the Dictionary in Schedule 1 |

2 | Federal Court | the Dictionary in Schedule 1 |

3 | insurance | section 5‑1 |

4 | Medicare Australia CEO | the Dictionary in Schedule 1 |

5 | Private Health Insurance Ombudsman | the Dictionary in Schedule 1 |

6 | private health insurer | the Dictionary in Schedule 1 |

Division 3—Overview of this Act

This Act is about private health insurance. It:

(a) provides incentives to encourage people to have private health insurance; and

(b) sets out rules governing private health insurance *products; and

(c) imposes requirements about how insurers conduct *health insurance business.

Chapter 2 provides the following incentives:

(a) reductions in premiums for *complying health insurance policies;

(b) payments by the Commonwealth in relation to premiums paid for complying health insurance policies;

(c) a lifetime health cover scheme, under which premiums may rise for people who do not maintain private health insurance from an early age.

3‑10 Complying health insurance products (Chapter 3)

Chapter 3 requires insurers who make private health insurance available to people to do so in a non‑discriminatory way, to offer *products that comply with this Act, and to meet certain other obligations imposed by this Act in relation to those products.

3‑15 Private health insurers (Chapter 4)

Chapter 4 requires registration of anyone carrying on *health insurance business, and imposes obligations aimed at ensuring health insurance businesses, and in particular *health benefits funds, are conducted appropriately.

Chapter 5 provides for a range of enforcement mechanisms aimed at monitoring and ensuring compliance with this Act and protecting the interests of *policy holders.

3‑25 Administration (Chapter 6)

Chapter 6 contains administrative and machinery provisions relating to the operation of this Act.

The Dictionary in Schedule 1 contains definitions of terms used throughout this Act.

Division 5—Constitutional matters

In this Act:

insurance means insurance to which paragraph 51(xiv) of the Constitution applies.

5‑5 Act not to apply to State insurance within that State

This Act does not apply with respect to State insurance that does not extend beyond the limits of the State concerned.

5‑10 Compensation for acquisition of property

(1) If the operation of this Act would result in an acquisition of property from a person otherwise than on just terms, the Commonwealth is liable to pay a reasonable amount of compensation to the person.

(2) If the Commonwealth and the person do not agree on the amount of the compensation, the person may institute proceedings in the Federal Court for the recovery from the Commonwealth of such reasonable amount of compensation as the court determines.

(3) In this section:

acquisition of property has the same meaning as in paragraph 51(xxxi) of the Constitution.

just terms has the same meaning as in paragraph 51(xxxi) of the Constitution.

15‑1 What this Chapter is about

This Chapter contains the following incentives to encourage people to have private health insurance:

(a) reductions in premiums (see Division 23);

(b) payments in return for payments of premiums under complying health insurance policies (see Division 26);

(c) lifetime health cover (see Part 2‑3).

Part 2‑2—Premiums reduction and incentive payments schemes

To encourage people to take out, and continue to hold, private health insurance, this Part provides that people may either:

(a) reduce the premiums payable for their complying health insurance policies by participating in the premiums reduction scheme in Division 23; or

(b) receive a payment from the Commonwealth under Division 26 in partial reimbursement for a payment of premiums under a complying health insurance policy.

Note: The premiums reduction scheme and the incentive payments scheme are complemented by the private health insurance offset provided for by Subdivision 61‑H of the Income Tax Assessment Act 1997.

20‑5 Private Health Insurance (Incentives) Rules

Matters relating to the *premiums reduction scheme and the *incentive payments scheme are also dealt with in the Private Health Insurance (Incentives) Rules. The provisions of this Part indicate when a particular matter is or might be dealt with in these Rules.

Note: The Private Health Insurance (Incentives) Rules are made by the Minister under section 333‑20.

Division 23—Premiums reduction scheme

Subdivision 23‑A—Amount of reduction

(1) The amount of premiums payable under a *complying health insurance policy in respect of a financial year is reduced in accordance with this section if a person is a *participant in the *premiums reduction scheme in respect of the policy.

(2) The amount of the reduction is the sum of:

(a) 30% of the amount of premiums payable under the policy in respect of days in the financial year on which no person covered by the policy was aged 65 years or over; and

(b) 35% of the amount of premiums payable under the policy in respect of days in the financial year on which:

(i) at least one person covered by the policy was aged 65 years or over; and

(ii) no person covered by the policy was aged 70 years or over; and

(c) 40% of the amount of premiums payable under the policy in respect of days in the financial year on which at least one person covered by the policy was aged 70 years or over.

(3) However, if, before 1 January 1999, a person was registered or eligible to be registered under the Private Health Insurance Incentives Act 1997 in respect of the policy, the amount of the reduction is the greater of:

(a) the amount worked out under subsection (2); and

(b) the *incentive amount for the policy for the financial year.

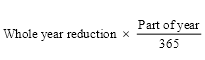

(4) If the amount of premiums is payable in respect of only part of a financial year, the amount of the reduction is worked out using this formula:

where:

part of year means the number of days in the part of the financial year.

whole year reduction means the amount that would have been the reduction if the premium had been payable in respect of the whole financial year.

23‑5 Meaning of incentive amount

(1) The incentive amount for a *complying health insurance policy for a financial year is the amount worked out under this table:

Incentive amount | ||||

Item | Number and kinds of people covered by the policy | Policy covers *hospital treatment but not *general treatment | Policy covers *general treatment but not *hospital treatment | Policy covers *hospital treatment and *general treatment |

1 | 3 or more people | $350 | $100 | $450 |

2 | One *dependent child and one other person | $350 | $100 | $450 |

3 | 2 people neither of whom is a *dependent child | $200 | $50 | $250 |

4 | One person | $100 | $25 | $125 |

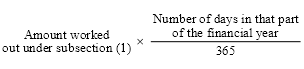

(2) If the amount of premiums is payable in respect of only part of a financial year, the incentive amount is worked out using this formula:

23‑10 Reduction after a person 65 years or over ceases to be covered by policy

(1) If:

(a) at any time, premiums under an insurance policy (the original policy) were reduced by 35% or 40% because a person aged 65 years or over (the entitling person) was insured under the original policy; and

(b) at that time, another person (other than a *dependent child) was also insured under the original policy; and

(c) the entitling person subsequently ceases to be insured under the original policy;

subsections 23‑1(2) and (3) apply in relation to a *complying health insurance policy (whether or not the original policy) under which the other person is insured (other than for the purposes of working out the *incentive amount) as if:

(d) the entitling person were also insured under that policy; and

(e) the entitling person were the same age as the age at which he or she ceased to be insured under the original policy.

(2) Subsection (1) ceases to apply if a person (other than a *dependent child) who was not insured under the original policy at the time the entitling person ceased to be insured under it becomes insured under the *complying health insurance policy.

(3) Subsection (1) does not apply if its application would result in the reduction under subsection 23‑1(2) or (3) being less than it would otherwise have been.

(4) Paragraph (1)(a) applies in relation to premiums reduced by 35% or 40% whether the reduction was under this Part or under Chapter 3 of the Private Health Insurance Incentives Act 1998.

Subdivision 23‑B—Participation in the premiums reduction scheme

23‑15 Registration as a participant in the premiums reduction scheme

(1) A person may apply to a private health insurer, in the *approved form, to become a *participant in the *premiums reduction scheme in respect of a *complying health insurance policy issued by the insurer if:

(a) the insurer is a *participating insurer; and

(b) either or both of the following apply:

(i) the person has paid, or the person’s employer has paid as a *fringe benefit on the person’s behalf, a premium under the policy in respect of a financial year;

(ii) the person is insured under the policy (and is not a *dependent child); and

(c) the person meets any requirements specified in the Private Health Insurance (Incentives) Rules for the purposes of this paragraph.

(2) A private health insurer that receives an application under subsection (1) must notify the Medicare Australia CEO of the application, in the *approved form, no more than 14 days (or any other period determined by the Medicare Australia CEO) after receiving the application.

(3) If notified of an application and satisfied that paragraphs (1)(a), (b) and (c) apply, the Medicare Australia CEO must register the applicant as a *participant in respect of the policy.

(4) The Medicare Australia CEO must notify the private health insurer that issued the policy if the Medicare Australia CEO registers a person as a *participant in the *premiums reduction scheme in respect of the policy.

(1) If the Medicare Australia CEO refuses to register the applicant in respect of a policy, the Medicare Australia CEO must give the applicant, and the private health insurer that issued the policy, notice of the refusal together with reasons for the refusal.

Note: Refusals to register are reviewable under Part 6‑9.

(2) The applicant is taken to be registered as a *participant in respect of the policy if the Medicare Australia CEO does not give notice of refusal within 14 days after receiving the notice under subsection 23‑15(2) from the private health insurer to which the applicant applied for registration.

23‑25 Pre‑1999 participants must keep information up to date

(1) If, before 1 January 1999, a person was registered or eligible to be registered under the Private Health Insurance Incentives Act 1997 in respect of the policy, a *participant in respect of the policy must notify the private health insurer that issued the policy if there is a change in a detail:

(a) stated in an application under subsection 23‑15(1); or

(b) relating to the number of people insured under the policy, or to whether any of those people are *dependent children;

that the participant should reasonably expect will affect the *incentive amount for the policy for a financial year. The participant must give the notice no more than 30 days after the change occurs.

(2) A person commits an offence if:

(a) the person is required by subsection (1) to give a notice to a private health insurer if a detail mentioned in that subsection changes as mentioned in that subsection; and

(b) the person fails to comply with the requirement.

Penalty: 60 penalty units.

(3) Subsection 4K(2) of the Crimes Act 1914 does not apply to the obligation to provide information under subsection (1).

(4) A private health insurer must notify the Medicare Australia CEO of each notice the insurer receives under subsection (1), in the *approved form and no more than 14 days (or any other period determined by the Medicare Australia CEO) after receiving the notice.

23‑30 Participants who want to withdraw from scheme

(1) A *participant must notify the private health insurer that issued the policy in respect of which a person is a participant if the person no longer wishes to be registered in respect of the policy.

(2) A private health insurer must notify the Medicare Australia CEO of each notice the insurer receives under subsection (1), in the *approved form and no more than 14 days (or any other period determined by the Medicare Australia CEO) after receiving the notice.

(3) If notified under subsection (2), the Medicare Australia CEO must revoke the person’s registration in respect of the policy.

23‑35 Revocation of registration

(1) The Medicare Australia CEO must revoke a person’s registration in respect of a *complying health insurance policy if the Medicare Australia CEO is satisfied that the person is not eligible to participate in the *premiums reduction scheme in respect of the policy.

Note: Revocations of registration are reviewable under section Part 6‑9.

(2) Revocation of registration under subsection (1) does not affect a person’s right to make another application for registration under section 23‑15.

(3) The Medicare Australia CEO must give notice of the revocation of a person’s registration in respect of a *complying health insurance policy to the person, and to the private health insurer that issued the policy, within 28 days after the day on which the revocation occurs.

23‑40 Variation of registration

(1) A private health insurer must notify the Medicare Australia CEO if the treatments *covered by a *complying health insurance policy, issued by the private health insurer and in respect of which a person is a *participant, are varied.

(2) On receiving such a notice, the Medicare Australia CEO must vary the details of the registration accordingly and give notice of the variation to the private health insurer.

23‑45 Retention of applications by private health insurers

(1) A private health insurer must retain an application made to it under subsection 23‑15(1) for the period of 5 years beginning on the day on which the application was made.

(2) The private health insurer may retain the application in any form approved in writing by the Medicare Australia CEO.

(3) An application retained in such a form must be received in all courts or tribunals as evidence as if it were the original.

Division 26—The incentive payments scheme

Subdivision 26‑A—Amount of incentive payment

26‑1 Payment in relation to premiums

(1) A person is entitled to a payment under this Division if:

(a) the person has paid, or a person’s employer has paid as a *fringe benefit for the person, premiums under a *complying health insurance policy for the whole or a part of a financial year; and

(b) the amount of premiums was not reduced under Division 23; and

(c) the person meets any requirements specified in the Private Health Insurance (Incentives) Rules for the purposes of this paragraph.

(2) The amount of the payment is the sum of:

(a) 30% of the amount of the premium paid by a person, or by a person’s employer as a *fringe benefit for the person, under the policy in respect of days in the financial year on which no person covered by the policy was aged 65 years or over;

(b) 35% of the amount of the premium paid by a person, or by a person’s employer as a fringe benefit for the person, under the policy in respect of days in the financial year on which:

(i) at least one person covered by the policy was aged 65 years or over; and

(ii) no person covered by the policy was aged 70 years or over;

(c) 40% of the amount of the premium paid by a person, or by a person’s employer as a fringe benefit for the person, under the policy in respect of days in the financial year on which at least one person covered by the policy was aged 70 years or over.

(3) However, if, before 1 January 1999, a person was registered, or eligible to be registered, under the Private Health Insurance Incentives Act 1997 in respect of the policy, the amount of the payment is the greater of:

(a) the amount worked out under subsection (2); and

(b) the *incentive amount for the policy for the financial year.

(4) The total amount payable under this Division for a policy for a financial year is reduced by the amount of any tax offset received under Subdivision 61‑H of the Income Tax Assessment Act 1997 for the total amount of the premium paid by a person, or by a person’s employer as a *fringe benefit for the person, under the policy for that financial year.

(5) A private health insurer must give a person a receipt, in the *approved form, for a payment of an amount of premiums (other than an amount that has been reduced under Division 23) if the person requests it.

26‑5 Payment after a person 65 years or over ceases to be covered by policy

(1) If:

(a) at any time, a payment of an amount of 35% or 40% of the premiums payable under an insurance policy (the original policy) was made to a person because a person aged 65 years or over (the entitling person) was insured under the original policy; and

(b) at that time, another person (other than a *dependent child) was insured under the original policy; and

(c) the entitling person subsequently ceases to be insured under the original policy;

subsections 26‑1(2) and (3) apply in relation to a *complying health insurance policy (whether or not the original policy) under which the other person is insured (other than for the purposes of working out the *incentive amount) as if:

(d) the entitling person were also insured under that policy; and

(e) the entitling person were the same age as the age at which he or she ceased to be insured under the original policy.

(2) Subsection (1) ceases to apply if a person (other than a *dependent child) who was not insured under the original policy at the time the entitling person ceased to be insured under it becomes insured under the *complying health insurance policy.

(3) Subsection (1) does not apply if its application would result in the amount payable under subsection 26‑1(2) or (3) being less than it would otherwise have been.

(4) Paragraph (1)(a) applies in relation to a payment of an amount of 35% or 40% of the premiums payable under an insurance policy whether the payment was made under this Part or under Chapter 2 of the Private Health Insurance Incentives Act 1998.

Subdivision 26‑B—Claiming payments under the incentive payments scheme

26‑10 Claim for payment under incentive payments scheme

(1) To be paid an amount to which a person is entitled under section 26‑1, the person must make a claim in the *approved form.

(2) The claim must be sent to or lodged at an office of Medicare Australia, or a place approved by the Medicare Australia CEO, in:

(a) the financial year in which the payment of premiums to which the claim relates was made; or

(b) the next financial year.

A claimant may at any time, by writing sent to or lodged at an office of Medicare Australia, or a place approved by the Medicare Australia CEO, withdraw a claim.

26‑20 Determination of claim and payment of amount

(1) The Medicare Australia CEO must make a decision granting or refusing the claim within 14 days after the day on which the claim is made.

(2) If the claim is granted, the Medicare Australia CEO must pay to the claimant the amount to which the claimant is entitled.

(3) If the claim is refused, the Medicare Australia CEO must give the claimant a notice stating that the claim has been refused and setting out the reasons for the refusal.

26‑25 Reconsideration of decision refusing a claim

(1) If a claim is refused, the claimant may apply to the Medicare Australia CEO for the Medicare Australia CEO to reconsider the decision.

(2) The application must:

(a) be in writing; and

(b) set out the reasons for the application.

(3) The application must be made within:

(a) 28 days after the day on which the claimant was notified of the decision; or

(b) if, either before or after the end of that period of 28 days, the Medicare Australia CEO extends the period within which the application may be made—the extended period for making the application.

(4) The Medicare Australia CEO must:

(a) reconsider the decision; and

(b) either affirm or revoke the decision;

within 28 days after receiving the application for reconsideration.

Note: Decisions affirming original decisions are reviewable under Part 6‑9.

(5) If the Medicare Australia CEO revokes the decision, the revocation is taken to be a decision granting the claim.

(6) The Medicare Australia CEO must give the claimant a notice stating his or her decision on the reconsideration together with a statement of his or her reasons for the decision.

(7) The Medicare Australia CEO is taken, for the purposes of this Subdivision, to have made a decision affirming the original decision if the Medicare Australia CEO has not told the claimant of the decision on the reconsideration before the end of the period of 28 days.

26‑30 Claimants to keep information up to date

(1) If, after a claimant has made a claim under section 26‑10 for a payment of an amount:

(a) a matter, event or circumstance occurs that affects the claimant’s entitlement to the payment; or

(b) a change occurs in the premium, or in the amounts or frequency of the payments in respect of the premium, under the policy;

the claimant must, within 30 days after the occurrence of the matter, event, circumstance or change, notify the Medicare Australia CEO of the details of the matter, event, circumstance or change.

(2) A person commits an offence if:

(a) the person is required by subsection (1) to notify the Medicare Australia CEO of the details of a matter, event, circumstance or change mentioned in that subsection; and

(b) the person fails to comply with the requirement.

Penalty: 60 penalty units.

(3) Subsection 4K(2) of the Crimes Act 1914 does not apply to the obligation to provide information under subsection (1).

Part 2‑3—Lifetime health cover

People are encouraged to take out hospital cover by the time they turn 30. A person who is older than 30 when he or she takes out hospital cover for the first time, or who drops hospital cover for a period after having turned 30, may have to pay higher premiums for hospital cover. This scheme is known as lifetime health cover.

31‑5 Private Health Insurance (Lifetime Health Cover) Rules

Matters relating to lifetime health cover are also dealt with in the Private Health Insurance (Lifetime Health Cover) Rules. The provisions of this Part indicate when a particular matter is or might be dealt with in these Rules.

Note: The Private Health Insurance (Lifetime Health Cover) Rules are made by the Minister under section 333‑20.

Division 34—General rules about lifetime health cover

34‑1 Increased premiums for person who is late in taking out hospital cover

(1) A private health insurer must increase the amount of premiums payable for *hospital cover in respect of an *adult if the adult did not have hospital cover on his or her *lifetime health cover base day.

(2) The amount of the increase is worked out as follows:

where:

base rate, for *hospital cover, is the amount of premiums that would be payable for the cover if:

(a) the premiums were not increased under this Part; and

(b) there was no discount of the kind allowed under subsection 66‑5(2).

lifetime health cover age, in relation to an *adult who takes out *hospital cover after his or her *lifetime health cover base day, means the adult’s age on the 1 July before the day on which the adult took out the hospital cover.

(1) A private health insurer must increase the amount of premiums payable for *hospital cover in respect of an *adult if, after the adult’s *lifetime health cover base day, the adult ceases to have hospital cover.

(2) The amount of the increase is worked out as follows:

where:

base rate is the *base rate for the *hospital cover.

years without hospital cover is the number obtained by:

(a) dividing by 365 the number of days (other than *permitted days without hospital cover), after the first day on which subsection (1) applied to the *adult, on which he or she did not have *hospital cover; and

(b) rounding up the result to the nearest whole number.

(3) Any increase under this section in the amount of premiums payable for *hospital cover is in addition to any increase under section 34‑1 in the amount of premiums payable for that hospital cover.

34‑10 Increased premiums stop after 10 years’ continuous cover

(1) A private health insurer must stop increasing the amount of premiums payable for *hospital cover in respect of an *adult under this Part if the adult has had hospital cover (including under an *applicable benefits arrangement), the premiums for which have been increased under this Part or *old Schedule 2:

(a) for a continuous period of 10 years; or

(b) for a period of 10 years that has been interrupted only by *permitted days without hospital cover or periods during which the adult was taken to have had hospital cover otherwise than because of paragraph 34‑15(2)(a) (none of which count towards the 10 years).

(2) The amount must stop being increased on the day after the last day of the 10 year period.

(3) The amount of premiums payable for *hospital cover in respect of the *adult must start to be increased under this Part again if:

(a) after the end of the 10 year period, the adult ceases to have hospital cover; and

(b) the adult later takes out hospital cover again; and

(c) the days in the period between ceasing to have the cover and taking it out again are not all *permitted days without hospital cover in respect of the adult.

(4) Subsection (3) does not prevent this section applying again in respect of any later 10 year period.

(5) In subsection (1):

old Schedule 2 means Schedule 2 to the National Health Act 1953 as in force before 1 April 2007.

34‑15 Meaning of hospital cover

(1) Hospital cover is so much of a *complying health insurance policy as *covers *hospital treatment. An *adult has hospital cover if he or she is insured under a complying health insurance policy that covers hospital treatment.

(2) An *adult is taken to have *hospital cover:

(a) at any time during which the adult was covered by an *applicable benefits arrangement; or

(b) at any time during which the adult holds a *gold card; or

(c) at any time during which the adult is in a class of adults specified in the Private Health Insurance (Lifetime Health Cover) Rules for the purposes of this paragraph.

(3) In this section:

gold card means a card that evidences a person’s entitlement to be provided with treatment:

(a) in accordance with the Treatment Principles prepared under section 90 of the Veterans’ Entitlements Act 1986; or

(b) in accordance with a determination made under section 286 of the Military Rehabilitation and Compensation Act 2004 in respect of the provision of treatment.

34‑20 Meaning of permitted days without hospital cover

(1) Any of the following days that occur after an *adult ceases, for the first time after his or her *lifetime health cover base day, to have *hospital cover are permitted days without hospital cover in respect of that adult:

(a) days on which the cover was suspended by the private health insurer in accordance with the rules for suspensions set out in the Private Health Insurance (Lifetime Health Cover) Rules;

(b) days (not counting days covered by paragraph (a)) on which the adult is *overseas that form part of a continuous period overseas of more than one year;

(c) the first 1,094 days (not counting days covered by paragraph (a) or (b)) on which the adult did not have hospital cover.

(2) The Private Health Insurance (Lifetime Health Cover) Rules may specify days that, despite subsection (1), are taken not to be *permitted days without hospital cover.

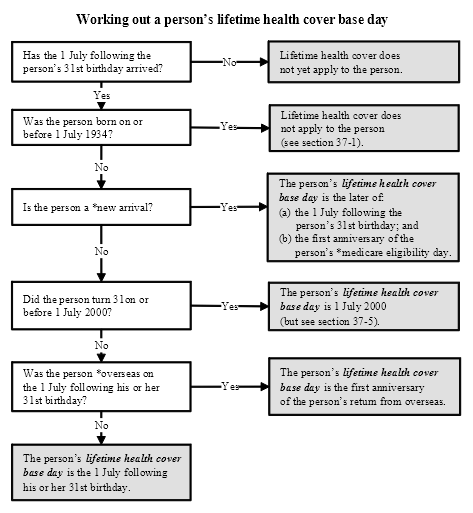

34‑25 Meaning of lifetime health cover base day

(1) A person’s lifetime health cover base day is the day worked out by using this diagram:

(2) A person is a new arrival if:

(a) the person entered Australia for the first time on or after 1 July 2000; and

(b) the person was not an Australian citizen or permanent resident of Australia at the time of the entry.

(3) A person’s medicare eligibility day is the day on which the person is registered by the Medicare Australia CEO as an eligible person within the meaning of section 3 of the Health Insurance Act 1973.

(4) Despite subsection (1), if:

(a) on or before 1 April 2007, a person’s Schedule 2 application day had arrived for the purposes of the National Health Act 1953; and

(b) the person had *hospital cover on 1 April 2007; and

(c) the person has had hospital cover continuously since that day;

the person’s lifetime health cover base day is the person’s Schedule 2 application day. For this purpose, a day on which the person has hospital cover does not include a *permitted day without hospital cover or a day on which the person would otherwise be taken to have hospital cover because of subsection 34‑15(2).

34‑30 When a person is overseas

Without limiting when a person is taken to be *overseas for the purposes of this Part:

(a) a person who lives on Norfolk Island is taken, while the person is living there, to be overseas; and

(b) any period in which a person returns to Australia for less than 90 days counts as part of a continuous period overseas; and

(c) a person is taken to have returned from overseas if the person returns to Australia for a period of at least 90 days.

Division 37—Exceptions to the general rules about lifetime health cover

37‑1 People born on or before 1 July 1934

(1) The amount of premiums payable for *hospital cover in respect of an *adult does not increase under this Part if the adult was born on or before 1 July 1934.

(2) However, this section does not prevent section 37‑20 applying to the *hospital cover in respect of any *adults who were born after 1 July 1934.

37‑5 People over 31 and overseas on 1 July 2000

A person:

(a) who turned 31 on or before 1 July 2000; and

(b) who was *overseas on 1 July 2000;

is taken, for the purposes of section 34‑1, to have had *hospital cover on the person’s *lifetime health cover base day.

A person is treated for the purposes of this Part as if he or she had *hospital cover on 1 July 2000 if a determination under clause 10 of Schedule 2 to the National Health Act 1953 (as in force immediately before 1 April 2007) had effect in relation to the person immediately before 1 April 2007.

37‑15 Increases cannot exceed 70% of base rates

The maximum amount of any increase under this Part in the amount of premiums payable for *hospital cover in respect of an *adult is an amount equal to 70% of the *base rate for the hospital cover.

(1) If:

(a) more than one *adult is covered under the same *hospital cover; and

(b) the amount of premiums payable for the cover in respect of at least one of those adults is increased under this Part;

the amount of the premiums payable for the cover in respect of all of the adults is increased.

(2) The amount of the increase in the premiums payable for the cover is worked out by:

(a) dividing the *base rate for the cover by the number of *adults it covers; and

(b) using that rate to work out for each adult what the amount of the increase for that adult (if any) would be; and

(c) adding together the results of paragraph (b).

Division 40—Administrative matters relating to lifetime health cover

40‑1 Notification to insured people etc.

(1) A private health insurer must comply with any requirements specified in the Private Health Insurance (Lifetime Health Cover) Rules relating to providing information to:

(a) *adults in respect of *hospital cover with the private health insurer; and

(b) other adults who apply for, or inquire about, that hospital cover;

about increases under this Part in the amounts of premiums payable for hospital cover in respect of those adults.

(2) A private health insurer must comply with any requirements specified in the Private Health Insurance (Lifetime Health Cover) Rules relating to providing information to other private health insurers about increases under this Part in the amounts of premiums payable for *hospital cover with the private health insurer.

(3) The Private Health Insurance (Lifetime Health Cover) Rules may require or permit a private health insurer to provide information of a kind referred to in this section in the form of an age notionally attributed, to an *adult or other person, as the age from which the adult or other person will be treated as having had continuous *hospital cover.

(4) A private health insurer must keep separate records in relation to each *adult who has *hospital cover.

(5) When an *adult ceases to be *covered by *hospital cover under which more than one adult was covered, the private health insurer must notify each other adult that the adult has ceased to be covered by the cover.

40‑5 Evidence of having had hospital cover, or of a person’s age

A private health insurer must comply with any requirements specified in the Private Health Insurance (Lifetime Health Cover) Rules relating to whether, and in what circumstances, particular kinds of evidence are to be accepted, for the purposes of this Part, as conclusive evidence of:

(a) whether a person had *hospital cover at a particular time, or during a particular period; or

(b) a person’s age.

Chapter 3—Complying health insurance products

50‑1 What this Chapter is about

Broadly, health insurance that is made available to the public must meet the requirements in this Chapter. This means that:

(a) the insurance must be community‑rated (that is, made available in a way that does not discriminate between people) (see Part 3‑2); and

(b) the insurance must be in the form of a complying health insurance product (see Part 3‑3); and

(c) the private health insurers who make the products available must meet certain obligations to people insured or seeking to be insured under the products (see Part 3‑4).

50‑5 Private Health Insurance Rules relevant to this Chapter

Matters relating to *complying health insurance products are also dealt with in the Private Health Insurance (Complying Product) Rules, the Private Health Insurance (Benefit Requirements) Rules, the Private Health Insurance (Prostheses) Rules and the Private Health Insurance (Accreditation) Rules. The provisions of this Chapter indicate when a particular matter is or may be dealt with in these Rules.

Note: These Rules are all made by the Minister under section 333‑20.

Division 55—Principle of community rating

To ensure that everybody who chooses has access to health insurance, the principle of community rating prevents private health insurers from discriminating between people on the basis of their health or for any other reason described in this Part.

55‑5 Principle of community rating

(1) A private health insurer must not:

(a) take or fail to take any action; or

(b) in making a decision, have regard or fail to have regard to any matter;

that would result in the insurer *improperly discriminating between people who are or wish to be insured under a *complying health insurance policy of the insurer.

(2) Improper discrimination is discrimination that relates to:

(a) the suffering by a person from a chronic disease, illness or other medical condition or from a disease, illness or medical condition of a particular kind; or

(b) the gender, race, sexual orientation or religious belief of a person; or

(c) the age of a person, except to the extent allowed under Part 2‑3 (lifetime health cover); or

(d) where a person lives, except to the extent allowed under subsection 66‑10(2) or section 66‑20; or

(e) any other characteristic of a person (including but not just matters such as occupation or leisure pursuits) that is likely to result in an increased need for *hospital treatment or *general treatment; or

(f) the frequency with which a person needs hospital treatment or general treatment; or

(g) the amount or extent of the benefits to which a person becomes entitled during a period under a *complying health insurance policy, except to the extent allowed under section 66‑15; or

(h) any matter set out in the Private Health Insurance (Complying Product) Rules for the purposes of this paragraph.

(3) Despite subsection (2), discrimination by a *restricted access insurer is not improper discrimination to the extent to which the insurer:

(a) takes or fails to take an action; or

(b) in making a decision, has regard or fails to have regard to a matter;

only to ensure that its *complying health insurance products are not made available to persons to whom its constitution prohibits it from making the products available.

The principle of community rating in section 55‑5 does not prevent a private health insurer from refusing to make available to a person a *complying health insurance product that the insurer is no longer making available to anyone.

Part 3‑3—Requirements for complying health insurance products

Complying health insurance products (which are made up of complying health insurance policies) are the only kind of insurance that private health insurers are allowed to make available as part of their health insurance business (see section 63‑1 and Division 84). This Part sets out the requirements that an insurance policy must meet in order to be a complying health insurance policy.

Division 63—Basic rules about complying health insurance products

63‑1 Obligation to ensure products are complying products

(1) A private health insurer must ensure that the only kind of insurance that it makes available as part of its *health insurance business is insurance in the form of *complying health insurance products.

(2) However, subsection (1) does not apply in relation to *health insurance business of a kind that the Private Health Insurance (Complying Product) Rules specify is excluded from subsection (1).

63‑5 Meaning of complying health insurance product

(1) A complying health insurance product is a *product made up of *complying health insurance policies.

(2) A product is all the insurance policies issued by a private health insurer:

(a) that *cover the same treatments; and

(b) that provide benefits that are worked out in the same way; and

(c) whose other terms and conditions are the same as each other.

(2A) A product subgroup, of a *product, is all the insurance policies in the product:

(a) under which the addresses of the people insured, as known to the private health insurer, are located in the same *risk equalisation jurisdiction; and

(b) under which the same kind of insured group (within the meaning of the Private Health Insurance (Complying Product) Rules) is insured.

(2B) The Private Health Insurance (Complying Product) Rules may specify insured groups for the purposes of paragraph (2A)(b). An insured group may be specified by reference to any or all of the number of people in the group, the kind of people in the group, or any other matter. A group may consist of only one person.

(3) Different premiums may be payable under policies in the same *product.

63‑10 Meaning of complying health insurance policy

A complying health insurance policy is an insurance policy that meets:

(a) the community rating requirements in Division 66; and

(b) the coverage requirements in Division 69; and

(c) if the policy *covers *hospital treatment—the benefit requirements in Division 72; and

(d) the waiting period requirements in Division 75; and

(e) the portability requirements in Division 78; and

(f) the quality assurance requirements in Division 81; and

(g) any requirements set out in the Private Health Insurance (Complying Product) Rules for the purposes of this paragraph.

Division 66—Community rating requirements

66‑1 Community rating requirements

(1) An insurance policy meets the community rating requirements in this Division if:

(a) the policy prohibits the private health insurer that issued the policy from breaching the principle of community rating in section 55‑5 in relation to a person insured under the policy; and