First Home Saver Accounts (Consequential Amendments) Act 2008

No. 45, 2008

An Act to amend the law relating to financial markets, taxation, superannuation, social security and veterans’ entitlements, and for related purposes

First Home Saver Accounts (Consequential Amendments) Act 2008

No. 45, 2008

An Act to amend the law relating to financial markets, taxation, superannuation, social security and veterans’ entitlements, and for related purposes

Contents

2 Commencement

3 Schedule(s)

Schedule 1—Main taxation related amendments

Income Tax Act 1986

Income Tax Assessment Act 1936

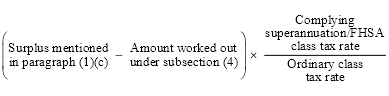

Income Tax Assessment Act 1997

Income Tax Rates Act 1986

Taxation Administration Act 1953

Schedule 2—Amendments relating to the Corporations Act

Australian Securities and Investments Commission Act 2001

Corporations Act 2001

Schedule 3—Other consequential amendments

Anti‑Money Laundering and Counter‑Terrorism Financing Act 2006

Australian Prudential Regulation Authority Act 1998

Banking Act 1959

Life Insurance Act 1995

Social Security Act 1991

Superannuation (Government Co‑contribution for Low Income Earners) Act 2003

Superannuation Industry (Supervision) Act 1993

Veterans’ Entitlements Act 1986

Schedule 4—Amendments to change references to virtual PST assets etc.

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Schedule 5—Amendments to change references to virtual PST

Income Tax Assessment Act 1997

Schedule 6—Amendments to change references to complying superannuation class

Income Tax Assessment Act 1997

Income Tax Rates Act 1986

Taxation Administration Act 1953

Schedule 7—Other amendments relating to changes of references to virtual PST etc.

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Income Tax Rates Act 1986

Taxation Administration Act 1953

First Home Saver Accounts (Consequential Amendments) Act 2008

No. 45, 2008

An Act to amend the law relating to financial markets, taxation, superannuation, social security and veterans’ entitlements, and for related purposes

[Assented to 25 June 2008]

The Parliament of Australia enacts:

This Act may be cited as the First Home Saver Accounts (Consequential Amendments) Act 2008.

This Act commences on the day after it receives the Royal Assent.

Each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

Schedule 1—Main taxation related amendments

1 After subsection 5(2A)

Insert:

(2B) This Act does not impose tax payable in accordance with section 345‑100 of the Income Tax Assessment Act 1997.

Income Tax Assessment Act 1936

2 Subsection 6(1) (at the end of the definition of assessment)

Add:

; or (i) the ascertainment of an amount of FHSA misuse tax (within the meaning of the Income Tax Assessment Act 1997) (or that no tax is payable).

3 Subsection 6(1)

Insert:

FHSA trust has the meaning given by the First Home Saver Accounts Act 2008.

4 After section 95

Insert:

95AA Division does not apply in relation to FHSA trust

This Division does not apply in relation to a trust estate that is an FHSA trust.

5 After paragraph 124ZM(3)(d)

Insert:

or (da) an FHSA trust;

6 After paragraph 202(ka)

Insert:

(kb) to facilitate:

(i) the administration of Division 2 of Part 5 of the First Home Saver Accounts Act 2008 in relation to individuals; and

(ii) the administration of that Act in relation to FHSA providers (within the meaning of that Act); and

7 At the end of section 272‑100 of Schedule 2F

Add:

; or (e) it is an FHSA trust at the particular time.

Income Tax Assessment Act 1997

8 Section 9‑1 (after table item 8)

Insert:

8A | An FHSA provider in relation to an FHSA trust | section 345‑5 |

9 Section 11‑55 (after table item headed “firearms surrender arrangements”)

Insert:

first home saver accounts |

|

credits to and payments from................... | 345‑50 |

10 Subparagraph 115‑100(a)(ii)

After “superannuation entity”, insert “or *FHSA trust”.

11 After subparagraph 115‑100(b)(i)

Insert:

(iia) by an FHSA trust; or

12 After subparagraph 115‑280(1)(a)(i)

Insert:

(ia) an *FHSA trust; or

13 Paragraph 115‑280(2)(a)

After “superannuation entity”, insert “or an *FHSA trust”.

14 Paragraph 115‑280(2)(b)

After “superannuation entity”, insert “, an FHSA trust”.

15 Paragraph 115‑280(5)(a)

After “superannuation entity”, insert “or an *FHSA trust”.

16 Paragraph 115‑280(5)(b)

After “superannuation entity”, insert “, an FHSA trust”.

17 After paragraph 166‑245(2)(b)

Insert:

(ba) an *FHSA trust; and

18 After paragraph 166‑245(3)(b)

Insert:

(ba) if the entity is an *FHSA trust—the entity is an FHSA trust; and

19 Paragraph 207‑15(2)(a)

After “a *complying superannuation entity”, insert “or *FHSA trust”.

20 Paragraph 207‑35(1)(c)

After “a *complying superannuation entity”, insert “or *FHSA trust”.

21 After paragraph 207‑45(c)

Insert:

(ca) the trustee of an *FHSA trust; or

22 At the end of section 290‑5

Add:

; (d) a payment from an *FHSA required under section 22 or 34 of the First Home Saver Accounts Act 2008;

(e) a *Government FHSA contribution.

23 Subsection 295‑10(2)

Repeal the subsection, substitute:

(2) Use this method for *RSA providers:

Method statement

Step 1. Work out the entity’s *no‑TFN contributions income. Apply the applicable rates as set out in the Income Tax Rates Act 1986 to that income.

Step 2. Work out the entity’s assessable income and deductions taking account of the special rules in this Division.

Step 3. Work out the *RSA component and *standard component of the entity’s taxable income.

Step 4. If the entity is also an *FHSA provider, work out the *FHSA component of the entity’s taxable income.

Step 5. Apply the applicable rates as set out in the Income Tax Rates Act 1986 to the components. The *RSA component and the *FHSA component are taxed at a concessional rate.

Step 6. Subtract the entity’s *tax offsets from the sum of the entity’s step 1 and step 5 amounts.

24 After section 295‑170

Insert:

295‑171 Exception—payments from FHSAs and Government FHSA contributions

Item 1 of the table in section 295‑160 does not include in assessable income a contribution that is:

(a) a payment from an *FHSA required under section 22 or 34 of the First Home Saver Accounts Act 2008; or

(b) a *Government FHSA contribution.

25 Subsection 295‑555(1)

Repeal the subsection, substitute:

(1) The taxable income of an *RSA provider is split into:

(a) an *RSA component; and

(b) if the RSA provider is also an *FHSA provider—an *FHSA component; and

(c) a *standard component.

Note: The RSA component and the FHSA component (if applicable) are taxed at the same concessional rate that applies to the low tax component of complying superannuation funds, complying approved deposit funds and pooled superannuation trusts (see section 23 of the Income Tax Rates Act 1986). The standard component is taxed at the standard company rate.

26 Subsections 295‑555(3) and (4)

Repeal the subsections, substitute:

(3) However, if the sum of the *RSA component and the *FHSA component (if any) is more than the *RSA provider’s taxable income:

(a) the provider’s taxable income is equal to that sum; and

(b) this Act applies to the provider as if it had a *tax loss for the income year of an amount that would have been that loss if the RSA component and the FHSA component (if any) were not *ordinary income or *statutory income.

(4) The standard component is the remaining part (if any) of the *RSA provider’s taxable income for the income year after subtracting the *RSA component and the *FHSA component (if any).

27 Section 320‑1

Omit “complying superannuation business and”, substitute “complying superannuation business or FHSAs, and”.

28 Section 320‑1

Omit “complying superannuation business;”, substitute “complying superannuation business or FHSAs;”.

29 Paragraph 320‑80(2)(b)

After “exempt life insurance policy”, insert “, *FHSA”.

30 After paragraph 320‑85(2)(b)

Insert:

(ba) is an *FHSA; or

31 After Division 328

Insert:

Table of Subdivisions

Guide to Division 345

345‑A Treatment of FHSA providers

345‑B Treatment of FHSA holders

345‑1 What this Division is about

FHSAs (short for first home saver accounts) are accounts, life policies and interests in trusts that comply with requirements in the First Home Saver Accounts Act 2008.

This Division sets out the income tax treatment of the financial institutions that provide FHSAs (Subdivision 345‑A) and of individuals that hold FHSAs (Subdivision 345‑B).

Certain payments from FHSAs are subject to FHSA misuse tax (Subdivision 345‑C).

Subdivision 345‑A—Treatment of FHSA providers

Table of sections

345‑5 FHSA provider that is trustee of FHSA trust—tax payable

345‑10 FHSA provider that is trustee of FHSA trust—CGT to be primary code for calculating gains or losses

345‑15 FHSA provider that is an ADI (other than RSA provider)—taxable income and standard component of taxable income

345‑20 FHSA provider that is an ADI—FHSA component of taxable income

345‑5 FHSA provider that is trustee of FHSA trust—tax payable

(1) The trustee of an *FHSA trust is liable to pay income tax for the *financial year on the taxable income of the trust.

(2) The amount of the tax is the amount of income tax that would be payable by the trust under section 4‑10 if the trust were an *Australian resident liable (in accordance with section 4‑1) to pay income tax for the *financial year.

(3) For the purposes of subsection (2):

(a) apply the special rules in this Subdivision in working out the taxable income of the trust; and

(b) apply the applicable rate of tax specified in section 30 of the Income Tax Rates Act 1986 to the taxable income of the trust.

(1) The modifications in subsection (2) apply if a *CGT event happens involving a *CGT asset that was owned by an *FHSA trust.

(2) These provisions do not apply to the *CGT event:

(a) sections 6‑5 (about *ordinary income);

(b) section 8‑1 (about amounts you can deduct);

(c) sections 15‑15 and 25‑40 (about profit‑making undertakings or plans).

Exceptions

(3) The provisions referred to in subsection (2) can apply to the *CGT event if:

(a) any *capital gain or *capital loss from the event is attributable to currency exchange rate fluctuations; or

(b) the *CGT asset is one of the following:

(i) debenture stock, a bond, *debenture, certificate of entitlement, bill of exchange, promissory note or other security;

(ii) a deposit with a bank, building society or other financial institution;

(iii) a loan (secured or not);

(iv) some other contract under which an entity is liable to pay an amount (whether the liability is secured or not).

(4) The provisions referred to in subsection (2) can also apply to the *CGT event if a *capital gain or *capital loss from the event is disregarded because of one of the provisions in this table:

Where gain or loss disregarded because of CGT provision | ||

Item | Provision | Brief description |

1 | Paragraph 104‑15(4)(a) | Title in a CGT asset does not pass when a hire purchase or similar agreement ends |

2 | Section 118‑5 | Cars, motor cycles and valour decorations |

3 | Section 118‑10 | Collectables and personal use assets |

4 | Section 118‑13 | Shares in a PDF |

5 | Section 118‑25 | Trading stock |

6 | Section 118‑30 | Film copyright |

7 | Section 118‑35 | Research and development |

8 | Section 118‑55 | Foreign currency hedging gains and losses |

9 | Section 118‑60 | Certain gifts |

10 | Section 118‑300 | Insurance policies |

11 | Section 118‑305 | Superannuation |

(1) The taxable income of an *FHSA provider that is an *ADI (other than an *RSA provider) is split into an *FHSA component and a *standard component.

Note: The taxable income of an FHSA provider that is an ADI and an RSA provider is split into an RSA component, an FHSA component and a standard component (see section 295‑555).

(2) If the *FHSA component exceeds the *FHSA provider’s taxable income:

(a) the provider’s taxable income is equal to the FHSA component; and

(b) this Act applies to the provider as if it had a *tax loss for the income year of an amount that would have been that loss if the FHSA component were not *ordinary income or *statutory income.

(3) The standard component is the remaining part (if any) of the *FHSA provider’s taxable income for the income year after subtracting the *FHSA component.

345‑20 FHSA provider that is an ADI—FHSA component of taxable income

The FHSA component for an income year of an *FHSA provider that is an *ADI is the total earnings or other return for the year credited to *FHSAs provided by the FHSA provider, reduced by the total amount of fees (however described) paid from those FHSAs to the FHSA provider for providing them.

Subdivision 345‑B—Treatment of FHSA holders

Table of sections

345‑50 Credits to and payments from FHSAs etc.

345‑50 Credits to and payments from FHSAs etc.

(1) An amount of earnings or other return credited to an *FHSA you hold is not your assessable income and is not your *exempt income.

(2) A payment made from an *FHSA you hold is not your assessable income and is not your *exempt income.

(3) A *Government FHSA contribution payable for you in accordance with the First Home Saver Accounts Act 2008, and paid in accordance with Part 4 of that Act, is not your assessable income and is not your *exempt income.

(4) A *capital gain or *capital loss that you make from a *CGT event happening in relation to a right to, or any part of, an *FHSA that you hold is disregarded.

Subdivision 345‑C—FHSA misuse tax

Table of sections

345‑100 Liability for FHSA misuse tax

345‑110 Due date for payment of FHSA misuse tax

345‑115 General interest charge

345‑100 Liability for FHSA misuse tax

A person is liable to pay tax imposed by the Income Tax (First Home Saver Accounts Misuse Tax) Act 2008 in respect of a *FHSA home acquisition payment from an *FHSA held by the person if:

(a) the payment fails to satisfy the *FHSA payment conditions; or

(b) the payment satisfies the FHSA payment conditions, but is an *FHSA ineligibility payment.

Note: The Commissioner may make an assessment of the amount of the tax under section 169 of the Income Tax Assessment Act 1936.

345‑110 Due date for payment of FHSA misuse tax

*FHSA misuse tax assessed for a person is due and payable 21 days after the Commissioner gives the person notice of the assessment.

345‑115 General interest charge

If *FHSA misuse tax payable by a person remains unpaid after the time by which it is due and payable, the person is liable to pay the *general interest charge on the unpaid amount for each day in the period that:

(a) starts at the beginning of the day on which the FHSA misuse tax was due to be paid; and

(b) ends at the end of the last day on which, at the end of the day, any of the following remains unpaid:

(i) the FHSA misuse tax;

(ii) general interest charge on any of the FHSA misuse tax.

Note: The general interest charge is worked out under Part IIA of the Taxation Administration Act 1953.

32 Subsection 995‑1(1) (paragraph (a) of the definition of contract of reinsurance)

Repeal the paragraph, substitute:

(a) the parts of *complying superannuation/FHSA life insurance policies in respect of which the liabilities of the company that issued the policies are to be discharged out of a *complying superannuation/FHSA asset pool; and

33 Subsection 995‑1(1) (definition of excluded virtual PST life insurance policy)

Repeal the definition.

34 Subsection 995‑1(1)

Insert:

FHSA has the meaning given by the First Home Saver Accounts Act 2008.

35 Subsection 995‑1(1)

Insert:

FHSA component has the meaning given by section 345‑20.

36 Subsection 995‑1(1)

Insert:

FHSA holder has the meaning given by the First Home Saver Accounts Act 2008.

37 Subsection 995‑1(1)

Insert:

FHSA home acquisition payment has the meaning given by the First Home Saver Accounts Act 2008.

38 Subsection 995‑1(1)

Insert:

FHSA ineligibility payment has the meaning given by the First Home Saver Accounts Act 2008.

39 Subsection 995‑1(1)

Insert:

FHSA misuse tax means tax imposed under the Income Tax (First Home Saver Accounts Misuse Tax) Act 2008.

40 Subsection 995‑1(1)

Insert:

FHSA payment conditions has the meaning given by the First Home Saver Accounts Act 2008.

41 Subsection 995‑1(1)

Insert:

FHSA provider has the meaning given by the First Home Saver Accounts Act 2008.

42 Subsection 995‑1(1)

Insert:

FHSA trust has the meaning given by the First Home Saver Accounts Act 2008.

43 Subsection 995‑1(1)

Insert:

Government FHSA contribution has the meaning given by the First Home Saver Accounts Act 2008.

44 Subsection 995‑1(1) (definition of standard component)

Repeal the definition, substitute:

standard component:

(a) in respect of an *RSA provider—has the meaning given by section 295‑555; or

(b) in respect of an *FHSA provider that is not an RSA provider—has the meaning given by section 345‑15.

45 Subsection 3(1)

Insert:

ADI has the same meaning as in the Income Tax Assessment Act 1997.

46 Subsection 3(1)

Insert:

FHSA component has the same meaning as in the Income Tax Assessment Act 1997.

47 Subsection 3(1)

Insert:

FHSA provider has the same meaning as in the Income Tax Assessment Act 1997.

48 Subsection 3(1)

Insert:

FHSA trust has the same meaning as in the Income Tax Assessment Act 1997.

49 After paragraph 23(2)(b)

Insert:

(ba) an FHSA provider; or

50 After paragraph 23(3)(a)

Insert:

(aa) in respect of the FHSA component (if any)—15%; and

51 After subsection 23(3)

Insert:

(3A) The rates of tax in respect of the taxable income of a company that is an ADI and an FHSA provider (but not an RSA provider) are:

(a) in respect of the FHSA component—15%; and

(b) in respect of the standard component—30%.

52 At the end of Part III

Add:

30 Rate of tax in relation to trustee of FHSA trust

The rate of tax for the purposes of section 345‑5 of the Income Tax Assessment Act 1997 is 15%.

Taxation Administration Act 1953

53 Subsection 8AAB(5) (after table item 1AA)

Insert:

1A | 52 | First Home Saver Accounts Act 2008 |

54 Subsection 8AAB(5) (after table item 2B)

Insert:

2C | 345‑115 | Income Tax Assessment Act 1997 |

55 Paragraph 8WA(1AA)(b)

After “(j),”, insert “(kb),”.

56 Paragraph 8WB(1A)(a)

After “(ka),”, insert “(kb),”.

57 Paragraph 8WB(1A)(b)

After “(ka),”, insert “(kb),”.

58 After paragraph 45‑120(2)(c) in Schedule 1

Insert:

or (ca) an *FHSA trust;

59 At the end of subsection 45‑290(2) in Schedule 1

Add:

; or (d) an *FHSA trust for that year.

60 At the end of subsection 45‑330(2) in Schedule 1

Add:

; or (d) an *FHSA trust for that year.

61 At the end of subsection 45‑370(2) in Schedule 1

Add:

; or (d) an *FHSA trust for the variation year.

62 Subsection 250‑10(2) in Schedule 1 (after item 24C of the table)

Insert:

24D | returnable Government FHSA contributions | 43 | First Home Saver Accounts Act 2008 |

24E | returnable underpaid amounts in relation to Government FHSA contributions | 47 | First Home Saver Accounts Act 2008 |

63 Subsection 250‑10(2) in Schedule 1 (after table item 38B)

Insert:

38C | FHSA misuse tax | section 345‑110 | Income Tax Assessment Act 1997 |

64 After subsection 286‑75(2A) in Schedule 1

Insert:

(2B) You are also liable to an administrative penalty if:

(a) you are required under Division 391 to give a statement to an entity (other than the Commissioner) in the *approved form by a particular day; and

(b) you do not give the statement in the approved form to the entity by that day.

(2C) You are also liable to an administrative penalty if:

(a) you are required under section 20 of the First Home Saver Accounts Act 2008 to give a notice to an entity in the *approved form by a particular day; and

(b) you do not give the notice in the approved form to the entity by that day.

65 Paragraph 286‑80(2)(a) in Schedule 1

Omit “or (2A)”, substitute “, (2A), (2B) or (2C)”.

66 After Division 390 of Part 5‑25 of Schedule 1

Insert:

Division 391—First home saver account reporting

Table of Subdivisions

Guide to Division 391

391‑A Account activity statements

391‑B Transfer statements

391‑1 What this Division is about

FHSA providers must give the Commissioner information periodically about FHSAs (such as information about contributions made to FHSAs).

FHSA providers are also required to give information to other FHSA providers when making transfer payments from FHSAs to other FHSAs or to superannuation interests.

Subdivision 391‑A—Account activity statements

Table of sections

391‑5 FHSA account activity statements

391‑5 FHSA account activity statements

(1) An *FHSA provider must give the Commissioner the following statements under this section:

(a) a statement in relation to the amount of *personal FHSA contributions (if any) made to each *FHSA provided by the provider during the period mentioned in subsection (3) for that kind of statement;

(b) a statement in relation to the balance of an FHSA provided by the provider during the period mentioned in subsection (3) for that kind of statement;

(c) a statement in relation to each FHSA opened or issued (if any) by the provider during the period specified in subsection (3) for that kind of statement;

(d) a statement in relation to each FHSA closed (if any) by the provider during the period specified in subsection (3) for that kind of statement;

(e) a statement in relation to payments (other than a payment of a kind mentioned in subparagraph 31(1)(b)(iii) or paragraph (1)(f) or (g) of the First Home Saver Accounts Act 2008) (if any) made from each FHSA provided by the provider during the period specified in subsection (3) for that kind of statement.

Note: Section 286‑75 in Schedule 1 to the Taxation Administration Act 1953 provides an administrative penalty for breach of any of these paragraphs. A breach of any of these paragraphs may also be an offence under section 8C of that Act.

(2) However, the provider is not required to give a statement mentioned in paragraph (1)(a) if, during the period, the provider transferred the balance of the *FHSA to another FHSA.

(3) The period for a particular kind of statement under subsection (1) is:

(a) a financial year; or

(b) if the Commissioner determines another period under subsection (4) for the kind of statement—that period.

(4) The Commissioner may determine, by legislative instrument, a period mentioned in subsection (1) for a kind of statement.

(5) A statement under subsection (1) must be in the *approved form.

(6) A statement must be given to the Commissioner on or before a day specified in the determination under subsection (7) for the statement.

Note: Section 388‑55 allows the Commissioner to defer the time for giving an approved form.

(7) The Commissioner may determine, by legislative instrument, the day, on or before which, a statement under subsection (1) must be given to the Commissioner.

(8) The day specified in the determination may be different:

(a) for different kinds of *FHSA provider; and

(b) in relation to any other matter.

(9) Subsection (8) does not limit the way in which the determination may specify the day.

(10) The *approved form may require a statement to contain the following:

(a) the *tax file number of the *FHSA holder;

(b) the tax file number of the *FHSA provider.

(11) Subsection (10) does not limit the information that the *approved form may require a statement to contain.

Subdivision 391‑B—Transfer statements

Table of sections

391‑10 Statements about transfer payments between FHSAs etc.

391‑10 Statements about transfer payments between FHSAs etc.

(1) This section applies if an *FHSA provider (the first provider) in relation to an *FHSA (the first FHSA) makes a payment from the FHSA:

(a) to an FHSA provided by another FHSA provider, in accordance with section 35 of the First Home Saver Accounts Act 2008; or

(b) to a *superannuation provider in relation to a *complying superannuation plan, in accordance with section 22 or 34 of that Act.

(2) The first provider must:

(a) give the other *FHSA provider or *superannuation provider a statement in relation to the payment within 7 days after the day on which the payment is made; and

(b) give the individual for whose benefit the payment is made a statement in relation to the payment within 30 days after the day on which the payment is made.

Note: Section 286‑75 provides an administrative penalty for breach of this subsection.

(3) A statement under subsection (2) must be in the *approved form.

Note: Section 388‑55 allows the Commissioner to defer the time for giving an approved form.

(4) The *approved form may require the statement to contain the following information:

(a) information relating to *personal FHSA contributions made to the first FHSA;

(b) information relating to the FHSA holder, including whether the individual is in breach of the account balance cap and whether the condition in subparagraph 32(1)(c)(i) of the First Home Saver Accounts Act 2008 has been met in relation to the individual.

(5) Subsection (4) does not limit the information that the *approved form may require the statement to contain.

(6) The *approved form may require the statement to contain the *tax file number of:

(a) the first provider; and

(b) the *FHSA holder.

Schedule 2—Amendments relating to the Corporations Act

Australian Securities and Investments Commission Act 2001

1 At the end of subsection 12A(1)

Add:

; (h) the First Home Saver Accounts Act 2008.

2 After paragraph 12BAA(7)(g)

Insert:

(ga) an FHSA (first home saver account) within the meaning of the First Home Saver Accounts Act 2008;

3 Section 9

Insert:

FHSA product when used in a provision outside Chapter 7, has the same meaning as it has in Chapter 7.

4 Section 9 (after paragraph (h) of the definition of managed investment scheme)

Insert:

(ha) an FHSA trust, within the meaning of the First Home Saver Accounts Act 2008;

5 Section 761A (after paragraph (d) of the definition of basic deposit product)

Insert:

(da) the facility is not an FHSA product; and

6 Section 761A

Insert:

FHSA product means an FHSA (within the meaning of the First Home Saver Accounts Act 2008).

7 Subsection 761E(3) (after item 2 of the table)

Insert:

2A | FHSA product | the person becomes the holder (within the meaning of the First Home Saver Accounts Act 2008) of the FHSA product |

8 After paragraph 761E(3A)(b)

Insert:

(ba) the client making a further contribution (within the meaning of the First Home Saver Accounts Act 2008) into an FHSA product maintained in the client’s name;

9 After paragraph 764A(1)(h)

Insert:

(ha) an FHSA (short for first home saver account) within the meaning of the First Home Saver Accounts Act 2008;

10 After paragraph 766E(3)(ca)

Insert:

(cb) the operation of an FHSA trust (within the meaning of the First Home Saver Accounts Act 2008) by an FHSA provider (within the meaning of that Act);

11 After subsection 946AA(1)

Insert:

(1A) The providing entity does not have to give the client a Statement of Advice as mentioned in subsection (1) if:

(a) the advice relates to an FHSA product; and

(b) both subparagraphs (1)(a)(i) and (ii) apply.

12 Subsection 1016A(1) (after paragraph (d) of the definition of relevant financial product)

Insert:

(da) an FHSA product; or

13 After subparagraph 1017D(1)(b)(iii)

Insert:

(iiia) an FHSA product; or

14 After subparagraph 1019A(1)(a)(iii)

Insert:

(iiia) FHSA products;

Schedule 3—Other consequential amendments

Anti‑Money Laundering and Counter‑Terrorism Financing Act 2006

1 Section 5 (definition of contribution)

Omit “an RSA”, substitute “an FHSA or RSA”.

2 Section 5

Insert:

FHSA (short for first home saver account) has the same meaning as in the First Home Saver Accounts Act 2008.

3 Section 5

Insert:

FHSA provider (short for first home saver account provider) has the same meaning as in the First Home Saver Accounts Act 2008.

4 Subsection 6(2) (after table item 43)

Insert:

43A | in the capacity of FHSA provider, accepting a contribution, roll‑over or transfer to an FHSA in respect of a new or existing FHSA holder | the FHSA holder |

43B | in the capacity of FHSA provider, cashing the whole or a part of an interest held by an FHSA holder | the FHSA holder, or if the FHSA holder has died, the person, or each of the persons, who receives the cashed whole or a cashed part of the relevant interest |

Australian Prudential Regulation Authority Act 1998

5 Subsection 3(1) (after paragraph (f) of the definition of prudential regulation framework law)

Insert:

(fa) the First Home Saver Accounts Act 2008;

6 At the end of subsection 3(2)

Add:

; (h) an FHSA provider, within the meaning of the First Home Saver Accounts Act 2008.

7 Subsection 3(2) (note)

Omit “and RSA is short for retirement savings account”, substitute “, RSA is short for retirement savings account and FHSA is short for first home saver account”.

8 Subsection 56(1) (at the end of the definition of protected document)

Add:

; or (f) a document given or produced under, or for the purposes of, a provision of the First Home Saver Accounts Act 2008:

(i) administered by the Commissioner of Taxation; or

(ii) being applied for the purposes of the administration of a provision administered by the Commissioner of Taxation.

9 Subsection 56(1) (at the end of the definition of protected information)

Add:

; or (f) information given or produced under, or for the purposes of, a provision of the First Home Saver Accounts Act 2008:

(i) administered by the Commissioner of Taxation; or

(ii) being applied for the purposes of the administration of a provision administered by the Commissioner of Taxation.

10 Paragraph 11CA(1)(a)

Repeal the paragraph, substitute:

(a) the body corporate has contravened a provision of:

(i) this Act; or

(ii) the Financial Sector (Collection of Data) Act 2001; or

(iii) the First Home Saver Accounts Act 2008; or

11 Paragraph 11CA(1)(c)

Omit “or the Financial Sector (Collection of Data) Act 2001”, substitute “, the Financial Sector (Collection of Data) Act 2001 or the First Home Saver Accounts Act 2008”.

12 Paragraph 11CA(2)(aa)

Repeal the paragraph, substitute:

(aa) to comply with the whole or a part of:

(i) this Act; or

(ii) the Financial Sector (Collection of Data) Act 2001; or

(iii) the First Home Saver Accounts Act 2008;

13 At the end of section 18A

Add:

(5) For the purposes of this section, treat a reference in this section to a matter in relation to which APRA has a power or function under this Act as including a matter in relation to which APRA has a power or function under the First Home Saver Accounts Act 2008 in respect of ADIs.

14 Section 51A (definition of reviewable decision of APRA)

After “this Act”, insert “or the First Home Saver Accounts Act 2008”.

15 At the end of section 62A

Add:

(4) For the purposes of this section, treat a reference in this section to this Act as including a reference to the First Home Saver Accounts Act 2008.

16 Subparagraph 14(2)(a)(ii)

Omit “may be; and”, substitute “may be; or”.

17 At the end of paragraph 14(2)(a)

Add:

(iii) in accordance with section 31 of the First Home Saver Accounts Act 2008; and

18 Subparagraph 14(4)(b)(ii)

Omit “may be.”, substitute “may be; or”.

19 At the end of paragraph 14(4)(b)

Add:

(iii) in accordance with section 31 of the First Home Saver Accounts Act 2008.

20 Section 74

Before “In”, insert “(1)”.

21 At the end of section 74

Add:

(2) For the purposes of sections 88, 88A, 98 and 98A of this Part, treat a reference in those sections to this Act as including a reference to the First Home Saver Accounts Act 2008.

22 Section 126

Before “In”, insert “(1)”.

23 At the end of section 126

Add:

(2) For the purposes of this Part, treat a reference in this Part to this Act as including a reference to the First Home Saver Accounts Act 2008.

24 At the end of section 230A

Add:

(14) For the purposes of this Part, treat a reference in this section to this Act as including a reference to the First Home Saver Accounts Act 2008.

25 At the end of section 230B

Add:

(11) For the purposes of this Part, treat a reference in this section to this Act as including a reference to the First Home Saver Accounts Act 2008.

26 Subsection 236(1) (definition of reviewable decision)

Omit “subsection (1A)”, substitute “subsections (1A) and (1AA)”.

27 After subsection 236(1)

Insert:

(1AA) For the purposes of this section, treat a reference in this section to a reviewable decision as including a reference to a decision of the Regulator (within the meaning of the First Home Saver Accounts Act 2008) to which, under that Act, this section applies.

28 After paragraph 8(8)(b)

Insert:

(ba) any return on a person’s investment in an FHSA (within the meaning of the First Home Saver Accounts Act 2008);

29 Subsection 9(1) (at the end of the definition of financial investment)

Add:

; but does not include an investment in an FHSA (within the meaning of the First Home Saver Accounts Act 2008).

30 Subsection 9(1) (at the end of the definition of investment)

Add:

; or (c) in relation to an investment in an FHSA (within the meaning of the First Home Saver Accounts Act 2008)—has the meaning given by subsection (9B).

31 Subsection 9(1) (at the end of the definition of return)

Add:

; or (c) in relation to an investment in an FHSA (within the meaning of the First Home Saver Accounts Act 2008)—means any increase, whether of a capital or income nature and whether or not distributed, in the value or amount of the investment.

32 After paragraph 9(1C)(ca)

Insert:

(cb) an investment in an FHSA (within the meaning of the First Home Saver Accounts Act 2008);

33 After subsection 9(9A)

Insert:

(9B) For the purposes of this Act, a person has an investment in an FHSA (within the meaning of the First Home Saver Accounts Act 2008) if the person has benefits in the FHSA (whether the benefits are attributable to amounts paid by the person or someone else).

34 Subsection 10B(2) (after paragraph (c) of the definition of trust)

Insert:

(ca) an FHSA trust (within the meaning of the First Home Saver Accounts Act 2008); or

35 After paragraph 1118(1)(f)

Insert:

(fa) the value of the person’s investment in an FHSA (within the meaning of the First Home Saver Accounts Act 2008);

36 At the end of subsection 1207P(1)

Add:

; or (d) the trust is an FHSA trust (within the meaning of the First Home Saver Accounts Act 2008).

Superannuation (Government Co‑contribution for Low Income Earners) Act 2003

37 At the end of paragraph 7(1)(c)

Add:

; (v) a payment from an FHSA required under section 22 or 34 of the First Home Saver Accounts Act 2008;

(vi) a Government FHSA contribution (within the meaning of the First Home Saver Accounts Act 2008).

Superannuation Industry (Supervision) Act 1993

38 At the end of subsection 29G(2)

Add:

; (v) where the RSE licensee is an FHSA provider (within the meaning of the First Home Saver Accounts Act 2008)—circumstances exist as described in paragraph 107(2)(b), (c), (d), (e) or (f) of that Act.

Veterans’ Entitlements Act 1986

39 After paragraph 5H(8)(i)

Insert:

(ia) any return on a person’s investment in an FHSA (within the meaning of the First Home Saver Accounts Act 2008);

40 Subsection 5J(1) (at the end of the definition of financial investment)

Add:

; but does not include an investment in an FHSA (within the meaning of the First Home Saver Accounts Act 2008).

41 Subsection 5J(1) (at the end of the definition of investment)

Add:

; or (c) in relation to an investment in an FHSA (within the meaning of the First Home Saver Accounts Act 2008)—has the meaning given by subsection (6B).

42 Subsection 5J(1) (after paragraph (a) of the definition of return)

Insert:

(aa) in relation to an investment in an FHSA (within the meaning of the First Home Saver Accounts Act 2008)—means any increase, whether of a capital or income nature and whether or not distributed, in the value or amount of the investment; or

43 After paragraph 5J(1C)(ca)

Insert:

(cb) an investment in an FHSA (within the meaning of the First Home Saver Accounts Act 2008);

44 After subsection 5J(6A)

Insert:

(6B) For the purposes of this Act, a person has an investment in an FHSA (within the meaning of the First Home Saver Accounts Act 2008) if the person has benefits in the FHSA (whether the benefits are attributable to amounts paid by the person or someone else).

45 After paragraph 52(1)(f)

Insert:

(faa) the value of the person’s investment in an FHSA (within the meaning of the First Home Saver Accounts Act 2008);

46 At the end of subsection 52ZZB(1)

; or (d) the trust is an FHSA trust (within the meaning of the First Home Saver Accounts Act 2008).

Schedule 4—Amendments to change references to virtual PST assets etc.

1 Amendment of Acts

The specified provisions of the Acts listed in this Schedule are amended by omitting “virtual PST” and substituting “complying superannuation/FHSA”.

Income Tax Assessment Act 1936

2 Subparagraph 26AH(7)(ba)(i)

3 Section 102M (paragraph (b) of the definition of eligible policy)

4 Paragraph 519A(a)

5 Subsection 519B(1)

Note: The heading to subsection 519B(1) is altered by omitting “Virtual PST” and substituting “Complying superannuation/FHSA”.

6 Subparagraph 519B(3)(b)(i)

7 Subparagraph 519B(4)(b)(i)

Income Tax Assessment Act 1997

8 Paragraph 102‑3(2)(d)

9 Subsection 110‑36(3)

10 Subsection 114‑5(3)

11 Paragraph 115‑10(d)

12 Subparagraph 115‑100(b)(ii)

13 Subparagraph 115‑280(1)(a)(ii)

14 Subsection 118‑300(1) (table item 6)

15 Paragraph 118‑350(2)(b)

16 Paragraph 295‑100(2)(a)

17 Paragraph 320‑35(a)

18 Section 320‑45

19 Subsection 320‑55(1)

20 Paragraph 320‑55(2)(a)

21 Section 320‑65

22 Paragraph 320‑120(1)(a)

23 Subsections 320‑125(1), (2) and (3) (wherever occurring)

24 Paragraph 320‑137(2)(a) (wherever occurring)

25 Paragraph 320‑137(4)(b) (wherever occurring)

26 Subparagraphs 320‑137(4)(e)(ii) and (iii)

27 Subparagraphs 320‑141(1)(c)(i) and (ii)

28 Subparagraphs 320‑143(1)(c)(i) and (ii)

29 Subparagraphs 320‑143(2)(a)(i) and (ii)

30 Subsections 320‑170(1), (1A) and (2)

31 Paragraph 320‑170(3)(a)

32 Subsection 320‑170(5)

33 Paragraphs 320‑175(1)(a) and (b)

34 Subsection 320‑180(1) (first occurring)

35 Paragraph 320‑180(1)(a)

36 Paragraph 320‑180(2)(a)

37 Subsection 320‑180(3) (first occurring)

38 Paragraph 320‑180(3)(a)

39 Paragraph 320‑180(4)(a)

40 Subsection 320‑185(1) (first occurring)

41 Paragraph 320‑185(1)(a)

42 Subsection 320‑185(3) (last occurring)

43 Subsection 320‑190(1) (wherever occurring)

44 Paragraphs 320‑195(3)(a), (b) and (c) (wherever occurring)

45 Paragraphs 320‑195(4)(b) and (c) (wherever occurring)

46 Subsection 320‑315(1) (wherever occurring)

47 Paragraph 320‑320(2)(a)

48 Subparagraph 713‑510(1)(a)(i)

49 Paragraph 713‑510(1)(b)

50 Subparagraph 713‑510(2)(a)(i)

51 Paragraph 713‑510(2)(b)

52 Paragraph 713‑515(1)(a)

53 Subsection 713‑515(4)

54 Subsections 713‑520(2) and (6)

55 Section 713‑525 (note) (wherever occurring)

56 Subparagraph 713‑530(1)(b)(ii)

57 Paragraphs 713‑535(1)(c) and (2)(b)

58 Paragraph 713‑545(5)(b)

59 Subparagraph 713‑570(1)(c)(ii)

60 Paragraph 713‑575(2)(a)

61 Subsections 713‑580(3) and (7)

62 Section 713‑585 (note) (wherever occurring)

63 Subsection 995‑1(1) (paragraph (a) of the definition of ordinary investment policy)

Taxation Administration Act 1953

64 Paragraph 288‑70(2)(a) in Schedule 1

Note: The headings to subsections 288‑70(1) and (2) in Schedule 1 are altered by omitting “Virtual PST” and substituting “Complying superannuation/FHSA asset pool”.

Schedule 5—Amendments to change references to virtual PST

1 Amendment of Act

The specified provisions of the Act listed in this Schedule are amended by omitting “virtual PST” and substituting “complying superannuation/FHSA asset pool”.

Income Tax Assessment Act 1997

2 Section 109‑60 (table item 11)

3 Section 112‑97 (table item 21)

4 Paragraphs 320‑15(1)(da), (db) and (e) (wherever occurring)

5 Subsections 320‑87(1) and (2)

6 Paragraphs 320‑87(3)(a) and (b)

7 Paragraphs 320‑137(2)(b) and (c)

8 Paragraph 320‑170(7)(a)

9 Subparagraph 320‑170(7)(a)(ii)

10 Paragraph 320‑170(7)(b)

11 Subsection 320‑175(1)

12 Paragraph 320‑175(2)(a)

13 Subsection 320‑180(1) (last occurring)

14 Subsection 320‑180(3) (last occurring)

15 Subsection 320‑185(1) (last occurring)

16 Subsection 320‑185(2)

17 Subsection 320‑185(3) (first occurring)

18 Subsection 320‑185(4)

19 Subsections 320‑195(1) and (2)

20 Subparagraph 320‑195(3)(b)(ii)

21 Subsection 320‑195(3) (last occurring)

22 Paragraph 320‑195(4)(a)

23 Subsection 320‑195(4) (last occurring)

24 Paragraphs 320‑200(1)(a) and (b)

25 Subsection 320‑200(3)

26 Paragraph 713‑570(1)(b)

Schedule 6—Amendments to change references to complying superannuation class

1 Amendment of Acts

The specified provisions of the Acts listed in this Schedule are amended by omitting “complying superannuation class” and substituting “complying superannuation/FHSA class”.

Income Tax Assessment Act 1997

2 Subsection 4‑15(2) (note)

3 Section 320‑1

4 Subparagraph 320‑5(2)(c)(i)

5 Paragraph 320‑35(b)

6 Subsection 320‑125(3) (note)

7 Section 320‑130

8 Paragraphs 320‑131(1)(a) and (b)

9 Subsection 320‑133(2)

10 Paragraph 320‑137(1)(c)

11 Paragraph 320‑149(1)(b)

12 Subsection 320‑149(2) (examples 1 and 2)

13 Subparagraph 713‑530(1)(b)(i)

14 Paragraph 713‑535(2)(a)

15 Subparagraph 713‑570(1)(c)(i)

16 Subsection 995‑1(1) (paragraph (a) of the definition of tax loss) (note 3)

17 Paragraph 23A(b)

Taxation Administration Act 1953

18 Paragraph 45‑120(2A)(b) in Schedule 1

19 Subsection 45‑290(3) in Schedule 1

20 Subsection 45‑330(3) in Schedule 1 (method statement, steps 4, 5 and 6) (wherever occurring)

21 Subsection 45‑370(3) in Schedule 1 (method statement, step 2)

Schedule 7—Other amendments relating to changes of references to virtual PST etc.

Income Tax Assessment Act 1936

1 Subsection 124ZM(6) (definition of complying superannuation class of taxable income)

Repeal the definition.

2 Subsection 124ZM(6) (before the definition of venture capital franked part)

Insert:

complying superannuation/FHSA class of taxable income is the life assurance company’s complying superannuation/FHSA class of taxable income, within the meaning of subsection 995‑1(1) of the Income Tax Assessment Act 1997, for the year of income in which the distribution is made.

3 Section 470 (definition of virtual PST asset)

Repeal the definition.

4 Section 470

Insert:

complying superannuation/FHSA asset has the same meaning as in the Income Tax Assessment Act 1997.

5 Division 11A of Part XI (heading)

Repeal the heading, substitute:

Income Tax Assessment Act 1997

6 Subsection 210‑175(2) (definition of complying superannuation class of taxable income)

Repeal the definition.

7 Subsection 210‑175(2) (before the definition of tax offset to which the entity would otherwise be entitled)

Insert:

complying superannuation/FHSA class of taxable income means the *complying superannuation/FHSA class of taxable income of the company for the income year in which the *distribution is made.

8 Section 320‑45 (heading)

Repeal the heading, substitute:

9 Section 320‑55 (heading)

Repeal the heading, substitute:

10 Section 320‑87 (heading)

Repeal the heading, substitute:

320‑87 Deduction for assets transferred from or to complying superannuation/FHSA asset pool

11 Paragraph 320‑107(1)(b)

Omit “virtual PST life insurance policy”, substitute “complying superannuation/FHSA life insurance policy”.

12 Subsection 320‑107(3) (formula)

Repeal the formula, substitute:

13 Subsection 320‑107(3) (definition of complying superannuation class rate)

Repeal the definition.

14 Subsection 320‑107(3)

After “where:”, insert:

complying superannuation/FHSA class rate is the rate of tax imposed on the *complying superannuation/FHSA class of the company’s taxable income for the income year.

15 Section 320‑120 (heading)

Repeal the heading, substitute:

16 Section 320‑125 (heading)

Repeal the heading, substitute:

320‑125 Capital losses from complying superannuation/FHSA assets

17 Section 320‑137 (heading)

Repeal the heading, substitute:

320‑137 Taxable income—complying superannuation/FHSA class

18 Subsection 320‑137(1)

Omit “complying superannuation class”, substitute “complying superannuation/FHSA class”.

19 Section 320‑141 (heading)

Repeal the heading, substitute:

320‑141 Tax loss—complying superannuation/FHSA class

20 Subsection 320‑141(1) (heading)

Repeal the heading, substitute:

Working out a tax loss of the complying superannuation/FHSA class

21 Subsection 320‑141(1)

Omit “complying superannuation class”, substitute “complying superannuation/FHSA class”.

22 Subsection 320‑141(2) (heading)

Repeal the heading, substitute:

Deducting a tax loss of the complying superannuation/FHSA class

23 Subsection 320‑141(2)

Omit “complying superannuation class”, substitute “complying superannuation/FHSA class”.

24 Subdivision 320‑F (heading)

Repeal the heading, substitute:

Subdivision 320‑F—Complying superannuation/FHSA asset pool

25 Section 320‑165

Omit “virtual PST”, substitute “complying superannuation/FHSA asset pool”.

26 Section 320‑170 (heading)

Repeal the heading, substitute:

320‑170 Establishment of complying superannuation/FHSA asset pool

27 Subsection 320‑170(1) (note)

Repeal the note.

28 Subsection 320‑170(6)

Repeal the subsection, substitute:

(6) The assets from time to time segregated are together to be known as the complying superannuation/FHSA asset pool and each asset from time to time included among those assets is to be known as a complying superannuation/FHSA asset.

29 Section 320‑175 (heading)

Repeal the heading, substitute:

30 Subsection 320‑180(1) (heading)

Repeal the heading, substitute:

Transfer from the complying superannuation/FHSA asset pool

31 Subsection 320‑180(3) (heading)

Repeal the heading, substitute:

Transfer to the complying superannuation/FHSA asset pool

32 Section 320‑185 (heading)

Repeal the heading, substitute:

33 Section 320‑190 (heading)

Repeal the heading, substitute:

320‑190 Complying superannuation/FHSA liabilities

34 Subsection 320‑190(2)

Omit “virtual PST liabilities”, substitute “complying superannuation/FHSA liabilities”.

35 Section 320‑195 (heading)

Repeal the heading, substitute:

36 Section 320‑200 (heading)

Repeal the heading, substitute:

320‑200 Consequences of transfer of assets to or from complying superannuation/FHSA asset pool

37 Section 320‑315 (heading)

Repeal the heading, substitute:

320‑315 Complying superannuation/FHSA asset pool and segregated exempt assets

38 Section 713‑535 (heading)

Repeal the heading, substitute:

39 Subsection 713‑545(6) (formula)

Repeal the formula, substitute:

40 Subsection 713‑545(6) (definition of complying superannuation class tax rate)

Repeal the definition.

41 Subsection 713‑545(6) (before the definition of ordinary class tax rate)

Insert:

complying superannuation/FHSA class tax rate means the rate of tax in respect of the *complying superannuation/FHSA class of the taxable income of a *life insurance company for the income year in which the joining time occurs (see paragraph 23A(b) of the Income Tax Rates Act 1986).

42 Subsection 995‑1(1)

Insert:

complying superannuation/FHSA asset has the meaning given by subsection 320‑170(6).

43 Subsection 995‑1(1)

Insert:

complying superannuation/FHSA asset pool has the meaning given by subsection 320‑170(6).

44 Subsection 995‑1(1) (all the definitions of complying superannuation class)

Repeal the definitions.

45 Subsection 995‑1(1)

Insert:

complying superannuation/FHSA class:

(a) for a taxable income of a *life insurance company—has the meaning given by section 320‑137; or

(b) for a *tax loss of a *life insurance company—has the meaning given by section 320‑141.

46 Subsection 995‑1(1)

Insert:

complying superannuation/FHSA liabilities of a *life insurance company means liabilities of the company under *life insurance policies referred to in subsection 320‑190(1).

47 Subsection 995‑1(1)

Insert:

complying superannuation/FHSA life insurance policy means a *life insurance policy that:

(a) is held by:

(i) the trustee of a fund that is a *complying superannuation fund or a *complying approved deposit fund; or

(ii) the trustee of a *pooled superannuation trust; or

(b) is held by an individual and:

(i) provides for an *annuity that is not presently payable, if the annuity was purchased out of a *superannuation lump sum or an *employment termination payment; or

(ii) is so held in the benefit fund of a *friendly society, being a fund that is a regulated superannuation fund under the Superannuation Industry (Supervision) Act 1993; or

(c) is held by another *life insurance company and is a *complying superannuation/FHSA asset of that company; or

(d) is an *FHSA;

and is not an *excluded complying superannuation/FHSA life insurance policy.

48 Subsection 995‑1(1)

Insert:

excluded complying superannuation/FHSA life insurance policy means a *life insurance policy that:

(a) provides only for *superannuation death benefits, *disability superannuation benefits or temporary disability benefits of a kind referred to in paragraph 295‑460(c), that are not *participating benefits; or

(b) is an *exempt life insurance policy.

49 Subsection 995‑1(1) (definition of virtual pooled superannuation trust)

Repeal the definition.

50 Subsection 995‑1(1) (definition of virtual PST)

Repeal the definition.

51 Subsection 995‑1(1) (definition of virtual PST asset)

Repeal the definition.

52 Subsection 995‑1(1) (definition of virtual PST liabilities)

Repeal the definition.

53 Subsection 995‑1(1) (definition of virtual PST life insurance policy)

Repeal the definition.

54 Subsection 3(1) (definition of complying superannuation class)

Repeal the definition.

55 Subsection 3(1)

Insert:

complying superannuation/FHSA class of the taxable income of a life insurance company has the same meaning as in the Income Tax Assessment Act 1997.

Taxation Administration Act 1953

56 Subsection 45‑290(3) in Schedule 1 (note)

Repeal the note.

[Minister’s second reading speech made in—

House of Representatives on 28 May 2008

Senate on 16 June 2008]

(108/08)