Tax Laws Amendment (2008 Measures No. 4) Act 2008

No. 97, 2008

An Act to amend the law relating to taxation, and for related purposes

Tax Laws Amendment (2008 Measures No. 4) Act 2008

No. 97, 2008

An Act to amend the law relating to taxation, and for related purposes

Contents

2 Commencement

3 Schedule(s)

Schedule 1—Demutualisation of private health insurers

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Schedule 3—Minor amendments

Part 1—General amendments

A New Tax System (Goods and Services Tax) Act 1999

Fringe Benefits Tax Assessment Act 1986

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Income Tax (Deferred Interest Securities) (Tax File Number Withholding Tax) Act 1991

Income Tax (Transitional Provisions) Act 1997

Superannuation Guarantee (Administration) Act 1992

Taxation Administration Act 1953

Taxation (Interest on Overpayments and Early Payments) Act 1983

Tax Laws Amendment (2007 Measures No. 5) Act 2007

Part 2—Asterisking amendments

Income Tax Assessment Act 1997

Tax Laws Amendment (2008 Measures No. 4) Act 2008

No. 97, 2008

An Act to amend the law relating to taxation, and for related purposes

[Assented to 3 October 2008]

The Parliament of Australia enacts:

This Act may be cited as the Tax Laws Amendment (2008 Measures No. 4) Act 2008.

(1) Each provision of this Act specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information | ||

Column 1 | Column 2 | Column 3 |

Provision(s) | Commencement | Date/Details |

1. Sections 1 to 3 and anything in this Act not elsewhere covered by this table | The day on which this Act receives the Royal Assent. | 3 October 2008 |

2. Schedule 1 | The day on which this Act receives the Royal Assent. | 3 October 2008 |

3. Schedule 3, items 1 to 86 | The day on which this Act receives the Royal Assent. | 3 October 2008 |

4. Schedule 3, item 87 | The later of: (a) immediately after the start of the day on which this Act receives the Royal Assent; and (b) immediately after the commencement of the First Home Saver Accounts (Consequential Amendments) Act 2008. However, the provision(s) do not commence at all if the event mentioned in paragraph (b) does not occur. | 3 October 2008 (paragraph (a) applies) |

5. Schedule 3, items 88 to 189 | The day on which this Act receives the Royal Assent. | 3 October 2008 |

Note: This table relates only to the provisions of this Act as originally passed by both Houses of the Parliament and assented to. It will not be expanded to deal with provisions inserted in this Act after assent.

(2) Column 3 of the table contains additional information that is not part of this Act. Information in this column may be added to or edited in any published version of this Act.

Each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

Schedule 1—Demutualisation of private health insurers

Income Tax Assessment Act 1936

1 At the end of section 326‑1 in Schedule 2H

Add “and health insurers”.

Note: The heading to Schedule 2H is replaced by the heading “Demutualisation of mutual entities other than insurance companies and health insurers”.

2 After paragraph 326‑10(1)(b) in Schedule 2H

Insert:

(ba) is not an entity to which item 6.3 of the table in section 50‑30 of the Income Tax Assessment Act 1997 (about private health insurers) applies; and

Income Tax Assessment Act 1997

3 Section 11‑55 (after table item headed “bonds”)

Insert:

demutualisation of private health insurers |

|

market value of shares and rights at time of issue...... | 315‑310 |

payments received in exchange for cancellation or variation of interests under the demutualisation | 315‑310 |

4 Section 109‑60 (cell at table item 4A, column headed “In these circumstances”)

Repeal the cell, substitute:

CGT event happens to CGT asset in connection with the demutualisation of a mutual entity other than an insurance company or health insurer |

5 Section 109‑60 (at the end of the table)

Add:

13 | You are issued with a share or right under a demutualisation of a health insurer | the time the share or right is issued | sections 315‑80, 315‑210 and 315‑260 |

14 | You are transferred a share or right by a lost policy holders trust under a demutualisation of a health insurer | the time the share or right is issued | sections 315‑145, 315‑210 and 315‑260 |

6 Section 112‑97 (cell at table item 5A, column headed “In this situation”)

Repeal the cell, substitute:

CGT event happens to CGT asset in connection with the demutualisation of a mutual entity other than an insurance company or health insurer |

7 Section 112‑97 (at the end of the table)

Add:

29 | You are issued with an asset under a demutualisation of a health insurer | First element of cost base and reduced cost base | sections 315‑80, 315‑210 and 315‑260 |

30 | You are transferred an asset by a lost policy holders trust under a demutualisation of a health insurer | First element of cost base and reduced cost base | sections 315‑145, 315‑210 and 315‑260 |

8 At the end of section 118‑1

Add:

Note 3: There are also exemptions in Division 315 (about demutualisation of private health insurers).

9 At the end of subsection 126‑190

Add:

Note: This Subdivision does not apply to the demutualisation of a private health insurer: see section 315‑160.

10 After section 197‑35

Insert:

197‑37 Exclusion for transfers made in connection with demutualisations of private health insurers

(1) Subject to subsection (2), this Division does not apply to the transferred amount if:

(a) the amount is transferred in connection with a demutualisation of a company; and

(b) Division 315 (about demutualisations of private health insurers) applies to the demutualisation; and

(c) the company (the issuing company) to whose *share capital account the amount is transferred is either:

(i) the demutualising health insurer; or

(ii) the company mentioned in subparagraph 315‑85(1)(a)(iii) issuing shares that are assets covered by section 315‑85 (demutualisation assets).

(2) Subsection (1) does not stop this Division from applying to so much, if any, of the transferred amount as exceeds the sum of the amounts worked out under subsection (3) for each demutualisation asset that is a share issued:

(a) by the issuing company under the demutualisation; and

(b) to an entity that is either:

(i) covered by section 315‑90 (about participating policy holders); or

(ii) the trustee of a trust covered by Subdivision 315‑C (about the lost policy holders trust).

(3) The amount worked out under this subsection for a share is:

(a) the *market value of the share on the day it is issued; or

(b) if the share is in a company covered by subparagraph 315‑85(1)(a)(iii) that owns other assets in addition to the shares in the demutualising health insurer—worked out using the method statement in subsection 315‑210(2).

11 After Part 3‑30

Insert:

Part 3‑32—Co‑operatives and mutual entities

Division 315—Demutualisation of private health insurers

Table of Subdivisions

Guide to Division 315

315‑A Capital gains and losses connected with a demutualisation of a private health insurer to be disregarded

315‑B Cost base of certain shares and rights in private health insurers

315‑C Lost policy holders trust

315‑D Special cost base rules for certain shares and rights in holding companies

315‑E Special CGT rule for legal personal representatives and beneficiaries

315‑F Non‑CGT consequences of demutualisation

315‑1 What this Division is about

This Division sets out the taxation consequences of the demutualisation of private health insurers.

Policy holders, demutualising health insurers and certain other entities can disregard capital gains and losses arising under a demutualisation (see Subdivision 315‑A).

Shares and rights issued under the demutualisation are given a cost base based on the market value of the demutualising health insurer at the time of issue (see Subdivisions 315‑B and 315‑D).

Assets held by a lost policy holders trust are given roll‑over relief if transferred to the lost policy holder, or if the lost policy holder becomes absolutely entitled to them. Otherwise the trustee of the lost policy holders trust is taxed on any capital gains (see Subdivision 315‑C).

A legal personal representative can disregard capital gains and losses made when passing an asset to a beneficiary of a policy holder’s estate (see Subdivision 315‑E).

Shares, rights or cash received under a demutualisation are not assessable income and not exempt income (see Subdivision 315‑F).

Table of sections

Rules for policy holders

315‑5 Policy holders to disregard capital gains and losses related to demutualisation of private health insurer

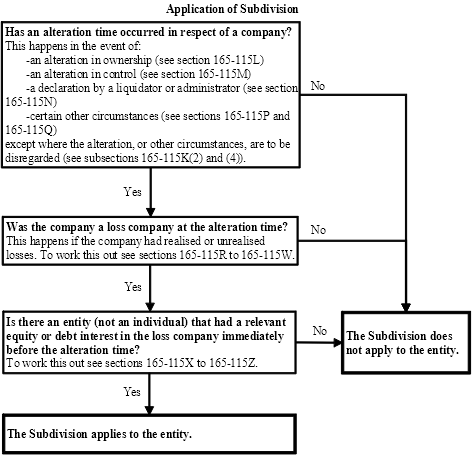

315‑10 Effect on the legal personal representative or beneficiary

315‑15 Demutualisations to which this Division applies

315‑20 What assets are covered

Rules for demutualising health insurer

315‑25 Demutualising health insurers to disregard capital gains and losses related to demutualisation

Rules for other entities

315‑30 Other entities to disregard capital gains and losses related to demutualisation

Disregard a *capital gain or *capital loss of an individual from a *CGT event that happens in relation to a *CGT asset if:

(a) the CGT event happens under a demutualisation to which this Division applies; and

(b) the individual is, or has been, a policy holder (within the meaning of the Private Health Insurance Act 2007) of, or another person insured through, the demutualising entity (the demutualising health insurer); and

(c) the CGT asset is covered by section 315‑20.

315‑10 Effect on the legal personal representative or beneficiary

Disregard a *capital gain or *capital loss of an entity from a *CGT event that happens in relation to a *CGT asset if:

(a) the CGT asset forms part of the estate of a deceased individual who is mentioned in paragraph 315‑5(b); and

(b) the entity is the deceased individual’s *legal personal representative or a beneficiary in the deceased individual’s estate; and

(c) the CGT asset devolves to the entity or *passes to the entity; and

(d) the CGT event happens under a demutualisation to which this Division applies; and

(e) the CGT asset is covered by section 315‑20.

315‑15 Demutualisations to which this Division applies

This Division applies to a demutualisation of an entity if:

(a) the entity:

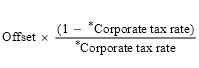

(i) is an entity to which item 6.3 of the table in section 50‑30 applies; and

(ii) is not registered under Part 3 of the Life Insurance Act 1995; and

(iii) does not have capital divided into shares; and

Note: Item 6.3 of the table in section 50‑30 applies to a private health insurer within the meaning of the Private Health Insurance Act 2007 that is not carried on for the profit or gain of its individual members.

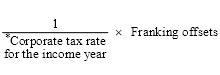

(b) an application by the entity to convert to being registered as a for profit insurer (within the meaning of the Private Health Insurance Act 2007) is approved under subsection 126‑42(5) of that Act; and

(c) consistently with the conversion scheme mentioned in paragraph 126‑42(2)(b) of that Act, the entity becomes registered as a for profit insurer (within the meaning of that Act).

315‑20 What assets are covered

These *CGT assets are covered:

(a) an interest in the demutualising health insurer as a policy holder;

(b) a membership interest in the demutualising health insurer;

(c) a right or interest of another kind in the demutualising health insurer;

(d) a right or interest of another kind that arises under the demutualisation.

Rules for demutualising health insurer

Disregard a *capital gain or *capital loss of an entity from a *CGT event if:

(a) the CGT event happened under a demutualisation to which this Division applies; and

(b) the entity is the demutualising health insurer.

315‑30 Other entities to disregard capital gains and losses related to demutualisation

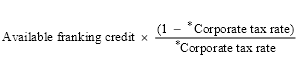

Disregard a *capital gain or *capital loss of an entity from a *CGT event if:

(a) the entity is established solely for the purpose of participating in a demutualisation to which this Division applies; and

(b) the entity is not a trust covered by Subdivision 315‑C (about lost policy holders); and

(c) the CGT event:

(i) happened under a demutualisation to which this Division applies; and

(ii) happened before or at the same time as the allocation or distribution (in the form of shares or cash) of the accumulated surplus of the demutualising health insurer; and

(iii) was connected to that allocation or distribution.

Note: The allocation or distribution of the accumulated surplus could happen through an arrangement involving more than one transaction.

Subdivision 315‑B—Cost base of certain shares and rights in private health insurers

Table of sections

315‑80 Cost base and acquisition time of demutualisation assets

315‑85 Demutualisation asset

315‑90 Participating policy holders

315‑80 Cost base and acquisition time of demutualisation assets

Cost base adjustment

(1) The first element of the *cost base and *reduced cost base of a *CGT asset is its *market value on the day it is issued if:

(a) the asset is covered by section 315‑85 (a demutualisation asset); and

(b) the asset is issued to an entity (a participating policy holder) covered by section 315‑90.

Note: There is an exception to this rule in Subdivision 315‑D where the asset is a share or right in a holding company with other assets.

Acquisition rule

(2) The participating policy holder is taken to have *acquired the demutualisation asset at the time it is issued.

(1) This section covers an asset if:

(a) the asset is:

(i) a share in the demutualising health insurer; or

(ii) a right to *acquire a share in the demutualising health insurer; or

(iii) a share in an entity that owns all of the shares in the demutualising health insurer; or

(iv) a right to acquire a share in an entity mentioned in subparagraph (iii); and

(b) the share or right is issued under a demutualisation to which this Division applies; and

(c) the share or right is issued in connection with:

(i) the variation or abrogation of rights attaching to or consisting of a *CGT asset covered by section 315‑20; or

(ii) the conversion, cancellation, extinguishment or redemption of such a CGT asset.

Exclusion for rights with an exercise price

(2) Despite subsection (1), this section does not cover a right to *acquire a share in an entity if the holder of the right must pay an amount to exercise the right.

Exclusion where assets not issued simultaneously

(3) Despite subsection (1), an asset is not covered by this section unless all of the assets covered by subsection (1) for the demutualisation in question are issued:

(a) at the same time; and

(b) to an entity that is either:

(i) a participating policy holder (see section 315‑90); or

(ii) the trustee of a trust covered by Subdivision 315‑C (about the lost policy holders trust).

315‑90 Participating policy holders

(1) This section covers an individual who:

(a) is, or has been, a policy holder (within the meaning of the Private Health Insurance Act 2007) of, or another person insured through, the demutualising health insurer; and

(b) is entitled, under the demutualisation, to an allocation of demutualisation assets.

(2) This section also covers an entity who became entitled to an allocation of demutualisation assets because of the death of an individual mentioned in subsection (1).

Subdivision 315‑C—Lost policy holders trust

Table of sections

315‑140 Lost policy holders trust

315‑145 CGT treatment of demutualisation assets in lost policy holders trust

315‑150 Roll‑over where assets transferred to lost policy holder

315‑155 Trustee assessed if assets dealt with not for benefit of lost policy holder

315‑160 Subdivision 126‑E does not apply to lost policy holders trust

315‑140 Lost policy holders trust

This Subdivision covers a trust (a lost policy holders trust) in relation to a demutualisation to which this Division applies if:

(a) the conversion scheme mentioned in paragraph 126‑42(2)(b) of the Private Health Insurance Act 2007 for the demutualisation provides for the trust; and

(b) under the demutualisation, demutualisation assets (see section 315‑85) are issued to the trustee of the trust; and

(c) the trust exists solely for the purpose of holding shares or rights to *acquire shares on behalf of:

(i) individuals (lost policy holders) who are, or have been, policy holders (within the meaning of the Private Health Insurance Act 2007) of, or other persons insured through, the demutualising health insurer; or

(ii) if the lost policy holder has died—the *legal personal representative of the lost policy holder or a beneficiary in the estate of the lost policy holder.

Example: An example of an individual on whose behalf the trust might hold assets would be an individual who has not completed a formal step required for them to be issued with demutualisation assets directly. Another example might be an individual living overseas.

315‑145 CGT treatment of demutualisation assets in lost policy holders trust

Cost base adjustment

(1) The first element of the *cost base and *reduced cost base of a demutualisation asset issued to the trustee of a lost policy holders trust is its *market value on the day it is issued.

Note: There is an exception to this rule in Subdivision 315‑D where the asset is a share or right in a holding company with other assets.

Acquisition rule

(2) The trustee is taken to have *acquired the demutualisation asset at the time it is issued.

315‑150 Roll‑over where assets transferred to lost policy holder

(1) This section applies in relation to a *CGT event if:

(a) the CGT event happens in relation to an asset held by the trustee of a lost policy holders trust on behalf of a lost policy holder; and

(b) the CGT event happens because the lost policy holder (or, if the lost policy holder has died, the *legal personal representative of the lost policy holder or a beneficiary in the estate of the lost policy holder) either:

(i) is transferred the asset by the trustee; or

(ii) becomes absolutely entitled to the asset.

Note: The asset may be a demutualisation asset, or some other asset.

Consequence for trustee

(2) Disregard a *capital gain or *capital loss the trustee makes from the *CGT event.

Consequence for lost policy holder

(3) The *cost base of the asset in the hands of the trustee of the lost policy holders trust just before the *CGT event becomes the first element of the cost base and *reduced cost base of the asset in the hands of the lost policy holder, *legal personal representative or beneficiary.

(4) The lost policy holder, *legal personal representative or beneficiary is taken to have *acquired the asset when the trustee of the lost policy holders trust acquired it.

315‑155 Trustee assessed if assets dealt with not for benefit of lost policy holder

(1) This section applies in relation to a *capital gain from a *CGT event if:

(a) the CGT event happens in relation to an asset held by the trustee of a lost policy holders trust; and

(b) section 315‑150 does not apply to the CGT event.

(2) If this section applies:

(a) for the purposes of sections 97, 98A and 100 of the Income Tax Assessment Act 1936, the share of the net income of the trust that is attributable to the *capital gain is taken not to be included in the assessable income of a beneficiary of the trust; and

(b) the trustee is not assessed, and is not liable to pay tax, in respect of the share under section 98 of the Income Tax Assessment Act 1936.

Note: Because of these consequences in relation to sections 97 and 98 of the Income Tax Assessment Act 1936, the trustee will be assessed on the beneficiary’s share under section 99A of that Act.

315‑160 Subdivision 126‑E does not apply to lost policy holders trust

Subdivision 126‑E does not apply in relation to a demutualisation to which this Division applies.

Subdivision 315‑D—Special cost base rules for certain shares and rights in holding companies

Table of sections

315‑210 Cost base for shares and rights in certain holding companies

315‑210 Cost base for shares and rights in certain holding companies

(1) This section applies in relation to a *CGT asset that is a demutualisation asset if:

(a) the demutualisation asset is:

(i) a share in an entity mentioned in subparagraph 315‑85(1)(a)(iii); or

(ii) a right to *acquire a share in an entity mentioned in that subparagraph; and

(b) the entity owns other assets in addition to the shares in the demutualising health insurer; and

(c) the share or right is issued to a participating policy holder or the trustee of a lost policy holders trust.

This section applies despite sections 315‑80 and 315‑145.

Cost base adjustment

(2) The first element of the *cost base and *reduced cost base of the *CGT asset is worked out under the method statement.

Method statement

Step 1. Start with the *market value of the demutualising health insurer on the day the asset is issued.

Step 2. Divide the result of step 1 by the sum of:

(a) the number of shares in the entity that are issued under the demutualisation; and

(b) the number of shares in the entity that can be *acquired under rights that are demutualisation assets issued under the demutualisation.

Step 3. The result of step 2 is the first element of the *cost base and *reduced cost base of the asset, unless the asset is a right.

Step 4. If the asset is a right, multiply the result of step 2 by the number of shares that can be *acquired under the right. The result is the first element of the *cost base and *reduced cost base of the asset.

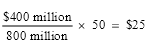

Example: Wellbeing Health demutualises on 1 April 2008 and has a market value of $400 million on that day. It distributes its accumulated mutual surplus in the form of rights to acquire shares in its holding company Healthiness Insurance Ltd (Healthiness). The rights do not have an exercise price.

A total of 800 million shares can be acquired in Healthiness under rights issued under the demutualisation. Each right allows the holder to acquire 50 shares. No shares in Healthiness are issued.

Under the method statement, the first element of the cost base and reduced cost base of each right is worked out by dividing the market value of Wellbeing Health (step 1) by the number of shares in Healthiness that can be acquired under the demutualisation (step 2) and multiplying the result by the number of shares that can be acquired under the right (step 4):

Acquisition rule

(3) The participating policy holder or trustee is taken to have *acquired the *CGT asset at the time it is issued.

Subdivision 315‑E—Special CGT rule for legal personal representatives and beneficiaries

Table of sections

315‑260 Special CGT rule for legal personal representatives and beneficiaries

315‑260 Special CGT rule for legal personal representatives and beneficiaries

(1) This section sets out what happens if a *CGT asset:

(a) is a demutualisation asset; and

(b) forms part of the estate of a participating policy holder mentioned in subsection 315‑90(1) who has died, but was not owned by the policy holder just before dying; and

(c) *passes to a beneficiary in the policy holder’s estate because the asset is transferred to the beneficiary by the policy holder’s *legal personal representative.

Note: Division 128 deals with the effect of death in relation to CGT assets a person owns just before dying.

(2) Disregard a *capital gain or *capital loss the *legal personal representative makes if the asset *passes to a beneficiary in the policy holder’s estate.

Consequence for beneficiary

(3) The *cost base and *reduced cost base of the asset in the hands of the *legal personal representative just before the asset *passes to the beneficiary becomes the first element of the cost base and reduced cost base of the asset in the hands of the beneficiary.

(4) The beneficiary is taken to have *acquired the asset when the *legal personal representative acquired it.

Subdivision 315‑F—Non‑CGT consequences of demutualisation

Table of sections

315‑310 General taxation consequences of issue of demutualisation assets etc.

315‑310 General taxation consequences of issue of demutualisation assets etc.

(1) An amount of *ordinary income or *statutory income of an entity to which subsection (2) applies is not assessable and not *exempt income if:

(a) the amount would otherwise be included in the ordinary income or statutory income of the entity only because a demutualisation asset was issued to the entity; or

(b) the amount is a payment made to the entity, under a demutualisation to which this Division applies, in connection with:

(i) the variation or abrogation of rights attaching to or consisting of a *CGT asset covered by section 315‑20; or

(ii) the conversion, cancellation, extinguishment or redemption of such a CGT asset.

(2) This subsection applies to an entity that:

(a) is, or has been, a policy holder (within the meaning of the Private Health Insurance Act 2007) of, or another person insured through, the demutualising health insurer; or

(b) is issued with the demutualisation asset, or receives the payment, because of the death of a policy holder mentioned in paragraph (a).

12 Application

The amendments made by this Schedule apply in relation to demutualisations occurring on and after 1 July 2007.

A New Tax System (Goods and Services Tax) Act 1999

1 At the end of section 87‑25

Add:

Note: If you choose not to apply this Division, your supplies (other than GST‑free supplies) of long‑term accommodation in commercial residential premises are input taxed under section 40‑35.

Fringe Benefits Tax Assessment Act 1986

2 Paragraph 135T(1)(a)

Repeal the paragraph, substitute:

(a) a department within the meaning of section 6 of the Public Sector Employment and Management Act 2002 of New South Wales;

3 Paragraph 135T(1)(h)

Repeal the paragraph, substitute:

(h) a government department within the meaning of subsection 3(1) of the State Service Act 2000 of Tasmania;

4 Application

The amendments made by items 2 and 3 of this Schedule apply to the first year of tax starting after the day on which this Act receives the Royal Assent and later years.

Income Tax Assessment Act 1936

5 Subsection 6(2)

Repeal the subsection.

6 Subsection 6(2AA)

Omit “(other than subsection (2) of this section)”.

7 Subsection 6(2A)

Repeal the subsection.

8 Subsection 16(4AA) (definition of research and development activities)

Repeal the definition.

9 Subsection 23E(3)

Omit “Commonwealth Inscribed Stock Act 1911‑1946”, substitute “Commonwealth Inscribed Stock Act 1911”.

10 Subsection 23L(1A)

Omit “section 15‑75”, substitute “section 15‑70”.

11 Application

The amendment made by item 10 of this Schedule applies to assessments for the 2006‑07 year of income and later income years.

12 Sub‑subparagraph 47A(18)(d)(ii)(G)

Omit “ultimate beneficiary non‑disclosure tax”, substitute “trustee beneficiary non‑disclosure tax”.

13 Paragraph 51AH(1)(c)

Omit “section 15‑75”, substitute “section 15‑70”.

14 Application

The amendment made by item 13 of this Schedule applies to assessments for the 2006‑07 year of income and later income years.

15 Subsection 73A(6) (definition of an approved research institute)

Omit “the Secretary to the Department of Community Services and Health or by the Secretary to the Department of Employment, Education and Training”, substitute “the Chief Executive Officer of the NHMRC or by the Research Secretary”.

16 Subsection 73A(6)

Insert:

NHMRC means the National Health and Medical Research Council established by section 5B of the National Health and Medical Research Council Act 1992.

17 Subsection 73A(6)

Insert:

Research Secretary means the Secretary of the Department that administers the Education Research Act 1970.

18 Transitional

The amendment made by item 15 of this Schedule does not affect the continuity of an approval given for the purposes of the definition of an approved research institute in subsection 73A(6) of the Income Tax Assessment Act 1936 before the commencement of this Schedule.

19 Subsection 102UC(4) (paragraph (b) of the definition of excluded trust)

Omit “the Australian Stock Exchange Limited”, substitute “the stock market operated by ASX Limited”.

20 Subsection 109Y(2) (paragraphs (a) and (b) of the definition of repayments of non‑commercial loans)

Omit “section, 109D”, substitute “section 109D”.

21 Section 121AQ (definition of first trading day price)

Omit “the price on the Australian stock exchange, as published by that exchange”, substitute “the price on the stock market operated by ASX Limited, as published by that company”.

22 Section 121AQ (definition of listed)

Omit “the Australian stock exchange”, substitute “ASX Limited”.

23 Paragraph 128B(3)(b)

Repeal the paragraph.

24 Section 139DSA

Omit “the Australian Stock Exchange”, substitute “the stock market operated by ASX Limited”.

25 Paragraph 139DSH(b)

Omit “the ASX Limited”, substitute “ASX Limited”.

26 Paragraph 139GCD(1)(d)

Omit “the ASX Limited”, substitute “ASX Limited”.

27 Subsection 159H(1)

Omit “(1)”.

28 Subsection 159H(2)

Repeal the subsection.

29 Subsection 159J(6) (paragraph (ac) of the definition of separate net income)

Omit “maternity allowance, maternity payment,”.

30 Subsection 159J(6) (paragraph (adaa) of the definition of separate net income)

Omit “or the Veterans’ Entitlements Act 1986”.

31 Subsection 159J(6) (paragraph (adab) of the definition of separate net income)

Repeal the paragraph.

32 Subsection 159J(6) (paragraph (adac) of the definition of separate net income)

Omit “or the Veterans’ Entitlements Act 1986”.

33 Subsection 159J(6) (paragraph (adad) of the definition of separate net income)

Repeal the paragraph.

34 Subsection 159J(6) (paragraph (ae) of the definition of separate net income)

Omit “maternity allowance,”.

35 Subsection 160AAA(1) (paragraph (db) of the definition of rebatable benefit)

Repeal the paragraph.

36 Paragraph 202EE(1)(d)

Omit “, (b)”.

37 Paragraph 251U(1)(d)

Repeal the paragraph, substitute:

(d) during the whole of that period the person was a non‑resident, or was a resident solely because subsection 7A(2) treats Norfolk Island as part of Australia;

38 Subsections 251U(1A) and (1B)

Repeal the subsections.

39 Paragraph 57‑25(4)(la) in Schedule 2D

Omit “property); and”, substitute “property).”.

40 Subsection 326‑15(1) in Schedule 2H

Omit “Australian Stock Exchange Limited”, substitute “ASX Limited”.

41 Subsection 326‑130(2) in Schedule 2H (definition of first day trading price of demutualisation shares)

Omit “Australian Stock Exchange Limited, at which the demutualisation shares were last traded, on the stock market maintained by Australian Stock Exchange Limited”, substitute “ASX Limited, at which the demutualisation shares were last traded, on the stock market operated by ASX Limited”.

42 Subsection 326‑220(4) in Schedule 2H (paragraph (a) of the definition of roll‑over provision)

Before “section 160X”, insert “former”.

43 Schedule 3

Omit “Australian Stock Exchange Limited ”, substitute “The stock market operated by ASX Limited”.

Income Tax Assessment Act 1997

44 After section 1‑3

Insert:

1‑7 Administration of this Act

The Commissioner has the general administration of this Act.

45 Paragraph 3‑10(1)(b)

Omit “returns”, substitute “income tax returns”.

46 Subsection 4‑10(1)

Repeal the subsection, substitute:

(1) You must pay income tax for each *financial year.

47 Section 9‑1 (table item 12)

Omit “section 102K”, substitute “section 102K”.

48 Section 9‑1 (table item 13)

Omit “section 102S”, substitute “section 102S”.

49 Section 11‑15 (table item headed “family assistance”)

Omit:

maternity allowance ........................ | 52‑150 |

50 Section 11‑15 (table item headed “family assistance”)

Omit:

maternity payment.......................... | 52‑150 |

51 Section 11‑15 (table item headed “foreign aspects of income taxation”)

Omit:

educational, scientific, religious or philanthropic society, income of a visiting representive of |

|

substitute:

educational, scientific, religious or philanthropic society, income of a visiting representative of |

|

52 Section 11‑15 (table item headed “foreign aspects of income taxation”)

Omit:

non‑resident, foreign sourced income ....... | 23(r) |

53 Section 11‑15 (table item headed “social security or like payments”)

Omit:

farm household support payment made by way of a grant of financial assistance . |

|

farm household support converted into a grant........ | 53‑25 |

54 Section 11‑15 (table item headed “social security or like payments”)

Omit:

2006 one‑off payment to older Australians under the Veterans’ Entitlements Act 1986 |

|

payments under the scheme determined under item 2 of Schedule 2 to the Social Security and Veterans’ Entitlements Legislation Amendment (One‑off Payments to Increase Assistance for Older Australians and Carers and Other Measures) Act 2006 |

|

55 Section 11‑15 (table item headed “social security or like payments”)

Omit:

2007 one‑off payment to older Australians under the Veterans’ Entitlements Act 1986 |

|

payments under the scheme determined under item 2 of Schedule 2 to the Social Security and Veterans’ Affairs Legislation Amendment (One‑off Payments and Other 2007 Budget Measures) Act 2007 |

|

56 Section 11‑15 (table item headed “social security or like payments”)

Omit:

social security, payment to .................... | Subdivision 52‑A |

substitute:

social security payments ...................... | Subdivision 52‑A |

57 Section 11‑15 (at the end of table item headed “social security or like payments”)

Add:

see also welfare |

|

58 Section 11‑15 (table item headed “vice‑regal”)

Repeal the item.

59 Section 11‑15 (table item headed “welfare”)

Repeal the item, substitute:

welfare |

|

maintenance payment........................ | 51‑30 and 51‑50 |

see also social security or like payments |

|

60 Section 13‑1 (table item headed “farm household support”)

Repeal the item.

61 Section 13‑1 (table item headed “social security and other benefit payments”)

Omit:

farm household support under the Farm Household Support Act 1992 |

|

62 Subsection 20‑30(1) (table item 1.8)

Before “25‑80”, insert “The former”.

63 Paragraph 27‑10(3)(a)

Omit “*registration”, substitute “registration under Part 2‑5 of the GST Act”.

64 Subsection 30‑230(1) (note)

Omit “tax return”, substitute “income tax return”.

65 Subsection 30‑230(6)

Repeal the subsection, substitute:

(6) If:

(a) you die before the last day of an income year; and

(b) section 26‑55 (which is about a limit on deductions) prevents the whole or a part of the gift from being deductible in the *income tax return lodged for you for that income year;

the trustee of your estate can claim the whole or part as a deduction in the trust’s income tax return for that income year.

Note: The trust’s income tax return covers the period from the day you die to the end of the income year.

66 Section 30‑255

Omit “Secretary to the Department of Environment, Sport and Territories”, substitute “*Environment Secretary”.

67 Subsection 30‑270(4)

Omit “Secretary to the Department of Environment, Sport and Territories”, substitute “*Environment Secretary”.

68 Subsection 30‑280(1)

Omit “Secretary to the Department of Environment, Sport and Territories”, substitute “*Environment Secretary”.

69 Subsection 30‑285(1)

Omit “Secretary to the Department of Environment, Sport and Territories”, substitute “*Environment Secretary”.

70 Section 51‑30 (table items 5.2 and 5.3)

Repeal the items.

71 Section 52‑10 (table items 7.1 and 7.2)

Repeal the items.

72 Section 52‑15 (table item 1)

Omit “Disability wage supplement”.

73 Subsection 52‑25(1) (table item dealing with disability wage supplement)

Repeal the item.

74 Section 52‑40 (table item 7)

Repeal the item.

75 Paragraphs 52‑65(1)(b) and (ba)

Repeal the paragraphs.

76 Subsection 52‑65(1B)

Repeal the subsection, substitute:

(1B) Payments of 2008 one‑off payment to older Australians under Part VIIF of the Veterans’ Entitlements Act 1986 are exempt from income tax.

77 Subsection 52‑65(1C)

Repeal the subsection, substitute:

(1C) Payments to older Australians under a scheme determined under item 2 of Schedule 2 to the Social Security and Veterans’ Entitlements Legislation Amendment (One‑off Payments and Other Budget Measures) Act 2008 are exempt from income tax.

78 Section 52‑75 (table items 1A and 1B)

Repeal the items.

79 Subsection 52‑150(1)

Omit “maternity allowance, maternity payment,”.

80 Section 53‑10 (table item 4A)

Repeal the item.

81 Subsection 53‑15(1)

Omit “(1)”.

82 Subsection 53‑15(2)

Repeal the subsection.

83 Section 53‑25

Repeal the section.

84 Paragraph 61‑405(a)

Omit “return”, substitute “*income tax return”.

85 Section 65‑10

Omit “years of income”, substitute “income years”.

86 Section 102‑20 (notes 3 and 4)

Repeal the notes, substitute:

Note 3: You may make a capital gain or capital loss as a result of a CGT event happening to another entity: see subsections 115‑215(3), 170‑275(1) and 170‑280(3).

Note 4: You cannot make a capital loss from a CGT event that happens to your original interests during a trust restructuring period if you choose a roll‑over under Subdivision 124‑N.

Note 5: The capital loss may be affected if the CGT asset was owned by a member of a demerger group just before a demerger: see section 125‑170.

87 Section 109‑60 (table)

Repeal the table, substitute:

Other acquisition rules | |||

|

| The asset is acquired at this time: |

|

1 | CGT event happens to Cocos (Keeling) Islands asset | 30 June 1991 | section 24P |

2 | Lender acquires a replacement security | before 20 September 1985 | subsection 26BC(6A) |

3 | Trust ceases to be a resident trust for CGT purposes and there is an attributable taxpayer | when it ceases | section |

4 | CGT event happens to CGT asset in connection with the demutualisation of an insurance company | on the demutualisation resolution day | section 121AS |

5 | CGT event happens to assets of NSW State Bank | at the first taxing time | section 121EN |

6 | You own shares in a company that stops being a PDF | just after it stops | section 124ZR |

7 | You acquire a number of shares that results in you obtaining a 10% (threshold) interest in a SME | when you obtained the threshold interest | section 128TI |

8 | A CGT asset of a CFC (that it owned on its commencing day) | on the CFC’s commencing day | section 411 |

9 | A CGT asset is owned by a tax exempt entity and it becomes taxable | at the transition time | section 57‑25 of Schedule 2D |

10 | CGT event happens to CGT asset in connection with the demutualisation of a mutual entity other than an insurance company or health insurer | on the demutualisation resolution day | Division 326 of Schedule 2H |

11 | You stop holding an item as trading stock | when you stop | paragraph 70‑110(b) |

12 | CGT event happens to 30 June 1988 asset of complying superannuation fund, complying approved deposit fund or pooled superannuation trust | 30 June 1988 | section 295‑90 |

13 | You are issued with a share or right under a demutualisation of a health insurer | the time the share or right is issued | sections 315‑80, 315‑210 and 315‑260 |

14 | You are transferred a share or right by a lost policy holders trust under a demutualisation of a health insurer | the time the share or right is issued | sections 315‑145, 315‑210 and 315‑260 |

15 | A CGT asset is transferred to or from a life insurance company’s complying superannuation/FHSA asset pool | at the time of the transfer | Division 320 |

16 | A CGT asset is transferred to or from the segregated exempt assets of a life insurance company | at the time of the transfer | Division 320 |

17 | Entity becomes a subsidiary member of a consolidated group | at the time it becomes a subsidiary member | 701‑5 |

18 | Entity ceases to be a subsidiary member of a consolidated group | at the time it ceases | 701‑40 |

88 Subsection 110‑40(1) (notes)

Repeal the notes, substitute:

Note: For the cost base of a partnership interest you acquire at or before that time, see section 110‑43.

89 Subsection 110‑43(1) (note)

Repeal the note.

90 Section 110‑53 (heading)

Repeal the heading, substitute:

110‑53 Exceptions to application of sections 110‑45 and 110‑50

91 Section 112‑87 (table item 1)

Omit “136‑40”, substitute “855‑45”.

92 Section 112‑87 (table item 2)

Omit “136‑45”, substitute “855‑50”.

93 Section 112‑97 (after table item 23)

Insert:

24 | An entity becomes a subsidiary member of a consolidated group | The total cost base and reduced cost base for the head company of the subsidiary’s assets | Section 701‑10 |

24A | An entity ceases to be a subsidiary member of a consolidated group | The total cost base and reduced cost base for the head company of membership interests in the subsidiary | Section 701‑15 |

24B | An entity ceases to be a subsidiary member of a consolidated group | The total cost base and reduced cost base for the head company of liabilities owed by the subsidiary | Section 701‑20 |

24C | An entity ceases to be a subsidiary member of a consolidated group and an asset becomes an asset of the entity because the single entity rule ceases to apply | The total cost base and reduced cost base for the entity of a liability owed to the entity | Section 701‑45 |

24D | 2 or more entities cease to be subsidiary members of a consolidated group | The total cost base and reduced cost base of the membership interests that one subsidiary member holds in another | Section 701‑50 |

24E | Determining an asset’s tax cost setting amount | The total cost base and reduced cost base of the asset | Section 701‑55 |

24F | Eligible tier‑1 company ceases to be a subsidiary member of a MEC group or a CGT event happens to a pooled interest in the company | The total cost base and reduced cost base | Section 719‑565 |

94 Section 112‑110 (note 3)

Omit “section 125‑175”, substitute “section 125‑170”.

95 Section 112‑115 (table item 6)

Omit “Subdivision 124‑CD”, substitute “Subdivision 124‑D”.

96 Section 112‑145 (note 2)

Omit “section 125‑175”, substitute “section 125‑170”.

97 Subsection 115‑280(3) (formula)

Repeal the formula, substitute:

98 Paragraph 115‑290(1)(b)

Omit “the Australian Stock Exchange Limited”, substitute “ASX Limited”.

99 Subsection 122‑70(2) (note 2)

Omit “section 125‑175”, substitute “section 125‑170”.

100 Subsection 122‑200(1) (note 2)

Omit “section 125‑175”, substitute “section 125‑170”.

101 Subsection 124‑10(3) (note 5)

Omit “section 125‑175”, substitute “section 125‑170”.

102 Subsection 124‑780(1) (note 2)

Omit “includes”, substitute “include”.

103 Subsection 124‑780(6) (note)

Omit “the Australian Stock Exchange”, substitute “the stock market operated by ASX Limited”.

104 Subsection 124‑781(1) (note 2)

Omit “includes”, substitute “include”.

105 Subsection 124‑781(5) (note)

Omit “the Australian Stock Exchange”, substitute “the stock market operated by ASX Limited”.

106 Subsection 124‑790(1)

Omit “includes”, substitute “include”.

107 Before subsection 125‑80(8)

Insert:

Partial roll‑over

108 Subsection 126‑15(4) (note)

Omit “section 125‑175”, substitute “section 125‑170”.

109 Subsection 126‑60(2) (note 2)

Omit “section 125‑175”, substitute “section 125‑170”.

110 Subsection 128‑15(1) (note)

Repeal the note, substitute:

Note 1: Section 128‑25 has different rules if the asset passes to a beneficiary in your estate who is the trustee of a complying superannuation entity.

Note 2: If the beneficiary is an exempt entity, Division 57 of Schedule 2D to the Income Tax Assessment Act 1936 has rules about exempt entities that become taxable. It sets out what the entity is taken to have purchased its assets for when it becomes taxable.

Note 3: If the beneficiary is a foreign resident, Subdivision 855‑B sets out what happens if the beneficiary becomes an Australian resident. The beneficiary is taken to have acquired each asset owned just before becoming an Australian resident for the market value of the asset at that time.

111 Subsection 128‑25(2) (notes 1 and 2)

Repeal the notes.

112 Subsection 130‑80(4) (note)

Omit “Note:”, substitute “Note 1:”.

113 Subsection 130‑83(4) (note)

Omit “Note 1”, substitute “Note”.

114 Paragraph 152‑310(2)(a)

Omit “*exempt income of”, substitute “exempt from income tax for”.

115 Section 165‑37 (heading)

Repeal the heading, substitute:

165‑37 Who has more than a 50% stake in the company during a period

116 Subsection 165‑37(1)

Omit “more than a 50% stake”, substitute “more than a 50% stake”.

117 Subsection 165‑55(6)

Omit “*full year deduction”, substitute “full year deduction”.

118 Subsection 165‑115H(2) (flowchart)

Repeal the flowchart, substitute:

119 Subsection 165‑235(2)

Omit “return of income”, substitute “*income tax return”.

120 Subsection 180‑5(2)

Omit “return of income”, substitute “*income tax return”.

121 Subsection 180‑10(7)

Omit “the company’s return”, substitute “the company’s *income tax return”.

122 Subsection 180‑20(5)

Omit “the company’s return”, substitute “the company’s *income tax return”.

123 Paragraph 208‑45(4)(b)

Omit “year of income”, substitute “income year”.

124 Paragraph 210‑115(2)(a)

Omit “return of income”, substitute “*income tax return”.

125 Subsection 214‑5(5)

Omit “first return”, substitute “first franking return”.

126 Subsection 214‑20(3)

Omit “a return under section 214‑15”, substitute “a *franking return”.

127 Section 214‑55

Omit “first return”, substitute “first franking return”.

128 Paragraph 214‑105(1)(b)

Omit “a further return”, substitute “a further *franking return”.

129 Section 214‑185

Omit “return given”, substitute “*franking return given”.

130 Subparagraph 250‑15(c)(iii)

Omit “that is not an Australian resident”, substitute “that is a foreign resident”.

131 Paragraph 250‑55(b)

Omit “that is not an Australian resident”, substitute “that is a foreign resident”.

132 Subparagraph 250‑60(2)(b)(ii)

Omit “(non‑resident)”, substitute “(foreign resident)”.

133 Subparagraph 250‑60(4)(b)(iii)

Omit “that is not an Australian resident”, substitute “that is a foreign resident”.

134 Paragraph 250‑115(3)(b)

Omit “non‑residents”, substitute “foreign residents”.

135 Subsection 292‑20(2)

Omit “Note:”, substitute “Note 1:”.

136 Subparagraphs 292‑100(2)(b)(i) and (7)(b)(i)

Omit “tax return”, substitute “*income tax return”.

137 Paragraph 320‑30(2)(a)

Omit “return of income”, substitute “*income tax return”.

138 Subsections 375‑805(3) and (5)

Omit “year of income”, substitute “income year”.

139 Subsection 396‑15(2) (formula)

Repeal the formula, substitute:

140 Subsection 396‑25(1) (formula)

Repeal the formula, substitute:

141 Subsection 703‑15(2) (table items 1 and 2)

Omit “*general company tax rate”, substitute “*corporate tax rate”.

142 Paragraph 705‑65(5A)(d)

Omit “*general company tax rate”, substitute “*corporate tax rate”.

143 Subsection 705‑75(1) (formula)

Repeal the formula, substitute:

144 Paragraph 705‑75(5)(d)

Omit “*general company tax rate”, substitute “*corporate tax rate”.

145 Subsection 705‑110(1)

Omit “*general company tax rate”, substitute “*corporate tax rate”.

146 Subsection 707‑310(3) (at the end of the table)

Add:

6 Assessable income that is not attributable to *capital gains and is not *assessable film income | The amount (if any) that would have been the transferee’s taxable income (if any) for the income year if the transferee had not had for the income year: (a) any *net capital gain; or (b) any *net assessable film income; reduced by the amount (the transferee’s grossed‑up franking offset amount) worked out in accordance with paragraph (3A)(c) |

147 Application

The amendment made by item 146 of this Schedule applies in relation to income years, statutory accounting periods and notional accounting periods starting on or after 1 July 2008.

148 Paragraph 707‑310(3A)(c) (formula)

Repeal the formula, substitute:

149 Subsection 717‑230(3)

Omit “year of income”, substitute “income year”.

150 Subsection 717‑265(4)

Omit “year of income”, substitute “income year”.

151 Subsection 719‑10(1) (table)

Omit “*general company tax rate”, substitute “*corporate tax rate”.

152 Subsection 719‑20(1) (table item 2)

Omit “*general company tax rate”, substitute “*corporate tax rate”.

153 At the end of subsection 770‑15(1)

Add:

Note: Foreign income tax includes only that which has been correctly imposed in accordance with the relevant foreign law or, where the foreign jurisdiction has a tax treaty with Australia (having the force of law under the International Tax Agreements Act 1953), has been correctly imposed in accordance with that tax treaty.

154 Subparagraph 770‑75(4)(b)(ii)

Repeal the subparagraph, substitute:

(ii) are deductions (other than debt deductions) that are reasonably related to amounts covered by paragraph (a) for that year.

155 Application

The amendment made by item 154 of this Schedule applies in relation to income years, statutory accounting periods and notional accounting periods starting on or after 1 July 2008.

156 Paragraph 802‑30(4)(c) (formula)

Repeal the formula, substitute:

157 Section 802‑40 (formula)

Repeal the formula, substitute:

158 Paragraph 820‑960(2)(a)

Omit “tax return”, substitute “*income tax return”.

159 Subsection 960‑120(1) (table item 2)

Omit “a year of income”, substitute “an income year”.

160 Paragraph 974‑10(5)(e)

Omit “subsection 974‑150(2)”, substitute “subsection 974‑150(1)”.

161 Subparagraph 974‑110(1A)(d)(i)

Omit “return of income”, substitute “*income tax return”.

162 Subparagraph 974‑110(1A)(d)(ii)

Omit “return of income”, substitute “income tax return”.

163 Paragraph 974‑112(1)(e)

Omit “subsection 974‑150(2)”, substitute “subsection 974‑150(1)”.

164 Subsection 974‑150(1)

Repeal the subsection.

165 Subsections 974‑150(2), (3) and (4)

Renumber as subsections 974‑150(1), (2) and (3).

166 Subsection 995‑1(1) (subparagraph (b)(i) of the definition of copyright collecting society)

Omit “a law in force in a State or Territory”, substitute “an *Australian law”.

167 Subsection 995‑1(1) (paragraphs (b), (c) and (d) of the definition of friendly society)

Omit “a law of a State or Territory”, substitute “a *State law or a *Territory law”.

168 Subsection 995‑1(1) (definition of full year deductions)

Omit “subsection 165‑55(5)”, substitute “subsections 165‑55(5) and (6)”.

169 Subsection 995‑1(1) (definition of general company tax rate)

Repeal the definition.

170 Subsection 995‑1(1) (definition of registration)

Repeal the definition.

171 Subsection 995‑1(1) (at the end of the definition of scheme)

Add:

Note: The Commissioner may determine that, for the purposes of the debt and equity interest rules in Division 974, what would otherwise be a single scheme is to be treated as 2 or more separate schemes, and that the schemes are not related: see section 974‑150.

172 Subsection 995‑1(1)

Omit:

short‑term hire agreement: a short‑term hire agreement is an agreement for the intermittent hire of an asset on an hourly, daily, weekly or monthly basis. However, an agreement for the hire of an asset is not a short‑term hire agreement if, having regard to any other agreements for the hire of the same asset to the same taxpayer or an *associate of that taxpayer, there is a substantial continuity of hiring so that the agreements together are for longer than a short‑term basis.

173 Subsection 995‑1(1) (definition of supplementary amount, table item 2)

Omit “or farm household support”.

Income Tax (Deferred Interest Securities) (Tax File Number Withholding Tax) Act 1991

174 Section 4

Omit “section section 14‑55”, substitute “section 14‑55”.

Income Tax (Transitional Provisions) Act 1997

175 After section 1‑5

Insert:

1‑7 Administration of this Act

The Commissioner has the general administration of this Act.

Superannuation Guarantee (Administration) Act 1992

176 Subparagraph 35(1)(d)(iv)

Omit “next quarter.”, substitute “next quarter; and”.

Taxation Administration Act 1953

177 Subsection 8AAB(5) (table item 2B)

Omit “section”.

178 Subsection 8AAB(5) (table item 17K) (table item dealing with section 263‑30 in Schedule 1)

Repeal the item.

179 Subsection 8AAB(5) (before table item 18)

Insert:

17L | 263‑30 in Schedule 1 | Taxation Administration Act 1953 |

180 Section 14ZQ (definition of private ruling)

Omit “section”.

181 Subsection 110‑50(2) in Schedule 1 (table items 3 to 7, 42 to 47, 50 and 54)

Omit “*registration”, substitute “registration”.

182 Subsection 250‑10(2) in Schedule 1 (table items 38A, 38B and 67)

Omit “section”.

183 Subsection 284‑220(1) in Schedule 1

Omit “The *base penalty amount for your *shortfall amount, or for part of it, for an accounting period is increased by 20% if”, substitute “The *base penalty amount for an accounting period is increased by 20% if”.

184 Paragraph 284‑220(1)(a) in Schedule 1

Omit “the shortfall amount”, substitute “a *shortfall amount in relation to which the base penalty amount was calculated”.

185 Paragraph 284‑220(1)(b) in Schedule 1

Omit “the shortfall amount or part”, substitute “such a shortfall amount”.

Taxation (Interest on Overpayments and Early Payments) Act 1983

186 Subsection 3A(2)

Omit “, or the applying of an income tax crediting amount also takes place,”.

Tax Laws Amendment (2007 Measures No. 5) Act 2007

187 Item 40 of Schedule 10

Omit “124KA(2)”, substitute “124K(2)”.

188 Item 56 of Schedule 10

Repeal the item, substitute:

56 Subsection 272‑140(1) in Schedule 2F (note to the definition of tax loss)

Repeal the note.

Income Tax Assessment Act 1997

189 Amendments relating to asterisking

The provisions of the Income Tax Assessment Act 1997 listed in the table are amended as set out in the table.

Asterisking amendments | |||

Item | Provision | Omit: | Substitute: |

1 | Subsection 30‑15(2) (table item 1, column headed “Type of gift or contribution”) | *trading stock if | trading stock if |

2 | Subsection 30‑15(2) (table item 1, column headed “How much you can deduct”) | *trading stock (wherever occurring) | trading stock |

3 | Subsection 30‑15(2) (table item 1, column headed “How much you can deduct”) | *business | business |

4 | Subsection 30‑15(2) (table item 2, column headed “Type of gift or contribution”) | *trading stock if | trading stock if |

5 | Subsection 30‑15(2) (table item 2, column headed “How much you can deduct”) | *trading stock (wherever occurring) | trading stock |

6 | Subsection 30‑15(2) (table item 2, column headed “How much you can deduct”) | *business | business |

7 | Subsection 30‑15(2) (table item 2, column headed “Special conditions”) | *prescribed private fund | prescribed private fund |

8 | Subsection 30‑15(2) (table item 8, column headed “How much you can deduct”) | *GST inclusive market value | GST inclusive market value |

9 | Paragraph 58‑65(3)(a) | income tax return | *income tax return |

10 | Subsection 104‑10(4) | those *capital proceeds | those capital proceeds |

11 | Subsection 104‑15(3) | those *capital proceeds | those capital proceeds |

12 | Subsection 104‑20(3) | those *capital proceeds | those capital proceeds |

13 | Subsection 104‑25(3) | those *capital proceeds | those capital proceeds |

14 | Subsection 104‑30(3) | those *capital proceeds | those capital proceeds |

15 | Subsection 104‑35(3) | those *capital proceeds | those capital proceeds |

16 | Subsection 104‑40(3) | those *capital proceeds | those capital proceeds |

17 | Subsection 104‑45(3) | those *capital proceeds | those capital proceeds |

18 | Subsection 104‑55(3) | those *capital proceeds | those capital proceeds |

19 | Subsection 104‑60(3) | those *capital proceeds | those capital proceeds |

20 | Subsection 104‑110(3) | those *capital proceeds | those capital proceeds |

21 | Subsection 104‑115(3) | those *capital proceeds | those capital proceeds |

22 | Subsection 104‑130(3) | those *capital proceeds | those capital proceeds |

23 | Subsection 104‑155(3) | those *capital proceeds | those capital proceeds |

24 | Subsection 116‑45(1) | The *capital proceeds are | The capital proceeds are |

25 | Subsection 116‑50(1) | *capital proceeds are not | capital proceeds are not |

26 | Subsection 124‑782(4) | arrangement | *arrangement |

27 | Subsections 149‑15(4) and (5) | *ultimate owner) | ultimate owner) |

28 | Paragraph 165‑115A(1C)(a) | income tax return | *income tax return |

29 | Paragraph 165‑115E(4)(a) | income tax return | *income tax return |

30 | Paragraph 165‑115U(1D)(a) | income tax return | *income tax return |

31 | Subparagraph 166‑3(2)(b)(ii) | *voting stakes, *dividend stakes and *capital stakes | voting stakes, dividend stakes and capital stakes |

32 | Section 214‑185 | income tax return | *income tax return |

33 | Paragraph 240‑20(2)(b) | *arrangement | arrangement |

[Minister’s second reading speech made in—

House of Representatives on 26 June 2008

Senate on 1 September 2008]

(141/08)