Tax Laws Amendment (2009 Measures No. 4) Act 2009

No. 88, 2009

An Act to amend the law relating to taxation, and for related purposes

Tax Laws Amendment (2009 Measures No. 4) Act 2009

No. 88, 2009

An Act to amend the law relating to taxation, and for related purposes

Contents

2 Commencement

3 Schedule(s)

4 Amendment of assessments

Schedule 1—Research and development

Income Tax Assessment Act 1936

Schedule 2—Private ancillary funds

Part 1—Amendments commencing on 1 October 2009

A New Tax System (Australian Business Number) Act 1999

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Part 2—Amendments commencing on 1 January 2010

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Part 3—Transitional provisions

Division 1—Preliminary

Division 2—Declared prescribed private funds

Division 3—Transitional private ancillary funds

Schedule 3—Demutualisation of friendly society health or life insurers

Part 1—Main amendment

Income Tax Assessment Act 1997

Part 2—Related amendments

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Schedule 4—Consolidation: application of losses with nil available fraction

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Schedule 5—Minor amendments

Part 1—References to Ministers, Departments and Secretaries

Division 1—Amendments commencing on Royal Assent

Excise Act 1901

Excise Tariff Act 1921

Fringe Benefits Tax (Application to the Commonwealth) Act 1986

Fringe Benefits Tax Assessment Act 1986

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Petroleum Resource Rent Tax Assessment Act 1987

Superannuation Contributions Tax (Application to the Commonwealth) Act 1997

Taxation Administration Act 1953

Division 2—Other amendments

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Part 2—Repeal of Part IV of the Taxation Administration Act 1953

Administrative Decisions (Judicial Review) Act 1977

Banking Act 1959

Taxation Administration Act 1953

Part 3—Amendments relating to foreign income tax offsets and foreign losses

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Part 4—Other amendments

A New Tax System (Australian Business Number) Act 1999

Fringe Benefits Tax Assessment Act 1986

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

International Tax Agreements Act 1953

Tax Laws Amendment (2007 Measures No. 5) Act 2007

Part 5—Transitional provision

Tax Laws Amendment (2009 Measures No. 4) Act 2009

No. 88, 2009

An Act to amend the law relating to taxation, and for related purposes

[Assented to 18 September 2009]

The Parliament of Australia enacts:

This Act may be cited as the Tax Laws Amendment (2009 Measures No. 4) Act 2009.

(1) Each provision of this Act specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information | ||

Column 1 | Column 2 | Column 3 |

Provision(s) | Commencement | Date/Details |

1. Sections 1 to 3 and anything in this Act not elsewhere covered by this table | The day on which this Act receives the Royal Assent. | 18 September 2009 |

2. Schedule 1 | The day on which this Act receives the Royal Assent. | 18 September 2009 |

3. Schedule 2, Part 1 | 1 October 2009. | 1 October 2009 |

4. Schedule 2, Part 2 | 1 January 2010. | 1 January 2010 |

5. Schedule 2, Part 3 | 1 October 2009. | 1 October 2009 |

6. Schedules 3 and 4 | The day on which this Act receives the Royal Assent. | 18 September 2009 |

7. Schedule 5, Part 1, Division 1 | The day on which this Act receives the Royal Assent. | 18 September 2009 |

8. Schedule 5, items 237 and 238 | The later of: (a) immediately after the start of the day on which this Act receives the Royal Assent; and (b) the time item 1 of Schedule 1 to the Nation Building Program (National Land Transport) Amendment Act 2009 commences. However, the provision(s) covered by this table item do not commence at all if the event mentioned in paragraph (b) does not occur. | 18 September 2009 |

9. Schedule 5, items 239 to 243 | The later of: (a) the start of the day on which this Act receives the Royal Assent; and (b) immediately after the commencement of item 1 of Schedule 2 to the Migration Legislation Amendment (Worker Protection) Act 2008. | 18 September 2009 |

10. Schedule 5, Parts 2 to 5 | The day on which this Act receives the Royal Assent. | 18 September 2009 |

Note: This table relates only to the provisions of this Act as originally passed by both Houses of the Parliament and assented to. It will not be expanded to deal with provisions inserted in this Act after assent.

(2) Column 3 of the table contains additional information that is not part of this Act. Information in this column may be added to or edited in any published version of this Act.

Each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

Section 170 of the Income Tax Assessment Act 1936 does not prevent the amendment of an assessment if:

(a) the assessment was made before the commencement of this section; and

(b) the amendment is made within 2 years after that commencement; and

(c) the amendment is made for the purpose of giving effect to Schedule 4.

Schedule 1—Research and development

Income Tax Assessment Act 1936

1 Paragraph 73J(1)(c)

Omit “$1,000,000”, substitute “$2,000,000”.

2 Application

The amendment made by this Schedule applies to years of income starting on or after 1 July 2009.

Schedule 2—Private ancillary funds

Part 1—Amendments commencing on 1 October 2009

A New Tax System (Australian Business Number) Act 1999

1 Paragraph 26(3)(ga)

After “section 426‑65”, insert “or 426‑115”.

Income Tax Assessment Act 1936

2 Subsection 6(1)

Insert:

private ancillary fund has the meaning given by section 426‑105 in Schedule 1 to the Taxation Administration Act 1953.

3 At the end of subsection 16(4)

Add:

; or (n) if the information relates to the non‑compliance of a private ancillary fund or charity (or a trustee of a private ancillary fund or charity) with a law of the Commonwealth, a State or a Territory—the Attorney‑General of a State or Territory for the purposes of the administration of a law of the State or Territory governing trusts or charities.

Income Tax Assessment Act 1997

4 Subsection 30‑15(2) (table item 2, column headed “Recipient”)

Omit “*prescribed private fund”, substitute “*private ancillary fund”.

5 Subsection 30‑15(2) (paragraph (c) of the cell at table item 2, column headed “Special conditions”)

Omit “, unless the fund is a prescribed private fund”.

6 Paragraph 30‑17(1)(b)

Repeal the paragraph.

7 Subsection 30‑125(1)

Repeal the subsection, substitute:

Endorsement of an entity that is a fund, authority or institution

(1) An entity is entitled to be endorsed as a *deductible gift recipient if:

(a) the entity has an *ABN; and

(b) the entity is a fund, authority or institution that:

(i) is described (but not by name) in item 1, 2 or 4 of the table in section 30‑15; and

(ii) is not described by name in Subdivision 30‑B if it is described in item 1 of that table; and

(iii) meets the relevant conditions (if any) identified in the column headed “Special conditions” of the item of that table in which it is described; and

(c) the entity meets the requirements of subsection (6), unless:

(i) the entity is established by an Act; and

(ii) the Act (or another Act) does not provide for the winding up or termination of the entity; and

(d) in the case of a *private ancillary fund:

(i) the fund complies with the rules in the *private ancillary fund guidelines; and

(ii) all of the trustees of the fund comply with those rules.

8 Subparagraph 30‑227(2)(a)(iii)

Repeal the subparagraph.

9 After subsection 30‑229(2)

Insert:

(2A) If:

(a) the *deductible gift recipient is:

(i) a fund, authority or institution; or

(ii) a deductible gift recipient only because it is endorsed under Subdivision 30‑BA as a deductible gift recipient for the operation of a fund, authority or institution; and

(b) the fund, authority or institution is covered by item 1, 2 or 4 of the table in section 30‑15;

the statement may specify that the fund, authority or institution is covered by that item.

10 Paragraph 31‑10(1)(b)

Omit “*prescribed private fund”, substitute “*private ancillary fund”.

11 Paragraph 31‑10(2)(b)

Omit “or be a *prescribed private fund”.

12 Subsection 995‑1(1)

Insert:

constitutional corporation means:

(a) a corporation to which paragraph 51(xx) of the Constitution applies; or

(b) a body corporate that is incorporated in a Territory.

13 Subsection 995‑1(1) (definition of prescribed private fund)

Repeal the definition.

14 Subsection 995‑1(1)

Insert:

private ancillary fund has the meaning given by section 426‑105 in Schedule 1 to the Taxation Administration Act 1953.

15 Subsection 995‑1(1)

Insert:

private ancillary fund guidelines has the meaning given by section 426‑110 in Schedule 1 to the Taxation Administration Act 1953.

Taxation Administration Act 1953

16 Subsection 2(1)

Insert:

private ancillary fund has the meaning given by section 426‑105 in Schedule 1.

17 Subsection 3C(4)

Repeal the subsection, substitute:

(4) Nothing in subsection (2) prohibits the Commissioner, a Second Commissioner, a Deputy Commissioner or a person authorised by the Commissioner, a Second Commissioner or a Deputy Commissioner from communicating any information to:

(a) a person performing, as an officer, duties in relation to a taxation law, for the purpose of enabling the person to perform those duties; or

(b) if the information relates to the non‑compliance of a private ancillary fund or charity (or a trustee of a private ancillary fund or charity) with a law of the Commonwealth, a State or a Territory—the Attorney‑General of a State or Territory for the purposes of the administration of a law of the State or Territory governing trusts and charities.

18 Subsection 250‑10(2) in Schedule 1 (table item 140, column headed “Provision”)

Omit “Divisions 284, 286 and 288”, substitute “298‑15”

19 Paragraph 298‑5(c) in Schedule 1

Omit “or Division 16”, substitute “, Division 16 or section 426‑120”.

20 Subsection 353‑20(3) in Schedule 1

Repeal the subsection, substitute:

(3) The Minister may only disclose information provided under subsection (2) for a purpose relating to the removal of the name of the *deductible gift recipient from Division 30 of the Income Tax Assessment Act 1997.

21 At the end of section 426‑1 in Schedule 1

Add:

Subdivision 426‑D deals with a type of private philanthropic trust fund known as a private ancillary fund.

22 At the end of Division 426 in Schedule 1

Add:

Subdivision 426‑D—Private ancillary funds

426‑100 What this Subdivision is about

This Subdivision deals with a type of private philanthropic trust fund known as a private ancillary fund.

The Minister may make guidelines determining when private ancillary funds are entitled to be endorsed as deductible gift recipients.

This Subdivision also provides for:

(a) penalties for trustees who fail to comply with the private ancillary fund guidelines, and the liability of directors of trustees to pay those penalties in certain circumstances; and

(b) powers for the Commissioner to suspend or remove trustees who breach their obligations.

Table of sections

Private ancillary funds

426‑105 Private ancillary funds

426‑110 Private ancillary fund guidelines

426‑115 Australian Business Register must show private ancillary fund status

Administrative penalties

426‑120 Administrative penalties for trustees of private ancillary funds

Suspension and removal of trustees

426‑125 Suspension or removal of trustees

426‑130 Commissioner to appoint acting trustee in cases of suspension or removal

426‑135 Terms and conditions of appointment of acting trustee

426‑140 Termination of appointment of acting trustee

426‑145 Resignation of acting trustee

426‑150 Property vesting orders

426‑155 Powers of acting trustee

426‑160 Commissioner may give directions to acting trustee

426‑105 Private ancillary funds

(1) A trust is a private ancillary fund if:

(a) each trustee of the trust is a *constitutional corporation; and

(b) each trustee has agreed, in the *approved form given to the Commissioner, to comply with the rules in the *private ancillary fund guidelines, as in force from time to time; and

(c) none of the trustees has revoked that agreement in accordance with subsection (2).

(2) A trustee may revoke an agreement mentioned in paragraph (1)(b) only by giving the revocation to the Commissioner in the *approved form.

426‑110 Private ancillary fund guidelines

The Minister must, by legislative instrument, formulate guidelines (the private ancillary fund guidelines) setting out:

(a) rules that *private ancillary funds and their trustees must comply with if the funds are to be, or are to remain, endorsed as *deductible gift recipients; and

(b) the amount of the administrative penalty, or how to work out the amount of the administrative penalty, under subsection 426‑120(1).

426‑115 Australian Business Register must show private ancillary fund status

(1) If a *private ancillary fund has an *ABN, the *Australian Business Registrar may enter in the *Australian Business Register in relation to the fund a statement that it is a private ancillary fund.

Note 1: An entry (or lack of entry) of a statement required by this section does not affect whether a trust is a private ancillary fund.

Note 2: The Australian Business Register will also show if a private ancillary fund is endorsed as a deductible gift recipient: see section 30‑229 of the Income Tax Assessment Act 1997.

(2) The *Australian Business Registrar must take reasonable steps to ensure that a statement appearing in the *Australian Business Register under this section is true. For this purpose, the Registrar may:

(a) change the statement; or

(b) remove the statement from the Register if the statement is not true.

426‑120 Administrative penalties for trustees of private ancillary funds

Administrative penalty

(1) The persons mentioned in subsection (2) are jointly and severally liable to an administrative penalty if:

(a) a trustee of a *private ancillary fund holds the fund out as being endorsed, entitled to be endorsed, or entitled to remain endorsed, as a *deductible gift recipient; and

(b) the fund is not so endorsed or entitled.

(2) The persons are:

(a) each person who is a trustee of the fund; and

(b) each director of each *constitutional corporation that is a trustee of the fund, if:

(i) any of the penalty cannot reasonably be recovered from the constitutional corporation; and

(ii) the constitutional corporation is not a registered trustee company.

Note: A person mentioned in paragraph (2)(a) may, in certain circumstances, not be a constitutional corporation: see item 28 of Schedule 2 to the Tax Laws Amendment (2009 Measures No. 4) Act 2009 (former prescribed private funds).

(3) The amount of the penalty is:

(a) the amount specified in the *private ancillary fund guidelines under paragraph 426‑110(b); or

(b) the amount worked out in accordance with the method specified under that paragraph.

The private ancillary fund guidelines may specify different penalties or methods for different circumstances.

(4) The penalty must not be reimbursed from the fund.

Note: Division 298 in this Schedule contains machinery provisions for administrative penalties.

Defences for directors

(5) Paragraph (2)(b) does not apply to a director if:

(a) the director was not aware of the holding out mentioned in paragraph (1)(a) and it would not have been reasonable to expect the director to have been aware of that holding out; or

(b) the director took all reasonable steps to ensure that the holding out mentioned in that paragraph did not occur; or

(c) there were no such steps that the director could have taken.

(6) In determining what is reasonable for the purposes of paragraph (5)(a), (b) or (c), have regard to all relevant circumstances.

(7) A person who wishes to rely on subsection (5) bears an evidential burden in relation to the matters in that subsection.

Power of courts to grant relief

(8) Section 1318 of the Corporations Act 2001 (power of Court to grant relief in case of breach of director’s duty) does not apply to a liability of a director under this section.

Suspension and removal of trustees

426‑125 Suspension or removal of trustees

Suspension

(1) The Commissioner may suspend all of the trustees of a *private ancillary fund if the Commissioner is satisfied that the fund, or any of the trustees of the fund, have breached:

(a) the *private ancillary fund guidelines; or

(b) any other *Australian law.

(2) The suspension of a trustee:

(a) starts when the Commissioner gives the trustee notice of the suspension under subsection (3); and

(b) ends at the time specified in the notice.

(3) If the Commissioner decides to suspend a trustee under this section, the Commissioner must give to the trustee a written notice:

(a) setting out the decision; and

(b) giving the reasons for the decision; and

(c) setting out the time the suspension ends.

Extension of suspensions

(4) The Commissioner may change the time the suspension of a trustee ends.

(5) If the Commissioner decides to change the time the suspension of a trustee ends under this section, the Commissioner must give to the trustee a written notice:

(a) setting out the decision; and

(b) giving the reasons for the decision; and

(c) setting out the new time the suspension ends.

Removal

(6) The Commissioner may remove all of the trustees of a *private ancillary fund if the Commissioner is satisfied that the fund, or any of the trustees of the fund, have breached:

(a) the *private ancillary fund guidelines; or

(b) any other *Australian law.

(7) If the Commissioner decides to remove a trustee under this section, the Commissioner must give to the trustee a written notice:

(a) setting out the decision; and

(b) giving the reasons for the decision.

Review of decisions under this section

(8) A trustee who is dissatisfied with any of the following decisions under this section may object in the manner set out in Part IVC of this Act:

(a) a decision to suspend the trustee;

(b) a decision to change the time a suspension of the trustee ends;

(c) a decision to remove the trustee.

426‑130 Commissioner to appoint acting trustee in cases of suspension or removal

Appointment of acting trustee

(1) If the Commissioner suspends all of the trustees of a *private ancillary fund under section 426‑125, the Commissioner must appoint a single entity to act as the trustee (the acting trustee) of the fund during the period of the suspension.

(2) If the Commissioner removes all of the trustees of a *private ancillary fund under section 426‑125, the Commissioner must appoint a single entity to act as the trustee (the acting trustee) of the fund until all of the vacancies in the position of trustee are filled.

Acting trustee need not be constitutional corporation

(3) An acting trustee need not be a *constitutional corporation, and may be the Commissioner. Paragraph 426‑105(1)(a) does not apply in relation to an acting trustee.

(4) An entity that is not a *constitutional corporation may not act as trustee under this section for longer than 6 months.

Acting trustee must have agreed to comply with guidelines

(5) An entity may only be appointed as acting trustee if the entity has, in accordance with paragraph 426‑105(1)(b), agreed to comply with the rules in the *private ancillary fund guidelines, as in force from time to time.

426‑135 Terms and conditions of appointment of acting trustee

(1) The Commissioner may determine the terms and conditions of the appointment of the acting trustee, including fees. The determination has effect despite anything in:

(a) any *Australian law other than this section; or

(b) the *private ancillary fund’s governing rules.

(2) Without limiting subsection (1), the Commissioner may make a determination under that subsection to the effect that the acting trustee’s fees are to be paid out of the corpus of the *private ancillary fund.

426‑140 Termination of appointment of acting trustee

The Commissioner may terminate the appointment of the acting trustee at any time.

426‑145 Resignation of acting trustee

(1) The acting trustee may resign by writing given to the Commissioner.

(2) The resignation does not take effect until the end of the seventh day after the day on which it was given to the Commissioner.

426‑150 Property vesting orders

(1) If the Commissioner appoints an acting trustee, the Commissioner must make a written order vesting the property of the *private ancillary fund in the acting trustee.

(2) If the appointment ends, the Commissioner must make a written order vesting the property of the fund in the new acting trustee, the previously suspended trustee or trustees or the new actual trustee or trustees (whichever is applicable).

(3) If the Commissioner makes an order under this section vesting property of a *private ancillary fund in an entity or entities, then, subject to subsection (4), the property immediately vests in the entity or entities by force of this section.

(4) If:

(a) the property is of a kind whose transfer or transmission may be registered under an *Australian law; and

(b) that law enables the registration of such an order, or enables the entity or entities to be registered as the owner of that property;

the property does not vest in the entity or entities until the requirements of the law referred to in paragraph (a) have been complied with.

426‑155 Powers of acting trustee

Subject to section 426‑150:

(a) the acting trustee has and may exercise all the rights, title and powers, and must perform all the functions and duties, of the original trustee or trustees; and

(b) the *private ancillary fund’s governing rules and every *Australian law apply in relation to the acting trustee as if the acting trustee were the trustee of the fund.

426‑160 Commissioner may give directions to acting trustee

(1) The Commissioner may give the acting trustee a written notice directing the acting trustee to do, or not to do, one or more specified acts or things in relation to the *private ancillary fund.

(2) The acting trustee commits an offence if:

(a) the acting trustee engages in conduct (within the meaning of subsection 2(1) of this Act); and

(b) that engagement in conduct contravenes a notice given to the acting trustee under subsection (1).

Penalty: 100 penalty units.

(3) This section does not affect the validity of a transaction entered into in contravention of a notice given under subsection (1).

Books

(1) An entity commits an offence if:

(a) the Commissioner makes an order under subsection 426‑150(1) or (2) vesting the property of a *private ancillary fund in an acting trustee; and

(b) just before the Commissioner made the order, the property was vested in:

(a) the entity (the former trustee); or

(b) 2 or more entities (the former trustees), including the entity; and

(c) the former trustee or former trustees do not, within 14 days of the Commissioner making the order, give the acting trustee all books (within the meaning of the Corporations Act 2001) relating to the fund’s affairs that are in the former trustee’s or former trustees’ possession, custody or control.

Penalty: 50 penalty units.

Identification of property and transfer of property

(2) Subsections (3) to (5) apply if:

(a) the property of a *private ancillary fund is vested in an entity (the former trustee) or entities (the former trustees); and

(b) the Commissioner makes an order under subsection 426‑150(1) or (2) vesting the property in an acting trustee.

(3) The acting trustee may, by notice in writing to the former trustee or former trustees, require the former trustee or former trustees, so far as the former trustee or former trustees can do so:

(a) to identify property of the fund; and

(b) to explain how the former trustee or former trustees have kept account of that property.

(4) The acting trustee may, by notice in writing to the former trustee or former trustees, require the former trustee or former trustees to take specified action that is necessary to bring about a transfer of specified property of the fund to the acting trustee.

(5) The former trustee, or each of the former trustees, commits an offence if:

(a) the acting trustee gives the former trustee or former trustees a notice under subsection (3) or (4); and

(b) the former trustee or former trustees do not, within 28 days of the notice being given, comply with the requirement in the notice.

Penalty: 50 penalty units.

Strict liability

(6) Subsections (1) and (5) are offences of strict liability.

Note: For strict liability, see section 6.1 of the Criminal Code.

Part 2—Amendments commencing on 1 January 2010

Income Tax Assessment Act 1997

23 Subsection 30‑229(2A)

Omit “may”, substitute “must”.

Taxation Administration Act 1953

24 Subsection 426‑115(1) in Schedule 1

Omit “may”, substitute “must”.

Part 3—Transitional provisions

25 Definitions

In this Part:

commencement time means the time at which this item commences.

constitutional corporation has the meaning given by the Income Tax Assessment Act 1997.

deductible gift recipient has the meaning given by the Income Tax Assessment Act 1997.

prescribed private fund has the meaning given by the Income Tax Assessment Act 1997 (as in force just before the commencement time).

private ancillary fund has the meaning given by section 426‑105 in Schedule 1 to the Taxation Administration Act 1953.

private ancillary fund guidelines has the meaning given by section 426‑110 in Schedule 1 to the Taxation Administration Act 1953.

Division 2—Declared prescribed private funds

26 Transitional—prescribed private fund declarations

(1) The Minister may, by legislative instrument, declare a trust to be a prescribed private fund.

(2) Despite subsection 12(2) of the Legislative Instruments Act 2003, the declaration has effect during the period:

(a) starting at the time specified in the declaration, which must be before the commencement time; and

(b) ending just before the commencement time.

Division 3—Transitional private ancillary funds

27 Application of Division

This Division applies to a trust if, just before the commencement time, the trust was a prescribed private fund (whether or not because of a declaration made under item 26).

28 Transitional—trustees need not be constitutional corporations

Paragraph 426‑105(1)(a) (trustees of private ancillary funds must be constitutional corporations) and sections 426‑125 to 426‑165 (Suspension and removal of trustees) in Schedule 1 to the Taxation Administration Act 1953 do not apply to the trust during the period:

(a) starting at the commencement time; and

(b) ending at the earlier of the following:

(i) the time (at or after the commencement time) the trust first satisfies the requirements of that paragraph (disregarding this item);

(ii) the first time any of the trustees of the trust revoke the agreement mentioned in item 29 in accordance with subsection 426‑105(2) in that Schedule.

29 Transitional—agreement to comply with private ancillary fund guidelines

(1) For the purposes of Subdivision 426‑D in Schedule 1 to the Taxation Administration Act 1953, each of the trustees of the trust is taken to have agreed, at the commencement time and in accordance with paragraph 426‑105(1)(b) in that Schedule, to comply with the rules in the private ancillary fund guidelines, as in force from time to time.

(2) To avoid doubt, subitem (1) does not prevent a trustee from revoking that agreement at a later time as mentioned in paragraph 426‑105(1)(c) in that Schedule.

30 Transitional—endorsement as a deductible gift recipient

(1) The trust is taken to have been endorsed as a deductible gift recipient under section 30‑120 of the Income Tax Assessment Act 1997 at the commencement time.

(2) To avoid doubt, subitem (1) does not prevent the Commissioner from revoking that endorsement at a later time under section 426‑55 in Schedule 1 to the Taxation Administration Act 1953.

31 Transitional—transfer of property

For the purposes of item 2 of the column headed “Recipient” of the table in subsection 30‑15(2) of the Income Tax Assessment Act 1997, disregard a transfer of all of the property of the trust to another private ancillary fund if:

(a) the other fund is a deductible gift recipient; and

(b) every trustee of the other fund is a constitutional corporation; and

(c) the transfer happens during the period mentioned in item 28.

Schedule 3—Demutualisation of friendly society health or life insurers

Income Tax Assessment Act 1997

1 At the end of Part 3‑32

Add:

Division 316—Demutualisation of friendly society health or life insurers

Table of Subdivisions

Guide to Division 316

316‑A Application

316‑B Capital gains and losses connected with the demutualisation

316‑C Cost base of shares and rights issued under the demutualisation

316‑D Lost policy holders trust

316‑E Special CGT rules for legal personal representatives and beneficiaries

316‑F Non‑CGT consequences of the demutualisation

316‑1 What this Division is about

Special tax consequences follow the demutualisation of a friendly society that provides health insurance or life insurance, or has a wholly‑owned subsidiary that does.

Table of sections

316‑5 Application of this Division

316‑5 Application of this Division

This Division applies in relation to a demutualisation of a *friendly society if:

(a) the society is, or has a *wholly‑owned subsidiary (a health/life insurance subsidiary) that is:

(i) a private health insurer as defined in the Private Health Insurance Act 2007; or

(ii) a company registered under section 21 of the Life Insurance Act 1995; and

(b) the society does not have capital divided into *shares held by its *members; and

(c) after the demutualisation the society is to be carried on for the object of securing a profit or pecuniary gain for its *members.

Subdivision 316‑B—Capital gains and losses connected with the demutualisation

316‑50 What this Subdivision is about

Disregard capital gains and losses made by any entity from a CGT event happening under the demutualisation, unless the entity:

(a) is or has been a member of the friendly society or insured through the society or any of its wholly‑owned subsidiaries; and

(b) receives money for the event.

Table of sections

Gains and losses of members, insured entities and successors

316‑55 Disregarding capital gains and losses, except some involving receipt of money

316‑60 Taking account of some capital gains and losses involving receipt of money

316‑65 Valuation factor for sections 316‑60, 316‑105 and 316‑165

316‑70 Value of the friendly society

Friendly society’s gains and losses

316‑75 Disregarding friendly society’s capital gains and losses

Other entities’ gains and losses

316‑80 Disregarding other entities’ capital gains and losses

Gains and losses of members, insured entities and successors

316‑55 Disregarding capital gains and losses, except some involving receipt of money

(1) Disregard an entity’s *capital gain or *capital loss from a *CGT event that happens under the demutualisation to a *CGT asset if:

(a) the entity:

(i) is or has been a *member of the *friendly society; or

(ii) is or has been insured through the friendly society or a health/life insurance subsidiary of the friendly society; and

(b) the CGT asset is one of these (an interest affected by demutualisation):

(i) an interest in the friendly society as the owner or holder of a policy of insurance with the friendly society or health/life insurance subsidiary;

(ii) a *membership interest in the friendly society;

(iii) a right or interest of another kind in the friendly society;

(iv) a right or interest of another kind that arises under the demutualisation, except an interest in a lost policy holders trust (see section 316‑155).

Note: Subdivision 316‑D deals with the effects of CGT events happening to interests in lost policy holders trusts.

(2) Disregard a *capital gain or *capital loss of an entity (the successor) from a *CGT event that happens under the demutualisation to a *CGT asset if:

(a) the successor is the *legal personal representative, or beneficiary in the estate, of a deceased individual who was:

(i) a *member of the *friendly society; or

(ii) insured through the friendly society or a health/life insurance subsidiary of the friendly society; and

(b) the CGT asset:

(i) forms part of the deceased individual’s estate; and

(ii) devolves or *passes to the successor; and

(iii) is an interest affected by demutualisation (see paragraph (1)(b)).

316‑60 Taking account of some capital gains and losses involving receipt of money

(1) This section applies if:

(a) a *CGT event happens under the demutualisation to an entity’s interest affected by demutualisation (see section 316‑55); and

(b) the event involves:

(i) the variation or abrogation of rights attaching to or consisting of the interest; or

(ii) the conversion, cancellation, extinguishment or redemption of the interest; and

(c) either:

(i) the entity is one described in paragraph 316‑55(1)(a); or

(ii) the entity is one described in paragraph 316‑55(2)(a) and the interest is a *CGT asset described in paragraph 316‑55(2)(b); and

(d) the *capital proceeds from the event include or consist of money received by the entity.

(2) Work out whether the entity makes a *capital gain or *capital loss from the *CGT event, and the amount of the gain or loss, assuming that:

(a) the *capital proceeds from the CGT event were the amount they would be if they did not include any *market value of property other than money; and

(b) the *cost base and *reduced cost base for the interest were the amount worked out using the formula:

Example: Assume the entity receives $50 in money and 10 shares with a market value of $4 each in respect of CGT event C2 happening, and that the valuation factor worked out under section 316‑65 is 0.9. The entity makes a capital gain from the event of $5, worked out as follows:

This ignores the market value of the shares because they are property other than money.

Note: Division 114 (Indexation of cost base) is not relevant, because this section provides exhaustively for working out the amount of the cost base.

(3) The *capital gain or *capital loss is not to be disregarded, despite:

(a) section 316‑55; and

(b) any provision of this Act for disregarding the *capital gain or *capital loss because the interest affected by demutualisation was *acquired before 20 September 1985.

Note: The capital gain is not a discount capital gain: see section 115‑55.

316‑65 Valuation factor for sections 316‑60, 316‑105 and 316‑165

(1) For the purposes of sections 316‑60, 316‑105 and 316‑165, the valuation factor is the amount worked out using the formula:

where:

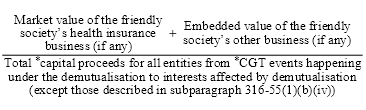

embedded value of the friendly society’s other business (if any) means the amount that would be the value of the *friendly society worked out under section 316‑70 assuming that neither the friendly society, nor any health/life insurance subsidiary of it, *carried on any health insurance business within the meaning of the Private Health Insurance Act 2007.

market value of the friendly society’s health insurance business (if any) means the total *market value of every health insurance business, within the meaning of the Private Health Insurance Act 2007, *carried on by either or both of the *friendly society and its health/life insurance subsidiaries (if any), taking account of any consideration paid to the society or subsidiary for disposal or control of that business.

(2) Disregard paragraph 316‑60(2)(a) for the purposes of the formula in subsection (1) of this section.

316‑70 Value of the friendly society

(1) The value of the *friendly society is the sum, worked out in accordance with this section, of the friendly society’s existing business value and its adjusted net worth on the day (the applicable accounting day) identified under subsection (3).

Eligible actuary and Australian actuarial practice

(2) The sum is to be worked out, according to Australian actuarial practice, by an *actuary who is not an employee of:

(a) the *friendly society; or

(b) a health/life insurance subsidiary of the friendly society; or

(c) an entity of which the friendly society is to become a *wholly‑owned subsidiary under the demutualisation.

Applicable accounting day

(3) The applicable accounting day is:

(a) if an accounting period of the *friendly society ends on the day (the demutualisation resolution day) identified under subsection (4)—that day; or

(b) in any other case—the last day of the most recent accounting period of the friendly society ending before the demutualisation resolution day.

Demutualisation resolution day

(4) The demutualisation resolution day is:

(a) the day on which the resolution to proceed with the demutualisation is passed; or

(b) if, under the demutualisation, the whole of the *life insurance business of the *friendly society or of a health/life insurance subsidiary of the friendly society is transferred to another company under a scheme confirmed by the Federal Court of Australia—the day (or the last day) on which the transfer takes place.

Adjustment for changes after applicable accounting day

(5) In a case covered by paragraph (3)(b), if any significant change in the amount of the existing business value or adjusted net worth occurs between the applicable accounting day and the demutualisation resolution day, the amount is to be adjusted to take account of the change.

Continued business assumption

(6) In working out the existing business value or the adjusted net worth, assume:

(a) that after the applicable accounting day the *friendly society, and any health/life insurance subsidiary of the friendly society, will continue to conduct *business and any other activity in the same way as before that day, and will not conduct any different business or other activity; and

(b) that the demutualisation will not occur; and

(c) that any health/life insurance subsidiary of the friendly society will continue to be a *wholly‑owned subsidiary of the friendly society.

Expenditure assumption

(7) In working out the existing business value, assume that expenditure that the *friendly society and any of its health/life insurance subsidiaries will incur, in conducting *business, on recurring items after the demutualisation resolution day will be of the same kinds and amounts (increased to take account of any inflation) as it incurred in the accounting period, or part of an accounting period, ending on the demutualisation resolution day.

Friendly society’s gains and losses

316‑75 Disregarding friendly society’s capital gains and losses

Disregard the *friendly society’s *capital gain or *capital loss from a *CGT event that happens under the demutualisation.

Other entities’ gains and losses

316‑80 Disregarding other entities’ capital gains and losses

Disregard an entity’s *capital gain or *capital loss from a *CGT event that happens under the demutualisation if:

(a) the entity is established solely for the purpose of participating in the demutualisation and is not a lost policy holders trust (see section 316‑155); and

(b) the CGT event:

(i) happens before or at the same time as the allocation or distribution of the accumulated surplus of the *friendly society; and

(ii) is connected to that allocation or distribution.

Note: The allocation or distribution of the accumulated surplus could happen through an arrangement involving more than one transaction.

Subdivision 316‑C—Cost base of shares and rights issued under the demutualisation

316‑100 What this Subdivision is about

The value of the friendly society and its business affects cost bases of shares and certain rights issued under the demutualisation to:

(a) entities that are or were members of the friendly society; or

(b) entities insured through the society or its subsidiaries; or

(c) successors of such entities; or

(d) the trustee of the lost policy holders trust.

Table of sections

316‑105 Cost base and time of acquisition of shares and certain rights issued under demutualisation

316‑110 Demutualisation assets

316‑115 Entities to which section 316‑105 applies

316‑105 Cost base and time of acquisition of shares and certain rights issued under demutualisation

First element of cost base

(1) The first element of the *cost base and *reduced cost base of a *CGT asset is the amount worked out using the formula in subsection (2) if:

(a) the asset is a CGT asset (a demutualisation asset) covered by section 316‑110; and

(b) the asset is issued to an entity covered by section 316‑115.

(2) The formula is:

Time of acquisition

(3) The entity is taken to have *acquired the *CGT asset at the time it is issued.

316‑110 Demutualisation assets

(1) This section covers a *CGT asset that:

(a) is:

(i) a *share in the *friendly society; or

(ii) a right to *acquire a share in the friendly society; or

(iii) a share in an entity that owns all of the shares in the friendly society; or

(iv) a right to acquire a share in an entity mentioned in subparagraph (iii); and

(b) is issued under the demutualisation; and

(c) is issued in connection with:

(i) the variation or abrogation of rights attaching to or consisting of an interest affected by demutualisation (see paragraph 316‑55(1)(b)); or

(ii) the conversion, cancellation, extinguishment or redemption of an interest affected by demutualisation.

Exclusion for rights with an exercise price

(2) Despite subsection (1), this section does not cover a right to *acquire a *share in an entity if the holder of the right must pay an amount to exercise the right.

Exclusion where assets not issued simultaneously

(3) Despite subsection (1), a *CGT asset is not covered by this section unless all of the CGT assets covered by subsection (1) for the demutualisation are issued:

(a) at the same time; and

(b) to entities that are covered by section 316‑115.

316‑115 Entities to which section 316‑105 applies

(1) This section covers an entity that:

(a) either:

(i) is or has been a *member of the *friendly society; or

(ii) is or has been insured through the friendly society or a health/life insurance subsidiary of the friendly society; and

(b) is entitled under the demutualisation to an allocation of demutualisation assets.

(2) This section also covers an entity that has become entitled to an allocation of demutualisation assets because of the death of an individual who was an entity described in subsection (1).

(3) This section also covers the trustee of a lost policy holders trust (see section 316‑155).

Subdivision 316‑D—Lost policy holders trust

316‑150 What this Subdivision is about

If the demutualisation creates a trust just to hold shares, rights to acquire shares or money for entities that were members of the friendly society or insured through the society or its subsidiary, or are successors of such entities, then:

(a) capital gains or losses from CGT events happening to beneficiaries’ interests in the trust are disregarded, except where the capital proceeds include money; and

(b) when a CGT event happens involving the transfer of the shares or rights to a beneficiary, or a beneficiary’s absolute entitlement to them, the trustee’s capital gain or loss is disregarded and the beneficiary has the same cost base and time of acquisition as the trustee; and

(c) the trustee is assessed on any capital gains from other CGT events happening to the shares or rights.

Table of sections

Application

316‑155 Lost policy holders trust

Effects of CGT events happening to interests and assets in trust

316‑160 Disregarding beneficiaries’ capital gains and losses, except some involving receipt of money

316‑165 Taking account of some capital gains and losses involving receipt of money by beneficiaries

316‑170 Roll‑over where shares or rights to acquire shares transferred to beneficiary of lost policy holders trust

316‑175 Trustee assessed if shares or rights dealt with not for benefit of beneficiary of lost policy holders trust

316‑180 Subdivision 126‑E does not apply

316‑155 Lost policy holders trust

(1) This Subdivision applies if the conditions in subsections (2) and (5) are met.

First condition

(2) The first condition is that the scheme approved by a court for the demutualisation provides for a trust (the lost policy holders trust) to exist solely for one or both of the purposes that are described in subsection (3) in relation to persons (beneficiaries of the lost policy holders trust) covered by subsection (4).

(3) The purposes are as follows:

(a) holding demutualisation assets (see section 316‑110) that are *shares or rights to *acquire shares, or proceeds from disposal of those assets, on behalf of one or more beneficiaries of the lost policy holders trust and transferring those assets or proceeds to those beneficiaries;

(b) holding on behalf of one or more beneficiaries of the lost policy holders trust, and paying to them, money payable to them for:

(i) the variation or abrogation of rights attaching to or consisting of the beneficiaries’ interests affected by demutualisation (see paragraph 316‑55(1)(b)); or

(ii) the conversion, cancellation, extinguishment or redemption of those interests.

(4) This subsection covers:

(a) a person who is or has been a *member of the friendly society or is or has been insured through the *friendly society or a health/life insurance subsidiary of the friendly society; and

(b) a *legal personal representative, or beneficiary in the estate, of such a person who has died.

Second condition

(5) The second condition is that, under the demutualisation, the trustee of the lost policy holders trust is:

(a) issued with demutualisation assets that are *shares, or rights to *acquire shares; or

(b) paid money described in paragraph (3)(b) to hold and pay to beneficiaries of the lost policy holders trust.

Effects of CGT events happening to interests and assets in trust

316‑160 Disregarding beneficiaries’ capital gains and losses, except some involving receipt of money

Disregard a *capital gain or *capital loss of a beneficiary of the lost policy holders trust from a *CGT event that happens to the beneficiary’s interest in the trust.

316‑165 Taking account of some capital gains and losses involving receipt of money by beneficiaries

(1) This section applies if:

(a) a *CGT event happens to an interest of a beneficiary of the lost policy holders trust in that trust; and

(b) the *capital proceeds from the event include or consist of money received by the beneficiary.

(2) Work out whether the beneficiary makes a *capital gain or *capital loss from the *CGT event, and the amount of the gain or loss, assuming that:

(a) the *capital proceeds from the CGT event were the amount they would be if they did not include any *market value of property other than money; and

(b) the *cost base and *reduced cost base for the interest were the amount worked out using the formula:

Example: Assume that the beneficiary of the lost policy holders trust is paid $50 in money by the trustee to satisfy the beneficiary’s interest in the trust so that a CGT event happens, and that the valuation factor worked out under section 316‑65 is 0.9. The beneficiary makes a capital gain from the event of $5, worked out as follows:

Note: Division 114 (Indexation of cost base) is not relevant, because this section provides exhaustively for working out the amount of the cost base.

(3) The *capital gain or *capital loss is not to be disregarded, despite sections 316‑55 and 316‑160.

Note: The capital gain is not a discount capital gain: see section 115‑55.

(1) This section applies in relation to a *CGT event if:

(a) the CGT event happens in relation to an asset that:

(i) is a *share or a right to *acquire one or more shares; and

(ii) is held by the trustee of the lost policy holders trust on behalf of a beneficiary of the lost policy holders trust; and

(b) the CGT event happens because the beneficiary of the lost policy holders trust either:

(i) is transferred the asset by the trustee; or

(ii) becomes absolutely entitled to the asset.

Consequence for trustee

(2) Disregard a *capital gain or *capital loss the trustee makes from the *CGT event.

Consequences for beneficiary

(3) The *cost base and *reduced cost base of the asset in the hands of the trustee of the lost policy holders trust just before the *CGT event becomes the first element of the cost base and reduced cost base of the asset in the hands of the beneficiary of the lost policy holders trust.

Note: Section 316‑105 affects the cost base of the asset in the hands of the trustee of the lost policy holders trust if the asset is covered by section 316‑110.

(4) The beneficiary of the lost policy holders trust is taken to have *acquired the asset when the trustee acquired it.

(1) This section applies in relation to a *capital gain from a *CGT event if:

(a) the CGT event happens in relation to a demutualisation asset that:

(i) is a *share or a right to *acquire a share; and

(ii) is held by the trustee of a lost policy holders trust; and

(b) section 316‑170 does not apply to the CGT event.

(2) For the purposes of sections 97, 98A and 100 of the Income Tax Assessment Act 1936, the share of the net income of the trust that is attributable to the *capital gain is taken not to be included in the assessable income of a beneficiary of the trust.

(3) The trustee is not assessed, and is not liable to pay tax, in respect of the share under section 98 of the Income Tax Assessment Act 1936.

Note: Because of these consequences in relation to sections 97 and 98 of the Income Tax Assessment Act 1936, the trustee will be assessed on the beneficiary’s share under section 99A of that Act.

316‑180 Subdivision 126‑E does not apply

Subdivision 126‑E does not apply in relation to the demutualisation.

Note: Subdivision 126‑E is about an entitlement to shares after demutualisation and scrip for scrip roll‑over.

Subdivision 316‑E—Special CGT rules for legal personal representatives and beneficiaries

Table of sections

316‑200 Demutualisation assets not owned by deceased but passing to beneficiary in deceased estate

316‑205 Interest in lost policy holders trust not owned by deceased but passing to beneficiary in deceased estate

316‑200 Demutualisation assets not owned by deceased but passing to beneficiary in deceased estate

(1) This section sets out what happens if a *CGT asset:

(a) is a demutualisation asset (see section 316‑110); and

(b) forms part of the estate of an individual who is an entity described in subsection 316‑115(1) and has died; and

(c) was not owned by the individual just before dying; and

(d) *passes to a beneficiary in the individual’s estate because the asset is transferred to the beneficiary by the individual’s *legal personal representative.

Note: Division 128 deals with the effect of death in relation to CGT assets a person owns just before dying.

Consequence for legal personal representative

(2) Disregard a *capital gain or *capital loss the *legal personal representative makes because the asset *passes to the beneficiary.

Consequence for beneficiary

(3) The *cost base and *reduced cost base of the asset in the hands of the *legal personal representative just before the asset *passes to the beneficiary becomes the first element of the cost base and reduced cost base of the asset in the hands of the beneficiary.

(4) The beneficiary is taken to have *acquired the asset when the *legal personal representative acquired it.

(1) This section sets out what happens if a *CGT asset:

(a) is an interest in a lost policy holders trust (see section 316‑155); and

(b) forms part of the estate of an individual who is an entity described in subsection 316‑115(1) and has died; and

(c) was not owned by the individual just before dying; and

(d) *passes to a beneficiary in the individual’s estate because the asset is transferred to the beneficiary by the individual’s *legal personal representative.

Note: Division 128 deals with the effect of death in relation to CGT assets a person owns just before dying.

Consequence for legal personal representative

(2) Disregard a *capital gain or *capital loss the *legal personal representative makes because the asset *passes to the beneficiary.

Subdivision 316‑F—Non‑CGT consequences of the demutualisation

316‑250 What this Subdivision is about

In many cases, income from demutualisation is assessed through the CGT provisions rather than as ordinary income or other statutory income.

Franking debits arise for the friendly society and its subsidiaries to ensure they do not enjoy a franking surplus. Franking debits and credits arise to negate credits and debits from things attributable to the time before demutualisation.

Table of sections

316‑255 General taxation consequences of issue of demutualisation assets etc.

316‑260 Franking debits to stop the friendly society and its subsidiaries having franking surpluses

316‑265 Franking debits to negate franking credits from some distributions to friendly society and subsidiaries

316‑270 Franking debits to negate franking credits from post‑demutualisation payments of pre‑demutualisation tax

316‑275 Franking credits to negate franking debits from refunds of tax paid before demutualisation

316‑255 General taxation consequences of issue of demutualisation assets etc.

(1) An amount of *ordinary income or *statutory income (other than a *net capital gain) of an entity covered by subsection (2) is not assessable income and is not *exempt income if:

(a) the amount would otherwise be included in the ordinary income or statutory income of the entity only because a demutualisation asset (see section 316‑110) was issued to the entity; or

(b) the amount is a payment made to the entity, under the demutualisation, in connection with:

(i) the variation or abrogation of rights attaching to or consisting of an interest affected by demutualisation (see paragraph 316‑55(1)(b)); or

(ii) the conversion, cancellation, extinguishment or redemption of an interest affected by demutualisation; or

(c) the amount would otherwise be included in the ordinary income or statutory income of the entity only because a *share or a right to *acquire one or more shares was transferred to the entity by the trustee of a lost policy holders trust (see section 316‑155); or

(d) the amount is a payment made to the entity from a lost policy holders trust in connection with:

(i) the variation or abrogation of rights attaching to or consisting of an interest affected by demutualisation; or

(ii) the conversion, cancellation, extinguishment or redemption of an interest affected by demutualisation.

(2) This subsection covers an entity that:

(a) is or has been a *member of the *friendly society; or

(b) is or has been insured through the friendly society or a health/life insurance subsidiary of the friendly society; or

(c) is issued with the demutualisation asset, or receives the payment, because of the death of a person covered by paragraph (a) or (b); or

(d) is a beneficiary of a lost policy holders trust (see section 316‑155).

316‑260 Franking debits to stop the friendly society and its subsidiaries having franking surpluses

(1) A *franking debit arises in the *franking account of the *friendly society or a *wholly‑owned subsidiary of the society if the account is in *surplus immediately before the demutualisation resolution day identified under subsection 316‑70(4).

(2) The amount of the *franking debit equals the *surplus.

(3) The *franking debit arises at the start of that day.

(1) This section applies if a *franking credit arises in the *franking account of the *friendly society or a *wholly‑owned subsidiary of the society because a *distribution declared before the demutualisation resolution day identified under subsection 316‑70(4) is made to the society or subsidiary on or after that day.

(2) A *franking debit arises in that account.

(3) The amount of the *franking debit equals the amount of the *franking credit.

(4) The *franking debit arises at the same time as the *franking credit arises.

(1) This section applies if a *franking credit arises in the *franking account of the *friendly society or a *wholly‑owned subsidiary of the society because, on or after the demutualisation resolution day identified under subsection 316‑70(4), the society or subsidiary *pays a PAYG instalment, or *pays income tax, that is wholly or partly attributable to a period before that day.

(2) A *franking debit arises in that account.

(3) The amount of the *franking debit is so much of the *franking credit as is attributable to the period before that day.

(4) The *franking debit arises at the same time as the *franking credit arises.

316‑275 Franking credits to negate franking debits from refunds of tax paid before demutualisation

(1) This section applies if a *franking debit arises in the *franking account of the *friendly society or a *wholly‑owned subsidiary of the society because, on or after the demutualisation resolution day identified under subsection 316‑70(4), the society or subsidiary *receives a refund of income tax that is wholly or partly attributable to a period before that day.

(2) A *franking credit arises in that account.

(3) The amount of the *franking credit is so much of the *franking debit as is attributable to the period before that day.

(4) The *franking credit arises at the same time as the *franking debit arises.

Income Tax Assessment Act 1936

2 At the end of Subdivision C of Division 9AA of Part III

Add:

121AU This Subdivision does not apply to demutualisation of friendly society health or life insurers

This Subdivision does not apply in relation to the demutualisation of a company in relation to whose demutualisation Division 316 (Demutualisation of friendly society health or life insurers) of the Income Tax Assessment Act 1997 applies.

Note: Section 316‑5 of the Income Tax Assessment Act 1997 explains which demutualisations of entities Division 316 of that Act applies to.

3 After paragraph 326‑10(1)(ba) in Schedule 2H

Insert:

(bb) is not an entity in relation to whose demutualisation Division 316 (Demutualisation of friendly society health or life insurers) of that Act applies; and

4 Application

The amendments of the Income Tax Assessment Act 1936 made by this Part apply in relation to demutualisations occurring on or after 1 July 2008.

Income Tax Assessment Act 1997

5 Section 11‑55 (before table item headed “demutualisation of private health insurers”)

Insert:

demutualisation of friendly society health or life insurers |

|

amounts related to issue, or transfer from lost policy holders trust, of demutualisation assets |

|

payments received directly, or from lost policy holders trust, in exchange for cancellation or variation of interests under the demutualisation |

|

6 Section 102‑30 (after table item 10)

Insert:

10A | All entities | Division 316 contains special rules affecting capital gains and capital losses connected with demutualisation of friendly society health or life insurers. | Division 316 |

7 Section 109‑60 (table item 4, column headed “In these circumstances:”)

After “company”, insert “except a friendly society health or life insurer”.

8 Section 109‑60 (table item 10, column headed “In these circumstances:”)

Omit “or health insurer”, substitute “, health insurer and friendly society health or life insurer”.

9 Section 109‑60 (table items 13 and 14, column headed “In these circumstances:”)

After “insurer”, insert “except a friendly society health or life insurer”.

10 Section 109‑60 (after table item 14)

Insert:

14A | You are issued with a share, or a right to acquire shares, under a demutualisation of a friendly society health or life insurer | the time the share or right is issued | section 316‑105 |

14B | You are transferred a share, or right to acquire shares, by a lost policy holders trust under a demutualisation of a friendly society health or life insurer | the time the share or right is issued to the trustee | section 316‑170 |

11 Section 112‑97 (table item 5, column headed “In this situation”)

After “company”, insert “except a friendly society health or life insurer”.

12 Section 112‑97 (table item 5A, column headed “In this situation”)

Omit “or health insurer”, substitute “, health insurer and friendly society health or life insurer”.

13 Section 112‑97 (table items 29 and 30, column headed “In this situation”)

After “insurer”, insert “except a friendly society health or life insurer”.

14 Section 112‑97 (after table item 30)

Insert:

30A | A CGT event occurs under a demutualisation of a friendly society health or life insurer and the capital proceeds from the event include money | All elements of cost base | section 316‑60 |

30B | You are issued with an asset under a demutualisation of a friendly society health or life insurer | First element of cost base and reduced cost base | section 316‑105 |

30C | A CGT event happens to an interest in a lost policy holders trust and the capital proceeds from the event include money | All elements of cost base | section 316‑165 |

30D | You are transferred a share, or right to acquire shares, by a lost policy holders trust under a demutualisation of a friendly society health or life insurer | The total cost base and reduced cost base | section 316‑170 |

15 At the end of Subdivision 115‑A

Add:

Your *capital gain from a *CGT event is not a discount capital gain if it is affected by section 316‑60 or 316‑165.

Note: Those sections affect capital gains involving the receipt of money as a result of the demutualisation of a friendly society health or life insurer.

16 Section 118‑1 (note 3)

Omit “Division 315 (about demutualisation of private health insurers)”, substitute “Divisions 315 and 316 (about demutualisation of certain insurers)”.

17 Subsection 118‑20(4)

Omit “section 59‑40”, substitute “sections 59‑40 and 316‑255”.

18 Paragraphs 149‑165(1)(b) and 149‑170(1)(b)

Repeal the paragraphs, substitute:

(b) has since stopped being a company of either of those kinds, but either:

(i) has continued in existence as a company covered by paragraph 149‑50(1)(a) or (e) or a *publicly traded unit trust; or

(ii) has undergone a demutualisation in relation to which Division 316 (Demutualisation of friendly society health or life insurers) applied and has continued in existence as a company; and

19 After section 197‑37

Insert:

(1) Subject to subsection (2), this Division does not apply to the transferred amount if:

(a) the amount is transferred in connection with a demutualisation of a company; and

(b) Division 316 (about demutualisations of friendly society health and life insurers) applies in relation to the demutualisation; and

(c) the company (the issuing company) to whose *share capital account the amount is transferred is either:

(i) the *friendly society described in that Division; or

(ii) the company that owns all the shares in the friendly society.

(2) Subsection (1) does not stop this Division from applying to so much, if any, of the transferred amount as exceeds the sum of the *cost bases of *shares in the issuing company that:

(a) are demutualisation assets (see section 316‑110); and

(b) are issued to an entity covered by section 316‑115.

Note: Section 316‑115 identifies entities connected directly or indirectly with the friendly society and affected by the special cost base rules in section 316‑105.

(3) For the purposes of subsection (2), work out the *cost base of a *share on the day on which it is issued, taking account of section 316‑105.

20 Subsection 205‑15(1) (at the end of the table)

Add:

6 | a *franking credit arises under section 316‑275 for the *friendly society or one of its *wholly‑owned subsidiaries because the society or subsidiary *receives a refund of income tax | the amount of the debit specified in subsection 316‑275(3) | at the time provided by subsection 316‑275(4) |

21 Subsection 205‑30(1) (at the end of the table)

Add:

10 | a *franking debit arises under section 316‑260 for the *friendly society or one of its *wholly‑owned subsidiaries because the *franking account of the society or subsidiary is in *surplus | the amount of the debit specified in subsection 316‑260(2) | at the time provided by subsection 316‑260(3) |

11 | a *franking debit arises under section 316‑265 for the *friendly society or one of its *wholly‑owned subsidiaries because a *franking credit arises for the society or subsidiary | the amount of the debit specified in subsection 316‑265(3) | at the time provided by subsection 316‑265(4) |

12 | a *franking debit arises under section 316‑270 for the *friendly society or one of its *wholly‑owned subsidiaries because a *franking credit arises for the society or subsidiary | the amount of the debit specified in subsection 316‑270(3) | at the time provided by subsection 316‑270(4) |

22 After subparagraph 315‑15(a)(ii)

Insert:

(iia) is not an entity to whose demutualisation Division 316 applies; and

23 Application

The amendments of the Income Tax Assessment Act 1997 made by this Part apply in relation to demutualisations occurring on or after 1 July 2008.

Income Tax (Transitional Provisions) Act 1997

24 After Part 3‑30

Insert:

Part 3‑32—Co‑operatives and mutual entities

Division 316—Demutualisation of friendly society health or life insurers

Table of Subdivisions

316‑A Application

Table of sections

316‑1 Application of Division 316 of the Income Tax Assessment Act 1997

316‑1 Application of Division 316 of the Income Tax Assessment Act 1997

Division 316 of the Income Tax Assessment Act 1997 applies in relation to demutualisations occurring on or after 1 July 2008.

Schedule 4—Consolidation: application of losses with nil available fraction

Income Tax Assessment Act 1936

1 At the end of subsection 245‑105(1) in Schedule 2C

Add:

Note: The total net forgiven amount may be reduced under section 707‑415 of the Income Tax Assessment Act 1997.

Income Tax Assessment Act 1997

2 At the end of subsection 104‑520(3)

Add:

Note: The amount remaining may be reduced under section 707‑415.

3 Subsection 243‑35(2) (method statement, at the end of step 1)

Add:

Note: The amount of a capital allowance deduction may be reduced under section 707‑415.

4 At the end of Subdivision 707‑D

Add:

707‑415 Application of losses with nil available fraction for certain purposes

(1) Subsection (2) applies if:

(a) an entity (the joining entity) becomes a *member of a *consolidated group at a time (the joining time); and

(b) a *tax loss or a *net capital loss was transferred from the joining entity to the *head company of the group at the joining time under Subdivision 707‑A; and

(c) that loss is included in a *bundle of losses for which the *available fraction is 0.

(2) The *head company can choose to apply the loss as shown in the table:

Item | If ... | the head company can choose to apply the loss in reduction of ... | for the purposes of ... |

1 | (a) the joining entity owed a debt just before the joining time to an entity that was not a *member of the group at the joining time; and (b) the loss is wholly or partly attributable to the debt; and (c) Subdivision 245‑E in Schedule 2C to the Income Tax Assessment Act 1936 applies in relation to the debt (or another debt that is reasonably connected to the debt) because the debt is forgiven after the joining time | the total net forgiven amount mentioned in subsection 245‑105(1) in that Schedule | applying that total net forgiven amount in accordance with subsections 245‑105(5), (6), (7) and (8) of that Schedule. |

2 | (a) the joining entity owed a *limited recourse debt just before the joining time to an entity that was not a *member of the group at the joining time; and (b) Division 243 applies in relation to the debt; and (c) the loss is wholly or partly attributable to a deduction mentioned in paragraph 243‑15(1)(c) for an income year ending before the joining time | the deduction | working out the excess referred to in subsection 243‑35(1). |

3 | (a) the joining entity ceases to be a *subsidiary member of the group at a time (the leaving time) after the joining time; and (b) the entity’s liabilities at the leaving time are the same as, or are reasonably connected to, the liabilities that it had at the joining time | the amount remaining mentioned in paragraph 104‑520(1)(b) | working out whether *CGT event L5 happens at the leaving time, and if so, the amount of any *capital gain under subsection 104‑520(3). |

Limits on application of loss

(3) The loss can be applied under subsection (2) in relation to an income year only to the extent that it could be *utilised by the *head company for the income year, on the assumption that the *available fraction for the *bundle of losses was 1.

(4) The amount of the loss that may be applied in accordance with item 1 of the table in subsection (2) cannot exceed the gross forgiven amount (within the meaning of section 245‑75 in Schedule 2C to the Income Tax Assessment Act 1936) of the debt to which the loss is attributable.

(5) The amount of the loss that may be applied in accordance with item 2 of the table in subsection (2) cannot exceed the amount of the loss that is attributable to the deduction mentioned in that item.

(6) For the purposes of item 3 of the table in subsection (2), if:

(a) assuming that the joining entity ceased to be a *subsidiary member of the *consolidated group just after the joining time, the *head company of the group would make a *capital gain because of *CGT event L5; and

(b) the sum of the losses in the *bundle of losses mentioned in paragraph (1)(c) exceeds the amount of the capital gain;

the total amount of those losses that may be applied in accordance with that item cannot exceed the amount of the capital gain.

(7) To avoid doubt, a loss can be applied under this section only to the extent that it has not already been applied.

5 Application

The amendments made by this Schedule apply on and after 1 July 2002.

Part 1—References to Ministers, Departments and Secretaries

Division 1—Amendments commencing on Royal Assent

1 Subsection 4(1)

Insert:

Finance Minister has the meaning given by the Income Tax Assessment Act 1997.

2 Subsection 4(1) (definition of Industry Minister)

Repeal the definition.

3 Subsection 4(1)

Insert:

Resources Minister has the meaning given by the Petroleum Resource Rent Tax Assessment Act 1987.

4 At the end of paragraphs 162B(5)(a) and (b)

Add “and”.

5 Subsection 162B(5)

Omit “Minister for Finance”, substitute “Finance Minister”.

6 Paragraph 165A(1)(b)

Omit “Industry Minister”, substitute “Resources Minister”.

7 Paragraph 165A(2)(b)

Omit “Industry Minister”, substitute “Resources Minister”.

8 Subsection 165A(3)

Omit “Industry Minister”, substitute “Resources Minister”.

9 Subsection 165A(4)

Omit “Industry Minister”, substitute “Resources Minister”.

10 Subsection 165A(11)

Omit “Minister for Finance”, substitute “Finance Minister”.

11 Subsection 165A(12)

Omit “Minister for Finance”, substitute “Finance Minister”.

12 Subsection 3(1) (definition of intermediate area)

Omit “Minister for Industry, Science and Resources”, substitute “Resources Minister”.

13 Subsection 3A(1)

Omit “Minister for Industry, Science and Resources”, substitute “Resources Minister”.

Fringe Benefits Tax (Application to the Commonwealth) Act 1986

14 Subsection 3(1)

Insert:

Finance Department means the Department that:

(a) deals with matters arising under section 1 of the Financial Management and Accountability Act 1997; and

(b) is administered by the Finance Minister.

15 Subsection 3(1)

Insert:

Finance Minister has the meaning given by the Income Tax Assessment Act 1997.

16 Subsection 3(1) (at the end of paragraph (a) of the definition of responsible Department)

Add “and”.

17 Subsection 3(1) (paragraph (c) of the definition of responsible Department)

Omit “Department of the Special Minister of State”, substitute “Finance Department”.

18 Subsection 7(1)

Omit “Minister for Finance”, substitute “Finance Minister”.

Note: The heading to section 7 is altered by omitting “Minister for Finance” and substituting “Finance Minister”.

Fringe Benefits Tax Assessment Act 1986

19 Paragraph 47(8)(b)

Omit “Department of Health, Housing, Local Government and Community Services”, substitute “Families Department”.

20 Subsection 136(1)

Insert:

Families Department has the meaning given by the Income Tax Assessment Act 1997.

Income Tax Assessment Act 1936

21 Subsection 6(1)

Insert:

Agriculture Secretary has the meaning given by the Income Tax Assessment Act 1997.

22 Subsection 6(1)

Insert:

Arts Department has the meaning given by the Income Tax Assessment Act 1997.

23 Subsection 6(1)

Insert:

Arts Minister has the meaning given by the Income Tax Assessment Act 1997.

24 Subsection 6(1)

Insert:

Arts Secretary has the meaning given by the Income Tax Assessment Act 1997.

25 Subsection 6(1)

Insert:

Defence Department means the Department that:

(a) deals with matters arising under section 1 of the Defence Act 1903; and

(b) is administered by the Defence Minister.

26 Subsection 6(1)

Insert:

Defence Minister has the meaning given by the Income Tax Assessment Act 1997.

27 Subsection 6(1)

Insert:

Defence Secretary means the Secretary of the Defence Department.

28 Subsection 6(1)

Insert:

Education Department has the meaning given by the Income Tax Assessment Act 1997.

29 Subsection 6(1)

Insert:

Education Secretary means the Secretary of the Education Department.

30 Subsection 6(1)

Insert:

Employment Department means the Department that:

(a) deals with matters arising under section 1 of the Fair Work Act 2009; and

(b) is administered by the Employment Minister.

31 Subsection 6(1)

Insert:

Employment Minister means the Minister administering section 1 of the Fair Work Act 2009.

32 Subsection 6(1)

Insert:

Employment Secretary means the Secretary of the Employment Department.

33 Subsection 6(1)

Insert:

Families Secretary has the meaning given by the Income Tax Assessment Act 1997.

34 Subsection 6(1)

Insert:

Health Department means the Department that:

(a) deals with matters arising under section 1 of the National Health Act 1953; and

(b) is administered by the Health Minister.

35 Subsection 6(1)

Insert:

Health Minister means the Minister administering section 1 of the National Health Act 1953.

36 Subsection 6(1)

Insert:

Health Secretary means the Secretary of the Health Department.

37 Subsection 6(1)