Midwife Professional Indemnity (Run‑off Cover Support Payment) Act 2010

No. 31, 2010

An Act to impose a tax on premium payments for midwife professional indemnity cover, and for related purposes

Midwife Professional Indemnity (Run‑off Cover Support Payment) Act 2010

No. 31, 2010

An Act to impose a tax on premium payments for midwife professional indemnity cover, and for related purposes

Contents

2 Commencement

3 Definitions

4 Imposition of run‑off cover support payment

5 Contribution year

6 Amount of run‑off cover support payment

7 Premium income

8 Rules

9 Regulations

Midwife Professional Indemnity (Run-off Cover Support Payment) Act 2010

No. 31, 2010

An Act to impose a tax on premium payments for midwife professional indemnity cover, and for related purposes

[Assented to 12 April 2010]

The Parliament of Australia enacts:

This Act may be cited as the Midwife Professional Indemnity (Run‑off Cover Support Payment) Act 2010.

This Act commences, or is taken to have commenced, on 1 July 2010.

In this Act, unless the contrary intention appears:

contribution year has the meaning given by section 5.

eligible insurer has the same meaning as in the Midwife Professional Indemnity (Commonwealth Contribution) Scheme Act 2010.

premium income, for a contribution year, has the meaning given by section 7.

run‑off cover support payment means a payment that is payable under Part 3 of the Midwife Professional Indemnity (Commonwealth Contribution) Scheme Act 2010.

4 Imposition of run‑off cover support payment

For each contribution year, a run‑off cover support payment is imposed as a tax on each eligible insurer.

(1) Subject to subsection (2), each:

(a) financial year; or

(b) other period of 12 months specified in the Rules;

that starts on or after 1 July 2010 is a contribution year.

(2) The Rules may declare that a financial year specified in the Rules is the last contribution year. If they do so, no subsequent financial year, or period of 12 months specified in the Rules for the purposes of paragraph (1)(b), is a contribution year.

(3) Rules made for the purposes of paragraph (1)(b) may specify a different period for a particular eligible insurer or class of eligible insurers. If they do so, the reference in subsection (1) to the period is taken, in its application to that insurer or to an insurer of that class, to be a reference to that period for that insurer or class.

6 Amount of run‑off cover support payment

(1) The amount of the run‑off cover support payment imposed on an eligible insurer for a contribution year is the applicable percentage of the insurer’s premium income for:

(a) the period of 12 months ending on 31 May in the contribution year; or

(b) such other period as is specified in the Rules.

(2) The applicable percentage is:

(a) 15%; or

(b) such lower percentage as is specified in the Rules for the contribution year.

(3) Rules made for the purposes of paragraph (1)(b) may specify a different period for a particular eligible insurer or class of eligible insurers. If they do so, the reference in subsection (1) to the period is taken, in its application to that insurer or to an insurer of that class, to be a reference to that period for that insurer or class.

(4) Rules made for the purposes of paragraph (2)(b) may specify a different applicable percentage for a particular eligible insurer or class of eligible insurers. If they do so, the reference in subsection (1) to the applicable percentage is taken, in its application to that insurer or to an insurer of that class, to be a reference to that percentage for that insurer or class.

(1) An eligible insurer’s premium income for a period is the sum of all of the premiums paid during the period to the insurer for midwife professional indemnity cover provided for eligible midwives by contracts of insurance with the insurer, and includes the sum of all amounts paid to the insurer during the period that are amounts of a kind specified in the Rules for the purposes of this subsection.

(2) However, the amount of an eligible insurer’s premium income for a period under subsection (1) is reduced by:

(a) any amount of GST payable during the period for any supply made by the insurer for which premiums and other amounts referred to in subsection (1) are consideration; and

(b) the sum of all amounts of stamp duty payable during the period, under a law of a State or Territory, in connection with midwife professional indemnity cover, or contracts of insurance, referred to in subsection (1); and

(c) the sum of all amounts payable during the period that are amounts of a kind specified in the Rules for the purposes of this subsection; and

(d) the amount worked out under subsection (3).

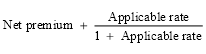

(3) The amount referred to in paragraph (2)(d) is worked out as follows:

where:

applicable rate is the applicable percentage under subsection 6(2) for the insurer, expressed as a decimal fraction.

net premium is the sum of all the premiums referred to in subsection (1) reduced by the amounts referred to in paragraphs (2)(a), (b) and (c) in relation to those premiums.

(4) In this section:

consideration has the same meaning as in the A New Tax System (Goods and Services Tax) Act 1999.

eligible midwife has the same meaning as in the Midwife Professional Indemnity (Commonwealth Contribution) Scheme Act 2010.

GST has the same meaning as in the A New Tax System (Goods and Services Tax) Act 1999.

midwife professional indemnity cover has the same meaning as in the Midwife Professional Indemnity (Commonwealth Contribution) Scheme Act 2010.

supply has the same meaning as in the A New Tax System (Goods and Services Tax) Act 1999.

The Minister may, by legislative instrument, make Rules providing for matters:

(a) required or permitted by this Act to be provided in the Rules; or

(b) necessary or convenient to be provided in order to carry out or give effect to this Act.

The Governor‑General may make regulations prescribing matters:

(a) required or permitted by this Act to be prescribed; or

(b) necessary or convenient to be prescribed for carrying out or giving effect to this Act.

[Minister’s second reading speech made in—

House of Representatives on 24 June 2009

Senate on 9 September 2009]

(136/09)