Tax Laws Amendment (2010 Measures No. 1) Act 2010

No. 56, 2010

An Act to amend the law relating to taxation, and for related purposes

Tax Laws Amendment (2010 Measures No. 1) Act 2010

No. 56, 2010

An Act to amend the law relating to taxation, and for related purposes

Contents

2 Commencement

3 Schedule(s)

4 Amendment of assessments

Schedule 1—Approved superannuation clearing house

Part 1—Main amendments

Retirement Savings Accounts Act 1997

Superannuation Guarantee (Administration) Act 1992

Superannuation Industry (Supervision) Act 1993

Part 2—Amendments conditional on the Tax Laws Amendment (Confidentiality of Taxpayer Information) Act 2010

Income Tax Assessment Act 1936

Taxation Administration Act 1953

Part 3—Application provision

Schedule 2—Forestry managed investment schemes

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Schedule 3—Managed investment trusts

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Taxation Administration Act 1953

Schedule 4—25% entrepreneurs’ tax offset

Income Tax Assessment Act 1997

Schedule 5—Consolidation

Part 1—Use of the tax cost setting amount

Division 1—Main amendments

Income Tax Assessment Act 1997

Division 2—Foreign currency gains and losses

Income Tax Assessment Act 1997

Division 3—Application and transitional provisions

Part 2—Group restructures

Income Tax Assessment Act 1997

Part 3—Pre‑CGT proportions

Income Tax Assessment Act 1997

Part 4—No double counting of amounts in ACA

Income Tax Assessment Act 1997

Part 5—Pre‑joining time roll‑overs

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Part 6—Phasing out over‑depreciation adjustments

Division 1—Joining times between 8 May 2007 and 30 June 2009

Income Tax Assessment Act 1997

Division 2—Repeal of section 705‑50 with effect from 1 July 2009

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Part 7—Leaving time liabilities

Division 1—Timing

Income Tax Assessment Act 1997

Division 2—Adjustment of step 4 amount

Income Tax Assessment Act 1997

Part 8—Accounting principles

Income Tax Assessment Act 1997

Part 9—Inherited deductions

Income Tax Assessment Act 1997

Part 10—General insurance companies

Income Tax Assessment Act 1997

Part 11—Retained cost base assets

Division 1—Cash management trusts

Income Tax Assessment Act 1997

Division 2—Rights to future income assets

Income Tax Assessment Act 1997

Division 3—Application provision

Part 12—Removal of CGT event L7

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Part 13—Reduction in tax cost setting amount that exceeds market value of certain retained cost base assets

Income Tax Assessment Act 1997

Part 14—Blackhole expenditure for MEC Groups

Income Tax Assessment Act 1997

Part 15—Transitional concession for SAPs

New Business Tax System (Consolidation and Other Measures) Act 2003

Part 16—Loss multiplication rules for widely held companies

Income Tax Assessment Act 1997

Part 17—CGT straddles

Income Tax Assessment Act 1997

Part 18—Choice to consolidate

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Taxation Administration Act 1953

Part 19—Life insurance companies

Division 1—Amendments applying before the introduction of first home saver accounts

Income Tax Assessment Act 1997

Division 2—Amendments applying from the introduction of first home savers accounts

Income Tax Assessment Act 1997

Part 20—Non‑membership equity interests

Income Tax Assessment Act 1997

Schedule 6—Miscellaneous amendments

Part 1—CGT main residence exemption for replacement dwelling

Income Tax Assessment Act 1997

Part 2—Small business retirement exemption

Division 1—Main amendment

Income Tax Assessment Act 1997

Division 2—Related amendments

Income Tax Assessment Act 1997

Part 3—Waiver connected with proceeds of crime proceedings

Taxation Administration Act 1953

Part 4—Amendments relating to higher education

A New Tax System (Goods and Services Tax) Act 1999

Fringe Benefits Tax Assessment Act 1986

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Taxation (Interest on Overpayments and Early Payments) Act 1983

Part 5—PAYG withholding from delayed payments for termination of employment

Division 1—Main amendments

Taxation Administration Act 1953

Division 2—Related amendments

Child Support (Registration and Collection) Act 1988

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Part 6—Administrative penalties for false or misleading statements

Division 1—Main amendments

Taxation Administration Act 1953

Division 2—Consequential amendments

Product Grants and Benefits Administration Act 2000

Superannuation Industry (Supervision) Act 1993

Division 3—Application provision

Division 4—Amendments with contingent commencement

Taxation Administration Act 1953

Part 7—Offsets against superannuation guarantee charge

Tax Laws Amendment (2008 Measures No. 2) Act 2008

Part 8—Status of certain superannuation funds

Income Tax Assessment Act 1936

Part 9—Technical corrections

A New Tax System (Luxury Car Tax) Act 1999

Taxation Administration Act 1953

Tax Laws Amendment (2009 Measures No. 4) Act 2009

Part 10—Repeal of redundant material

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Part 11—Other minor changes

A New Tax System (Goods and Services Tax) Act 1999

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Taxation Administration Act 1953

Tax Laws Amendment (2010 Measures No. 1) Act 2010

No. 56, 2010

An Act to amend the law relating to taxation, and for related purposes

[Assented to 3 June 2010]

The Parliament of Australia enacts:

This Act may be cited as the Tax Laws Amendment (2010 Measures No. 1) Act 2010.

(1) Each provision of this Act specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information | ||

Column 1 | Column 2 | Column 3 |

Provision(s) | Commencement | Date/Details |

1. Sections 1 to 4 and anything in this Act not elsewhere covered by this table | The day this Act receives the Royal Assent. | 3 June 2010 |

2. Schedule 1, Part 1 | 1 July 2010. | 1 July 2010 |

3. Schedule 1, item 7 | 1 July 2010. However, if item 32 of Schedule 2 to the Tax Laws Amendment (Confidentiality of Taxpayer Information) Act 2010 commences on or before 1 July 2010, the provision(s) do not commence at all. | 1 July 2010 |

4. Schedule 1, item 8 | The later of: (a) the start of 1 July 2010; and (b) immediately after the commencement of item 1 of Schedule 1 to the Tax Laws Amendment (Confidentiality of Taxpayer Information) Act 2010. However, the provision(s) do not commence at all if the event mentioned in paragraph (b) does not occur. | 17 December 2010 (paragraph (b) applies) |

5. Schedule 1, Part 3 | 1 July 2010. | 1 July 2010 |

6. Schedule 2 | The day after this Act receives the Royal Assent. | 4 June 2010 |

7. Schedules 3 and 4 | The day this Act receives the Royal Assent. | 3 June 2010 |

8. Schedule 5, Parts 1 to 5 | The day this Act receives the Royal Assent. | 3 June 2010 |

9. Schedule 5, Part 6, Division 1 | The day this Act receives the Royal Assent. | 3 June 2010 |

10. Schedule 5, Part 6, Division 2 | Immediately after the commencement of the provision(s) covered by table item 9. | 3 June 2010 |

11. Schedule 5, Parts 7 to 18 | The day this Act receives the Royal Assent. | 3 June 2010 |

12. Schedule 5, Part 19, Division 1 | The day this Act receives the Royal Assent. | 3 June 2010 |

13. Schedule 5, Part 19, Division 2 | Immediately after the commencement of the provision(s) covered by table item 12. | 3 June 2010 |

14. Schedule 5, Part 20 | The day this Act receives the Royal Assent. | 3 June 2010 |

15. Schedule 6, Parts 1 to 5 | The day this Act receives the Royal Assent. | 3 June 2010 |

16. Schedule 6, Part 6, Divisions 1 to 3 | The day after this Act receives the Royal Assent. | 4 June 2010 |

17. Schedule 6, Part 6, Division 4 | The later of: (a) the start of the day after this Act receives the Royal Assent; and (b) immediately after the commencement of item 23 of Schedule 1 to the Tax Agent Services (Transitional Provisions and Consequential Amendments) Act 2009. | 4 June 2010 (paragraph (a) applies) |

18. Schedule 6, Part 7 | Immediately after the commencement of Schedule 2 to the Tax Laws Amendment (2008 Measures No. 2) Act 2008. | 24 June 2008 |

19. Schedule 6, Part 8 | 1 July 2006. | 1 July 2006 |

20. Schedule 6, items 109 to 111 | The day this Act receives the Royal Assent. | 3 June 2010 |

21. Schedule 6, item 112 | Immediately after the time specified in the Tax Laws Amendment (2009 Measures No. 4) Act 2009 for the commencement of item 132 of Schedule 5 to that Act. | 18 September 2009 |

22. Schedule 6, item 113 | Immediately after the time specified in the Tax Laws Amendment (2009 Measures No. 4) Act 2009 for the commencement of item 133 of Schedule 5 to that Act. | 18 September 2009 |

23. Schedule 6, Parts 10 and 11 | The day this Act receives the Royal Assent. | 3 June 2010 |

Note: This table relates only to the provisions of this Act as originally passed by both Houses of the Parliament and assented to. It will not be expanded to deal with provisions inserted in this Act after assent.

(2) Column 3 of the table contains additional information that is not part of this Act. Information in this column may be added to or edited in any published version of this Act.

Each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

(1) Section 170 of the Income Tax Assessment Act 1936 does not prevent the amendment of an assessment if:

(a) the assessment was made before the commencement of Schedule 2 to this Act; and

(b) the amendment is made for the purpose of giving effect to item 1 or 2 of that Schedule; and

(c) the amendment is made within 4 years after the end of the income year in which the relevant CGT event happened.

(2) Section 170 of the Income Tax Assessment Act 1936 does not prevent the amendment of an assessment if:

(a) the assessment was made before the commencement of this section; and

(b) the amendment is made within 2 years after that commencement; and

(c) the amendment is made for the purpose of giving effect to Schedule 5 to this Act.

Schedule 1—Approved superannuation clearing house

Retirement Savings Accounts Act 1997

1 After subsection 183(2)

Insert:

(2A) Subsection (2) does not apply if:

(a) the employer pays to an approved clearing house (within the meaning of the Superannuation Guarantee (Administration) Act 1992) the amount of the deduction before the end of period mentioned in that subsection; and

(b) the approved clearing house accepts the payment.

Superannuation Guarantee (Administration) Act 1992

2 Subsection 6(1)

Insert:

approved clearing house has the meaning given by subsection 79A(3).

3 After section 23A

Insert:

23B Contributions through an approved clearing house

For the purposes of sections 23 and 23A:

(a) treat an employer that, at a particular time, pays an amount to an approved clearing house for the benefit of an employee as having made a contribution of the same amount to a complying superannuation fund or an RSA for the benefit of the employee at that time, if the approved clearing house accepts the payment; and

(b) disregard any contribution that the approved clearing house makes to a complying superannuation fund or an RSA as a result of the payment.

4 After subsection 32C(2A)

Insert:

Contributions through an approved clearing house

(2B) A contribution to a fund by an employer for the benefit of an employee is made in compliance with the choice of fund requirements if:

(a) section 79A (which is about a contribution through an approved clearing house) applies to the contribution; and

(b) the employee gives the employer written notice to the effect that the employee wants a fund to be a chosen fund for the employee in accordance with Division 4 of Part 3A (Choosing a fund); and

Note: Under section 32G (Limit on funds that may be chosen), the fund chosen by the employee must be an eligible choice fund and must be a fund to which the employer can make contributions.

(c) the employer passes onto the approved clearing house mentioned in section 79A the information that the employee included in the written notice, and any other prescribed information:

(i) within 21 days after the employee gives the notice to the employer; and

(ii) before or at the time the contribution is made; and

(d) the approved clearing house accepts the information.

5 After section 79

Insert:

(1) This section applies if:

(a) an employer pays an amount to an approved clearing house for the benefit of an employee; and

(b) as a result, the approved clearing house makes a contribution to an RSA, a superannuation fund or a superannuation scheme for the benefit of the employee.

(2) To avoid doubt, the approved clearing house makes the contribution to the RSA, superannuation fund or superannuation scheme on behalf of the employer, as the employer’s agent.

(3) Approved clearing house means a body specified in the regulations for the purposes of this subsection.

Superannuation Industry (Supervision) Act 1993

6 After subsection 64(2)

Insert:

(2A) Subsection (2) does not apply if:

(a) the employer pays to an approved clearing house (within the meaning of the Superannuation Guarantee (Administration) Act 1992) the amount of the deduction before the end of the period mentioned in that subsection; and

(b) the approved clearing house accepts the payment.

Income Tax Assessment Act 1936

7 After paragraph 16(4)(hba)

Insert:

(hbb) an approved clearing house (within the meaning of the Superannuation Guarantee (Administration) Act 1992), for the purposes of that body performing its functions in relation to superannuation contributions; or

Taxation Administration Act 1953

8 Subsection 355‑65(3) in Schedule 1 (at the end of the table)

Add:

9 | an approved clearing house (within the meaning of the Superannuation Guarantee (Administration) Act 1992) | is for the purposes of that body performing its functions in relation to superannuation contributions. |

9 Application provision

The amendments made by Part 1 of this Schedule apply to a payment made to an approved clearing house on or after the commencement of this item.

Schedule 2—Forestry managed investment schemes

Income Tax Assessment Act 1936

1 After subsection 82KZMGA(1)

Insert:

(1A) Paragraph (1)(b) does not apply to a CGT event if:

(a) the CGT event happens because of circumstances outside the taxpayer’s control; and

Example: The interest is compulsorily acquired.

(b) when the taxpayer acquired the interest, the taxpayer could not reasonably have foreseen the CGT event happening.

Income Tax Assessment Act 1997

2 After subsection 394‑10(5)

Insert:

(5A) Paragraph (5)(b) does not apply to a *CGT event if:

(a) the CGT event happens because of circumstances outside your control; and

Example: The forestry interest is compulsorily acquired.

(b) when you acquired the *forestry interest, you could not reasonably have foreseen the CGT event happening.

Taxation Administration Act 1953

3 After subsection 290‑50(2) in Schedule 1

Insert:

(2A) For the purposes of subsection (2), disregard:

(a) subsection 82KZMGA(1A) of the Income Tax Assessment Act 1936; and

(b) subsection 394‑10(5A) of the Income Tax Assessment Act 1997.

Note 1: Those 2 subsections relate to forestry managed investment schemes.

Note 2: The effect of this subsection is that a scheme will have been implemented in a way that is materially different from that described in a product ruling if the tax outcome for participants in the scheme is the same as that described in the ruling only because of the operation of the subsections mentioned in paragraphs (a) and (b).

4 Application provision

The amendments made by this Schedule apply to CGT events that happen on or after 1 July 2007.

Schedule 3—Managed investment trusts

Income Tax Assessment Act 1936

1 Subsection 95(1) (at the end of the note to the definition of net income)

Add “to this Act or Division 275 of the Income Tax Assessment Act 1997”.

Income Tax Assessment Act 1997

2 Section 10‑5 (after table item headed “lotteries”)

Insert:

managed investment trusts |

|

gains etc. from carried interests ................. | 275‑200(2) |

3 Section 12‑5 (after table item headed “losses”)

Insert:

managed investment trusts |

|

losses from carried interests ................... | 275‑200(4) |

4 After Part 3‑10

Insert:

Part 3‑25—Particular kinds of trusts

Division 275—Australian managed investment trusts

Table of Subdivisions

Guide to Division 275

275‑A Extended concept of managed investment trust for the purposes of this Division

275‑B Choice for capital treatment of managed investment trust gains and losses

275‑C Carried interests in managed investment trusts

275‑1 What this Division is about

The trustee of certain Australian managed investment trusts may make a choice that certain assets of the trust be dealt with under CGT rules. If the trustee does not make such a choice, those assets will be treated as revenue assets (see Subdivision 275‑B).

Gains and profits from carried interests held in entities that are or were Australian managed investment trusts are included in the assessable income of the holder of the interests. The holder is entitled to a deduction from losses from such interests (see Subdivision 275‑C).

Subdivision 275‑A—Extended concept of managed investment trust for the purposes of this Division

Table of sections

275‑5 Trust operated or managed by a financial services licensee etc.

275‑10 Managed investment schemes that are not subject to requirement to be operated by financial services licensee

275‑15 Every member of trust is a managed investment trust

275‑20 No fund payment made in relation to the income year

275‑25 Trust held by small group not to be treated as managed investment trust

275‑30 Temporary circumstances outside the control of the trustee

275‑35 Application of subsections 102L(15) and 102T(16)

275‑15 Every member of trust is a managed investment trust

(1) For the purposes of this Division, treat a trust in the same way as a *managed investment trust in relation to an income year if:

(a) the condition in item 1 of the table in subsection 12‑400(1) in Schedule 1 to the Taxation Administration Act 1953 is satisfied; and

(b) every *member of the trust is a managed investment trust in relation to the income year (or a trust that is treated in the same way as a managed investment trust in relation to the income year through the operation of this Subdivision).

(2) A requirement in paragraph (1)(a) is satisfied if, and only if, it is satisfied:

(a) at the time the trustee of the trust makes the first *fund payment in relation to the income year; or

(b) if the trustee does not make such a payment in relation to the income year—at both the start and the end of the income year.

275‑20 No fund payment made in relation to the income year

For the purposes of this Division, treat a trust in the same way as a *managed investment trust in relation to an income year if:

(a) the trustee of the trust does not make a *fund payment in relation to the income year; and

(b) the trust would be a managed investment trust in relation to the income year (or a trust that would be treated in the same way as a managed investment trust in relation to the income year through the operation of this Subdivision) if the trustee of the trust had made the first fund payment in relation to the income year on the first day of the income year; and

(c) the trust would be a managed investment trust in relation to the income year (or a trust that would be treated in the same way as a managed investment trust in relation to the income year through the operation of this Subdivision) if the trustee of the trust had made the first fund payment in relation to the income year on the last day of the income year.

275‑30 Temporary circumstances outside the control of the trustee

If, apart from a particular circumstance, a trust would be treated under this Subdivision in the same way as a *managed investment trust in relation to an income year, treat the trust in the same way as a managed investment trust in relation to the income year for the purposes of this Division if:

(a) the circumstance is temporary; and

(b) the circumstance arose outside the control of the trustee of the trust; and

(c) it is fair and reasonable to treat the trust as a managed investment trust in relation to the income year, having regard to the following matters:

(i) the matters in paragraphs (a) and (b);

(ii) the nature of the circumstance;

(iii) the actions (if any) taken by the trustee of the trust to address or remove the circumstance, and the speed with which such actions are taken;

(iv) the extent to which treating the trust as a managed investment trust in relation to the income year would increase or reduce the amount of tax otherwise payable by the trustee, the beneficiaries of the trust or any other entity;

(v) any other relevant matter.

275‑35 Application of subsections 102L(15) and 102T(16)

To avoid doubt, subsections 102L(15) and 102T(16) of the Income Tax Assessment Act 1936 do not apply for the purposes of this Division.

Subdivision 275‑B—Choice for capital treatment of managed investment trust gains and losses

Table of sections

275‑100 Consequences of making choice—CGT to be primary code for calculating MIT gains or losses

275‑105 Covered assets

275‑110 MIT not to be corporate unit trust or trading trust

275‑115 MIT CGT choices

275‑120 Consequences of not making choice—revenue account treatment

275‑100 Consequences of making choice—CGT to be primary code for calculating MIT gains or losses

(1) The modifications in subsection (2) apply if:

(a) a *CGT event happens at a time involving a *CGT asset; and

(b) the CGT asset is owned at that time by an entity that is a *managed investment trust in relation to the income year in which the time occurs; and

(c) the CGT event happens because the managed investment trust *disposes of, ceases to own or otherwise realises the asset; and

(d) the asset is covered by section 275‑105; and

(e) the entity meets the requirement in section 275‑110 at the time; and

(f) a choice under section 275‑115 covering the entity is in force for the income year in which the time occurs.

(2) These provisions do not apply to the *CGT event:

(a) sections 6‑5 (about *ordinary income), 8‑1 (about amounts you can deduct), and 15‑15 and 25‑40 (about profit‑making undertakings or plans);

(b) sections 25A and 52 of the Income Tax Assessment Act 1936 (about profit‑making undertakings or schemes);

(c) section 118‑20 (about reducing capital gains if amount otherwise assessable);

(d) Division 70 and section 118‑25 (about trading stock).

General exceptions

(3) The provisions referred to in subsection (2) can apply to the *CGT event if a *capital gain or *capital loss from the event is disregarded because of one of the provisions in this table:

Where gain or loss disregarded because of CGT provision | ||

Item | Provision | Brief description |

1 | Paragraph 104‑15(4)(a) | Title in a CGT asset does not pass when a hire purchase or similar agreement ends |

2 | Section 118‑13 | Shares in a PDF |

3 | Section 118‑60 | Certain gifts |

Trading stock and profit‑making undertakings or plans involving land etc.

(4) The provisions referred to in subsection (2) can also apply to the *CGT event if:

(a) where the *CGT asset is land (including an interest in land), or a right or option to *acquire or *dispose of land (including an interest in land):

(i) the CGT asset is *trading stock; or

(ii) the circumstances existing at the time of the event would, disregarding this Subdivision, give rise to an amount being included in the assessable income of the entity under section 15‑15 or to a deduction for the entity under section 25‑40 (about profit‑making undertakings or plans); or

(b) where paragraph (a) does not apply:

(i) the *managed investment trust acquired the CGT asset in an income year for which the choice mentioned in paragraph (1)(f) was not in force; and

(ii) the CGT asset was treated as trading stock in the managed investment trust’s financial report for the most recent income year ending before the start of the income year in which that choice first came into force; and

(iii) the CGT asset was treated as trading stock in the *income tax return for the managed investment trust for the most recent income year ending before the start of the income year in which that choice first came into force; and

(iv) the CGT asset was treated as trading stock in the managed investment trust’s financial report for the most recent income year ending before the time of the event; and

(v) the CGT asset was treated as trading stock in the income tax return for the managed investment trust for the most recent income year ending before the time of the event.

Treatment of outgoings to acquire trading stock

(5) The modifications in subsection (6) apply if:

(a) an entity that is a *managed investment trust in relation to the income year *acquires a *CGT asset at a time in that income year; and

(b) the CGT asset is an item of *trading stock; and

(c) the CGT asset is not land (including an interest in land), or a right or option to acquire or *dispose of land (including an interest in land); and

(d) the entity incurs an outgoing in connection with acquiring the asset; and

(e) the asset is covered by section 275‑105; and

(f) the entity meets the requirement in section 275‑110 at the time; and

(g) a choice under section 275‑115 covering the entity is in force for the income year in which the time occurs.

(6) The modifications are as follows:

(a) section 8‑1 (about amounts you can deduct) does not apply to the *acquisition;

(b) Division 70 (about trading stock) does not apply in relation to the asset in respect of:

(i) the income year in which the time occurs; and

(ii) any later income year in relation to which the entity is a *managed investment trust and throughout which the entity meets the requirement in section 275‑110.

(1) An asset is covered by this section if it is any of the following:

(a) a *share in a company (including a share in a *foreign hybrid company);

(b) a *non‑share equity interest in a company;

(c) a unit in a unit trust;

(d) land (including an interest in land);

(e) a right or option to *acquire or *dispose of an asset of a kind mentioned in paragraph (a), (b), (c) or (d).

(2) However, the asset is not covered by this section if it is any of the following:

(a) a *Division 230 financial arrangement;

(b) a *debt interest.

275‑110 MIT not to be corporate unit trust or trading trust

(1) An entity that is a trust meets the requirement in this section at a time if the entity is not any of the following at that time:

(a) a corporate unit trust (within the meaning of section 102J of the Income Tax Assessment Act 1936) in relation to the income year in which the time occurs;

(b) a trading trust for the purposes of Division 6C of Part III of that Act in relation to that income year.

(2) If, apart from a particular circumstance, a trust would meet the requirement in paragraph (1)(b) at a time, the trust also meets the requirement in this section at a time if:

(a) the circumstance is temporary; and

(b) the circumstance arose outside the control of the trustee of the trust; and

(c) the trustee of the trust is not liable to pay income tax on the net income of the trust under section 102S of the Income Tax Assessment Act 1936 for the income year in which the time occurs; and

(d) it is fair and reasonable to treat the trust as meeting the requirement in this section at that time, having regard to the following matters:

(i) the matters in paragraphs (a), (b) and (c);

(ii) the nature of the circumstance;

(iii) the actions (if any) taken by the trustee of the trust to address or remove the circumstance, and the speed with which such actions are taken;

(iv) the extent to which treating the trust as meeting the requirement in this section at that time would increase or reduce the amount of tax otherwise payable by the trustee, the beneficiaries of the trust or any other entity;

(v) any other relevant matter.

(1) The trustee of an entity that is a *managed investment trust may make a choice under this section that covers the managed investment trust.

(2) The choice must be made in the *approved form.

(3) The choice can be made only:

(a) if the entity became a *managed investment trust in the 2009‑10 income year or a later income year (whether or not the entity existed before it became a managed investment trust)—on or before the latest of the following days:

(i) the day it is required to lodge its *income tax return for the income year in which it became a managed investment trust;

(ii) if the Commissioner allows a later day for the managed investment trust—that later day; or

(b) otherwise—on or before the latest of the following days:

(i) the last day in the 3 month period starting on the day on which this section commences;

(ii) the last day of the 2009‑10 income year;

(iii) if the Commissioner allows a later day for the managed investment trust—that later day.

(4) The choice, once made, cannot be revoked.

(5) The choice is in force:

(a) in the circumstances mentioned in paragraph (3)(a)—for the income year in which the entity became a *managed investment trust (whether or not the entity existed before it became a managed investment trust) and later income years; or

(b) in the circumstances mentioned in paragraph (3)(b)—for the 2008‑09 income year and later income years.

275‑120 Consequences of not making choice—revenue account treatment

(1) This section applies if:

(a) the requirements in subsection 275‑100(1) are met in relation to a *CGT asset held by a *managed investment trust, apart from the requirement in paragraph 275‑100(1)(f); and

(b) the CGT asset is not:

(i) land (including an interest in land); or

(ii) a right or option to *acquire or *dispose of land (including an interest in land); and

(c) the managed investment trust disposes of, ceases to own or otherwise realises the asset; and

(d) disregarding this section:

(i) the net proceeds (if any) from the disposal, cessation or realisation would not be reflected in an amount being included in the assessable income of the managed investment trust (other than under Part 3‑1 or 3‑3); and

(ii) the gain or profit (if any) on the disposal, cessation or realisation would not be reflected in an amount being included in the assessable income of the managed investment trust (other than under Part 3‑1 or 3‑3); and

(iii) the loss (if any) on the disposal, cessation or realisation would not be reflected in an amount being deductible by the managed investment trust.

(2) For the purposes of this Act, treat the disposal, cessation of ownership of or realisation of the asset in the same way as the disposal, cessation of ownership of or realisation of a *revenue asset.

Subdivision 275‑C—Carried interests in managed investment trusts

Table of sections

275‑200 Gains and losses etc. from carried interests in managed investment trusts reflected in assessable income or deduction

(1) This section applies if:

(a) you hold a *CGT asset in an income year that carries an entitlement to a distribution from an entity; and

(b) the entitlement to such a distribution is contingent upon the attainment of profits by the entity; and

(c) the entity satisfies any of these requirements:

(i) it is a *managed investment trust in relation to the income year;

(ii) it was a managed investment trust in relation to a previous income year; and

(d) you acquired the asset because of services you or your *associate provided, or will provide, to the entity; and

(e) you or your associate provided, or will provide, those services:

(i) as a manager of the entity; or

(ii) as an associate of a manager of the entity; or

(iii) as an employee of a manager of the entity; or

(iv) as an associate of an employee of a manager of the entity; and

(f) any of the following apply:

(i) you become entitled in the income year to such a distribution (regardless of whether the distribution is made immediately, or is to be made in the future);

(ii) a *CGT event happens in relation to the asset in the income year.

(2) Include in your assessable income for the income year:

(a) the amount of the distribution (except to the extent that it represents a return of capital that you or your associate contributed in order for you to *acquire the asset); or

(b) the amount of your gain or profit (if any) on the *CGT event.

(3) Subsection (2) does not apply to the extent that the amount is included in your assessable income as:

(a) *ordinary income under section 6‑5; or

(b) *statutory income under a section of this Act, other than a provision in Part 3‑1 or 3‑3.

(4) An amount to which subsection (2) applies is taken, for the purposes of the *income tax laws, to have a source in Australia. For the purposes of this subsection, disregard subsection (3).

(5) You are entitled to a deduction for the income year for the amount of your loss (if any) on the *CGT event.

(6) Subsection (5) does not apply to the extent that you can deduct the amount under another provision of this Act.

(7) Subdivision 115‑C does not apply to the amount of a distribution mentioned in subparagraph (1)(f)(i) if:

(a) that amount is included in your assessable income under subsection (2); or

(b) an amount referable to that amount is included in your assessable income under Division 6 of Part III of the Income Tax Assessment Act 1936.

5 Subsection 840‑805(6) (subsection heading)

Repeal the heading, substitute:

Exception—Australian permanent establishments

6 At the end of section 840‑805

Add:

Exception—distributions on carried interests

(7) Subsections (2) and (3) do not apply to you to the extent that the fund payment part:

(a) is included in your assessable income under subsection 275‑200(2) (Gains etc. from carried interests) for the income year because you hold or held a *CGT asset that carries an entitlement to a distribution mentioned in subsection 275‑200(2); or

(b) would be so included if subsection 275‑200(3) were disregarded.

(8) Subsection (4) does not apply to you to the extent that the fund payment part:

(a) is attributable to an amount included in the net income of the trust mentioned in that subsection because of subsection 275‑200(2) (Gains etc. from carried interests) for the income year because the trust holds or held a *CGT asset that carries an entitlement to a distribution mentioned in subsection 275‑200(2); or

(b) would be so included if subsection 275‑200(3) were disregarded.

7 Subsection 995‑1(1) (definition of instalment income)

Omit “and 45‑465”, substitute “, 45‑286 and 45‑465”.

Income Tax (Transitional Provisions) Act 1997

8 After Part 3‑10

Insert:

Part 3‑25—Particular kinds of trusts

Division 275—Australian managed investment trusts

Table of Subdivisions

275‑A Choice for capital treatment of MIT gains and losses

Subdivision 275‑A—Choice for capital treatment of MIT gains and losses

Table of sections

275‑10 Consequences of making choice—Commissioner cannot make certain amendments to previous assessments

(1) This section applies if:

(a) the trustee of a managed investment trust makes a choice under section 275‑115 of the Income Tax Assessment Act 1997 covering the trust that is in force for the 2008‑09 income year; and

(b) the Commissioner made an assessment (the previous assessment) for a previous income year for any of the following entities:

(i) the trustee of the managed investment trust;

(ii) a beneficiary of the managed investment trust;

(iii) an entity that holds interests in the managed investment trust indirectly, through a chain of trusts; and

(c) the previous assessment was made on the basis that:

(i) a CGT event happened at a time involving a CGT asset that was owned by the managed investment trust; and

(ii) a gain or loss was realised for income tax purposes because of the circumstances that gave rise to the CGT event; and

(d) the previous assessment was also made on the basis that:

(i) the gain or loss should be reflected in the net income of the managed investment trust for that previous income year; or

(ii) the gain or loss should be reflected in a tax loss or net capital loss of the managed investment trust for that previous income year; and

(e) the previous assessment was also made on one of these bases:

(i) the CGT asset was a revenue asset;

(ii) the CGT asset was not a revenue asset; and

(f) none of the provisions mentioned in subsection 275‑100(2) of the Income Tax Assessment Act 1997 would have applied at the time of the CGT event in relation to the asset, if these assumptions were made:

(i) Subdivision 275‑B of the Income Tax Assessment Act 1997 (and any other provision of that Act or of the Income Tax Assessment Act 1936, to the extent that it relates to that Subdivision) had applied in relation to the CGT event;

(ii) a choice under section 275‑115 of the Income Tax Assessment Act 1997 covering the entity for which the assessment was made was in force for the previous income year.

(2) The Commissioner cannot amend the previous assessment on the basis that:

(a) if subparagraph (1)(e)(i) applies—the CGT asset should not have been treated as a revenue asset; or

(b) if subparagraph (1)(e)(ii) applies—the CGT asset should have been treated as a revenue asset.

(3) Subsection (2) applies despite any other provision of this Act (apart from subsection (4) of this section), the Income Tax Assessment Act 1997 and the Income Tax Assessment Act 1936.

(4) Subsection (2) does not apply in any of these cases:

(a) if the entity for which the assessment was made gives the Commissioner a written consent to the amendment;

(b) if the Commissioner may amend the assessment in accordance with item 5 (fraud or evasion) or 6 (review or appeal) of the table in subsection 170(1) of the Income Tax Assessment Act 1936;

(c) if the amendment is made for the purpose of giving effect to a provision specified in the regulations for the purposes of this paragraph.

Taxation Administration Act 1953

9 After section 45‑285 in Schedule 1

Insert:

45‑286 Instalment income includes distributions by certain managed investment trusts

Your instalment income for a period includes trust income or trust capital that a trust distributes to you, or applies for your benefit, during that period if:

(a) the income or capital is not included in your instalment income under section 45‑280 or 45‑285; and

(b) the trust satisfies the condition in item 1 of the table in subsection 12‑400(1) in relation to the income year that is or includes that period; and

(c) the trust is:

(i) a *managed investment trust for that income year; or

(ii) treated as a managed investment trust for that income year for the purposes of Division 275 of the Income Tax Assessment Act 1997; and

(d) the trust meets the requirement in section 275‑110 of that Act throughout the income year.

(It does not matter whether the trust income or trust capital is included in your assessable income for the income year that is or includes that period.)

10 Application provision

(1) The amendments made by this Schedule apply in relation to CGT events that happen on or after the start of the 2008‑09 income year.

(2) Despite subitem (1), subsections 275‑100(5) and (6) of the Income Tax Assessment Act 1997 as inserted by this Schedule (and any other provision inserted by this Schedule, to the extent that it relates to those subsections) apply in relation to acquisitions of assets that happen on or after the start of the 2008‑09 income year.

(3) Despite subitem (1), section 275‑120 of the Income Tax Assessment Act 1997 as inserted by this Schedule (and any other provision inserted by this Schedule, to the extent that it relates to that section) applies in relation to:

(a) disposals of assets; and

(b) cessations of ownership of assets; and

(c) other realisations of assets;

that happen on or after the commencement of this item.

(4) Despite subitem (1), Subdivision 275‑C of the Income Tax Assessment Act 1997 as inserted by this Schedule (and any other provision inserted by this Schedule, to the extent that it relates to that Subdivision) applies in relation to:

(a) entitlements to distributions that arise on or after the commencement of this item; and

(b) CGT events that happen on or after the commencement of this item.

(5) Despite subitem (1), section 45‑286 in Schedule 1 to the Taxation Administration Act 1953 as inserted by this Schedule (and any other provision inserted by this Schedule, to the extent that it relates to that section) applies in relation to distributions or applications of benefits that are made on or after the commencement of this item.

Schedule 4—25% entrepreneurs’ tax offset

Income Tax Assessment Act 1997

1 Section 61‑500

Omit:

Your entitlement to the offset varies depending on what kind of entity you are. The amount of your offset varies depending on whether your aggregated turnover is $50,000 or less or is more than $50,000.

Substitute:

Your entitlement to the offset varies depending on what kind of entity you are. The amount of your offset varies depending on:

(a) whether your aggregated turnover is $50,000 or less or is more than $50,000; and

(b) if you are an individual—whether you (and your spouse, if you have a spouse) have significant income from sources other than your small business.

2 Subsection 61‑505(2) (at the end of step 4 of the method statement)

Add:

Note: If you are an individual, section 61‑523 may reduce the amount of the tax offset.

3 Subsection 61‑505(2) (at the end of step 5 of the method statement)

Add:

Note: If you are an individual, section 61‑523 may reduce the amount of the tax offset.

4 Subsection 61‑510(2) (at the end of step 4 of the method statement)

Add:

Note: If you are an individual, section 61‑523 may reduce the amount of the tax offset.

5 Subsection 61‑510(2) (at the end of step 5 of the method statement)

Add:

Note: If you are an individual, section 61‑523 may reduce the amount of the tax offset.

6 Subsection 61‑520(2) (at the end of step 4 of the method statement)

Add:

Note: If you are an individual, section 61‑523 may reduce the amount of the tax offset.

7 Subsection 61‑520(2) (at the end of step 5 of the method statement)

Add:

Note: If you are an individual, section 61‑523 may reduce the amount of the tax offset.

8 After section 61‑520

Insert:

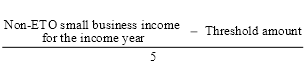

61‑523 25% entrepreneurs’ tax offset—reduction for non‑small business income

Reduce the amount of your *tax offset worked out under subsection 61‑505(2), 61‑510(2) or 61‑520(2) by the amount worked out using the following formula (but not below nil), if:

(a) you are an individual; and

(b) the amount worked out using the formula is greater than nil:

where:

non‑ETO small business income for the income year is worked out by:

(a) adding up the following:

(i) your taxable income for the year;

(ii) your *reportable fringe benefits total for the year;

(iii) your *reportable superannuation contributions (if any) for the year;

(iv) your *total net investment loss for the year; and

(b) subtracting:

(i) in a case covered by subsection 61‑505(2)—your *net small business income for the year; or

(ii) in a case covered by subsection 61‑510(2) or 61‑520(2)—your net small business income share for the year (within the meaning of paragraph 61‑510(1)(e) or 61‑520(1)(e), whichever is applicable); and

(c) adding the following in relation to each individual (if any) who, on the last day of the year, is your *spouse:

(i) your spouse’s taxable income for the year;

(ii) your spouse’s reportable fringe benefits total for the year;

(iii) your spouse’s reportable superannuation contributions (if any) for the year;

(iv) your spouse’s total net investment loss for the year.

Note: ETO is short for 25% entrepreneurs’ tax offset.

threshold amount means:

(a) $120,000 if:

(i) on any day during the income year, you have a dependant (within the meaning of the definition of dependant in subsection 159P(4) of the Income Tax Assessment Act 1936, disregarding paragraph (a) (spouse) of that definition); or

(ii) on the last day of the income year, you have a *spouse; or

(b) otherwise—$70,000.

9 Application provision

The amendments made by this Schedule apply in relation to assessments for income years that commence on or after 1 July 2009.

Part 1—Use of the tax cost setting amount

Income Tax Assessment Act 1997

1 Section 12‑5 (table item headed “financial arrangements” (first occurring))

Repeal the item, substitute:

consolidated groups and MEC groups |

|

assets in relation to Division 230 financial arrangement . | 701‑61(4) |

rights to future income ....................... | 716‑405 |

2 Subsection 701‑55(3)

After “Division 70”, insert “(other than Subdivision 70‑E)”.

3 Subsection 701‑55(6)

Repeal the subsection, substitute:

Rights to future amounts to be included in assessable income of head company

(5C) If section 716‑410 (rights to future amounts that are expected to be included in assessable income) covers the asset at the particular time, the expression means that section 716‑405 may apply in relation to the asset after the particular time.

Other provisions

(6) If any provision of this Act that is not mentioned above is to apply in relation to the asset by including an amount in assessable income, or by allowing an amount as a deduction, in a way that brings into account (directly or indirectly) any of the following amounts:

(a) the cost of the asset;

(b) outgoings incurred, or amounts paid, in respect of the asset;

(c) expenditure in respect of the asset;

(d) an amount of a similar kind in respect of the asset;

the expression means that the provision applies, for the purpose of determining the amount included in assessable income or the amount of the deduction, as if the cost, outgoing, expenditure or other amount had been incurred or paid to acquire the asset at the particular time for an amount equal to its tax cost setting amount.

Note 1: This subsection modifies the application of the provision only for the purpose of determining the amount included in assessable income or the amount of the deduction. Therefore:

(a) the acquisition mentioned in this subsection is recognised only for that purpose; and

(b) apart from the things mentioned in subsection 701‑56(1), that acquisition does not affect the operation of section 701‑5 (the entry history rule) in relation to the asset for other purposes.

Note 2: For specific clarifications of the operation of this subsection in relation to bad debts, see Subdivision 716‑S.

701‑56 Setting the tax cost of an asset—subsection 701‑55(6)

Entry history rule

(1) To avoid doubt, if subsection 701‑55(6) applies in relation to an asset at the time (the joining time) an entity (the joining entity) became a *subsidiary member of a *consolidated group, the things that are taken to have happened in relation to the *head company of the group under section 701‑5 (entry history rule) do not include:

(a) the cost, outgoing, expenditure or other amount incurred or paid to acquire the asset by the joining entity; and

(b) whether the cost, outgoing, expenditure or other amount incurred or paid by the joining entity to acquire the asset has been deducted by the joining entity before the joining time.

Trading stock

(2) Subsection 701‑55(6) does not apply in relation to an asset if it is *trading stock.

Certain depreciating assets etc.

(3) Subsection 701‑55(6) does not apply in relation to an asset if any of the following provisions are to apply in relation to the asset:

(a) Subdivision 40‑F (Primary production depreciating assets);

(b) Subdivision 40‑G (Capital expenditure of primary producers and other landholders);

(c) Subdivision 40‑H (Capital expenditure that is immediately deductible);

(d) Subdivision 40‑I (Capital expenditure that is deductible over time), other than section 40‑880 (Business related costs);

(e) Subdivision 40‑J (Capital expenditure for the establishment of trees in carbon sink forests);

(f) Division 41 (Additional deduction for certain new business investment);

(g) Division 43 (Deductions for capital works).

3A Subsection 701‑58(2)

After “(5A)”, insert “, (5C)”.

3B At the end of Division 701

Add:

701‑90 Valuable right to future income treated as separate asset

(1) This subsection covers a valuable right (including a contingent right) to receive an amount for the performance of work or services or the provision of goods (other than *trading stock) if:

(a) the valuable right forms part of a contract or agreement; and

(b) the *market value of the valuable right (taking into account all the obligations and conditions relating to the right) is greater than nil.

(2) For the purposes of this Part, treat a valuable right covered by subsection (1) as a separate asset.

(3) For the purposes of this Part, if:

(a) a valuable right is treated as a separate asset under subsection (2); and

(b) the contract or agreement mentioned in paragraph (1)(a) also includes one or more other rights;

for the purposes of this Part, treat the contract or agreement (excluding the valuable right) as a separate asset.

(4) For the purposes of this Part:

(a) take into account all the obligations and conditions relating to a valuable right treated as a separate asset under subsection (2) in working out the *market value of that separate asset; and

(b) if a contract or agreement (excluding the valuable right) is treated as a separate asset under subsection (3)—take into account all the obligations and conditions relating to each right (other than the valuable right) that forms part of the contract or agreement in working out the market value of that separate asset.

4 After Subdivision 716‑G

Insert:

Subdivision 716‑S—Miscellenous consequences of tax cost setting

Table of sections

716‑400 Tax cost setting and bad debts

716‑405 Tax cost setting and rights to future income—deduction

716‑410 Rights to amounts that are expected to be included in assessable income after joining time

716‑400 Tax cost setting and bad debts

(1) The object of this section is to clarify the effect of section 701‑5 (entry history rule) and subsection 701‑55(6) in relation to an asset that may give rise to a bad debt. It achieves this object by clarifying that certain things are taken to have happened in relation to the asset through the operation of section 701‑5 and subsection 701‑55(6).

(2) This section applies if:

(a) the tax cost of an asset was set at the time (the joining time) an entity (the joining entity) became a subsidiary member of a *consolidated group at the asset’s tax cost setting amount; and

(b) the asset is a debt; and

(c) any of the following apply:

(i) the debt was included in the joining entity’s assessable income before the joining time;

(ii) the debt was in respect of money that the joining entity lent before the joining time in the ordinary course of a business of lending money;

(iii) the joining entity bought the debt before the joining time in the ordinary course of a business of lending money; and

(d) the requirements in subsection 701‑58(1) (intra‑group assets) are not satisfied in relation to the asset.

(3) To avoid doubt, in determining the extent to which the *head company of the group can deduct an amount under section 25‑35 (bad debts) in relation to the asset, section 701‑5 (entry history rule) and subsection 701‑55(6) have the effect that, before the joining time:

(a) in a case covered by subparagraph (2)(c)(i)—the head company included an amount equal to the tax cost setting amount in its assessable income in respect of the debt; or

(b) in a case covered by subparagraph (2)(c)(ii)—the head company lent an amount of money in respect of the debt equal to the tax cost setting amount in the ordinary course of a business of lending money; or

(c) in a case covered by subparagraph (2)(c)(iii)—the head company incurred expenditure equal to the tax cost setting amount in buying the debt in the ordinary course of a business of lending money.

716‑405 Tax cost setting and rights to future income—deduction

(1) This section applies if:

(a) an entity (the joining entity) became a subsidiary member of a *consolidated group at a time (the joining time); and

(b) subsection 701‑55(5C) applies in relation to the asset at the joining time.

Note: Subsection 701‑55(5C) deals with assets covered by section 716‑410 (Rights to amounts that are expected to be included in assessable income after joining time).

(2) An entity qualified for a deduction under subsection (5) for the asset for an income year ending after the joining time can deduct, for that income year:

(a) unless paragraph (b) applies—the amount determined under subsection (3A); or

(b) if it is reasonable to expect that no amount will be included in the assessable income of an entity qualified for a deduction under subsection (5) for the asset for any later income year—the unexpended tax cost setting amount for the asset for that income year.

(3) Paragraph (2)(b) does not apply in relation to an entity qualified for a deduction under subsection (5) for the asset for that income year if:

(a) the entity is the *head company of the group; and

(b) another entity ceased to be a *subsidiary member of the group in that income year; and

(c) the other entity can deduct an amount under subsection (2) for that income year because it is also qualified for a deduction under subsection (5) for the asset for that income year.

(3A) For the purposes of paragraph (2)(a), the amount is the lesser of the following:

(a) the *unexpended tax cost setting amount for the asset for that income year;

(b) the unexpended tax cost setting amount for the asset for the first income year ending after the joining time, divided by the lesser of:

(i) 10; or

(ii) if the contract or agreement giving rise to the valuable right mentioned in paragraph 716‑410(a) is for a specified period—the number of days in that period that end after the joining time, divided by 365 and rounded upwards to the nearest whole number.

(4) The unexpended tax cost setting amount for the asset for an income year is the *tax cost setting amount for the asset, reduced by:

(a) the amounts (if any) of all deductions under this section in respect of the asset for previous income years ending after the joining time; and

(b) in determining the amount of a deduction under this section in respect of the asset for that income year for an entity that ceased to be a *subsidiary member of the group in that income year—the amount (if any) that the *head company of the group can deduct under this section in respect of the asset for that income year.

(5) An entity is qualified for a deduction under this subsection for an income year for the asset if:

(a) the entity:

(i) is the *head company of the group; and

(ii) held the asset at a time in that income year (whether or not because of the operation of subsection 701‑1(1) (the single entity rule)); or

(b) the entity:

(i) held the asset at a time in that income year; and

(ii) ceased to be a *subsidiary member of the group in that income year or an earlier income year.

(6) An amount deducted under this section:

(a) is not to be deducted under any other provision of this Act; and

(b) is not to be taken into account in determining an amount that is included in the assessable income of any entity qualified for a deduction under subsection (5) for any income year for the asset; and

(c) is not to be taken into account in determining an amount of a deduction of any entity qualified for a deduction under subsection (5) for any income year for the asset; and

(d) despite paragraphs (b) and (c), is taken never to have been included in any of the elements of the *cost base of the asset.

716‑410 Rights to amounts that are expected to be included in assessable income after joining time

This section covers an asset at a time if:

(a) the asset is a valuable right covered by subsection 701‑90(1); and

Note: Such a valuable right is treated as a separate asset for the purposes of this Part (see subsection 701‑90(2)).

(b) the asset is held by an entity just before the time (the joining time) it became a *subsidiary member of a *consolidated group; and

(c) it is reasonable to expect that an amount attributable to the asset will be included in the assessable income of the entity or any other entity after the joining time; and

(d) Division 230 does not apply in relation to the asset (disregarding section 230‑455).

5 Subsection 995‑1(1)

Insert:

unexpended tax cost setting amount has the meaning given by section 716‑405.

Division 2—Foreign currency gains and losses

Income Tax Assessment Act 1997

6 After Subdivision 715‑D

Insert:

Subdivision 715‑E—Interactions with Division 775 (Foreign currency gains and losses)

Table of sections

715‑370 Cost setting—reference time for determining currency exchange rate effect

715‑370 Cost setting—reference time for determining currency exchange rate effect

(1) This section applies if:

(a) an entity (the joining entity) becomes a *subsidiary member of a *consolidated group at a time (the joining time); and

(b) taking into account the operation of subsection 701‑1(1) (the single entity rule), the *head company of the group held an asset at the joining time because the joining entity became a subsidiary member of the group; and

(c) the asset is a reset cost base asset at the joining time (within the meaning of section 705‑35); and

(d) in working out the asset’s *tax cost setting amount, the currency exchange rate of a particular *foreign currency is taken into account in determining the *market value of the asset.

(2) For the purposes of Division 775, determine the extent of any *currency exchange rate effect after the joining time in relation to the asset, by reference to the currency exchange rate for the *foreign currency at the joining time.

Division 3—Application and transitional provisions

7 Application provision

(1) The amendments made by Division 1 of this Part apply on and after 1 July 2002.

(2) The amendment made by Division 2 of this Part applies in relation to a consolidated group or MEC group on and after:

(a) if the head company of the group makes a choice in accordance with subitems (3) and (4)—1 July 2002; or

(b) otherwise—the day on which the Bill that became this Act was introduced into the House of Representatives.

(3) A choice mentioned in paragraph (2)(a) must be made:

(a) on or before 30 June 2011; or

(b) within a further time allowed by the Commissioner.

(4) A choice mentioned in paragraph (2)(a) must be made in writing.

8 Transitional provision—use of the tax cost setting amount

(1) This item applies if:

(a) the tax cost of an asset was set at the time (the joining time) an entity (the joining entity) became a subsidiary member of a consolidated group or MEC group, at the asset’s tax cost setting amount; and

(b) the asset is a trade receivable that is denominated in foreign currency; and

(c) CGT event C2 happens in relation to the asset:

(i) after the joining time; and

(ii) before 23 August 2006; and

(d) just before the CGT event, the head company of the group held the asset because of the operation of subsection 701‑1(1) of the Income Tax Assessment Act 1997 (the single entity rule); and

(e) disregarding section 118‑20 of that Act, there is a capital gain or capital loss from the event; and

(f) the head company of the group makes a choice to apply this item, in accordance with subitems (4) and (5).

(2) These provisions do not apply to the CGT event:

(a) section 6‑5 of the Income Tax Assessment Act 1997 (about ordinary income);

(b) any other provision of that Act that includes an amount in assessable income, other than a provision in Part 3‑1 or 3‑3 of that Act;

(c) section 8‑1 of that Act (about amounts you can deduct);

(d) any other provision of that Act that allows you to deduct an amount from your assessable income;

(e) section 118‑20 of that Act.

(3) The provisions referred to in subitem (2) can apply to the CGT event to the extent that any capital gain or capital loss from the event is attributable to currency exchange rate fluctuations.

(4) A choice mentioned in paragraph (1)(f) must be made:

(a) on or before 30 June 2011; or

(b) within a further time allowed by the Commissioner.

(5) The way the head company prepares its income tax return is sufficient evidence of the making of the choice.

Income Tax Assessment Act 1997

9 Paragraph 703‑75(2)(d)

Omit “group);”, substitute “group); or”.

10 After paragraph 703‑75(2)(d)

Insert:

(e) section 719‑125 (about the effects of a group conversion involving a MEC group);

11 Section 719‑25 (heading)

Repeal the heading, substitute:

719‑25 Head company, subsidiary members and members of a MEC group

12 At the end of section 719‑25

Add:

(3) The members of a *MEC group are the *head company of the group and the *subsidiary members of the group.

13 Subparagraph 719‑65(3)(d)(i)

Omit “the group came into existence as a result of a choice under section 719‑50, and”.

14 After paragraph 719‑90(2)(c)

Insert:

(ca) section 719‑125 (about the effects of a group conversion involving a MEC group); or

15 After Subdivision 719‑B

Insert:

Subdivision 719‑BA—Group conversions involving MEC groups

Table of sections

719‑120 Application

719‑125 Head company of new group retains history of head company of old group

719‑130 Provisions of this Part not to apply to conversion

719‑135 Provisions of this Part applying to conversion despite section 719‑130

719‑140 Other provisions of this Part not applying to conversion

(1) This Subdivision applies if, at a particular time (the conversion time):

(a) a *consolidated group (the new group) is *created from a *MEC group (the old group); or

(b) a MEC group (the new group) is created from a consolidated group (the old group).

(2) However, sections 719‑130 and 719‑135 apply only in relation to entities that:

(a) were *members of the old group just before the conversion time; and

(b) are members of the new group at that time.

719‑125 Head company of new group retains history of head company of old group

(1) Everything that happened in relation to the *head company of the old group before the conversion time is taken instead to have happened in relation to:

(a) if the head company of the old group is the same entity as the head company of the new group—that entity in its role as head company of the new group; or

(b) otherwise—the head company of the new group (just as if the head company of the new group had been the head company of the old group at all times before the conversion time).

(2) To avoid doubt, subsection (1) also covers everything that, immediately before the conversion time, was taken to have happened in relation to the *head company of the old group because of:

(a) section 701‑1 (the single entity rule); or

(b) section 701‑5 (the entry history rule); or

(c) section 703‑75 (about the effects of choice to continue *consolidated group after shelf company becomes new head company); or

(d) section 719‑90 (about the effects of a change of head company of a *MEC group); or

(e) one or more previous applications of this Division.

(3) Subsections (1) and (2) have effect:

(a) for the *head company core purposes in relation to an income year ending after the conversion time; and

(b) for the entity core purposes in relation to an income year ending after the conversion time; and

(c) for the purposes of determining the balance of the *franking account of the head company of the new group at and after the conversion time.

(4) Subsections (1) and (2) have effect subject to:

(a) section 701‑40 (Exit history rule); and

(b) a provision of this Act to which section 701‑40 is subject because of section 701‑85 (about exceptions to the core rules in Division 701).

Note: An example of provisions covered by paragraph (b) of this subsection is Subdivision 717‑E (about transferring to a company leaving a consolidated group various surpluses under the CFC rules in Part X of the Income Tax Assessment Act 1936).

719‑130 Provisions of this Part not to apply to conversion

(1) A provision mentioned in subsection (5) that applies on an entity becoming a *member of a *consolidated group or *MEC group does not apply to an entity becoming such a member because of a situation described in subsection 719‑120(1), unless the provision is expressed to apply despite this subsection.

Note 1: An example of the effect of this subsection is that section 701‑5 (entry history rule) does not apply. See instead section 719‑125.

Note 2: Further examples of the effect of this subsection are that Division 705 (cost setting on entry) and Division 707 (losses) do not apply.

(2) Subsection (1) does not affect the application of subsection 701‑1(1) (the single entity rule).

(3) A provision mentioned in subsection (5) that applies on an entity ceasing to be a *member of a *consolidated group or *MEC group does not apply to an entity ceasing being such a member because of a situation described in subsection 719‑120(1), unless the provision is expressed to apply despite this subsection.

Note 1: An example of the effect of this subsection is that section 701‑40 (Exit history rule) does not apply. See instead section 719‑125.

Note 2: Another example of the effect of this subsection is that Division 711 (cost setting on exit) does not apply.

(4) Subsection (3) does not apply if:

(a) the old group mentioned in subsection 719‑120(1) is a *consolidated group; and

(b) the new group mentioned in subsection 719‑120(1) is a *MEC group; and

(c) the entity ceasing to be a *member of the old group becomes an *eligible tier‑1 company in respect of the new group.

(5) The provisions are as follows:

(a) Subdivision 104‑L;

(b) section 165‑212E;

(c) this Part (other than this Subdivision);

(d) Part 3‑90 of the Income Tax (Transitional Provisions) Act 1997.

719‑135 Provisions of this Part applying to conversion despite section 719‑130

(1) This section applies despite subsections 719‑130(1) and (3).

(2) If the new group is a *consolidated group, the following provisions may apply on an entity ceasing to be a *member of the old group:

(a) Subdivision 719‑K;

(b) any other provision of this Part, to the extent that the application of the provision is necessary for the application of Subdivision 719‑K.

719‑140 Other provisions of this Part not applying to conversion

If the new group is a *consolidated group, the following provisions do not apply merely because the old group ceases to exist at the conversion time (or merely because the *potential MEC group of which the old group consisted ceases to exist at that time):

(a) section 719‑280;

(b) section 719‑465;

(c) section 719‑705;

(d) section 719‑725;

(e) any other provision of this Part, to the extent that the application of the provision is necessary for the application of any of those sections.

16 Subsection 995‑1(1) (after paragraph (b) of the definition of member)

Insert:

(ba) in relation to a *MEC group—has the meaning given by section 719‑25; and

(bb) in relation to a *potential MEC group—has the meaning given by section 719‑10; and

17 Application provision

(1) The amendments made by this Part apply in relation to the creation of a MEC group from a consolidated group, or a consolidated group from a MEC group, on or after:

(a) if the head company of the group makes a choice in accordance with subitems (2) and (3)—1 July 2002; or

(b) otherwise—27 October 2006.

(2) A choice mentioned in paragraph (1)(a) must be made:

(a) on or before 30 June 2011; or

(b) within a further time allowed by the Commissioner.

(3) A choice mentioned in paragraph (1)(a) must be made in writing.

(4) Despite subitem (1), the amendment made by item 13 of this Schedule applies on and after 1 July 2002.

Income Tax Assessment Act 1997

18 Section 705‑125 (heading)

Repeal the heading, substitute:

705‑125 Pre‑CGT proportion for joining entity

19 Subsection 705‑125(1)

Omit “That mechanism involves working out a factor by which the pre‑CGT status can be attached to the joining entity’s assets and then recognised in membership interests held in an entity that owns the assets on ceasing to be a *subsidiary member of the joined group.”, substitute “That mechanism involves:

(a) working out the proportion (measured by market value) of the membership interests in the joining entity that have pre‑CGT status; and

(b) if the joining entity later ceases being a member of the group, attaching pre‑CGT status to that proportion of membership interests in it (see section 711‑65), subject to integrity rules (see section 711‑70).”.

20 Subsections 705‑125(2) and (3)

Repeal the subsections, substitute:

How to work out pre‑CGT proportion

(2) The pre‑CGT proportion is the amount worked out by dividing:

(a) the sum of the *market value of each *membership interest in the joining entity that is:

(i) held by a *member of the group at the joining time; and

(ii) is a *pre‑CGT asset;

by:

(b) the sum of the market value of each membership interest in the joining entity that is held by a member of the group at the joining time.

21 Subsection 705‑125(4)

Omit “paragraph (3)(a)”, substitute “subsection (2)”.

22 Section 705‑165

Repeal the section.

23 Section 705‑205

Repeal the section.

24 Section 705‑245

Repeal the section.

25 Section 711‑65 (heading)

Repeal the heading, substitute:

711‑65 Membership interests treated as having been acquired before 20 September 1985

26 Subsection 711‑65(1)

Repeal the subsection, substitute:

When this section applies

(1) This section applies unless:

(a) Subdivision 705‑C (about one group joining another consolidated group) applies in relation to the old group; and

(b) the leaving entity is a *subsidiary member of the old group.

(1A) To avoid doubt, this section applies regardless of whether the leaving entity ceases to be a *subsidiary member of the old group at the leaving time because another entity also ceases to be a subsidiary member of the old group at the leaving time.

27 Subsection 711‑65(2) (note)

Repeal the note.

28 Subsection 711‑65(4) (definition of leaving entity’s pre‑CGT proportion)

Omit “subsection (5)”, substitute “section 705‑125”.

29 Subsection 711‑65(5)

Repeal the subsection.

30 Section 711‑70

Repeal the section, substitute:

(1) This section applies if:

(a) the leaving entity held assets at the time it became a *subsidiary member of the old group (disregarding subsection 701‑1(1) (the single entity rule)); and

(b) some or all of the assets:

(i) stopped being *pre‑CGT assets under Division 149 at a time (the Division 149 time) when the *head company of the group held them under subsection 701‑1(1) (the single entity rule); or

(ii) would have stopped being pre‑CGT assets under Division 149 at a time (also the Division 149 time) when the head company of the group held them under subsection 701‑1(1) (the single entity rule) if they had been pre‑CGT assets just before that time; and

(c) the leaving entity was a subsidiary member of the group at that time.

(2) The *pre‑CGT proportion of the leaving entity at the leaving time is taken to be nil.

(3) Adjust the old group’s *allocable cost amount for the leaving entity as follows:

(a) if the amount under subsection (4) exceeds the amount under subsection (6)—increase the allocable cost amount by the excess;

(b) if the amount under subsection (4) falls short of the amount under subsection (6)—reduce the allocable cost amount by the shortfall.

(4) Subject to subsection (5), the amount under this subsection is:

(a) if Subdivision 705‑A applied in relation to the leaving entity at the time it became a *subsidiary member of the old group—the total of the amounts that were taken into account under subsection 705‑65(1) for *membership interests in the leaving entity at that time; or

(b) otherwise—assuming that Subdivision 705‑A had applied in relation to the leaving entity at the time it became a subsidiary member of the old group, the total of the amounts that would have been taken into account under subsection 705‑65(1) for membership interests in the leaving entity at that time.

(5) For the purposes of subsection (4), if a *membership interest in the leaving entity was covered under paragraph 705‑125(2)(a) (pre‑CGT interests) when it became a *subsidiary member of the old group, treat the amount that was taken into account for the membership interest under subsection 705‑65(1) as the interest’s *market value just after the Division 149 time.

(6) The amount under this subsection is the old group’s *allocable cost amount for the leaving entity, worked out on the assumption that the leaving entity ceased to be a *subsidiary member of the old group just after the Division 149 time.

(1) This section applies if the leaving entity ceases to be a *subsidiary member of the old group because of a situation giving rise to *CGT event A1, C2, E1, E2 or E8 in relation to one or more *membership interests in the leaving entity.

(2) For the purposes of applying subsections 104‑230(2) and (8) in relation to those *membership interests:

(a) disregard subsection 701‑1(1) (the single entity rule) in working out the *net value of the leaving entity; and

(b) treat the reference in subsection 104‑230(2) to “Just before the other event happened” as a reference to “Just before the leaving time”.

Note 1: The single entity rule will continue to apply in determining whether the property mentioned in subsection 104‑230(2) for the leaving entity was acquired on or after 20 September 1985.

Note 2: However, in a case of multiple exit from a consolidated group (see section 711‑55), the property mentioned in subsection 104‑230(2) for the leaving entity may include membership interests in another entity leaving the group at the leaving time. To determine which of those membership interests were acquired on or after 20 September 1985 for the purposes of applying subsection 104‑230(2) to the leaving entity, see section 711‑65.

(3) In determining the sum of the *cost bases of the property mentioned in subsection 104‑230(6), treat the cost base of an asset that is included in that property as:

(a) if the asset has its *tax cost set at the leaving time under section 701‑50—its *tax cost setting amount; or