Tax Laws Amendment (2011 Measures No. 2) Act 2011

No. 41, 2011

An Act to amend the law relating to taxation and superannuation, and for related purposes

Tax Laws Amendment (2011 Measures No. 2) Act 2011

No. 41, 2011

An Act to amend the law relating to taxation and superannuation, and for related purposes

Contents

2 Commencement

3 Schedule(s)

Schedule 1—Deductible gift recipients

Part 1—Amendments commencing on 1 January 2011

Income Tax Assessment Act 1997

Part 2—Amendments commencing on Royal Assent

Income Tax Assessment Act 1997

Part 3—Sunsetting on 1 July 2016

Income Tax Assessment Act 1997

Schedule 2—Self managed superannuation funds

Superannuation Industry (Supervision) Act 1993

Schedule 3—Use of TFNs for superannuation purposes

Part 1—Amendments commencing on 1 July 2011

Retirement Savings Accounts Act 1997

Superannuation Industry (Supervision) Act 1993

Part 2—Amendments commencing on Proclamation

Retirement Savings Accounts Act 1997

Superannuation Industry (Supervision) Act 1993

Schedule 4—GST: payments of taxes, fees and charges

A New Tax System (Goods and Services Tax) Act 1999

A New Tax System (Luxury Car Tax) Act 1999

Schedule 5—Other amendments

Part 1—A New Tax System (Goods and Services Tax) Act 1999

Part 2—Approved worker entitlement funds

Fringe Benefits Tax Assessment Act 1986

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Part 3—Confidentiality of taxpayer Information

Division 1—Main amendments

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Division 2—Amendment contingent on the Human Services Legislation Amendment Act 2011

Taxation Administration Act 1953

Part 4—Employee share schemes

Division 1—Income Tax Assessment Act 1997

Division 2—Income Tax (Transitional Provisions) Act 1997

Division 3—Minor amendment

Income Tax Assessment Act 1997

Part 5—General interest charge

Taxation Administration Act 1953

Part 6—Deductible gift recipients

Division 1—Amendments commencing on Royal Assent

Income Tax Assessment Act 1997

Division 2—Amendments commencing on 1 July 2011

Income Tax Assessment Act 1997

Division 3—Other amendment

Tax Laws Amendment (Repeal of Inoperative Provisions) Act 2006

Part 7—Section 23AB of the Income Tax Assessment Act 1936

Income Tax Assessment Act 1936

Part 8—Definitions and signposts to related material

Income Tax Assessment Act 1936

Part 9—Repeal of redundant reference to Papua New Guinea

Income Tax Assessment Act 1936

Part 10—Repeal of redundant references to franking

Income Tax Assessment Act 1936

Part 11—Correction of cross‑reference in provision about dividend streaming etc.

Income Tax Assessment Act 1936

Part 12—Minor changes to provisions about concessional rebates

Income Tax Assessment Act 1936

Part 13—Fixing outdated references to Medicare levy

Income Tax Assessment Act 1997

Part 14—Repeal of references to previously repealed provisions

Income Tax Assessment Act 1997

Part 15—Correction of asterisking of reference to tax debts

Income Tax Assessment Act 1997

Part 16—Repeal of outdated provisions about exemption from income tax

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Part 17—Correction of asterisking of references to quarter

Income Tax Assessment Act 1997

Part 18—Inclusion of Commissioner’s discretion to extend main residence exemption from CGT

Income Tax Assessment Act 1997

Part 19—Nomination of controllers of discretionary trust

Income Tax Assessment Act 1997

Part 20—Definitions mainly relevant to Subdivision 165‑F of the Income Tax Assessment Act 1997

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Part 21—Removal of definition from imputation provisions

Income Tax Assessment Act 1997

Part 22—Correction of outdated references to virtual PST assets

Income Tax Assessment Act 1997

Part 23—Repeal of spent provisions about land transport facilities borrowings

Income Tax Assessment Act 1997

Part 24—Prevention of double counting for direct value shifts

Income Tax Assessment Act 1997

Part 25—Ineligible income tax remission decisions

Taxation Administration Act 1953

Part 26—Correction of references to chains of fixed trusts

Income Tax Assessment Act 1997

Part 27—Gender‑specific language

Income Tax Assessment Act 1936

Part 28—Misdescribed amendments

Tax Laws Amendment (2010 Measures No. 1) Act 2010

Tax Laws Amendment (Transfer of Provisions) Act 2010

Part 29—References to Schedules

Family Trust Distribution Tax (Primary Liability) Act 1998

Family Trust Distribution Tax (Secondary Liability) Act 1998

Fringe Benefits Tax Assessment Act 1986

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Medicare Levy Act 1986

Superannuation Contributions Tax (Assessment and Collection) Act 1997

Part 30—References to taxation laws

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Part 31—Other amendments

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Superannuation Legislation Amendment Act 2010

Taxation Administration Act 1953

Taxation (Interest on Overpayments and Early Payments) Act 1983

Tax Laws Amendment (2007 Measures No. 5) Act 2007

Tax Laws Amendment (2011 Measures No. 2) Act 2011

No. 41, 2011

An Act to amend the law relating to taxation and superannuation, and for related purposes

[Assented to 27 June 2011]

The Parliament of Australia enacts:

This Act may be cited as the Tax Laws Amendment (2011 Measures No. 2) Act 2011.

(1) Each provision of this Act specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Note: This table relates only to the provisions of this Act as originally enacted. It will not be amended to deal with any later amendments of this Act.

(2) Any information in column 3 of the table is not part of this Act. Information may be inserted in this column, or information in it may be edited, in any published version of this Act.

Each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

1 Section 30‑90 (cell at table item 10.2.2, column headed “Fund, authority or institution”)

Repeal the cell, substitute:

Girl Guides Australia |

2 Section 30‑90 (table item 10.2.3)

Omit “Guides Australia Incorporated”, substitute “Girl Guides Australia”.

3 Section 30‑315 (cell at table item 53A, column without a heading)

Repeal the cell, substitute:

Girl Guides Australia |

4 Subsection 30‑25(2) (at the end of the table)

Add:

2.2.39 | The Charlie Perkins Scholarship Trust | the gift must be made after 1 August 2010 and before 2 August 2013 |

2.2.40 | Roberta Sykes Indigenous Education Foundation | the gift must be made after 1 August 2010 and before 2 August 2013 |

5 Section 30‑315 (after table item 30AA)

Insert:

30A | Charlie Perkins Scholarship Trust | item 2.2.39 |

6 Section 30‑315 (after table item 97)

Insert:

97AA | Roberta Sykes Indigenous Education Foundation | item 2.2.40 |

7 Subsection 30‑25(2) (table items 2.2.39 and 2.2.40)

Repeal the table items.

8 Section 30‑315 (table items 30A and 97AA)

Repeal the table items.

1 After section 62

Insert:

The regulations may prescribe rules in relation to the trustees of regulated superannuation funds that are self managed superannuation funds making, holding and realising investments involving:

(a) artwork (within the meaning of the Income Tax Assessment Act 1997); or

(b) jewellery; or

(c) antiques; or

(d) artefacts; or

(e) coins or medallions; or

(f) postage stamps or first day covers; or

(g) rare folios, manuscripts or books; or

(h) memorabilia; or

(i) wine; or

(j) cars; or

(k) recreational boats; or

(l) memberships of sporting or social clubs; or

(m) assets of a particular kind, if assets of that kind are ordinarily used or kept mainly for personal use or enjoyment (not including land).

Note: The regulations may prescribe penalties of not more than 10 penalty units for offences against the regulations. See paragraph 353(1)(d).

2 Paragraph 353(1)(d)

Omit “subject to subsection 376(6),”.

Note: This item removes a cross‑reference to a provision that has been repealed.

3 Application provision

(1) The amendment made by item 1 of this Schedule applies to investments made before, on or after the commencement of this item.

(2) To avoid doubt, regulations made for the purposes of section 62A of the Superannuation Industry (Supervision) Act 1993, inserted by item 1 of this Schedule, may be expressed to apply to only some of those investments.

1 Subsections 137(4) and (5)

Repeal the subsections.

2 After section 137

Insert:

(1) This section applies if:

(a) a holder of an RSA; or

(b) a person applying to become such a holder;

quotes his or her tax file number to the RSA provider in connection with the operation, or the possible future operation, of this Act and the other Superannuation Acts.

(2) An RSA provider may, subject to any conditions contained in the regulations, use tax file numbers quoted as mentioned in subsection (1) in order to locate, in the records or accounts of the RSA provider, amounts held in RSAs provided by it.

Note: Sections 8WA and 8WB of the Taxation Administration Act 1953 contain offences for unauthorised use etc. of tax file numbers.

(3) This section does not affect the operation of subclauses 7.1 and 7.1A of National Privacy Principle 7 in Schedule 3 to the Privacy Act 1988.

Note 1: Subclause 7.1 prohibits an RSA provider adopting a tax file number of an individual as the RSA provider’s own identifier of the individual, such as by using the tax file number as an account or membership number.

Note 2: See also Division 4 of Part III of the Privacy Act 1988 and the guidelines issued under that Division concerning the collection, storage, use and security of tax file number information.

3 Subsections 299H(4) and (5)

Repeal the subsections.

4 Subsection 299H(6)

Omit “subsection (2), (3) or (5)”, substitute “subsection (2) or (3)”.

Note: The following heading to subsection 299H(6) is inserted “Offences”.

5 Subsection 299H(7)

Omit “(2), (3) or (5)”, substitute “subsection (2) or (3)”.

6 Subsections 299J(4) and (5)

Repeal the subsections.

7 Subsections 299J(6) and (7)

Omit “or (5)”.

Note: The following heading to subsection 299J(6) is inserted “Offences”.

8 Subsections 299K(4) and (5)

Repeal the subsections.

9 Subsections 299K(6) and (7)

Omit “subsection (2), (3) or (5)”, substitute “subsection (2) or (3)”.

Note: The following heading to subsection 299K(6) is inserted “Offences”.

10 Subsections 299L(4) and (5)

Repeal the subsections.

11 Subsections 299L(6) and (7)

Omit “or (5)”.

Note: The following heading to subsection 299L(6) is inserted “Offences”.

12 After section 299L

Insert:

(1) This section applies if:

(a) a beneficiary of an eligible superannuation entity, or of a regulated exempt public sector superannuation scheme; or

(b) an applicant to become such a beneficiary;

quotes his or her tax file number to a trustee of the entity or scheme in connection with the operation, or the possible future operation, of this Act and the other Superannuation Acts.

(2) A trustee of an eligible superannuation entity, or of a regulated exempt public sector superannuation scheme, may, subject to any conditions contained in the regulations, use tax file numbers quoted as mentioned in subsection (1) in order to locate, in the records or accounts of the entity or scheme, amounts held for the benefit of persons.

Note: Sections 8WA and 8WB of the Taxation Administration Act 1953 contain offences for unauthorised use etc. of tax file numbers.

(3) This section does not affect the operation of subclauses 7.1 and 7.1A of National Privacy Principle 7 in Schedule 3 to the Privacy Act 1988.

Note 1: Subclause 7.1 prohibits a trustee adopting a tax file number of an individual as the trustee’s own identifier of the individual, such as by using the tax file number as an account or membership number.

Note 2: See also Division 4 of Part III of the Privacy Act 1988 and the guidelines issued under that Division concerning the collection, storage, use and security of tax file number information.

13 Application provision

The amendments made by this Part apply to the use of tax file numbers on or after the commencement of this item, whether the tax file numbers were quoted before, on or after that commencement.

14 Section 16

Insert:

eligible superannuation entity has the meaning given by Part 25A of the Superannuation Industry (Supervision) Act 1993.

15 Section 16

Insert:

regulated exempt public sector superannuation scheme has the meaning given by Part 25A of the Superannuation Industry (Supervision) Act 1993.

16 Subsection 137A(2)

Repeal the subsection, substitute:

(2) An RSA provider may, subject to any conditions contained in the regulations, use tax file numbers quoted as mentioned in subsection (1):

(a) in order to locate, in the records or accounts of the RSA provider, amounts held in RSAs provided by it; or

(b) in order to facilitate the consolidation of any of the following in relation to a particular person:

(i) RSAs provided by one or more RSA providers and held by the person;

(ii) interests of the person in eligible superannuation entities or regulated exempt public sector superannuation schemes.

Note: Sections 8WA and 8WB of the Taxation Administration Act 1953 contain offences for unauthorised use etc. of tax file numbers.

(2A) Without limiting subsection (2), regulations made for the purposes of that subsection may contain conditions relating to:

(a) a person consenting to use of a tax file number; or

(b) procedures to be followed in a consolidation mentioned in paragraph (2)(b), including procedures to safeguard the integrity of the consolidation; or

(c) an RSA provider disclosing tax file numbers to another RSA provider, or to a trustee of an eligible superannuation entity or of a regulated exempt public sector superannuation scheme, in order to facilitate such a consolidation.

Note: The heading to section 137A is altered by adding at the end “or for consolidation”.

17 Subsection 299LA(2)

Repeal the subsection, substitute:

(2) A trustee of an eligible superannuation entity, or of a regulated exempt public sector superannuation scheme, may, subject to any conditions contained in the regulations, use tax file numbers quoted as mentioned in subsection (1):

(a) in order to locate, in the records or accounts of the entity or scheme, amounts held for the benefit of persons; or

(b) in order to facilitate the consolidation of any of the following in relation to a particular person:

(i) RSAs provided by one or more RSA providers and held by the person;

(ii) interests of the person in eligible superannuation entities or regulated exempt public sector superannuation schemes.

Note: Sections 8WA and 8WB of the Taxation Administration Act 1953 contain offences for unauthorised use etc. of tax file numbers.

(2A) Without limiting subsection (2), regulations made for the purposes of that subsection may contain conditions relating to:

(a) a person consenting to use of a tax file number; or

(b) procedures that must be followed in a consolidation mentioned in paragraph (2)(b), including procedures to safeguard the integrity of the consolidation; or

(c) a trustee disclosing tax file numbers to another trustee, or to an RSA provider, in order to facilitate such a consolidation.

Note: The heading to section 299LA is altered by adding at the end “or for consolidation”.

18 Application provision

The amendments made by this Part apply to the use of tax file numbers on or after the commencement of this item, whether the tax file numbers were quoted before, on or after that commencement.

19 Transitional provision—regulations

(1) A regulation:

(a) made for the purposes of subsection 137A(2) of the Retirement Savings Accounts Act 1997; and

(b) in force immediately before the commencement of this item;

has effect, after the commencement of this item, as if it had been made for the purposes of that subsection as amended by this Part.

(2) A regulation:

(a) made for the purposes of subsection 299LA(2) of the Superannuation Industry (Supervision) Act 1993; and

(b) in force immediately before the commencement of this item;

has effect, after the commencement of this item, as if it had been made for the purposes of that subsection as amended by this Part.

1 Subparagraph 13‑20(2)(ba)(i)

Repeal the subparagraph, substitute:

(i) is not an amount, the payment of which (or the discharging of a liability to make a payment of which), because of Division 81 or regulations made under that Division, is not the provision of *consideration; and

Note: Division 81 excludes certain taxes, fees and charges from the provision of consideration.

2 Division 81

Repeal the Division, substitute:

GST does not apply to payments of taxes, fees and charges that are excluded from the GST by this Division or by regulations.

GST applies to certain taxes, fees and charges prescribed by regulations.

Australian tax not consideration

(1) A payment, or the discharging of a liability to make a payment, is not the provision of *consideration to the extent the payment is an *Australian tax.

Regulations may provide for exceptions

(2) However, a payment you make, or a discharging of your liability to make a payment, is treated as the provision of *consideration to the extent the payment is an *Australian tax that is, or is of a kind, prescribed by the regulations.

(3) For the purposes of subsection (2), the *consideration is taken to be provided to the entity to which the tax is payable, for a supply that the entity makes to you.

Certain fees and charges not consideration

(1) A payment, or the discharging of a liability to make a payment, is not the provision of *consideration to the extent the payment is an *Australian fee or charge that is of a kind covered by subsection (4) or (5).

Prescribed fees and charges treated as consideration

(2) However, a payment you make, or a discharging of your liability to make a payment, is treated as the provision of *consideration to the extent the payment is an *Australian fee or charge that is, or is of a kind, prescribed by the regulations.

(3) For the purposes of subsection (2), the *consideration is taken to be provided to the entity to which the fee or charge is payable, for a supply that the entity makes to you.

Fees or charges paid for permissions etc.

(4) This subsection covers a fee or charge if the fee or charge:

(a) relates to; or

(b) relates to an application for;

the provision, retention, or amendment, under an *Australian law, of a permission, exemption, authority or licence (however described).

Fees or charges relating to information and record‑keeping etc.

(5) This subsection covers a fee or charge paid to an *Australian government agency if the fee or charge relates to the agency doing any of the following:

(a) recording information;

(b) copying information;

(c) modifying information;

(d) allowing access to information;

(e) receiving information;

(f) processing information;

(g) searching for information.

The regulations may provide that the payment of a prescribed *Australian fee or charge, or of an Australian fee or charge of a prescribed kind, or the discharging of a liability to make such a payment, is not the provision of *consideration.

This Division has effect despite section 9‑15 (which is about consideration).

Despite subsection 12(2) of the Legislative Instruments Act 2003, regulations made for the purposes of subsection 81‑5(2), 81‑10(2) or section 81‑15 may be expressed to take effect from a date before the regulations are registered under that Act.

3 Subsection 82‑10(3)

Repeal the subsection, substitute:

(3) If the other supply constitutes the payment of:

(a) an *Australian tax prescribed by regulations made for the purposes of subsection 81‑5(2); or

(b) an *Australian fee or charge prescribed by regulations made for the purposes of subsection 81‑10(2);

this section overrides those regulations in relation to the payment.

4 Subparagraph 117‑5(1)(ba)(i)

Repeal the subparagraph, substitute:

(i) is not an amount, the payment of which (or the discharging of a liability to make a payment of which), because of Division 81 or regulations made under that Division, is not the provision of *consideration; and

Note: Division 81 excludes certain taxes, fees and charges from the provision of consideration.

5 Section 195‑1

Insert:

Australian fee or charge means a fee or charge (however described), other than an *Australian tax, imposed under an *Australian law and payable to an *Australian government agency.

6 Section 195‑1

Insert:

Australian tax means a tax (however described) imposed under an *Australian law.

7 Section 195‑1 (definition of Australian tax, fee or charge)

Repeal the definition.

8 Section 195‑1 (note at the end of the definition of connected with Australia)

Omit “sections 81‑10 and 96‑5”, substitute “section 96‑5”.

9 Section 195‑1 (note at the end of the definition of consideration)

After “81‑5,”, insert “81‑10, 81‑15,”.

10 Section 195‑1 (note at the end of the definition of taxable supply)

Omit “81‑10,”.

11 Paragraph 5‑20(1)(b)

Omit “*Australian tax, fee or charge”, substitute “*Australian tax or *Australian fee or charge”.

12 Paragraph 5‑20(6)(b)

Omit “*Australian tax, fee or charge”, substitute “*Australian tax or *Australian fee or charge”.

13 Section 27‑1

Insert:

Australian fee or charge has the meaning given by section 195‑1 of the *GST Act.

14 Section 27‑1

Insert:

Australian tax has the meaning given by section 195‑1 of the *GST Act.

15 Section 27‑1 (definition of Australian tax, fee or charge)

Repeal the definition.

16 Application provision

(1) The amendments made by this Schedule apply in relation to the payment, or the discharging of liability to make a payment, relating to an Australian tax, or an Australian fee or charge, imposed on or after 1 July 2011.

(2) However, the amendments do not apply in relation to a payment, or a discharge of a liability to make a payment, relating to an Australian tax, or an Australian fee or charge, imposed before 1 July 2012 if the payment is of a kind specified by legislative instrument (a Division 81 determination):

(a) made for the purposes of subsection 81‑5(2) of the A New Tax System (Goods and Services Tax) Act 1999; and

(b) in force immediately before the commencement of this item.

(3) Despite the repeal of subsection 81‑5(2) of the A New Tax System (Goods and Services Tax) Act 1999 by item 2 of this Schedule, a Division 81 determination continues to have effect, after the commencement of this item and before 1 July 2012, as if the repeal had not happened.

1 Subparagraph 153‑50(1)(d)(i)

Omit “agent’s”, substitute “intermediary’s”.

Note: This item amends a reference to “agent’s” that was not amended when Schedule 3 to the Tax Laws Amendment (2009 GST Administration Measures) Act 2010 replaced references to “agent” in section 153‑50 of the A New Tax System (Goods and Services Tax) Act 1999 with references to “intermediary”.

2 Section 195‑1 (definition of member)

Omit “means”.

Note: Items 2 and 3 fix a grammatical error.

3 Section 195‑1 (paragraph (b) of the definition of member)

Before “an entity”, insert “means”.

4 Subsections 58PB(2) and (3)

Repeal the subsections, substitute:

Endorsed funds

(2) A fund is also an approved worker entitlement fund if:

(a) the fund is endorsed as an approved worker entitlement fund under subsection (3); or

(b) the entity that operates the fund is endorsed for the operation of the fund under subsection (3A).

(3) The Commissioner must endorse a fund as an approved worker entitlement fund if:

(a) the fund is entitled to be endorsed as an approved worker entitlement fund (see subsection (4)); and

(b) the fund has applied for the endorsement in accordance with Division 426 in Schedule 1 to the Taxation Administration Act 1953.

(3A) The Commissioner must endorse an entity for the operation of a fund as an approved worker entitlement fund if:

(a) the entity is entitled to be endorsed for the operation of the fund as an approved worker entitlement fund (see subsection (4A)); and

(b) the entity has applied for the endorsement in accordance with Division 426 in Schedule 1 to the Taxation Administration Act 1953.

5 Subsection 58PB(4)

Omit “Before the Governor‑General makes a regulation under paragraph (2)(a) prescribing a fund for the purposes of that paragraph, the Commissioner must be satisfied that”, substitute “A fund is entitled to be endorsed as an approved worker entitlement fund if”.

6 At the end of subsection 58PB(4)

Add:

; and (f) the fund, or the entity that operates the fund, has an ABN.

7 After subsection 58PB(4)

Insert:

(4A) An entity is entitled to be endorsed for the operation of a fund as an approved worker entitlement fund if the fund is entitled to be endorsed as an approved worker entitlement fund.

8 Section 58PC

Repeal the section.

9 Paragraph 126‑130(2)(b)

Repeal the paragraph, substitute:

(b) the amendment or replacement is done for the purpose of having:

(i) the fund endorsed as an approved worker entitlement fund under subsection 58PB(3) of the Fringe Benefits Tax Assessment Act 1986; or

(ii) the entity that operates the fund endorsed for the operation of the fund as an approved worker entitlement fund under subsection 58PB(3A) of that Act.

10 After paragraph 426‑5(b) in Schedule 1

Insert:

(ba) endorsement of:

(i) a fund as an approved worker entitlement fund under subsection 58PB(3) of the Fringe Benefits Tax Assessment Act 1986; or

(ii) an entity for the operation of a fund as an approved worker entitlement fund under subsection 58PB(3A) of that Act;

11 Section 426‑55 in Schedule 1 (paragraph (b) of the note)

After “subsections”, insert “58PB(4) and (4A),”.

12 After paragraph 426‑65(1)(b) in Schedule 1

Insert:

(ba) as an approved worker entitlement fund under subsection 58PB(3) of the Fringe Benefits Tax Assessment Act 1986;

(bb) for the operation of an approved worker entitlement fund under subsection 58PB(3A) of the Fringe Benefits Tax Assessment Act 1986;

13 Transitional provision—approved worker entitlement funds

Scope

(1) This item applies to a fund that, just before the commencement of this item, was an approved worker entitlement fund under subsection 58PB(2) of the Fringe Benefits Tax Assessment Act 1986.

Fund taken to have been endorsed

(2) Treat the fund as having been endorsed, on that commencement, by the Commissioner under subsection 58PB(3) of that Act, as amended by this Part.

(3) To avoid doubt, subitem (2) does not prevent the Commissioner from revoking that endorsement at a later time under section 426‑55 in Schedule 1 to the Taxation Administration Act 1953.

Fund not required to have ABN for 6 months

(4) Paragraph 58PB(4)(f) of the Fringe Benefits Tax Assessment Act 1986, as added by this Part, does not apply to the fund before the end of the period of 6 months starting on the day this item commences.

14 Transitional provision—Australian Business Registrar

During the period of 18 months starting on the day this item commences, the Australian Business Registrar:

(a) may enter, but is not required to enter, in the Australian Business Register under subsection 426‑65(1) in Schedule 1 to the Taxation Administration Act 1953 a statement that:

(i) an approved worker entitlement fund is endorsed as mentioned in paragraph (ba) of that subsection, as inserted by this Part; or

(ii) an entity is endorsed as mentioned in paragraph (bb) of that subsection, as inserted by this Part; and

(b) may publish on the Australian Taxation Office website, in relation to an approved worker entitlement fund:

(i) the name of the fund; and

(ii) the ABN (within the meaning of the A New Tax System (Australian Business Number) Act 1999) of the fund, or of the entity that operates the fund; and

(iii) the date on which the fund was endorsed as mentioned in paragraph (ba) of that subsection, or on which an entity was endorsed for the operation of the fund under paragraph (bb) of that subsection.

15 Subsection 6(1) (definition of Employment Department)

Repeal the definition.

16 Subsection 6(1) (definition of Employment Minister)

Repeal the definition.

17 Subsection 6(1) (definition of Employment Secretary)

Repeal the definition, substitute:

Employment Secretary has the meaning given by the Income Tax Assessment Act 1997.

18 Subsection 995‑1(1)

Insert:

Employment Department means the Department that:

(a) deals with matters arising under Chapter 2 of the Fair Work Act 2009; and

(b) is administered by the *Employment Minister.

19 Subsection 995‑1(1)

Insert:

Employment Minister means the Minister administering Chapter 2 of the Fair Work Act 2009.

20 Subsection 995‑1(1)

Insert:

Employment Secretary means the Secretary of the *Employment Department.

21 Subsection 355‑65(2) in Schedule 1 (cell at table item 4, column headed “The record is made for or the disclosure is to ...”)

At the end of the cell, add “or the *Employment Secretary”.

22 Subsection 355‑65(2) in Schedule 1 (cell at table item 6, column headed “The record is made for or the disclosure is to ...”)

At the end of the cell, add “or the Chief Executive Officer of Centrelink”.

23 Subsection 355‑65(5) in Schedule 1 (paragraph (b) of the cell at table item 2, column headed “and the record or disclosure ...”)

Omit “or residential address information”, substitute “, residential address information or spousal information”.

24 Subsection 355‑65(2) in Schedule 1 (table item 6, column headed “The record is made for or the disclosure is to ...”)

Omit “Chief Executive Officer of Centrelink”, substitute “Chief Executive Centrelink (within the meaning of the Human Services (Centrelink) Act 1997)”.

25 Subsection 104‑75(6) (note)

Repeal the note, substitute:

Note: There are also exceptions for employee share trusts: see sections 130‑80 and 130‑90.

26 At the end of subsection 104‑85(6)

Add:

Note: There is also an exception for employee share trusts: see section 130‑90.

27 Before subsection 130‑90(1)

Insert:

Shares held for future acquisition under employee share schemes

(1A) Disregard any *capital gain or *capital loss made by an *employee share trust to the extent that it results from a *CGT event, if:

(a) immediately before the event happens, an *ESS interest is a *CGT asset of the trust; and

(b) either of the following subparagraphs applies:

(i) the event is CGT event E5, and the event happens because a beneficiary of the trust becomes absolutely entitled to the ESS interest as against the trustee;

(ii) the event is CGT event E7, and the event happens because the trustee *disposes of the ESS interest to a beneficiary of the trust; and

(c) Subdivision 83A‑B or 83A‑C (about employee share schemes) applies to the ESS interest.

Shares held to satisfy the future exercise of rights acquired under employee share schemes

28 Subsection 130‑90(2)

After “Subsection”, insert “(1A) or”.

29 Application provision

The amendments made by this Division apply in relation to CGT events that happened, or that happen, on or after 1 July 2009.

30 After subsection 83A‑5(2)

Insert:

(2A) To avoid doubt, for the purposes of subparagraph (2)(a)(i), section 139CDA of the Income Tax Assessment Act 1936 applied to the interest at the pre‑Division 83A time if the taxpayer in question first became or becomes an employee, as mentioned in that section, before the cessation time for the interest. It does not matter whether the employee so became or becomes an employee before, on or after the pre‑Division 83A time.

Note: Section 139CDA was about shares or rights acquired while engaged in foreign service.

31 At the end of section 83A‑15

Add:

Amendment of assessments

(3) Section 170 of the Income Tax Assessment Act 1936 does not prevent the amendment of an assessment at any time for the purpose of giving effect to subsection (2) of this section.

32 After Division 124

Insert:

Table of Subdivisions

125‑B Consequences for owners of interests

Table of sections

125‑75 Employee share schemes

Despite the amendment of section 125‑75 of the Income Tax Assessment Act 1997 made by Schedule 1 to the Tax Laws Amendment (2009 Budget Measures No. 2) Act 2009, subsection (1) of that section continues to apply, from the commencement of that Schedule, to each ownership interest that it applied to just before that commencement.

33 Section 130‑100 (the section 130‑100 inserted by item 40 of Schedule 1 to the Tax Laws Amendment (2009 Budget Measures No. 2) Act 2009)

Renumber as section 130‑97.

34 Subsection 8AAB(1)

Omit “Subsections (4) and (5) list”, substitute “Subsection (4) lists”.

35 Subsections 8AAB(4) and (5)

Repeal the subsections, substitute:

(4) The following table is an index of the laws that deal with liability to the charge.

Liability to general interest charge | |||

Item | Column 1 Section | Column 2 Act | Column 3 Topic |

1 | 162‑100 | A New Tax System (Goods and Services Tax) Act 1999 | payment of GST instalments |

2 | 168‑10 | A New Tax System (Goods and Services Tax) Act 1999 | supplies later found to be GST‑free supplies |

3 | 25‑10 | A New Tax System (Wine Equalisation Tax) Act 1999 | purchases later found to be GST free supplies |

4 | 52 | First Home Saver Accounts Act 2008 | repayment of FHSA contributions |

5 | 93 | Fringe Benefits Tax Assessment Act 1986 | payment of fringe benefits tax or penalty tax |

6 | 112B | Fringe Benefits Tax Assessment Act 1986 | payment of fringe benefits tax instalments |

7 | 102UP | Income Tax Assessment Act 1936 | payment of trustee beneficiary non‑disclosure tax |

8 | 128C | Income Tax Assessment Act 1936 | payment of withholding tax |

9 | 163AA | Income Tax Assessment Act 1936 | returns by instalment taxpayers |

10 | 163B | Income Tax Assessment Act 1936 | returns by persons other than instalment taxpayers |

11 | 271‑80 in Schedule 2F | Income Tax Assessment Act 1936 | payment of family trust distribution tax |

12 | 5‑15 | Income Tax Assessment Act 1997 | unpaid income tax or shortfall interest charge |

13 | 197‑75 | Income Tax Assessment Act 1997 | payment of untainting tax |

14 | 214‑155 | Income Tax Assessment Act 1997 | payment of franking tax by a corporate tax entity |

15 | 292‑390 | Income Tax Assessment Act 1997 | payment of excess contributions tax or shortfall interest charge |

16 | 345‑115 | Income Tax Assessment Act 1997 | payment of FHSA misuse tax |

17 | 721‑30 | Income Tax Assessment Act 1997 | liability of members of consolidated groups |

18 | 840‑810 | Income Tax Assessment Act 1997 | payment of managed investment trust withholding tax |

19 | 214‑105 | Income Tax (Transitional Provisions) Act 1997 | payment of franking deficit tax |

20 | 85 | Petroleum Resource Rent Tax Assessment Act 1987 | payment of petroleum resource rent tax, shortfall interest charge or instalment transfer interest charge |

21 | 35 | Product Grants and Benefits Administration Act 2000 | payment of a designated scheme debt |

22 | 21 | Superannuation Contributions Tax (Assessment and Collection) Act 1997 | increase in liability to pay superannuation contributions surcharge because of amendment of assessment |

23 | 22 | Superannuation Contributions Tax (Assessment and Collection) Act 1997 | liability to pay superannuation contributions surcharge because of new assessment |

24 | 25 | Superannuation Contributions Tax (Assessment and Collection) Act 1997 | payment of superannuation contributions surcharge or advance instalment |

25 | 18 | Superannuation Contributions Tax (Members of Constitutionally Protected Superannuation Funds) Assessment and Collection Act 1997 | increase in liability to pay superannuation contributions surcharge because of amendment of assessment |

26 | 21 | Superannuation Contributions Tax (Members of Constitutionally Protected Superannuation Funds) Assessment and Collection Act 1997 | payment of superannuation contributions surcharge |

27 | 25 | Superannuation (Government Co‑contribution for Low Income Earners) Act 2003 | repayments or underpayments of Government co‑contributions that cannot be credited to an account |

28 | 49 | Superannuation Guarantee (Administration) Act 1992 | payment of superannuation guarantee charge |

29 | 15DC | Superannuation (Self Managed Superannuation Funds) Taxation Act 1987 | payment of superannuation (self managed superannuation funds) supervisory levy |

30 | 17A | Superannuation (Unclaimed Money and Lost Members) Act 1999 | payment of unclaimed money |

31 | 18C | Superannuation (Unclaimed Money and Lost Members) Act 1999 | repayment of Commissioner’s payment that cannot be credited to an account |

32 | 20F | Superannuation (Unclaimed Money and Lost Members) Act 1999 | payment of unclaimed superannuation of former temporary residents |

33 | 20M | Superannuation (Unclaimed Money and Lost Members) Act 1999 | repayment of Commissioner’s payment for former temporary resident that cannot be credited to an account |

34 | 24F | Superannuation (Unclaimed Money and Lost Members) Act 1999 | payment in respect of lost member accounts |

35 | 24L | Superannuation (Unclaimed Money and Lost Members) Act 1999 | repayment of Commissioner’s payment for former lost member that cannot be credited to an account |

36 | 8AAZF | Taxation Administration Act 1953 | RBA deficit debts |

37 | 8AAZN | Taxation Administration Act 1953 | overpayments made by the Commissioner |

38 | 16‑80 in Schedule 1 | Taxation Administration Act 1953 | payment of PAYG withholding amounts |

39 | 45‑80 in Schedule 1 | Taxation Administration Act 1953 | payment of PAYG instalments |

40 | 45‑230 in Schedule 1 | Taxation Administration Act 1953 | shortfall in quarterly PAYG instalments worked out on the basis of a varied rate |

41 | 45‑232 in Schedule 1 | Taxation Administration Act 1953 | shortfall in quarterly PAYG instalments worked out on the basis of estimated benchmark tax |

42 | 45‑235 in Schedule 1 | Taxation Administration Act 1953 | shortfall in annual PAYG instalments |

43 | 45‑600 and 45‑620 in Schedule 1 | Taxation Administration Act 1953 | tax benefits relating to PAYG instalments |

44 | 45‑870 and 45‑875 in Schedule 1 | Taxation Administration Act 1953 | head company’s liability on shortfall in quarterly PAYG instalments |

45 | 105‑80 in Schedule 1 | Taxation Administration Act 1953 | payment of a net fuel amount or an amount of indirect tax |

46 | 263‑30 in Schedule 1 | Taxation Administration Act 1953 | payment of a foreign revenue claim |

47 | 268‑75 in Schedule 1 | Taxation Administration Act 1953 | late payment of estimate |

48 | 298‑25 in Schedule 1 | Taxation Administration Act 1953 | payment of administrative penalty |

49 | 9 | Tax Bonus for Working Australians Act (No. 2) 2009 | repayment of overpayment of tax bonus |

50 | 13 | Termination Payments Tax (Assessment and Collection) Act 1997 | increase in liability to pay termination payments surcharge because of amendment of assessment |

51 | 16 | Termination Payments Tax (Assessment and Collection) Act 1997 | payment of termination payments surcharge |

36 Subsection 30‑20(2) (table items 1.2.2 and 1.2.3)

Repeal the items.

37 Subsection 30‑20(2) (cell at table item 1.2.4, column headed “Fund, authority or institution”)

Repeal the cell, substitute:

The Royal Australian and New Zealand College of Radiologists |

38 Subsection 30‑20(2) (table items 1.2.11 and 1.2.15)

Repeal the items.

39 Subsection 30‑25(2) (table items 2.2.15 and 2.2.19)

Repeal the items.

40 Subsection 30‑40(2) (table item 3.2.3)

Repeal the item.

41 Subsection 30‑45(2) (table items 4.2.5 and 4.2.15)

Repeal the items.

42 Subsection 30‑50(2) (table items 5.2.16, 5.2.24 and 5.2.27)

Repeal the items.

43 Section 30‑65 (table items 7.2.1, 7.2.2 and 7.2.4)

Repeal the items.

44 Subsection 30‑80(2) (table items 9.2.2, 9.2.15 and 9.2.16)

Repeal the items.

45 Section 30‑90 (table item 10.2.6)

Repeal the item.

46 Section 30‑105 (table items 13.2.5, 13.2.11 and 13.2.14)

Repeal the items.

47 Section 30‑315 (table items 5, 19, 21, 24, 25, 25C, 26, 28AAA, 28A, 28AB, 31A, 34, 38, 50A, 60A, 61, 83 and 91)

Repeal the items.

48 Section 30‑315 (after table item 98)

Insert:

98A | Royal Australian and New Zealand College of Radiologists | item 1.2.4 |

49 Section 30‑315 (table items 105B, 112AFA, 112AG, 112BA and 121C)

Repeal the items.

50 Transitional provision—endorsement as deductible gift recipients

(1) Treat Breast Cancer Network Australia and Indigenous Community Volunteers Limited as having been endorsed as deductible gift recipients under section 30‑120 of the Income Tax Assessment Act 1997 at the commencement of this item.

(2) To avoid doubt, subitem (1) does not prevent the Commissioner from revoking either or both of those endorsements at a later time under section 426‑55 in Schedule 1 to the Taxation Administration Act 1953.

51 Subsection 30‑50(2) (table item 5.2.25)

Repeal the item.

52 Subsection 30‑80(2) (table item 9.2.20)

Repeal the item.

53 Section 30‑105 (table items 13.2.4, 13.2.6, 13.2.12 and 13.2.13)

Repeal the items.

54 Section 30‑315 (table items 20AA, 45AA, 49A, 81, 86F and 127AA)

Repeal the items.

55 Item 15 of Schedule 3 (heading)

Omit “49A,”.

Note: This item makes an amendment consequential on item 3 of Schedule 6 to the Tax Laws Amendment (2008 Measures No. 2) Act 2008.

56 Effect of omission

To avoid doubt, item 15 of Schedule 3 to the Tax Laws Amendment (Repeal of Inoperative Provisions) Act 2006 is taken never to have repealed item 49A of the table in section 30‑105 of the Income Tax Assessment Act 1997.

57 At the end of paragraph 23AB(5)(a)

Add “and”.

Note: This item and items 59 and 60 add conjunctions at the end of paragraphs, for consistency with current drafting practice.

58 Subsection 23AB(7)

After “that service” (first occurring), insert “. The amount of the rebate is”.

59 At the end of paragraph 23AB(7)(a)

Add “and”.

60 At the end of paragraph 23AB(10)(a)

Add “or”.

61 Subsection 6(1) (at the end of the definition of dividend)

Add:

Note: Subsection (4) sets out when paragraph (d) of this definition does not apply.

62 Subsection 6(1) (at the end of the definition of permanent establishment)

Add:

Note: Subsection (6) treats a person as carrying on, at or through a permanent establishment that is a place described in paragraph (d) of this definition, the business of selling the goods manufactured, assembled, processed, packed or distributed by the other person as described in that paragraph.

63 Subsection 6(1) (definition of RSA)

Repeal the definition, substitute:

RSA has the same meaning as in the Income Tax Assessment Act 1997.

Note: That Act defines RSA as having the meaning given by the Retirement Savings Accounts Act 1997.

64 Subsection 6(1) (definition of RSA provider)

Repeal the definition, substitute:

RSA provider has the same meaning as in the Income Tax Assessment Act 1997.

Note: That Act defines RSA provider as having the same meaning as in the Retirement Savings Accounts Act 1997.

65 At the end of paragraph 6AA(1)(d)

Add “and”.

66 Paragraph 6AA(1)(e)

Omit “Australia; and”, substitute “Australia.”.

67 Paragraph 6AA(1)(f)

Repeal the paragraph.

68 Paragraph 45C(3)(a)

Omit “class C”.

69 Application provision—amendment of paragraph 45C(3)(a)

The amendment of paragraph 45C(3)(a) of the Income Tax Assessment Act 1936 made by this Part applies to notices of determination under section 45B of that Act served on or after 1 July 2002.

70 Subsections 45C(5) and (6)

Repeal the subsections.

71 Subsection 45D(2)

Omit “referred to in paragraph (1)(b)”, substitute “under section 45A”.

72 Application provision—amendment of subsection 45D(2)

The amendment of subsection 45D(2) of the Income Tax Assessment Act 1936 made by this Part applies to determinations made under section 45A of that Act on or after 24 October 2002.

Note: The heading to section 159HA is altered by omitting “, 159K”.

73 Subsection 159J(1B)

Omit “the the”, substitute “the”.

74 Section 3‑1

Repeal the section.

75 Subsection 3‑5(1) (note 1)

Omit “Division 785”, substitute “the Medicare Levy Act 1986 and Part VIIB of the Income Tax Assessment Act 1936”.

76 Section 11‑15 (table item headed “United Nations”)

Omit:

Australian Federal Police member in Cambodia, pay and allowance |

|

77 Section 830‑75

Omit “*subject to tax” (wherever occurring), substitute “*subject to foreign tax”.

Note: This item corrects references to a definition that was repealed.

78 Subsection 25‑5(7)

Omit “tax debts”, substitute “*tax debts”.

79 Paragraph 128B(3)(ab)

Repeal the paragraph.

80 Section 11‑5 (table item headed “film”)

Repeal the item.

81 Section 11‑5 (table item headed “mining”)

Omit:

Phosphate Mining Company of Christmas Island...... | 50‑35 |

82 Section 50‑35 (table item 7.1)

Repeal the item.

83 Section 50‑45 (heading)

Repeal the heading, substitute:

84 Section 50‑45 (table items 9.3 and 9.4)

Repeal the items.

85 Subsection 114‑15(2)

Omit “quarter”, substitute “*quarter”.

86 Subsection 114‑15(3) (method statement, steps 1 and 3)

Omit “quarter”, substitute “*quarter”.

87 Subsections 114‑15(5) and (6)

Omit “quarter”, substitute “*quarter”.

88 Section 114‑20

Omit “quarter”, substitute “*quarter”.

89 Paragraph 118‑150(4)(a)

Repeal the paragraph, substitute:

(a) 4 years, or a longer time allowed by the Commissioner, before the *dwelling becomes your main residence; and

90 Application provision—amendment of subsection 118‑150(4)

The amendment of subsection 118‑150(4) of the Income Tax Assessment Act 1997 made by this Part applies in relation to CGT events happening on or after the day this Act receives the Royal Assent.

91 Paragraph 152‑10(1)(c) (note)

Repeal the note, substitute:

Note: For determining whether an entity is a small business entity, see Subdivision 328‑C (as affected by sections 152‑48 and 152‑78).

92 Subsection 152‑10(1A) (note 1)

Repeal the note, substitute:

Note 1: The meaning of connected with is affected by section 152‑78.

Note 2: For determining whether an entity is a small business entity, see Subdivision 328‑C (as affected by sections 152‑48 and 152‑78).

93 Subsection 152‑10(1A) (note 2)

Omit “Note 2:”, substitute “Note 3:”.

94 Section 152‑15 (note)

After “Note”, insert “1”.

95 At the end of section 152‑15

Add:

Note 2: The meaning of connected with is affected by section 152‑78.

96 At the end of subsections 152‑20(2), (3) and (4)

Add:

Note: The meaning of connected with is affected by section 152‑78.

97 Subsection 152‑40(1) (note 2)

Omit “152‑42”, substitute “152‑78”.

98 At the end of subsections 152‑40(4) and (4A)

Add:

Note: The meaning of connected with is affected by section 152‑78.

99 Section 152‑42

Repeal the section.

100 At the end of subsection 152‑47(1)

Add:

Note: The meaning of connected with an entity is affected by section 152‑78.

101 At the end of subsection 152‑48(2)

Add:

Note: Paragraphs (a) and (b)—the meaning of connected with is affected by section 152‑78.

102 After section 152‑75

Insert:

(1) This section applies for the purposes of determining whether an entity is *connected with you, for the purposes of:

(a) this Subdivision; and

(b) sections 328‑110, 328‑115 and 328‑125 so far as they relate to this Subdivision.

(2) The trustee of a discretionary trust may nominate not more than 4 beneficiaries as being controllers of the trust for an income year (the relevant income year) for which the trustee did not make a distribution of income or capital if the trust had a *tax loss, or no *net income, for that year.

(3) A nomination under subsection (2) has effect as if each nominated beneficiary controlled the trust for the relevant income year in a way described in section 328‑125.

Note: This means each nominated beneficiary is connected with the trust.

(4) A nomination under subsection (2) must:

(a) be in writing; and

(b) be signed by the trustee and by each nominated beneficiary.

103 Subsection 328‑115(1) (note)

Repeal the note, substitute:

Note: For small business CGT relief purposes, additional entities may be treated as being connected with you or your affiliate under sections 152‑48 and 152‑78.

104 Subsection 995‑1(1) (note at the end of the definition of connected with)

Omit “152‑42”, substitute “152‑78”.

105 Application and transitional provisions

Application provision

(1) Section 152‑78 of the Income Tax Assessment Act 1997 applies:

(a) for the purposes of the following provisions relating to CGT events that happen on or after the day this Act receives the Royal Assent:

(i) Subdivision 152‑A of that Act;

(ii) sections 328‑110, 328‑115 and 328‑125 of that Act so far as they relate to that Subdivision; and

(b) for the purposes of the following provisions (and not any other provisions of Subdivision 152‑A of that Act) relating to CGT events that happen before the day this Act receives the Royal Assent but after the start of the 2007‑08 income year:

(i) paragraph 152‑10(1A)(a) of that Act;

(ii) another provision of that Subdivision so far as the provision relates to that paragraph;

(iii) sections 328‑110, 328‑115 and 328‑125 of that Act so far as they relate to a provision covered by subparagraph (i) or (ii) of this paragraph.

Note: Section 152‑78 of the Income Tax Assessment Act 1997 does not apply for the purposes of a provision of Subdivision 152‑A of that Act that is not covered by subparagraph (1)(b)(i) or (ii) of this item relating to CGT events that happen between the start of the 2007‑08 income year and the day this Act receives the Royal Assent.

(2) The repeal of section 152‑42 of the Income Tax Assessment Act 1997 applies for the purposes of subparagraph 152‑40(1)(a)(iii) or paragraph 152‑40(1)(b) of that Act relating to CGT events that happen on or after the day this Act receives the Royal Assent.

Extension of time to make choice

(3) Subitem (4) applies in relation to:

(a) a CGT event that happened before the day this Act receives the Royal Assent; and

(b) an entity that becomes eligible to make a choice under Division 152 of the Income Tax Assessment Act 1997 in relation to that event because of the satisfaction of the conditions in subsection 152‑10(1A) of that Act because of this Part.

(4) Despite subsection 103‑25(1) of the Income Tax Assessment Act 1997, any such choice by the entity must be made by the latest of:

(a) the day the entity lodges its income tax return for the income year in which the relevant CGT event happened; and

(b) 12 months after the day this Act receives the Royal Assent; and

(c) a later day allowed by the Commissioner of Taxation.

106 Paragraphs 115‑50(2)(a), (3)(a) and (4)(a)

Omit “fixed entitlements”, substitute “*fixed entitlements”.

107 Subsection 121‑30(2)

Omit “fixed trusts”, substitute “*fixed trusts”.

108 Paragraph 124‑810(3)(a)

Omit “fixed entitlements”, substitute “*fixed entitlements”.

109 Subsection 165‑45(4) (note 2)

After “to”, insert “subsections (3) and (4) of”.

110 Subparagraph 165‑215(2)(a)(i)

Omit “fixed entitlements”, substitute “*fixed entitlements”.

111 Subparagraph 165‑215(2)(a)(ii)

Omit “non‑fixed trusts”, substitute “*non‑fixed trusts”.

112 Subparagraph 165‑215(2)(b)(i)

Omit “fixed trust”, substitute “*fixed trust”.

113 Subsection 165‑215(3)

Omit “fixed entitlements” (first occurring), substitute “*fixed entitlements”.

114 Paragraph 165‑215(4)(a)

Omit “fixed entitlements”, substitute “*fixed entitlements”.

115 Subsection 165‑215(5)

Omit “non‑fixed trust (other than an excepted trust) that, at any time during the *ownership test period, held directly or indirectly a fixed entitlement”, substitute “*non‑fixed trust (other than an *excepted trust) that, at any time during the *ownership test period, held directly or indirectly a *fixed entitlement”.

116 At the end of subsection 165‑215(5)

Add:

Note: See section 165‑245 for when an entity is taken to have held or had, directly or indirectly, a fixed entitlement to a share of income or capital of a company.

117 Subparagraph 165‑220(2)(a)(i)

Omit “fixed entitlements”, substitute “*fixed entitlements”.

118 Subparagraph 165‑220(2)(a)(ii)

Omit “non‑fixed trusts”, substitute “*non‑fixed trusts”.

119 Subparagraph 165‑220(2)(b)(i)

Omit “fixed trust”, substitute “*fixed trust”.

120 Subparagraph 165‑220(2)(b)(ii)

Omit “*family trusts”, substitute “family trusts”.

121 Subsection 165‑220(3)

Omit “fixed entitlements” (first occurring), substitute “*fixed entitlements”.

122 Paragraph 165‑220(4)(a)

Omit “fixed entitlements”, substitute “*fixed entitlements”.

123 Subsection 165‑220(5)

Omit “non‑fixed trust (other than an excepted trust) that, at any time in the income year, held directly or indirectly a fixed entitlement”, substitute “*non‑fixed trust (other than an *excepted trust) that, at any time in the income year, held directly or indirectly a *fixed entitlement”.

124 At the end of subsection 165‑220(5)

Add:

Note: See section 165‑245 for when an entity is taken to have held or had, directly or indirectly, a fixed entitlement to a share of income or capital of a company.

125 Section 165‑225

Repeal the section, substitute:

(1) If:

(a) the company is required to calculate:

(i) its taxable income and *tax loss for the income year under Subdivision 165‑B; and

(ii) its *net capital gain and *net capital loss for the income year under Subdivision 165‑CB; and

(b) the company meets the requirements of subsections 165‑220(2) and (4);

then, in dividing the income year into periods, apply subsection (2) of this section instead of subsections 165‑45(3) and (4).

(2) The last period ends at the end of the income year. Each period (except the last) ends at the earliest of:

(a) the latest time that would result in the persons holding *fixed entitlements to shares of the income or shares of the capital of:

(i) if the company meets the requirements of paragraph 165‑220(2)(a)—the company; or

(ii) if the company meets the requirements of paragraph 165‑220(2)(b)—the holding entity mentioned in that paragraph;

and the percentages of the shares that they hold, remaining the same during the whole of the period; and

(b) the times that, for all of the *non‑fixed trusts, other than *excepted trusts, holding directly or indirectly a fixed entitlement to a share of the income or capital of the company at any time during the income year, are the latest times that would result in individuals having *more than a 50% stake in their income or capital; and

(c) the earliest time in the period when a group (within the meaning of Schedule 2F to the Income Tax Assessment Act 1936) begins to *control a non‑fixed trust, other than an excepted trust, that holds directly or indirectly a fixed entitlement to a share of the income or capital of the company at any time during the income year.

Note: See section 165‑245 for when an entity is taken to have held or had, directly or indirectly, a fixed entitlement to a share of income or capital of a company.

126 Subparagraph 165‑230(2)(a)(i)

Omit “fixed entitlements”, substitute “*fixed entitlements”.

127 Subparagraph 165‑230(2)(a)(ii)

Omit “non‑fixed trusts”, substitute “*non‑fixed trusts”.

128 Subparagraph 165‑230(2)(b)(i)

Omit “fixed trust”, substitute “*fixed trust”.

129 Subparagraph 165‑230(2)(b)(ii)

Omit “*family trusts”, substitute “family trusts”.

130 Subsection 165‑230(3)

Omit “fixed entitlements” (first occurring), substitute “*fixed entitlements”.

131 Paragraph 165‑230(4)(a)

Omit “fixed entitlements”, substitute “*fixed entitlements”.

132 Subsection 165‑230(5)

Omit “non‑fixed trust (other than an excepted trust) that, at any time during the *ownership test period, held directly or indirectly a fixed entitlement”, substitute “*non‑fixed trust (other than an *excepted trust) that, at any time during the *ownership test period, held directly or indirectly a *fixed entitlement”.

133 At the end of subsection 165‑230(5)

Add:

Note: See section 165‑245 for when an entity is taken to have held or had, directly or indirectly, a fixed entitlement to a share of income or capital of a company.

134 Subsection 165‑235(3)

Omit “non‑fixed trust”, substitute “*non‑fixed trust”.

135 Paragraph 165‑235(4)(a)

Omit “non‑fixed trust”, substitute “*non‑fixed trust”.

136 Subsection 165‑240(1)

Omit “non‑fixed trust”, substitute “*non‑fixed trust”.

137 Section 165‑245

Repeal the section, substitute:

For the purposes of this Act, an entity is taken to have held or had, directly or indirectly, a *fixed entitlement to a share of income or capital of a company at a time if and only if the entity held or had, directly or indirectly, that fixed entitlement at that time for the purposes of Schedule 2F to the Income Tax Assessment Act 1936.

138 Paragraph 207‑130(6)(f)

Omit “more than a 50% stake”, substitute “*more than a 50% stake”.

139 Subsection 707‑130(1) (note 1)

Omit “(as defined in that Schedule)”.

140 Subsection 707‑130(1) (note 1)

Omit “, as defined in that Schedule,”.

141 Subsection 995‑1(1)

Insert:

control a non‑fixed trust has the meaning given by Subdivision 269‑E in Schedule 2F to the Income Tax Assessment Act 1936.

142 Subsection 995‑1(1)

Insert:

excepted trust has the meaning given by section 272‑100 in Schedule 2F to the Income Tax Assessment Act 1936.

143 Subsection 995‑1(1) (definition of fixed entitlement)

After “capital of a”, insert “company, partnership or”.

144 Subsection 995‑1(1) (at the end of the definition of fixed entitlement)

Add:

Note: Section 165‑245 affects when an entity is taken to have held or had, directly or indirectly, a fixed entitlement to a share of income or capital of a company.

145 Subsection 995‑1(1) (definition of more than a 50% stake)

Repeal the definition, substitute:

more than a 50% stake:

(a) more than a 50% stake in a company has the meaning given by section 165‑37; and

(b) more than a 50% stake in the income or capital of a trust has the meaning given by section 269‑50 in Schedule 2F to the Income Tax Assessment Act 1936.

146 Paragraph 45‑287(1)(a) in Schedule 1

Omit “fixed entitlements”, substitute “*fixed entitlements”.

147 Paragraph 45‑287(4)(a) in Schedule 1

Omit “fixed entitlement”, substitute “*fixed entitlement”.

148 Section 204‑70

Repeal the section, substitute:

(1) This Subdivision applies to an entity if the difference between:

(a) the *benchmark franking percentage for the entity for a *franking period (the current franking period); and

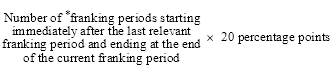

(b) the benchmark franking percentage for the entity for the last franking period in which a *frankable distribution was made (the last relevant franking period);

is more than the amount worked out using the following formula (whether the percentage for the current franking period is more than or less than the percentage for the last relevant franking period):

(2) However, this Subdivision does not apply to an entity to which the benchmark rule does not apply.

Note: Section 203‑20 identifies the entities to which the benchmark rule does not apply.

149 Subsections 204‑75(1) and (2)

Repeal the subsections, substitute:

(1) The entity must notify the Commissioner in writing of the difference.

150 Subsection 204‑80(1)

Omit “If the *benchmark franking percentage for an entity for a *franking period (the current franking period) *differs significantly from the benchmark franking percentage for the entity for the last franking period in which a *frankable distribution was made (the last relevant franking period), the”, substitute “The”.

151 Subparagraph 320‑141(2)(a)(i)

Omit “*virtual PST assets”, substitute “*complying superannuation/FHSA assets”.

152 Subparagraph 320‑141(2)(a)(ii)

Omit “virtual PST assets”, substitute “complying superannuation/FHSA assets”.

153 Application provision—amendments of paragraph 320‑141(2)(a)

The amendments of paragraph 320‑141(2)(a) of the Income Tax Assessment Act 1997 made by this Part apply on and after 26 June 2008.

154 Section 13‑1 (table item headed “land transport facilities borrowings”)

Repeal the item.

155 Subsection 250‑60(3)

Omit “facilities”, substitute “facilities”.

156 Paragraph 250‑60(3)(d)

Repeal the paragraph.

157 Paragraph 250‑60(3)(e)

Omit “other”.

158 Division 396

Repeal the Division.

159 Subsection 995‑1(1) (definition of land transport facilities borrowings agreement)

Repeal the definition.

160 Subsection 995‑1(1) (definition of land transport facility)

Repeal the definition.

161 Subsection 995‑1(1) (definition of LTF interest)

Repeal the definition.

162 Subsection 995‑1(1) (definition of related facility)

Repeal the definition.

163 At the end of section 725‑250

Add:

Reducing uplift to prevent double increase in cost base etc.

(3) However, if, apart from paragraph (2)(b), an amount is included in the *cost base or *reduced cost base of an *up interest as a result of the *scheme under which the *direct value shift happens, the uplift in the *adjustable value of the interest under that paragraph is reduced by that amount.

164 At the end of subsection 725‑255(2)

Add:

Note: If subsection 725‑250(3) is relevant, it will affect all the uplifts worked out under all those items.

165 After subsection 725‑335(3)

Insert:

Reducing uplift to prevent double increase in adjustable value

(3A) However, if, apart from paragraph (3)(b), an amount is included, as a result of the *scheme under which the *direct value shift happens, in the *adjustable value of an *up interest that is your *trading stock or *revenue asset, the uplift in the adjustable value of the interest under that paragraph is reduced by that amount.

166 At the end of subsection 725‑340(2)

Add:

Note: If subsection 725‑335(3A) is relevant, it will affect all the uplifts worked out under all those items.

167 Application provision

Subsections 725‑250(3) and 725‑335(3A) of the Income Tax Assessment Act 1997 apply in relation to schemes entered into on or after the commencement of those subsections.

168 Subsection 2(1)

Insert:

ineligible income tax remission decision has the meaning given by section 14ZS.

169 Section 14ZQ (definition of ineligible income tax remission decision)

Repeal the definition.

170 Subsection 14ZS(1)

Repeal the subsection.

171 Subsection 14ZS(2)

Omit “(2) An objection decision is an ineligible income tax remission decision”, substitute “(1) An objection decision is an ineligible income tax remission decision”.

172 Subsection 14ZS(5)

Renumber as subsection (2).

173 Subparagraph 855‑40(2)(b)(i)

Omit “fixed trust”, substitute “*fixed trust”.

174 Subparagraph 855‑40(2)(b)(ii)

Omit “a *chain of fixed trusts”, substitute “a *chain of trusts, each trust in which is a fixed trust”.

175 Paragraph 855‑40(6)(b)

Omit “a *chain of fixed trusts”, substitute “a *chain of trusts, each trust in which is a fixed trust”.

176 Subsection 6(1) (definition of income from personal exertion)

Omit “him” (wherever occurring), substitute “the taxpayer”.

177 Subsection 6(1) (paragraph (a) of the definition of income from personal exertion)

Omit “his”, substitute “the taxpayer’s”.

178 Subsection 6(1) (paragraph (e) of the definition of permanent establishment)

After “his”, insert “or her”.

179 Subsection 6(1) (subparagraphs (a)(i) and (ii) of the definition of resident)

Omit “his”, substitute “the person’s”.

180 Subsection 6(1) (subparagraph (a)(ii) of the definition of resident)

Omit “he”, substitute “the person”.

181 Section 6A

Omit “his” (wherever occurring), substitute “the person’s”.

182 Subsection 14(2)

After “him”, insert “or her”.

183 Subsection 14(2)

After “he”, insert “or she”.

184 Subsection 23AA(2)

After “him”, insert “or her”.

185 Paragraphs 23AA(3)(a), (b) and (c) and (6)(a)

Omit “he”, substitute “the person”.

186 Subsection 23AB(2)

After “his”, insert “, her”.

187 Subsection 23AB(7)

After “his”, insert “or her”.

188 Subsection 23AB(7)

After “he”, insert “or she”.

189 Paragraph 23AB(7)(b)

After “him”, insert “or her”.

190 Subsection 23AB(11)

After “his”, insert “or her”.

191 Subparagraph 23AC(3)(a)(i)

Omit “he” (wherever occurring), substitute “the member”.

192 Subparagraph 23AC(3)(a)(i)

Omit “his”, substitute “the member’s”.

193 Subparagraphs 23AC(3)(a)(ii) and (iii)

Omit “he” (wherever occurring), substitute “the member”.

194 Subparagraph 23AC(3)(a)(iii)

Omit “his”, substitute “the member’s”.

195 Subparagraph 23AC(3)(a)(iv)

Omit “he” (wherever occurring), substitute “the member”.

196 Subparagraph 23AC(3)(b)(i)

Omit “his” (first occurring), substitute “the member’s”.

197 Subparagraph 23AC(3)(b)(i)

Omit “he” (wherever occurring), substitute “the member”.

198 Subparagraph 23AC(3)(b)(i)

Omit “his” (second occurring), substitute “the member’s”.

199 Subparagraph 23AC(3)(b)(ii)

Omit “he” (wherever occurring), substitute “the member”.

200 Subsection 23AF(11)

Omit “he”, substitute “that Minister”.

201 Subsection 23AF(11)

Omit “him”, substitute “that Minister”.

202 Subsection 23AF(12)

Omit “him”, substitute “that Minister”.

203 Subsection 23AF(12)

Omit “his”, substitute “that Minister’s”.

204 Subsection 23AF(18) (paragraph (a) of the definition of eligible foreign remuneration)

After “his”, insert “or her”.

205 Subsection 24B(1) (paragraph (b) of the definition of prescribed person)

After “his”, insert “or her”.

206 Paragraph 24C(a)

After “his”, insert “or her”.

207 Subsection 24D(4)

Omit “his”, substitute “that holder’s”.

208 Paragraph 24E(1)(b)

After “his”, insert “or her”.

209 Paragraph 24E(4)(b)

Omit “he”, substitute “the trustee”.

210 Paragraph 24E(4)(c)

Omit “his”, substitute “the trustee’s”.

211 Paragraph 24G(1)(e)

After “he”, insert “or she”.

212 Subsection 25A(1)

Omit “him”, substitute “the taxpayer”.

213 Paragraph 25A(10)(a)

Omit “his”, substitute “the Commissioner’s”.

214 Subparagraph 25A(11)(b)(i)

Omit “his”, substitute “the transferee’s”.

215 Subsection 26AB(4)

Omit “he”, substitute “the taxpayer”.

216 Paragraphs 26AG(3)(d) and (e)

After “his”, insert “or her”.

217 Subsection 26AG(4)

After “his”, insert “or her”.

218 Paragraphs 26AG(10)(f) and (g)

After “his” (wherever occurring), insert “or her”.

219 Paragraph 26AH(2)(b)

After “he”, insert “or she”.

220 Subsection 26AH(4)

After “his”, insert “or her”.

221 Subsection 26AH(4)

After “he”, insert “or she”.

222 Subparagraph 26C(2)(b)(i)

After “his”, insert “or her”.

223 Subsection 27(1)

Omit “him”, substitute “the resident”.

224 Subsection 27(1)

Omit “his”, substitute “the resident’s”.

225 Subsection 51AD(9)

Omit “he” (wherever occurring), substitute “the Commissioner”.

226 Paragraph 51AD(20)(f)

Omit “he”, substitute “the taxpayer”.

227 Subsection 52(1)

Omit “his” (first occurring), substitute “the taxpayer’s”.

228 Subsection 52(1)

After “he”, insert “or she”.

229 Subsection 52(1)

After “his” (second occurring), insert “or her”.

230 Subsection 52(1)

Omit “him”, substitute “the taxpayer”.

231 Paragraph 52A(3)(j)

After “he”, insert “or she”.

232 Subsection 73A(2)

Omit “by him or on his behalf”, substitute “by or on behalf of the taxpayer”.

233 Paragraph 73A(2)(b)

Omit “he”, substitute “the taxpayer”.

234 Subsection 79A(1)

Omit “his”, substitute “the taxpayer’s”.

235 Paragraph 79A(2)(f)

Omit “him” (first occurring), substitute “the taxpayer”.

236 Paragraph 79A(2)(f)

Omit “he”, substitute “the taxpayer”.

237 Paragraph 79A(2)(f)

Omit “him” (last occurring), substitute “the taxpayer”.

238 Subsection 79A(2A)

Omit “his”, substitute “the taxpayer’s”.

239 Paragraph 79A(3B)(c)

After “his”, insert “or her”.

240 Subsection 79A(3E)

After “he”, insert “or she”.

241 Subsection 79B(1)

After “his”, insert “or her”.

242 Paragraph 79B(2)(b)

After “him”, insert “or her”.

243 Subsections 79B(5) and (5A)

Omit “him”, substitute “the Treasurer”.

244 Section 82

Omit “him”, substitute “the person”.

245 Subsection 82KL(8)

Omit “his”, substitute “the Commissioner’s”.

246 Subsection 82L(1) (paragraph (b) of the definition of convertible note)

After “him” (wherever occurring), insert “or her”.

247 Paragraph 82M(1)(b)

After “him” (wherever occurring), insert “or her”.

248 Paragraphs 82P(2)(b) and (3)(b)

After “him” (wherever occurring), insert “or her”.

249 Subsection 82R(2)

After “him” (wherever occurring), insert “or her”.

250 Subparagraph 82SA(1)(d)(i)

After “him”, insert “or her”.

251 Subparagraph 82SA(1)(d)(vii)

After “his”, insert “or her”.

252 Subparagraph 82SA(1)(d)(vii)

After “he” (first occurring), insert “or she”.

253 Subparagraph 82SA(1)(d)(vii)

After “he” (last occurring), insert “, she”.

254 Subparagraph 82SA(1)(d)(viii)

After “he”, insert “or she”.

255 Paragraph 94(2)(a)

After “his”, insert “or her”.

256 Subsections 94(9), (10), (10A) and (10B)

After “his” (wherever occurring), insert “or her”.

257 Sub‑subparagraph 94(10C)(a)(i)(A)

After “his”, insert “or her”.

258 Section 95B

After “his”, insert “or her”.

259 Paragraph 99A(3)(c)

After “he”, insert “or she”.

260 Paragraph 99C(2)(e)

After “his”, insert “or her”.

261 Section 101

Omit “his” (first occurring), substitute “the trustee’s”.

262 Section 101

Omit “him”, substitute “the beneficiary”.

263 Section 101

Omit “his” (second occurring), substitute “the beneficiary’s”.

264 Subsection 101A(1)

Omit “him during his”, substitute “him or her during his or her”.

265 Subsection 101A(2)

After “his”, insert “or her”.

266 Paragraph 102(1)(a)

Omit “he”, substitute “the person”.

267 Subsection 102(2)

Omit “his”, substitute “the person’s”.

268 Subsection 102(2)

Omit “him” (first occurring), substitute “the person”.

269 Subsection 102(2)

After “he” (first occurring), insert “or she”.

270 Subsection 102(2)

Omit “him” (last occurring), substitute “the person”.

271 Paragraphs 102(2)(a) and (b)

After “he”, insert “or she”.

272 Subsection 102(3)

After “his” (wherever occurring), insert “or her”.

273 Subparagraphs 102A(4)(a)(i) and (b)(i)

After “he”, insert “or she”.

274 Paragraph 102G(11)(a)

After “he”, insert “or she”.

275 Paragraphs 102G(11)(b) and (c)

After “his” (wherever occurring), insert “or her”.

276 Subsection 103(2)

After “his”, insert “or her”.

277 Paragraph 103A(5)(d)

Omit “he”, substitute “the Commissioner”.

278 Paragraph 103A(7)(a)

After “he”, insert “or she”.

279 Paragraphs 103A(7)(b) and (c)

After “his” (wherever occurring), insert “or her”.

280 Subsection 120(2)

After “his” (wherever occurring), insert “or her”.

281 Subsection 126(3)

Omit “he shall refund to him the amount of tax paid by the company in respect of his debentures”, substitute “the Commissioner must refund to that person the amount of tax paid by the company in respect of his or her debentures”.

282 Subsection 128A(3)

After “he”, insert “or she”.

283 Subsections 128B(10) and (11)

After “him”, insert “or her”.

284 Sections 129 and 130

After “him” (wherever occurring), insert “or her”.

285 Section 131

Omit “he”, substitute “the Commissioner”.

286 Section 134

Omit “him”, substitute “the person”.

287 Sections 134 and 135

After “he”, insert “or she”.

288 Subsections 136AF(1) and (3)

Omit “he”, substitute “the Commissioner”.

289 Subsection 136AF(5)

Omit “his”, substitute “the Commissioner’s”.

290 Sections 142, 143 and 147

Omit “him” (wherever occurring), substitute “the insurer”.

291 Subsection 148(2)

Omit “his” (wherever occurring), substitute “that person’s”.

292 Paragraph 148(2)(b)

Omit “he”, substitute “that person”.

293 Subsection 148(3)

After “he”, insert “or she”.

294 Subsection 148(3)

After “him”, insert “or her”.

295 Subsection 148(4)

Omit “him” (wherever occurring), substitute “that person”.

296 Subsections 148(5) and (8)

Omit “he”, substitute “that person”.

297 Subsection 148(9)

Omit “him”, substitute “that person”.

298 Paragraph 148(9)(a)

Omit “he”, substitute “that person”.

299 Paragraph 148(9)(a)

Omit “his”, substitute “that person’s”.

300 Paragraph 148(9)(b)

Omit “he” (wherever occurring), substitute “that person”.

301 Section 152

Omit “him as if he”, substitute “the taxpayer as if he or she”.

302 Subsection 155(1)

After “his” (wherever occurring), insert “or her”.

303 Subsection 155(1)

After “he” (first occurring), insert “or she”.

304 Subsection 155(1)

After “him”, insert “or her”.

305 Subsection 155(1)

After “he” (last occurring), insert “or she”.

306 Subsection 155(2)

After “him”, insert “or her”.

307 Subsection 155(2)

After “he”, insert “or she”.

308 Subsection 156(1) (definition of relevant primary production deductions)

Omit “his” (wherever occurring), substitute “the taxpayer’s”.

309 Subsection 156(5)

After “his”, insert “or her”.

310 Subsection 157(3)

After “he”, insert “or she”.

311 Subsection 157(4)

Omit “him as if he”, substitute “the taxpayer as if he or she”.

312 Paragraph 159H(a)

After “him”, insert “or her”.

313 Subsections 159J(1), (1A) and (1B)

After “his”, insert “or her”.

314 Subsections 159L(1) and (3)

After “his” (wherever occurring), insert “or her”.

315 Paragraph 159L(4)(a)

Omit “he”, substitute “the taxpayer”.

316 Paragraph 159L(4)(a)

After “his”, insert “or her”.

317 Section 159M

After “his”, insert “or her”.

318 Subsection 159P(4) (paragraph (h) of the definition of medical expenses)

After “him”, insert “or her”.

319 Subsections 160AAB(2), (3) and (6)