Tax Laws Amendment (Research and Development) Act 2011

No. 93, 2011

An Act to amend the law relating to taxation and research and development, and for other purposes

Tax Laws Amendment (Research and Development) Act 2011

No. 93, 2011

An Act to amend the law relating to taxation and research and development, and for other purposes

Contents

2 Commencement

3 Schedule(s)

Schedule 1—Main components of new R&D incentive

Income Tax Assessment Act 1997

Schedule 2—Innovation Australia’s role

Part 1—Main amendment

Industry Research and Development Act 1986

Part 2—Other amendments

Industry Research and Development Act 1986

Schedule 3—Other amendments relating to new R&D incentive

Part 1—Tax offset rules

Income Tax Assessment Act 1997

Part 2—Prepayments of expenditure

Income Tax Assessment Act 1936

Part 3—Capital allowances

Income Tax Assessment Act 1997

Part 4—Capital works

Income Tax Assessment Act 1997

Part 5—Forgiveness of commercial debts

Division 1—Amending the new law

Income Tax Assessment Act 1997

Division 2—Amending the old law

Income Tax Assessment Act 1936

Part 6—Other amendments

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Taxation Administration Act 1953

Schedule 3A—Quarterly credits

Part 1—Introduction

Part 2—Power to make regulations to modify operation of Acts

Part 3—Modified Acts may provide for certain matters

Part 4—Alternative constitutional basis

Part 5—Other matters

Schedule 4—Application, savings and transitional provisions

Part 1—Application provisions

Part 2—General savings provisions

Part 3—Transitional provisions appearing as amendments of other Acts

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Part 4—Other savings and transitional provisions

Tax Laws Amendment (Research and Development) Act 2011

No. 93, 2011

An Act to amend the law relating to taxation and research and development, and for other purposes

[Assented to 8 September 2011]

The Parliament of Australia enacts:

This Act may be cited as the Tax Laws Amendment (Research and Development) Act 2011.

(1) Each provision of this Act specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information | ||

Column 1 | Column 2 | Column 3 |

Provision(s) | Commencement | Date/Details |

1. Sections 1 to 3 and anything in this Act not elsewhere covered by this table | The day this Act receives the Royal Assent. | 8 September 2011 |

2. Schedules 1 and 2 | The day this Act receives the Royal Assent. | 8 September 2011 |

3. Schedule 3, Parts 1 to 4 | The day this Act receives the Royal Assent. | 8 September 2011 |

4. Schedule 3, Part 5, Division 1 | The later of: (a) the start of the day this Act receives the Royal Assent; and (b) immediately after the commencement of Schedule 2 to the Tax Laws Amendment (Transfer of Provisions) Act 2010. However, the provision(s) do not commence at all if the event mentioned in paragraph (b) does not occur. | 8 September 2011 |

5. Schedule 3, Part 5, Division 2 | The day this Act receives the Royal Assent. However, if Schedule 2 to the Tax Laws Amendment (Transfer of Provisions) Act 2010 commences on or before that day, the provision(s) do not commence at all. | Does not commence |

6. Schedule 3, Part 6 | The day this Act receives the Royal Assent. | 8 September 2011 |

7. Schedules 3A and 4 | The day this Act receives the Royal Assent. | 8 September 2011 |

Note: This table relates only to the provisions of this Act as originally enacted. It will not be amended to deal with any later amendments of this Act.

(2) Any information in Column 3 of the table is not part of this Act. Information may be inserted in this column, or information in it may be edited, in any published version of this Act.

Each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

Schedule 1—Main components of new R&D incentive

Income Tax Assessment Act 1997

1 After Division 345

Insert:

Division 355—Research and Development

Table of Subdivisions

Guide to Division 355

355‑A Object

355‑B Meaning of R&D activities and other terms

355‑C Entitlement to tax offset

355‑D Notional deductions for R&D expenditure

355‑E Notional deductions for decline in value of depreciating assets used for R&D activities

355‑F Integrity Rules

355‑G Clawback of R&D recoupments

355‑H Feedstock adjustments

355‑I Application to earlier income year R&D expenditure incurred to associates

355‑J Application to R&D partnerships

355‑K Application to Cooperative Research Centres

355‑W Other matters

355‑1 What this Division is about

An R&D entity may be entitled to a tax offset for R&D activities. The tax offset may be a refundable tax offset if the R&D entity’s aggregated turnover is less than $20 million.

To be entitled to the tax offset, the R&D entity needs one or more notional deductions under this Division.

There are 2 main kinds of notional deductions. One is for expenditure on R&D activities. The other is for the decline in value of tangible depreciating assets used for R&D activities.

Note: All of these notional deductions require the R&D entity to be registered for the R&D activities under Part III of the Industry Research and Development Act 1986.

Table of sections

355‑5 Object

(1) The object of this Division is to encourage industry to conduct research and development activities that might otherwise not be conducted because of an uncertain return from the activities, in cases where the knowledge gained is likely to benefit the wider Australian economy.

(2) This object is to be achieved by providing a tax incentive for industry to conduct, in a scientific way, experimental activities for the purpose of generating new knowledge or information in either a general or applied form (including new knowledge in the form of new or improved materials, products, devices, processes or services).

Subdivision 355‑B—Meaning of R&D activities and other terms

Table of sections

355‑20 R&D activities

355‑25 Core R&D activities

355‑30 Supporting R&D activities

355‑35 R&D entities

R&D activities are *core R&D activities or *supporting R&D activities.

(1) Core R&D activities are experimental activities:

(a) whose outcome cannot be known or determined in advance on the basis of current knowledge, information or experience, but can only be determined by applying a systematic progression of work that:

(i) is based on principles of established science; and

(ii) proceeds from hypothesis to experiment, observation and evaluation, and leads to logical conclusions; and

(b) that are conducted for the purpose of generating new knowledge (including new knowledge in the form of new or improved materials, products, devices, processes or services).

(2) However, none of the following activities are core R&D activities:

(a) market research, market testing or market development, or sales promotion (including consumer surveys);

(b) prospecting, exploring or drilling for minerals or *petroleum for the purposes of one or more of the following:

(i) discovering deposits;

(ii) determining more precisely the location of deposits;

(iii) determining the size or quality of deposits;

(c) management studies or efficiency surveys;

(d) research in social sciences, arts or humanities;

(e) commercial, legal and administrative aspects of patenting, licensing or other activities;

(f) activities associated with complying with statutory requirements or standards, including one or more of the following:

(i) maintaining national standards;

(ii) calibrating secondary standards;

(iii) routine testing and analysis of materials, components, products, processes, soils, atmospheres and other things;

(g) any activity related to the reproduction of a commercial product or process:

(i) by a physical examination of an existing system; or

(ii) from plans, blueprints, detailed specifications or publically available information;

(h) developing, modifying or customising computer software for the dominant purpose of use by any of the following entities for their internal administration (including the internal administration of their business functions):

(i) the entity (the developer) for which the software is developed, modified or customised;

(ii) an entity *connected with the developer;

(iii) an *affiliate of the developer, or an entity of which the developer is an affiliate.

355‑30 Supporting R&D activities

(1) Supporting R&D activities are activities directly related to *core R&D activities.

(2) However, if an activity:

(a) is an activity referred to in subsection 355‑25(2); or

(b) produces goods or services; or

(c) is directly related to producing goods or services;

the activity is a supporting R&D activity only if it is undertaken for the dominant purpose of supporting *core R&D activities.

(1) Each of the following is an R&D entity:

(a) a body corporate incorporated under an *Australian law;

(b) a body corporate incorporated under a *foreign law that is an Australian resident.

Note: Each of the above paragraphs extends to a body corporate acting in its capacity as trustee of a public trading trust (see subsection 102T(9) of the Income Tax Assessment Act 1936).

(2) A body corporate incorporated under a *foreign law that:

(a) is a resident of a foreign country for the purposes of an agreement in force between that country and Australia that:

(i) is a double tax agreement (as defined in Part X of the Income Tax Assessment Act 1936); and

(ii) includes a definition of permanent establishment; and

(b) carries on business in Australia through a permanent establishment (within the meaning of that definition) of the body corporate in Australia;

is an R&D entity to the extent that it carries on business through that permanent establishment.

(3) However, an *exempt entity cannot be an R&D entity.

Subdivision 355‑C—Entitlement to tax offset

Table of sections

355‑100 Entitlement to tax offset

355‑105 Deductions under this Division are notional only

355‑110 Notional deductions include prepaid expenditure

355‑100 Entitlement to tax offset

If notional deductions are at least $20,000

(1) An *R&D entity is entitled to a *tax offset for an income year equal to the percentage, set out in the table, of the total of the amounts (if any) that the entity can deduct for the income year under any or all of the following provisions:

(a) section 355‑205 (R&D expenditure);

(b) section 355‑305 (decline in value of R&D assets);

(c) section 355‑315 (balancing adjustment for R&D assets);

(d) section 355‑480 (earlier year associate R&D expenditure);

(e) section 355‑520 (decline in value of R&D partnership assets);

(f) section 355‑525 (balancing adjustment for R&D partnership assets);

(g) section 355‑580 (CRC contributions).

Rate of R&D tax offset | ||

Item | In this case: | The percentage is: |

1 | the *R&D entity’s *aggregated turnover for the income year is less than $20 million (and item 2 of this table does not apply) | 45% |

2 | an *exempt entity, or combination of exempt entities, would control the *R&D entity in a way described in section 328‑125 (connected entities) if: (a) references in section 328‑125 to 40% were references to 50%; and (b) subsection 328‑125(6) were ignored | 40% |

3 | any other case | 40% |

Note: The tax offset will be a refundable tax offset if the percentage applicable to the entity is 45% (see section 67‑30).

If notional deductions are less than $20,000

(2) However, if the total of those amounts is less than $20,000, the *R&D entity is instead entitled to a *tax offset for the income year equal to that percentage of the total of the following kinds of expenditure (if any):

Expenditure not subject to $20,000 threshold | |

Item | Kind of expenditure |

1 | Expenditure: (a) that the *R&D entity can deduct under section 355‑205 (R&D expenditure) for the income year; and (b) that was incurred to a research service provider (within the meaning of the Industry Research and Development Act 1986) that is not an *associate of the R&D entity or of the relevant *R&D partnership (as appropriate); and (c) that was for the provider to provide services, within a research field for which the provider is registered under Division 4 of Part III of that Act, applicable to one or more of the *R&D activities to which the deduction relates |

2 | Expenditure that the *R&D entity can deduct under section 355‑580 (CRC contributions) for the income year |

355‑105 Deductions under this Division are notional only

An amount (the notional amount) that an *R&D entity can deduct under this Division is disregarded except for the purposes of:

(a) working out whether the R&D entity is entitled under section 355‑100 to a *tax offset; and

(b) a provision (of this Act or any other Act) that refers to an entitlement of the R&D entity under section 355‑100 to a tax offset; and

(c) a provision (of this Act or any other Act) that:

(i) prevents some or all of the notional amount from being deducted; or

(ii) changes the income year for which some or all of the notional amount can be deducted; and

Note: Examples are Divisions 26 and 27 of this Act, Subdivision H of Division 3 of Part III of the Income Tax Assessment Act 1936 and Part IVA of that Act.

(d) a provision (of this Act or any other Act) that includes an amount in assessable income wholly or partly because of the notional amount; and

Note: An example is Subdivision 20‑A, which may include in assessable income a recoupment of a loss or outgoing if the entity can deduct an amount for the loss or outgoing.

(e) a provision (of this Act or any other Act) that excludes expenditure from:

(i) the *cost base or *reduced cost base of a *CGT asset; or

(ii) an element of that cost base or reduced cost base.

Note: An example is section 110‑45, which may exclude deductible expenditure from elements of the cost base of an asset.

355‑110 Notional deductions include prepaid expenditure

For the purposes of this Division, if:

(a) apart from Subdivision H (prepaid expenditure) of Division 3 of Part III of the Income Tax Assessment Act 1936, an *R&D entity can deduct an amount under section 355‑205 or 355‑480 for an income year (the present year) or an earlier income year; and

(b) that Subdivision applies to the calculation of that amount; and

(c) the entity can deduct an amount, as a result of that application of that Subdivision, for the present year;

the entity is taken to be able to deduct under section 355‑205 or 355‑480 (as appropriate) the amount referred to in paragraph (c) for the present year.

Note: Section 355‑205 is about deductions for R&D expenditure. Section 355‑480 is about deductions for earlier year associate R&D expenditure.

Subdivision 355‑D—Notional deductions for R&D expenditure

Table of sections

355‑200 What this Subdivision is about

355‑205 When notional deductions for R&D expenditure arise

355‑210 Conditions for R&D activities

355‑215 R&D activities conducted by a permanent establishment for other parts of the body corporate

355‑220 R&D activities conducted for a foreign entity

355‑225 Expenditure that cannot be notionally deducted

355‑200 What this Subdivision is about

An R&D entity can notionally deduct its expenditure on registered R&D activities for which certain conditions are met.

There are special conditions for R&D activities conducted for foreign residents.

355‑205 When notional deductions for R&D expenditure arise

(1) An *R&D entity can deduct for an income year (the present year) expenditure it incurs during that year to the extent that the expenditure:

(a) is incurred on one or more *R&D activities:

(i) for which the R&D entity is registered under section 27A of the Industry Research and Development Act 1986 for an income year; and

(ii) that are activities to which section 355‑210 (conditions for R&D activities) applies; and

(b) if the expenditure is incurred to the R&D entity’s *associate—is paid to that associate during the present year.

Note 1: If the matters in subparagraphs (a)(i) and (ii) are not satisfied until a later income year, the R&D entity will need to wait until then before it can deduct the expenditure for the present year.

Note 2: The R&D activities will need to be conducted during the income year the R&D entity is registered for those activities (see sections 27A and 27J of the Industry Research and Development Act 1986).

Note 3: The entity may also be able to deduct expenditure incurred to an associate in an earlier income year (see section 355‑480).

Note 4: Expenditure incurred in income years starting on or after 1 July 2011 may be deductible for activities registered for income years starting before 1 July 2011 (see section 355‑200 of the Income Tax (Transitional Provisions) Act 1997).

(2) This section has effect subject to section 355‑225 (excluded expenditure), Subdivision 355‑F (integrity rules) and subsection 355‑580(3) (CRC contributions).

355‑210 Conditions for R&D activities

(1) An *R&D activity covered by one or more of the following paragraphs is an activity to which this section applies:

(a) the R&D activity is conducted for the *R&D entity solely within Australia or an external Territory;

(b) if the R&D entity is a body corporate carrying on business through a permanent establishment (as described in subsection 355‑35(2))—the R&D activity is conducted:

(i) for the body corporate; but

(ii) not for the purposes of that permanent establishment;

and the conditions in section 355‑215 (activities conducted for a body corporate by its permanent establishment) are met for the R&D activity;

(c) the R&D activity is conducted for one or more foreign residents who are each:

(i) incorporated under a *foreign law; and

(ii) a resident of a foreign country for the purposes of an agreement of a kind described in subsection 355‑35(2);

and the conditions in section 355‑220 (activities conducted for a foreign entity) are met for the R&D activity;

(d) the R&D activity is:

(i) conducted for the R&D entity solely outside Australia and the external Territories; and

(ii) covered by a finding in force under paragraph 28C(1)(a) of the Industry Research and Development Act 1986;

(e) the R&D activity consists of several parts, with:

(i) some parts being conducted for the R&D entity solely within Australia or an external Territory; and

(ii) the other parts being conducted for the R&D entity outside Australia and the external Territories while covered by a finding in force under paragraph 28C(1)(a) of the Industry Research and Development Act 1986.

Note: An activity can be covered by a finding under paragraph 28C(1)(a) of the Industry Research and Development Act 1986 if the activity cannot be conducted in Australia or the external Territories.

(2) However, an *R&D activity is not an activity to which this section applies if the activity is conducted, to a significant extent, for one or more other entities not covered by any paragraph of subsection (1).

Note: An entity would not be covered by, for example, paragraph (1)(c) if the conditions in section 355‑220 were not met for the R&D activity in relation to that entity.

355‑215 R&D activities conducted by a permanent establishment for other parts of the body corporate

For the purposes of paragraph 355‑210(1)(b), the conditions for an *R&D activity are as follows:

(a) the R&D activity is conducted solely within Australia or an external Territory;

(b) if the R&D activity is a *supporting R&D activity, each corresponding *core R&D activity must be:

(i) an activity conducted, or to be conducted, solely within Australia or an external Territory; and

(ii) an activity for which the *R&D entity is or has been registered under section 27A of the Industry Research and Development Act 1986, or could be registered for an income year if that core R&D activity were conducted during the income year;

(c) there is written evidence that the R&D activity is conducted for the body corporate but not for the purposes of that permanent establishment.

Note: The body corporate is the R&D entity to the extent that it carries on business through that permanent establishment (see subsection 355‑35(2)).

355‑220 R&D activities conducted for a foreign entity

(1) For the purposes of paragraph 355‑210(1)(c), the conditions for an *R&D activity conducted for one or more foreign residents are as follows:

(a) the R&D activity is conducted solely within Australia or an external Territory;

(b) if the R&D activity is a *supporting R&D activity, each corresponding *core R&D activity must be:

(i) an activity conducted, or to be conducted, solely within Australia or an external Territory; and

(ii) an activity for which the *R&D entity is or has been registered under section 27A of the Industry Research and Development Act 1986, or could be registered for an income year if that core R&D activity were conducted during the income year;

(c) when the R&D activity is conducted:

(i) each foreign resident is *connected with the R&D entity; or

(ii) for each foreign resident—either the foreign resident is an *affiliate of the R&D entity or the R&D entity is an affiliate of the foreign resident;

(d) the R&D activity is conducted:

(i) in accordance with a written agreement binding on only the R&D entity and each foreign resident; and

(ii) either directly by the R&D entity, or indirectly by another entity under an agreement binding on the R&D entity;

(e) the R&D activity is not conducted in connection with an agreement covered by subsection (2).

Note: An example of conducting an R&D activity indirectly under a contract is conducting the R&D activity under a subcontract, or one of a chain of subcontracts, under the contract.

(2) An agreement is covered by this subsection if:

(a) the agreement is binding on the R&D entity (the first entity) and an R&D entity that:

(i) is *connected with the first entity; or

(ii) has the first entity as an *affiliate, or is an affiliate of the first entity;

while the *R&D activity is conducted; and

(b) the R&D activity is to be conducted under the agreement by the first entity or by an entity:

(i) who is not bound by the agreement; and

(ii) who is to conduct the R&D activity directly or indirectly under another agreement to which the first entity is, or will become, bound.

Note: One effect of this subsection is that, even if the R&D entity has an agreement with the foreign resident for conducting the R&D activity, the R&D entity cannot deduct expenditure incurred:

(a) for conducting the R&D activity as a subcontractor under a subcontract with an affiliated R&D entity; or

(b) if the R&D entity is a subcontractor to an affiliated R&D entity—for further subcontracting the conducting of the R&D activity.

355‑225 Expenditure that cannot be notionally deducted

Expenditure on buildings, certain assets and interest

(1) Sections 355‑205 (deductions for R&D expenditure) and 355‑480 (deductions for earlier year associate R&D expenditure) do not apply to the following expenditure:

(a) expenditure incurred to acquire or construct:

(i) a building or a part of a building; or

(ii) an extension, alteration or improvement to a building;

(b) expenditure included in the *cost of a tangible *depreciating asset for the purposes of Division 40 (as that Division applies as described in section 355‑310 or otherwise);

(c) expenditure incurred for interest (within the meaning of Division 11A of Part III of the Income Tax Assessment Act 1936) payable to an entity.

Note 1: Expenditure covered by paragraph (a) may be deductible under Division 43 (capital works).

Note 2: The decline in value of an asset covered by paragraph (b) may be notionally deductible under section 355‑305.

Note 3: Expenditure covered by paragraph (c) may be deductible under section 8‑1.

Expenditure on core technology

(2) Sections 355‑205 (deductions for R&D expenditure) and 355‑480 (deductions for earlier year associate R&D expenditure) do not apply to expenditure incurred in acquiring, or in acquiring the right to use, technology wholly or partly for the purposes of one or more *R&D activities if:

(a) a purpose of the R&D activities was or is:

(i) to obtain new knowledge based on that technology; or

(ii) to create new or improved materials, products, devices, processes, techniques or services to be based on that technology; or

(b) the R&D activities were or are an extension, continuation, development or completion of the activities that produced that technology.

Table of sections

355‑300 What this Subdivision is about

355‑305 When notional deductions for decline in value arise

355‑310 Notional application of Division 40

355‑315 Balancing adjustments—assets only used for R&D activities

355‑300 What this Subdivision is about

An R&D entity can notionally deduct the decline in value of a tangible depreciating asset used for R&D activities.

If a balancing adjustment event later happens for the asset, the R&D entity may be able to notionally deduct a further amount. Alternatively, an amount may be included in the R&D entity’s assessable income.

355‑305 When notional deductions for decline in value arise

(1) If:

(a) an *R&D entity is registered under section 27A of the Industry Research and Development Act 1986 for an income year (the present year) for one or more *R&D activities that are activities to which section 355‑210 (conditions for R&D activities) applies; and

(b) while a tangible *depreciating asset is *held by the R&D entity during the present year, the asset is used for the purpose of conducting one or more of those R&D activities; and

(c) the R&D entity could deduct an amount under section 40‑25 for the asset for the present year if Division 40 applied with the changes described in section 355‑310; and

(d) the R&D entity cannot deduct an amount for the asset for:

(i) an earlier income year under Subdivision 328‑D (capital allowances for small business entities); or

(ii) an earlier income year under Division 40 (as that Division applies apart from this Division), in a case where section 40‑440 (low‑value pools) applied;

the R&D entity can deduct the amount referred to in paragraph (c) for the present year.

(2) This section has effect subject to subsection 355‑580(4) (CRC contributions).

355‑310 Notional application of Division 40

(1) In addition to its application apart from this section, Division 40 also applies with the changes set out in this section for the purposes of:

(a) paragraph 355‑225(1)(b) (excluded expenditure); and

(b) paragraph 355‑305(1)(c); and

(c) section 355‑315 (balancing adjustments).

(2) Firstly, substitute the following for references to a *taxable purpose in Subdivisions 40‑A to 40‑D (other than for the purposes of sections 40‑100, 40‑105 and 40‑110):

Replacing references to a taxable purpose | ||

Item | If this application of Division 40 is for the purposes of: | Substitute a reference to: |

1 | paragraph 355‑225(1)(b) or 355‑305(1)(c) | the purpose of conducting one or more of the *R&D activities covered by paragraph 355‑305(1)(b) |

2 | section 355‑315 | the purpose of conducting one or more of the *R&D activities to which the R&D deductions (within the meaning of that section) relate |

Note: Sections 40‑100, 40‑105 and 40‑110 are about working out an asset’s effective life. Those sections already refer to the use of the asset for R&D activities.

(3) Secondly, assume that Division 40 does not apply to a building, nor to an extension, alteration or improvement to a building, (the building works) for which the *R&D entity:

(a) can deduct amounts under Division 43 (capital works); or

(b) could deduct amounts under Division 43:

(i) apart from expenditure being incurred, or the building works being started, before a particular day; or

(ii) had the R&D entity used the building works for a purpose relevant to those building works under section 43‑140 (using an area in a deductible way).

(4) Finally, assume that the following provisions had not been enacted:

(a) subsection 40‑25(7) (meaning of taxable purpose);

(b) subsection 40‑45(2) (assets to which Division 40 does not apply);

(c) section 40‑425 (low‑value pools);

(d) Subdivision 328‑D (capital allowances for small business entities).

Note: Subsection (3) and paragraph (4)(b) mean that deductions under section 355‑305 may be available for capital works other than building works.

355‑315 Balancing adjustments—assets only used for R&D activities

(1) This section applies to an *R&D entity if:

(a) a *balancing adjustment event happens in an income year (the event year) for an asset *held by the R&D entity; and

(b) the R&D entity cannot deduct an amount under section 40‑25, as that section applies apart from:

(i) this Division; and

(ii) former section 73BC of the Income Tax Assessment Act 1936;

for the asset for an income year; and

(c) the R&D entity is entitled under section 355‑100 to *tax offsets for one or more income years for deductions (the R&D deductions) under section 355‑305 for the asset; and

(d) the entity is registered under section 27A of the Industry Research and Development Act 1986 for one or more *R&D activities for the event year; and

(e) if Division 40 applied with the changes described in section 355‑310:

(i) the entity could deduct for the event year an amount under subsection 40‑285(2) for the asset and the balancing adjustment event; or

(ii) an amount would be included in the entity’s assessable income for the event year under subsection 40‑285(1) for the asset and the balancing adjustment event.

Note 1: This section applies in a modified way if the entity also has deductions for the asset under former section 73BA or 73BH of the Income Tax Assessment Act 1936 (see section 355‑320 of the Income Tax (Transitional Provisions) Act 1997).

Note 2: Section 40‑292 applies if the entity can deduct an amount under section 40‑25, as that section applies apart from this Division and former section 73BC of the Income Tax Assessment Act 1936.

Notional deduction

(2) If the *R&D entity could deduct for the event year an amount under subsection 40‑285(2) for the asset and the event if Division 40 applied as described in paragraph (1)(e), the R&D entity can deduct that amount for the event year.

Amount to be included in assessable income

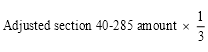

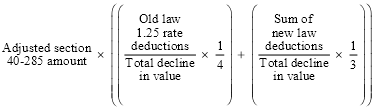

(3) If an amount (the section 40‑285 amount) would be included in the *R&D entity’s assessable income for the event year under subsection 40‑285(1) for the asset and the event if Division 40 applied as described in paragraph (1)(e), the sum of that amount and the following amount is included in the R&D entity’s assessable income for the event year:

where:

adjusted section 40‑285 amount means so much of the section 40‑285 amount as does not exceed the total decline in value.

total decline in value means the asset’s *cost, less its *adjustable value, worked out under Division 40 as it applies as described in paragraph (1)(e).

Subdivision 355‑F—Integrity Rules

Table of sections

355‑400 Expenditure incurred while not at arm’s length

355‑405 Expenditure not at risk

355‑410 Disposal of R&D results

355‑415 Reducing deductions to reflect mark‑ups within groups

355‑400 Expenditure incurred while not at arm’s length

If:

(a) an *R&D entity incurs expenditure to another entity on all or part of an *R&D activity; and

(b) either:

(i) when the R&D entity incurs the expenditure, the R&D entity and the other entity do not deal with each other at *arm’s length; or

(ii) the other entity is the R&D entity’s *associate; and

(c) the expenditure exceeds the *market value of the relevant R&D activity or part (as appropriate);

for the purposes of this Division, the R&D entity is treated as if the amount of expenditure it incurred on the relevant R&D activity or part (as appropriate) were equal to that market value.

Note 1: For the purposes of a deduction under section 355‑305 or 355‑520 for an asset’s decline in value, the arms’ length rules in Division 40 apply as part of the notional application of that Division under that section.

Note 2: In the application of Division 13 of Part III of the Income Tax Assessment Act 1936 (about international transfer‑pricing arrangements), this section is disregarded (see subsection 136AB(2) of that Act).

355‑405 Expenditure not at risk

(1) An *R&D entity cannot deduct expenditure under section 355‑205 or 355‑480 if:

(a) when it incurs the expenditure, the R&D entity or its *associate had received, or could reasonably be expected to receive, consideration:

(i) as a direct or indirect result of the expenditure being incurred; and

(ii) regardless of the results of the activities on which the expenditure is incurred; and

(b) that consideration is equal to or greater than the expenditure.

Note: Section 355‑205 is about deductions for R&D expenditure. Section 355‑480 is about deductions for earlier year associate R&D expenditure.

(2) If:

(a) when an *R&D entity incurs expenditure, the R&D entity or its *associate had received, or could reasonably be expected to receive, consideration:

(i) as a direct or indirect result of the expenditure being incurred; and

(ii) regardless of the results of the activities on which the expenditure is incurred; and

(b) that consideration is less than the expenditure;

the R&D entity cannot deduct under section 355‑205 or 355‑480 so much of the expenditure as is equal to the consideration.

(3) For the purposes of paragraphs (1)(a) and (2)(a), have regard to:

(a) anything that happened or existed before or at the time the expenditure is incurred; and

(b) anything that is likely to happen or exist after that time.

(4) This section does not apply to expenditure incurred on *R&D activities covered by paragraph 355‑210(1)(b) or (c).

Note: Those paragraphs cover R&D activities conducted for foreign residents.

355‑410 Disposal of R&D results

(1) This section applies to an *R&D entity if:

(a) the R&D entity is entitled under section 355‑100 to a *tax offset because it can:

(i) deduct under section 355‑205 or 355‑480 expenditure incurred on *R&D activities; or

(ii) deduct under section 355‑305 or 355‑520 an amount for an asset (the R&D asset) used for the purpose of conducting one or more R&D activities; and

(b) the R&D entity receives or becomes entitled to receive one or more of the following amounts (the results amounts) in an income year (the results year):

(i) an amount for the results of any of the R&D activities;

(ii) an amount from granting access to, or the right to use, any of those results;

(iii) an amount attributable to the R&D entity having incurred the expenditure, including an amount it is entitled to receive regardless of the results of the R&D activities;

(iv) an amount attributable to the R&D asset being used for the purpose mentioned in subparagraph (a)(ii), including an amount the R&D entity is entitled to receive regardless of the results of the R&D activities;

(v) an amount from *disposing of a *CGT asset, or from granting a right to occupy or use a CGT asset, where the disposal or grant resulted in another person acquiring a right to access or use any of those results.

Note: This section also applies with changes to the partners of an R&D partnership (see section 355‑535).

(2) For each results amount, the following amount is included in the *R&D entity’s assessable income for the results year:

(a) if the results amount is only a results amount because of subparagraph (1)(b)(v), and the asset referred to in that subparagraph is a *depreciating asset—an amount equal to the extent (if any) that the results amount exceeds the asset’s *cost just before the disposal or grant;

(b) if the results amount is only a results amount because of subparagraph (1)(b)(v), and the asset referred to in that subparagraph is not a depreciating asset—an amount equal to the extent (if any) that the results amount exceeds the asset’s *cost base just before the disposal or grant;

(c) otherwise—the results amount.

(3) For the purposes of paragraph (2)(a), assume that subsection 40‑45(2) did not, except in the case of buildings and extensions, alterations and improvements to buildings, prevent Division 40 from applying to certain capital works.

355‑415 Reducing deductions to reflect mark‑ups within groups

(1) This section applies to an *R&D entity if:

(a) the R&D entity can deduct an amount under section 355‑205 or 355‑480 for an income year for one or more *R&D activities; and

(b) one or more other entities (the grouped entities) incurred expenditure during the income year, or an earlier income year, on one or more of those *R&D activities; and

(c) when each grouped entity incurred the expenditure:

(i) the grouped entity was *connected with the R&D entity; or

(ii) the grouped entity was an *affiliate of the R&D entity or the R&D entity was an affiliate of the grouped entity.

Note: Section 355‑205 is about deductions for R&D expenditure. Section 355‑480 is about deductions for earlier year associate R&D expenditure.

Reducing deductions by group mark‑ups

(2) The amount the *R&D entity can deduct, apart from this section, under section 355‑205 or 355‑480 for the income year is reduced by the amount (the reduction amount) worked out as follows:

Method statement

Step 1. For each grouped entity, work out the sum of the amounts derived during the income year, or an earlier income year, by the grouped entity for goods or services relating to one or more of the *R&D activities while:

(a) the grouped entity was *connected with the *R&D entity; or

(b) the grouped entity was an *affiliate of the R&D entity or the R&D entity was an affiliate of the grouped entity.

Step 2. From the sum of those amounts, subtract the actual cost to each grouped entity of providing the goods or services that correspond to those amounts.

If R&D entity has deductions for both R&D expenditure and earlier year associate R&D expenditure

(3) However, if the *R&D entity can deduct amounts under both sections 355‑205 and 355‑480 for the income year, those amounts are reduced as follows:

(a) apply the reduction amount to reduce the amount otherwise deductible under section 355‑205 (but not below zero); and

(b) then apply any remainder of the reduction amount to reduce the amount otherwise deductible under section 355‑480 (but not below zero).

Disregard mark‑ups already taken into account

(4) For the purposes of step 1 of the method statement in subsection (2), disregard any of the amounts from that step that have already been taken into account under this section for the *R&D entity and the *R&D activities for an earlier income year.

Subdivision 355‑G—Clawback of R&D recoupments

Table of sections

355‑430 What this Subdivision is about

355‑435 When extra income tax is payable

355‑440 Entity receives government recoupment

355‑445 Recoupment could relate to R&D activities

355‑450 Amount on which extra income tax is payable

355‑430 What this Subdivision is about

An entity must pay extra income tax on its recoupments from government of expenditure on R&D activities for which it has obtained tax offsets under this Division.

355‑435 When extra income tax is payable

An entity must pay extra income tax on a *recoupment if the conditions in sections 355‑440 and 355‑445 are met for the recoupment.

Note 1: Section 355‑450 sets out how much of the recoupment is subject to extra income tax.

Note 2: A recoupment includes a grant (see subsection 20‑25(1)).

355‑440 Entity receives government recoupment

The condition in this section is met if the entity receives or becomes entitled to receive the *recoupment from:

(a) an *Australian government agency; or

(b) an STB (within the meaning of Division 1AB of Part III of the Income Tax Assessment Act 1936);

otherwise than under the *CRC program.

355‑445 Recoupment could relate to R&D activities

The condition in this section is met if:

(a) the *recoupment is received, or the entitlement to receive the recoupment arises, during an income year (the trigger year); and

(b) either:

(i) the recoupment is of expenditure incurred on or in relation to certain activities; or

(ii) the recoupment requires expenditure (the project expenditure) to have been incurred, or to be incurred, on certain activities.

Note: Paragraph (b) includes expenditure incurred in purchasing a tangible depreciating asset to be used when conducting R&D activities.

355‑450 Amount on which extra income tax is payable

Amount on which extra income tax is payable

(1) The extra income tax is payable for the trigger year on an amount (the R&D expenditure) equal to the sum of:

(a) so much of the expenditure referred to in section 355‑445 that is deducted under this Division; and

(b) for each asset (if any) for which expenditure referred to in section 355‑445 is included in the asset’s *cost—each amount (if any) equal to the asset’s decline in value that is deducted under this Division;

in working out *tax offsets under section 355‑100 obtained by the entity (the recipient), or an entity mentioned in subsection (4), for one or more income years.

Note 1: Section 12B or 31 of the Income Tax Rates Act 1986 sets the rate at which the entity must pay extra income tax on this amount.

Note 2: Paragraphs (a) and (b) of this subsection refer to amounts notionally deducted under this Division (see section 355‑105).

Amount is reduced by any repayments of the recoupment

(2) For the purposes of subsection (1), reduce the expenditure referred to in subparagraph 355‑445(b)(i) by any repayments of the *recoupment during an income year.

Cap on extra income tax if recoupment relates to a project

(3) Despite subsection (1), if the *recoupment is covered by subparagraph 355‑445(b)(ii), the amount of extra income tax payable for the trigger year on the recoupment cannot exceed the following amount:

where:

net amount of the recoupment means the total amount of the *recoupment, less any repayments of the recoupment during an income year.

Related entities

(4) The other entities for the purposes of subsection (1) are as follows:

(a) an entity *connected with the recipient;

(b) an *affiliate of the recipient or an entity of which the recipient is an affiliate.

Subdivision 355‑H—Feedstock adjustments

Table of sections

355‑460 What this Subdivision is about

355‑465 Feedstock adjustment to assessable income

355‑470 Feedstock revenue

355‑475 Application to connected entities and affiliates

355‑460 What this Subdivision is about

An amount is included in an R&D entity’s assessable income if it can deduct under this Division expenditure on goods, materials or energy used during R&D activities to produce:

(a) marketable products; or

(b) products applied to the R&D entity’s own use.

355‑465 Feedstock adjustment to assessable income

(1) This section applies to an *R&D entity for an income year (the present year) if:

(a) it incurs expenditure in one or more income years in acquiring or producing goods, or materials, (the feedstock inputs) transformed or processed during *R&D activities in producing one or more tangible products (the feedstock outputs); and

(b) it obtains under section 355‑100 *tax offsets for one or more income years for deductions under this Division:

(i) for the expenditure; or

(ii) for expenditure it incurs on any energy input directly into the transformation or processing; or

(iii) for the decline in value of assets used in acquiring or producing the feedstock inputs; and

(c) during the present year, a feedstock output, or a transformed feedstock output, (the marketable product) is:

(i) *supplied by the R&D entity to another entity; or

(ii) applied by the R&D entity to the R&D entity’s own use, other than use for the purpose of transforming that product for supply.

(2) The *R&D entity’s assessable income for the present year includes an amount equal to 1/3 of the lesser of:

(a) the *feedstock revenue for the feedstock output; and

(b) so much of the total of the amounts deducted as described in paragraph (1)(b) that is reasonably attributable to the production of the feedstock output.

Note: This subsection applies separately for each of the feedstock outputs.

(3) Subsection (2) does not apply to the feedstock output if:

(a) it becomes, or is transformed into, a feedstock input; or

(b) that subsection already applies to the feedstock output because of the application of paragraph (1)(c) to:

(i) an earlier time during the present year; or

(ii) an earlier income year.

The feedstock revenue, for the feedstock output, is worked out as follows:

where:

market value of the marketable product means the marketable product’s *market value at the time it is:

(a) *supplied by the *R&D entity to the other entity; or

(b) first applied by the R&D entity to the R&D entity’s own use, other than use for the purpose of transforming that product for supply.

355‑475 Application to connected entities and affiliates

This Subdivision applies to a *supply or use of the marketable product by:

(a) an entity *connected with the *R&D entity; or

(b) an *affiliate of the R&D entity or an entity of which the R&D entity is an affiliate;

as if it were by the R&D entity.

Subdivision 355‑I—Application to earlier income year R&D expenditure incurred to associates

Table of sections

355‑480 Notional deductions for expenditure incurred to associate in earlier income years

355‑480 Notional deductions for expenditure incurred to associate in earlier income years

Notional deductions for earlier year associate expenditure

(1) An *R&D entity can deduct for an income year (the present year) expenditure it incurred to its *associate during an earlier income year to the extent that:

(a) the expenditure was incurred on one or more *R&D activities:

(i) for which the R&D entity is registered under section 27A of the Industry Research and Development Act 1986 for an income year; and

(ii) that are activities to which section 355‑210 (conditions for R&D activities) applies; and

(b) the expenditure is paid to that associate during the present year; and

(c) subsection (2) applies to the expenditure.

Note 1: This section applies in a modified way to R&D partnership expenditure (see sections 355‑510 and 355‑515).

Note 2: Expenditure paid in income years starting on or after 1 July 2011 may be deductible for activities registered for income years starting before 1 July 2011 (see section 355‑200 of the Income Tax (Transitional Provisions) Act 1997).

Expenditure cannot have been otherwise deducted etc.

(2) This subsection applies to the expenditure if:

(a) the *R&D entity can deduct the expenditure, or is entitled to a *tax offset for the expenditure, under any other Division of this Act for an earlier income year; and

(b) by the time of lodging its *income tax return for the most recent income year before the present year, the R&D entity had neither:

(i) deducted the expenditure; nor

(ii) obtained a tax offset for the expenditure;

as described in paragraph (a).

(3) The entitlement to the deduction, or *tax offset, described in paragraph (2)(a) ceases to the extent that subsection (2) applies to the expenditure.

Example: If, by the time mentioned in paragraph (2)(b), an R&D entity chose to deduct only a third of the expenditure it could have deducted under another Division, then the remaining 2 thirds of that expenditure:

(a) can be deducted under this section; but

(b) can no longer be deducted under the other Division.

Notional deduction is subject to integrity rules etc.

(4) This section has effect subject to section 355‑225 (excluded expenditure), Subdivision 355‑F (integrity rules) and subsection 355‑580(3) (CRC contributions).

Subdivision 355‑J—Application to R&D partnerships

Table of sections

355‑500 What this Subdivision is about

355‑505 Meaning of R&D partnership and partner’s proportion

355‑510 R&D partnership expenditure on R&D activities

355‑515 R&D activities conducted by or for an R&D partnership

355‑520 When notional deductions arise for decline in value of depreciating assets of R&D partnerships

355‑525 Balancing adjustments for R&D partnership assets only used for R&D activities

355‑530 Implications for partner’s aggregated turnover

355‑535 Disposal of R&D results—assets of R&D partnerships

355‑540 Application of recoupment rules

355‑545 Relevance for net income, and losses, of the R&D partnership

355‑500 What this Subdivision is about

This Subdivision modifies the rules in this Division for partners of R&D partnerships.

In particular, the rules about deducting R&D expenditure are modified to allow a partner to deduct the partner’s proportion of the R&D partnership’s expenditure on R&D activities.

A partner of an R&D partnership may also be able to deduct under this Subdivision the decline in value of partnership assets used for R&D activities.

355‑505 Meaning of R&D partnership and partner’s proportion

(1) A partnership is an R&D partnership at a particular time if, at that time, each of the partners is an *R&D entity.

(2) For an amount attributable to an *R&D partnership for an income year, each partner of the R&D partnership is taken to bear or be entitled to (as appropriate) this proportion (the partner’s proportion) of the amount:

(a) the proportion the partners agreed the partner should bear or be entitled to (as appropriate); or

(b) if there is no such agreement—the proportion of the partner’s interest in the *net income or *partnership loss of the R&D partnership for the income year.

355‑510 R&D partnership expenditure on R&D activities

If an *R&D partnership incurs expenditure on one or more R&D activities during an income year, this Division applies in relation to each *R&D entity that is a partner of the R&D partnership at some time during the income year as if:

(a) the partner incurred the partner’s proportion of that expenditure when the R&D partnership incurred that expenditure; and

(b) neither the R&D partnership, nor any other partner of the R&D partnership, incurred expenditure during the income year on the R&D activities; and

(c) such other changes were made to this Division as are appropriate having regard to that partner’s proportion of amounts attributable to the R&D partnership.

Note: This section and section 355‑515 may result in:

(a) the partner being able to deduct the partner’s proportion of the partnership expenditure under section 355‑205 (R&D expenditure) or 355‑480 (earlier year associate R&D expenditure) for the R&D activities; and

(b) the partner being affected by the integrity rules in Subdivisions 355‑F, 355‑G and 355‑H.

355‑515 R&D activities conducted by or for an R&D partnership

If one or more *R&D activities are conducted by or for an *R&D partnership during an income year, this Division applies in relation to each *R&D entity that is a partner of the R&D partnership at some time during the income year as if:

(a) the R&D activities were conducted by or for the partner in a corresponding way to the way the R&D activities were conducted by or for the R&D partnership; and

(b) the partner had relationships with other entities in relation to the R&D activities that corresponded to the relationships the R&D partnership had with those other entities in relation to the R&D activities; and

(c) a thing done by, or in relation to, the R&D partnership in relation to the R&D activities were a thing done by, or in relation to, the partner; and

(d) the R&D activities were neither:

(i) conducted by or for the R&D partnership; nor

(ii) conducted by or for any other partner of the R&D partnership; and

(e) such other changes were made to this Division as are appropriate having regard to that partner’s proportion of amounts attributable to the R&D partnership.

Note 1: For the purposes of this Division, entities that are associates or affiliates of, or connected with, the R&D partnership are taken to be associates or affiliates of, or connected with, the partner (see paragraph (b)).

Note 2: For the purposes of this Division, payments and agreements made by the R&D partnership for the R&D activities are taken to be made by the partner (see paragraph (c)).

When notional deductions arise

(1) If:

(a) an *R&D entity is a partner of an *R&D partnership at some time during an income year (the present year); and

(b) the partner is registered under section 27A of the Industry Research and Development Act 1986 for the present year for one or more *R&D activities that are activities to which section 355‑210 (conditions for R&D activities) applies; and

Note: Section 355‑210 applies with changes for this paragraph (see section 355‑515).

(c) while a tangible *depreciating asset is *held by the R&D partnership during the present year, the asset is used for the purpose of conducting one or more of those R&D activities; and

(d) the R&D partnership could deduct an amount under section 40‑25 for the asset for the present year if Division 40 applied with the changes described in section 355‑310; and

Note: Section 355‑310 applies with changes for this paragraph (see subsection (2) of this section).

(e) the R&D partnership cannot deduct an amount for the asset for:

(i) an earlier income year under Subdivision 328‑D (capital allowances for small business entities); or

(ii) an earlier income year under Division 40 (as that Division applies apart from this Division), in a case where section 40‑440 (low‑value pools) applied;

the partner can deduct the partner’s proportion of the amount referred to in paragraph (d) for the present year.

Changed application of Division 40 for this Subdivision

(2) For the purposes of this Subdivision, section 355‑310 applies as if the following changes were made:

Changes to be made | ||

Item | For a reference in section 355‑310 to... | substitute a reference to... |

1 | paragraph 355‑305(1)(c) | paragraph 355‑520(1)(d) |

2 | section 355‑315 | section 355‑525 |

3 | paragraph 355‑305(1)(b) | paragraph 355‑520(1)(c) |

4 | *R&D entity | *R&D partnership |

Disregard certain assets held because of CRC contributions

(3) This section has effect subject to subsection 355‑580(4) (CRC contributions).

355‑525 Balancing adjustments for R&D partnership assets only used for R&D activities

(1) This section applies to an *R&D entity (the partner) if:

(a) a *balancing adjustment event happens in an income year (the event year) for an asset *held by an *R&D partnership; and

(b) the R&D partnership cannot deduct an amount under section 40‑25, as that section applies apart from:

(i) this Division; and

(ii) former section 73BC of the Income Tax Assessment Act 1936;

for the asset for an income year; and

(c) the partner is entitled under section 355‑100 to *tax offsets for one or more income years for deductions (the R&D deductions) under section 355‑520 for the asset; and

(d) the partner is registered under section 27A of the Industry Research and Development Act 1986 for one or more *R&D activities for the event year; and

(e) if Division 40 applied with the changes described in section 355‑310 (as affected by subsection 355‑520(2)):

(i) the R&D partnership could deduct for the event year an amount under subsection 40‑285(2) for the asset and the balancing adjustment event; or

(ii) an amount would be included in the R&D partnership’s assessable income for the event year under subsection 40‑285(1) for the asset and the balancing adjustment event.

Note 1: This section applies in a modified way if the partner has deductions for the asset under former section 73BA or 73BH of the Income Tax Assessment Act 1936 (see section 355‑325 of the Income Tax (Transitional Provisions) Act 1997).

Note 2: Section 40‑293 applies if the R&D partnership can deduct an amount under section 40‑25, as that section applies apart from this Division and former section 73BC of the Income Tax Assessment Act 1936.

Notional deduction

(2) If the *R&D partnership could deduct for the event year an amount under subsection 40‑285(2) for the asset and the event if Division 40 applied as described in paragraph (1)(e), the partner can deduct the partner’s proportion of that amount for the event year.

Amount to be included in assessable income

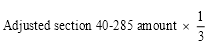

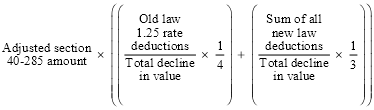

(3) If an amount (the section 40‑285 amount) would be included in the *R&D partnership’s assessable income for the event year under subsection 40‑285(1) for the asset and the event if Division 40 applied as described in paragraph (1)(e), the partner’s proportion of the sum of:

(a) that amount; and

(b) the following amount;

is included in the partner’s assessable income for the event year:

where:

adjusted section 40‑285 amount means so much of the section 40‑285 amount as does not exceed the total decline in value.

total decline in value means the asset’s *cost, less its *adjustable value, worked out under Division 40 as it applies as described in paragraph (1)(e).

355‑530 Implications for partner’s aggregated turnover

For the purposes of sections 40‑292 (balancing adjustments for decline in value) and 355‑100 (tax offsets for R&D), if:

(a) an *R&D entity is a partner of an *R&D partnership at some time during an income year; and

(b) the partner’s *aggregated turnover for the income year does not include the R&D partnership’s *annual turnover for the income year;

the partner’s aggregated turnover for the income year includes the *partner’s proportion of the R&D partnership’s annual turnover for the income year.

355‑535 Disposal of R&D results for R&D partnerships

In addition to its application apart from this section, section 355‑410 (disposal of R&D results) also applies to each partner of an *R&D partnership with such changes as are appropriate having regard to:

(a) amounts (the results amounts) of a kind set out in subparagraphs 355‑410(1)(b)(i) to (v) that the R&D partnership receives or becomes entitled to receive in an income year; and

(b) the principle that any amount to be included in the partner’s assessable income for the income year for a results amount should be the partner’s proportion of the amount arising under subsection 355‑410(2) for the results amount.

Note: The ordinary application of section 355‑410 will apply to any of the partner’s deductions under this Division that do not relate to the R&D partnership.

355‑540 Application of recoupment rules

(1) If:

(a) an *R&D partnership incurs expenditure (the partnership expenditure) on *R&D activities; and

(b) an *R&D entity (the partner) is entitled under section 355‑100 to a *tax offset because it can, under section 355‑205 or 355‑480, deduct some or all of that expenditure; and

(c) the R&D partnership receives an amount as a *recoupment of any or all of the partnership expenditure;

the partner is taken, for the purposes of Subdivisions 20‑A and 355‑G:

(d) to have incurred the partner’s proportion of the partnership expenditure when the R&D partnership incurred that expenditure; and

(e) to have received the partner’s proportion of the recoupment when the R&D partnership received the recoupment.

(2) If:

(a) an *R&D entity (the partner) is entitled under section 355‑100 to a *tax offset because it can, under section 355‑520, deduct an amount for an income year for an asset; and

(b) the applicable *R&D partnership receives an amount as a *recoupment of any or all of the R&D partnership’s expenditure included in the *cost of the asset for the purposes of the application of Division 40 as described in paragraph 355‑520(1)(d);

the partner is taken, for the purposes of Subdivisions 20‑A and 355‑G:

(c) to have incurred the partner’s proportion of that expenditure when the R&D partnership incurred that expenditure; and

(d) to have received the partner’s proportion of the recoupment when the R&D partnership received the recoupment.

355‑545 Relevance for net income, and losses, of the R&D partnership

For an *R&D entity that is a partner of an *R&D partnership, none of the following:

(a) any expenditure the R&D entity is taken to have incurred because of this Subdivision;

(b) any amount the R&D entity can deduct under this Subdivision;

(c) any *recoupment the R&D entity is taken to have received because of this Subdivision;

are to be taken into account in determining the *net income of the R&D partnership, or any *partnership loss of the R&D partnership, for an income year.

Subdivision 355‑K—Application to Cooperative Research Centres

Table of sections

355‑580 When notional deductions for CRC contributions arise

355‑580 When notional deductions for CRC contributions arise

Monetary contributions are deductible

(1) An *R&D entity can deduct for an income year expenditure it incurs during that year to the extent that:

(a) the expenditure is in the form of monetary contributions under the *CRC program; and

(b) the contributions have been or will be spent under the CRC program on one or more *R&D activities for which the R&D entity is registered under section 27A of the Industry Research and Development Act 1986 for an income year.

Note 1: The R&D activities will need to be conducted during the income year the R&D entity is registered for those activities (see sections 27A and 27J of the Industry Research and Development Act 1986).

Note 2: Expenditure incurred in income years starting on or after 1 July 2011 may be deductible for activities registered for income years starting before 1 July 2011 (see section 355‑200 of the Income Tax (Transitional Provisions) Act 1997).

(2) Subsection (1) does not apply to expenditure to the extent that it is incurred out of Commonwealth funding.

No other deductions arise for monetary contributions etc.

(3) Neither:

(a) a contribution an *R&D entity can deduct under subsection (1); nor

(b) expenditure incurred under the *CRC program, to the extent that the expenditure is incurred out of:

(i) a contribution an R&D entity can deduct under subsection (1); or

(ii) Commonwealth funding;

can be deducted by any R&D entity under any other provision of this Division for any income year.

(4) If an asset’s *cost includes expenditure incurred under the *CRC program out of:

(a) a contribution an *R&D entity can deduct under subsection (1); or

(b) Commonwealth funding;

an amount equal to the asset’s decline in value cannot be deducted under this Division by any R&D entity for any income year.

Subdivision 355‑W—Other matters

Table of sections

355‑700 Objecting to assessment of refundable tax offset

355‑705 Effect of findings by Innovation Australia

355‑710 Amendment of assessments

355‑715 Implications for other deductions and tax offsets

355‑700 Objecting to assessment of refundable tax offset

(1) An *R&D entity may object under subsection 175A(1) of the Income Tax Assessment Act 1936 against an assessment made in relation to the R&D entity to the extent that the assessment relates to the amount of a *tax offset under section 355‑100 that is subject to the refundable tax offset rules.

Note: See section 67‑30 for when a tax offset under section 355‑100 is subject to the refundable tax offset rules.

(2) This section does not limit subsection 175A(1) of that Act, and has effect despite subsection 175A(2) of that Act.

Note: Subsection 175A(2) of that Act prevents objections if the taxpayer has no taxable income, or if there is no tax payable on the taxpayer’s taxable income.

355‑705 Effect of findings by Innovation Australia

Findings about registration or core technology

(1) If:

(a) a certificate given to the Commissioner under the Industry Research and Development Act 1986 sets out:

(i) a finding under section 27B of that Act about an *R&D entity’s application for registration under section 27A of that Act for an income year; or

(ii) a finding under section 27J of that Act about an R&D entity’s registration under section 27A of that Act for an income year; or

(iii) a finding under section 28E of that Act about an R&D entity and one or more *R&D activities conducted or to be conducted during one or more income years; and

(b) the finding was made within 4 years after the end of the income year or the last of the income years (as appropriate);

the finding binds the Commissioner for the purposes of assessments of the R&D entity for the income year or years (as appropriate).

Note: Section 28E of the Industry Research and Development Act 1986 deals with findings that technology is core technology for particular R&D activities. Expenditure incurred in acquiring such technology is not deductible under this Division (see subsection 355‑225(2)).

Advance findings about activities yet to be completed

(2) If:

(a) an activity is being conducted, or is yet to be conducted, in an income year; and

(b) an *R&D entity applies in the income year for a finding under section 28A of the Industry Research and Development Act 1986 about the activity; and

(c) Innovation Australia makes the finding and gives the Commissioner a certificate under that Act setting out the finding;

the finding binds the Commissioner for the purposes of assessments of the R&D entity for the income year and the next 2 income years.

Advance findings about completed activities

(3) However, if:

(a) an activity is completed during an income year; and

(b) an *R&D entity applies in the income year for a finding under section 28A of the Industry Research and Development Act 1986 about the activity; and

(c) Innovation Australia makes the finding and gives the Commissioner a certificate under that Act setting out the finding;

the finding binds the Commissioner for the purposes of assessments of the R&D entity for the income year.

355‑710 Amendment of assessments

Dealing with findings of Innovation Australia

(1) If:

(a) a certificate given to the Commissioner under the Industry Research and Development Act 1986 sets out:

(i) a finding under section 27B of that Act about an *R&D entity’s application for registration under section 27A of that Act for an income year; or

(ii) a finding under section 27J of that Act about an R&D entity’s registration under section 27A of that Act for an income year; or

(iii) a finding under section 28A or 28C of that Act made on application by an R&D entity during an income year; or

(iv) a finding under section 28E of that Act about an R&D entity and one or more R&D activities conducted or to be conducted during one or more income years; and

(b) the finding was made within 4 years after the end of the income year or the last of the income years (as appropriate);

despite section 170 of the Income Tax Assessment Act 1936, the Commissioner may amend the R&D entity’s assessment for an income year affected by the finding at any time for the purposes of giving effect to the finding.

(2) However, the Commissioner may only do so within 2 years after the Commissioner is given the certificate if giving effect to the finding would increase the R&D entity’s liability.

Dealing with key decisions of Innovation Australia and others

(3) If:

(a) an internal review decision (the key decision) under subsection 30D(2) of the Industry Research and Development Act 1986 relates to an *R&D entity; or

(b) a decision (also the key decision) under the Administrative Appeals Tribunal Act 1975:

(i) varies a decision covered by paragraph (a); or

(ii) sets aside a decision covered by paragraph (a), whether or not that key decision also includes a decision made in substitution for the decision covered by paragraph (a); or

(c) a decision (also the key decision) of a court is about:

(i) a decision under Part III of the Industry Research and Development Act 1986 relating to an R&D entity; or

(ii) a decision covered by paragraph (b);

despite section 170 of the Income Tax Assessment Act 1936, the Commissioner may amend the R&D entity’s assessment for an income year affected by the key decision at any time for the purposes of giving effect to that decision.

355‑715 Implications for other deductions and tax offsets

(1) If an *R&D entity is entitled under section 355‑100 to a *tax offset for an income year for expenditure it can deduct under section 355‑205, 355‑480 or 355‑580, that expenditure:

(a) cannot be taken into account by any entity in working out a deduction under any other Division of this Act for any income year; and

(b) cannot be taken into account by any entity in working out a tax offset under any other Division of this Act for any income year.

Note: Section 355‑205 is about R&D expenditure, section 355‑480 is about earlier year associate R&D expenditure, and section 355‑580 is about CRC contributions.

(2) If an *R&D entity is entitled under section 355‑100 to a *tax offset for an income year for a deduction under section 355‑305, 355‑315, 355‑520 or 355‑525 of an amount equal to the decline in value of an asset, that decline in value:

(a) cannot be taken into account by any entity in working out a deduction under any other Division of this Act (other than section 40‑292 or 40‑293) for any income year; and

(b) cannot be taken into account by any entity in working out a tax offset under any other Division of this Act for any income year;

to the extent that the decline in value is attributable to the use of the asset for the purpose of conducting one or more of the *R&D activities to which the deduction relates.

Note 1: A deduction may be available under section 40‑25 to the extent that the asset’s decline in value is attributable to another purpose. If so, that deduction under section 40‑25 will not take into account the asset’s decline in value to the extent that it is attributable to the R&D activities (see also subsection 40‑25(2)).

Note 2: Section 355‑305 is about the decline in value of R&D assets, section 355‑315 is about balancing adjustments for R&D assets, section 355‑520 is about the decline in value of R&D partnership assets, and section 355‑525 is about balancing adjustments for R&D partnership assets.

Note 3: Sections 40‑292 and 40‑293 deal with balancing adjustments when deductions have been available for the asset’s decline in value both under this Division and section 40‑25.

2 Subsection 995‑1(1)

Insert:

core R&D activities has the meaning given by section 355‑25.

3 Subsection 995‑1(1)

Insert:

CRC program means the program administered by the Commonwealth known as the Cooperative Research Centres Program.

4 Subsection 995‑1(1)

Insert:

feedstock revenue has the meaning given by section 355‑470.

5 Subsection 995‑1(1)

Insert:

partner’s proportion has the meaning given by subsection 355‑505(2).

6 Subsection 995‑1(1)

Insert:

R&D activities has the meaning given by section 355‑20.

7 Subsection 995‑1(1)

Insert:

R&D entity has the meaning given by section 355‑35.

8 Subsection 995‑1(1)

Insert:

R&D partnership has the meaning given by subsection 355‑505(1).

9 Subsection 995‑1(1) (definition of research and development activities)

Repeal the definition.

10 Subsection 995‑1(1)

Insert:

supporting R&D activities has the meaning given by section 355‑30.

Schedule 2—Innovation Australia’s role

Industry Research and Development Act 1986

1 After Part II

Insert:

Part III—Functions relating to the R&D tax offset

The objects of this Part are:

(a) to provide integrity for the working out of tax offsets under Division 355 (about R&D) of the Income Tax Assessment Act 1997; and

(b) to increase certainty through findings about matters relevant to the working out of those tax offsets; and

(c) to improve access for small and medium R&D entities to quality research services by maintaining a register of research service providers.

Note: The integrity mentioned in paragraph (a) is provided, for example, by:

(a) the Board registering entities seeking these tax offsets; and

(b) the Board conducting compliance checks on those entities.

The following is a simplified outline of this Part:

• The Board may, on application by an R&D entity, register the R&D entity for R&D activities. This registration is needed before the R&D entity can be entitled to a tax offset (an R&D tax offset) under Division 355 of the Income Tax Assessment Act 1997 for the R&D activities.

• The R&D entity can seek an advance finding to get early notice about whether an activity is considered to be an R&D activity.

• The R&D entity can seek a finding that an activity cannot be conducted in Australia. The finding is needed before expenditure incurred on the activity can count towards an R&D tax offset.

• The Board may register entities as research service providers capable of providing research services to R&D entities.

• Internal and external review can be sought for certain decisions under this Part.

Division 2—Registering for the R&D tax offset

The following is a simplified outline of this Division:

• The Board may register an R&D entity for R&D activities conducted during an income year.

• The Board may make findings about the nature of an R&D entity’s activities both before and after registration. This includes findings made on application by the R&D entity after registration.

• These findings bind the Commissioner for the purposes of any entitlement of the R&D entity to a tax offset under Division 355 of the Income Tax Assessment Act 1997 for the activities.

• The Board will register an R&D entity’s activities consistently with any findings made about the entity’s application. Any findings made about these activities after registration will, if necessary, automatically vary the entity’s registration.

• Registrations can also be varied and revoked.

Subdivision B—Registering R&D entities for R&D activities

27A Registering R&D entities for R&D activities

(1) The Board must, on application by an R&D entity, decide whether to register or refuse to register the entity for either or both of the following for an income year:

(a) one or more specified activities as core R&D activities conducted during the income year;

(b) one or more specified activities as supporting R&D activities conducted during the income year.

Note 1: A decision under this subsection is reviewable (see Division 5).

Note 2: For requirements of applications, see section 27D.

(2) If the Board decides under subsection (1) to register the R&D entity, the Board must do so consistently with:

(a) any findings already in force under subsection 27B(1) in relation to the application; and

(b) any findings already in force under subsection 28A(1) (advance findings about the nature of activities) in relation to the R&D entity.

(3) For each activity registered under subsection (1) as a supporting R&D activity for an R&D entity for an income year, the registration is to also specify:

(a) one or more activities as the corresponding core R&D activities; and

(b) if any of those activities specified as a core R&D activity is not registered under paragraph (1)(a) for the R&D entity for the income year—each income year for which that core R&D activity:

(i) was registered under paragraph (1)(a) for the R&D entity; or

(ii) is proposed to be registered under paragraph (1)(a) for the R&D entity.

27B Findings about applications for registration

(1) The Board may make one or more findings to the following effect when considering an R&D entity’s application for the purposes of subsection 27A(1):

(a) that all or part of an activity mentioned in the application was a core R&D activity conducted during the income year;

(b) that all or part of an activity mentioned in the application was not an activity of a kind covered by paragraph (a);

(c) that all or part of an activity mentioned in the application was a supporting R&D activity conducted: