Clean Energy (Income Tax Rates Amendments) Act 2011

No. 150, 2011

An Act to amend the Income Tax Rates Act 1986, and for related purposes

Clean Energy (Income Tax Rates Amendments) Act 2011

No. 150, 2011

An Act to amend the Income Tax Rates Act 1986, and for related purposes

Contents

2 Commencement

3 Schedule(s)

Schedule 1—Personal tax rates

Part 1—Amendments applying from the 2012‑13 year of income

Income Tax Rates Act 1986

Part 2—Amendments applying from the 2015‑16 year of income

Income Tax Rates Act 1986

Clean Energy (Income Tax Rates Amendments) Act 2011

No. 150, 2011

An Act to amend the Income Tax Rates Act 1986, and for related purposes

[Assented to 4 December 2011]

The Parliament of Australia enacts:

This Act may be cited as the Clean Energy (Income Tax Rates Amendments) Act 2011.

(1) Each provision of this Act specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information | ||

Column 1 | Column 2 | Column 3 |

Provision(s) | Commencement | Date/Details |

1. Sections 1 to 3 and anything in this Act not elsewhere covered by this table | The day this Act receives the Royal Assent. | 4 December 2011 |

2. Schedule 1, Part 1 | The latest of: (a) the start of 1 July 2012; and (b) the commencement of section 3 of the Clean Energy Act 2011; and (c) the start of the day the Clean Energy (Tax Laws Amendments) Act 2011 receives the Royal Assent. However, the provision(s) do not commence at all unless both of the events mentioned in paragraphs (b) and (c) occur. | 1 July 2012 |

3. Schedule 1, Part 2 | The latest of: (a) the start of 1 July 2015; and (b) the commencement of section 3 of the Clean Energy Act 2011; and (c) the start of the day the Clean Energy (Tax Laws Amendments) Act 2011 receives the Royal Assent. However, the provision(s) do not commence at all unless both of the events mentioned in paragraphs (b) and (c) occur. | 1 July 2015 |

Note: This table relates only to the provisions of this Act as originally enacted. It will not be amended to deal with any later amendments of this Act.

(2) Any information in column 3 of the table is not part of this Act. Information may be inserted in this column, or information in it may be edited, in any published version of this Act.

Each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

1 Subsection 3(1)

Insert:

tax‑free threshold means $18,200.

2 Subsections 20(1) and (2)

Repeal the subsections, substitute:

Part‑year residency periods

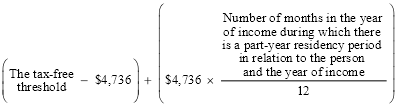

(1) This Act applies in relation to a person and a year of income as if the reference in the table in Part I of Schedule 7 to the tax‑free threshold were a reference to the amount calculated in accordance with the following formula, if there are one or more part‑year residency periods in relation to the person in relation to the year of income:

Trustees

(1A) Subsection (1) does not apply in calculating the tax payable by the trustee of a trust estate under section 98 of the Assessment Act in respect of a share of a beneficiary of the net income of the trust estate of a year of income.

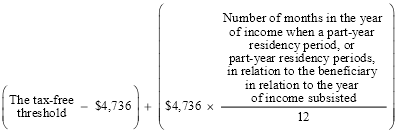

(2) However, this Act applies in calculating the tax payable by the trustee in respect of that share as if the reference in the table in Part I of Schedule 7 to the tax‑free threshold were a reference to the amount calculated in accordance with the following formula, if there are one or more part‑year residency periods in relation to the beneficiary in relation to the year of income:

3 Clause 1 of Part I of Schedule 7 (table items 1 and 2)

Repeal the items, substitute:

1 | exceeds the tax‑free threshold but does not exceed $37,000 | 19% |

2 | exceeds $37,000 but does not exceed $80,000 | 32.5% |

4 Subparagraph 2(b)(ii) of Division 2 of Part I of Schedule 8

Omit “$6,000”, substitute “the tax‑free threshold”.

5 Paragraph 2(b) of Part I of Schedule 10

Omit “$6,000”, substitute “the tax‑free threshold”.

6 Application provision

The amendments made by this Part apply to the 2012‑13 year of income and later years of income.

7 Subsection 3(1) (definition of tax‑free threshold)

Omit “$18,200”, substitute “$19,400”.

8 Clause 1 of Part I of Schedule 7 (table item 2)

Repeal the item, substitute:

2 | exceeds $37,000 but does not exceed $80,000 | 33% |

9 Application provision

The amendments made by this Part apply to the 2015‑16 year of income and later years of income.

[Minister’s second reading speech made in—

House of Representatives on 13 September 2011

Senate on 12 October 2011]

(176/11)