Petroleum Resource Rent Tax Assessment Amendment Act 2012

No. 18, 2012

An Act to amend the Petroleum Resource Rent Tax Assessment Act 1987, and for other purposes

Petroleum Resource Rent Tax Assessment Amendment Act 2012

No. 18, 2012

An Act to amend the Petroleum Resource Rent Tax Assessment Act 1987, and for other purposes

Contents

2 Commencement

3 Schedule(s)

Schedule 1—Extension to onshore projects etc.

Petroleum Resource Rent Tax Assessment Act 1987

Schedule 2—Assessable receipts

Part 1—Amendments commencing on 1 July 2012

Petroleum Resource Rent Tax Assessment Act 1987

Part 2—Amendments commencing on Proclamation

Petroleum Resource Rent Tax Assessment Act 1987

Schedule 3—Deductible expenditure

Petroleum Resource Rent Tax Assessment Act 1987

Schedule 4—Starting base for onshore petroleum projects and the North West Shelf project

Part 1—Main amendments

Petroleum Resource Rent Tax Assessment Act 1987

Part 2—Other amendments

Petroleum Resource Rent Tax Assessment Act 1987

Schedule 5—Consolidated groups

Part 1—Main amendments

Petroleum Resource Rent Tax Assessment Act 1987

Part 2—Other amendments

Income Tax Assessment Act 1997

Petroleum Resource Rent Tax Assessment Act 1987

Schedule 6—Other amendments

Part 1—Amendments related to clean energy package

Petroleum Resource Rent Tax Assessment Act 1987

Part 2—Amendments related to repeal of an Act

Petroleum Resource Rent Tax Act 1987

Part 3—Other amendments

Crimes (Taxation Offences) Act 1980

Excise Tariff Act 1921

Income Tax Assessment Act 1997

Petroleum Resource Rent Tax Assessment Act 1987

Petroleum Resource Rent Tax Assessment Amendment Act 2012

No. 18, 2012

An Act to amend the Petroleum Resource Rent Tax Assessment Act 1987, and for other purposes

[Assented to 29 March 2012]

The Parliament of Australia enacts:

This Act may be cited as the Petroleum Resource Rent Tax Assessment Amendment Act 2012.

(1) Each provision of this Act specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information | ||

Column 1 | Column 2 | Column 3 |

Provision(s) | Commencement | Date/Details |

1. Sections 1 to 3 and anything in this Act not elsewhere covered by this table | The day this Act receives the Royal Assent. | 29 March 2012 |

2. Schedule 1, items 1 to 10 | 1 July 2012. | 1 July 2012 |

3. Schedule 1, item 11 | 1 July 2012. However, the provision(s) do not commence at all if the Tax Laws Amendment (2011 Measures No. 8) Act 2011 receives the Royal Assent on or before 1 July 2012. | Does not commence |

4. Schedule 1, items 12 to 24 | 1 July 2012. | 1 July 2012 |

5. Schedule 1, item 25 | The later of: (a) the start of 1 July 2012; and (b) immediately after the commencement of Schedule 2 to the Tax Laws Amendment (2011 Measures No. 8) Act 2011. However, the provision(s) do not commence at all if the event mentioned in paragraph (b) does not occur. | 1 July 2012 (paragraph (a) applies) |

6. Schedule 1, items 26 to 46 | 1 July 2012. | 1 July 2012 |

7. Schedule 2, Part 1 | 1 July 2012. | 1 July 2012 |

8. Schedule 2, Part 2 | A single day to be fixed by Proclamation. However, if the provision(s) do not commence within the period of 6 months beginning on the day this Act receives the Royal Assent, they commence on the day after the end of that period. | 29 September 2012 |

9. Schedules 3 and 4 | 1 July 2012. | 1 July 2012 |

10. Schedule 5, item 1 | 1 July 2012. | 1 July 2012 |

11. Schedule 5, items 2 to 5 | The later of: (a) immediately after the commencement of the provision(s) covered by table item 2; and (b) immediately after the commencement of Schedule 3 to the Minerals Resource Rent Tax (Consequential Amendments and Transitional Provisions) Act 2012. However, the provision(s) do not commence at all if the event mentioned in paragraph (b) does not occur. | 1 July 2012 (paragraph (b) applies) |

12. Schedule 5, items 6 to 12 | 1 July 2012. | 1 July 2012 |

13. Schedule 6, Part 1 | The later of: (a) immediately after the commencement of the provision(s) covered by table item 2; and (b) immediately after the commencement of section 3 of the Clean Energy Act 2011. However, the provision(s) do not commence at all if the event mentioned in paragraph (b) does not occur. | 1 July 2012 (paragraph (a) applies) |

14. Schedule 6, Parts 2 and 3 | 1 July 2012. | 1 July 2012 |

Note: This table relates only to the provisions of this Act as originally enacted. It will not be amended to deal with any later amendments of this Act.

(2) Any information in column 3 of the table is not part of this Act. Information may be inserted in this column, or information in it may be edited, in any published version of this Act.

Each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

Schedule 1—Extension to onshore projects etc.

Petroleum Resource Rent Tax Assessment Act 1987

1 Section 2 (definition of access authority)

Repeal the definition, substitute:

access authority means:

(a) a petroleum access authority within the meaning of the Offshore Petroleum and Greenhouse Gas Storage Act 2006; or

(b) an authority or right (however described) under another Australian law to carry on, in relation to petroleum, specified operations in a specified area (other than an authority or right that is an exploration permit, retention lease, production licence or infrastructure licence).

Note: The Resources Minister may determine that an authority or right is, or is not, an authority or right of a kind mentioned in this paragraph: see section 2AA.

2 Section 2 (paragraph (a) of the definition of applicable commencement date)

After “(b)”, insert “or (c)”.

3 Section 2 (at the end of the definition of applicable commencement date)

Add:

; or (c) if the project is an onshore petroleum project or the North West Shelf project, or if an onshore petroleum project is a pre‑combination project in relation to the project—1 July 2012.

4 Section 2 (definition of block)

Repeal the definition, substitute:

block means:

(a) in relation to an offshore area—a block within the meaning of the Offshore Petroleum and Greenhouse Gas Storage Act 2006; or

(b) in relation to an onshore area—an area (however described) referred to in another Australian law relating to exploration for, or recovery of, petroleum.

5 Section 2 (definition of eligible production licence)

Repeal the definition.

6 Section 2 (definition of excluded fee)

Repeal the definition, substitute:

excluded fee means:

(a) an amount of a kind referred to in paragraph 113(1)(c), subsection 115(5), paragraph 118(1)(c), subsection 178(4) or paragraph 181(1)(c) of the Offshore Petroleum and Greenhouse Gas Storage Act 2006; or

(b) a similar amount payable, under another Australian law, in relation to the grant of an exploration permit, retention lease or production licence.

7 Section 2 (definition of exploration permit)

Repeal the definition, substitute:

exploration permit means:

(a) a petroleum exploration permit within the meaning of the Offshore Petroleum and Greenhouse Gas Storage Act 2006; or

(b) an authority or right (however described) under another Australian law:

(i) to explore for petroleum in an area; or

(ii) to recover petroleum on an appraisal basis in that area; or

(iii) to carry on such operations, and execute such works, in the area as are necessary for those purposes;

that is not an authority or right to recover petroleum other than on an appraisal basis.

Note: The Resources Minister may determine that an authority or right is, or is not, an authority or right of a kind mentioned in this paragraph: see section 2AA.

8 Section 2 (definition of exploration permit area)

Repeal the definition, substitute:

exploration permit area means:

(a) a petroleum exploration permit area within the meaning of the Offshore Petroleum and Greenhouse Gas Storage Act 2006; or

(b) the area covered by an authority or right mentioned in paragraph (b) of the definition of exploration permit.

9 Section 2 (definition of holder of a registered interest)

Repeal the definition, substitute:

holder of a registered interest, in relation to a production licence, means a person holding an interest in the production licence, being an interest created by a dealing in relation to which:

(a) an entry has been made under subsection 494(3) of the Offshore Petroleum and Greenhouse Gas Storage Act 2006; or

(b) an entry has been made in a register mentioned in paragraph (b) of the definition of registered holder.

10 Section 2 (definition of infrastructure licence)

Repeal the definition, substitute:

infrastructure licence means:

(a) an infrastructure licence within the meaning of section 7 of the Offshore Petroleum and Greenhouse Gas Storage Act 2006; or

(b) an authority or right (however described) under another Australian law to construct and operate facilities in a specified area for engaging in any of the following activities (other than an authority or right that is an exploration permit, retention lease, production licence or pipeline licence):

(i) remote control of facilities, structures or installations used to recover petroleum in a production licence area;

(ii) processing petroleum recovered in any place, including converting petroleum into another form by physical or chemical means, or both, and partial processing of petroleum;

(iii) storing petroleum before it is transported to another place;

(iv) preparing petroleum for transport to another place (for example, pumping or compressing);

(v) activities related to any of the above.

Note: The Resources Minister may determine that an authority or right is, or is not, an authority or right of a kind mentioned in this paragraph: see section 2AA.

11 Section 2 (after paragraph (e) of the definition of marketable petroleum commodity)

Insert:

(ea) shale oil;

12 Section 2

Insert:

North West Shelf project means the petroleum project referred to in subsection 19(1B).

13 Section 2

Insert:

oil shale means any shale or other rock (other than coal) from which a fluid consisting of or including hydrocarbons may be extracted or produced.

14 Section 2

Insert:

onshore area, in relation to a State or Territory, means the area of the State or Territory that is not part of that State’s or Territory’s offshore area within the meaning of the Offshore Petroleum and Greenhouse Gas Storage Act 2006 and is not within the Joint Petroleum Development Area within the meaning of that Act.

15 Section 2

Insert:

onshore petroleum project means a petroleum project for which:

(a) no part of the production licence area is a petroleum production licence area within the meaning of the Offshore Petroleum and Greenhouse Gas Storage Act 2006; and

(b) no part of the production licence area is an area within the Joint Petroleum Development Area within the meaning of that Act.

16 Section 2 (definition of petroleum)

Repeal the definition, substitute:

petroleum means:

(a) petroleum within the meaning of the Offshore Petroleum and Greenhouse Gas Storage Act 2006; or

(b) oil shale.

However, petroleum does not include a taxable resource within the meaning of the Minerals Resource Rent Tax Act 2012.

17 Section 2 (definition of pipeline licence)

Repeal the definition, substitute:

pipeline licence means:

(a) a pipeline licence within the meaning of the Offshore Petroleum and Greenhouse Gas Storage Act 2006; or

(b) an authority or right (however described) under another Australian law:

(i) to construct a pipeline in a specified area in accordance with any specified conditions; and

(ii) to construct in that area specified pumping stations, tank stations and valve stations at specified positions; and

(iii) to operate that pipeline and those pumping stations, tank stations and valve stations; and

(iv) to carry on such operations, to execute such works and to do all such other things in that area as are necessary for, or incidental to, the construction or operation of that pipeline and those pumping stations, tank stations and valve stations.

Note: The Resources Minister may determine that an authority or right is, or is not, an authority or right of a kind mentioned in this paragraph: see section 2AA.

18 Section 2 (paragraph (a) of the definition of pre‑combination project)

Omit “eligible”.

19 Section 2 (at the end of the definition of production licence)

Add:

; or (c) an authority or right (however described) under another Australian law to undertake activities for the recovery of petroleum from an area (other than an authority or right that is an exploration permit or a retention lease).

Note: The Resources Minister may determine that an authority or right is, or is not, an authority or right of a kind mentioned in this paragraph: see section 2AA.

20 Section 2 (definition of production licence area)

Repeal the definition, substitute:

production licence area means the following:

(a) a petroleum production licence area within the meaning of the Offshore Petroleum and Greenhouse Gas Storage Act 2006;

(b) the area covered by an authority or right mentioned in paragraph (c) of the definition of production licence;

and, in relation to the Greater Sunrise project, includes the Western Greater Sunrise area.

21 Section 2 (definition of registered holder)

Repeal the definition, substitute:

registered holder means:

(a) in relation to a title under the Offshore Petroleum and Greenhouse Gas Storage Act 2006—the registered holder within the meaning of that Act; and

(b) in relation to an authority or right (however described) under another Australian law—the person whose name is shown in the register (however described) kept under the relevant Australian law concerned.

22 Section 2 (definition of retention lease)

Repeal the definition, substitute:

retention lease means:

(a) a petroleum retention lease within the meaning of the Offshore Petroleum and Greenhouse Gas Storage Act 2006; or

(b) an authority or right (however described) under another Australian law:

(i) to explore for petroleum in an area; or

(ii) to recover petroleum on an appraisal basis in that area; or

(iii) to carry on such operations, and execute such works, in the area as are necessary for those purposes;

that is not an authority or right to recover petroleum other than on an appraisal basis, and that is granted on the basis that the area contains petroleum and that recovery of that petroleum is likely to become commercially viable in the future.

Note: The Resources Minister may determine that an authority or right is, or is not, an authority or right of a kind mentioned in this paragraph: see section 2AA.

23 Section 2 (definition of retention lease area)

Repeal the definition, substitute:

retention lease area means:

(a) a petroleum retention lease area within the meaning of the Offshore Petroleum and Greenhouse Gas Storage Act 2006; or

(b) the area covered by an authority or right mentioned in paragraph (b) of the definition of retention lease.

24 After section 2

Insert:

2AA Determinations relating to certain defined terms

(1) An authority or right under an Australian law is taken, for the purposes of this Act, to be an authority or right mentioned in one of the paragraphs to which this section applies if the Resources Minister determines, by legislative instrument, that it is an authority or right of that kind.

(2) An authority or right under an Australian law is taken, for the purposes of this Act, not to be an authority or right mentioned in one of the paragraphs to which this section applies if the Resources Minister determines, by legislative instrument, that it is not an authority or right of that kind.

(3) This section applies to the following paragraphs in section 2:

(a) paragraph (b) of the definition of access authority;

(b) paragraph (b) of the definition of exploration permit;

(c) paragraph (b) of the definition of infrastructure licence;

(d) paragraph (b) of the definition of pipeline licence;

(e) paragraph (c) of the definition of production licence;

(f) paragraph (b) of the definition of retention lease.

25 After paragraph 2E(2)(e)

Insert:

(ea) shale oil;

26 Subsection 19(1)

After “(1A)”, insert “and (1B)”.

27 Subsection 19(1)

Omit “an eligible”, substitute “a”.

28 Subsection 19(1)

Omit “eligible” (second occurring).

29 After subsection 19(1A)

Insert:

(1B) For the purposes of this Act, there is taken to be a single petroleum project in relation to all production licences that are related to the North West Shelf exploration permits and that are in force from time to time.

30 Subsection 19(2)

Omit “eligible” (wherever occurring).

31 Paragraph 19(2B)(a)

Omit “an eligible”, substitute “a”.

32 Paragraph 19(2B)(b)

Omit “eligible”.

33 Paragraph 19(2C)(a)

Omit “an eligible”, substitute “a”.

34 Paragraph 19(2C)(b)

Omit “eligible”.

35 Subsection 19(3)

Omit “eligible” (wherever occurring).

36 Subsection 20(1)

Repeal the subsection, substitute:

(1) Subject to this section, where within the qualifying period in relation to a production licence in relation to a petroleum project, the Resources Minister, whether on application, request or otherwise, having regard to:

(a) the respective operations, facilities and other things that comprise, have comprised or will comprise that project and any other petroleum project or projects existing at the time at which the production licence came into force; and

(b) the persons by whom or on whose behalf the operations, facilities and other things referred to in paragraph (a) are being, have been or are proposed to be carried on or provided; and

(c) to the extent (if any) that the projects are onshore petroleum projects—the respective operations, facilities and other things that are involved, have been involved or will be involved in any further processing or treating of any petroleum or marketable petroleum commodity produced in relation to the projects; and

(d) to the extent (if any) that the projects are not onshore petroleum projects—the geological, geophysical and geochemical and other features of the production licence areas in relation to the projects;

considers that the projects are sufficiently related to be treated for the purposes of this Act as a single petroleum project, the Minister must issue a certificate under this subsection specifying the production licence or production licences in relation to each of the projects.

(1A) Despite subsection (1), the Minister cannot specify, under that subsection:

(a) a production licence relating to the North West Shelf project; or

(b) if one of the projects is not an onshore petroleum project—a production licence relating to:

(i) an onshore petroleum project existing on 30 June 2012; or

(ii) if a pre‑combination project in relation to a combined project is such a project—the combined project.

37 Subsection 20(2)

Omit “eligible” (first occurring).

38 Paragraph 20(2)(a)

Repeal the paragraph, substitute:

(a) the period of 90 days after the latest of the following:

(i) the time the licence comes into force;

(ii) the commencement of this Act;

(iii) if the licence relates to an onshore petroleum project—the start of 1 January 2013; or

39 Paragraph 20(2)(b)

Omit “eligible”.

40 Subsection 20(4)

After “sale of” insert “petroleum or”.

41 Subsections 20(6) and (7)

Omit “eligible” (wherever occurring).

42 Clause 1 of the Schedule (paragraph (a) of the definition of starting day)

Omit “or the Bass Strait project”, substitute “, the Bass Strait project or the North West Shelf project”.

43 Clause 1 of the Schedule (after paragraph (c) of the definition of starting day)

Insert:

(ca) in relation to the North West Shelf project—the earlier of the day on which the exploration permit known as WA‑1‑P was granted and the day on which the exploration permit known as WA‑28‑P was granted; or

44 Subclause 13(1) of the Schedule

Omit “subclauses (2) and (3)”, substitute “subclause (2)”.

45 Subclause 13(3) of the Schedule

Repeal the subclause.

46 Transitional

Division 2 of Part VIII of the Petroleum Resource Rent Tax Assessment Act 1987 (collection by instalments) does not apply, in respect of the year of tax commencing on 1 July 2012, in relation to an onshore petroleum project or the North West Shelf project.

Schedule 2—Assessable receipts

Part 1—Amendments commencing on 1 July 2012

Petroleum Resource Rent Tax Assessment Act 1987

1 At the end of subsection 23(1)

Add:

; (f) assessable incidental production receipts.

2 Subsection 23(2)

Omit “(e)”, substitute “(f)”.

3 Section 28

Before “For”, insert “(1)”.

4 At the end of section 28

Add:

(2) However, an amount referred to in subparagraph (b)(ii) that is a refund of resource tax expenditure is increased by dividing the amount by the rate mentioned in section 5 of the Petroleum Resource Rent Tax (Imposition—General) Act 2012.

5 After section 29

Insert:

29A Assessable incidental production receipts

(1) For the purposes of this Act, a reference to assessable incidental production receipts derived by a person in relation to a petroleum project is a reference to the consideration receivable, less the amount mentioned in subsection (2), by the person in relation to the sale of a product, or the provision of a service relating to carbon capture and storage, if:

(a) it has been recovered, extracted, provided or produced in carrying on operations, facilities or other things of a kind mentioned in section 37, 38 or 39 in relation to the project; and

(b) it is not petroleum or a marketable petroleum commodity; and

(c) eligible real expenditure in relation to the project (including, in the case of a combined project, any pre‑combination project in relation to the project) was incurred by the person in relation to those operations, facilities, or other things.

Example: The following are some examples:

(a) water from a water treatment facility that is an integral part of a coal seam gas project is sold;

(b) excess electricity that is produced as part of the petroleum project is sold.

(2) The amount is the sum of any expenditure (whether of a capital or revenue nature) incurred by the person to the extent that:

(a) it is incurred in deriving assessable incidental production receipts in relation to the petroleum project; and

(b) it is not eligible real expenditure in relation to the petroleum project.

6 Paragraph 30(a)

Omit “or assessable employee amenities receipts”, substitute “, assessable employee amenities receipts or assessable incidental production receipts”.

7 At the end of paragraphs 31(b) and (c)

Add “or”.

8 After paragraph 31(e)

Insert:

; or (ea) assessable incidental production receipts;

9 Paragraph 31(f)

Omit “except in the case of the Bass Strait Project”, substitute “unless paragraph (g) or (h) applies”.

10 At the end of section 31

Add:

; or (h) in the case of an onshore petroleum project or the North West Shelf project—at any time on or after 1 July 2012, including a time before the project commenced or after the project has ceased.

11 At the end of Division 2 of Part V

Add:

31AA Eligible real expenditure—onshore petroleum projects and the North West Shelf project

Despite section 45, this Division applies in relation to:

(a) an onshore petroleum project; or

(b) the North West Shelf project; or

(c) a project in relation to which an onshore petroleum project is a pre‑combination project;

as if eligible real expenditure could be incurred in relation to such a project at any time, including a time before 1 July 2012.

12 Paragraphs 57(1)(a) and (2)(a)

Omit “24, 25, 27, 28 or 29”, substitute “23”.

13 Transitional

(1) For the purposes of applying section 31 of the Petroleum Resource Rent Tax Assessment Act 1987 to an onshore petroleum project or the North West Shelf project, treat any receipts:

(a) of a kind referred to in that section; and

(b) derived before 1 July 2012 in relation to activities undertaken in relation to the project on or after that day;

as having been derived in the financial year in which the activities are undertaken.

(2) For the purposes of applying subparagraph 28(b)(ii) of the Petroleum Resource Rent Tax Assessment Act 1987 in relation to an onshore petroleum project or the North West Shelf project, disregard any receipts:

(a) of a kind referred to in that subparagraph; and

(b) that relate to resource tax expenditure incurred in relation to the project before 1 July 2012.

Part 2—Amendments commencing on Proclamation

Petroleum Resource Rent Tax Assessment Act 1987

14 Paragraph 24(1)(a)

After “any petroleum” insert “(other than project natural gas (within the meaning of the regulations) to which paragraph (f) applies)”.

15 Subparagraph 24(1)(d)(ii)

Repeal the subparagraph.

16 At the end of subsection 24(1)

Add:

; and (f) where:

(i) any project natural gas (within the meaning of the regulations) recovered from the project is or has been sold; and

(ii) the regulations apply to the project natural gas;

the amount worked out in accordance with the regulations.

Schedule 3—Deductible expenditure

Petroleum Resource Rent Tax Assessment Act 1987

1 Section 2

Insert:

Aboriginal person has the meaning given by subsection 4(1) of the Aboriginal and Torres Strait Islander Act 2005.

2 Section 2

Insert:

Australian law has the meaning given by subsection 995‑1(1) of the Income Tax Assessment Act 1997.

3 Section 2 (definition of eligible real expenditure)

After “general project expenditure”, insert “, resource tax expenditure”.

4 Section 2

Insert:

production licence notice, in relation to a petroleum project, means:

(a) a notice issued under subsection 258(7) of the Offshore Petroleum and Greenhouse Gas Storage Act 2006 in relation to the project; or

(b) a notice issued by a State or Territory authority that specifies the day that sufficient information has been provided to determine the application for the production licence in relation to the project.

5 Section 2

Insert:

Torres Strait Islander has the meaning given by subsection 4(1) of the Aboriginal and Torres Strait Islander Act 2005.

6 At the end of paragraph 19(4)(b)

Add:

; (vi) operations and facilities, carried on or provided, for an environmental purpose, in relation to the carrying on or provision of the operations, facilities and services referred to in this section.

7 After paragraph 32(f)

Insert:

(fa) resource tax expenditure;

8 Subsection 33(1)

Omit “or the Bass Strait project”, substitute “, the Bass Strait project or the North West Shelf project”.

9 Subsection 34(1)

Omit “or the Bass Strait project”, substitute “, the Bass Strait project or the North West Shelf project”.

10 Subsection 34A(1)

Omit “or the Bass Strait project”, substitute “, the Bass Strait project or the North West Shelf project”.

11 Paragraph 34A(1)(a)

Repeal the paragraph, substitute:

(a) any amount of class 2 general project expenditure actually incurred by the person in relation to the project in the financial year, not being expenditure incurred more than 5 years before the earlier of the following:

(i) the day specified in the production licence notice in relation to the project;

(ii) the day the production licence was issued in relation to the project; and

12 Subsection 34A(3)

After “Bass Strait project”, insert “or the North West Shelf project”.

13 Subsection 35(1)

Omit “or the Bass Strait project”, substitute “, the Bass Strait project or the North West Shelf project”.

14 After section 35B

Insert:

(1) For the purposes of this Act, a reference to the resource tax expenditure incurred by a person in a financial year in relation to a petroleum project (not being a combined project) is a reference to the sum of:

(a) any amount of resource tax expenditure actually incurred by the person in relation to the project in the financial year; and

(b) any amount that is taken by subsection (5) or Division 5 to be resource tax expenditure incurred by the person in relation to the project in the financial year.

(2) For the purposes of this Act, a reference to the resource tax expenditure incurred by a person in a financial year in relation to a combined project is a reference to the sum of:

(a) any amount of resource tax expenditure actually incurred by the person in relation to the project in the financial year (not being expenditure incurred before the project combination certificate in relation to the project came into force); and

(b) any amount that is taken by subsection (5) or Division 5 to be resource tax expenditure incurred by the person in relation to the project in the financial year; and

(c) if the financial year is the year in which the project combination certificate in relation to the project came into force—any amount of resource tax expenditure, or any amount that is taken by subsection (5) or Division 5 to be resource tax expenditure, incurred by the person in relation to the pre‑combination projects in the financial year.

(3) For the purposes of subsections (1) or (2), a reference to resource tax expenditure incurred by a person in a financial year in relation to a petroleum project is a reference to resource tax expenditure incurred by the person in the year to the extent the expenditure:

(a) is incurred in relation to petroleum recovered, on or after 1 July 2012, from the production licence area for the project; and

(b) is incurred under an Australian law (other than this Act); and

(c) is expenditure to which one of the following applies:

(i) the expenditure is a royalty, or would be a royalty if the petroleum were owned by the Commonwealth, or a State or Territory, just before the recovery of the petroleum;

(ii) the expenditure is an excise;

(iii) the expenditure is an amount calculated by reference to the revenue, expenditure or profits made or incurred by a person in relation to petroleum recovered from the production licence area for the project;

(iv) the expenditure is an amount calculated by reference to the value, at the wellhead, of petroleum recovered from the production licence area for the project.

(4) However, the amount of resource tax expenditure under subsection (3) is increased by dividing it by the rate of tax mentioned in section 5 of the Petroleum Resource Rent Tax (Imposition—General) Act 2012.

(5) For the purposes of subsection (1), (2) or (3), if the sum of the following incurred by a person in a financial year (the assessable year) in relation to a petroleum project exceeds the assessable receipts derived by the person in the assessable year in relation to the project:

(a) the class 1 augmented bond rate general expenditure;

(b) the class 1 augmented bond rate exploration expenditure;

(c) the class 2 augmented bond rate general expenditure;

(d) the class 1 GDP factor expenditure;

(e) the class 2 augmented bond rate exploration expenditure;

(f) the class 2 GDP factor expenditure;

(g) the resource tax expenditure;

the person is taken to incur, in relation to the project and on the first day of the next financial year, an amount of resource tax expenditure worked out in accordance with the formula:

where:

augmented bond rate means the long term bond rate in relation to the assessable year plus 1.05.

available excess means so much of the excess as does not exceed the resource tax expenditure incurred in the assessable year.

(6) Despite subsection (3), if a person (the eligible person) incurs a liability to make a payment to procure expenditure of a kind mentioned in subsection (3) by another person, then the expenditure is taken to have been incurred by the eligible person, and not by the other person, to the extent of the liability.

15 Subparagraph 37(1)(b)(vi)

Omit “and”.

16 At the end of paragraph 37(1)(b)

Add:

(vii) operations and facilities, carried on or provided, for an environmental purpose, in relation to the carrying on or provision of the operations, facilities and services referred to in this section; and

17 Section 44

Before “For”, insert “(1)”.

18 At the end of section 44

Add:

(2) For the purposes of paragraph (1)(e), a private override royalty payment does not include a payment to the extent:

(a) it is by way of compensation for carrying on or providing, in an area the operations, facilities or other things comprising a petroleum project; and

(b) it is paid:

(i) to a native title holder (within the meaning of the Native Title Act 1993) whose approved determination of native title (within the meaning of that Act) relates to that area; or

(ii) to a registered native title claimant (within the meaning of the Native Title Act 1993) whose claimant application (within the meaning of that Act) relates to that area; or

(iii) to a person who holds a right that relates to that area and arises under another Australian law dealing with the rights of Aboriginal persons or Torres Strait Islanders in relation to land or waters.

19 After paragraph 58B(1)(a)

Insert:

(aa) if the election was made by the person within 30 days after the commencement of Schedule 1 to the Petroleum Resource Rent Tax Assessment Amendment Act 2012—1 July 2012; or

20 Clause 1 of the Schedule (definition of relevant pre‑commencement day)

Repeal the definition, substitute:

relevant pre‑commencement day, in relation to a petroleum project, means:

(a) if the petroleum project is not a combined project, the Bass Strait project or the North West Shelf project—the day occurring 5 years before the earlier of the following:

(i) the day specified in the production licence notice in relation to the project;

(ii) the day the production licence was issued in relation to the project; or

(b) if the petroleum project is a combined project, the Bass Strait project or the North West Shelf project—the day occurring 5 years before the earlier of the following:

(i) the earliest day specified in a production licence notice in relation to a pre‑combination project in relation to the project;

(ii) the earliest day a production licence was issued in relation to a pre‑combination project in relation to the project.

Schedule 4—Starting base for onshore petroleum projects and the North West Shelf project

Petroleum Resource Rent Tax Assessment Act 1987

1 Section 2 (at the end of the definition of assessment)

Add:

Note: Under clause 23 of Schedule 2, assessments may also be made for starting base purposes.

2 Section 2 (definition of eligible real expenditure)

Before “or closing‑down expenditure”, insert “, acquired exploration expenditure, starting base expenditure”.

3 Section 2

Insert:

starting base amount has the meaning given by Division 1 of Part 3 of Schedule 2.

4 Section 2

Insert:

starting base asset has the meaning given by clause 10 of Schedule 2.

5 Section 2

Insert:

value, of a starting base asset, means:

(a) if, under Part 2 of Schedule 2, the book value approach is the valuation approach for the interest, in a petroleum project, to which the asset relates—the book value of the asset, worked out under Division 3 of Part 3 of that Schedule; or

(b) if, under Part 2 of Schedule 2, the market value approach is the valuation approach for the interest, in a petroleum project, to which the asset relates—the market value of the asset, worked out under Division 3 of Part 3 of that Schedule.

6 Section 31

Before “For the purposes of”, insert “(1)”.

7 At the end of section 31

Add:

(2) Despite paragraph (1)(h), an assessable receipt that is an assessable receipt because of clause 21 of Schedule 2 may be derived at any time, including a time before the project commences or after the project ceases.

8 Before paragraph 32(g)

Insert:

(fb) acquired exploration expenditure;

(fc) starting base expenditure;

9 Subsection 34A(5) (at the end of the definition of class 2 general project expenditure)

Add “(other than acquired exploration expenditure or starting base expenditure)”.

10 Before section 36

Insert:

35D Acquired exploration expenditure

(1) For the purposes of this Act, a reference to the acquired exploration expenditure incurred by a person in a financial year in relation to a petroleum project (not being a combined project) is a reference to:

(a) in relation to the financial year commencing on 1 July 2009—the person’s acquired exploration expenditure amount in relation to the project, under clause 19 of Schedule 2; or

(b) in relation to any subsequent financial year—any amount that is taken by subsection (3) or (4) or Division 5 to be acquired exploration expenditure incurred by the person in relation to the project in the financial year.

(2) For the purposes of this Act, a reference to the acquired exploration expenditure incurred by a person in a financial year in relation to a combined project is a reference to:

(a) any amount that is taken by subsection (3) or (4) or Division 5 to be acquired exploration expenditure incurred by the person in relation to the project in the financial year; or

(b) if the project combination certificate in relation to the project came into force in the financial year:

(i) any amount of acquired exploration expenditure; or

(ii) any amount that is taken by subsection (3) or (4) or Division 5 to be acquired exploration expenditure;

incurred by the person in relation to the pre‑combination projects in relation to the project in the financial year.

(3) For the purposes of subsection (1) or (2), if:

(a) the sum of:

(i) the class 1 augmented bond rate general expenditure; and

(ii) the class 1 augmented bond rate exploration expenditure; and

(iii) the class 2 augmented bond rate general expenditure; and

(iv) the class 1 GDP factor expenditure; and

(v) the class 2 augmented bond rate exploration expenditure; and

(vi) the class 2 GDP factor expenditure; and

(vii) the resource tax expenditure; and

(viii) the acquired exploration expenditure;

incurred by a person in a financial year (the assessable year) in relation to the petroleum project exceeds the assessable receipts derived by the person in the assessable year in relation to the project; and

(b) the next financial year starts not later than 5 years after 2 May 2010;

the person is taken to incur, in relation to the project and on the first day of the next financial year, an amount of acquired exploration expenditure worked out in accordance with the formula:

where:

augmented bond rate means the long term bond rate in relation to the assessable year plus 1.15.

available excess means so much of the excess as does not exceed the acquired exploration expenditure incurred in the assessable year.

(4) For the purposes of subsection (1) or (2), if:

(a) the sum of:

(i) the class 1 augmented bond rate general expenditure; and

(ii) the class 1 augmented bond rate exploration expenditure; and

(iii) the class 2 augmented bond rate general expenditure; and

(iv) the class 1 GDP factor expenditure; and

(v) the class 2 augmented bond rate exploration expenditure; and

(vi) the class 2 GDP factor expenditure; and

(vii) the resource tax expenditure; and

(viii) the acquired exploration expenditure;

incurred by a person in a financial year (the assessable year) in relation to the petroleum project exceeds the assessable receipts derived by the person in the assessable year in relation to the project; and

(b) the next financial year starts later than 5 years after 2 May 2010;

the person is taken to incur, in relation to the project and on the first day of the next financial year, an amount of acquired exploration expenditure worked out in accordance with the formula:

where:

augmented bond rate means the long term bond rate in relation to the assessable year plus 1.05.

available excess means so much of the excess as does not exceed the acquired exploration expenditure incurred in the assessable year.

(1) For the purposes of this Act, a reference to the starting base expenditure incurred by a person in a financial year in relation to a petroleum project (not being a combined project) is a reference to:

(a) in relation to the starting base financial year for the project:

(i) if the look‑back approach is not the valuation approach for the person’s interest in the project under Part 2 of Schedule 2—the person’s starting base amount in relation to the interest; or

(ii) if subparagraph (i) does not apply—an amount included in the person’s starting base expenditure in relation to the project under clause 18 of Schedule 2; or

(b) in relation to any subsequent financial year—any amount that is taken by subsection (3) or Division 5 to be starting base expenditure incurred by the person in relation to the project in the financial year.

Note: For starting base amounts, see Division 1 of Part 3 of Schedule 2.

(2) For the purposes of this Act, a reference to the starting base expenditure incurred by a person in a financial year in relation to a combined project is a reference to:

(a) any amount that is taken by subsection (3) or Division 5 to be starting base expenditure incurred by the person in relation to the project in the financial year; or

(b) if the project combination certificate in relation to the project came into force in the financial year:

(i) any amount of starting base expenditure; or

(ii) any amount that is taken by subsection (3) or Division 5 to be starting base expenditure;

incurred by the person in relation to the pre‑combination projects in relation to the project in the financial year.

(3) For the purposes of subsection (1) or (2), if the sum of:

(a) the class 1 augmented bond rate general expenditure; and

(b) the class 1 augmented bond rate exploration expenditure; and

(c) the class 2 augmented bond rate general expenditure; and

(d) the class 1 GDP factor expenditure; and

(e) the class 2 augmented bond rate exploration expenditure; and

(f) the class 2 GDP factor expenditure; and

(g) the resource tax expenditure; and

(h) the acquired exploration expenditure; and

(i) the starting base expenditure;

incurred by a person in a financial year (the assessable year) in relation to the petroleum project exceeds the assessable receipts derived by the person in the assessable year in relation to the project, the person is taken to incur, in relation to the project and on the first day of the next financial year, an amount of starting base expenditure worked out in accordance with the formula:

where:

augmented bond rate means the long term bond rate in relation to the assessable year plus 1.05.

available excess means so much of the excess as does not exceed the starting base expenditure incurred in the assessable year.

(4) The reference in paragraph (1)(a) to the starting base financial year for a petroleum project is a reference to:

(a) if the look‑back approach is not the valuation approach for the person’s interest in the project under Part 2 of Schedule 2—the earliest financial year, after 30 June 2012, in which a production licence relating to the project is in existence; or

(b) if paragraph (a) of this subsection does not apply—the financial year commencing on 1 July 2009.

11 Section 45

Repeal the section, substitute:

45 Time of incurring of expenditure

Petroleum projects generally

(1) For the purposes of this Act, eligible real expenditure may be incurred by a person in relation to a petroleum project (other than an onshore petroleum project, the Bass Strait project or the North West Shelf project) at any time, including a time:

(a) before the project commences or after the project ceases; or

(b) before the commencement of this Act.

Onshore petroleum projects

(2) For the purposes of this Act, eligible real expenditure may be incurred by a person in relation to an onshore petroleum project:

(a) if the project, or the exploration permit or retention lease from which the production licence to which the project relates is derived, came into existence before 2 May 2010—at any time on or after the starting base day under subsection (5) for the person’s interest in the project, including a time before the project commences or after the project ceases; or

(b) if the project, or the exploration permit or retention lease from which the production licence to which the project relates is derived, came into existence on or after 2 May 2010—at any time on or after 2 May 2010, including a time before the project commences or after the project ceases.

The Bass Strait project

(3) For the purposes of this Act, eligible real expenditure may be incurred by a person in relation to the Bass Strait project at any time on or after 1 July 1990, including a time after the project ceases.

The North West Shelf project

(4) For the purposes of this Act, eligible real expenditure may be incurred by a person in relation to the North West Shelf project at any time on or after the starting base day under subsection (5) for the person’s interest in the project, including a time after the project ceases.

Starting base days

(5) For the purposes of paragraph (2)(a) or subsection (4), the starting base day for a person’s interest in an onshore petroleum project, or in the North West Shelf project, is:

Starting base days | ||

Item | If ... | The starting base day is ... |

1 | the look‑back approach is not the valuation approach for the interest that the person holds in the project | 1 July 2012 |

2 | (a) the look‑back approach is the valuation approach for the interest; and (b) the person who held the interest at the start of 2 May 2010 had first acquired the interest, or (being a company) had been acquired, on or after 1 July 2007 | the day on which that acquisition occurred |

3 | (a) the look‑back approach is the valuation approach for the interest; and (b) item 2 does not apply | 1 July 2002 |

Note: Eligible real expenditure incurred before 1 July 2012 in relation to an onshore petroleum project that came into existence before 2 May 2010, or in relation to the North West Shelf project, is taken into account in a person’s starting base amount under Schedule 2, if the look‑back approach does not apply to the person’s interest in the project.

(6) For the purposes of subsection (5), a person holding an interest in an onshore petroleum project or the North West Shelf project is taken:

(a) to have acquired the interest if, and when, the person is taken to have acquired that interest for the purposes of clause 18 of Schedule 2; and

(b) (not being an individual) to have been acquired if, and when, the person is taken to have been acquired for the purposes of that clause.

Resource tax expenditure

(7) Despite subsections (1), (2), (3) and (4), resource tax expenditure cannot be incurred by a person, in relation to a petroleum project, before 1 July 2012.

12 After subparagraph 48(1)(a)(ia)

Insert:

(ib) if section 35E does not apply in relation to the financial year in which the transaction is or was entered into, and the look‑back approach is not the valuation approach for vendor’s interest in the project under Part 2 of Schedule 2—to have incurred starting base expenditure, in relation to the project, of the starting base amount in relation to the vendor’s interest; and

13 After subsection 48(2)

Insert:

(2A) Expenditure that the purchaser, or a purchaser, is taken to have incurred by subparagraph (1)(a)(ib) is taken to have been so incurred in the first financial year in relation to which section 35E applies in relation to the project.

14 After paragraph 48A(5)(c)

Insert:

(ca) if:

(i) section 35E does not apply in relation to the transfer year; and

(ii) the look‑back approach is not the valuation approach for vendor’s interest in the project under Part 2 of Schedule 2;

to have incurred starting base expenditure, in relation to the project, of the transfer percentage of the starting base amount in relation to the vendor’s interest; and

15 After subsection 48A(7)

Insert:

Time when purchaser taken to have incurred expenditure to which paragraph (5)(ca) applies

(7A) Expenditure that the purchaser, or any of the purchasers, is taken by paragraph (5)(ca) to have incurred is taken to have been so incurred in the first financial year in relation to which section 35E applies in relation to the project.

16 At the end of the Act

Add:

Schedule 2—Starting base for onshore petroleum projects and the North West Shelf project

Note: See sections 35D and 35E.

The object of this Schedule is to recognise the value, when resource tax reforms were announced on 2 May 2010, of:

(a) onshore petroleum projects; and

(b) the North West Shelf project;

by allowing certain amounts to be included in the deductible expenditure for the projects.

In this Schedule:

accounting standard has the same meaning as in the Corporations Act 2001.

arrangement has the meaning given by subsection 995‑1(1) of the Income Tax Assessment Act 1997.

auditing standard has the same meaning as in the Corporations Act 2001.

CGT asset has the meaning given by subsection 995‑1(1) of the Income Tax Assessment Act 1997.

cost base has the meaning given by subsection 995‑1(1) of the Income Tax Assessment Act 1997.

depreciating asset has the meaning given by subsection 995‑1(1) of the Income Tax Assessment Act 1997.

entity has the meaning given by subsection 995‑1(1) of the Income Tax Assessment Act 1997.

hold, in relation to a starting base asset, has the meaning given by clause 11.

interim expenditure, in relation to a person’s starting base asset relating to a petroleum project, has the meaning given by clause 15.

market value has a meaning affected by Subdivision 960‑S of the Income Tax Assessment Act 1997.

mining, quarrying or prospecting information has the meaning given by subsection 995‑1(1) of the Income Tax Assessment Act 1997.

project activity: a thing done is a project activity in relation to a petroleum project if it is done in carrying on or providing the operations, facilities and other things (including services and amenities) of a kind referred to in section 37 or 38 in relation to the project.

starting base return means a return of the kind referred to in clause 22, that complies with all the requirements of that clause and section 388‑75 in Schedule 1 to the Taxation Administration Act 1953.

Part 2—Choosing a valuation approach

3 Choosing a valuation approach

(1) A person may choose the valuation approach for:

(a) an interest that, on 30 June 2013, the person holds in an onshore petroleum project or the North West Shelf project; or

(b) an interest that the person may in the future hold in such a project, if the project:

(i) does not exist at the time the person makes the choice; and

(ii) would, if it later came into existence, be derived from an exploration permit or retention lease in which the person held an interest at that time.

(2) The choice is not valid unless the person gives to the Commissioner a valid starting base return.

(3) The choice must specify whether the person has chosen:

(a) the book value approach; or

(b) the market value approach; or

(c) the look‑back approach.

Note 1: The book value approach and the market value approach affect a person’s starting base amount under Part 3, through the valuation of starting base assets under Division 3 of that Part and the way in which interim expenditure is taken into account under Division 4 of that Part.

Note 2: There is no starting base amount if the look‑back approach applies, but expenditure incurred before 1 July 2012 may be eligible real expenditure: see subsections 45(2), (4) and (5).

(4) The choice is irrevocable after:

(a) 30 August 2013; or

(b) if, under paragraph 22(2)(c), the Commissioner allows further time for the person to give a starting base return—after that time elapses.

(5) The choice applies to:

(a) the year of tax commencing on 1 July 2012; and

(b) all later years of tax.

Note: Making a choice obliges the person to give to the Commissioner a starting base return under clause 22.

4 Restriction on specifying the book value approach

(1) The choice cannot specify the book value approach unless:

(a) during the 18 months preceding 2 May 2010, a person who held in that period:

(i) the interest in the onshore petroleum project or the North West Shelf project; or

(ii) if that interest did not exist in that period—an interest in the exploration permit or retention lease mentioned in subparagraph 3(1)(b)(ii);

prepared a financial report relating to the interest in accordance with accounting standards; and

(b) the report relates to a financial period that ended in the 18 months preceding 2 May 2010; and

(c) the report has been audited in accordance with auditing standards.

(2) If, during the 18 months preceding 2 May 2010, the person was a part of a consolidated entity (within the meaning of the Corporations Act 2001), for the purposes of paragraph (1)(a), treat any financial report for the consolidated entity, relating to the interest, as a report that the person prepared.

5 The valuation approach for starting base assets

The valuation approach for an interest in an onshore petroleum project or the North West Shelf project is the approach specified in a choice under clause 3 relating to:

(a) the interest; or

(b) an interest in an exploration permit or retention lease from which the interest is derived.

Division 1—Starting base amounts

6 When a person has a starting base amount

A person has a starting base amount in relation to an interest in a petroleum project if:

(a) the project is an onshore petroleum project or is the North West Shelf project; and

(b) the person holds the interest; and

(c) either:

(i) the production licence relating to the project existed at the start of 1 July 2012; or

(ii) there existed at that time an exploration permit, or a retention lease, from which is derived the production licence to which the project relates; and

(d) the look‑back approach is not the valuation approach for the interest under Part 2; and

(e) there are one or more starting base assets relating to the interest.

Note: In order for a starting base asset to relate to an interest in a petroleum project, the production licence relating to the project, or the retention lease or exploration permit from which it is derived, must have existed just before 2 May 2010: see clause 10.

7 The amount of the starting base amount

(1) If, under Part 2, the book value approach is the valuation approach for an interest in an onshore petroleum project or the North West Shelf project, the amount of the starting base amount relating to the interest is the sum of:

(a) the book values, worked out under Division 3, of all the starting base assets, relating to the interest, to which subclause (3) applies; and

(b) the adjusted interim expenditure amounts relating to the interest, worked out under clause 16.

(2) If, under Part 2, the market value approach is the valuation approach for an interest in an onshore petroleum project or the North West Shelf project, the amount of the starting base amount relating to the interest is the sum of:

(a) unless clause 8 applies—the market values, worked out under Division 3, of all the starting base assets, relating to the interest, to which subclause (3) applies; and

(b) if clause 8 applies—the amount worked out under subclause 8(2); and

(c) the amounts of interim expenditure incurred in relation to the interest.

(3) This subclause applies to a starting base asset if, at all times between 2 May 2010 and 30 June 2012, the person holding the asset simultaneously held:

(a) the interest in the project; or

(b) if, for some or all of that period, the project did not exist—an interest in a retention lease, or in an exploration permit, from which the project is derived.

Note: This subsection allows for a transfer of the starting base asset between 2 May 2010 and 30 June 2012, if it matches a transfer of the interest.

8 Alternative valuation method for coal seam gas projects

(1) This clause applies if:

(a) under Part 2, the market value approach is the valuation approach for an interest in an onshore petroleum project; and

(b) the project includes a known reserve of coal seam gas; and

(c) either:

(i) the interest, or another interest in the project, was acquired, by any person, between 1 July 2007 and 2 May 2010; or

(ii) a company that held the interest, or another interest in the project, was acquired, by any person, between 1 July 2007 and 2 May 2010; and

(d) the person who chose the market value approach in relation to the interest (the interest holder) chooses under subclause (4) of this clause to apply the alternative valuation method for coal seam gas projects.

(2) For the purposes of paragraph 7(2)(b), the amount worked out under this subclause is:

where:

estimated reserves is:

(a) if paragraph (b) does not apply—the most recent approved estimate, made before 2 May 2010, of the proved, probable and possible reserves of coal seam gas for the project, expressed in gigajoules; or

(b) if the interest holder does not hold the entire interest in the project—the portion of that estimate, expressed in gigajoules, of those reserves that reflects the interest holder’s interest in the project.

production since estimate is:

(a) if paragraph (b) does not apply—the amount of coal seam gas produced from the project, expressed in gigajoules, between the day on which that approved estimate was made and 2 May 2010; or

(b) if the interest holder does not hold the entire interest in the project—the portion of that production, expressed in gigajoules, that reflects the interest holder’s interest in the project.

(3) To be an approved estimate for the purposes of subclause (2), an estimate of the proved, probable and possible reserves of coal seam gas for the project must have been:

(a) determined in accordance with the requirements of the document known as the Petroleum Resources Management System, issued by the Society of Petroleum Engineers, as in force at the time the estimate was made; and

(b) independently certified as being determined in accordance with the requirements of that document as so in force.

(4) The interest holder may choose to apply the alternative valuation method for coal seam gas projects.

(5) The choice is not valid unless the interest holder gives it to the Commissioner:

(a) in the approved form; and

(b) on or before 30 August 2013, or within a further time that the Commissioner allows.

(6) The choice is irrevocable, and applies to:

(a) the year of tax commencing on 1 July 2012; and

(b) all later years of tax.

(7) For the purposes of paragraph (1)(c):

(a) a person holding an interest in the project is taken to have acquired the interest if, and when, the person is taken to have acquired that interest for the purposes of clause 18; and

(b) a company holding an interest in the project is taken to have been acquired if, and when, the company is taken to have been acquired for the purposes of that clause.

9 Reducing the starting base amount

(1) Despite clause 7, a starting base amount under that clause is reduced by the sum of all the reductions (if any) required by subclauses (2) and (3) of this clause in relation to any starting base assets to which the starting base amount relates.

Use etc. that is not related to project activities

(2) Reduce the starting base amount to the extent (if any) that the amount relates to a starting base asset that, during the starting base period relating to the asset, was used, or being constructed for use, for a purpose other than carrying on project activities relating to the petroleum project.

Use etc. that equates to excluded expenditure

(3) Reduce the starting base amount (or, if that amount is reduced under subclause (2), that amount as so reduced) to the extent (if any) that the amount:

(a) relates to a starting base asset that, during the starting base period relating to the asset, was used, or being constructed for use, for carrying on project activities relating to the petroleum project; but

(b) would have been excluded expenditure if it had been an amount of expenditure that the person holding the interest in the project incurred.

(4) However, subclause (3) does not apply if:

(a) under Part 2, the market value approach is the valuation approach for the person’s starting base assets relating to the petroleum project; and

(b) the amount would have been excluded expenditure only because of paragraph 44(e), (f) or (g).

Note: Subclause (4) ensures that a starting base amount in relation to an interest in a petroleum project is not reduced under the market value approach.

Starting base period

(5) The starting base period in relation to a starting base asset is a period, between 2 May 2010 and 1 July 2012:

(a) during which a person held both the asset and the interest in the project; and

(b) during which the asset was, for any purpose, used or being constructed for use.

Division 2—Starting base assets

10 Meaning of starting base asset

(1) Property, or a legal or equitable right that is not property, is a starting base asset relating to an interest in an onshore petroleum project or the North West Shelf project if:

(a) either of the following existed just before 2 May 2010:

(i) the production licence relating to the project, or (if the project is a combined project) a pre‑combination project in relation to the project;

(ii) a retention lease, or exploration permit, from which the project (or pre‑combination project) is derived; and

(b) on 2 May 2010, the property or right was used, or being constructed for use, in carrying on project activities relating to the project (or pre‑combination project); and

(c) the look‑back approach is not the valuation approach for the interest under Part 2.

(2) Despite subclause (1):

(a) if, under Part 2, the book value approach is the valuation approach for the interest in the petroleum project, the following are not starting base assets:

(i) rights and interests constituting the petroleum project;

(ii) mining, quarrying or prospecting information, or rights to such information;

(iii) goodwill; and

(b) property, or a legal or equitable right, is not, and is taken never to have been, a starting base asset if:

(i) a valid choice has not been made under section 3 specifying the valuation approach for the interest; or

(ii) a valid starting base return that covers the property or right has not been given to the Commissioner.

(3) If, under Part 2, the market value approach is the valuation approach for the person’s starting base assets relating to the interest in the petroleum project, treat:

(a) any mining, quarrying or prospecting information; or

(b) any rights to such information;

as property, or a legal or equitable right, for the purposes of subsection (1).

(4) Despite subsection (1), something that has already become a starting base asset relating to an interest in a petroleum project derived from a particular retention lease or exploration permit cannot become a starting base asset relating to an interest in another petroleum project derived from that lease or permit.

(5) This Schedule applies to any improvement to, or any fixture on, land as if it were an asset separate from the land, whether the improvement or fixture is removable or not.

11 Holding a starting base asset

(1) A person holds a starting base asset relating to an onshore petroleum project or the North West Shelf project if:

(a) the asset is a depreciating asset that the person holds (within the meaning of section 40‑40 of the Income Tax Assessment Act 1997); or

(b) the person would hold the asset (within the meaning of that section) if it were a depreciating asset.

(2) However, a person who is entitled to the interest in a petroleum project is taken to hold the rights and interests constituting the interest in the project.

Division 3—Valuation of starting base assets

12 The book value of a starting base asset

(1) If, under Part 2, the book value approach is the valuation approach for an interest in an onshore petroleum project or the North West Shelf project, the book value of a starting base asset relating to the interest is the book value under subclause (2) or (3).

(2) If:

(a) the value of the asset is recorded in the accounts from which the most recent audited financial report before 2 May 2010 was prepared; and

(b) the financial report relates to a financial period that ended in the 18 months preceding that day;

the book value of the asset is as follows:

where:

accepted value is:

(a) the value recorded in those accounts, unless paragraph (b) applies; or

(b) if that value is inconsistent with an auditor’s report on the financial report—a value that is consistent with the auditor’s report.

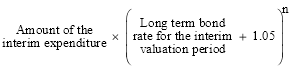

long term bond rate for the valuation period is the long term bond rate for the valuation period under subclause (4).

n is the number of days in that valuation period, divided by 365.

(3) However, the initial book value of the asset is zero if the value of the asset is not recorded as mentioned in subclause (2).

(4) The valuation period for the asset is the period:

(a) starting:

(i) on the day the financial report mentioned in paragraph (2)(a) was prepared, unless subparagraph (ii) of this paragraph applies; or

(ii) if the value of the asset recorded in the accounts from which the financial report was produced is inconsistent with an auditor’s report on the financial report—on the day of the auditor’s report; and

(b) ending at the end of 30 June 2012.

13 The market value of a starting base asset

(1) If, under Part 2, the market value approach is the valuation approach for an interest in an onshore petroleum project or the North West Shelf project, the market value of a starting base asset relating to the interest is the market value of the asset on 1 May 2010.

(2) However, if the asset is a right or interest constituting the interest in the project, in working out its market value for the purposes of this section, disregard any liability of the person to make any payments, of a kind known as private override royalty payments, relating to:

(a) petroleum recovered from:

(i) the production licence area in relation to the project; or

(ii) an exploration permit area for an exploration permit from which the production licence to which the project relates is derived; or

(iii) a retention lease area for a retention lease from which the production licence to which the project relates is derived; or

(b) marketable petroleum commodities produced from such petroleum.

14 Partial disposal of a starting base asset before 1 July 2012

(1) The book value under clause 12, or the market value under clause 13, of a starting base asset relating to an interest that a person holds in an onshore petroleum project or the North West Shelf project is reduced to the extent (if any) that any of the person’s interest in the asset is disposed of during the period:

(a) starting on the day provided under subclause (2); and

(b) ending at the end of 30 June 2012.

(2) The period starts:

(a) if, under Part 2, the book value approach is the valuation approach for the interest:

(i) on the day of the financial report (if any) mentioned in paragraph 12(2)(a) of this Schedule in relation to the accounts in which the value of the asset is recorded; or

(ii) if subparagraph (i) of this paragraph does not apply—on 2 May 2010; or

(b) if, under Part 2, the market value approach is the valuation approach for the interest—on 2 May 2010.

(3) Treat, for the purposes of this clause, as a disposal of part of the person’s interest in the starting base asset an arrangement that has the effect of transferring to another person part of the benefits or entitlements that the person has in relation to the asset.

Division 4—Interim expenditure

15 Meaning of interim expenditure

(1) An amount of expenditure that a person incurs relating to an interest in an onshore petroleum project or the North West Shelf project is interim expenditure relating to the interest to the extent that:

(a) the amount:

(i) relates to a depreciating asset that is used, or being constructed for use, on 1 July 2012 in carrying on project activities relating to the project; and

(ii) is included in the cost of the asset under Subdivision 40‑C of the Income Tax Assessment Act 1997; and

(iii) was incurred during the period starting on the day provided under subclause (3) or (4) and ending at the end of 30 June 2012; or

(b) the amount:

(i) relates to a CGT asset that is not a depreciating asset and that is used, or being constructed for use, on 1 July 2012 in carrying on project activities relating to the project; and

(ii) is included in the cost base of the asset; and

(iii) was incurred during the period starting on the day provided under subclause (3) or (4) and ending at the end of 30 June 2012; or

(c) the amount:

(i) is mining capital expenditure (within the meaning of the Income Tax Assessment Act 1997) relating to project activities relating to the project; and

(ii) was incurred between 2 May 2010 and 30 June 2012.

(2) However, if the asset is a CGT asset (but not a depreciating asset), treat the amount of the interim expenditure as not including any part of the amount that consists of the third element of the cost base under subsection 110‑25(4) of the Income Tax Assessment Act 1997.

Start of the expenditure period

(3) If, under Part 2, the book value approach is the valuation approach for the interest in the petroleum project, the period starts:

(a) if subclause (5) applies to the asset:

(i) on the day of the financial report (if any) mentioned in paragraph 12(2)(a) of this Schedule in relation to the accounts in which the value of the asset is recorded; or

(ii) if subparagraph (i) of this paragraph does not apply—on 2 May 2010; or

(b) otherwise—on the first day, before the end of 30 June 2012, from which the person held the asset at all times until the end of 30 June 2012.

Example: The person bought an asset on 1 January 2011 and sold it on 1 May 2011. The person bought the asset again on 1 June 2011 and still held it at the end of 30 June 2012.

The expenditure incurred in buying the asset the first time (on 1 January 2011) is not interim expenditure, because the person did not hold the asset until the end of 30 June 2012, as required by paragraph (3)(b).

The expenditure incurred in buying the asset the second time (on 1 June 2011) is interim expenditure (if it is covered by paragraph (1)(a)), because the person held the asset until the end of 30 June 2012.

(4) If, under Part 2, the market value approach is the valuation approach for the interest in the petroleum project, the period starts:

(a) if subclause (5) applies to the asset—on 2 May 2010; or

(b) otherwise—on the first day, before the end of 30 June 2012, from which the person held the asset at all times until the end of 30 June 2012.

(5) This subclause applies to an asset if, at all times between 2 May 2010 and 30 June 2012, the person holding the asset simultaneously held:

(a) the interest in the project; or

(b) if, for some or all of that period, the project did not exist—an interest in a retention lease, or in an exploration permit, from which the project is derived.

(6) For the purposes of subclauses (3) to (5), an amount of expenditure to which paragraph (1)(c) applies is taken to be an asset that the person incurring the expenditure holds from the day the expenditure was incurred until the day on which the person ceases to hold the interest in the project.

Excluded expenditure

(7) Despite subclause (1), the amount is not interim expenditure to the extent (if any) that the amount would have been excluded expenditure if it had been incurred after 1 July 2012.

16 Adjusted interim expenditure amounts

(1) If:

(a) under Part 2, the book value approach is the valuation approach for an interest in an onshore petroleum project or the North West Shelf project; and

(b) a person holding an interest in the project incurred an amount of interim expenditure relating to the interest;

there is an adjusted interim expenditure amount relating to the interest.

(2) The adjusted interim expenditure amount is as follows:

where:

long term bond rate for the interim valuation period is the long term bond rate for the interim valuation period under subclause (3).

n is the number of days in the interim valuation period, divided by 365.

(3) The interim valuation period for an amount of interim expenditure is the period:

(a) starting on the day on which the person holding the interest in the petroleum project incurred the amount; and

(b) ending at the end of 30 June 2012.

17 Partial disposal of an asset before 1 July 2012

(1) If:

(a) a person incurs interim expenditure relating to an interest that a person holds in an onshore petroleum project or the North West Shelf project; and

(b) the interim expenditure relates to a depreciating asset or a CGT asset; and

(c) any of the person’s interest in the asset is disposed of between 2 May 2010 and 1 July 2012;

the amount of the interim expenditure is taken to be reduced to the extent the person’s interest in the asset is disposed of.

(2) Treat, for the purposes of this clause, as a disposal of part of the person’s interest in the asset an arrangement that has the effect of transferring to another person part of the benefits or entitlements that the person has in relation to the asset.

Note: Section 45 deals generally with when eligible real expenditure may be incurred in relation to onshore petroleum projects and the North West shelf project, including under the look‑back approach. This Part deals with some specific issues under the look‑back approach, in particular issues relating to the costs of acquiring projects.

18 Expenditure incurred in acquiring interests in petroleum projects

Interests acquired between 1 July 2007 and 2 May 2010

(1) If:

(a) under Part 2, the look‑back approach is the valuation approach for an interest in an onshore petroleum project or the North West Shelf project; and

(b) during the period between 1 July 2007 and 2 May 2010, either or both of the following events occurred:

(i) a person acquired the interest;

(ii) if the person holding the interest is a company—the person was acquired by another company;

the starting base expenditure, incurred by the person referred to in paragraph (b) in relation to the last such event to occur in relation to the interest during that period, includes the expenditure (acquisition expenditure) referred to in subsection (2).

(2) The acquisition expenditure is whichever of the following is applicable:

(a) the expenditure incurred by the person in acquiring the interest;

(b) the expenditure incurred by the other company in making the acquisition.

(3) Despite subclause (1), the starting base expenditure incurred by the person in relation to the project does not include acquisition expenditure to the extent (if any) that the acquisition expenditure reflects the value of things that are not project activities relating to the project.

(4) Despite subclause (1), the starting base expenditure incurred by the person in relation to the project does not include acquisition expenditure to the extent that the expenditure relates to an acquired exploration expenditure amount.

(5) Acquisition expenditure included under subclause (1) in the starting base expenditure incurred by the person is taken, for the purposes of this Act, to have been incurred on 2 May 2010.

Interests acquired before 30 June 2007