Tax and Superannuation Laws Amendment (2013 Measures No. 2) Act 2013

No. 85, 2013

An Act to amend the law relating to taxation and superannuation, and for related purposes

Tax and Superannuation Laws Amendment (2013 Measures No. 2) Act 2013

No. 85, 2013

An Act to amend the law relating to taxation and superannuation, and for related purposes

Contents

2 Commencement

3 Schedule(s)

4 Amendment of assessments

Schedule 1—Definition of documentary

Income Tax Assessment Act 1997

Schedule 2—Ex‑gratia payments for natural disasters

Part 1—Amendments commencing on Royal Assent

Income Tax Assessment Act 1997

Tax Laws Amendment (2011 Measures No. 1) Act 2011

Tax Laws Amendment (2012 Measures No. 1) Act 2012

Part 2—Sunsetting

Division 1—Repeal on 1 July 2016

Income Tax Assessment Act 1997

Division 2—Repeal on 1 July 2017

Income Tax Assessment Act 1997

Schedule 3—GST instalment system

A New Tax System (Goods and Services Tax) Act 1999

Schedule 4—Deductible gift recipients

Part 1—Amendments commencing on Royal Assent

Income Tax Assessment Act 1997

Part 2—Sunsetting

Division 1—Repeal on 1 July 2019

Income Tax Assessment Act 1997

Division 2—Repeal on 1 July 2023

Income Tax Assessment Act 1997

Schedule 5—Merging multiple accounts in a superannuation entity

Superannuation Industry (Supervision) Act 1993

Schedule 6—Government co‑contribution for low income earners

Superannuation (Government Co‑contribution for Low Income Earners) Act 2003

Schedule 7—Consolidating the dependency tax offsets

Part 1—Main amendments

Income Tax Assessment Act 1997

Part 2—Other amendments

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Part 3—Application of amendments

Schedule 8—Taxation of financial arrangements

Part 1—Core rules

Division 1—Attribution of costs

Income Tax Assessment Act 1997

Division 2—Interest

Income Tax Assessment Act 1997

Division 3—Consistency in working out gains or losses

Income Tax Assessment Act 1997

Part 2—Accruals/realisation methods

Division 1—Sufficiently certain particular gains or losses

Income Tax Assessment Act 1997

Division 2—Precedence of particular gains or losses

Income Tax Assessment Act 1997

Division 3—Spreading prepayments

Income Tax Assessment Act 1997

Division 4—Spreading single payment

Income Tax Assessment Act 1997

Division 5—Re‑estimations

Income Tax Assessment Act 1997

Division 6—Impairments and reversals

Income Tax Assessment Act 1997

Division 7—Running balancing adjustments

Income Tax Assessment Act 1997

Division 8—Ceasing of rights or obligations

Income Tax Assessment Act 1997

Part 3—Fair value method

Income Tax Assessment Act 1997

Part 4—Hedging financial arrangements method

Division 1—One in all in principle

Income Tax Assessment Act 1997

Division 2—Hedging net investments in foreign operations

Income Tax Assessment Act 1997

Part 5—Transitional balancing adjustments

Tax Laws Amendment (Taxation of Financial Arrangements) Act 2009

Part 6—Elective requirements

Income Tax Assessment Act 1997

Part 7—Miscellaneous amendments

Division 1—Consistency of language

Income Tax Assessment Act 1997

Division 2—Other amendments

Income Tax Assessment Act 1997

Tax and Superannuation Laws Amendment (2013 Measures No. 2) Act 2013

No. 85, 2013

An Act to amend the law relating to taxation and superannuation, and for related purposes

[Assented to 28 June 2013]

The Parliament of Australia enacts:

This Act may be cited as the Tax and Superannuation Laws Amendment (2013 Measures No. 2) Act 2013.

(1) Each provision of this Act specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information | ||

Column 1 | Column 2 | Column 3 |

Provision(s) | Commencement | Date/Details |

1. Sections 1 to 4 and anything in this Act not elsewhere covered by this table | The day this Act receives the Royal Assent. | 28 June 2013 |

The day this Act receives the Royal Assent. | 28 June 2013 | |

3. Schedule 2, Part 1 | The day this Act receives the Royal Assent. | 28 June 2013 |

4. Schedule 2, Part 2, Division 1 | 1 July 2016. | 1 July 2016 |

5. Schedule 2, Part 2, Division 2 | 1 July 2017. | 1 July 2017 |

6. Schedule 3 | The day this Act receives the Royal Assent. | 28 June 2013 |

7. Schedule 4, Part 1 | The day this Act receives the Royal Assent. | 28 June 2013 |

8. Schedule 4, Part 2, Division 1 | 1 July 2019. | 1 July 2019 |

9. Schedule 4, Part 2, Division 2 | 1 July 2023. | 1 July 2023 |

10. Schedules 5 to 7 | The day this Act receives the Royal Assent. | 28 June 2013 |

11. Schedule 8 | Immediately after the commencement of item 1 of Schedule 3 to the Tax Laws Amendment (2010 Measures No. 4) Act 2010. | 26 March 2009 |

Note: This table relates only to the provisions of this Act as originally enacted. It will not be amended to deal with any later amendments of this Act.

(2) Any information in column 3 of the table is not part of this Act. Information may be inserted in this column, or information in it may be edited, in any published version of this Act.

Each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

Section 170 of the Income Tax Assessment Act 1936 does not prevent the amendment of an assessment if:

(a) the assessment was made on or before the day this section commences; and

(b) the amendment is made within 2 years after that day; and

(c) the amendment is made for the purpose of giving effect to Schedule 8 to this Act (Taxation of financial arrangements).

Schedule 1—Definition of documentary

Income Tax Assessment Act 1997

1 Subparagraph 376‑20(2)(c)(i)

Omit “documentary”, substitute “*documentary”.

2 Subparagraph 376‑20(2)(c)(iii)

Omit “quiz program”, substitute “quiz program, game show”.

3 After section 376‑20

Insert:

Meaning of documentary

(1) A *film is a documentary if the film is a creative treatment of actuality, having regard to:

(a) the extent and purpose of any contrived situation featured in the film; and

(b) the extent to which the film explores an idea or a theme; and

(c) the extent to which the film has an overall narrative structure; and

(d) any other relevant matters.

Exclusion of infotainment or lifestyle programs and magazine programs

(2) However, a *film is not a documentary if it is:

(a) an infotainment or lifestyle program (within the meaning of Schedule 6 to the Broadcasting Services Act 1992); or

(b) a film that:

(i) presents factual information; and

(ii) has 2 or more discrete parts, each dealing with a different subject or a different aspect of the same subject; and

(iii) does not contain an over‑arching narrative structure or thesis.

4 Subparagraph 376‑45(2)(c)(i)

Omit “documentary”, substitute “*documentary”.

5 Subparagraph 376‑45(2)(c)(iii)

Omit “quiz program”, substitute “quiz program, game show”.

6 Subparagraph 376‑65(2)(d)(ii)

Omit “quiz program”, substitute “quiz program, game show”.

7 Subparagraph 376‑65(2)(d)(iii)

Omit “documentary”, substitute “*documentary”.

8 Paragraph 376‑65(3)(c)

Omit “documentary”, substitute “*documentary”.

9 Subsection 376‑65(6) (cells at table items 2, 3, 5, 6, 7 and 8, column headed “For this type of film …”)

Omit “documentary”, substitute “*documentary”.

10 Subsection 376‑170(4A)

Omit “documentary”, substitute “*documentary”.

11 Subsection 995‑1(1)

documentary has the meaning given by section 376‑25.

12 Application of amendments

(1) The amendments made by items 1, 3, 4, 7, 8, 9, 10 and 11 apply in relation to films commencing principal photography on or after 1 July 2012.

(2) The amendments made by items 2, 5 and 6 apply in relation to films commencing principal photography on or after the day this Schedule commences.

Schedule 2—Ex‑gratia payments for natural disasters

Part 1—Amendments commencing on Royal Assent

Income Tax Assessment Act 1997

1 Section 11‑15 (table item headed “welfare”)

Omit:

Assistance for New Zealand non‑protected special category visa holders for a disaster that occurred in Australia during the 2010‑11 financial year |

|

Assistance for New Zealand non‑protected special category visa holders for the floods that occurred in New South Wales and Queensland in January, February and March 2012 |

|

Disaster Income Recovery Subsidy for the floods that occurred in Australia during the period starting on 29 November 2010, or for Cyclone Yasi |

|

substitute:

Disaster assistance for New Zealand non‑protected special category visa holders |

|

Disaster Income Recovery Subsidy............... | 51‑30 |

2 Section 51‑30 (table item 5.1C)

Repeal the item, substitute:

5.2 | an individual in receipt of an ex‑gratia payment from the Commonwealth known as assistance for New Zealand non‑protected special category visa holders for a disaster: (a) that occurred in Australia during the 2011‑12 *financial year; and (b) that the *Emergency Management Minister has declared to be a major disaster for the purposes of the Australian Government Disaster Recovery Payment | the payment | the payment must be claimed: (a) after 5 February 2012; and (b) before 1 December 2012; and the Minister must make the declaration before 1 June 2012 |

5.3 | an individual in receipt of an ex‑gratia payment from the Commonwealth known as assistance for New Zealand non‑protected special category visa holders for a disaster: (a) that occurred in Australia during the 2012‑13 *financial year; and (b) that the *Emergency Management Minister has declared to be a major disaster for the purposes of the Australian Government Disaster Recovery Payment | the payment | the payment must be claimed: (a) after 24 August 2012; and (b) before 1 January 2014; and the Minister must make the declaration before 1 July 2013 |

5.4 | an individual in receipt of an ex‑gratia payment from the Commonwealth known as Disaster Income Recovery Subsidy for the floods that occurred in Queensland during the period starting on 21 January 2013 | the payment | the payment must be claimed: (a) after 20 January 2013; and (b) before 5 August 2013 |

3 Subsection 995‑1(1)

Insert:

Emergency Management Minister means the Minister who administers the Social Security Act 1991, insofar as it relates to Australian Government Disaster Recovery Payment.

Tax Laws Amendment (2011 Measures No. 1) Act 2011

4 Item 3 of Schedule 1

Repeal the item.

Tax Laws Amendment (2012 Measures No. 1) Act 2012

5 Part 2 of Schedule 3

Repeal the Part.

Division 1—Repeal on 1 July 2016

Income Tax Assessment Act 1997

6 Section 51‑30 (table item 5.2)

Repeal the item.

Division 2—Repeal on 1 July 2017

Income Tax Assessment Act 1997

7 Section 11‑15 (table item headed “welfare”)

Omit:

Disaster assistance for New Zealand non‑protected special category visa holders |

|

Disaster Income Recovery Subsidy............... | 51‑30 |

8 Section 51‑30 (table items 5.3 and 5.4)

Repeal the items.

9 Subsection 995‑1(1) (definition of Emergency Management Minister)

Repeal the definition.

Schedule 3—GST instalment system

A New Tax System (Goods and Services Tax) Act 1999

1 Paragraph 162‑30(1)(d)

Repeal the paragraph.

2 Subsection 162‑30(6)

Repeal the subsection.

3 At the end of subsection 162‑135(1)

Add:

The amount must not be less than zero.

4 Subsection 162‑140(4) (note)

Omit “Note”, substitute “Note 1”.

5 At the end of subsection 162‑140(4)

Add:

Note 2: Your estimated annual GST amount is taken to be zero if it would otherwise be less than zero (see subsection (6)).

6 At the end of section 162‑140

Add:

(6) Your estimated annual GST amount relating to the *GST instalment quarter is zero if, apart from this subsection, this estimate would be less than zero.

7 Section 195‑1 (definition of estimated annual GST amount)

Omit “subsection 162‑140(4) and paragraph 162‑140(5)(b)”, substitute “section 162‑140”.

8 Application of amendments

The amendments made by this Schedule apply in relation to GST instalment quarters starting on or after the first 1 July that is on or after the commencement of this Schedule.

Schedule 4—Deductible gift recipients

Part 1—Amendments commencing on Royal Assent

Income Tax Assessment Act 1997

1 Subsection 30‑25(2) (at the end of the table)

Add:

2.2.42 | The Conversation Trust | the gift must be made after 21 November 2012 |

2 Subsection 30‑45(2) (at the end of the table)

Add:

4.2.42 | National Congress of Australia’s First Peoples Limited | the gift must be made after 30 June 2013 |

3 Subsection 30‑50(2) (at the end of the table)

Add:

5.2.31 | the Anzac Centenary Public Fund | the gift must be made after 30 November 2012 and before 1 May 2019 |

5.2.32 | the Australian Peacekeeping Memorial Project Incorporated | the gift must be made after 31 December 2012 and before 1 January 2015 |

5.2.33 | National Boer War Memorial Association Incorporated | the gift must be made after 31 December 2012 and before 1 January 2015 |

4 Section 30‑105 (table item 13.2.15)

Repeal the item.

5 Section 30‑105 (at the end of the table)

Add:

13.2.19 | Philanthropy Australia Inc. | the gift must be made after 27 February 2013 |

6 Section 30‑315 (after table item 4A)

Insert:

5 | Anzac Centenary Public Fund | item 5.2.31 |

7 Section 30‑315 (cell at table item 24B, column headed “Provision”)

Repeal the cell, substitute:

item 5.2.32 |

8 Section 30‑315 (after table item 37)

Insert:

38 | Conversation Trust | item 2.2.42 |

9 Section 30‑315 (after table item 73)

Insert:

73AA | National Boer War Memorial Association Incorporated | item 5.2.33 |

10 Section 30‑315 (after table item 73A)

Insert:

73B | National Congress of Australia’s First Peoples Limited | item 4.2.42 |

11 Section 30‑315 (after table item 85)

Insert:

85A | Philanthropy Australia Inc. | item 13.2.19 |

Division 1—Repeal on 1 July 2019

Income Tax Assessment Act 1997

12 Subsection 30‑50(2) (table items 5.2.32 and 5.2.33)

Repeal the items.

13 Section 30‑315 (table items 24B and 73AA)

Repeal the items.

Division 2—Repeal on 1 July 2023

Income Tax Assessment Act 1997

14 Subsection 30‑50(2) (table item 5.2.31)

Repeal the item.

15 Section 30‑315 (table item 5)

Repeal the item.

Schedule 5—Merging multiple accounts in a superannuation entity

Superannuation Industry (Supervision) Act 1993

1 Subsection 10(1)

Insert:

buy‑sell spread has the meaning given by subsection 29V(4).

2 Subsection 10(1)

Insert:

superannuation account has the meaning given by subsection 108A(3).

3 Before subsection 29E(7)

Insert:

Complying with rules relating to merging multiple accounts in a superannuation entity

(6E) The following additional condition is imposed on each RSE licence that relates to a superannuation entity for which the RSE licensee has obligations under section 108A. The condition is that the RSE licensee must ensure that the rules that that section requires in relation to the superannuation entity are complied with.

4 After section 108

Insert:

108A Trustee’s duty to identify etc. multiple superannuation accounts of members

(1) Each trustee of a superannuation entity (other than the trustee of a pooled superannuation trust or a self managed superannuation fund) must ensure that rules are established, which:

(a) set out a procedure for identifying when a member of the superannuation entity has more than one superannuation account in the superannuation entity; and

(b) require the trustee to carry out the procedure to identify such members at least once each financial year; and

(c) if the member has 2 or more superannuation accounts in the superannuation entity—require the trustee to merge the accounts so that the member has only one account balance in respect of those accounts, if the trustee reasonably believes that it is in the best interests of the member to do so; and

(d) provide that fees are not payable (other than a buy‑sell spread) for any merger of superannuation accounts that occurs as a result of paragraphs (a) to (c).

(2) The requirement in paragraph (1)(c) does not apply if:

(a) it is not practicable in the circumstances to merge the member’s superannuation accounts; or

(b) one or more of the superannuation accounts is a defined benefit interest or income stream.

(3) A superannuation account is a record of the member’s benefits, in relation to a superannuation entity in which the member has an interest, which is recorded separately:

(a) from other benefits of the member in relation to the entity (if any); and

(b) from other benefits of any other member in relation to the entity.

To avoid doubt, an FHSA (within the meaning of the First Home Saver Accounts Act 2008) is not a superannuation account.

Note: FHSA is short for first home saver account

(4) In determining, for the purpose of paragraph (1)(c), whether it is in the best interests of a member to merge his or her superannuation accounts, the trustee must consider the total amount of fees and charges payable by the member in respect of all of his or her accounts in the superannuation entity (including any fees and charges payable by the member for insurance provided in respect of all of his or her accounts).

(5) A trustee commits an offence if the trustee contravenes subsection (1). This is an offence of strict liability.

Penalty: 50 penalty units.

Note 1: Chapter 2 of the Criminal Code sets out the general principles of criminal responsibility.

Note 2: For strict liability, see section 6.1 of the Criminal Code.

5 Application of amendments

The amendments made by this Schedule apply from 1 July 2013.

Schedule 6—Government co‑contribution for low income earners

Superannuation (Government Co‑contribution for Low Income Earners) Act 2003

1 Paragraph 9(1)(c)

Omit “2009‑10 income year or a later income year”, substitute “2009‑10, 2010‑11 and 2011‑12 income years”.

2 At the end of subsection 9(1)

Add:

; and (d) for the 2012‑13 income year or a later income year—an amount equal to 50% of the sum of the eligible personal superannuation contributions the person makes during the income year.

3 Subsection 10(1B)

Omit “2009‑10 income year or a later income year”, substitute “2009‑10 income year, 2010‑11 income year or 2011‑12 income year”.

4 After subsection 10(1B)

Add:

(1C) The amount of the Government co‑contribution in respect of a person for the 2012‑13 income year or a later income year must not exceed the maximum amount worked out using the following table:

Maximum Government co‑contribution | ||

Item | Person’s total income for the income year | Maximum amount |

1 | the lower income threshold or less | $500 |

2 | more than the lower income threshold but less than the higher income threshold | $500 reduced by 3.333 cents for each dollar by which the person’s total income for the income year exceeds the lower income threshold |

5 Subsection 10(2)

Omit “and (1B)”, substitute “, (1B) and (1C)”.

6 Paragraph 10A(1)

Omit “and 2011‑12” (wherever occurring), substitute “, 2011‑12 and 2012‑13”.

7 Paragraph 10A(3)(c)

Omit “2007‑08 income year or a later income year”, substitute “2007‑08 income year or a later income year before the 2012‑13 income year”.

8 At the end of subsection 10A(3)

Add:

; or (d) for the 2012‑13 income year or a later income year—the sum of:

(i) the lower income threshold for that income year; and

(ii) $15,000.

9 Subsection 10A(5A)

Omit “and 2011‑12”, substitute “, 2011‑12 and 2012‑13”.

10 Application of amendments

The amendments made by this Schedule apply to the 2012‑13 income year and later income years.

Schedule 7—Consolidating the dependency tax offsets

Income Tax Assessment Act 1997

1 Before Subdivision 61‑G

Insert:

Subdivision 61‑A—Dependant (invalid and carer) tax offset

61‑1 What this Subdivision is about

You are entitled to a tax offset for an income year if you maintain certain dependants who are unable to work.

Table of sections

Object of this Subdivision

61‑5 Object of this Subdivision

Entitlement to the dependant (invalid and carer) tax offset

61‑10 Who is entitled to the tax offset

61‑15 Cases involving more than one spouse

61‑20 Exceeding the income limit for family tax benefit (Part B)

61‑25 Eligibility for family tax benefit (Part B) without shared care

Amount of the dependant (invalid and carer) tax offset

61‑30 Amount of the dependant (invalid and carer) tax offset

61‑35 Families with shared care percentages

61‑40 Reduced amounts of dependant (invalid and carer) tax offset

61‑45 Reductions to take account of the other individual’s income

61‑5 Object of this Subdivision

The object of this Subdivision is to provide a *tax offset to assist with the maintenance of certain types of dependants who are genuinely unable to work because of invalidity, or because of their care obligations.

Entitlement to the dependant (invalid and carer) tax offset

61‑10 Who is entitled to the tax offset

(1) You are entitled to a *tax offset for an income year if:

(a) during the year you contribute to the maintenance of another individual who:

(i) is your *spouse; or

(ii) is your *parent or your spouse’s parent; or

(iii) is aged 16 years or over, and is your *child, brother or sister or a brother or sister of your spouse; and

(b) during the year, the other individual meets the requirements of one or more of subsections (2), (3) and (4); and

(c) during the year:

(i) the other individual is an Australian resident; or

(ii) if the other individual is your spouse or your child—you had a domicile in Australia; and

(d) you are not entitled to a rebate of tax under section 159J (rebates for dependants) of the Income Tax Assessment Act 1936 in respect of the other individual for the year; and

(e) you are not entitled to a rebate of tax under section 159L (rebates for housekeepers) of the Income Tax Assessment Act 1936 in respect of the other individual for the year.

Note: To be entitled to a rebate under section 159J or 159L of the Income Tax Assessment Act 1936, you must also be entitled to either or both of the following:

(a) a rebate under section 23AB (service with an armed force under the control of the United Nations), section 79A (residents of isolated areas) or section 79B (members of Defence Force serving overseas) of that Act;

(b) a rebate under subsection 159J(2) of that Act in respect of a spouse born before 1 July 1952.

(2) The other individual meets the requirements of this subsection if he or she is being paid:

(a) a disability support pension or a special needs disability support pension under the Social Security Act 1991; or

(b) an invalidity service pension under the Veterans’ Entitlements Act 1986.

(3) The other individual meets the requirements of this subsection if he or she:

(a) is your *spouse or parent, or your spouse’s parent; and

(b) is being paid a carer allowance or carer payment under the Social Security Act 1991 in relation to provision of care to a person who:

(i) is your *child, brother or sister, or the brother or sister of your spouse; and

(ii) is aged 16 years or over.

(4) The other individual meets the requirements of this subsection if he or she is your *spouse or parent, or your spouse’s parent, and is wholly engaged in providing care to an individual who:

(a) is your *child, brother or sister, or the brother or sister of your spouse; and

(b) is aged 16 years or over; and

(c) is being paid:

(i) a disability support pension or a special needs disability support pension under the Social Security Act 1991; or

(ii) an invalidity service pension under the Veterans’ Entitlements Act 1986.

(5) You may be entitled to more than one *tax offset for the year under subsection (1) if:

(a) you contributed to the maintenance of more than one other individual (none of whom are your *spouse) during the year; or

(b) you had different *spouses at different times during the year.

Note 1: If paragraph (b) applies, the amount of the tax offset in relation to each spouse would be only part of the full amount: see section 61‑40.

Note 2: Section 960‑255 may be relevant to determining relationships for the purposes of this section.

61‑15 Cases involving more than one spouse

(1) Despite paragraph 61‑10(1)(a), if, during a period comprising some or all of the year, there are 2 or more individuals who are your *spouse, you are taken, for the purposes of section 61‑10, only to contribute to the maintenance of the spouse with whom you reside during that period.

(2) Despite paragraph 61‑10(1)(a) and subsection (1) of this section, if, during a period comprising some or all of the year:

(a) you reside with 2 or more individuals who are your *spouse; or

(b) 2 or more individuals are your *spouse but you reside with none of them;

you are taken, for the purposes of section 61‑10, only to contribute to the maintenance of whichever of those individuals in relation to whom you are entitled to the smaller, or smallest, amount (including a nil amount) of tax offset under this Subdivision in relation to that period.

(3) If, but for this subsection, subsection (2) would apply in relation to more than one other individual, that paragraph is taken to apply only in relation to one of those other individuals.

61‑20 Exceeding the income limit for family tax benefit (Part B)

(1) Despite section 61‑10, you are not entitled to a *tax offset for an income year if the sum of:

(a) your *adjusted taxable income for offsets for the year; and

(b) if you had a *spouse for the whole or part of the year, and your spouse was not the other individual referred to in subsection 61‑10(1)—the spouse’s adjusted taxable income for offsets for the year;

is more than the amount specified in subclause 28B(1) of Schedule 1 to the A New Tax System (Family Assistance) Act 1999, as indexed under Part 2 of Schedule 4 to that Act.

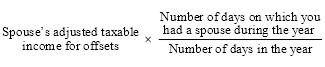

(2) However, if you had a *spouse for only part of the year, the spouse’s *adjusted taxable income for offsets for the year is taken, for the purposes of paragraph (1)(b), to be this amount:

(3) If you had a different *spouse during different parts of the year, include the *adjusted taxable income for offsets of each spouse under paragraph (1)(b) and subsection (2).

61‑25 Eligibility for family tax benefit (Part B) without shared care

Despite section 61‑10, you are not entitled to a *tax offset in relation to another individual for an income year if:

(a) your entitlement to the tax offset would, apart from this section, be based on the other individual being your spouse during the year; and

(b) during the whole of the year:

(i) you, or your *spouse while being your partner (within the meaning of the A New Tax System (Family Assistance) Act 1999), is eligible for family tax benefit at the Part B rate (within the meaning of that Act); and

(ii) clause 31 of Schedule 1 to that Act does not apply in respect of the Part B rate.

Amount of the dependant (invalid and carer) tax offset

61‑30 Amount of the dependant (invalid and carer) tax offset

The amount of the *tax offset to which you are entitled in relation to another individual under section 61‑10 for an income year is $2,423. The amount is indexed annually.

Note 1: Subdivision 960‑M shows you how to index amounts.

Note 2: The amount of the tax offset may be reduced by the application, in order, of sections 61‑35 to 61‑45.

61‑35 Families with shared care percentages

(1) The amount of the *tax offset under section 61‑30 in relation to the other individual for the year is reduced by the amount worked out under subsection (2) of this section if:

(a) your entitlement to the tax offset is based on the other individual being your spouse during the year; and

(b) during a period (the shared care period) comprising the whole or part of the year:

(i) you, or your *spouse while being your partner (within the meaning of the A New Tax System (Family Assistance) Act 1999), was eligible for family tax benefit at the Part B rate within the meaning of that Act; and

(ii) clause 31 of Schedule 1 to that Act applied in respect of that Part B rate because you, or your spouse, had a shared care percentage for an FTB child (within the meaning of that Act).

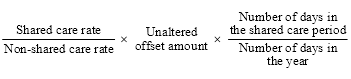

(2) The reduction is worked out as follows:

where:

non‑shared care rate is the rate that would be the standard rate in relation to you or your *spouse under clause 30 of Schedule 1 to the A New Tax System (Family Assistance) Act 1999 if:

(a) clause 31 of that Schedule did not apply; and

(b) the FTB child in relation to whom the standard rate was determined under clause 31 of that Schedule was the only FTB child of you or your spouse, as the case requires.

shared care rate is the standard rate in relation to you or your *spouse worked out under clause 31 of Schedule 1 to the A New Tax System (Family Assistance) Act 1999.

unaltered offset amount is what would, but for this section, be the amount of your *tax offset in relation to the other individual under section 61‑10 for the year.

61‑40 Reduced amounts of dependant (invalid and carer) tax offset

(1) The amount of the *tax offset under sections 61‑30 and 61‑35 in relation to the other individual for the year is reduced by the amount in accordance with subsection (2) of this section if one or more of the following applies:

(a) you contribute to the maintenance of the other individual during part only of the year;

(b) during the whole or part of the year, 2 or more individuals contribute to the maintenance of the other individual;

(c) the other individual is an individual of a kind referred to in subparagraph 61‑10(1)(a)(i), (ii) or (iii) during part only of the year;

(d) paragraph 61‑10(1)(b) applies to the other individual during part only of the year;

(e) paragraph 61‑10(1)(c) applies during part only of the year;

(f) during part of the year:

(i) you, or your *spouse while being your partner (within the meaning of the A New Tax System (Family Assistance) Act 1999), is eligible for family tax benefit at the Part B rate (within the meaning of that Act); and

(ii) clause 31 of Schedule 1 to that Act does not apply in respect of the Part B rate;

(g) the other individual is your spouse, and, during part of the year, parental leave pay is payable under the Paid Parental Leave Act 2010 to you, or to your spouse while being your partner (within the meaning of that Act).

(2) The amount of the tax offset under sections 61‑30 and 61‑35 is reduced to an amount that, in the Commissioner’s opinion, is reasonable in the circumstances, having regard to the applicable matters referred to in paragraphs (1)(a) to (g).

(3) If paragraph (1)(f) or (g) applies, the Commissioner is not to consider the part of the year covered by that paragraph.

61‑45 Reductions to take account of the other individual’s income

The amount of the *tax offset under sections 61‑30 to 61‑40 in relation to the other individual for the year is reduced by $1 for every $4 by which the following exceeds $282:

(a) if you contribute to the maintenance of the other individual for the whole of the year—the other individual’s *adjusted taxable income for offsets for the year;

(b) if paragraph (a) does not apply—the other individual’s *adjusted taxable income for offsets for that part of the year during which you contribute to the maintenance of the other individual.

Income Tax Assessment Act 1936

2 After subsection 159J(1E)

Insert:

(1F) A taxpayer is not entitled, in his or her assessment in respect of a year of income, to a rebate under this section in respect of a dependant included in class 2, 3, 4, 5 or 6 in the table in subsection (2) unless the taxpayer is entitled, in his or her assessment in respect of that year of income, to a rebate under:

(a) section 23AB (certain persons serving with an armed force under the control of the United Nations); or

(b) section 79A (residents of isolated areas); or

(c) section 79B (members of Defence Force serving overseas).

(1G) Subsection (1F) does not affect a taxpayer’s entitlement to a rebate in respect of a dependant who is also a dependant included in class 1 in the table in subsection (2).

3 Subsection 159J(6) (definition of invalid relative)

Repeal the definition, substitute:

invalid relative means a person who:

(a) is not less than 16 years of age and is a child, brother or sister of the taxpayer or of the taxpayer’s spouse; and

(b) is being paid a disability support pension or a special needs disability support pension under the Social Security Act 1991.

Note: Section 960‑255 of the Income Tax Assessment Act 1997 may be relevant to determining relationships for the purposes of this definition.

4 Subsection 159J(6) (definition of invalid spouse)

Repeal the definition, substitute:

invalid spouse means a person who:

(a) is a spouse of the taxpayer; and

(b) is being paid a disability support pension or a special needs disability support pension under the Social Security Act 1991.

5 After subsection 159L(3B)

Insert:

(3C) A taxpayer is not entitled, in his or her assessment in respect of a year of income, to a rebate under this section unless the taxpayer is entitled, in his or her assessment in respect of that year of income, to a rebate under:

(a) section 23AB (certain persons serving with an armed force under the control of the United Nations); or

(b) section 79A (residents of isolated areas); or

(c) section 79B (members of Defence Force serving overseas).

6 Subsection 159P(4) (at the end of the definition of dependant)

Add:

; or (e) a person in respect of whom the taxpayer is entitled to a tax offset under Subdivision 61‑A of the Income Tax Assessment Act 1997; or

(f) a person in respect of whom the taxpayer would be entitled to a tax offset under Subdivision 61‑A of the Income Tax Assessment Act 1997 but for section 61‑20 of that Act.

Income Tax Assessment Act 1997

7 Section 13‑1 (table item headed “dependants”)

Omit:

invalid relative, invalid spouse or carer spouse....... | 159J |

substitute:

invalid relative, invalid spouse or carer in receipt of carer benefit....................... | 159J, Subdivision 61‑A |

8 After section 960‑265 (table item 3)

Insert:

3A | Dependant (invalid and carer) tax offset | section 61‑30 |

9 Subsection 995‑1(1)

Insert:

adjusted taxable income for offsets means adjusted taxable income for rebates within the meaning of subsection 6(1) of the Income Tax Assessment Act 1936.

Part 3—Application of amendments

10 Application of amendments

The amendments made by this Schedule apply to assessments for the 2012‑13 income year and later income years.

Schedule 8—Taxation of financial arrangements

Division 1—Attribution of costs

Income Tax Assessment Act 1997

1 Subsection 230‑70(2)

After “are to provide”, insert “or might provide”.

2 Subsection 230‑75(2)

After “are to receive”, insert “or might receive”.

Income Tax Assessment Act 1997

3 Subsection 230‑70(4)

Repeal the subsection.

4 At the end of section 230‑70

Add:

Note: Generally, no financial benefit you have provided, or are to provide or might provide, under a financial arrangement is reasonably attributable to an amount you receive that is in the nature of interest.

5 Subsection 230‑75(4)

Repeal the subsection.

6 At the end of section 230‑75

Add:

Note: Generally, no financial benefit you have received, or are to receive or might receive, under a financial arrangement is reasonably attributable to an amount you provide that is in the nature of interest.

7 Subsection 230‑200(2)

Omit all the words after paragraph (b).

Division 3—Consistency in working out gains or losses

Income Tax Assessment Act 1997

8 At the end of section 230‑80

Add:

(4) Subsection (3) does not require you to use that same manner consistently for:

(a) a *financial arrangement that you start to have on or after the time a *Commonwealth law that amends the method is made; and

(b) a financial arrangement that you start to have before that time;

if:

(c) the Commonwealth law allows you to choose to apply the method in a particular manner (being a manner in which you are not, apart from the Commonwealth law, allowed to apply the method); and

(d) the inconsistency is entirely due to you choosing to apply the method in that manner to the financial arrangement mentioned in paragraph (a).

9 Application of amendment

The amendment made by this Division applies in relation to the following Commonwealth laws:

(a) this Schedule;

(b) other Commonwealth laws made on or after the day this Act receives the Royal Assent.

Part 2—Accruals/realisation methods

Division 1—Sufficiently certain particular gains or losses

Income Tax Assessment Act 1997

10 Paragraph 230‑110(2)(a)

After “gain or loss”, insert “, and the extent to which such a financial benefit is, for the purposes of subsection 230‑70(2) or 230‑75(2), reasonably attributable to the benefit, right or obligation mentioned in paragraph (1)(c) or (d) of this section at the time mentioned in subsection (1)”.

Division 2—Precedence of particular gains or losses

Income Tax Assessment Act 1997

11 At the end of subsection 230‑100(2) (before the note)

Add:

; and (c) you choose to apply the accruals method to the gain or loss, or subsection (4) applies to the gain or loss.

12 Subparagraph 230‑100(3)(b)(i)

Before “at the time”, insert “before or”.

13 Paragraph 230‑110(2)(b)

Repeal the paragraph, substitute:

(b) disregard any financial benefit that has already been taken into account, under subsection 230‑105(1), in working out, at the time when you started to have the arrangement, the amount of a sufficiently certain overall gain or loss from the *financial arrangement to which the accruals method applies; and

14 Subsection 230‑130(2)

Repeal the subsection.

Division 3—Spreading prepayments

Income Tax Assessment Act 1997

15 After subsection 230‑100(3)

Insert:

Accruals method—particular gain or loss becomes sufficiently certain

(3A) The accruals method provided for in this Subdivision also applies to a gain or loss you have from a *financial arrangement if:

(a) the gain or loss arises from a *financial benefit that you are to receive or are to provide under the arrangement; and

(b) the gain or loss becomes sufficiently certain at the time you receive or provide the benefit; and

(c) at least part of the period over which the gain or loss would be spread under that method (assuming that method applied) occurs after the time you receive or provide the benefit.

This subsection has effect subject to subsection (4).

Note 1: Subsection 230‑110(1) tells you when you have a sufficiently certain gain or loss at a particular time.

Note 2: For the period over which the gain or loss would be spread, see subsections 230‑130(3) to (5).

Accruals method—particular gain or loss from qualifying security

16 Subsection 230‑100(4)

After “Subsection (3)”, insert “or (3A)”.

17 Subsection 230‑110(1)

Omit “will make”, substitute “make, or will make,”.

18 Subsection 230‑115(1)

Omit “will make”, substitute “make, or will make,”.

19 Paragraph 230‑130(4)(b)

Before “not start”, insert “other than in the case of a gain or loss to which subsection 230‑100(3A) or subsection (4A) of this section applies—”.

20 Subsection 230‑130(5)

Repeal the subsection, substitute:

(5) The end of the period over which a gain or loss to which subsection (3) applies is to be spread must not end later than the time when you will cease to have the *financial arrangement.

21 After subsection 230‑170(2)

Insert:

(2A) Subsections (1) and (2) do not apply to a part of a gain or loss if:

(a) subsection 230‑100(3A) or 230‑130(4A) applies to the gain or loss; and

(b) that part of the gain or loss is allocated to an interval under section 230‑135; and

(c) that interval ends before or during the income year during which the gain or loss becomes sufficiently certain (as mentioned in paragraph 230‑100(3A)(b) or 230‑130(4A)(f), whichever is applicable).

Instead, you are taken, for the purposes of section 230‑15, to make, for that income year, a gain or loss equal to that part of that gain or loss.

Division 4—Spreading single payment

Income Tax Assessment Act 1997

22 After subsection 230‑135(6)

Insert:

(6A) However, if there is only one *financial benefit that is to be taken into account in working out the amount of the gain or loss, then, for the purposes of paragraph (5)(b), in determining the amount to which you apply the rate of return, have regard to a notional principal:

(a) by reference to which the financial benefit is calculated; or

(b) which is reasonably related to the financial benefit.

Income Tax Assessment Act 1997

23 Paragraph 230‑190(1)(c)

Omit “section 230‑200; and”, substitute “section 230‑200.”.

24 Paragraph 230‑190(1)(d)

Repeal the paragraph.

25 Subsection 230‑190(2)

Repeal the subsection, substitute:

(2) You must re‑estimate the gain or loss as soon as reasonably practicable after you become aware of the circumstances referred to in paragraph (1)(b), if subsection (1) applies.

26 After subsection 230‑190(3)

Insert:

(3A) You also re‑estimate a gain or loss from a *financial arrangement under subsection (5) if:

(a) the gain or loss is spread using the method referred to in paragraph 230‑135(2)(b) in accordance with section 230‑140 (effective interest method); and

(b) you recalculate the effective interest rate in accordance with that method; and

(c) the terms and conditions of the arrangement provide for reset dates to occur no more than 12 months apart; and

(d) the maximum life of the arrangement (as determined under the terms and conditions of the arrangement) is more than 12 months.

(3B) You must re‑estimate the gain or loss at the relevant reset date if subsection (3A) applies.

Division 6—Impairments and reversals

Income Tax Assessment Act 1997

27 After subsection 230‑130(4)

Insert:

(4A) This subsection applies to a gain or loss to which subsection (3) applies, if:

(a) there is an impairment (within the meaning of the *accounting principles) of:

(i) the *financial arrangement; or

(ii) a financial asset or financial liability that forms part of the arrangement; and

(b) because of the impairment, you make a reassessment under section 230‑185 in relation to the arrangement; and

(c) you determine on the reassessment that the gain or loss is not sufficiently certain (whether or not the gain or loss was sufficiently certain before the reassessment); and

(d) there is a reversal of the impairment loss (within the meaning of the accounting principles) that resulted from the impairment; and

(e) because of the reversal, you make a reassessment under section 230‑185 in relation to the arrangement; and

(f) you determine on the reassessment that the gain or loss has become sufficiently certain.

Note: For the income years to which the gain or loss is allocated, see section 230‑170.

28 After section 230‑170

Insert:

230‑172 Applying accruals method to loss resulting from impairment

(1) This section applies if:

(a) there is an impairment (within the meaning of the *accounting principles) of:

(i) a *financial arrangement; or

(ii) a financial asset or financial liability that forms part of a financial arrangement; and

(b) you make a loss from the financial arrangement as a result of the impairment; and

(c) the accruals method applies to the loss.

(2) You cannot deduct a loss you make for an income year under section 230‑15, to the extent that the loss results from the impairment (including as affected by any later reversal of the impairment loss (within the meaning of the *accounting principles) that resulted from the impairment).

(3) Disregard subsection (2) for the purposes of paragraph (c) of step 1 of the method statement in subsection 230‑445(1).

29 Subsections 230‑190(8) to (10)

Repeal the subsections.

30 After section 230‑190

Insert:

230‑192 Re‑estimation—impairments and reversals

(1) This section applies if the re‑estimation mentioned in section 230‑190 arises because of:

(a) an impairment (within the meaning of the *accounting principles) of:

(i) the *financial arrangement; or

(ii) a financial asset or financial liability that forms part of the arrangement; or

(b) a reversal of an impairment loss (within the meaning of the accounting principles) that resulted from such an impairment.

(2) Despite paragraph 230‑190(6)(a), you must make the fresh allocation in accordance with paragraph 230‑190(6)(b).

Losses non‑deductible

(3) You cannot deduct a loss you make for an income year under section 230‑15, to the extent that the loss results from:

(a) the impairment (including as affected by any later reversal of the impairment loss that resulted from the impairment); or

(b) the operation of subsection (7).

(4) Disregard subsection (3) for the purposes of paragraph (c) of step 1 of the method statement in subsection 230‑445(1).

Reversals

(5) Subsections (7) and (8) apply to the part of the gain or loss that is to be reallocated in accordance with paragraph 230‑190(6)(b), if:

(a) the fresh determination under paragraph 230‑190(5)(a) that arose because of the reversal resulted in that part being a gain; and

(b) there are losses that:

(i) resulted from the impairment; and

(ii) you could have deducted apart from subsection 230‑172(2) or subsection (3) of this section.

(6) Paragraph (5)(b) does not apply to a loss to the extent that:

(a) the loss reflects the amount of a loss you make under paragraph 230‑195(1)(b) or (c); and

(b) the loss you make under paragraph 230‑195(1)(b) or (c) relates to you writing off, as a bad debt, a right to receive a *financial benefit (or a part of a financial benefit).

(7) Treat the fresh determination as having resulted in that part being a loss, if the total of the losses mentioned in paragraph (5)(b) of this section exceeds the amount of the gain mentioned in paragraph (5)(a). The amount of the loss is equal to the amount of the excess.

(8) Otherwise, reduce the amount of that gain by the total of those losses.

Division 7—Running balancing adjustments

Income Tax Assessment Act 1997

31 After subsection 230‑175(1)

Insert:

(1A) Subsection (1) does not apply to the extent that the difference results from:

(a) an impairment (within the meaning of the *accounting principles) of:

(i) the *financial arrangement; or

(ii) a financial asset or financial liability that forms part of the arrangement; or

(b) you writing off, as a bad debt, a right to a *financial benefit (or a part of a financial benefit).

32 After subsection 230‑175(2)

Insert:

(2A) Subsection (2) does not apply to the extent that the difference results from the reversal of an impairment loss (within the meaning of the *accounting principles) that resulted from an impairment (within the meaning of the accounting principles) of:

(a) the *financial arrangement; or

(b) a financial asset or financial liability that forms part of the arrangement.

Division 8—Ceasing of rights or obligations

Income Tax Assessment Act 1997

33 Subsection 230‑180(2)

Repeal the subsection, substitute:

(2) For the purposes of subsection (1), a gain or loss from a *financial arrangement is taken to occur at:

(a) if the last of the *financial benefits, rights and obligations taken into account in determining the amount of the gain or loss is a financial benefit—the time the financial benefit:

(i) is provided; or

(ii) if the financial benefit is not provided at the time when it is due to be provided under the arrangement and it is reasonable to expect that the financial benefit will be provided—is due to be provided; or

(b) if the last of the financial benefits, rights and obligations taken into account in determining the amount of the gain or loss is a right to receive a financial benefit or an obligation to provide a financial benefit—the time:

(i) if the right or obligation ceases before the financial benefit is provided—the right or obligation ceases; or

(ii) otherwise—the financial benefit is provided.

This subsection has effect subject to subsection (3).

Income Tax Assessment Act 1997

34 Paragraph 230‑40(4)(a)

Repeal the paragraph, substitute:

(a) to the extent that Subdivision 230‑C (fair value method) applies to the gain or loss; or

Note: See subsection (5) of this section and subsection 230‑230(4).

35 Paragraph 230‑220(1)(c)

Omit “to classify or designate”, substitute “to classify, designate or (in whole or in part) otherwise treat”.

36 Subsection 230‑230(1)

Repeal the subsection, substitute:

(1) You make a gain or loss for an income year from a *financial arrangement to which a *fair value election applies if:

(a) the principles or standards mentioned in paragraph 230‑210(2)(a) require you to recognise a gain or loss in profit or loss for the income year from the asset or liability mentioned in paragraph 230‑220(1)(c); or

(b) in the case of an arrangement to which subsection 230‑220(2) applies—the principles or standards referred to in paragraph 230‑220(1)(c) would have required you to recognise a gain or loss in profit or loss for the year from the asset or liability mentioned in paragraph 230‑220(1)(c) if the arrangement had not been an intra‑group transaction for the purposes of the standard referred to in paragraph 230‑220(2)(b); or

(c) in the case of an arrangement to which subsection 230‑220(3) applies—the principles or standards referred to in paragraph 230‑220(1)(c) would have required you to recognise a gain or loss in profit or loss for the year from the asset or liability mentioned in paragraph 230‑220(1)(c) if the arrangement had been between 2 separate entities.

Note: Subsection 230‑40(7) provides that an election under Subdivision 230‑E (hedging financial arrangements method) or Subdivision 230‑F (method of relying on financial reports) may override a fair value election.

(1A) The gain or loss you make is the gain or loss the principles or standards require, or would have required, you to recognise in profit or loss as mentioned in subsection (1).

37 At the end of section 230‑230

Add:

Subdivision does not apply to extent gains or losses not recognised as at fair value

(4) This Subdivision does not apply to a gain or loss you make from the *financial arrangement, to the extent:

(a) you are required, as mentioned in paragraph 230‑220(1)(c), to otherwise treat as at fair value through profit and loss the assets or liabilities that the financial arrangement is; and

(b) the principles or standards referred to in paragraph 230‑210(2)(a) do not require you to recognise the gain or loss as at fair value through profit or loss.

Note: See also subsection 230‑40(5).

38 At the end of section 230‑245

Add:

(6) In determining, for the purposes of the balancing adjustment under subsection (2) or (4) or for the purposes of subsection (5), the fair value of the *financial arrangement at a time, disregard any changes in the fair value to the extent that:

(a) you are required, as mentioned in paragraph 230‑220(1)(c), to otherwise treat the financial arrangement as at fair value through profit and loss; and

(b) the principles or standards referred to in paragraph 230‑210(2)(a) do not require you to recognise the changes as at fair value through profit or loss.

Part 4—Hedging financial arrangements method

Division 1—One in all in principle

Income Tax Assessment Act 1997

39 Section 230‑325

Repeal the section, substitute:

230‑325 Hedging financial arrangements to which election applies

A *hedging financial arrangement election applies to a *hedging financial arrangement:

(a) that you start to have in the income year in which you make the election or in a later income year; and

(b) that is not excluded from the application of the election by section 230‑330.

Note: Subject to a determination by the Commissioner, the hedging financial arrangement election does not apply to a financial arrangement you start to have after you fail to comply with the requirements in sections 230‑355 and 230‑360 and paragraph 230‑365(c) in relation to a hedging financial arrangement to which the election does apply: see section 230‑385. See also subsection 230‑305(1).

40 Paragraph 230‑335(3)(d)

Before “you satisfy”, insert “in a case in which none of subsections (5), (6) and (7) are satisfied—”.

41 Paragraph 230‑335(3)(e)

Before “you satisfy”, insert “in any case—”.

42 After subsection 230‑335(3)

Insert:

(3A) Disregard paragraph (3)(d) if subsection (4) is satisfied and:

(a) a *hedging financial arrangement election applies to the *financial arrangement (because you previously satisfied the additional recording requirements mentioned in that paragraph at a time when the election applied); or

(b) all of the following subparagraphs apply:

(i) a hedging financial arrangement election would apply to the financial arrangement if you satisfied the additional recording requirements mentioned in paragraph (3)(d);

(ii) the election and subsection (3) apply to another financial arrangement;

(iii) subsection (4) is or was satisfied in relation to that other arrangement at a time when the election applied to that other arrangement.

43 Paragraph 230‑365(c)

Omit all the words after subparagraph (ii).

44 At the end of section 230‑365

Add:

; and (d) your assessment must be that the hedging of the risk will be highly effective (within the meaning of the principles or standards referred to in paragraph 230‑315(2)(a)) in reducing your exposure to changes in the fair value of the hedged item or items or cash flows attributable to the hedged risk throughout the remainder of the period for which you expect to have the arrangement.

45 Section 230‑380 (heading)

Repeal the heading, substitute:

230‑380 Commissioner may determine that requirement met

46 Subsection 230‑380(6)

Omit “and the Commissioner’s”, substitute “, in a way that satisfies the requirements of section 230‑360. The Commissioner’s”.

47 Section 230‑385

Repeal the section, substitute:

230‑385 Consequences of failure to meet requirements

When this section applies

(1) This section applies if:

(a) your *hedging financial arrangement election applies to a *hedging financial arrangement; and

(b) you do not meet a requirement of section 230‑355 or 230‑360 or paragraph 230‑365(c) in relation to the arrangement.

(2) For the purposes of paragraph (1)(b), treat the requirement in paragraph 230‑365(c) as being met even if you do not assess the hedging of the risk mentioned in that paragraph, but you can demonstrate that you intend to do so.

Commissioner may determine matter under section 230‑360

(3) If:

(a) you fail to determine a matter in relation to the *hedging financial arrangement under section 230‑360; or

(b) you determine a matter in relation to the arrangement under section 230‑360 but the determination does not satisfy the requirements of subsection 230‑360(2);

the Commissioner may determine that matter, in a way that satisfies the requirements of section 230‑360. A reference in this Division to a determination made under that section is treated as including a reference to a determination under this subsection.

Election does not apply to hedging financial arrangements you start to have after failing to comply with requirements

(4) Your *hedging financial arrangement election does not apply to a *hedging financial arrangement you start to have:

(a) after you fail to meet the requirement mentioned in paragraph (1)(b) in relation to the arrangement mentioned in that paragraph; and

(b) before a date (if any) determined by the Commissioner.

(5) The Commissioner may make a determination under paragraph (4)(b) only if satisfied that you are unlikely to fail again to meet a requirement of section 230‑355 or 230‑360 or paragraph 230‑365(c) in relation to a *hedging financial arrangement.

(6) In deciding whether to make a determination under paragraph (4)(b), the Commissioner must have regard to:

(a) your record keeping practices; and

(b) your compliance history; and

(c) any changes that have been made to:

(i) your accounting systems and controls; and

(ii) your internal governance processes;

to ensure that failures of the kind mentioned in paragraph (1)(b) do not happen again; and

(d) any other relevant matter.

Commissioner may still exercise powers under section 230‑380

(7) This section does not prevent the Commissioner from exercising the Commissioner’s powers under section 230‑380 in relation to the *hedging financial arrangement mentioned in subsection (1).

Division 2—Hedging net investments in foreign operations

Income Tax Assessment Act 1997

48 Subsection 230‑310(5)

Repeal the subsection, substitute:

(5) Subsection (6) applies if:

(a) a *hedged item is your net investment in a foreign operation (within the meaning of the *accounting principles); and

(b) the foreign operation is carried on through:

(i) a company in which you hold *shares; or

(ii) a company that is a subsidiary of yours (within the meaning of the Corporations Act 2001).

(6) The table in subsection (4) has effect as if:

(a) to the extent that the *hedging financial arrangement hedges a risk or risks in relation to *shares you hold in the company—the reference in that table to the *hedged item were a reference to your interest in those shares; and

(b) to the extent that the hedging financial arrangement hedges a risk or risks in relation to another interest you have in the company—the reference in that table to the hedged item were a reference to that interest.

Part 5—Transitional balancing adjustments

Tax Laws Amendment (Taxation of Financial Arrangements) Act 2009

49 At the end of paragraph 104(14)(c) of Schedule 1

Add “and”.

50 After paragraph 104(14)(c) of Schedule 1

Insert:

(ca) the attributable assessable amount represents the whole of the deferred tax effect of a gain or loss from the financial arrangement that has been recognised in profit or loss in accordance with the accounting principles mentioned in paragraph 230‑395(2)(a) of the Income Tax Assessment Act 1997;

51 At the end of subitem 104(14) of Schedule 1

Add:

Note: The deferred tax effect to be taken into account for the purposes of paragraph (ca) might be affected by a later assessment, the amendment of an assessment or a law that applies retrospectively.

52 At the end of paragraph 104(15)(c) of Schedule 1

Add “and”.

53 After paragraph 104(15)(c) of Schedule 1

Insert:

(ca) the attributable deductible amount represents the whole of the deferred tax effect of a gain or loss from the financial arrangement that has been recognised in profit or loss in accordance with the accounting principles mentioned in paragraph 230‑395(2)(a) of the Income Tax Assessment Act 1997;

54 At the end of subitem 104(15) of Schedule 1

Add:

Note: The deferred tax effect to be taken into account for the purposes of paragraph (ca) might be affected by a later assessment, the amendment of an assessment or a law that applies retrospectively.

Income Tax Assessment Act 1997

55 At the end of Subdivision 230‑I

Add:

230‑527 Elections—reporting documents of foreign ADIs

(1) So much of a Statement of Financial Performance and a Statement of Financial Position, given to *APRA by a foreign ADI (within the meaning of the Banking Act 1959) as required under section 13 of the Financial Sector (Collection of Data) Act 2001, as:

(a) cover the activities of an *Australian permanent establishment of the foreign ADI for the year; and

(b) are prepared in accordance with the recognition and measurement standards under the *accounting principles; and

(c) are audited in accordance with the *auditing principles;

are treated, for the purposes of the provisions mentioned in subsection (2), as being a financial report for a year:

(d) prepared by the foreign ADI in accordance with the accounting principles; and

(e) audited in accordance with the auditing principles.

(2) The provisions are as follows:

(a) sections 230‑150 to 230‑165 (election for portfolio treatment of fees);

(b) sections 230‑210 to 230‑220 (fair value election);

(c) sections 230‑255 to 230‑265 (foreign exchange retranslation election);

(d) sections 230‑315 to 230‑335 (hedging financial arrangement election);

(e) sections 230‑395, 230‑400, 230‑410 and 230‑430 (election to rely on financial reports).

Part 7—Miscellaneous amendments

Division 1—Consistency of language

Income Tax Assessment Act 1997

56 Paragraphs 230‑80(2)(a) and (3)(a)

Omit “make”, substitute “have”.

57 Subsections 230‑100(2), (3), (4) and (5)

Omit “make”, substitute “have”.

58 Section 230‑125

Omit “make”, substitute “have”.

Income Tax Assessment Act 1997

59 Subparagraph 230‑5(2)(a)(iv) (second occurring)

Renumber as subparagraph (iva).

60 Paragraph 230‑85(a)

After “even”, insert “if”.

Note: This item fixes a typographical error.

61 Subparagraph 230‑140(3)(c)(ii)

Omit “will be provided or received”, substitute “is to be provided or received”.

62 Paragraph 230‑190(7)(a)

Omit “are to apply”, substitute “is to apply”.

Note: This item fixes a grammatical error.

63 Subsections 230‑290(1) and (3)

Omit “*foreign currency retranslation election”, substitute “*foreign exchange retranslation election”.

Note: This item fixes typographical errors.

64 Paragraph 230‑455(1)(d)

Omit “subparagraph (iv)”, substitute “subparagraph (a)(iv)”.

Note: This item clarifies a cross‑reference.

[Minister’s second reading speech made in—

House of Representatives on 20 March 2013

Senate on 17 June 2013]

(69/13)