Tax Laws Amendment (2013 Measures No. 2) Act 2013

No. 124, 2013

An Act to amend the law relating to taxation and the Tax Agent Services Act 2009, and for other purposes

Tax Laws Amendment (2013 Measures No. 2) Act 2013

No. 124, 2013

An Act to amend the law relating to taxation and the Tax Agent Services Act 2009, and for other purposes

Contents

2 Commencement

3 Schedule(s)

Schedule 1—Monthly PAYG instalments

Part 1—Main amendments

Taxation Administration Act 1953

Part 2—Consequential amendments

Income Tax Assessment Act 1997

Part 3—Application and transitional provisions

Schedule 2—Incentives for designated infrastructure projects

Part 1—Main amendments

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Part 2—Consequential amendments

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Infrastructure Australia Act 2008

Part 3—Application of amendments

Income Tax (Transitional Provisions) Act 1997

Part 4—Miscellaneous amendments

Division 1—Income Tax Assessment Act 1936

Division 2—Income Tax Assessment Act 1997

Schedule 5—Tax secrecy and transparency

Part 1—Main amendments

Taxation Administration Act 1953

Part 2—Consequential amendments

Income Tax Assessment Act 1997

Part 3—Application of amendments

Schedule 6—Petroleum resource rent tax

Petroleum Resource Rent Tax Assessment Act 1987

Schedule 7—Removing CGT discount for foreign individuals

Income Tax Assessment Act 1997

Schedule 8—Tax exemption for payments under Defence Abuse Reparation Scheme

Income Tax Assessment Act 1997

Schedule 9—GST‑free treatment for National Disability Insurance Scheme funded supports

A New Tax System (Goods and Services Tax) Act 1999

Schedule 10—Deductible gift recipients

Part 1—Main amendments

Income Tax Assessment Act 1997

Tax Laws Amendment (2011 Measures No. 2) Act 2011

Part 2—The Charlie Perkins Scholarship Trust

Income Tax Assessment Act 1997

Tax Laws Amendment (Special Conditions for Not‑for‑profit Concessions) Act 2013

Schedule 11—Miscellaneous amendments

Part 1—Amendments commencing after the Australian Charities and Not‑for‑profits Commission Act 2012

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Part 2—Amendment commencing after Schedule 1 to the Tax Laws Amendment (2012 Measures No. 6) Act 2013

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Part 3—Fringe Benefits Tax

Fringe Benefits Tax Assessment Act 1986

Taxation Administration Act 1953

Part 4—Updating indexation provisions

Income Tax Assessment Act 1997

Superannuation (Government Co‑contribution for Low Income Earners) Act 2003

Superannuation Guarantee (Administration) Act 1992

Part 5—Other amendments

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Tax Laws Amendment (2013 Measures No. 2) Act 2013

No. 124, 2013

An Act to amend the law relating to taxation and the Tax Agent Services Act 2009, and for other purposes

[Assented to 29 June 2013]

The Parliament of Australia enacts:

This Act may be cited as the Tax Laws Amendment (2013 Measures No. 2) Act 2013.

(1) Each provision of this Act specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information | ||

Column 1 | Column 2 | Column 3 |

Provision(s) | Commencement | Date/Details |

1. Sections 1 to 3 and anything in this Act not elsewhere covered by this table | The day this Act receives the Royal Assent. | 29 June 2013 |

2. Schedule 1 | The day this Act receives the Royal Assent. | 29 June 2013 |

3. Schedule 2, Parts 1 to 3 | A single day to be fixed by Proclamation. However, if the provision(s) do not commence within the period of 6 months beginning on the day this Act receives the Royal Assent, they commence on the day after the end of that period. | 11 July 2013 (see F2013L01359) |

4. Schedule 2, Part 4, Division 1 | The day this Act receives the Royal Assent. | 29 June 2013 |

5. Schedule 2, Part 4, Division 2 | The later of: (a) immediately after the commencement of the provision(s) covered by table item 3; and (b) the commencement of item 34 of Schedule 6 to the Tax and Superannuation Laws Amendment (2013 Measures No. 1) Act 2013. However, the provision(s) do not commence at all if the event mentioned in paragraph (b) does not occur. | 11 July 2013 (paragraph (a) applies) |

10. Schedules 5 to 9 | The day this Act receives the Royal Assent. | 29 June 2013 |

11. Schedule 10, Part 1 | The day this Act receives the Royal Assent. | 29 June 2013 |

12. Schedule 10, item 13 | The day this Act receives the Royal Assent. However, the provision(s) do not commence at all if item 5 of Schedule 1 to the Tax Laws Amendment (Special Conditions for Not‑for‑profit Concessions) Act 2013 commences on or before that day. | 29 June 2013 |

13. Schedule 10, item 14 | The later of: (a) the start of the day this Act receives the Royal Assent; and (b) immediately after the commencement of item 13 of Schedule 1 to the Tax Laws Amendment (Special Conditions for Not‑for‑profit Concessions) Act 2013. However, the provision(s) do not commence at all if the event mentioned in paragraph (b) does not occur. | Does not commence |

14. Schedule 10, item 15 | Immediately after the commencement of Schedule 1 to the Tax Laws Amendment (Special Conditions for Not‑for‑profit Concessions) Act 2013. However, the provision(s) do not commence at all if that Schedule commences before the day this Act receives the Royal Assent. | Does not commence |

15. Schedule 11, Part 1 | Immediately after the commencement of Chapter 2 of the Australian Charities and Not‑for‑profits Commission Act 2012. | 3 December 2012 |

16. Schedule 11, Part 2 | Immediately after the commencement of Schedule 1 to the Tax Laws Amendment (2012 Measures No. 6) Act 2013. | 28 June 2013 |

17. Schedule 11, Part 3 | The day after this Act receives the Royal Assent. | 30 June 2013 |

18. Schedule 11, item 28 | The later of: (a) the start of the day after this Act receives the Royal Assent; and (b) immediately after the commencement of item 238 of Schedule 7 to the Tax and Superannuation Laws Amendment (2013 Measures No. 1) Act 2013. However, the provision(s) do not commence at all if the event mentioned in paragraph (b) does not occur. | 30 June 2013 (paragraph (a) applies) |

19. Schedule 11, items 29 to 31 | The day after this Act receives the Royal Assent. | 30 June 2013 |

20. Schedule 11, subitem 32(1) | (a) the start of the day after this Act receives the Royal Assent; and (b) immediately after the commencement of item 238 of Schedule 7 to the Tax and Superannuation Laws Amendment (2013 Measures No. 1) Act 2013. However, the provision(s) do not commence at all if the event mentioned in paragraph (b) does not occur. | 30 June 2013 (paragraph (a) applies) |

21. Schedule 11, subitems 32(2) and (3) | The day after this Act receives the Royal Assent. | 30 June 2013 |

22. Schedule 11, Part 5 | The day after this Act receives the Royal Assent. | 30 June 2013 |

Note: This table relates only to the provisions of this Act as originally enacted. It will not be amended to deal with any later amendments of this Act.

(2) Any information in column 3 of the table is not part of this Act. Information may be inserted in this column, or information in it may be edited, in any published version of this Act.

Each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

1 Section 45‑1 in Schedule 1

Omit:

Generally, instalments are payable for each quarter of your income year.

substitute:

Generally, instalments are payable for each quarter of your income year. Alternatively, instalments could be payable monthly or annually.

2 Section 45‑1 in Schedule 1

Omit:

If you are not required to be registered for GST purposes, you may be able to choose to pay an annual instalment after the end of the income year. (In this case, you are an annual payer).

substitute:

If your business or investment income exceeds a certain limit, you may have to pay an instalment after the end of each month. (In this case, you are a monthly payer).

If you are not required to be registered for GST purposes, you may be able to choose to pay an annual instalment after the end of the income year. (In this case, you are an annual payer).

3 After subsection 45‑5(2) in Schedule 1

Insert:

(2A) Alternatively:

(a) you may be required to pay instalments after the end of each *instalment month worked out on the basis of your instalment income for that month; or

(b) you may be able to choose to pay an annual instalment for the income year.

4 After subsection 45‑5(5) in Schedule 1

Insert:

(5A) If you are a *monthly payer, the amount of each of your instalments for an income year is the same proportion (as nearly as possible, subject to the principles in subsections (3) and (4)) of the total of those instalments as your *instalment income for that *instalment month is of your total instalment income for the income year.

5 After subsection 45‑20(2) in Schedule 1

Insert:

(2A) If you are a *monthly payer for the period, you must give the notification electronically, unless the Commissioner otherwise approves.

Note: A penalty applies if you fail to give the notification electronically as required—see section 288‑10.

(2B) The notification is given electronically if it is transmitted to the Commissioner in an electronic format approved by the Commissioner.

6 After subsection 45‑50(2) in Schedule 1

Insert:

(2A) Subject to subsection (4), you are liable to pay an instalment for an *instalment month if, at the end of that month, you are a *monthly payer.

7 Subsection 45‑50(4) in Schedule 1

After “an *instalment quarter”, insert “, an *instalment month”.

8 Paragraph 45‑50(4)(b) in Schedule 1

After “quarter”, insert “, month”.

9 After section 45‑61 in Schedule 1

Insert:

For an income year (whether it ends on 30 June or not), the following are instalment months:

(a) the month that starts on the first day of the income year;

(b) each subsequent month.

Note: For the meaning of month, see section 2G of the Acts Interpretation Act 1901.

You are not a deferred BAS payer

(1) If you are a *monthly payer, the instalment for an *instalment month that you are liable to pay is due on or before the 21st day of the next instalment month.

(2) If:

(a) subsection (1) would, but for this subsection, have applied to you in relation to an *instalment month; but

(b) you are a *deferred BAS payer on the 21st day of the next instalment month;

the instalment for the month mentioned in paragraph (a) is instead due on or before:

(c) the 28th day of that next instalment month unless that next instalment month is January; or

(d) if that next instalment month is January—the next 28 February.

Note: If you are the head company of a consolidated group to which Subdivision 45‑Q applies, the instalment is due on or before the 21st day of that next month: see section 45‑715 (as it has effect because of section 45‑703).

10 After section 45‑70 in Schedule 1

Insert:

11 After section 45‑112 in Schedule 1

Insert:

(1) Work out the amount of an instalment you are liable to pay for an *instalment month as follows if, at the end of that instalment month, you are a *monthly payer:

(2) For the purposes of the formula in subsection (1):

applicable instalment rate means:

(a) unless paragraph (b) or (c) applies—the most recent instalment rate given to you by the Commissioner under section 45‑15 before the end of that month; or

(b) if you have chosen an instalment rate for that month under section 45‑205—that rate; or

(c) if you have chosen an instalment rate under section 45‑205 for an earlier *instalment month in that income year (and paragraph (b) does not apply)—that rate.

Note: If you believe the Commissioner’s rate is not appropriate for the current income year, you may choose a different instalment rate under Subdivision 45‑F.

(3) The Commissioner may, by legislative instrument, determine one or more specified additional methods by which a specified class of entity that is a *monthly payer at the end of an *instalment month may work out, in specified circumstances, the amount of an instalment that it is liable to pay for the instalment month.

Note: For specification by class, see subsection 13(3) of the Legislative Instruments Act 2003.

(4) You may choose a method specified in the determination:

(a) unless paragraph (b) applies—for any *instalment month; or

(b) if the determination provides that that method can be chosen only for the first instalment month in an *instalment quarter—for the first instalment month in an instalment quarter.

(5) The determination may provide that an entity that chooses a method in accordance with paragraph (4)(b) for the first *instalment month in an *instalment quarter is taken to have chosen that method under subsection (4) for the other instalment months in that quarter. The determination has effect accordingly.

(6) Subsection (7) applies if:

(a) the Commissioner has made a determination under subsection (3); and

(b) at the end of an *instalment month, you are a *monthly payer; and

(c) you choose under subsection (4), for that month:

(i) if the determination specifies one additional method to work out that amount—that method; or

(ii) if the determination specifies more than one additional method to work out that amount—one of those methods.

(7) Despite subsection (1), work out the amount of an instalment you are liable to pay for that *instalment month in accordance with the method that you chose for that month under subsection (4).

12 Paragraph 45‑125(1)(a) in Schedule 1

Omit “you are not an *annual payer”, substitute “you are not a *monthly payer or an *annual payer”.

13 Subsection 45‑125(5) in Schedule 1

Repeal the subsection, substitute:

How and when you stop being such a payer

(5) If you are a *quarterly payer who pays on the basis of instalment income because of paragraph (1)(a), you stop being such a payer at the start of the first *instalment quarter in the next income year if:

(a) at the end of that quarter, you become:

(i) a quarterly payer who pays on the basis of GDP‑adjusted notional tax; or

(ii) an *annual payer; or

(b) at the end of the first *instalment month of that quarter, you become a *monthly payer.

No quarterly payer status in quarter if monthly payer in following month

(5A) Despite subsections (1) and (3), you cannot be a *quarterly payer who pays on the basis of instalment income at a time in an *instalment quarter if you are a *monthly payer at a time in the first *instalment month that ends after that quarter.

14 Paragraph 45‑130(1)(a) in Schedule 1

Omit “an *annual payer or a *quarterly payer”, substitute “an *annual payer, a *monthly payer or a *quarterly payer”.

15 After subparagraph 45‑130(1)(c)(ii) in Schedule 1

Insert:

(iia) you are not a *monthly payer;

16 Subsection 45‑130(4) in Schedule 1

Repeal the subsection, substitute:

(4) In addition, you stop being such a payer at the start of the first *instalment quarter in the next income year if:

(a) at the end of that quarter, you become:

(i) a *quarterly payer who pays on the basis of instalment income; or

(ii) an *annual payer; or

(b) at the end of the first *instalment month of that quarter, you become a *monthly payer.

No quarterly payer status in quarter if monthly payer in following month

(5) Despite subsections (1) and (2), you cannot be a *quarterly payer who pays on the basis of GDP‑adjusted notional tax at a time in an *instalment quarter if you are a *monthly payer at a time in the first *instalment month that ends after that quarter.

17 Subsection 45‑132(4) in Schedule 1

Repeal the subsection, substitute:

(4) In addition, you stop being such a payer at the start of the first *instalment quarter in the next income year if:

(a) at the end of that quarter, you become:

(i) a *quarterly payer who pays on the basis of instalment income; or

(ii) an *annual payer; or

(b) at the end of the first *instalment month of that quarter, you become a *monthly payer.

18 Subsection 45‑134(4) in Schedule 1

Repeal the subsection, substitute:

(4) In addition, you stop being such a payer at the start of the first *instalment quarter in the next income year if:

(a) at the end of that quarter, you become:

(i) a *quarterly payer who pays on the basis of instalment income; or

(ii) an *annual payer; or

(b) at the end of the first *instalment month of that quarter, you become a *monthly payer.

19 After Subdivision 45‑D in Schedule 1

Insert:

Table of sections

45‑136 Monthly payer

45‑138 Monthly payer requirement

(1) You are a monthly payer at a time if:

(a) you were a monthly payer immediately before that time; or

(b) if paragraph (a) does not apply—you satisfy the requirement in subsection 45‑138(1) for the income year in which that time occurs.

Note: If paragraph (b) applies, see subsection (3) for the time at which you become a monthly payer.

(2) The starting instalment month in an income year (the current year) is:

(a) if the Commissioner gives you an instalment rate for the first time during an *instalment month in the current year—the next instalment month in the current year; or

(b) if the Commissioner has given you an instalment rate during a previous income year and your instalment rate has not been withdrawn—the first instalment month in the current year.

How and when you become such a payer

(3) Despite subsection (1), if paragraph (1)(b) applies, you become a *monthly payer just before the end of the *starting instalment month in the income year.

How and when you stop being such a payer

(4) Despite subsection (1), you stop being a *monthly payer at the start of the first *instalment month in a later income year if:

(a) you do not satisfy the requirement in subsection 45‑138(1) for that later income year; and

(b) you give the Commissioner a notice (the MP stop notice) in the *approved form for that later income year before the start of that later income year.

(1) You satisfy the requirement in this subsection for an income year if at the start of your *MPR test day for that income year, your base assessment instalment income (within the meaning of section 45‑320) for the *base year equals or exceeds:

(a) $20 million; or

(b) if regulations made for the purposes of this paragraph specify a different amount—that amount.

(2) However, you do not satisfy the requirement in subsection (1) for an income year if, at the start of your *MPR test day for that income year:

(a) you have (or, if you are a *member of a *GST group, the *representative member of the GST group has) an obligation to give the Commissioner a *GST return for a quarterly *tax period; and

(b) you are not the *head company of a *consolidated group nor the *provisional head company of a *MEC group; and

(c) your base assessment instalment income (within the meaning of section 45‑320) for the *base year is less than $100 million.

(3) For the purposes of subsections (1) and (2), at the start of an entity’s *MPR test day:

(a) determine the amount of the entity’s base assessment instalment income (within the meaning of section 45‑320) for the *base year only on the basis of the information provided by the Commissioner to the entity before that start of that day; and

(b) in determining on that day whether an entity has an obligation mentioned in paragraph (2)(a), disregard any creation or removal of such an obligation after that day (even if that change is made retrospective to that day).

(4) An entity’s MPR test day for an income year is:

(a) if the Commissioner gives the entity an instalment rate for the first time during an *instalment month in the income year—the last day of that month; or

(b) otherwise—the first day of the third last month of the previous income year.

(5) Subsection (6) applies if, disregarding that subsection, an entity does not satisfy the requirement in subsection (1) for an income year.

(6) For the purposes of this section, in determining the entity’s base assessment instalment income (within the meaning of section 45‑320) for the *base year:

(a) disregard subsection 45‑120(2C); and

(b) disregard paragraph (3)(a) of this section, to the extent that that paragraph relates to the operation of subsection 45‑120(2C).

(7) If, because of subsection (6), the entity satisfies the requirement in subsection (1) for an income year, the entity must give the Commissioner a notice in the *approved form in respect of that income year before:

(a) if the *starting instalment month in the income year is determined under paragraph 45‑136(2)(a)—the end of that starting instalment month; or

(b) if the starting instalment month in the income year is determined under paragraph 45‑136(2)(b)—the start of that starting instalment month.

20 Subdivision 45‑F in Schedule 1 (heading)

Repeal the heading, substitute:

21 Section 45‑200 in Schedule 1

Before “This”, insert “(1)”.

22 At the end of section 45‑200 in Schedule 1

Add:

(2) If you are a *monthly payer, this Subdivision has effect in relation to you in respect of an *instalment month in the same way in which it has effect in relation to a *quarterly payer in respect of an *instalment quarter.

23 At the end of section 45‑205 in Schedule 1

Add:

(5) Subsection (6) applies if you are a monthly payer.

(6) Treat the references in subsections (1) and (4) to section 45‑110 as instead being references to section 45‑114.

24 Before section 45‑230 in Schedule 1

Insert:

If you are a *monthly payer, this Subdivision has effect in relation to you in respect of an *instalment month in the same way in which it has effect in relation to a *quarterly payer in respect of an *instalment quarter.

25 After section 45‑595 in Schedule 1

Insert:

This Subdivision has effect in relation to an *instalment month in the same way in which it has effect in relation to an *instalment quarter.

26 Before section 45‑705 in Schedule 1

Insert:

(1) If:

(a) a company is the *head company of a *consolidated group; and

(b) the company is a *monthly payer;

this Subdivision and Subdivision 45‑R have effect in relation to the company as the head company of the group in respect of an *instalment month in the same way in which they have effect in relation to a company that is a *quarterly payer as the head company of a consolidated group in respect of an *instalment quarter.

(2) If:

(a) an entity is a *subsidiary member of a *consolidated group; and

(b) the entity is a *monthly payer;

this Subdivision and Subdivision 45‑R have effect in relation to the entity in respect of an *instalment month in the same way in which they have effect in relation to an entity that is a *quarterly payer in respect of an *instalment quarter.

(3) However, those effects are subject to any modifications set out in those Subdivisions.

Note: Subdivision 45‑S can also have effect in relation to a monthly payer because of the operation of this section and section 45‑910.

27 After subsection 45‑705(4) in Schedule 1

Insert:

When the period begins—modified timing for head company that is monthly payer

(4A) Subsection (4B) applies if:

(a) apart from subsection (4B), this Subdivision starts to apply to a company as the *head company of a *consolidated group at a particular time because of the operation of subsection (2), (3) or (4); and

(b) the company is a *monthly payer; and

(c) the Commissioner gave the *initial head company instalment rate as mentioned in subsection (2), subparagraph (3)(c)(ii), subparagraph (4)(d)(ii) or subparagraph (4)(d)(iv) in an *instalment month.

(4B) Treat subsection (2), (3) or (4) (as the case requires) as providing that this Subdivision starts to apply to the company as the *head company of the group at the start of the next *instalment month.

Note: For the application of this Subdivision to a monthly payer, see section 45‑703.

28 Section 45‑715 in Schedule 1

Before “If”, insert “(1)”.

29 At the end of section 45‑715 in Schedule 1

Add:

(2) Subsection (3) applies if section 45‑703 applies to the *head company of the *consolidated group (because it is a *monthly payer).

(3) Treat the reference in subsection (1) to subsection 45‑61(2) as instead being a reference to subsection 45‑67(2).

30 Paragraph 45‑860(1)(b) in Schedule 1

Omit “ends before the end”, substitute “starts before the start”.

31 At the end of section 45‑870 in Schedule 1

Add:

(5) Subsections (6) and (7) apply if:

(a) the *head company of the *consolidated group is a *monthly payer at a time in an *instalment month (the current month); and

(b) any of the other *members of the group (the subsidiary quarterly payers) are *quarterly payers at a time in the *instalment quarter (the current quarter) in which the current month starts.

(6) Apply the following rules:

(a) treat the reference in subsection (1) to an *instalment quarter as being a reference to the current month;

(b) treat the references in this section to that quarter (or that instalment quarter) as being references to the current month.

(7) Also apply the following rules, for the purposes of subsections (1) to (5):

(a) treat the subsidiary quarterly payers as *monthly payers for each *instalment month (a notional instalment month) that starts (disregarding paragraph (6)(a)) in the current quarter;

(b) apply this section separately in relation to each of those notional instalment months;

(c) treat the amount of instalment or credit for a subsidiary quarterly payer in respect of a notional instalment month as being the extent to which the amount of instalment or credit for the subsidiary quarterly payer for the current quarter is attributable to that notional instalment month.

32 After subsection 45‑915(4) in Schedule 1

Insert:

When the period begins—modified timing for provisional head company that is monthly payer

(4A) Subsection (4B) applies if:

(a) apart from subsection (4B), Subdivision 45‑Q starts to apply to a company as the *provisional head company of a *MEC group at a particular time because of the operation of subsection (2), (3) or (4); and

(b) the company is a *monthly payer; and

(c) the Commissioner gave the *initial head company instalment rate as mentioned in subsection (2), subparagraph (3)(c)(ii), subparagraph (4)(b)(ii) or subparagraph (4)(b)(iv) in an *instalment month.

(4B) Treat subsection (2), (3) or (4) (as the case requires) as providing that Subdivision 45‑Q starts to apply to the company as the *provisional head company of the *MEC group at the start of the next *instalment month.

Note: For the application of this Subdivision to a monthly payer, see sections 45‑703 and 45‑910.

33 Subsection 250‑10(2) in Schedule 1 (after table item 115)

Insert:

115A | monthly PAYG instalment | 45‑67 in Schedule 1 | Taxation Administration Act 1953 |

34 After paragraph 288‑10(a) in Schedule 1

Insert:

(aa) under subsection 45‑20(2A) in this Schedule, is required to give a notification electronically; or

35 Subsection 288‑10(a) in Schedule 1

Omit “lodges or notifies”, substitute “lodges, gives or notifies”.

36 Paragraph 288‑20(b) in Schedule 1

After “or subsection 16‑85(1)”, insert “or section 45‑72”.

37 Subsection 721‑10(2) (after table item 30)

Insert:

32 | section 45‑67 in Schedule 1 to the Taxation Administration Act 1953 (monthly *PAYG instalment) | the *instalment month to which the *instalment relates |

38 After subsection 721‑10(3)

Insert:

(3A) Item 32 of the table in subsection (2) is taken not to include a *PAYG instalment of the *head company if the Commissioner gave the head company its *initial head company instalment rate on or after the start of the *instalment month of the head company to which the PAYG instalment relates.

39 Subsection 721‑10(2) (table item 45)

Repeal the item, substitute:

45 | subsection 45‑230(4) in Schedule 1 to the Taxation Administration Act 1953 (general interest charge on shortfall in instalment worked out on basis of varied rate) | the *instalment quarter or *instalment month to which the general interest charge relates |

40 Subsection 721‑10(2) (table item 60)

Repeal the item, substitute:

60 | subsection 45‑875(2) in Schedule 1 to the Taxation Administration Act 1953 (head company’s liability to GIC on shortfall in instalment) | the *instalment quarter or *instalment month to which the general interest charge relates |

41 Subsection 995‑1(1)

Insert:

instalment month has the meaning given by section 45‑65 in Schedule 1 to the Taxation Administration Act 1953.

42 Subsection 995‑1(1)

Insert:

monthly payer has the meaning given by section 45‑136 in Schedule 1 to the Taxation Administration Act 1953.

43 Subsection 995‑1(1)

Insert:

MPR test day has the meaning given by subsection 45‑138(4) in Schedule 1 to the Taxation Administration Act 1953.

44 Subsection 995‑1(1) (definition of quarterly payer)

Omit “*annual payer”, substitute “*annual payer or *monthly payer”.

45 General application of amendments

The amendments made by this Schedule apply to starting instalment months that start on or after 1 January 2014.

46 Delayed application to non‑corporate tax entities

Despite subsection 45‑138(1) in Schedule 1 to the Taxation Administration Act 1953, an entity cannot be a monthly payer at a time if:

(a) the entity is not a corporate tax entity at the time; and

(b) the time is before 1 January 2016.

47 Transitional MPR thresholds

(1) Subitem (2) applies if an entity is a corporate tax entity.

(2) If the entity’s MPR test day for an income year mentioned in subsection 45‑138(1) in Schedule 1 to the Taxation Administration Act 1953 is before 1 October 2015, treat the reference in paragraph (a) of that subsection to $20 million as a reference to:

(a) if that MPR test day is before 1 October 2014—$1 billion; or

(b) otherwise—$100 million.

(3) Subitem (4) applies if an entity is not a corporate tax entity.

(4) If the entity’s MPR test day for an income year mentioned in subsection 45‑138(1) in Schedule 1 to the Taxation Administration Act 1953 is before 1 October 2016, treat the reference in paragraph (a) of that subsection to $20 million as a reference to $1 billion.

(5) Disregard subitems (2) and (4) for the purposes of subsection 45‑136(4) in Schedule 1 to the Taxation Administration Act 1953 (MP stop notice).

48 Additional MPR test days

(1) This item applies if:

(a) (apart from this item) there is a time in an income year when you are not a monthly payer; and

(b) either:

(i) if you are a corporate tax entity at the time—the income year includes 1 January 2014, 1 January 2015 or 1 January 2016; or

(ii) if you are not a corporate tax entity at the time—the income year includes 1 January 2016 or 1 January 2017.

Note: This item may have a separate application for each of a number of income years.

(a) in a case where subparagraph (1)(b)(i) applies:

(i) if the income year includes 1 January 2014—1 October 2013; or

(ii) if the income year includes 1 January 2015—1 October 2014; or

(iii) if the income year includes 1 January 2016—1 October 2015; or

(b) in a case where subparagraph (1)(b)(ii) applies:

(i) if the income year includes 1 January 2016—1 October 2015; or

(ii) if the income year includes 1 January 2017—1 October 2016.

(3) If you are a monthly payer at a time in an income year because of subitem (2), treat the starting instalment month in the income year as being:

(a) unless paragraph (b) applies—the first instalment month that starts on or after the following day (the application day):

(i) if subparagraph (2)(a)(i) applies—1 January 2014;

(ii) if subparagraph (2)(a)(ii) applies—1 January 2015;

(iii) if subparagraph (2)(a)(iii) applies—1 January 2016;

(iv) if subparagraph (2)(b)(i) applies—1 January 2016;

(v) if subparagraph (2)(b)(ii) applies—1 January 2017; or

(b) if:

(i) apart from subitem (2), you are a quarterly payer; and

(ii) the application day is not the first day of an instalment quarter;

the first instalment month that starts on or after the start of the next instalment quarter.

(4) If you would (apart from subitem (2)) be an annual payer and you would (apart from this subitem) become a monthly payer at a time in the income year under paragraph (3)(a):

(a) you are taken not to satisfy the requirement in subsection 45‑138(1) in Schedule 1 to the Taxation Administration Act 1953 for the income year because of the operation of subitem (2); and

(b) instead, you are taken to satisfy that requirement for the next income year.

Note: In this case, you become a monthly payer in that next income year at the time specified in subsection 45‑136(3) in Schedule 1 to the Taxation Administration Act 1953.

49 Deadline for TOFA BAII calculation notice

(1) Subitem (2) applies if an entity must give the Commissioner a notice under subsection 45‑138(7) in Schedule 1 to the Taxation Administration Act 1953 in respect of an income year because its MPR test day for that income year is treated under item 48 as being a particular day (the additional MPR test day).

(2) Despite subsection 45‑138(7) in Schedule 1 to the Taxation Administration Act 1953, the entity must give the notice before the 1 January that follows the additional MPR test day.

1 At the end of section 272‑100 in Schedule 2F

Add:

; or (f) it is a designated infrastructure project entity at the particular time.

2 Paragraph 165‑35(b)

Omit “period).”, substitute “period); or”.

3 After paragraph 165‑35(b)

Insert:

(c) the company was a *designated infrastructure project entity during the whole of the income year.

Note: See subsection 415‑35(7) if there is only part of the income year during which the company was a designated infrastructure project entity.

4 At the end of Part 3‑45

Add:

Table of Subdivisions

Guide to Division 415

415‑A Object of this Division

415‑B Tax losses and bad debts

415‑C Designating infrastructure projects

This Division provides for special treatment for tax losses and bad debts for certain entities (called “designated infrastructure project entities”) that carry on infrastructure projects that the Infrastructure Coordinator designates under Subdivision 415‑C.

Table of sections

415‑5 Object of this Division

The object of this Division is to reduce the disincentives for private expenditure on nationally significant infrastructure that result from the long lead times between incurring deductions for, and earning assessable income from, such expenditure.

The unutilised amounts of a designated infrastructure project entity’s tax losses are increased each year by the long term bond rate. A designated infrastructure project entity is a fixed trust or company that:

(a) carries on an infrastructure project designated under Subdivision 415‑C; and

(b) only engages, and has only ever engaged, in activities for the purposes of carrying on that designated infrastructure project.

The tests that apply in relation to tax losses and bad debts if there is a change of ownership of an entity are modified so that periods during which the entity is a designated infrastructure project entity are not tested.

The loss utilisation rules in Subdivision 707‑C do not apply if the head company of a consolidated group is a designated infrastructure project entity after another designated infrastructure project entity joins the group.

Note: The transfer rules in subsection 707‑120(1A) do not apply if a designated infrastructure project entity joins a consolidated group: see subsection 707‑120(5).

Table of sections

Uplift of tax losses

415‑15 Uplift of tax losses of designated infrastructure project entities

415‑20 Designated infrastructure project entity

Change of ownership of trusts and companies

415‑25 Tax losses of trusts

415‑30 Bad debts written off etc. by trusts

415‑35 Tax losses of companies

415‑40 Bad debts written off by companies

Consolidated groups

415‑45 Losses transferred to head companies of consolidated groups

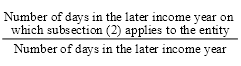

(1) The amount of a *tax loss of a *loss year of an entity is increased, at the end of each later income year (and before any *utilisation of the tax loss by the entity in the later income year), by the amount worked out using the following formula:

where:

eligible portion of the later income year means the amount worked out using the following formula:

(2) This subsection applies to the entity on a day in the later income year if:

(a) the entity is a *designated infrastructure project entity on that day; and

(b) on the day mentioned in subsection (3), the entity has notified the Commissioner (whether before, during or after the later income year) in the *approved form that the entity was, at any time, a designated infrastructure project entity.

(3) For the purposes of paragraph (2)(b), the day is the day after the latest of the following days:

(a) the day before which the entity:

(i) is required to lodge its *income tax return for the later income year with the Commissioner; or

(ii) if the entity is not required to lodge an income tax return for the later income year—would be required to lodge its income tax return for the later income year were the entity required to lodge such a return;

(b) the 28th day after the first day the entity *carries on the infrastructure project mentioned in paragraph 415‑20(1)(b);

(c) the 28th day after the day the Infrastructure Coordinator designates the infrastructure project under section 415‑70;

(d) a later day allowed by the Commissioner.

Note: The increase under this section can occur at the end of an income year even if, at the end of the year, the entity does not know the entity is a designated infrastructure project entity (e.g. because the Infrastructure Coordinator has not yet designated the infrastructure project that the entity carries on, but the Infrastructure Coordinator does so later).

Consolidated groups

(4) Disregard paragraph 701‑30(3)(a) for the purposes of the denominator in the formula in the definition of eligible portion of the later income year in subsection (1) of this section.

Note: Paragraph 701‑30(3)(a) applies if the entity becomes a subsidiary member of a consolidated group during the later income year.

(5) For the purposes of applying this section to a *tax loss the *head company of a *consolidated group makes as mentioned in subsection 707‑140(1):

(a) the head company is treated as having made the loss in the income year before the income year in which the transfer mentioned in that subsection occurs; and

(b) subsection (2) of this section is treated as not applying to the head company on or before the day the transfer occurs;

unless the transferred loss was a non‑membership period loss (within the meaning of subsection 701‑30(3)) in relation to the group.

Note: Subsection 707‑140(1) treats the head company of a consolidated group as having made a loss in an income year in which a loss is transferred to the head company from an entity that joins the group.

Total net forgiven amounts

(6) A reference in subsection (1) to any *utilisation of a *tax loss is treated as including a reference to any reduction of the loss by the application of a *total net forgiven amount.

Designated infrastructure project entity

(1) An entity is a designated infrastructure project entity at a time (the relevant time) if:

(a) at the relevant time, the entity is a *fixed trust or a company; and

(b) at or after the relevant time, the entity *carries on a single *designated infrastructure project; and

(c) the entity does not, at or before the relevant time, carry on any other designated infrastructure project; and

(d) the only activities in which the entity engages at the relevant time, or engaged before the relevant time, are or were for the purposes of the entity carrying on the single designated infrastructure project.

(2) For the purposes of this section:

(a) an *enterprise that becomes a *designated infrastructure project at a time is treated as having been a designated infrastructure project at all earlier times; and

(b) if the entity *carries on (whether or not at the same time) one or more parts, but not the whole, of a single designated infrastructure project—the parts are treated as being a single designated infrastructure project; and

(c) in any case—the following are treated as being a single designated infrastructure project:

(i) a single designated infrastructure project (the listed infrastructure project) that is included on an Infrastructure Priority List;

(ii) any designated infrastructure projects that the entity carries on (whether or not at the same time) and that are part of the listed infrastructure project; and

Note: For Infrastructure Priority Lists, see paragraph 5(2)(b) of the Infrastructure Australia Act 2008.

(d) in any case—any designated infrastructure projects that the entity carries on (whether or not at the same time) and that are part of a single infrastructure project that:

(i) is included on an Infrastructure Priority List; and

(ii) is not a designated infrastructure project;

are treated as being a single designated infrastructure project.

Partnerships

(3) Subsection (4) applies to an entity if:

(a) the entity is a *fixed trust or a company; and

(b) the person that is the trustee of the trust, or the person that is the company, is a partner in a partnership.

(4) For the purposes of subsections (1) and (2), the entity:

(a) is treated as *carrying on any *designated infrastructure project carried on by the partnership; and

(b) is treated as engaging in any activity engaged in by the partnership; and

(c) if the partnership engages in an activity for the purpose of the partnership carrying on a designated infrastructure project—is treated as engaging in that activity for the purpose of the entity carrying on that designated infrastructure project.

Consolidated groups

(5) For the purposes of working out whether the *head company of a *consolidated group was a *designated infrastructure project entity at a time (whether before or after the group consolidates), section 701‑5 (Entry history rule) is treated as not applying to the head company in relation to an entity that was not a *member of the consolidated group at that time.

(6) For the purposes of working out whether an entity is a *designated infrastructure project entity at a time after the entity ceases to be a *subsidiary member of a *consolidated group, section 701‑40 (Exit history rule) is treated as not applying to the entity in relation to the group.

Scope

(1) This section applies to a *tax loss of a *trust if the trust is a *designated infrastructure project entity at a time (the status time) in the *loss year.

Modifications of Schedule 2F to the Income Tax Assessment Act 1936

(2) Despite paragraph 266‑25(1)(b), 266‑30(a), 266‑75(1)(b) or (2)(b), 266‑80(1)(a) or (2)(a), 266‑110(1)(b), 266‑115(a), 266‑150(2)(a), 266‑155(2)(a), 267‑20(1)(b) or 267‑60(a) in Schedule 2F to the Income Tax Assessment Act 1936, for the purposes of sections 266‑40 and 266‑45, section 266‑90, subsections 266‑125(1) and (2), subsections 266‑165(1) and (2), sections 267‑40 and 267‑45 or sections 267‑70 and 267‑75 in that Schedule (whichever are applicable), the test period starts at the first time:

(a) that occurs after the status time; and

(b) at which the trust is not a *designated infrastructure project entity;

if, apart from this subsection, the test period would start earlier.

(3) For the purposes of section 267‑30 in that Schedule, disregard any part of an income year during which the trust is a *designated infrastructure project entity.

(4) For the purposes of working out, under subsection 268‑10(3), 268‑15(3) or 268‑20(3) in that Schedule, the end of the first period, disregard any part of the income year mentioned in that subsection during which the trust is a *designated infrastructure project entity.

Note: A trust does not calculate its net income and tax loss under Division 268 in that Schedule if the trust was a designated infrastructure project entity during the whole of the income year: see paragraphs 266‑30(c), 266‑80(1)(d) and (2)(c), 266‑115(b), 266‑155(2)(b), 267‑60(b) and 272‑100(f) in that Schedule.

(5) For the purposes paragraph 268‑20(4)(b) in that Schedule, disregard any part of the first of the successive periods during which the trust is a *designated infrastructure project entity.

Scope

(1) This section applies to a debt to which paragraph 266‑35(1)(a), 266‑85(1)(a) or (2)(a), 266‑120(1)(a), 266‑160(1)(a) or (b), 267‑25(1)(a) or 267‑65(1)(a) in Schedule 2F to the Income Tax Assessment Act 1936 applies, if the trust is a *designated infrastructure project entity at a time (the status time) in the income year in which the debt was incurred.

Modifications of Schedule 2F to the Income Tax Assessment Act 1936

(2) Despite paragraph 266‑35(1)(b), 266‑85(1)(b) or (2)(b), 266‑120(1)(b), 266‑160(2)(a), 267‑25(1)(b) or 267‑65(1)(a) in that Schedule, for the purposes of sections 266‑40 and 266‑45, section 266‑90, subsections 266‑125(1) and (2), subsections 266‑165(1) and (2), sections 267‑40 and 267‑45 or sections 267‑70 and 267‑75 in that Schedule (whichever are applicable), the test period starts at the first time:

(a) that occurs after the status time; and

(b) at which the trust is not a *designated infrastructure project entity.

(3) For the purposes of section 267‑30 in that Schedule, disregard any part of an income year during which the trust is a *designated infrastructure project entity.

Scope

(1) This section applies to a *tax loss of a company if the company is a *designated infrastructure project entity at a time (the status time) in the *loss year.

Modifications of Divisions 165 and 166

(2) Despite subsection 165‑12(1), 166‑5(2) or 166‑20(1), the *ownership test period or *test period under that subsection starts at the earlier of:

(a) the first time:

(i) that occurs after the status time; and

(ii) at which the company is not a *designated infrastructure project entity; and

(b) the end of the income year referred to in that subsection as the income year.

(3) In a case to which paragraph (2)(b) applies, the company is treated as meeting the conditions in section 165‑12.

(4) Despite subsection 165‑13(2), 166‑5(5), 165‑15(2) or 166‑20(4), the *same business test period under that subsection starts at the start of the *ownership test period or *test period (whichever is applicable) if, apart from this subsection, the same business test period would start earlier.

(5) Despite subsection 165‑13(2), 165‑15(3), 166‑5(6) or 166‑20(4), the *test time under that subsection occurs just after the start of the *ownership test period or *test period (whichever is applicable) if, apart from this subsection, the test time would occur earlier.

(6) A reference in subsection 165‑15(1) to the *loss year is treated as being a reference to the period:

(a) starting at the start of the *ownership test period; and

(b) ending at the end of the income year in which the ownership test period starts.

(7) For the purposes of working out, under paragraph 165‑45(3)(a) or (b) or subsection 165‑45(4), the end of the first period, disregard any part of the income year mentioned in section 165‑45 during which the company is a *designated infrastructure project entity.

Note: A company does not calculate its taxable income and tax loss under Subdivision 165‑B if the company was a designated infrastructure project entity during the whole of the income year: see paragraph 165‑35(c).

Exceptions

(8) Disregard this section for the purposes of Subdivisions 165‑CA and 165‑CB (about net capital losses) and 175‑A and 175‑CA (about tax benefits).

Scope

(1) This section applies to a debt that a company writes off as bad, if the company is a *designated infrastructure project entity at a time (the status time) in the income year in which the debt was incurred.

Modifications of Divisions 165 and 166

(2) Despite subsection 165‑123(1) or 166‑40(2), the *ownership test period or *test period under that subsection starts at the earlier of:

(a) the first time that occurs after the status time and on or after:

(i) in the case of subsection 165‑123(1)—the start of the *first continuity period; or

(ii) in the case of subsection 166‑40(2)—the time the company chooses under that subsection;

and at which the company is not a *designated infrastructure project entity; and

(b) the end of the *second continuity period.

(3) In a case to which paragraph (2)(b) applies, the company is treated as meeting the conditions in section 165‑123.

(4) Despite subsection 165‑126(2), 165‑129(2), 165‑132(1) or 166‑40(5), the *same business test period under that subsection starts at the start of the *ownership test period or *test period (whichever is applicable) if, apart from this subsection, the same business test period would start earlier.

(5) Despite subsection 165‑126(2), 165‑129(3) or 166‑40(6), the *test time under that subsection occurs just after the start of the *ownership test period or *test period (whichever is applicable) if, apart from this subsection, the test time would occur earlier.

(6) A reference in subsection 165‑129(1) to the *first continuity period is treated as being a reference to the period:

(a) starting at the start of the *ownership test period; and

(b) ending at the end of the income year in which the ownership test period starts.

Exception

(7) Disregard this section for the purposes of Subdivision 175‑C (about tax benefits).

Subdivision 707‑C (Amount of transferred losses that can be utilised) does not apply to a loss transferred under Subdivision 707‑A (Transfer of previously unutilised losses to head company), if:

(a) just before the transfer, the transferor of the loss was a *designated infrastructure project entity; and

(b) just after the transfer, the transferee of the loss is a designated infrastructure project entity.

To receive the special treatment for tax losses and bad debts under Subdivision 415‑B, an entity must only engage in activities for the purposes of carrying on an infrastructure project designated by the Infrastructure Coordinator under this Subdivision.

Designation is dependent on:

(a) criteria prescribed by the Minister; and

(b) a cap on the total estimated private capital expenditure that would be incurred for all provisionally designated and designated infrastructure projects.

Table of sections

Designating infrastructure projects

415‑55 Applications for designation

415‑60 Dealing with applications

415‑65 Provisional designation

415‑70 Designation

Infrastructure project capital expenditure cap

415‑75 Infrastructure project capital expenditure cap

415‑80 Acceptance of estimates of infrastructure project capital expenditure

Miscellaneous

415‑85 Review of decisions

415‑90 Information to be made public

415‑95 Delegation

415‑100 Infrastructure project designation rules

(1) An entity may apply to the Infrastructure Coordinator to have the Infrastructure Coordinator designate an *enterprise (the infrastructure project) that is a proposed investment in, or enhancement to, infrastructure as being an infrastructure project in relation to which Subdivision 415‑B applies.

Note: The Infrastructure Coordinator holds office under the Infrastructure Australia Act 2008.

(2) The application must include an estimate of the *infrastructure project capital expenditure that would be incurred for the purpose of the infrastructure project.

(3) Subsection (2) does not apply to *infrastructure project capital expenditure to the extent that the infrastructure project capital expenditure would be:

(a) incurred by an *Australian government agency; or

(b) funded by a grant from an Australian government agency.

(4) The application must:

(a) be in a form (if any) approved by the Infrastructure Coordinator; and

(b) be accompanied by the fee (if any) prescribed by the *infrastructure project designation rules.

Dealing with applications

(1) The Infrastructure Coordinator must deal with applications made under this Division:

(a) in accordance with the requirements prescribed by the *infrastructure project designation rules; or

(b) if the infrastructure project designation rules do not prescribe any requirements—in the order in which the applications are made.

(2) Without limiting paragraph (1)(a), the requirements the *infrastructure project designation rules may prescribe for the purposes of that paragraph include:

(a) requirements relating to the time at which or by which the Infrastructure Coordinator must deal with an application; and

(b) requirements relating to applications that, in the opinion of the Infrastructure Coordinator, are incomplete or do not contain sufficient information for the Infrastructure Coordinator to deal with the applications.

(3) For the purposes of subsection (1), the Infrastructure Coordinator deals with an application by:

(a) designating the infrastructure project provisionally under section 415‑65, or deciding not to designate the infrastructure project provisionally under that section; or

(b) designating the infrastructure project under section 415‑70 or deciding not to designate the infrastructure project under that section (whether or not the Infrastructure Coordinator has previously dealt with the application by designating the infrastructure project provisionally under section 415‑65).

(4) Paragraph (1)(b) does not apply to the Infrastructure Coordinator deciding whether to designate a *provisionally designated infrastructure project under section 415‑70.

No designation after 30 June 2017 or later prescribed day

(5) Despite anything else in this Subdivision, the Infrastructure Coordinator must not provisionally designate the infrastructure project under section 415‑65, or designate the infrastructure project under section 415‑70, after:

(a) 30 June 2017; or

(b) a later day (if any) prescribed by the *infrastructure project designation rules.

Provisional designation

(1) The Infrastructure Coordinator must, by instrument in writing, designate the infrastructure project provisionally for the purposes of this Division if:

(a) the entity applies to have the Infrastructure Coordinator designate the infrastructure project in accordance with section 415‑55; and

(b) the Infrastructure Coordinator accepts the estimate of the *infrastructure project capital expenditure under section 415‑80; and

(c) the provisional designation would not breach the infrastructure project capital expenditure cap under section 415‑75; and

(d) the following conditions are satisfied:

(i) the conditions prescribed by the *infrastructure project designation rules;

(ii) if the infrastructure project designation rules do not prescribe any conditions—in the opinion of the Infrastructure Coordinator, the infrastructure is nationally significant infrastructure (within the meaning of the Infrastructure Australia Act 2008); and

(e) the infrastructure project is not a *designated infrastructure project.

(2) The instrument of provisional designation must contain any details prescribed by the *infrastructure project designation rules.

Amendment of instruments of provisional designation

(3) The Infrastructure Coordinator must, by instrument in writing, amend the instrument of provisional designation in accordance with any requirements prescribed by the *infrastructure project designation rules. The Infrastructure Coordinator must not amend the instrument in any other circumstances.

(4) Without limiting subsection (3), the requirements the *infrastructure project designation rules may prescribe for the purposes of that subsection include requirements relating to when an amendment must take effect, which may be a time before the amendment is made.

Revocation of instruments of provisional designation

(5) The Infrastructure Coordinator must, by instrument in writing, revoke the instrument of provisional designation:

(a) if the Infrastructure Coordinator has designated the project under section 415‑70, or decides not to designate the project; or

(b) if the Infrastructure Coordinator has revoked the instrument of acceptance of the estimate under section 415‑80; or

(c) in the circumstances (if any) prescribed by the *infrastructure project designation rules.

The Infrastructure Coordinator must not revoke the instrument in any other circumstances.

(6) Without limiting paragraph (5)(c), the circumstances the *infrastructure project designation rules may prescribe for the purposes of that paragraph include:

(a) circumstances involving a failure by a prescribed entity to give prescribed information to the Infrastructure Coordinator; and

(b) circumstances involving a breach of conditions set by the Infrastructure Coordinator for the *provisionally designated infrastructure project to remain provisionally designated.

(7) The *infrastructure project designation rules must prescribe matters to which the Infrastructure Coordinator must have regard in setting conditions for a *provisionally designated infrastructure project to remain provisionally designated, if the infrastructure project designation rules provide for the Infrastructure Coordinator to set such conditions, as mentioned in paragraph (6)(b).

Designation

(1) The Infrastructure Coordinator must, by instrument in writing, designate the infrastructure project for the purposes of this Division if:

(a) the entity applies to have the Infrastructure Coordinator designate the infrastructure project in accordance with section 415‑55; and

(b) the Infrastructure Coordinator accepts the estimate of the *infrastructure project capital expenditure under section 415‑80; and

(c) the designation would not breach the infrastructure project capital expenditure cap under section 415‑75; and

(d) the following conditions are satisfied:

(i) the conditions prescribed by the *infrastructure project designation rules;

(ii) if the infrastructure project designation rules do not prescribe any conditions—the conditions mentioned in subsection (2);

(whether or not the infrastructure project is a *provisionally designated infrastructure project).

(2) For the purposes of subparagraph (1)(d)(ii), the following are the conditions:

(a) in the opinion of the Infrastructure Coordinator, the infrastructure is nationally significant infrastructure (within the meaning of the Infrastructure Australia Act 2008);

(b) in the opinion of the Infrastructure Coordinator, financial close on the infrastructure project has occurred or is imminent.

(3) The instrument of designation must contain any details prescribed by the *infrastructure project designation rules.

Amendment of instruments of designation

(4) The Infrastructure Coordinator must, by instrument in writing, amend the instrument of designation in accordance with any requirements prescribed by the *infrastructure project designation rules. The Infrastructure Coordinator must not amend the instrument in any other circumstances.

(5) Without limiting subsection (4), the requirements the *infrastructure project designation rules may prescribe for the purposes of that subsection include requirements relating to when an amendment must take effect, which may be a time before the amendment is made.

Revocation of instruments of designation

(6) The Infrastructure Coordinator must, by instrument in writing, revoke the instrument of designation in the circumstances prescribed by the *infrastructure project designation rules. The Infrastructure Coordinator must not revoke the instrument in any other circumstances.

(7) Without limiting subsection (6), the circumstances the *infrastructure project designation rules may prescribe for the purposes of that subsection include:

(a) circumstances involving a failure by a prescribed entity to give prescribed information to the Infrastructure Coordinator; and

(b) circumstances involving a breach of conditions set by the Infrastructure Coordinator for the *designated infrastructure project to remain designated.

(8) The *infrastructure project designation rules must prescribe matters to which the Infrastructure Coordinator must have regard in setting conditions for a *designated infrastructure project to remain designated, if the infrastructure project designation rules provide for the Infrastructure Coordinator to set such conditions, as mentioned in paragraph (7)(b).

Infrastructure Coordinator must notify Commissioner

(9) The Infrastructure Coordinator must notify the Commissioner of a decision made by the Infrastructure Coordinator:

(a) to designate the infrastructure project; or

(b) to amend or to revoke the instrument of designation;

within 28 days after making the decision.

(1) Provisional designation, or designation, of the infrastructure project would breach the *infrastructure project capital expenditure cap under this section if, were the provisional designation or designation to occur, the total of the estimates accepted under section 415‑80 for each infrastructure project that, just after the provisional designation or designation, would be:

(a) a *provisionally designated infrastructure project; or

(b) a *designated infrastructure project;

would exceed the amount mentioned in subsection (2).

(2) The amount is:

(a) $25 billion; or

(b) if the *infrastructure project designation rules prescribe a greater amount—that prescribed amount.

(3) For the purposes of subsection (1), disregard so much of the amount of an estimate for an infrastructure project (the listed infrastructure project) as relates to a part of the listed infrastructure project, if:

(a) that part of the listed project is (or would be, were the provisional designation or designation mentioned in that subsection to occur):

(i) a *provisionally designated infrastructure project; or

(ii) a *designated infrastructure project; and

(b) the listed infrastructure project is included on an Infrastructure Priority List.

Note: For Infrastructure Priority Lists, see paragraph 5(2)(b) of the Infrastructure Australia Act 2008.

(4) In this Act:

infrastructure project capital expenditure:

(a) has the meaning given by the *infrastructure project designation rules; or

(b) if the infrastructure project designation rules do not give infrastructure project capital expenditure a meaning—means capital expenditure.

Acceptance of estimates

(1) The Infrastructure Coordinator must, by instrument in writing, accept the estimate of *infrastructure project capital expenditure if the following conditions are satisfied:

(a) the conditions prescribed by the *infrastructure project designation rules;

(b) if the infrastructure project designation rules do not prescribe any conditions—in the opinion of the Infrastructure Coordinator, the estimate is acceptable.

Revocation of instruments of acceptance

(2) The Infrastructure Coordinator must not revoke the instrument of acceptance if the infrastructure project is a *designated infrastructure project.

(3) Subject to subsection (2), the Infrastructure Coordinator must, by instrument in writing, revoke the instrument of acceptance in the circumstances prescribed by the *infrastructure project designation rules. The Infrastructure Coordinator must not revoke the instrument in any other circumstances.

(4) Without limiting subsection (3), the circumstances the *infrastructure project designation rules may prescribe for the purposes of that subsection include:

(a) circumstances involving a failure by a prescribed entity to give prescribed information to the Infrastructure Coordinator; and

(b) circumstances involving a failure by the applicant to amend the estimate in accordance with a request made by the Infrastructure Coordinator.

(5) The *infrastructure project designation rules must prescribe matters to which the Infrastructure Coordinator must have regard in requesting the applicant to amend the estimate, if the infrastructure project designation rules provide for the Infrastructure Coordinator to make such requests as mentioned in paragraph (4)(b).

(6) If:

(a) the *infrastructure project designation rules provide for the Infrastructure Coordinator to request the applicant to amend the estimate; and

(b) the applicant amends the estimate in accordance with such a request;

the acceptance is treated, from the time the amendment is made, as being an acceptance of the amended estimate.

Applications may be made to the *AAT for review of the following decisions of the Infrastructure Coordinator:

(a) a decision not to designate the infrastructure project provisionally under section 415‑65;

(b) a decision to amend or revoke the instrument of provisional designation under section 415‑65;

(c) a decision not to designate the infrastructure project under section 415‑70;

(d) a decision to amend or revoke the instrument of designation under section 415‑70.

The Infrastructure Coordinator must comply with any requirements prescribed by the *infrastructure project designation rules in relation to the publication of information about:

(a) *provisionally designated infrastructure projects and *designated infrastructure projects; and

(b) the *infrastructure project capital expenditure cap under section 415‑75.

The Infrastructure Coordinator may, by instrument in writing, delegate any of the Infrastructure Coordinator’s powers or functions under this Subdivision to an SES employee, or acting SES employee, who is a member of the staff assisting the Infrastructure Coordinator as mentioned in section 39 of the Infrastructure Australia Act 2008.

(1) The Minister may, by legislative instrument, make rules (the infrastructure project designation rules) prescribing matters:

(a) required or permitted by this Subdivision to be prescribed by the rules; or

(b) necessary or convenient to be prescribed for carrying out or giving effect to this Subdivision.

(2) Despite subsection 14(2) of the Legislative Instruments Act 2003, the *infrastructure project designation rules may make provision in relation to a matter by applying, adopting or incorporating any matter contained in an instrument, or other writing, made by Infrastructure Australia as in force or existing from time to time.

5 At the end of section 707‑120

Add:

Designated infrastructure project entities

(5) Despite subsection (1A), the loss is transferred under subsection (1) to the full extent if:

(a) the loss is a *tax loss; and

(b) the joining entity is a *designated infrastructure project entity:

(i) at a time in the *loss year; and

(ii) just before the joining time.

6 After subsection 719‑265(3)

Insert:

Transfer of tax loss from designated infrastructure project entity

(3A) If:

(a) the focal company made the loss because the loss was transferred under Subdivision 707‑A to the focal company as the *head company of a *MEC group; and

(b) subsection 707‑120(5) (about designated infrastructure project entities joining consolidated groups) applies to the transfer;

the test company for the focal company is the company that was the *top company for the MEC group at the time of a transfer.

7 At the end of section 266‑15 in Schedule 2F

Add:

Note: The exceptions mentioned in this section apply differently in relation to designated infrastructure project entities: see sections 415‑25 and 415‑30 of the Income Tax Assessment Act 1997.

8 At the end of section 266‑30 in Schedule 2F

Add:

Note: See section 415‑25 of the Income Tax Assessment Act 1997 if the trust was a designated infrastructure project entity during part, but not the whole, of the test period.

9 At the end of section 266‑65 in Schedule 2F

Add:

Note: The exception mentioned in this section applies differently in relation to designated infrastructure project entities: see sections 415‑25 and 415‑30 of the Income Tax Assessment Act 1997.

10 At the end of section 266‑80 in Schedule 2F

Add:

Note: See section 415‑25 of the Income Tax Assessment Act 1997 if the trust was a designated infrastructure project entity during part, but not the whole, of the test period.

11 At the end of section 266‑100 in Schedule 2F

Add:

Note: The exceptions mentioned in this section apply differently in relation to designated infrastructure project entities: see sections 415‑25 and 415‑30 of the Income Tax Assessment Act 1997.

12 At the end of section 266‑115 in Schedule 2F

Add:

Note: See section 415‑25 of the Income Tax Assessment Act 1997 if the trust was a designated infrastructure project entity during part, but not the whole, of the test period.

13 At the end of section 266‑140 in Schedule 2F

Add:

Note: The exceptions mentioned in this section apply differently in relation to designated infrastructure project entities: see sections 415‑25 and 415‑30 of the Income Tax Assessment Act 1997.

14 At the end of section 266‑155 in Schedule 2F

Add:

Note: See section 415‑25 of the Income Tax Assessment Act 1997 if the trust was a designated infrastructure project entity during part, but not the whole, of the test period.

15 At the end of section 267‑15 in Schedule 2F

Add:

Note: The exceptions mentioned in this section apply differently in relation to designated infrastructure project entities: see sections 415‑25 and 415‑30 of the Income Tax Assessment Act 1997.

16 At the end of section 267‑55 in Schedule 2F

Add:

Note: The exceptions mentioned in this section apply differently in relation to designated infrastructure project entities: see sections 415‑25 and 415‑30 of the Income Tax Assessment Act 1997.

17 At the end of section 267‑60 in Schedule 2F

Add:

Note: See section 415‑25 of the Income Tax Assessment Act 1997 if the trust was a designated infrastructure project entity during part, but not the whole, of the test period.

18 Subsection 268‑20(4) in Schedule 2F

Repeal the subsection, substitute:

(4) However, what would, apart from this subsection, be 2 or more successive periods are treated as a single period if:

(a) the trust is a listed widely held trust; and

(b) during all of the periods the trust passed the same business test in relation to the time immediately before the end of the first of the successive periods.

19 Subsection 272‑140(1) in Schedule 2F

Insert:

designated infrastructure project entity has the meaning given by the Income Tax Assessment Act 1997.

20 Subsection 272‑140(1) in Schedule 2F (at the end of paragraph (c) of the definition of tax loss)

Add “(including such a tax loss as increased under section 415‑15 of that Act)”.

21 Section 12‑5 (table item headed “financial arrangements”)

Omit “borrowings”.

22 Section 12‑5 (table item headed “infrastructure borrowings”)

Repeal the item, substitute:

infrastructure |

|

infrastructure borrowings ..................... | 159GZZZZD to 159GZZZZH |

see also tax losses |

|

23 Section 12‑5 (table item headed “interest”)

Omit “borrowings”.

24 Section 12‑5 (table item headed “tax losses”)

After:

change of ownership or control of a company |

|

generally ......................... | Division 165 |

for earlier income years ............... | Subdivision 165‑A |

for income year of the change ........... | Subdivision 165‑B |

insert:

designated infrastructure project entities ........... | Division 415 |

25 Section 36‑25 (at the end of the table dealing with tax losses of companies)

Add:

6. | A company is a designated infrastructure project entity. | Subdivision 415‑B |

26 Section 36‑25 (at the end of the table dealing with tax losses of trusts)

Add:

3. | A trust is a designated infrastructure project entity. | Subdivision 415‑B |

27 At the end of section 165‑5

Add:

Note: The exceptions mentioned in this section apply differently in relation to designated infrastructure project entities: see section 415‑35.

28 At the end of section 165‑117

Add:

Note: The exceptions mentioned in this section apply differently in relation to designated infrastructure project entities: see section 415‑40.

29 Subsection 707‑120(1)

Repeal the subsection, substitute:

Transfer of loss from joining entity to head company

(1) Subject to subsection (1A), the loss is transferred at the joining time from the joining entity to the *head company of the joined group (even if they are the same entity).

(1A) The loss is transferred under subsection (1) only to the extent (if any) that the loss could have been *utilised by the joining entity for an income year consisting of the *trial year if:

(a) at the joining time, the joining entity had not become a *member of the joined group (but had been a *wholly‑owned subsidiary of the *head company if the joining entity is not the head company); and

(b) the amount of the loss that could be utilised for the trial year were not limited by the joining entity’s income or gains for the trial year.

30 Paragraph 707‑125(1)(b)

Omit “subsection 707‑120(1)”, substitute “section 707‑120”.

31 Subsection 707‑130(1)

Omit “subsection 707‑120(1)”, substitute “section 707‑120”.

32 At the end of section 707‑300

Add:

Note: This Subdivision does not apply if the joining entity is a designated infrastructure project entity just before the transfer and the head company is a designated infrastructure project entity just after the transfer: see section 415‑45.

33 Paragraph 719‑265(1)(a)

After “(3),”, insert “(3A),”.

34 Subsection 719‑265(7)

After “(3),”, insert “(3A),”.

35 Subsection 995‑1(1)

Insert:

designated infrastructure project means an infrastructure project designated under section 415‑70.

designated infrastructure project entity has the meaning given by section 415‑20.

infrastructure project capital expenditure has the meaning given by subsection 415‑75(4).

infrastructure project designation rules has the meaning given by section 415‑100.

36 Subsection 995‑1(1) (at the end of the definition of ownership test period)

Add “, and affected by sections 415‑35 and 415‑40”.

37 Subsection 995‑1(1)

Insert:

provisionally designated infrastructure project means an infrastructure project designated provisionally under section 415‑65.

38 Subsection 995‑1(1) (definition of same business test period)

Omit “section 707‑400”, substitute “sections 415‑35, 415‑40 and 707‑400”.

39 Subsection 995‑1(1) (paragraph (a) of the definition of tax loss)

After “this Act”, insert “(including such a tax loss as increased under section 415‑15)”.

40 Subsection 995‑1(1) (at the end of paragraph (d) of the definition of tax loss)

Add “(including such a tax loss as increased under section 415‑15 of this Act)”.

41 Subsection 995‑1(1) (at the end of the definition of test period)

Add “, and affected by sections 415‑35 and 415‑40”.

42 Subsection 995‑1(1) (at the end of the definition of test time)

Add “, and affected by sections 415‑35 and 415‑40”.

43 Subsection 28(2)

Repeal the subsection, substitute:

(2) The Infrastructure Coordinator has the following additional functions:

(a) any functions that the Minister, by writing, directs the Infrastructure Coordinator to perform;

(b) any other functions conferred on the Infrastructure Coordinator by this Act or any other law.

44 Subsections 28(3) and (4)

Omit “subsection (2)”, substitute “paragraph (2)(a)”.

45 Subsection 40(1)

Omit “subsection 28(2)”, substitute “paragraph 28(2)(a)”.

46 Saving provision—directions

A direction:

(a) made under subsection 28(2) of the Infrastructure Australia Act 2008; and

(b) in force just before the commencement of this item;

has effect, from that commencement, as if it had been made under paragraph 28(2)(a) of that Act, as amended by this Schedule.

47 At the end of Part 3‑45

Add:

Table of Subdivisions