Excise Act 1901

NOTICE OF INTENTION TO PROPOSE EXCISE TARIFF ALTERATION

Notice No. 4 (2013)

Pursuant to section 160B of the Excise Act 1901, I, James O’Halloran, Deputy Commissioner of Taxation, hereby give notice that it is intended, within seven sitting days of the House of Representatives after the date of publication of this Notice in the Gazette, to propose in the Parliament an Excise Tariff alteration in accordance with the following particulars and operating as follows:

1. That the Excise Tariff Act 1921 be altered as set out in Schedule 1 to this Notice, that the alterations operate on and after 1 December 2013 and that:

(a) in the case of the alterations set out in Part 1 of that Schedule—the alterations apply in relation to goods entered for home consumption on or after 1 December 2013; and

(b) in the case of the alterations set out in Part 2 of that Schedule:

(i) section 6A of the Excise Tariff Act 1921, as altered by that Part, applies in relation to the indexation day that is 1 February 2014 and each later indexation day; and

(ii) section 6AA of the Excise Tariff Act 1921, as altered by that Part, applies in relation to the indexation day that is 1 March 2014 and each later indexation day.

Schedule 1—Alterations to the Excise Tariff Act 1921

Part 1—Increase in tobacco duty rates on 1 December 2013

1 Schedule (cell at table subitem 5.1, column headed “Rate of Duty”)

Repeal the cell, substitute:

$0.40197 per stick |

2 Schedule (cell at table subitem 5.5, column headed “Rate of Duty”)

Repeal the cell, substitute:

$502.48 per kilogram of tobacco content |

3 Section 6A

Repeal the section, substitute:

6A Indexation of alcohol duty rates

(1) If the indexation factor for an indexation day is greater than 1, each rate of duty set out in item 1, 2 or 3 of the Schedule (each alcohol duty rate) is, on that day, replaced by the rate of duty worked out using the formula:

Note: For indexation factor see subsection (3) and for indexation day see subsection (10).

(2) The amount worked out under subsection (1) is to be rounded to the same number of decimal places as the alcohol duty rate was on the day before the indexation day (rounding up if the next decimal place is 5 or more).

Indexation factor

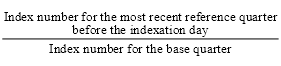

(3) The indexation factor for an indexation day is the number worked out using the formula:

Note: For index number, reference quarter and base quarter see subsection (10).

(4) The indexation factor is to be worked out to 3 decimal places (rounding up if the fourth decimal place is 5 or more).

Effect of delay in publication of index number

(5) If the index number for the most recent reference quarter before the indexation day is published by the Statistician on a day (the publication day) that is not at least 5 days before the indexation day, then, despite subsection (1), any replacement of an alcohol duty rate under subsection (1) happens on the fifth day after the publication day.

Effect of Excise Tariff alteration

(6) If an Excise Tariff alteration proposed in the Parliament proposes to substitute, on and after a particular day, a rate for an alcohol duty rate, treat that substitution as having had effect on and after that day for the purposes of this section.

Changes to CPI index reference period and publication of substituted index numbers

(7) Amounts are to be worked out under this section:

(a) using only the index numbers published in terms of the most recently published index reference period for the Consumer Price Index; and

(b) disregarding index numbers published in substitution for previously published index numbers (except where the substituted numbers are published to take account of changes in the index reference period).

Application of replacement rate

(8) If an alcohol duty rate is replaced under this section on a particular day, the replacement rate applies in relation to goods entered for home consumption on or after that day.

Publication of replacement rate

(9) The CEO must, on or as soon as practicable after the day an alcohol duty rate is replaced under this section, publish a notice in the Gazette advertising the replacement rate and the goods it applies to.

Definitions

(10) In this section:

base quarter means the June quarter or December quarter that has the highest index number of all the June quarters and December quarters that occur:

(a) before the most recent reference quarter before the indexation day; and

(b) after the June quarter of 1983.

December quarter means a period of 3 months starting on 1 October.

indexation day means each 1 February and 1 August.

index number, for a quarter, means the All Groups Consumer Price Index number that is the weighted average of the 8 capital cities and is published by the Statistician in relation to that quarter.

June quarter means a period of 3 months starting on 1 April.

reference quarter means the June quarter or December quarter.

6AA Indexation of tobacco duty rates

(1) If the indexation factor for an indexation day is at least 1, each rate of duty set out in item 5 of the Schedule (each tobacco duty rate) is, on that day, replaced by the rate of duty worked out using the formula:

Note: For indexation factor see subsections (3) and (5), for indexation day see subsection (12) and for additional factor see subsection (6).

(2) The amount worked out under subsection (1) is to be rounded to the same number of decimal places as the tobacco duty rate was on the day before the indexation day (rounding up if the next decimal place is 5 or more).

Indexation factor

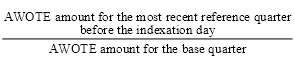

(3) The indexation factor for an indexation day is the number worked out using the formula:

Note: For AWOTE amount, reference quarter and base quarter see subsection (12).

(4) The indexation factor is to be worked out to 3 decimal places (rounding up if the fourth decimal place is 5 or more).

(5) Despite subsection (3), treat the indexation factor for 1 September 2014, 1 September 2015 or 1 September 2016 as 1 if, on that day, it would otherwise be less than 1.

Additional factor

(6) The additional factor for an indexation day is:

(a) 1.125, if the indexation day is 1 September 2014, 1 September 2015 or 1 September 2016; or

(b) 1, for each other indexation day.

Effect of delay in publication of AWOTE amount

(7) If the AWOTE amount for the most recent reference quarter before the indexation day is published by the Statistician on a day (the publication day) that is not at least 5 days before the indexation day, then, despite subsection (1), any replacement of a tobacco duty rate under subsection (1) happens on the fifth day after the publication day.

Effect of Excise Tariff alteration

(8) If an Excise Tariff alteration proposed in the Parliament proposes to substitute, on and after a particular day, a rate for a tobacco duty rate, treat that substitution as having had effect on and after that day for the purposes of this section.

Publication of substituted AWOTE amounts

(9) If the Statistician publishes an estimate of full‑time adult average weekly ordinary time earnings for persons in Australia for a period for which such an estimate was previously published by the Statistician, the publication of the later estimate is to be disregarded for the purposes of this section.

Application of replacement rate

(10) If a tobacco duty rate is replaced under this section on a particular day, the replacement rate applies in relation to goods entered for home consumption on or after that day.

Publication of replacement rate

(11) The CEO must, on or as soon as practicable after the day a tobacco duty rate is replaced under this section, publish a notice in the Gazette advertising the replacement rate and the goods it applies to.

Definitions

(12) In this section:

AWOTE amount, for a quarter, means the estimate of the full‑time adult average weekly ordinary time earnings for persons in Australia for the middle month of the quarter published by the Statistician in relation to that month.

base quarter means the June quarter or December quarter that has the highest AWOTE amount of all the June quarters and December quarters that occur:

(a) before the most recent reference quarter before the indexation day; and

(b) after the December quarter of 2012.

December quarter means a period of 3 months starting on 1 October.

indexation day means each 1 March and 1 September.

June quarter means a period of 3 months starting on 1 April.

reference quarter means the June quarter or December quarter.

4 Schedule (note 2 to Schedule heading)

After “Sections 6A,”, insert “6AA,”.

5 Schedule (table heading)

Repeal the heading, substitute:

Excise duties (subject to sections 6A, 6AA, 6FA and 6FB) |

Dated this 29th day of November 2013.

James O’Halloran

Delegate of the Commissioner of Taxation