Tax and Superannuation Laws Amendment (2014 Measures No. 6) Act 2014

No. 133, 2014

An Act to amend the law relating to taxation and grants, and for related purposes

Tax and Superannuation Laws Amendment (2014 Measures No. 6) Act 2014

No. 133, 2014

An Act to amend the law relating to taxation and grants, and for related purposes

Contents

2 Commencement

3 Schedules

4 Amendment of assessments

Schedule 1—Roll‑overs for business restructures

Part 1—Main amendments

Income Tax Assessment Act 1997

Part 2—Consequential amendments

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Petroleum Resource Rent Tax Assessment Act 1987

Taxation Administration Act 1953

Part 3—Rights under arrangements

Division 1—Disposals by a trust to a company

Income Tax Assessment Act 1997

Division 2—Transfers between certain trusts

Income Tax Assessment Act 1997

Part 4—Application and transitional provisions

Income Tax (Transitional Provisions) Act 1997

Schedule 2—MIT withholding regime for foreign pension funds

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Schedule 3—Income tax exemption for Force Posture Initiatives

Income Tax Assessment Act 1936

Schedule 4—Fuel tax credits

Fuel Tax Act 2006

Schedule 5—Energy Grants (Cleaner Fuels) Scheme

Energy Grants (Cleaner Fuels) Scheme Regulations 2004

Tax and Superannuation Laws Amendment (2014 Measures No. 6) Act 2014

No. 133, 2014

An Act to amend the law relating to taxation and grants, and for related purposes

[Assented to 12 December 2014]

The Parliament of Australia enacts:

This Act may be cited as the Tax and Superannuation Laws Amendment (2014 Measures No. 6) Act 2014.

(1) Each provision of this Act specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information | ||

Column 1 | Column 2 | Column 3 |

Provisions | Commencement | Date/Details |

1. Sections 1 to 4 and anything in this Act not elsewhere covered by this table | The day this Act receives the Royal Assent. | 12 December 2014 |

2. Schedules 1 to 3 | The day this Act receives the Royal Assent. | 12 December 2014 |

3. Schedules 4 and 5 | 10 November 2014. | 10 November 2014 |

Note: This table relates only to the provisions of this Act as originally enacted. It will not be amended to deal with any later amendments of this Act.

(2) Any information in column 3 of the table is not part of this Act. Information may be inserted in this column, or information in it may be edited, in any published version of this Act.

(1) Legislation that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

(2) The amendment of any regulation under subsection (1) does not prevent the regulation, as so amended, from being amended or repealed by the Governor‑General.

(1) Section 170 of the Income Tax Assessment Act 1936 does not prevent the amendment of an assessment if:

(a) the assessment was made before the commencement of Schedule 1 (about roll‑overs for business restructures) to this Act; and

(b) the amendment is made for the purpose of giving effect to that Schedule; and

(c) the amendment is made within 2 years after the day that Schedule commences.

(2) Section 170 of the Income Tax Assessment Act 1936 does not prevent the amendment of an assessment if:

(a) the assessment was made before the commencement of Schedule 2 (about MIT withholding regime for foreign pension funds) to this Act; and

(b) the amendment is made for the purpose of giving effect to that Schedule; and

(c) the amendment is made within 2 years after the day that Schedule commences.

Schedule 1—Roll‑overs for business restructures

Income Tax Assessment Act 1997

1 Before Division 620

Insert:

Division 615—Roll‑overs for business restructures

Table of Subdivisions

Guide to Division 615

615‑A Choosing to obtain roll‑overs

615‑B Further requirements for choosing to obtain roll‑overs

615‑C Consequences of roll‑overs

615‑D Consequences for the interposed company

615‑1 What this Division is about

You can choose for transactions under a scheme to restructure a company’s or unit trust’s business to be tax neutral if, under the scheme:

(a) you cease to own shares in the company or units in the trust; and

(b) in exchange, you become the owner of new shares in another company.

Subdivision 615‑A—Choosing to obtain roll‑overs

Table of sections

615‑5 Disposing of interests in one entity for shares in a company

615‑10 Redeeming or cancelling interests in one entity for shares in a company

615‑5 Disposing of interests in one entity for shares in a company

(1) You can choose to obtain a roll‑over if:

(a) you are a *member of a company or a unit trust (the original entity); and

(b) you and at least one other entity (the exchanging members) own all the *shares or units in it; and

(c) under a *scheme for reorganising its affairs, the exchanging members *dispose of all their shares or units in it to a company (the interposed company) in exchange for shares in the interposed company (and nothing else); and

(d) the requirements in Subdivision 615‑B are satisfied.

Note 1: For paragraph (c), see section 124‑20 if an exchanging member uses a share sale facility.

Note 2: After the completion of the scheme, later dealings between the interposed company and the original entity may be subject to the rules for consolidated groups (see Part 3‑90).

(2) You are taken to have chosen to obtain the roll‑over if:

(a) immediately before the completion time (see section 615‑15), the original entity is the *head company of a *consolidated group; and

(b) immediately after the completion time, the interposed company is the head company of the group.

Note: The consolidated group continues in existence because of section 703‑70.

615‑10 Redeeming or cancelling interests in one entity for shares in a company

(1) You can choose to obtain a roll‑over if you are a *member of a company or a unit trust (the original entity), and under a *scheme for reorganising its affairs:

(a) a company (the interposed company) *acquires no more than 5 *shares or units in the original entity; and

(b) these are the first shares or units that the interposed company acquires in the original entity; and

(c) you and at least one other entity (the exchanging members) own all the remaining shares or units in the original entity; and

(d) those remaining shares or units are redeemed or cancelled; and

(e) each exchanging member receives shares (and nothing else) in the interposed company in return for their shares or units in the original entity being redeemed or cancelled;

and the requirements in Subdivision 615‑B are satisfied.

Note: For paragraph (e), see section 124‑20 if an exchanging member uses a share sale facility.

(2) You are taken to have chosen to obtain the roll‑over if:

(a) immediately before the completion time (see section 615‑15), the original entity is the *head company of a *consolidated group; and

(b) immediately after the completion time, the interposed company is the head company of the group.

Note: The consolidated group continues in existence because of section 703‑70.

(3) The original entity, or its trustee if it is a unit trust, can issue other *shares or units to the interposed company as part of the *scheme.

Note: Some of the interposed company’s shares or units in the original entity may be taken to be acquired before 20 September 1985: see section 615‑65.

Subdivision 615‑B—Further requirements for choosing to obtain roll‑overs

Table of sections

615‑15 Interposed company must own all the original interests

615‑20 Requirements relating to your interests in the original entity

615‑25 Requirements relating to the interposed company

615‑30 Interposed company must make a particular choice

615‑35 ADI restructures—disregard certain preference shares

615‑15 Interposed company must own all the original interests

The interposed company must own all the *shares or units in the original entity immediately after the time (the completion time) all the exchanging members have had their shares or units in the original entity disposed of, redeemed or cancelled under the *scheme.

615‑20 Requirements relating to your interests in the original entity

(1) Immediately after the completion time, each exchanging member must own:

(a) a whole number of *shares in the interposed company; and

(b) a percentage of the shares in the interposed company that were issued to all the exchanging members that is equal to the percentage of the shares or units in the original entity that were:

(i) owned by the member; and

(ii) disposed of, redeemed or cancelled under the *scheme.

(2) The following ratios must be equal:

(a) the ratio of:

(i) the *market value of each exchanging member’s *shares in the interposed company; to

(ii) the market value of the shares in the interposed company issued to all the exchanging members (worked out immediately after the completion time);

(b) the ratio of:

(i) the market value of that member’s shares or units in the original entity that were disposed of, redeemed or cancelled under the *scheme; to

(ii) the market value of all the shares or units in the original entity that were disposed of, redeemed or cancelled under the scheme (worked out immediately before the first disposal, redemption or cancellation).

Example 1: There are 100 shares in A Pty Ltd (the original entity), all having the same rights. B Pty Ltd (the interposed company) acquires all the shares in A by issuing each shareholder in A 10 shares in itself for each share they have in A. All shares in B have the same rights. Bill owned 15 shares in A and received 150 shares in B in exchange.

Example 2: There are 1,000 units in the A unit trust (the original entity), all having the same rights. 2 new units in A are issued to B Pty Ltd (the interposed company), and all other units in A are cancelled. Each unitholder in A is issued 10 shares in B for each 100 units they have in A. All shares in B have the same rights. Alison owned 200 units in A and received 20 shares in B in exchange.

(3) Either:

(a) you are an Australian resident at the time your *shares or units in the original entity are disposed of, redeemed or cancelled under the *scheme; or

(b) if you are a foreign resident at that time:

(i) your shares or units in the original entity were *taxable Australian property immediately before that time; and

(ii) your shares in the interposed company are taxable Australian property immediately after the completion time.

615‑25 Requirements relating to the interposed company

(1) The *shares issued in the interposed company must not be *redeemable shares.

(2) Each exchanging member who is issued *shares in the interposed company must own the shares from the time they are issued until at least the completion time.

(3) Immediately after the completion time:

(a) the exchanging members must own all the *shares in the interposed company; or

(b) entities other than those members must own no more than 5 shares in the interposed company, and the *market value of those shares expressed as a percentage of the market value of all the shares in the interposed company must be such that it is reasonable to treat the exchanging members as owning all the shares.

615‑30 Interposed company must make a particular choice

(1) Unless subsection (2) applies, the interposed company must choose that section 615‑65 applies.

(2) The interposed company must choose that a *consolidated group continues in existence at and after the completion time with the interposed company as its *head company, if:

(a) immediately before the completion time, the consolidated group consisted of the original entity as head company and one or more other members (the other group members); and

(b) immediately after the completion time, the interposed company is the head company of a *consolidatable group consisting only of itself and the other group members.

Note: Sections 703‑65 to 703‑80 deal with the effects of the choice for the consolidated group.

(3) A choice under subsection (1) or (2) must be made:

(a) within 2 months after the completion time, if the choice is under subsection (1); or

(b) within 28 days after the completion time, if the choice is under subsection (2); or

(c) within such further time as the Commissioner allows.

The choice cannot be revoked.

(4) The way the interposed company prepares its *income tax returns is sufficient evidence of the making of the choice.

615‑35 ADI restructures—disregard certain preference shares

For the purposes of this Division, disregard any *shares in the original entity that can be disregarded under subsection 703‑37(4) if:

(a) the interposed company is a non‑operating holding company within the meaning of the Financial Sector (Business Transfer and Group Restructure) Act 1999; and

(b) a restructure instrument under Part 4A of that Act is in force in relation to the interposed company; and

(c) because of the restructure to which the instrument relates, an *ADI becomes a subsidiary (within the meaning of that Act) of the interposed company; and

(d) the original entity is:

(i) the ADI; or

(ii) part of an extended licensed entity (within the meaning of the *prudential standards) that includes the ADI.

Subdivision 615‑C—Consequences of roll‑overs

Table of sections

615‑40 CGT consequences

615‑45 Additional consequences—deferral of profit or loss

615‑50 Trading stock

615‑55 Revenue assets

615‑60 Disregard CGT exemption for trading stock

The consequences set out in Subdivision 124‑A also apply to a roll‑over under this Division as if that roll‑over were a roll‑over covered by Division 124 (about replacement‑asset roll‑overs).

Note: Those consequences generally involve:

(a) disregarding a capital gain or capital loss you make from the disposal, redemption or cancellation of your shares or units in the original entity; and

(b) working out the first element of the cost base of each of your new shares in the interposed entity by reference to the cost bases of your shares or units in the original entity.

615‑45 Additional consequences—deferral of profit or loss

The additional consequences in sections 615‑50 and 615‑55 apply if:

(a) under this Division:

(i) you are taken to have chosen to obtain the roll‑over; or

(ii) you otherwise choose to obtain the roll‑over; and

(b) if subparagraph (a)(ii) applies to you, you choose for these additional consequences to apply; and

(c) some or all of your *shares or units in the original entity at the time immediately before they were:

(i) disposed of as described in paragraph 615‑5(1)(c); or

(ii) redeemed or cancelled as described in paragraph 615‑10(1)(d);

had the character of being your *trading stock or *revenue assets; and

(d) the shares in the interposed company that you acquired in return for those shares or units have the same character.

Note 1: Apply this section separately for assets of each character.

Note 2: The CGT exemption for trading stock does not prevent you obtaining the roll‑over (see section 615‑60).

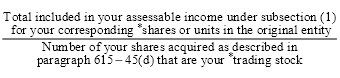

(1) The amount included in your assessable income because of the disposal, redemption or cancellation of each of your *shares or units described in paragraph 615‑45(c) that was your *trading stock at the time mentioned in that paragraph is equal to:

(a) if the share or unit had been your trading stock ever since the start of the income year that included that time—the total of:

(i) its *value as trading stock at the start of the income year; and

(ii) the amount (if any) by which its cost had increased since the start of the income year; or

(b) otherwise—its cost at that time.

(2) For each of the *shares that you acquired as described in paragraph 615‑45(d) that is your *trading stock, you are taken to have paid:

(3) For the purposes of Division 70 (about trading stock), you, the original entity and the interposed company are taken to have dealt with each other in the ordinary course of *business and at *arm’s length for each of the transactions referred to in paragraph 615‑5(1)(c) or 615‑10(1)(d) or (e).

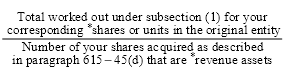

(1) For each of your *shares or units that:

(a) is described in paragraph 615‑45(c); and

(b) was a *revenue asset immediately before its disposal, redemption or cancellation;

your gross proceeds for that disposal, redemption or cancellation are taken to be the amount you would have needed to have received in order to have a nil profit and nil loss for that disposal, redemption or cancellation.

(2) For the purpose of calculating any profit or loss on a future disposal, cessation of ownership, or other realisation of a *share that:

(a) you acquired as described in paragraph 615‑45(d); and

(b) is a *revenue asset;

you are taken to have paid the following for your acquisition of that share:

615‑60 Disregard CGT exemption for trading stock

For the purposes of this Division, disregard section 118‑25 (which gives a CGT exemption for trading stock).

Subdivision 615‑D—Consequences for the interposed company

Table of sections

615‑65 Consequences for the interposed company

615‑65 Consequences for the interposed company

(1) This section applies if the interposed company so chooses under subsection 615‑30(1).

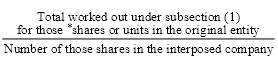

(2) A number of the *shares or units that the interposed company owns in the original entity (immediately after the completion time) are taken to have been *acquired before 20 September 1985 if any of the original entity’s assets as at the completion time were acquired by it before that day.

Note: Generally, a capital gain or capital loss you make from a CGT asset that you acquired before 20 September 1985 can be disregarded: see Division 104.

(3) That number (worked out as at the completion time) is the greatest possible whole number that (when expressed as a percentage of all the *shares or units) does not exceed:

(a) the *market value of the original entity’s assets that it *acquired before 20 September 1985; less

(b) its liabilities (if any) in respect of those assets;

expressed as a percentage of the market value of all the original entity’s assets less all of its liabilities.

(4) The first element of the *cost base of the interposed company’s *shares or units in the original entity that are not taken to have been *acquired before 20 September 1985 is:

(a) the total of the cost bases (as at the completion time) of the original entity’s assets that it acquired on or after that day; less

(b) its liabilities (if any) in respect of those assets.

The first element of the *reduced cost base of those shares or units is worked out similarly.

(5) A liability of the original entity that is not a liability in respect of a specific asset or assets of the original entity is taken to be a liability in respect of all the assets of the original entity.

Note: An example is a bank overdraft.

(6) If a liability is in respect of 2 or more assets, the proportion of the liability that is in respect of any one of those assets is equal to:

Part 2—Consequential amendments

Income Tax Assessment Act 1936

2 Section 121AS (note 5)

Omit “124‑G, 124‑H,”.

3 Section 121AS (note 5)

After “section 128‑10 or 128‑15”, insert “, or Division 615,”.

Income Tax Assessment Act 1997

4 Paragraph 103‑25(3)(a)

Repeal the paragraph.

5 Section 112‑115 (table items 9 and 10)

Repeal the items.

6 Section 112‑115 (after table item 14C)

Insert:

14D | Exchange of shares in one company for shares in an interposed company | Division 615 |

14E | Exchange of units in a unit trust for shares in a company | Division 615 |

7 Subparagraphs 124‑20(3)(a)(i) and (ii)

Repeal the subparagraphs.

8 Subparagraph 124‑20(3)(a)(v)

Omit “and”.

9 At the end of paragraph 124‑20(3)(a)

Add:

(vi) Division 615 (Roll‑overs for business restructures); and

10 Subdivisions 124‑G and 124‑H

Repeal the Subdivisions.

11 Subsection 124‑795(3)

Omit “Subdivision 124‑G”, substitute “615”.

12 Subsection 124‑795(3) (note)

Omit “Subdivision 124‑G deals with company reorganisation”, substitute “Division 615 deals with business restructures”.

13 Subsection 125‑70(5) (note)

Omit “124‑G, 124‑H or 124‑M”, substitute “or 124‑M or Division 615”.

14 Subsection 703‑5(2) (note)

Omit “124‑380(5)”, substitute “615‑30(2)”.

15 Section 703‑65

Omit “subsection 124‑380(5)”, substitute “subsection 615‑30(2)”.

16 Section 703‑65 (note)

Omit “Subdivision 124‑G”, substitute “Division 615”.

17 Section 703‑70 (heading)

Repeal the heading, substitute:

18 Subsection 703‑70(1)

Omit “124‑380(5) as the original company”, substitute “615‑30(2) as the original entity”.

19 Subsection 703‑70(2)

Omit “original company” (wherever occurring), substitute “original entity”.

20 Subsection 703‑70(2) (note)

Omit “original company’s”, substitute “original entity’s”.

21 Subsection 703‑70(3) (note)

Omit “original company”, substitute “original entity”.

22 Section 703‑75 (heading)

Repeal the heading, substitute:

23 Subsection 703‑75(1)

Omit “original company” (wherever occurring), substitute “original entity”.

24 Subsection 703‑75(1) (note)

Omit “original company’s”, substitute “original entity’s”.

25 Subsections 703‑75(2) and (3)

Omit “original company”, substitute “original entity”.

26 Section 703‑80 (heading)

Repeal the heading, substitute:

703‑80 Effects on the original entity’s tax position

27 Section 703‑80

Omit “original company” (first occurring), substitute “original entity”.

28 Section 703‑80 (note 2)

Omit “original company’s” (wherever occurring), substitute “original entity’s”.

29 Section 703‑80 (note 2)

Omit “original company”, substitute “original entity”.

Petroleum Resource Rent Tax Assessment Act 1987

30 Subsection 58T(1)

Omit “124‑380(5)” (wherever occurring), substitute “615‑30(2)”.

31 Subsections 58T(1) and (2)

Omit “original company” (wherever occurring), substitute “original entity”.

32 Subsection 58T(2) (note)

Omit “original company’s”, substitute “original entity’s”.

Taxation Administration Act 1953

33 Paragraph 45‑705(4)(a) in Schedule 1

Omit “124‑380(5)”, substitute “615‑30(2)”.

34 Subparagraphs 45‑705(4)(d)(i) and (ii) in Schedule 1

Omit “original company”, substitute “original entity”.

35 Paragraph 45‑705(5)(d) in Schedule 1

Omit “124‑380(5)”, substitute “615‑30(2)”.

36 Paragraph 45‑740(2)(a) in Schedule 1

Omit “124‑380(5)”, substitute “615‑30(2)”.

Part 3—Rights under arrangements

Division 1—Disposals by a trust to a company

Income Tax Assessment Act 1997

37 Paragraph 124‑860(4)(b)

Repeal the paragraph, substitute:

(b) has no *CGT assets, other than any or all of the following:

(i) small amounts of cash or debt;

(ii) its rights under an *arrangement, if (collectively) those rights only facilitate the transfer of assets to the transferee from the transferor; and

Division 2—Transfers between certain trusts

Income Tax Assessment Act 1997

38 Paragraph 126‑225(1)(b)

Repeal the paragraph, substitute:

(b) if subparagraph (a)(ii) applies—the receiving trust has no CGT assets immediately before the transfer time, other than any or all of the following:

(i) small amounts of cash or debt;

(ii) its rights under an *arrangement, if (collectively) those rights only facilitate the transfer of assets to it from the transferring trust; and

Part 4—Application and transitional provisions

39 Application of amendments

(1) The amendments made by Parts 1 and 2 apply in relation to shares or units disposed of, redeemed or cancelled at or after 7.30 pm, by legal time in the Australian Capital Territory, on 10 May 2011.

(2) The amendment made by Division 1 of Part 3 applies in relation to CGT events happening at or after 7.30 pm, by legal time in the Australian Capital Territory, on 10 May 2011.

(3) The amendment made by Division 2 of Part 3 applies in relation to CGT events happening on or after 1 November 2008.

40 Transitional provision—transfers between certain trusts

(1) This item applies if:

(a) a roll‑over under Subdivision 126‑G of the Income Tax Assessment Act 1997 is chosen after the commencement of this Schedule; and

(b) the transfer time (within the meaning of paragraph 126‑225(1)(a) of that Act) for the roll‑over happens during an income year ending before the commencement of this Schedule.

(2) Subsection 126‑260(1) of that Act applies to the trustee of the transferring trust as if the reference in that subsection to “within 3 months after the end of the transfer year” were a reference to “within 3 months after the time the roll‑over is chosen”.

Income Tax (Transitional Provisions) Act 1997

41 Before Division 620

Insert:

Division 615—Roll‑overs for business restructures

Table of Subdivisions

615‑A Modifications for roll‑overs between the 2011 and 2012 Budget times

Subdivision 615‑A—Modifications for roll‑overs between the 2011 and 2012 Budget times

Table of sections

615‑5 Roll‑overs between the 2011 and 2012 Budget times

615‑10 Modifications—when additional consequences can apply

615‑15 Modifications—trading stock

615‑20 Modifications—revenue assets

615‑5 Roll‑overs between the 2011 and 2012 Budget times

Subdivision 615‑C of the Income Tax Assessment Act 1997 applies to you with the modifications set out in this Subdivision if you chose to obtain a roll‑over involving *shares or units that:

(a) were disposed of, redeemed or cancelled during the period:

(i) starting at 7.30 pm, by legal time in the Australian Capital Territory, on 10 May 2011; and

(ii) ending immediately before 7.30 pm, by legal time in the Australian Capital Territory, on 8 May 2012; and

(b) were your trading stock, or revenue assets, at the time immediately before that disposal, redemption or cancellation.

615‑10 Modifications—when additional consequences can apply

(1) Disregard subparagraph 615‑45(a)(ii), and paragraph 615‑45(b), of the Income Tax Assessment Act 1997 if the roll‑over relates to *shares that were disposed of, redeemed or cancelled.

(2) Disregard paragraph 615‑45(d) of that Act.

615‑15 Modifications—trading stock

Substitute the following for subsection 615‑50(2) of that Act:

(2) For each of the *shares in the interposed company that you acquired in return for those of your shares or units in the original entity that were your *trading stock at the time mentioned in paragraph 615‑45(c), you are taken to have paid:

615‑20 Modifications—revenue assets

Substitute the following for subsection 615‑55(2) of that Act:

(2) For the purpose of calculating any profit or loss on a future disposal, cessation of ownership, or other realisation of a *share in the interposed company that you acquired in return for those of your shares or units in the original entity that were *revenue assets at the time mentioned in paragraph 615‑45(c), you are taken to have paid:

Schedule 2—MIT withholding regime for foreign pension funds

Income Tax Assessment Act 1997

1 Section 840‑800

After “beneficiary”, insert “(other than a foreign pension fund)”.

2 After subsection 840‑805(4)

Insert:

Modification—foreign pension funds

(4A) For the purposes of subsections (2), (3) and (4), if:

(a) the beneficiary, in respect of a fund payment part, is a beneficiary in the capacity of a trustee of another trust; and

(b) the beneficiary is a *foreign pension fund;

the foreign pension fund is taken, in respect of that fund payment part, to be a beneficiary in its own right, and not a beneficiary in the capacity of the trustee of another trust.

(4B) Foreign pension fund means:

(a) an entity, the principal purpose of which is to fund pensions (including disability and similar benefits) for the citizens or other contributors of a foreign country, if:

(i) the entity is a fund established by an *exempt foreign government agency; or

(ii) the entity is established under a *foreign law for an exempt foreign government agency; or

(b) a *foreign superannuation fund that has at least 50 *members.

(4C) If:

(a) a *foreign pension fund is liable to pay income tax on a fund payment part (a taxed part) because of the operation of subsection (4A); and

(b) you are a beneficiary of the foreign pension fund and are presently entitled to a share of the income or capital of the foreign pension fund;

then, in working out for the purposes of paragraph (4)(b) whether all or part of that share is reasonably attributable to a payment that is a *fund payment, disregard the taxed part.

3 Subsection 995‑1(1)

Insert:

foreign pension fund has the meaning given by subsection 840‑805(4B).

Taxation Administration Act 1953

4 At the end of section 18‑32 in Schedule 1

Add:

(3) Subsection (4) applies if:

(a) all or part of an amount (the fund payment part) is represented by a payment that is a *fund payment; and

(b) under subsection 840‑805(4A) of the Income Tax Assessment Act 1997, a *foreign pension fund is taken, in respect of the fund payment part, to be a beneficiary in its own right, and not a beneficiary in the capacity of the trustee of another trust; and

(c) there is an *amount withheld from the fund payment under Subdivision 12‑H.

(4) For the purposes of paragraph (1)(b):

(a) treat the *foreign pension fund as having borne all or part of the amount withheld; and

(b) treat a beneficiary of the foreign pension fund as not having borne all or part of the amount withheld.

5 Application

The amendments made by this Schedule apply to fund payments made in relation to the first income year starting on or after 1 July 2008 and later income years.

Schedule 3—Income tax exemption for Force Posture Initiatives

Income Tax Assessment Act 1936

1 Subsection 23AA(1) (definition of approved project)

Omit “or of the Joint Defence Space Communications Station”, substitute “, of the Joint Defence Space Communications Station or of a Force Posture Initiative”.

2 Subsection 23AA(1)

Insert:

Force Posture Agreement means the Force Posture Agreement between the Government of Australia and the Government of the United States of America done at Sydney on 12 August 2014, as amended and in force for Australia from time to time.

Note: The Treaty could in 2014 be viewed in the Australian Treaties Library on the AustLII website (http://www.austlii.edu.au).

Force Posture Initiative has the same meaning as in the Force Posture Agreement.

Note: As well as some announced initiatives, this includes future initiatives that Australia and the United States mutually decide to be Force Posture Initiatives for the purposes of that Agreement.

3 Application of amendments

The amendments made by this Schedule apply in relation to assessments for the 2014‑15 income year and later income years.

1 Subsection 43‑5(2A)

Repeal the subsection, substitute:

Day for rate of fuel tax, grant or subsidy

(2A) Work out the day using the table:

Day for rate of fuel tax, grant or subsidy | ||

| If: | The day is: |

1 | You acquired or imported the fuel | The day you acquired or imported the fuel |

2 | You: (a) manufactured the fuel; and (b) entered the fuel for home consumption (within the meaning of the Excise Act 1901) | The day you entered the fuel for home consumption (within the meaning of the Excise Act 1901) |

Note: Division 65 sets out which tax period a credit is attributable to.

2 After section 43‑5

Insert:

(1) Fuel tax is duty that is payable on fuel under:

(a) the Excise Act 1901 and the Excise Tariff Act 1921; or

(b) the Customs Act 1901 and the Customs Tariff Act 1995;

other than any duty that is expressed as a percentage of the value of fuel for the purposes of section 9 of the Customs Tariff Act 1995.

(2) For the purposes of subsection (1), if:

(a) an Excise Tariff alteration, proposed by a motion moved in the House of Representatives, relates to duty payable on fuel; or

(b) a Customs Tariff alteration, proposed by a motion moved in the House of Representatives, relates to duty payable on fuel;

the alteration is taken to have effect as if it is an amendment of the Act it proposes to alter, and as if that amendment is in force.

(3) However, the alteration ceases to be taken to have that effect unless, before whichever of the following first happens:

(a) the close of the session in which the Excise Tariff alteration or Customs Tariff alteration, is proposed;

(b) the expiration of 12 months after the Excise Tariff alteration or Customs Tariff alteration, is proposed;

one or more amendments of an Act come into force that have the effect proposed by the alteration.

(4) For the purposes of subsection (3), the Excise Tariff alteration, or the Customs Tariff alteration, is taken to have been proposed at the time the motion referred to in subsection (2) was moved.

3 Subsection 43‑10(6)

Repeal the subsection, substitute:

Working out the amount of the reduction

(6) The *amount by which a fuel tax credit for taxable fuel is reduced under subsection (1) or (3) is worked out by reference to the rate of fuel tax or road user charge in force on the day worked out using the table in subsection 43‑5(2A).

4 Subsection 44‑5(1)

Repeal the subsection, substitute:

(1) You have a *fuel tax adjustment if you use fuel, or make a *taxable supply of fuel, and the *amount of the fuel tax credit to which you would have been entitled for the use or supply would have been different from the amount to which you are or were entitled if one or both of the following were to apply:

(a) you had originally acquired, manufactured or imported the fuel to use or make a taxable supply in the circumstances in which you did use, or make a taxable supply of, the fuel;

(b) an alteration of a kind referred to in subsection 43‑6(2) that:

(i) under that subsection, had been taken to have effect as if it is an amendment of an Act; and

(ii) under subsection 43‑6(3) ceased to be taken to have that effect;

had never been proposed as mentioned in subsection 43‑6(2).

5 Section 110‑5 (definition of fuel tax)

Repeal the definition, substitute:

fuel tax has the meaning given by section 43‑6.

6 Application

The amendments made by items 1 and 3 apply in relation to:

(a) a tax period that starts on or after 1 July 2014; or

(b) a fuel tax return period, if the return for that period is lodged on or after 1 July 2014.

Schedule 5—Energy Grants (Cleaner Fuels) Scheme

Energy Grants (Cleaner Fuels) Scheme Regulations 2004

1 After regulation 3

Insert:

3A Effect on the duty rate of proposed Excise Tariff alterations

(1) For the purposes of the definition of duty rate in regulation 3, if an Excise Tariff alteration, proposed by a motion moved in the House of Representatives, relates to the excise duty rate for biodiesel, the alteration is taken to have effect as if:

(a) it is an amendment of the Act it proposes to alter; and

(b) that amendment is in force.

(2) However, the alteration does not have, and is taken never to have had, that effect unless, before whichever of the following first happens:

(a) the close of the session in which the Excise Tariff alteration is proposed;

(b) the expiration of 12 months after the Excise Tariff alteration is proposed;

one or more amendments of an Act come into force that have the effect proposed by the alteration.

(3) For the purposes of subregulation (2), Excise Tariff alteration is taken to have been proposed at the time the motion referred to in subregulation (1) was moved.

2 Regulation 6 (formula)

Repeal the formula, substitute:

3 Regulation 6 (after the definition of V)

Insert:

relevant duty rate means the duty rate at the time when the biodiesel is entered.

4 Regulation 7C (formula)

Repeal the formula, substitute:

5 Regulation 7C (after the definition of renewable diesel amount)

Insert:

relevant duty rate means the duty rate at the time when the renewable diesel is entered.

[Minister’s second reading speech made in—

House of Representatives on 30 October 2014

Senate on 26 November 2014]

(195/14)