Tax Laws Amendment (Small Business Measures No. 1) Act 2015

No. 66, 2015

An Act to amend the law relating to taxation, and for related purposes

Tax Laws Amendment (Small Business Measures No. 1) Act 2015

No. 66, 2015

An Act to amend the law relating to taxation, and for related purposes

Contents

2 Commencement

3 Schedules

Schedule 1—Amendments

Part 1—Reducing the corporate tax rate for small business entities

Income Tax Rates Act 1986

Part 2—Consequential amendments

Division 1—Main amendments

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Income Tax Rates Act 1986

Division 2—Amendment of the Tax and Superannuation Laws Amendment (2015 Measures No. 1) Act 2015

Tax and Superannuation Laws Amendment (2015 Measures No. 1) Act 2015

Part 3—Application of amendments

Tax Laws Amendment (Small Business Measures No. 1) Act 2015

No. 66, 2015

An Act to amend the law relating to taxation, and for related purposes

[Assented to 22 June 2015]

The Parliament of Australia enacts:

This Act may be cited as the Tax Laws Amendment (Small Business Measures No. 1) Act 2015.

(1) Each provision of this Act specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information | ||

Column 1 | Column 2 | Column 3 |

Provisions | Commencement | Date/Details |

1. Sections 1 to 3 and anything in this Act not elsewhere covered by this table | The day this Act receives the Royal Assent. | 22 June 2015 |

2. Schedule 1, Part 1 | The day this Act receives the Royal Assent. | 22 June 2015 |

3. Schedule 1, Part 2, Division 1 | The day this Act receives the Royal Assent. | 22 June 2015 |

4. Schedule 1, Part 2, Division 2 | Immediately after the commencement of Division 1 of Part 2 of Schedule 1 to the Tax and Superannuation Laws Amendment (2015 Measures No. 1) Act 2015. However, if that Division commences before the day this Act receives the Royal Assent, the provisions do not commence at all. | 1 July 2015 |

5. Schedule 1, Part 3 | The day this Act receives the Royal Assent. | 22 June 2015 |

Note: This table relates only to the provisions of this Act as originally enacted. It will not be amended to deal with any later amendments of this Act.

(2) Any information in column 3 of the table is not part of this Act. Information may be inserted in this column, or information in it may be edited, in any published version of this Act.

Legislation that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

Part 1—Reducing the corporate tax rate for small business entities

1 Subsection 23(2)

Repeal the subsection, substitute:

(2) The rate of tax in respect of the taxable income of a company is:

(a) if the company is a small business entity for a year of income—28.5%; or

(b) otherwise—30%;

if subsections (3) to (5) and section 23A do not apply to the company.

2 Subsections 23(6) and (7)

Repeal the subsections, substitute:

(6) The amount of tax payable by a company (before applying any rebate, credit or other tax offset (within the meaning of the Income Tax Assessment Act 1997)) must not be greater than 55% of the amount (if any) by which the taxable income of the company exceeds $416, if:

(a) the company is a non‑profit company; and

(b) the taxable income is not greater than:

(i) if the company is a small business entity for a year of income—$863; or

(ii) otherwise—$915.

(7) The amount of tax payable by a company (before applying any rebate, credit or other tax offset (within the meaning of the Income Tax Assessment Act 1997)) must not be greater than:

(a) if the company is a small business entity for a year of income—42.75%; or

(b) otherwise—45%;

of the amount by which the taxable income of the company exceeds $49,999, if the company is a recognised medium credit union in relation to the year of income.

3 Sections 24 and 25

Repeal the sections, substitute:

24 Rate of tax payable by trustees of corporate unit trusts

The rate of tax payable by a trustee of a corporate unit trust in respect of the net income of the corporate unit trust in respect of which the trustee is liable, under section 102K of the Assessment Act, to be assessed and to pay tax is:

(a) if the trust is a small business entity for a year of income—28.5%; or

(b) otherwise—30%.

25 Rate of tax payable by trustees of public trading trusts

The rate of tax payable by a trustee of a public trading trust in respect of the net income of the public trading trust in respect of which the trustee is liable, under section 102S of the Assessment Act, to be assessed and to pay tax is:

(a) if the trust is a small business entity for a year of income—28.5%; or

(b) otherwise—30%.

Part 2—Consequential amendments

Income Tax Assessment Act 1936

4 Paragraph 159GZZZZG(1)(d)

Omit “30% of the IB amounts”, substitute “all of the IB amounts multiplied by the corporate tax rate”.

5 Paragraphs 159GZZZZG(2)(e), (3)(e) and (4)(e)

Omit “30% of the IB attributable amount”, substitute “the IB attributable amount multiplied by the corporate tax rate”.

Income Tax Assessment Act 1997

6 Subsection 36‑17(5) (example)

Omit “2002‑2003 income year, Company A”, substitute “2015‑16 income year, Company A (which is not a small business entity)”.

7 Subsection 36‑55(1) (example)

Omit “2002‑2003 income year, Company E”, substitute “2015‑16 income year, Company E (which is not a small business entity)”.

8 Subsection 36‑55(2) (method statement, step 2)

Omit “*corporate tax rate”, substitute “*standard corporate tax rate”.

9 Section 65‑30

Repeal the section, substitute:

(1) The amount of the *tax offset that is carried forward is the amount of the excess worked out under Division 63.

(2) However, reduce the *tax offset by the amount worked out by multiplying your *net exempt income by:

(a) if you are a *small business entity for the income year—0.285; or

(b) otherwise—0.3;

if you have a taxable income for the income year.

10 Subsection 65‑35(3)

Omit “In reducing net exempt income, each 30 cents of tax offset reduces the net exempt income by $1.”

11 After subsection 65‑35(3)

Insert:

(3A) In reducing *net exempt income for an income year under subsection (3):

(a) if you were a *small business entity for the year—each 28.5 cents of *tax offset reduces the net exempt income by $1; or

(b) otherwise—each 30 cents of tax offset reduces the net exempt income by $1.

12 Subsection 115‑280(3) (example)

After “A listed investment company”, insert “(which is not a small business entity)”.

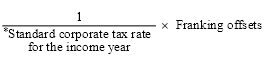

13 Subsection 197‑45(2) (formula)

Repeal the formula, substitute:

14 Subsection 197‑60(3) (paragraph (a) of the definition of applicable tax rate)

Omit “*corporate tax rate”, substitute “*standard corporate tax rate”.

15 Subsection 197‑60(4) (formula)

Repeal the formula, substitute:

16 Subsection 197‑65(3) (formula)

Repeal the formula, substitute:

17 Subsection 200‑25(1)

Omit “by the entity”, substitute “, at the standard corporate tax rate,”.

18 Section 202‑55

Omit “corporate tax rate”, substitute “standard corporate tax rate”.

19 Subsection 202‑60(2) (formula)

Repeal the formula, substitute:

20 Subsection 203‑50(2) (formula)

Repeal the formula, substitute:

21 Subsection 215‑20(2) (formula)

Repeal the formula, substitute:

22 Subsection 705‑90(3) (formula)

Repeal the formula, substitute:

23 Paragraph 707‑310(3A)(c) (formula)

Repeal the formula, substitute:

24 Section 976‑1 (formula)

Repeal the formula, substitute:

25 Section 976‑10 (formula)

Repeal the formula, substitute:

26 Section 976‑15 (formula)

Repeal the formula, substitute:

27 Subsection 995‑1(1)

Insert:

corporate tax gross‑up rate means the amount worked out using the following formula:

28 Subsection 995‑1(1) (definition of corporate tax rate)

Repeal the definition, substitute:

corporate tax rate:

(a) in relation to a company to which paragraph 23(2)(a) of the Income Tax Rates Act 1986 applies—means the rate of tax in respect of the taxable income of the company; or

(b) in relation to another entity—means the *standard corporate tax rate.

29 Subsection 995‑1(1)

Insert:

standard corporate tax rate means the rate of tax in respect of the taxable income of a company covered by paragraph 23(2)(b) of the Income Tax Rates Act 1986.

30 Paragraph 28(a)

Repeal the paragraph, substitute:

(a) if paragraph 98(3)(b) of the Assessment Act (about beneficiaries that are companies) applies:

(i) if the beneficiary is a company to which paragraph 23(2)(a) of this Act applies—the rate specified in paragraph 23(2)(a); or

(ii) otherwise—the rate specified in paragraph 23(2)(b); and

Division 2—Amendment of the Tax and Superannuation Laws Amendment (2015 Measures No. 1) Act 2015

Tax and Superannuation Laws Amendment (2015 Measures No. 1) Act 2015

31 Item 114 of Schedule 1

Repeal the item, substitute:

114 Paragraph 23(3)(aa)

Repeal the paragraph.

Part 3—Application of amendments

32 Application of amendments

The amendments made by this Schedule apply to assessments for years of income starting on or after 1 July 2015.

[Minister’s second reading speech made in—

House of Representatives on 28 May 2015

Senate on 15 June 2015]

(78/15)