Tax and Superannuation Laws Amendment (2015 Measures No. 1) Act 2015

No. 70, 2015

An Act to amend the law relating to first home saver accounts, taxation, superannuation and charities, and to amend the Product Stewardship (Oil) Act 2000, and for related purposes

[Assented to 25 June 2015]

The Parliament of Australia enacts:

1 Short title

This Act may be cited as the Tax and Superannuation Laws Amendment (2015 Measures No. 1) Act 2015.

2 Commencement

(1) Each provision of this Act specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information |

Column 1 | Column 2 | Column 3 |

Provisions | Commencement | Date/Details |

1. Sections 1 to 4 and anything in this Act not elsewhere covered by this table | The day this Act receives the Royal Assent. | 25 June 2015 |

2. Schedule 1, Part 1 | 1 July 2015. | 1 July 2015 |

3. Schedule 1, Part 2, Divisions 1 and 2 | 1 July 2015. | 1 July 2015 |

4. Schedule 1, Part 2, Division 3 | Immediately after the commencement of the provisions covered by table item 3. | 1 July 2015 |

5. Schedule 1, Part 3 | Immediately after the commencement of item 4 of Schedule 8 to the Omnibus Repeal Day (Spring 2014) Act 2015. However, the provisions do not commence at all if that item 4 commences before 1 July 2015. | Never commenced |

6. Schedule 1, Part 4 | 1 July 2015. | 1 July 2015 |

7. Schedules 2, 3 and 4 | The day this Act receives the Royal Assent. | 25 June 2015 |

8. Schedule 5 | The day after this Act receives the Royal Assent. | 26 June 2015 |

9. Schedule 6, items 1 and 2 | The day this Act receives the Royal Assent. | 25 June 2015 |

10. Schedule 6, item 3 | Immediately after the commencement of Part 1 of Schedule 1 to the Charities (Consequential Amendments and Transitional Provisions) Act 2013. | 1 January 2014 |

11. Schedule 6, items 4 to 30 | The day this Act receives the Royal Assent. | 25 June 2015 |

12. Schedule 6, item 31 | Immediately after the commencement of Schedule 6 to the Tax and Superannuation Laws Amendment (2013 Measures No. 1) Act 2013. | 29 June 2013 |

13. Schedule 6, items 32 to 40 | The day this Act receives the Royal Assent. | 25 June 2015 |

14. Schedule 6, item 41 | Immediately after the commencement of Part 1 of Schedule 3 to the Minerals Resource Rent Tax (Consequential Amendments and Transitional Provisions) Act 2012. | 1 July 2012 |

15. Schedule 6, items 42 to 46 | The day this Act receives the Royal Assent. | 25 June 2015 |

16. Schedule 6, items 47 to 50 | Immediately after the commencement of items 6 and 8 of Schedule 1 to the Tax Laws Amendment (2013 Measures No. 3) Act 2013. | 1 July 2014 |

17. Schedule 6, items 51 to 63 | The day this Act receives the Royal Assent. | 25 June 2015 |

18. Schedule 6, item 64 | Immediately after the commencement of Part 2 of Schedule 2 to the Treasury Legislation Amendment (Repeal Day) Act 2015. | 25 February 2015 |

19. Schedule 6, Part 2 | Immediately after the commencement of section 6 of the Public Governance, Performance and Accountability Act 2013. | 1 July 2014 |

20. Schedule 7 | The day this Act receives the Royal Assent. | 25 June 2015 |

Note: This table relates only to the provisions of this Act as originally enacted. It will not be amended to deal with any later amendments of this Act.

(2) Any information in column 3 of the table is not part of this Act. Information may be inserted in this column, or information in it may be edited, in any published version of this Act.

3 Schedules

Legislation that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

Schedule 1—First Home Saver Accounts

Part 1—Repeals of Acts

First Home Saver Account Providers Supervisory Levy Imposition Act 2008

1 The whole of the Act

Repeal the Act.

First Home Saver Accounts Act 2008

2 The whole of the Act

Repeal the Act.

Income Tax (First Home Saver Accounts Misuse Tax) Act 2008

3 The whole of the Act

Repeal the Act.

Part 2—Consequential amendments

Division 1—Main amendments

Anti‑Money Laundering and Counter‑Terrorism Financing Act 2006

4 Section 5 (definition of contribution)

Repeal the definition, substitute:

contribution, in relation to an RSA, has the same meaning as in the Retirement Savings Accounts Act 1997.

5 Section 5 (definition of FHSA)

Repeal the definition.

6 Section 5 (definition of FHSA provider)

Repeal the definition.

7 Subsection 6(2) (table items 43A and 43B)

Repeal the items.

Australian Prudential Regulation Authority Act 1998

8 Subsection 3(1) (paragraph (fa) of the definition of prudential regulation framework law)

Repeal the paragraph.

9 Paragraph 3(2)(g)

Omit “1997;”, substitute “1997.”.

10 Paragraph 3(2)(h)

Repeal the paragraph.

11 Subsection 3(2) (note)

Omit “, RSA is short for retirement savings account and FHSA is short for first home saver account”, substitute “and RSA is short for retirement savings account”.

12 Subsection 56(1) (subparagraph (e)(ii) of the definition of protected document)

Omit “Taxation; or”, substitute “Taxation.”.

13 Subsection 56(1) (paragraph (f) of the definition of protected document)

Repeal the paragraph.

14 Subsection 56(1) (subparagraph (e)(ii) of the definition of protected information)

Omit “Taxation; or”, substitute “Taxation.”.

15 Subsection 56(1) (paragraph (f) of the definition of protected information)

Repeal the paragraph.

Australian Securities and Investments Commission Act 2001

16 Paragraph 12A(1)(h)

Repeal the paragraph.

17 Paragraph 12BAA(7)(ga)

Repeal the paragraph.

Banking Act 1959

18 Subparagraph 11CA(1)(a)(iii)

Repeal the subparagraph.

19 Paragraph 11CA(1)(c)

Omit “, the Financial Sector (Collection of Data) Act 2001 or the First Home Saver Accounts Act 2008”, substitute “or the Financial Sector (Collection of Data) Act 2001”.

20 Subparagraph 11CA(2)(aa)(ii)

Omit “or”.

21 Subparagraph 11CA(2)(aa)(iii)

Repeal the subparagraph.

22 Subsection 18A(5)

Repeal the subsection.

23 Section 51A (definition of reviewable decision of APRA)

Omit “or the First Home Saver Accounts Act 2008”.

24 Subsection 62A(4)

Repeal the subsection.

25 Paragraph 69(3)(b)

Repeal the paragraph.

26 Subsection 69(3) (note)

Repeal the note.

Corporations Act 2001

27 Section 9 (definition of FHSA product)

Repeal the definition.

28 Section 9 (paragraph (ha) of the definition of managed investment scheme)

Repeal the paragraph.

29 Section 761A (paragraph (da) of the definition of basic deposit product)

Repeal the paragraph.

30 Section 761A (definition of FHSA product)

Repeal the definition.

31 Subsection 761E(3) (table item 2A)

Repeal the item.

32 Paragraph 761E(3A)(ba)

Repeal the paragraph.

33 Paragraph 764A(1)(ha)

Repeal the paragraph.

34 Paragraph 766E(3)(cb)

Repeal the paragraph.

35 Subsection 946AA(1A)

Repeal the subsection.

36 Paragraph 961F(c)

Repeal the paragraph.

37 Subsection 1016A(1) (paragraph (da) of the definition of relevant financial product)

Repeal the paragraph.

38 Subparagraphs 1017D(1)(b)(iiia) and 1019A(1)(a)(iiia)

Repeal the subparagraphs.

Financial Institutions Supervisory Levies Collection Act 1998

39 Section 7 (paragraph (f) of the definition of leviable body)

Omit “entity;”, substitute “entity.”.

40 Section 7 (paragraph (g) of the definition of leviable body)

Repeal the paragraph.

41 Section 7 (definition of leviable FHSA entity)

Repeal the definition.

42 Section 7 (paragraph (f) of the definition of levy)

Omit “1998; or”, substitute “1998.”.

43 Section 7 (paragraph (g) of the definition of levy)

Repeal the paragraph.

44 Subsection 8(7)

Repeal the subsection.

Fringe Benefits Tax Assessment Act 1986

45 Subsection 136(1) (paragraph (hd) of the definition of fringe benefit)

Repeal the paragraph.

Income Tax Act 1986

46 Subsection 5(2B)

Repeal the subsection.

Income Tax Assessment Act 1936

47 Subsection 6(1) (paragraph (h) of the definition of assessment)

Omit “payable); or”, substitute “payable).”.

48 Subsection 6(1) (paragraph (i) of the definition of assessment)

Repeal the paragraph.

49 Subsection 6(1) (definition of FHSA)

Repeal the definition.

50 Subsection 6(1) (definition of FHSA trust)

Repeal the definition.

51 Subsection 6(1) (paragraph (f) of the definition of full self‑assessment taxpayer)

Omit “year;”, substitute “year.”.

52 Subsection 6(1) (paragraph (g) of the definition of full self‑assessment taxpayer)

Repeal the paragraph.

53 Subparagraph 26AH(7)(ba)(i)

Omit “superannuation/FHSA”, substitute “superannuation”.

54 Section 95AA

Repeal the section.

55 Subparagraph 102MD(a)(ii)

Omit “superannuation/FHSA”, substitute “superannuation”.

56 Paragraph 124ZM(3)(d)

Omit “or” (last occurring).

57 Paragraph 124ZM(3)(da)

Repeal the paragraph.

58 Paragraph 124ZM(6)(a)

Insert:

complying superannuation class of taxable income is the life assurance company’s complying superannuation class of taxable income, within the meaning of the Income Tax Assessment Act 1997, for the year of income in which the distribution is made.

59 Paragraph 124ZM(6)(a) (definition of complying superannuation/FHSA class of taxable income)

Repeal the definition.

60 Paragraph 202(kb)

Repeal the paragraph.

61 Section 202A (definition of interest‑bearing account)

Omit “or FHSA”.

62 Section 202A (definition of interest‑bearing deposit)

Omit “or FHSA”.

63 Section 202A (definition of unit trust)

Omit “an FHSA trust or”.

64 Paragraph 272‑100(e) in Schedule 2F

Repeal the paragraph.

Income Tax Assessment Act 1997

65 Section 9‑1 (table item 8A)

Repeal the item.

66 Section 10‑5 (table item headed “first home saver accounts”)

Repeal the item.

67 Section 10‑5 (table item headed “reimbursements”)

Omit “first home saver accounts,”.

68 Section 11‑55 (table item headed “first home saver accounts”)

Repeal the item.

69 Section 15‑80

Repeal the section.

70 Paragraphs 51‑120(c) and (d)

Repeal the paragraphs.

71 Subparagraph 115‑100(a)(ii)

Omit “or *FHSA trust”.

72 Subparagraphs 115‑100(b)(iia) and 115‑280(1)(a)(ia)

Repeal the subparagraphs.

73 Paragraph 115‑280(2)(a)

Omit “or an *FHSA trust”.

74 Paragraph 115‑280(2)(b)

Omit “, an FHSA trust”.

75 Paragraph 115‑280(5)(a)

Omit “or an *FHSA trust”.

76 Paragraph 115‑280(5)(b)

Omit “, an FHSA trust”.

77 Paragraphs 166‑245(2)(ba) and (3)(ba)

Repeal the paragraphs.

78 Subsection 205‑15(3)

Repeal the subsection, substitute:

(3) Despite item 1 or 2 of the table in subsection (1), no credit arises on that part of the payment that is attributable to a payment of income tax in relation to an *RSA component.

79 Paragraph 205‑30(2)(a)

Repeal the paragraph, substitute:

(a) a payment of income tax in relation to an *RSA component;

80 Paragraphs 207‑15(2)(a) and 207‑35(1)(c)

Omit “or *FHSA trust”.

81 Paragraph 207‑45(ca)

Repeal the paragraph.

82 Subsection 210‑175(2)

Insert:

complying superannuation class of taxable income means the *complying superannuation class of taxable income of the company for the income year in which the *distribution is made.

83 Subsection 210‑175(2) (definition of complying superannuation/FHSA class of taxable income)

Repeal the definition.

84 Subparagraph 290‑5(c)(iii)

Omit “Australia;”, substitute “Australia.”.

85 Paragraphs 290‑5(d) and (e)

Repeal the paragraphs.

86 Subsection 295‑10(2) (step 4 of the method statement)

Repeal the step.

87 Subsection 295‑10(2) (step 5 of the method statement)

Omit “and the *FHSA component are”, substitute “is”.

88 Section 295‑171

Repeal the section.

89 Section 295‑495 (table item 4A)

Repeal the item.

90 Paragraph 295‑555(1)(b)

Repeal the paragraph.

91 Subsection 295‑555(1) (note)

Omit “and the FHSA component (if applicable) are”, substitute “is”.

92 Subsection 295‑555(3)

Omit “sum of the *RSA component and the *FHSA component (if any)”, substitute “*RSA component”.

93 Paragraph 295‑555(3)(b)

Omit “and the FHSA component (if any)”.

94 Subsection 295‑555(4)

Omit “and the *FHSA component (if any)”.

95 Paragraph 295‑615(1)(b)

Omit “, the First Home Saver Accounts Act 2008”.

96 Paragraph 295‑615(1)(d)

Omit “1997;”, substitute “1997.”.

97 Paragraph 295‑615(1)(e)

Repeal the paragraph.

98 Section 320‑1

Omit “or FHSAs” (wherever occurring).

99 Paragraph 320‑80(2)(b)

Omit “, *FHSA”.

100 Paragraph 320‑85(2)(ba)

Repeal the paragraph.

101 Subsection 320‑107(3)

Insert:

complying superannuation class rate is the rate of tax imposed on the *complying superannuation class of the company’s taxable income for the income year.

102 Subsection 320‑107(3) (definition of complying superannuation/FHSA class rate)

Repeal the definition.

103 Division 345

Repeal the Division.

104 Subparagraph 380‑15(1)(d)(iv)

Repeal the subparagraph.

105 Subsection 713‑545(6)

Insert:

complying superannuation class tax rate means the rate of tax in respect of the *complying superannuation class of the taxable income of a *life insurance company for the income year in which the joining time occurs (see paragraph 23A(b) of the Income Tax Rates Act 1986).

106 Subsection 713‑545(6) (definition of complying superannuation/FHSA class tax rate)

Repeal the definition.

107 Subsection 995‑1(1)

Insert:

complying superannuation asset has the meaning given by subsection 320‑170(6).

complying superannuation asset pool has the meaning given by subsection 320‑170(6).

complying superannuation class:

(a) for a taxable income of a *life insurance company—has the meaning given by section 320‑137; or

(b) for a *tax loss of a *life insurance company—has the meaning given by section 320‑141.

complying superannuation liabilities of a *life insurance company means liabilities of the company under *life insurance policies referred to in subsection 320‑190(1).

complying superannuation life insurance policy means a *life insurance policy that:

(a) is held by:

(i) the trustee of a fund that is a *complying superannuation fund or a *complying approved deposit fund; or

(ii) the trustee of a *pooled superannuation trust; or

(b) is held by an individual and:

(i) provides for an *annuity that is not presently payable, if the annuity was purchased out of a *superannuation lump sum or an *employment termination payment; or

(ii) is so held in the benefit fund of a *friendly society, being a fund that is a *regulated superannuation fund; or

(c) is held by another *life insurance company and is a *complying superannuation asset of that company;

and is not an *excluded complying superannuation life insurance policy.

excluded complying superannuation life insurance policy means a *life insurance policy that:

(a) provides only for *superannuation death benefits, *disability superannuation benefits or temporary disability benefits of a kind referred to in paragraph 295‑460(c), that are not *participating benefits; or

(b) is an *exempt life insurance policy.

108 Subsection 995‑1(1) (definition of standard component)

Repeal the definition, substitute:

standard component has the meaning given by section 295‑555.

Income Tax Rates Act 1986

109 Subsection 3(1)

Insert:

complying superannuation class of the taxable income of a life insurance company has the same meaning as in the Income Tax Assessment Act 1997.

110 Subsection 3(1) (definition of complying superannuation/FHSA class)

Repeal the definition.

111 Subsection 3(1) (definition of FHSA component)

Repeal the definition.

112 Subsection 3(1) (definition of FHSA provider)

Repeal the definition.

113 Subsection 3(1) (definition of FHSA trust)

Repeal the definition.

114 Paragraphs 23(2)(ba) and (3)(aa)

Repeal the paragraphs.

115 Subsection 23(3A)

Repeal the subsection.

116 Paragraph 23A(b)

Omit “superannuation/FHSA”, substitute “superannuation”.

117 Section 30

Repeal the section.

Life Insurance Act 1995

118 Subparagraph 14(2)(a)(ii)

Omit “or” (last occurring), substitute “and”.

119 Subparagraph 14(2)(a)(iii)

Repeal the subparagraph.

120 Subparagraph 14(4)(b)(ii)

Omit “be; or”, substitute “be.”.

121 Subparagraph 14(4)(b)(iii)

Repeal the subparagraph.

122 Subsection 74(1)

Omit “(1)”.

123 Subsection 74(2)

Repeal the subsection.

124 Subsection 126(1)

Omit “(1) In”, substitute “In”.

125 Subsection 126(2)

Repeal the subsection.

126 Subsection 216(1)

Omit “or FHSAs (within the meaning of the First Home Saver Accounts Act 2008)”.

127 Subsection 216(1) (note)

Repeal the note.

128 Subsections 230A(14), 230B(11) and 236(1AA)

Repeal the subsections.

Social Security Act 1991

129 Paragraph 8(8)(ba)

Repeal the paragraph.

130 Subsection 9(1) (definition of financial investment)

Omit “an investment in an FHSA (within the meaning of the First Home Saver Accounts Act 2008) or”.

131 Subsection 9(1) (paragraph (b) of the definition of investment)

Omit “(9A); or”, substitute “(9A).”.

132 Subsection 9(1) (paragraph (c) of the definition of investment)

Repeal the paragraph.

133 Subsection 9(1) (paragraph (b) of the definition of return)

Omit “investment; or”, substitute “investment.”.

134 Subsection 9(1) (paragraph (c) of the definition of return)

Repeal the paragraph.

135 Paragraph 9(1C)(cb)

Repeal the paragraph.

136 Subsection 9(9B)

Repeal the subsection.

137 Subsection 10B(2) (paragraph (ca) of the definition of trust)

Repeal the paragraph.

138 Subsection 23(1) (paragraph (b) of the definition of investment)

Omit “(9A); or”, substitute “(9A).”.

139 Subsection 23(1) (paragraph (c) of the definition of investment)

Repeal the paragraph.

140 Subsection 23(1) (paragraph (b) of the definition of return)

Omit “9(1); or”, substitute “9(1).”.

141 Subsection 23(1) (paragraph (c) of the definition of return)

Repeal the paragraph.

142 Paragraph 1118(1)(fa)

Repeal the paragraph.

143 Paragraph 1207P(1)(c)

Omit “(4)); or”, substitute “(4)).”.

144 Paragraph 1207P(1)(d)

Repeal the paragraph.

Superannuation (Government Co‑contribution for Low Income Earners) Act 2003

145 Subparagraph 7(1)(c)(iv)

Omit “1997;”, substitute “1997.”.

146 Subparagraphs 7(1)(c)(v) and (vi)

Repeal the subparagraphs.

Superannuation Industry (Supervision) Act 1993

147 Paragraph 29G(2)(f)

Omit “29EB;”, substitute “29EB.”.

148 Paragraph 29G(2)(v)

Repeal the paragraph.

149 Subsection 108A(3)

Omit all the words after paragraph (b).

150 Subsection 108A(3) (note)

Repeal the note.

Taxation Administration Act 1953

151 Subsection 8AAB(4) (table items 4 and 16)

Repeal the items.

152 Paragraph 15C(8)(c)

Repeal the paragraph.

153 Paragraph 12‑1(3)(b) in Schedule 1

Repeal the paragraph, substitute:

(b) is not an exempt benefit under section 22 of that Act (about reimbursement of car expenses on the basis of distance travelled).

154 Paragraph 45‑120(2)(c) in Schedule 1

Omit “or”.

155 Paragraph 45‑120(2)(ca) in Schedule 1

Repeal the paragraph.

156 Paragraph 45‑120(2A)(b) in Schedule 1

Omit “superannuation/FHSA”, substitute “superannuation”.

157 Paragraph 45‑290(2)(c) in Schedule 1

Omit “year; or”, substitute “year.”.

158 Paragraph 45‑290(2)(d) in Schedule 1

Repeal the paragraph.

159 Subsection 45‑290(3) in Schedule 1

Omit “superannuation/FHSA”, substitute “superannuation”.

160 Paragraph 45‑330(2)(c) in Schedule 1

Omit “year; or”, substitute “year.”.

161 Paragraph 45‑330(2)(d) in Schedule 1

Repeal the paragraph.

162 Subsection 45‑330(3) in Schedule 1 (steps 4, 5 and 6 of the method statement)

Omit “superannuation/FHSA” (wherever occurring), substitute “superannuation”.

163 Paragraph 45‑370(2)(c) in Schedule 1

Omit “year; or”, substitute “year.”.

164 Paragraph 45‑370(2)(d) in Schedule 1

Repeal the paragraph.

165 Subsection 45‑370(3) in Schedule 1 (step 2 of the method statement)

Omit “superannuation/FHSA”, substitute “superannuation”.

166 Subsection 250‑10(2) in Schedule 1 (table items 24D, 24E and 38C)

Repeal the items.

167 Subsections 286‑75(2B) and (2C) in Schedule 1

Repeal the subsections.

168 Subsection 288‑70(1) in Schedule 1 (heading)

Repeal the heading, substitute:

Complying superannuation asset pool—calculation of an amount

169 Subsection 288‑70(2) in Schedule 1 (heading)

Repeal the heading, substitute:

Complying superannuation asset pool—transfer following valuation

170 Paragraph 288‑70(2)(a) in Schedule 1

Omit “superannuation/FHSA”, substitute “superannuation”.

171 Subsection 355‑65(3) in Schedule 1 (table item 6)

Repeal the item.

172 Subsection 355‑65(4) in Schedule 1 (table item 5)

Repeal the item.

173 Subsection 355‑65(5) in Schedule 1 (cell at table item 2, column headed “and the record or disclosure …”)

Repeal the cell, substitute:

(a) is of rental information, residential address information or spousal information; and (b) is for the purpose of administering the First Home Owner Grant (New Homes) Act 2000 (NSW), or a similar *State law or *Territory law. |

174 Division 391 in Schedule 1

Repeal the Division.

Veterans’ Entitlements Act 1986

175 Paragraph 5H(8)(ia)

Repeal the paragraph.

176 Subsection 5J(1) (definition of financial investment)

Omit “an investment in an FHSA (within the meaning of the First Home Saver Accounts Act 2008) or”.

177 Subsection 5J(1) (paragraph (b) of the definition of investment)

Omit “(6A); or”, substitute “(6A).”.

178 Subsection 5J(1) (paragraph (c) of the definition of investment)

Repeal the paragraph.

179 Subsection 5J(1) (paragraph (aa) of the definition of return)

Repeal the paragraph.

180 Paragraph 5J(1C)(cb)

Repeal the paragraph.

181 Subsection 5J(6B)

Repeal the subsection.

182 Subsection 5Q(1) (paragraph (b) of the definition of investment)

Omit “subsection 5J(6A); or”, substitute “subsection 5J(6A).”.

183 Subsection 5Q(1) (paragraph (c) of the definition of investment)

Repeal the paragraph.

184 Subsection 5Q(1) (paragraph (b) of the definition of return)

Repeal the paragraph.

185 Paragraph 52(1)(faa)

Repeal the paragraph.

186 Paragraph 52ZZB(1)(c)

Omit “(4)); or”, substitute “(4)).”.

187 Paragraph 52ZZB(1)(d)

Repeal the paragraph.

Division 2—Repeals of Tax Code definitions

Income Tax Assessment Act 1997

188 Subsection 995‑1(1)

Repeal the following definitions:

(a) definition of complying superannuation/FHSA asset;

(b) definition of complying superannuation/FHSA asset pool;

(c) definition of complying superannuation/FHSA class;

(d) definition of complying superannuation/FHSA liabilities;

(e) definition of complying superannuation/FHSA life insurance policy;

(f) definition of excluded complying superannuation/FHSA life insurance policy;

(g) definition of FHSA;

(h) definition of FHSA component;

(i) definition of FHSA holder;

(j) definition of FHSA home acquisition payment;

(k) definition of FHSA ineligibility payment;

(l) definition of FHSA misuse tax;

(m) definition of FHSA mortgage payment;

(n) definition of FHSA payment conditions;

(o) definition of FHSA provider;

(p) definition of FHSA trust;

(q) definition of Government FHSA contribution.

Division 3—Other bulk amendments

Income Tax Assessment Act 1997

189 The whole of the Act

Omit every occurrence of “superannuation/FHSA”, substitute “superannuation”.

190 The whole of the Act

Omit every occurrence of “superannuation/FHSA”, substitute “superannuation”.

191 The whole of the Act

Omit every occurrence of “superannuation/FHSA”, substitute “superannuation”.

192 The whole of the Act

Omit every occurrence of “superannuation/FHSA”, substitute “superannuation”.

Part 3—Amendment of the Omnibus Repeal Day (Spring 2014) Act 2015

Omnibus Repeal Day (Spring 2014) Act 2015

193 Division 2 of Part 1 of Schedule 8 (heading specifying First Home Saver Accounts Act 2008)

Repeal the heading.

194 Items 4 and 5 of Schedule 8

Repeal the items.

Part 4—Application and transitional provisions

Division 1—Definitions

195 Definitions

In this Part:

FHSA Act means the First Home Saver Accounts Act 2008, as in force just before the commencement of this item.

Division 2—General provisions

196 No new FHSAs

(1) An account, life policy or beneficial interest opened or issued after 7:30 pm (by legal time in the Australian Capital Territory) on 13 May 2014 is not, and never was, an FHSA.

(2) Subitem (1) does not apply if:

(a) the application for that opening or issuing (see paragraph 19(1)(a) of the FHSA Act) was given to the provider before that 7:30 pm; and

(b) the account, life policy or beneficial interest was opened or issued on or before 30 June 2015.

197 FHSA regime ends on 1 July 2015

(1) On 1 July 2015, an FHSA ceases to be an FHSA.

(2) Despite subitem (1), the repeals and amendments made by this Schedule do not apply in relation to acts done or omitted to be done, or states of affairs existing:

(a) before 1 July 2015; or

(b) on or after 1 July 2015 as a result of the operation of this Part (including this subitem).

198 Making and amending assessments, and doing other things, in relation to past matters

Even though an Act is repealed or amended by this Schedule, the repeal or amendment is disregarded for the purpose of doing any of the following under any Act or legislative instrument:

(a) making or amending an assessment (including under a provision that is itself repealed or amended);

(b) exercising any right or power, performing any obligation or duty or doing any other thing (including under a provision that is itself repealed or amended);

in relation to any act done or omitted to be done, any state of affairs existing, or any period ending, before the repeal or amendment applies.

199 Saving of provisions about effect of assessments

If a provision or part of a provision that is repealed or amended by this Schedule deals with the effect of an assessment, the repeal or amendment is disregarded in relation to assessments made, before or after the repeal or amendment applies, in relation to any act done or omitted to be done, any state of affairs existing, or any period ending, before the repeal or amendment applies.

200 Saving of provisions about FHSA misuse tax, general interest charge and interest

If:

(a) a provision or part of a provision that is repealed or amended by this Schedule provides for the payment of:

(i) FHSA misuse tax (within the meaning of the Income Tax Assessment Act 1997, as in force just before the commencement of this item); or

(ii) general interest charge (within the meaning of the Taxation Administration Act 1953); or

(iii) interest under the Taxation (Interest on Overpayments and Early Payments) Act 1983; and

(b) in a particular case, the period in respect of which the tax, charge or interest is payable (whether under the provision or under the Taxation Administration Act 1953) has not begun, or has begun but not ended, when the provision is repealed or amended;

then, despite the repeal or amendment, the provision or part continues to apply in the particular case until the end of the period.

201 Repeals disregarded for the purposes of dependent provisions

(1) If the operation of a provision (the subject provision) of any Act or legislative instrument made under any Act depends to any extent on an Act, or a provision of an Act, that is repealed by this Schedule, the repeal is disregarded so far as it affects the operation of the subject provision.

(2) Subitem (1) does not apply to the repeal of a provision of the Social Security Act 1991 or the Veterans’ Entitlements Act 1986 by this Schedule.

202 Interaction with other laws

(1) This Division does not limit the operation of section 7 of the Acts Interpretation Act 1901.

(2) This Division has effect subject to Division 3.

Division 3—Specific provisions

203 FHSA eligibility requirements

(1) Section 20 of the FHSA Act (including that section as affected by subsection 128A(5)) does not apply, on or after 1 July 2015, in respect of circumstances that arose on or after 1 June 2015.

(2) Section 21 of the FHSA Act does not apply on or after 1 July 2015, even in relation to circumstances that arose before 1 July 2015.

(3) Section 22 of the FHSA Act does not apply, on or after 1 July 2015, in relation to trigger days that occur on or after 17 June 2015.

204 Government FHSA contributions

(1) A Government FHSA contribution is not payable for the 2014‑15 financial year or a later financial year.

(2) The amendments made by this Schedule do not apply in relation to Government FHSA contributions for the 2013‑14 financial year or an earlier financial year.

Example: Subsection 345‑50(3) of the Income Tax Assessment Act 1997 (which makes Government FHSA contributions not assessable income and not exempt income) applies to a Government FHSA contribution for the 2013‑14 year, even if it is paid after the repeal of that subsection by this Schedule.

(3) Despite anything in the FHSA Act or this Schedule, the Commissioner must not pay a Government FHSA contribution after 30 June 2017, unless the relevant income tax return is lodged, or the relevant notice is given, (as mentioned in paragraph 41(2)(a) of the FHSA Act) on or before 30 June 2017.

205 Tax file numbers

An individual who, just before the commencement of this item:

(a) had quoted his or her tax file number to an FHSA provider in connection with the operation or the possible future operation of the FHSA Act and the Superannuation Acts; and

(b) holds an FHSA provided by the FHSA provider that is an account;

is treated, from that commencement, as having quoted the individual’s TFN to the FHSA provider in connection with the account under Division 4 of Part VA of the Income Tax Assessment Act 1936.

Schedule 2—Dependent spouse tax offset

Part 1—Main amendments

Income Tax Assessment Act 1936

1 Subparagraphs 23AB(7)(a)(ii) and (iii)

Repeal the subparagraphs, substitute:

(ii) the amount worked out using subsection (7A); or

2 Subsection 23AB(7) (notes 1 and 2)

Repeal the notes.

3 Subsection 23AB(7A)

Repeal the subsection, substitute:

(7A) For the purposes of subparagraph (7)(a)(ii), the amount is equal to 50% of the sum of the following rebates (if any) in respect of the year of income:

(a) any tax offset to which the taxpayer is entitled under Subdivision 61‑A of the Income Tax Assessment Act 1997;

(b) any notional tax offset to which the taxpayer is entitled under Subdivision 961‑A of the Income Tax Assessment Act 1997.

4 Paragraphs 79A(2)(a), (d) and (e)

Repeal the paragraphs, substitute:

(a) if the taxpayer is a resident of the special area in Zone A, or of the special area in Zone B, in the year of income—an amount equal to the sum of:

(i) $1,173; and

(ii) an amount equal to 50% of the relevant rebate amount in relation to the taxpayer in relation to the year of income; or

(b) if the taxpayer is a resident of Zone A in the year of income but has not resided or actually been in the special area in Zone A or the special area in Zone B during any part of the year of income—an amount equal to the sum of:

(i) $338; and

(ii) an amount equal to 50% of the relevant rebate amount in relation to the taxpayer in relation to the year of income; or

(c) if the taxpayer is a resident of Zone B in the year of income but has not resided or actually been in Zone A or the special area in Zone B during any part of the year of income—an amount equal to the sum of:

(i) $57; and

(ii) an amount equal to 20% of the relevant rebate amount in relation to the taxpayer in relation to the year of income; or

5 Paragraph 79A(2)(f)

Omit “paragraph (e)”, substitute “paragraph (c)”.

6 Subsection 79A(4) (definition of dependent spouse relevant rebate amount)

Repeal the definition.

7 Subsection 79A(4) (definition of relevant rebate amount)

Repeal the definition (including the notes), substitute:

relevant rebate amount, in relation to a taxpayer in relation to a year of income, means the sum of the following rebates (if any):

(a) any tax offset to which the taxpayer is entitled under Subdivision 61‑A of the Income Tax Assessment Act 1997;

(b) any notional tax offset to which the taxpayer is entitled under Subdivision 961‑A of the Income Tax Assessment Act 1997;

(c) any notional tax offset to which the taxpayer is entitled under Subdivision 961‑B of the Income Tax Assessment Act 1997.

8 Subparagraph 79B(2)(a)(ii)

Omit “amount; and”, substitute “amount; or”.

9 Subparagraph 79B(2)(a)(iii)

Repeal the subparagraph.

10 Paragraph 79B(4)(b)

Omit “amount; and”, substitute “amount.”

11 Paragraph 79B(4)(c)

Repeal the paragraph.

12 Subparagraph 79B(4A)(b)(ii)

Omit “amount; and”, substitute “amount;”.

13 Subparagraph 79B(4A)(b)(iii)

Repeal the subparagraph.

14 Subsection 79B(6) (definition of concessional rebate amount)

Repeal the definition (including the notes), substitute:

concessional rebate amount, in relation to a taxpayer in relation to a year of income, means the sum of the following rebates (if any):

(a) any tax offset to which the taxpayer is entitled under Subdivision 61‑A of the Income Tax Assessment Act 1997;

(b) any notional tax offset to which the taxpayer is entitled under Subdivision 961‑A of the Income Tax Assessment Act 1997;

(c) any notional tax offset to which the taxpayer is entitled under Subdivision 961‑B of the Income Tax Assessment Act 1997.

15 Subsection 79B(6) (definition of dependent spouse concessional rebate amount)

Repeal the definition.

16 Sections 159J, 159JA, 159K, 159L, 159LA and 159M

Repeal the sections.

Income Tax Assessment Act 1997

17 After Division 960

Insert:

Division 961—Notional tax offsets

Table of Subdivisions

961‑A Dependant (non‑student child under 21 or student) notional tax offset

961‑B Dependant (sole parent of a non‑student child under 21 or student) notional tax offset

Subdivision 961‑A—Dependant (non‑student child under 21 or student) notional tax offset

Guide to Subdivision 961‑A

961‑1 What this Subdivision is about

This Subdivision provides for a notional tax offset for an income year if you contribute to the maintenance of a non‑student child or a student dependant. The notional tax offset can only be taken into account in working out certain tax offsets under the Income Tax Assessment Act 1936.

Table of sections

Entitlement to the notional tax offset

961‑5 Who is entitled to the notional tax offset

Amount of the notional tax offset

961‑10 Amount of the dependant (non‑student child under 21 or student) notional tax offset

961‑15 Reduced amounts of the dependant (non‑student child under 21 or student) notional tax offset

961‑20 Reductions to take account of the dependant’s income

Entitlement to the notional tax offset

961‑5 Who is entitled to the notional tax offset

(1) You are entitled to a notional tax offset for an income year if:

(a) you are an individual; and

(b) you are an Australian resident; and

(c) during the year you contribute to the maintenance of another individual (the dependant) who:

(i) is less than 25 years of age, and is a full‑time student at a school, college or university; or

(ii) if subparagraph (i) does not apply—is less than 21 years of age; and

(d) during the year:

(i) the dependant is an Australian resident; or

(ii) you had a domicile in Australia.

(2) You may be entitled to more than one notional tax offset for the year under subsection (1) if you contributed to the maintenance of more than one dependant during the year.

Note: The amount of the notional tax offset in relation to each subsequent dependant may only be part of the full amount: see subsection 961‑15(1).

(3) The notional tax offset only affects your income tax liability as provided for by sections 23AB, 79A and 79B of the Income Tax Assessment Act 1936.

Note: Section 23AB of that Act provides a tax offset for service with an armed force under the control of the United Nations; section 79A provides a tax offset for residents of isolated areas; section 79B provides a tax offset for members of the Defence Force who are serving overseas.

Amount of the notional tax offset

961‑10 Amount of the dependant (non‑student child under 21 or student) notional tax offset

(1) The amount of the notional tax offset to which you are entitled in relation to a dependant under section 961‑5 for an income year is $376.

(2) However, if you are entitled to 2 or more such notional tax offsets for the income year in relation to individuals covered by subparagraph 961‑5(1)(c)(ii), the amount of the notional tax offset under section 961‑5 is:

(a) in relation to the oldest of those individuals—$376; and

(b) in relation to each of the others—$282.

961‑15 Reduced amounts of the dependant (non‑student child under 21 or student) notional tax offset

(1) The amount of the notional tax offset under section 961‑10 is reduced by the amount in accordance with subsection (2) of this section if one or more of the following applies:

(a) paragraph 961‑5(1)(c) applies during part only of the year;

(b) paragraph 961‑5(1)(d) applies during part only of the year;

(c) during the whole or part of the year, 2 or more individuals contribute to the maintenance of the dependant;

(d) the dependant only meets the description of the individual covered by subparagraph 961‑5(1)(c)(i) or (ii) for part of the year.

(2) The amount of a notional tax offset is reduced to an amount that, in the Commissioner’s opinion, is a reasonable apportionment in the circumstances, having regard to the applicable matters referred to in paragraphs (1)(a) to (d).

961‑20 Reductions to take account of the dependant’s income

The amount of the notional tax offset under sections 961‑10 and 961‑15 in relation to the dependant for the year is reduced by $1 for every $4 by which the following exceeds $282:

(a) if you contribute to the maintenance of the dependant for the whole of the year—the dependant’s *adjusted taxable income for offsets for the year;

(b) if paragraph (a) does not apply—the dependant’s adjusted taxable income for offsets for that part of the year during which you contribute to the dependant’s maintenance.

Subdivision 961‑B—Dependant (sole parent of a non‑student child under 21 or student) notional tax offset

Guide to Subdivision 961‑B

961‑50 What this Subdivision is about

This Subdivision provides for a notional tax offset for an income year if you are the sole contributor to the maintenance of a non‑student child or a student dependant. The notional tax offset can only be taken into account in working out certain tax offsets under the Income Tax Assessment Act 1936.

Table of sections

Operative provisions

961‑55 Who is entitled to the notional tax offset

961‑60 Amount of the dependant (sole parent of a non‑student child under 21 or student) notional tax offset

961‑65 Reductions to take account of change in circumstances

Operative provisions

961‑55 Who is entitled to the notional tax offset

(1) You are entitled to a notional tax offset for an income year if:

(a) during the year you have the sole care of another individual (the dependant) who:

(i) is less than 25 years of age, and is a full‑time student at a school, college or university; or

(ii) if subparagraph (i) does not apply—is less than 21 years of age; and

(b) you are entitled to a notional tax offset under Subdivision 961‑A for the dependant; and

(c) during the year you did not have a *spouse.

(2) Paragraph (1)(c) does not apply if, in the opinion of the Commissioner, because of special circumstances, the paragraph should not apply.

(3) The notional tax offset only affects your income tax liability as provided for by sections 79A and 79B of the Income Tax Assessment Act 1936.

Note: Section 79A of that Act provides a tax offset for residents of isolated areas; section 79B provides a tax offset for members of the Defence Force who are serving overseas.

961‑60 Amount of the dependant (sole parent of a non‑student child under 21 or student) notional tax offset

The amount of the notional tax offset to which you are entitled under section 961‑55 for an income year is $1,607.

Note: The amount of the offset under this section applies regardless of whether you have one or more dependants that satisfy section 961‑55.

961‑65 Reductions to take account of change in circumstances

(1) The amount of the notional tax offset under section 961‑60 is reduced in accordance with subsection (2) if:

(a) paragraph 961‑55(1)(a) applies during only part of the year; or

(b) paragraph 961‑55(1)(c) does not apply because of subsection 961‑55(2).

(2) The amount of the notional tax offset is reduced to an amount that, in the Commissioner’s opinion, is a reasonable apportionment in the circumstances, having regard to the matters referred to in paragraphs (1)(a) and (b).

Part 2—Consequential amendments

Income Tax Assessment Act 1936

18 Subsection 159HA(1)

Omit “Sections 159J, 159L and 159Q apply”, substitute “Section 159Q applies”.

19 Subsection 159HA(6A)

Repeal the subsection.

20 Subsection 159HA(7) (table items 1, 2 and 3)

Repeal the items.

21 Subsection 159P(4) (paragraphs (c), (ca) and (d) of the definition of dependant)

Repeal the paragraphs.

22 Subsection 159P(4) (at the end of the definition of dependant)

Add:

; or (g) a person in respect of whom the taxpayer is entitled to a notional tax offset under Subdivision 961‑A of the Income Tax Assessment Act 1997.

23 Subsection 251R(4)

Omit “would be entitled to a rebate in respect of that child under section 159J in the person’s assessment in respect of income of that year of income but for subsections 159J(1A) and (1F)”, substitute “is entitled to a notional tax offset in respect of that child under Subdivision 961‑A of the Income Tax Assessment Act 1997”.

Income Tax Assessment Act 1997

24 Section 13‑1 (table item headed “child/housekeeper”)

Repeal the item.

25 Section 13‑1 (table item headed “dependants”)

Omit:

child of person keeping house for the person......... | 159J |

housekeeper, caring for child, invalid relative or disabled spouse | 159L |

invalid relative, invalid spouse or carer in receipt of carer benefit | 159J, Subdivision 61‑A |

parents/parents in law........................ | 159J |

spouse.................................. | 159J |

substitute:

invalid relative, invalid spouse or carer in receipt of carer benefit | Subdivision 61‑A |

26 Section 13‑1 (table items headed “housekeeper”, “parent/parent‑in‑law” and “spouse”)

Repeal the items.

27 Subparagraph 61‑10(1)(c)(ii)

Omit “Australia; and”, substitute “Australia.”.

28 Paragraphs 61‑10(1)(d) and (e)

Repeal the paragraphs.

29 Subsection 61‑10(1) (note)

Repeal the note.

Medicare Levy Act 1986

30 Paragraphs 8(1)(b), (c) and (d)

Repeal the paragraphs, substitute:

(b) is entitled to a tax offset under Subdivision 61‑A of the Income Tax Assessment Act 1997 for the year of income in respect of the person’s child (within the meaning of that Act); or

(c) is entitled to a notional tax offset under Subdivision 961‑B of the Income Tax Assessment Act 1997 for the year of income;

31 Paragraphs 8(2)(b), (c) and (d)

Repeal the paragraphs, substitute:

(b) is entitled to a tax offset under Subdivision 61‑A of the Income Tax Assessment Act 1997 for the year of income in respect of the person’s child (within the meaning of that Act); or

(c) is entitled to a notional tax offset under Subdivision 961‑B of the Income Tax Assessment Act 1997 for the year of income;

32 Subsection 8(5) (definition of family income threshold)

Repeal the definition, substitute:

family income threshold, in relation to a person (the relevant person), means $35,261 increased by $3,238 for each person covered by paragraph 961‑5(1)(c) of the Income Tax Assessment Act 1997 in respect of whom:

(a) in a case to which paragraph (b) does not apply—the relevant person; or

(b) if the relevant person was a married person on the last day of the year of income—the relevant person or the spouse of the relevant person;

is entitled to a notional tax offset under Subdivision 961‑A of the Income Tax Assessment Act 1997 for the year of income.

Tax and Superannuation Laws Amendment (2014 Measures No. 1) Act 2014

33 Items 4 and 5 of Schedule 3

Repeal the items, substitute:

4 Section 159HA

Repeal the section.

Part 3—Technical amendments

Income Tax Assessment Act 1997

34 Subsection 61‑15(3)

Repeal the subsection.

35 At the end of section 61‑25

Add:

Note: Clause 31 of Schedule 1 to the A New Tax System (Family Assistance) Act 1999 reduces the standard rate for the family tax benefit to take account of shared care percentages.

36 Paragraph 61‑40(1)(f)

Before “during”, insert “the other individual is your spouse, and,”.

37 Subsection 61‑40(2)

Omit “is reasonable”, substitute “is a reasonable apportionment”.

Part 4—Application of amendments

38 Application of amendments—Parts 1 and 2

The amendments made by Parts 1 and 2 of this Schedule apply in relation to assessments for the 2014‑15 income year and later income years.

39 Application of amendments—Part 3

The amendments made by Part 3 of this Schedule apply in relation to assessments for the 2012‑13 income year and later income years.

Schedule 3—Offshore banking units

Part 1—Trading in subsidiaries

Income Tax Assessment Act 1936

1 Paragraph 121D(1)(c)

After “subsection (4)”, insert “(subject to subsection (4A))”.

2 After subsection 121D(4)

Insert:

(4A) However, paragraph (1)(c) does not apply to a trading activity done by an OBU if:

(a) the thing traded in affected the OBU’s total participation interest (within the meaning of the Income Tax Assessment Act 1997) in another entity; and

(b) just before the trading activity:

(i) the OBU’s total participation interest in the other entity was at least 10%; or

(ii) any of the thing traded in was held by the OBU, and was not recorded in the OBU’s accounting records as held for trading in accordance with accounting standards (within the meaning of that Act).

(4B) For the purposes of subsection (4A), disregard rights on winding‑up.

Part 2—The choice principle

Income Tax Assessment Act 1936

3 Paragraph 121B(2)(a)

Repeal the paragraph, substitute:

(a) OB activity (sections 121D, 121EA and 121EAA) together with the related definition of offshore person (section 121E); and

4 Section 121C

Insert:

non‑OB accounting records has the meaning given by subsection 121EAA(3).

5 Subsection 121D(1)

Omit “, provided that the requirement relating to the OBU in section 121EA is met”, substitute “(subject to sections 121EA and 121EAA)”.

6 After section 121EA

Insert:

121EAA Activities recorded in domestic books not OB activities

(1) An OBU may, when it does a thing that would otherwise be an OB activity of the OBU, choose to have the thing not be an OB activity.

Accounting records

(2) The OBU recording the thing in the OBU’s non‑OB accounting records is sufficient evidence of the making of the choice, if the OBU uses money in the thing.

Note 1: The OBU must maintain accounting records, separate from its non‑OB accounting records, in respect of money used in its OB activities: see subsection 262A(1A).

Note 2: Subsection (2) of this section and subsection 262A(1A) do not apply if the OBU does not use money in the thing, but the OBU must keep documents containing particulars of the choice: see paragraph 262A(2)(b).

Note 3: Subsection (2) does not prevent the OBU from correcting a mistake in its accounting records.

(3) The OBU’s non‑OB accounting records are the OBU’s accounting records, other than the accounting records maintained in respect of money used in the OBU’s OB activities under subsection 262A(1A).

Grouping

(4) The OBU is treated as having chosen under subsection (1) to have a thing (the transaction) done by the OBU not be an OB activity if:

(a) it is reasonable to regard the transaction and one or more other things done by the OBU as constituting a single scheme (within the meaning of the Income Tax Assessment Act 1997); and

(b) the OBU chooses under subsection (1) to have any of those other things done by the OBU not be an OB activity.

(5) For the purposes of subsection (4), whether the transaction and one or more other things constitute a single scheme is a question of fact and degree determined having regard to the following (whichever are applicable):

(a) the nature of the transaction and the other things;

(b) their terms and conditions (including those relating to any payment or other consideration for them);

(c) the circumstances surrounding their creation and their proposed exercise or performance (including what can reasonably be seen as the purposes of one or more of the entities involved);

(d) whether they can be dealt with separately or must be dealt with together;

(e) normal commercial understandings and practices in relation to them (including whether they are regarded commercially as separate things or as a group or series that forms a whole);

(f) the objects of this Division.

(6) In applying subsection (5), have regard to the matters mentioned in paragraphs (5)(a) to (f) both:

(a) in relation to the transaction and other things separately; and

(b) in relation to the transaction and other things in combination with each other.

7 Subsection 121EB(1)

Omit “121EA”, substitute “121EAA”.

Part 3—Allocation of expenses

Income Tax Assessment Act 1936

8 Subsection 6(1)

Insert:

statutory income has the meaning given by the Income Tax Assessment Act 1997.

9 Paragraph 121B(2)(b)

Repeal the paragraph, substitute:

(b) special income and allowable deduction definitions relating to OB activities (sections 121EDA to 121EF).

10 Section 121C (definition of assessable OB income)

Repeal the definition, substitute:

assessable OB income has the meaning given by subsection 121EE(2).

11 Section 121C

Insert:

OB income has the meaning given by section 121EDA.

12 Section 121E

Omit “For the purposes of section 121D, a reference in that section”, substitute “A reference”.

13 After section 121ED

Insert:

121EDA Meaning of OB income

OB income

(1) Subject to subsections (2) to (5), the OB income of an OBU of a year of income is so much of the OBU’s ordinary income and statutory income of the year of income as is:

(a) derived from OB activities of the OBU or the part of the OBU to which paragraph 121EB(1)(c) applies; or

(b) included in the statutory income because of such activities.

(2) Subsection (1) does not apply to amounts included under Part 3‑1 of the Income Tax Assessment Act 1997 (about capital gains).

(3) Subsection (1) does not apply to the extent that the money lent, invested or otherwise used in carrying on the OB activities is non‑OB money of the OBU.

(4) A typical example of an amount covered by the exception in subsection (3) is interest derived from the OB activity of lending money to an offshore person, where the money lent is non‑OB money.

Reduction of OB income because of certain investment activities

(5) Ordinary or statutory income that:

(a) would otherwise be taken into account under subsection (1); and

(b) is derived from an investment activity (within the meaning of subsection 121D(6A) or (6B)) included in OB activities of the OBU or the part of the OBU to which paragraph 121EB(1)(c) applies;

is reduced by the average Australian asset percentage (within the meaning of subsection 121DA(2)) of the portfolio investment concerned.

14 Subsections 121EE(2) to (3A)

Repeal the subsections, substitute:

Assessable OB income

(2) The assessable OB income of an OBU is so much of the OBU’s OB income of the year of income as is assessable income.

15 Subsection 121EF(4)

Repeal the subsection, substitute:

General OB deduction

(4) A deduction that:

(a) is none of the following:

(i) a loss deduction;

(ii) an apportionable deduction;

(iii) an exclusive OB deduction;

(iv) an exclusive non‑OB deduction; and

(b) is allowable from the OBU’s assessable income of the year of income;

is a general OB deduction to the extent that:

(c) it is incurred in gaining or producing the OB income of the OBU; or

(d) it is necessarily incurred in carrying on a business for the purpose of gaining or producing the OB income of the OBU.

16 Paragraph 121EH(a)

Omit “subsection 121EE(2)”, substitute “subsection 121EDA(3)”.

Part 4—Eligible OB activities

Income Tax Assessment Act 1936

17 Section 121C (definition of eligible contract)

Repeal the definition, substitute:

eligible contract means:

(a) any of the following:

(i) a futures contract;

(ii) a forward contract;

(iii) an options contract;

(iv) a swap contract;

(v) a cap, collar, floor or similar contract; or

(b) a loan contract; or

(c) a securities lending or repurchase arrangement; or

(d) a non‑deliverable forward foreign currency contract.

18 Section 121C

Insert:

OB advisory activity has the meaning given by section 121DC.

OB eligible contract activity has the meaning given by section 121DB.

OB leasing activity has the meaning given by section 121DD.

offshore property means property that:

(a) cannot be in Australia; or

Example: Land outside Australia.

(b) is used, or will be used:

(i) wholly outside Australia; or

(ii) in Australia to an extent that is not material.

19 Paragraph 121D(1)(d)

Repeal the paragraph, substitute:

(d) an OB eligible contract activity (see section 121DB); or

20 Paragraph 121D(1)(f)

Repeal the paragraph, substitute:

(f) an OB advisory activity (see section 121DC); or

21 After paragraph 121D(1)(g)

Insert:

(ga) an OB leasing activity (see section 121DD); or

22 Paragraph 121D(2)(b)

After “lending money”, insert “, or making commitments to lend money,”.

23 At the end of subsection 121D(2)

Add:

; or (e) acting as an arranger in a syndicated lending arrangement that includes a borrowing or lending activity to which paragraph (a), (b), (c) or (d) applies.

24 Paragraphs 121D(3)(a) and (b)

Repeal the paragraphs, substitute:

(a) providing a guarantee or letter of credit to an offshore person in relation to activities that are, or will be, conducted:

(i) wholly outside Australia; or

(ii) in Australia to an extent that is not material; or

(b) underwriting a risk for an offshore person in respect of:

(i) offshore property; or

(ii) an event, if the likelihood of the event happening in Australia is not material; or

25 Paragraph 121D(3)(d)

Repeal the paragraph, substitute:

(d) issuing a performance bond to an offshore person in relation to activities that are, or will be, conducted:

(i) wholly outside Australia; or

(ii) in Australia to an extent that is not material;

26 After paragraph 121D(4)(a)

Insert:

(aa) trading with any person in non‑deliverable forward foreign currency contracts; or

27 At the end of subsection 121D(4)

Add:

; or (i) trading with an offshore person in commodities, or in options or rights in respect of commodities, if:

(i) the commodities, options or rights are not mentioned in another paragraph of this subsection; and

(ii) the trading is incidental to an OB eligible contract activity.

28 Subsection 121D(5)

Repeal the subsection.

29 Paragraph 121D(6A)(e)

Omit “subsection 121DA(5)); and”, substitute “subsection 121DA(5)).”.

30 Paragraph 121D(6A)(f)

Repeal the paragraph.

31 Subsection 121D(7)

Repeal the subsection.

32 After section 121DA

Insert:

121DB Meaning of OB eligible contract activity

An OB eligible contract activity is entering into an eligible contract (other than a loan contract that is not a securities lending or repurchase arrangement) with:

(a) an offshore person; or

(b) if the eligible contract is a non‑deliverable forward foreign currency contract—any person.

121DC Meaning of OB advisory activity

(1) An OB advisory activity is giving investment or other financial advice to an offshore person, including advice about disposing of an investment.

(2) Giving advice about the making of a particular investment is not an OB advisory activity unless the investment is of a kind mentioned in subsection 121D(6) (Investment activity).

(3) Subsection (2) does not exclude giving advice about a particular investment of a different kind if doing so is incidental to advising on an investment of a kind mentioned in subsection 121D(6) (for example for the purpose of comparison or because the investments are commercially related).

(4) To avoid doubt, for the purposes of this section, advice about disposing of an investment is not advice about the making of the investment.

121DD Meaning of OB leasing activity

(1) An OB leasing activity is leasing activity with an offshore person involving offshore property.

(2) Without limiting subsection (1), OB leasing activity includes entering into:

(a) any arrangement (within the meaning of section 51AD) under which a right to use offshore property is granted by the owner to another person; or

(b) any arrangement (within the meaning of that section) under which a right to use offshore property, being a right derived directly or indirectly from a right mentioned in paragraph (a) in relation to the property, is granted by a person to another person;

with an offshore person.

Part 5—Internal financial dealings

Income Tax Assessment Act 1936

33 At the end of section 121EB

Add:

Arm’s length pricing

(4) For the purposes of this Division, treat an amount that, because of subsections (1) to (3):

(a) is included in the OBU’s OB income; or

(b) is an allowable OB deduction of the OBU;

as being the amount that would be so included, or that would be the amount of the allowable OB deduction, were the OBU and the permanent establishments mentioned in paragraph (1)(d) dealing with each other at arm’s length.

(5) For the purposes of determining the effect subsection (4) has in relation to the amount that is included or allowable, work out the arm’s length dealing so as best to achieve consistency with:

(a) the documents covered by section 815‑235 of the Income Tax Assessment Act 1997 (Guidance); and

(b) subject to paragraph (a), the documents covered by section 815‑135 of that Act.

Part 6—Application of amendments

34 Application of amendments

(1) The amendments made by this Schedule (other than Part 2) apply in relation to years of income starting on or after 1 July 2015.

(2) The amendments made by Part 2 apply in relation to a thing an OBU does on or after 1 July 2015.

Schedule 4—Exemption for Global Infrastructure Hub Ltd

Part 1—Amendments commencing day after Royal Assent

Income Tax Assessment Act 1997

1 Section 11‑5 (table item headed “primary or secondary resources, and tourism”)

Before:

horticultural society etc. ...................... | 50‑40 |

insert:

Global Infrastructure Hub Ltd .................. | 50‑40 |

2 Section 50‑40 (at the end of the table)

Add:

8.4 | Global Infrastructure Hub Ltd | only amounts included in assessable income: (a) on or after 24 December 2014; and (b) before 1 July 2019 |

Part 2—Sunsetting on 1 July 2021

Income Tax Assessment Act 1997

3 Section 11‑5 (table item headed “primary or secondary resources, and tourism”)

Omit:

Global Infrastructure Hub Ltd .................. | 50‑40 |

4 Section 50‑40 (table item 8.4)

Repeal the item.

Schedule 5—Deductible gift recipient extensions

Income Tax Assessment Act 1997

1 Subsection 30‑50(2) (table items 5.2.32 and 5.2.33)

Omit “1 January 2015”, substitute “1 January 2018”.

Tax and Superannuation Laws Amendment (2013 Measures No. 2) Act 2013

2 Subsection 2(1) (table item 8)

Repeal the item, substitute:

8. Schedule 4, Part 2, Division 1 | 1 July 2022. | 1 July 2022 |

3 Division 1 of Part 2 of Schedule 4 (heading)

Repeal the heading, substitute:

Division 1—Repeal on 1 July 2022

Schedule 6—Miscellaneous amendments

Part 1—General amendments

A New Tax System (Goods and Services Tax) Act 1999

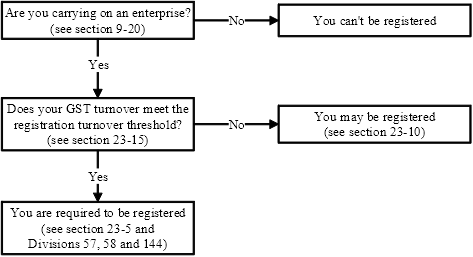

1 Section 23‑1 (diagram)

Repeal the diagram, substitute:

2 Paragraph 134‑10(1)(e)

Omit “from you”, substitute “you make”.

Charities (Consequential Amendments and Transitional Provisions) Act 2013

3 Item 31 of Schedule 1

Omit “trusts”, substitute “trust”.

Fringe Benefits Tax Assessment Act 1986

4 Subsection 136(1) (subparagraph (b)(iii) of the definition of in‑house residual fringe benefit)

Omit “property”, substitute “benefits”.

Fuel Tax Act 2006

5 Subsection 3‑5(3) (table)

Repeal the table, substitute:

Common definitions that are not asterisked |

Item | This term: |

1 | Commissioner |

2 | entity |

3 | fuel tax |

4 | fuel tax credit |

5 | indirect tax zone |

6 | taxable fuel |

7 | you |

6 Subsections 41‑5(1) and 41‑10(1), (2) and (3)

Omit “Australia”, substitute “the indirect tax zone”.

7 Section 42‑5

Omit “Australia”, substitute “the indirect tax zone”.

8 Paragraph 43‑7(5)(a)

Omit “Australia”, substitute “the indirect tax zone”.

9 Section 110‑5 (definition of Australia)

Repeal the definition.

10 Section 110‑5

Insert:

indirect tax zone has the meaning given by section 195‑1 of the *GST Act.

11 Section 110‑5 (paragraph (d) of the definition of taxable fuel)

Omit “Australia”, substitute “the indirect tax zone”.

12 Application

The amendments of the Fuel Tax Act 2006 made by this Part apply to taxable fuel acquired, manufactured or imported on or after 1 July 2015.

Income Tax Assessment Act 1997

13 Section 13‑1 (table item headed “primary production”)

Omit:

farm household allowance see social security and other benefit payments |

|

substitute:

farm household allowance see social security and other benefit payments |

|

14 Section 13‑1 (table item headed “social security and other benefit payments”)

Omit:

farm household allowance under the Farm Household Support Act 2014 see unemployment, sickness and other benefit payments under the Social Security Act 1991 |

|

substitute:

farm household allowance under the Farm Household Support Act 2014 see unemployment, sickness and other benefit payments under the Social Security Act 1991 |

|

15 Paragraph 25‑110(1)(a)

Omit “*carrying on”, substitute “carrying on”.

16 Paragraph 26‑47(3)(b)

Omit “*carry on”, substitute “carry on”.

17 Paragraph 30‑242(3A)(b)

Omit “*carrying on”, substitute “carrying on”.

18 Paragraph 35‑5(1)(a)

Omit “*carried on”, substitute “carried on”.

19 Subsection 35‑5(2)

Omit “*carrying on”, substitute “carrying on”.

20 Subsection 35‑10(2A)

Omit “*carry on”, substitute “carry on”.

21 Paragraph 35‑10(2B)(a)

Omit “*carry on”, substitute “carry on”.

22 Subsections 35‑10(2C) and (2D)

Omit “*carried on”, substitute “carried on”.

23 Paragraphs 40‑880(1)(c) and (2)(b)

Omit “*carried on”, substitute “carried on”.

24 Subsections 40‑880(3) and (4)

Omit “*carry on”, substitute “carry on”.

25 Subsection 40‑880(7)

Omit “*carried on”, substitute “carried on”.

26 Paragraph 41‑20(1)(d)

Omit “*carrying on”, substitute “carrying on”.

27 Subparagraph 83A‑130(1)(a)(ii)

After “of the old company”, insert “or a *demerger subsidiary of the old company”.

28 Application

The amendment of section 83A‑130 of the Income Tax Assessment Act 1997 made by this Part applies in relation to ESS interests acquired on or after 1 July 2009.

29 Section 104‑5 (cell at table item dealing with CGT event K1, column headed “Event number and description”)

Omit “*Kyoto unit or an *Australian carbon credit unit”, substitute “Kyoto unit or an Australian carbon credit unit”.

30 Section 112‑97 (table item 18A, column headed “In this situation”)

Omit “*Kyoto unit”, substitute “Kyoto unit”.

31 Subsection 219‑30(1)

Omit “items 2 and 3”, substitute “items 2 and 2A”.

32 Subsection 316‑65(1) (definitions of embedded value of the friendly society’s other business (if any) and market value of the friendly society’s health insurance business (if any))

Omit “*carried on”, substitute “carried on”.

33 Paragraphs 415‑15(3)(b) and 415‑20(1)(b) and (2)(b)

Omit “*carries on”, substitute “carries on”.

34 Paragraph 415‑20(4)(a)

Omit “*carrying on”, substitute “carrying on”.

35 Subsection 995‑1(1) (definition of available frankable profits)

Omit “give”, substitute “given”.

36 Subsection 995‑1(1) (paragraph (a) of the definition of foreign resident life insurance policy)

Omit “*carrying on”, substitute “carrying on”.

37 Subsection 995‑1(1)

Insert:

taxable dealing, in relation to *wine, has the meaning given by section 33‑1 of the *Wine Tax Act.

wine has the meaning given by Subdivision 31‑A of the *Wine Tax Act.

38 Subsection 995‑1(1) (definition of wine taxable dealing)

Repeal the definition.

Income Tax Rates Act 1986

39 Section 12B (the section 12B inserted by item 1 of Schedule 1 to the Income Tax Rates Amendment (Temporary Flood and Cyclone Reconstruction Levy) Act 2011)

Renumber as section 12C.

Income Tax Rates Amendment (Temporary Flood and Cyclone Reconstruction Levy) Act 2011

40 Item 1 of Schedule 2 (heading)

Omit “12B”, substitute “12C”.

Minerals Resource Rent Tax (Consequential Amendments and Transitional Provisions) Act 2012

41 Item 16 of Schedule 3

Omit “*mining operations”, substitute “mining operations”.

Product Stewardship (Oil) Act 2000

42 After section 4

Insert:

4A Alternative constitutional basis

(1) Without limiting its effect apart from this section, this Act also has effect as provided by this section.

(2) This Act also has the effect it would have if its operation in relation to product stewardship (oil) benefits were expressly confined to an operation limited to product stewardship (oil) benefits in relation to external affairs.

(3) This Act also has the effect it would have if its operation in relation to product stewardship (oil) benefits were expressly confined to an operation limited to product stewardship (oil) benefits in relation to taxation.

Superannuation (Government Co‑contribution for Low Income Earners) Act 2003

43 Paragraph 16(1)(d)

Omit “approved form”, substitute “approved form,”.

44 Subsection 16(3)

Omit “the prescribed information”, substitute “a statement, in the approved form,”.

45 Paragraph 20(1)(d)

Omit “approved form”, substitute “approved form,”.

46 Subsection 20(3)

Omit “the prescribed information”, substitute “a statement, in the approved form,”.

Tax Agent Services Act 2009

47 Subparagraph 20‑5(2)(c)(ii)

Omit “; and; or”, substitute “; or”.

48 Subparagraph 20‑5(2)(c)(iii)

Omit “arrangements.”, substitute “arrangements; and”.

49 Subparagraph 20‑5(3)(d)(ii)

Omit “; and; or”, substitute “; or”.

50 Subparagraph 20‑5(3)(d)(iii)

Omit “arrangements.”, substitute “arrangements; and”.

Taxation Administration Act 1953

51 Subsection 12‑390(4) in Schedule 1 (note)

After “If the recipient”, insert “is”.

52 Section 105‑1 in Schedule 1

Omit “your address for service of documents and”.

53 Section 105‑140 in Schedule 1

Repeal the section.

54 Application

The amendments of sections 105‑1 and 105‑140 in Schedule 1 to the Taxation Administration Act 1953 made by this Part apply on and after 1 July 2015.

55 Subsection 111‑60(1) in Schedule 1

Omit “or a *wine taxable dealing”, substitute “, or a *taxable dealing in relation to *wine,”.

56 Paragraph 382‑5(2)(c) in Schedule 1

Omit “*wine taxable dealing”, substitute “*taxable dealing, in relation to *wine,”.

57 Paragraph 426‑55(1)(a) in Schedule 1

Repeal the paragraph, substitute:

(a) at any time after the date of effect of the endorsement, the entity is not, or was not, entitled to be endorsed; or

58 Subsection 426‑55(3) in Schedule 1

After “is not”, insert “, or was not,”.

59 Application of amendments

The amendments of section 426‑55 in Schedule 1 to the Taxation Administration Act 1953 made by this Part apply to a decision, on or after the commencement of this Part, to revoke an endorsement (regardless of when the endorsement took effect).

Taxation (Deficit Reduction) Act (No. 3) 1993

60 Subsection 2(3)

Repeal the subsection.

61 Division 4 of Part 2

Repeal the Division.

Taxation (Interest on Overpayments and Early Payments) Act 1983

62 Subparagraph 12A(1)(a)(i)

Omit “and subsection 204(3) of the Tax Act”, substitute “of the Tax Act or section 5‑15 of the Income Tax Assessment Act 1997”.

63 Application

The amendment of section 12A of the Taxation (Interest on Overpayments and Early Payments) Act 1983 made by this Part is taken to have applied from the commencement of Schedule 1 to the Tax Laws Amendment (Transfer of Provisions) Act 2010.

Treasury Legislation Amendment (Repeal Day) Act 2015

64 Item 73 of Schedule 2

Omit “Schedule”, substitute “Part of this Schedule”.

Part 2—Consequential amendments relating to the Public Governance, Performance and Accountability Act 2013

Australian Charities and Not‑for‑profits Commission Act 2012

65 Section 110‑15 (note)

Repeal the note, substitute:

Note: The expenditure of relevant money (within the meaning of the Public Governance, Performance and Accountability Act 2013) must comply with the requirements in that Act.

66 Section 115‑30

Repeal the section, substitute:

115‑30 Disclosure of interests

(1) A disclosure by the Commissioner under section 29 of the Public Governance, Performance and Accountability Act 2013 (which deals with the duty to disclose interests) must be made to the Minister.

(2) Subsection (1) applies in addition to any rules made for the purposes of that section.

(3) For the purposes of this Act and the Public Governance, Performance and Accountability Act 2013, the Commissioner is taken not to have complied with section 29 of that Act if the Commissioner does not comply with subsection (1) of this section.

67 Paragraph 115‑50(2)(c)

Repeal the paragraph, substitute:

(c) the Commissioner fails, without reasonable excuse, to comply with section 29 of the Public Governance, Performance and Accountability Act 2013 (which deals with the duty to disclose interests) or rules made for the purposes of that section; or

68 Subsection 125‑5(1)

Omit “(the Account)”.

69 Subsection 125‑5(2)

Repeal the subsection, substitute:

(2) The account is a special account for the purposes of the Public Governance, Performance and Accountability Act 2013.

70 Section 125‑10 (heading)

Repeal the heading, substitute:

125‑10 Credits to the account

71 Section 125‑10

Omit “Account” (first, second and third occurring), substitute “account”.

72 Section 125‑10 (note)

Omit “Special Account if any of the purposes of the Account”, substitute “special account if any of the purposes of the special account”.

73 Section 125‑15 (heading)

Repeal the heading, substitute:

125‑15 Purposes of the account

74 Section 125‑15

Omit “Account” (first and second occurring), substitute “account”.

75 Section 125‑15 (note)

Repeal the note, substitute:

Note: See section 80 of the Public Governance, Performance and Accountability Act 2013 (which deals with special accounts).

76 Subsection 135‑15(2) (note)

Repeal the note, substitute:

Note: The expenditure of relevant money (within the meaning of the Public Governance, Performance and Accountability Act 2013) must comply with the requirements in that Act.

77 Section 140‑20

Repeal the section, substitute:

140‑20 Disclosure of interests

(1) A disclosure by a member of the Advisory Board under section 29 of the Public Governance, Performance and Accountability Act 2013 (which deals with the duty to disclose interests) must be made to the Minister.

(2) Subsection (1) applies in addition to any rules made for the purposes of that section.

(3) For the purposes of this Act and the Public Governance, Performance and Accountability Act 2013, the member is taken not to have complied with section 29 of that Act if the member does not comply with subsection (1) of this section.

78 Subsections 145‑5(5), (6) and (7)

Repeal the subsections.

79 Subsection 175‑70(2) (note 1)

Omit “Note 1”, substitute “Note”.

80 Subsection 175‑70(2) (note 2)

Repeal the note.

81 Section 300‑5 (definition of Account)

Repeal the definition.

Schedule 7—Investment Manager Regime

Part 1—Main amendments

Income Tax Assessment Act 1997

1 Subdivision 842‑I

Repeal the Subdivision, substitute:

Subdivision 842‑I—Investment manager regime

Guide to Subdivision 842‑I

842‑200 What this Subdivision is about

This Subdivision sets out rules about the taxation of some foreign residents (known as IMR entities) that invest into or through Australia.

Income and capital gains from IMR financial arrangements are not subject to Australian income tax. Deductions and capital losses from IMR financial arrangements are disregarded for the purposes of this Act.

Table of sections

Object of this Subdivision

842‑205 Object of this Subdivision

IMR concessions

842‑210 IMR concessions apply only to foreign residents etc.

842‑215 IMR concessions

842‑220 Meaning of IMR entity

842‑225 Meaning of IMR financial arrangement

IMR widely held entities

842‑230 Meaning of IMR widely held entity

842‑235 Rules for determining total participation interests for the purposes of the widely held test

842‑240 Extended definition of IMR widely held entity—temporary circumstances outside entity’s control

Independent Australian fund managers

842‑245 Meaning of independent Australian fund manager

842‑250 Reductions in IMR concessions if independent Australian fund manager entitled to substantial share of IMR entity’s income

Object of this Subdivision

842‑205 Object of this Subdivision

The object of this Subdivision is to encourage particular kinds of investment made into or through Australia by some foreign residents that have wide membership, or that use Australian fund managers.

IMR concessions

842‑210 IMR concessions apply only to foreign residents etc.