Treasury Laws Amendment (Enterprise Tax Plan) Act 2017

No. 41, 2017

An Act to amend the law relating to taxation, and for related purposes

Treasury Laws Amendment (Enterprise Tax Plan) Act 2017

No. 41, 2017

An Act to amend the law relating to taxation, and for related purposes

Contents

2 Commencement

3 Schedules

Schedule 1—Reducing the corporate tax rate

Part 1—Amendments commencing 1 July 2016

Income Tax Rates Act 1986

Part 2—Amendments commencing 1 July 2017

Income Tax Rates Act 1986

Part 3—Amendments commencing 1 July 2018

Income Tax Rates Act 1986

Part 9—Amendments commencing 1 July 2024

Income Tax Rates Act 1986

Part 10—Amendments commencing 1 July 2025

Income Tax Rates Act 1986

Part 11—Amendments commencing 1 July 2026

Income Tax Rates Act 1986

Part 12—Application of amendments

Schedule 2—Amount of tax discount for unincorporated small businesses

Part 1—Amendments commencing 1 July 2016

Income Tax Assessment Act 1997

Part 2—Amendments commencing 1 July 2024

Income Tax Assessment Act 1997

Part 3—Amendments commencing 1 July 2025

Income Tax Assessment Act 1997

Part 4—Amendments commencing 1 July 2026

Income Tax Assessment Act 1997

Part 5—Application of amendments

Schedule 3—Access to small business concessions, etc.

Part 1—Amendments

Income Tax Assessment Act 1997

Part 2—Application of amendments

Schedule 4—Main consequential amendments relating to imputation

Part 1—Amendments commencing 1 July 2016

Income Tax Assessment Act 1997

Part 3—Application of amendments

Schedule 5—Other consequential amendments

Part 1—Amendments commencing 1 July 2016

Income Tax Assessment Act 1997

Part 2—Amendments commencing 1 July 2017

Income Tax Assessment Act 1997

Part 4—Amendments commencing 1 July 2024

Income Tax Assessment Act 1997

Part 5—Amendments commencing 1 July 2025

Income Tax Assessment Act 1997

Part 6—Amendments commencing 1 July 2026

Income Tax Assessment Act 1997

Treasury Laws Amendment (Enterprise Tax Plan) Act 2017

No. 41, 2017

An Act to amend the law relating to taxation, and for related purposes

[Assented to 19 May 2017]

The Parliament of Australia enacts:

This Act is the Treasury Laws Amendment (Enterprise Tax Plan) Act 2017.

(1) Each provision of this Act specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information | ||

Column 1 | Column 2 | Column 3 |

Provisions | Commencement | Date/Details |

1. Sections 1 to 3 and anything in this Act not elsewhere covered by this table | The day this Act receives the Royal Assent. | 19 May 2017 |

2. Schedule 1, Part 1 | 1 July 2016. | 1 July 2016 |

3. Schedule 1, Part 2 | 1 July 2017. | 1 July 2017 |

4. Schedule 1, Part 3 | 1 July 2018. | 1 July 2018 |

5. Schedule 1, Part 9 | 1 July 2024. | 1 July 2024 |

6. Schedule 1, Part 10 | 1 July 2025. | 1 July 2025 |

7. Schedule 1, Part 11 | 1 July 2026. | 1 July 2026 |

8. Schedule 1, Part 12 | The day this Act receives the Royal Assent. | 19 May 2017 |

9. Schedule 2, Part 1 | 1 July 2016. | 1 July 2016 |

10. Schedule 2, Part 2 | 1 July 2024. | 1 July 2024 |

11. Schedule 2, Part 3 | 1 July 2025. | 1 July 2025 |

12. Schedule 2, Part 4 | 1 July 2026. | 1 July 2026 |

13. Schedule 2, Part 5 | The day this Act receives the Royal Assent. | 19 May 2017 |

14. Schedule 3, Part 1 | 1 July 2016. | 1 July 2016 |

15. Schedule 3, Part 2 | The day this Act receives the Royal Assent. | 19 May 2017 |

16. Schedule 4, Part 1 | 1 July 2016. | 1 July 2016 |

17. Schedule 4, Part 3 | The day this Act receives the Royal Assent. | 19 May 2017 |

18. Schedule 5, Part 1 | 1 July 2016. | 1 July 2016 |

19. Schedule 5, Part 2 | 1 July 2017. | 1 July 2017 |

20. Schedule 5, Part 4 | 1 July 2024. | 1 July 2024 |

21. Schedule 5, Part 5 | 1 July 2025. | 1 July 2025 |

22. Schedule 5, Part 6 | 1 July 2026. | 1 July 2026 |

Note: This table relates only to the provisions of this Act as originally enacted. It will not be amended to deal with any later amendments of this Act.

(2) Any information in column 3 of the table is not part of this Act. Information may be inserted in this column, or information in it may be edited, in any published version of this Act.

Legislation that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

Schedule 1—Reducing the corporate tax rate

Part 1—Amendments commencing 1 July 2016

1 Paragraph 23(2)(a)

Omit “28.5%”, substitute “27.5%”.

2 Paragraph 23(3)(b)

Repeal the paragraph, substitute:

(b) in respect of the standard component:

(i) if the company is a small business entity for a year of income—27.5%; or

(ii) otherwise—30%.

3 Paragraph 23(4)(c)

Repeal the paragraph, substitute:

(c) in respect of so much of the taxable income as exceeds the PDF component:

(i) if the company is a small business entity for a year of income—27.5%; or

(ii) otherwise—30%.

4 Subparagraph 23(6)(b)(i)

Omit “$863”, substitute “$832”.

5 Paragraph 23(7)(a)

Omit “42.75%”, substitute “41.25%”.

6 Paragraph 25(a)

Omit “28.5%”, substitute “27.5%”.

Part 2—Amendments commencing 1 July 2017

7 Subsection 3(1)

Insert:

base rate entity has the meaning given by section 23AA.

8 Paragraph 23(2)(a)

Omit “small business entity”, substitute “base rate entity”.

9 Subparagraph 23(3)(b)(i)

Omit “small business entity”, substitute “base rate entity”.

10 Subparagraph 23(4)(c)(i)

Omit “small business entity”, substitute “base rate entity”.

11 Subparagraph 23(6)(b)(i)

Omit “small business entity”, substitute “base rate entity”.

12 Paragraph 23(7)(a)

Omit “small business entity”, substitute “base rate entity”.

13 After section 23

Insert:

23AA Meaning of base rate entity

An entity is a base rate entity for a year of income if:

(a) it carries on a business (within the meaning of the Income Tax Assessment Act 1997) in the year of income; and

(b) its aggregated turnover (within the meaning of that Act) for the year of income, worked out as at the end of that year, is less than $25 million.

14 Paragraph 25(a)

Omit “small business entity”, substitute “base rate entity”.

15 Paragraph 28A(a)

Omit “the rate specified in paragraph 23(2)(b) (about companies other than small business entities)”, substitute “the rate specified in paragraph 23(2)(b) of this Act”.

Part 3—Amendments commencing 1 July 2018

16 Paragraph 23AA(b)

Omit “$25 million”, substitute “$50 million”.

Part 9—Amendments commencing 1 July 2024

33 Paragraph 23(2)(a)

Omit “27.5%”, substitute “27%”.

34 Subparagraph 23(3)(b)(i)

Omit “27.5%”, substitute “27%”.

35 Subparagraph 23(4)(c)(i)

Omit “27.5%”, substitute “27%”.

36 Subparagraph 23(6)(b)(i)

Omit “$832”, substitute “$817”.

37 Paragraph 23(7)(a)

Omit “41.25%”, substitute “40.5%”.

38 Paragraph 25(a)

Omit “27.5%”, substitute “27%”.

Part 10—Amendments commencing 1 July 2025

39 Paragraph 23(2)(a)

Omit “27%”, substitute “26%”.

40 Subparagraph 23(3)(b)(i)

Omit “27%”, substitute “26%”.

41 Subparagraph 23(4)(c)(i)

Omit “27%”, substitute “26%”.

42 Subparagraph 23(6)(b)(i)

Omit “$817”, substitute “$788”.

43 Paragraph 23(7)(a)

Omit “40.5%”, substitute “39%”.

44 Paragraph 25(a)

Omit “27%”, substitute “26%”.

Part 11—Amendments commencing 1 July 2026

45 Paragraph 23(2)(a)

Omit “26%”, substitute “25%”.

46 Subparagraph 23(3)(b)(i)

Omit “26%”, substitute “25%”.

47 Subparagraph 23(4)(c)(i)

Omit “26%”, substitute “25%”.

48 Subparagraph 23(6)(b)(i)

Omit “$788”, substitute “$762”.

49 Paragraph 23(7)(a)

Omit “39%”, substitute “37.5%”.

50 Paragraph 25(a)

Omit “26%”, substitute “25%”.

Part 12—Application of amendments

57 Application of amendments

(1) Subject to the following subitems, the amendments made by Part 1 of this Schedule apply to the 2016‑17 year of income and later years of income.

(2) Subject to the following subitems, the amendments made by Part 2 of this Schedule apply to the 2017‑18 year of income and later years of income.

(3) Subject to the following subitems, the amendments made by Part 3 of this Schedule apply to the 2018‑19 year of income and later years of income.

(9) Subject to the following subitems, the amendments made by Part 9 of this Schedule apply to the 2024‑25 year of income and later years of income.

(10) Subject to the following subitem, the amendments made by Part 10 of this Schedule apply to the 2025‑26 year of income and later years of income.

(11) The amendments made by Part 11 of this Schedule apply to the 2026‑27 year of income and later years of income.

Schedule 2—Amount of tax discount for unincorporated small businesses

Part 1—Amendments commencing 1 July 2016

Income Tax Assessment Act 1997

1 Subsection 328‑360(1)

Omit “5%”, substitute “8%”.

Part 2—Amendments commencing 1 July 2024

Income Tax Assessment Act 1997

2 Subsection 328‑360(1)

Omit “8%”, substitute “10%”.

Part 3—Amendments commencing 1 July 2025

Income Tax Assessment Act 1997

3 Subsection 328‑360(1)

Omit “10%”, substitute “13%”.

Part 4—Amendments commencing 1 July 2026

Income Tax Assessment Act 1997

4 Subsection 328‑360(1)

Omit “13%”, substitute “16%”.

Part 5—Application of amendments

5 Application of amendments

(1) Subject to the following subitems, the amendments made by Part 1 of this Schedule apply to the 2016‑17 income year and later income years.

(2) Subject to the following subitems, the amendments made by Part 2 of this Schedule apply to the 2024‑25 income year and later income years.

(3) Subject to the following subitem, the amendments made by Part 3 of this Schedule apply to the 2025‑26 income year and later income years.

(4) The amendments made by Part 4 of this Schedule apply to the 2026‑27 income year and later income years.

Schedule 3—Access to small business concessions, etc.

Income Tax Assessment Act 1997

1 Section 152‑5

Omit:

(a) the entity must be a small business entity or a partner in a partnership that is a small business entity, or the net value of assets that the entity and related entities own must not exceed $6,000,000;

substitute:

(a) the entity must be a CGT small business entity or a partner in a partnership that is a CGT small business entity, or the net value of assets that the entity and related entities own must not exceed $6,000,000;

2 Subparagraph 152‑10(1)(c)(i)

Omit “*small business entity”, substitute “*CGT small business entity”.

3 Subparagraph 152‑10(1)(c)(iii)

Omit “small business entity”, substitute “CGT small business entity”.

4 Paragraph 152‑10(1)(c) (note)

Repeal the note.

5 After subsection 152‑10(1)

Insert:

CGT small business entity

(1AA) You are a CGT small business entity for an income year if:

(a) you are a *small business entity for the income year; and

(b) you would be a small business entity for the income year if each reference in section 328‑110 to $10 million were a reference to $2 million.

Note: For the purposes of subsection (1A) or (1B), in determining whether an entity would be a small business entity, see also sections 152‑48 and 152‑78.

6 Paragraph 152‑10(1A)(a)

Omit “*small business entity”, substitute “*CGT small business entity”.

7 Paragraph 152‑10(1A)(d)

Omit “small business entity”, substitute “CGT small business entity”.

8 Subsection 152‑10(1A) (note 2)

Repeal the note.

9 Paragraph 152‑10(1B)(b)

Omit “*small business entity”, substitute “*CGT small business entity”.

10 Subsection 152‑10(1B) (note 1)

Repeal the note.

11 Subsection 152‑10(1B) (note 2)

Omit “Note 2”, substitute “Note”.

12 Subsection 152‑48(1)

Omit “*small business entity”, substitute “*CGT small business entity”.

13 Section 152‑100

Omit “small business entity”, substitute “CGT small business entity”.

14 At the end of subsection 328‑10(1)

Add:

Note 1: The CGT concessions mentioned in items 1, 2, 3 and 4 of the table apply only if you are a CGT small business entity (see section 152‑10).

Note 2: The small business income tax offset mentioned in item 6A of the table applies only if you are a small business entity as defined for the purposes of Subdivision 328‑F (see section 328‑357).

15 Paragraph 328‑110(1)(b)

Omit “$2 million” (wherever occurring), substitute “$10 million”.

16 Subsection 328‑110(3) (heading)

Repeal the heading, substitute:

Exception: aggregated turnover for 2 previous income years was $10 million or more

17 Paragraph 328‑110(3)(b)

Omit “$2 million”, substitute “$10 million”.

18 Paragraph 328‑110(4)(b)

Omit “$2 million”, substitute “$10 million”.

19 Section 328‑350

Repeal the section, substitute:

328‑350 What this Subdivision is about

You may be entitled to a tax offset if you are an individual:

(a) who is a small business entity; or

(b) whose assessable income includes a share of the net small business income of an unincorporated small business entity; or

(c) whose assessable income includes an amount because you are a partner in a partnership, or a beneficiary in a trust, that is a small business entity.

In working out whether you are or another entity is a small business entity, a special $5 million turnover threshold applies (see section 328‑357).

20 After section 328‑355

Insert:

For the purposes of this Subdivision, in working out whether you are a *small business entity for an income year, assume that each reference in section 328‑110 to $10 million were a reference to $5 million.

21 Subsection 995‑1(1)

Insert:

CGT small business entity has the meaning given by subsection 152‑10(1AA).

Part 2—Application of amendments

22 Application of amendments

(1) Subject to the following subitems, the amendments made by Part 1 of this Schedule apply to the 2016‑17 income year and later income years.

(2) The following apply to CGT events happening on or after the start of the 2016‑17 income year:

(a) the amendments made by items 1 to 13 of this Schedule;

(b) any other amendments made by this Schedule, to the extent that they relate to the amendments mentioned in paragraph (a).

(3) The amendments made by items 15 to 18 of this Schedule, to the extent that they relate to the operation of the Fringe Benefits Tax Assessment Act 1986, apply to the FBT year starting on 1 April 2017 and to later FBT years.

Schedule 4—Main consequential amendments relating to imputation

Part 1—Amendments commencing 1 July 2016

Income Tax Assessment Act 1997

1 Subsection 36‑55(2) (method statement, step 2)

Omit “the *standard corporate tax rate”, substitute “the entity’s *corporate tax rate for imputation purposes for that year”.

2 Subsection 197‑45(2) (formula)

Repeal the formula, substitute:

3 Subsection 197‑45(2)

Insert:

applicable gross‑up rate means the company’s *corporate tax gross‑up rate for the income year in which the franking debit arises.

4 Subsection 197‑60(3) (paragraph (a) of the definition of applicable tax rate)

Omit “the *standard corporate tax rate”, substitute “the company’s *corporate tax rate for imputation purposes for the income year in which the choice is made”.

5 Subsection 197‑60(4) (formula)

Repeal the formula, substitute:

6 At the end of subsection 197‑60(4)

Add:

where:

applicable gross‑up rate means the company’s *corporate tax gross‑up rate for the income year in which the choice is made.

7 Subsection 197‑65(3) (formula)

Repeal the formula, substitute:

8 Subsection 197‑65(3)

Insert:

applicable gross‑up rate means the company’s *corporate tax gross‑up rate for the income year in which the franking debit arises.

9 Subsection 200‑25(1)

Omit “the standard corporate tax rate”, substitute “the entity’s corporate tax rate for imputation purposes for the income year in which the distribution is made”.

10 Section 202‑55

Omit “the current standard corporate tax rate”, substitute “the entity’s corporate tax rate for imputation purposes for the income year in which the distribution is made”.

11 Subsection 202‑60(2) (formula)

Repeal the formula, substitute:

12 At the end of subsection 202‑60(2)

Add:

where:

applicable gross‑up rate means the *corporate tax gross‑up rate of the entity making the distribution for the income year in which the distribution is made.

13 Subsection 203‑50(2) (formula)

Repeal the formula, substitute:

14 Subsection 203‑50(2)

Insert:

applicable gross‑up rate means the *corporate tax gross‑up rate of the entity making the distribution for the income year in which the distribution is made.

15 Subsection 215‑20(2) (formula)

Repeal the formula, substitute:

16 At the end of subsection 215‑20(2)

Add:

where:

applicable gross‑up rate means the *corporate tax gross‑up rate of the entity making the distribution for the income year in which the distribution is made.

17 Subsection 705‑90(3) (formula)

Repeal the formula, substitute:

18 At the end of subsection 705‑90(3)

Add:

where:

applicable gross‑up rate means the joining entity’s *corporate tax gross‑up rate for the income year that ends, or, if section 701‑30 applies, for the income year that is taken by subsection (3) of that section to end, at the joining time.

19 Paragraph 707‑310(3A)(c) (formula)

Repeal the formula, substitute:

20 Section 976‑1 (formula)

Repeal the formula, substitute:

21 At the end of section 976‑1

Add:

where:

applicable gross‑up rate means the *corporate tax gross‑up rate of the entity making the distribution for the income year in which the distribution is made.

22 Section 976‑10 (formula)

Repeal the formula, substitute:

23 At the end of section 976‑10

Add:

where:

applicable gross‑up rate means the *corporate tax gross‑up rate of the entity making the distribution for the income year in which the distribution is made.

24 Section 976‑15 (formula)

Repeal the formula, substitute:

25 At the end of section 976‑15

Add:

where:

applicable gross‑up rate means the *corporate tax gross‑up rate of the entity making the distribution for the income year in which the distribution is made.

26 Subsection 995‑1(1) (definition of corporate tax gross‑up rate)

Repeal the definition, substitute:

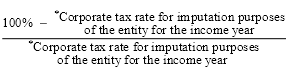

corporate tax gross‑up rate, of an entity for an income year, means the amount worked out using the following formula:

27 Subsection 995‑1(1) (definition of corporate tax rate)

Repeal the definition, substitute:

corporate tax rate:

(a) in relation to a company to which paragraph 23(2)(a) of the Income Tax Rates Act 1986 applies—means the rate of tax in respect of the taxable income of a company covered by that paragraph; or

(b) in relation to another entity—means the rate of tax in respect of the taxable income of a company covered by paragraph 23(2)(b) of that Act.

28 Subsection 995‑1(1)

Insert:

corporate tax rate for imputation purposes, of an entity for an income year, means:

(a) unless paragraph (b) applies—the entity’s *corporate tax rate for the income year, worked out on the assumption that the entity’s *aggregated turnover for the income year is equal to its aggregated turnover for the previous income year; or

(b) if the entity did not exist in the previous income year—the rate of tax in respect of the taxable income of a company covered by paragraph 23(2)(a) of the Income Tax Rates Act 1986.

29 Subsection 995‑1(1) (definition of standard corporate tax rate)

Repeal the definition.

Part 3—Application of amendments

The amendments made by Part 1 of this Schedule apply to the 2016‑17 income year and later income years.

Schedule 5—Other consequential amendments

Part 1—Amendments commencing 1 July 2016

Income Tax Assessment Act 1997

1 Paragraph 65‑30(2)(a)

Omit “0.285”, substitute “0.275”.

2 Paragraph 65‑35(3A)(a)

Omit “28.5”, substitute “27.5”.

Part 2—Amendments commencing 1 July 2017

Income Tax Assessment Act 1997

3 Subsection 36‑17(5) (example)

Omit “For the 2015‑16 income year, Company A (which is not a small business entity)”, substitute “For the 2017‑18 income year, Company A (which is not a base rate entity)”.

4 Subsection 36‑55(1) (example)

Omit “For the 2015‑16 income year, Company E (which is not a small business entity)”, substitute “For the 2017‑18 income year, Company E (which is not a base rate entity)”.

5 Subsection 36‑55(2) (example)

Omit “2002‑2003”, substitute “2017‑2018”.

6 Paragraph 65‑30(2)(a)

Omit “*small business entity”, substitute “base rate entity (within the meaning of the Income Tax Rates Act 1986)”.

7 Paragraph 65‑35(3A)(a)

Omit “*small business entity”, substitute “base rate entity (within the meaning of the Income Tax Rates Act 1986)”.

8 Subsection 115‑280(3) (example)

Omit “A listed investment company (which is not a small business entity)”, substitute “A listed investment company (which is not a base rate entity)”.

Part 4—Amendments commencing 1 July 2024

Income Tax Assessment Act 1997

17 Paragraph 65‑30(2)(a)

Omit “0.275”, substitute “0.27”.

18 Paragraph 65‑35(3A)(a)

Omit “27.5”, substitute “27”.

Part 5—Amendments commencing 1 July 2025

Income Tax Assessment Act 1997

19 Paragraph 65‑30(2)(a)

Omit “0.27”, substitute “0.26”.

20 Paragraph 65‑35(3A)(a)

Omit “27”, substitute “26”.

Part 6—Amendments commencing 1 July 2026

Income Tax Assessment Act 1997

21 Paragraph 65‑30(2)(a)

Omit “0.26”, substitute “0.25”.

22 Paragraph 65‑35(3A)(a)

Omit “26”, substitute “25”.

[Minister’s second reading speech made in—

House of Representatives on 1 September 2016

Senate on 27 March 2017]

(88/16)