Commercial Broadcasting (Tax) Act 2017

No. 110, 2017

An Act to impose a tax relating to transmitter licences that are associated with commercial broadcasting licences, and for related purposes

Commercial Broadcasting (Tax) Act 2017

No. 110, 2017

An Act to impose a tax relating to transmitter licences that are associated with commercial broadcasting licences, and for related purposes

Contents

2 Commencement

3 Definitions

4 Transmitter licence associated with a commercial broadcasting licence

5 Extension to external Territories

6 Imposition of tax

7 Amount of tax

8 Individual transmitter amount

9 Individual transmitter amount cap

10 Person liable to pay tax

11 Termination time

12 Indexation factor

13 Disallowance of determinations

14 Rebates

15 Act does not impose a tax on property of a State

16 Transitional—power to make legislative instruments

Commercial Broadcasting (Tax) Act 2017

No. 110, 2017

An Act to impose a tax relating to transmitter licences that are associated with commercial broadcasting licences, and for related purposes

[Assented to 18 September 2017]

The Parliament of Australia enacts:

This Act is the Commercial Broadcasting (Tax) Act 2017.

(1) Each provision of this Act specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information | ||

Column 1 | Column 2 | Column 3 |

Provisions | Commencement | Date/Details |

1. The whole of this Act | 1 July 2017. However, the provisions do not commence at all if the Broadcasting Legislation Amendment (Broadcasting Reform) Act 2017 does not receive the Royal Assent. | 1 July 2017 |

Note: This table relates only to the provisions of this Act as originally enacted. It will not be amended to deal with any later amendments of this Act.

(2) Any information in column 3 of the table is not part of this Act. Information may be inserted in this column, or information in it may be edited, in any published version of this Act.

In this Act:

associated with a commercial broadcasting licence has the meaning given by section 4.

broadcasting service has the same meaning as in the Broadcasting Services Act 1992.

commercial radio broadcasting licence has the same meaning as in the Broadcasting Services Act 1992.

commercial television broadcasting licence has the same meaning as in the Broadcasting Services Act 1992.

indexation factor, for a financial year, has the meaning given by section 12.

index number, in relation to a quarter, means the All Groups Consumer Price Index number, being the weighted average of the 8 capital cities, published by the Australian Statistician in respect of that quarter.

individual transmitter amount has the meaning given by section 8.

individual transmitter amount cap has the meaning given by section 9.

tax means tax imposed by this Act.

termination time has the meaning given by section 11.

transmitter means a radiocommunications transmitter (within the meaning of the Radiocommunications Act 1992).

transmitter licence has the same meaning as in the Radiocommunications Act 1992.

(1) For the purposes of this Act, if:

(a) a transmitter licence was or is issued under section 102 of the Radiocommunications Act 1992; and

(b) the related licence referred to in that section was allocated under Part 4 of the Broadcasting Services Act 1992;

the transmitter licence is associated with a commercial broadcasting licence.

(2) For the purposes of this Act, if:

(a) a transmitter licence was or is issued under section 100 of the Radiocommunications Act 1992; and

(b) the transmitter licence is held by the holder of:

(i) a commercial television broadcasting licence; or

(ii) a commercial radio broadcasting licence; and

(c) the transmitter licence authorises operation of a transmitter for transmitting or re‑transmitting the broadcasting service or services authorised by:

(i) the commercial television broadcasting licence; or

(ii) the commercial radio broadcasting licence;

as the case requires; and

(d) the issue of the transmitter licence is in accordance with a decision of the Australian Communications and Media Authority under subsection 34(1) of the Broadcasting Services Act 1992;

the transmitter licence is associated with a commercial broadcasting licence.

This Act extends to every external Territory.

General

(1) If:

(a) a transmitter licence is issued during the period:

(i) beginning at the start of 1 July 2017; and

(ii) ending at the termination time; and

(b) the transmitter licence is associated with a commercial broadcasting licence;

tax is imposed on:

(c) the issue of the transmitter licence; and

(d) each anniversary of the day the licence came into force that occurs:

(i) during the period the licence is in force; and

(ii) before the termination time.

(2) If:

(a) a transmitter licence was issued before 1 July 2017; and

(b) the transmitter licence is associated with a commercial broadcasting licence;

tax is imposed on each anniversary of the day the licence came into force that occurs:

(c) during the period the licence is in force; and

(d) on or after 1 July 2017; and

(e) before the termination time.

(3) If:

(a) a transmitter licence ceases to be in force during the period:

(i) beginning at the start of 1 July 2017; and

(ii) ending at the termination time; and

(b) the licence is not renewed; and

(c) the licence was varied on one or more occasions during the period:

(i) beginning at the end of the last anniversary of the day the licence came into force that occurred before the licence ceased to be in force; and

(ii) ending when the licence ceased to be in force; and

(d) if it were assumed that an anniversary of the day the licence came into force occurred on the day before the licence ceased to be in force, the amount of tax imposed by subsection 6(1) or (2) on the anniversary would have exceeded the tax that would have been imposed by that subsection on the anniversary if the licence had not been varied; and

(e) the transmitter licence was associated with a commercial broadcasting licence;

tax is imposed on the licence ceasing to be in force.

(4) For the purposes of paragraph (3)(c), disregard a variation that was made before 1 July 2017.

Transitional

(5) If:

(a) a person holds a transmitter licence at the start of 1 July 2017; and

(b) the transmitter licence is associated with a commercial broadcasting licence; and

(c) 1 July 2017 is not an anniversary of the day the licence came into force;

tax is imposed on the holding of the transmitter licence at the start of 1 July 2017.

General

(1) The amount of tax imposed by subsection 6(1) on the issue of a transmitter licence is the total of the individual transmitter amounts for the transmitters covered by the licence immediately after the licence came into force.

(2) The amount of tax imposed by subsection 6(1) or (2) on an anniversary of the day a transmitter licence came into force is the total of the individual transmitter amounts for the transmitters covered by the licence at the start of the anniversary.

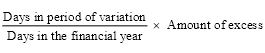

(3) The amount of tax imposed by subsection 6(3) on a transmitter licence ceasing to be in force during a financial year is worked out using the following formula:

where:

amount of excess means the amount of the excess mentioned in paragraph 6(3)(d).

days in period of variation means the number of days in the period:

(a) beginning at the start of the day after the first or only occasion on which the licence was varied as mentioned in paragraph 6(3)(c); and

(b) ending at the end of the day before the licence ceased to be in force.

days in the financial year means the number of days in the financial year.

Transitional

(4) The amount of tax imposed by subsection 6(5) on the holding of a transmitter licence at the start of 1 July 2017 is worked out using the following formula:

where:

amount of anniversary tax means the amount of tax that would be imposed by subsection 6(2) on a particular anniversary of the day the transmitter licence came into force, if it were assumed that 1 July 2017 were that particular anniversary.

pre‑anniversary days means the number of days in the period:

(a) beginning at the start of 1 July 2017; and

(b) ending at the start of the anniversary of the day the licence came into force that occurs during the financial year beginning on 1 July 2017.

(1) For the purposes of this Act, the individual transmitter amount for a transmitter covered by a transmitter licence at a particular time in a financial year is:

(a) if a determination is in force under subsection (2) at that time—the amount worked out under the determination; or

(b) otherwise—the individual transmitter amount cap for the transmitter for the financial year.

(2) The Minister may, by legislative instrument, make a determination for the purposes of paragraph (1)(a).

Note: See also section 13 (disallowance of determinations).

(3) A determination under subsection (2) may provide for different amounts in relation to:

(a) different classes of transmitters; or

(b) different periods; or

(c) different classes of licences; or

(d) licences held by different classes of persons.

(4) Subsection (3) does not limit subsection 33(3A) of the Acts Interpretation Act 1901.

(5) Subsection 12(2) of the Legislation Act 2003 does not apply to the first determination made under subsection (2) of this section.

(6) The individual transmitter amount for a transmitter covered by a transmitter licence at a particular time in a financial year must not exceed the individual transmitter amount cap for the transmitter for the financial year.

Note: See section 9, which deals with the individual transmitter amount cap.

(1) For the purposes of this Act, the individual transmitter amount cap for a transmitter for the financial year beginning on 1 July 2017 is worked out using the following table:

Individual transmitter amount cap—financial year beginning on 1 July 2017 | |||||

Item | Maximum power of the transmitter | Cap if transmitter operates in the AM band | Cap if transmitter operates in the FM band | Cap if transmitter operates in the VHF band | Cap if transmitter operates in the UHF band |

1 | Low | $40 | $405 | $18,661 | $18,661 |

2 | Medium | $365 | $4,053 | $186,611 | $186,611 |

3 | High | $3,648 | $40,533 | $1,866,114 | $1,866,114 |

(2) For the purposes of this Act, the individual transmitter amount cap for a transmitter for:

(a) the financial year beginning on 1 July 2018; or

(b) a later financial year;

is the amount worked out using the following formula:

where:

indexation factor means the indexation factor for the financial year.

previous individual transmitter amount cap means the individual transmitter amount cap for the transmitter for the previous financial year.

Band

(3) For the purposes of this section, the band in which a transmitter operates is worked out using the following table:

Band | ||

Item | A transmitter operates in this band … | … if the transmitter operates in this frequency range |

1 | AM band | 526.6 to 1606.5 kHz (inclusive) |

2 | FM band | 87.5 to 108 MHz (inclusive) |

3 | VHF band | 174 to 230 MHz (inclusive) |

4 | UHF band | 520 to 694 MHz (inclusive) |

Maximum power of transmitter

(4) For the purposes of this section, the maximum power of a transmitter is worked out using the following table:

Maximum power of transmitter | |||||

Item | The maximum power of a transmitter is … | … if the transmitter operates in the AM band and, under the transmitter licence, the maximum power for the transmitter is … | … if the transmitter operates in the FM band and, under the transmitter licence, the maximum power for the transmitter is … | … if the transmitter operates in the VHF band and, under the transmitter licence, the maximum power for the transmitter is … | … if the transmitter operates in the UHF band and, under the transmitter licence, the maximum power for the transmitter is … |

1 | Low | n/a | not more than 150 Watts ERP | not more than 150 Watts ERP | not more than 600 Watts ERP |

2 | Medium | not more than 220 volts CMF | greater than 150 Watts ERP but not more than 15,000 Watts ERP | greater than 150 Watts ERP but not more than 15,000 Watts ERP | greater than 600 Watts ERP but not more than 60,000 Watts ERP |

3 | High | greater than 220 volts CMF | greater than 15,000 Watts ERP | greater than 15,000 Watts ERP | greater than 60,000 Watts ERP |

(1) Tax imposed by this Act on the issue of a transmitter licence is payable by the person who held the licence when the licence was issued.

(2) Tax imposed by this Act on an anniversary of the day a transmitter licence came into force is payable by the person who held the licence at the start of the anniversary.

(3) Tax imposed by this Act on a licence ceasing to be in force is payable by the person who held the licence immediately before the licence ceased to be in force.

(4) Tax imposed by this Act on the holding of a transmitter licence at the start of 1 July 2017 is payable by the person who held the licence at the start of 1 July 2017.

(1) The Minister may, by legislative instrument, determine that a specified time is the termination time for the purposes of this Act.

(2) The termination time must not be earlier than the commencement of the determination.

(1) For the purposes of this Act, the indexation factor for a financial year is the number calculated, to 3 decimal places (rounding up if the fourth decimal place is 5 or more), using the formula:

where:

base March quarter means the last March quarter before the reference March quarter.

reference March quarter means the last March quarter before the financial year.

(2) Subject to subsection (3), if (whether before or after the commencement of this section) the Australian Statistician has published or publishes an index number in respect of a quarter in substitution for an index number previously published in respect of that quarter, the publication of the later index number must be disregarded for the purposes of this section.

(3) If (whether before or after the commencement of this section) the Australian Statistician has changed or changes the index reference period for the Consumer Price Index, then, for the purposes of the application of this section after the change took place or takes place, regard must only be had to the index number published in terms of the new index reference period.

Scope

(1) This section applies to a determination made under subsection 8(2).

Disallowance

(2) Either House of the Parliament may, following a motion upon notice, pass a resolution disallowing the determination. For the resolution to be effective:

(a) the notice must be given in that House within 15 sitting days of that House after the copy of the determination was tabled in the House under section 38 of the Legislation Act 2003; and

(b) the resolution must be passed, in pursuance of the motion, within 15 sitting days of that House after the giving of that notice.

(3) If:

(a) the determination is the first determination made under subsection 8(2); and

(b) neither House passes such a resolution;

the determination takes effect at the start of 1 July 2017.

(4) If:

(a) the determination is not the first determination made under subsection 8(2); and

(b) neither House passes such a resolution;

the determination takes effect on the day immediately after the last day upon which such a resolution could have been passed if it were assumed that notice of a motion to disallow the determination was given in each House on the last day of the 15 sitting day period of that House mentioned in paragraph (2)(a).

(5) Section 42 (disallowance) of the Legislation Act 2003 does not apply to the determination.

Note 1: The 15 sitting day notice period mentioned in paragraph (2)(a) of this section is the same as the 15 sitting day notice period mentioned in paragraph 42(1)(a) of the Legislation Act 2003.

Note 2: The 15 sitting day disallowance period mentioned in paragraph (2)(b) of this section is the same as the 15 sitting day disallowance period mentioned in paragraph 42(1)(b) of the Legislation Act 2003.

The Minister may, by legislative instrument, make rules that make provision for rebates of the whole or a part of an amount of tax payable by a person.

(1) This Act has no effect to the extent (if any) to which it imposes a tax on property of any kind belonging to a State.

(2) In this section, property of any kind belonging to a State has the same meaning as in section 114 of the Constitution.

The Minister must not make a legislative instrument under this Act before the day after this Act receives the Royal Assent.

[Minister’s second reading speech made in—

House of Representatives on 15 June 2017

Senate on 22 June 2017]

(125/17)