Banking (prudential standard) determination No. 5 of 2012

Prudential Standard APS 112 Capital Adequacy: Standardised Approach to Credit Risk

Banking Act 1959

I, John Francis Laker, delegate of APRA:

(a) under subsection 11AF(3) of the Banking Act 1959 (the Act) REVOKE Banking (prudential standard) determination No. 1 of 2010 including Prudential Standard APS 112 Capital Adequacy: Standardised Approach to Credit Risk made under that Determination; and

(b) under subsection 11AF(1) of the Act DETERMINE Prudential Standard APS 112 Capital Adequacy: Standardised Approach to Credit Risk in the form set out in the attached Schedule, which applies to ADIs and authorised NOHCs to the extent provided in paragraphs 2 to 4 of the prudential standard.

This instrument takes effect on 1 January 2013.

Dated 29 November 2012

[Signed]

John Francis Laker

Chair

Interpretation

In this instrument:

ADI is short for authorised deposit-taking institution which has the meaning given in section 5 of the Act.

APRA means the Australian Prudential Regulation Authority.

authorised NOHC has the meaning given in section 5 of the Act.

Schedule

Prudential Standard APS 112 Capital Adequacy: Standardised Approach to Credit Risk comprises the 70 pages commencing on the following page.

Prudential Standard APS 112

Capital Adequacy: Standardised Approach to Credit Risk

Objective and key requirements of this Prudential Standard

This Prudential Standard requires an authorised deposit-taking institution to hold sufficient regulatory capital against credit risk exposures.

The key requirements of this Prudential Standard are that an authorised deposit-taking institution:

- must apply risk-weights to on-balance sheet assets and off-balance sheet exposures for capital adequacy purposes. Risk-weights are based on credit rating grades or fixed weights broadly aligned with the likelihood of counterparty default; and

- may reduce the credit risk capital requirement for on-balance sheet assets and off-balance sheet exposures where the asset or exposure is secured against eligible collateral, where the authorised deposit-taking institution has obtained direct, irrevocable and unconditional credit protection in the form of a guarantee from an eligible guarantor, mortgage insurance from an acceptable lenders mortgage insurer, a credit derivative from a protection provider or where there are eligible netting arrangements in place.

Table of contents

Authority

Application

Interpretation

Scope

Definitions

Key principles

Risk-weighting approach

Use of ratings of external credit assessment institutions

Credit risk mitigation

Attachments

Attachment A - Risk-weights for on-balance sheet assets

Attachment B - Credit equivalent amounts for off-balance sheet exposures

Attachment C - Counterparty credit risk for bilateral and centrally cleared transactions

Attachment D - Residential mortgages

Attachment E - Unsettled and failed transactions

Attachment F - Short-term and long-term credit ratings

Attachment G - Guarantees

Attachment H - Simple and comprehensive approaches to the recognition of collateral

Attachment I - Credit derivatives in the banking book

Attachment J - Netting

- This Prudential Standard is made under section 11AF of the Banking Act 1959 (the Banking Act).

2. This Prudential Standard applies to all authorised deposit-taking institutions (ADIs) with the exception of:

(a) foreign ADIs;

(b) purchased payment facility providers (PPF providers); and

(c) ADIs that have approval from APRA to use an internal ratings-based approach to credit risk under Prudential Standard APS 113 Capital Adequacy: Internal Ratings-based Approach to Credit Risk (APS 113).

3. A reference to an ADI in this Prudential Standard, unless otherwise indicated, is a reference to:

(a) an ADI on a Level 1 basis; and

(b) a group of which an ADI is a member on a Level 2 basis.

4. If an ADI to which this Prudential Standard applies is:

(a) the holding company for a group of bodies corporate, the ADI must ensure that the requirements in this Prudential Standard are met on a Level 2 basis, where applicable; or

(b) a subsidiary of an authorised non-operating holding company (authorised NOHC), the authorised NOHC must ensure that the requirements in this Prudential Standard are met on a Level 2 basis, where applicable.

5. Terms that are defined in Prudential Standard APS 001 Definitions appear in bold the first time they are used in this prudential standard.

6. This Prudential Standard, subject to paragraphs 7 and 8, applies to all on-balance sheet assets held by an ADI and all its off-balance sheet exposures.

7. The following items are excluded from the scope of this Prudential Standard:

(a) assets or investments that are required to be deducted from Common Equity Tier 1 Capital, Additional Tier 1 Capital and/or Tier 2 Capital under Prudential Standard APS 111 Capital Adequacy: Measurement of Capital (APS 111);

(b) securitisation exposures which are subject to the requirements of Prudential Standard APS 120 Securitisation (APS 120); and

(c) liabilities of a covered bond special purpose vehicle to an issuing ADI as specified in Prudential Standard APS 121 Covered Bonds (APS 121).

8. Items subject to capital requirements under Prudential Standard APS 116 Capital Adequacy: Market Risk (APS 116) are excluded for the purpose of calculating risk-weighted assets for credit risk under this Prudential Standard, but not for the purpose of calculating counterparty credit risk capital requirements (refer to Attachment C).

9. The following definitions are used in this Prudential Standard:

(a) central counterparty (CCP) - a clearing house that interposes itself between counterparties to contracts traded in one or more financial markets, becoming the buyer to every seller and the seller to every buyer. A CCP becomes counterparty to trades with market participants through novation, an open offer system, or another legally binding arrangement. For the purposes of the capital framework, a CCP is a financial institution;

(b) clearing member - a member of, or a direct participant in, a CCP that is entitled to enter into a transaction with the CCP;

(c) client of a clearing member - a party to a transaction with a CCP through either a clearing member acting as a financial intermediary, or a clearing member guaranteeing the performance of the client to the CCP;

(d) close-out netting - the process of combining all outstanding transactions and reducing them to a single net payment in the event of default by a counterparty to a netting agreement;

(e) counterparty credit risk (CCR) - the risk that the counterparty to a transaction could default before the final settlement of the transaction’s cash flows. An economic loss would occur if the transactions or portfolio of transactions with the counterparty has a positive economic value at the time of default;

(f) credit-event payment - the amount that is payable by the credit protection provider to the credit protection buyer under the terms of a credit derivative contract following the occurrence of a credit event. The payment can be in the form of ‘physical settlement’ (payment of par in exchange for physical delivery of a deliverable obligation of the reference entity) or ‘cash settlement’ (either a payment determined on a par-less-recovery basis, i.e. determined using the par value of the reference obligation less that obligation’s recovery value, or a fixed amount, or a fixed percentage of the par amount);

(g) credit events - events affecting the reference entity that trigger a credit‑event payment under the terms of a credit derivative contract;

(h) credit protection - the extent of credit risk transference from the party buying credit protection to the party selling credit protection under the terms of a credit derivative contract;

(i) credit rating grades - grades of credit ratings to which external credit assessment institution (ECAI) ratings are mapped, and that correspond to relevant risk-weights;

(j) default funds - clearing members’ funded or unfunded contributions towards, or underwriting of, a CCP’s mutualised loss-sharing arrangements;

(k) deliverable obligation - any obligation of the reference entity that can be delivered, under the terms of a credit derivative contract, if a credit event occurs. A deliverable obligation is relevant for credit derivatives that are to be physically settled;

(l) eligible bilateral netting agreement - has the meaning in paragraph 7 of Attachment J;

(m) initial margin - the funded collateral posted by a clearing member or a client of a clearing member to a CCP to mitigate the potential future exposure of the CCP to the clearing member arising from the possible future change in value of their transactions. Initial margin does not include contributions to a CCP for mutualised loss-sharing arrangements;

(n) netting - the process under a netting agreement of combining all relevant outstanding transactions between two counterparties and reducing them to a single net sum for a party to either pay or receive;

(o) netting by novation - a netting agreement between two counterparties under which any obligation between the parties to deliver a given currency (or equity, debt instrument or commodity) on a given date is automatically amalgamated with all other obligations under the netting agreement for the same currency (or other instrument or commodity) and value date. The result is to legally substitute a single net amount for the previous gross obligations;

(p) normal settlement period - a contractual settlement period that is equal to or less than the market standard for the instrument underlying the transaction and, in any case, less than five business days;

(q) off-balance sheet exposures - exposures that must be converted to a credit equivalent amount (CEA) in order to be risk-weighted;

(r) offsetting transaction - the transaction leg between the clearing member and the CCP when the clearing member acts on behalf of a client (e.g. when a clearing member clears or novates a client’s trade);

(s) on-balance sheet netting - a netting agreement covering loans and deposits under which obligations between the parties are determined on a net basis. Loans are to be treated as an exposure and deposits with a lending ADI that are subject to on-balance sheet netting are to be treated as cash collateral as defined in Attachment H;

(t) overseas bank - for the purposes of this Prudential Standard, a reference to an overseas bank includes a financial institution which:

(i) has the power to accept deposits in the ordinary course of business;

(ii) is supervised by the supervisor of banks in its home country; and

(iii) is subject to substantially the same prudential requirements as ADIs (including capital adequacy);

(u) over-the-counter (OTC) derivative transaction - a customised, privately negotiated, risk-shifting agreement, the value of which is derived from the value of an underlying asset;

(v) payments netting - a process designed to reduce operational costs and risks associated with daily settlement of transactions. Payments netting is not recognised for credit risk mitigation (CRM) purposes under this Prudential Standard;

(w) positive current exposure amount - the difference between the agreed settlement price of a transaction and the current market price of the transaction where this would result in a loss to an ADI;

(x) qualifying CCP (QCCP) - an entity that is licensed to operate as a CCP (including a licence granted by way of confirming an exemption), and is permitted by the CCP’s regulator/supervisor to operate as such with respect to the products offered. This is subject to the provision that the CCP is based and prudentially supervised in a jurisdiction where the relevant regulator/overseer has established, and publicly indicated that it applies to the CCP on an ongoing basis, domestic rules and regulations that are consistent with the CPSS-IOSCO Principles for Financial Market Infrastructures;

(y) reference entity - the entity or entities whose obligations are used to determine whether a credit event has occurred under the terms of a credit derivative contract;

(z) reference obligation - the obligation used to calculate the amount payable when a credit event occurs under the terms of a credit derivative contract. A reference obligation is relevant for obligations that are to be cash settled (on a par-less-recovery basis);

(aa) roll-off risk - the risk of a sudden material increase in an exposure(s) when short-term obligations that have been netted against longer term claims either mature, are rescinded or are generally no longer available to offset the obligation;

(bb) securities financing transactions (SFTs) - transactions such as repurchase agreements, reverse repurchase agreements, and security lending and borrowing transactions where the value of the transactions depends on the market valuation of securities and the transactions are typically subject to margin agreements;

(cc) trade exposures - the current exposure (replacement cost) plus the potential future exposure of a clearing member or a client of a clearing member to a CCP arising from OTC derivatives, exchange traded derivatives or SFTs, plus the initial margin posted by the ADI, plus the variation margin due to the ADI from the CCP but is not yet received;

(dd) underlying exposure - the banking book exposure that is being protected by a credit derivative;

(ee) variation margin - the funded collateral posted on a daily or intraday basis by a clearing member or a client of a clearing member to a CCP based upon price movements of their transactions; and

(ff) walkaway clause - a provision that permits a non-defaulting counterparty to make only limited payments, or no payments at all, to a defaulting party, even if the defaulting party is a net creditor.

10. An ADI must apply risk-weights to its on-balance sheet assets and off-balance sheet exposures in accordance with the risk classes set out in this Prudential Standard for Regulatory Capital purposes. Risk-weights are based on credit rating grades or fixed risk-weights as determined by this Prudential Standard and are broadly aligned with the likelihood of counterparty default. An ADI must, where appropriate, use the ratings of ECAIs to determine the credit rating grades of an exposure, as set out in Attachment A and Attachment F.

11. An ADI may, subject to meeting the requirements of this Prudential Standard, use certain CRM techniques in determining the capital requirement for a transaction or exposure. The CRM techniques allowed in this Prudential Standard are the recognition of eligible collateral, lenders mortgage insurance, guarantees and the use of credit derivatives and netting.

12. APRA may, in writing, determine the risk-weighted amount of a particular on-balance sheet asset or off-balance sheet exposure of an ADI if APRA considers that the ADI has not risk-weighted the exposure appropriately.

On-balance sheet assets

13. An ADI’s total risk-weighted on-balance sheet assets (for the purpose of assessing its credit risk capital requirement) must equal the sum of the risk-weighted amounts of each on-balance sheet asset.

14. The risk-weighted amount of an on-balance sheet asset is determined by multiplying its current book value (including accrued interest or revaluations, and net of any specific provision or associated depreciation) by the relevant risk-weight in Attachment A. Where the transaction is secured by eligible collateral, or there is an eligible guarantee, lenders mortgage insurance, credit derivative or netting arrangement in place, the CRM techniques detailed in Attachment D, Attachment G, Attachment H, Attachment I and Attachment J may be used to reduce the capital requirement of the exposure.

Off-balance sheet exposures

15. An ADI’s total risk-weighted off-balance sheet credit exposures must be calculated as the sum of the risk-weighted amount of all its market-related and non-market-related transactions.

16. The risk-weighted amount of an off-balance sheet transaction that gives rise to credit exposure must be calculated by the following two-step process:

(a) first, the notional amount of the transaction must be converted into an on-balance sheet equivalent (CEA) (refer to Attachment B); and

(b) second, the resulting CEA must be multiplied by the risk-weight (refer to Attachment A) applicable to the counterparty or type of exposure. Where the transaction is secured by eligible collateral or there is an eligible guarantee, credit derivative or netting arrangement in place, the CRM techniques detailed in Attachments G, H, I and J may be used to reduce the capital requirement of the exposure.

17. An ADI must include all market-related off-balance sheet transactions (including on-balance sheet unrealised gains on market-related off-balance sheet transactions) held in the banking and trading books in calculating its risk-weighted credit exposures. Refer to Attachment C for the capital treatment for counterparty credit risk.

18. An ADI may only use the solicited ratings of ECAIs to determine the credit rating grades that correspond to the risk-weights for counterparties and exposures. Ratings must be used consistently for each type of claim.

19. An ADI may not use credit ratings for one entity within a corporate group to determine the risk-weight for other (unrated) entities within the same group. If the rated entity has guaranteed the unrated entity’s exposure to the ADI, the guarantee may be recognised for risk-weighting purposes if the recognition criteria detailed in Attachment G are satisfied.

20. An ADI may not recognise additional CRM on claims where the risk-weight is mapped from an ECAI issue-specific rating and that rating already reflects CRM.

21. For an ADI to obtain capital relief for use of a CRM technique, all documentation must be binding on all parties and legally enforceable in all relevant jurisdictions.The ADI must have undertaken sufficient legal review to be satisfied of the legal enforceability of the technique and its documentation. The ADI will be expected to undertake periodic reviews to confirm the ongoing enforceability of the technique and its documentation.

22. An ADI must have policies and procedures to manage the risks associated with its CRM techniques.

23. Where multiple CRM techniques cover a single exposure, an ADI will be required to divide the exposure into portions covered by each CRM technique. The risk-weighted assets of each portion must be calculated, and then totalled.

Claim | Credit rating grade | Risk- weight (%) |

7. Claims on local governments and non-commercial public sector entities in Australia and overseas (refer to Attachment F). | 1 2 3,4,5 6 Unrated | 20 50 100 150 100 |

Class III - Claims on international banking agencies, regional development banks, ADIs and overseas banks | | |

8. Claims on international banking agencies and multilateral regional development banks (refer to Attachment F). | 1 2,3 4,5 6 Unrated | 20 50 100 150 50 |

9. Claims (other than equity) on ADIs and overseas banks, being claims with an original maturity of three months or less (refer to Attachment F). | 1,2,3 4,5 6 Unrated | 20 50 150 20 |

10. Claims (other than equity) on ADIs and overseas banks with an original maturity of more than three months (refer to Attachment F). | 1 2,3 4,5 6 Unrated | 20 50 100 150 50 |

Class IV - Claims secured against eligible residential mortgages | | |

11. Refer to the risk-weighting schedule in Attachment D. | | |

Class V - Unsettled and failed transactions | | |

12. Refer to Attachment E. | | |

Claim | Credit rating grade | Risk- weight (%) |

Class VI - Past due claims | | |

13. The unsecured portion of any claim(other than a loan or claim secured against eligible residential mortgages in paragraph 14 of this Attachment) that is past due for more than 90 days and/or impaired: (a) where specific provisions are less than 20 per cent of the outstanding amount of the past due claim or impaired asset; or (b) where specific provisions are no less than 20 per cent of the outstanding amount of the past due claim or impaired asset. | | 150 100 |

14. Refer to the risk-weighting schedule in Attachment D for loans and claims secured against eligible residential mortgages that are past due for more than 90 days and/or impaired. | | |

Class VII – Other assets and claims | | |

15. Claims (other than equity) on Australian and international corporate counterparties (including insurance and securities companies) and commercial public sector entities (refer to Attachment F). Alternatively, if an ADI has obtained approval in writing from APRA, it may risk-weight all claims (other than equity) held on the banking book on Australian and international corporate counterparties (including insurance and securities companies) and commercial public sector entities at 100 per cent. If an ADI has obtained approval in writing to use a 100 per cent risk-weight for these claims, it must do so in a consistent manner and not use any credit ratings for any of these claims. | 1 2 3,4 5,6 Unrated | 20 50 100 150 100 |

16. All claims (other than equity) on private sector counterparties (other than ADIs, overseas banks and corporate counterparties). | | 100 |

Claim | Credit rating grade | Risk- weight (%) |

17. Investments in premises, plant and equipment and all other fixed assets. | | 100 |

18. Claims on all fixed assets under operating leases. | | 100 |

19. Equity exposures (as defined in paragraphs 49 to 52 of APS 113) that are not deducted from capital and that are listed on a recognised exchange. | | 300 |

20. Equity exposures (as defined in paragraphs 49 to 52 of APS 113) that are not deducted from capital and that are not listed on a recognised exchange. | | 400 |

21. Margin lending against listed instruments on recognised exchanges that is not deducted from capital as required under APS 111. | | 20 |

22. All other assets and claims not specified elsewhere. | | 100 |

- For the purposes of calculating counterparty credit risk capital requirements, an ADI must calculate the CEA of its market-related contracts. Where these contracts are not covered by an eligible bilateral netting agreement as set out in Attachment J, the ADI must calculate the CEA by using the current exposure method; this method is the sum of current credit exposure and potential future credit exposure (the add-on) of these contracts. Current credit exposure is defined as the sum of the positive mark-to-market value (or replacement cost) of these contracts.

- An ADI must, for the purpose of calculating its potential future credit exposure for each transaction, multiply the notional principal amount of each of these transactions by the relevant CCF specified in Table 1.

Residual maturity | Interest rate contracts (%) | Foreign exchange and gold contracts (%) | Equity contracts (%) | Precious metal contracts (other than gold) (%) | Other commodity contracts (other than precious metals) (%) |

1 year or less | 0.0 | 1.0 | 6.0 | 7.0 | 10.0 |

> 1 year to 5 years | 0.5 | 5.0 | 8.0 | 7.0 | 12.0 |

> 5 years | 1.5 | 7.5 | 10.0 | 8.0 | 15.0 |

3. The notional or nominal principal amount, or value, of a contract must be the reference amount used to calculate payment streams between counterparties to a contract.

4. Potential future credit exposure must be based on effective rather than apparent notional amounts. In the event that the stated notional amount of a contract is leveraged or enhanced by the structure of the transaction, an ADI must use the effective notional amount when calculating potential future credit exposure.

5. No potential future credit exposure is calculated for single currency floating/floating interest rate swaps as the credit exposure on these contracts must be evaluated solely on the basis of their mark-to-market values.

6. For contracts that are structured to settle outstanding exposures following specified payment dates where the terms are reset such that the mark-to-market value of the contract is zero on these specified dates, the residual maturity must be set equal to the time until the next reset date. In the case of interest rate contracts with these features and a remaining maturity of more than one year, the CCF to be applied is subject to a floor of 0.5 per cent even if there are reset dates of a shorter maturity.

7. For contracts with multiple exchanges of principal, the CCFs must be multiplied by the number of remaining payments (i.e. exchanges of principal) still to be made under the contract.

8. Contracts that do not fall within one of the specific categories listed in Table 1 must be treated as ‘other commodities contracts’.

9. An ADI may use all instruments included in its trading book as eligible collateral for securities financing transactions included in the trading book. Instruments that would otherwise not be treated as eligible collateral for the purposes of this Prudential Standard are subject to a haircut at the level applicable to non-main index equities listed on recognised exchanges. Where an ADI uses the own-estimates approach to haircutting, haircuts must be calculated for each individual security that counts as eligible collateral in the trading book but not the banking book.

10. An ADI must calculate the counterparty credit risk capital requirement for single name credit default swaps and single name total-rate-of-return swaps in the trading book using the potential future exposure CCFs in Table 2.

Table 2: Potential future exposure credit conversion factors

Type of swap | Protection buyer | Protection seller |

Credit default swap | | |

Qualifying reference obligation | 5% | 5% |

Non-qualifying reference obligation | 10% | 10% |

Total-rate-of-return swap | | |

Qualifying reference obligation | 5% | 5% |

Non-qualifying reference obligation | 10% | 10% |

11. An ADI, in calculating the counterparty credit risk capital requirement for an nth-to-default credit derivative transaction (such as a first-to-default transaction), must use the add-on determined by the nth-lowest credit quality underlying asset in the basket.

Pricing market-related contracts

12. An ADI must not enter into contracts at off-market prices other than historical rate rollovers on foreign exchange contracts. An ADI must have a policy framework in place agreed to by APRA that sets out its systems and controls for approving and monitoring these rollovers and adequately restrict the ADI’s capacity to enter into such contracts. Transactions outside of the agreed framework must be discussed with APRA to determine their appropriate treatment.

13. With the exception of a default fund guarantee in relation to clearing through central counterparties, the CEA for a non-market-related off-balance sheet transaction is calculated by multiplying the contracted amount of the transaction by the relevant CCF specified in Table 3.

Nature of transaction | Credit conversion factor (%) |

- Direct credit substitutes

| 100 |

2. Performance-related contingencies | 50 |

3. Trade-related contingencies | 20 |

4. Lending of securities or posting of securities as collateral | 100 |

5. Assets sold with recourse | 100 |

6. Forward asset purchases | 100 |

7. Partly paid shares and securities | 100 |

8. Placements of forward deposits | 100 |

9. Note issuance and underwriting facilities | 50 |

10. Other commitments (a) Commitments with certain drawdown (b) Commitments (e.g. undrawn formal standby facilities and credit lines) with an original maturity of: (i) one year or less; or (ii) over one year (c) Commitments that can be unconditionally cancelled at any time without notice (e.g. undrawn overdraft and credit card facilities providing that any outstanding unused balance is subject to review at least annually) or effectively provide for automatic cancellation due to deterioration in a borrower’s creditworthiness | 100 20 50 0 |

11. Irrevocable standby commitments provided under APRA-approved industry support arrangements | 0 |

14. Where a non-market-related off-balance sheet transaction is an undrawn or partially undrawn facility, in calculating the CEA, the ADI must use the amount of undrawn commitment or the maximum unused portion of the commitment available to be drawn during the remaining period to maturity.

15. In the case of irrevocable commitments to provide off‑balance sheet facilities, the original maturity must be measured from the commencement of the commitment up until the time the associated facility expires.

16. Irrevocable commitments to provide off-balance sheet facilities may be assigned the lower of the two applicable CCFs.

17. For capital adequacy purposes, an ADI must include all commitments in its capital calculation regardless of whether or not they contain material adverse change clauses or any other provisions that are intended to relieve the ADI of its obligations under certain conditions.

18. The capital treatment for a default fund guarantee provided to a central counterparty (CCP) is provided in paragraphs 27 to 30 of Attachment C.

- CCR capital requirements apply to off-balance sheet contracts only, including OTC derivatives transactions, exchange-traded derivatives and secured financing transactions (SFTs).

- For bilateral trades with a counterparty that is not recognised as a qualifying central counterparty (QCCP), the CCR capital requirement comprises the counterparty credit default risk capital requirement and the credit value adjustment (CVA) risk capital charge. The counterparty credit default risk requirement covers the losses arising from the default of a counterparty, and the CVA risk capital charge accounts for mark-to-market losses arising from the deterioration of the counterparty’s credit quality.

- For centrally cleared trades with a QCCP, the CCR capital requirement comprises the default fund charge (for an ADI accessing the QCCP directly as a clearing member), and a lower risk-weighted counterparty credit default risk charge on trade exposures including posted collateral. Trades cleared through a non-qualifying CCP, and client trades that do not meet the requirements set out in paragraph 25 of this Attachment, must be treated on a bilateral basis according to paragraph 2 of this Attachment.

- An ADI, other than an ADI with either funded or unfunded default fund contributions to a central counterparty, may apply to APRA for permission to calculate its CVA risk capital requirement using a simplified approach, instead of the approach set out in paragraphs 8 to 13 of this Attachment. Where APRA is satisfied that the nature and scale of the ADI’s OTC derivatives usage are such that the resulting CCR exposures are not sufficiently material, then it may allow an ADI to calculate its CVA risk capital charge as equal to its counterparty credit default risk capital requirement.

5. The risk-weighted assets (RWA) requirement for counterparty credit default risk for an off-balance sheet transaction that gives rise to credit exposure must be calculated by the following three-step process:

(a) the notional amount of the transaction must be converted into an on-balance sheet equivalent (CEA), by multiplying the amount by a specified CCF (refer to Attachment B), and adding this to the replacement cost (the marked-to-market value, if positive). For OTC derivatives, the CEA is calculated on a counterparty level and is then adjusted by subtracting the credit value adjustment (CVA) amount for that counterparty, which has already been recognised by the ADI as an incurred write-down (i.e. a CVA loss). The ADI must calculate the incurred CVA loss according to its own valuation methodology. The CVA must not include any debit value adjustment. No such adjustment is required for SFT transactions;

(b) where the transaction is secured by eligible collateral or there is an eligible guarantee, credit derivative or netting arrangement in place, the CRM techniques detailed in Attachment G, Attachment H, Attachment I and Attachment J may be used to reduce the capital requirement of the exposure; and

(c) the resulting CEA must be multiplied by the risk-weight (refer to Attachment A) applicable to the counterparty or type of exposure.

6. The counterparty-level CEA for bilateral OTC derivatives and exchange-traded derivatives is calculated by adding together the following:

(a) for each transaction not covered by an eligible bilateral netting agreement, the CEA is calculated under Attachment B and adjusted for collateralisation of that transaction under paragraph 27 of Attachment H;

(b) for transactions covered by an eligible bilateral netting agreement, the CEA is calculated under paragraph 28 of Attachment J and adjusted for collateralisation of that netting set under paragraph 27 of Attachment H.

7. The CEA amount for securities financing transactions (SFTs) is calculated by adding together the following:

(a) for a single uncollateralised SFT, the CEA calculated under paragraph 13 of Attachment B;

(b) for a single collateralised SFT, the CEA calculated under paragraph 26 of Attachment H; and

(c) for collateralised SFTs covered by an eligible bilateral netting agreement, the CEA calculated under paragraph 38 of Attachment J.

8. An ADI must calculate a CVA risk capital charge to cover the risk of mark-to-market losses on the expected CCR (CVA loss) to OTC derivatives. An ADI is not required to include in its CVA risk capital charge:

(a) transactions with a qualifying central counterparty (QCCP); and

(b) SFTs, unless APRA determines that the ADI’s CVA loss exposures arising from SFT transactions are material.

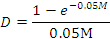

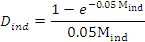

9. An ADI must calculate its CVA risk capital charge  according to one of the three following formulae:

according to one of the three following formulae:

(a) an ADI that has exposures arising from OTC derivatives with only one counterparty must calculate its CVA risk capital charge as:

where:

the weight applicable to the counterparty determined according to paragraph 10 of this Attachment;

the weight applicable to the counterparty determined according to paragraph 10 of this Attachment;

the weighted average maturity in years (weighted by notional amount) of all OTC transactions with the counterparty, determined according to paragraphs 33 to 41 of Attachment B to APS 113, except that

the weighted average maturity in years (weighted by notional amount) of all OTC transactions with the counterparty, determined according to paragraphs 33 to 41 of Attachment B to APS 113, except that  is not capped at 5 years;

is not capped at 5 years;

= the total CEA for the counterparty calculated according to paragraph 6 of this Attachment, without any adjustment for incurred CVA; and

= the total CEA for the counterparty calculated according to paragraph 6 of this Attachment, without any adjustment for incurred CVA; and

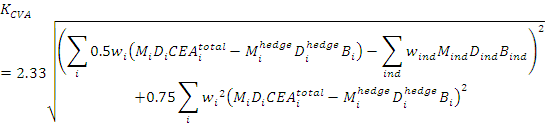

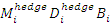

(b) an ADI that has exposures arising from OTC derivatives with more than one counterparty, but does not allow for CVA hedges in accordance with paragraph 12 of this Attachment, must calculate its CVA risk capital charge as:

where the summations (subscript i) are by counterparty;

(c) an ADI that has exposures arising from OTC derivatives with more than one counterparty, and has in place eligible CVA hedges in accordance with paragraph 12 of this Attachment, must calculate its CVA risk capital charge as:

where:

the maturity in years of the purchased single name CDS hedge referencing counterparty i and used to hedge CVA risk;

the maturity in years of the purchased single name CDS hedge referencing counterparty i and used to hedge CVA risk;

the notional amount of the purchased single-name CDS hedge referencing counterparty i and used to hedge CVA risk;

the notional amount of the purchased single-name CDS hedge referencing counterparty i and used to hedge CVA risk;

the weight applicable to the credit index ‘ind’ determined according to paragraph 10 of this Attachment;

the weight applicable to the credit index ‘ind’ determined according to paragraph 10 of this Attachment;

the maturity in years of ‘ind’ CDS index purchased protection.

the maturity in years of ‘ind’ CDS index purchased protection.

the notional amount of ‘ind’ CDS index purchased protection used to hedge CVA risk.

the notional amount of ‘ind’ CDS index purchased protection used to hedge CVA risk.

An ADI that has more than one purchased single-name CDS hedge referencing counterparty i used to hedge CVA risk, must replace  in the formula above by the sum over all such hedges:

in the formula above by the sum over all such hedges:

where each hedge is denoted by the subscript j = 1, 2, 3,..

An ADI that has purchased more than one CDS index protection to hedge CVA risk replace  in the formula above by the sum over all such hedges:

in the formula above by the sum over all such hedges:

where each hedge is denoted by the subscript j = 1, 2, 3,..

10. For the purposes of calculating the CVA risk capital charge, an ADI must determine the weight for a counterparty or credit index by its credit rating grade according to Table 4 below.

Table 4: CVA risk capital formula weights

Long term credit rating grade | Weight (%) |

1 | 0.7 |

2 | 0.8 |

3 | 1.0 |

4 or unrated | 2.0 |

5 | 3.0 |

6 | 10.0 |

11. An ADI may include eligible CVA hedges in the calculation of the CVA risk capital charge as set out in paragraph 9(c) of this Attachment subject to the following conditions:

(a) to qualify as an eligible CVA hedge, the hedge must be transacted with an external counterparty, used for the purpose of mitigating CVA risk, and managed as such;

(b) the only CDS hedges that may qualify as eligible CVA hedges are single-name CDS (including sovereign CDS), single-name contingent CDS, other equivalent hedging instruments referencing the counterparty directly, and index CDS. A tranched or nth-to-default CDS may not be treated as an eligible CVA hedge; and

(c) an instrument for which the associated payment depends on cross-default (such as a related entity hedged with a reference entity CDS and CDS triggers) may not be treated as an eligible CVA hedge. If restructuring is not included in the CDS contract then the proportion of that CDS hedge that may be treated as an eligible CVA hedge is as in accordance with the rules regarding specific risk offsetting set out in Attachment D to APS 116.

12. Other types of counterparty risk hedges must not be reflected within the calculation of the CVA risk capital charge, and these other hedges must be treated as any other instrument in the ADI’s inventory for Regulatory Capital purposes. Eligible CVA hedges that are included in the CVA risk capital charge must not be included in the ADI’s market risk capital charge calculation under APS 116.

13. If a counterparty is also a constituent of an index on which a CDS is used for hedging CCR, the notional amount attributable to that single name (as per its reference entity weight) may, with APRA’s approval, be subtracted from the index CDS notional amount and treated as a single name eligible CVA hedge of the individual counterparty with maturity based on the maturity of the index.

14. This section outlines the various types of exposures to central counterparties arising from OTC derivatives, exchanged-traded derivatives transactions and SFTs, and the capital and risk management practice requirements applied to them. Exposures arising from the settlement of cash transactions (equities, fixed income, spot FX and spot commodities) are not subject to this treatment.

15. An ADI that is either a clearing member or a client of a clearing member for an exchange-traded derivatives transaction for which the clearing member-to-client leg is conducted under a bilateral agreement, must treat the transaction as an OTC derivative for the purpose of calculating capital requirements.

16. APRA may require an ADI to hold additional capital against its exposures to a QCCP if an external assessment has found material shortcomings in the regulation of the QCCP and the CCP regulator has not since publicly addressed the issues identified.

17. Where the CCP is in a jurisdiction that does not have a CCP regulator applying the CPSS/IOSCO Principles for Financial Market Infrastructures to the CCP, APRA may make a determination as to whether the CCP meets the definition of a qualifying CCP.

18. An ADI must monitor and report to senior management and the appropriate committee of the Board on a regular basis all of its exposures to CCPs, including exposures arising from trading through a CCP and exposures arising from CCP membership obligations such as default fund contributions.

19. An ADI acting as a clearing member to a QCCP (i.e. direct access) must hold capital for trade exposures and default fund exposure. An ADI acting as a client of a clearing member to a QCCP (i.e. indirect access) must hold capital for its trade-related exposures, and (if applicable) CVA risk. A clearing member ADI that guarantees the trade for its client must hold capital for all of the above exposures. The risk-weight applied to the trade-related exposures depends on whether and to what extent the conditions set out in paragraph 25 of this Attachment are met. The risk-weights are summarised in paragraphs 23 to 26 of this Attachment.

20. An ADI that has trade exposures to a QCCP must, as part of its capital management planning, assess whether the level of capital held against trade exposures to a QCCP adequately relates to the inherent risks of those transactions. In particular, the ADI must consider if (i) its dealings with the QCCP give rise to higher risk exposures; or (ii) it is dealing with a CCP where, given the context of that ADI’s dealings, it is unclear that the CCP meets the QCCP definition in paragraph 9(x) of this Prudential Standard.

21. An ADI that is a clearing member must, as part of its capital management planning, assess through appropriate scenario analysis and stress testing whether the level of capital held against exposures to a QCCP adequately relates to the inherent risks of those transactions. This assessment must include potential future or contingent exposures resulting from future drawings on default fund commitments, and/or from secondary commitments to take over or replace offsetting transactions from clients of another clearing member in the event that the clearing member defaults or becomes insolvent.

22. Within three months of a central counterparty ceasing to qualify as a QCCP, an ADI must apply risk-weights for the bilateral counterparties to its trades with the central counterparty. Until that time, unless APRA otherwise requires, the trades with a former QCCP may be treated as though they continue to be with a QCCP.

Trade exposure capital calculations for clearing members

23. An ADI that is acting as a clearing member of a QCCP, for its own purposes, must apply a risk-weight of two per cent to its trade exposures to the QCCP, calculated in respect of its OTC derivatives, exchange-traded derivatives and SFT transactions with the QCCP. Where the clearing member offers clearing services to clients, the two per cent risk-weight also applies to the clearing member’s trade exposure to the QCCP that arises when the clearing member is obligated to reimburse the client for any losses suffered due to changes in the value of its transactions in the event that the QCCP defaults. Furthermore, to the extent that the rules referenced in Attachment J include the term ‘master netting agreement’, this term is to be read as including any ‘netting agreement’ that provides legally enforceable rights of set-off. If an ADI cannot demonstrate that the netting agreements meet the rules set out in Attachment J, it must treat each single transaction as a netting set of its own for the calculation of trade exposure.

24. For capital purposes, a clearing member ADI must treat its CEA to its clients as bilateral trades, and calculate a CVA risk capital charge. However, to recognise the shorter close-out period for cleared transactions, the clearing member ADI may apply a multiplication factor to its CEA to these exposures according to the following scale:

Table 5: Multiplication factor for clearing members’ exposures to their clients

Margin period of risk | Multiplication factor |

5 days or less | 0.71 |

6 days | 0.77 |

7 days | 0.84 |

8 days | 0.89 |

9 days | 0.95 |

10 days | 1.00 |

Trade exposure capital calculations for clients of clearing members

25. An ADI that:

(a) clears through a QCCP indirectly as a client of a clearing member acting as a financial intermediary (i.e. the clearing member completes an offsetting transaction with the QCCP); or

(b) enters into a transaction with the QCCP, with the clearing member guaranteeing its performance

must treat its exposure to the clearing member or QCCP, respectively, as if it were a clearing member’s exposure to the QCCP and risk-weight its exposure according to paragraph 23 when the following conditions are met:

(i) the offsetting transactions are identified by the QCCP as client transactions, and the collateral to support the offsetting transactions is held in a manner that prevents any losses to the client ADI due to either the default or insolvency of the clearing member, or the default or insolvency of the clearing member’s other clients. Additionally, upon request, the client ADI must provide to APRA an independent, legal opinion, in writing, that proves the validity of this condition in the presence of any legal challenges under relevant laws;

(ii) collateral supporting the offsetting transactions is held in a manner that prevents any losses to the client ADI due to the joint default or insolvency of the clearing member and any of its other clients. Additionally, on request, the client ADI must provide to APRA an independent legal opinion, in writing, that proves the validity of these conditions in the presence of any legal challenges under relevant laws; and

(iii) in case the clearing member defaults or becomes insolvent, the relevant laws, rules, contractual or administrative arrangements provide that offsetting transactions are highly likely to continue to be indirectly transacted through the QCCP, or by the QCCP. In such circumstances, the client positions and collateral with the QCCP will be transferred at market value unless the client ADI requests closing out the position at market value.

If only conditions (i) and (iii) are satisfied, a risk-weight of four per cent must be applied to the ADI’s exposure to the clearing member. In any other cases, the ADI must, for capital purposes, treat its exposure to the clearing member as bilateral trades, including the calculation of the CVA risk capital charge.

Capital treatment of posted collateral

26. An ADI (either as a clearing member or a client of a clearing member) that has posted collateral must risk-weight those assets in accordance with the risk-weights that otherwise apply under this Prudential Standard or APS 113 as applicable, if the collateral is held in the banking book, or under APS 116, if the collateral is held in the trading book, regardless of the fact that such assets have been posted as collateral. In addition, an ADI must apply risk-weights to posted collateral reflecting the circumstances under which the collateral is held and the creditworthiness of the entity holding the collateral. In particular:

(a) an ADI that is a clearing member:

(i) must apply a two per cent risk-weight to posted collateral held by the QCCP where that collateral is included in the definition of trade exposures to a QCCP and not held in a bankruptcy-remote manner; and

(ii) may apply a zero risk-weight to posted collateral (including cash, securities and excess initial and variation margin) held by a custodian where that collateral is bankruptcy remote from the QCCP;

(b) an ADI that is a client of a clearing member:

(i) may apply a zero risk-weight to posted collateral held by a custodian where the collateral is bankruptcy remote from the QCCP, the clearing member, and the clearing member’s other clients;

(ii) must apply a two per cent risk-weight to posted collateral held by the QCCP if the collateral is not bankruptcy remote from the QCCP, and all conditions (i), (ii) and (iii) in paragraph 25 of this Attachment are all satisfied; and

(iii) must apply a four per cent risk-weight to posted collateral held by the QCCP if the collateral is not bankruptcy remote from the QCCP, and only conditions (i) and (iii) in paragraph 25 of this Attachment are all satisfied.

Capital requirements for default fund exposure to a QCCP

27. Where a default fund is shared between products or types of businesses with settlement risk only and products or types of business that give rise to counterparty credit risk, all of the default fund contributions will receive the risk-weight determined according to the formula set out in paragraph 28 of this Attachment, without apportioning between different classes or types of products. However, where the default fund contributions from clearing members are segregated by product types and only accessible for specific product types, the capital requirements for those default fund exposures determined according to the formulae and methodology set out in paragraph 28 of this Attachment must be calculated for each specific product giving rise to counterparty credit risk.

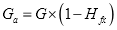

28. The risk-weighted assets (RWA) for the clearing member ADI’s default fund exposure is calculated by the following formula:

where

= the ADI’s pre-funded contribution to the QCCP’s default fund

= the ADI’s pre-funded contribution to the QCCP’s default fund

= trade exposure to the QCCP calculated according to paragraph 23 of this Attachment.

= trade exposure to the QCCP calculated according to paragraph 23 of this Attachment.

29. An ADI must risk-weight its trade exposures to a non-qualifying CCP in accordance with Attachment A, and calculate a CVA risk capital charge in respect of those exposures.

30. An ADI that is a clearing member of a non-qualifying CCP must calculate a capital requirement in respect of its default fund contributions to that CCP according to the following formula:

where:

= the ADI’s risk-weighted assets in respect of its default fund exposure to the CCP

= the ADI’s risk-weighted assets in respect of its default fund exposure to the CCP

= the ADI’s pre-funded contribution to the default fund of the CCP, plus a proportion, to be specified by APRA, of the ADI’s unfunded contributions that are liable to be paid should the CCP so require.

= the ADI’s pre-funded contribution to the default fund of the CCP, plus a proportion, to be specified by APRA, of the ADI’s unfunded contributions that are liable to be paid should the CCP so require.

- An ADI must at all times have unequivocal enforcement rights over a mortgaged residential property (including a power of sale and a right to possession) in the event of default by the borrower.

- An ADI that outsources any part of its credit assessment process to a third party (such as a mortgage originator or broker) must ensure that the arrangement complies with Prudential Standard APS 231 Outsourcing[26].

- Loans covered by security provided by third parties, where the relevant mortgage is unenforceable under the National Credit Code, are risk-weighted at 100 per cent in the absence of any eligible collateral and guarantees.

- Subject to satisfying other criteria set out in this Attachment, loans for purposes other than housing must be secured against mortgages over existing residential property to receive a risk-weight of less than 100 per cent. Loans, for whatever purpose, secured against speculative residential construction or property development do not qualify for a risk-weight of less than 100 per cent.

5. In order to determine the appropriate risk-weight for a residential mortgage, an ADI must classify the loan as either a standard or non-standard eligible mortgage (refer to paragraphs 6 and 7 of this Attachment) and determine the ratio of the outstanding amount (refer to paragraphs 8 and 9 of this Attachment) of the loan to the value of the residential property or properties that secure the exposure (loan-to-valuation ratio, LVR). For this purpose, the valuation may be based on the valuation at origination or, where relevant, on a subsequent formal revaluation by an independent accredited valuer. The determination of the appropriate risk-weight is also dependent upon mortgage insurance provided by an acceptable lenders mortgage insurer (LMI) (refer to paragraph 14 of this Attachment). For this purpose, lenders mortgage insurance must provide cover for all losses up to at least 40 per cent of the higher of the original loan amount and outstanding loan amount (if higher than the original loan amount). Risk-weights are as detailed in Table 4.

Table 4: Risk-weights for residential mortgages

LVR (%) | Standard eligible mortgages | Non-standard eligible mortgages |

| Risk-weight (no mortgage insurance) % | Risk-weight (with at least 40% of the mortgage insured by an acceptable LMI) % | Risk-weight (no mortgage insurance) % | Risk-weight (with at least 40% of the mortgage insured by an acceptable LMI) % |

0 – 60 | 35 | 35 | 50 | 35 |

60.01 – 80 | 35 | 35 | 75 | 50 |

80.01 – 90 | 50 | 35 | 100 | 75 |

90.01 – 100 | 75 | 50 | 100 | 75 |

> 100.01 | 100 | 75 | 100 | 100 |

6. A standard eligible mortgage is defined as a residential mortgage where the ADI has:

(a) prior to loan approval and as part of the loan origination and approval process, documented, assessed and verified the ability of the borrowers to meet their repayment obligation;

(b) valued any residential property offered as security; and

(c) established that any property offered as security for the loan is readily marketable.

The ADI must also revalue any property offered as security for such loans when it becomes aware of a material change in the market value of property in an area or region.

7. Loans that are secured by residential properties but fail to meet the criteria detailed in paragraph 6 of this Attachment must be classified as non-standard eligible mortgages. Such loans may be reclassified as standard loans where the borrowers have substantially met their contractual loan repayments to the ADI continuously over the previous 36 months. Criteria defining when contractual loan repayments are substantially met must be set out in the ADI’s lending/credit policy and procedures manual.

8. For the purposes of paragraph 5 of this Attachment, the outstanding amount of a loan must be calculated as the balance of all claims on the borrower that are secured against the mortgaged residential property. This includes accrued interest and fees, as well as the gross value of any undrawn limits on commitments that cannot be cancelled at any time without notice. The outstanding amount under an ‘all moneys mortgage’ must include all loans and other exposures to the borrower that are effectively secured against the mortgage.

9. If a loan is also secured against a second mortgage, the outstanding amount of the loan must be calculated as the sum of all claims on the borrower secured by both the first and second mortgages over the same residential property for the purpose of assessing the LVR.

10. If a loan is secured by more than one property, the LVR must be determined on the basis of the outstanding amount of all claims on the borrower that are secured against the mortgaged residential properties to the aggregate value of the mortgaged residential properties.

11. An ADI may, in risk-weighting a loan secured by a residential mortgage, make allowance for eligible collateral and guarantees. The recognition of eligible collateral and guarantees is detailed in Attachment G and Attachment H. A mortgage offset or other similar account may only be netted off against the outstanding amount of the loan where the arrangement meets the requirements for eligible cash collateral as set out in Attachment H.

Past due claims

12. Risk-weights for loans and claims secured against eligible residential mortgages that are past due for more than 90 days and/or impaired are detailed in Table 6.

Table 6: Risk-weights for past due eligible residential mortgages

Eligible residential mortgages | Risk-weight (%) |

Where the claim is not mortgage insured with an acceptable LMI. | 100 |

Where the claim is mortgage insured with an acceptable LMI[28] to the extent that the total of loans and claims covered by a single insurer that are past due for more than 90 days and/or impaired do not exceed the ADI’s large exposure limit. | Original risk-weights |

Where the claim is mortgage insured with an acceptable LMI[30] to the extent that the total of loans and claims covered by a single insurer that are past due for more than 90 days and/or impaired exceed the ADI’s large exposure limit[31]. | 100 |

13. To qualify for a risk-weight of less than 100 per cent, any loans secured by a second mortgage over residential property must, in addition to the requirements in this Attachment, satisfy the following conditions:

(a) the first mortgage must not be extended without being subordinated to the second mortgage;

(b) an ADI must obtain written consent of the first mortgagee for the second mortgage and confirm the maximum outstanding amount of the loan secured by the first mortgage (including maximum drawdown or limit of facility) for LVR purposes; and

(c) an ADI must ensure that its interest as second mortgagee is noted on the title.

14. To qualify as a mortgage insured by an acceptable LMI:

(a) for the purposes of the Level 1 Regulatory Capital, the LMI must be regulated by APRA; and

(b) for the purposes of the Level 2 Regulatory Capital, in the case of overseas subsidiaries of Australian ADIs, APRA will accept the host supervisors’ requirements on what constitutes an acceptable LMI in those jurisdictions.

- The risk-weights for delivery-versus-payment (DvP), transactions with a normal settlement period that remain unsettled after their due delivery dates are detailed in Table 7. The amount that must be multiplied by the relevant risk-weight is the positive current exposure amount.

Table 7: Risk-weights: delivery-versus-payment transactions

Number of business days after due settlement date | Risk-weight (%) |

5 to 15 | 100 |

16 to 30 | 625 |

31 to 45 | 937.5 |

46 or more | 1250 |

2. An ADI must hold Regulatory Capital against a non-DvP transaction with a normal settlement period where:

(a) it has paid for debt instruments, equities, foreign currencies or commodities before receiving them or it has delivered debt instruments, equities, foreign currencies or commodities before receiving payment for them; and

(b) in the case of a cross-border transaction, one day or more has elapsed since it made that payment or delivery.

3. The capital requirement for a non-DvP transaction referred to in paragraph 2 of this Attachment is calculated as follows:

(a) from the business day after the ADI has made its payment or delivery for up to and including four business days after the counterparty payment or delivery is due, the ADI must treat the transaction as an exposure; and

(b) from five business days after the ADI has made its payment or delivery until extinction of the transaction, the ADI must apply a 1250 per cent risk-weight (refer to APS 111) to the value transferred plus the positive current exposure.

4. Where a non-DvP transaction is required to be treated as an exposure (refer to paragraph 3(a) of this Attachment) an ADI may apply the relevant risk-weight as detailed in Attachment A. Alternatively, where exposures are not material, the ADI may apply a 100 per cent risk-weight provided that all such exposures are risk-weighted consistently.

- For capital adequacy purposes, an ADI may only use an ECAI rating that takes into account all amounts, both principal and interest, owed to it.

2. Where a counterparty has multiple ECAI general issuer ratings or where an issue has multiple ECAI issue-specific ratings, and these ratings correspond to multiple credit rating grades, an ADI must apply the following principles for capital requirement purposes:

(a) where there are two ratings that correspond to different credit rating grades, the credit rating grade that corresponds to the higher risk-weight must be used; or

(b) where there are three or more ratings that correspond to different credit rating grades, the credit rating grades corresponding to the two lowest risk-weights must be applied and the higher of those two risk-weights must be used.

3. An ADI must not use an ECAI rating that refers to a claim denominated in a particular currency to derive the credit rating grade for another claim on the same counterparty if that claim is denominated in another currency.

4. An ADI’s claim must be assessed as unrated for risk-weighting purposes if:

(a) the ADI’s claim does not have an ECAI issue-specific rating;

(b) a credit rating grade for the ADI’s claim cannot be inferred from an ECAI issue-specific rating of an issued debt of the counterparty; and

(c) the counterparty does not have a general ECAI issuer rating from which a credit rating grade for the ADI’s claim can be inferred.

5. Short-term ratings by ECAIs must only be used for short-term claims against ADIs, overseas banks and corporate counterparties.

6. If there is an ECAI issue-specific short-term rating in respect of a claim, an ADI must use this rating to determine the credit rating grade of the claim. However, this ECAI issue-specific short-term rating cannot be used to risk-weight any other claim.

7. The risk-weights in Table 8 apply to ECAI issue-specific short-term ratings:

Table 8: Risk-weights for short-term claims

Credit rating grade (short-term claims on corporates, ADIs and overseas banks) | 1 | 2 | 3 | 4 |

Risk-weight (%) | 20 | 50 | 100 | 150 |

8. Notwithstanding paragraph 6 of this Attachment, where the counterparty has a short-term claim that attracts a 50 per cent risk-weight, unrated short-term claims on the same counterparty cannot be risk-weighted at less than 100 per cent.

9. Notwithstanding paragraph 6 of this Attachment, where the counterparty has a short-term claim that attracts a risk-weight of 150 per cent, all unrated claims (short-term and long-term) on the same counterparty must be risk-weighted at not less than 150 per cent.

10. Where there is no ECAI issue-specific short-term rating, the general preferential treatment for short-term claims detailed in item 9 of Attachment A may apply to all claims on ADIs and overseas banks that have an original maturity of up to three months.

11. Where there is an ECAI issue-specific short-term rating on a claim held by an ADI, and that rating corresponds to a credit rating grade that is lower than or identical to that derived from the general treatment detailed in item 9 of Attachment A, the ECAI issue-specific short-term rating may be used for the specific claim.

12. Where there is an ECAI issue-specific rating for a short-term claim on an ADI or overseas bank and that rating corresponds to a higher credit rating grade than that which would be applied by item 9 of Attachment A, the general short-term preferential treatment cannot be used for any short-term claim on the counterparty. All unrated short-term claims on that counterparty would be assigned the same credit rating grade as that implied by the ECAI issue-specific short-term rating.

13. For the purposes of this Attachment, where the ECAI is Standard & Poor’s, Moody’s or Fitch, ratings are to be mapped as shown in Table 9 and Table 10 below.

Table 9: Recognised long-term ratings and equivalent credit rating grades

Credit rating grade | Standard & Poor’s Corporation | Moody’s Investor Services | Fitch Ratings |

1 | AAA AA+ AA AA- | Aaa Aa1 Aa2 Aa3 | AAA AA+ AA AA- |

2 | A+ AA- | A1 A2 A3 | A+ A A- |

3 | BBB+ BBB BBB- | Baa1 Baa2 Baa3 | BBB+ BBB BBB- |

4 | BB+ BB BB- | Ba1 Ba2 Ba3 | BB+ BB BB- |

5 | B+ B B- | B1 B2 B3 | B+ B B- |

6 | CCC+ CCC CCC- CC C D | Caa1 Caa2 Caa3 Ca C | CCC+ CCC CCC- CC C D |

Table 10: Recognised short-term ratings and equivalent credit rating grades

Credit rating grade | Standard & Poor’s Corporation | Moody’s Investor Services | Fitch Ratings |

1 | A-1 | P-1 | F-1 |

2 | A-2 | P-2 | F-2 |

3 | A-3 | P-3 | F-3 |

4 | Others | Others | Others |

- Where a claim on a counterparty is secured by a guarantee from an eligible guarantor (refer to paragraph 3 of this Attachment), the portion of the claim that is supported by the guarantee may be weighted according to the risk-weight appropriate to the guarantor. The unsecured portion of the claim must be weighted according to the risk-weight applicable to the original counterparty (refer to Attachment A).

- A guarantee must represent a direct claim on the guarantor with the extent of the cover being clearly defined and incontrovertible. A guarantee must be irrevocable such that there must be no clause in the guarantee that would allow the guarantor to cancel unilaterally the cover of the guarantee or that would increase the effective cost of cover as a result of deteriorating credit quality in the guaranteed exposure[37]. A guarantee must also be unconditional; there must be no clause in the guarantee outside the direct control of an ADI that could prevent the guarantor from being obliged to pay out in a timely manner in the event that the original counterparty fails to make the due payment(s).

- Subject to the conditions in this Prudential Standard, the following entities are recognised as eligible guarantors:

(a) Commonwealth, State, Territory and local governments in Australia (including State and Territory central borrowing authorities); central, state, regional and local governments in other countries; public sector entities in Australia and overseas; the Reserve Bank of Australia; central banks in other countries; ADIs and overseas banks; international banking agencies and multilateral regional development banks; and

(b) other entities that are externally rated, where credit protection is provided to a non-securitisation exposure. This would include guarantees provided by parent, subsidiary and affiliate companies where they have a lower risk-weight than the obligor. Where credit protection is provided to a securitisation exposure, other entities with a credit rating grade of three or better and that were externally rated two or better at the time the credit protection was provided. This also includes guarantees provided by parent, subsidiary and affiliated companies where they have a lower risk-weight than the obligor.

4. A claim that is indirectly guaranteed by the Australian Government (i.e. guarantee of guarantee, such as the Commonwealth’s guarantee of the entity that provides the guarantee) may be treated as guaranteed by the Australian Government provided that:

(a) the indirect guarantee covers all credit risk elements of the claim;

(b) both the original guarantee and the indirect guarantee meet all the operational requirements for guarantees except that the indirect guarantee need not be direct and explicit to the original claim; and

(c) the ADI is satisfied that the cover of the indirect guarantee is robust and there is no historical evidence to suggest that the coverage of the indirect guarantee is not equivalent to that of a direct guarantee of the Australian Government.

5. Letters of comfort do not qualify as eligible guarantees for CRM purposes.

6. In addition to the requirements detailed in paragraph 21 of this Prudential Standard and paragraph 2 of this Attachment, in order for a guarantee to be recognised the following conditions must be satisfied:

(a) on the qualifying default/non-payment of the counterparty, the ADI has the capacity to pursue, in a timely manner, the guarantor for any monies outstanding under the documentation governing the transaction. The ADI must have the right to receive payment from the guarantor without first having to take legal action in order to pursue the counterparty for payment;

(b) the guarantee is an explicitly documented obligation assumed by the guarantor; and

(c) except as noted in this paragraph, the guarantee covers all types of payments the underlying obligor is expected to make under the documentation governing the transaction. Where a guarantee covers payment of principal only, interest and other amounts not covered by the guarantee must be treated as uncovered.

7. Where a guarantee provides for a materiality threshold on payments below which no payment will be made in the event of loss, this is equivalent to a retained first loss position and must be deducted from Common Equity Tier 1 Capital (refer to APS 111). This deduction will be capped at the amount of capital the ADI would be required to hold against the full value of the exposure.

8. Where there is partial coverage of an exposure by a guarantee and the covered and uncovered portions are of equal seniority (i.e. the ADI and the guarantor share losses on a pro rata basis), capital relief will be afforded on a proportional basis. This means that the covered portion of the exposure will receive the treatment applicable to eligible guarantees with the remainder treated as uncovered.

9. Where there is partial coverage of an exposure by a guarantee and there is a difference in seniority between the covered and uncovered portions of the exposure, then the arrangement is considered to be a synthetic securitisation and is subject to APS 120.

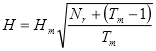

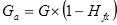

10. A currency mismatch exists where a guarantee is denominated in a different currency from that in which the exposure is denominated. In this case the amount of the exposure deemed to be protected (Ga) must be reduced by the application of a haircut (Hfx) as follows:

where:

G = nominal amount of the guarantee

Hfx = haircut appropriate for the currency mismatch between the guarantee and the underlying exposure.

11. The Hfx haircut detailed in paragraph 10 of this Attachment is the same as that applied to collateral in the comprehensive approach (refer to Attachment H). If an ADI uses the comprehensive approach and it uses the standard haircuts, the haircut to be applied for a currency mismatch will be eight per cent (assuming daily mark-to-market). If the ADI uses its own-estimate haircuts, the estimates for a currency mismatch must be based on a 10-business day holding period. Where the ADI uses the simple approach it may use the standard haircut of eight per cent for the currency mismatch (assuming daily mark-to-market) or own-estimate haircuts based on a 10-business day holding period.

12. Using the formula detailed in paragraph 40 of Attachment H, haircuts must be adjusted depending on the actual frequency of revaluation of the currency mismatch.

13. A maturity mismatch exists where the residual maturity of a guarantee is less than the maturity of the exposure covered by the guarantee.

14. Where there is a maturity mismatch, a guarantee may only be recognised for CRM purposes where the original maturity of the guarantee is greater than or equal to 12 months. Guarantees with an original maturity of less than 12 months will not be eligible unless the maturity of the guarantee matches the maturity of the underlying exposure. In all cases where there is a maturity mismatch, a guarantee will not be eligible where it has a residual maturity of three months or less.

15. Where credit protection provided by a single guarantor has different maturities, an ADI must divide the exposure into separate covered portions for risk-weighting purposes.

16. For capital adequacy purposes, an ADI must take the effective maturity of the underlying exposure to be the longest possible remaining time before the counterparty is scheduled to fulfil its obligation.

17. In the case of a guarantee, an ADI must take into account any clause within the documentation supporting the transaction that may reduce its maturity so that the shortest possible effective maturity is used. For this purpose, the ADI must consider clauses that give the guarantor the capacity to reduce the effective maturity of the guarantee and those that give the ADI, at origination of the guarantee, a discretion and positive incentive to reduce its effective maturity.

18. Where there is a maturity mismatch between a guarantee and the covered exposure, for capital adequacy purposes an ADI must apply the following adjustment:

where:

Pa = value of the guarantee adjusted for maturity mismatch

P = guarantee amount adjusted for any haircuts (in which case, P = Ga as determined in paragraph 10 of this Attachment)

t = min (T, residual maturity of the guarantee) expressed in years

T = min (5, residual maturity of the exposure) expressed in years.

- A capital requirement will be applied to an ADI on both sides of a collateralised transaction.

- An ADI must select either the simple or the comprehensive approach and apply that approach to all its on-balance sheet assets and off-balance sheet exposures on the banking book that are secured by eligible collateral.

- For trading book exposures, an ADI must use the comprehensive approach to the recognition of eligible collateral where collateral is pledged against counterparty credit risk exposure.

- An ADI must ensure that sufficient resources are devoted to the orderly operation of margin agreements with OTC derivative and securities-financing counterparties, as measured by the timeliness and accuracy of its outgoing calls and response time to incoming calls. An ADI must have collateral management policies in place to control, monitor and report:

(a) the risk to which margin agreements exposes it (such as the volatility and liquidity of the securities exchanged as collateral);

(b) the concentration risk to particular types of collateral;

(c) the re-use of collateral (both cash and non-cash) including the potential liquidity shortfalls resulting from the re-use of collateral received from counterparties; and

(d) the surrender of rights on collateral posted to counterparties.

5. Subject to the conditions set out in this Attachment, the following forms of collateral may be recognised as eligible collateral:

(a) cash collateral (cash, certificates of deposit and bank bills issued by the lending ADI) on deposit with the ADI incurring the exposure ;

(b) gold bullion;

(c) subject to paragraph 11 of this Attachment, debt securities rated by an ECAI where these debt securities have a credit rating gradeof either:

(i) four (or better) for long-term securities issued by: Commonwealth, State and Territory governments in Australia (including State and Territory central borrowing authorities); central, state and regional governments in other countries; the Reserve Bank of Australia; central banks in other countries; and the international banking agencies and multilateral regional development banks that qualify for a zero per cent risk-weight as detailed in Attachment A; or

(ii) three (or better) for short-term or long-term securities issued by ADIs, overseas banks, Australian and international local governments and corporates;

(d) subject to paragraph 11 of this Attachment, debt securities not rated by an ECAI where these securities are issued by an ADI or overseas bank as senior debt and are listed on a recognised exchange. This is subject to the condition that all rated issues of the same seniority by the issuing ADI or overseas bank have a long-term or short-term credit rating grade of at least three and the ADI holding the security has no information suggesting that the security justifies a rating below this level; and

(e) subject to paragraph 11 of this Attachment, units in a listed trust where the unit price of the trust is publicly quoted on a daily basis and the listed trust is limited to investing in the instruments detailed in paragraphs 5(a) to 5(d) of this Attachment.

6. Claims secured or collateralised in other ways (e.g. by insurance contracts, put options, forward sales contracts or agreements) are not considered to be covered by eligible collateral.

7. Re-securitisations, irrespective of credit ratings, are not eligible financial collateral.

8. There must be a formal written contractual agreement between the lender (or party holding the claim) and the party lodging the collateral which establishes the lender’s direct, explicit, irrevocable and unconditional recourse to the collateral. In the case of cash collateral, this may include a contractual right of set-off on credit balances, but a common law right of set-off is insufficient on its own to satisfy this condition.

9. The legal mechanism by which collateral is pledged or transferred must allow the ADI the right to liquidate or take legal possession of the collateral in a timely manner. The ADI must take all steps necessary to satisfy the legal requirements applicable to the ADI’s interest in the collateral. This would include clear and robust procedures for the timely liquidation of collateral to ensure that any legal conditions required for declaring the default of the counterparty and liquidating the collateral are observed and that the collateral can be liquidated promptly.

10. In the event of default, any requirement on the lender to serve notice on the party lodging the collateral must not unnecessarily impede the lender’s recourse to the collateral.