Part 1—Preliminary

1 Name

This is the Foreign Acquisitions and Takeovers Regulation 2015.

2 Commencement

(1) Each provision of this instrument specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information |

Column 1 | Column 2 | Column 3 |

Provisions | Commencement | Date/Details |

1. The whole of this instrument | The later of: (a) the start of the day after this instrument is registered; and (b) immediately after the commencement of Schedule 1 to the Foreign Acquisitions and Takeovers Legislation Amendment Act 2015. | 1 December 2015 |

Note: This table relates only to the provisions of this instrument as originally made. It will not be amended to deal with any later amendments of this instrument.

(2) Any information in column 3 of the table is not part of this instrument. Information may be inserted in this column, or information in it may be edited, in any published version of this instrument.

3 Authority

This instrument is made under the Foreign Acquisitions and Takeovers Act 1975.

4 Simplified outline of this Part

This Part defines terms that are used in this instrument.

Terms used in this instrument that are not defined in this Part may be defined in section 4 of the Act.

5 Definitions

Note: A number of expressions used in this instrument are defined in the Act, including the following:

(a) asset;

(b) Australian business;

(c) Australian land;

(d) entity;

(e) foreign person;

(f) interest;

(g) security;

(h) share.

In this instrument:

acquire an interest of a specified percentage in a business has the meaning given by section 6.

Act means the Foreign Acquisitions and Takeovers Act 1975.

ADI has the same meaning as in the Banking Act 1959.

Note: ADI is short for authorised deposit‑taking institution.

agreement country means any of the following countries:

(a) the United States of America;

(b) New Zealand;

(c) Chile;

(d) Japan;

(e) the Republic of Korea.

agreement country investor means an entity (within the ordinary meaning of the term) that is an enterprise or a national of an agreement country (other than a foreign government investor).

agribusiness: see section 12.

Note: Agribusiness is defined in section 4 of the Act.

agricultural land corporation has the meaning given by subsection 13(2).

agricultural land trust has the meaning given by subsection 13(3).

Australian and New Zealand Standard Industrial Classification Codes means the Australian and New Zealand Standard Industrial Classification Codes, as in force from time to time, published by the Australian Bureau of Statistics.

Australian land corporation has the meaning given by subsection 13(4).

Australian land trust has the meaning given by subsection 13(5).

Australian media business means an Australian business of publishing daily newspapers, or broadcasting television or radio, in Australia (including on websites from which all or part of those newspapers or broadcasts may be accessed).

class value has the meaning given by subsections 21(3) and (5).

consideration has a meaning affected by subsection 14(2).

consideration for the acquisition or issue of a class of securities has the meaning given by subsection 21(4).

direct interest in an entity or business has the meaning given by section 16.

enterprise of a country has the meaning given by section 7.

excluded provisions has the meaning given by section 28.

existing value has the meaning given by subsection 53(6).

exploration tenement means any of the following:

(a) a right (however described) under a law of the Commonwealth, a State or a Territory to recover minerals (such as coal or ore), oil or gas in Australia or from the seabed or subsoil of the offshore area for the purposes of prospecting or exploring for minerals, oil or gas;

(b) a right that preserves a right mentioned in paragraph (a);

(c) a lease under which the lessee has a right mentioned in paragraph (a) or (b);

(d) an interest in a right mentioned in paragraph (a) or (b) or under a lease mentioned in paragraph (c).

foreign government investor has the meaning given by section 17.

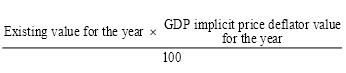

GDP implicit price deflator value has the meaning given by subsection 53(6).

general insurer has the meaning given by the Insurance Act 1973.

general partner means a partner of a limited partnership whose liability relating to the partnership is not limited.

government authority has the meaning given by subsection 44(3).

interest: a person holds an interest of a specified percentage in a business if the value of the interests in assets of the business held by the person, alone or together with one or more associates of the person, is that specified percentage of the value of the total assets of the business.

Note 1: See also the definition in this section of acquire an interest of a specified percentage in a business.

Note 2: A percentage may be specified by referring to:

(a) “20%”; or

(b) “any percentage”; or

(c) a “direct interest”; or

(d) a percentage that a person holds in other assets.

land entity means an agricultural land corporation, an agricultural land trust, an Australian land corporation or an Australian land trust.

life company has the meaning given by the Life Insurance Act 1995.

limited partner means a partner of a limited partnership whose liability relating to the partnership is limited.

limited partnership means an association of persons that:

(a) was formed solely for the purposes of becoming a partnership where the liability of at least one partner relating to the partnership is limited; and

(b) is recognised under a law of the Commonwealth, a State, a Territory, a foreign country or a part of a foreign country as such a partnership.

mining operation has the meaning given by subparagraph 44(4)(b)(ii).

mining, production or exploration entity means an entity where the total value of legal or equitable interests in tenements held by the entity, or any subsidiary of the entity, exceeds 50% of the total asset value for the entity.

moneylending agreement means:

(a) an agreement entered into in good faith, on ordinary commercial terms and in the ordinary course of carrying on a business (a moneylending business) of lending money or otherwise providing financial accommodation, except an agreement dealing with any matter unrelated to the carrying on of that business; and

(b) for a person carrying on a moneylending business, or a subsidiary or holding entity of a person carrying on a moneylending business—an agreement to acquire an interest arising from a moneylending agreement (within the meaning of paragraph (a)).

most recent financial statement has the meaning given by subsection 23(2).

national of a country has the meaning given by section 8.

public infrastructure means:

(a) an airport or airport site (within the meaning of the Airports Act 1996); or

(b) a port (within the meaning of the Maritime Transport and Offshore Facilities Security Act 2003); or

(c) infrastructure for public transport (whether or not the infrastructure is operated or owned by a Commonwealth, State or Territory body); or

(d) a system or facility that is used to provide any of the following services to the public:

(i) the generation, transmission, distribution or supply of electricity;

(ii) the supply of gas;

(iii) the storage, treatment or distribution of water;

(iv) the treatment of sewage.

public utility means a body that provides any of the following products or services, or any similar products or services, to the public:

(a) reticulated products or services, such as electricity, gas, water, sewerage or drainage;

(b) telecommunication services;

(c) transport services.

relevant agreement country investor means an entity (within the ordinary meaning of the term) that is an enterprise or national of:

(a) the United States of America; or

(b) New Zealand; or

(c) Chile;

(other than a foreign government investor).

relevant subsidiary of an entity (the higher entity) means an entity that is:

(a) a subsidiary of the higher entity; and

(b) either:

(i) for a corporation—a relevant entity that is carrying on an Australian business; or

(ii) for a unit trust—a relevant entity the trustee of which holds assets of an Australian business.

resident trust means a trust that is taken to be a resident trust estate under subsection 95(2) of the Income Tax Assessment Act 1936.

sensitive business: see section 22.

Note: Sensitive business is defined in section 26 of the Act.

starts an Australian business has the meaning given by section 10.

tenement means an exploration tenement or a mining or production tenement.

Note: Although an agreement giving rights that form the basis of a tenement may be any duration, the duration of the agreement must be at least 5 years for an interest in the agreement to be an interest in Australian land. (See the definitions of exploration tenement in this section, and mining or production tenement and interest in Australian land in sections 4 and 12 of the Act.)

total asset value has the meaning given by section 20.

total earnings has the meaning given by subsection 12(2).

vacant: land is vacant if there is no substantive permanent building on the land that can be lawfully occupied by persons, goods or livestock.

6 Meaning of acquire an interest of a specified percentage in a business

(1) A person acquires an interest of a specified percentage in a business if the person:

(a) starts to hold an interest of that percentage in the business; or

(b) would start to hold an interest of that percentage in the business on the assumption that the person held interests in assets of the business that are interests that he or she has offered to acquire; or

(c) for a person who already holds an interest of that percentage in the business:

(i) starts to hold additional interests in assets of the business; or

(ii) would start to hold additional interests in assets of the business if interests in assets of the business were transferred as the result of the exercise of rights of a kind mentioned in paragraph 15(1)(b) or (c) of the Act.

Note: A percentage may be specified by referring to:

(a) “20%”; or

(b) “any percentage”; or

(c) a “substantial interest” or a “direct interest”; or

(d) a percentage that a person holds in another entity.

(2) For the purposes of subsection (1), a reference to a person offering to acquire interests in assets of a business includes a reference to a person making or publishing a statement (however expressed) that expressly or impliedly invites a holder of interests in assets to offer to dispose of interests in assets.

7 Meaning of enterprise of a country

(1) An enterprise of a country is:

(a) an entity (within the ordinary meaning of the term) of a kind mentioned in subsections (2) to (4); or

(b) a branch of an entity (within the ordinary meaning of the term) mentioned in subsection (5);

that is not excluded under subsection (6).

(2) The entity is constituted or organised under a law of the country.

Note: For references to a law of the United States of America, see section 9.

(3) The form in which the entity may be constituted or organised may be, but is not limited to, any of the following forms:

(a) a corporation;

(b) a trust;

(c) a partnership;

(d) a sole proprietorship;

(e) a joint venture;

(f) an unincorporated association.

(4) It is immaterial whether the entity:

(a) is carried on for profit; or

(b) is owned or controlled privately.

Branches of entities

(5) A branch of an entity (within the ordinary meaning of the term) is an enterprise of a country if:

(a) the entity is not described in subsections (2) to (4); and

(b) the branch is located in the country; and

(c) the branch is carrying on business activities in the country:

(i) in a way other than being solely a representative office; and

(ii) in a way other than being engaged solely in agency activities, including the sale of goods or services that cannot reasonably be regarded as undertaken in the country; and

(iii) by having its administration in the country.

When entities are not enterprises of a country

(6) An entity, or a branch of an entity, (within the ordinary meaning of the term) is not an enterprise of a particular country if the Treasurer is satisfied that:

(a) it is owned or controlled by one or more persons of another country; and

(b) any one or more of the following applies:

(i) Australia does not maintain diplomatic relations with the other country;

(ii) Australia adopts or maintains measures relating to the other country or a person of the other country that have the effect of prohibiting transactions with the entity or branch;

(iii) the entity or branch has no substantial business activities in the particular country.

8 Meaning of national of a country

General definition

(1) A national of a country (other than the United States of America) is:

(a) an individual who is a citizen of the country; or

(b) an individual who is entitled to live indefinitely in the country.

Definition for the United States of America

(2) A national of the United States of America is:

(a) a national of the United States of America, as defined in Title III of the Immigration and Nationality Act of the United States of America; or

(b) a permanent resident of the United States of America.

Exception for New Zealand

(3) Despite subsection (1), a national of New Zealand does not include an individual who:

(a) is entitled to live in the Cook Islands, Niue or Tokelau; and

(b) does not live in New Zealand.

9 References to United States of America

In this instrument, a reference (whether or not expressly) to:

(a) the territory of the United States of America includes Puerto Rico and the District of Columbia; and

(b) a law of the United States of America includes a law that applies in a State of the United States of America or in any part of the territory of the United States of America.

10 Meaning of starts an Australian business

(1) A foreign government investor starts an Australian business if:

(a) the investor starts to carry on an Australian business; or

(b) for a foreign government investor that already carries on an Australian business—the business starts a new activity that:

(i) is not incidental to an existing activity of the Australian business; and

(ii) is within a different Division under the Australian and New Zealand Standard Industrial Classification Codes from the current activities of the Australian business.

(2) However, if a foreign government investor carries on an Australian business, the foreign government investor does not start an Australian business merely because the foreign government investor establishes a new subsidiary:

(a) that carries on the same Australian business; or

(b) for the purposes of acquiring interests in assets of the same Australian business.

Part 2—Provisions relating to definitions and rules of interpretation

11 Simplified outline of this Part

This Part prescribes various matters for the purposes of Part 1 of the Act (which deals mainly with interpretation). The main section in that Part is section 4 which lists all the terms defined for the purposes of the Act. That Part also contains some other rules of interpretation.

This Part prescribes:

(a) definitions for section 4 of the Act; and

(b) particular matters for definitions listed in that section; and

(c) some rules for interpreting the Act and this instrument, such as rules for valuing assets of entities or businesses, and for translating amounts expressed in foreign currencies.

12 When an Australian entity or Australian business is an agribusiness

(1) For the definition of agribusiness in section 4 of the Act, the following table prescribes the circumstances in which an Australian entity or Australian business is an agribusiness.

Australian entities and Australian businesses that are agribusinesses |

Item | Column 1 This kind of Australian entity or Australian business … | Column 2 is an agribusiness if … |

1 | an Australian entity | (a) any one or more of the following entities (the agribusiness entities) derive earnings from carrying on a business of the kind mentioned in subsection (3): (i) the entity; (ii) a subsidiary of the entity; and (b) the amount of those earnings before interest and tax, derived by the agribusiness entities in the most recent financial year for which the financial accounts of the entity have been audited, exceeds 25% of the amount of the total earnings for the entity. |

2 | an Australian entity | (a) any one or more of the following entities use assets in carrying on a business of the kind mentioned in subsection (3): (i) the entity; (ii) a subsidiary of the entity; and (b) the value of those assets exceeds 25% of the total asset value for the entity. |

3 | an Australian business | (a) the business uses assets in carrying on a business of the kind mentioned in subsection (3); and (b) the value of those assets exceeds 25% of the value of the total assets of the business. |

Note: See also sections 23 (value of assets of entities or businesses) and 24 (value of assets of entities that prepare consolidated financial statements).

Meaning of total earnings

(2) The total earnings for the entity is the total of all earnings before interest and tax in that year by the entity and any one or more subsidiaries of the entity.

Classes of business

(3) The business must be carried on wholly or partly in any of the following classes of the Australian and New Zealand Standard Industrial Classification Codes:

(a) any of the classes in Division A (agriculture, forestry and fishing);

(b) any of the classes in Subdivision 11 of Division C (food product manufacturing), other than any of the following:

(i) class 1113 (cured meat and smallgoods manufacturing);

(ii) class 1132 (ice cream manufacturing);

(iii) class 1162 (cereal, pasta and baking mix manufacturing);

(iv) a class in group 117 (bakery product manufacturing);

(v) class 1182 (confectionery manufacturing);

(vi) a class in group 119 (other food product manufacturing).

Mixed earnings and mixed‑use assets

(4) For the purposes of this section:

(a) earnings that are derived from carrying on a business that is not wholly in a class mentioned in subsection (3); or

(b) the value of assets that are used in carrying on a business that is not wholly in a class mentioned in subsection (3);

may be apportioned, on the basis of information available to a foreign person taking an action in relation to the business, between the part of the business that is in the class and the other parts of the business.

13 Land entities

(1) This section prescribes the meanings of the following for section 4 of the Act:

(a) agricultural land corporation;

(b) agricultural land trust;

(c) Australian land corporation;

(d) Australian land trust.

Note: Any of these corporations or trusts may be formed or established in or outside Australia.

(2) A corporation (the entity) of a kind mentioned in column 1 of the table in subsection (6) is an agricultural land corporation if the value of interests in agricultural land mentioned in column 2 of the table exceeds 50% of the value of total assets mentioned in column 3 of the table.

(3) A trust (the entity) of a kind mentioned in column 1 of the table in subsection (6) is an agricultural land trust if:

(a) the entity is a unit trust; and

(b) the value of interests in agricultural land mentioned in column 2 of the table exceeds 50% of the value of total assets mentioned in column 3 of the table.

(4) A corporation (the entity) of a kind mentioned in column 1 of the table in subsection (6) is an Australian land corporation if the value of interests in Australian land mentioned in column 2 of the table exceeds 50% of the value of total assets mentioned in column 3 of the table.

(5) A trust (the entity) of a kind mentioned in column 1 of the table in subsection (6) is an Australian land trust if:

(a) the entity is a unit trust; and

(b) the value of interests in Australian land mentioned in column 2 of the table exceeds 50% of the value of total assets mentioned in column 3 of the table.

(6) The following table sets out the interests in land and total assets taken into account for land entities.

Interests of land entities |

Item | Column 1 Entity | Column 2 Interests in land | Column 3 Total assets |

1 | An Australian entity that: (a) is a holding entity; and (b) prepares financial statements or another document in accordance with subsection 24(2) or (3) | Interests in agricultural land or Australian land (as the case requires) set out in the financial statements | Total assets set out in the financial statements or other document |

2 | Any other entity | Interests in agricultural land or Australian land (as the case requires) held by the entity or a trustee of the entity | Total assets of the entity or the trustee of the entity |

14 Meaning of consideration

(1) This section prescribes the meaning of consideration for section 4 of the Act.

(2) The consideration for an acquisition of an interest in securities, assets, Australian land or a tenement, or for an issue of securities in an entity, includes the following:

(a) consideration in any form;

(b) any GST (within the meaning of the A New Tax System (Goods and Services Tax) Act 1999), or equivalent tax under a law of a foreign country or a part of a foreign country, that is payable in relation to the acquisition or issue;

(c) any consideration that is contingent on the occurrence or non‑occurrence of a particular event.

Assessing the value of consideration

(3) The value of the consideration for an acquisition of an interest in securities, assets, Australian land or a tenement, or for an issue of securities in an entity, is:

(a) if there is an agreement relating to the acquisition or issue and the parties to the agreement are not dealing at arm’s length, or if there is no agreement that sets out the value of the consideration—a reasonable assessment of the value of the consideration for the acquisition or issue; or

(b) otherwise—the value of the consideration set out in the agreement relating to the acquisition or issue.

(4) Without limiting paragraph (3)(a), an assessment of consideration is reasonable on a particular day if it is worked out on the basis of:

(a) for an acquisition of an interest in securities, assets, Australian land or a tenement that has a publicly available price—a price that was publicly available no more than 7 days earlier; and

(b) for an acquisition of an interest in securities made under a takeover bid (whether under the Corporations Act 2001 or a law of a foreign country or part of a foreign country)—the first amount specified for the interest in the bidder’s statement (within the meaning of the Corporations Act 2001) or any equivalent document under a law of a foreign country or part of a foreign country.

Consideration for acquisition of interests in securities of foreign entities

(5) The consideration for the acquisition of an interest in securities in a foreign entity may be apportioned between the relevant Australian business or Australian entity and any other business or entity on the basis of the earnings before interest and tax of the Australian business or Australian entity and the other business or entity.

15 Number of independent self‑contained dwellings in a development

For paragraph (c) of the definition of development in section 4 of the Act, the number of independent self‑contained dwellings is 50.

16 Meaning of direct interest in an entity or business

For the definition of direct interest in section 4 of the Act, a direct interest in an entity or business is:

(a) an interest of at least 10% in the entity or business; or

(b) an interest of at least 5% in the entity or business if the person who acquires the interest has entered a legal arrangement relating to the businesses of the person and the entity or business; or

(c) an interest of any percentage in the entity or business if the person who acquired the interest is in a position:

(i) to influence or participate in the central management and control of the entity or business; or

(ii) to influence, participate in or determine the policy of the entity or business.

Note: Section 17 of the Act defines interest of a specified percentage in an entity. Section 5 of this instrument defines interest of a specified percentage in a business.

17 Meaning of foreign government investor

For the definition of foreign government investor in section 4 of the Act, a person is a foreign government investor if the person is:

(a) a foreign government or separate government entity; or

(b) a corporation in which:

(i) a foreign government or separate government entity, alone or together with one or more associates, holds a substantial interest; or

(ii) foreign governments or separate government entities of more than one foreign country (or parts of more than one foreign country), together with any one or more associates, hold an aggregate substantial interest; or

(c) the trustee of a trust in which:

(i) a foreign government or separate government entity, alone or together with one or more associates, holds a substantial interest; or

(ii) foreign governments or separate government entities of more than one foreign country (or parts of more than one foreign country), together with any one or more associates, hold an aggregate substantial interest; or

(d) the general partner of a limited partnership in which:

(i) a foreign government or separate government entity, alone or together with one or more associates, holds an interest of at least 20%; or

(ii) foreign governments or separate government entities of more than one foreign country (or parts of more than one foreign country), together with any one or more associates, hold an aggregate interest of at least 40%; or

(e) a corporation, trustee or partner of a kind described in paragraph (b), (c) or (d) assuming the references to foreign government (or foreign governments) in those paragraphs included references to a foreign government investor (or foreign government investors):

(i) within the meaning of those paragraphs; or

(ii) as a result of a previous application of this paragraph.

18 Meaning of foreign person

General partners of limited partnerships

(1) For paragraph (g) of the definition of foreign person in section 4 of the Act, a person is a foreign person if:

(a) the person is a general partner of a limited partnership; and

(b) either:

(i) an individual not ordinarily resident in Australia, a foreign corporation or a foreign government holds an interest of at least 20% in the limited partnership; or

(ii) 2 or more persons, each of whom is an individual not ordinarily resident in Australia, a foreign corporation or a foreign government hold an aggregate interest of at least 40% in the limited partnership.

Certain foreign government investors

(2) For paragraph (g) of the definition of foreign person in section 4 of the Act, a person is a foreign person if:

(a) the person is a foreign government investor; and

(b) apart from this subsection, the person would not be a foreign person.

19 Number of future dwellings on residential land

For subparagraph (a)(ii) of the definition of residential land in section 4 of the Act, the number of dwellings is 10.

20 Meaning of total asset value

(1) This section prescribes the meaning of total asset value for an entity for section 4 of the Act.

Entities that are not holding entities

(2) The total asset value for an entity that is not a holding entity is the value of the assets mentioned in subsection (5) of the entity.

Note: See also section 23 (value of assets of entities or businesses).

Holding entities

(3) The total asset value for a holding entity that does not prepare financial statements or another document in accordance with subsection 24(2) or (3) is the aggregate value of the assets, mentioned in subsection (5) of this section, of:

(a) the entity; and

(b) each relevant subsidiary of the entity (disregarding any securities in those subsidiaries of the holding entity).

Note 1: See subsections (6) and (7) for valuing stapled securities and the assets of entities operating on a unified basis.

Note 2: See also section 23 (value of assets of entities or businesses).

(4) The total asset value for a holding entity that prepares financial statements or another document in accordance with subsection 24(2) or (3) is the aggregate value of the total assets, mentioned in subsection (5) of this section, set out in the financial statements or other document.

Note: See also section 23 (value of assets of entities or businesses).

Assets of entities that are taken into account

(5) The assets of an entity that are taken into account for the purposes of this section are:

(a) for an Australian entity—the total assets of the entity; and

(b) for a foreign entity—the total relevant Australian assets, and any other assets in Australia, of the entity.

Note: For the definition of relevant Australian assets, see section 4 of the Act.

Entities whose securities are stapled

(6) If any of the securities in an entity (the first entity) whose assets are valued under this section can only be transferred together with securities in one or more other entities whose assets would not (apart from this subsection) be valued under this section, the value of the assets of the first entity is taken to include the value of the assets mentioned in subsection (5) of the other entities.

Entities operating on a unified basis

(7) If:

(a) an entity (the first entity) whose assets are valued under this section has entered an arrangement with one or more other entities resulting in the entities being under a legal obligation to operate on a unified basis; and

(b) the value of the assets of the other entities would not (apart from this subsection) be valued under this section;

the value of the assets of the first entity is taken to include the value of the assets mentioned in subsection (5) of the other entities.

21 Meaning of total issued securities value

(1) This section prescribes the meaning of total issued securities value for an entity for section 4 of the Act.

(2) The total issued securities value for an entity is the total of the class values worked out under subsection (3) or (5) for each class of securities in the entity.

Meaning of class value

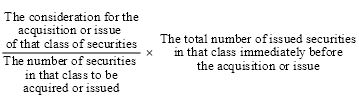

(3) The class value for a class of securities in an entity is worked out using the following formula if securities in that class are being acquired or issued:

(4) The consideration for the acquisition or issue of a class of securities is:

(a) for an acquisition of interests in securities—the total consideration for the acquisition of securities in that class; or

(b) for an issue of securities—the total issue price of all the securities in that class to be issued.

Note: Consideration is defined in section 14. The consideration for the acquisition of an interest in securities in a foreign entity may be apportioned in certain cases (see subsection 14(5)).

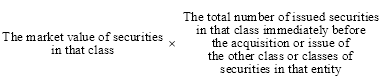

(5) The class value for a class of securities in an entity is worked out using the following formula if securities in that class are not being acquired or issued:

22 Businesses that are sensitive businesses

(1) This section prescribes conditions for subsection 26(1) of the Act.

(2) A business is a sensitive business if:

(a) the business is carried on wholly or partly in any of the following sectors (including such a business relating to infrastructure for those sectors):

(i) media;

(ii) telecommunications;

(iii) transport; or

(b) the business is wholly or partly:

(i) the supply of training or human resources to, the manufacture of military goods, equipment or technology for, or the supply of military goods, equipment or technology to, the Australian Defence Force or other defence forces; or

(ii) the manufacture or supply of goods, equipment or technology able to be used for a military purpose; or

(iii) the development, manufacture or supply of, or the provision of services relating to, encryption and security technologies and communications systems; or

(iv) the extraction of (or the holding of rights to extract) uranium or plutonium or the operation of a nuclear facility.

23 Value of assets of entities or businesses

(1) For section 27 of the Act, the value on a particular day of an asset of an entity or business is (subject to subsections (3) and (4) of this section) the following value:

(a) if there is a most recent financial statement and an event affecting the value of the asset as shown in that financial statement has not occurred since the financial statement was most recently audited or reviewed—the value of the asset as shown in the financial statement;

(b) otherwise—the value of the asset as shown on that day in the accounting records of the entity or business.

(2) The most recent financial statement, in relation to a day, is the financial statement of the entity or business that was most recently audited or reviewed by an auditor before that day.

(3) Subsection (1) does not apply if the value shown is not a reasonable value.

(4) This section does not limit how the value of an asset of an entity or business may be determined.

24 Value of assets of entities that prepare consolidated financial statements

(1) This section applies in relation to an entity that prepares consolidated financial statements.

(2) If the entity’s consolidated financial statements are prepared in accordance with the international financial reporting standards, the value of the assets of the entity is the value set out in those statements.

(3) If an entity produces financial statements or another document (each of which is the reconciliation document) for the purpose of reconciling the value of the assets of the entity set out in the entity’s consolidated financial statements with the value produced using the method, set out in the international financial reporting standards, for valuing assets for consolidated financial statements, the value of the assets of the entity is the value set out in the reconciliation document.

25 Foreign currencies

(1) For section 27 of the Act, this section applies if:

(a) the Act requires the determination of a value (however described) of a thing; and

(b) either:

(i) that value has been expressed in an agreement or other document only in a currency that is not Australian dollars; or

(ii) a notice is given for the purposes of the Act in relation to an acquisition of an interest or an issue of securities in an entity and there is no agreement relating to the acquisition or issue.

Note: Examples of a thing whose value is required by the Act to be determined include assets (and interests in assets) and consideration.

(2) The value of the thing is the value expressed in Australian dollars, worked out using the following exchange rate for the end of the day covered by subsection (3):

(a) if the Reserve Bank of Australia publishes a daily exchange rate for the currency—that exchange rate;

(b) otherwise—any exchange rate:

(i) that is publicly or commercially available; and

(ii) that it is reasonable to use.

(3) The day covered by this subsection is:

(a) either:

(i) for subparagraph (1)(b)(i)—the day the agreement is entered into or the document is made; or

(ii) for subparagraph (1)(b)(ii)—any of the 7 days before the notice is given; or

(b) if there is no exchange rate published or made publicly available on that day or any of those days—the day before that day or the earliest of those days (as the case requires) on which the exchange rate was most recently published or made publicly available.

Part 3—Exemptions

Division 1—Simplified outline of this Part

26 Simplified outline of this Part

This Part prescribes matters for sections 37 (regulations providing for exemptions) and 63 (exemption certificates provided for by the regulations) of the Act.

Division 2 exempts certain interests that relate to moneylending agreements entirely from the operation of the Act.

Division 3 exempts the acquisition of certain interests from being significant actions or notifiable actions. Those interests are, however, taken into account in determining whether a person is a foreign person for the purposes of the Act.

Division 4 provides exemptions relating to particular significant actions or notifiable actions. The Division also deals with the effect of exemption certificates prescribed by this instrument.

Division 5 contains exemptions from various provisions for certain other limited purposes.

Division 2—Exemptions applying for all purposes

27 Moneylending agreements

(1) The Act does not (subject to subsections (2) and (3)) apply in relation to an interest in securities, assets, a trust, Australian land or a tenement if:

(a) the interest is:

(i) held solely by way of security for the purposes of a moneylending agreement; or

(ii) acquired by way of enforcement of a security held solely for the purposes of a moneylending agreement; and

(b) the entity that holds or acquires the interest is:

(i) the entity (the first entity) that entered the moneylending agreement; or

(ii) a subsidiary or holding entity of the first entity; or

(iii) a person who is (alone or with others) in a position to determine the investments or policy of the first entity; or

(iv) a security trustee who holds or acquires the interest on behalf of the first entity; or

(v) a receiver, or a receiver and manager, appointed in relation to a person or entity mentioned in any of subparagraphs (i) to (iv).

Interests relating to residential land

(2) For an interest in residential land where the first entity is not a foreign government investor, the Act does not apply in relation to the interest only if:

(a) an entity (the key entity) that is:

(i) the first entity; or

(ii) a holding entity of the first entity;

is an ADI, or otherwise licensed (whether or not in Australia) as a financial institution; and

(b) if the key entity is not an ADI:

(i) there are at least 100 holders of securities in the key entity; or

(ii) the key entity is listed for quotation in the official list of a stock exchange (whether or not in Australia).

Interests acquired by foreign government investors

(3) For an interest acquired by a foreign government investor by way of enforcement of a security as mentioned in subparagraph (1)(a)(ii), the Act does not apply in relation to the interest only if:

(a) for a foreign government investor that is an ADI or a subsidiary of an ADI:

(i) 12 months have not passed since the acquisition of the interest; or

(ii) at least 12 months have passed since the acquisition of the interest and the foreign government investor is making a genuine attempt to dispose of the interest; or

(b) otherwise:

(i) 6 months have not passed since the acquisition of the interest; or

(ii) at least 6 months have passed since the acquisition of the interest and the foreign government investor is making a genuine attempt to dispose of the interest.

Note 1: Examples of the kinds of actions that may constitute a genuine attempt to dispose of an interest include deciding on the method of disposal, and complying with any requirements of a law that apply before the interest can be disposed of.

Note 2: The effect of this section is that:

(a) acquisitions of interests mentioned in this section are not significant actions or notifiable actions; and

(b) such interests are to be disregarded for other purposes, such as in determining whether a person holds a substantial interest in an entity or is a subsidiary of another entity.

Division 3—Exemptions for certain actions from being significant and notifiable actions

Subdivision A—Application of this Division

28 Application of this Division

This Division applies to the provisions of the Act, other than:

(a) the definition of foreign person in section 4 of the Act; and

(b) any other provision of the Act to the extent that it relates to that definition.

The provisions of the Act that this Division applies to are the excluded provisions.

Note: The effect of this Division is that acquisitions of interests of a kind mentioned in this Division are not significant actions or notifiable actions, but are taken into account for the purposes of the definition of foreign person in section 4 of the Act.

Subdivision B—General exemptions

29 Will or devolution

The excluded provisions do not apply in relation to an acquisition of an interest in securities, assets, a trust or Australian land that is acquired by will or devolution by operation of law, other than as a result of an arrangement under Part 5.1 or 5.3A of the Corporations Act 2001.

30 Certain interests held by foreign custodian corporations

The excluded provisions do not apply in relation to an acquisition of an interest in securities, assets, a trust, Australian land or a tenement by a foreign person if:

(a) the foreign person is a corporation that is in the business of providing custodian services to other persons in relation to the holding of interests in securities, assets, trusts, Australian land or tenements; and

(b) the foreign person acquires the interest in the course of the foreign person’s business of providing such services; and

(c) the interest is a legal interest; and

(d) the equitable interest in the securities, assets, trust, land or tenement is not held by the foreign person; and

(e) the foreign person exercises voting rights associated with the interest only at, or in accordance with, the direction of:

(i) another person that is providing custodian services to a person in relation to the holding of the legal interest in the securities, assets, trust, land or tenement; or

(ii) the holder of an equitable interest in the securities, assets, trust, land or tenement that is receiving custodian services that are related to that interest.

31 Australian businesses carried on by or land acquired from government

(1) The excluded provisions do not (subject to subsection (2)) apply in relation to an Australian business that is carried on (whether alone or together with one or more other persons) by, or an acquisition of an interest in Australian land from, any of the following persons:

(a) the Commonwealth, a State, a Territory or a local governing body;

(b) an entity wholly owned by the Commonwealth, a State, a Territory or a local governing body.

(2) However, this section does not apply in relation to an acquisition of an interest by a foreign government investor.

Subdivision C—Significant and notifiable actions relating to entities

32 Investments in financial sector companies

(1) The excluded provisions do not (subject to subsection (2)) apply in relation to an acquisition of an interest in shares if the shares are in a financial sector company (within the meaning of the Financial Sector (Shareholdings) Act 1998).

(2) This section does not apply in relation to an acquisition of an interest by a foreign government investor.

33 Compulsory acquisitions and compulsory buy‑outs

The excluded provisions do not apply in relation to an acquisition of an interest in securities if the securities are acquired under a compulsory acquisition or compulsory buy‑out.

34 Convertible instruments that include a requirement for loss absorption if entity becomes non‑viable

The excluded provisions do not apply in relation to an acquisition of an interest in securities if:

(a) the securities are Additional Tier 1 Capital or Tier 2 Capital instruments (within the meaning of the Prudential Standard APS 111—Capital Adequacy: Measurement of Capital, as in force at the time this section commences); and

(b) the securities have not been converted into ordinary shares.

Note: The Prudential Standard APS 111—Capital Adequacy: Measurement of Capital is made under subsection 11AF(1) of the Banking Act 1959.

Subdivision D—Significant and notifiable actions relating to Australian land etc.

35 Acquisitions by persons with a close connection to Australia

Acquisitions of any land by persons with a close connection to Australia

(1) The excluded provisions do not apply in relation to an acquisition of an interest in Australian land by any of the following persons:

(a) an Australian citizen not ordinarily resident in Australia;

(b) a foreign person that is an Australian corporation and would not be a foreign person if interests held directly in it by any one or more of the following persons were disregarded:

(i) a person to whom either of paragraphs (a) and (c) applies;

(ii) a person covered by a previous application of this paragraph;

(c) a foreign person that is the trustee of a resident trust at the time of the acquisition and would not be a foreign person if interests held directly in it by any one or more of the following persons were disregarded:

(i) a person to whom either of paragraphs (a) and (b) applies;

(ii) a person covered by a previous application of this paragraph;

(d) a charity operating in Australia primarily for the benefit of persons ordinarily resident in Australia.

Note: Charity is defined in the Charities Act 2013.

Acquisitions of interests in agricultural land by spouses and de facto partners of Australian citizens

(2) The excluded provisions do not apply in relation to an acquisition of an interest in agricultural land by a foreign person if both of the following apply:

(a) the person is the spouse or de facto partner (within the meaning of the Acts Interpretation Act 1901) of an Australian citizen;

(b) the interest is held by the person and his or her spouse or partner as joint tenants.

Note: A similar exemption applies in relation to residential land (see subsection 38(3)).

36 Acquisitions by funds and schemes

The excluded provisions do not apply in relation to an acquisition of:

(a) an interest in Australian land; or

(b) an interest in a tenement; or

(c) an interest in securities in a mining, production or exploration entity;

by any of the foreign persons mentioned in column 1 of the following table in the circumstances mentioned in column 2 of the table.

Acquisitions by funds and schemes |

Item | Column 1 Foreign person | Column 2 Circumstances |

1 | A life company operating in Australia or a subsidiary of such a life company | The acquisition is made by way of investment of its statutory funds (within the meaning of the Life Insurance Act 1995) primarily for the benefit of owners of policies who are ordinarily resident in Australia |

2 | A body corporate that is: (a) a general insurer (other than a life company) operating in Australia; or (b) a subsidiary of such a general insurer | The acquisition: (a) is made from the reserves of the body corporate; and (b) is consistent with the body corporate’s obligations under the Insurance Act 1973 |

3 | An Australian business that maintains a superannuation fund for its employees (within the meaning of the Superannuation Industry (Supervision) Act 1993) primarily for the benefit of the members of the fund, or their dependants, who are ordinarily resident in Australia | The acquisition is made as an investment of all or part of the assets of that fund |

4 | A responsible entity of a managed investment scheme registered under section 601EB of the Corporations Act 2001 | The acquisition is primarily for the benefit of scheme members ordinarily resident in Australia |

37 Acquisition in certain circumstances

(1) The excluded provisions do not apply in relation to an acquisition of an interest in Australian land by a foreign person if a subsection of this section applies in relation to the acquisition.

Securities in listed Australian land entities and stapled securities

(2) All of the following apply:

(a) the acquisition is of an interest in Australian land that is an acquisition of an interest in shares or units in a land entity;

(b) the land entity is or will be listed for quotation in the official list of a stock exchange (whether or not in Australia);

(c) after the acquisition, the foreign person, alone or together with one or more associates, holds an interest of less than 10% in the land entity;

(d) the foreign person is not in a position:

(i) to influence or participate in the central management and control of the land entity; or

(ii) to influence, participate in or determine the policy of the land entity.

(3) All of the following apply:

(a) the acquisition is of an interest in Australian land that is an acquisition of an interest in shares or units in a land entity;

(b) the interest in the shares or units can only be transferred together with interests in one or more securities in another entity;

(c) the interest in the securities in the other entity is covered by subsection (2).

Securities in unlisted Australian land entities

(4) All of the following apply:

(a) the acquisition is of an interest in Australian land that is an acquisition of an interest in shares or units in a land entity;

(b) the land entity is not, and will not be, listed for quotation in the official list of a stock exchange (whether or not in Australia);

(c) after the acquisition, the foreign person, alone or together with one or more associates, holds an interest of less than 5% in the land entity;

(d) the foreign person is not in a position:

(i) to influence or participate in the central management and control of the land entity; or

(ii) to influence, participate in or determine the policy of the land entity;

(e) there are or will be at least 100 holders of securities in the land entity;

(f) the land entity carries on a business that does not include (other than incidentally) investing directly or indirectly in established dwellings.

Acquisitions for diplomatic or consular purposes

(5) Both of the following apply:

(a) the foreign person is:

(i) a foreign government or a separate government entity; or

(ii) an entity (within the ordinary meaning of the term) in which a foreign government holds a substantial interest;

(b) the acquisition is of an interest in commercial land or residential land to be used exclusively as any of the following:

(i) a diplomatic mission or consular post;

(ii) a diplomatic residence or the residence of the head of a consular post.

38 Acquisitions of interests in residential land

(1) The excluded provisions do not apply in relation to an acquisition of an interest in residential land by a foreign person if a subsection of this section applies in relation to the acquisition.

Acquisitions by persons with connection to Australia

(2) The foreign person meets any of the following conditions:

(a) the foreign person is, at the time of acquisition, the holder of a permanent visa (within the meaning of the Migration Act 1958);

(b) the foreign person is, at the time of acquisition, the holder of a special category visa (within the meaning of that Act);

(c) if the foreign person had entered Australia lawfully immediately before the acquisition, he or she would have been entitled to the grant, on presentation of a passport, of a special category visa (within the meaning of that Act);

(d) the foreign person is an Australian corporation and would not be a foreign person if interests held directly in it by any one or more of the following persons were disregarded:

(i) a person to whom any of paragraphs (a), (b), (c) and (e) applies;

(ii) a person to whom any of paragraphs 35(1)(a) to (c) applies;

(iii) a person covered by a previous application of this paragraph;

(e) the foreign person is the trustee of a resident trust at the time of the acquisition, and would not be a foreign person if interests held directly in it by any one or more of the following persons were disregarded:

(i) a person to whom any of paragraphs (a) to (d) of this subsection applies;

(ii) a person to whom any of paragraphs 35(1)(a) to (c) applies;

(iii) a person covered by a previous application of this paragraph.

Acquisitions of interests in residential land by spouses and de facto partners of Australian citizens etc.

(3) Both of the following apply:

(a) the person is the spouse or de facto partner (within the meaning of the Acts Interpretation Act 1901) of:

(i) a person who is, at the time of acquisition, an Australian citizen; or

(ii) a person who is, at the time of acquisition, the holder of a permanent visa (within the meaning of the Migration Act 1958); or

(iii) a person who is, at the time of acquisition, the holder of a special category visa (within the meaning of that Act); or

(iv) a person who, if the person had entered Australia lawfully immediately before the acquisition, would have been entitled to the grant, on presentation of a passport, of a special category visa (within the meaning of that Act);

(b) the interest is held by the person and his or her spouse or partner as joint tenants.

Acquisitions of interests in residential timeshare schemes

(4) Both of the following apply:

(a) the acquisition is of an interest in a timeshare scheme that relates to residential land;

(b) the foreign person’s total entitlement, alone or together with one or more associates, under the timeshare scheme to access the land is no more than 4 weeks in any year.

39 Acquisitions of certain easements

The excluded provisions do not apply in relation to an acquisition of a legal or equitable interest in an easement if:

(a) the following conditions are met:

(i) the interest is acquired by a foreign person other than a foreign government investor;

(ii) the easement is not an easement in gross; or

(b) the following conditions are met:

(i) the easement is an easement in gross;

(ii) the easement is created for the purposes of a public utility providing products or services to the public;

(iii) the public utility that acquires the interest is authorised by or under a law of the Commonwealth, a State or a Territory to provide those products or services.

Division 4—Other exemptions relating to significant and notifiable actions

Subdivision A—Exemptions relating to particular significant and notifiable actions

40 Action relating to agribusinesses and agricultural land for certain investors

Relevant agreement country investors—exemption in relation to agribusinesses

(1) Paragraphs 40(2)(a) and 41(2)(a) (significant action in relation to agribusinesses) of the Act, and any other provision of the Act to the extent that it relates to those paragraphs, do not apply in relation to relevant agreement country investors.

Thresholds for agricultural land acquired by certain investors

(2) A relevant agreement country investor, or an enterprise or national of Singapore or Thailand (other than a foreign government investor), who takes an action relating to an interest in agricultural land may, for the purposes of subsections 52(2) and (3) of the Act, disregard the fact that the land is agricultural land.

Note 1: The effect of this subsection is that the threshold test in, and the thresholds prescribed for the purposes of, subsection 52(3) (and not subsection 52(2)) of the Act apply in relation to the land.

Note 2: Agricultural land that is not used wholly and exclusively for a primary production business may also be residential land or commercial land.

Land entities

(3) A relevant agreement country investor, or an enterprise or national of Singapore or Thailand (other than a foreign government investor), who takes an action relating to an interest in agricultural land that is used wholly and exclusively for a primary production business may, for the purposes of section 13 of this instrument, disregard the fact that the land is agricultural land.

Note: The effect of this subsection is that such land is disregarded entirely in working out whether an entity is a land entity for the purposes of that section.

(4) To avoid doubt, an action taken in relation to an interest in agricultural land that is used wholly and exclusively for a primary production business includes an action taken by acquiring a security in a land entity that holds agricultural land that is used wholly and exclusively for a primary production business.

41 Exemptions for certain acquisitions

(1) This section applies for the following provisions:

(a) Division 3 of Part 2 of the Act (meaning of notifiable action);

(b) Part 4 of the Act (notice of notifiable actions and significant actions);

(c) any other provision of the Act to the extent that it relates to either of those provisions.

(2) The provisions specified in subsection (1) of this section do not apply in relation to an acquisition of an interest in securities in an entity (including securities in a land entity) if:

(a) both of the following apply:

(i) the acquisition is under a rights issue;

(ii) the interest has not been previously offered for issue under the rights issue; or

(b) all of the following apply:

(i) the entity is listed for quotation in the official list of a stock exchange in Australia;

(ii) that listing is the entity’s primary listing in an official list of a stock exchange;

(iii) the acquisition is under a dividend reinvestment plan, a bonus share plan, a distribution reinvestment plan or a switching facility.

Subdivision B—Exemption certificates

42 Exemption certificates for underwriters

(1) A foreign person may apply for a certificate under this section if:

(a) the foreign person has a business of underwriting securities; and

(b) the foreign person or any other foreign person proposes to acquire kinds of interests in securities (including securities of land entities); and

(c) that person proposes to acquire the interests for the purposes of, or in the course of, the foreign person’s business of underwriting securities.

Note 1: An acquisition of an interest in securities of a kind specified in the certificate by the foreign person specified in the certificate is generally not a significant action or a notifiable action (see section 58).

Note 2: See also Part 6 (fees) and section 135 (manner of notification and application) of the Act.

Note 3: Underwrite includes sub‑underwrite (see section 9 of the Corporations Act 2001).

(2) The Treasurer may give a certificate if the Treasurer is satisfied that acquisitions of those kinds of interests by that foreign person are not contrary to the national interest.

(3) The certificate must specify:

(a) the person (who may not yet be incorporated or established) to whom the certificate relates; and

(b) the kinds of interests in securities to which the certificate relates.

Note: For other things that the certificate may specify, see section 60 of the Act.

43 Exemption certificates for certain interests in tenements and mining, production or exploration entities

(1) A foreign person may apply for a certificate under this section if the foreign person or any other foreign person proposes to acquire:

(a) either:

(i) one or more kinds of interests in a tenement; or

(ii) one or more kinds of interests in securities in a mining, production or exploration entity; and

(b) those kinds of interests are not interests in Australian land.

Note: See also Part 6 (fees) and section 135 (manner of notification and application) of the Act.

(2) The Treasurer may give a certificate if the Treasurer is satisfied that acquisitions of those kinds of interests by that foreign person is not contrary to the national interest.

(3) The certificate must specify:

(a) the person (who may not yet be incorporated or established) to whom the certificate relates; and

(b) the kinds of interests to which the certificate relates.

Note: For other things that the certificate may specify, see section 60 of the Act.

Division 5—Exemptions from other specified provisions

44 Meaning of agricultural land

(1) The kind of land that is not agricultural land at a particular time is land:

(a) in relation to which one or more conditions in this section are met at that time; and

(b) that, subject to subsection (2), is not being used wholly or predominantly at that time for a primary production business.

(2) Paragraph (1)(b) does not apply in relation to land that meets the condition in subsection (13).

Land whose zoning requires approval for primary production businesses

(3) The zoning of the land requires any of the following (a government authority) to approve the use of the land for any primary production business:

(a) the Commonwealth, a State or a Territory;

(b) a Commonwealth, State or Territory body;

(c) a local governing body.

Note: Land is agricultural land if the zoning of the land allows use for one kind of primary production business without approval, but requires approval for another kind of primary production business.

(4) The land meets the following conditions:

(a) the zoning of the land allows use for a primary production business;

(b) an application has been made to a government authority for:

(i) the land to be rezoned as land whose zoning does not allow use for a primary production business; or

(ii) approval for a mine, oil or gas well, quarry, or other similar operation under a mining or production tenement, (a mining operation) to be established on the land; or

(iii) approval to locate infrastructure relating to a mining operation on the land; or

(iv) approval for waste from a mining operation to be stored on the land;

(c) the application is yet to be finally determined and has not been withdrawn or otherwise disposed of.

Note: Examples of infrastructure relating to a mining operation include infrastructure for processing the material extracted by the operation and accommodation for miners.

Land used in relation to mining operations

(5) The land is used wholly or predominantly:

(a) for a mining operation; or

(b) to locate infrastructure relating to a mining operation; or

(c) to store waste from a mining operation.

(6) An approval (that is not a mining or production tenement) of a government authority is in force allowing the following:

(a) a mining operation to be established or operated on the land;

(b) infrastructure relating to a mining operation to be located on the land;

(c) waste from a mining operation to be stored on the land.

(7) The land was acquired solely, or is used wholly or predominantly, to meet a condition of an approval mentioned in subsection (6) that relates to other land.

Land used for protecting or conserving the environment

(8) The land is used, under a law of the Commonwealth, a State or a Territory or a legally binding agreement, wholly or predominantly for the purposes of the protection or conservation of the environment.

(9) The land is used wholly or predominantly for the purposes of a wildlife sanctuary or for rehabilitating animals.

Land within industrial estates

(10) The land is located within an area that has been approved by a government authority as an industrial estate.

Small areas of land

(11) The area of the land is 1 hectare or less.

Tourism, education and outdoor recreation facilities

(12) The use of the land has been approved by a government authority for providing facilities for tourism, outdoor education or outdoor recreation to the public.

Primary production businesses relating to submerged plants and animals etc.

(13) The only primary production business that the land is or could reasonably be used for is:

(a) a business mentioned in paragraph (d) or (e) of the definition of primary production business in subsection 995‑1(1) of the Income Tax Assessment Act 1997; or

(b) a business of cultivating or propagating under water (whether or not all of the time) plants, fungi or their products or parts; or

(c) a business of maintaining animals under water (whether or not all of the time) for the purpose of selling them or their bodily produce.

Note: Paragraph (13)(a) covers the businesses of conducting operations relating directly to taking or catching fish or culturing pearls or other aquatic life.

45 Meaning of associate—exemptions

Consortiums

(1) Paragraph 6(1)(b) of the Act does not apply to a person (the first person) to the extent that:

(a) the first person holds an interest in a body established for the purposes of a consortium with one or more other persons (the consortium partners); and

(b) the first person, and its associates, do not hold a substantial interest or an aggregate substantial interest in the body; and

(c) none of the consortium partners that are foreign persons, and their associates, hold a substantial interest or an aggregate substantial interest in the body.

Note: Under paragraph 6(1)(b) of the Act, 2 persons who act in concert are associates. The effect of this subsection is that partners in a consortium are not associates if none of the partners, or their associates, that are foreign persons hold a substantial interest or an aggregate substantial interest in the body established for the purposes of the consortium.

(2) Subsection (1) is to be disregarded in determining whether a person is an associate for the purposes of paragraphs (1)(b) and (c).

Limited partners

(3) Paragraph 6(1)(c) of the Act does not apply to a person (the first person) to the extent that:

(a) the first person is a limited partner of a limited partnership; and

(b) another person would (apart from this subsection) be an associate of the first person under that paragraph because the other person is also a limited partner or general partner of the partnership; and

(c) the first person (whether alone, or together with one or more associates) is not in a position to participate in the management and control of the partnership, or of any of the general partners of the partnership, in relation to any matter.

Note: Under paragraph 6(1)(c) of the Act, 2 persons who carry on a business in partnership are associates. The effect of this subsection is that the limited partners or general partners of the limited partnership are not associates of the first person.

(4) Subsection (3) is to be disregarded in determining whether a person is an associate for the purposes of paragraph (3)(c).

Foreign government investors

(5) Paragraph 6(1)(l) of the Act does not apply to a foreign government investor mentioned in:

(a) subparagraph (b)(ii), (c)(ii) or (d)(ii) of the definition of foreign government investor in section 17 of this instrument; or

(b) paragraph (e) of that definition to the extent that it relates to any of those subparagraphs.

46 Meaning of foreign person—potential voting power and future rights

(1) This section applies for paragraphs (b), (c), (d) and (e) of the definition of foreign person in section 4 of the Act, to the extent that that definition applies for the purposes of the following:

(a) item 8 of the table in subsection 67(2) of the Act (orders prohibiting proposed significant action);

(b) item 3 of the table in subsection 67(3) of the Act (additional orders);

(c) item 7 of the table in subsection 69(2) of the Act (disposal orders);

(d) Part 4 of the Act (notice of notifiable actions and significant actions).

Note 1: Paragraphs (b), (c), (d) and (e) of the definition of foreign person cover corporations and trustees of trusts in which foreign persons hold substantial interests or aggregate substantial interests.

Note 2: The items mentioned in paragraphs (a) to (c) of this subsection relate to acquisitions of interests in Australian land.

(2) The provisions specified in subsection (1) of this section do not apply in relation to an interest in a security that a person holds that is part of a substantial interest or an aggregate substantial interest in an entity because:

(a) the person is in a position to control a specified percentage of the potential voting power of the entity; or

(b) the person would hold at least a specified percentage of the issued securities in the entity if securities in the entity were issued as a result of the exercise of some or all rights of a kind mentioned in paragraph 15(1)(b) or (c) of the Act.

47 Meaning of foreign person—disregarding small holdings of securities in primary listed entities

(1) Paragraphs (c) and (e) of the definition of foreign person in section 4 of the Act do not apply in relation to an interest in securities in an entity if:

(a) the entity is listed for quotation in the official list of a stock exchange in Australia; and

(b) that listing is the entity’s primary listing in an official list of a stock exchange; and

(c) the interest, together with any interests held by any associates of the person, is not a substantial holding (within the meaning of the Corporations Act 2001).

Note 1: Paragraphs (c) and (e) of the definition of foreign person cover corporations and trustees of trusts in which foreign persons hold aggregate substantial interests.

Note 2: The interests that are taken into account in working out whether a person has a substantial holding may be modified by ASIC under the Corporations Act 2001 (see for example section 601QA of that Act).

(2) However, an interest mentioned in subsection (1) is to be taken into account for the purposes of working out the percentage of that or any other interest in the entity.

Note: The effect of this section is that an interest of, for example, 2% held by a foreign person is to be disregarded for the purposes of determining whether 2 or more foreign persons hold an aggregate substantial interest in an entity. However, the interest is to be taken into account in working out the percentage of any interest in the entity.

48 Tracing of substantial interests in corporations and trusts

Subsection 19(3) of the Act does not apply in relation to a significant action or notifiable action taken by a foreign government investor.

Note: The effect of this section is that, for an action taken by a foreign government investor, section 19 of the Act (tracing of substantial interests in corporations and trusts) applies in the circumstances specified in subsection 19(3) of the Act.

Part 4—Thresholds

49 Simplified outline of this Part

Certain actions are only significant actions or notifiable actions if the threshold test is met. This Part prescribes values for that test.

There is a single threshold value for action taken in relation to agribusinesses.

For entities (being corporations or unit trusts) and Australian businesses other than agribusinesses, the threshold value depends on who takes the action and whether the action is taken in relation to a sensitive business.

The threshold value for land depends on who takes the action, the kind of land in relation to which the action is taken and other circumstances. Some land has no threshold value.

Most of the threshold values prescribed under this Part are indexed each year.

50 Certain actions taken in relation to agribusinesses

The following table prescribes a value for section 51 of the Act (agribusinesses) to the extent that that section relates to item 1 of the table in that section.

Threshold value for certain actions take in relation to agribusinesses |

Item | For action taken by … | the value (in millions of dollars) is … |

1 | any foreign person | 55. |

Note: A value prescribed by this section is indexed under section 53.

51 Taking action in relation to entities and businesses

The following table prescribes values for section 51 of the Act (entities and businesses) to the extent that that section relates to items 2 to 5 of the table in that section.

Threshold value for entities and businesses |

Item | For action taken by … | the value (in millions of dollars) is … |

1 | an agreement country investor where the action relates to: (a) an entity, or a subsidiary of an entity, that is not carrying on a sensitive business or a trustee of a trust that does not hold assets of a sensitive business; or (b) a business that is not a sensitive business | 1 094. |

2 | any foreign person in any other circumstances | 252. |

Note: A value prescribed by this section is indexed under section 53.

52 Land

Land without threshold value

(1) For subsection 52(1) of the Act, the following land is prescribed:

(a) residential land, except residential land covered by subsection (2);

(b) commercial land that is vacant;

(c) a mining or production tenement, except a tenement being acquired by a relevant agreement country investor;

(d) land (including land otherwise covered by subsection (4) or (5)) acquired by a foreign government investor;

(e) land held by an Australian land corporation or the trustee of an Australian land trust (except an agricultural land corporation or an agricultural land trust) if:

(i) the interest in Australian land that is acquired by a foreign person is an interest in a share in the corporation or a unit in the trust; and

(ii) the land is not covered by subsection (3).

Residential land not covered by subsection (1)

(2) Residential land is covered by this subsection if:

(a) the land is also commercial land that is not vacant; and

(b) the area of land that is residential land (excluding any commercial residential premises) is less than 10% of the total area of the land; and

(c) the value of the land that is residential land (excluding any commercial residential premises) is less than 10% of the total value of the land; and

(d) a reasonable assessment of the area and value of the land was made in determining that the land is covered by paragraphs (b) and (c).

Note: The threshold for land covered by this subsection is in the table in subsection (5).

Land held by Australian land corporation or trustee not covered by subsection (1)

(3) Land held by an Australian land corporation or the trustee of an Australian land trust is covered by this subsection if:

(a) the total value of interests in residential land, and commercial land that is vacant, that are held by the corporation or trustee is less than 10% of the value of the total assets of the corporation or trustee; and

(b) a reasonable assessment of the value of the interests was made in determining that the land is covered by paragraph (a).

Note: The threshold for land covered by this subsection is in the table in subsection (5).

Threshold value for agricultural land

(4) The following table prescribes a value for paragraph 52(2)(b) of the Act (agricultural land).

Threshold value for agricultural land |

Item | For this kind of land … | the value (in millions of dollars) is … |

1 | agricultural land that is being acquired by a foreign person | 15. |

2 | agricultural land that is held by an agricultural land corporation or an agricultural land trust if the interest that is being acquired by a foreign person is an interest in a share in the corporation or a unit in the trust | 15. |

Note: The threshold test and thresholds relating to agricultural land do not apply in relation to land acquired by a relevant agreement country investor or an enterprise or national (other than a foreign government investor) of Singapore or Thailand (see subsection 40(2)).

Threshold value for any other land

(5) The following table prescribes values for paragraph 52(3)(b) of the Act (any other land).

Threshold value for any other land |

Item | For this kind of land … | the value (in millions of dollars) is … |

1 | land described in paragraph 52(3)(a) of the Act that is being acquired by an agreement country investor | 1 094. |

2 | land described in paragraph 52(3)(a) of the Act that is: (a) being acquired by an enterprise or national of Singapore or Thailand (other than a foreign government investor); and (b) used wholly and exclusively for a primary production business | 50. |

3 | land described in paragraph 52(3)(a) of the Act that: (a) meets all the conditions mentioned in subsection (6) of this section; and (b) is being acquired by a foreign person (except an agreement country investor) | 55. |