Part 1—Preliminary

Division 1—Preliminary

1 Name

This is the Petroleum Resource Rent Tax Assessment Regulation 2015.

2 Commencement

(1) Each provision of this instrument specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information |

Column 1 | Column 2 | Column 3 |

Provisions | Commencement | Date/Details |

1. The whole of this instrument | 1 April 2016. | 1 April 2016 |

Note: This table relates only to the provisions of this instrument as originally made. It will not be amended to deal with any later amendments of this instrument.

(2) Any information in column 3 of the table is not part of this instrument. Information may be inserted in this column, or information in it may be edited, in any published version of this instrument.

3 Authority

This instrument is made under the Petroleum Resource Rent Tax Assessment Act 1987.

4 Schedules

Each instrument that is specified in a Schedule to this instrument is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this instrument has effect according to its terms.

Division 2—Definitions

5 Definitions

Note: Other definitions are set out in section 2 of the Act, including the following:

(a) excluded commodity;

(b) financial year;

(c) instalment period;

(d) long‑term bond rate;

(e) marketable petroleum commodity;

(f) onshore petroleum project;

(g) petroleum;

(h) petroleum project;

(i) sales gas;

(j) year of tax.

In this instrument:

Act means the Petroleum Resource Rent Tax Assessment Act 1987.

actual mass of project natural gas, for an integrated operation and a year of tax in which the operation produces project liquid or project electricity, means the mass of project natural gas that was used to produce project liquid or project electricity.

actual volume of project natural gas, for an integrated operation and a year of tax in which the operation produces project liquid or project electricity, means the volume of project natural gas that was used to produce project liquid or project electricity.

advance pricing arrangement has the meaning given by subsection 22(1).

annual allocation, for a capital cost, has the meaning given by section 42.

arm’s length price means the consideration received or receivable in relation to a transaction in which the parties are dealing with each other at arm’s length.

assessable gas means:

(a) for calculating assessable petroleum receipts relating to sales gas—project sales gas; or

(b) for calculating assessable petroleum receipts relating to natural gas—project natural gas.

assessment year means the year of tax for which an RPM price is to be calculated by applying the residual pricing method.

augmented, for a capital cost, has the meaning given by section 16.

capital allowance, for a financial year, has the meaning given by section 18.

capital cost has the meaning given by subsection 36(1).

comparable uncontrolled price or CUP has the meaning given by:

(a) for sales gas—subsection 23(1); and

(b) for natural gas—subsection 23(2).

cost‑plus price has the meaning given by section 26.

direct cost has the meaning given by section 33.

downstream, for a cost, has the meaning given by subsection 38(6).

downstream stage has the meaning given by:

(a) for an integrated GTL operation for the purposes of calculating assessable petroleum receipts relating to sales gas—subsection 8(2); and

(b) for an integrated GTE operation for the purposes of calculating assessable petroleum receipts relating to sales gas—subsection 8(3); and

(c) for an integrated GTL operation for the purposes of calculating assessable petroleum receipts relating to natural gas—subsection 8(5); and

(d) for an integrated GTE operation for the purposes of calculating assessable petroleum receipts relating to natural gas—subsection 8(6).

estimated average annual mass of project natural gas, for an integrated operation, has the meaning given by subsection 13(7).

estimated average annual volume of project natural gas, for an integrated operation, has the meaning given by subsection 13(6).

expected operating life, of an integrated operation, has the meaning given by subsection 13(8).

included cost has the meaning given by section 35.

indirect cost has the meaning given by subsection 33(5).

integrated GTE operation has the meaning given by subsection 7(1).

integrated GTL operation has the meaning given by subsection 6(1).

integrated operation means an integrated GTE operation or an integrated GTL operation.

mass coefficient, for an integrated operation in a year of tax, has the meaning given by subsection 15(2).

MPC production year has the meaning given by:

(a) for an integrated GTL operation—subsection 6(9); and

(b) for an integrated GTE operation—subsection 7(9).

multiple use, of a unit of property, has the meaning given by section 10.

netback price has the meaning given by section 27.

non‑arm’s length transaction has the meaning given by section 12.

operating cost has the meaning given by subsection 36(3).

operating life has the meaning given by:

(a) for an integrated GTL operation—subsection 6(8); and

(b) for an integrated GTE operation—subsection 7(8).

participant, in an integrated operation, has the meaning given by section 11.

personal cost has the meaning given by subsection 33(6).

petroleum product, of an operation, means petroleum, or a product of petroleum, that is recovered, produced or processed in the operation.

phase, of an integrated operation, has the meaning given by subsection 9(4).

phase cost, for a phase of an integrated operation, means the phase cost worked out using subsections 38(2) and (3).

production date has the meaning given by:

(a) for an integrated GTL operation—subsection 6(7); and

(b) for an integrated GTE operation—subsection 7(7).

production year has the meaning given by:

(a) for an integrated GTL operation—subsection 6(6); and

(b) for an integrated GTE operation—subsection 7(6).

project electricity, of an integrated GTE operation, has the meaning given by subsection 7(4).

project liquid, of an integrated GTL operation, has the meaning given by subsection 6(4).

project natural gas has the meaning given by:

(a) for an integrated GTL operation—subsection 6(2); and

(b) for an integrated GTE operation—subsection 7(2).

project product has the meaning given by:

(a) for an integrated GTL operation—subsection 6(5); and

(b) for an integrated GTE operation—subsection 7(5).

project sales gas has the meaning given by:

(a) for an integrated GTL operation—subsection 6(3); and

(b) for an integrated GTE operation—subsection 7(3).

reduced, for a capital cost, has the meaning given by section 17.

relevant sector cost has the meaning given by subsection 33(2).

residual pricing method means the method statement in section 30.

RPM price, for a participant in an integrated operation in a year of tax, has the meaning given by sections 24 and 25.

start date, for capital cost incurred in an integrated operation, means 1 January of the financial year in which the cost is incurred.

taxpayer means a person who is a participant in an integrated operation and whose assessable petroleum receipts in relation to sales gas or natural gas from that operation are to be worked out under this instrument because of section 19, 20 or 21.

upstream, for a cost, has the meaning given by subsection 38(5).

upstream stage has the meaning given by:

(a) for an integrated operation for the purposes of calculating assessable petroleum receipts relating to sales gas—subsection 8(1); and

(b) for an integrated operation for the purposes of calculating assessable petroleum receipts relating to natural gas—subsection 8(4).

volume coefficient, for an integrated operation in a year of tax, has the meaning given by subsection 14(2).

6 When an integrated GTL operation exists

(1) An integrated GTL operation exists if there is an operation (the overall operation) in which:

(a) petroleum is, or will be, recovered from a petroleum project; and

(b) sales gas is, or will be, produced from some or all of the petroleum; and

(c) some or all of the sales gas is, or will be, processed into a liquefied product.

(2) The project natural gas of the integrated GTL operation is the petroleum (in the form of natural gas) mentioned in paragraph (1)(a) from which sales gas will be produced and processed into liquefied product within the overall operation (including any of that natural gas that is used in that production and processing).

(3) The project sales gas of the integrated GTL operation is the sales gas mentioned in paragraph (1)(b) that will be processed into liquefied product within the overall operation (including any of that sales gas that is used in that processing).

(4) The liquefied product mentioned in paragraph (1)(c) is project liquid of the integrated GTL operation.

(5) The project natural gas, project sales gas and project liquid are project product of the integrated GTL operation.

(6) The production year for the integrated GTL operation is:

(a) if an election has been made in relation to the integrated GTL operation under section 50—the 2012‑13 year of tax; and

(b) otherwise—the year of tax in which processing first occurred.

(7) The 31 December of the production year is the production date for the integrated GTL operation.

(8) The period beginning with the production year and ending with the year of tax in which project sales gas is last processed into project liquid is the operating life of the integrated GTL operation.

(9) If the integrated GTL operation produces a marketable petroleum commodity other than project sales gas, the year of tax in which it is first produced is the MPC production year for the integrated GTL operation.

7 When an integrated GTE operation exists

(1) An integrated GTE operation exists if there is an operation (the overall operation) in which:

(a) petroleum is, or will be, recovered from a petroleum project; and

(b) sales gas is, or will be, produced from some or all of the petroleum; and

(c) some or all of the sales gas is, or will be, consumed in the commercial production of electricity.

(2) The project natural gas of the integrated GTE operation is the petroleum (in the form of natural gas) mentioned in paragraph (1)(a) from which sales gas will be produced and consumed in the production of electricity within the overall operation (including any of that natural gas that is used in that production).

(3) The project sales gas of the integrated GTE operation is the sales gas mentioned in paragraph (1)(b) that will be consumed in the production of electricity within the overall operation (including any of that sales gas that is used in that production).

(4) The electricity mentioned in paragraph (1)(c) is project electricity of the integrated GTE operation.

(5) The project natural gas, project sales gas and project electricity are project product of the integrated GTE operation.

(6) The year of tax in which the project sales gas is first consumed in the production of project electricity is the production year for the integrated GTE operation.

(7) The production date for the integrated GTE operation is 31 December of the production year.

(8) The period beginning with the production year and ending with the year of tax in which projects sales gas is last consumed in the production of project electricity is the operating life of the integrated GTE operation.

(9) If the integrated GTE operation produces a marketable petroleum commodity other than project sales gas, the year of tax in which it is first produced is the MPC production year for the integrated GTE operation.

8 Upstream and downstream stages of integrated operation

Assessable petroleum receipts relating to sales gas

(1) For the purposes of calculating assessable petroleum receipts relating to sales gas under section 19 or 20, the upstream stage of an integrated operation is a series of phases ending when all of the following actions have been completed:

(a) the recovery of project natural gas;

(b) any multiple use of units of property that are used in the recovery of project natural gas;

(c) the storage of recovered project natural gas before being used in the production of sales gas;

(d) any multiple use of the units of property that are used to store recovered project natural gas;

(e) the production of project sales gas;

(f) any multiple use of units of property that are used in the production of project sales gas;

(g) the transportation of project product for the recovery mentioned in paragraph (a) or the production mentioned in paragraph (e);

(h) any multiple use of units of property for transportation mentioned in paragraph (g);

(i) the storage of project sales gas at or adjacent to the place at which it is produced, if the storage occurs:

(i) before the sale referred to in paragraph 24(1)(d) of the Act; or

(ii) before the gas becomes or became an excluded commodity as described in paragraph 24(1)(e) of the Act;

(as applicable);

(j) any multiple use of units of property that are used for the storage of project sales gas mentioned in paragraph (i).

(2) For the purposes of calculating assessable petroleum receipts relating to sales gas under section 19 or 20, the downstream stage of an integrated GTL operation is a series of phases beginning when the upstream stage ends and ending when all of the following actions have been completed:

(a) the storage of project sales gas at or adjacent to the place at which it is produced, if the storage occurs:

(i) after the sale referred to in paragraph 24(1)(d) of the Act; or

(ii) after the gas becomes or became an excluded commodity as described in paragraph 24(1)(e) of the Act;

(as applicable);

(b) the transportation (if any) of project sales gas from the upstream stage for processing into project liquid;

(c) the processing of the project sales gas into project liquid;

(d) any multiple use of units of property that are used in the processing of the project sales gas into project liquid;

(e) the transportation of project product for the processing of project sales gas mentioned in paragraph (c);

(f) any activity associated with an action mentioned in paragraphs (b) to (e) for the purpose of using project sales gas to produce project liquid;

(g) any multiple use of units of property for the transportation mentioned in paragraph (e);

(h) the sale of project liquid without further processing;

(i) the storage of project liquid at or adjacent to the place at which it is produced by the processing mentioned in paragraph (c);

(j) the loading of project liquid at a loading facility:

(i) adjacent to the place at which it is produced by the processing mentioned in paragraph (c); or

(ii) adjacent to the place at which it is stored as mentioned in paragraph (i);

(k) the transportation of project liquid between any or all of:

(i) the place at which it is produced by the processing mentioned in paragraph (c); and

(ii) the place at which it is stored as mentioned in paragraph (i); and

(iii) the place at which it is loaded as mentioned in paragraph (j);

(l) any multiple use of units of property for the storage, loading or transportation mentioned in paragraphs (i), (j) and (k).

(3) For the purposes of calculating assessable petroleum receipts relating to sales gas under section 19 or 20, the downstream stage of an integrated GTE operation is a series of phases beginning when the upstream stage ends and ending when all of the following actions have been completed:

(a) the storage of project sales gas at or adjacent to the place at which it is produced, if the storage occurs:

(i) after the sale referred to in paragraph 24(1)(d) of the Act; or

(ii) after the gas becomes or became an excluded commodity as described in paragraph 24(1)(e) of the Act;

(as applicable);

(b) the transportation (if any) of the project sales gas from the upstream stage for combustion to produce project electricity;

(c) the combustion of the project sales gas to produce project electricity;

(d) any multiple use of units of property that are used in the combustion of the project sales gas to produce project electricity;

(e) any activity associated with an action mentioned in paragraphs (b) to (d) for the purposes of using project sales gas to produce project electricity;

(f) the sale of project electricity.

Assessable petroleum receipts relating to natural gas

(4) For the purposes of calculating assessable petroleum receipts relating to natural gas under section 21, the upstream stage of an integrated operation is a series of phases ending when all of the following actions have been completed:

(a) the recovery of project natural gas;

(b) any multiple use of units of property that are used in the recovery of project natural gas;

(c) the storage of recovered project natural gas before use in the production of sales gas, if the storage occurs before the sale referred to in paragraph 24(1)(f) of the Act;

(d) any multiple use of the units of property that are used to store recovered project natural gas (including units of property that are used to store recovered project natural gas before use in the production of sales gas, if the storage occurs before the sale referred to in paragraph 24(1)(f) of the Act);

(e) the transportation of project product for the recovery mentioned in paragraph (a);

(f) any multiple use of units of property for transportation referred to in paragraph (e).

(5) For the purposes of calculating assessable petroleum receipts relating to natural gas under section 21, the downstream stage of an integrated GTL operation is a series of phases beginning when the upstream stage ends and ending when all of the following actions have been completed:

(a) the storage of recovered project natural gas, if the storage occurs after the sale referred to in paragraph 24(1)(f) of the Act;

(b) any multiple use of the units of property that are used to store recovered project natural gas (including units of property that are used to store recovered project natural gas, if the storage occurs after the sale referred to in paragraph 24(1)(f) of the Act);

(c) the production of project sales gas;

(d) any multiple use of units of property that are used in the production of project sales gas;

(e) the transportation of project product for the production mentioned in paragraph (c);

(f) any multiple use of units of property for transportation mentioned in paragraph (e).

(g) the storage of project sales gas at or adjacent to the place at which it is produced;

(h) any multiple use of units of property that are used for the storage of project sales gas mentioned in paragraph (g);

(i) the transportation (if any) of project sales gas for processing into project liquid;

(j) the processing of the project sales gas into project liquid;

(k) any multiple use of units of property that are used in the processing of the project sales gas into project liquid;

(l) the transportation of project product for the processing of project sales gas mentioned in paragraph (j);

(m) any activity associated with an action mentioned in paragraphs (i) to (l) for the purpose of using project sales gas to produce project liquid;

(n) any multiple use of units of property for the transportation mentioned in paragraph (l);

(o) the sale of project liquid without further processing;

(p) the storage of project liquid at or adjacent to the place at which it is produced by the processing mentioned in paragraph (j);

(q) the loading of project liquid at a loading facility:

(i) adjacent to the place at which it is produced by the processing mentioned in paragraph (j); or

(ii) adjacent to the place at which it is stored as mentioned in paragraph (p);

(r) the transportation of project liquid between any or all of:

(i) the place at which it is produced by the processing mentioned in paragraph (j); and

(ii) the place at which it is stored as mentioned in paragraph (p); and

(iii) the place at which it is loaded as mentioned in paragraph (q);

(s) any multiple use of units of property for the storage, loading or transportation mentioned in paragraphs (p), (q) and (r).

(6) For the purposes of calculating assessable petroleum receipts relating to natural gas under section 21, the downstream stage of an integrated GTE operation is a series of phases beginning when the upstream stage ends and ending when all of the following actions have been completed:

(a) the production of project sales gas;

(b) any multiple use of units of property that are used in the production of project sales gas;

(c) the transportation of project product for the production mentioned in paragraph (a);

(d) any multiple use of units of property for transportation mentioned in paragraph (c).

(e) the storage of project sales gas at or adjacent to the place at which it is produced;

(f) any multiple use of units of property that are used for the storage of project sales gas mentioned in paragraph (e);

(g) the transportation (if any) of the project sales gas for combustion to produce project electricity;

(h) the combustion of the project sales gas to produce project electricity;

(i) any multiple use of units of property that are used in the combustion of the project sales gas to produce project electricity;

(j) any activity associated with an action mentioned in paragraphs (g) to (i) for the purposes of using project sales gas to produce project electricity;

(k) the sale of project electricity.

Note 1: Phases are explained using subsections 9(1) and (4).

Note 2: In general terms, a phase is a part of an operation during which the ratio of project product to total product flowing through the operation remains the same (and is expected to remain the same). The upstream and downstream stages of an integrated operation may include a number of phases, but each stage ends when the actions associated with the last phase have been completed.

9 Phase points of integrated operation

(1) The phase points of an integrated operation are:

(a) the point where the upstream stage ends and the downstream stage begins; and

(b) any point in the flow of project product through the operation at which there is expected to be a difference in the ratio of project product to total product flowing through the operation before and after the point.

Note 1: This section divides the integrated operation into phases in such a way that petroleum product is not brought into or taken out of the operation except at the beginning or end of a phase. In obtaining the cost‑plus and netback prices:

(a) the various joint costs incurred by participants in the operation are attributed to each phase (see section 38); and

(b) the capital costs are annualised (see Division 3 of Part 4); and

(c) the costs for the assessment year are apportioned between the project product and other product, using an energy coefficient appropriate for the phase (see section 43).

Note 2: This procedure assumes that the same phase points apply over the life of the project. If a new phase point emerges that was not identified before the production year, there may need to be a recalculation of the annualised capital costs.

Example 1: An integrated GTL operation begins with the recovery of natural gas and liquid petroleum, using the same extraction facilities. Separate pipelines are used to carry off the natural gas and the liquid petroleum, so that only the gas pipeline is part of the operation. The total product flowing through the operation is reduced, as the liquid petroleum is removed. The ratio of project product in relation to total product therefore changes at the beginning of the gas pipeline, and the beginning of the pipeline is therefore a phase point.

Example 2: At the sales gas production facility of an integrated GTL operation, natural gas from another source is added to the project natural gas. The point at which the natural gas is added is a phase point.

Example 3: Some of the sales gas produced in an integrated GTL operation is transported in a pipeline that is part of the operation, and therefore enters the downstream phase; it is then sold before liquefaction. The ratio of project product to total product changes when the sales gas is sold before liquefaction, as the total product in the operation is reduced. The point of sale is therefore a phase point.

(2) However, paragraph (1)(b) does not apply to an integrated GTL operation for which an election has been made under section 50.

(3) Any phase points of an integrated GTL operation before the end of the upstream stage do not apply for the purposes of working out under section 21 the assessable petroleum receipts of a taxpayer who is a participant in the operation if:

(a) the operation recovers petroleum from an onshore petroleum project; and

(b) an election under section 48 has been made for the operation.

(4) The integrated operation is divided into phases by the phase points.

Note: In general terms, a phase is a stage of an operation during which the ratio of project product to total product flowing through the operation remains the same (and is expected to remain the same).

(5) The participants in the integrated operation must:

(a) in the financial year before the production year, notify the Commissioner of any phase points of the operation that are apparent to any of them at that time; and

(b) notify the Commissioner as soon as practicable of any phase point that becomes apparent at a later time.

(6) However, subsection (5) does not apply if an election has been made in relation to the integrated operation under section 50.

(7) The participants in the integrated operation must satisfy the Commissioner that they can provide accurate records of the quantities of petroleum product before and after each phase point (for example, by including metering facilities at the phase point or using other reliable estimation techniques).

10 When there is multiple use of a phase

(1) A reference to multiple use of a phase relating to the recovery of project natural gas is a reference to the use of the unit of property, at any time during the operating life of the integrated operation, in operations to recover petroleum other than project natural gas from the petroleum project.

Example 1: An oil platform is used to recover both natural gas and liquid petroleum.

Example 2: An oil platform is used to recover petroleum from a petroleum project outside the operation.

(2) A reference to the multiple use of a phase relating to the production of project sales gas is a reference to the use of the unit of property, at any time during the operating life of the integrated operation, to produce marketable petroleum commodities other than project sales gas from petroleum (whether or not the petroleum was recovered from the petroleum project of the operation).

Example 1: Plant is used to produce sales gas, some of which is to be sold for direct consumption as energy.

Example 2: Plant is used to produce sales gas from natural gas recovered outside the operation.

(3) A reference to the multiple use of a phase relating to the processing of project sales gas into project liquid is a reference to the use of the unit of property, at any time during the operating life of the integrated GTL operation, to process marketable petroleum commodities other than project sales gas into liquefied product (whether or not the other marketable petroleum commodities were produced in the operation).

Example: Plant used to liquefy project sales gas is also used to liquefy sales gas produced outside the operation.

(4) A reference to the multiple use of a phase relating to the combustion of project sales gas to produce electricity is a reference to the use of the unit of property, at any time during the operating life of the integrated GTE operation, to combust petroleum products other than project sales gas to produce electricity (whether or not the other petroleum products were produced in the operation).

Example: Plant used to combust project sales gas is also used to combust sales gas produced outside the operation.

(5) A reference to the multiple use of a phase relating to the transportation of project product is a reference to the use of the unit of property, at any time during the operating life of the integrated operation, to transport petroleum product other than project product within the operation (whether or not the petroleum product was recovered or produced in the operation).

Example: A pipeline from an offshore petroleum recovery platform that carries natural gas to shore, only some of which is project natural gas.

(6) A reference to the multiple use of a storage facility is a reference to the use of the storage facility, at any time during the operating life of the integrated operation, to store petroleum product other than project product within the operation (whether or not the petroleum product was recovered or produced in the operation).

Example: The use of a storage facility both:

(a) to store project liquid; and

(b) to store petroleum that is not project liquid.

(7) A reference to the multiple use of a loading facility is a reference to the use of the loading facility, at any time during the operating life of the integrated GTL operation, to load petroleum product other than project product within the operation (whether or not the petroleum product was recovered or produced in the operation).

Example: The use of a loading facility to load petroleum product of another operation.

11 Participants in an integrated operation

A person is a participant in an integrated operation if the person holds an interest in the operation that entitles the person to petroleum product or electricity of the operation at the end of at least one phase.

12 Non‑arm’s length transaction

A transaction is a non‑arm’s length transaction if the Commissioner, having regard to any connection between the parties to the transaction or to any other relevant circumstances, is satisfied that the parties to the transaction are not dealing with each other at arm’s length in relation to the transaction.

13 Estimated average annual volume or mass of project natural gas

(1) The participants in an integrated operation must give to the Commissioner estimates of:

(a) the operating life of the operation, in years; and

(b) either:

(i) if the participants will measure by volume—the total volume of project natural gas to be recovered during the life of the operation; or

(ii) if the participants will measure by mass—the total mass of project natural gas to be recovered during the life of the operation.

(2) The estimates must be given to the Commissioner:

(a) if an election has been made in relation to the integrated operation under section 50—no later than:

(i) the day on which the participants must give to the Commissioner a starting base return under subclause 22(2) of Schedule 2 to the Act; or

(ii) a later day that the Commissioner allows; or

(b) otherwise—in the financial year before the production year.

(3) As soon as practicable after receiving an estimate (including a revised estimate under subsection (4)) from the participants, the Commissioner must notify them in writing that the Commissioner:

(a) accepts the estimate or revised estimate; or

(b) has substituted an estimate under subsection (5).

(4) If, from new information, it appears that an estimate notified by the Commissioner is inaccurate, the participants must give to the Commissioner a revised estimate.

(5) If, having regard to relevant information, the Commissioner is not satisfied that an estimate given by the participants for the purposes of subsection (1) or (4) is reasonable, the Commissioner may substitute an estimate that the Commissioner is satisfied is reasonable.

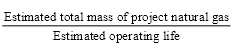

(6) For an operation in which natural gas will be measured by volume, the estimated average annual volume of project natural gas is (using the estimates notified by the Commissioner):

(7) For an operation in which natural gas will be measured by mass, the estimated average annual mass of project natural gas is (using the estimates notified by the Commissioner):

(8) The expected operating life of the integrated operation is the period of years estimated as the operating life, as notified by the Commissioner, beginning with the production year.

14 Meaning of volume coefficient

(1) In this section, for an integrated operation in which natural gas is measured by volume:

base year means:

(a) if an election has been made in relation to the operation under section 50—the 2012‑13 year of tax; or

(b) otherwise—the year of tax in which the actual volume of project natural gas first exceeds the estimated average annual volume of project natural gas for the operation.

Note: If the estimated average annual volume of project natural gas changes from one year of tax to another, the base year for the calculation of the volume coefficient may also change.

(2) The volume coefficient for an integrated operation in which natural gas is measured by volume in a year of tax (the current year) is:

where:

VA means the actual volume of project natural gas for the current year.

VB means:

(a) if the current year is before the base year—the estimated average annual volume of project natural gas; or

(b) if the current year is the base year—VA; or

(c) if the current year is after the base year—the amount calculated using the formula:

where:

n means a year of tax, with the base year being year 1, the year after the base year being year 2, and so on.

N means the number of years of tax from the base year to the current year (inclusive).

Vn means the actual volume of project natural gas for year n.

15 Meaning of mass coefficient

(1) In this section, for an integrated operation in which natural gas is measured by mass:

base year means:

(a) if an election has been made in relation to the operation under section 50—the 2012‑13 year of tax; or

(b) otherwise—the year of tax in which the actual mass of project natural gas first exceeds the estimated average annual mass of project natural gas for the operation.

Note: If the estimated average annual mass of project natural gas changes from one year of tax to another, the base year for the calculation of the mass coefficient may also change.

(2) The mass coefficient for an integrated operation in which natural gas is measured by mass in a year of tax (the current year) is:

where:

MA means the actual mass of project natural gas for the current year.

MB means:

(a) if the current year is before the base year—the estimated average annual mass of project natural gas; or

(b) if the current year is the base year—MA; or

(c) if the current year is after the base year—the amount calculated using the formula:

where:

Mn means the actual mass of project natural gas for year n.

n means a year of tax, with the base year being year 1, the year after the base year being year 2, and so on.

N means the number of years of tax from the base year to the current year (inclusive).

16 Augmentation of a capital cost

A capital cost for an integrated operation is augmented for a number of years by applying the formula:

where:

capital allowance means the capital allowance for:

(a) in the case of subsection 39(2)—the final cost year; and

(b) in the case of subsection 40(2)—the production year; and

(c) in the case of subsection 41(2)—the production year; and

(d) in the case of paragraph 41(3)(a)—the MPC production year.

N means the number of years.

17 Reduction of a capital cost

A capital cost for an integrated operation is reduced for a number of years by applying the formula:

where:

Capital allowance means the capital allowance for:

(a) in the case of paragraph 41(3)(b)—the MPC production year; and

(b) in the case of subsection 41(4)—the year of tax of the start date for the capital cost.

N means the number of years.

18 Capital allowance

The capital allowance, for a financial year, is calculated using the formula:

Part 2—Assessable petroleum receipts

19 Assessable petroleum receipts—sales gas of integrated operation with non‑arm’s length sale

(1) For the purposes of subparagraph 24(1)(d)(iii) of the Act, this section applies to sales gas that has been sold if:

(a) it is project sales gas of an integrated operation; and

(b) the sale is a non‑arm’s length transaction.

Note: Paragraph 24(1)(b) of the Act applies to other sales of sales gas.

Advance pricing arrangement

(2) If an advance pricing arrangement applies to the sale, the amount of assessable petroleum receipts of a taxpayer is the amount calculated in accordance with the arrangement.

Comparable uncontrolled price

(3) The assessable petroleum receipts of a taxpayer in relation to the sale is the amount calculated under subsection (4) if:

(a) no advance pricing arrangement applies to the sale; and

(b) a comparable uncontrolled price exists for the sale; and

(c) no election has been made in relation to the integrated operation under section 49 or 50.

(4) The amount is the higher of:

(a) the consideration received or receivable, less any expenses payable, by the taxpayer in relation to the sale; and

(b) the comparable uncontrolled price multiplied by the volume or mass of project sales gas sold.

Residual pricing method

(5) The assessable petroleum receipts of a taxpayer in relation to the sale is the amount calculated under subsection (6) if:

(a) no advance pricing arrangement applies to the sale; and

(b) either:

(i) no comparable uncontrolled price exists for the sale; or

(ii) an election has been made in relation to the integrated operation under section 49 or 50.

(6) The amount is the higher of:

(a) the consideration received or receivable, less any expenses payable, by the taxpayer in relation to the sale; and

(b) the RPM price of project sales gas for the taxpayer in the year of tax in which the sale took place multiplied by the volume or mass of project sales gas sold.

20 Assessable petroleum receipts—sales gas of integrated operation becoming excluded commodity other than by being sold

(1) For the purposes of paragraph 24(1)(e) of the Act, this section applies to sales gas that becomes or became an excluded commodity if it is project sales gas of an integrated operation.

Note: Paragraph 24(1)(c) of the Act applies to other sales gas that becomes an excluded commodity.

Advance pricing arrangement

(2) If an advance pricing arrangement applies to the transaction, the amount of assessable petroleum receipts of a taxpayer is the amount calculated in accordance with the arrangement.

Comparable uncontrolled price

(3) The assessable petroleum receipts of a taxpayer in relation to the transaction is the amount calculated under subsection (4) if:

(a) no advance pricing arrangement applies to the transaction; and

(b) a comparable uncontrolled price exists for the transaction; and

(c) no election has been made in relation to the integrated operation under section 49 or 50.

(4) The amount is the comparable uncontrolled price multiplied by the volume or mass of project sales gas subject to the transaction.

Residual pricing method

(5) The assessable petroleum receipts of a taxpayer in relation to the transaction is the amount calculated under subsection (6) if:

(a) no advance pricing arrangement applies to the sale; and

(b) either:

(i) no comparable uncontrolled price exists for the sale; or

(ii) an election has been made in relation to the integrated operation under section 49 or 50.

(6) The amount is the RPM price of project sales gas for the taxpayer in the year of tax in which the transaction took place multiplied by the volume or mass of project sales gas subject to the transaction.

(7) In this section:

transaction means the act by which the project sales gas becomes or became an excluded commodity.

21 Assessable petroleum receipts—natural gas of onshore integrated operation with non‑arm’s length sale

(1) For the purposes of subparagraph 24(1)(f)(ii) of the Act, this section applies to natural gas that has been sold if:

(a) it is project natural gas of an integrated operation that recovers petroleum from an onshore petroleum project; and

(b) the sale is a non‑arm’s length transaction.

Note: Paragraph 24(1)(a) of the Act applies to other sales of natural gas.

Advance pricing arrangement

(2) If an advance pricing arrangement applies to the sale, the amount of assessable petroleum receipts of a taxpayer is the amount calculated in accordance with the arrangement.

Comparable uncontrolled price

(3) The assessable petroleum receipts of a taxpayer in relation to the sale is the amount calculated under subsection (4) if:

(a) no advance pricing arrangement applies to the sale; and

(b) a comparable uncontrolled price exists for the sale; and

(c) no election has been made in relation to the integrated operation under section 49 or 50.

(4) The amount is the higher of:

(a) the consideration received or receivable, less any expenses payable, by the taxpayer in relation to the sale; and

(b) the comparable uncontrolled price multiplied by the volume or mass of project natural gas sold.

Residual pricing method

(5) The assessable petroleum receipts of a taxpayer in relation to the sale is the amount calculated under subsection (6) if:

(a) no advance pricing arrangement applies to the sale; and

(b) either:

(i) no comparable uncontrolled price exists for the sale; or

(ii) an election has been made in relation to the integrated operation under section 49 or 50.

(6) The amount is the higher of:

(a) the consideration received or receivable, less any expenses payable, by the taxpayer in relation to the sale; and

(b) the RPM price of project natural gas for the taxpayer in the year of tax in which the sale took place multiplied by the volume or mass of project natural gas sold.

22 Advance pricing arrangements

(1) The Commissioner may, at the request of a participant in an integrated operation, make an agreement (advance pricing arrangement) with the participant about how the assessable petroleum receipts of the participant are to be calculated in relation to project sales gas or project natural gas to which paragraph 24(1)(d), (e) or (f) of the Act applies.

(2) An advance pricing arrangement must specify:

(a) the term of the arrangement; and

(b) how the assessable receipts of the participant are to be calculated; and

(c) conditions under which the arrangement will apply.

Part 3—The substitute prices

23 The comparable uncontrolled price

(1) A comparable uncontrolled price, or CUP, in relation to a relevant transaction for a volume or mass of project sales gas, is a price for sales gas:

(a) that was obtained for a sale in a market that the Commissioner is satisfied is a relevant market in relation to the transaction; and

(b) that the Commissioner is satisfied is an observable arm’s length price.

(2) A comparable uncontrolled price, or CUP, in relation to a sale of a volume or mass of project natural gas to which paragraph 24(1)(f) of the Act applies, is a price for natural gas:

(a) that was obtained for a sale in a market that the Commissioner is satisfied is a relevant market in relation to the transaction; and

(b) that the Commissioner is satisfied is an observable arm’s length price.

(3) In determining whether a market is relevant, the demand and supply characteristics of the market must be taken into account, including:

(a) the composition of sales gas or natural gas sold in the market; and

(b) geographic differences between the production facilities and the product delivery point of the sales gas or natural gas sold in the market; and

(c) the end use for the sales gas or natural gas sold in the market.

Example: Retail, wholesale, manufacturing, feedstock, domestic.

(4) In determining whether a market is relevant, the following factors must also be taken into account:

(a) the terms of contracts usual in the market, including volumes, discounts, exchange exposures and other relevant conditions that would reasonably be considered to affect the price;

(b) market strategies;

(c) the existence of spot sales (including market penetration sales) below or above marginal cost;

(d) processing costs;

(e) technology used in processing;

(f) any other factors that it would be reasonable to consider.

(5) In this section:

relevant transaction, for a volume or mass of project sales gas, means:

(a) a sale of the gas to which paragraph 24(1)(d) of the Act applies; or

(b) an act by which the gas becomes an excluded commodity to which paragraph 24(1)(e) of the Act applies.

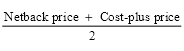

24 RPM price (transfer price using the residual pricing method)

Subject to this Part, the RPM price for an assessable gas for a taxpayer in a year of tax, is:

(a) if the cost‑plus price of the assessable gas is higher than the netback price—the netback price; and

(b) otherwise—the price given by the formula:

if the cost‑plus price and the netback price of the assessable gas can be obtained by applying the residual pricing method.

Note: The residual pricing method can only be applied if certain information is available (see section 29).

25 RPM price where information is not available

(1) This section applies if a taxpayer does not have sufficient information to work out the taxpayer’s RPM price for an assessable gas for a year of tax by applying the residual pricing method (see section 29).

(2) If the taxpayer and the Commissioner are able to agree on a price for the purposes of this subsection, that price is the RPM price.

(3) If the Commissioner and the taxpayer cannot agree on a price, and the Commissioner is satisfied that a price worked out:

(a) by the Commissioner applying the residual pricing method (disregarding section 29); and

(b) using the information available from other participants in the integrated operation;

is a fair and reasonable price, that price is the RPM price.

(4) If the Commissioner and the participant cannot agree on a price, but the Commissioner is not satisfied as to a price under subsection (3), the RPM price is the price determined by the Commissioner as fair and reasonable.

Example 1: If a participant incurs direct costs in the participant’s own right in relation to the integrated operation, and there is no agreement between the participants as to how those costs are to be shared amongst them, information about those direct costs may not be available to the other participants to allow them to work out the RPM price.

Example 2: This section would apply if a person becomes a participant in the integrated operation, but does not have access to all the information required to work out the RPM price.

Example 3: This section would apply if a participant in an onshore integrated GTL operation elects to apply the residual pricing method (under section 49), but has practical or commercial difficulties in accessing the information needed to apply that method because other participants in the operation have not elected to use that method.

26 Cost‑plus price

The cost‑plus price of an assessable gas for a taxpayer who is a participant in an integrated operation in a year of tax is:

where:

quantity coefficient means:

(a) for an integrated operation that measures by volume—the volume coefficient for the year of tax; or

(b) for an integrated operation that measures by mass—the mass coefficient for the year of tax.

quantity of assessable gas means the quantity, measured by volume or mass, of the assessable gas that was produced in the operation in the year of tax.

upstream capital costs means the total amount of upstream capital costs incurred by the participants and allocated to the year of tax (see section 30).

upstream operating costs means the total amount of upstream operating costs incurred by the participants in the year of tax (see section 30).

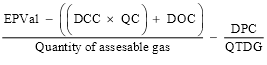

27 Netback price

(1) The netback price of an assessable gas for a taxpayer who is a participant in an integrated operation in a year of tax is:

where:

DCC (short for downstream capital costs) means the total amount of downstream capital costs incurred by the participants and allocated to the year of tax (see section 30).

DOC (short for downstream operating costs) means the total amount of downstream operating costs incurred by the participants in the year of tax (see section 30).

DPC (short for downstream personal costs) means the total amount of downstream personal costs of the taxpayer for the year of tax.

EPVal (short for end product value) means:

(a) if an election under section 52 has been made for the operation—the amount worked out under subsection (2); or

(b) otherwise—the total market value in the year of tax of:

(i) for an integrated GTL operation—the project liquid produced; or

(ii) for an integrated GTE operation—the project electricity produced.

QC (short for quantity coefficient) means:

(a) for an integrated operation that measures by volume—the volume coefficient for the year of tax; or

(b) for an integrated operation that measures by mass—the mass coefficient for the year of tax.

QTDG (short for quantity of taxpayer’s downstream gas) means the quantity, measured by volume or mass, of the assessable gas that was produced in the operation in the year of tax and:

(a) for an integrated GTL operation—processed into project liquid that the taxpayer was entitled to receive (including any of that gas that was used in that processing); or

(b) for an integrated GTE operation—consumed in the production of project electricity that the taxpayer was entitled to receive.

quantity of assessable gas means the quantity, measured by volume or mass, of the assessable gas that was produced in the operation in the year of tax.

(2) For the purposes of paragraph (a) of the definition of EPVal in subsection (1), work out the following for the taxpayer for the year of tax:

where:

market value of taxpayer product means the market value of the quantity of taxpayer product.

quantity of taxpayer product means the quantity, measured by volume or mass, of:

(a) for an integrated GTL operation—project liquid; or

(b) for an integrated GTE operation—project electricity;

that the taxpayer was entitled to receive in the year of tax.

quantity of total product means the total quantity, measured by volume or mass, of:

(a) for an integrated GTL operation—project liquid; or

(b) for an integrated GTE operation—project electricity;

produced in the operation in the year of tax.

(3) If the taxpayer sells a quantity of project liquid or project electricity from the operation as part of the operation in the year of tax, and the sale is an arm’s length transaction, the market value of the quantity is taken to be the amount received for the sale.

(4) For a quantity of project liquid or project electricity to which subsection (3) does not apply, the market value of the quantity is the market value at the end of the downstream stage.

(5) If the Commissioner is not satisfied that sufficient information is available to determine a market value for the purposes of subsection (4), the market value of the quantity of project liquid or project electricity is the amount determined by the Commissioner as fair and reasonable.

(6) If the value of QTDG is zero, the value of DPC divided by QTDG is taken to be zero.

Part 4—The residual pricing method

Division 1—The residual pricing method

28 Costs are net of GST tax credits and adjustments

A reference in this Part to a cost incurred by a person is a reference to the cost as reduced by:

(a) an input tax credit to which the person is, or becomes, entitled; or

(b) a decreasing adjustment.

29 When the residual pricing method can be applied

A cost‑plus price and netback price (and the related RPM price) can be calculated by applying the residual pricing method only if information is available about the direct costs (other than marketing and selling costs) associated with the relevant integrated operation that were incurred:

(a) by all participants in the operation; and

(b) for the relevant year of tax and previous financial years.

Note 1: If the information is not available, then section 25 will apply.

Note 2: The residual pricing method identifies:

(a) the pooled costs of the operation attributable to the project product; and

(b) the personal costs of the taxpayer attributable to the taxpayer’s share of project product.

Note 3: These pooled costs are used to calculate the major element of the cost‑plus and netback prices, and will be the same for each taxpayer participating in the operation. In contrast, the personal costs are used only to calculate a minor element of the netback price, and will vary for each taxpayer.

Note 4: These pooled costs and personal costs are used to work out the taxpayer’s cost‑plus price and netback price, which are then used to work out the RPM price under section 24.

30 The residual pricing method for working out cost‑plus price and netback price

This method statement is the residual pricing method for calculating a cost‑plus price and netback price (and the related RPM price) for a taxpayer who is a participant in an integrated operation in the assessment year:

Method statement

Step 1. Under section 31, identify all types of cost associated with the integrated operation up to and including the assessment year.

Step 2. Under section 32, exclude certain types of cost.

Step 3. Under section 33, classify each remaining type of cost as a direct cost or an indirect cost of the integrated operation, or a personal cost of a participant.

Step 4. Under section 34, exclude any personal costs of other participants. The costs that are left are the included costs for the taxpayer (see section 35).

Step 5. Under section 36, classify each included cost as an operating cost or a capital cost.

Step 6. Identify the amount of:

(a) each included operating cost incurred in the assessment year; and

(b) each included capital cost incurred up to and including the assessment year.

When doing so, use section 37 (about the amount and timing of certain included capital costs) if that section applies to an included capital cost.

Step 7. Under section 38:

(a) classify each included direct cost as a phase cost of one of the phases of the integrated operation; and

(b) classify each phase cost as an upstream cost or a downstream cost; and

(c) divide each included indirect cost into an upstream cost and a downstream cost.

Step 8. Under section 39 (about capital costs for units of property completed over several years), adjust the amount and timing of an included capital cost if that section applies to that cost.

Step 9. Under sections 40 and 41, adjust the amount and timing of an included capital cost whenever one of those sections applies to that cost.

Step 10. For each included capital cost, allocate to each year of tax from the production year onward a cost with the amount given by section 42.

Step 11. The costs for the assessment year are:

(a) the included upstream and downstream operating costs for the assessment year; and

(b) the upstream and downstream capital costs allocated to the assessment year under step 10; and

(c) the downstream personal costs of the taxpayer for the assessment year.

Step 12. For each phase cost for the assessment year, adjust the amount of that cost under subsection 43(1) if that subsection applies to the phase cost.

Step 13. Use the costs for the assessment year to calculate the participant’s cost‑plus price (see section 26) and netback price (see section 27) for the assessment year.

Note 1: This cost‑plus price and netback price can then be used to work out the participant’s RPM price for the assessment year (see section 24).

Note 2: Step 12 removes that part of each cost attributable to multiple use of a phase.

Division 2—Identifying and classifying included costs

31 Types of cost associated with integrated operation

(1) For the purposes of step 1 of the residual pricing method, identify all costs associated with an integrated operation in accordance with this section.

(2) Include all costs incurred by or on behalf of the participants that are attributable, indirectly attributable or partly attributable to the operation, whether incurred during the operating life of the operation or before the production year.

(3) A payment or allowance between participants is not a cost associated with the integrated operation.

(4) A capital cost that was incurred in relation to a unit of property that:

(a) was not, at the time it was incurred, used in the integrated operation; and

(b) was later used in the operation;

may be treated as a cost partly attributable to the operation.

(5) If a cost is only partly attributable to the integrated operation, the amount of the cost is taken to be the amount that can reasonably be apportioned to the operation.

32 Exclusion of certain costs of integrated operation

For the purposes of step 2 of the residual pricing method, exclude a cost associated with the integrated operation if it is one of the following:

(a) an exploration cost under section 37 of the Act;

(b) a cost incurred in carrying out a feasibility or environmental study before the production of project sales gas;

(c) a cost incurred in removing infrastructure facilities used for an integrated GTL operation;

(d) an environment or site restoration cost;

(e) expenditure listed in paragraphs 44(1)(a) to (h) of the Act.

33 Direct, indirect and personal costs

(1) For the purposes of step 3 of the residual pricing method, classify the remaining costs associated with the integrated operation as direct costs or indirect costs in accordance with this section.

(2) A cost is a relevant sector cost if it is wholly and directly attributable to one or more of the following activities of the operation:

(a) production;

(b) transport;

(c) storage;

(d) marketing;

(e) selling.

(3) A relevant sector cost that is wholly attributable to either the upstream stage or the downstream stage of the operation is a direct cost.

(4) A relevant sector cost that:

(a) is not wholly attributable to either the upstream stage or the downstream stage; and

(b) is greater than the threshold amount;

is taken to be divided into 2 direct costs, attributed to the upstream and downstream stages, each of the amount that can reasonably be apportioned to that stage.

(5) A cost that is not a direct cost because of subsection (3) or (4) is an indirect cost.

Note: Examples of indirect costs are business insurance, office expenses, administrative and accounting costs, payments in respect of land and buildings used in connection with administrative or accounting activities, intra company charges, contract penalties, legal and audit costs, travel and buyer liaison costs.

(6) If a cost is related to the marketing and selling of project liquid or project electricity, the cost is a personal cost of the participant that incurred it.

(7) For the purposes of this section, the threshold amount for a financial year is:

(a) an amount agreed by the taxpayer and the Commissioner for that financial year; or

(b) if the taxpayer and the Commissioner cannot agree on an amount for a financial year:

(i) if that financial year is the financial year 2005–2006 or an earlier financial year—$20 million; or

(ii) if that financial year is a later financial year—$20 million indexed by the GDP factor as applied under the Act, adjusted from 1 January each year.

34 Exclusion of personal costs of other participants

For the purposes of step 4 of the residual pricing method, exclude any personal cost that was incurred by another participant in the operation.

35 Included costs

A cost associated with an integrated operation is an included cost for the taxpayer if it is not excluded after applying sections 32 and 34.

Note: These included costs are the pooled non‑personal costs of all the participants in the integrated operation, and the personal costs of the taxpayer.

36 Capital costs and operating costs

(1) For the purposes of step 5 of the residual pricing method, an included cost for a participant in an integrated operation is a capital cost if:

(a) it is not a personal cost; and

(b) any of the following subparagraphs apply:

(i) it was incurred before the production date;

(ii) the unit of property for which it was incurred is a depreciating asset for the purposes of section 40–30 of the Income Tax Assessment Act 1997;

(iii) it is a project amount within the meaning of section 40‑840 of the Income Tax Assessment Act 1997.

Note: Subparagraph (b)(i) applies if, for example, a person incurs operating expenses before the production date. Those expenses will be capital costs for the purposes of this instrument.

(2) A cost that is a capital cost only because of subparagraph (1)(b)(i) is taken to have been incurred on 1 January in the financial year in which it was incurred.

Note: Costs that relate to a unit of property that is constructed over several years of tax are dealt with in section 39.

(3) For the purposes of step 5 of the residual pricing method, an included cost for a participant in an integrated operation is an operating cost if:

(a) it is not a personal cost; and

(b) it is not a capital cost.

37 Amount and timing of included capital cost

(1) This section applies to an included capital cost if:

(a) the cost is for:

(i) an integrated GTL operation for which an election has been made under section 50; or

(ii) an integrated operation that recovers petroleum from an onshore petroleum project for which an election has been made under section 51; and

(b) the cost was incurred before 1 July 2012.

(2) For the purposes of step 6 of the residual pricing method, the included capital cost is taken to have been incurred on 1 July 2012 and not incurred when it was actually incurred.

Note: This will affect how steps 8 to 10 of the method apply to the included capital cost. The steps of the method work sequentially. So, (assuming this subsection applies to the cost) the next applicable step or provision that refers to the start date for the cost will be referring to 1 January in the 2012‑13 financial year.

(3) For the purposes of step 6 of the residual pricing method, if the included capital cost was for a unit of property that was completed before 2 May 2010, the amount of the cost is taken to be the depreciated replacement cost of the unit as at 1 May 2010.

(4) In this section:

depreciated replacement cost has the same meaning as in Accounting Standard AASB 136 Impairment of Assets.

38 Phase costs and upstream and downstream costs

(1) For the purposes of step 7 of the residual pricing method, the included direct and indirect costs are attributed to the various phases or stages of the operation in accordance with this section.

Attributing costs to phases

(2) For each phase of the integrated operation, each included direct cost that can be wholly attributed to the phase is a phase cost for the phase.

(3) If a direct cost for the integrated operation cannot be wholly attributed to activities of a single phase:

(a) the cost is taken to be made up of separate costs for each phase, each of the amount (if any) that can reasonably be apportioned to that phase; and

(b) each of those costs is attributed to the appropriate phase.

Attributing costs to stages

(4) Each included indirect cost for the integrated operation is taken to be made up of 2 costs of equal amounts, of which one is attributable to the upstream stage and one to the downstream stage.

Note: Section 43 does not apply to these costs, so that they are not reduced because of the multiple use of a phase.

(5) A cost that is a phase cost of a phase in the upstream stage, or an indirect cost allocated to the upstream stage by subsection (4), is an upstream cost.

(6) A cost that is a phase cost of a phase in the downstream stage (which will include marketing and selling costs), or an indirect cost allocated to the downstream stage by subsection (4), is a downstream cost.

Division 3—Allocating capital costs to years of tax

39 Capital costs incurred for a unit of property completed over several years

(1) This section applies to an included capital cost for the taxpayer if the cost is incurred in relation to a unit of property:

(a) that is constructed over a period of time; and

(b) for which the last capital cost is incurred in a later financial year (the final cost year).

(2) For the purposes of step 8 of the residual pricing method, the included capital cost:

(a) is augmented for the number of calendar years between the start date for the included capital cost and 1 January in the final cost year; and

(b) is taken to be incurred in the final cost year.

Note 1: The start date for the included capital cost may have been affected by subsection 37(2).

Note 2: The steps of the method work sequentially. So, (assuming this subsection applies to the cost) the next applicable step or provision that refers to the cost will be referring to:

(a) the cost as augmented under this subsection; and

(b) a start date for the cost of 1 January in the final cost year.

40 Capital costs incurred before the production year—project sales gas produced first

(1) For the purposes of step 9 of the residual pricing method, this section applies to an included capital cost for the taxpayer if:

(a) the included capital cost is incurred before the production year; and

(b) the MPC production year for the operation, if any, is not before the production year.

(2) The included capital cost:

(a) is augmented for the number of calendar years between the start date for the included capital cost and the production date; and

(b) is taken to be incurred in the production year.

Note 1: The start date for the included capital cost may have been affected:

(a) by subsection 39(2), if that subsection applied to the cost; or

(b) by subsection 37(2), if subsection 39(2) did not apply to the cost and an election was made under section 50 or 51.

The amount of the cost may also have been affected by subsection 39(2), if that subsection applied to the cost.

Note 2: The steps of the method work sequentially. So, (assuming this subsection applies to the cost) the next applicable step or provision that refers to the cost will be referring to:

(a) the cost as augmented under this subsection; and

(b) a start date for the cost of 1 January in the production year.

41 Capital costs incurred before the production year—other marketable petroleum commodities produced first

(1) For the purposes of step 9 of the residual pricing method, this section applies to an included capital cost for the taxpayer if:

(a) the included capital cost is incurred before the production year; and

(b) marketable petroleum commodities other than project sales gas are produced in the operation; and

(c) the MPC production year for the operation is before the production year.

Note 1: The start date for the included capital cost may have been affected:

(a) by subsection 39(2), if that subsection applied to the cost; or

(b) by subsection 37(2), if subsection 39(2) did not apply to the cost and an election was made under section 50 or 51.

The amount of the cost may also have been affected by subsection 39(2), if that subsection applied to the cost.

Note 2: The steps of the method work sequentially. So, (assuming this section applies to the cost) the next applicable step or provision that refers to the cost will be referring to:

(a) the cost as augmented or reduced under subsection (2), (3) or (4); and

(b) a start date for the cost of 1 January in the production year (see subsection (5)).

(2) If the included capital cost is incurred for a unit of property that will be used solely for:

(a) the recovery of project natural gas; or

(b) the production of project sales gas; or

(c) the processing of project sales gas into project liquid; or

(d) the combustion of project sales gas to produce project electricity; or

(e) the transportation or storage of project product;

the included capital cost is augmented for the number of calendar years between the start date for the included capital cost and the production date.

(3) If subsection (2) does not apply, and the included capital cost is incurred before the MPC production year, the included capital cost is:

(a) augmented for the number of calendar years between the start date for the included capital cost and the 31 December of the MPC production year; and

(b) reduced for the number of calendar years between the 31 December of the MPC production year and the production date.

(4) If subsection (2) does not apply, and the included capital cost is incurred in or after the MPC production year and before the production year, the included capital cost is reduced for the number of calendar years between the start date for the included capital cost and the production date.

(5) An included capital cost as reduced, or as augmented and reduced, under this section is taken to be incurred in the production year.

42 Allocating capital costs to a year of tax

(1) For the purposes of step 10 of the residual pricing method, this section applies to an included capital cost for the taxpayer (the capital cost) that was incurred in a year of tax (the cost year) in relation to a unit of property (the unit) and has, if appropriate, been augmented or reduced under section 40 or 41.

(2) The annual allocation for the capital cost is allocated to the cost year and to each subsequent year of tax during the remainder of the expected life of the unit.

(3) If the expected operating life of the unit is 15 years or less, the annual allocation for the capital cost is:

where:

N means the number of calendar years in the expected operating life of the unit.

(4) If the expected operating life of the unit is more than 15 years, the annual allocation for the capital cost is:

(5) If, at the end of the assessment year, the expected operating life of the unit has changed since the end of the cost year:

(a) the annual allocation of the capital cost for the assessment year is calculated using the new expected operating life of the unit; and

(b) the annual allocations of the capital cost for the calculation of RPM prices for years before the change are unaffected.

(6) For the purposes of this section, the expected operating life of the unit is the period of N calendar years between:

(a) the start date for the capital cost; and

(b) the 31 December of the last year of tax that is within the expected operating life of the operation and during which the unit of property is expected to be used for the operation.

(7) For the purposes of this section, a cost that is a capital cost only because of subparagraph 36(1)(b)(i) is taken to have been incurred in relation to a unit of property that has an expected operating life that is the expected operating life of the operation.

Division 4—Accounting for multiple use of a phase

43 Applying the energy coefficients to costs of each phase

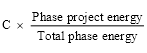

(1) For the purposes of step 12 of the residual pricing method, the amount of each phase cost for a phase, for the year of tax, is taken to be:

where:

C means the amount of the cost before the application of this section.

phase project energy means the energy content of the project product that enters the phase in the year of tax.

total phase energy means the energy content of all the petroleum product that enters the phase in the year of tax.

(2) However, subsection (1) does not apply to the phase cost for the phase ending at the end of the upstream stage of an integrated GTL operation if an election under section 48 has been made for the operation.

Part 5—Notional tax amount—sales gas

44 Notional tax amount when RPM price not used

For the purposes of paragraph 97(1AA)(b) of the Act, if any of the following is used in working out assessable petroleum receipts for a person under section 19, 20 or 21 of this instrument:

(a) the comparable uncontrolled price;

(b) the consideration received or receivable, less any expenses payable, by the person in relation to the sale;

(c) an advance pricing arrangement;

the amount that is to be included in calculating the current period liability under subsection 97(1A) of the Act is the amount of assessable petroleum receipts worked out under section 19, 20 or 21 of this instrument.

45 Notional tax amount when RPM price used

(1) This section applies if a participant in an integrated operation uses an RPM price for an assessable gas in working out assessable petroleum receipts under section 19, 20 or 21, and had an RPM price for the previous year of tax.

(2) For the purposes of paragraph 97(1AA)(b) of the Act, the amount that is to be included in calculating the current period liability under subsection 97(1A) of the Act is:

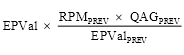

where:

EPVal (short for end product value) means the end product value for the participant in the instalment period.

EPValPREV means the end product value for the participant in the previous year of tax.

QAGPREV means the quantity of the assessable gas, measured by volume or mass, that was in the previous year of tax:

(a) for an integrated GTL operation—processed into project liquid that the participant was entitled to receive in the downstream stage (including any of that assessable gas that was used in that processing); or

(b) for an integrated GTE operation—consumed in the production of project electricity that the participant was entitled to receive in the downstream stage.

RPMPREV means the RPM price for the assessable gas for the participant for the previous year of tax.

(3) If the participant sells a quantity of project liquid or project electricity from the operation as part of the operation in the period, and the sale is an arm’s length transaction, the market value of the quantity is taken to be the amount received for the sale.

(4) For a quantity of project liquid or project electricity to which subsection (3) does not apply, the market value of the quantity is the market value at the end of the downstream stage.

(5) If the Commissioner is not satisfied that sufficient information is available to determine a market value for the purposes of subsection (4), the market value of the quantity of project liquid or project electricity is the amount determined by the Commissioner as fair and reasonable.

46 Notional tax amount when no previous RPM price

(1) This section applies if a taxpayer uses an RPM price for an assessable gas in working out assessable petroleum receipts under section 19, 20 or 21, but does not have an RPM price for the previous year of tax.

(2) Subject to subsection (3), the amount that is to be included in calculating the current period liability under subsection 97(1A) of the Act is:

where:

quantity of assessable gas means the quantity of assessable gas, measured by volume or mass, that in the instalment period was:

(a) for an integrated GTL operation—processed into project liquid that the participant was entitled to receive in the downstream stage (including any of that assessable gas that was used in that processing); or

(b) for an integrated GTE operation—consumed in the production of project electricity that the taxpayer was entitled to receive in the downstream stage.

RPM price means the RPM price for the assessable gas calculated under section 24 or 25 as if the instalment period were the assessment year.

(3) If the taxpayer became a participant in the assessment year because of a transfer of interests from a participant or participants (the previous participants), the taxpayer may elect to apply subsection 45(2) as if the factors in the formula were replaced by the following:

EPValPREV is the total end product value for the previous participants in the previous year of tax.

QAGPREV is the total quantity of the assessable gas, measured by volume or mass, that was in the previous year of tax: