Financial Sector (Collection of Data) (reporting standard) determination No. 30 of 2016

Reporting Standard RRS 332.0 Statement of Economic Activity

Financial Sector (Collection of Data) Act 2001

I, Steve Davies, a delegate of APRA, under paragraph 13(1)(a) of the Financial Sector (Collection of Data) Act 2001 (the Act) and subsection 33(3) of the Acts Interpretation Act 1901:

(a) REVOKE Financial Sector (Collection of Data) (reporting standard) determination No. 56 of 2006, including Reporting Standard RRS 332.0 Statement of Economic Activity made under that Determination; and

(b) DETERMINE Reporting Standard RRS 332.0 Statement of Economic Activity, in the form set out in the Schedule, which applies to the financial sector entities to the extent provided in paragraph 3 of the reporting standard.

Under section 15 of the Act, I DECLARE that the reporting standard shall begin to apply to those financial sector entities, and the revoked reporting standard shall cease to apply, upon registration of this instrument on the Federal Register of Legislation.

This instrument commences upon registration on the Federal Register of Legislation.

Dated: 23 September 2016

[Signed]

Steve Davies

General Manager

Supervisory Support Division

Interpretation

In this Determination:

APRA means the Australian Prudential Regulation Authority.

financial sector entity has the meaning given by section 5 of the Act.

Schedule

Reporting Standard RRS 332.0 Statement of Economic Activity comprises the 17 pages commencing on the following page.

Reporting Standard RRS 332.0

Statement of Economic Activity

Objective of this reporting standard

This reporting standard is made under section 13 of the Financial Sector (Collection of Data) Act 2001.

Subject to what follows, it requires a registered entity that had total assets of $500 million or more at the end of the most recent complete financial year at the time of reporting, to give APRA annual statements of economic activity.

It also provides that if there are two or more registered entities of the same category[1] in a group of related bodies corporate (e.g. two or more money market corporations in the group), and the combined value of their total assets was $500 million or more at the end of the most recent complete financial year, one of them must give APRA annual statements of economic activity.

If there is more than one registered entity of the same category in a group of related bodies corporate, only one of them will have to report to APRA under this reporting standard.[2] That report must cover all registered entities of the same category in the group.

This reporting standard outlines the overall requirements for the provision of the required information to APRA. It should be read in conjunction with Form RRF 332.0 Statement of Economic Activity and the associated instructions (all of which are attached and form part of this reporting standard).

Purpose

- Data collected in Form RRF 332.0 Statement of Economic Activity (Form RRF 332.0) is used for the purposes of the Reserve Bank of Australia. It may also be used by APRA, for the purpose of prudential supervision, and the Australian Bureau of Statistics.

Application

2. This reporting standard applies to those registered entities outlined in paragraph 3.

Information required

3. Subject to paragraph 4, a registered entity must provide APRA with the information required by Form RRF 332.0 in respect of a reporting period if, at the end of the most recent complete financial year for the registered entity, it:

(a) had total assets of $500 million or more;[3] or

(b) was one of a number of registered entities that, during the reporting period, were:

(i) of the same category as the first-mentioned registered entity; and

(ii) related bodies corporate of each other

and, at the end of the most recent complete financial year for the first-mentioned registered entity, had combined total assets of $500 million or more.

4. However, a registered entity is not required to report in respect of a particular reporting period if another registered entity has reported under this reporting standard in respect of that reporting period, and that other entity is both:

(a) a related body corporate of the first-mentioned registered entity; and

(b) of the same category as the first-mentioned registered entity.

Example of the application of paragraphs 3 and 4: RE1 Ltd is a registered entity. Under section 11 of the Collection of Data Act it has been allocated to the category of ‘money market corporation’. At the end of the most recent complete financial year it had assets of $40 million. RE2 Pty Ltd is a subsidiary, and therefore a related body corporate, of RE1. It is also a money market corporation. At the end of the most recent complete financial year it had assets of $20 million. For the purposes of the test in paragraph 3(b) their respective total assets are added together, producing a total of $60 million. This exceeds the $50 million test in paragraph 3(b). Having regard to paragraph 4, one of the two companies is required to report to APRA under this reporting standard in respect of the reporting period (assuming there are no other money market corporations in the group that have reported to APRA in respect of that reporting period).

Reporting periods and due dates

5. Subject to paragraph 6, a registered entity must provide the information required by this reporting standard for each financial year.

6. APRA may, by notice in writing to a particular registered entity, vary the timing of a reporting period for the registered entity or vary the duration of a reporting period for the registered entity.

7. The information required by this reporting standard must be provided to APRA within 40 business days after the end of the reporting period to which it relates.

8. APRA may grant a registered entity an extension of a due date in writing, in which case the new due date for the provision of the information will be the date on the notice of extension.

Forms and method of submission

9. The information required by this reporting standard must be given to APRA either:

(a) in electronic form, using one of the electronic submission mechanisms provided by the 'Direct to APRA' (also known as 'D2A') application; or

(b) manually completed on paper, which must be faxed or mailed to APRA's head office.

Note: the Direct to APRA application software and paper forms may be obtained from APRA.

Authorisation

10. All information provided by a registered entity under this reporting standard must be subject to processes and controls developed by the registered entity for the internal review and authorisation of that information. It is the responsibility of the board and senior management of the registered entity to ensure that an appropriate set of policies and procedures for the authorisation of data submitted to APRA is in place.

11. If a registered entity submits information under this reporting standard using the ‘Direct to APRA’ software, it will be necessary for an officer of the registered entity to digitally sign, authorise and encrypt the relevant data. For this purpose APRA’s certificate authority will issue 'digital certificates', for use with the software, to officers of the registered entity who have authority from the registered entity to transmit the data to APRA.

12. If information under this reporting standard is provided in paper form, it must be signed on the front page of the relevant completed form by either:

(a) the Principal Executive Officer of the registered entity; or

(b) the Chief Financial Officer of the registered entity (whatever his or her official title may be).

Minor alterations to forms and instructions

13. APRA may make minor variations to:

(a) a form that is part of this reporting standard, and the instructions to such a form, to correct technical, programming or logical errors, inconsistencies or anomalies; or

(b) the instructions, to clarify their application to the form

without changing any substantive requirement in the form or instructions.

14. If APRA makes such a variation it must notify in writing each registered entity that is required to report under this reporting standard.

Transitional

15. A registered entity must report under the old reporting standard in respect of a transitional reporting period. For these purposes:

old reporting standard means the reporting standard revoked in the determination making this reporting standard (being the reporting standard which this reporting standard replaces).

transitional reporting period means a reporting period under the old reporting standard:

(a) which ended before the date of revocation of the old reporting standard; and

(b) in relation to which the registered entity was required, under the old reporting standard, to report by a date on or after the date of revocation of the old reporting standard.

Interpretation

16. In this reporting standard:

business days means ordinary business days, exclusive of Saturdays, Sundays and public holidays.

category means a category to which a registered entity has been allocated under section 11 of the Financial Sector (Collection of Data) Act 2001.

Principal Executive Officer means the principal executive officer of the registered entity for the time being, by whatever name called, and whether or not he or she is a member of the governing board of the entity.

registered entity has the meaning given in the Financial Sector (Collection of Data) Act 2001 (that is, a corporation whose name is entered in the Register of Entities kept by APRA under section 8 of that Act).

Note: references to registered financial corporations in the forms and instructions that form part of this reporting standard are taken to have the same meaning as registered entity.

related body corporate has the meaning given in section 50 of the Corporations Act 2001. reporting period means a period defined in paragraph 5 or, if applicable, paragraph 6.

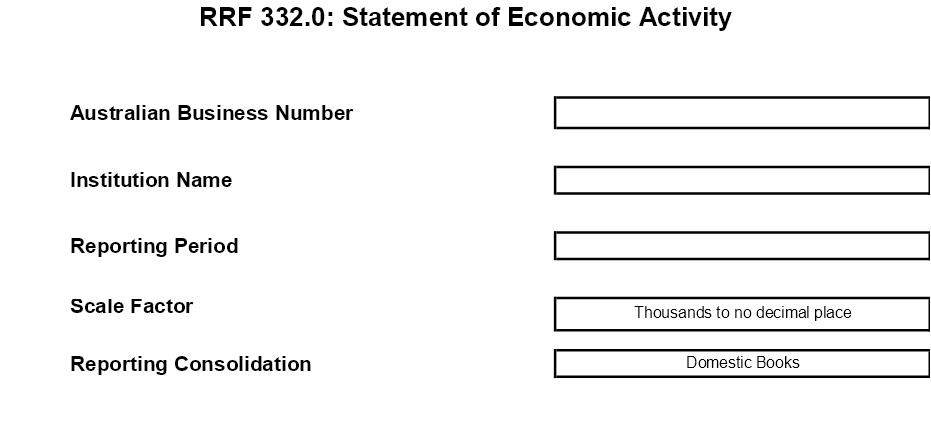

Reporting Form RRF 332.0

Statement of Economic Activity

Instruction Guide

General directions and notes

Reporting entity

This form is to be completed by all Registered Financial Corporations (RFCs) that have total assets equal to or greater than $500 million, after consolidating all RFCs of the same category in a group of related bodies corporate (e.g. two or more money market corporations in the same group) on a Domestic books basis.

The Domestic books of the registered entity relates to the Australian books of the Australian entity and has the following scope:

- this form should be completed on a consolidated basis for all legal entities in your Australian enterprise group that are required to file this return;

- do not consolidate Australian and offshore controlled entities or associated entities that are not required to complete this form;

- exclude offshore branches of the Australian registered entity from this reporting unit;

- report your Australian consolidated entity’s operations/transactions that are booked inside Australia; and

- include transactions with non-residents recorded on Australian books.

Reporting period

This form is for the financial year ended 30 June. If this business has a different financial year, please report for a twelve month period that ends between 1 October in the previous calendar year and 30 September in the current calendar year. All RFCs that have total assets equal to or greater than $500 million should submit the completed form to APRA within 40 business days of the end of the 30 June financial year. If this business has a financial year ending between 1 July and 30 September, please submit this form within 40 business days of the end of the relevant financial year.

Unit of measurement

All RFCs that have total assets equal to or greater than $500 million are asked to complete the form in thousands of Australian dollars rounded to the nearest whole number (no decimal place).

Amounts denominated in foreign currency are to be converted to AUD using the spot exchange rate effective as at the reporting date.

Specific instructions

The items listed under ‘Include’ and ‘Exclude’ are examples and should not be taken as a complete list of items to be included or excluded.

Part A: Selected expenses

Postage, mailing and courier expenses

Expenses incurred for the picking up, transport, and delivery (domestic or international) of addressed or unaddressed mail, packages and parcels.

Include:

- postage stamps;

- mailbox rental services;

- customised express pick up and delivery services; and

- messenger services.

Exclude:

- storage (where this expense can be distinguished from courier expenses).

Telecommunication charges

Telecommunication services are all payments (of a non-capital nature) for telecommunication services which engage wire, cable or radio transmission.

Include:

- telephone charges;

- facsimile charges;

- internet charges; and

- cost of leased lines for computers and internet services.

Exclude:

Insurance premiums other than workers' compensation

Include:

- optional third party and comprehensive motor vehicle insurance premiums;

- fire, general, accident and public liability premiums; and

- professional indemnity insurance premiums.

Exclude:

- workers’ compensation insurance premiums/levies (report to workers' compensation premiums/costs in RRF 331.0 Selected Revenues and Expenses (RRF 331.0)); and

- compulsory third party motor vehicle insurance premiums.

Legal expenses

Legal expenses are fees incurred when a business secures the services of a legal representative, or requires legal representation, or seeks professional advice on legal matters.

Audit and other accounting services

Audit and other accounting expenses are the costs incurred for the professional advice and skills of an auditor or accountant.

Include:

- cost of producing annual or sub-annual financial reports;

- preparing other financial accounts;

- auditing services; and

- carrying out other accounting services.

Advertising expenses

Advertising expenses are the costs incurred by a business for promotional and publicity campaigns aimed at bringing the activities of the business to the attention of consumers for the purpose of increasing sales.

Exclude:

- in-house costs (e.g. wages and salaries of own advertising staff); and

- sponsorship expenses.

Paper, printing and stationery

Paper, printing and stationery expenses are costs incurred for office supplies and printing carried out by or for the business.

Include:

- all office stationery; and

- production of financial reports, etc.

Data processing services provided by other businesses

Payments for data processing services provided by other businesses. Data processing services relate to the transformation of data into a suitable output.

Include:

- expenses incurred for data entry and manipulation services.

Staff training services

Staff training expenses are payments to consultants, institutions or other businesses for the provision of staff training and education services.

Include:

- training costs relating to all workers employed in this business (e.g. working proprietors and partners, contract/agency staff);

- all fees paid to consultants and institutions for designing, conducting, evaluating or providing facilities for training courses; and

- conference registration fees.

Exclude:

- informal on-the-job training;

- wages and salaries of this business' trainers and trainees for the time spent providing and receiving training (reported as wages and salaries on RRF 331.0);

- accommodation, meals and drinks (include in the data item "Travel, accommodation and entertainment");

- stationery (include in the data item "Paper, printing and stationery"); and

- venue hire.

Travel, accommodation and entertainment

Travelling expenses are costs incurred for transportation services relating to business activities which occur away from the normal place of business. These costs are only to be included if they are incurred in connection with business activities. Accommodation expenses are those costs incurred in providing accommodation to staff when business activities occur away from the normal place of business. Entertainment expenses are the costs incurred by a business for the provision of entertainment activities.

Other management and administrative expenses

Other management and administrative services expenses are payments to another business/consultant for providing administrative services or management expertise not elsewhere collected e.g. services such as accounting or legal, could be carried out by the corporate office for the whole group, then costs distributed proportionally across the group. The individual business pays a fee to the head office for the service rendered but is unable to separately identify the individual components which constitute the fee.

Include:

- payments made to related or unrelated business for management and administrative services.

Exclude:

- payments for data processing services;

- payments for secretarial, word processing, typing and copying services;

- payments for staff training services; and

- paper, printing and stationery expenses.

Cleaning services provided by other businesses

Cleaning services expenses are incurred when the business' premises are cleaned by an external business.

Include:

- building cleaning;

- office cleaning;

- window cleaning;

- furniture cleaning; and

- removal of waste from inside to areas outside the office compounds.

Exclude:

- wages and salaries of own employees engaged in cleaning activities (reported as wages and salaries on RRF 331.0);

- motor vehicle cleaning; and

- carpet, laundry and dry-cleaning.

Other commission expenses

Commission expenses are payments to other businesses and self-employed persons for work done or sales made on a commission basis. Amounts shown here are commission expenses not included elsewhere. Commission expenses should be initially recorded under any other relevant expense items.

Include:

- payments to other businesses and self employed persons for work done or sales made on a commission basis;

- payments to persons paid by commission without a retainer; and

- investigation fees paid to non-employees (on commission).

Exclude:

- commissions paid to persons who receive a retainer;

- commissions paid to own employees;

- payments to consultants; and

- investigation fees if paid to own employees.

Other contract expenses

Contract expenses are payments to other businesses and self-employed persons for work done on a contract basis. Amounts shown here are contract expenses not elsewhere included. Contract expenses should be initially recorded under any other relevant expense items (e.g. contract expenses for repair and maintenance would be recorded under “Repair and maintenance”).

Include:

- payments to other businesses and self employed persons for work done on a contract basis;

- contractors and subcontractors and their employees; and

- owner/drivers.

Royalty expenses

Royalties (other than royalties for natural resources) are payments made by one business or individual for the use of rights owned by another company/person. Do not deduct withholding tax.

Include:

- payments under licensing arrangements; and

- payments for royalties from intellectual property (e.g. patents, copyrights, etc).

Exclude:

- expensed computer software licence fees (include in “Computer software expensed”); and

- capitalised computer software licence fees (include in “Capital expenditure”).

Computer software expensed

These items represent the cost of any computer software (including license fees) that has been charged to profit as an expense in the current accounting period.

Include:

- installation costs paid to external service providers;

- purchase costs; and

- expensed computer software licence fees.

Exclude:

- other licence fees and royalties (include in “Royalty expenses”);

- computer software capitalised (include in “Capital expenditure”); and

- software maintenance (include in “Repairs and maintenance”).

Computer equipment expensed

These items represent the cost of any computer equipment that has been charged to profit as an expense in the current accounting period.

Water charges

Include:

- water rates and any excess water charges.

Repairs and maintenance

Include:

- computer software and hardware maintenance.

Exclude:

- wages and salaries of own employees (reported as wages and salaries on RRF 331.0).

Part B: Employees

Number of persons working for this business during the last pay period in the financial year of the reporting ADI.

Include:

- persons paid a retainer, wage or salary;

- working proprietors and partners;

- full-time and part-time employees;

- permanent, temporary and casual employees;

- managerial and executive employees;

- employees absent on paid or prepaid leave; and

- employees on workers' compensation who continue to be paid through the payroll.

Exclude:

- persons paid by commission only;

- non-salaried directors;

- self employed persons such as consultants and contractors; and

- volunteers.

Part C: Capital expenditure

Capital expenditure is the sum of outlays for the purchase of fixed tangible and/or intangible assets by the business during the reference period. Capital work done by own employees should be included in the appropriate capital expenditure item(s), and also separately identified in the data item of which “Capitalised work done by own employees”.

Include:

- all costs capitalised in this business’ books (including legal fees, real estate transfer costs and assets acquired under finance leases);

- progress payments made to contractors for capital work done by them; and

- major improvements, alterations and additions to fixed assets.

Exclude:

- progress payments for plant, machinery and equipment being produced on order;

- payments for repair and maintenance of fixed assets;

- payments of fixed assets on rental or acquired through an operating lease; and

- interest paid.

Computer software capitalised

If software and hardware costs cannot be separated, include total in “Computers and computer peripherals capitalised”.

Include:

- capitalised computer software license fees;

- installation costs;

- purchase or development of large databases; and

- computer software developed in-house.

Exclude:

- computer software expensed (include in “Computer software expensed”); and

- software maintenance (include in “Repairs and maintenance”).

Intangible assets

Include:

- patents, licences and goodwill.

Exclude:

- capitalised computer software licence fees.

Capital expenditure - Of which capitalised work done by own employees

Include:

- capitalised work done by own employees in developing computer software in-house.

Exclude:

- interest associated with the cost of the assets (reported as interest expenses on RRF 331.0); and

- payments made to other businesses for costs associated with the original acquisition of the assets (include in capital expenditure).

Part D: Disposal of assets

Report the proceeds from sales of assets